investigating perceptions concerning the adoption of

TRANSCRIPT

Investigating Perceptions Concerning the Adoption of

International Financial Reporting Standards (IFRS)

Among College Students

by

Hyun-Pyo Kim, M.S.

A THESIS

In

INTERDISCIPLINARY STUDIES

Submitted to the Graduate Faculty

of Texas Tech University in

Partial Fulfillment of

the Requirements for

the Degree of

MASTER OF SCIENCE

Approved

Dr. Young-Kyu Moh

Chair of Committee

Dr. Jessica Yuan

Dr. Dakshina G. De Silva

Peggy Gordon Miller

Dean of the Graduate School

May, 2011

Copyright 2011, Hyun-Pyo Kim

Texas Tech University, Hyun-Pyo Kim, May 2011

ii

ACKNOWLEDGMENTS

This research would not have been possible without the help of several

individuals who in one way or another contributed and extended their valuable

assistance in the preparation and completion of this study. I really appreciated every

kind of assistance they gave to me.

First and foremost, my greatest gratitude to Dr. Young-Kyu Moh, whose

sincerity and support I will never forget. He helped me to make my thesis accurate

with his passion and great effort. I also offer my sincere appreciation to my committee

members, Dr. Jessica Yuan and Dr. Dakshina G. De-Silva. I appreciate their kind

concern and consideration regarding my academic requirements. I would also like to

say how much I admire Dr. Wendell Aycock, Dr Ben Goh and Dr. Deborah Fowler.

They have always supported and trusted me. I could not have finished this great thesis

without their help. I would also like to acknowledge Dr. Do-Jin Jung who was my

master’s advisor when I was a graduate student in South Korea.

I would like to express my gratitude to my good friend and English teacher,

Barbara Werden, for her help and consideration. I could not have finished this thesis

without her assistance. It has been my honor to meet you here in Lubbock, Texas. I

also want to thank many other friends who contributed to the success of this study. To

my best friends: Dong-Soo Lee, Hyuk-Ki Lee, Han-Mo Oh, Hyo-Jin Kim, Hyun-Oh

Kang, Sang-Mook Lee, Joo Ahn, Yong-Ho Cho, Hyun-Woo Joung and Eun-Kyung

Choi, thank you for your contributions to this study.

Texas Tech University, Hyun-Pyo Kim, May 2011

iii

Finally, I want to thank my parents: Jong-Ku Kim and Mal-Yeon Lee, and

family: Bo-Hyang Kim, Tae-Bum Ryu, Hyun-Woo Ryu and Hyun-Oh Ryu. Without

their financial and emotional support, this thesis would have been impossible to finish.

I love them so much, and you all “make my life.” I want to dedicate this thesis to them.

Thank you, again.

Texas Tech University, Hyun-Pyo Kim, May 2011

iv

TABLE OF CONTENTS

ACKNOWLEDGMENTS ............................................................................................. ii

ABSTRACT .................................................................................................................. vi

LIST OF TABLES ...................................................................................................... viii

LIST OF FIGURES ...................................................................................................... ix

I. INTRODUCTION ...................................................................................................... 1

II. LITERATURE REVIEW ........................................................................................ 15

Part 1. A comparison between the IFRS and a country’s own GAAP ............. 15

Part 2. Adopting the IFRS voluntarily and mandatorily .................................. 18

Part 3. Education system for accounting .......................................................... 18

Research questions ........................................................................................... 20

III. METHODOLOGY ................................................................................................. 22

Data and sample ............................................................................................... 22

Data analysis .................................................................................................... 23

Definition of variables and research model ..................................................... 24

IV. RESULTS AND DISCUSSION ............................................................................ 28

Descriptive analysis ......................................................................................... 28

T-test and ANOVA (Analysis of Variance) ..................................................... 31

Correlation........................................................................................................ 34

Texas Tech University, Hyun-Pyo Kim, May 2011

v

Regression ........................................................................................................ 37

Additional analyses with business major students ........................................... 39

Descriptive analysis ......................................................................................... 39

T-test and ANOVA (Analysis of Variance) ..................................................... 42

Correlation........................................................................................................ 43

Regression ........................................................................................................ 43

V. CONCLUSIONS AND LIMITATIONS ................................................................ 46

REFERENCES ............................................................................................................. 49

APPENDICES

A. QUESTIONNAIRE ................................................................................................. 52

B. IRB APPROVAL LETTER .................................................................................... 54

Texas Tech University, Hyun-Pyo Kim, May 2011

vi

ABSTRACT

As capital markets become increasingly global, many investors have a great

interest in international investment opportunities. Also, many countries use dissimilar

standards when they create financial statements for their stakeholders. In the United

States, the SEC (Securities and Exchange Commission) has long expressed its support

for a single set of high-quality global accounting standards as an important means of

enhancing comparability and unification. IFRS as a single set of global accounting

standards has the potential to best provide the common platform on which companies

can report, and stakeholders can compare, corporate financial information. The goal

with IFRS is to make international comparisons as easy as possible.

Although the standards have a critical impact on capital markets, students and

investors know very little about this standard. Therefore, by investigating the

perception of the IFRS among college students, this study could determine the status

of preparation for the standards and help colleges and universities with decisions

regarding offering classes about these standards. The primary objective of this study is

to investigate perceptions and knowledge concerning the adoption of International

Financial Reporting Standards (IFRS) among college students.

The findings are as follows; first, I found there was a difference in knowledge

about IFRS between male and female respondents. While it is difficult to generalize

these results to all college or university student populations, universities or colleges

should consider evaluating students to determine their level of knowledge about IFRS

Texas Tech University, Hyun-Pyo Kim, May 2011

vii

and then have provisions in place for extra classes or assignments in order to raise the

extent of knowledge of IFRS for any group of students (male and female) who show

deficiencies in basic knowledge of these standards. Second, there were no differences

in knowledge about IFRS for each age group and each school year among respondents.

Third, I found a difference in knowledge about IFRS between students majoring in

business and students who were non-business majors. This implies that in this

population of respondents business major students are taking more classes about

financial events such as the adoption of IFRS in U.S. than are non-business major

students. Therefore, business major students have more knowledge of IFRS than do

non-business major students. Fourth, I found a correlation between the perception

about evaluating the positive effect of IFRS on capital markets and the intention to

take classes about IFRS. This means that students who believe there will be a positive

effect on capital markets by the adoption of IFRS will take classes concerning IFRS.

Also, these students will take more classes in order to analyze their perceptions about

the IFRS. Finally, the results predicted that students who showed a great interest in

IFRS are more likely to take these courses if colleges or universities offer classes.

These results mean that interest is a very critical determinant for taking classes

concerning IFRS among college students. The more students have an interest about

IFRS, the more they will take classes. There are also similar results shown in the

additional analyses section pertaining to business major respondents.

Texas Tech University, Hyun-Pyo Kim, May 2011

viii

LIST OF TABLES

1. Frequencies of the respondents (N=246) ................................................... 29

2. Descriptive statistics (N=246) .................................................................... 30

3. t-test result for knowledge of IFRS ........................................................... 32

4. Results of ANOVA demographics and knowledge of IFRS ..................... 33

5. t-test result for knowledge of IFRS ........................................................... 34

6. Correlation of the respondents within business majors............................. 35

7. Correlation of the respondents within non-business majors ..................... 36

8. Regression analysis among variables ........................................................ 39

9. Frequencies for the respondents with business majors ............................ 40

10. Descriptive statistics with business majors .............................................. 41

11. t-test result for knowledge of IFRS with business majors ....................... 42

12. Results of ANOVA and knowledge of IFRS for business majors ........... 43

13. Regression analysis among variables for business majors ....................... 45

Texas Tech University, Hyun-Pyo Kim, May 2011

ix

LIST OF FIGURES

1. SEC (Securities and Exchange Commission) Time line ............................................ 7

2. The Global Move Towards IFRS ............................................................................. 16

Texas Tech University, Hyun-Pyo Kim, May 2011

1

CHAPTER I

INTRODUCTION

As capital markets become increasingly global, many investors have a great

interest in international investment opportunities. The world of investing is fascinating

and complex and investors in the United States could gain economically from an

enhanced ability to compare financial statements such as balance sheets or income

statements between U.S. companies using the U.S. GAAP (Generally Accepted

Accounting Principle) and non-U.S. companies using different accounting principles

such as IFRS (International Financial Reporting Standards) or their own country’s

GAAP. The fact is, many countries use dissimilar standards when they create financial

statements for their stakeholders.

In the United States, the SEC 1 (Securities and Exchange Commission) is a

federal agency which holds primary responsibility for enforcing the federal securities

laws and regulating the securities industry, the nation’s stock and options exchanges,

and other electronic securities markets. The primary reason for creating the SEC was

to regulate the stock market and prevent corporate abuses relating to the offering and

sale of securities and corporate reporting. The mission of the U.S. SEC (Securities and

Exchange Commission) is to protect investors, maintain fair, orderly, and efficient

markets, and facilitate capital formation. The SEC has long expressed its support for a

1. The organization was formed by the United States Congress in June 1934. There are five departments

in the SEC. 1) Corporation Finance, 2) Trading and Markets, 3) Investment Management, 4)

Enforcement, and 5) Risk, Strategy, and Financial Innovation.

Texas Tech University, Hyun-Pyo Kim, May 2011

2

single set of high-quality global accounting standards as an important means of

enhancing comparability and unification.

IFRS as a single set of global accounting standards has the potential to best

provide the common platform on which companies can report, and stakeholders can

compare, corporate financial information. It is a set of international accounting

standards stating how particular types of transactions and other events should be

reported in financial statements such as balance sheets. These standards are issued by

the IASB (International Accounting Standards Board). The goal with IFRS is to make

international comparisons as easy as possible. Currently, this is difficult because, to a

large extent, each country has its own set of rules. For example, U.S. GAAP is

different from the Canadian GAAP (http://www.investopedia.com/terms/i/ifrs.asp,

2010).

According to proponents of International Financial Reporting Standards

(IFRS), publicly traded companies must apply a single set of high quality accounting

standards in the preparation of their consolidated financial statements, in order to

contribute to improved functioning capital markets (Quigley, 2007). Also, IFRS has

the potential to facilitate cross-border comparability, increase reporting transparency,

decrease information costs, reduce information asymmetry and thereby increase the

liquidity, competition, and efficiency of markets (Ball, 2006). As a result of examining

the economic consequences of mandatory IFRS reporting around the world, it was

shown that market liquidity increases around the time of the introduction of IFRS.

Also, firms’ cost of capital decreased and equity valuations which were measured with

Texas Tech University, Hyun-Pyo Kim, May 2011

3

Tobin’s Q2 increased (Daske, Hail, Leuz, & Verdi, 2008). Accordingly, because of the

importance of IFRS in the capital market, the SEC announced in 2005 plans for a

roadmap towards requiring the use of IFRS as issued by the IASB (International

Accounting Standards Board) by U.S. issuers as part of its consideration of the role a

single set of high-quality accounting standards plays in investor protection and the

efficiency and effectiveness of capital formation and allocation in the U.S.

Up until now, use of the IFRS has been developing in the capital markets of

the U.S. There are three phases in this evolution. Some of which have been completed.

The following description of the three phases is documented ("US GAAP vs. IFRS,"

2009).

1. Phase I — 2001 and prior

1973: International Accounting Standards Committee (IASC) formed. The

IASC was founded to formulate and publish International Accounting

Standards (IAS) that would improve financial reporting and that could be

accepted worldwide.

1994: IOSCO (International Organization of Securities Commissions)

completed its review of current IASC standards and communicated its findings

to the IASC. The review identified areas that required improvement before

IOSCO could consider recommending IAS for use in cross-border listings and

offerings.

2 . Tobin’s q was developed by James Tobin (Tobin, 1969) as the ratio between the market value and

replacement value of the same physical asset. If the market value reflected solely the recorded assets of

a company, Tobin’s q would be 1.0.

Texas Tech University, Hyun-Pyo Kim, May 2011

4

1995: IASC developed its Core Standards Work Program. IOSCO’s Technical

Committee agreed that the Work Program would result, upon successful

completion, in IAS comprising a comprehensive core set of standards. The

European Commission (EC) supported this agreement between IASC and

IOSCO and associated itself with the work of the IASC in order to foster a

broader international harmonization of accounting standards.

1999: IASC Board approved a restructuring that resulted in the current

International Accounting Standards Board (IASB). The newly constituted

IASB structure comprises: 1) the IASC Foundation, an independent

organization with 22 trustees who appoint the IASB members, exercise

oversight, and raise the funds needed; 2) the IASB (Board) which has 12 full-

time, independent board members and two part-time board members with sole

responsibility for setting accounting standards; 3) the Standards Advisory

Council; ,and 4) the International Financial Reporting Interpretations

Committee (IFRIC) that replaced the SIC (Standing Interpretations Committee)

and was mandated with interpreting existing IAS and IFRS standards, and

providing timely guidance on matters not addressed by current standards.

2000: IOSCO recommended that multinational issuers be allowed to use IAS

in cross-border offerings and listings.

April 2001: IASB assumed standard-setting responsibility from the IASC. The

IASB met with representatives from eight national standard-setting bodies to

Texas Tech University, Hyun-Pyo Kim, May 2011

5

begin coordinating agendas and discussing convergence and adopted the

existing IAS standards and SIC Interpretations.

February 2002: IFRIC assumed responsibility for interpretation of IFRS.

2. Phase II — 2002 to 2005

July 2002: EC (European Commission is the executive body of the European

Union) required EU-listed companies to prepare their consolidated financial

statements in accordance with IFRS as endorsed by the EC, generally from

2005 onward. This was a critically important milestone that acted as a primary

driver behind the expanded use of IFRS.

September 2002: Norwalk Agreement executed between the FASB and the

IASB.

December 2004: EC issued its Transparency Directive. This directive would

require non-EU companies with listings on an EU exchange to use IFRS unless

the Committee of European Securities Regulators (CESR) determined that the

national GAAP was “equivalent” to IFRS. Although CESR advised in 2005

that the U.S. GAAP was “equivalent” subject to certain additional disclosure

requirements, the final decision as to U.S. GAAP equivalency, and what

additional disclosures, if any, will be required, has not yet been reached.

April 2005: SEC published the “Roadmap.” An article published by then SEC

Chief Accountant discussed the possible elimination of the U.S. GAAP

reconciliation for foreign, private issuers that use IFRS. This Roadmap laid out

Texas Tech University, Hyun-Pyo Kim, May 2011

6

a series of milestones, which if achieved, would result in the elimination of the

U.S. GAAP reconciliation by 2009, if not sooner.

3. Phase III — 2006 to present

February 2006: The FASB and IASB published a Memorandum of

Understanding (MOU). The MOU reaffirmed the Boards’ shared objective to

develop high quality, common accounting standards for use in the world’s

capital markets and further elaborated on the Norwalk Agreement. According

to the agreement, the Boards would proceed along two tracks for convergence:

1) a series of short-term standard setting projects designed to eliminate major

differences in focused areas, and 2) the development of new common

standards.

November 2007: the SEC eliminated the U.S. GAAP reconciliation for foreign,

private issuers. After hosting a roundtable discussion in March 2007 to discuss

the effects that the acceptance of IFRS would have on investors, issuers, and

capital raising in U.S. capital markets and issuing a summary of its

observations regarding foreign, private issuers that adopted IFRS for the first

time in 2005, the SEC determined that the milestones on its 2005 Roadmap

had been sufficiently met so as to eliminate the reconciliation requirement.

Mid-2007, continuing into 2008: the SEC explored the future use of IFRS by

U.S. companies. Also in August 2007, the SEC issued a Concept Release

asking the public to comment on the possible use of IFRS by U.S. domestic

Texas Tech University, Hyun-Pyo Kim, May 2011

7

registrants. In December 2007, and August 2008, the SEC held three additional

roundtables on the topic of IFRS, with the roundtables focusing on the

potential use of IFRS for U.S. issuers. Further, in August 2008, the SEC

approved for public issuance an updated Roadmap which anticipated

mandatory reporting under IFRS beginning in 2014, 2015 or 2016, depending

on the size of the company.

Looking ahead: The future remains uncertain, but momentum continues to

build for a single set of high quality, global standards. The possible use of

IFRS by U.S. domestic registrants is a topic that remains active on the SEC’s

agenda. The updated proposed Roadmap identifies certain milestones to be

considered in determining whether reporting under IFRS should be mandated

for U.S. companies, and calls for future SEC action in 2011 to make that

assessment.

Figure 1: SEC (Securities and Exchange Commission) Time line

Texas Tech University, Hyun-Pyo Kim, May 2011

8

The roadmap of adoption of IFRS first addresses the basis for considering the

mandatory use of IFRS by U.S. issuers. It then sets forth seven milestones which, if

achieved, could lead to the use of IFRS by U.S. issuers in their filings with the SEC.

The SEC will judge progress on these milestones as a prerequisite for moving forward

with a mandate for IFRS adoption. In 2011, the SEC will determine whether to

proceed with rulemaking to require that U.S. issuers use IFRS beginning in 2014, if it

is in the public interest and for the protection of investors. The seven milestones are as

follows (Henson, 2011).

1. Improving specific accounting standards

2. Improving the structure and funding of the IASB

3. Facilitating the use of interactive data (XBRL) under IFRS

4. Updating the education and licensing of U.S. accountants

5. Evaluating the early adoption experiences of a limited group of companies

6. Timing of future rulemaking

7. Sequencing of companies required to use IFRS

The first four milestones are conditions precedent to the adoption of IFRS in

the United States. The remaining three milestones pertain to the experience of

adopting IFRS and how IFRS should be adopted in the United States.

Milestone 1: Improving specific accounting standards

The FASB (Financial Accounting Standards Board) and the IASB are

continuing their progress on accounting standard convergence. They hope to complete

Texas Tech University, Hyun-Pyo Kim, May 2011

9

their convergence plan by the end of 2011. Their objective is a set of common, high

quality reporting standards for companies around the world. The FASB and IASB

have made significant progress on some important standards, but still have work to do

in order to reach their goal. The FASB and IASB are working hard on convergence

and are trying to complete their work by the end of 2011 at which time somewhat of a

moratorium on modifying standards is expected in order to give companies a chance to

transition to IFRS with a stable set of accounting standards.

Milestone 2: Improving the structure and funding of the IASB

The second milestone involves progress on improving the structure and

funding of the IASB. The International Accounting Standards Board (IASB) is trying

to improve its structure and funding. To date they have made progress, but still need to

continue to work on establishing a structure and funding an approach that global

securities regulators will support. The most significant area left to be addressed is

funding.

Milestone 3: Facilitating the use of interactive data (XBRL) under IFRS

The International Accounting Standards Committee Foundation (IASC

Foundation) released the 2009 IFRS Taxonomy for comment. Development and

approval of an IFRS Taxonomy is essential for being able to utilize XBRL for IFRS

reporting. Taxonomies describe in detail the contextual information related to data

tags used to describe and report business information. XBRL is an open standard that

is used to store and transport business information. It is clear that the IASC

Texas Tech University, Hyun-Pyo Kim, May 2011

10

Foundation is trying to facilitate the use of XBRL for IFRS reporting. The IASC

foundation is beginning to enable XBRL use for IFRS reporting.

Milestone 4: Updating the education and licensing of U.S. accountants

University professors are beginning to analyze global accounting convergence

and the potential adoption of IFRS by the United States. A few IFRS textbooks are

also becoming available including: IFRS 2008: Interpretation and Application of

International Accounting and Financial Reporting Standards 2008 by Barry J. Epstein

and Eva K. Jermakowicz and Applying International Accounting Standards by Keith

Alfredson, Ken Leo, Ruth Picker, Paul Pacter and Jennie Radford. Universities are

beginning to prepare for inclusion of IFRS in their accounting curricula. Students are

also beginning to realize that they will need to learn more about IFRS because it will

be important in the future, even though it is expected that this will add significantly to

their required courses.

In February 2009, a major CPA firm announced the awarding of $700,000 in

grants to 26 colleges and universities to accelerate the preparedness of U.S. accounting

students for eventual adoption of IFRS. Major CPA firms are also making a significant

amount of information on IFRS available in the form of online materials and free

webcasts.

Milestone 5: Evaluating the early adoption experiences of a limited group of

companies

Texas Tech University, Hyun-Pyo Kim, May 2011

11

The fifth IFRS milestone involved the SEC’s evaluation of the IFRS adoption

experience of companies that elected early adoption of the IFRS. The SEC established

rules that would allow some companies to adopt IFRS as early as fiscal years ending

after December 15, 2009. Early adoption required that a company met both of the

following criteria:

1. IFRS would have to be the most-often-used set of standards by the 20 largest

companies in an entity’s industry

2. The entity must be among the largest 20 public companies by market

capitalization in its industry. Industries are defined by a company’s two digit

SIC code.

Qualifying companies were permitted to file financial statements based on

IFRS for fiscal years ending after December 15, 2009. Whether the early adoption

experience was positive or negative, might influence the decision to mandate the use

of IFRS for U.S. companies. If a company chose early adoption of the IFRS, the

commissioner anticipated that they might have needed to return to the U.S. GAAP if

necessary, an obvious disincentive to early adoption.

Milestone 6: Timing of future rulemaking

The SEC decision on when to migrate to IFRS has been the topic of much

speculation. The SEC was a strong advocate of moving to IFRS, and their draft

Roadmap envisioned migrating to IFRS beginning in 2014 with some companies

eligible for early adoption for the fiscal period ending after December 15, 2009.

Texas Tech University, Hyun-Pyo Kim, May 2011

12

When the SEC issued its draft Roadmap for public comment, they based the

transition to IFRS on seven milestones. The SEC is analyzing the results of early

adopter experiences. A favorable outcome on early adopter experiences would be a

harbinger for earlier (“on-time”2014 adoption); however, adoption of IFRS and

unfavorable experiences could point toward a delay in adoption.

There are risks to both adopting IFRS and to not adopting IFRS. The risks of

adopting IFRS are relatively intuitive such as cost of adoption, adoption error or

omission risk, risk of limited or no ROI (Return on Investment) on adoption, lack of

expertise risk, and so on. The risks for not adopting IFRS include: lack of access to

global capital markets, lack of comparability with international competitors, and/or

lack of cost reduction through international efficiencies.

Most people agree that having a single global accounting and reporting

standard would be a very good thing. With about 120 countries using IFRS and one

country using U.S. GAAP, it is clear that the only one way a global accounting

standard will be achieved is if the U.S. adopts IFRS. By 2011, the U.S will be the only

major nation in the world not using IFRS. It seems clear that U.S. adoption of IFRS is

ultimately inevitable.

Milestone 7: Sequencing of companies required to use IFRS

The eventual adoption of IFRS in the United States is certain. What is not

certain is when IFRS will be adopted here and whether IFRS adoption will be

sequenced as proposed in the SEC’s preliminary IFRS Roadmap. It would surprise no

Texas Tech University, Hyun-Pyo Kim, May 2011

13

one in the finance industry if the United States elected to defer mandatory adoption for

some additional years due to current economic pressures. This seventh roadmap

milestone involves the SEC’s decision on whether, when, and how to sequence the

adoption of IFRS.

The SEC proposed its IFRS Roadmap on November 14, 2008 and the

comment period for the proposed Roadmap ended April 20, 2009. Under the proposed

Roadmap, the SEC envisioned a sequenced approach to adoption according to which a

limited number of U.S. filers would be permitted, at their option, to adopt IFRS early

beginning with fiscal periods ending after December 15, 2009. The mandatory

adoption of IFRS was expected to follow with large accelerated filers implementing

IFRS for fiscal years ending on or after December 15, 2014, accelerated filers

implementing IFRS for years ending on or after December 15, 2015, and non-

accelerated filers implementing IFRS for years ending on or after December 15, 2016.

This timetable is thought to allow filers time to implement IFRS books, records and

internal accounting controls for the fiscal year end reporting periods from 2012 to

2014 for large accelerated filers, 2013 to 2015 for accelerated filers, and 2014 to 2016

for non-accelerated filers.

This staged approach is based on the premise that larger SEC filers would be

better able to allocate resources to the IFRS transition more quickly than smaller filers.

By staging or sequencing IFRS adoption, the SEC would also allow later adopters the

ability to learn from the adoption experiences of larger filers. In addition, a staged

transition may also help manage resource demands on consultants and other market

Texas Tech University, Hyun-Pyo Kim, May 2011

14

participants. While sequenced adoption of IFRS permits some transition cost

avoidance, sequencing would result in non-comparability of financial information due

to application of the IFRS transition provisions at differing dates. Staging the

transition would temporarily create a “two GAAP” system in the United States for at

least three years. Further, it would require investors to be familiar with IFRS and U.S.

GAAP as well as how each affects the financial statements of target companies when

comparing investment alternatives.

As you can see in Milestone 4, education about the IFRS is very important

now, and in the future, at college or universities. Many researchers are evaluating the

global accounting convergence, the adoption of IFRS, and the importance of offering

classes in the U.S. Also, some students have realized the importance of IFRS on their

own. Although the standards have a critical impact on capital market, students and

investors know very little about this standard. Therefore, by investigating the

perception of the IFRS among college students, this study could determine the status

of preparation for the standards and help colleges and universities with decisions

regarding offering classes about these standards. The primary objective of this study is

to investigate perceptions and knowledge concerning the adoption of International

Financial Reporting Standards (IFRS) among college students.

The remainder of the thesis is organized as follows. Chapter II reviews the

literature. Chapter III describes the research design. Chapter IV presents the results,

and Chapter V states the conclusion including limitations.

Texas Tech University, Hyun-Pyo Kim, May 2011

15

CHAPTER II

LITERATURE REVIEW

There are many empirical studies about the IFRS, focusing mainly on Europe,

because these standards have been mandatory since 2005 in the European Union. To

organize my review of the literature, I categorized the empirical studies into three

parts: 1) a comparison between the IFRS and each country’s own GAAP; 2) adoption

of the IFRS voluntarily and mandatorily; and 3) research on the education system for

accounting after the adoption of IFRS.

Part 1. A comparison between the IFRS and a country’s own GAAP

Some countries such as Australia, South Africa, and the EU (European Union)

were mandated to use the IFRS for traded companies in their capital markets after

2005. South Korea will use the IFRS beginning in 2011. The United States also has a

timeline for adoption of the IFRS for companies trading in the U.S. The rate of use for

the IFRS is increasing in many countries as shown in Figure 2: The Global Move

Towards IFRS (Deloitte, 2008).

Texas Tech University, Hyun-Pyo Kim, May 2011

16

Figure 2: The Global Move Towards IFRS

By investigating whether and how managerial incentives influence the

decision to elect optional exemptions when first adopting International Financial

Reporting Standards (IFRS) in France, there were three major findings: 1) managerial

incentives influenced the decision to strategically elect one or more optional

exemptions; 2) mandatory equity adjustments were more valued than in the French

GAAP; and 3) the first-time adoption of IFRS by French firms was perceived as a

signal of an increase in the quality of each firm’s financial statements (Comier,

Demaria, Lapointe-Antunes, & Teller, 2009). For the economic and policy factors

related to the potential adoption of IFRS in the U.S., there were three conclusions in

this research showing that the decision to adopt IFRS mainly involved a cost-benefit

tradeoff that were: 1) recurring, albeit modest, comparability benefits for investors; 2)

recurring future cost savings that will largely accrue to multinational companies, and 3)

one-time transition costs borne by all firms and the U.S. economy as a whole (Hail,

Leuz, & Wysocki, 2009).

Texas Tech University, Hyun-Pyo Kim, May 2011

17

Daske, et al., determined that the decision to adopt IFRS was a good strategic

method to increase a company’s overall transparency (Daske, et al., 2008). Examining

application of International Accounting Standards and accounting quality showed that

firms applying IAS from 21 countries generally evidenced less earnings management,

more timely loss recognition, and more value relevance of accounting amounts than do

a matched sample of firms applying non-U.S. domestic standards, and showed an

improvement in the accounting quality between the pre- and post-adoption periods

(Barth, Landsman, & Lang, 2007).

In addition to this research, Flynn outlined the advantages to the United States

of changing from its own GAAP to IFRS: 1) the use of IFRS as the single, common

language of financial reporting to make true comparisons; 2) the IFRS require a strong

international standards body to assure consistency, and 3) this change also offers the

potential for reduced complexity by offering a high-quality global set of standards

(Flynn, 2008).

However, changing from GAAP to IFRS also has potential disadvantages.

Companies without operations in other countries have no incentive to follow the

standards. Also, many countries claiming to convert to IFRS never get to full

compliance, and the IFRS could lead to incompatibility (Olson, 2008). Another

disadvantage relates to financial statements. Financial statements prior to conversion

will need to be maintained on both standards, GAAP and IFRS, for at least two years

in order to meet the requirement that financial statements contain three years of

financial data.

Texas Tech University, Hyun-Pyo Kim, May 2011

18

The adoption of IFRS among countries and companies creates different results.

These results are due to different entities’ situations such as their economic status and

their capital markets. Also, all countries have differing timetables and preparations for

adoption of IFRS.

Part 2. Adopting the IFRS voluntarily and mandatorily

Adoption of the IFRS separates into two possibilities: voluntary adoption or

mandatory adoption. Based on a company’s circumstances, it might choose either

voluntary or mandatory adoption of the new standards. By examining the determinants

and consequences of voluntary adoption of non-local accounting principles (non-local

GAAP) by firms listed in the European Union, research by Cuijpers and Buijink

showed that 133 non-financial firms in the EU voluntarily used non-local GAAP in

1999 suggesting that the majority of listed EU firms does not expect to benefit from

non-local GAAP adoption (Cuijpers & Buijink, 2005). When comparing mandatory

and voluntary adopters, Daske, et al., found that capital market effects were most

pronounced for firms that voluntarily switched to IFRS (Daske, et al., 2008).

Part 3. Education system for accounting

The adoption of IFRS will have a large impact on colleges and universities.

Although this is a very important step forward, the education associations in some

countries and professors of accounting are not yet fully prepared to incorporate IFRS

into their curricula.

Texas Tech University, Hyun-Pyo Kim, May 2011

19

Preparations have begun to incorporate IFRS and IAS (International

Accounting Standards) into accounting curricula; as a result several problems need to

be addressed. The research shows that in Ukraine, for example, the first problem is the

lack of good course materials and the second is out-of-date of textbooks due to the

rapid changes in Ukrainian national accounting standards that adoption of IFRS will

require. Also, some of the most prestigious universities in Ukraine still do not have a

course devoted solely to IFRS (McGee & Preobragenskaya, 2005). However, when we

look at the U.S academic community (accounting and auditing students and professors)

as well as practitioners (auditors, accountants, CPAs, and financial analysts), the

United States appears ready to converge to IFRS.

There are three results revealed in this research: 1) auditors, accountants, and

accounting students are ready for the convergence to IFRS; 2) convergence to IFRS

can increase global comparability; 3) a proper plan to transition all U.S. companies to

IFRS requires IFRS training for investors, management, auditors, and IFRS education

in the accounting curriculum (Moqbel & Bakay, 2010).

With conversion to IFRS likely but not certain, many professors are having

difficulty discerning the “how, when, and what” of incorporating IFRS into today’s

accounting curriculum (Nilsen, 2008). A 2008 study identified some problems in the

accounting curricula of business information at the high school level and suggested

improvements needed in the accounting textbooks. The suggestions for revision were

developed after comparing the current U.S. curriculum with K-IFRS (Korean IFRS).

That study itemized some ways to improve accounting education curriculum as

Texas Tech University, Hyun-Pyo Kim, May 2011

20

follows: 1) the concepts and the need for introduction of K-IFRS should be reflected

in the new courses; 2) the contents of the consolidated financial statements should be

reflected in the new courses, and 3) the contents of the textbooks should be

reorganized (Kim & Chung, 2008).

An associate professor of accounting at Butler University in Indianapolis,

Indiana was quoted as saying that “he is going to have to basically replace his

understanding and relearn it based on IFRS (International Financial Reporting

Standards).” Also, he stated that because students are already being taught U.S.

standards, the transition may be more difficult, and that the adoption of IFRS is

probably the biggest accounting change in his professional life (Olson, 2008). The

adoption of IFRS is a very powerful event in the capital market. Many researchers cite

the lack of stability in accounting curricula as one of the reasons for their concern.

Research questions

Although the standards have a critical impact on the capital market, not all of

the associations, colleges, and universities offer new classes covering IFRS to their

students. By investigating the perception of the IFRS among college students, this

study will determine the status of preparation for the standards and help business

departments offer high quality classes about the IFRS (International Financial

Reporting Standards).

Based on the above discussion, I address the following research hypotheses:

Texas Tech University, Hyun-Pyo Kim, May 2011

21

H 1: There is a difference in knowledge about IFRS between male and female

college students.

H 2: There are differences in knowledge about IFRS for each age group among

college students.

H 3: There are differences in knowledge about IFRS for each school year group

among college students.

H 4: Students who are majoring in business will have more information about IFRS

than non-business students.

H 5: There is a relationship between the perception about evaluating the positive

effect of IFRS on capital markets and the intention to take classes about IFRS.

H 6: Students who have an interest in IFRS are more likely to take classes

concerning IFRS if colleges or universities offer them.

Texas Tech University, Hyun-Pyo Kim, May 2011

22

CHAPTER III

METHODOLOGY

Data and sample

The data were collected using a questionnaire during spring 2011. The

researchers distributed the survey to college students. A survey was distributed to

freshman, sophomore, junior, senior, and graduate-level students. Three hundred

questionnaires were distributed, and 246 questionnaires were collected in February

2011. It took participants about 10 minutes to complete this questionnaire.

During the recruitment procedure, students were informed that participation

was voluntary and that they could stop completing the survey at anytime. The study

measured this population of student’s perceptions and knowledge of the International

Financial Reporting Standards (IFRS). The findings from this study will be a good

reference for college students and future researchers, and will help business

departments offer high-quality classes about the IFRS (International Financial

Reporting Standards). College students attending TTU (Texas Tech University) and

participants for this study were recruited at the SUB (Student Union Building) at

Texas Tech University in Lubbock, Texas. This study asked students in the SUB

(Student Union Building) to complete an anonymous survey. Their participation in

this study was purely voluntary. All students were over the age of 18.

Texas Tech University, Hyun-Pyo Kim, May 2011

23

1. Data collection was conducted at Texas Tech University in the SUB

(Student Union Building) during the spring semester 2011.

2. The researcher approached college students in the SUB (Students Union

Building) requesting their participation in a research study.

3. An information sheet was affixed as a cover page on the survey. The

survey was distributed in a paper handout or affixed to a clipboard.

Directions were provided about how to complete the survey.

4. The questionnaire was distributed by the researcher at the SUB (Student

Union Building) at Texas Tech University who used an oral script for

consistency of presentation.

5. Participants were asked to fill out the questionnaire.

Data analysis

Data were compiled and analyzed by using the PASW (Predictive Analytics

Software) Statistics 18.

The data was analyzed in four steps.

1. The descriptive statistics

2. The t-test and analysis of variance (ANOVA)

3. The correlation (Pearson and Spearman)

4. The regression.

Texas Tech University, Hyun-Pyo Kim, May 2011

24

Definition of variables and research model

In order to investigate the perception of adoption of IFRS among college

students, I used many variables in this study. However, there are 6 main variables in

this research model. To test for the intention to take classes about IFRS among college

students, I used the following research design:

INTENT = a0 + a1 MAJOR + a2 KNOWLEDGE + a3 INTEREST +

a4 PERCEPTION1 + a5 PERCEPTION2 + a6 PERCEPTION3 + e (1)

I defined the above variables as follows:

1. INTENT: This variable is about the intent among college students to take class or

classes about the IFRS.

2. MAJOR: This variable was divided into two groups: 1) Business major and 2) Non-

business major. I used this variable as the dummy variable to analyze in research

(Business=1 and Non-business=0).

3. KNOWLEDGE: I collected this variable from students, by asking about some

keywords that are shared or differ between U.S. GAAP and IFRS. I measured this

variable as proxy for a degree of knowledge of IFRS.

The adoption of IFRS is a critical event for the business department in many

colleges and universities. In order to evaluate the amount and accuracy of student

respondents’ knowledge and/or information about IFRS, I selected some

Texas Tech University, Hyun-Pyo Kim, May 2011

25

keywords/concepts that are shared or differ between the U.S. GAAP and IFRS with

which to compare this knowledge. I have described these differences below.

For the present, companies in the United States are allowed to use LIFO (Last-

In, First-Out), an inventory valuation method in the U.S. GAAP, that also enables

them to use LIFO for U.S. tax purposes. However, IFRS does not allow the use of

LIFO (Last-In, First-Out). A company in accordance with IFRS must use a method of

accounting for inventory that is acceptable under IFRS, such as First-In, First-Out or

FIFO ("US GAAP vs. IFRS," 2009).

IFRS permits the revaluation of certain assets to fair value, whereas U.S.

GAAP generally does not. Fair value is the amount for which an asset could be

exchanged or a liability settled (IAS39, 2008).

Under IFRS, adjustments are permitted to be made to financial statements for

significant transactions that occur in the gap period. However, adjustments are

generally not made for transactions that occur in the gap period in the U.S. GAAP

(Kaiser, 2010).

By utilizing IFRS, companies will have more flexibility for applying

accounting principles because these standards are more principles based, whereas

GAAP is more rules based. Kaiser suggested that the IFRS should be confined to

principles and not become detailed rules. As a result of this, IFRS was justified by the

same experts as principles-based accounting standards, in contrast to FASB’s rules-based

standards (Kaiser, 2010).

Texas Tech University, Hyun-Pyo Kim, May 2011

26

As another example, let’s look at the differences in testing for the potential

impairment of long-lived assets held for use that might lead to earlier impairment

recognition under IFRS. IFRS requires the use of entity-specific discounted cash flows

or a fair value measure in tests for the recoverability of an asset. By comparison, the

U.S. GAAP uses a two-step model that begins with undiscounted cash flows. This

fundamental distinction between the impairment models can make a difference in

whether an asset is considered impaired ("US GAAP vs. IFRS," 2009).

As mentioned above, there are specific differences between IFRS and U.S.

GAAP standards:

1) LIFO prohibition

2) Fair market measurement

3) Financial periods

4) Principle-based accounting

5) Impairment

4. INTEREST: This variable is about the interest in IFRS among college students.

5. PERCEPTION 1: To develop this variable, I asked students whether they had a

perception about how the adoption of IFRS would affect financial performance.

6. PERCEPTION 2: To develop this variable, I asked students whether they had a

perception that the adoption of IFRS would have an effect on operating performance.

Texas Tech University, Hyun-Pyo Kim, May 2011

27

7. PERCEPTION 3: To develop this variable, I asked students whether they had a

perception about how the adoption of IFRS would affect stakeholders such as

investors or shareholders.

Texas Tech University, Hyun-Pyo Kim, May 2011

28

CHAPTER IV

RESULTS AND DISCUSSION

Descriptive analysis

Descriptive analyses have frequencies, measures of maximum, mean, median,

and minimum, and dispersions of standard deviation based on gender, age, school year,

race, and major.

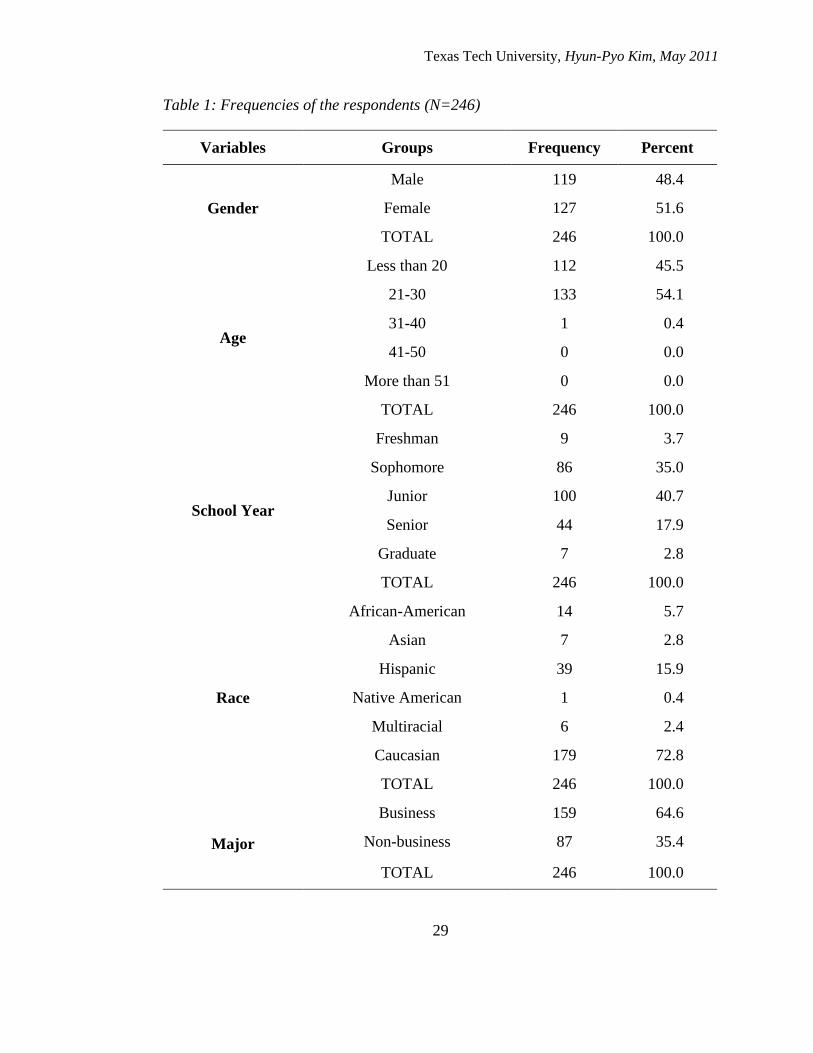

Table 1 addresses the demographic characteristics of the sample of respondents.

The respondents’ socio-demographic were profiled in frequencies and percentages. As

clearly shown, a majority of the sample was composed of young people (99.6% who

reported being less than 30 years old). In this category, 48.4% of respondents were

male and 51.6% were female. 45.5% of the respondents were less than 20 years of age

and 54.1% were between the ages of 21 and 30. Finally, 0.4% of respondents were

more than 30 years old. The most frequently occurring classification group was junior

(40.7%), followed by sophomore (35.0%), senior (17.9%), freshman (3.7%), and

graduate (2.8%). About 72.8% of the respondents were Caucasian, 15.9%, 5.7%, 2.8%,

2.4%, and 0.4% were Hispanic, African-American, Asian, Multiracial, and Native

American, respectively. 64.6% of the respondents were students who noted having a

business major, such as accounting, marketing, and/or finance. 35.6% of the

respondents were non-business majors.

Texas Tech University, Hyun-Pyo Kim, May 2011

29

Table 1: Frequencies of the respondents (N=246)

Variables Groups Frequency Percent

Gender

Male 119 48.4

Female 127 51.6

TOTAL 246 100.0

Age

Less than 20 112 45.5

21-30 133 54.1

31-40 1 0.4

41-50 0 0.0

More than 51 0 0.0

TOTAL 246 100.0

School Year

Freshman 9 3.7

Sophomore 86 35.0

Junior 100 40.7

Senior 44 17.9

Graduate 7 2.8

TOTAL 246 100.0

Race

African-American 14 5.7

Asian 7 2.8

Hispanic 39 15.9

Native American 1 0.4

Multiracial 6 2.4

Caucasian 179 72.8

TOTAL 246 100.0

Major

Business 159 64.6

Non-business 87 35.4

TOTAL 246 100.0

Texas Tech University, Hyun-Pyo Kim, May 2011

30

Table 2 also addresses the demographic characteristics of the sample of

respondents based on measures and dispersions. In the section pertaining to gender,

1.52 was the mean, 0.5, 2, 2, and 1 were standard deviation, maximum, median, and

minimum measures, respectively. The mean, 1.52, shows that there were more females

than males in the sample. The mean of the age of the respondents was 1.55. This

measure confirmed that a great portion of respondents were below age 30. Because the

maximum value is 3, there were no respondents in two of the age groups: 41-50 and

more than 51. A score of 2.82 showed that most of the respondents were between their

sophomore and junior years at the university. However, since 2.82 is closer to 3 than

to 2, this shows that there were more respondents participating from the junior class.

The maximum value was 5; this means that few respondents reported being in a

graduate course. In the major category, 1.35 was the mean, 0.48, 2, 1, and 1 were

standard deviation, maximum, median, and minimum measures, respectively. Because

the median was 1, this shows that business students were over 50% of the respondents.

Table 2: Descriptive statistics (N=246)

Variables Mean STD Max 75% Median 25% Min

Gender 1.52 0.50 2 2 2 1 1

Age 1.55 0.51 3 2 2 1 1

School Year 2.81 0.87 5 3 3 2 1

Race 5.09 1.59 6 6 6 4.75 1

Major 1.35 0.48 2 2 1 1 1

Texas Tech University, Hyun-Pyo Kim, May 2011

31

The definition of variables

1) Gender: Male=1 and Female=2

2) Age: Less than 20=1, 21-30=2, 31-40=3, 41-50=4, and More than 51=5

3) School Year: Freshman=1, Sophomore=2, Junior=3, Senior=4, and Graduate=5

4) Race: African-American=1, Asian=2, Hispanic=3, Native American=4,

Multiracial=5, and Caucasian=6

5) Major: Business=1 and Non-business=2

T-test and ANOVA (Analysis of Variance)

Comparing the means of two populations such as gender and major, I used the

t-test method. To extend this method to problems involving more than two populations,

I used the ANOVA (Analysis of Variance). I computed a two-sample t statistic and its

P-value to assess the statistical significance of the difference in the sample means.

However, ANOVA uses an F statistic and its P-value to evaluate the null hypothesis

that all of several population means are equal.

As you can see in Table 3, there is a difference in the knowledge of IFRS

between male and female respondents. The extent of knowledge of IFRS for male

students (M=3.48, SD=1.48) is significantly higher than for female students (M=3.11,

SD=1.28) with t-value of 2.029 and p-value < .05. Although the study was conducted

at one university in the American Southwest, these results suggest that there may be a

difference in knowledge about IFRS between men and women. While it is difficult to

generalize these results to all college or university student populations, universities or

colleges should consider evaluating students to determine their level of knowledge

Texas Tech University, Hyun-Pyo Kim, May 2011

32

about IFRS and then have provisions in place for extra classes or assignments in order

to raise the extent of knowledge of IFRS for any group of students (male and female)

who show deficiencies in basic knowledge of these standards.

Table 3: t-test result for knowledge of IFRS between male and female respondents

Gender of respondents N Mean SD t-value

Male 112 3.48 1.48

2.029*

Female 112 3.11 1.28

* P < 0.05.

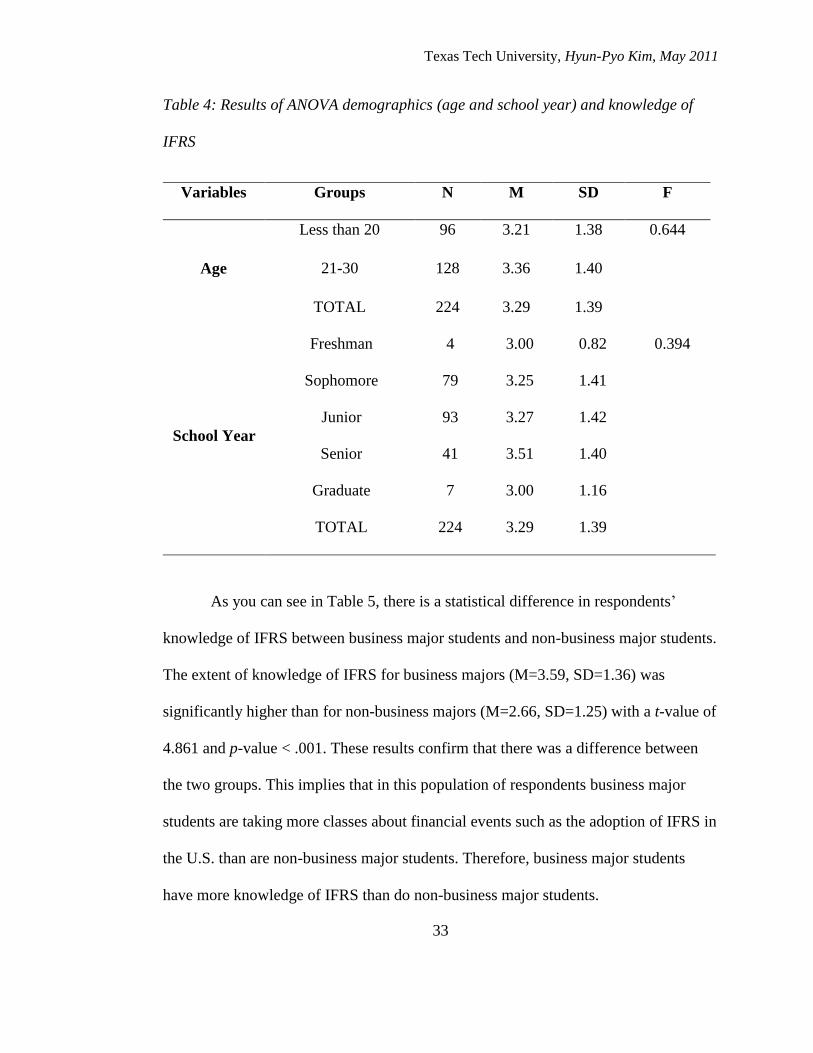

In Table 4, with the F value of 0.644 and the corresponding p value of 0.423,

no significance was found in ANOVA between the age groups. There are no

differences between the age groups regarding their knowledge of IFRS that were

evaluated as proxy because the F is 0.644 associated probability value (0.423) does

not meet the criterion for statistical significance (that is, p < .05). Also, there are no

differences between each school year group among respondents pertaining to their

knowledge of IFRS. With the F value of 0.394 and the corresponding p value of 0.813,

no significance was found in ANOVA within the school year groups. These results

show that there were no differences in knowledge of IFRS for age groups and school

year groups among respondents.

Texas Tech University, Hyun-Pyo Kim, May 2011

33

Table 4: Results of ANOVA demographics (age and school year) and knowledge of

IFRS

Variables Groups N M SD F

Age

Less than 20 96 3.21 1.38 0.644

21-30 128 3.36 1.40

TOTAL 224 3.29 1.39

School Year

Freshman 4 3.00 0.82 0.394

Sophomore 79 3.25 1.41

Junior 93 3.27 1.42

Senior 41 3.51 1.40

Graduate 7 3.00 1.16

TOTAL 224 3.29 1.39

As you can see in Table 5, there is a statistical difference in respondents’

knowledge of IFRS between business major students and non-business major students.

The extent of knowledge of IFRS for business majors (M=3.59, SD=1.36) was

significantly higher than for non-business majors (M=2.66, SD=1.25) with a t-value of

4.861 and p-value < .001. These results confirm that there was a difference between

the two groups. This implies that in this population of respondents business major

students are taking more classes about financial events such as the adoption of IFRS in

the U.S. than are non-business major students. Therefore, business major students

have more knowledge of IFRS than do non-business major students.

Texas Tech University, Hyun-Pyo Kim, May 2011

34

Table 5: t-test result for knowledge of IFRS between business students and non-

business students

Major of respondents N Mean SD t-value

Business 153 3.59 1.36

4.861***

Non-business 71 2.66 1.25

*** P < 0.001

Correlation

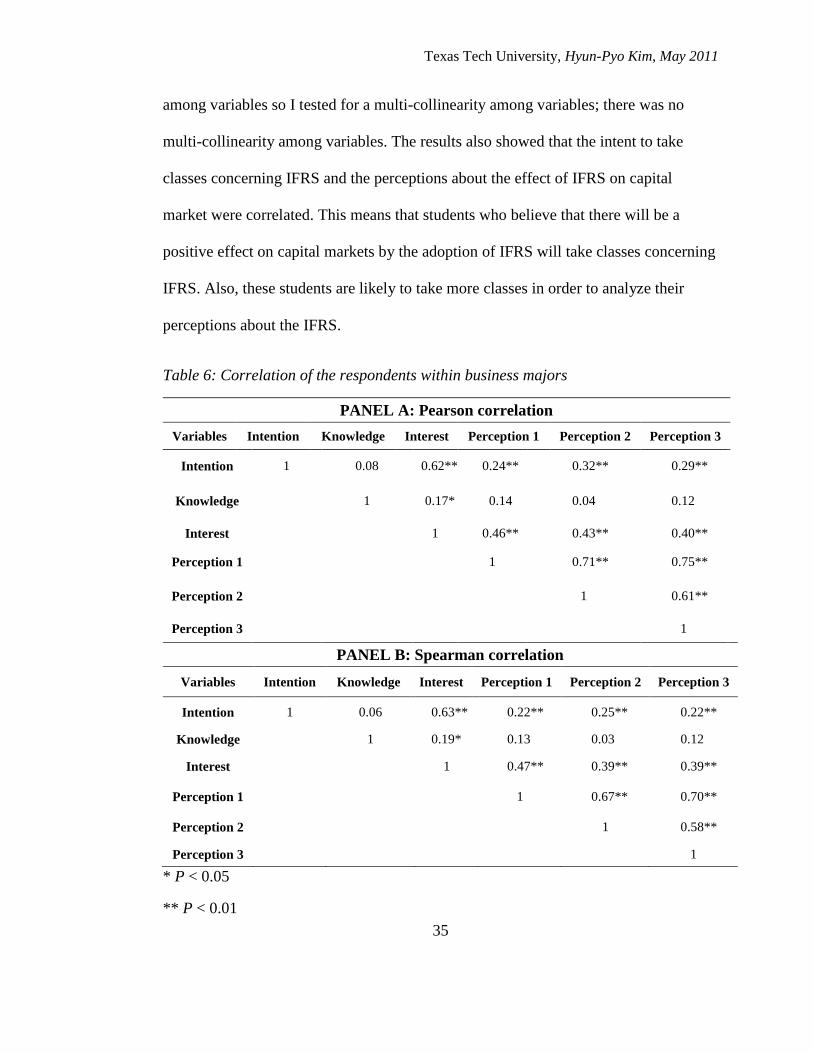

The Pearson correlation (PANEL A) test and the Spearman correlation

(PANEL B) test were performed using variables such as intention, knowledge, and

interest. I separated the results into two groups: business majors and non-business

majors. The results for the first group (business major) are presented in Table 6. The

results for collation among variables for non-business majors are presented in Table 7.

As it is shown in Table 6, there are correlations among the variables. The relationships

between INTENTION and INTEREST, PERCEPTION1, 2, and 3 are significantly

correlated (γ = 0.62, P < 0.01, γ = 0.24, P < 0.01, γ = 0.32, P < 0.01, and γ = 0.29, P <

0.01 in Panel A and γ = 0.63, P < 0.01, γ = 0.22, P < 0.01, γ = 0.25, P < 0.01, and γ =

0.22, P < 0.01 in Panel B, respectively) and all directions were positive. The

INTEREST variable also had a positive correlation to others variables such as

PERCEPTION1, 2, and 3 in Panel A and B. Among PERCEPTION variables, there

was a strong correlation. However, the KNOWLEDGE variable showed correlation

with only the INTEREST variable (γ = 0.17, P < 0.05 in Panel A and γ = 0.19, P <

0.05 in Panel B) and the directions were positive. Many correlations were very high

Texas Tech University, Hyun-Pyo Kim, May 2011

35

among variables so I tested for a multi-collinearity among variables; there was no

multi-collinearity among variables. The results also showed that the intent to take

classes concerning IFRS and the perceptions about the effect of IFRS on capital

market were correlated. This means that students who believe that there will be a

positive effect on capital markets by the adoption of IFRS will take classes concerning

IFRS. Also, these students are likely to take more classes in order to analyze their

perceptions about the IFRS.

Table 6: Correlation of the respondents within business majors

PANEL A: Pearson correlation

Variables Intention Knowledge Interest Perception 1 Perception 2 Perception 3

Intention 1 0.08 0.62** 0.24** 0.32** 0.29**

Knowledge 1 0.17* 0.14 0.04 0.12

Interest 1 0.46** 0.43** 0.40**

Perception 1 1 0.71** 0.75**

Perception 2 1 0.61**

Perception 3 1

PANEL B: Spearman correlation

Variables Intention Knowledge Interest Perception 1 Perception 2 Perception 3

Intention 1 0.06 0.63** 0.22** 0.25** 0.22**

Knowledge 1 0.19* 0.13 0.03 0.12

Interest 1 0.47** 0.39** 0.39**

Perception 1 1 0.67** 0.70**

Perception 2 1 0.58**

Perception 3 1

* P < 0.05

** P < 0.01

Texas Tech University, Hyun-Pyo Kim, May 2011

36

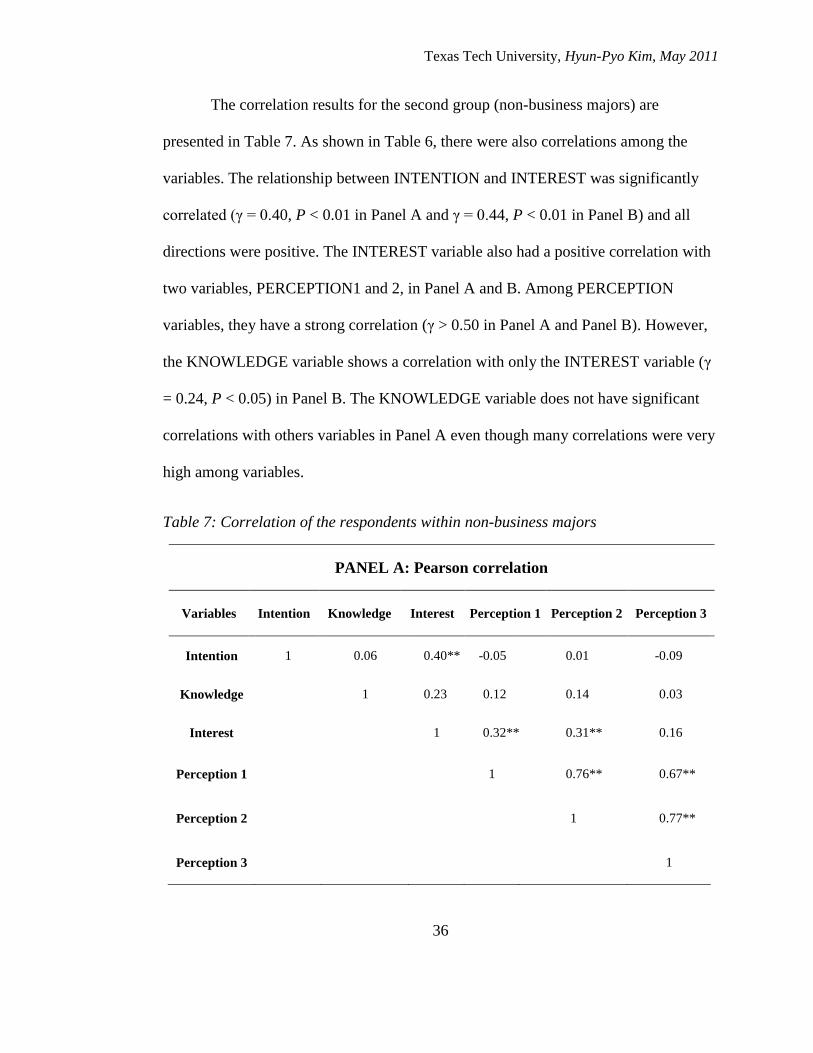

The correlation results for the second group (non-business majors) are

presented in Table 7. As shown in Table 6, there were also correlations among the

variables. The relationship between INTENTION and INTEREST was significantly

correlated (γ = 0.40, P < 0.01 in Panel A and γ = 0.44, P < 0.01 in Panel B) and all

directions were positive. The INTEREST variable also had a positive correlation with

two variables, PERCEPTION1 and 2, in Panel A and B. Among PERCEPTION

variables, they have a strong correlation (γ > 0.50 in Panel A and Panel B). However,

the KNOWLEDGE variable shows a correlation with only the INTEREST variable (γ

= 0.24, P < 0.05) in Panel B. The KNOWLEDGE variable does not have significant

correlations with others variables in Panel A even though many correlations were very

high among variables.

Table 7: Correlation of the respondents within non-business majors

PANEL A: Pearson correlation

Variables Intention Knowledge Interest Perception 1 Perception 2 Perception 3

Intention 1 0.06 0.40** -0.05 0.01 -0.09

Knowledge 1 0.23 0.12 0.14 0.03

Interest 1 0.32** 0.31** 0.16

Perception 1 1 0.76** 0.67**

Perception 2 1 0.77**

Perception 3 1

Texas Tech University, Hyun-Pyo Kim, May 2011

37

Table 8(Continued): Correlation of the respondents within non-business majors

PANEL B: Spearman correlation

Variables Intention Knowledge Interest Perception 1 Perception 2 Perception 3

Intention 1 0.09 0.44** -0.02 0.06 -0.12

Knowledge 1 0.24* 0.06 0.13 0.06

Interest 1 0.25* 0.29** 0.09

Perception 1 1 0.75** 0.66**

Perception 2 1 0.69**

Perception 3 1

* P < 0.05

** P < 0.01

Regression

I analyzed variables in order to investigate, empirically, the intent of college

students (H6). Also, to test this hypothesis, I utilized the following research design:

INTENT = a0 + a1 MAJOR + a2 KNOWLEDGE + a3 INTEREST +

a4 PERCEPTION1 + a5 PERCEPTION2 + a6 PERCEPTION3 + e (1)

In this research design, the three variables (PERCEPTION 1, 2, and 3) that measured

students’ perception of adoption of IFRS on capital markets, should have high

correlation value among these variables. However, high correlation among variables

Texas Tech University, Hyun-Pyo Kim, May 2011

38

did not yield reliable data. Therefore, I tested for multi-collinearity. Also, in this

model, respondents’ major was a critical variable. To control the effect of respondents’

major, I used this variable as dummy variable.

Table 8 presents the estimated coefficients from multivariate regression for the

sample. As with the expectation of H 6, I found that INTEREST improved the intent

to take classes, significantly. This is significant at the 0.1% level for students. The

regression model I used significant with 3 variables. In particular, we can use the level

of interest about the IFRS to predict the intent to take classes of IFRS (t = 9.553 and p

< .001). Also, the results for PERCEPTION 1 (financial performance) of IFRS

predicted the intent to take classes about IFRS (t = -2.644 and p < .01).

These results showed that respondents who have an interest about IFRS will

take classes, if classes about the IFRS are offered by the college or university.

Therefore, respondents’ level of interest and level of perception about financial

performance can be used to predict their intention to take classes from their college or

university. These results mean that interest is a very critical determinant among

college students for taking classes concerning IFRS. This showed that the more

students have an interest about IFRS, the more they will take classes.

Texas Tech University, Hyun-Pyo Kim, May 2011

39

Table 9: Regression analysis among variables

Variables Beta coefficient Standard error t

Intercept 1.261 0.317 3.978***

Major 0.077 0.121 0.635

Knowledge -0.006 0.041 -0.150

Interest 0.623 0.065 9.553***

Perception 1 -0.343 0.130 -2.644**

Perception 2 0.169 0.127 1.333

Perception 3 0.147 0.121 1.214

Adjusted R2 0.337

F 19.813***

** P < 0.01

*** P < 0.001

Additional analyses with business major students

Descriptive analysis

Table 9 addresses the demographic characteristics of the sample of respondents

with business major. The respondents’ socio-demographic were profiled in

frequencies and percentages. As clearly shown, a majority of the sample was

composed of young people (99.4% who reported being less than 30 years old). In this

category, 59.1% of respondents were male and 40.9% were female. 44.7% of the

respondents were less than 20 years of age and 54.7% were between the ages of 21

Texas Tech University, Hyun-Pyo Kim, May 2011

40

and 30. Finally, 0.6% of respondents were more than 30 years old. The most

frequently occurring classification group was junior (41.5%), followed by sophomore

(37.7%), senior (15.7%), freshman (3.1%), and graduate (1.9%). About 70.4% of the

respondents were Caucasian, 18.9%, 6.3%, 1.9%, and 0.6% were Hispanic, African-

American, Asian and Multiracial, and Native American, respectively.

Table 10: Frequencies for the respondents with business majors (N=159)

Variables Groups Frequency Percent

Gender

Male 94 59.1

Female 65 40.9

TOTAL 159 100.0

Age

Less than 20 71 44.7

21-30 87 54.7

31-40 1 0.6

41-50 0 0.0

More than 51 0 0.0

TOTAL 159 100.0

School Year

Freshman 5 3.1

Sophomore 60 37.7

Junior 66 41.5

Senior 25 15.7

Graduate 3 1.9

TOTAL 159 100.0

Race

African-American 10 5.7

Asian 3 2.8

Hispanic 30 15.9

Native American 1 0.4

Multiracial 3 2.4

Caucasian 112 72.8

TOTAL 159 100.0

Texas Tech University, Hyun-Pyo Kim, May 2011

41

Table 10 also addresses the demographic characteristics of the sample of

respondents with business major based on measures and dispersions. In the section

pertaining to gender, 1.41 was the mean, 0.49, 2, 1, and 1 were standard deviation,

maximum, median, and minimum measures, respectively. The mean, 1.41, shows that

there were more males than females in the sample. The mean of the age of the

respondents was 1.56. This measure confirmed that a great portion of respondents

were below age 30. Because the maximum value is 3, there were no respondents in

two of the age groups: 41-50 and more than 51. A score of 2.75 showed that most of

the respondents were between their sophomore and junior years at the university.

However, since 2.75 is closer to 3 than to 2, this shows that there were more

respondents participating from the junior class. The maximum value was 5; this means

that few respondents reported being in a graduate course.

Table 11: Descriptive statistics with business majors (N=159)

Variables Mean STD Max 75% Median 25% Min

Gender 1.41 0.49 2 2 1 1 1

Age 1.56 0.51 3 2 2 1 1

School Year 2.75 0.83 5 3 3 2 1

Race 5.01 1.63 6 6 6 3 1

Texas Tech University, Hyun-Pyo Kim, May 2011

42

T-test and ANOVA (Analysis of Variance)

As you can see in Table 11, there is no difference in the knowledge of IFRS

between male and female respondents with business major. The extent of knowledge

of IFRS for male students (M=3.62, SD=1.44) is not significantly higher than for

female students (M=3.55, SD=1.28).

Table 12: t-test result for knowledge of IFRS between male and female respondents

with business majors

Gender of respondents N Mean SD t-value

Male 91 3.62 1.44

0.298

Female 62 3.55 1.24

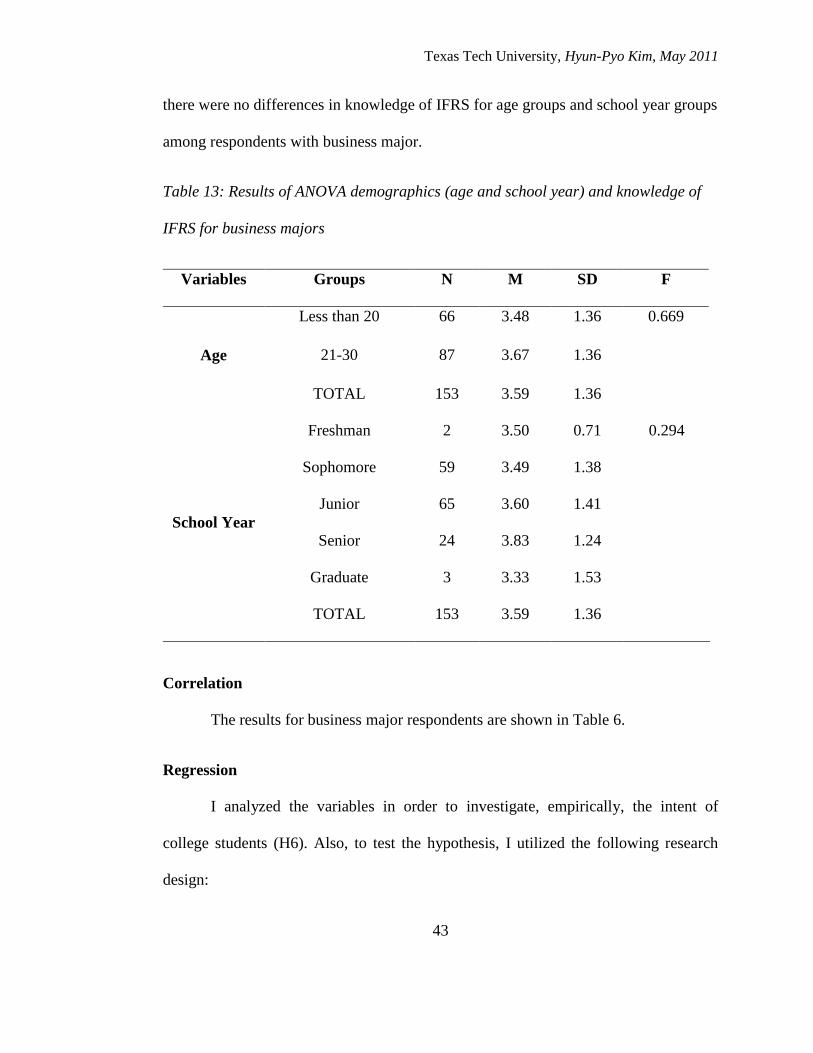

In Table 12, with the F value of 0.669 and the corresponding p value of 0.415,

no significance was found in ANOVA between the age groups with business major.

There are no differences between the age groups with business major regarding their

knowledge of IFRS that were evaluated as proxy because the F is 0.669 associated

probability value (0.415) does not meet the criterion for statistical significance (that is,

p < .05). Also, there are no differences between each school year group among

respondents with business major pertaining to their knowledge of IFRS. With the F

value of 0.294 and the corresponding p value of 0.882, no significance was found in

ANOVA within the school year groups with business major. These results show that

Texas Tech University, Hyun-Pyo Kim, May 2011

43

there were no differences in knowledge of IFRS for age groups and school year groups

among respondents with business major.

Table 13: Results of ANOVA demographics (age and school year) and knowledge of

IFRS for business majors

Variables Groups N M SD F

Age

Less than 20 66 3.48 1.36 0.669

21-30 87 3.67 1.36

TOTAL 153 3.59 1.36

School Year

Freshman 2 3.50 0.71 0.294

Sophomore 59 3.49 1.38

Junior 65 3.60 1.41

Senior 24 3.83 1.24

Graduate 3 3.33 1.53

TOTAL 153 3.59 1.36

Correlation

The results for business major respondents are shown in Table 6.

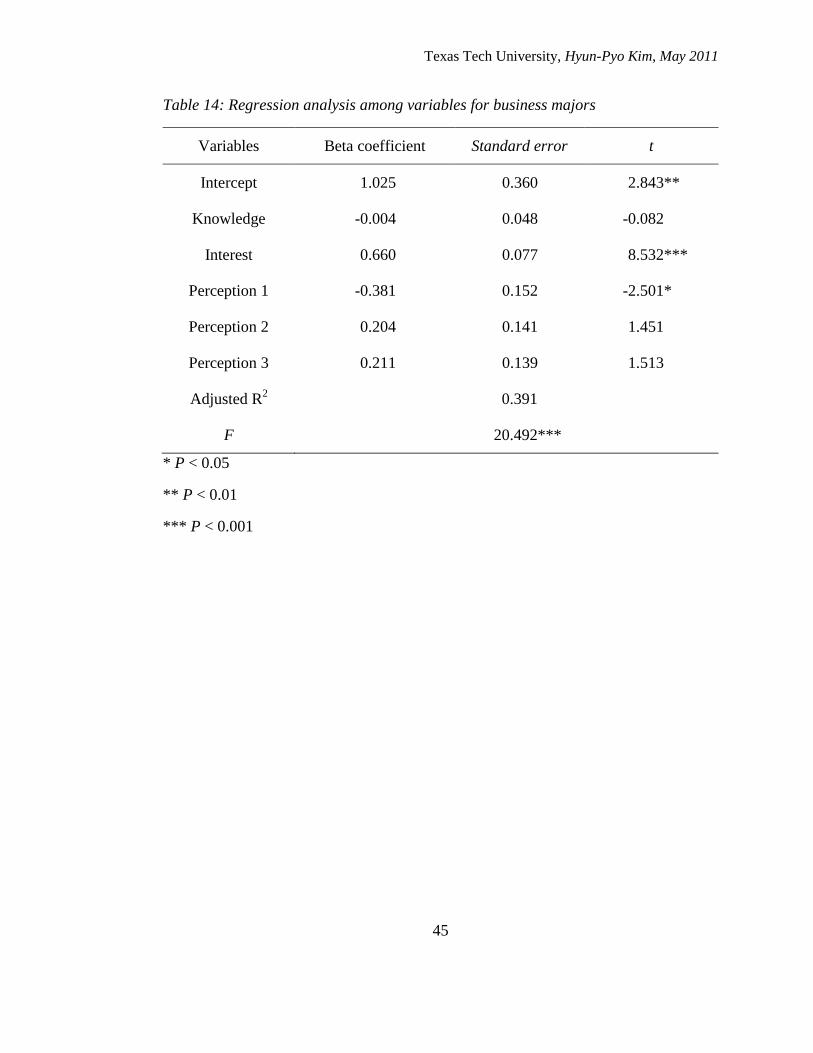

Regression

I analyzed the variables in order to investigate, empirically, the intent of

college students (H6). Also, to test the hypothesis, I utilized the following research

design:

Texas Tech University, Hyun-Pyo Kim, May 2011

44

INTENT = a0 + a1 KNOWLEDGE + a2 INTEREST + a3 PERCEPTION1 +

a4 PERCEPTION2 + a5 PERCEPTION3+ e (2)

Table 13 presents the estimated coefficients from multivariate regression for

the sample respondents with a business major. As with the expectation of H 6, I found

that INTEREST improved the intent to take classes, significantly. This was significant

at the 0.1% level for business students. In particular, we can use the level of interest

about the IFRS to predict the intent to take classes of IFRS (t = 8.532 and p < .001).

Also, the results for PERCEPTION 1 (financial performance) of IFRS predicted the

intent to take classes of IFRS (t = -2.501 and p < .05).

These results showed that respondents with a business major who have an

interest about IFRS will take classes, if classes about the IFRS are offered by the

college or university. Therefore, business major respondents’ level of interest and

level of perception about financial performance can be used to predict their intention

to take classes from their college and university.

Texas Tech University, Hyun-Pyo Kim, May 2011

45

Table 14: Regression analysis among variables for business majors

Variables Beta coefficient Standard error t

Intercept 1.025 0.360 2.843**

Knowledge -0.004 0.048 -0.082

Interest 0.660 0.077 8.532***

Perception 1 -0.381 0.152 -2.501*

Perception 2 0.204 0.141 1.451

Perception 3 0.211 0.139 1.513

Adjusted R2 0.391

F 20.492***

* P < 0.05

** P < 0.01

*** P < 0.001

Texas Tech University, Hyun-Pyo Kim, May 2011

46

CHAPTER V

CONCLUSIONS AND LIMITATIONS

The primary objective of this study was to investigate perceptions concerning

the adoption of International Financial Reporting Standards (IFRS) among college

students. The study measured a population of students’ perceptions and knowledge of

IFRS at a large university in the American Southwest. By utilizing the results of this

study, we can see college students’ perceptions concerning the status of preparation

for the standards, and these results could help colleges and universities with decisions

regarding offering classes about these standards.

The findings are as follows; first, I found there was a difference in knowledge

about IFRS between male and female respondents. While it is difficult to generalize

these results to all college or university student populations, universities and colleges

should consider evaluating students to determine their level of knowledge about IFRS

and then have provisions in place for extra classes or assignments in order to raise the

extent of knowledge of IFRS for any group of students (male and female) who show

deficiencies in basic knowledge of these standards. Second, there were no differences

in knowledge about IFRS for each age group and each school year among respondents.

Third, I found a difference in knowledge about IFRS between students majoring in

business and students who were non-business majors. This implies that in this

population of respondents, business major students are taking more classes about

financial events such as the adoption of IFRS in the U.S. than are non-business major

students. Therefore, business major students have more knowledge of IFRS than do

Texas Tech University, Hyun-Pyo Kim, May 2011

47

non-business major students. Fourth, I found a correlation between the perception

about evaluating the positive effect of IFRS on capital markets and the intention to

take classes about IFRS. This means that students who believe there will be a positive

effect on capital markets by the adoption of IFRS are more likely to take classes

concerning IFRS. Also, these students will take more classes in order to analyze their

perceptions about the IFRS. Finally, the results predicted that students who showed a

great interest in IFRS are more likely to take these courses if colleges or universities

offer classes. These results mean that interest is a very critical determinant among

college students for taking classes concerning IFRS. The more that students have an

interest about IFRS; the more they will take classes. There are also similar results

shown in the additional analyses section pertaining to business major respondents.

These findings regarding college students’ perceptions about the adoption of

IFRS supply many direct implications for business departments in colleges and

universities. According to the literature review, while the corporate adoption of IFRS

is not decreasing costs, there have been increased economic benefits in capital markets.

It makes economic sense that accounting information from financial statements should

be comparable among countries and companies and that users of accounting

information be allowed to assess the similarities and/or differences among different

entities; this includes business departments in colleges and universities. By adopting

IFRS in the U.S., the comparability of the framework for accounting will be increased,

and this reliability will improve the transparency of financial statements.

Texas Tech University, Hyun-Pyo Kim, May 2011

48

Because of the planned adoption of IFRS, courses about the standards should

be considered or installed at all levels of the education system in the U.S., particularly

in colleges and universities because the adoption of IFRS will be a critical event in the

capital market. However, because the IFRS are not currently in use in the United

States totally, this research concerning the standards was conducted and analyzed

indirectly by examining college students’ perception of IFRS. Additionally, this study

was conducted with participants attending a university in the U.S. Southwest, so it

might not be possible to generalize these findings to all areas of the United States. I