international fish farming company (pjsc) and …fs.sca.ae/.../annualreports/asmak2006are.pdf ·...

TRANSCRIPT

INTERNATIONAL FISH FARMING COMPANY (PJSC) AND SUBSIDIARIES ABU DHABI - UNITED ARAB EMIRATES CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR’S REPORT FOR THE YEAR ENDED DECEMBER 31, 2006

International Fish Farming Company (PJSC) and Subsidiaries Abu Dhabi - United Arab Emirates Consolidated Financial Statements and Independent Auditor’s Report For the Year Ended December 31, 2006 Table of Contents Page Independent Auditor's Report 1 & 2

Consolidated Balance Sheet 3

Consolidated Income Statement 4

Consolidated Statement of Changes in Equity 5

Consolidated Cash Flow Statement 6

Notes to the Consolidated Financial Statements 7 - 34

International Fish Farming Company (PJSC) and Subsidiaries 4 Abu Dhabi - United Arab Emirates Consolidated Income Statement For the year ended December 31, 2006 (In Thousands Arab Emirates Dirhams)

Note 2006 2005

Revenue 23 & 24 103,498 96,950

Cost of sales 19 ( 94,044) ( 87,904)

Gross profit 9,454 9,046

General and administrative expenses 18 ( 31,887) ( 27,562)

(Loss)/gain arising from changes in fair value less estimated point of sales of biological assets ( 380) 5,281

Earnings from investments 20 6,642 12,284

Share of loss in associates ( 76) ( 144)

(Loss)/gain on revaluation of marketable securities ( 1,832) 2,734

Impairment of goodwill ( 601) -

Impairment of property, plant and equipment ( 1,411) ( 394)

Loss on sale of property, plant and equipment ( 14) ( 349)

Net (loss)/profit for the year ( 20,105) 896 ======== ========

Attributable to: Equity holders of the parent ( 17,697) 889 Minority interest ( 2,408) 7

( 20,105) 896 ======== ========

(Loss)/earnings per share in AED 16 (0.59) 0.03 ======== ========

The accompanying notes form an integral part of these consolidated financial statements.

International Fish Farming Company (PJSC) and Subsidiaries 5 Abu Dhabi - United Arab Emirates Consolidated Statement of Changes in Equity For the year ended December 31, 2006 (In Thousands Arab Emirates Dirhams) Equity attributable to equity Total Share Statutory Accumulated holders of Minority Shareholders’ capital reserve losses the parent interest equity

Balance at December 31, 2004 300,000 478 ( 110,347) 190,131 372 190,503 Net profit for the year ended December 31, 2005 - - 889 889 7 896 Transfer to statutory reserve - 89 ( 89) - - - Balance at December 31, 2005 300,000 567 ( 109,547) 191,020 379 191,399

Net loss for the year ended December 31, 2006 - - ( 17,697) ( 17,697) ( 2,408) ( 20,105) Balance at December 31, 2006 300,000 567 ( 127,244) 173,323 ( 2,029) 171,294 ======== ======== ========= ======== ======== ========

The accompanying notes form an integral part of these consolidated financial statements.

International Fish Farming Company (PJSC) and Subsidiaries 6 Abu Dhabi - United Arab Emirates Consolidated Cash Flow Statement For the year ended December 31, 2006 (In Thousands Arab Emirates Dirhams)

2006 2005 Cash flows from operating activities Net loss for the year ( 20,105) 896

Adjustments for: Depreciation of property, plant and equipment 6,293 6,717 Impairment of goodwill 601 - Loss on sale and write off of property, plant and equipment 14 413 Interest income ( 4,358) ( 1,155) Provision of impairment of property, plant and equipment 1,411 394 Share of loss in associates 76 144 Provision for employees’ end of service indemnity 832 504 Changes in fair value of investments in marketable securities 1,832 ( 2,734) Provision for doubtful receivables 7,313 924 Loss/(gain) arising from changes in fair value less estimated point of sales cost of biological assets 380 ( 5,281)

Operating (loss)/profit before changes in operating assets and liabilities ( 5,711) 822

Increase in biological assets ( 1,775) ( 1,309) Increase in trade and other receivables ( 1,700) ( 10,552) Decrease/(increase) in inventories 6,066 ( 1,376) Decrease in due from related parties 3,683 119 Increase/(decrease) in due to related parties 612 ( 49) (Decrease)/increase in trade and other payables ( 563) 1,602

Cash generated from/(used in) operations 612 ( 10,743)

Employees’ end of service indemnity paid ( 719) ( 578)

Net cash used in operating activities ( 107) ( 11,321)

Cash flows from investing activities Decrease/(increase) in other financial assets 49,325 ( 49,325) Purchases of property, plant and equipment ( 11,050) ( 4,674) Proceeds from sale of property, plant and equipment 134 183 Interest received 3,796 636 Investments in associates ( 5,391) ( 165) Investment in marketable securities (Net) 3,276 66,186

Net cash from investing activities 40,090 12,841

Net increase in cash and cash equivalents 39,983 1,520

Cash and cash equivalents at the beginning of the year 40,957 39,437

Cash and cash equivalent at the end of the year (Note 5) 80,940 40,957 ========= ========= The accompanying notes form an integral part of these consolidated financial statements.

International Fish Farming Company (PJSC) and Subsidiaries 7 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements For the year ended December 31, 2006

1. Legal status and principal activities

International Fish Farming Company (PJSC) - Abu Dhabi (“the Company”), a Public Joint Stock Company, was incorporated on May 22, 1999, in the Emirate of Abu Dhabi by Emiri Decree No. 15 dated November 23, 1998. The Company is subject to UAE Federal Commercial Companies Law No. 8 of 1984, as amended. The registered address of the Company is P.O. Box 32619, Abu Dhabi, United Arab Emirates. Details of the Company’s subsidiaries at December 31, 2006, are as follows:

Proportion of ownership interest and Name of Place of incorporation Principal voting power subsidiary and operation activities held Alliance Foods United Arab Emirates Freezing fish and Company LLC seafood. 100%

Asmak Consulting United Arab Emirates Trading in fish and Company LLC seafood, and providing consulting services in field of sea resources. 100%

Asmak Seafood Processing United Arab Emirates Preparing and packing Company LLC seafood products. 100%

Asmak Quriyat LLC Sultanate of Oman Fish farming and (incorporated in trading in fish and November 2006) seafood products. 90% On November 1, 2006, in accordance with the Board of Directors’ resolution dated May 28, 2006, the operations of Ocean Fish of Oman LLC and Quriyat Aquaculture Company LLC, previously-owned subsidiaries in Oman, merged their operations into a new subsidiary Asmak Quriyat LLC, Oman. The assets and liabilities of the two old subsidiaries were transferred to the newly established subsidiary at cost. The principal activities of the Company and its subsidiaries (the “Group”) include investing in aquacultural projects, trading in fish and fish products, exporting, preserving fish and fish products and other sea living resources through cooling and freezing.

International Fish Farming Company (PJSC) and Subsidiaries 8 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

2. Adoption of new and revised International Financial Reporting Standards

In the current year, the Group has adopted all of the new and revised Standards and Interpretations issued by the International Accounting Standards Board (the IASB) and the International Financial Reporting Interpretations Committee (the IFRIC) of the IASB that are relevant to its operations and effective for annual reporting periods beginning on January 1, 2006. The adoption of these new and revised Standards and Interpretations has resulted in no changes to the Group accounting policies. At the date of authorisation of these consolidated financial statements, the following Standards and Interpretations were in issue but not yet effective:

IAS 1 IAS 1 (Amendment) – Capital Disclosure - effective January 1, 2007

IAS 1 (Amendment) requires the disclosure of information that enables users of the financial statements to evaluate the entity’s objectives, policies and processes for managing capital.

IFRS 7 Financial Instruments Disclosures - effective January 1, 2007

IFRS 7 replaces the disclosures required by IAS 30, Disclosures in the Financial Statements of Banks and Similar Financial Institutions, and parts of the disclosure requirements in IAS 32, Financial Instruments: Disclosure and Presentation. The Group will apply IFRS 7 from annual periods beginning January 1, 2007.

IFRS 8 Operating Segments - effective January 1, 2009

IFRS 8 replaces IAS 14 Segment Reporting. It extends the scope of segment reporting to include entities that hold assets in a fiduciary capacity for a broad group of outsiders as well as entities whose equity or debt securities are publicly traded and entities that are in the process of issuing equity or debt securities in public securities markets.

IFRIC 7 Applying the Restatement Approach under IAS 29, Financial Reporting in Hyperinflationary Economies - effective for annual period beginning on or after March 1, 2006.

IFRIC 8 Scope of IFRS 2 - effective for annual periods beginning on or after May 1, 2006.

IFRIC 9 Reassessment of Embedded Derivatives - effective for annual periods beginning on or after June 1, 2006.

International Fish Farming Company (PJSC) and Subsidiaries 9 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

2. Adoption of new and revised International Financial Reporting Standards (continued)

IFRIC 10 Interim Financial Reporting and Impairment - effective for annual periods beginning on or after November 1, 2006.

IFRIC 11 IFRS-2: Group Treasury Shares Transactions - effective for periods beginning March 1, 2007.

IFRIC 12 Service Concession Arrangements - effective for periods beginning January 1, 2009.

The management anticipates that the adoption of these Standards and Interpretations (where applicable) in future periods will have no material impact on the consolidated financial statements of the Group, except for IFRS 7 which when adopted will impact disclosures substantially.

3. Significant accounting policies

Statement of compliance

The financial statements are prepared in accordance with International Financial Reporting Standards (IFRS). These financial statements are presented in United Arab Emirates Dirhams (AED) since it is the currency of the primary economic environment in which the Group operates. The principal accounting policies are set out below.

Basis of preparations

The financial statements have been prepared on the historical cost basis except for the

revaluation of certain financial instruments and biological assets that are presented at fair value.

Basis of consolidation

The consolidated financial statements incorporate the financial statements of the Company and entities controlled by the Company (its subsidiaries). Control is achieved where the Company has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

The results of subsidiaries acquired or disposed of during the year are included in the consolidated income statement from the effective date of acquisition or up to the effective date of disposal, as appropriate.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies in line with those used by other members of the Group.

International Fish Farming Company (PJSC) and Subsidiaries 10 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Basis of consolidation - continued All intra-group transactions, balances, income and expenses are eliminated on consolidation. Minority interests in the net assets (excluding goodwill) of consolidated subsidiaries are identified separately from the Group’s equity therein. Minority interests consist of the amount of those interests at the date of the original business combination and the minority’s share of changes in equity since the date of the combination. Losses applicable to the minority in excess of the minority’s interest in the subsidiary’s equity are allocated against the interests of the Group except to the extent that the minority has a binding obligation and is able to make an additional investment to cover the losses. Investments in associates An associate is an entity over which the Group has significant influence and that is neither a subsidiary nor an interest in a joint venture. Significant influence is the power to participate in the financial and operating policy decisions of the investee but is not control or joint control over those policies.

The results and assets and liabilities of associates are incorporated in these consolidated financial statements using the equity method of accounting, except when the investment is classified as held for sale, in which case it is accounted for in accordance with IFRS 5 Non-current Assets Held for Sale and Discontinued Operations. Under the equity method, investments in associates are carried in the consolidated balance sheet at cost as adjusted for post-acquisition changes in the Group’s share of the net assets of the associate, less any impairment in the value of individual investments. Losses of an associate in excess of the Group’s interest in that associate (which includes any long-term interests that, in substance, form part of the Group’s net investment in the associate) are not recognised, unless the Group has incurred legal or constructive obligations or made payments on behalf of the associate.

Any excess of the cost of acquisition over the Group’s share of the net fair value of the identifiable assets, liabilities and contingent liabilities of the associate recognised at the date of acquisition, is recognised as goodwill. The goodwill is included within the carrying amount of the investment and is assessed for impairment as part of the investment. Any excess of the Group’s share of the net fair value of the identifiable assets, liabilities and contingent liabilities over the cost of acquisition, after reassessment, is recognised immediately in the profit or loss.

Where a group entity transacts with an associate of the Group, profits and losses are eliminated to the extent of the Group’s interest in the relevant associate.

International Fish Farming Company (PJSC) and Subsidiaries 11 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Goodwill Goodwill arising on the acquisition of a subsidiary or a jointly controlled entity represents the excess of the cost of acquisition over the Group’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities of the subsidiary or jointly controlled entity recognised at the date of acquisition. Goodwill is initially recognised as an asset at cost and is subsequently measured at cost less any impairment losses.

For the purpose of impairment testing, goodwill is allocated to each of the Group’s cash-generating units expected to benefit from the synergies of the combination. Cash-generating units to which goodwill has been allocated are tested for impairment annually, or more frequently when there is an indication that the unit may be impaired. If the recoverable amount of the cash-generating unit is less than the carrying amount of the unit, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to the unit and then to the other assets of the unit pro-rata on the basis of the carrying amount of each asset in the unit. An impairment loss recognised for goodwill is not reversed in a subsequent period.

On disposal of a subsidiary or a jointly controlled entity, the attributable amount of goodwill is included in the determination of the profit or loss on disposal. Revenue recognition

Revenue is measured at the fair value of the consideration received or receivable. Revenue is reduced for estimated customer returns, rebates and other similar allowances.

Sale of goods

Revenue from the sale of goods is recognised when all the following conditions are satisfied:

� The Group has transferred to the buyer the significant risks and rewards of ownership of the goods;

� The Group retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold;

� The amount of revenue can be measured reliably; � It is probable that the economic benefits associated with the transaction will flow to

the Group; and � The costs incurred or to be incurred in respect of the transaction can be measured

reliably.

International Fish Farming Company (PJSC) and Subsidiaries 12 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Revenue recognition - continued

Dividend and interest revenue Dividend from investments is recognised when the shareholder’s right to receive payment has been established.

Interest revenue is accrued on a time basis, by reference to the principal outstanding and at the effective interest rate applicable, which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial asset to that asset’s net carrying amount.

Foreign currency transactions The individual financial statements of each group entity are presented in the currency of the primary economic environment in which the entity operates (its functional currency). For the purpose of the consolidated financial statements, the results and financial position of each entity are expressed in Arab Emirates Dirhams (‘AED’), which is the functional currency of the Group and the presentation currency for the consolidated financial statements.

In preparing the financial statements of the individual entities, transactions in currencies other than the entity’s functional currency (foreign currencies) are recorded at the rates of exchange prevailing at the dates of the transactions. At each balance sheet date, monetary items denominated in foreign currencies are retranslated at the rates prevailing at the balance sheet date. Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated at the rates prevailing at the date when the fair value was determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are not retranslated. Exchange differences are recognised in profit or loss in the period in which they arise.

For the purpose of presenting consolidated financial statements, the assets and liabilities of the Group’s foreign operations are expressed in Arab Emirates Dirhams using exchange rates prevailing at the balance sheet date. Income and expense items are translated at the average exchange rates for the period, unless exchange rates fluctuated significantly during that period, in which case the exchange rates at the dates of the transactions are used. Exchange differences arising, if any, are classified as equity and transferred to the Group’s translation reserve. Such exchange differences are recognised in profit or loss in the period in which the foreign operation is disposed of.

International Fish Farming Company (PJSC) and Subsidiaries 13 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Property, plant and equipment

Property, plant and equipment are stated at cost less accumulated depreciation and any

accumulated impairment loss. Depreciation is charged so as to write off the cost of assets other than capital work-in-

progress, over their estimated useful lives, using the straight-line method, as follows:

Years

Nets 5 Moorings and cages 12 Buildings and leasehold improvement 5 to 15 Plant and equipment 3 to 5 Furniture, fixtures and equipment 3 to 5 Motor vehicles 4 to 5 Marine vessels 10

The gain or loss arising on the disposal or retirement of an item of property and equipment is determined as the difference between the sales proceeds and the carrying amount of the asset and is recognized in profit and loss. Impairment of tangible assets At each balance sheet date, the Group reviews the carrying amounts of its tangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Where it is not possible to estimate the recoverable amount of an individual asset, the Group estimates the recoverable amount of the cash-generating unit to which the asset belongs. Where a reasonable and consistent basis of allocation can be identified, corporate assets are also allocated to individual cash-generating units, or otherwise they are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation basis can be identified. Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

International Fish Farming Company (PJSC) and Subsidiaries 14 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Impairment of tangible assets - continued

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (cash-generating unit) is reduced to its recoverable amount. An impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.

Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (cash-generating unit) in prior years. A reversal of an impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase. Provision for employees’ end of service indemnity Provision for employees’ end of service indemnity is made in accordance with labour laws in the countries where the Group operates. Statutory reserve

In accordance with UAE Federal Companies Law Number 8 of 1984, as amended, the Company has established a statutory reserve by appropriation of 10% of its net profit for each year until the reserve equals 50% of the share capital. This reserve is not available for distribution, except as stipulated by the Law.

Taxation

When applicable, provision is made for current and differed taxes arising from operating results of subsidiaries that are operating in taxable jurisdictions. Inventories Fish products comprise purchased and processed raw fish which are valued at the lower of cost and net realisable value. Cost of fish products is determined under first in-first out (FIFO) cost method and includes all expenditure incurred in bringing inventory to their current location and condition. The processed raw fish costs include also handling costs.

Net realizable value represents the estimated selling price for inventories less estimated costs necessary to make the sale.

International Fish Farming Company (PJSC) and Subsidiaries 15 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Biological assets

The Group valued the matured fish at fair value less estimated point of sales costs with any resultant gain or loss recognised in the consolidated income statement. The immatured fish are valued at the lower of cost or net realizable value.

The fair value of matured fish is arrived at by averaging the sales price less cost of selling from the last fifteen days before the year-end.

Cost of immatured fish comprise cost of the juvenile fish, fish feed and direct overhead.

Net realisable value represents the estimated selling price for inventories less all estimated costs of completion and costs necessary to make the sale.

Leasing

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. All other leases are classified as operating leases.

Operating lease payments are recognised as an expense on a straight-line basis over the lease term, except where another systematic basis is more representative of the time pattern in which economic benefits from the leased asset are consumed. Contingent rentals arising under operating leases are recognised as an expense in the period in which they are incurred.

In the event that lease incentives are received to enter into operating leases, such incentives are recognised as a liability. The aggregate benefit of incentives is recognised as a reduction of rental expense on a straight-line basis, except where another systematic basis is more representative of the time pattern in which economic benefits from the leased asset are consumed.

Provisions

Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of a past event, it is probable that the Group will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation.

The amount recognised as a provision is the best estimate of the consideration required to settle the present obligation at the balance sheet date, taking into account the risks and uncertainties surrounding the obligation. Where a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows.

When some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, the receivable is recognised as an asset if it is virtually certain that reimbursement will be received and the amount of the receivable can be measured reliably.

International Fish Farming Company (PJSC) and Subsidiaries 16 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Financial assets

Investments are recognised and derecognised on a trade date where the purchase or sale of an investment is under a contract whose terms require delivery of the investment within the timeframe established by the market concerned, and are initially measured at fair value, net of transaction costs, except for those financial assets classified as at fair value through profit or loss, which are initially measured at fair value.

Financial assets are classified into the following specified categories: financial assets as ‘at fair value through profit or loss’ (FVTPL), and ‘available-for-sale’ (AFS) financial assets. The classification depends on the nature and purpose of the financial assets and is determined at the time of initial recognition.

Effective interest method

The effective interest method is a method of calculating the amortised cost of a financial asset and of allocating interest income over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash receipts through the expected life of the financial asset, or, where appropriate, a shorter period.

Income is recognised on an effective interest basis for debt instruments other than those financial assets designated as at FVTPL.

Financial assets at FVTPL

Financial assets are classified as at FVTPL where the financial asset is either held for trading or it is designated as at FVTPL.

A financial asset is classified as held for trading if:

� It has been acquired principally for the purpose of selling in the near future; or � It is a part of an identified portfolio of financial instruments that the Group manages

together and has a recent actual pattern of short-term profit-taking; or � It is a derivative that is not designated and effective as a hedging instrument.

A financial asset other than a financial asset held for trading may be designated as at FVTPL upon initial recognition if:

� Such designation eliminates or significantly reduces a measurement or recognition inconsistency that would otherwise arise; or

� The financial asset forms part of a group of financial assets or financial liabilities or both, which is managed and its performance is evaluated on a fair value basis, in accordance with the Group’s documented risk management or investment strategy, and information about the grouping is provided internally on that basis; or

� It forms part of a contract containing one or more embedded derivatives, and IAS 39 permits the entire combined contract (asset or liability) to be designated as at FVTPL.

International Fish Farming Company (PJSC) and Subsidiaries 17 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Financial assets - continued

Financial assets at FVTPL (continued)

Financial assets at FVTPL are stated at fair value, with any resultant gain or loss recognised in the consolidated income statement. The net gain or loss recognised in consolidated income statement incorporates any dividend or interest earned on the financial asset.

AFS financial assets

Listed shares and convertible bonds held by the Group that are traded in an active market are classified as being AFS and are stated at fair value. Gains and losses arising from changes in fair value of AFS are recognised directly in equity in the investments revaluation reserve with the exception of impairment losses, interest calculated using the effective interest rate method and foreign exchange gains and losses on monetary assets, which are recognised directly in profit or loss. Where the investment is disposed of or is determined to be impaired, the cumulative gain or loss previously recognised in the investments revaluation reserve is included in the profit or loss for the year.

Dividends on AFS equity instruments are recognised then in profit or loss when the Group’s right to receive payments is established.

The fair value of AFS monetary assets denominated in a foreign currency is determined in that foreign currency and translated at the spot rate at the balance sheet date. The change in fair value attributable to translation differences that result from a change in amortised cost of the asset is recognised in profit or loss, and other changes are recognised in equity. Fair values

For investments traded in organized financial markets, fair value is determined by reference to quoted market bid prices at the close of business at the balance sheet date.

For investments where there is no quoted market price, a reasonable estimate of the fair value is determined by reference to the current market value of another instrument which is substantially the same, or is based on the expected cash flows, or the underlying net asset base of the investment.

Impairment of financial assets

Financial assets, other than those at FVTPL, are assessed for indicators of impairment at each balance sheet date. Financial assets are impaired where there is objective evidence that, as a result of one or more events that occurred after the initial recognition of the financial asset, the estimated future cash flows of the investment have been impacted. For financial assets carried at amortised cost, the amount of the impairment is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate.

International Fish Farming Company (PJSC) and Subsidiaries 18 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Financial assets - continued Impairment of financial assets (continued)

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets with the exception of trade receivables where the carrying amount is reduced through the use of an allowance account. When a trade receivable is uncollectible, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited against the allowance account. Changes in the carrying amount of the allowance account are recognised in profit or loss.

With the exception of AFS equity instruments, if, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised, the previously recognised impairment loss is reversed through profit or loss to the extent that the carrying amount of the investment, at the date the impairment is reversed, does not exceed what the amortised cost would have been had the impairment not been recognised.

In respect of AFS equity securities, any increase in fair value subsequent to an impairment loss is recognised directly in equity. Financial instruments

Financial assets and financial liabilities are recognized on the Group’s consolidated balance sheet when the Group has become a party to the contractual provisions of the instrument. Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and demand deposits, and other short-term highly liquid investments that are readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value. Trade and other receivables

Trade and other receivables are measured at their fair value as reduced by appropriate allowance for estimated doubtful amounts, if required. Trade and other payables

Trade and other payables are measured at fair value. Due from/to related parties

Amounts due from/to related parties are measured at their fair value.

International Fish Farming Company (PJSC) and Subsidiaries 19 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

3. Significant accounting policies (continued)

Financial instruments - continued Embedded derivatives

Derivatives embedded in other financial instruments or other host contracts are treated as separate derivatives when their risks and characteristics are not closely related to those of the host contracts and the host contracts are not measured at fair value with changes in fair value recognised in profit or loss.

4. Critical accounting judgments and key sources of estimation uncertainty

In the application of the Group’s accounting policies, which are described in Note 3 to the consolidated financial statements, management is required to make judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period, or in the period of the revision and future periods if the revision affects both current and future periods.

Critical judgments in applying Group’s accounting policies

The following are the critical judgments, apart from those involving estimations (see below), that management has made in the process of applying the Group’s accounting policies and that have the most significant effect on the amounts recognised in the consolidated financial statements.

Classification of investments

Management decides on acquisition of an investment whether it should be classified as FVTPL - held for trading or available-for-sale.

Management classifies investments as FVTPL – held for trading if they are acquired primarily for the purpose of making a short term profit. Investments are designated as being available-for-sale if management has the positive intention and ability to hold to maturity.

International Fish Farming Company (PJSC) and Subsidiaries 20 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

4. Critical accounting judgments and key sources of estimation uncertainty

(continued)

Critical judgments in applying Group’s accounting policies - continued

Impairment of financial assets

Management determines whether available for sale equity financial assets are impaired when there has been a significant or prolonged decline in their fair value below cost. This determination of what is significant or prolonged requires judgment. In making this judgment and to record whether an impairment occurred, management evaluates among other factors, the normal volatility in share price, the financial health of the investee, industry and sector performance, changes in technology and operational and financial cash flows. Impairment of assets values

At each balance sheet date, management reviews the assets values to determine that their book values have not exceeded their recoverable amounts. Management estimates the recoverable amount of various assets individually or based on the cash generating unit to which the individual asset belongs. Biological assets In case of inventory of “immatured” fish, Management values the inventory using the cost basis instead of the fair value under the assumption that the fair value cannot be reliably estimated based on the industry practice in general.

In case of inventory of “matured” fish, Management values this inventory based on “fair value” (less cost of selling) which is estimated on latest market prices considering volume, quality, mortality and normal cost of harvest.

The classification of fish between matured and immatured categories is done by Management on the assumption of harvestable weight. For the purposes of classifying fish under “immatured” category, Management uses the threshold of 300 grams weight. The profit or loss which will be recognised on the sale of fish may differ materially from that implied by the fair value adjustment at the end of a period.

Key sources of estimation uncertainty The following are the key assumptions concerning the future, and other key sources of estimation uncertainty at the balance sheet date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year.

International Fish Farming Company (PJSC) and Subsidiaries 21 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

4. Critical accounting judgments and key sources of estimation uncertainty

(continued) Key sources of estimation uncertainty - continued Impairment of goodwill Determining whether goodwill is impaired requires an estimation of the value in use of the cash-generating units to which goodwill has been allocated. The value in use calculation requires the Group to estimate the future cash flows expected to arise from the cash-generating unit and a suitable discount rate in order to calculate present value. Allowance for doubtful debts Allowance for doubtful debts is determined using a combination of factors to ensure that the trade receivables are not overstated due to uncollectability. The allowance for irrecoverable debts is based on a variety of factors, including the overall quality and aging of receivables, continuing credit evaluation of the customers’ financial conditions and collateral requirements from customers in certain circumstances. Also, specific allowances for individual accounts are recorded when the Group becomes aware of the customer’s inability to meet its financial obligations. Property, plant and equipment

The costs of property, plant and equipment is depreciated over their estimated useful lives, which are based on expected usage of the assets, expected physical wear and tear, which depend on operational factors. Management has not considered any residual value as it is deemed immaterial.

5. Cash and cash equivalents December 31, 2006 2005 AED ’000 AED ’000

Cash on hand 141 503 Bank balances: Current Accounts 6,137 6,770 Short-term deposits 74,662 33,684

80,940 40,957 ======== ========

At December 31, 2006, the effective interest rates on short-term deposits varied between 5.00 % and 5.33 % per annum (2005: between 2.5% and 4.9% per annum). These deposits have maturity periods of 90 days or less from the dates of deposits.

International Fish Farming Company (PJSC) and Subsidiaries 22 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

5. Cash and cash equivalents (continued)

The Group had unused credit facilities secured by convertible bonds amounting to AED 15 million as follows:

December 31, 2006 2005 AED ’000 AED ’000

Unused overdraft and documentary credits 23,000 23,000 ======== ========

2006 2005 USD ’000 USD ’000

Unused foreign exchange forward limit 10,000 10,000 ======== ========

6. Other financial assets

Other financial assets represented bank deposits with maturity dates over 90 days from the date of deposits. These deposits carried effective interest rates ranging between 2.5% to 4.9% per annum.

7. Investments in marketable securities

December 31, 2006 2005 AED ’000 AED ’000

Investments at fair value through profit and loss: Investments in marketable securities 1,992 3,420 Capital guaranteed investment deposits - 14,572

Investments available for sale: Convertible bonds 15,000 - Investments in property portfolio - 4,108

16,992 22,100 ========= =========

Convertible bonds carry interest rate of EIBOR plus 0.25% per annum. The Group has an option of converting these bonds at a predetermined conversion rate between 2 to 5 years from the date of issuance. These bonds are under lien to a bank against credit facilities provided to the Group.

At December 31, 2006, investments in marketable securities amounting to AED 714,600 (2005: AED 1,816,600) are in the names of related parties held on trust and for the benefit of the Group.

International Fish Farming Company (PJSC) and Subsidiaries 23 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

8. Trade and other receivables

December 31, 2006 2005 AED ’000 AED ’000

Trade receivables 23,433 24,702

Less: Allowance for doubtful debts ( 8,131) ( 4,852) 15,302 19,850 Prepayments 839 1,176 Accrued interest receivable 981 419 Other receivables 3,318 4,047

20,440 25,492 ========= =========

9. Inventories December 31, 2006 2005 AED ’000 AED ’000

Fish and fish products 6,036 11,934 Fish feed 647 815

6,683 12,749 ========= ========

10. Biological assets Biological assets represent fish held in cages at several fish farms in United Arab

Emirates and Sultanate of Oman. The biological assets held at the end of the year are as follows:

December 31, 2006 2005 AED’000 AED’000

Biological assets - matured fish, at cost 11,152 10,638 Fair value adjustment 865 1,412

Biological assets - matured fish, at fair value 12,017 12,050 Biological assets - immatured fish, at cost 5,748 5,774

Biological assets held with third party, at cost 1,454 -

19,219 17,824 ======== ========

International Fish Farming Company (PJSC) and Subsidiaries 24 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

10. Biological assets (continued)

Fair value adjustment is the difference between the fair value and accumulated cost of matured fish.

The Group invested AED 1.4 million with Maremar-Su Urunleri Eud, Istanbul, Turkey, to grow Sea Bass for the benefit of the Group. At December 31, 2006, Maremar held 120 metric tons of Sea Bass for the benefit of the Group.

The movements in the carrying value of biological assets are as follows:

2006 2005 AED’000 AED’000

At January 1, 17,824 11,234 Purchases 4,619 12,235 Cost incurred that increases weight of biological assets 16,492 7,372 Decrease due to harvest ( 18,624) ( 15,973) Decrease due to mortality ( 712) ( 2,325) Change in fair value less estimated point-of-sale costs ( 380) 5,281

At December 31, 19,219 17,824 ======= ========

11. Related party transactions

The Group enters into transactions with companies and entities that fall within the definition

of a related party as contained in International Accounting Standard No. 24. Related parties comprise companies under common ownership and/or common management and control and key management personnel. The management decides on the terms and conditions of the transactions with related parties as well as on other services and charges.

International Fish Farming Company (PJSC) and Subsidiaries 25 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

11. Related party transactions (continued)

At the balance sheet date, due from/to related parties are as follows: Year ended December 31, 2006 2005 AED’000 AED’000

Due from related parties

Associates

Worldwide Sea Foods LLC, USA 1,345 5,455 CPI Trading, USA 3,885 727

5,230 6,182 Less: Allowance for doubtful debts ( 2,731) -

2,499 6,182 ======== ======= Due to a related party

Associate

Al Awal Fishing Co., Kingdom of Bahrain 612 - ======== ======= The Group entered into the following significant transactions and amounts with related parties during the year:

Year ended December 31, 2006 2005 AED’000 AED’000

Purchase of fish 2,881 243 Sales of fish farming 7,913 196 Compensation of key management personnel

The remuneration of members of key management personnel are as follows: Year ended December 31, 2006 2005 AED’000 AED’000

Short term benefits 1,859 1,394 Post-employment benefits 143 71

2,002 1,465 ======== ========

International Fish Farming Company (PJSC) and Subsidiaries 26 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

12. Property, plant and equipment Buildings Plant Furniture, Capital and leasehold and fixtures and Motor Marine work in Nets Moorings Cages improvement equipment equipment vehicles vessels progress Total AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 Cost Balance at December 31, 2004 6,859 7,440 5,903 7,635 12,480 1,541 5,936 3,779 5,203 56,776 Additions 379 1 315 926 1,293 64 880 - 816 4,674 Disposals ( 26) - ( 18) ( 531) ( 133) ( 130) ( 331) ( 10) - ( 1,179) Transfers - - - ( 535) 1,972 ( 351) - 124 ( 1,210) - Balance at December 31, 2005 7,212 7,441 6,200 7,495 15,612 1,124 6,485 3,893 4,809 60,271 Additions 956 20 12 258 797 25 381 - 8,601 11,050 Disposals - - - - - ( 29) ( 35) - - ( 64) Write off - ( 145) - - - - - - ( 89) ( 234) Transfers - - - - 237 - - - ( 237) - Balance at December 31, 2006 8,168 7,316 6,212 7,753 16,646 1,120 6,831 3,893 13,084 71,023 Depreciation Balance at December 31, 2004 4,027 2,081 1,698 3,841 7,290 1,100 3,129 1,385 2,302 26,853 Charge for the year 955 623 550 756 2,303 192 1,043 295 - 6,717 Disposals - - - ( 242) ( 40) ( 144) ( 150) ( 6) - ( 582) Transfers ( 28) 42 19 2 57 ( 127) - 35 - -

Impairment provision 716 563 465 - - - - 239 370 2,353 Impairment during year - 394 - - - - - - - 394 Balance at December 31, 2005 5,670 3,703 2,732 4,357 9,610 1,021 4,022 1,948 2,672 35,735 Charge for the year 765 588 567 560 2,321 145 990 357 - 6,293 Disposals - - - - - ( 6) ( 21) - - ( 27) Write off - ( 69) - - - ( 55) - - - ( 124) Impairment provision ( 101) ( 55) ( 28) - - - - 114 1,481 1,411 Balance at December 31, 2006 6,334 4,167 3,271 4,917 11,931 1,105 4,991 2,419 4,153 43,288 Net book value At December 31, 2006 1,834 3,149 2,941 2,836 4,715 15 1,840 1,474 8,931 27,735 ===== ====== ====== ====== ====== ===== ====== ====== ====== ====== At December 31, 2005 1,542 3,738 3,468 3,138 6,002 103 2,463 1,945 2,137 24,536 ===== ====== ====== ====== ====== ===== ====== ====== ====== ======

International Fish Farming Company (PJSC) and Subsidiaries 27 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

13. Investments in associates

2006 2005 AED’000 AED’000

Balance, at the beginning of the year 21 - Acquired during the year 5,391 165 Share in the loss of associates for the year ( 76) ( 144)

Balance, at end of the year 5,336 21 ======== ========

Details of the Group’s associates are as follows: Proportion of ownership interest and Place of incorporation voting power Name of the associate and operation held Worldwide Sea Foods L.L.C. USA 45% CPI USA 30% Awal Fishing L.L.C. Kingdom of Bahrain 50%

14. Trade and other payables

December 31, 2006 2005 AED’000 AED’000

Trade payables 2,073 3,168 Accruals and other payables 4,062 3,530

6,135 6,698 ======== ========

15. Share capital December 31, 2006 2005 AED’000 AED’000

Authorized, issued and fully paid: 30 million ordinary shares of AED 10, each 300,000 300,000

========= ========

International Fish Farming Company (PJSC) and Subsidiaries 28 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

16. (Loss)/earnings per share Year ended December 31, 2006 2005

Net (loss)/profit for the year (Thousands of AED) ( 17,697) 889 ========= ========= Number of ordinary shares outstanding during the year 30,000,000 30,000,000 ========= ========= (Loss)/earnings per share - (AED) (0.59) 0.03 ========= =========

17. Provision for employees’ end of service indemnity

2006 2005 AED’000 AED’000

Balance, at beginning of the year 1,690 1,764 Amount charged to income during the year 832 504 Amounts paid during the year ( 719) ( 578)

Balance, at end of the year 1,803 1,690 ======== ========

18. General and administrative expenses General and administrative expenses included the following: Year ended December 31,

2006 2005 AED’000 AED’000

Employees’ salaries and wages and related expenses 7,303 7,334 Depreciation of property, plant and equipment 1,478 1,517 Allowance for doubtful debts 7,313 924 ======== ========

International Fish Farming Company (PJSC) and Subsidiaries 29 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

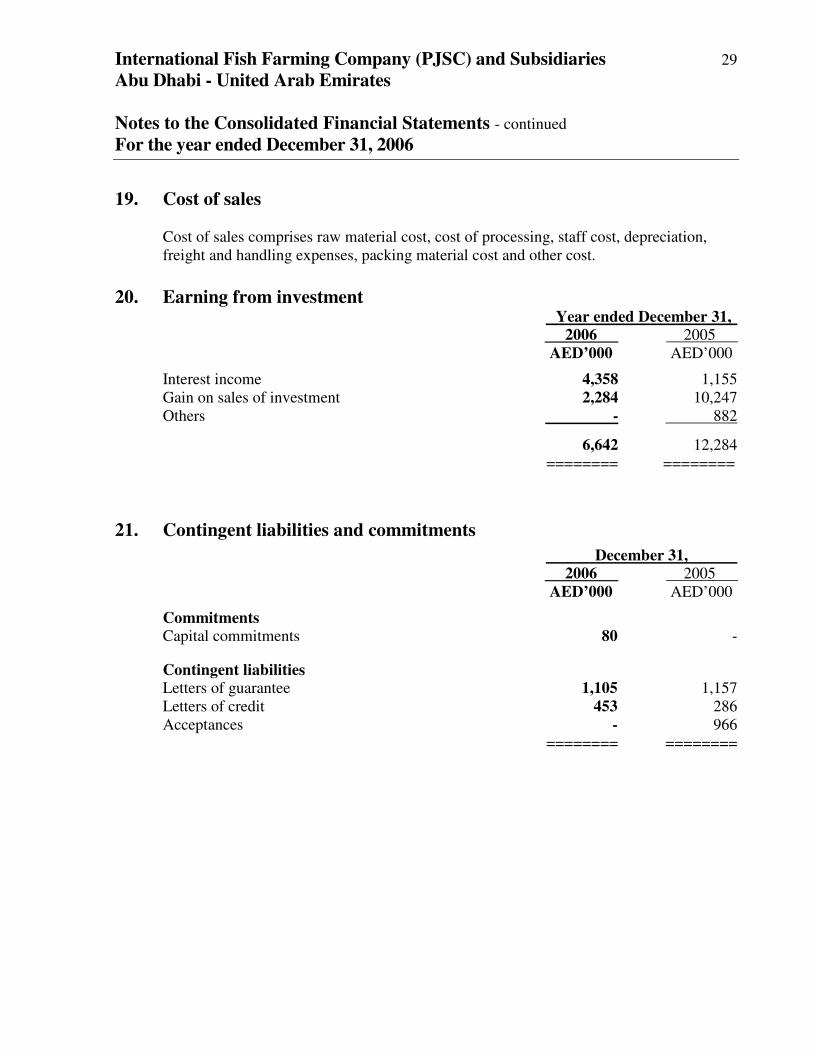

19. Cost of sales Cost of sales comprises raw material cost, cost of processing, staff cost, depreciation, freight and handling expenses, packing material cost and other cost.

20. Earning from investment Year ended December 31,

2006 2005 AED’000 AED’000

Interest income 4,358 1,155 Gain on sales of investment 2,284 10,247 Others - 882

6,642 12,284 ======== ========

21. Contingent liabilities and commitments December 31,

2006 2005 AED’000 AED’000

Commitments Capital commitments 80 - Contingent liabilities Letters of guarantee 1,105 1,157 Letters of credit 453 286 Acceptances - 966 ======== ========

International Fish Farming Company (PJSC) and Subsidiaries 30 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

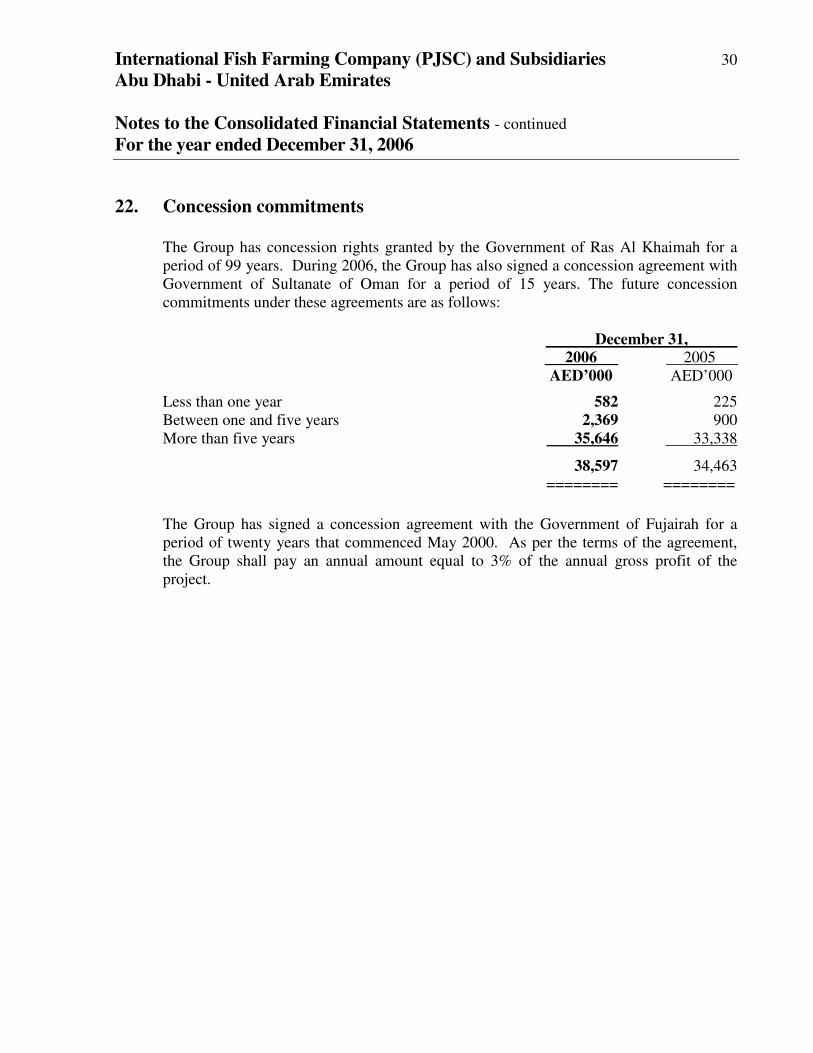

22. Concession commitments The Group has concession rights granted by the Government of Ras Al Khaimah for a

period of 99 years. During 2006, the Group has also signed a concession agreement with Government of Sultanate of Oman for a period of 15 years. The future concession commitments under these agreements are as follows:

December 31,

2006 2005 AED’000 AED’000

Less than one year 582 225 Between one and five years 2,369 900 More than five years 35,646 33,338

38,597 34,463 ======== ========

The Group has signed a concession agreement with the Government of Fujairah for a period of twenty years that commenced May 2000. As per the terms of the agreement, the Group shall pay an annual amount equal to 3% of the annual gross profit of the project.

International Fish Farming Company (PJSC) and Subsidiaries 31 Abu Dhabi – United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

23. Segment analysis Trading Fish farming Processing Total

2006 2005 2006 2005 2006 2005 2006 2005 AED ’000 AED’000 AED ’000 AED ’000 AED ’000 AED ’000 AED ’000 AED ’000 Revenue 82,780 77,828 39,458 37,416 129 331 122,367 115,575 Inter-segment revenue ( 1,160) ( 2,347) ( 17,580) ( 15,947) ( 129) ( 331) ( 18,869) ( 18,625)

Revenue to third parties 81,620 75,481 21,878 21,469 - - 103,498 96,950 ======= ========= ====== ========= ====== ======= ======= =========

Segment result ( 10,467) ( 12,303) ( 11,127) ( 5,503) ( 839) ( 710) ( 22,433) ( 18,516) (Loss)/gain arising from changes in fair value of biological assets less estimated point of biological assets ( 380) 5,281 Earnings from investment 6,642 12,284 Share of loss from associates ( 76) ( 144) (Loss)/gain on revaluation of marketable securities ( 1,832) 2,734 Impairment of goodwill ( 601) - Impairment of property, plant and equipment ( 1,411) ( 394) Loss on sale of property, plant and equipment ( 14) ( 349)

Net loss for the year ( 20,105) 896 7) ======= ======== Attributable to: Equity holders of the parent ( 17,697) 889 Minority interest ( 2,408) 7

( 20,105) 896 ====== =======

Other information: Segment Assets 139,890 158,651 39,206 38,967 1,186 2,169 180,282 199,787 Segment liabilities 4,420 6,170 3,981 2,059 29 159 8,430 8,388

======= ========= ====== ========= ====== ======= ====== =========

International Fish Farming Company (PJSC) and Subsidiaries 32 Abu Dhabi – United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

24. Geographical segments UAE GCC Europe USA Other region Total

2006 2005 2006 2005 2006 2005 2006 2005 2006 2005 2006 2005 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000

Revenue to third party 44,738 29,602 8,904 15,684 18,762 21,170 7,659 19,710 23,435 10,784 103,498 96,950

UAE Sultanate of Oman Total

2006 2005 2006 2005 2006 2005 AED’000 AED’000 AED’000 AED’000 AED’000 AED’000

Segments assets 157,957 183,070 21,887 16,717 179,844 199,787 Segments liabilities 7,461 7,083 1,089 1,305 8,550 8,388 Capital expenditure 2,324 3,908 8,726 766 11,052 4,674 Depreciation expenses 4,308 4,433 1,985 2,284 6,293 6,717

International Fish Farming Company (PJSC) and Subsidiaries 33 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

25. Financial instruments

Interest rate risk At December 31, 2006, the Group’s exposure to interest risk relates to its bank deposits which carried an interest rate that range between 5.05% and 5.33% (2005: between 2.5% and 4.9% per annum).

Credit risk

The Group’s principal financial assets are bank balances and cash, and trade and other receivables. Cash at banks are maintained with high credit-ratings assigned by international credit-rating agencies. The Group’s credit risk is primarily attributable to its trade receivables. The amounts presented in the balance sheet are net of allowances for doubtful receivables. An allowance for impairment is made where there is an identified loss event which, based on previous experience, is evidence of a reduction in the recoverability of the cash flows.

The Group’s maximum exposure to credit risk from trade situated outside the UAE were as follows:

December 31,

2006 2005 AED’000 AED’000

UAE 7,659 4,708 GCC other than UAE 3,929 2,419 Europe 2,147 3,540 USA 41 8,042 Others 1,526 1,141

15,302 19,850 ======== ========

There is no significant concentration of credit risk outside the industry in which the Group operates.

International Fish Farming Company (PJSC) and Subsidiaries 34 Abu Dhabi - United Arab Emirates Notes to the Consolidated Financial Statements - continued For the year ended December 31, 2006

25. Financial instruments (continued)

Exchange rate risk

There are no significant exchange rate risks as substantially all financial assets and financial liabilities are denominated in Arab Emirates Dirhams or US Dollars or Omani Riyal to which the Dirham is fixed. Fair values

The fair values of financial assets and liabilities at year end approximate their carrying amounts in the balance sheet.

26. Comparative amounts

Certain amounts for the prior year were reclassified to conform to current year presentation.