internal revenue bulletin no. 2000–43 bulletin …this document contains corrections to a notice...

TRANSCRIPT

INCOME TAX

Notice 2000–56, page 393.This notice provides guidance under section 1032 of the Codeon which entity is treated as the grantor and owner of a grantortrust when a parent corporation contributes its stock to a rabbitrust for the benefit of the employees of a subsidiary.

Rev. Proc. 2000–42, page 394.This procedure informs taxpayers of the information they mustsubmit to request a closing agreement under section1.1503–2(g)(2)(iv)(B) of the regulations to prevent the recap-ture of dual consolidated losses (DCLs) upon the occurrence ofcertain triggering events.

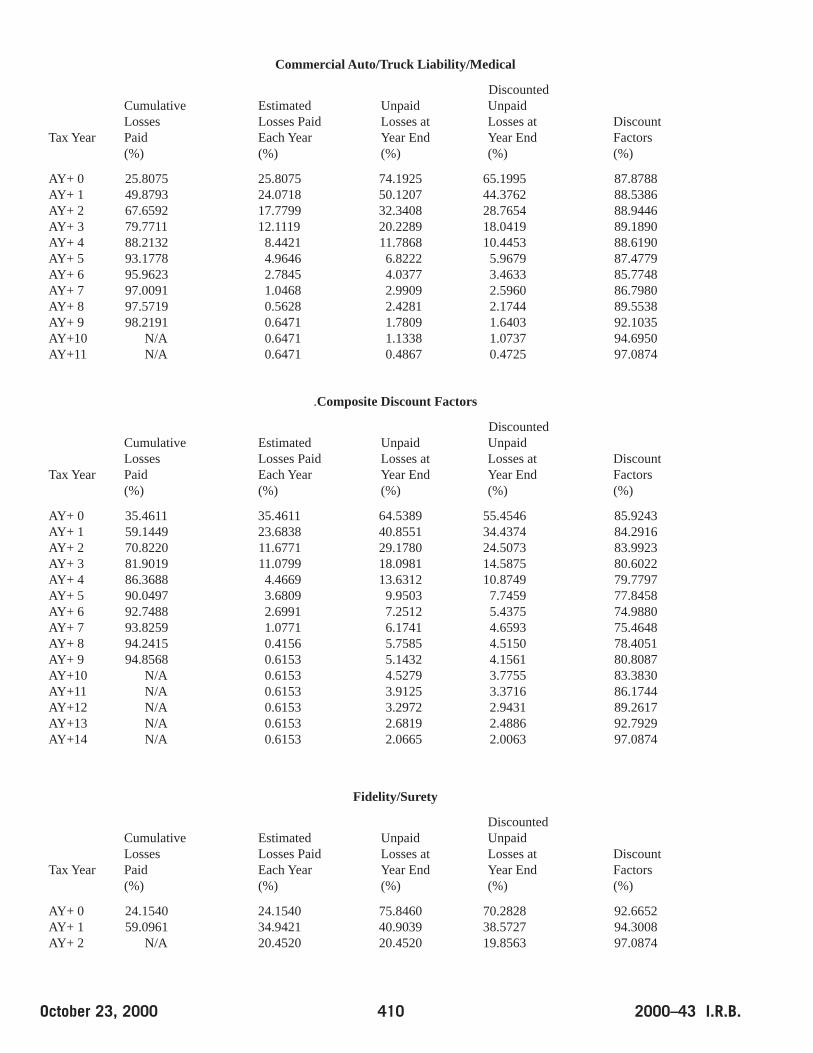

Rev. Proc. 2000–44, page 409.Insurance companies; loss reserves; discounting unpaidlosses. The loss payment patterns and discount factors areset forth for the 2000 accident year. These factors will be usedfor computing discounted unpaid losses under section 846 ofthe Code.

Rev. Proc. 2000–45, page 417.Insurance companies; discounted estimated salvagerecoverable. The salvage discount factors are set forth forthe 2000 accident year. These factors will be used for com-puting estimated salvage recoverable under section 832 of theCode.

Announcement 2000–78, page 428.The Service is requesting comments on the proposed regula-tions regarding the monthly limit for transit passes and trans-portation, in a commuter highway vehicle, provided by anemployer to employees under section 132(f) of the Code.

EMPLOYEE PLANS

REG–114697–00, page 421.Nondiscrimination requirements for certain definedcontribution retirement plans. Proposed regulations wouldprescribe conditions under which certain defined contributionretirement plans (sometimes referred to as “new comparabili-ty” plans) are permitted to demonstrate compliance withapplicable nondiscrimination requirements based on plan ben-efits rather than plan contributions. A public hearing is sched-uled for January 25, 2001.

Notice 2000–55, page 393.Weighted average interest rate update. The weightedaverage interest rate for October 2000 and the resulting per-missible range of interest rates used to calculate current liabil-ity for purposes of the full funding limitation of section412(c)(7) of the Code are set forth.

TAX CONVENTIONS

Notice 2000–57, page 389.The agreement between the United States and Netherlandsidentifying U.S. and Dutch pension plans for tax treaty benefitsis set forth.

ADMINISTRATIVE

Rev. Proc. 2000–43, page 404.Ex parte communication prohibition. Guidance is providedto taxpayers and IRS employees about ex parte communica-tions during the appeals process.

Internal Revenue

bbuulllleettiinnBulletin No. 2000–43

October 23, 2000

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

Department of the TreasuryInternal Revenue Service

Finding Lists begin on page ii.

(Continued on the next page)

October 23, 2000 2000–43 I.R.B.

ADMINISTRATIVE—continued

Announcement 2000–85, page 429.This document contains corrections to a notice of proposed rule-making (REG–108522–00, 2000–34 I.R.B 187) relating to therecognition of gain on certain transfers to certain foreign trustsand estates.

2000–43 I.R.B. October 23, 2000

The Internal Revenue Bulletin is the authoritative instrumentof the Commissioner of Internal Revenue for announcing offi-cial rulings and procedures of the Internal Revenue Serviceand for publishing Treasury Decisions, Executive Orders, TaxConventions, legislation, court decisions, and other items ofgeneral interest. It is published weekly and may be obtainedfrom the Superintendent of Documents on a subscriptionbasis. Bulletin contents are consolidated semiannually intoCumulative Bulletins, which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform applicationof the tax laws, including all rulings that supersede, revoke,modify, or amend any of those previously published in theBulletin. All published rulings apply retroactively unless other-wise indicated. Procedures relating solely to matters of in-ternal management are not published; however, statementsof internal practices and procedures that affect the rightsand duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service onthe application of the law to the pivotal facts stated in therevenue ruling. In those based on positions taken in rulingsto taxpayers or technical advice to Service field offices,identifying details and information of a confidential natureare deleted to prevent unwarranted invasions of privacy andto comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not havethe force and effect of Treasury Department Regulations,but they may be used as precedents. Unpublished rulingswill not be relied on, used, or cited as precedents by Servicepersonnel in the disposition of other cases. In applying pub-lished rulings and procedures, the effect of subsequent leg-islation, regulations, court decisions, rulings, and proce-

dures must be considered, and Service personnel and oth-ers concerned are cautioned against reaching the same con-clusions in other cases unless the facts and circumstancesare substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisionsof the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions, and Subpart B, Legislation and RelatedCommittee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references tothese subjects are contained in the other Parts and Sub-parts. Also included in this part are Bank Secrecy Act Admin-istrative Rulings. Bank Secrecy Act Administrative Rulingsare issued by the Department of the Treasury’s Office of theAssistant Secretary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The first Bulletin for each month includes a cumulative indexfor the matters published during the preceding months.These monthly indexes are cumulated on a semiannual basis,and are published in the first Bulletin of the succeeding semi-annual period, respectively.

The IRS Mission

Provide America’s taxpayers top quality service by help-ing them understand and meet their tax responsibilities

and by applying the tax law with integrity and fairness toall.

Introduction

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

October 23, 2000 388 2000–43 I.R.B.

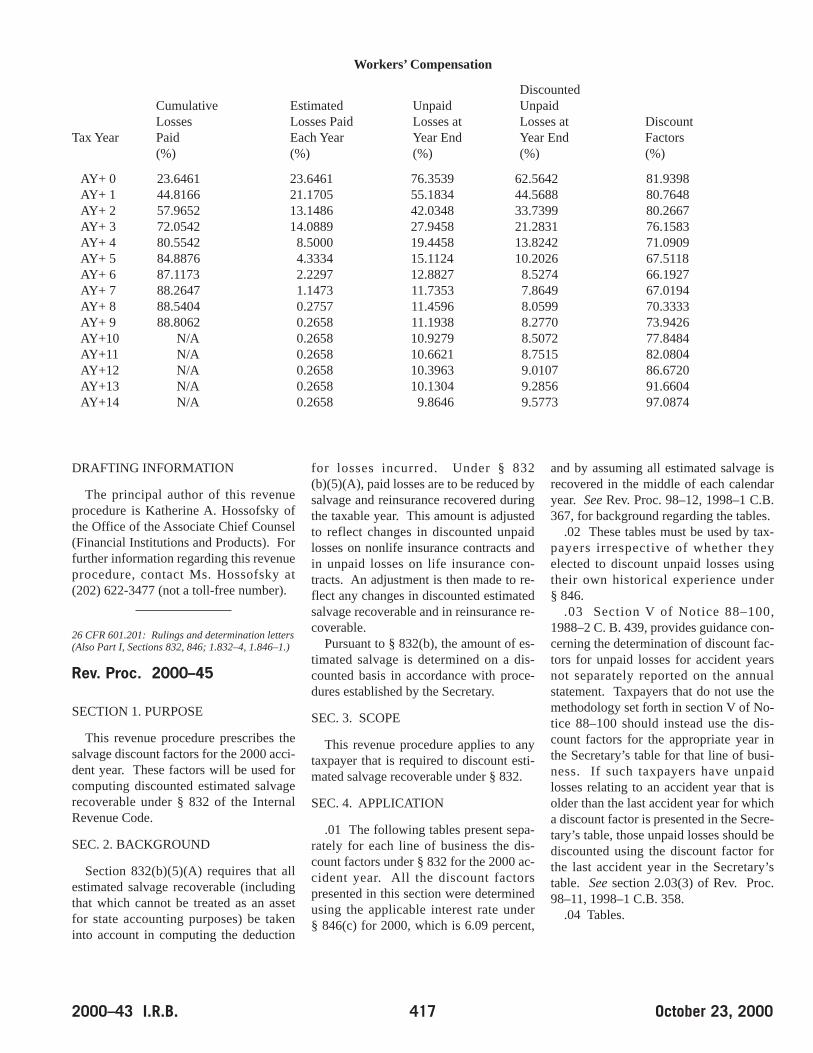

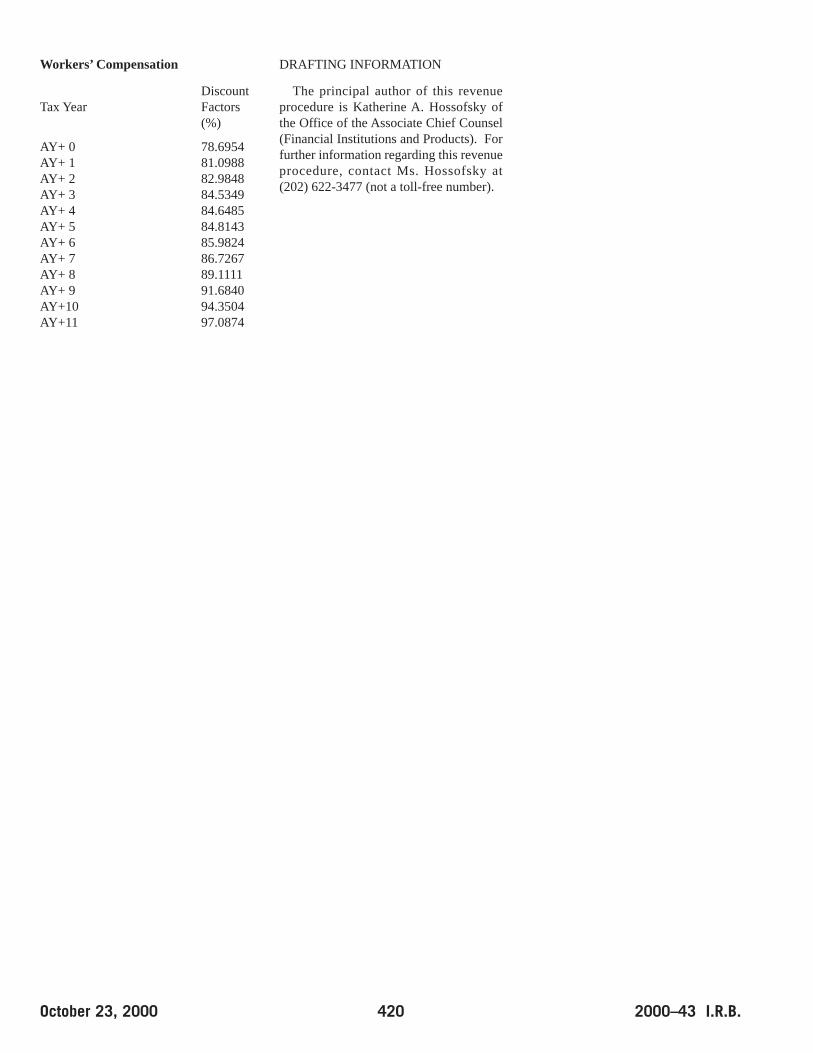

Section 832.—InsuranceCompany Taxable Income

26 CFR 1.832–4: Gross income.

The salvage discount factors are set forth for the2000 accident year. These factors will be used forcomputing estimated salvage recoverable for pur-poses of section 832 of the Code. See Rev. Proc.2000–45, page 417.

Section 846.—DiscountedUnpaid Losses Defined

26 CFR 1.846–1: Application of discount factors.

The loss payment patterns and discount factorsare set forth for the 2000 accident year. These fac-tors will be used for computing discounted unpaidlosses under section 846 of the Code. See Rev. Proc.2000–44, page 409.

26 CFR 1.846–1: Application of discount factors.

The salvage discount factors are set forth for the2000 accident year. These factors will be used forcomputing estimated salvage recoverable for pur-poses of section 832 of the Code. See Rev. Proc.2000–45, page 417.

Part I. Rulings and Decisions Under the Internal Revenue Code of 1986

2000–43 I.R.B. 389 October 23, 2000

Subpart A.—Tax Conventions

Following is a Copy of the NewsRelease Issued by International(U.S. Competent Authority) onApril 20, 2000 (IR–INT–2000–9)

Notice 2000–57

AGREEMENT IDENTIFIES U.S.AND DUTCH PENSION PLANSFOR TAX TREATY BENEFITS

Washington – The Competent Authori-ties of the The Netherlands and the UnitedStates reached a mutual agreement on thequalification of certain Dutch and U.S.pensions for treaty benefits under Article35 of the US-Netherlands Income TaxTreaty. The agreement specifies the proce-dures for claiming treaty benefits in eachcountry and the methods each country willuse to grant treaty benefits.

The agreement constitutes a MutualAgreement in accordance with the Con-vention between the Kingdom of theNetherlands and the United States ofAmerica for the avoidance of double taxa-tion and the prevention of fiscal evasionwith respect to taxes on income, signed onDecember 18, 1992, and amended by Pro-tocol signed on October 13, 1993.

The agreement is as follows:

Chapter I

Qualification for treaty benefits underarticle 35 of the 1992 Netherlands-US

income tax treaty

Questions have been raised regardingthe types of US and Netherlands residenttax exempt trusts, companies or other or-ganisations providing pension or retire-ment benefits that qualify for treaty bene-fits under article 35 of the Conventionbetween the Kingdom of the Netherlandsand the United States of America for theavoidance of double taxation and the pre-vention of fiscal evasion with respect totaxes on income, signed on 18 December1992, and amended by Protocol signed on13 October 1993 (in the following: theTreaty). In practise there are many differ-ent types of funds or plans established toprovide pension or retirement benefits andit is not always clear which of these funds

or plans fulfill the requirements of article35 of the Treaty. This issue is being dis-cussed between the Netherlands and theUS competent authorities under the mutualagreement procedure of article 29 of theTreaty, with the following initial conclu-sions.

In view of the present uncertainty it hasbeen decided to identify all the differenttypes of US and Netherlands resident taxexempt trusts, companies or other organi-sations providing pension or retirementbenefits that are considered to fall withinthe scope of article 35 of the Treaty andalso to indicate the appropriate proceduresfor filing a request for an application oftreaty benefits under said treaty provision.

In the course of the mutual agreementdiscussions it became apparent that,whereas with respect to certain types of USand Netherlands resident tax exempt trusts,companies or other organisations providingpension or retirement benefits it is beyonddoubt that they fall within the scope of arti-cle 35 of the Treaty, with respect to othertypes of US and Netherlands resident taxexempt trusts, companies or other organi-sations providing pension or retirementbenefits this is less clear. The Netherlandsand US authorities concluded that all thedifferent types of Netherlands and US resi-dent tax exempt trusts, companies or otherorganisations providing pension or retire-ment benefits mentioned in chapter II andIV of this agreement would be consideredto fall within the scope of article 35 of theTreaty.

However, in order to ensure that treatyprotection is restricted to qualifying USresident tax exempt trusts providing pen-sion or retirement benefits, the Netherlandscompetent authority would -at least for thetime being- prefer a closer monitoring ofall requests filed for an application of treatybenefits under article 35 of the Treaty.

It is understood that for the purpose ofthis publication the term “Code section”refers to sections of the US Internal Rev-enue Code and that the term “trust” in-cludes a custodial account treated as a trustfor US federal income tax purposes.

Chapter II

US resident tax exempt trusts providingpension or retirement benefits

Subject to the conditions of article 26,article 35, paragraph 2, and article 34,paragraph 4, of the Treaty:

1. a US resident tax exempt trust pro-viding pension or retirement benefitsunder a Code section 401 (a) qualifiedpension plan, profit sharing plan or stockbonus plan (including Code section 401(k) arrangements); or

2. a US resident tax exempt trust pro-viding pension or retirement benefitsunder a Code section 457(b) pension planor under a Code section 403(b) plan; or

3. a US resident tax exempt trustwhich is an Individual retirement account(Code section 408), a Roth Individual re-tirement account (Code section 408A), ora Simple retirement account, or a US resi-dent tax exempt trust which is providingpension or retirement benefits under aSimplified employee pension plan; or

4. a US resident common trust fund orgroup trust which is tax exempt underCode section 501 (a) with respect to fundsthat equitably belong to its participatingtrusts, all of which are entities mentionedunder point 1) above; or

5. a US resident common trust fund orgroup trust which is tax exempt under theInternal Revenue Code with respect tofunds that equitably belong to its partici-pating trusts, some of which are trustsother than those mentioned under point 1)above, but all of which are trusts men-tioned under point 1), 2), or 3) above, isconsidered to qualify for treaty benefitsunder article 35 of the Treaty and mayclaim application of treaty benefits withrespect to income derived from theNetherlands referred to in article 10 (divi-dends) of the Treaty. The Netherlandsdoes not apply a withholding tax on out-going interest payments as meant in arti-cle 12 of the Treaty.

However, a US resident tax exempttrust mentioned under point 2) or 3) abovewill not be considered to qualify for treatybenefits under article 35 of the Treaty inany taxable year if less than 70% of thetotal amount of the withdrawals fromsuch US trust during that year is used toprovide pension, retirement or other em-ployee benefits as meant in article 35 ofthe Treaty.

Any type of US resident tax exempttrust not mentioned above, which consid-

Part II. Treaties and Tax Legislation

October 23, 2000 390 2000–43 I.R.B.

ers itself to qualify for treaty benefitsunder article 35 of the Treaty, may presentits case to the Netherlands tax unit BPObuitenland, Heerlen (address: P.O. Box2865, 6401 DJ HEERLEN, The Nether-lands), or to the US competent authoritiesrequesting for a competent authority con-sideration under article 29 of the Treaty.

Chapter III

Appropriate procedures for filing arequest for an application of treaty

benefits in the Netherlands

The Netherlands has two methods forgranting treaty benefits for income re-ferred to in article 10 (dividends) of theTreaty, these methods being: the so-calledexemption method (in which case thetreaty rate is applied at source) and the so-called refund method.

As a general rule, the Netherlands ap-plies the exemption method when grant-ing treaty benefits in the case of Dutchsource dividend income received by a res-ident of the US, which means that treatybenefits will be granted by means of anexemption from Netherlands withholdingtax at source. In view of the Netherlandscompetent authority’s preference for acloser monitoring of all requests filed foran application of treaty benefits under ar-ticle 35 of the Treaty, a US resident taxexempt trust (including a US commontrust fund or group trust) mentioned inpoint 1) through 5) of chapter II of thispublication shall - as a general rule - berequired to use the refund method whenfiling its request for an application oftreaty benefits under article 35 of theTreaty. Only if certain conditions are ful-filled, such US resident tax exempt trustmay use the exemption method when fil-ing its request for an application of treatybenefits under article 35 of the Treaty.

The Netherlands regulations for the im-plementation of the Treaty, published inthe “Staatscourant” 5 January 1994, nr. 3and lastly amended on December 1996(“Staatscourant” 30 December 1996, nr.250), give a detailed description of theprocedures to be applied in the case of re-spectively the exemption method and therefund method.

The exemption method may be used ifthe US resident tax exempt trust request-ing treaty benefits under article 35 of theTreaty:

* has been issued a certification letter(Form 6166) by the US Internal RevenueService for the taxable year(s) in ques-tion, stating that the trust in question is atrust forming part of a pension, profitsharing, or stock bonus plan qualifiedunder Code section 401 (a) of the InternalRevenue Code (an example of a certifica-tion letter (Form 6166) is attached); or

* has been issued a so-called “qualifi-cation” certification by the competentNetherlands tax authorities, stating thatthe trust in question is a US resident taxexempt trust as described in article 35,paragraph 1, of the Treaty. Requests for a “qualification” certifica-tion may be filed with the tax unit BPObuitenland, Heerlen (address: P.O. Box2865, 6401 DJ HEERLEN, The Nether-lands).

A “qualification” certification, issuedby the competent Netherlands authorities,is in principle valid indefinitely. How-ever, a “qualification” certification willno longer be valid in the event:

*there is a material change in facts orcircumstances; or

*It is determined that the “qualifica-tion” certification was issued erroneously;or

*the US resident tax exempt trust inquestion has not claimed an application oftreaty benefits under article 35 of theTreaty for five consecutive calendaryears. Since a certification letter (Form6166) issued by the US Internal RevenueService is not valid indefinitely, a US res-ident tax exempt trust which has been is-sued a certification letter (Form 6166) bythe US Internal Revenue Service may alsofile a request for a “qualification” certifi-cate with the competent Netherlands taxauthorities.

Irrespective of the above, use of the re-fund method is mandatory in any taxableyear for a US resident tax exempt trustmentioned under point 2) or 3) of chapterII, if less than 70% of the total amount ofthe withdrawals from such US trust dur-ing that year is used to provide pension orretirement benefits.

Where assets of the pension fund(s) orpension plan(s) are held in custodial ac-counts, the amended form IB 92 USA willrequire a certification that the claim for arefund of Dutch dividend tax is filed forthe benefit of the custodial accounts inquestion.

The status of all US resident tax exempttrusts providing pension or retirement ben-efits and claiming treaty benefits under ar-ticle 35 of the Treaty may at any time besubject to verification by the competentNetherlands tax authority. If considerednecessary, use will be made of the ex-change of information procedure (article30 of the Treaty).

The Netherlands regulations for the im-plementation of the Treaty (including the“special arrangements” issued by theNetherlands competent authority in the re-lation to the US) and Form IB 92 USA will- where necessary - be amended in accor-dance with the above. A model of the“special arrangements” is published in theInfobulletin of 12 January 1999.

The new procedures will become ap-plicable beginning with dividends madepayable after 30 June 2000. The presentlyexisting procedures will remain applicablefor dividends made payable before or on30 June 2000.

Chapter IV

Netherlands resident tax exemptcompanies providing pension or

retirement benefits

Subject to the conditions of article 26,article 35, paragraph 2, and article 34,paragraph 4, of the Treaty, a Netherlandsresident tax exempt company constitutedand operated exclusively to administer orprovide benefits as meant in article 5, para-graph b), of the Netherlands corporationtax act (including a Netherlands residenttax exempt company constituted and oper-ated exclusively to administer or providebenefits under a pension plan as meant inarticle 8, paragraph 1, under f), of theNetherlands income tax act) is consideredto qualify for treaty benefits under article35 of the Treaty and may claim applicationof treaty benefits with respect to incomederived from the United States of Americareferred to in article 10 (dividends) and inarticle 12 (interest) of the Treaty.

Any type of Netherlands resident tax ex-empt company not mentioned above,which considers itself to qualify for treatybenefits under article 35 of the Treaty, maypresent its case to the United States com-petent authority, or to the Netherlandscompetent authority requesting for a com-petent authority consideration under article29 of the Treaty.

2000–43 I.R.B. 391 October 23, 2000

Chapter V

Appropriate procedures for filing arequest for an application of treaty

benefits in the United States of America

Under US tax law a Netherlands resi-dent taxpayer (including a Netherlandsresident tax exempt company referred toin article 35 of the Treaty) may file for anapplication of treaty benefits at source, ormay claim a refund of US income taxwithheld according to regulations setforth under the Internal Revenue Code.The following procedures apply to aNetherlands resident tax exempt com-pany.

A Netherlands resident tax exemptcompany described in this agreementshould claim exemption from US incometax withholding under Article 35 of the1992 Netherlands-US income tax treatyon dividends or interest income referredto in articles 10 and 12, respectively, ofthat treaty by providing a properly com-pleted IRS Form W-8BEN to the with-holding agent or payer of such income be-fore the income is paid or credited to thecompany. A company filing Form W-8BEN should cite Article 35 of the treatyon line 10 thereof, and state that it is aNetherlands resident tax exempt companydescribed in this agreement.

Notwithstanding the foregoing, untilDecember 31, 2000, and to the extent pro-vided in transition rules set forth in regu-lations under Internal Revenue Code sec-tion 1441 and Notice 99–25, 1999–20I.R.B. 75, a Netherlands resident tax ex-empt company may provide, and a with-holding agent may rely upon, other appro-priate documentation of the company’sexempt status, including, for example, aForm 1001, supplemented by a statement,or a valid Netherlands Form IB 93 USA

(certified by the tax inspector competentin the case of the Netherlands tax exemptcompany in question) stating that thecompany is a Netherlands resident tax ex-empt company described in this agree-ment.

Alternatively, the company may seek arefund of taxes withheld on such dividendor interest income by timely filing aUnited States income tax return andclaiming a refund of such taxes.

The status of all Netherlands residenttax exempt companies providing pensionor retirement benefits and claiming treatybenefits under article 35 of the Treatymay be subject to verification by the In-ternal Revenue Service. If considerednecessary, use will be made of the ex-change of information procedure (article30 of the Treaty).

A Netherlands resident tax exemptcompany as meant in article 5, paragraphb), of the Netherlands corporation tax act(including a Netherlands resident tax ex-empt company providing pension or re-tirement benefits as meant in article 8,paragraph 1, under f), of the Netherlandsincome tax act) may have the Netherlandstax authority concur in its claim of tax ex-empt status by means of a so-called article26 declaration (Form IB 93 USA), certi-fied by the tax inspector competent in thecase of the Netherlands tax exempt com-pany in question. This will not, however,preclude an audit and determination of thecompany’s substantive liability.

As noted in Article 6 of the Protocol,Article 35(2) of the Treaty provides thatdividends from a Real Estate InvestmentTrust are not eligible for Article 35 bene-fits. Article 35(2) also provides that in-come of an exempt pension trust is not ex-empt under Article 35 if it is receivedfrom a related person that is not itself anexempt pension trust. Paragraph VIII of

the Agreed Minutes to the Protocol pro-vides the understanding of the negotiatorsthat for purposes of Article 35(2), a per-son will be considered to be a “relatedperson” if more than 80 percent of thevote or value of any class of shares isowned by the person deriving the income.

Chapter VI

Tax exempt trusts, companies or otherorganisations providing other employee

benefits

In order to determine whether a clarifi-cation of the qualification under article 35of the Treaty for the various types of taxexempt trusts, companies or other organi-sations providing other employee benefitsis also considered necessary, comments orquestions regarding this issue are invitedand may be sent to to one of the followingaddresses:

Ministry of Finance of the NetherlandsDirectorate for International Tax Policyand LegislationP.O. Box 202012500 EE Den HaagThe Netherlands

Assistant Commissioner(International)attn. Tax Treaty DivisionInternal Revenue ServiceP.O. Box 23598Washington, D.C. 20024United States of America

Attachment:Form 6166 (Rev. 6–96)

October 23, 2000 392 2000–43 I.R.B.

2000–43 I.R.B. 393 October 23, 2000

Weighted Average Interest RateUpdate

Notice 2000–55

Notice 88–73 provides guidelines fordetermining the weighted average inter-est rate and the resulting permissible

range of interest rates used to calculatecurrent liability for the purpose of the fullfunding limitation of § 412(c)(7) of theInternal Revenue Code as amended bythe Omnibus Budget Reconciliation Actof 1987 and as further amended by theUruguay Round Agreements Act, Pub. L.103–465 (GATT).

The average yield on the 30-yearTreasury Constant Maturities for Oc-tober 2000 is 5.83 percent.

The following rates were deter-mined for the plan years beginning inthe month shown below.

Part III. Administrative, Procedural, and Miscellanous

90% to 105% 90% to 110%Weighted Permissible Permissible

Month Year Average Range Range

October 2000 5.95 5.35 to 6.24 5.35 to 6.54

Drafting Information

The principal author of this notice isTodd Newman of the Employee Plans,Tax Exempt and Government Entities Di-vision. For further information regardingthis notice, call the Employee Plans Actu-arial hotline, (202) 622-6076 between2:30 and 3:30 p.m. Eastern time (not atoll-free number). Mr. Newman’s numberis (202) 622-8458 (also not a toll-freenumber).

Rabbi Trusts

Notice 2000–56

I. PURPOSE

This notice provides guidance onwhich entity is treated as the grantor andowner of a grantor trust when a parentcorporation contributes its stock to a rabbitrust for the benefit of the employees of asubsidiary.

II. BACKGROUND

(i) Rabbi Trust Model Rev. Proc. 92–64, 1992–2 C.B. 422,

contains a model grantor trust for use innonqualified executive compensationarrangements that are popularly referredto as “rabbi trust” arrangements. Underthat revenue procedure, the Service willnot rule on unfunded deferred compensa-tion arrangements that use a trust otherthan the model trust, except in rare andunusual circumstances. Section 1(d) ofthe model trust document states that “Anyassets held by the Trust will be subject tothe claims of the Company’s general cred-

itors under federal and state law in theevent of Insolvency, as defined in Section3(a) herein.” In the case of a trust thatprovides benefits to employees of a sub-sidiary, it is the Service’s position thatSection 1(d) will not be satisfied unlessthe assets held by the trust are subject tothe claims of the subsidiary’s creditors(whether or not those assets are also sub-ject to the claims of the parent’s credi-tors). In this case, it has been the Ser-vice’s position that the subsidiary istreated as the grantor and owner of therabbi trust.

(ii) Final Regulations under Section1032 of the Internal Revenue Code

Section 1032 states that no gain or lossis recognized to a corporation on the re-ceipt of money or other property in ex-change for stock of the corporation. Regu-lations were recently issued under section1032 of the Internal Revenue Code (see65F.R. 31073 (May 16, 2000)). Section1.1032–3(b)(1) of these regulations pro-vides that no gain or loss is recognized onthe disposition of the issuing corporation’sstock by an acquiring entity if the require-ments set forth in Reg. § 1.1032–3(c) aremet. Section 1.1032–3(c)(2) requires,among other things, that the acquiring en-tity transfer the stock of the issuing corpo-ration to another person immediately afteracquiring the stock from the issuing corpo-ration (the “immediacy requirement”).Under the regulations, if the requirementsof Reg. § 1.1032–3(c), including the im-mediacy requirement, are met, the transac-tion is treated as if, immediately before theacquiring entity transfers the stock of theissuing corporation, the acquiring entity

purchased the issuing corporation’s stockfrom the issuing corporation for fair mar-ket value with cash contributed to the ac-quiring entity by the issuing corporation(or, if necessary, through intermediate cor-porations or partnerships). This series oftransactions is commonly referred to as the“cash purchase model.”

Rabbi trust arrangements typically donot involve an immediate transfer of stockto employees. In the case of a rabbi trustarrangement in which Parent Stock istreated for federal tax purposes as ownedby a subsidiary for a period of time beforethe Parent Stock is transferred to the em-ployees of the subsidiary, the immediacyrequirement of Reg. §1.1032–3(c)(2) willnot be satisfied when the Parent Stock istransferred from the rabbi trust to employ-ees of the subsidiary. Because the cashpurchase model of those Regulations willas a result not apply, the nonrecognitiontreatment of section 1032 will be inapplic-able in such a case, and, thus, the sub-sidiary typically will recognize gain on thetransfer of the Parent Stock from the rabbitrust to employees of the subsidiary.

III. TREATMENT OF PARENTCORPORATION AS GRANTOR OF ARABBI TRUST

The Service and Treasury have deter-mined that when a parent corporationcontributes Parent Stock to a rabbi trust toassist a subsidiary in meeting the sub-sidiary’s deferred compensation obliga-tions to its employees or serviceproviders, and the Parent Stock is bothsubject to the claims of the creditors ofthe parent corporation and subject to therequirement that any Parent Stock not

October 23, 2000 394 2000–43 I.R.B.

transferred to the subsidiary’s employeeswill revert to the parent on termination ofthe trust, then the parent corporation willbe considered the grantor and the ownerof the Parent Stock held in the trust, eventhough the Parent Stock is also subject tothe claims of the creditors of the sub-sidiary. If these conditions are satisfied,the Parent Stock (or other assets) will notbe considered transferred to the sub-sidiary until such time as they are used tosatisfy the subsidiary’s deferred compen-sation obligation to its employees or ser-vice providers, or when a claim is madeagainst the trust by a creditor of the sub-sidiary in the case of the subsidiary’s in-solvency. Thus, the immediacy require-ment of Reg. § 1.1032–3(c)(2) would besatisfied with respect to the Parent Stock.

This concept is illustrated in Example10 of Reg. § 1.1032–3(e). In the example,in Year 1, the issuing corporation, X,forms a trust which it will use to satisfydeferred compensation obligations owedby Y, X’s wholly owned subsidiary, to Y’semployees. X funds the trust with Xstock which would revert to X upon ter-mination of the trust, subject to the em-ployees’ rights to be paid the deferredcompensation. The creditors of X canreach all trust assets upon the insolvencyof X. Similarly, the creditors of Y canreach all trust assets upon the insolvencyof Y. In Year 5, the trust transfers X stockto the employees of Y in satisfaction ofthe deferred compensation obligation.The example states that X is considered tobe the grantor of the trust, and, under sec-tion 677 of the Code, X is also the ownerof the trust. Y is not considered a grantoror owner of the trust corpus at the time Xtransfers X stock to the trust. Any incomeearned by the trust would be reflected onX’s income tax return. In Year 5, whenemployees of Y receive X stock in satis-faction of the deferred compensationobligation, no gain or loss is recognizedby X or Y on the deemed disposition ofthe X stock by Y. Immediately before Y’sdeemed disposition of the X stock, Y istreated as purchasing the X stock from Xfor fair market value using cash con-tributed to Y by X. Under section 358,X’s basis in its Y stock increases by theamount of cash deemed contributed. Ac-cordingly, when employees or serviceproviders of Y receive X stock in satisfac-tion of the deferred compensation obliga-

tion, the requirements of § 1.1032–3(c)are satisfied, and no gain or loss is recog-nized by X or Y on the deemed disposi-tion of the X stock by Y.

Similarly, the parent corporation willbe treated as the grantor and owner of as-sets other than Parent Stock that are con-tributed by the parent corporation to arabbi trust if the assets are both subject tothe claims of the creditors of the parentcorporation and subject to the require-ment that any such assets not transferredto the subsidiary’s employees or serviceproviders will revert to the parent on ter-mination of the trust, even though suchassets are also subject to the claims of thecreditors of the subsidiary. The cash pur-chase model applies only to transfers ofstock by the parent corporation to thetrust. Therefore, when assets other thanParent Stock are transferred from the trustto the employees of the subsidiary, thesubsidiary is treated as receiving the otherassets from the parent corporation withthe parent’s carryover basis and the sub-sidiary will recognize gain or loss (if any)on the transfer of the assets to the sub-sidiary’s employees or service providers.

IV. MODIFICATION TO MODELTRUST UNDER REV. PROC. 92–64

The Service will rule on a request sub-mitted under Rev. Proc. 92–64 where themodel language has been modified to pro-vide that Parent Stock (or other assets)contributed by a parent corporation to arabbi trust for the benefit of employees orservice providers of a subsidiary is sub-ject to the claims of the creditors of boththe parent corporation and the subsidiary,and the remaining Parent Stock (or otherassets) contributed by the parent corpora-tion reverts to the parent corporation upontermination of the trust.

V. TRANSITION PROVISIONS FOREXISTING TRUSTS

The Service will not challenge a tax-payer’s position that no gain or loss is rec-ognized by a subsidiary upon the rabbitrust’s disposition of Parent Stock con-tributed to the rabbi trust by the parentcorporation on or before May 16, 2001,with respect to trusts in existence on orbefore June 15, 2000.

If the terms of the rabbi trust areamended to provide that assets (includingParent Stock) contributed by the parent

corporation to the rabbi trust are subjectto claims of the parent corporation’s cred-itors (in addition to being subject to theclaims of the subsidiary’s creditors) andthose assets not transferred to the sub-sidiary’s employees or service providerswill revert to the parent corporation upontermination of the rabbi trust, the Servicewill not treat such amendment as a con-structive dividend to the parent corpora-tion, provided the amendment is adoptedby May 16, 2001.

VI. EFFECT ON OTHER GUIDANCE

Rev. Proc. 92–64 will not fail to be sat-isfied if Parent Stock (or other assets)contributed by a parent corporation to arabbi trust for the benefit of employees orservice providers of a subsidiary is sub-ject to the claims of the creditors of theparent corporation and the subsidiary, andthe remaining Parent Stock (or other as-sets) contributed by the parent corpora-tion reverts to the parent corporation upontermination of the trust.

DRAFTING INFORMATION

The principal author of this notice isSusan Lennon of the Office of the Associ-ate Chief Counsel (Tax Exempt and Gov-ernment Entities). However, other per-sonnel from the Service and the TreasuryDepartment participated in its develop-ment. For further information regardingthis notice, contact Ms. Lennon at (202)622-6030 (not a toll-free telephone num-ber).

26 CFR 1.1503–2 Dual consolidated loss.26 CFR 301.7121–1 Closing agreements.

Rev. Proc. 2000–42

SECTION 1. PURPOSE

This revenue procedure informs tax-payers of the information they must sub-mit to request a closing agreement under§1.1503–2(g)(2)(iv)(B)(2)(i) to preventthe recapture of dual consolidated losses(DCLs) upon the occurrence of certaintriggering events.

Before this revenue procedure, the In-ternal Revenue Service and the Depart-ment of the Treasury had not specified indetail how taxpayers should request these

2000–43 I.R.B. 395 October 23, 2000

closing agreements. The Service andTreasury are issuing this revenue proce-dure to provide taxpayers with guidanceon the information and representationsthey should include in a §1503(d) closingagreement request and to facilitate theprocess and reduce the time necessary forthe Service to process requests.

Appendix A to this revenue procedureis a model closing agreement. The Ser-vice intends the model closing agreementto serve as an example of the format andcontents of a §1.1503–2(g)(2)(iv)(B)(2)(i)closing agreement and to aid taxpayers inunderstanding how the information re-quired by this revenue procedure will beused in the closing agreement. Taxpayersshould note, however, that the modelagreement is only an example. A tax-payer’s actual agreement could differfrom the model. Finally, Appendix B is aflow chart of the entities included in themodel closing agreement, along withnotes explaining the model agreement.

SECTION 2. BACKGROUND

The United States taxes the worldwideincome of domestic corporations. TheUnited States allows certain domestic cor-porations to file consolidated returns withother affiliated domestic corporations.When two or more domestic corporationsfile a consolidated return, losses that onecorporation incurs generally may reduceor eliminate tax on income that anothercorporation earns.

Because other countries may apply dif-ferent standards for determining the resi-dence and taxability of a corporation (e.g.,based on the management and control ofthe corporation), some domestic corpora-tions are dual resident corporations and, assuch, are also subject to the income tax ofa foreign country on their income on a res-idence basis (and not on a source basis).Foreign countries often have provisionsthat permit commonly owned entities tocombine their income and losses throughconsolidation or some other form of com-bined reporting for income tax purposes.

Prior to the Tax Reform Act of 1986, ifa dual resident corporation were a residentof a foreign country with tax laws that per-mitted the losses of the corporation to beused to offset the income of another per-son (e.g., under a consolidated return pro-vision), then the dual resident corporationcould use any losses it generated twice:

once to offset the income of affiliates resi-dent in the United States (but not abroad),and again to offset the income of its affili-ates resident only in the other country.Thus, such a dual resident corporationcould use a single economic loss to offsettwo separate items of income in two juris-dictions. Congress expressed concernsthat this dual use of a loss could result inan undue tax advantage to certain foreigninvestors that made investments in domes-tic corporations, and could create anundue incentive for certain foreign corpo-rations to acquire domestic corporationsand for domestic corporations to acquireforeign rather than domestic assets. Staffof Joint Committee on Taxation, 99th

Cong., 2nd Sess., General Explanation ofthe Tax Reform Act of 1986, at 1064 –1065 (1987). As part of the Tax ReformAct of 1986, Congress responded by en-acting §1503(d) to prevent the use ofDCLs that resulted from consolidation inmultiple jurisdictions.

The Treasury and Service issued tempo-rary regulations under §1503(d) in 1989(T.D. 8261, 1989–2 C.B. 220), and finalregulations in 1992 (T.D. 8434, 1992–2C.B. 240). The final regulations in§1.1503–2 are generally effective for tax-able years beginning on or after October 1,1992; the temporary regulations in§1.1503–2A are effective for taxable yearsbeginning after December 31, 1986, andbefore October 1, 1992. The temporaryregulations were initially designated as§1.1503–2T, but were redesignated as§1.1503–2A by the final regulations.

Section 1503(d) provides that a DCL ofa dual resident corporation shall not be al-lowed to reduce the taxable income of anyother member of the corporation’s affili-ated group for any taxable year. The termdual resident corporation includes a do-mestic corporation that is subject to the in-come tax of a foreign country on itsworldwide income or on a residence basisand a separate unit of a domestic corpora-tion (e.g., a foreign branch, an interest in apartnership, an interest in a trust, or a dis-regarded entity that a foreign countrytaxes at the entity level). SeeTreas. Reg.§1.1503–2(c)(2) – (4). This revenue pro-cedure will collectively refer to dual resi-dent corporations and separate units as“DRCs.”

The final §1503(d) regulations permit ataxpayer to elect to use a DCL of a DRC

by entering into an agreement under§1.1503–2(g)(2)(i) in which the taxpayercertifies that the DCL has not been, andwill not be, used to offset the income ofanother person under the laws of a foreigncountry. Certain subsequent events,known as “triggering events” require thetaxpayer to recapture the losses as income,including an interest charge. Treas. Reg.§§1.1503–2(g)(2)(iii) and (vii). If a tax-payer fails to comply with the §1503(d)recapture provisions upon the occurrenceof a triggering event, then the DRC (or asuccessor-in-interest) that incurred theDCL generally will not be eligible for re-lief to use any DCLs incurred in the five(5) taxable years beginning with the yearin which recapture is required. Treas.Reg. §1.1503–2(g)(2)(vii)(F)(1).

Triggering events occur when: (1) anyportion of the loss taken into account incomputing the DCL is used by any meansto offset the income of any other personfor foreign tax purposes within fifteen(15) years; (2) a DRC or domestic ownerof a separate unit ceases to be a memberof the consolidated group that filed theagreement at a time when there is a con-tinuing ability to use the DCL to offset in-come of another person for foreign taxpurposes; (3) an unaffiliated DRC or un-affiliated domestic owner of a separateunit becomes a member of a consolidatedgroup, unless there is no continuing abil-ity to use the DCL to offset income of an-other person for foreign tax purposes; (4)a DRC transfers its assets to a transfereein a transaction that results, under thelaws of a foreign country, in a carryoverof the losses, expenses, or deductions thatmake up the DCL; (5) a domestic ownerof a separate unit disposes of fifty (50)percent or more of the assets of, or its in-terest in, the separate unit at a time whenthere is a continuing ability to use theDCL to offset income of another personfor foreign tax purposes; (6) an unaffili-ated DRC or unaffiliated domestic ownerof a separate unit becomes a foreign cor-poration in a transaction that, for foreigntax purposes, is not treated as involving atransfer of assets to a new entity, unlessthere is no continuing ability to use theDCL to offset income of another personfor foreign tax purposes; or (7) the tax-payer fails to file an annual certificationrequired under §1.1503–2(g)(2)(vi)(B).Treas. Reg. §1.1503–2(g)(2)(iii)(A).

October 23, 2000 396 2000–43 I.R.B.

The final regulations provide two ex-ceptions to events described as triggeringevents, making the events not triggeringevents requiring recapture of losses andan interest charge. The first exception,under §1.1503–2(g)(2)(iv)(A), applieswhen a DRC, or its assets, is acquired byanother member of the DRC’s consoli-dated group. The second exception,under §1.1503–2(g)(2)(iv)(B), applies,provided the taxpayer enters into a clos-ing agreement, when a DRC or a domes-tic owner of a separate unit becomes dis-affiliated from its consolidated group, orwhen an unaffiliated domestic corpora-tion or new consolidated group acquiresthe DRC or its assets.

The Service is aware that as a result oftaxpayers’ ability to elect entity classifica-tion under the §7701 elective Federal taxclassification regulations that became ef-fective as of January 1, 1997 (i.e., thecheck-the-box regulations), the number ofDRCs may increase, and taxpayers maybecome subject to the §1503(d) DCL pro-visions, including the recapture provi-sions. For instance, the conversion of aforeign branch to a foreign corporationmay be treated as a triggering event underthe final §1503(d) regulations. SeeTreas.Reg. §§1.1503–2(g)(2)(iii)(A)(4) – (7)and Treas. Reg. §301.7701–3(g)(1).Therefore, this procedure is also intendedto publicize the Service’s procedures andrequirements that will prevent certain re-organization and disposition transactionsinvolving DRCs from resulting in§1503(d) recapture consequences.

SECTION 3. SCOPE

.01 General.

This section provides the conditionsthat must be satisfied for the Service toconsider requests from taxpayers for a§1.1503–2(g)(2)(iv)(B)(2)(i) closingagreement.

.02 Taxpayers Must Be InCompliance And Must FirstRequest Any Treas. Reg.§301.9100 Relief Needed.

Before requesting a closing agreementunder §1.1503–2(g)(2)(iv)(B)(2)(i), thetaxpayer should ensure that it has com-plied with the regulations issued under§1503(d), including having filed the req-

uisite agreements, elections, and certifica-tions under §1.1503–2(g)(2) (or§1.1503–2A(c)(3) or (d)(3) if the tax-payer is asking for relief under§1.1503–2A). See infra, section 3.07(which provides when the Service willconsider including in a §1.1503–2(g)(2)(iv)(B)(2)(i) closing agreement, DCLscovered by the temporary §1503(d) regu-lations). In practical terms, this meansthat the taxpayer should first request andsecure (or at least simultaneously request)any necessary relief under §301.9100 foran extension of time to make any requiredelection or application under the §1503(d)regulations. For example, a taxpayer thathas not filed the requisite agreements andelections under §1.1503–2(g)(2)(i) mustfirst request (or simultaneously request)§301.9100 relief to file the elections andagreements.

Under §§1.1503–2(g)(2)(iii)(A) and(iv)(B), a taxpayer must enter into a clos-ing agreement with the Service before thetaxpayer files its tax return for the taxableyear of a triggering event to prevent therecapture of losses and the accompanyinginterest charge. Under this revenue pro-cedure, however, a taxpayer can preventthe recapture of losses and the interestcharge if the taxpayer submits its requestfor a closing agreement by the due date ofits tax return (including extensions) forthe triggering event year and specifies onits tax return that it is requesting a§1503(d) closing agreement.

.03 Statutes Of Limitations.

The Service may request a taxpayer toexecute a consent to extend the period oflimitations for assessment of tax for thetaxable periods related to the DCLs forwhich the taxpayer has requested a clos-ing agreement.

.04 When And By Whom A ClosingAgreements May Be Executed.

Treas. Reg. §1.1503–2(g)(2)(iv)(B)(1)provides that if the requirements of§1.1503–2(g)(2)(iv)(B)(2) are met, thefollowing events will not constitute trig-gering events requiring the recapture ofDCLs: (1) an affiliated DRC or an affili-ated domestic owner becomes an unaffili-ated domestic corporation or a member ofa new consolidated group; (2) an unaffili-ated DRC or an unaffiliated domestic

owner becomes a member of a consoli-dated group; (3) assets of a DRC are ac-quired by an unaffiliated domestic corpo-ration or a member of a new consolidatedgroup; or (4) a domestic owner of a sepa-rate unit transfers its interest in the sepa-rate unit to an unaffiliated domestic cor-poration or to a member of a newconsolidated group. Treas. Reg.§1.1503–2(g)(2)(iv)(B)(2) requires(among other requirements) that the tax-payers enter into a closing agreement withthe Service which provides that the tax-payers will be jointly and severally liablefor the total amount of the recapture of theDCLs and an interest charge upon anysubsequent triggering event.

The Service may execute a closingagreement under §1.1503–2(g)(2)(iv)(B)(2)(i) and §7121 with the followingtaxpayers: (1) the consolidated group(i.e., the parent on behalf of the consoli-dated group), the unaffiliated DRC, or theunaffiliated domestic owner that filed the§1.1503–2(g)(2)(i) agreement for the rel-evant DCLs, and (2) the unaffiliated do-mestic corporation or the new consoli-dated group, provided the requirements of§1.1503–2(g)(2)(iv)(B) are satisfied.This revenue procedure will refer to thesetaxpayers as the “Taxpayer Parties.” Au-thorized officers of the Taxpayer Partiesmust sign the closing agreement (gener-ally two originals per party to the agree-ment).

.05 Taxpayers That Cannot Execute AClosing Agreement.

The Service will not execute a§1.1503–2(g)(2)(iv)(B)(2)(i) closingagreement with foreign entities/transfer-ees, individuals, or partnerships. Section1.1503–2 does not provide for closingagreements with such taxpayers.

.06 Losses Must Be DCLs.

The Service will not execute a closingagreement with taxpayers for net operat-ing losses (NOLs) that are not DCLs.Therefore, taxpayers must represent thatthe losses at issue are DCLs.

.07 Closing Agreements For LossesUnder The TemporaryRegulations.

The final regulations provide for tax-payers to enter into a §1.1503–2(g)(2)-

2000–43 I.R.B. 397 October 23, 2000

(iv)(B)(2)(i) closing agreement with theService to prevent certain events from re-sulting in recapture and an interestcharge; the temporary regulations do notcontain such a provision. In appropriatecircumstances, taxpayers may elect toapply the final regulations to DCLs whichare otherwise subject to §1.1503–2A.Treas. Reg. §1.1503–2(h). If a taxpayerfiles a request to enter into a closingagreement for losses covered by the finalregulations, under this revenue procedure,the Service will consider a request to in-clude in the closing agreement DCLs oth-erwise covered by §1.1503–2A for whichthe taxpayer has not made a §1.1503–2(h)election to apply the final regulations.This revenue procedure’s reference to“representations and citations as appropri-ate under §1.1503–2A,” means represen-tations and citations related to a DCL cov-ered by §1.1503–2A.

SECTION 4. PROCEDURE TO ENTERINTO A CLOSING AGREEMENT

.01 General.

The first revenue procedure publishedeach year (the Annual Revenue Proce-dure) outlines the general procedures ofthe Service for the issuance of letter rul-ings and determination letters, includingclosing agreements entered into under theauthority of §7121, by the National Of-fice. See, e.g., Rev. Proc. 2000–1,2000–1 I.R.B. 4. Taxpayers should notethat the Service also publishes an annualrevenue procedure, generally in the firstInternal Revenue Bulletin of the year,which provides a list of those areas of theCode under the jurisdiction of the Associ-ate Chief Counsel (International), forwhich the Service will not issue advanceletter rulings, (e.g., certain §1503(d) de-terminations, such as whether the condi-tions for excepting losses of a DRC fromthe definition of a DCL are satisfied).See, e.g., Rev. Proc. 2000–7, 2000–1I.R.B. 227.

The consolidated group (i.e., the parenton behalf of the consolidated group), theunaffiliated DRC, or the unaffiliated do-mestic owner that filed the agreementsunder §1.1503–2(g)(2)(i) for the DCLsfor which the closing agreement wouldrelate may file a request to enter into a§1.1503–2(g)(2)(iv)(B)(2)(i) closingagreement by following the procedures

of the most recent Annual Revenue Pro-cedure and this revenue procedure. Tax-payers must include the user fee requiredby the most recent Annual Revenue Pro-cedure.

.02 Additional Information.

Because the information, representa-tions, and documentation necessary toenter into a closing agreement depend onall the facts and circumstances, the Ser-vice may require information, representa-tions, and documentation in addition tothat set forth in this revenue procedureand the most recent Annual Revenue Pro-cedure. Taxpayers should submit suchadditional information in accordance withthe Annual Revenue Procedure and withinthe time allowed by the Annual RevenueProcedure. If a taxpayer does not submitthe information requested within the timeprovided, the request will be closed andthe taxpayer will be notified in writing.See, e.g., section 10.06(3), Rev. Proc.2000–1. If while processing a taxpayer’srequest for a §1503(d) closing agreement,the Service determines that the taxpayer isnot in compliance with the §1503(d) regu-lations and needs relief under §301.9100to obtain an extension of time to make arequired election or application under the§1503(d) regulations, then the taxpayerhas thirty (30) days from the date the Ser-vice notifies the taxpayer to file a requestfor relief under §301.9100. If a taxpayerdoes not submit the §301.9100 requestwithin the thirty-day period, the§1.1503–2(g)(2)(iv)(B)(2)(i) closingagreement request will be closed and thetaxpayer will be notified in writing.

Taxpayers are responsible for keepingthe Service informed of all materialchanges to the information, representa-tions, and documentation submitted aspart of the closing agreement request.

SECTION 5. INFORMATIONTAXPAYERS MUST INCLUDE INREQUEST

.01 General.

This section describes the information,representations, and documentation thattaxpayers are expected to provide with a§1.1503–2(g)(2)(iv)(B)(2)(i) closingagreement request. Taxpayers should or-ganize information and representations

following the format of this procedureand should use appropriate descriptiveheadings. To facilitate the processing ofthe closing agreement request, taxpayersmust also provide a full statement of allrelevant facts related to the taxpayers andthe DCLs.

Taxpayers must address each item inthis section, providing all relevant facts.If an item is not applicable, taxpayersshould so state and briefly explain why.

.02 Information Related To TaxpayerParties, Relevant Members OfThe Consolidated Group, AndDRCs.

Taxpayers must provide a full state-ment of the facts, including the followinggeneral information, as appropriate, abouteach Taxpayer Party, relevant member ofthe consolidated group, and DRC withlosses that will be covered by the closingagreement.

1. Name, address, and employer iden-tification number.

2. Type of entity, and date and place ofincorporation or other formation.

3. Information about the formation andtreatment of disregarded entities di-rectly or indirectly owned by a Tax-payer Party (including the date theentity became or elected to becomea disregarded entity under§301.7701–3).

4. Classifications of the entity under§1.1503–2(c)(2) – (4) (e.g., dualresident corporation, foreign branchseparate unit, hybrid entity separateunit) before and after any triggeringevent. If the taxpayer is requestingthat the closing agreement includelosses covered by the temporaryregulations, the taxpayer shouldclassify the entity under§1.1503–2A(b) (e.g., dual residentcorporation, foreign branch separateunit, partnership interest separateunit).

5. Detailed explanation of the chain ofownership between the parent of theconsolidated group (or in the casewhere there is no U.S. consolidatedgroup, the unaffiliated domesticowner of the DRC) and the DRC be-fore and after any triggering event(as described in §1.1503–2(g)(2)(iii)or §1.1503–2A(c)(3)(iii), as appro-priate).

October 23, 2000 398 2000–43 I.R.B.

6. The taxable year of a TaxpayerParty to the closing agreement (bothbefore and after any triggeringevent). If as a result of a triggeringevent there is a requirement for fil-ing a short-period return under§1.1502–76(b) or other relevantprovision, taxpayer should providerelated information and an explana-tion.

7. The office that has jurisdiction overthe Federal income tax returns of aTaxpayer Party to the closing agree-ment.

.03 Additional Information RelatedTo DRCs.

Taxpayers must provide the followingadditional information for each DRC withlosses that will be covered by the closingagreement:

1. The country or countries that tax theDRC on its worldwide income or ona residence basis. If the DRC is aseparate unit, identify the separateunit and name under which it con-ducts business, and the country inwhich its principal place of businessis located.

2. Description of the principal busi-ness activity.

3. Amounts and taxable years ofDRC’s NOLs.

4. Date the period of limitations on as-sessment of tax expires related toeach DCL.

.04 List And Description Of AllTriggering Events.

For all losses to be included in the§1.1503–2(g)(2)(iv)(B)(2)(i) closingagreement, taxpayers must provide a listand description of all triggering eventsdescribed in §1.1503–2(g)(2)(iii) and§1.1503–2A(c)(3)(iii) as appropriate (in-cluding specific citations). In particular,taxpayers should explain how the trigger-ing events are treated under the Code, in-cluding information about any taxabletransfers or any nonrecognition provi-sions that apply, and should provide infor-mation about all parties, stock, and assetsinvolved. Taxpayers should indicatewhether any triggering event listed in-cludes a transaction within the meaning of§1.1502–75(d)(2) or (3) whereby thecommon parent of the consolidated groupthat filed the §1.1503–2(g)(2)(i) agree-

ments is no longer in existence orwhereby the common parent was a partyto a reverse acquisition, through whichthe consolidated group continues.

Taxpayers should state whether an ex-ception to a triggering event applies andshould explain the exception in detail andinclude a citation to the relevant provision(e.g., §1.1503–2(g)(2)(iv)(A), §1.1503–2(g)(2)(iv)(B), or §1.1503–2A(c)(3)(vi)).If a taxpayer has exercised rebuttal rightsprovided in §§1.1503–2(g)(2)(iii)(A)(2) –(7), taxpayer must provide informationrelated to those rebuttals.

.05 Specific Representations AndAgreements Required For ClosingAgreement.

Taxpayers must provide the followingrepresentations and agreements, when ap-plicable, to secure a §1.1503–2(g)(2)(iv)(B)(2)(i) closing agreement:

1. That a corporation is a DRC as de-scribed in §1.1503–2(c)(2). Taxpay-ers must provide a representation foreach relevant entity, and provide a§1.1503–2A representation as appro-priate.

2. That a foreign branch, interest in apartnership, or interest in a trust is aseparate unit as described in the ap-propriate subsection of §1.1503–2(c)(3) and a DRC as described in§1.1503–2(c)(2). Taxpayers mustprovide a representation for each rel-evant entity, and provide a§1.1503–2A representation as appro-priate.

3. That a hybrid entity separate unit is ahybrid entity separate unit as de-scribed in §1.1503–2(c)(4) and aDRC as described in §1.1503–2(c)(2). Taxpayers must provide arepresentation for each relevant en-tity, and provide a §1.1503–2A repre-sentation as appropriate.

4. That the NOLs described are DCLsunder §1.1503–2(c)(5) (or under§1.1503–2A(b)(2) as appropriate).

5. That the requisite elections, agree-ments, and certifications were timelymade under §1.1503–2(g)(2)(i) (or§1.1503–2A(c)(3) or (d)(3) as appro-priate).

6. That the DCLs were computed as re-quired under §1.1503–2(d)(1) (or§1.1503–2A(f)(1) as appropriate).

7. That the necessary reporting and cer-

tifications were made under§1.1503–2(g)(2)(vi) (or §1.1503–2A(c)(3)(v) as appropriate).

8. That the consolidated group, unaffili-ated DRC, or unaffiliated domesticowner will or has filed an electionand agreement described in§1.1503–2(g)(2)(i) with its timelyfiled Federal income tax return forthe year(s) of the triggering event(s)described in §1.1503–2(g)(2)(iii).Taxpayers should provide a§1.1503–2A representation as appro-priate.

9. That apart from the triggering eventslisted, no triggering event describedin §1.1503–2(g)(2)(iii) (or§1.1503–2A(c)(3)(iii) as appropriate)has occurred applicable to the DCLs.

10. That upon any subsequent trigger-ing event described in §1.1503–2(g)(2)(iii), the Taxpayer Parties will bejointly and severally liable for thetotal amount of the recapture of theDCLs to which the closing agree-ment relates and the related interestcharge under §1.1503–2 (g)(2)(vii),to the extent the triggering eventdoes not fall under one of the excep-tions provided in §1.1503–2(g)(2)(iv)(A) or (B).

11. That the new consolidated group orunaffiliated domestic corporationwill treat any potential recapture ofthe DCLs under §1.1503–2(g)(2)(vii) as unrealized built–in gainfor purposes of §384(a), subject toany applicable exceptions thereun-der, and will treat the total recaptureamount of the described DCLs asrecognized built-in gain for pur-poses of §384(a), subject to any ap-plicable exceptions thereunder.

12. That the new consolidated groupor unaffiliated domestic corpora-tion will comply with the reportingrequirements described in§1.1503–2(g)(2)(vi) for each DCLfor the taxable years covered bythe closing agreement.

13. That an election was made (or wasnot made) under §1.1503–2(h)(2)or (3) for any DCLs incurred intaxable years beginning before Oc-tober 1, 1992. Taxpayers shouldprovide an explanation for theelection provision used.

14. That an event described in

2000–43 I.R.B. 399 October 23, 2000

§§1.1503–2(g)(2)(iii)(A)(2) – (7) isnot a triggering event under suchprovision because the transfer didnot result in a carryover under for-eign law of such losses, or becausesuch losses cannot be used to offsetthe income of another person underforeign law. Taxpayers should rep-resent the specific requirementsunder the provision cited. See, e.g.,section 3.01(4) and section4.01(22), Rev. Proc. 2000–7 (theNational Office of the Service gen-erally will not make a determinationrelated to the rebuttals).

.06 Documents Required.

As part of the initial submission request-ing a §1.1503–2(g)(2)(iv)(B)(2)(i) closingagreement, taxpayers must provide the fol-lowing documents when applicable:

1. Copies of all elections, agreementsand certifications required by§1.1503–2(g)(2) (or §1.1503–2A(c)(3) or (d)(3)).

2. Copies of all ruling letters issued bythe Service under §301.9100 provid-ing for an extension of time to makea required election or applicationunder the §1503(d) regulations.

3. Copy of all consents to an extensionof the statute of limitations on assess-ment and collection.

4. Documents supporting the rebuttal ofa presumption of a triggering eventdescribed in §§1.1503–2(g)(2)(iii)(A)(2) – (7).

5. Other documents as requested by theService.

SECTION 6. PAPERWORKREDUCTION ACT

The collection of information containedin this revenue procedure has been re-viewed and approved by the Office ofManagement and Budget in accordancewith the Paperwork Reduction Act (44U.S.C. 3507) under control number 1545-1706.

An agency may not conduct or sponsor,and a person is not required to respond to,a collection of information unless the col-lection of information displays a validOMB control number.

The collection of information is con-tained in sections 4 and 5 of this revenueprocedure. This information will enablethe Service to determine whether to exe-

cute a closing agreement under §§1503(d)and 7121 of the Code. The likely respon-dents are domestic corporations.

The estimated average annual reportingand/or recordkeeping burden is two-thou-sand (2,000) hours.

The estimated average annual burdenper applicant is one-hundred (100) hours.The estimated number of applicants istwenty (20). The estimated frequency ofresponses is on occasion.

Books and records relating to a collec-tion of information must be retained aslong as their contents may become mater-ial in the administration of any internalrevenue law. Generally, tax returns and taxreturn information are confidential, as re-quired by 26 U.S.C. 6103.

SECTION 7. DRAFTINGINFORMATION

The principal author of this revenue pro-cedure is Camille B. Evans of the Office ofthe Associate Chief Counsel (Interna-tional). For further information regardingthis revenue procedure contact Camille B.Evans or Kenneth D. Allison of the Officeof the Associate Chief Counsel (Interna-tional) at (202) 622-3860 (not a toll freecall).

Appendix A

DEPARTMENT OF THE TREASURYINTERNAL REVNUE SERVICE

MODEL CLOSING AGREEMENT ONFINAL DETERMINATION

COVERING SPECIFIC MATTERS

Under section 7121 of the Internal Rev-enue Code of 1986, as amended (theCode), Corporation A, 123 Main Street,Wilmington, DE 20000, EIN 11-1234567,a domestic corporation, as common parenton behalf of all the members of a consoli-dated group (the Corporation A Group);Corporation B, 124 Main Street, Wilming-ton, DE 20000, EIN 22-1234567, a do-mestic corporation, as common parent onbehalf of all the members of a consolidatedgroup as of January 1, Year 3 (the Corpora-tion B Group); and the Commissioner ofInternal Revenue hereby make the follow-ing closing agreement (Closing Agree-ment) based on the representations madeby Corporation A and Corporation B, in

paragraphs one (1) through fourteen (14)below:

WHEREAS:

(1) Corporation A, a Delaware corpora-tion and party to this Closing Agreement,owned through December 31, Year 2, all ofthe stock of Corporation B, a Delawarecorporation and party to this ClosingAgreement. Until December 31, Year 2,Corporation A had outstanding Class Xcommon stock and Class Y common stock.Corporation A is the common parent of anaffiliated group of corporations that files aconsolidated federal income tax return on acalendar year basis (the Corporation AGroup). Corporation B was a member ofthe Corporation A Group through Decem-ber 31, Year 2. On January 1, Year 3, Cor-poration B became the common parent ofan affiliated group of corporations thatfiles a consolidated federal income tax re-turn on a calendar year basis (the Corpora-tion B Group).

(2) Corporation B owns all of the stockof Corporation D, a Delaware corporation(EIN 33-1234567) and a member of theCorporation A Group through December31, Year 2, and of Corporation E, aDelaware corporation (EIN 44-1234567)and a member of the Corporation A Groupthrough December 31, Year 2. Corpora-tion D and Corporation E became mem-bers of the Corporation B Group on Janu-ary 1, Year 3.

(3) Since 1970, Corporation D hasmaintained assets and operated a widgetsbusiness in Country 1 through a branch inCountry 1 (Branch 1). Branch 1 is a sepa-rate unit as described in Treas. Reg.§1.1503–2(c)(3)(i)(A) and a dual residentcorporation (DRC) as defined in Treas.Reg. §1.1503–2(c)(2).

(4) Since 1970, Corporation E hasmaintained assets and operated a widgetsbusiness in Country 2 through a branch inCountry 2 (Branch 2). Branch 2 is a sepa-rate unit as described in Treas. Reg.§1.1503–2(c)(3)(i)(A) and a DRC as de-fined in Treas. Reg. §1.1503–2(c)(2).

(5) Since 1975, Corporation E hasmaintained assets and operated a widgetsbusiness in Country 3 through a branch in

October 23, 2000 400 2000–43 I.R.B.

The Corporation B Branches’ NOLs forthe Year 1 taxable year and the Year 2taxable year will hereinafter collectivelybe referred to as the Corporation BBranches NOLs.

(12) The Corporation A Group usedall of the Corporation B Branches NOLswithin the meaning of Treas. Reg.§1.1503–2(c)(15).

(13) Corporation A, as common par-ent of the Corporation A Group, filed theelections and agreements described inTreas. Reg. §1.1503–2(g)(2)(i) for theCorporation B Branches NOLs incurred

for the Year 1 taxable year and the Year2 taxable year.

(14) Excluding the distribution ofCorporation B stock to the CorporationA Class X common stockholders in aCode §355 split-off transaction, on De-cember 31, Year 2, (as described in para-graph 9 above), causing Corporation Band its affiliates to cease being membersof the Corporation A Group, no trigger-ing event described in Treas. Reg.§1.1503–2 (g)(2)(iii) has occurred thatis appl icable to the Corporation BBranches NOLs.

THEREFORE, based on the above infor-mation and material submitted by Corpo-ration A and Corporation B in connectionwith this Closing Agreement, and in theabsence of other material factual or legalcircumstances concerning the events de-scribed above, it is determined for federalincome tax purposes that with respect tothe Corporation B Branches NOLs:

(1) This Closing Agreement is a clos-ing agreement described in Treas. Reg.§1.1503–2(g)(2)(iv)(B)(2)(i).

(2) The Corporation B Branches areseparate units as described in Treas. Reg.

Country 3 (Branch 3). Branch 3 is a sepa-rate unit as described in Treas. Reg.§1.1503–2(c)(3)(i)(A) and a DRC as de-fined in Treas. Reg. §1.1503–2(c)(2).

(6) Since 1972, Corporation E hasmaintained assets and operated a widgetsbusiness in Country 4 through a branch inCountry 4 (Branch 4). Branch 4 is a sepa-rate unit as described in Treas. Reg.§1.1503–2(c)(3)(i)(A) and a DRC as de-fined in Treas. Reg. §1.1503–2(c)(2).

Branch 1, Branch 2, Branch 3, andBranch 4 will hereinafter collectively bereferred to as the “Corporation BBranches.”

(7) The income and losses of Branch 4were included in the Corporation A Groupthrough Date A, Year 2. The income andlosses of Branch 1, Branch 2, and Branch3 were included in the Corporation AGroup through December 31, Year 2.

(8) On Date A, Year 2, Corporation E,sold all of the assets of Branch 4 to an un-related Country 4 company, Corporation4. Corporation E’s sale of Branch 4’s as-sets is not a triggering event under Treas.Reg. §1.1503–2(g)(2)(iii)(A)(5) becausethe sale did not result in a carryover under

Country 4 law of Branch 4’s losses, ex-penses, or deductions to Corporation 4.As a result of this Date A, Year 2 sale,Branch 4 ceased to be a separate unit asdescribed in Treas. Reg.§1.1503–2(c)(3)(i)(A) and a DRC as de-fined in Treas. Reg. §1.1503–2(c)(2). SeeAppendix B, Note 1.

(9) On December 31, Year 2, Corpora-tion A distributed all of the stock of Cor-poration B to its Corporation A Class Xcommon stockholders in exchange for allof the Corporation A Class X commonstock in a split-off transaction describedin Code §355. As a result of this split-offtransaction: (a) Corporation B, Corpora-tion D, and Corporation E, and the in-come and losses of Branch 1, Branch 2,and Branch 3 ceased to be included in theCorporation A Group; (b) Corporation Bbecame the common parent of the Corpo-ration B Group; and (c) the income andlosses of Branch 1, Branch 2, and Branch3 became included with the CorporationB Group. See Appendix B, Note 2.

(10) On Date C, Year 3, Corporation Esold the Branch 3 assets to an unrelatedCountry 3 company, Corporation 3. Cor-poration E’s sale of Branch 3’s assets isnot a triggering event under Treas. Reg.

§1.1503–2(g)(2)(iii)(A)(5) because thesale did not result in a carryover under thelaws of Country 3 of Branch 3’s losses,expenses, or deductions to Corporation 3.As a result of this Date C, Year 3 sale,Branch 3 ceased to be a separate unit asdescribed in Treas. Reg.§1.1503–2(c)(3)(i)(A) and a DRC as de-fined in Treas. Reg. §1.1503–2(c)(2). SeeAppendix B, Note 3.

(11) The Corporation B Branches in-curred net operating losses (NOLs) for theYear 1 taxable year and the Year 2 taxableyear. Such losses were computed in ac-cordance with Treas. Reg. §1.1503–2(d)(1) and are as follows:

BRANCH Year 1 Tax Year Year 2 Tax YearBranch 1 $ $Branch 2 $ $Branch 3 $ $Branch 4 $ $ N.A. * TOTAL $ $

*See Appendix B, Note 4.

2000–43 I.R.B. 401 October 23, 2000

§1.1503–2(c)(3)(i)(A) and are dual resi-dent corporations as defined in Treas.Reg. §1.1503–2(c)(2).

(3) The Corporation B Branch NOLs aredual consolidated losses under Treas. Reg.§1.1503–2(c)(5).

(4) But for Treas. Reg. §1.1503–2(g)(2)(iv)(B)(2), the distribution of Corpo-ration B stock to the Corporation A Class Xcommon stockholders in a Code §355 split-off transaction, causing Corporation B,Corporation D, and Corporation E to ceasebeing members of the Corporation A Groupand the income and losses of the Corpora-tion B Branches to cease being included inthe Corporation A Group, was a triggeringevent under Treas. Reg.§1.1503–2(g)(2)(iii)(A)(2) requiring the re-capture of Corporation B Branch NOLs asrequired by Treas. Reg.§1.1503–2(g)(2)(vii).

(5) Under Treas. Reg. §1.1503–2(g)(2)(iv)(B)(2), the distribution of Corpo-ration B stock to Corporation A Class Xcommon stockholders in a Code §355 split-off transaction, whereby Corporation B,Corporation D, and Corporation E ceasedto be members of the Corporation A Groupand the income and losses of the Corpora-tion B Branches ceased to be included inthe Corporation A Group, is not consideredto be a triggering event requiring the recap-

ture of the Corporation B Branch NOLsand an interest charge.

(6) Upon any subsequent triggeringevent described in Treas. Reg.§1.1503–2(g)(2)(iii), the Corporation AGroup and the Corporation B Group will bejointly and severally liable for the totalamount of recapture of the dual consoli-dated losses of the Corporation B Branchesand the related interest charge under Treas.Reg. §1.1503–2(g)(2)(vii), to the extent thetriggering event does not fall under one ofthe exceptions provided in Treas. Reg.§1.1503–2(g)(2)(iv)(A) or (B). The charac-ter and source of the recapture amount shallbe determined pursuant to Treas. Reg.§1.1503-2(g)(2)(vii)(D). An event other-wise constituting a triggering event applica-ble to the Corporation B Branch NOLsunder Treas. Reg. §1.1503–2(g)(2)(iii)(A)shall not constitute a triggering event if itoccurs in any taxable year after the fifteenth(15th) taxable year following the year inwhich the Corporation B Branch NOLswere incurred.

(7) The Corporation B Group will treatany potential recapture amount underTreas. Reg. §1.1503–2(g)(2)(vii) as unreal-ized built-in gain for purposes of Code§384(a), subject to any applicable excep-tions thereunder, and such total recaptureamount shall constitute recognized built-ingain of the Corporation B Group for pur-

poses of Code §384(a), subject to any ap-plicable exceptions thereunder.

(8) The Corporation B Group will com-ply with the reporting requirements de-scribed in Treas. Reg. §1.1503–2 (g)(2)(vi)with respect to each Corporation B BranchNOL for the Year 1 taxable year and theYear 2 taxable year.

(9) If the amount of the Corporation BBranch NOLs is adjusted by the InternalRevenue Service, judicial authority, or oth-erwise in a final determination of taxes fortaxable years ending December 31, Year 1,and December 31, Year 2, the provisions ofthis Closing Agreement will apply mutatismutandisto such final adjusted lossamounts.

NOW THIS CLOSING AGREEMENTWITNESSETH, that Corporation A, Cor-poration B, and the Commissioner of Inter-nal Revenue hereby mutually agree to thedeterminations set forth above and furthermutually agree that those determinationsshall be final and conclusive, subject, how-ever, to reopening in the event of fraud,malfeasance, or misrepresentation of mate-rial fact, and provided that any change ormodification of applicable statutes or taxconventions shall render this ClosingAgreement ineffective to the extent that it isdependent upon such statutes or tax con-ventions.

IN WITNESS WHEREOF, by signing the foregoing, the above parties signify that they have read and agreed to the terms of thisdocument.

CORPORATION A

By: Date:

Title:

CORPORATION B

By: Date:

Title:

COMMISSIONER OF INTERNAL REVENUE

By: Date:

Title: Associate Chief Counsel (International)

By: Date:

Title: Director, International

October 23, 2000 402 2000–43 I.R.B.

2000–43 I.R.B. 403 October 23, 2000

October 23, 2000 404 2000–43 I.R.B.

Prohibition of Ex ParteCommunications BetweenAppeals Officers And OtherInternal Revenue ServiceEmployees

Rev. Proc. 2000–43

TABLE OF CONTENTS

SECTION 1. PURPOSE AND SCOPE

SECTION 2. BACKGROUND

SECTION 3. GUIDANCECONCERNING THE EX PARTECOMMUNICATIONS

PROHIBITION DESCRIBED INSECTION 1001(a)(4) OF THEINTERNAL REVENUE SERVICERESTRUCTURING AND REFORMACT OF 1998

SECTION 4. EFFECTIVE DATE

SECTION 1. PURPOSE AND SCOPE

Section 1001(a) of the Internal RevenueService Restructuring and Reform Act of1998, Pub. L. 105–206, 112 Stat. 685(RRA 98), states that “The Commissionerof Internal Revenue shall develop and im-plement a plan to reorganize the InternalRevenue Service. The plan shall ...

(4) ensure an independent appealsfunction within the Internal Rev-enue Service, including the prohibi-tion in the plan of ex parte commu-nications between appeals officersand other Internal Revenue Serviceemployees to the extent that suchcommunications appear to compro-mise the independence of the ap-peals officers.”

Notice 99–50, 1999–40 I.R.B. 444 (Octo-ber 4, 1999), set forth a proposed revenueprocedure concerning the ex parte com-munication prohibition. The proposedrevenue procedure provided guidance inthe form of a series of questions and an-swers that address situations frequentlyencountered by the Service during thecourse of an administrative appeal and in-vited public comment. The Departmentof the Treasury and the Internal Revenue

Service have considered all comments re-ceived, and the proposed revenue proce-dure has been modified to take into ac-count the concerns raised. Specifically,the scope of permissible communicationshas been clarified, limitations have beenplaced on communications between Ap-peals and certain employees in the Officeof Chief Counsel, concerns about com-munications that take place in the contextof multi-functional meetings have beenaddressed, and other questions and an-swers have been modified. In addition,new questions and answers have been in-cluded to define key terms and clarify re-sponsibilities of the parties, permit tax-payers/representatives to waive theprohibition, and to address certain man-agement issues.

SECTION 2. BACKGROUND

In 1927, the Internal Revenue Serviceestablished an administrative appealprocess to resolve tax disputes without lit-igation. The Appeals mission is to re-solve tax controversies, without litigation,on a basis that is fair and impartial to boththe Government and the taxpayer. LocalAppeals Officers have traditionally re-ported to different managers than the Ser-vice officials who proposed the adjust-ment. Appeals has historically been ableto settle the vast majority of the cases thatcome within its jurisdiction.