international methods of payment avv. alessandro russo trade finance and international trade law...

TRANSCRIPT

International Methods of Payment

Avv. Alessandro RussoTrade Finance and International trade law expert

International Business Law Firm

Risk Issues in International Trade

In any business transaction, there are risks. However, these risks are emphasized when dealing internationally. Added to the commercial risks present in a domestic transaction are foreign exchange as well as country risks.

COUNTRY RISKS

Stable political climate? War? Revolution?

Positive economic environment?

Solid legal infrastructure?

Foreign exchange restrictions?

FOREIGN EXCHANGE RISKS

Volatile foreign currency?

COMMERCIAL RISKS

Reliable information concerning the company’s track record? Insolvency of your trading partner?

Default or termination on your contract?

Making and Receiving Payment Internationally :International Payment Instruments

• Clean Payments

• Documentary Collections

• Letters of Credit

We now introduce you to the different payment methods available in settling an international trade transaction. The mechanics of these methods and their advantages and disadvantages from the point of view of both the Importer and the Exporter will be discussed.

Foreign Market Risk

Two Primary Risk Classifications

Country

Commercial

Country Risk Factors

Economic Stability Political Stability Legal System Language Foreign Exchange

Country Risk

Examples

Unstable government War or Rebellion Embargoes Import License Issues Expropriation Import / Tariff RestrictionsExchange Controls or Currency

Restrictions

Commercial Risk Factors Ownership / Management Financial Performance Market Sector Market Share Past Payment History Documentary Risk Customs, Business Practices Language Barriers

Commercial Risk

Examples

Bankruptcy Liquidity Dispute Fraud History of Slow Payments

Methods of Payment

Risk Assessment

• Open Account

• Documentary Collections– Time Drafts (D/A)– Sight Drafts (D/P)

• Letters of Credit

• Cash in Advance

Exporter’s Risk Importer’s Risk

High

High

LOW

LOW

Evaluating the Risks

Resources

International Banker International Credit Dept Overseas Banking Dept

Trade Associations Credit Reports (D&B, Veritas, etc.) Other Exporters Newspapers & Publications Internet

International Money Transfers

Wire Transfer

What is it? Moves funds quickly, securely

around the world. Can be USD or foreign currency. Initiate by phone, teller, PC, or automatic standing instructions.

When would you use it? Large dollar amounts or urgent

payments.

Wire Transfer Cycle

1. Buyer provides bank with payment instructions & authorization to debit

2. Buyer’s bank makes payment to seller’s bank, OR

2(a) Buyer’s bank makes payment to correspondent bank, who makes payment to seller’s bank

3. Seller’s bank credits seller’s account

Corresp. Bank

Seller Buyer

Seller’sBank

Buyer’s Bank

2(a)

13

2

Foreign Check

What is it? Corporate check drawn on a local

bank, but sent overseas.

When would you send one? For a relatively small amount To avoid wire fees To get a longer float time

When would you accept one?

Hmmm...

You receive a corporate check from a buyer in Japan.

Would you notice the difference from a U.S. check?

What do you look for?

Can you simply deposit or cash it?

When will you get use of funds?

Foreign Checks

BFC Banque Francaise CommercialeAntilles- GuyaneGroupe Credit Agricole Indosuez

A rediger exclusivementPayez contre ce cheque 8459,80 USD en U.S. Dollars

A Bleu Export USD ******8459,80

le 01-12-2003Payable en 18029 10060 70497 00 40 91

Bank of New York S.A. SomardisNew York, New York BP 3174 Howell Center Elise Beauchamps10286 97068 St Martin Cedex signature

4849016 971018 0729800 040638291837

ABC Company

PO Box 365

Shinooka, IL

60011

IRQ Holden, Inc.

IRQ Holden, Inc.

Teagard

For Teagard

Collection of a USD Check Drawn on a Foreign Bank

1. Buyer sends check to seller.2. Seller sends check to seller’s bank.3. Seller’s bank sends advice of receipt to seller.4. Seller’s bank sends check to buyer’s bank.5. Check is processed / buyer’s account debited.6. Buyer’s bank makes payment to seller’s bank.7. Seller’s bank credit’s seller’s account.

Seller Buyer

Seller’sBank

Buyer’sBank

52

4

7

1

3

6

If You Suspect Fraud...

Do not return the check to the sender! The address on the check is often just a mail pick-up, so the item would not be recovered.

Contact your legal counsel for assistance if you suspect a fraudulent item

Refer this item to the Federal Reserve Bank

Your bank will not be able to process this item

Fraud

Your banker will examine every check to see how it is drawn.

Special attention is given to items originating in Nigeria (usually drawn on the U.K.) or the West Indies.

Foreign Currency DraftsWhat is it?The foreign draft is, in effect, a check drawn on a foreign bank, by a US Bank, to the order of a specific party.

When would you use one?For bills that are recurring and need to be paid in local currency.

monthly rent payments on an office space in Japan support O/A purchases where local currency required

To reduce fees (less costly than wire); but there’s no float. Fee paid at issuance.

Unlike a wire, you can attach an invoice, BL, etc. to assure proper credit

Foreign Currency Drafts

When would you accept one?Faster receipt of funds than personal, corporate or cashier’s check, but not as fast as a wire

Payable in payee’s country and in local currency. No FX risk.

Clean Payments

• Introduction: What is a Clean Payment?

• Basic Facts: Open Account & Payment in Advance

• Mechanics: How does a Clean Payment transaction work?

• Risk Analysis: Advantages and Disadvantages

Clean Payments

Introduction: What is a Clean Payment?

•Clean Payments are characterized by trust. Either the Exporter sends the goods and trusts the Importer to pay once the goods have been received, or the Importer trusts the Exporter to send the goods after payment is effected.

•In the case of Clean Payment transactions, all shipping documents, including title documents, are handled directly by the trading parties. The role of banks is limited to clearing funds as required.

Clean Payments

Basic Facts: Open Account & Payment in Advance

•There are two types of Clean Payments: Open Account & Payment in Advance.

•Open Account. The Importer is trusted to pay the Exporter after receipt of the goods.

•Payment in Advance. An arrangement whereby the Exporter is trusted to ship the goods after receiving payment from the Importer.

Clean PaymentsMechanics: How does an Open Account transaction work?

OPEN ACCOUNT: The Exporter ships the goods and the documents directly to the Importer and waits for the Importer to send payment.

Exporter

Importer

2GOODS

1PAYMENT

Clean Payments

Mechanics: How does a Payment in Advance transaction work?

PAYMENT IN ADVANCE: The Importer sends payment directly to the Exporter and waits for the Exporter to send the goods and documents.

Note: The Payment in Advance and Open Account schematics vary only in the order in which events take place.

Exporter

Importer

2GOODS

1

PAYMENT

Risk Analysis: Clean Payments

Advantages to Exporter:

•Assumes no risks

Disadvantages to Exporter:

•None

Advantages to Importer:

•None - but could secure low cost!

Disadvantages to Importer:

•Assumes all risks

•Opportunity cost of using company’s cash resources until goods are received.

Open Account Payment in Advance

Advantages to Exporter:

•None - but could clinch the sale!

Disadvantages to Exporter:

•Assumes all risks

Advantages to Importer:

•Assumes no risks

•Delays use of company’s cash resources.

Disadvantages to Importer:

•None

INTERNATIONAL PAYMENTS RISK SPECTRUMAs we move through the different ways to effect payment in international trade, we will build the Risk Spectrum. The Risk Spectrum is intended to summarize the risks associated with the payment methods in relation to the Exporter and the Importer. Notice that Open Account and Payment in Advance sit at opposite ends of the Risk Spectrum.

LEAST RISK TO

IMPORTER

HIGHEST RISK TO

IMPORTER

HIGHEST RISK TO

EXPORTER

LEAST RISK TO

EXPORTER

•Open Account

•Payment in Advance

Documentary Collections

Introduction: What is a Documentary Collection?

Basic Facts: Documents Against Payment (D/P) & Documents Against Acceptance (D/A)

Mechanics: How does a Documentary Collection work?

Risk Analysis: Advantages and Disadvantages of Documentary Collections

Documentary Collections

Introduction: What is a Documentary Collection?

•A method of payment used in international trade whereby the Exporter entrusts the handling of commercial and often financial documents to banks and gives the banks instructions concerning the release of these documents to the Importer.

•Banks involved do not provide any guarantee of payment.

•Collections are subject to the the Uniform Rules for Collections published by the International Chamber of Commerce. The last revision of these rules came into effect on January 1, 1996 and is referred to as the URC 522. TD provides copies on request at the nearest International Trade Services office.

Except in the case of availized drafts. Please inquire at the nearest TD International Trade Centre for

details.

Documentary Collections

Basic Facts: Documents Against Payment (D/P) & Documents Against Acceptance (D/A)

Documentary Collections may be carried out in two different ways:

•Documents Against Payment. Documents are released to the Importer only against payment. Also known as a Sight Collection or Cash Against Documents (CAD).

•Documents Against Acceptance. Documents are released to the Importer only against acceptance of a draft. Also known as a Term Collection.

Documentary CollectionsMechanics: How does a Documentary Collection work?

The mechanics of a Documentary Collection are easily understood when separated into the following three steps:

» Flow of Goods

» Flow of Documents

» Flow of Payment

Documentary Collections: Flow of Goods

After the Importer and the Exporter have established a sales contract and agree on a Documentary Collection as the method of payment, the Exporter ships the goods. In a Documentary Collection, the Importer is known as the “drawee” and the Exporter as the “drawer”.

GOODS

Exporter/Drawer

Importer/Drawee

Documentary Collections: Flow of Documents

After the goods are shipped, documents originating with the Exporter (e.g. commercial invoice) and the transport company (e.g. bill of lading) are delivered to a bank, called the Remitting Bank in the Collection process. The role of the Remitting Bank is to send these documents accompanied by a Collection Instruction giving complete and precise instructions to a bank in the Importer’s country, referred to as the Collecting/ Presenting Bank in the Collection process.

The Collecting/ Presenting Bank acts in accordance with the instructions given in the Collection Instruction and releases the documents to the Importer against payment or acceptance, according to the Remitting Bank’s Collection instructions.

Note: The Exporter’s Bank and the Remitting Bank need not be the same. Also, the Collecting Bank and Presenting Bank need not be the same. Each role could be performed by a different bank.

Collecting/ Presenting Bank

Importer/Drawee

Remitting Bank

2

3

4

Exporter/Drawer

GOODS

1

Documents

Doc

umen

ts

Documents

Documentary Collections: Flow of Payment

Payment is forwarded to the Remitting Bank for the Exporter’s account. And the Importer can now present the transport document* to the carrier in exchange for the goods.

Remitting Bank

Presenting/ Collecting Bank

1

2

Exporter/Drawer

Importer/Drawee

Documents

4

3

*In this case, we are assuming that the transport document is a title document.

GOODS

Risk Analysis: Documentary CollectionsAs discussed earlier, Documentary Collections may be settled in two different ways. Documents Against Payment (D/P) refers to a Collection where the Importer receives the documents only in exchange for payment. With Documents Against Acceptance (D/A), the Importer may obtain the documents in exchange for the acceptance of the obligation to pay at a specified future date. These two methods of settlement carry different risks for both Importers and Exporters.

Documents Against Payment (D/P)

Documents Against Acceptance (D/A)

Advantages to the Exporter:

•Documents are not released to the Importer until payment has been effected.

•Less costly than a Letter of Credit.

Disadvantages to the Exporter:

•Risk of refusal of payment.

•Commercial and country risks not hedged.

Advantages to the Importer:

•Ability to examine documents before authorizing payment.

•Unlike a Letter of Credit, a line of credit is not required, and fees are minimal.

Disadvantages to the Importer:

•In the case that transport documents carry title, cannot access goods until payment has been made.

Advantages to the Exporter:

•Less costly than a Letter of Credit.

•May provide formal/legal means to collect unpaid obligation.

Disadvantages to the Exporter:

•Risk of non-acceptance of documents.

•Commercial and country risks not hedged.

•Although bill of exchange/draft is accepted by the Importer, there is no guarantee of payment by the banks involved.

•Legal enforcement of unpaid obligation costly and time-consuming.

Advantages to the Importer:

•Will receive goods before having to make payment.

Disadvantages to the Importer:

•Dishonouring an accepted draft is a legal liability and may ruin business reputation.

INTERNATIONAL PAYMENTS RISK SPECTRUM

Documentary Collections offer more of a compromise in risk-taking between the Importer and the Exporter than Clean Payments as illustrated in the diagram below.

LEAST RISK TO

IMPORTER

HIGHEST RISK TO

IMPORTER

HIGHEST RISK TO

EXPORTER

LEAST RISK TO

EXPORTER

•Open Account

•Documentary Collections

Documents Against Acceptance

Documents Against Payment

•Payment in Advance

Letters of Credit

• Introduction: What is a Letter of Credit?• Basic Facts:

Revocable & Irrevocable Letter of Credit Sight & Term Letter of CreditConfirmed Letter of Credit

• Mechanics: How does a Letter of Credit transaction work?• Risk Analysis: Advantages & Disadvantages

Letters of Credit

•A Letter of Credit is a written undertaking by the Importer’s bank, known as the Issuing Bank, on behalf of its customer, the Importer (Applicant), promising to effect payment in favour of the Exporter (Beneficiary) up to a stated sum of money, within a prescribed time limit and against stipulated documents.

•A key principle underlying Letters of Credit is that banks deal only in documents and not in goods. The decision to pay under a Letter of Credit will be based entirely on whether the documents presented to the bank appear on their face to be in accordance with the terms and conditions of the Letter of Credit. It would be prohibitive for the banks to physically check whether all merchandise has been shipped exactly as per each letter of Credit.

•The International Chamber of Commerce (ICC) publishes internationally agreed-upon rules, definitions and practices governing Letters of Credit, called “Uniform Customs and Practice for Documentary Credits” (UCP). The last revision of these rules was effective Jan. 1, 1994 and is referred to as the UCP 500. Copies of the UCP 500 are available from a TD branch or our nearest TD International Trade Services office.

Introduction:What is a Letter of Credit?

Letters of Credit

• Letters of Credit are either Revocable or Irrevocable:– A Revocable Letter of Credit

can be revoked without the consent of the Exporter, meaning that it may be canceled or changed up to the time the documents are presented. Revocable Letters of Credit are very rarely used.

– An Irrevocable Letter of Credit cannot be canceled or amended without the consent of all parties including the Exporter. Unless otherwise stipulated, all Letters of Credit are irrevocable.

• Letters of Credit may be settled either by sight or by acceptance:

– If payment is to be made at the time that documents are presented, this is referred to as a sight Letter of Credit.

– If payment is to be made at a future fixed time from the presentation of documents, this is referred to as a term Letter of Credit

Basic Facts: Revocable/Irrevocable & Sight/Term

Letters of CreditBasic Facts: Confirmed Letter of Credit

•Under a Confirmed Letter of Credit, a bank, called the Confirming Bank, adds its commitment to that of the Issuing Bank to pay the Exporter under the Letter of Credit provided all terms and conditions of the Letter of Credit are met. The Confirming Bank is usually located in the same country as the Exporter.

•An Exporter would request a Confirmed Letter of Credit if it does not consider the financial strength of the Issuing Bank or the country in which it is located to be acceptable risks.

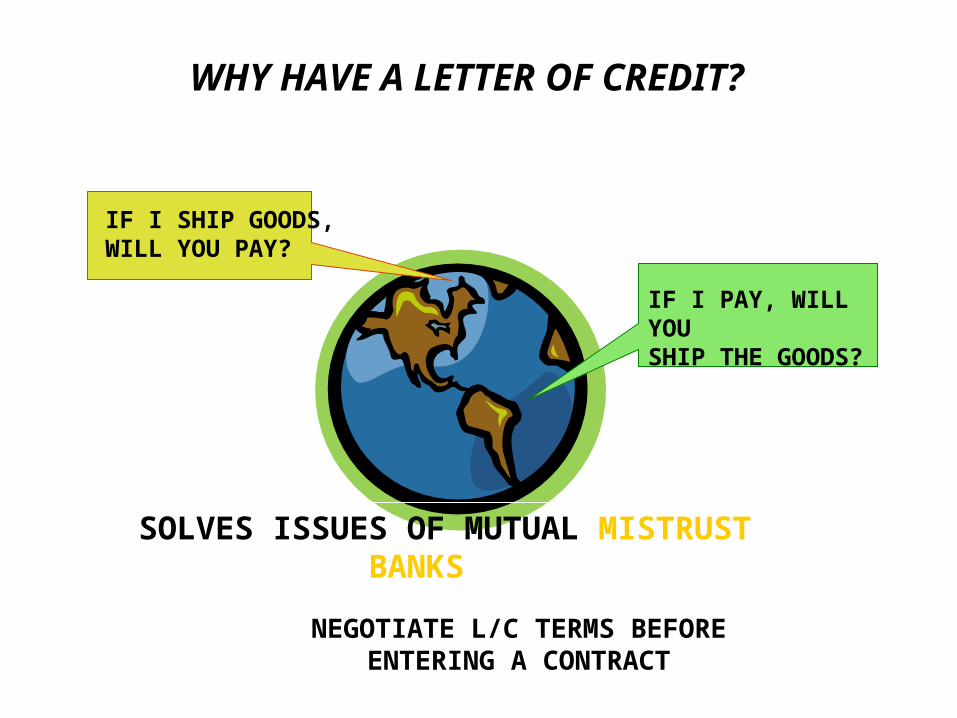

WHY HAVE A LETTER OF CREDIT?

IF I SHIP GOODS,WILL YOU PAY?

IF I PAY, WILL YOUSHIP THE GOODS?

SOLVES ISSUES OF MUTUAL MISTRUST BY USINGBANKS AS ARBITERS

NEGOTIATE L/C TERMS BEFOREENTERING A CONTRACT

LETTERS OF CREDITWHO ARE THE PLAYERS?

REGIONSCUSTOMERIMPORTER

(Buyer)

FGN BANK

CUSTOMEREXPORTER

(Seller)

REGIONS BANK(ISSUING

BANK) L/C

FOREIGN BANK(ADVISING

BANK)

CONTRACT

(MAY CONFIRM)

Letters of CreditMechanics: How does a Letter of Credit work?

The mechanics of a Letter of Credit are easily understood when separated into the following three steps:

» Issuance

» Flow of Goods

» Flow of Documents & Payment

Letters of Credit: Issuance

After the trading parties agree on a sale of goods where payment is made by Letter of Credit, the Importer requests that its bank (the Issuing Bank) issue a Letter of Credit in favour of the Exporter (Beneficiary).

The Issuing Bank then sends the Letter of Credit to the Advising Bank. A request may be included for the Advising Bank to add its confirmation. The Advising Bank is usually located in the country where the Exporter does business and may be the Exporter’s bank, but does not have to be.

Next, the Advising/Confirming Bank verifies the Letter of Credit for authenticity and sends it to the Exporter.

1

Importer applies for Letter of Credit.

3

Request to advise & possibly confirm the Letter of Credit

Advice /Confirmation of the Letter of Credit.

Advising/ Confirming Bank

Issuing Bank2

4

Exporter/ Beneficiary

Importer/Applicant

ContractNegotiations

Note: For the purpose of the Crash Course, the Advising Bank is also acting as the Confirming Bank. However, the roles of advising and confirmingthe Letter of Credit may be performed by two separate banks.

Letters of Credit: Flow of Goods

Upon receipt of the Letter of Credit, the Exporter reviews the Letter of Credit to ensure that it corresponds to the terms and conditions in the purchase and sales agreement; that the documents stipulated in the Letter of Credit can be produced; and that the terms and conditions of the Letter of Credit can be fulfilled. Assuming the Exporter is in agreement with the above, it arranges for shipment of the goods.

GOODS

Exporter/Beneficiary

Importer/Applicant

Letters of Credit: Flow of Documents & Payment

After the goods are shipped, the Exporter presents the documents specified in the Letter of Credit to the Advising/ Confirming Bank.

Once the documents are checked and found to comply with the Letter of Credit (i.e. without discrepancies), the Advising/ Confirming Bank forwards these documents to the Issuing Bank. The drawing is negotiated, paid or accepted as the case may be.

Con’d...Issuing Bank

2

4

Exporter/ Beneficiary

Importer/Applicant

Documents

5

Doc

umen

ts

3

Advising/ Confirming Bank

1

GOODS

Letters of Credit: Flow of Documents & Payment

In turn, the Issuing Bank examines the documents to ensure they comply with the Letter of Credit. If the documents are in order, the Issuing Bank will obtain payment from the Importer for payment already made to the Confirming Bank.

Documents are delivered to the Importer to allow it to take possession of the goods.

Issuing Bank

2

4

Exporter/ Beneficiary

Importer/Applicant

Documents

6

5

Doc

umen

ts

Documents

3

7

Advising/ Confirming Bank

1

GOODS

Risk Analysis: Letters of Credit

Importer Exporter

Advantages:

•An undertaking from the Issuing Bank that you will receive payment under the Letter of Credit provided that you meet all terms and conditions of the Letter of Credit.

•Shifts credit risk from the Importer to the Issuing bank.

•Not obligated to ship against a Letter of Credit that is not issued as agreed.

Disadvantages:

•Documents must be prepared in strict compliance with the requirements stipulated in the Letter of Credit. Non-compliance leaves Exporter exposed to risk of non-payment.

Advantages:

•Importer is assured that, for the Exporter to be paid, all terms and conditions of the Letter of Credit must be met.

•Ability to negotiate more favourable trade terms with the Exporter when payment by Letter of Credit is offered.

Disadvantages:

•A Letter of Credit assures correct documents but not necessarily correct goods.

•Ties up line of credit.

THE DOCUMENTS REQUIRED BYTHE LETTER OF CREDIT

ALL DOCUMENTS MUST CONFORM TO THE LETTEROF CREDIT AND BE CONSISTENT WITH EACH OTHER

THREE FORMS OF DOCUMENTS:

THE FINANCIAL CLAIM

THE TRANSPORT DOCUMENT

OTHER DOCUMENTS

1

2

3

THE FINANCIAL CLAIM: THE “DRAFT”

(A NEGOTIABLE INSTRUMENT SIMILAR TO A CHECK)

GENERALLY THE DRAFT IS:1) DRAWN ON THE BANK THAT ISSUED THE L/C2) PAYABLE AT A CERTAIN TIME (OR TENOR)3) IN THE CURRENCY SPECIFIED IN THE L/C

EXAMPLES OF “TENOR”: AT SIGHT, AT 120 DAYS BILLOF LADING DATE, ON AUGUST 31, 20XX, 30 DAYS DATE,OR ANY DETERMINABLE DATE.

NOTE: “AT SIGHT” IS FOR IMMEDIATE PAYMENT.FOR ANY TENOR BEYOND SIGHT, THE BANK “ACCEPTS”

THE DRAFT TO MATURE/BE PAYABLE AT A FUTURE DATE.(THIS IS CALLED A BANKER’S ACCEPTANCE, AND CAN BE DISCOUNTED)

THE TRANSPORTDOCUMENT:

THE BILL OF LADING1) A “CONTRACT OF CARRIAGE” TO SHIP GOODS2) A “TITLE DOCUMENT” TO OWNERSHIP OF THE

GOODS (EXCEPT TRUCK, RAIL, AIR B/L’S)3) CONSIGNMENT “TO ORDER”=NEGOTIABLE

4) NOTIFY PARTY (FOR ARRIVAL OF GOODS)5) FREIGHT CHARGES (PREPAID OR COLLECT)6) SHIPPING PORTS (“FROM” & “TO”)

NOTE: ALL ASPECTS MUST CONFORM TO THE L/C, AND BE CONSISTENT WITH OTHER DOCUMENTS

• COMMERCIAL INVOICE – DESCRIPTION OF GOODS CRITICAL—MUST BE VERBATIM

• PACKING LIST – AMOUNT OF GOODS IN EACH PACKAGE OR CONTAINER

• INSURANCE CERTIFICATE – USUALLY 110% OF VALUE OF GOODS, COVERING RISKS SPECIFIED IN THE L/C

• CERTIFICATE OF ORIGIN – ATTESTS TO THE COUNTRY OF ORIGIN

• INSPECTION CERTIFICATE – INDEPENDENT VERIFICATION OF QUALITY/QUANTITY

• OTHER DOCUMENTS – ANY REQUIRED FOR CERTAIN PRODUCTS

INVOICE PKG.LIST INSURANCE

ORIGINCERT.

• OTHER DOCUMENTS

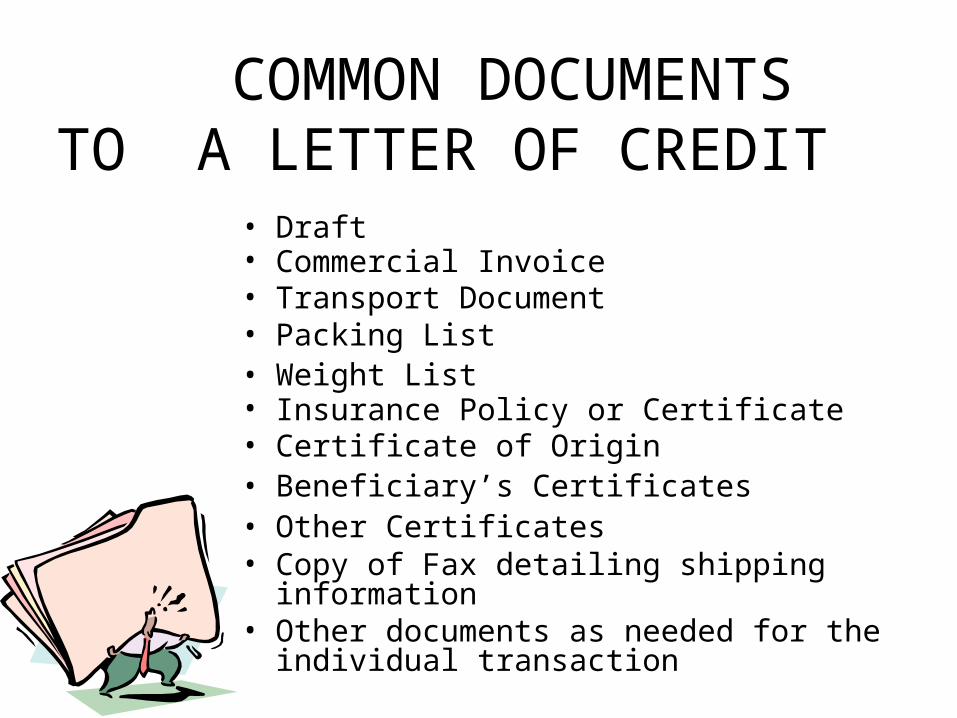

COMMON DOCUMENTS TO A LETTER OF CREDIT

• Draft• Commercial Invoice• Transport Document• Packing List• Weight List• Insurance Policy or Certificate• Certificate of Origin• Beneficiary’s Certificates• Other Certificates• Copy of Fax detailing shipping information• Other documents as needed for the individual

transaction

AMENDMENTS TO THE L/C

• Are costly

• Are time consuming

• The seller instructs the buyer of the necessary amendment

• The buyer must then request their bank to issue the amendment

• The seller’s bank cannot request the issuing bank to make an amendment

• Amendments have to be advised through the same bank which advised the original L/C

• The beneficiary should notify the advising bank of the approval or rejection of the amendment

What Governs Letters of Credit

• Commercial - UCP 600 and ISBP (International Standard Banking Practice)

• Standby - Either UCP600 or ISP98

INTERNATIONAL PAYMENTS RISK SPECTRUMWe have completed the International Payments Risk Spectrum. Whereas payment settled via Open Account and Payment in Advance represent a high degree of risk for one of the parties involved, both Documentary Collections and Letters of Credit offer a compromise in risks facing the Importer and the Exporter.

LEAST RISK TO

IMPORTER

HIGHEST RISK TO

IMPORTER

HIGHEST RISK TO

EXPORTER

LEAST RISK TO

EXPORTER

•Open Account

•Documentary Collections

Documents Against Acceptance

Documents Against Payment

•Letters of Credit

Unconfirmed

Confirmed

•Payment in Advance

Guarantees

Introduction: What is a Guarantee?

Basic Facts: Bid, Advance Payment & Performance Guarantees

Mechanics: How does a transaction involving a Guarantee work?

GuaranteesIntroduction: What is a Guarantee?

•A Guarantee is issued by a bank on behalf of its customer, the Exporter, as financial assurance to the Importer to be collected in the event that the Exporter defaults on certain specified contractual obligations.

•The bank that issues a Guarantee will pay the named beneficiary the amount specified on presentation of a written demand as outlined in the Guarantee.

•While there are standard Guarantee formats, Guarantees can be tailored to meet your specific contractual needs.

•Often Standby Letters of Credit are used instead of Guarantees. Standby Letters of Credit work in much the same way as Guarantees, offering financial assurance to the Importer if the Exporter defaults on agreed-upon contractual obligations. However, there are at least two important ways in which Standby Letters of Credit differ from Guarantees :

Standby Letters of Credit are governed by the International Chamber of Commerce’s UCP while Guarantees are subject to the laws of the country of the Issuing Bank.

Banks in several countries, including the United States, are not empowered to issue Guarantees, and therefore use Standby Letters of Credit instead.

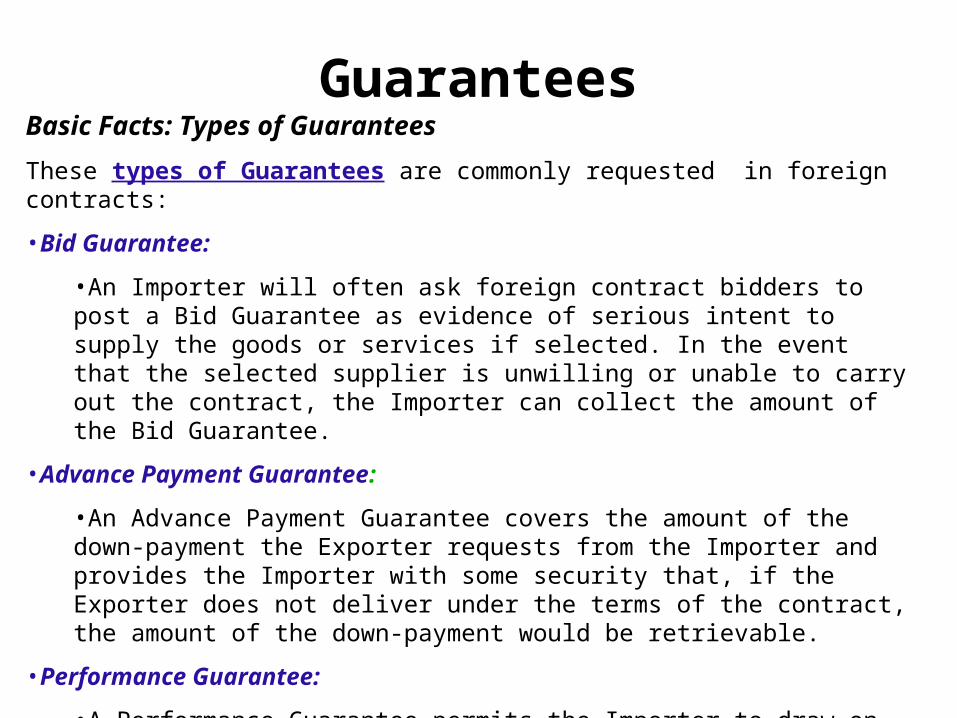

GuaranteesBasic Facts: Types of Guarantees

These types of Guarantees are commonly requested in foreign contracts:

•Bid Guarantee:

•An Importer will often ask foreign contract bidders to post a Bid Guarantee as evidence of serious intent to supply the goods or services if selected. In the event that the selected supplier is unwilling or unable to carry out the contract, the Importer can collect the amount of the Bid Guarantee.

•Advance Payment Guarantee:

•An Advance Payment Guarantee covers the amount of the down-payment the Exporter requests from the Importer and provides the Importer with some security that, if the Exporter does not deliver under the terms of the contract, the amount of the down-payment would be retrievable.

•Performance Guarantee:

•A Performance Guarantee permits the Importer to draw on the Guarantee if the Exporter fails to perform according to the terms of the contract. For example, in the event that the Exporter is unable to complete the contract as agreed halfway through a project, the Importer is compensated with the amount of the Performance Guarantee.

Guarantees

During contract negotiations, the Importer requests that the Exporter provide a Guarantee securing an aspect of the contract (e.g. bid, advance payment). The Exporter (Applicant) enlists its bank (Issuing Bank) to issue the Guarantee in favour of the Importer (Beneficiary) for a specified amount and within a stated time frame.

In the event of default by the Exporter, the Importer would demand against the Guarantee through the Advising Bank.

Mechanics: How does a transaction involving a Guarantee work?

1

Advice of the Guarantee.

3

Guarantee is sent to a correspondent bank of the Issuing Bank for advice to the Importer.

Applies for Guarantee.

Issuing Bank

Advising Bank

2

4

Exporter/ Applicant

Importer/ Beneficiary

ContractNegotiations

A correspondent bank is a foreign bank with which the Issuing Bank

has established a relationship where secure transactions may be processed.

A correspondent bank is a foreign bank with which the Issuing Bank

has established a relationship where secure transactions may be processed.