introduction to modern risk management a brief survey by juhani raatikainen university of...

TRANSCRIPT

INTRODUCTION TO MODERN RISK MANAGEMENT

A brief survey

by

Juhani Raatikainen

University of Jyväskylä

Juhani Raatikainen 5.6.2002 2

Introduction• Often risk management is defined as measures

to hedge against such large unexpected losses, that might threaten existence of a bank or a non-financial company. However, we should probably define risk management as a part of usual business decision making, including, of course, hedging against the risks, but also hedging against all other unexpected losses. The target of risk management is to contribute

Juhani Raatikainen 5.6.2002 3

directly to profitability of a bank or a corporation.

• We can loosely define modern risk manage-ment as any quantitative approach applying probabilistic measurement and forecasting methods in decision making with regard of risks. However, when accepting this defini-tion, we have to bear in mind, that the area of risk management is much wider than just the technical methodology, including as its core decision making at the board level.

Juhani Raatikainen 5.6.2002 4

• There are several types of risks which any bank or corporation has to face. Today and tomorrow we are focusing especially on two of them, namely market risk (risk caused by changes in market prices) and credit risk (risk caused by changes in creditworthiness of our debtors or counterparties).

• Origins of the modern quantitative risk management, especially the Value-at-Risk analysis, is in the late 1980’s and late 1990’s, when the first applications were born.

Juhani Raatikainen 5.6.2002 5

• During the 90’s Value-at-Risk (VaR) became the standard tool used by (almost without exceptions) all large or medium sized banks.

• Also since the mid 90’ VaR has won popu-larity among large international (non-financial) companies.

• Today, credit risk analysis, especially credit risk at portfolio level, is the hot topic. The first general (commercial) solutions or approaches have been on the market about five years, however most of the banks are just now building their credit risk analysis systems.

Juhani Raatikainen 5.6.2002 6

• The Basle Accord gives banks (under certain conditions) an opportunity to use their own in-house models to calculate minimum capital requirement instead of a calculation rule given by the Basle Group. This has contributed much to the fast speed with which VaR -models have gain popularity inside the banking community. With the New Basle Accord now changes, the same will happen also with credit risk models.

Juhani Raatikainen 5.6.2002 7

What the “New” Approach Offers

• It forecasts probability of outcomes (instead of ad hoc scenario calculations)

• Measures portfolio effect (gains offered by diversification)

• Makes all different types of risks compa-rable (“integrated risk management”)

• Statistically testable models

Juhani Raatikainen 5.6.2002 8

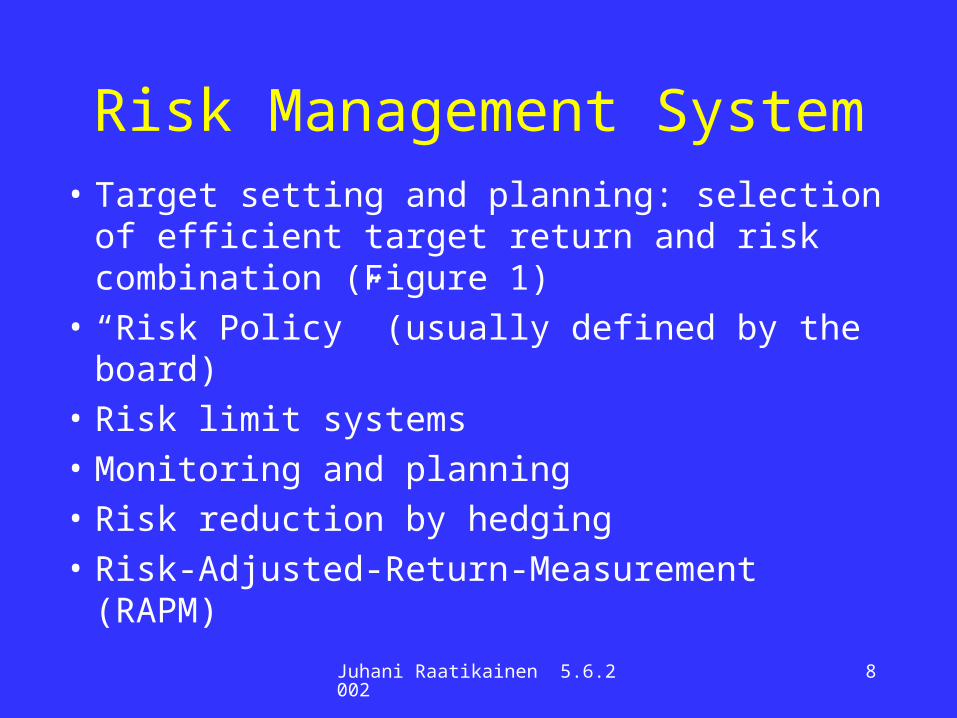

Risk Management System

• Target setting and planning: selection of efficient target return and risk combination (Figure 1)

• “Risk Policy” (usually defined by the board)

• Risk limit systems

• Monitoring and planning

• Risk reduction by hedging

• Risk-Adjusted-Return-Measurement (RAPM)

Juhani Raatikainen 5.6.2002 9

Figure 1. The Efficient Set of Investment Opportunities

Expected risk

Expectedreturn

Juhani Raatikainen 5.6.2002 10

Value-at-Risk

• In Value-at-Risk analysis we are forecasting probability distribution of returns at a given horizon, often with special emphasis on size of the possible losses with given probability.

• Typical type of answer to be sought is what is the maximum one week loss at 95 % confidence level, or what is the minimum loss with 5 % probability.

Juhani Raatikainen 5.6.2002 11

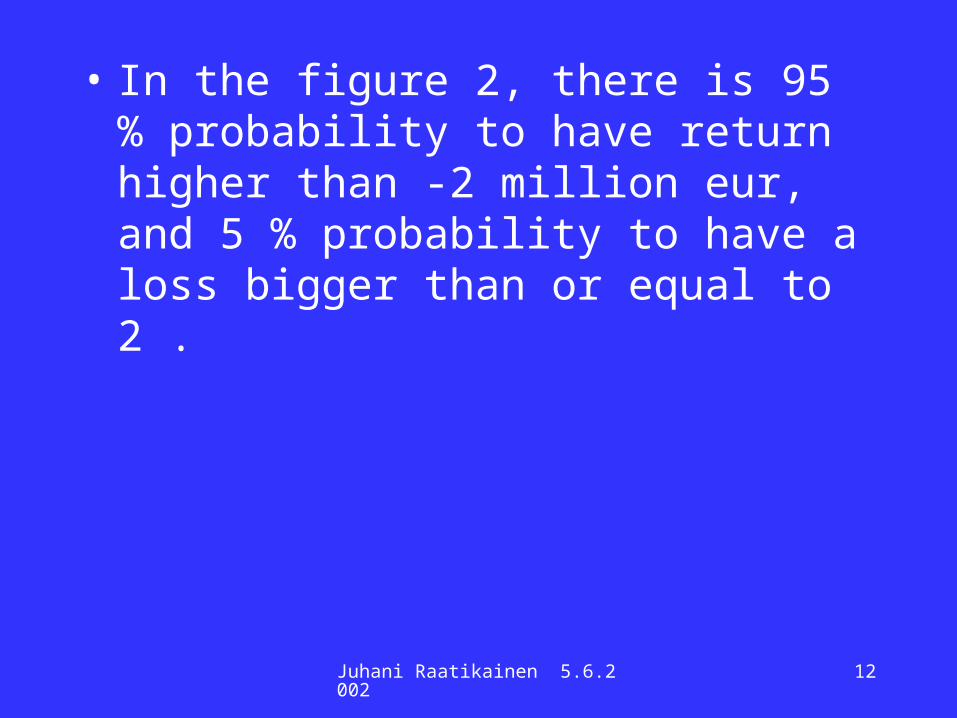

Figure 2. Forecasted Return Distribution

Profit/Loss Millions of EUR

TodennäköisyysProbability

SAS RiskDimensions

Juhani Raatikainen 5.6.2002 12

• In the figure 2, there is 95 % probability to have return higher than -2 million eur, and 5 % probability to have a loss bigger than or equal to 2 .

Juhani Raatikainen 5.6.2002 13

Figure 3. Structure of a Value-at-Risk -model

Simulation

Engine

Market Prices

Statistical

Models

Describing

Behaviour of

the Risk

Factors

Structure of

Portfolio

Instrument

Valuation

VaR -Forecast

Juhani Raatikainen 5.6.2002 14

Traditional VaR Techniques

• Analytical Approach (“Delta-Normal Approach, RiskMetrics Approach)– usually base on the multi-Normal probability

distribution and approximation of pricing functions of the financial instruments

• Historical Simulation– Assumes, that returns are generated by a

unknown probability distribution, which does not change in time

Juhani Raatikainen 5.6.2002 15

• Monte Carlo Simulation– very flexible, can be built on a huge variety of

different types of statistical models– traditionally built on EWMA covariance

estimate or simplest forms of GARCH models, and assumption of multi-normally distributed returns

Juhani Raatikainen 5.6.2002 16

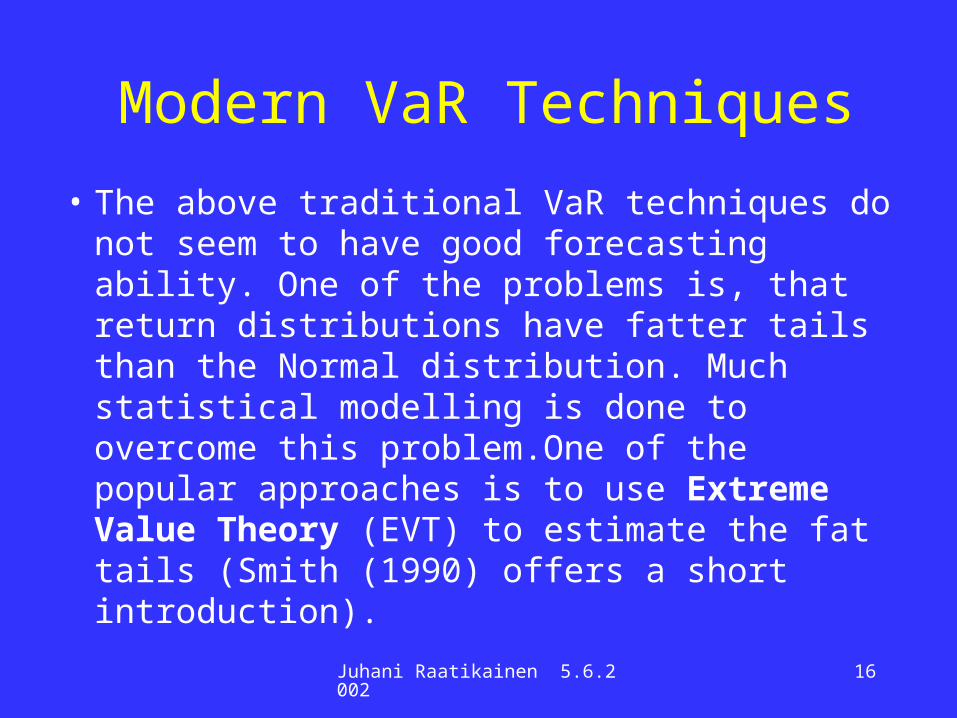

Modern VaR Techniques

• The above traditional VaR techniques do not seem to have good forecasting ability. One of the problems is, that return distributions have fatter tails than the Normal distribution. Much statistical modelling is done to overcome this problem.One of the popular approaches is to use Extreme Value Theory (EVT) to estimate the fat tails (Smith (1990) offers a short introduction).

Juhani Raatikainen 5.6.2002 17

• In standard approaches dependence is measured by a covariance matrix. However, more accurate and flexible approach is offered by Copula functions (copula is a function connecting two or more marginal probability distribution functions to a multidimensional probability distribution function).

• It is interesting to note, that use of EVT and Copula functions is very close to models applied in medicine, engineering, physics, and geology.

Juhani Raatikainen 5.6.2002 18

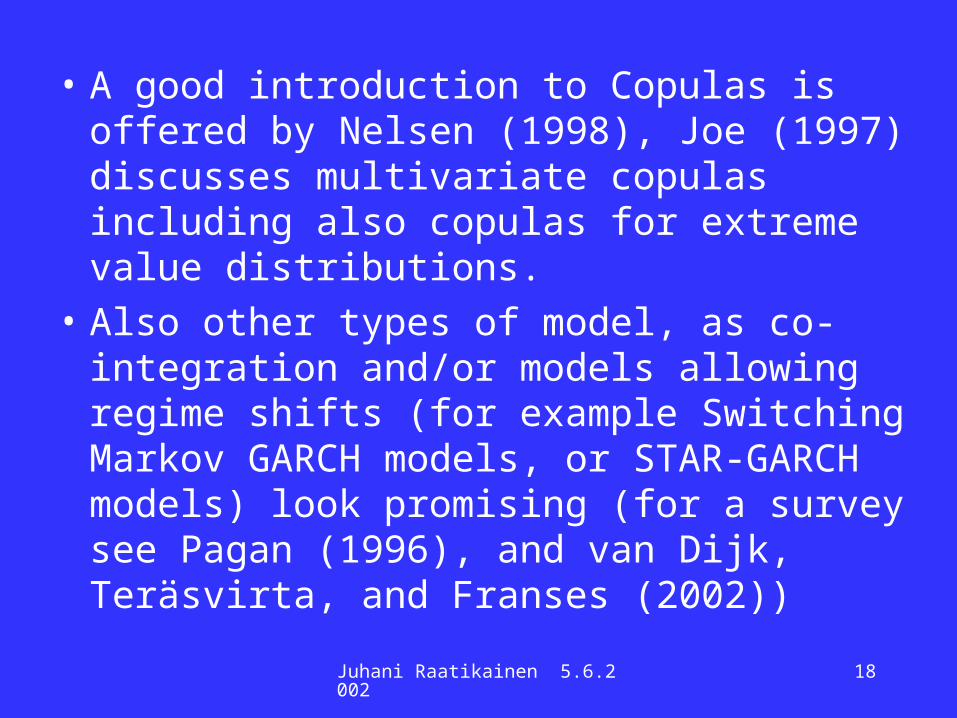

• A good introduction to Copulas is offered by Nelsen (1998), Joe (1997) discusses multivariate copulas including also copulas for extreme value distributions.

• Also other types of model, as co-integration and/or models allowing regime shifts (for example Switching Markov GARCH models, or STAR-GARCH models) look promising (for a survey see Pagan (1996), and van Dijk, Teräsvirta, and Franses (2002))

Juhani Raatikainen 5.6.2002 19

• Later today Mr. Esa Vilhonen (OKO Bank) will present us an example of a very good banking solution (both VaR and credit risk). One interesting point to notice is that the OKO Bank is one of the first in the world to use Copula functions in a business solution.

Juhani Raatikainen 5.6.2002 20

Corporate Risk Management

• Value-at-Risk approach applied to corporations differ from the above “banking models”, because– forecasting horizon is longer– nature of the exposure items differ: the exposure

of the included business items have to be forecas-ted (for example sales volume)

Juhani Raatikainen 5.6.2002 21

– The target exposure is different• Cash-Flow-at-Risk (CFaR) (value of

business)• Profit-at-Risk (profitability)• Earning-at-Risk (EaR), (earning of a

company)

• Industries using Value-at-Risk– Pulp and Paper production– Energy companies, and especially companies

on the electricity market

Juhani Raatikainen 5.6.2002 22

– Aviation– Metal industry– Large international high-tech companies

• After a couple of minutes Mr. Jean-Marc Servat (Nokia Corporation) will discuss more thoroughly Corporate Risk Management while presenting the Nokia Risk Management solution.

Juhani Raatikainen 5.6.2002 23

Credit Risk Management

• Focus of credit (or counterparty) risk manage-ment is portfolio level risk. A bank can not run a profitable business without having also clients, who will default. But, if a bank is able to forecast total amount of the losses (portfolio level risk) and price that risk in an appropriate way, it will have a flourishing business.

Juhani Raatikainen 5.6.2002 24

• Market risk is very often incorporated into credit risk: the question to be asked is what is probability of a default, and in that case what is market value of the instrument

• Credit risk analysis consists of two parts– “micro analysis” (for example

“creditworthiness of a counterparty)– portfolio level analysis

Juhani Raatikainen 5.6.2002 25

“Micro Analysis”

• Use of statistical techniques or neural networks to estimate– credit quality of a counterparty– recovery rate– conditional or unconditional credit migration

probabilities

• Key concept is the Loss Given Default: the amount of loss when value of the collateral is subtracted and recovery is taken into account

Juhani Raatikainen 5.6.2002 26

Portfolio Level Analysis

• May be based on – unconditional credit migration probabilities and

correlations (CreditMetrics)– conditional credit migration probabilities and

correlations, key dependece is between portfolio credit risk and macroeconomic fluctuations

– both the above “micro analysis” and portfolio-level analysis may be based on option theory (this is the traditional academic approach)

Juhani Raatikainen 5.6.2002 27

Credit Risk Forecast

SAS RiskDimensionsLoss Millions of EUR

TodennäköisyysProbability

Juhani Raatikainen 5.6.2002 28

• The presentation by Ph.D. Esa Jokivuolle (Bank of Finland) tomorrow at 10.00 o’clock will discuss credit risk measurement especially with regard of the new Basel Accord.

Juhani Raatikainen 5.6.2002 29

Future Trends

• The greatest change during the 90’ has been in business philosophy: financial commu-nity has adopted systematic “technical” (portfolio) approach to business and risk management (applied also in pricing of risk)

• Use of modern risk management concepts in business decision making continue to increase

Juhani Raatikainen 5.6.2002 30

• One of the great challenges is to develop more accurate forecasting models both for market risk and credit risk.

• From technical point of view, use of non-Gaussian statistical distributions and “new” dependence measures (Copulas) will be the direction of future research work.

• The presentation by Ph.D. Esa Mangeloja University of Jyväskylä) tomorrow at 12.30 o’clock will discuss dependence between the Nordic Stock exchanges.

Juhani Raatikainen 5.6.2002 31

• My own presentation tomorrow will discuss how to test forecasting accuracy of VaR models using as an example test results of some popular models.

Juhani Raatikainen 5.6.2002 32

ReferencesJoe, H. (1997) Multivariate Models and Dependence Concepts, Chapman & Hall, London.

Nelsen, R. (1998) An Introduction to Copulas, Lecture Notes in Statistics, Springer, New York.

Pagan, A. (1996) The Econometrics of Financial Markets, Journal of Empirical Finance, 3: 15 - 102.

Juhani Raatikainen 5.6.2002 33

Smith, R. (1990) Extreme Value Theory, in Handbook of Applicable Mathematics, (ed. W. Lederman), vol 7, Wiley, Chichester, 437 - 472.

Van Dijk, D., Teräsvirta, T. and Franses, H. (2002) Smooth Transition Autoregressive Models - A Survey of Recent Developments, Econometric Reviews, vol. 21, 1 - 47.