international financial management · impact on competitiveness. the firm has to obtain an optimum...

TRANSCRIPT

INTERNATIONALFINANCIAL

MANAGEMENT

H.R. MACHIRAJUPh.D. (Indiana, USA)

Financial Economist

ISO 9001:2015 CERTIFIED

(ii)

© AUTHOR

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form orby any means, electronic, mechanical, photocopying, recording and/or otherwise without the prior writtenpermission of the author and the publisher.

First Edition : 2006Second Edition : 2008Reprint : 2009Third Revised Edition : 2011Fourth Revised Edition : 2019

Published by : Mrs. Meena Pandey for Himalaya Publishing House Pvt. Ltd.,Ramdoot, Dr. Bhalerao Marg, Girgaon, Mumbai - 400 004.Phone: 022-23860170/23863863; Fax: 022-23877178E-mail: [email protected]; Website: www.himpub.com

Branch Offices :

New Delhi : Pooja Apartments, 4-B, Murari Lal Street, Ansari Road, Darya Ganj,New Delhi - 110 002. Phone: 011-23270392, 23278631; Fax: 011-23256286

Nagpur : Kundanlal Chandak Industrial Estate, Ghat Road, Nagpur - 440 018.Phone: 0712-2738731, 3296733; Telefax: 0712-2721216

Bengaluru : Plot No. 91-33, 2nd Main Road, Seshadripuram, Behind Nataraja Theatre,Bengaluru - 560 020. Phone: 080-41138821;Mobile: 09379847017, 09379847005

Hyderabad : No. 3-4-184, Lingampally, Besides Raghavendra Swamy Matham, Kachiguda,Hyderabad - 500 027. Phone: 040-27560041, 27550139

Chennai : New No. 48/2, Old No. 28/2, Ground Floor, Sarangapani Street, T. Nagar,Chennai-600 012. Mobile: 09380460419

Pune : First Floor, Laksha Apartment, No. 527, Mehunpura, Shaniwarpeth(Near Prabhat Theatre), Pune - 411 030. Phone: 020-24496323, 24496333;Mobile: 09370579333

Lucknow : House No. 731, Shekhupura Colony, Near B.D. Convent School, Aliganj,Lucknow - 226 022. Phone: 0522-4012353; Mobile: 09307501549

Ahmedabad : 114, SHAIL, 1st Floor, Opp. Madhu Sudan House, C.G. Road, Navrang Pura,Ahmedabad - 380 009. Phone: 079-26560126; Mobile: 09377088847

Ernakulam : 39/176 (New No. 60/251), 1st Floor, Karikkamuri Road, Ernakulam,Kochi - 682011. Phone: 0484-2378012, 2378016; Mobile: 09387122121

Bhubaneswar : Plot No. 214/1342, Budheswari Colony, Behind Durga Mandap,Bhubaneswar - 751 006. Phone: 0674-2575129; Mobile: 09338746007

Kolkata : 108/4, Beliaghata Main Road, Near ID Hospital, Opp. SBI Bank, Kolkata - 700 010,Phone: 033-32449649; Mobile: 07439040301

DTP by : Rajani Jadhav.Printed at : M/s. Sri Sai Art Printer, Hyderabad. On behalf of HPH.

(iii)

Dedication

Om Sri Pitrubhyo NamahaSri Ramabrahmam (Panditji to those who knew him)

B.A., B.L. (1885-1937)

A great scholar of Sanskrit, Telugu and English anda High Court lawyer in Nizam’s Hyderabad who was

respected and well liked by all who came into contact withhim. An enduring quality I inherited from him was to

persevere against all odds.

(v)

Revision to the book started two years ago was interrupted for health reasons. The delayafforded an opportunity to analyze issues of market and inequality in India which limited a consumerpivot as in China. The provision of incentives and ease of doing business may attract MNEs to locatetheir business. But their impact on growth is extremely limited. MNEs contributed in a big way toincomes and of incomes prosperity in China by bringing technology, location of labor-intensive industries(not merely call centers) and exports. As a result, there is a hiatus between the creation of anopportunity and the ability to avail it. The poor do not possess the skills. Six decades of planneddevelopment did not impact on the problem. Now, automation further limits opportunities. Around athird of under 25s are not in employment, education or training. Participation of woman remains lowat 27 percent. Acquisition of the consumer durables and smartphones, taste for fast food andecommerce requires income from productive activity in which most of the population cannot participate.

The fruit of economic growth accrue to those with skills and possessing property rightsexacerbating the problem of equality. MNEs face a welcoming policy to locate industries but mustrekon the market which is much narrow than the size of the population.

H.R. Machiraju

Preface to the Fourth Revised Edition

(vi)

Multinational enterprises (MNEs) in the new millennium face conflicting pull and push factors.The pull factors consist of the huge and critical contribution they make to society in terms of productivitygains, innovation and research, employment, large-scale investment, human capital development andorganization. In developing countries, multinational enterprises contribute critical technology throughforeign direct investment, skills and other poverty reducing spillovers. There is big clamour for attractingthem through foreign direct investment (FDI) from developed as well as developing countries byoffer of incentives, provision of infrastructure, educated labour force, tax optimization and flexiblelabour laws. The tax revenue and employment MNEs generate are necessary to increase spendingon social overheads and infrastructure. The positive impact of FDI on China in Asia and Ireland inEurope are widely discussed. Multinational enterprises on their part have to face stiff competition toaccess the markets which are promising and survive potential competition because technology andcapital move swiftly across the globe.

MNEs face push factors in the form of social pressures from groups and activists involved incorporate social responsibility enforcement. The push factors based on the perceived misdeeds ofone company (gas leak in Bhopal) have shaped the attitudes of public around the globe. In the pastfew decades, social and political pressures had redefined the tobacco industry, the oil and miningindustries and emission controls of automobile industry. In the last decade, a storm of social pressurearose on excessive prices charged for HIV drugs in developing countries, especially in Africa, marketingof unhealthy foods leading to obesity in the food and restaurant sector (McDonald’s) not to sayanything of colonial past when multinationals exploited vulnerable economies wherever they couldgain foothold.

The other push factor is outsourcing which is resorted to by MNEs to stay internationallycompetitive. In today’s globalized world, the share value is influenced not only by the financial factorsbut on how competitive the firm is. New technologies, novel ways of organizing production to ensurequality of product, innovative response to customer needs, market leadership and trade policiesimpact on competitiveness. The firm has to obtain an optimum combination of inputs from the globalmarket. Companies have been outsourcing anything that is not tied directly to competitivedifferentiation. Outsourcing is an integral part of global supply chain management not only for valuemaximization but also for staying competitive.

The present is the time for multinational enterprises to face the challenges of staying internationallycompetitive and aligning social issues with corporate strategy plans.

Multinational enterprises instead of concentrating on short-term performance to improve sharevalue should pursue long-term economic opportunities and social issues which include trust of customers,investment in innovation and other growth prospects. The adoption of Corporate Social Responsibility(CSR) which includes stakeholder dialogue, social and environmental reports and corporate policies

Preface to the First Edition

(vii)

on ethical issues does not capture the potential importance of social issues for corporate strategy. Itis too limited and too disconnected from corporate strategy and does not keep pace with the tsunamilike changes in socially driven business environment.

Multinational enterprises have to integrate social issues and emerging social forces into strategicplanning (a’la Ian McKinsey & Company). The efficient provision by business of goods and servicessociety wants is measured and rewarded by profits. MNEs should also establish ever higher standardsof integrity and transparency by adoption of best international corporate governance practices whichinnure to their benefit.

Author

(ix)

Brief Contents

Sr. No. Title Page No.1. Financial Management of a Multinational Enterprise 1 – 18

2. Balance of Payments 19 – 36

3. Exchange Rate Systems 37 – 55

4. Foreign Exchange Market 56 – 76

5. International Parity Relationships 77 – 92

6. Currency and Interest Rate Derivatives 93 – 139

7. International Banking and Indian Corporates 140 – 160

8. Financing in the International Bond Market 161 – 180

9. Foreign Direct Investment 181 – 192

10. International Equity Markets 193 – 218

11. Cost of Capital for Foreign Investment 219 – 222

12. International Capital Budgeting 223 – 228

13. Financing International Trade 229 – 233

14. Working Capital Management: Management of Current Assets 234 – 237

15. Taxation of Multinational Enterprise 238 – 241

16. Compliance of Corporate Governance Provisions 242 – 265

Glossary 266 – 273

Index 274 – 276

(xi)

1. FINANCIAL MANAGEMENT OF A MULTINATIONAL ENTERPRISE 1 – 18

Introduction. Investment by Multinational Enterprises. Trends in FDI. Impact of FDI.Largest TNCs. Investing in Sustainable Developement Goals. FDI by Sovereign WealthFunds (SWFs). Impact of Globalization. Rationale of Multinational Enterprise.Maximizing the Value of Firm. Social Contract between Business and Society.Investment Decision. Financing Decision. Dividend Decision. Global Competitiveness.Factors Influencing Competitiveness. Corporate Governance. Criteria forCompetitiveness. Production Efficiency. Global Manufacturing and Supply ChainManagement. Supply Chaining is a Flattener. Global Manufacturing Strategy. Sourcing.Stages of Outsourcing. Reorganizing Production. Outsourcing Manufacturing.Outsourcing Administrative Work. Outsourcing White Collar Work. Impact ofInformation and Communication Technologies on Outsourcing. Size of OutsourcingMarket. Relative Comparative Advantage. References.

2. BALANCE OF PAYMENTS 19 – 36

Definition. Significance. Components. Trends in Trade. Exports. Overall Balance ofPayments. Components of Current Account. Merchandise Trade. Invisibles (factorservices, private transfers and official transfers). Capital Account. Direct Investment.Trade Credit. Portfolio Investment. External Assistance. External Commercial Banking.NRI Deposits. Trade Agreements. World Trade Organization. Factors AffectingInternational Trade. Exchange Rates. Foreign Exchange Reserves. Fiscal Deficits andthe Current Account. Inflation. National Income. Government Restrictions. InternationalMonetary Fund. The Keynes Plan and the White Plan. Purpose of the IMF. Members’Quotas. Principal Functions. Resources of the Fund. Financial Assistance by Fund.IMF Stabilization Programmes. Aim. Conditions. The Process. Approach of IMF.Credit Ceilings and Inflation. Devaluation. Financial Liberalization. StabilizationProgramme. Burden of Adjustment. Financial Transactions Plan. References.

3. EXCHANGE RATE SYSTEMS 37– 55

Introduction. Classification of Exchange Rate Systems. Fixed Exchange Rate vis-a-visGold. Fixed Exchange Rates vis-a-vis One Currency. Advantages of Fixed Rate. FixedExchange Rate vis-a-vis A Basket. Flexible Exchange Rates. Managed Float. ExchangeRate Peg. Currency Board Arrangement. Dollarization. The Euro. Criteria for Evaluationof Exchange Regimes. The Choice of Exchange Rate. Size and Openness of theEconomy. Inflation Rates. Labour Market Flexibility. Degree of Financial Development.The Credibility of Policy Makers. Capital Mobility. Exchange Rates in India. ExchangeControl in India. Foreign Exchange Regulation Act, 1974. Liberalized Exchange RateManagement System, 1992. Unified Market Determined System, 1993. Cross CurrencyOptions. Cross Currency Swaps. Foreign Exchange Management Act, 1999. ForeignExchange Transactions of Commercial Banks in India. Foreign Currency Accounts.Nostro Account. Vostro Account. RBI Management of Forex Reserves. Market

Contents

(xii)

Stabilization Scheme April, 2004. Currency Convertibility. Current AccountConvertibility. Capital Account Convertibility. Competitiveness of Indian Economy.Fuller Capital Account Convertibility. References.

4. FOREIGN EXCHANGE MARKET 56 – 76

Introduction. Foreign Exchange Market and Euro-dollar Market. Purpose andOrganization. Impact of Technology on Trading. Relationship between Exchange andMoney Markets. Term Money Market and Interest Differentials Based Forward.Interdependence of External Value of Rupee and Money Market Rates. Participants.International Banks. Traders and Investors. Dealers and Brokers. Investment Banks.Central Banks. Arbitrageurs. Arbitrage. Speculation. Bulls and Bears. CorrespondentBanking. Foreign Exchange Rates. Exchange Quotations. Market Makers. ExchangeRate Points. Spot Exchange Rates. The Bid-Ask Spread. Ready Exchange Rates inIndia. Turnover in Foreign Exchange Market. Forward Exchange Rates. Calculationof the Forward Exchange Rate. Efficiency of the Foreign Exchange Market. CrossRate. Spot Exchange: Settlement Procedure. Currency Arbitrage. Two Point CurrencyArbitrage. Triangular Arbitrage. Nominal, Real and Effective Exchange Rates. NominalExchange Rate. Real Exchange Rate. Effective Exchange Rate. References.

5. INTERNATIONAL PARITY RELATIONSHIPS 77 – 92

Introduction. Law of One Price. Purchasing Power Parity. Basis of PPP. Inflation andExchange Rate. Absolute Purchasing Power Parity. Relative Purchasing Power Parity.Empirical Evidence. Implications. The Fisher Effect. The International Fisher Effect.Interest Rate Parity. Covered Interest Arbitrage. Implications of IRP, PPP and IFETheories. Features of IRP, PPP and IFE Theories. Expected Exchange Rate. PortfolioTheory of Exchange Rate Determination. References.

6. CURRENCY AND INTEREST RATE DERIVATIVES 93 – 139

Objectives of Risk Management. Smoothing Earnings. Value at Risk. Cash Flow atRisk. External Techniques. Foreign Exchange Risk. Economic Exposure. TransactionExposure. Translation Exposure. Hedging. Restructuring to Reduce EconomicExposure. Translation Exposure and Hedging. Forwards and Futures to HedgeTranslation Exposure. Limitations of Hedging Translation Exposure. HedgingTransaction Exposure. Matching. Hedging Techniques. Forward Hedge. ForwardRates. Forward Contracts. Money Market Hedge. Money Market and Forward Market.Futures. Definition and Nature. Outstanding and Turnover. Trading of Futures. Typesof Traders. Contract Characteristics. Prices and Daily Settlement. Future and ForwardContracts. Determining Gains and Losses. Futures and Forward Exchange RatesDiffer. Currency Futures in India. Trading. Carry Trade. Foreign Currency Options.Introduction. Definition. American and European Options. ETC and OTC Options. ITM,ATM and OTM Options. Intrinsic Value. Time Value. Total Value, Time Value and IntrinsicValue. Hedging with Options. Basic Option Strategies. Compound Strategies. Tunnel.Spread. Vertical Spread. Horizontal Spread. Butterfly Spread. Diagnol Spread. RatioSpread. Straddle and Strangle. Second Generation Strategies. Basket Option. AverageRate Option. Look Back Option. Shared Currency Option under Tender. Hybrids.

(xiii)

Pricing of Currency Options. Role of Strike Price. Role of Spot Rate. Role of Time toExpiration. Interest Rate Differential. Role of Foreign Exchange Rate Volatility. HistoricVolatility. Implied Volatility.Garman and Kohlhagen Model for Valuation of Currency Option. Currency OptionManagement Tools – The Delta, The Gamma, The Theta, The Vega, The Phi and TheRho. Cross Currency Options Trading in India. RBI Guidelines for Currency OptionsTrading. Trading of Currency Options in India. Viability of Currency Options Tradingin India. Recommendations of the Sub-Group on Derivatives (1-6-95). BroadeningForeign Exchange Derivatives Market.Currency and Interest Rate Swaps. Interest Rate Swaps. Swap Bank. Interest RateRisk. Interest Rate Swaps. Growth of Interest Rate Swaps. Maturity Distribution.Location. Type of End-user. Types of Interest Rate Swaps. Fixed-for-Floating. QualitySpread Differential. Base Swaps. Cocktail Swaps. Zero Coupon for Floating Swaps.Forward Swaps. Rate Capped Swaps. Uses of Swaps. Swaps and Hedge Funds.Comparative Advantages of Swaps. Separation of Interest Rate Risk and Credit Risk.Pricing Interest Rate Swaps.Swap Related Instruments.Currency Swaps. Definition. Uses of Swaps. Pricing of Swaps. Swaps by Locationand End-user. Swaps by Currency and Type of End-user. Secondary Market SwapTransactions.Cross Currency Swaps in India (1997).References.

7. INTERNATIONAL BANKING AND INDIAN CORPORATES 140 – 160

Nature. Definition. Development of International Banking. Why Engage in InternationalBanking? Growth in Deposits in International Banks. Financial Intermediation byInternational Banks. Functions of Euro Dollar Market. Organizational Form ofInternational Banking. Correspondent Bank. Representative Office. Foreign Branch.Subsidiary Bank. Offshore Banking Centre. Globalization of Banking Systems.Regulation of International Banking. Country Risk Analysis. Country Risk andEuromoney. Country Risk Analysis of Morgan Guarantee Trust Company. SovereignRatings of India.Syndicated Loans. Introduction. Definition and Nature. Assessment of SyndicatedLoans. Structure of Syndicated Loan. Pricing Structure. Defaults and Recoveries.Secondary Market. LSTA. Credit Default Swaps. Globalization. Revised Guidelinesfor External Commercial Borrowing (ECB) January 2004. External CommercialBorrowings Policy (January 2004). Initiatives to Liberalize ECBs. Trends in ExternalCommercial Borrowings in India. References.

8. FINANCING IN THE INTERNATIONAL BOND MARKET 161 – 180

Introduction. Domestic Bonds, Foreign Bonds and Euro Bonds. Origin. Developmentof International Bond Market. Size of Bond Market. Types of Bonds. Straight Bonds.Floating Rate Notes. Zero Coupon Bonds. Convertible Bonds. Bonds with Equity Warrants.Putable Bonds. Medium Term Notes (MTNs). International Bonds by Nationality. Term

(xiv)

Structure of Interest Rates. Yield Curve. Relationship between Time and Money. MarketSegmentation Theory. Unbiased Expectations Theory. Liquidity Preference Theory.Preferred Habitat. Pricing of Bonds. Relationship between Price and Yield. Coupon Rate,Required Yield and Price. Yield Measures. Current Yield. Yield to Maturity. Price Volatilityof a Bond. Measures of Bond Price Volatility. Price Value of a Basic Point. Duration.Convexity. Procedure for Issue of Bonds. Technique of assimilation. Gray Market.Major Stages in Issue of Bonds. Tombstone. The Bought Deal. International Bond MarketRatings. Listing and Trading. Secondary Market. References.

9. FOREIGN DIRECT INVESTMENT 181 – 192

Introduction. Forms of FDI. Extent of FDI. MNE Approach to FDI. Exports. Licensing.Technology Transfer. Competitive Advantage. Theories of Foreign Direct Investment.Market Imperfections. Transaction Cost Theory. Internalization Theory. LocationSpecific Theory. Product Life Cycle Theory. Electic Theory. Globalization Theory.Game Theory and International Strategy. Foreign Investment Flows to DevelopingCountries. Factors Affecting FDI Movements. FDI in China and India. Impact ofGreat Recession on FDI into India. Foreign Direct Investment Policy of India. Impactof Antiglobalisation and Protectionism.References.

10. INTERNATIONAL EQUITY MARKETS 193 – 218

Introduction. Issuance of International Equities. Internationalization of Stock Markets.Measures of Liquidity. Trading Systems. Settlement. United Kingdom. InternationalStock Exchange. SEAQ. Trading and Settlement. Derivatives. United States of America.New York Stock Exchange. Floor Brokers. Specialists. Registered Representatives.Listed Securities. Listing and Registration. Advantages of Listing. Listing Requirements.Trading. Settlement. NYSE Circuit Breakers. NASDAQ. Nature. Negotiated Market.Third Market. Size. Listing Requirements. Trading Hours. Trading. AQCESS. AmericanStock Exchange. Objective. Listing Criteria. Electronic Trading System. Inter MarketTrading System.Euro Issues by Indian Companies. Introduction. Role of Intermediaries. AmericanDepository Receipts. Origin and Nature. Types of ADRs. Book Runners and GlobalCoordinators in 1997. Euro Issues. Global Depository Receipts. Nature and Definition.Fungibility. Advantages for the Issuer. Advantages to the Investor. Permission forIssue. Guidelines for Issue of GDRs and FCCBs (1993). Modifications to Guidelines(Issued on 11.5.1994). Guidelines, October 1994. Changes in Guidelines, June 1996.Changes in 1998-99. Investment of ADR/GDR Proceeds Abroad (28.2.2001). Pricingof GDRs. Investment in GDRs by FIIs. Management of GDR Issue. PreferenceShares. Indian Depository Receipts. References.

11. COST OF CAPITAL FOR FOREIGN INVESTMENT 219 – 222

Definition. Cost of Capital for Domestic Firms and MNE. Factors Affecting Lot ofCapital Cost of Equity Capital. Cost of Debt. Weighted Cost of Capital for ForeignProjects. Discount Rate for Foreign Investment. Advantages of InternationalDiversification. Financial Structure of Subsidiaries. References.

(xv)

12. INTERNATIONAL CAPITAL BUDGETING 223 – 228

Introduction. Domestic vs. International Projects. Project vs. Parent Valuation. Adjustingfor Risk. Adjusting Cash Flows. Appraisal. Assessing Political Risk. Capital BudgetingAnalysis. Technique to Estimate Cash Flows. Factors to be Considered in InternationalCapital Budgeting. Foreign Exchange Rate. Inflation. Sensitivity Analysis. Simulation.References.

13. FINANCING INTERNATIONAL TRADE 229 – 233

Introduction. Payment Methods. Prepayment Letter of Credit. Bill of Exchange (Draft).Consignment. Open Account. Trade Finance. Account Receivables. Factoring. BankersAcceptance. Forfeiting. Counter Trade.

14. WORKING CAPITAL MANAGEMENT: MANAGEMENT OF CURRENT ASSETS 234 – 237

Introduction. Cash Management. Payments Netting Systems. Management of Short -term Investment Portfolio. Receivables. Inventory Management.

15. TAXATION OF MULTINATIONAL ENTERPRISE 238 – 241

Introduction. Organizational Structure. Tax Credit. Taxes and Capital Structure. DoubleTaxation Avoidance. Transfer Pricing. Transfer Payments. Investment Decision.

16. COMPLIANCE OF CORPORATE GOVERNANCE PROVISIONS 242 – 265

Introduction. Features of Public Limited Company. Constituents of a CompanyCorporation. Corporate Governance. Agency Theory. Definition and Scope. Benefitsof Good Governance. Shareholder Democracy. Incentives to Align Managers, Interestwith Shareholders. Participation of Stakeholders. Legal Origins of Commercial LegalSystems. Outsider Model. Features of Companies in Outsider Model in UK and USA.Centralization of Regulation in US. Comply or Explain. Shareholders. Market forCorporate Control. Disclosures. Insider Model. Market vs. Bank Oriented Systems ofGovernance. Insider vs. Outsider Systems of Ownership and Control. Protection ofShareholders’ Interests. Definition of Shareholder. Shareholder Democracy. Role ofShareholders. Index of Shareholder Rights. Corporate Social Responsibility. Introduction.Stakeholders. Sustainable Governance. Role of NGOs. Governance Reforms in India.Issues in Corporate Governance. Reforming the Boards. Separation of Board andManagement. Board Performance. Management. Objective. Information for the Board.Whistle Blower Policy. Compensation. CEO Compensation in India. Long-term ShareOwnership. Share Owners. Partnership Capitalism. Empowering Shareholders.Compliance of SEBI Guidelines for Corporate Governance. Corporate Ethics. References.

Glossary 266 – 273

Index 274 – 276

(xvi)

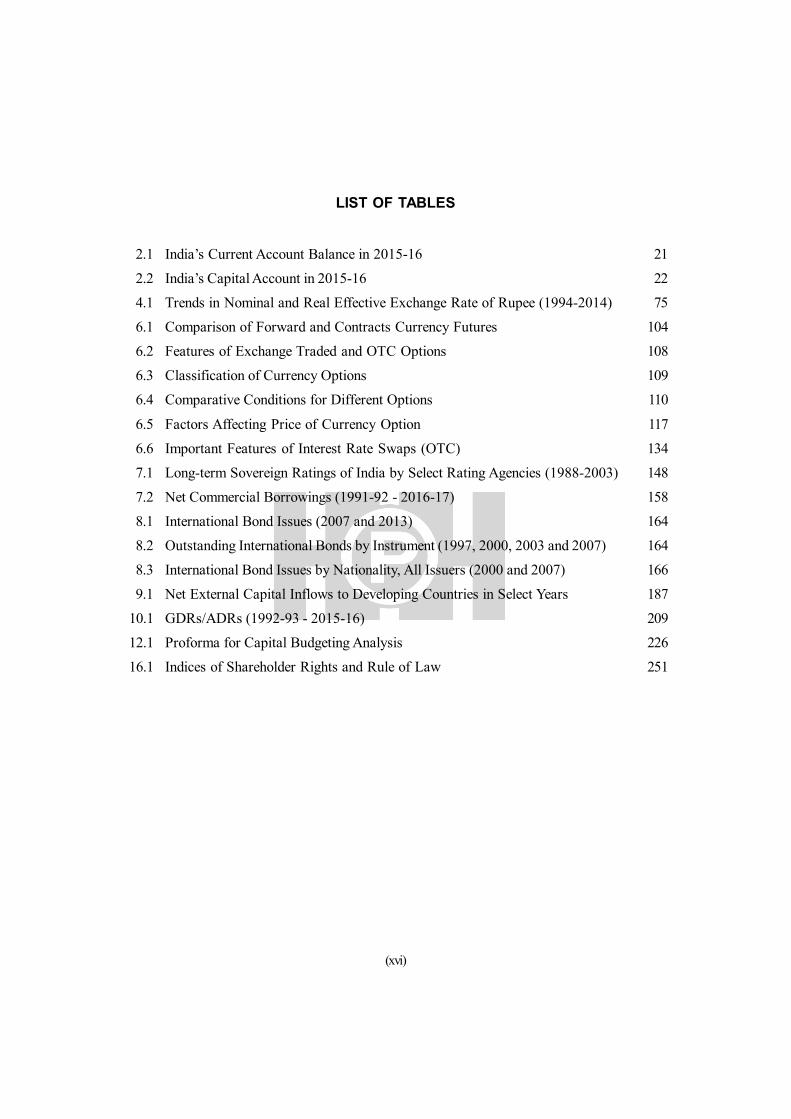

LIST OF TABLES

2.1 India’s Current Account Balance in 2015-16 21

2.2 India’s Capital Account in 2015-16 22

4.1 Trends in Nominal and Real Effective Exchange Rate of Rupee (1994-2014) 75

6.1 Comparison of Forward and Contracts Currency Futures 104

6.2 Features of Exchange Traded and OTC Options 108

6.3 Classification of Currency Options 109

6.4 Comparative Conditions for Different Options 110

6.5 Factors Affecting Price of Currency Option 117

6.6 Important Features of Interest Rate Swaps (OTC) 134

7.1 Long-term Sovereign Ratings of India by Select Rating Agencies (1988-2003) 148

7.2 Net Commercial Borrowings (1991-92 - 2016-17) 158

8.1 International Bond Issues (2007 and 2013) 164

8.2 Outstanding International Bonds by Instrument (1997, 2000, 2003 and 2007) 164

8.3 International Bond Issues by Nationality, All Issuers (2000 and 2007) 166

9.1 Net External Capital Inflows to Developing Countries in Select Years 187

10.1 GDRs/ADRs (1992-93 - 2015-16) 209

12.1 Proforma for Capital Budgeting Analysis 226

16.1 Indices of Shareholder Rights and Rule of Law 251

(xvii)

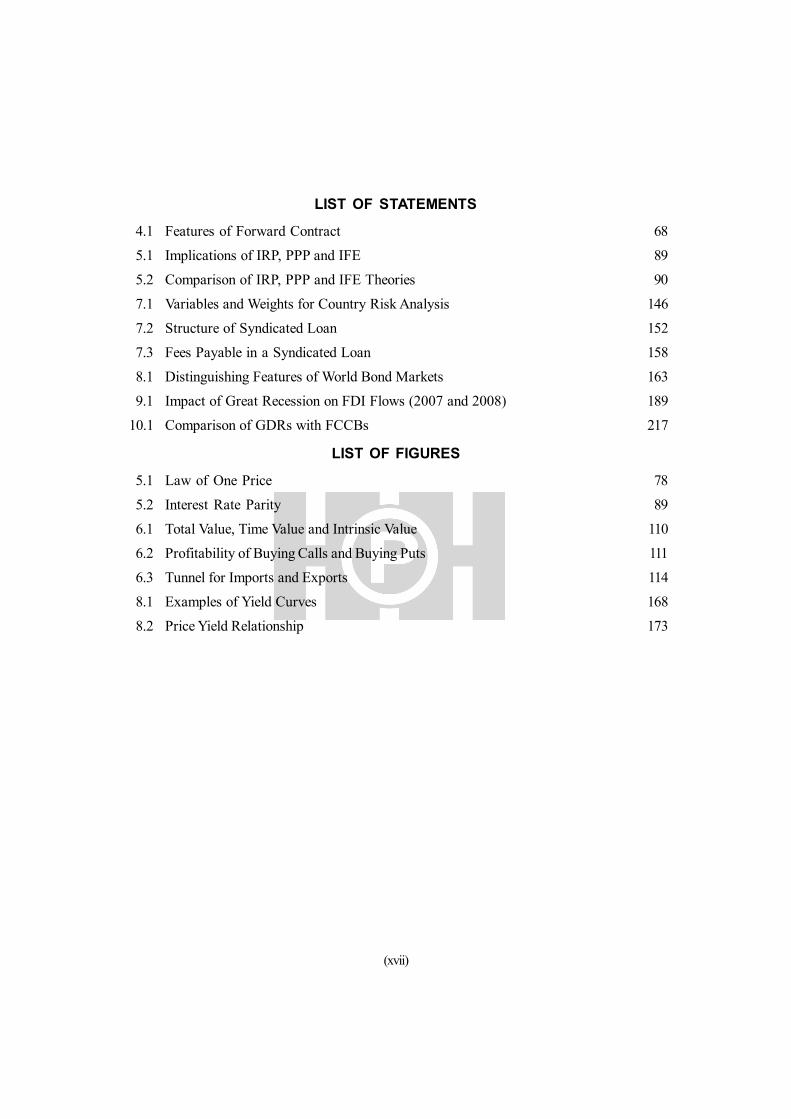

LIST OF STATEMENTS

4.1 Features of Forward Contract 68

5.1 Implications of IRP, PPP and IFE 89

5.2 Comparison of IRP, PPP and IFE Theories 90

7.1 Variables and Weights for Country Risk Analysis 146

7.2 Structure of Syndicated Loan 152

7.3 Fees Payable in a Syndicated Loan 158

8.1 Distinguishing Features of World Bond Markets 163

9.1 Impact of Great Recession on FDI Flows (2007 and 2008) 189

10.1 Comparison of GDRs with FCCBs 217

LIST OF FIGURES

5.1 Law of One Price 78

5.2 Interest Rate Parity 89

6.1 Total Value, Time Value and Intrinsic Value 110

6.2 Profitability of Buying Calls and Buying Puts 111

6.3 Tunnel for Imports and Exports 114

8.1 Examples of Yield Curves 168

8.2 Price Yield Relationship 173

Introduction

Traditionally international financial management has been viewed as management of multinationalcorporations that engage in some form of international business.1 These corporations continuouslydevise strategies to improve their cash flows and enhance shareholder wealth. Penetration of foreignmarkets creates opportunities for improving the firms cash flows. The dismantling of barriers toentry encourage firms to pursue international business. Liberal trade is the principal driver ofglobalization which encompasses unimpeded flows of capital, labor and technology across nationalboundaries. David Ricardo in 1817 furnished the theoretical underpinning of globalization and thevirtues of free trade by arguing that free trade is always beneficial because it encourages nations tospecialize in the products they are best at and import those they are less good at. This results inefficient allocation of resources and maximization of welfare.

Firms go through different stages in this pursuit, export products or import supplies from foreignmanufacturer initially to establishing subsidiaries in foreign countries. These are the large multinationals,Dow Chemical, Exxon Mobil, Colgate Palmolive, Levers, Coca-Cola. They distribute their productsin more than 100 countries and generate more than half of their operating income outside their homecountry. The Institute of International Economics in Washington estimates that global trade brings$1 trillion in benefits to the US annually or roughly $9,000 per US household.

Number, Origin and Growth of MNEs

There were 79,000 MNEs in the world with over 790,000 foreign affiliates. By country of originmultinationals are from US, Japan, France, Germany and U.K. Several Swiss firms are multinational.Throughout the 1990s, foreign direct investment by MNEs grew at an annual rate of 10% whereasinternational trade grew at the rate of 3.5%. Sales of MNEs are larger than world exports (in 1998,$11 trillion vs. $7 trillion). Over half of the world’s 100 largest economic entities are transnationalcorporations not sovereign national economies. Value added activity of foreign affiliates accounted

1. A business firm is considered a global player according to Fortune magazine when its international sales exceed 20%of total.

FINANCIAL MANAGEMENT OF AMULTINATIONAL ENTERPRISE

CHAPTER

1

2 International Financial Management

for 11% of global GDP in 2007. Sales amounted to $31 trillion, about one fifth of which representedexports and the number of employees 82 million.

Some smaller firms generating 20% of their sales from international business focus on nichesthat made them successful in their home country. These small firms with fewer than 100 employeespenetrate specialty markets where they will not have to compete with large firms flourishing oneconomies of scale. Small firms establish subsidiaries or confine themselves to exports.

Investment by Multinational Enterprises

The extent, pattern and modes of MNE activity have been greatly influenced by the political,technological and economic events in the last two decades. Computer technologies and wireless aidMNEs cross-border movement and/or geographical dispersion of assets, notably money capital andinnovating capacity and of intermediate products, technology and management skills. The mobilityaided by computer technologies and wireless is offering MNEs wider options in respect of both thecreation and use of these assets and products.

The data on stock of outward foreign direct investment by large countries and inbound foreigninvestment by major host countries, show that foreign based activities of MNEs is the method forserving foreign markets. In all major economies of the world, the role of domestic and/or foreignbased MNEs is increasing. The data show that the ratio of foreign direct investment (FDI) to GDPdoubled since 1980 from 5.3% to 11.9% in 1998 (outward) and 5% to 11.7% (inward). Outwarddirect investment has been influenced by the opening up of erstwhile communist countries especiallyChina. Further widespread privatization and deregulation of many service sectors have opened newopportunities for FDI in utility, telecommunications and banking and finance sectors. Professionaland business services are getting internationalized. Regional economic integration especially in theEuropean Union has encouraged MNEs to internalize trade flows. Outsourcing of manufactures andlater white collar work has assumed significant level.

Data on inbound foreign direct investment show that nearly 70% of the inward stock of FDIcontinued to be located in the three great trading blocks North America, Western Europe and Japan.Further, four fifths of the innovatory activities of MNEs was also undertaken there.

While the share of developing countries in FDI remained around 30% it has more than doubledas a ratio of GDP between 1980 and 2008.

Trends in FDI, Share of Developed and Developing Countries2

The trends in FDI, impact of FDI and Top 100 largest TNCs and Top 100 largest TNCs fromdeveloping countries are presented to appreciate the significant role TNCs play in the global economy.

2. UNCTAD, World Investment Report, 2008. Since UNCTAD uses TNC for MNE, it is retained in this write up.

Financial Management of a Multinational Enterprise 3

Foreign direct investment inflows in 2007 were $1833 billion as compared to $16,206 billion in2008. The financial and credit crisis of 2007-2009 has, however, added new uncertainities and risksto the world economy. The global FDI market is in a state of flux rendering future forecast uncertain.

Recent Trends in FDI

Global FDI in 2007 reached a new record high surpassing the previous record of 2000. All thethree major groups of economies witnessed continued growth. The continued rise in FDI largelyreflected relatively high economic growth and strong economic performance in many parts of theworld. Increased corporate profits of parent firms provided funds to finance investment and reducedthe impact of decreasing loans from the banks affected by the subprime credit crisis. In foreignaffiliates, higher profits, amounting to over $1,100 billion in 2007 contributed to higher reinvestedearnings (30% of total FDI flows in 2007). These profits are generated in developing countries.

FDI inflaws in 2013 were $1,452 billion, income $1,748 billion and rate of return 6.8%. Sales offoreign affiliates were $ 34,508 billion total assets of foreign affiliates $ 96,625 billion exports byforeign affiliates $ 7,721 and employment by foreign affiliates 70,726 (thousands).

FDI inflows to China were $124 billion in 2013 and India $128 billion. Defying the overalltrends, investments in the retail sector did not increase despite the opening up of multi brand retail.

In terms of global share developed countries accounted for 39% of total inflows and 61% oftotal outflows, both historically low levels.

Sectoral Pattern

The primary sector’s share in world FDI is now back to a level comparable to that of late1980’s. The flows to the primary sector were mainly extractive industries. In 2006 the primarysector’s share of total world inward FDI stock was 8% and the sector accounted for 13% of worldFDI inflows in the period 2004-06. The increase in FDI in the primary sector in 2007 was moreevident in green field investments (463 in 2005, 490 in 2006 and 605 in 2007).

Manufacturing accounted for nearly one-third of the estimated world inward FDI stock in2006. Its share in world FDI stock has fallen noticeably since 1990 in both developed and developingeconomies, declining by 10 percentage points.

The services sector accounted for 60% of estimated world inward FDI stock in 2006 benefitingall the major groups. While trade, financial services and business activities account for lion’s shareother services, including infrastructure have begun to attract increasing shares of FDI since 1990s.Electricity, gas and water account for 8% of the total in 2007. The increase in the shares of infrastructureincluding in developing countries raises the question as to how FDI can contribute to MilleniumDevelopment Goals through more and better infrastructure to the poor.

4 International Financial Management

Largest TNCs

The foreign activities of 100 largest TNCs are evaluated from the viewpoint of theirinternationalization (Table I:2). They accounted for 10, 16 and 12% of the estimated foreign assetssales and employment respectively of all TNCs in the world. Many of the largest TNCs are involvedin infrastructure development (telecommunications, electricity and water). The liberalization andprivatization in the late 80s’ and throughout 1990s had a particularly marked effect on internationalizationof these services.

General Electric heads the list with more than 8% of total foreign assets of top 100 companies.The top 10 with about $1.7 trillion in the foreign assets, or more than 32% of the total foreign assetsof the top 100 include four petroleum and two motor vehicle companies, two infrastructure companies,one company in the electrical/electronic equipment industry and one retail company. The ten companiesalso account for 29% of all foreign sale, but only for 15% of all foreign employment of the 100 largestTNCs.

Among the multinationals with state share-holders, Enel, an Italian firm holds forign assets $15billion abroad (2009).

Six industries dominated the list of the largest TNCs. Motor vehicles (13) and petroleum (10)represent more than half the companies in the first quartile. Electrical/electronic equipment (9)utilities (8) telecoms (8) and pharmaceutical (7) followed. The six industries accounted for 55% oflargest TNCs. Metals and non-metallic products, retail and wholesale trade, and food and beveragesaccounted for another 23%.

Investing in Sustainable Development Goals (SDGs)

SDGs which are being formulated by United Nations together with the widest possiblestakeholders are intended to galvanise action worldwide. Through concrete goals for the 2015 –2030 period for poverty reduction, food security, human health and education and climate changemitigation. Investments needs are in the range of $3.3 trillion to $4.5 trillion.

Private sector contributions would be good governance in business practices transparency andaccountability in honouring sustainable development practices.

Promotion and facilitation of investment in sustainable development should include according toUNCTAD marketing of prepackaged and structured projects with priority consideration andsponsorship at the highest political level. This requires specialist expertise and dedicated units, e.g.,government sponored brokers of sustainable development investment projects.

Transnationality Index: UNCTADs Transnationality Index is a composite of three ratios:foreign assets to total assets, foreign sales to total sales, and foreign employment to total employment.TNI value is higher than average for TNCs from France and United Kingdom and it is lower thanaverage for TNCs from Germany, Japan and the United States.

Financial Management of a Multinational Enterprise 5

The internationalization Index (II), the ratio of foreign to total affiliates shows that on averagemore than 70% of the affiliates of the world’s largest TNCs are located abroad.

Top 100 TNCs’ from Developing Countries

The foreign assets of 100 largest TNCs from developing countries amounted to $570 billion in2006. The ten largest accounted for almost half of the foreign assets of the top 100. Companies fromthe electrical/electronic and computer industries dominate the group with 20 entries. By economyHong Kong, Taiwan dominate the list with 26 and 16 respectively. Singapore and China have 11 and9 companies, respectively, in the list.

Affiliates: Developing economy TNCs have a smaller number of affiliates, nine on averagecompared to largest TNCs worldwide. The most preferred locations for the foreign affiliates of thetop 100 developing economy TNCs are the United Kingdom and the United States.

TNI value for the largest TNCs from developing economies is quite close to world’s largestTNCs. The internationalization index, shows that on average more than 50% of the affiliates of thelargest TNCs from developing economies are located abroad.

FDI by Sovereign Wealth Funds (SWFs)

SWFs existed since the 1950s in countries that were rich in oil. Kuwait Investment Authorityand Temasek Holdings of Singapore were founded in 1953 and 1974 respectively. Other examplesare Abu Dhabi Investment Authority, China Investment Corporation and GPFG Norway. SWFs arebecoming aggressive investment vehicles with equivalent to 2% of the global value of traded securities.SWFs hold more financial resources than private equity or hedge funds. SWFs are controlled directlyby home government, hold stakes for long period and non economic rationale influence investmentdecisions.

There are some 70 such funds in 44 countries with assets ranging from $20 million to $500billion. Their holdings are concentrated in China, Hong Kong, Kuwait, Norway, Russia and SaudiArabia.

FDI by SWFs was $10 billion in 2007 accounting for only 0.6% of total FDI flows. SWFs haveinvested heavily in low yield government bonds in the US and Europe. Their acquisitions constituteownership shares of less than 10% which is the threshold for an investment to be classified as FDI.FDI by SWFs are mainly in developed countries, UK, USA and Germany and 73% were in servicessector at end 2007. Developing countries notably Asia received 27% of the total, $105 billion. SWFsinvestment concentrated in business services. The total volume is $5,000 billion.

Concerns About SWFs

1. SWFs could pose a threat to security and barriers should be erected against these investors.

2. Lack transparency: Do not disclose their asset portfolios and investment decisions. TheNorwegian and Canadian SWFs are exceptions.

6 International Financial Management

They recycle the huge dollar inflows of the countries concerned thereby contributing to thefinancing needs of deficit countries. Several initiatives are underway to establish principles andguidelines relating to FDI by SWFs (European Commission and OECD are engaged).

Impact of Globalization

MNCs gain from their global presence by economies of scale in R&D expenditures, advertisingcosts and utilizing their technological and managerial know how globally with minimum additionalcosts. Consumption patterns around the world are converging on account of the highly globalized andintegrated world economy. The liberalization of international trade is likely to further internationalizeconsumption patterns. The production of goods and services has also become globalized on accountof the efforts of international firms to source inputs and locate production anywhere in the worldwhere costs are lower and profits higher. This has given rise to outsourcing which is viewed asexporting jobs from advanced countries to countries where costs are lower, India for IT and Chinafor manufacturing. In US globalization is now seen as a phenomenon that makes rich countriespoorer.

Financial markets around the globe are getting integrated. US pension and mutual funds diversifytheir investment portfolios internationally. The Japanese investors have been investing in US andother financial markets in efforts to recycle their trade surpluses. Cross listing of shares on foreignstock exchanges has helped trading of shares and provides access to foreign capital as well. Financialglobalization which may give rise to higher capital inflows may not however lead to higher growthsince it influences capital labor ratios and not total factor productivity. International firms now face aworld where consumption, production and investment decisions are globalized. The world has becomea vast interconnected marketplace in which corporations search for the most advantageous locationsto buy, produce and sell their goods and services.

These trends especially of globalization cannot be stopped. The hostility towards globalizationarises from the uneven distribution of benefits and costs across countries. Anti globalists claim thatliberal trade which is essential to raising the incomes and improving the longer term developmentprospects of the world’s poor worsens poverty. The benefits of globalization can only be harnessedif the risks are contained. Countries pursuing sound macroeconomic policies and with strong andresilient financial systems can reap the benefits of globalization. Globalization involves free flow oflabor as much as free flow of goods and services.

Reasons for Evolution of MNEs

The classical theory of international trade as first developed by Adam Smith and David Ricardorests at the doctrine of comparative advantage, each nation should specialise in the production andexport of those goods that it can produce with highest efficiency and import those goods that othernations can produce relatively more efficiently. The theory assumes that goods and services canmove internationally but factors of production such as capital, labor and land are relatively immobile.

Financial Management of a Multinational Enterprise 7

The classical theory deals with only undifferentiated products and ignores the role of uncertainty,economies of sales, transportation costs and availability of technology. The theory however remainsthe best to base the case for free trade.

But in recent times the differences in corporations rather than differences among countrieshave become material. Natural resources have lost their previous role in national specialization.Capital and technology move freely across continents. Labor skills are no longer fundamentallydifferent. Technology and knowhow have become a global pool. Corporations of all sizes can tap theglobally available factors of production. Further value addition is split among different countries as inthe case of Barbie doll (10 countries).

The rise of multinational corporations may be prompted by the search for best productionlocation in terms of cost efficiency or the best market in terms of profitability.

Search for raw materials: The British, Dutch and French East India companies grew underthe protective mantle of British, Dutch, French and Belgian Colonial empires. Raw materials werethe attraction.

Market seeking: IBM, Unilever, Mcdonald maintain vast manufacturing and distribution networksfrom which they derive substantial sales and income. Firm specific advantages (which include uniqueproducts, processes, technologies, patents, specific rights or specific knowledge and skills) can alsobe used in foreign markets. The exploitation of foreign markets may be possible at considerablylower costs. Foreign markets may in some cases be essential to lower costs. Global scanning capabilitycan help seek out lower cost production sites or production technologies worldwide. Off shoring andoutsourcing can help remain cost competitive at home and abroad.

Rationale of Multinational Enterprise

The theory of multinational enterprise presents the rationale of MNEs in terms of their efficiency.MNEs are efficient because they create rents when they establish interdependences among economicagents located across national boundaries. Hennart defines the MNE as a private institution devisedto organize through employment contracts interdependencies between individuals located in morethan one country.3 The contributions of J.F. Hennart to business literature viewed the MNE as anefficiency driven, transaction cost reducing and welfare enhancing institution.

Transaction Cost Theory

Agents located in two different countries have the potential if they combine their capabilitiesthrough international markets or within MNE of creating rents. Transaction costs theory focuses onthe problem of organizing interdependencies between individuals who can generate rents by poolingtogether different or similar capabilities. Transaction costs are incurred to organize cooperation through

3. Hennart, J. Vean-Francois. “Theories of the Multinational Enterprise” in Eds Rugman, Alan M and Brewer, ThomasL., The Oxford Handbook of International Business.

8 International Financial Management

information, enforcement and cooperation. MNEs arise because they are efficient at organizinginterdependencies between agents located in different countries than markets and contracts.

According to transaction costs theory the cost of organizing a transaction varies with the methodof organization chosen to organize it. Prices and hierarchy are methods of organization while marketsand firms are institutions. Both institutions make use of both methods but markets use predominantlyprices and firms hierarchy. According to transaction costs theory the cost of organizing a giventransaction varies with the choice of organization (hierarchy vs. prices) and institution (markets vs.firms). While both institutions make use of the both methods simultaneously, markets use predominantlyprices and firms hierarchy. Firms can be more efficient than markets if they replace output bybehaviour constraints.

Transaction cost theory is based on a comparison of the cost of organizing interdependencies infirms and in markets. Firms are more efficient than markets because they replace output by behaviourconstraints. The combination of assets is more efficiently done within a MNE than through spotmarkets or contracts. The characteristics of interdependencies that make their organization withinmarkets more costly than within MNEs are know-how, raw materials and components, marketingand distribution services and financial capital. An emerging area is knowledge related assets.

“Globalization, and the critical importance of upgrading intellectual capital as a wealth enhancingprocess, is demanding that scholars should give more attention to the harnessing, creation andorganization of knowledge related assets from different locations as a competitive advantage in itsown right. The variables affecting the ‘where’ of MNE activity, as firms seek to reconcile themobility of many of their intangible assets with the need to deploy these with other assets which arenot only location bound but concentrated in a limited spatial area is also under scrutiny”4.

It has to be noted that the rise of international markets would increase and decrease that ofMNEs if property rights are well defined and enforced. On the other hand, the efficiency of MNEsand their role in international economy would be enhanced by improvements in business technologythat reduce the costs of managing the firms. Given the trends in a globalisation it is likely that MNEswill assume the management of interdependencies that used to be managed by markets. MNE isconsidered an appropriate vehicle for the transfer and exploitation of proprietary knowledge as wellas for knowledge development, and extension or acquisition across borders. They also contribute toglobal diffusion of knowledge by increasing the foreign knowledge absorption capacity of localizedinvestment clusters.

Maximizing the Value of Firm

The conventional approach to financial management is concerned with how to optimally makevarious corporate financial decisions relating to investment, capital structure and dividend policy witha view to maximize shareholder wealth. The idea is to acquire assets whose expected return exceeds

4. Dunning, John, H. “The Key Literature on IB Activities” in Oxford Handbook of International Business, Eds. Rugman,Alan M and Brewer, Thomas L.

Financial Management of a Multinational Enterprise 9

their cost, to finance with those instruments where there is particular advantage, tax or otherwiseand to undertake a meaningful dividend policy for stockholders.

The objective of maximizing shareholder wealth provides a rational guide for running a businessand for the efficient allocation of resources in society. The market value of a firm’s share embodiesreturn and risk and reflects the markets trade off between risk and return. An investment decision atthe level of the firm which takes into account the likely effect on the market value of its share willattract capital only when its investment opportunity justifies the use of that capital in the overalleconomy. Maximization of the share value alone will lead to optimal capital formation and growth.

Social Contract between Business and Society

The objective of shareholder value maximization has however to be viewed as a part of thesocial contract between business and society. This contract has obligations, opportunities and mutualadvantage for both sides according to Ian Davis of McKinsey and Company5. Otherwise it couldlead managers to focus excessively on improving the short term performance of their businessneglecting important long term opportunities and issues such as trust of customers, investment ininnovation and other growth prospects. Maximization of shareholder value also obscures questionsof ethics and legitimacy. Multinational enterprises need to tackle such issues for reasons of integrityand enlightened self interest.

The new approach calls for

Introduction of explicit processes to make sure that social issues and emerging social forcesare a part of overall strategic planning.

Active management of individual contracts by more transparent reporting, shifts in R&Dor asset reorganization to capture expected future opportunities or to shed perceived liabilities,changes in regulatory approach.

Development and deployment of voluntary standards of behaviour at an industry level.

Establishment of ever higher standard of integrity and transparency and active involvementin debates on social issues that shape their business context.

The ultimate purpose of business is the efficient provision of goods and services that societywants. It is the fundamental basis of the contract between business and society. Such a noble purposeis not only more motivating but also beneficial to shareholder value over the long term. Shareholdervalue creation or profits are a measure and reward of efficient provision of goods. Restating andreinforcing the business’ own social contacts will also secure for the long term the shareholders’investment.

5. “The Biggest Contract”, The Economist, May 28, 2005.

10 International Financial Management

Investment Decision

The optimal combination of the three decisions, investment decision, the financing decision andthe dividend decision will maximize the value of the firm. The investment decision determines thetotal amount of assets held by the firm, the composition of the assets and the business risk of the firmas perceived by creditors. Since investment proposals involve risk they should be evaluated in relationto their expected return and risk. The choice of a required rate of return is crucial.

Financing Decision

Determination of the capital structure of the company, the mix of debt and equity. The degreeto which companies use debt known as leverage instead of equity varies from country to country.Leveraging is often perceived as the most effective route to capitalization, because interest on debtis tax deductible while dividends paid to investors are not. Leverage increases financial risk andrequires a higher return for investors. Access to local capital markets may be limited for foreignsubsidiaries. The Asian financial crisis was partly on account of the reliance by Asian companies ondebt to fund their growth.

Dividend Decision

Dividend decision includes the percentage of earnings paid to shareholders in cash dividends,the stability of absolute dividend about a trend, bonus issues and buy- back of shares. The value ofdividend to investors must be balanced against the opportunity cost of the retained earnings cost as ameans of equity.

Global Competitiveness

With globalization, technology and finance move swiftly across countries to exploit markets. Nofirm can be complacent. It is not only at the macro or country level that competitiveness has to beattained. It has to start at the micro or firm level. Competitiveness of a firm which promotes efficiencyhas a favourable impact on the use of resources, costs and profits. Every firm engaged in businesshas to be internationally competitive. Otherwise, it cannot survive. In today’s globalized world theshare value is influenced by not only the financial factors but how competitive the firm is. Accordingto Vohn Roberts, high performance in a business results from establishing and maintaining a fitamong the strategy of the firm, its organizational design and the environment in which it operates.6

Global competition and changes in technology require that overall strategy should include as notedearlier social issues and emerging social forces.

6. “The Biggest Contract”, The Economist, May 28, 2005.

Financial Management of a Multinational Enterprise 11

Factors Influencing Competitiveness

Technology has played a key role in improving the terms of global trade competitiveness. Thepresence of dynamic and discernable buyers at home contributes to the improvement in products.The presence of suppliers and firms in supportive industries in the vicinity of the exporting firms hasbeen a major source of competitive advantage. Export competitiveness defined as the ability of acountry to expand its share in world markets was related earlier to production abilities. It is recognizednow that structural changes in production also impact on competitiveness. These consist of newtechnologies, novel ways of organizing production and trade policies. The exchange rate is regardedas a crucial determinant of price competitiveness. Other important non price factors are productquality, brand equity, packaging, delivery and after sales service.

The opportunities provided by global developments were exploited by India by industrial andtrade liberalization. There has been a turnaround in total factor productivity growth in Indianmanufacturing since the mid 1980s on account of the reorientation in trade policies and improvedinfrastructure performance. Efficiency in the use of material inputs has also been recorded in thesecond half of 1990s. Transaction costs of exporters have declined. India’s share in world exportsrose to 0.8%, in 2002 from about 0.5% in mid 1980s. In the past five years India’s exports haveshifted towards technology intensive high value manufactures as well as IT services.

According to the Global Competitiveness Reports of the World Economic Forum India ranked48 in “Global Competitiveness rank” in 2002 as compared with 52 in 1999. In 2002 India ranked firstin prevalence of foreign technology licensing, second in availability of scientists and engineers, fifth inaccess to credit, seventh in intensity of local competition and eleventh in interest rate spread.

The assessment of UNCTAD of the pattern of global trade competitiveness reveals that in agroup of 20 top gainers of export market share during 1985-2000 India ranks 14th in terms of overallexports, fifth in resource based manufactures and seventeenth in medium technology manufactures.

Corporate Governance

In the new millennium corporate governance providing the systems and processes which ensurethe efficient functioning of the firm in a transparent manner for the benefit of all the stakeholders andaccountable to them has assumed significance because of audit failure and excessive executive payin several countries. The watchdogs, the boards and external auditors who are supposed to exerciseoversight to protect the interests of shareholders have failed to do so. Any system of governance hasto provide for checks and balances and countries across the world have failed to do so. The mix upbetween board and management has left the shareholders bereft of any protection they should getfrom the board elected by them to protect their interests. There should be firewalls between boardand management in case of any public limited company which accesses capital market.7 It is essentialto present a corporate governance report for information of stakeholders and investors on thecompany’s web site to ensure transparency and accountability.

7. H.R. Machiraju, Corporate Governance, 2004, Himalaya Publishing House, Mumbai.

12 International Financial Management

Criteria for Competitiveness

The Far Eastern Economic Review which conducts the survey of Asian top 200 companiesconsiders criteria for competitiveness8

Premium quality of product and services. Innovative response to customer needs. Long term vision. Financial strength. Market leadership/role model for others.

In Asia only 14 companies satisfied these criteria; and among Indian companies only threecompanies met the criteria, Hindustan Lever, Reliance Industries and Larsen & Toubro. The commontrait among all the 200 companies that survived and thrived through the Asian crisis was their abilityto act quickly, decisively and provide an innovative solution to the turbulent market needs. Thesecompanies identified new opportunities, took a fresh look at their products and markets and challengedthe existing paradigms.

An integral part of competitiveness is the decision to obtain the optimum combination of inputsfrom the variety of opportunities open in the global market. This decision also influences the valuationof the firm.

Production Efficiency

International companies may compete by seeking maximum production efficiency on a globalscale. To achieve this objective the company’s production would use the best inputs for the priceeven if the production location moved abroad. The management in MNEs are slicing off the activitiesof firms more finely and finding optimum locations for each closely defined activity. While doing sothey are deepening international division of labor. It is observed in practice that the demand andincome for higher paid employees in the US for instance has increased as a result of US companiesoutsourcing to low labor cost countries. Companies should have global efficiency objective keepingin view that they are entities of a given society with national objectives.

Global Manufacturing and Supply Chain Management

The efforts of international firms to source inputs and locate production anywhere in the worldwhere costs are lower and profitability better guides investment. Global outsourcing is an integralpart of supply chain management which results in value addition. FDI has poured into the manufacturingunits in China in the past decade at almost an annual rate of $50 billion dollars since risk returntradeoffs of such investment are better than in the home country. In companies’ international businessstrategies, global manufacturing and supply chain management are quite important. The supply chain

8. Saxena Rajan, “Global Competi tiveness of Indian Enterprises”, Chartered Secretary, November 2001.

Financial Management of a Multinational Enterprise 13

encompasses the coordination of materials, information and funds from the initial raw material supplierto the ultimate customer. The supplier can be located in the country where manufacturing or assemblytakes place or at a different location from where they can be shipped to the country of manufactureor assembly. The global supply chain links the suppliers’ supplier with customers’ customer accountingfor every step of the process between the raw material and the final consumer of good or service.

Supply Chaining is a Flattener9

According to Thomas L. Friedman supply chaining is one of the flatteners that have made theworld flat (metaphor for globalization). Flatness is simply a company’s ability to use newcommunications technologies to cut costs by speeding up the work process and sourcing labour andinputs from every corner of the globe. Flateners include windows, the internet, workflow and opensource software, outsourcing, offshoring (FDI), supply chaining, insourcing, google and wirelesscommunication. Friedman contends that flatness is making the world less hierarchical, more prosperousand equal, more transparent and democratic and less prone to war.

Global Manufacturing Strategy

The success of global manufacturing strategy depends on

Compatability.

Configuration.

Coordination.

Control.

The compatability decision pertains to the consistency between foreign investment decision andthe company’s competitive strategies in terms of efficiency/cost, dependability, quality, flexibility andinnovation. The objective of reduction of manufacturing costs drives international firms to establishmanufacturing units in areas of low labor cost in Asia, East Europe and Mexico. This type of foreigninvestment known as offshore manufacturing spread widely in 1960s and 1970s in the electronicsindustry when several companies set up production facilities in Taiwan and Singapore. At thoselocations labor costs were low and cheap raw materials and components were available. Manufacturingshifted to other low cost countries such as China, Indonesia, Malaysia, Thailand and Vietnam.

Manufacturing configuration consists of centralized manufacturing and export, regional facilitiesto serve specific regions and multi domestic manufacturing in which companies manufacture productsto meet local needs. International firms choose a combination of these approaches depending ontheir product strategies.

Coordination is the linking of activities along the global supply chain from purchase to storage toshipment. Finally control system including organizational structure ensures the implementation ofcompany strategies.

9. Friedman Thomas L., The World is Flat, 2005 Farrar, Straus and Giroux, New York.

14 International Financial Management

Sourcing

Sourcing is the process of having raw material and parts supplied to it for the production process.Global sourcing is the first step in the process of materials management called logistics. Outsourcingis a situation in which an organization purchases or processes from external vendors that it couldhave produced inhouse. Ford used global sourcing of parts from plants in 15 countries for finalassembly in UK and Germany. If domestic sources are unavailable or more expensive than foreignsources international sourcing is resorted. Japan imports all of its requirement of uranium, bauxite,nickel, crude oil, iron ore, copper, coking coal and 30% of agricultural production.

Global sourcing is undertaken to

Reduce costs, labor, land and other facilities.

Improve delivery of supplies.

To gain access to materials available only abroad.

To establish a presence in foreign markets.

Vertical integration is a major outsourcing configuration where the company owns the entiresupplier network or a major part of it. In determining whether to buy/outsource parts to suppliers, adistinct comparative advantage, such as greater scale, lower cost structure or stronger performanceincentives should exist. Outsourcing from abroad is subject to factors such as distance, time anduncertainty of political and economic environment. Outsourcing or offshoring has been going on forcenturies but still accounts for a tiny proportion of the jobs constantly being created and destroyedwith America’s economy. Low wage India ranks eighth in 2002 among countries to which the USsends business, professional and technical service tasks. Ranking ahead of India were Canada,U.K., Japan, Germany, France, Mexico and the Netherlands. According to the Chamber of Commerceof US the global sourcing practices mention several balancing factors.

The cost savings to consumers and tax payers that can be achieved through sourcing.

The relatively small number of jobs lost to sourcing.

The risks of retaliation should America try to close its markets.

The tens of millions of jobs that foreign companies support in the US.

The $60 billion surplus in service trade that US enjoys.

The idea that the freedom to source, trade and compete around the world can lead to thebetter, high paying, jobs at home.

Stages of Outsourcing

Outsourcing passes through five stages.

Embryonic stage: Ancillary activities and basic commodity type offering where little valueis added are outsourced. The basis of outsourcing is transaction based.

Financial Management of a Multinational Enterprise 15

Developmental stage: Outsourcing is deployed to areas which are more central to businessprocess. Value is realized in various areas of support activities in the value chain.

Consolidation and interlinking outsourcing stage: Organizations adopt an overarchingoutsourcing strategy which is dovetailed to business strategizing. Outsourcing is considereda key strategic resource.

Business process outsourcing stage is the highest order stage where key process activitiesare outsourced with full contractual responsibility granted to the outsourcing vendor.

Bespoke and customs built frameworks for outsourcing offer the organization the benefitof releasing resources to focus upon key competencies. Key process activities areoutsourced with full contractual responsibility granted.

Companies should outsource anything that is not tied directly to competitive differentiation. Anoutsourcing plan should identify core competencies that make the organization distinctive and buildingvalue creating outsourcing arrangements around these so as to augment these competencies. It hasto be noted that outsourcing is a strategic issue not a tactical consideration. Outsourcing should bebased on,

a statement of work interface methods on a day to day basis plan of communication shared vision and common end goals.

Reorganizing Production

Cheaper labor brings down production costs. This keeps companies competitive, raises profitsand reduces prices as firms pass lower costs on to their customers. Ultimately innovation is stimulatedand new jobs created. Sourcing from cheaper countries also spreads the productivity enhancingeffects of such technology. Globalized production and international trade has made IT hardware10-30% cheaper.

If the system is administered by lower cost country it would restrain the spending. Outsourcingis a win-win proposition. Buying goods and services from poor countries is not only hugely beneficialto rich countries but also provides opportunities for people in poor countries.

The rise of MNEs would not have been possible without outsourcing. No company can hope toproduce all its requirements inhouse and has to procure raw materials and components from otherparties. Pioneers like Intel and Texas Instruments followed the FDI strategy of assembling chips inwholly owned subsidiaries in China, Malaysia and Hong Kong. Outsourcing was the driving forcebehind the global computer development.

By reorganizing production intelligently a multinational enterprise can hope to reduce its costsby 50 to 70%. Reorganization consists of handing over white collar work to specialist outside suppliers.Specialists offer corporate human resources services, credit card processing, debt collection or

16 International Financial Management

information technology work. Secondly the separation of geography of production and consumption.The manufacturing hubs were followed by hubs for televisions, cars, computers and other goodswhich emerged with the fall in transport costs in countries such as Mexico, Brazil, the Czech Republicand China. In the next decade hubs for producing such services as software engineering, insurance,underwriting and market research will emerge in Russia, China and India. The globalization work inmanufacturing involved investment in building factories in China to make clothes, toys, computersand consumer goods. Further investment to shift the production of cars, chemicals, plastics, medicalequipment and industrial goods is likely.

Outsourcing Manufacturing

Manufacturing is revolutionized by technology and economics. As industries advancemanufacturers manage the growing complexity of their products by outsourcing; they share the workof making them with others. This enables each company in the production chain to specialize in partof the complicated task. At each level of production, outsourcing divides up-growing complexity intomore manageable pieces. International playing field is being levelled by information technology.

Outsourcing Administrative Work

Computer is the tool used to mechanize work in the office. Computers save labor, bring downcosts and raise profits. They automate paper work and hence the flow of information. Banks andinsurance firms which sell information products employ computers to automate production. Computersare used by all companies to automate the administrative work: Keeping their books in good order,complying with rules and regulations, recruiting, training and looking after employees. Banks andinsurance companies have used some of the profits resulting from the use of computers to add bellsand whistles to their products making them more complex. The spread of computers through companieshas added a third layer of complexity, the task of managing the information systems themselves.

White collar work has become quite complex. The solution is to do less inhouse. Half of world’sbiggest companies have outsourced IT work. When companies outsource, the workers who operatethe business system is called business process outsourcing (BPO), e.g. First Data Corporation (FDC)employs 30,000 people who administer 417 m. Credit card accounts for 1400 card issuers.Administrative work and their supporting systems such as processing invoices, collecting paymentsfrom debtors and payroll work are outsourced.

Common standards in manufacturing have helped in use of common production platforms formanufacture of cars and consumer electronics. In white collar work a similar platform productionsystem is emerging. Extreme specialization is emerging in outsourced business. Business softwarepackages offer standard ways of organizing and delivering administrative office work.

Outsourcing White Collar Work

Supplying a service is a continuous process. It takes trust and cross cultural understanding toachieve a good working relationship. Secondly, white collar work is much less structured and rule

Financial Management of a Multinational Enterprise 17

bound than work done on shop floor. The concern about exporting jobs for instance in USA is similarto mechanization 75 years ago. Outsourcing is only changing the way to produce things. This changein production technology has the same effect as automation. But the same changes in productiontechnology that destroy jobs also create new ones. During 1999-2003, IT related white collar jobs inUS have risen.

Impact of Information and Communication Technologies on Outsourcing

The driving force behind information and communication technologies (ICT) is for global laborarbitrage. U.S. companies which segmented earlier production chain and shifted labor intensiveparts to low wage locations, now digitize them and access services from abroad through wires at20% of US wages. Digitization converts labor or service from a non-tradable into tradable units. Formany services physical presence is no longer necessary and the service personnel may be locatedany where in the world. The jobs were exported to cost effective locations like India. Offshoresoftware development started the IT and BPO industries. The services initially were restricted toback office functions like call centers, helpdesks and customer support coming under the category ofBPO. From BPO to other IT enabled services such as engineering design, architecture and radiographyis a short hop. Estimates of the market are $300 billion per annum.

Any service that can be electronically transmitted is produced in India more cheaply. Off shoring(work sent overseas) has spread from manufacturing to white collar services. New economycommunications and computer technologies have brought down costs, raised profits and gave aboost to growth. Cheaper communications allow companies to move back office tasks such as dataentry, call centers and payroll processing to poorer countries. A fair part of the work that movesabroad represents an attempt by companies to provide a round the clock service by making use oftime zones which improves efficiency. Further every dollar of costs according to Makinsey GlobalInstitute, the US moves offshore brings America a net benefit of $1.12 to $1.14. The benefit arisesbecause, as low value added jobs go abroad, labor and investment can switch to jobs that generatemore economic value. When employment dwindled in manufacturing, workers in USA have movedto educational and health services where pay is higher and conditions more agreeable. A recentsuccess story of moving workers from Europe to India (Delhi) to work at a call centre on Indianwages with accommodation and return air passage on an annual contract could be tried in USA.That would take the sting out of outsourcing. The movement of jobs to the developing countries doesnot alter the overall level of employment in the advanced countries. The pattern however is sure tochange.

Size of Outsourcing Market

The offshore movement set off in early 1990s when American Express, British Airways, GeneralElectric and Swiss Air set up their own captive outsourcing operations in India. The captive units findthat their costs are 50% higher than those of independent third parties. The captive business is nowbeing spun off as independent firms.

18 International Financial Management

The world outsourcing market is estimated to be about $5 trillion in 2002 according to theOutsourcing Research Council. America accounts for 70% of all offshore business. Of the totalbusiness, 20% is constituted by the IT and ITES market which is growing at about 15% p.a. Of thisIndia received about 2%. India’s IT market has grown from $1.73 billion in 1994-95 to $16.5 billion in2002-03. BPO activities (call center operations) in India are projected to touch $3.6 billion in 2004and $13.4 billion in the next three years. India’s biggest regional competitors are China and Philippines.

REFERENCES Bhagvati, Jagdish, In Defence of Globalization, 2004, Oxford University Press. Buckley, Peter, J. and Ghauri Perrez, N., “Globalization, Economic Geography and the Strategy of

Multinational Enterprises”, Journal of International Business Studies, December 2003. Daniels, John, D. and Radebaugh, Lee, H. International Business, 9 edn, Prentice Hall, New Jersey. Dunning, John, H., Location and the Multinational Enterprise, Journal of International Business

Studies, (2009), 40, 5-19. Eun, Chirol, S. and Resnick, Isruce, G., International Financial Management, 3 edn, Irwin. Friedman Thomas L., The World is Flat, 2005 Farrar, Straus and Giroux, New York. Madura, Jeff, International Financial Management, 7 edn. Thomson. Ross, Stephen, A., Wester Field, Randolph, W. and Jordan Bradford, D., Fundamentals of

Corporate Finance, 3 edn. Irwin, Chicago. Saxena, Rajan, “Global Competitiveness of Indian Enterprises”, Chartered Secretary, November 2001. Van Home, James, C., Financial Management and Policy, 8 edn., Prentice Hall of India. The Economist, December 13, 2003, February 21, 2004 and November 13, 2004. Morgan, Robert, E., “Outsourcing: Towards the Shamrock Organization”, Journal of General

Management, Winter, 2003. Reserve Bank of India, Annual Report, 2002-03 and Report on Currency and Finance, 2002-03. UNCTAD, World Investment Report, 2002 and 2014. Dunning, J.H., Multinational Enterprises and the Global Economy (1992) Workingham: Addison-Wesley, The Globalization of Business, 1993 Routledge, London. Hennart, J.E., A Theory of Multinational Enterprise, 1982, University of Michigan Press, Ann

Arbor. And “Transactions Costs Theory and the Multinational Enterprise” in C. Pitelis and R.Sugdyen (eds) The Nature of the Transnational Firm, 2nd edn. Routledge, London.

Ian Davis, The Biggest Contract, The Economist, May 28, 2005.John Roberts, The Modern Firm, 2004, Oxford University Press.

Desai, Mihir, A., C. Fritz Foley and James, R. Hines (Jr.), “Domestic Effects of the Foreign Activitiesof US Multinationals” American Economic Journal: Economic Policy 2009.

UNCTAD, World Investment Report, 2014.