international business chapter nineteen the multinational finance function

TRANSCRIPT

International Business

Chapter Nineteen

The Multinational Finance Function

19-2

Chapter Objectives• To describe the multinational finance function and how it

fits in the MNE’s organizational structure• To show how companies can acquire outside funds for

normal operations and expansion• To explore how offshore financial centers are used to

raise funds and manage cash flows• To explain how companies include international factors in

the capital budgeting process• To discuss the major internal sources of funds available to

the MNE and to show how these funds are managed globally

• To explain how companies pay for exports and imports• To describe how companies protect against the major

finan-cial risks of inflation and exchange rate movements• To highlight some of the tax issues facing MNEs

19-3

Introduction

• The role of corporate financial manage- ment is to create and maintain economic value by maximizing shareholder wealth, i.e., the market value of existing share- holders’ common stock.

• The corporate finance function focuses upon the acquisition and allocation of financial resources among a firm’s activities and investments, i.e., short-term and long-term cash flows.

MNEs access both local and global capital markets to finance their current and future operations.

19-4

Financial Management ActivitiesActivities related to the management of

international cash flows include:• capital structure management: determining the

proper mix of debt and equity• long-term financing: selecting, issuing, and

managing long-term debt and equity capital, both at home and abroad

• capital budgeting: determining which projects in which countries will receive capital investment funds

• working capital management: properly managing the firm’s current assets and liabilities [cash, receivables, mar-ketable securities, inventory, trade receivables and payables, short-term bank debt]

19-5

Fig. 19.1: Finance in International Business

19-6

The Role of the Chief Financial Officer

Chief Financial Officer (CFO): the executive responsible for acquiring and allocating a firm’s financial resources

Financial resource acquisition (financing): internally or externally generating funds at the lowest possible cost

Financial resource allocation (investing): increasing shareholder wealth through the allocation of funds to selected projects and investment opportunities

• The CFO’s job becomes increasingly complex in a global environment because of foreign exchange risk,

cur- rency flows and restrictions, political and economic risk, differences in tax rates and laws, regulations regarding access to capital, etc.

19-7

Fig. 19.2: Location of the Treasury Function in the Corporate Organizational Structure

19-8

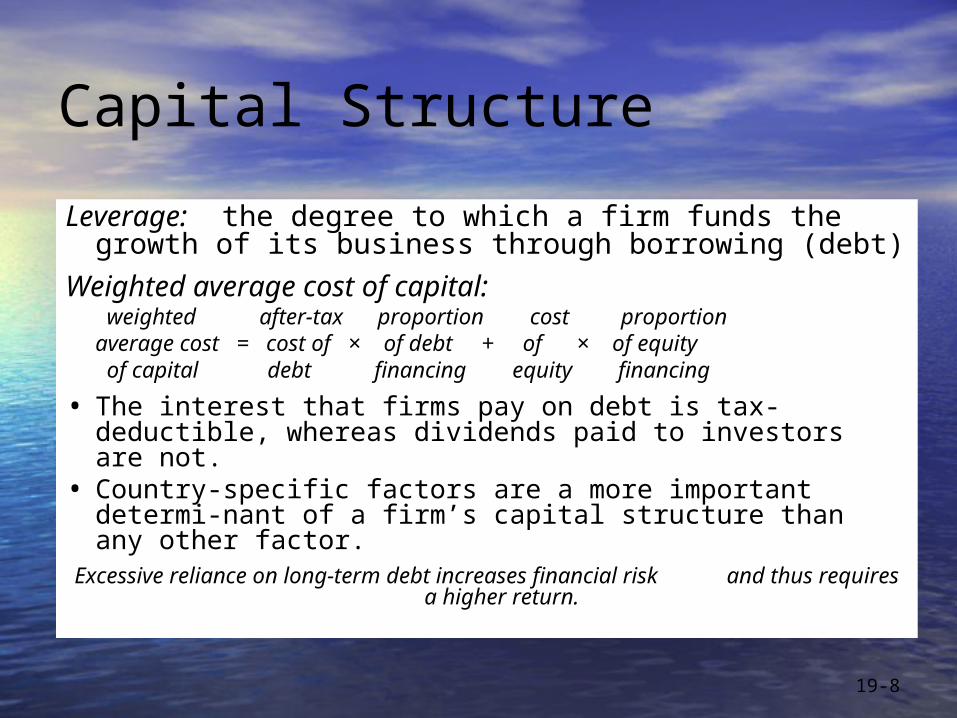

Capital Structure

Leverage: the degree to which a firm funds the growth of its business through borrowing (debt)

Weighted average cost of capital: weighted after-tax proportion cost proportionaverage cost = cost of × of debt + of × of equity of capital debt financing equity financing

• The interest that firms pay on debt is tax-deductible, whereas dividends paid to investors are not.

• Country-specific factors are a more important determi-nant of a firm’s capital structure than any other factor.

Excessive reliance on long-term debt increases financial risk and thus requires a higher return.

19-9

Capital Structures Around the World: Ranked by Common Equity Ratios, 1995

LONG- SHORT- TERM TERM

COUNTRY EQUITY TOTAL DEBT DEBTUnited Kingdom 68.3% 31.7% N/A N/AUnited States 48.4% 51.6% 26.8% 24.8%Canada 47.5% 52.5% 30.2% 22.7%Germany 39.7% 60.3% 15.6% 44.7%France 38.8% 61.2% 23.5% 43.0%Japan 33.7% 66.3% 23.3% 43.0%Italy 23.5% 76.5% 24.2% 52.3%Source: Scott Besley and Eugene F. Brigham, 2005. Essentials of Managerial Finance, 13th Ed.

19-10

Choice of Capital Structure

• A firm’s choice of capital structure depends upon:– tax rates– the degree of development of local equity markets– creditor rights

• MNEs have an advantage because they can tap local debt and equity markets, foreign debt and equity markets, and internal funds from the corporate family.

• Different tax rates, dividend remission policies, and foreign exchange controls may cause a firm to rely more on debt in some situations and more on equity in others.

The lack of the development of the bond and equity markets in Southeast Asia led to excessive dollar bank debt and was a major cause of the Asian financial crisis of

1997.

19-11

Offshore Financial CentersOffshore financing: the provision of financial services

by banks and other agents to nonresidents, i.e., the borrowing of money from and the lending of money to nonresidents

Offshore financial centers (OFCs): countries or city-states that (i) provide large amounts of funds in cur-rencies other than their own and thus are centers for the Eurocurrency market and (ii) are used as locations in which to raise and/or accumulate cash

• OFCs offer low or zero taxation, moderate or light financial regulation, and banking secrecy and anonymity.

The OECD is working to eliminate the harmful tax practices of tax-haven countries by improving their transparency and the effective exchange rate information they provide.

19-12

OFC Characteristics An offshore financial center possesses one or

more of the following characteristics:• a large foreign currency (Eurocurrency) market

for deposits and loans• a market that serves as a large, net supplier of

funds to the world’s financial markets• a market that serves as an intermediary or pass-

through for international loan funds• economic and political stability• an efficient and experienced financial community• good communications and supportive services• an official regulatory climate that is favorable to

the financial industry [continued]

19-13

OFCs are either:• operational centers, with extensive banking

activities involving short-term financial transactions[e.g., London, Singapore, Switzerland]

or

• booking centers, in which little banking activity takes place but where transactions are recorded to take advantage of secrecy laws and/or low or no tax rates [e.g., Bahrain, the Bahamas, the Cayman Islands,

the Netherlands Antilles]

Offshore financial centers offer a more flexible and less expensive source of funding for MNEs.

19-14

Capital BudgetingCapital budgeting: the process whereby firms

deter-mine which projects in which countries will receive capital investment funds

• MNEs determine their free cash flows based on cash flow estimates and tax rates in different countries as well as an appropriate required rate of return adjusted for risk.

• Capital budgeting techniques include:– payback period: the number of years required to

recover the original investment– the net present value of a project (NPV): the present

value of future cash outflows minus the present value of future cash inflows

– the internal rate of return (IRR): the rate that equates the present value of future cash flows with the present value of the initial investment

19-15

Capital Budgeting: Foreign Project Assessment

Unique capital budgeting aspects of foreign project assessment include:

• distinguishing parent cash flows from project cash flows

• accounting for the effects of legal and political con-straints on the movement and remittance of funds

• anticipating differing rates of inflation and exchange rate fluctuations

• evaluating potential economic and political risk• estimating the terminal value of a project

[continued]

19-16

Ways to deal with the variations in future cash flows in the capital budgeting process include:

• developing optimistic, most likely, and pessimistic scenarios

• adjusting the hurdle rate, i.e., the minimum required rate of return, for a project

Once a budget is complete, the return must be con-sidered in terms of both (i) local currency and (ii) the parent’s currency.

Finally, capital budgeting decisions must ultimately be made in the strategic context of related invest-ments, as well as their financial context.

19-17

Internal Sources of Funds

Funds: working capital, i.e., current assets minus current liabilities

• Internal sources of funds include:– operations: intercompany receivables and

payables, dividends– financing activities: securing loans, issuing bonds,

selling shares• Uses of funds include:

– the purchase of fixed assets – the purchase of materials and supplies– paying employee wages and benefits – investing in marketable securities and/or long-term

investments

19-18

Fig. 19.4: Internal Sources of Funds for MNEs

19-19

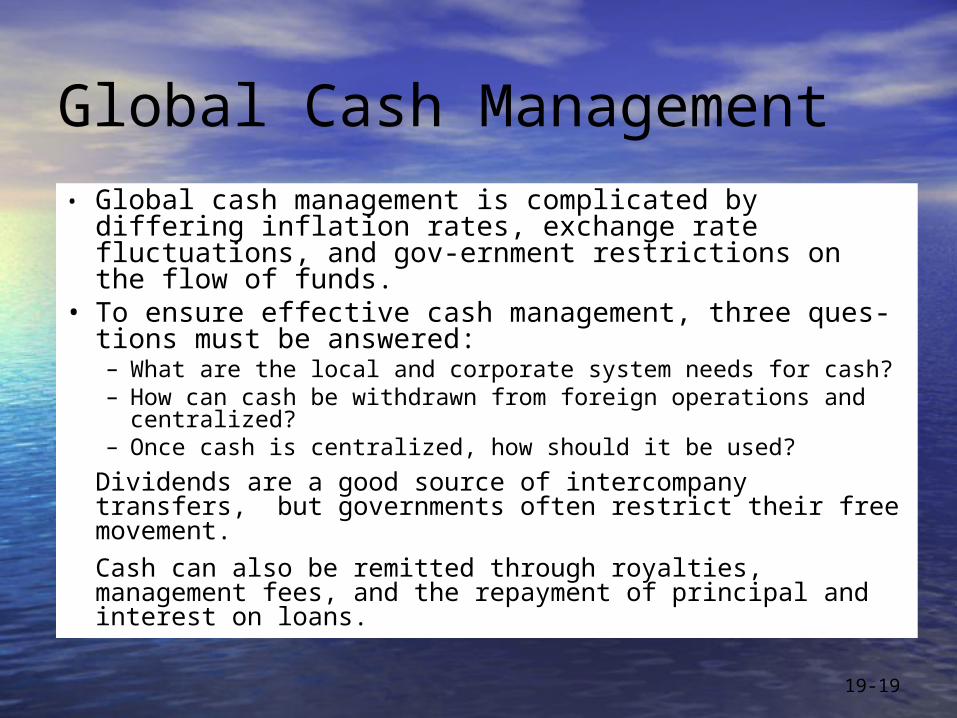

Global Cash Management• Global cash management is complicated by differing

inflation rates, exchange rate fluctuations, and gov-ernment restrictions on the flow of funds.

• To ensure effective cash management, three ques-tions must be answered:– What are the local and corporate system needs for cash?– How can cash be withdrawn from foreign operations and

centralized?– Once cash is centralized, how should it be used?

Dividends are a good source of intercompany transfers, but governments often restrict their free movement.

Cash can also be remitted through royalties, management fees, and the repayment of principal and interest on loans.

19-20

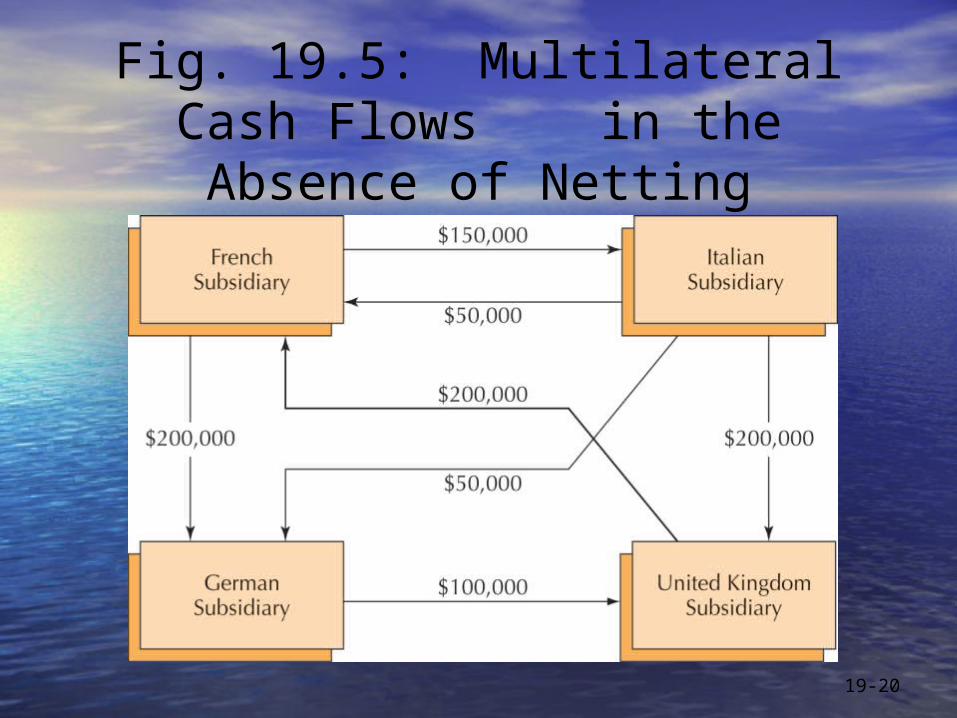

Fig. 19.5: Multilateral Cash Flows in the Absence of

Netting

19-21

Multilateral Netting

Multilateral netting: the process of coordinating cash inflows and outflows among subsidiaries so that only net cash is transferred, thus minimizing transaction costs

• Multilateral netting allows subsidiaries to transfer net intercompany flows to a cash center, or clearing account, which then disburses cash to net receivers.

• Netting requires sophisticated software and good banking relationships in relevant countries.

Generally, transfers take place in the payer's currency, and the foreign exchange conversion takes place centrally.

19-22

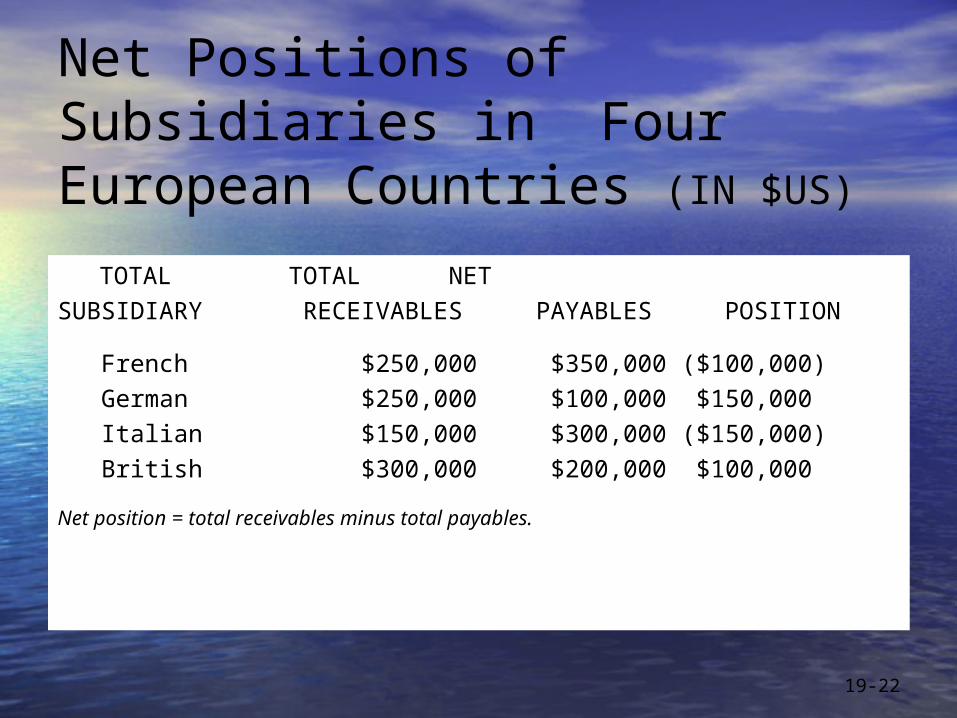

Net Positions of Subsidiaries in Four European Countries (IN $US)

TOTAL TOTAL NETSUBSIDIARY RECEIVABLES PAYABLES POSITION

French $250,000 $350,000 ($100,000) German $250,000 $100,000 $150,000 Italian $150,000 $300,000 ($150,000) British $300,000 $200,000 $100,000

Net position = total receivables minus total payables.

19-23

Fig. 19.6: Multilateral Netting

19-24

Cash Flow Aspects of Imports and Exports

In terms of security to the exporter, the basic methods of payments for exports are:

• cash in advance• letter of credit (L/C): obligates the buyer’s bank to

pay the exporter either at sight or in time [may be revocable or irrevocable and/or confirmed by an additional bank]

• draft or commercial bill of exchange: either paid im-mediately via a sight draft or later via a time draft

• open account: generally reserved for members of the same corporate group

Documentary drafts and letters of credit require that payment be made upon presentation of documents conveying the title.

19-25

Fig. 19.7: Letter of Credit Relationships

19-26

Foreign Exchange Risk ManagementTypes of exposure that can result from foreign

exchange fluctuations include:

• translation exposure: the change in value of an exposed asset or liability due to exchange rate changes

[the gain or loss does not represent an actual cash flow effect because it is only translated, not converted]

• transaction exposure: the change in value of a pay- able or receivable due to exchange rate changes

[foreign exchange risk]• economic (operating) exposure: the potential change

in expected cash flows arising from product prices, the sourcing and cost of inputs, the location of investments, and the competitive position of the firm

[cash flow impact may be both immediate and long-term]

19-27

Exposure Management Strategy

To adequately protect assets, management must:• define and measure all three types of exposure• organize and implement a uniform reporting system

to monitor exposure and exchange rate movements using both central control and foreign input

• adopt a centralized hedging policy that assigns responsi-bility for minimizing exposure

• formulate operational and/or financial strategies for hedging exposure

The safest position is a balanced one in which exposed assets equal exposed liabilities.

19-28

Hedging StrategiesOperational strategies: adjusting the flow of money

and other resources in normal operations so as to reduce foreign exchange risk

• the use of local debt to balance local assets• lead strategies, i.e., collecting foreign currency

receivables before they are due when that currency is expected to weaken, or paying foreign currency payables before they are due when that currency is expected to strengthen

• lag strategies, i.e., delaying the collection of foreign cur-rency receivables when that currency is expected to strengthen, or delaying the payment of foreign currency payables when that currency is expected to weaken

• shifting assets overseas to capture advantages embedded in currency fluctuations

[continued]

19-29

Financial strategies: using the forward market to specify future exchange rates

• using forward contracts to establish fixed exchange rates for future transactions

• using currency options to ensure access to a foreign cur-rency at a fixed exchanged rate for a specific period of time

By consolidating its foreign currency exposure, a firm can net its exposures from different operations around the world and thus take advantage of natural offsets.

Both operational and financial hedging strategies have cost/benefit as well as operational implications.

19-30

Taxation of Foreign Source Income

Taxation can profoundly affect profitability and cash flow via the following decisions:

• the location of operations• the choice of operating form (trade, licensing, FDI)• the legal form of a foreign enterprise (branch vs.

subsidiary)• the location of facilities in tax haven countries to

raise capital and manage cash• the methods of financing (external sourcing, debt,

or equity)• capital budgeting• transfer pricing methods

19-31

Legal Forms of Foreign Enterprises

Foreign branch: a foreign extension of the parent company [profits or losses are directly included in the parent’s taxable income]

Foreign subsidiary: an independent legal entity estab-lished in a foreign country according to its laws of incorporation

[income is either reinvested in the subsidiary or remitted as a dividend to the parent company]

Controlled foreign corporation (CFC): a foreign cor-poration in which more than 50 percent of the voting stock is held by U.S. shareholders[a U.S. shareholder is any U.S. person or company that

holds 10 percent or more of the CFC’s voting stock]

19-32

Determination of Controlled Foreign Corporations

PERCENTAGES OF VOTING STOCK FOREIGN FOREIGN

FOREIGN CORPORATION CORPORATION

CORPORATION

SHAREHOLDER A B C

U.S. person V 100% 45% 30%U.S. person W 10% 10%U.S. person X 20% 8%U.S. person Y 8%Foreign person Z 25% 44%

Total 100% 100% 100%

19-33

Active vs. Passive Income

Active income: derived from the direct conduct of trade or business of the foreign subsidiary of a U.S. corporation

Passive income (Subpart F income): usually derived from the operations of a foreign subsidiary of a U.S. corporation in a tax-haven country via:• holding company income• sales income• service income

The U.S. government treats any country whose income tax is lower that that of the United States as a tax-haven country.

19-34

Fig. 19.8: A Tax-haven Subsidiary as a Holding

Company

19-35

Fig. 19.9: Tax Status of Active Subpart F Income from Foreign Operations of U.S.

Companies

19-36

Transfer Prices and Tax CreditsTransfer price: the price at which one member

of a corporate family sells (transfers) inputs, compo-nents, finished goods and/or services to another entity, i.e., an internal price

Arm’s-length price: the price between two parties that have no ownership interest in the other, i.e., an external market price

Tax credit: a dollar-for-dollar reduction of a U.S. tax liability that directly coincides with the recognition of income

The OECD has established transfer pricing guidelines in order to eliminate the manipulation of prices and taxes paid

by MNEs.

19-37

Non-U.S. Tax PracticesVariations in countries’ generally accepted accounting

principles (GAAPs) can lead to differences in their determinations of taxable income.

• Corporate tax rates may be determined by:– the separate entity (classical) approach: taxes each

separate entity (firm or individual) when it earns income– the integrated system approach: splits tax rates and/or

gives tax credits in order to avoid the double taxation of corporate income

• Taxes on the earnings of foreign subsidiaries may be determined by:– the territorial approach: taxes only domestically-sourced

income – the global approach: taxes both the profits of foreign

branches and dividends received from foreign subsidiaries

19-38

Selected Corporate Income Tax Rates

Cent.Gov. Adj.Cent. Sub-cent. Combined Corp. Gov.Corp. Gov.Corp. Corp.

TargetedInc.Tax Inc.Tax Inc.Tax Inc.Tax

Corp.TaxCOUNTRY Rate Rate Rate Rate Rate

Australia 34.0 34.0 - 34.0 YesCanada 29.1 29.1 15.5 44.6 YesFinland 29.0 29.0 - 29.0 NoGermany 42.2 35.0 17.0 52.0 NoHungary 18.0 18.0 - 18.0 YesIreland 24.0 24.0 - 24.0 YesJapan 30.0 27.4 13.5 40.9 YesKorea 28.0 28.0 2.8 30.8 YesNorway 28.0 28.0 - 28.0 YesSwitzerland 8.5 6.38 18.54 24.9 NoUnited Kingdom 30.0 30.0 - 30.0 YesUnited States 35.0 32.7 6.7 39.4 YesSource: OECD Tax Rate Base, May 30,2005.

19-39

The VAT and Tax Treaties

Value added tax: each independent firm is taxed a percentage of the value added at each stage of the business process

Tax treaty: a treaty between two nations that usually results in a reciprocal reduction on dividend with-holding taxes, as well as the exemption of taxes on royalties and, occasionally, interest payments

• The primary purpose of tax treaties is to prevent inter-national double taxation, or to provide remedies when it occurs.

The OECD, the IMF, and the EU are all working to help nations narrow their tax differences and crack down on

the illegal transfer of money for illegal purposes.

19-40

Implications/Conclusions

• MNEs may employ internal capital markets in order to overcome imperfections in external capital markets.

• Offshore financial centers represent jurisdictions with relatively large numbers of financial insti-tutions primarily engaged in business with non-residents.

[continued]

19-41

• Exchange rate fluctuations can influence the equivalency of foreign currency financial state-ments, the amount of cash that can be earned from foreign currency transactions, and a firm’s production and marketing decisions.

• International tax planning has a strong impact on the choice of location for the initial invest-ment, the legal form of a new enterprise, the method of financing, and the method of setting transfer prices.