international financial reporting standards - cinif · international financial reporting standards...

TRANSCRIPT

International Financial Reporting Standards

H d tiHedge accounting

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

International Financial Reporting Standards

Exposure draft

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

3Components of the hedge accounting model

Objective

Alternatives to hedge accounting Hedged items

j

Presentation and Disclosure Hedging instruments Hedge accounting

(exposure draft) g g(exposure draft)

Groups and net positions

Discontinuation and rebalancing

Effectiveness assessment

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

and rebalancing

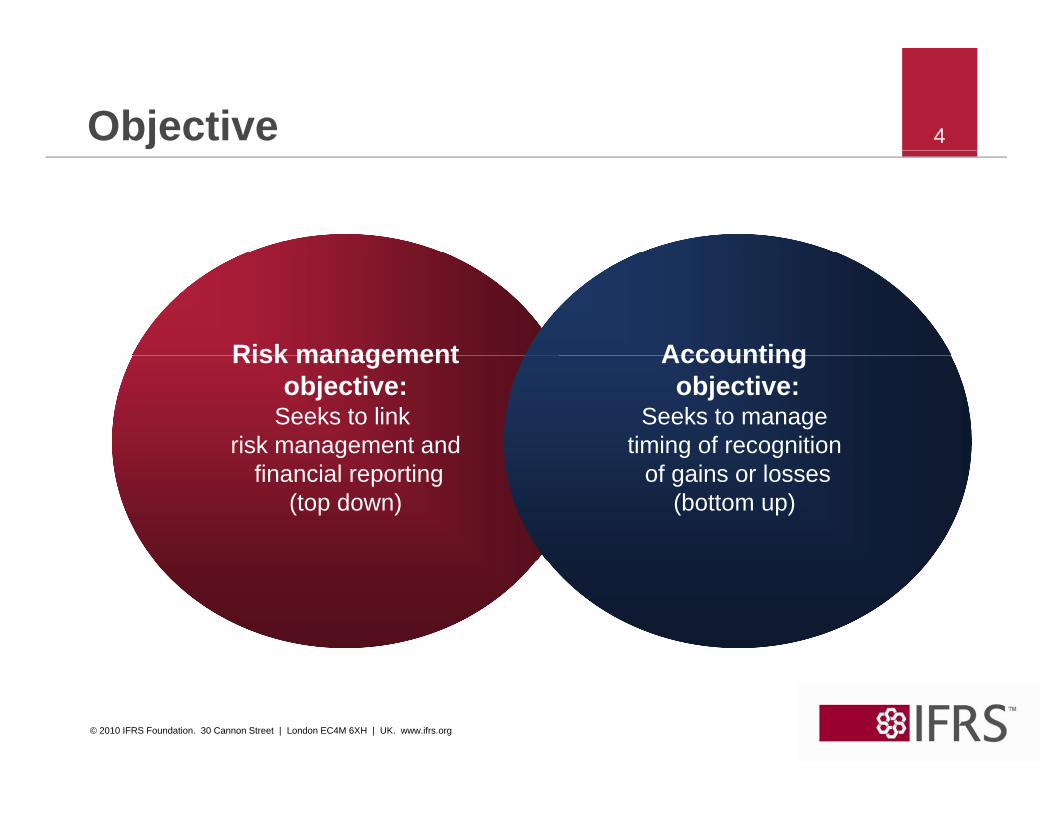

4Objective

Risk management AccountingRisk managementobjective:

Seeks to link risk management and

Accounting objective:

Seeks to manage timing of recognition g

financial reporting(top down)

g gof gains or losses

(bottom up)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

5Hedged items

Qualifying hedged itemhedged item

Entire item Component

Risk component(separately identifiable and reliably

measurable)

Nominal component or selected contractual CFs

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

6Hedged items: risk components

IAS 39 ED

Variable

Fixed element

Variable

Fixed element

Benchmark Benchmark

Variable element

Benchmark Benchmark

Variable element

(eg interest rate or

commodity price)

(eg interest rate or

commodity price)

(eg interest rate or

commodity price)

(eg interest rate or

commodity price)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

7Hedging instruments

Qualifying hedging instrumentsinstruments

Entire item Partial designation

FX risk component Percentage of nominal amount

• Intrinsic value• Spot element

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

8Time value of options

Time valueTime valueof options

Transaction related Time periodTransaction related hedged item

Time period related hedged item

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

9Hedge effectiveness

HedgeHedge effectiveness

Hedge effectiveness requirements(qualifying criteria):(qualifying criteria):1. Objective of effectiveness

assessment is met2. More than accidental offset

Measuring and recognisinghedge ineffectiveness

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

10Discontinuation and rebalancing Objective of hedge

effectiveness assessment not metassessment not met

Risk management objective remained The risk management objective remained

the same

gobjective changed

Discontinue hedge accounting

Other than accidental offset

Merely accidental offset

Discontinue hedge accounting

Continue Hedge accounting

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

hedge accountingHedge accounting

11Disclosures: scopeProposed scope for hedge accounting disclosures

Total entity risk exposure(no specific disclosure requirements)

Hedged exposure(Exposure to risks being

IFRS 7 Disclosure requirements

hedged)

Significance of financial instruments for financial position and performance

Nature and extent of risks arising from financial instruments

Entity’s exposure attributable to the hedged risk

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

and performance

12Disclosures proposed

H d tiHedge accountingdisclosures

Ri k t The amount, timing Effects of hedgeti thRisk management

strategy

The amount, timingand uncertainty offuture cash flows

accounting on theprimary financial

statements

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

13Alternatives to hedge accounting

Alternatives

‘Own use’ scope exception in IAS 39

Credit derivatives(not proposed)in IAS 39 (not proposed)

Fair value accounting(3 alternatives considered)

Proposed consequential

amendment

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

( )amendment

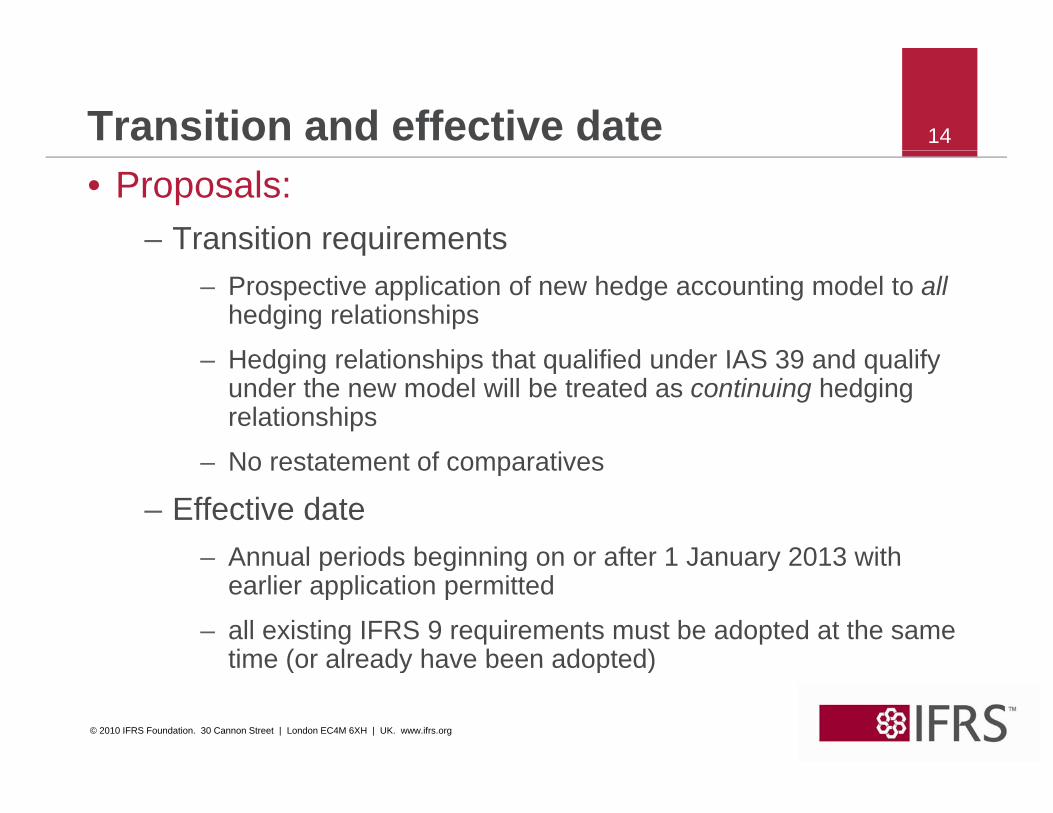

14Transition and effective date• Proposals:

– Transition requirementsq– Prospective application of new hedge accounting model to all

hedging relationships

Hedging relationships that qualified under IAS 39 and qualify– Hedging relationships that qualified under IAS 39 and qualify under the new model will be treated as continuing hedging relationships

No restatement of comparatives– No restatement of comparatives

– Effective date– Annual periods beginning on or after 1 January 2013 withAnnual periods beginning on or after 1 January 2013 with

earlier application permitted

– all existing IFRS 9 requirements must be adopted at the same time (or already have been adopted)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

time (or already have been adopted)

International Financial Reporting Standards

Outreach

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

16Exposure draft Hedge Accounting

• Exposure draft issued in December 2010• Comment letter deadline was 9 March 2011• During the 3-month consultation period for the exposure draft

the Board conducted extensive outreach across all majorthe Board conducted extensive outreach across all major geographical regions

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

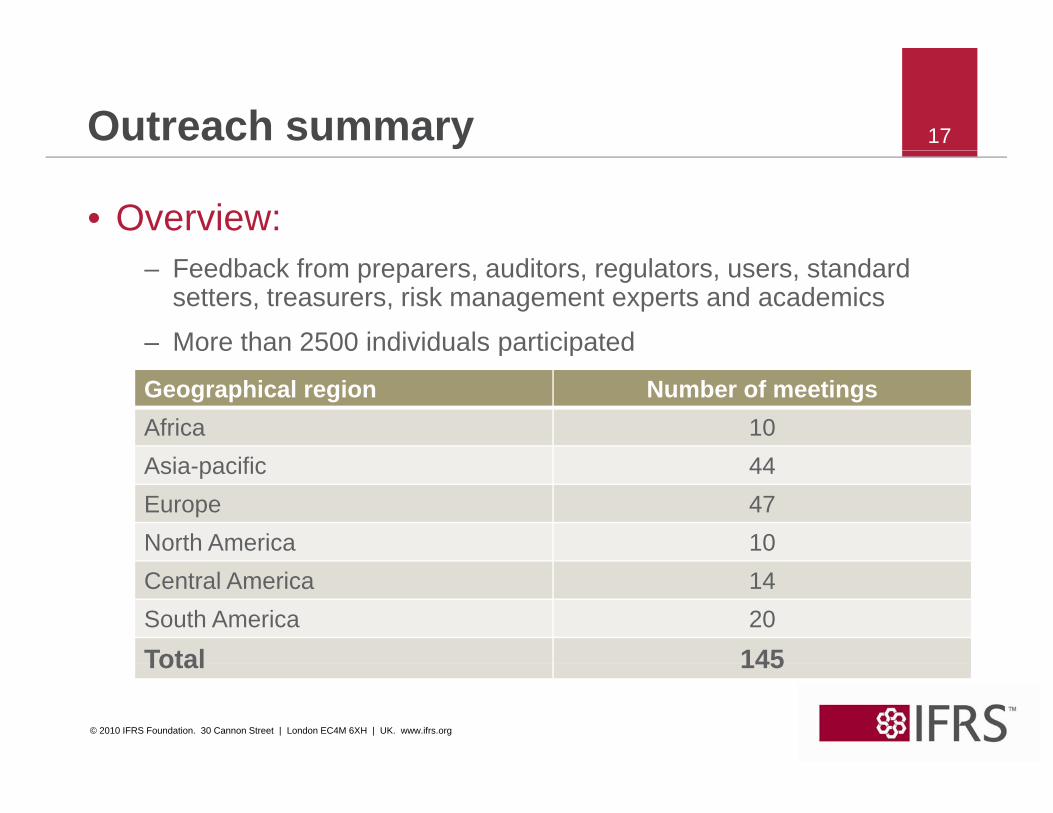

17Outreach summary

• Overview:– Feedback from preparers, auditors, regulators, users, standard

setters, treasurers, risk management experts and academics

– More than 2500 individuals participatedp p

Geographical region Number of meetingsAfrica 10A i ifi 44Asia-pacific 44Europe 47North America 10Central America 14South America 20

Total 145

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Total 145

Outreach summary 18

• Main positives include:– The Board’s objective to link hedge accounting with risk

management

The Board’s proposal to remove the 80 125% bright line for hedge– The Board s proposal to remove the 80-125% bright line for hedge effectiveness

– The Board’s proposal to allow risk components for non-financial ititems

• Main negatives include:– Disappointment that the exposure draft does not address macro

hedging

– The exposure draft does not enable entities to fully reflect their risk

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The exposure draft does not enable entities to fully reflect their risk management strategy for some economic hedges

Papers discussed at the April 2011 IASB meeting 19

For more detail please refer to Agenda PaperFor more detail please refer to Agenda Paper 7A of the April 2011 IASB meeting(R f t A d 7B f f th t l tt i d)(Refer to Agenda paper 7B for a summary of the comment letters received)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

International Financial Reporting Standards

Tentative decisionsTentative decisionsRedeliberations taking into consideration the

feedback received form the comment letters and the outreach activities

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

Feedback on Hedge Accounting ED 21

• Strong support for the ED including– improved link with risk managementp g

– proposal to remove the 80-125% bright line

– proposal to allow risk components for non-financial items

• Some concerns:– restriction on hedging for items affecting OCI (particularly equity g g g (p y q y

investments)

– Necessity for clarification of concepts

– Absence of topic of macro hedge accounting

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Changed in redeliberations 22

Topic Decision Equity investments measured at fair value through OCI

• Agreed to allow hedge accounting.

Fair value hedge accounting • Retain mechanics of IAS 39.mechanics • Require single note about cash flow

and fair value hedges.• Disclosure of fair value hedge

adjustment.

Hedging of layers with t ti

• Can hedge: l t ithi th h d d itprepayment options • a layer component within the hedged item

for the amounts that are not pre-payable.

• pre-payable layer if prepayment effect i l d d i t f h d d it

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

included in measurement of hedged item.

Changed in redeliberations 23

Topic Decision Net position cash flow hedges C h fl h d f t itiNet position cash flow hedges • Cash flow hedges of net positions are

only be available for hedges of foreign currency risk.

• Remove the restriction that the• Remove the restriction that the offsetting cash flows in a net position must all affect the income statement in the same reporting period.the same reporting period.

• Instead, the eligibility criteria are extended to require that the items within the net position must be specified in such a way that the pattern of how they will affect the income statement is set out as part of the initial hedge

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

designation.

Changed in redeliberations 24

Topic Decision ‘Own-use’ scope exception • Extend to contracts that meet the ‘own

use’ scope exception the FVO in IFRS 9 if it eliminates or significantly reduces an accounting mismatch.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Changed in redeliberations 25

Topic Decision

Accounting for forward points • Permit forward points that exist at inception of the hedging relationship to be recognised in profit or loss over time on a rational basis.

• Recognise the difference betweencumulative amortisation and

b t f i l h isubsequent fair value change in accumulated other comprehensive income.

This is to provide a better representation of the economic substance of eg a ‘funding swap’ transaction and the performance of

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

swap transaction and the performance of the net interest margin.

26Changed in redeliberationsTopic Decision

Disclosures • Changed the disclosure requirements related to the amount, timing and uncertainty of future cash flows in the exposure draft. The Board tentatively decided to rather focus on the terms and conditions of the hedging instrument.

• Entities that use a dynamic hedging strategy that involves frequent resetting of hedging relationships are exempt from disclosing terms and conditions of the hedging instruments. Instead, they will:

• expand the risk management strategy description and explain how hedge accounting is used to reflect the dynamic hedging strategy; and

• if applicable, disclose that the volumes at year end do not reflect normal volumes.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

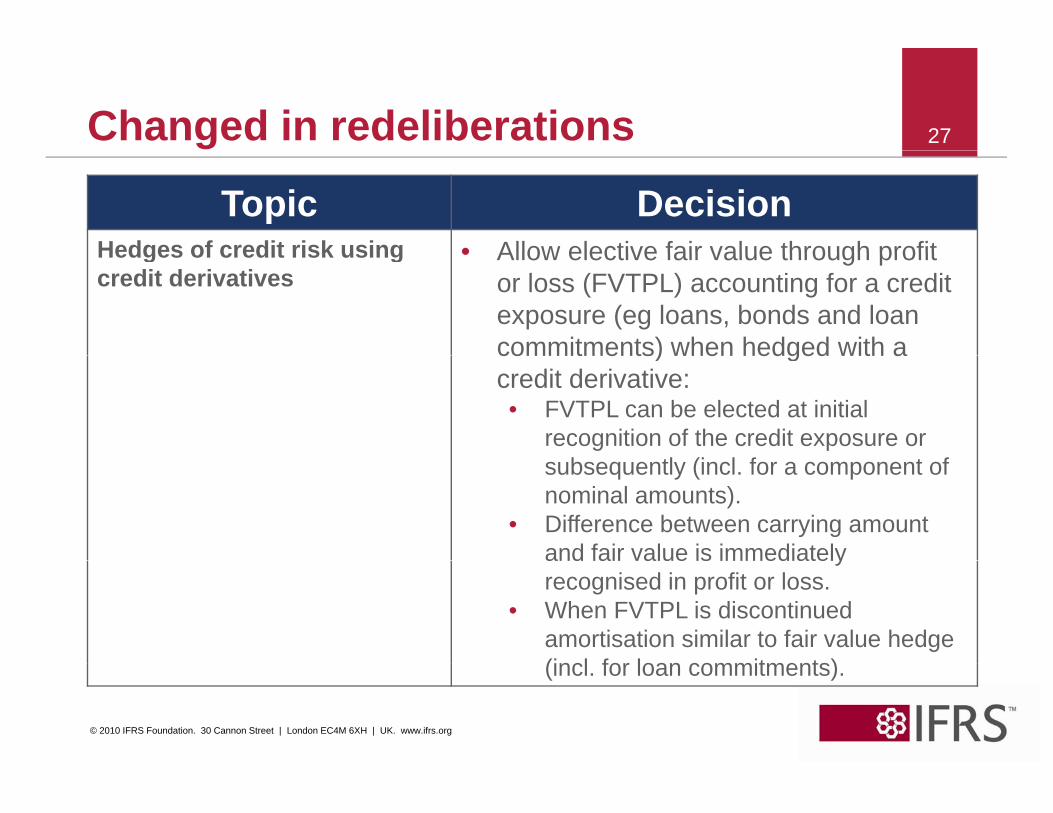

27Changed in redeliberations

Topic Decision Hedges of credit risk using • Allow elective fair value through profitHedges of credit risk using credit derivatives

• Allow elective fair value through profit or loss (FVTPL) accounting for a credit exposure (eg loans, bonds and loan commitments) when hedged with acommitments) when hedged with a credit derivative:• FVTPL can be elected at initial

recognition of the credit exposure or b tl (i l f t fsubsequently (incl. for a component of

nominal amounts).• Difference between carrying amount

and fair value is immediatelyand fair value is immediately recognised in profit or loss.

• When FVTPL is discontinued amortisation similar to fair value hedge (incl for loan commitments)

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

(incl. for loan commitments).

28Changed in redeliberations

Topic Decision Hedges of credit risk using credit derivatives (cont.)

• Disclosure requirements added:• A reconciliation of the nominal amount

and the fair value of the credit d i ti th t h b d tderivatives that have been used to manage the credit exposure.

• Gain or loss recognised in profit or loss as a result of electing fair value through g gprofit or loss.

• For discontinuations of elective fair value through profit or loss accounting for credit derivatives the fair value thatfor credit derivatives, the fair value that becomes the new deemed cost or amortisable amount.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 29

Topic Decision Cash instruments measured at FVTPL as eligible hedging instruments

• Did not extend to other cash instruments (ie those not at FVTPL).

• Clarified that liabilities measured at fair value under the FVO with the own credit effect in OCI are NOT eligible hedging instruments.

Hedging sub-LIBOR cash flows

• Cannot hedge a (‘full’) LIBOR component of a sub-LIBOR cash flow.Will l if th t t t l h fl b• Will clarify that total cash flows can be hedged for changes in LIBOR.

• Also applies to non-financial items.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 30

Topic Decision Effectiveness testing: clarification of the term ‘other than accidental offsetting’

• Clarify intention and rather refer to:• The notion of an economic

relationship between the hedged it d th h d i i t titem and the hedging instrument, which gives rise to offset.

• The effect of credit risk on the level of offsetting gains or losses on theof offsetting gains or losses on the hedging instrument and the hedged item that may reduce or modify the extent of offsettingextent of offsetting.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 31

Topic Decision Effectiveness testing: clarification of ‘unbiased’ and ‘minimise expected hedge ineffectiveness’

• Clarify intention that the hedge ratio of the hedging relationship shall be based on the entity’s ‘economic hedge’ ie:

ineffectiveness’ • The quantity of hedged item that it actually hedges.

• The quantity of the hedging instrument that it actually uses to hedge thatthat it actually uses to hedge that quantity of hedged item.

• But designation must not reflect an imbalance that would create hedge ineffectiveness in order to achieve an accounting outcome that is inconsistent with the purpose of hedge accounting.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 32

Topic Decision Accounting for time value of Confirm the accounting outcomes forAccounting for time value of options

• Confirm the accounting outcomes for the accounting for time value of options as proposed in the ED (ie based on the nature of the hedged item)nature of the hedged item).

• Expand the application guidance in the ED to assist distinguishing accounting for ‘transaction related’ and ‘time period prelated’ hedged items.

• Not introduce an accounting choice to account for time value of options either as: (i) proposed in the ED or (ii) in accordance with IAS 39.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 33

Topic Decision Designation of combinations of options as hedging instruments

• To amend the requirements such that a combination of a written and a purchased option (regardless of whether the hedging instrument arises from one or several different contracts) can be jointly designated as the h d i i t t id d th t thhedging instrument provided that the combination is not a net written option.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 34

Topic Decision Rebalancing • Align the notion of rebalancing with the

Board’s tentative decision on the hedge effectiveness assessment, hence:

• The hedging relationship is rebalanced for hedge accounting purposes when the ‘hedge ratio’ is adjusted for risk managementadjusted for risk management purposes.

• But designation must not reflect an imbalance that would create hedge

ffineffectiveness in order to achieve an accounting outcome that is inconsistent with the purpose of hedge accounting.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

hedge accounting.

Confirmed in redeliberations 35

Topic Decision Rebalancing (cont.) • The notion of proactive rebalancing is

eliminated.• Clarify that rebalancing covers only

adjustments to the quantities of the hedged item or the hedging instrument for the purpose of maintaining a hedge

ti th t li ith thratio that complies with the requirements of the hedge effectiveness assessment.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 36

Topic Decision (No) Voluntary Discontinuation

• Add guidance about how the risk management objective and the risk management strategy relate to each other using examples contrasting these two notions.

• Confirm the proposals in the ED and h hibit l t di ti tihence prohibit voluntary discontinuation of hedge accounting when the risk management objective remains the same and all the other qualifying criteriasame and all the other qualifying criteria are still met.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 37

Topic Decision Aggregated exposures • Confirm proposal in the ED, that is,

allow designation of an aggregated exposure as the hedged item in a hedging relationship.

• Add illustrative examples to accompany the final standard.E li itl l if i th fi l t d d• Explicitly clarify in the final standard that the proposal does not allow 'synthetic accounting'.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 38

Topic Decision Aggregated exposures • Do not impose achieving hedge accounting

for the relationship between the exposure and the derivative that constitute the aggregated exposure as a precondition foraggregated exposure as a precondition for the aggregated exposure being eligible as the hedged item.

• Provide additional clarification by:y• explaining how aggregated exposures

relate to forecast transactions; and• adding application guidance on how to

apply the general requirement in theapply the general requirement in the context of aggregated exposures.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 39

Topic Decision Net presentation in a separate line item in the income statement

• Confirm the proposals in the ED regarding presentation in the income statement and that the separate line item for hedging gains and losses also includes the gains or losses on forecast transactions deferred to later periods.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

40Confirmed in redeliberations

Topic Decision Linked Presentation • Confirm the proposal in the ED that

linked presentation not be allowed for fair value hedges.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

41Confirmed in redeliberations

Topic Decision Hedging of risk components • Retain the notion of risk components as

eligible hedged items.• Determine eligible risk components on the

basis of the criteria proposed in the ED iebasis of the criteria proposed in the ED, ie that a risk component must be separately identifiable and reliably measureable.

• Use a single set of criteria for all items, ie gthat the criteria should apply for all types of items—risk components of financial and non-financial items.

• Provide guidance on how to apply the• Provide guidance on how to apply the criteria.

• Eliminate the general prohibition regarding designating inflation risk components (but

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

add a ‘caution’ and rebuttable presumption).

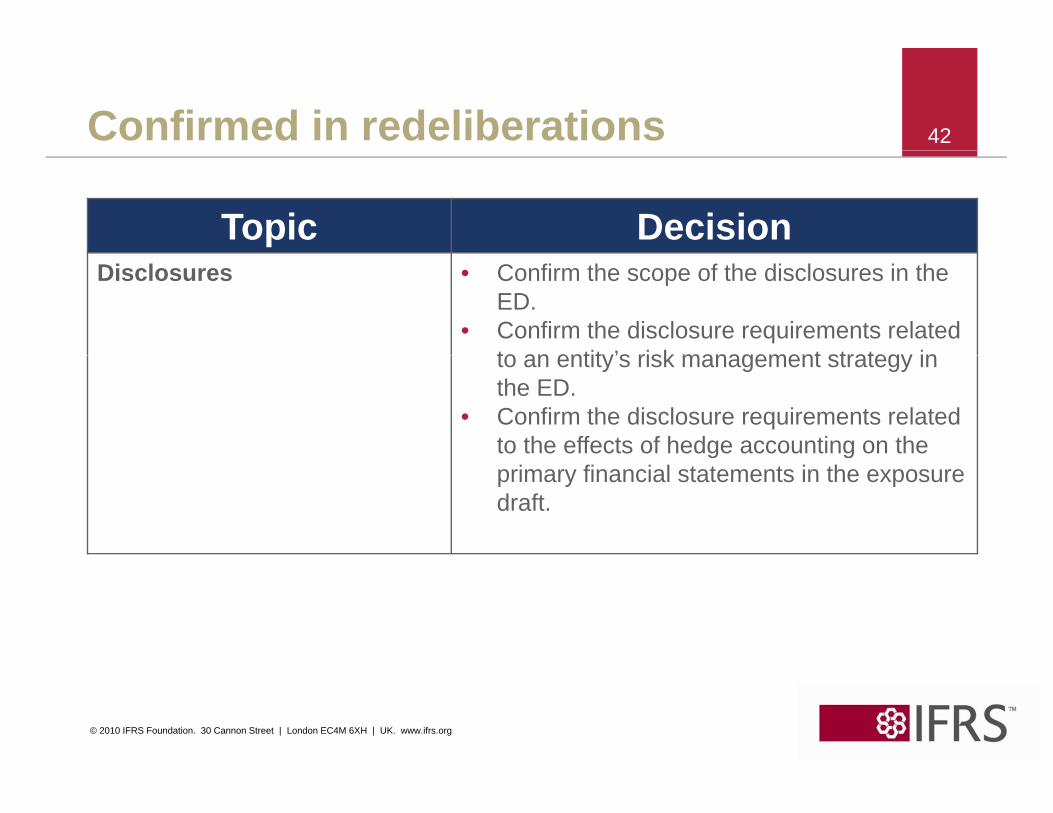

42Confirmed in redeliberations

Topic Decision Disclosures • Confirm the scope of the disclosures in the

ED.• Confirm the disclosure requirements related

to an entity’s risk management strategy into an entity s risk management strategy in the ED.

• Confirm the disclosure requirements related to the effects of hedge accounting on the g gprimary financial statements in the exposure draft.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 43

Topic Decision Transition requirements • Prospective with limited exceptions.

• Exceptions (for hedging relationships that exist at the beginning of the comparative period [or later]):• Required retrospective application

f ti f ti l ffor accounting for time value of options.

• Permitted retrospective application for accounting for forward elementsfor accounting for forward elements (if elected, applies to all such hedging relationships).

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Confirmed in redeliberations 44

Topic Decision Transition requirements Practical expedientsTransition requirements • Practical expedients

• Entities allowed to consider the moment IAS 39 ceases to applymoment IAS 39 ceases to apply and the moment from which the new model applies as one point in time.

• For the purpose of rebalancing, the starting point will be the hedge ratio used under IAS 39 (any gains or losses will be recognised in profit or loss).

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

General hedge accounting: timetable 45

E D ft l h d ti bli h d D b 2010• Exposure Draft on general hedge accounting published December 2010

• Redeliberations started in March 2011—completed in September 2011

• Staff draft of final general hedge accounting requirements available on website inStaff draft of final general hedge accounting requirements available on website in Q4 2011 (for about 3 months)

• Effective date will be aligned with other phases of IFRS 9

A l i d b i i f 1 J 2013/2015* i h liAnnual periods beginning on or after 1 January 2013/2015* with earlier application permitted

All existing IFRS 9 requirements must be adopted at the same time (or l d h b d t d)

2011 October | IFRS 9 Implementation Conference

already have been adopted)

International Financial Reporting Standards

Hedge Accounting:Macro Model

2011 October | IFRS 9 Implementation Conference

47Macro hedge accounting• In April the Board discussed portfolio risk

management activities• In June a group of banks presented information

about their risk management practices at a (public) education sessioneducation session.

• In September the Board discussed differences between the existing accounting and risk management and what broad approaches might be used to provide more useful information.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Status of the Macro Hedge Accounting Project 48

Fact finding Project status

Common themes Common themes

Implications for accounting model

Implications for accounting model Sept 2011accounting model

Design of

accounting model

Design of accounting model accounting model

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Interest rate risk Other risks

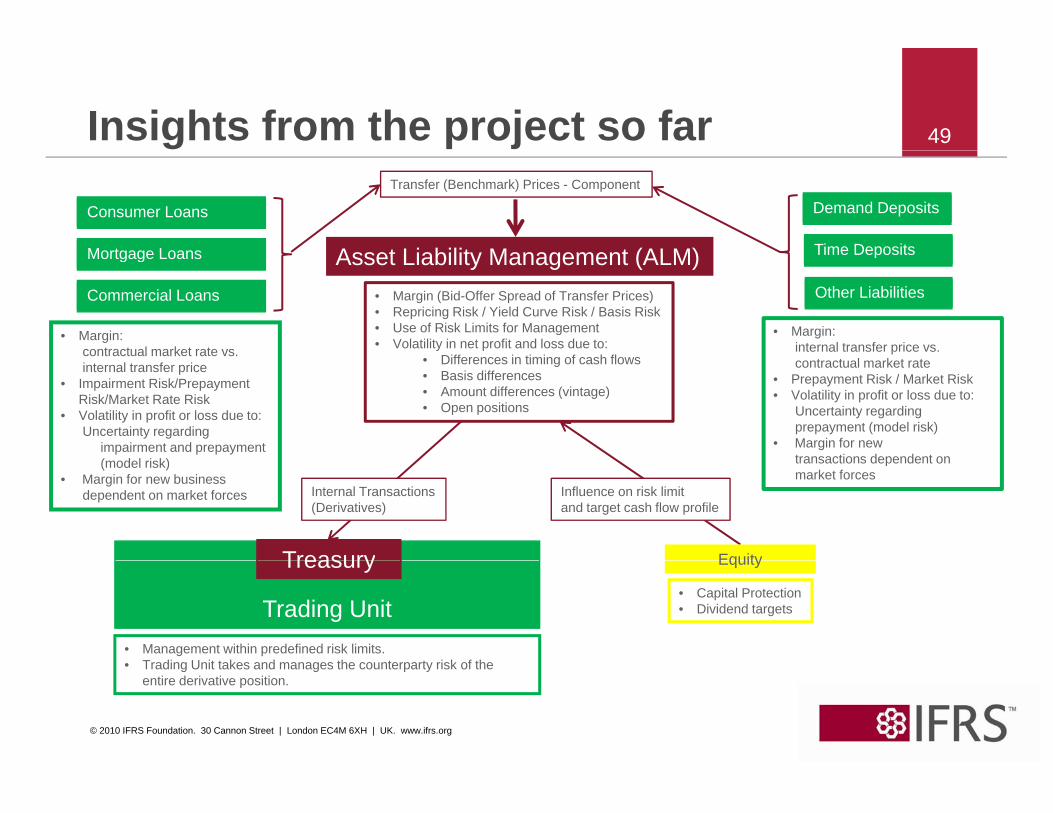

Insights from the project so far 49

Consumer Loans

Mortgage Loans

Demand Deposits

Time DepositsAsset Liability Management (ALM)

Consumer Loans

Mortgage Loans

Demand Deposits

Time Deposits

Transfer (Benchmark) Prices - Component

Mortgage Loans

Commercial Loans

Time Deposits

Other Liabilities• Margin (Bid-Offer Spread of Transfer Prices)• Repricing Risk / Yield Curve Risk / Basis Risk• Use of Risk Limits for Management• Volatility in net profit and loss due to:

Diff i ti i f h fl

• Margin:contractual market rate vs.

• Margin:internal transfer price vs.

Asset Liability Management (ALM)Mortgage Loans

Commercial Loans

Time Deposits

Other Liabilities

• Differences in timing of cash flows• Basis differences• Amount differences (vintage)• Open positions

contractual market rate vs. internal transfer price

• Impairment Risk/Prepayment Risk/Market Rate Risk

• Volatility in profit or loss due to:Uncertainty regarding

impairment and prepayment

contractual market rate • Prepayment Risk / Market Risk• Volatility in profit or loss due to:

Uncertainty regarding prepayment (model risk)

• Margin for new transactions dependent on

Treasury

(model risk)• Margin for new business

dependent on market forces

transactions dependent on market forces

EquityTreasury

Influence on risk limitand target cash flow profile

Internal Transactions(Derivatives)

Treasury• Capital Protection• Dividend targetsTrading Unit

Equity

• Management within predefined risk limits.• Trading Unit takes and manages the counterparty risk of the

Treasury

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Trading Unit takes and manages the counterparty risk of the entire derivative position.

EU IAS 39 ‘carve out’ 50

Remainder...

Hedged itemsHedged items

Hedge effectiveness

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Applicability to other industries 51

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

52Questions or comments?

Expressions of individual views by members of the IASB andby members of the IASB and its staff are encouraged. The views expressed in this presentation pare those of the presenter. Official positions of the IASB on accounting matters are determined only after extensive due process and deliberation.

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org