international monetary fund · • a budget approval process in parliament which allows a...

TRANSCRIPT

INTERNATIONAL MONETARY FUND

Fiscal Affairs Department

ITALY

BUDGET SYSTEM REFORMS

Teresa Ter-Minassian, James Daniel, Annalisa Fedelino, Marc Robinson, Justin Tyson, and Michael Keating

May 2007

Contents Page Abbreviations and Acronyms ....................................................................................................3

Executive Summary ...................................................................................................................5

I. Introduction ............................................................................................................................8

II. The Main Constraints on Transparent and Effective Spending Decisions..........................10

III. Lessons of Selected International Experience of Budget Reforms....................................16

A. Improving Expenditure Prioritization .....................................................................18 B. Delivering Better Services ......................................................................................27 C. Enhancing Accountability for Performance............................................................30

IV. A short-to-medium term budget reform strategy for Italy.................................................32

A. Current Reform Plans and Steps to Date ................................................................32 B. Main Components of a Further Reform Strategy....................................................38

Tables 1. Mandatory Spending by Economic Classification, 2007.....................................................11 2. Reserve and Special Funds ..................................................................................................15 3. The Relation between Goals and Tools for Budget Reform................................................17 4. Spending by Ministries Selected for the Spending Review.................................................35 5. Possible Outline of a Spending Review Process in Italy .....................................................42 Boxes 1. Italy Budget Process: Main Documents.................................................................................9 2. Top-down policy priorities ..................................................................................................11 3. The basic budget appropriation units...................................................................................12 4. Reprioritization in the U.K. and Australia under the Spending Review Process ................16 5. Outcome and Output-Based Programs.................................................................................19 6. Main Differences between Program Classification and Functional Classification of Expenditures ........................................................................................................................20 7. Program and Ministry Structure in the French System: An Example .................................21 8. UK Departmental Spending Review: Sequence of Activity................................................23 9. Public Service Agreements in the United Kingdom............................................................29 10. Initial steps with spending review in Italy .........................................................................36 Annexes I. Program Costing ...................................................................................................................48 II. Selected Performance Indicators – New York City, U.K., Australia..................................52 III. Australia: Reconciliation of Expense Estimates ................................................................51

I.

3

ABBREVIATIONS AND ACRONYMS

BOI Banca d’Italia CIPE Comitato Interministeriale per la Programmazione Economica COFOG Classification of the Functions of Government DPEF Documento di Programmazione Economica e Finanziaria EMU European Monetary Union ESA 95 European System of Accounts EU European Union GFS Government Finance Statistics ISTAT Istituto Nazionale di Statistica MEF Ministero dell’Economia e delle Finanze RGS Ragioneria Generale dello Stato RPP Relazione Previsionale e Programmatica SIOPE Sistema Informativo per le Operazioni degli Enti Pubblici

4

PREFACE

In response to a request from the Italian authorities, a mission from the Fiscal Affairs Department (FAD) of the International Monetary Fund visited Rome during March 21–April 3, 2007 to advise on reforms of the budget system to support better spending prioritization and efficiency. The staff team comprised Mrs. Ter-Minassian (head), Messrs. Robinson and Tyson, and Ms. Fedelino (all FAD), and Mr. Keating (expert, Australia). Mr. Daniel (EUR) joined the mission for the last few days. In addition, Messrs. Dufty and Hughes (UK Treasury) participated in a workshop on international experience organized on March 29, and in other meetings during March 28-April 01, 2007. The mission met with Minister Padoa Schioppa, Undersecretary for Economy and Finance Sartor, other representatives from the Ministry of Economy and Finance, the newly formed Technical Commission for Public Finance, an inter-ministerial working group on education, the Audit Court, the Bank of Italy, the Department of the Government Program, the Department of Public Function, the ministries of Education, Justice, Transport, Infrastructure, Interior, and the parliamentary Budgetary Committees of the Senate and the Chamber of Deputies with their respective Technical Offices. The mission would like to express its gratitude for the excellent cooperation it received from all government officials, and the hospitality provided by the Ministry of Economy and Finance.

5

EXECUTIVE SUMMARY

There is a growing recognition among Italian policy makers, and in the society at large, of the need to substantially improve the effectiveness and cost efficiency of public spending programs. This is needed to create fiscal space to attend to new spending priorities, while further reducing the general government deficit and debt and moderating the already relatively high tax burden; and to increase the transparency of allocation of budgetary resources, and the value citizens receive from their taxes through public goods and services. However, the current budget system poses significant obstacles to the achievement of these objectives. This report reviews the main weaknesses of the system, and outlines, also in the light of relevant international experience, a number of possible steps—several of which build on initiatives already begun by the Italian authorities—to tackle them. Weaknesses of the current budget system The main weaknesses of the current budget system can be summarized as follows (Chapter II):

• An “incrementalist” approach to budget formulation, with the bulk of public spending extrapolated from year to year with marginal changes, without a proper re-examination of the relative value of spending programs; and with limited reflection of the government’s priorities into budgetary choices.

• An excessively fragmented structure of the voted budget, with some 1,500 line items which bear no clear relation to the objectives of public spending.

• The lack of a meaningful medium-term orientation in the budget process, with existing forward projections not representing true baselines for subsequent budgets.

• A budget approval process in Parliament which allows a proliferation of micro-oriented amendments (about 12,000 presented during the discussion of the 2007 budget).

• A plethora of ex-ante controls on budget execution, constraining budget managers’ flexibility in using inputs and fostering a focus on legal compliance, rather than on efficiency in the delivery of public services

• A relatively weak information base on the cost of different spending programs, and on their effectiveness in terms of relevant outcomes; and, relatedly

• Little focus by policy makers on the budget outturn, especially in terms of the results of public spending programs and their cost; and weak accountability for performance.

6

Ongoing and planned reforms

The Italian authorities have already taken a number of steps aimed to address some of the weaknesses outlined above. More specifically, they have:

• initiated the preparation of a program classification for the budget;

• begun a spending review for selected ministries;

• started strengthening capacities both in the Ministry of Economy and Finance (MEF) and in Parliament to evaluate spending;

• made significant progress in strengthening the information base on the execution of the cash budget, including at the subnational level;

• begun a restructuring of ministries, to better align organizational structures and manpower allocation with policy priorities; and

• signed a memorandum of understanding with the social partners, to open a dialogue on the human resource implications of these reforms.

These steps clearly go in the right direction, but will need to be carried forward, in some cases expanded, and complemented by additional actions.

The way forward

Drawing lessons from international experience (Chapter III), this report suggests a package of reforms (Chapter IV).

• On reforming the budget structure, progress should be made in developing a sound program-based budget classification, with full involvement of spending ministries and the MEF in defining programs; and the accounting system should be modernized to measure accurately programs’ costs. It would be prudent to introduce the new program structure in the 2008 budget on a pilot basis, and to make it fully operational in the 2009 budget.

• On spending reviews, these should: (i) become an integral part of the Italian budget system; (ii) generate information to be reflected in improved baseline budget estimates; and (iii) point to any needed revision of spending legislation. Line ministries should receive appropriate incentives to cooperate fully, for example by being allowed to keep part of the savings identified in the spending review. The Education and Transport ministries, which are more advanced in preparations, should complete their reviews in time for the 2008 budget; other ministries, including some already identified, should follow in 2008. A review cutting across ministries should also be given consideration.

7

• On reforms of the budget preparation process, a number of steps could be taken to improve the content and transparency of current documentation, including a substantial recasting of the rolling three-year budget estimates to reflect the cost of delivering policy objectives embedded in existing legislation. The budget documentation should also provide a consolidated picture of how the baseline budget and the proposed legge finanziaria map into the final budget estimates, by program.

• On reforms of the budget approval process, once the spending programs are defined and properly costed, the Parliament should appropriate the budget on a program basis. The much reduced number of spending programs (compared to the 1,500 line items currently included in the budget) would allow to focus parliamentary discussions on strategic policy priorities and their trade-offs with current policies.

• On reforms of budget execution, monitoring, and reporting, ex-ante controls during budget execution should be drastically streamlined, so as to allow managers to allocate funds within each program. Performance indicators for programs should be developed, based on existing and new information (such as users’ surveys), to strengthen ex-post monitoring and budget managers’ accountability for results.

This package of reforms will need to be supported by a well-structured communication strategy. This should highlight how the different stakeholders (parliament, the MEF, the spending ministries, civil servants, and society at large) can benefit from these reforms; and establish milestones for implementation that are sufficiently ambitious to deliver visible results in the relatively near term, but not unrealistic so as to make them unachievable. For their success, reforms will also need to be appropriately sequenced. In this regard, international experience suggests that: (i) the development of a well-structured program classification should be the first step; (ii) appropriations by programs should take place only after reliable cost estimates of programs have been developed and reflected in the accounting system; and (iii) the development of reliable indicators of performance and review of relevant programs should precede the introduction of performance targets. In addition to possible political resistance, additional stumbling blocks stand in the way of reform implementation. There may be a need to modernize the legal system—while the current reforms are predicated on an “unchanged legal framework”, it is possible that the 1978 accounting law may need to be amended. Implementing these reforms will also have significant human resource implications, including a need for increased geographic and functional mobility of civil servants. Finally, these reforms will only affect the central government, which accounts for about 40 percent of total spending; hence, addressing the quality of spending in a meaningful way will require complementary reforms in the complex system of intergovernmental relations—an area where some progress is being attempted.

I. INTRODUCTION

There is an increasing recognition in Italy that the quality of public spending needs to be improved. On one hand, the country faces a number of fiscal challenges that include continuing steadily on the path of fiscal consolidation and public debt reduction while halting unsustainable increases in the (already relatively high) tax burden; and creating the fiscal space for meeting rising spending needs (such as the costs of an ageing population, and the need to revamp deteriorating infrastructure and boost research) that loom ahead. On the other hand, enhancing Italy’s productivity will be essential for raising its growth potential and addressing competitiveness shortfalls vis-à-vis important trade partners. It is in this context that the issue of spending better—that is, leveraging available resources to deliver improved public goods and services, and/or generating savings to be channeled to new priority initiatives—has gained prominence in the political debate. Aware of these challenges, the government is preparing to undertake a number of structural reforms. In a document approved by the Council of Ministers on January 25, 2007, the Minister of Economy and Finance noted that, among other shortcomings, the current budget process has not allowed a proper allocation of scarce resources, supported by the definition of spending priorities and monitoring of achievable results.1 To this end, the government has initiated several reforms, such as an assessment of public spending in selected ministries through spending reviews; the introduction of a program-based budget classification; and support to parliament in its efforts to reform the parliamentary budget approval procedures. These initiatives, to be supported by a new public finance commission (Commissione Tecnica per la Finanza Pubblica), are seen as initial steps to enhance public spending’s effectiveness and efficiency. Significantly improving the quality of spending will require overcoming a number of weaknesses. This report provides a diagnostic of these shortcomings (Section II); distills lessons from international experience with relevant reforms (Section III); and outlines a recommended reform strategy for Italy over the short to medium term (Section IV). The report addresses only selected aspects of the budget process in Italy. A comprehensive analysis of the Italian public financial management system would go beyond the scope of this report; in any case, the detailed workings of the system are well documented elsewhere.2 For comprehensiveness, Box 1 highlights the main steps and documentation of the current budget process, as a quick reference for the discussion in the rest of the report. 1 “Orientamento del Ministero dell’Economia e delle Finanze in materia di struttura del bilancio e di valutazione della spesa.” 2 See, for example, Vegas, G., D. Da Empoli, and P. De Ioanna, Il bilancio dello Stato. La finanza pubblica tra governo e parlamento, Le Guide Il Sole 24 Ore (Milan: 2005 edition).

9

Box 1. Italy Budget Process: Main Documents

Timing

Document

Purpose

June-July

DPEF Documento di Programmazione Economico-Finanziaria

Officially starting the budget cycle for the following year, it contains a medium-term plan for the budget and prospects for the economy. It is presented separately to both houses of parliament, and requires a resolution. The deficit limit approved in the resolution is binding for the finance law, unless an adjustment note to the DPEF (nota di variazione) is presented by the government jointly with the RPP (see below).

September

Relazione Previsionale e Programmatica (RPP) (Sezione I and II) Note Preliminari al Bilancio di Previsione (per Ministeri)

It provides a draft fiscal program with estimates and description of new proposed policies; and includes draft finance law and supporting documents from each ministry. It needs to be presented to parliament by end-September. It contains two sections. Sezione 1: international and domestic medium-term prospects Sezione II: technical details on the baseline budget projections (bilancio a legislazione vigente) and impact of finance law Ministries submit detailed budget proposals by UPBs (the basic budget classification unit, see Box 3).

Disposizioni per la Formazione del Bilancio Annuale e Pluriennale dello Stato (Legge finanziaria)

The Finance law (finanziaria) puts into law new budget proposals. It needs to be approved before the end of the year (typically approved in mid/late December)

Bilancio di Previsione dello Stato per l’Anno Finanziario e Bilancio Pluriennale per il Triennio

The Budget law (legge di bilancio) authorizes all revenue and spending consistent with existing law. It needs to be approved before the end of the year (typically approved in mid/late December)

September- December

Provvedimenti collegati

These are legislative measures associated with the finance law, to be approved by mid-November.

Bilancio per Capitoli This ministerial decree informs line ministries of their budget broken down by chapters.

January

Bilancio dello Stato per Centri di Costo

This is the state budget (accrual by cost centers).

Rendiconto Generale della Amministrazione dello Stato

It provides an annual statement of budgetary outturns.

Disposizioni per l’Assestamento del Bilancio dello Stato e dei Bilanci delle Amministrazioni Autonome

This is the revised/adjusted budget for previous year. Typically presented to parliament in June, it may remain open for a few months.

June

Relazione sul Rendiconto Generale dello Stato

This is the report by Auditor General (Corte dei Conti) on the budget outcome for the preceding year.

Source: MEF website; and “Italy: Report on the Observance of Standards and Codes—Fiscal Transparency Module” (International Monetary Fund, October 2002) http://www.imf.org/external/pubs/cat/longres.cfm?sk=16137.0

10

The primary focus of this report is on central government spending. This is also the coverage of the Italian budget law (legge di bilancio, Box 1), which relates to the state level (central ministries and autonomous agencies). As this accounts (net of intergovernmental transfers) for only about 40 percent of general government’s spending, it is evident that addressing the quality of spending in a meaningful way will require complementary reforms in the complex system of intergovernmental fiscal relations—an area that has remained undefined years after a major constitutional reform assigned new responsibilities to subnational governments. While these issues are not covered in this report, it is nonetheless important to acknowledge their relevance, as reflected in a new legislative proposal recently put forward by the government.

II. THE MAIN CONSTRAINTS ON TRANSPARENT AND EFFECTIVE SPENDING DECISIONS

The current system for formulating and managing public spending decisions in Italy is affected by a number of shortcomings, spanning budget formulation, execution, and reporting. These are briefly reviewed in this chapter.3 Spending decisions do not appear to reflect fully and clearly the government’s policy priorities. In principle, line ministries are supposed to reflect the priorities outlined in the government program in their budget proposals (Box 2); in practice, the current budget structure (see below) and the legal requirements associated with spending decisions do not facilitate the budget prioritization process.4 As outlined in the 2002 Report on the Observance of Fiscal Standards and Codes (ROSC) Fiscal Transparency Module, the budget preparation process mainly reflects the impact of past legislation on spending, and therefore has come to have an incremental focus. The budget that emerges tends to have a strong focus on legal compliance, rather than on strategy, driven by the so-called current (pre-existing) legislation (legislazione vigente).

3 For a more detailed diagnostic, see “Italy: Report on the Observance of Standards and Codes (ROSC)—Fiscal Transparency Module (IMF, 2002). See also Monticelli, Carlo (2006) “La Trasparenza dei Conti Pubblici in Italia: Alcune Proposte” (mimeo).

4 Article 81 (clause 4) of the Constitution establishes that “any other [than the budget] law involving new or increased expenditures must specify the resources to meet these expenditures.” This requirement has been interpreted as an obligation to establish all spending by law and indicate the source of its funding,

11

Box 2. Top-down policy priorities

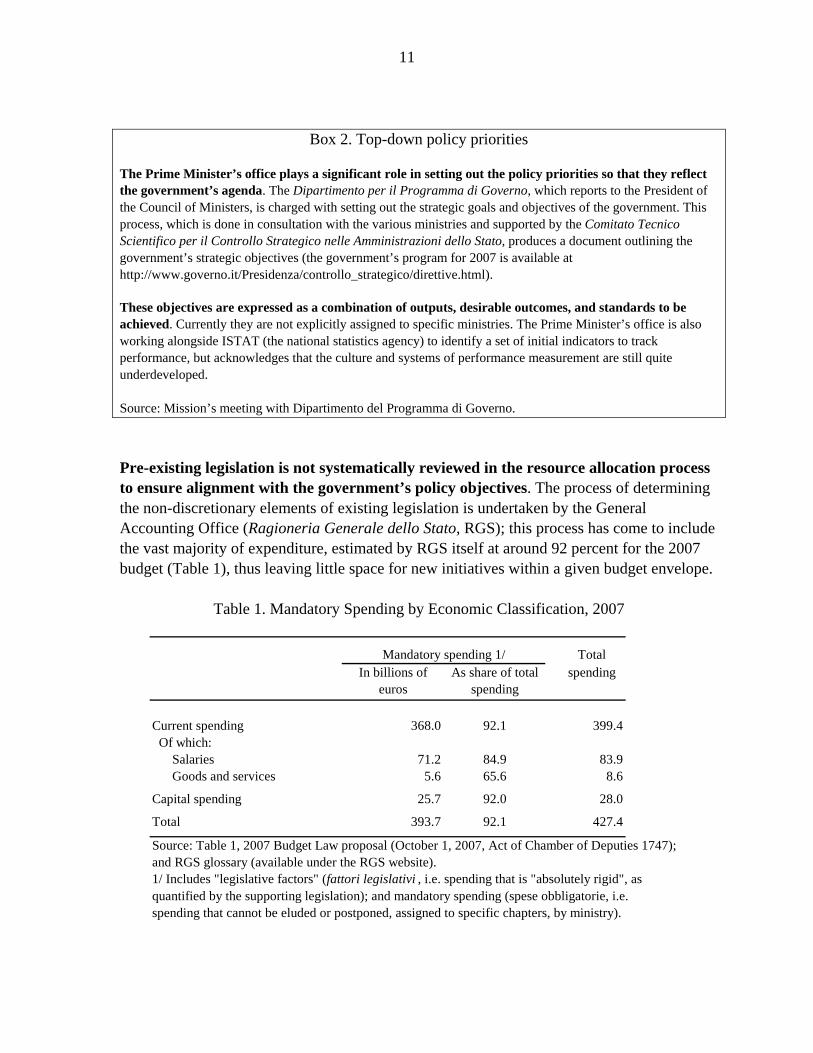

The Prime Minister’s office plays a significant role in setting out the policy priorities so that they reflect the government’s agenda. The Dipartimento per il Programma di Governo, which reports to the President of the Council of Ministers, is charged with setting out the strategic goals and objectives of the government. This process, which is done in consultation with the various ministries and supported by the Comitato Tecnico Scientifico per il Controllo Strategico nelle Amministrazioni dello Stato, produces a document outlining the government’s strategic objectives (the government’s program for 2007 is available at http://www.governo.it/Presidenza/controllo_strategico/direttive.html).

These objectives are expressed as a combination of outputs, desirable outcomes, and standards to be achieved. Currently they are not explicitly assigned to specific ministries. The Prime Minister’s office is also working alongside ISTAT (the national statistics agency) to identify a set of initial indicators to track performance, but acknowledges that the culture and systems of performance measurement are still quite underdeveloped. Source: Mission’s meeting with Dipartimento del Programma di Governo. Pre-existing legislation is not systematically reviewed in the resource allocation process to ensure alignment with the government’s policy objectives. The process of determining the non-discretionary elements of existing legislation is undertaken by the General Accounting Office (Ragioneria Generale dello Stato, RGS); this process has come to include the vast majority of expenditure, estimated by RGS itself at around 92 percent for the 2007 budget (Table 1), thus leaving little space for new initiatives within a given budget envelope.

Table 1. Mandatory Spending by Economic Classification, 2007

Mandatory spending 1/ TotalIn billions of

eurosAs share of total

spendingspending

Current spending 368.0 92.1 399.4 Of which:

Salaries 71.2 84.9 83.9Goods and services 5.6 65.6 8.6

Capital spending 25.7 92.0 28.0

Total 393.7 92.1 427.4

Source: Table 1, 2007 Budget Law proposal (October 1, 2007, Act of Chamber of Deputies 1747); and RGS glossary (available under the RGS website).1/ Includes "legislative factors" (fattori legislativi , i.e. spending that is "absolutely rigid", asquantified by the supporting legislation); and mandatory spending (spese obbligatorie, i.e.spending that cannot be eluded or postponed, assigned to specific chapters, by ministry).

12

The current budget classification, which is not structured around programs, does not allow analysis and implementation of allocation decisions in line with policy priorities. The budget is appropriated on the basis of UPBs (unità previsionali di base), which in turn are composed of chapters that provide information of a functional and economic nature (capitoli). The content and size of the UPBs vary significantly, with little resemblance to standard functional budget classification categories (Box 3).

Box 3. The Current Budget Classification

The basic unit of budget classification is the chapter (capitolo). Each chapter is mapped into standard economic and COFOG functional classification, and has a four digit code: the first number indicates whether it is for current payments (numbers 1 to 6); capital payments (numbers 7 and 8); or for payments with respect to financial transactions (number 9). A chapter may be prorated across as many as ten functions (at the third level), but must map to one economic object. For example, chapter 2643 (goods and services of the Ministry of Economy and Finance) maps into 10 different functions (on the basis of 10 coefficients; the largest share, equal to 37 percent, is attributed to function 1.1.2.3: budget policies). Given that most spending requires a legal basis, chapters are also mapped to the substantive laws which give rise to them. These are listed in a document (nomenclatore degli atti), which quotes all the laws relating to each chapter. For example, chapter 2643 is associated with 14 pieces of legislation, ranging from a 1929 royal decree to the 2004 finanziaria. Chapters are grouped into Unità Previsionali di Base (UPBs), which provide the minimum level of parliamentary appropriation. The Ciampi reform (Law 94/1997) introduced UPBs to reduce considerably the number of budget items from some 6,000 chapters to about 1,000 units. Each UPB was assigned to a specific manager, but without functional or programmatic purpose. There is a general prohibition on transferring budgetary appropriations between UPBs, except for the office of the prime minister. In the 2007 budget, there were about 1,500 UPBs and some 4,500 chapters. UPBs may vary significantly in size. For example, in the 2007 budget, UPB 4.2.1.18 (fiscal federalism) amounts to some €45 billion; UPB 4.1.1.0 (administrative spending, funzionamento) to which the above mentioned chapter 2643 belongs, amounts to €120 million; while UPB 4.2.3.25 (management of port workers) amounts only to some €870,000. Source: “Italy: ROSC Fiscal Transparency Module” (2002); and various MEF documents available at http://www.rgs.mef.gov.it/VERSIONE-I/Norme-e-do/Bilancio-e/Disegno-di/index.asp The budget is structured around a three-year framework, yet budget discussions focus narrowly on a one-year horizon. This is due to a number of factors:

• A sound system of forward estimates is not implemented. Estimates for outer years are not binding or sufficiently robust to give certainty to both the MEF and line ministries about “baseline” spending in the bilancio a legislazione vigente (budget law, Box 1)—this is a critical shortcoming in a system, like the Italian one, where most spending is driven by pre-existing legislation.

• While information on the macroeconomic framework underlying the budget projections and the main aggregate revenue/spending is generally available, it is not

13

immediately clear, nor transparently reported, how the various macroeconomic assumptions translate into budget projections—with the concomitant risk that, as macroeconomic projections change, budget forecasts are re-opened.5

• There is no top-down medium-term overall expenditure ceiling that would guide the budget preparation process.6

The non-binding nature of estimates in the outer years has led to haggling between the MEF and line ministries in the budget preparation stage over the appropriate costing of existing legislation. Line ministries do not have confidence that any savings identified within the baseline can be kept and directed to new policies—hence, they do not face the right incentives for properly costing their spending but rather tend to overstate the projected cost of delivering existing policies in an incrementalist approach to budget planning. Moreover, there is as no systematic review of current expenditure and legislation, nor an explicit requirement for an up-front identification of fiscal space for new initiatives. The lack of a strategic approach in the budget preparation process carries over to the parliamentary budget discussions. As resource allocation discussions at the executive level focus on small and detail-oriented inputs, rather than on programs and results, so do parliamentary discussions, where elected members juggle multiple amendments with reportedly limited awareness of their policy impact. The budget baseline (tendenziale) per se receives almost no scrutiny by parliament, to the point that there are no proposed amendments to it—a further proof that its construction is not transparent or well understood. Indeed, the excessive number of UPBs (even if they corresponded to well-defined objectives) prevents coherent choices and decisions by parliament; and the cumbersome approval process for the financial law (finanziaria, which contains new spending proposals) has led to an ever increasing number of proposed amendments to the law (which topped 12,000 in 2006). This has often culminated in last-minute omnibus financial laws where strategic priorities are not (and cannot) be identified, and where UPBs may be used as vehicles to cater to particular interests. As a result, the relationship between the initial budget estimates and the subsequently voted appropriations is not transparent. There is no reconciliation of how UPBs have

5 The macroeconomic framework is available in the beginning of the budget process (as highlighted in the Relazione Previsionale e Programmatica); however, details of the underlying model are unavailable and no updates to the overall macro or fiscal framework are formally issued at the end of the budget process, regardless of changes in the targeted deficit ratios. For some information on modeling techniques currently applied, see Dipartimento del Tesoro. I Documenti Programmatici: Ruolo, Strutture, Processi e Strumenti del MEF, 2006. 6 The Document of Economic and Financial Programming (DPEF), presented by end-June, includes only a nominal deficit target that is binding for the budget documents submitted to parliament at end-September.

14

varied from the initial baseline projections to the final voted allocations—a process that would nonetheless prove formidable in the current system of 1,500 UPBs. The current system for allocating and managing resources is not conducive to a culture of managerial responsibility. Pre-existing legislation tends to be interpreted as binding the content of specific chapters; and during the fiscal year, the RGS exerts a function of ex-ante control to ensure compliance with the law. All these factors combined—the perceived non-discretionary nature of most expenditure, the focus on legal compliance rather than outcomes, and the rigidities imposed by ex-ante controls—do not foster a culture where managers feel responsible for budget outcomes. In addition, as additional spending can be financed via special funds during the year (Table 2), managers do not face hard budget constraints. Operational flexibility is also hindered by the rules on reallocation of funds across budget chapters. Article 2 clause 4.5 (2.4 quinquies) of the 1978 Accounting Law allows managers (through a ministerial decree) to reallocate between budget chapters in the same UBP; however, this flexibility only applies to those UPBs that are classified as discretionary. The only exception is capital expenditures under certain conditions. A notable example of a non-discretionary input in the Italian context is staff, thus depriving managers of important trade-offs in the cost-effective delivery of public services. In practice, this limits reallocations to a small portion of total expenditure (as shown in Table 1). Virements across UPBs need approval from the RGS and supplementary approval from parliament. Consequently, there is currently little accountability for the cost-effective use of resources. The process for approving and controlling the use of resources, together with the lack of routine performance information, breaks the link between managerial actions and attainment of the policy objectives established at the beginning of the budget cycle, thus making it hard to create incentives for accountability. Line ministries feel that spending is driven by, and controlled from, the MEF; while the MEF believes that line ministries should have greater ownership of their budgets and better prioritize within their budget envelopes. The budget outturn is audited by the Audit Court to ensure legal compliance with the approved budget, but this is done primarily on the basis of financial information. Limited use is made of non-financial information to measure performance; in any case, this would be a hard task given the absence of clear performance expectations at the formulation and approval stages of the budget. According to the parliamentary Budget Committees, reports by the Audit Court do not receive much attention from legislators, nor do they play a significant role in the resource allocation decisions for the following year.

15

Table 2. Reserve and Special Funds

Name Legislative basis

Ministry Purpose

Access rules

Fund for mandatory spending (fondo di riserva per le spese obbligatorie e d’ordine)

Accounting Law 468/1978 article 7

MEF Elenco 1 Budget Law

To increase allocations of chapters related to mandatory spending (listed by ministry/chapter in Elenco 1).

Decree of Minister of Economy, to be registered by Audit Court.

Fund for carry-over of unspent capital allocations (fondo speciale per la riassegnazione dei residui perenti delle spese in c. capitale)

Accounting Law 468/1978 article 8

MEF To release funds previously authorized but not yet spent for projects.

Decree of Minister of Economy, to be registered by Audit Court.

Fund for unforeseen spending (fondo di riserva per le spese impreviste)

Accounting Law 468/1978 article 9

MEF Elenco 4 Budget Law

To increase allocations for spending chapters, without impinging on future budgets on a continuous basis.

Decree of President of the Republic; proposed by Economy Minister and to be registered by the Audit Court.

Fund for cash authorizations (fondo di riserva per le autorizzazioni di cassa)

Accounting Law 468/1978

article 9-bis

MEF To increase cash allocations to chapters with insufficient funds, in line with the “objectives of public finance.”

Decree of Minister of Economy, to be communicated to Audit Court.

Fund for authorization of current spending from permanent law (fondo di riserva per le autorizzazioni di spesa delle legge permanenti di natura corrente)

Accounting Law 468/1978

article 9-ter

MEF To provide additional funds for UPBs that face funding shortfalls, consistent with “objectives of public finance”

Decree of the Minister of Economy; proposed by relevant minister and to be communicated to the relevant parliamentary commissions.

Special funds (fondi speciali)

Accounting Law 468/1978 article 11

MEF Elenco 5&6 Budget Law

(and tabella A and B finanziaria)

To fund financial impact of legislative changes to be introduced after the budget is approved (finanziaria lists them, their cost, and the relevant ministries).

Can be accessed after the relevant laws are approved. Funds expire if not used.

Various reserve funds

Various laws (typically,

finanziaria laws)

Relevant ministries Purpose established in the law creating these funds; for example, fund for good and services.

Funds to integrate budget allocations (assegnazioni/integrazioni di bilancio)

Accounting Law 468/1978 article 12

MEF Elenco 2&3 Budget Law

These funds are not included in the budget; they provide an ex post channel to address shortfalls in budgetary appropriations for specified purposes (tax refunds; debt service, etc.)

Decree of President; proposed by Economy Minister. The rendiconto lists, ex post, the decrees that effected such integrations and their reasons.

Source: Law 268/1978; Vegas, G., D. Da Empoli, and P. De Ioanna (2005); and various budget documents. Note: Amounts of these funds cannot be immediately traced in the budget documents. According to RGS and other government officials met by the mission, the amounts allocated to theses funds are not significant, and have become less relevant over time. Some funds are actually “emptied” during the parliamentary budget discussions, as resources originally allocated to some of these reserve funds are “siphoned off” to other budgetary uses.

16

III. LESSONS OF SELECTED INTERNATIONAL EXPERIENCE OF BUDGET REFORMS

Over recent decades, many countries have implemented major reforms of their budgeting systems, as part of wider strategies of public sector reform with broadly three overarching goals: (i) delivering the government’s policy priorities; (ii) improving the efficiency and effectiveness of public services; and (iii) enhancing accountability for the use of taxpayers’ money. More specifically:

• A key focus of international budget reforms has been the improvement of expenditure prioritization to deliver the government’s policy priorities. Budgeting systems should be capable of allocating limited public funds to the services that deliver greatest perceived benefit to the community. The social payoffs of these prioritization reforms have been clearly demonstrated. (Box 4).

• Better prioritization is important, but it is only part of what is required to improve the efficiency and effectiveness of services. Prioritization per se does little to improve efficiency—that is, to lower the cost at which services are delivered. And while better prioritization is a significant part of improving service effectiveness, improved program design and management are equally relevant. An important element in the reform agenda for improving the efficiency and effectiveness of public spending has been the improvement of performance information, particularly through performance measures and evaluation.

• The provision of performance information to the public and to Parliament is shown to play a significant role in holding the government to account for the results achieved by its policies.

Box 4. Reprioritization in the United Kingdom and Australia under the Spending Review Process

Under the Spending Review (SR) system initiated in 1998, the United Kingdom has demonstrated a striking capacity to achieve major shifts in expenditure, creating scope to fund important new expenditure priorities by cutting low priority/ineffective programs. Over the decade since the first SR, there has been a deliberate and large shift in priorities toward frontline public services in three key sectors: health, education and transport. As a result, the share of these three priority services in total public expenditure increased from 28 percent in 1997-98 to 34 percent by 2007-08. By contrast, the share of social security spending has fallen from 30 percent to 27 percent over this period due in part to the success of the Government’s welfare-to-work program. The Expenditure Review Committee (ERC) system which has operated in Australia for more than twenty years demonstrated a capacity, during two episodes of fiscal consolidation in the mid-1980s and mid-1990s respectively, to target expenditure cuts at low-priority programs, and thereby avoid recourse to clumsy and indiscriminate “across-the-board” cuts. This not only softened the pain of expenditure cuts, but also made fiscal consolidation more sustainable

17

There are a number of key tools that have been experimented with for achieving these goals. For simplicity, the tools described here are mapped into the three goals above: (i) tools for improving expenditure prioritization; (ii) tools for delivering better services; and (iii) tools for enhancing accountability. This grouping should not be rigidly interpreted, as in most cases these tools are useful in the attainment of more than one overarching goal. Table 3 shows the relationship between goals and tools for achieving them.

Table 3.The Relation between Goals and Tools for Budget Reform

GOALS TOOLS

Improving expenditure

prioritization

Delivering better services

Enhancing accountability

for performance

Program budgeting

X X X

Spending reviews

X X X

Medium-term focus/ sound forward estimates

X X

Budget process for prioritization

X

Performance indicators X X

Evaluation X X

Performance targets X X

Results-based funding X

Input flexibility X X

Performance information to parliament

X

Performance auditing

X

18

A. Improving Expenditure Prioritization

Tool 1: Program Budgeting

For expenditure prioritization purposes, the program classification of expenditure is particularly valuable. It is for this reason that the French have, following in the footsteps of many other countries, introduced a program classification to replace their previous budget classification (by chapters which were largely input-based). This was a cornerstone of the budgeting reforms undertaken following the Loi Organique relative aux lois des finance (LOLF) of 2001. The Italian government has decided to adopt a similar approach to program budgeting, in which overarching missions are designated, and a number of programs are then identified within each mission.7 Programs should be the basis of budgeting, and not solely an instrument of transparency. While one of the purposes of programs is to report, after the event, the purposes for which government used public money, programs can do much more than that. They can be used as the basis of budget preparation by the government, with agency budget requirements being estimated and evaluated on a program-by-program basis. They can also be the basis on which the parliament appropriates money to ministries in the budget law, as is done in a large number of countries including France. As part of this, “forward estimates”—discussed below—can be formulated on a program basis. To be of maximum use for priority-setting, programs should generally be outcome and output-based. That is, they should represent groups of services (“outputs”) which are unified first and foremost by the fact that they share (one or more) common intended outcomes.

7 For example, the 34 missions employed in France in 2005 included “health”, “security” and “justice.” As an example of the program structure, the justice mission comprised 5 programs including “judicial justice,” “prison administration,” and “judicial protection of youth.”

19

Box 5. Outcome and Output-Based Programs Outcomes are impacts of government services on individuals, social structures and/or the physical environment. Examples are the protection of natural flora and fauna; the acquisition of knowledge (literacy, numeracy etc) by students; and reduced crime. Thus a Nature Conservation program is an outcome-based program which groups all outputs designed to protect natural flora and fauna. Similarly, a Higher Education program would group a range of services with aim to achieve (amongst other things) knowledge outcomes. This example of a Higher Education program illustrates a further point which applies to many programs in a well-designed classification system: although shared outcome(s) are the first criterion upon which the program is based, the program is further defined (and distinguished from related programs such as Primary Education) by the nature of its client group (students who have completed and advanced beyond secondary education). The reason why programs should in general be outcome-based is that in this way they will best capture the key expenditure prioritization choices which most concern the government at the highest level of budget decision-making. Concretely, what ministers and the finance ministry should be most concerned about in setting expenditure priorities is “guns or butter” type choices: how much should be spent on defense versus education, how much on preventative health versus health treatment services, etc. Some of the lessons for international experience for good program design are: • Programs may not correspond exactly with a functional classification of outlays (see

Box 6).8

• The objective of each program should be clearly and briefly stated, as should the program’s strategy for delivering this objective.

• Strategic planning, at the government-wide or agency-specific level, should be harmonized with program planning. In particular, the objectives and strategies articulated with respect to a ministry’s programs should be part of its strategic plan.

• Programs should be agreed by the Finance Ministry and relevant line ministry, rather than decided unilaterally by the latter. The best approach is for the line ministry to develop a proposed structure, and for this to be reviewed by, and coordinated with, the Finance Ministry.

8 There is a limited number of exceptions to this proposition, the principal being “administration” programs.

20

Box 6. Main Differences between Program Classification and Functional Classificationof Expenditures

Both the functional classification (COFOG) and a program classification have the overall objective of classifying expenditures according to the purpose for which the expenditure is incurred. Beyond that common objective, however, the two classification systems have different purposes. The objective of a program classification is operational, i.e. to allocate resources on the basis of government policy priorities, so as to focus budget managers on the achievement of policy goals. In a program classification, transfer of responsibility for a program from one ministry to another would see the classification of expenditure transferred as well, so as to ensure accountability for program delivery. The objective of COFOG, on the other hand, is statistical, i.e. to provide a consistent basis for reporting expenditure that does not vary over time or between countries. COFOG is therefore independent of the structure of government. Expenditure on a particular program will always be classified in COFOG in the same way, irrespective of whether administrative responsibility for the program is shifted from one ministry to another. This is a strength of a reporting system such as COFOG. An important practical difference between the two classification systems is in the aggregation principle (i.e. the rule or basis for grouping expenditures together). In COFOG, the second and third levels combine activities that have quite different characteristics from a management perspective. For instance, lower secondary education (the third level in COFOG) includes the provision of education in schools, second-chance secondary education for adults, inspection of schools, and grants or other support provided to students to attend schools.1 Typically, different institutional units within an Education Ministry would be involved in delivering some of these services, and performance would be measured differently. The management perspective should be kept in mind when designing programs if the objective is to facilitate greater flexibility and accountability. When defining programs, the first question that should be asked is: do these services have a common specific policy objective? ________________________________ 1 See http://unstats.un.org/unsd/cr/registry/regcs.asp?Cl=4&Lg=1&Co=09.2.1

• Programs should generally not cross the boundaries of ministries, because each

ministry needs to receive a clearly defined budget. (In the new French system, some missions cross ministries, but all ministries receive program appropriations which are theirs alone. See Box 7.)

• Following the introduction of programs, the organizational structures of ministries should be reviewed, to make them more results-focused and align them more closely with the program structure. It is generally a mistake to base programs structure on pre-existing organizational structures as this is often defined around processes or functions, and not the purpose of the programs.

21

Box 7. Program and Ministry Structure in the French System: An Example

Mission Solidarity and

Integration

Program Policies for

Social Inclusion

Program Equality Between Men and Women

Program Sickness

Protection

Program Actions for Vulnerable

Families

Program Welcome and Integration of

Foreigners

Program Handicap and Dependence

Program Implement-

ation & Support of Health and

Social Policy

Ministry of Employment, Social Cohesion and Housing Ministry of Health and Solidarity

• Budgeting by programs requires that accounting systems be enhanced, to provide reasonably accurate program costings. Program budgeting requires that expenditure on inputs be allocated to programs. As discussed in Annex 1, cost allocation is a demanding challenge, particularly with respect to “indirect” costs.

• Because of the complexity of indirect cost allocation, it is reasonable in the early years of a program budgeting system to have “administrative” programs in each ministry covering overhead costs (such as ministry-wide support services), notwithstanding that such programs violate the principle that programs should be outcome and output based. The objective should, however, be to gradually reduce and then finally eliminate such programs, as improvements in the capacity of accounting systems to allocate indirect costs to programs improve. (See Annex 1).

Tool 2: Spending Reviews

The basic purpose of a spending review is to improve the quality of public services. It focuses on the objectives of government programs, their relevance to current government priorities, the outcomes being achieved and at what cost. Because of its in-depth probing, a

22

spending review is an important source of information to improve the prioritization of public expenditures and resource allocation. Spending reviews are normally based on programs, and it is difficult to carry them out if information is not available on a program basis. In some cases, however, activities such as the provision of information and technology services across government ministries may be the subject of a spending review. Major spending reviews may also cut across a number of departments and involve a group of programs that impinge on a policy outcome such as improving the transfer of disadvantaged people from welfare to work.9 In addition, it is also important that tax expenditures be included in the range of spending reviews, and this is normally best done in conjunction with a review of those spending programs that service a broadly similar purpose.10 Spending reviews are necessarily about changing programs and thus require that choices are made. Where spending reviews have proved most useful, such choices have not been confined to only a small amount of “discretionary” expenditure, as that limits what can be achieved by spending reviews. Indeed, countries have been prepared to review entitlement programs, such as pensions, to improve, for example, their effectiveness in encouraging people to move from welfare to work or to postpone their retirement. All spending ministries are typically expected to develop an agenda of spending reviews and undertake some review activity regularly. These spending ministries are best placed to identify the areas with the best potential for efficiency gains within their programs. Spending reviews are, however, most effective if they target those programs where there is reason to believe that cost effectiveness can be substantially increased and significant savings realized (for the criteria to identify priorities for a spending review, see Box 8). Some of the most significant spending reviews consider cross-cutting issues—such as child poverty or how to improve assistance to disabled people to return to work—that cover a range of programs in more than one ministry. Such reviews necessarily involve staff from the relevant spending ministries, but are often led by someone from a central agency to ensure proper coordination; for example, from the Prime Minister’s office. 9 These cross-cutting reviews can also encourage closer cooperation between ministries on common policy problems and can identify duplication of functions

10 For example, a review of income support to families might cover the tax expenditures along with the government outlays for this purpose.

23

Box 8. UK Departmental Spending Review: Sequence of Activity

Analysis of Expenditure by Program/Objective

Breakdown of expenditure by program with analysis of historic cost profile, current expenditure and forecast trends.

Identifying Areas of Highest Priority/Return

Identify areas of high priority programs based on, e.g.:

Identify scope for improving value for money in programs or processes where, e.g.:

• the relationship with Government priorities and objectives;

• high economic or social returns to additional expenditure;

• substantial baseline pressures on forward expenditure; or

• the impact of exogenous pressures.

• objectives have lapsed or been achieved;

• the link between spending and outcomes is weak;

• input or unit costs are high relative to public, private or international benchmarks; or

• there is large performance variation across delivery units.

Reprioritization of Expenditure

Revised forward estimate based on: Revised performance framework including

• resources that can released from low value for money programs or areas of expenditure; and

• additional expenditure required on high priority programs or areas of expenditure.

• outcome objectives for new programs; and

• performance targets, measurement and monitoring arrangements.

Delivery Planning and Implementation

Agreed delivery plan setting out revised appropriation, policy reforms, legislative and administrative changes and other actions required to refocus expenditure on objectives identified and remove obstacles to their

achievement. Source: U.K Treasury’s contributions during the mission. Often a spending review will extend beyond identifying the scope for improved efficiency and will propose options for re-designing the program(s) to improve overall cost effectiveness. The outcome of such a review will typically identify the scope for some savings, but some or all of these savings may be used to improve the quality of those programs, and in some cases spending reviews may result in well-formed proposals for additional expenditures on high priority programs or areas of expenditure.

24

Establishing the right incentives is crucial to secure ministries’ participation in spending reviews. In this regard, the prospect of being able to retain some or all of the savings from a spending review, along with the scope to reallocate resources more effectively and the development of firmer forward estimates of future program expenditures, are important incentives for ministries to undertake spending reviews. The share of savings retained by the program ministry typically depends upon the significance of the savings and where the main ideas for achieving the savings originated—inside or outside the program ministry. The experience shows that spending reviews can lead to decisions—often taken in the budget context—to seek parliament’s approval to change legislation. In particular, where mandatory programs, such as entitlements, are subject to a spending review, that may well lead to proposals that require changes in legislation. More generally, spending reviews will lead to proposals to change legislation where there is a need to redesign a program to meet its objectives more efficiently or effectively. In effect, legislation is then seen as the means for delivering policy objectives rather than as a constraint that confines policy objectives, and the means for achieving them, to preservation of the status quo. The procedures and timing of spending reviews are flexible, with some broad common features. In the United Kingdom, spending review occurs every three years, with two Comprehensive Reviews across all spending ministries over the last decade. One important outcome of the UK spending review is an agreed set of budget forward estimates for the next three years. In other countries, there is a regular rolling agenda of spending reviews that focus on particular programs or on particular policy issues. These reviews are usually monitored by the Finance ministry, with its more direct involvement for the more significant reviews. Although these reviews are less comprehensive than the approach in the U.K., the sequence of activity is generally the same as shown for the U.K. in Box 7. The activities of officials in both the spending ministries and especially in the budget department change from a focus on haggling over funding for existing activities to program analysis—which focuses mainly on program efficiency and effectiveness. The skill set required is different from that of “traditional” budget analysts and managers. Also, the relations between spending agencies and the budget department should reflect joint efforts to improve program effectiveness rather than centering on an essentially adversarial role. The budget department should be a source of advice to agencies in the development of performance indicators and on best practice evaluation. Often in countries where spending reviews are most advanced, the budget department is expected to keep a register of all significant evaluations and advise the government on the planning of future evaluations that the government might want to commission.

25

Tool 3: Strong Medium-Term Framework and Sound Forward Estimates

A strong medium-term focus for the budget is the basis for resource allocation, helps maintain expenditure control over time, and assists in responding to new priorities. It also helps with prioritization by forcing baseline changes to be linked to policy changes.

A robust system of forward estimates of the cost of existing policy—which does not need to be renegotiated each year—is essential to achieve a medium-term budget focus. Budget systems based on forward estimates work best where agencies accept that they are properly funded, and that their estimates will be updated by an agreed set of rules for future years to cover the cost of continuing existing policies. For example, this updating can involve an agreed set of rules, so that it becomes a purely technical exercise by Finance ministry officials, as in Australia. All changes in the estimates from one budget to the next are in response to changes in budget parameters (such as the rate of inflation), and are subject to agreed rules, or reflect changes in existing policy; it is possible to track these changes from one budget to the next (Annex II). In the U.K., forward estimates are set for the three-year period following a spending review, but there is scope to re-examine the base estimates of the cost of existing policies at the time of the next spending review.11 The important feature of a robust forward estimates system—however updated and rolled forward—is that it removes annual haggling over the cost of existing policy and allows agencies to plan with confidence. The budget process is then focused on policy changes and how the effectiveness of programs can be improved. The incentives for spending review are maximized as agencies can then identify the potential savings against firm estimates of program costs. For some purposes projections of future government outlays can be extended beyond the normal budget year plus three to consider the budgetary pressures that may result from longer term challenges. For example, the response to climate change, the future needs for the provision of infrastructure, and the fiscal implications of an ageing population all require a longer time frame to inform current policy making. Forward estimates of programs also provide the basis for ensuring that managers confine their spending within the limits of those estimates. Any potential overspends are then matched by savings found elsewhere or (to a limited extent) by shifting funds between

11 Most countries provide for some reserve funding in their budget to cover unforeseeable and unavoidable new expenditures and forecasting errors. These reserves are, however, typically no more than 2 percent of total outlays in the budget year, and rather more as they increase over the forward estimates period. Brazil, Spain, and the U.K. all cap contingency reserves at 2 percent of spending; Australia, which imposes very tight constraints over its budget estimates, has a contingency reserve in the budget year of only 0.7 percent.

26

years.12 In addition, the experience has been that, where the Finance ministry only attempts to control the total spending on a program, it is typically more successful than when it tries to control many different program inputs. The reality is that managers will only take responsibility for living within their budgets if they have the necessary flexibility and there is limited central intervention.

Tool 4: Budget Process’ Focus on Priority Setting

International experience suggests that an effective budget process must be driven from the top, especially in the initial stage when the broad strategic directions for the budget must be set. This initial strategic guidance is essential if the budget is to truly reflect the government’s principal priorities and if spending reviews are to realize their full potential. The advice normally covers an assessment of the budgetary scope for spending, taking into account any commitments on the size of government outlays and taxation and the fiscal deficit and/or government debt. The strategic guidance might also extend to areas identified for review and possibly targets for savings to be achieved, and/or an envelope for new spending on a net basis after savings have been included. This advice on spending/savings targets does not necessarily cover all spending ministries or even all activities/programs of those ministries receiving such advice. The expectation is, however, that any changes in areas not covered by the advice would be budget neutral, at least on a net basis when aggregated across a ministry. A budget process focusing on priority setting and incorporating a spending review necessarily entails more policy choices and therefore calls for ministers’ stronger role. In those countries which have the most advanced budgeting systems, the strategic guidance is typically provided by the Prime Minister working in collaboration with the Finance Minister. It may then be ratified by the full Council of Ministers. Subsequently, ministers will then bring forward their budget submissions that reflect the initial guidance and cover all new policy proposals to spend or to save, including the outcomes from the individual spending reviews for relevant ministries. Ministers usually have the right to shift resources from one program to another when preparing their budgets, as long as these transfers are agreed to be cost-neutral. The full realization of this flexibility requires that staff are also transferable. In a number of countries, a sub-committee of senior ministers undertakes the intense process of examining budget submissions. This always includes the Finance Minister, and

12 In Australia, for example, program managers can carry over funds to the next year where there is underspending, but they must borrow forward from next year’s forward estimates, when they over-spend in the current year.

27

sometime the Prime Minister.13 The decisions taken by this sub-committee may, in some countries, need to be ratified by the full cabinet; in other countries, such sub-committees have sufficient authority to determine the budget without reference to full cabinet. Less significant decisions may be taken bilaterally by the Finance Minister and the relevant spending minister.

B. Delivering Better Services

Tool 1: Performance Indicators The evolution of public service performance management systems in countries such as Australia, France, Netherlands, the U.K., and the U.S. has been toward the development of high-quality performance indicators underpinned by robust measurement, monitoring and accountability arrangements. Experience in these countries suggests that performance indicators are most effective in driving behavior and improving outcomes when they are: • Focused primarily on outcomes and outputs, rather than inputs and processes.

• Developed in consultation with frontline delivery agents and service users to ensure that their definition, measurement, and delivery reflect their experience and preferences and perverse incentives—such as the incentive to sacrifice the quality of service in favor of increased quantity of service when the targets are set for the latter but the former is not measured—are minimized.

• Subject to effective quality assurance. Both internal control and the external auditor have an important role to play in this respect. Explicit, publicly-available statements of the methodology used for each indicator—as in the U.K.—represent another valuable quality assurance measure.

For the purposes of external users and decision makers, a small number (3 to 5) of key indicators per program should be identified. Managers within the agency will, of course, use a larger set. Central agencies, including the Finance Ministry, should play a key role in agreeing on these key indicators with line ministries, so as to ensure that they meet the needs of central decision-makers. Some examples of performance indicators used in selected countries are in Annex III. Developing a set of performance measures for the whole government that is robust and relevant enough for use in the budget process takes considerable time. Countries that are 13 For example, Australia, Canada, New Zealand, and sometimes the U.K.

28

leaders in this field took decades to build the sophisticated systems they have today. While all ministries can be expected to develop some performance indicators from the outset, it should be expected that these will be subject to revision in the light of experience. Also, starting with a small number of measures and expanding the set gradually over time is the only practical strategy. The main function of government officials is the provision of information regarding program performance. This includes identifying options to improve program performance and to meet new priorities identified by ministers, and ensuring agreement on costings with the Finance ministry before the budget submissions are finalized and lodged for ministerial consideration. The Finance ministry provides alternative options for savings when those proposed by spending ministries are found to be inadequate; it also keeps a running score card of how the various decisions are affecting the total for budget outlays

Tool 2: Evaluation As performance measures per se rarely provide conclusive evidence of performance, program evaluation is also critical. Evaluations are analytic assessments typically addressing the cost-effectiveness or appropriateness of expenditure policies. Countries like Chile have had great success in integrating evaluations into their budgeting systems; there is currently a new wave of international interest in evaluation, with many countries—such as, for example, Canada and Australia—working on building useful evaluation systems. International experience shows that evaluation needs to be in a form valuable to policy-makers without being too resource-consuming. This means that most evaluations should be carried out quickly, focus on drawing conclusions of specific value to managers and budgeters, and should not set unrealistically high “scientific” standards of proof in drawing these conclusions. Tool 3: Performance targets Quantitative statements on outputs and/or outcomes have been an important part of performance management regimes in a number of countries. The most effective example of the target-based approach is the UK Public Service Agreement (PSA) system, under which performance targets have been set as part of the spending review process and have been related to the level of funding provided (Box 9).

29

Box 9. Public Service Agreements in the United Kingdom

The centerpiece of performance management in the U.K. are Public Service Agreements (PSAs), agreed between the Treasury and 18 departments. Introduced in the 1998 spending review (SR), the aim of PSAs was to focus resources on improving outcomes for the public and strengthen accountability for cost effective service delivery. Published alongside departments’ 3-year allocations, PSAs specify the department’s aim, 5 to 10 supporting objectives, and targets with respect to performance against those objectives. PSA targets, currently 110 in total, are defined primarily in terms of outcomes rather than the inputs or processes, to allow departments the flexibility to find the most effective route to delivering the expected results. Examples include targets to reduce mortality rates from cancer for under 75s by 20 percent by 2010 and to halve the number of children in relative poverty by 2010, on the way to eradication by 2020.

Source: http://www.hm-treasury.gov.uk/spending_review/spend_sr04/psa/spend_sr04_psaindex.cfm

International experience indicates that targets need to be set carefully, in order to minimize perverse effects and to avoid damaging rather than enhancing performance. Arbitrary and inappropriate targets with no relation to the level of resources must be avoided. The implementation of a targeting regime presupposes the existence of well-developed performance measurement and costing. Tool 4: Input Flexibility Many countries have given ministries and managers greatly increased discretion to choose the mix of inputs that will deliver services most efficiently, within the context of a move to program-based budgeting and management. This involves the removal of a large part of the detailed control of budgets by economic classification, internal organizational unit, “chapters” and similar, which characterize traditional budgeting systems. Thus, in the United Kingdom, many ministries are free to use the funding provided for each program in any way they wish, subject to only two minimum restrictions: firstly, that the amount of money provided for employing staff cannot be increased and, secondly, that money cannot be shifted away from capital to current expenditure. In France, only the first of these restrictions applies. More generally, greater freedom to let the managers manage has normally been accompanied by tighter requirements to manage within their budgets. Tool 5: Funding based directly on results Many countries have had considerable success in improving the efficiency of service delivery in sectors such as hospitals and universities, without loss of quality, through the adoption of systems in which funding is based on the services delivered to the community. The effectiveness of the output-based “diagnostic related group” funding

30

system for public hospitals has been particularly clearly demonstrated, and this has led to the adoption of this system by a number of countries, including Portugal (1990), Australia (from 1993), Norway (1997), Singapore (1997), the United Kingdom (2004) and Germany (2006).14

C. Enhancing Accountability for Performance

rol t, and a culture of integrity in the civil service, so as to safeguard against

ossible abuses.

ool 1: Information to Parliament

hes

es

f pending ministers and other enquiries frequently inform future policy developments.

iate

Input flexibility needs to be accompanied by a strong managerial accountability for results—that is, the results (outcomes and outputs) delivered by ministries—and staff withinministries—are scrutinized and those concerned are held accountable for their performance. This needs to be accompanied with a change in civil service remuneration arrangements and other relevant employment conditions to create better incentives for performance. Increasing managerial freedom over the choice of inputs also requires a robust regime of internal contand external audip T The provision of performance information on a program basis allows Parliament to play a significant role in holding the government to account for the results achieved by its policies. The focus on programs and the provision of information that readily establisthe cost of those programs and the results achieved enable parliament to assess the cost effectiveness of each program, and thus to hold the government to account, as well as to reflect such information in budgetary decisions. Ministries or associated groups of ministriare typically oversighted by specific parliamentary committees that are able to enquire in depth into their performance. Over time the findings from parliament’s interrogations os Parliament retains its role to approve the government’s budget proposals, but it also has a major role in holding the government to account for the results achieved by thespending proposals. In order to hold the government fully accountable for its budgetary strategy, in a number of countries, either by convention and/or by law, there is an expectationthat the budget will emerge from parliament intact. The alternative is that the government is defeated by a confidence vote. This requirement means that parliament, as in France, is frequently not able to alter the total of spending from that proposed by the government, nor its broad allocation among functions. In some other countries the budget bills that appropr

14 See Chapter IV of Marc Robinson and Jim Brumby, Does Performance Budgeting Work? An Analytical Review of the Empirical Literature, IMF Working Paper WP/05/210 (2005), available at www.imf.org/external/pubs/ft/wp/2005/wp05210.pdf

31

funds for the normal functioning of the state cannot be amended. In any event, numerous detailed amendments are normally prevented. However, in most countries all proposals that require changes in legislation have to be agreed by parliament voting. There is normally also time limit imposed for parliament’s consideration of the budget

ool 2: Performance Auditing

e taken

ntability to

dit tors in

to

as

y include assessments of the performance management systems of the agencies under review.

a T One important element in the results-oriented public management reforms which havplace around the world has been the enhancement of the mandates of supreme audit institutions (SAIs). This has seen them transformed from bodies concerned only with financial accountability into bodies with a crucial role to play in respect of accouthe parliament and the public for performance. There are two different types of “performance auditing” that have emerged and that should be carefully distinguished. The first is the auditing of performance indicators—the approach taken by the UK National AuOffice, which reviews the adequacy of the systems generating performance indicaministries, has particular advantages. The second is what is known as “systemic” performance auditing—that is, reviews of the adequacy of management systems—staffing, organizational structures, information systems and other components of internal control, enable the organization to operate effectively and efficiently, rather than on substantive performance measurement. Australia is a country where systemic performance auditing hbeen developed; performance audits carried out by the Australian National Audit Office routinel

32

IV. A SHORT-TO-MEDIUM TERM BUDGET REFORM STRATEGY FOR ITALY

A. Current Reform Plans and Steps to Date

Recognizing the weaknesses in the existing budget system, the Italian authorities have initiated a number of reforms. These include the introduction of a program-based budget classification; support to parliament in its efforts to reform the budget approval procedures; and an assessment of public spending in selected ministries through spending reviews. Increasing the transparency of the budget: a new program classification A new program budget classification is under preparation to improve transparency. This effort, led by RGS in close coordination with spending ministries and the Department for the Government Program, will facilitate a more transparent presentation of the budget. The revised structure to be submitted to parliament (bilancio decisionale) will significantly reduce the number of UPBs from the current some 1,500 (see Section II), to about 200, each representing a specific program. In a model based on the French reforms, the intention is to identify a number of broad missions aligned with the government’s strategic objectives, and define a number of programs within each of these missions. Programs will be used as the unit of budget appropriation. As a result, Parliament will be in a better position to focus on strategic priorities and decide resource allocation accordingly.15 The challenge will be, however, to ensure that improved transparency is accompanied by greater operational flexibility for managers to deliver results (bilancio gestionale). A number of crucial issues remained unresolved at the time of the mission: • Structure of programs: how these programs will be concretely defined so as to make

them as relevant as possible for government decisions about strategic expenditure priorities, and more generally to ensure that the program budgeting system will work well.