investment analysis and portfolio management lecture 2 gareth myles

TRANSCRIPT

Investment Analysis and Portfolio Management

Lecture 2

Gareth Myles

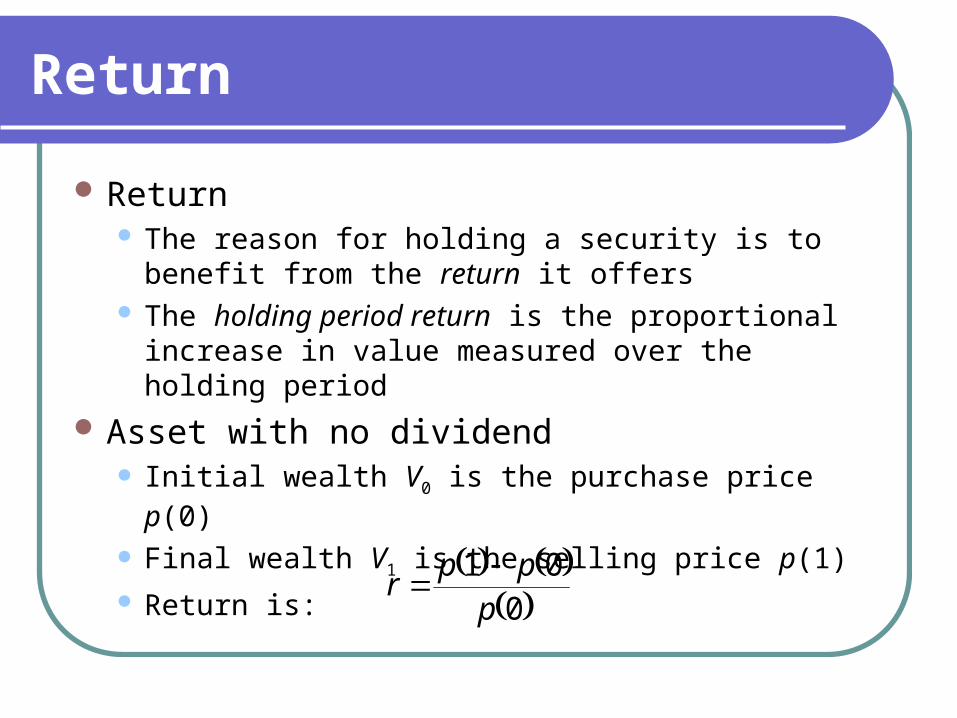

Return

Return The reason for holding a security is to benefit from

the return it offers The holding period return is the proportional

increase in value measured over the holding period

Asset with no dividend Initial wealth V0 is the purchase price p(0)

Final wealth V1 is the selling price p(1) Return is:

001

ppp

r

Return

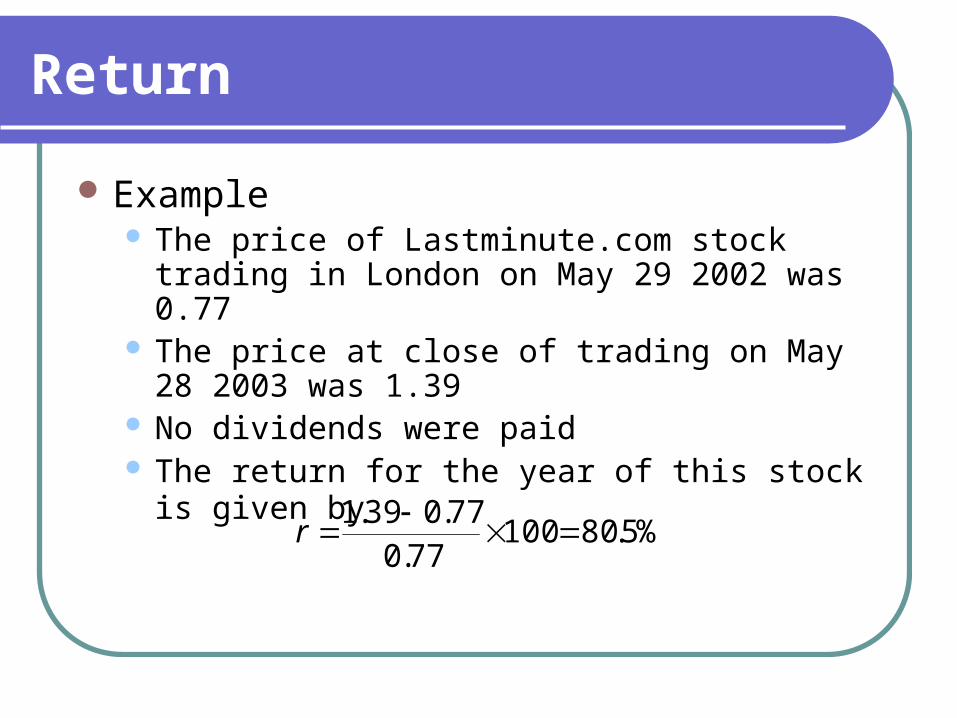

Example The price of Lastminute.com stock trading in

London on May 29 2002 was 0.77 The price at close of trading on May 28 2003 was

1.39 No dividends were paid The return for the year of this stock is given by

%5.8010077.0

77.039.1 r

Return

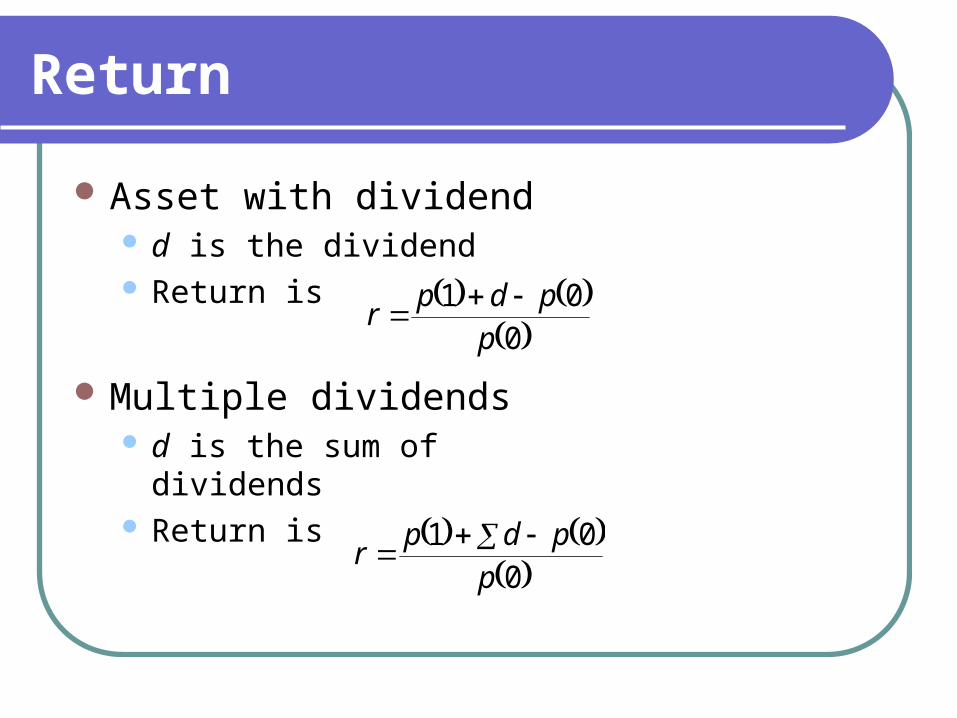

Asset with dividend d is the dividend Return is

Multiple dividends d is the sum of dividends Return is

0

01p

pdpr

0

01p

pdpr

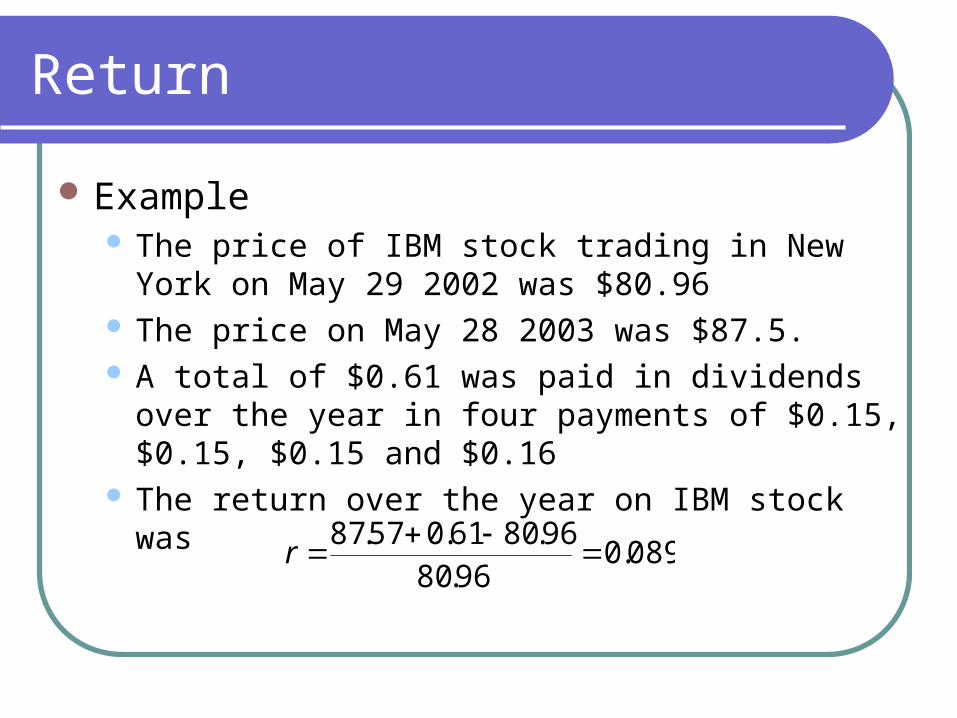

Return

Example The price of IBM stock trading in New York on May 29

2002 was $80.96 The price on May 28 2003 was $87.5. A total of $0.61 was paid in dividends over the year in

four payments of $0.15, $0.15, $0.15 and $0.16 The return over the year on IBM stock was

089.096.80

96.8061.057.87 r

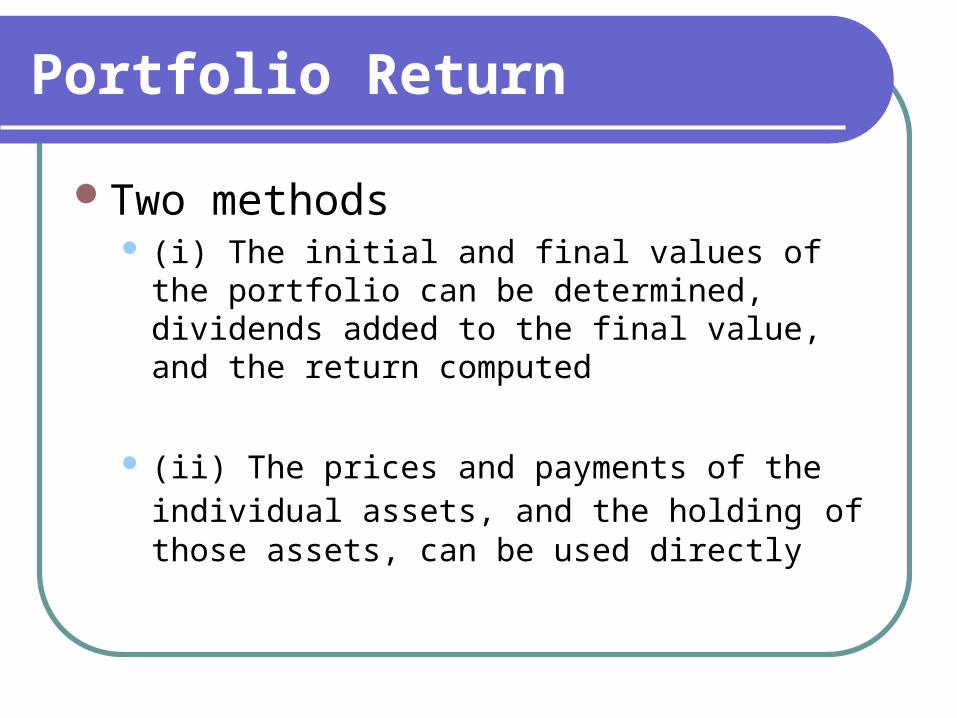

Portfolio Return

Two methods (i) The initial and final values of the portfolio can be

determined, dividends added to the final value, and the return computed

(ii) The prices and payments of the individual assets, and the holding of those assets, can be used directly

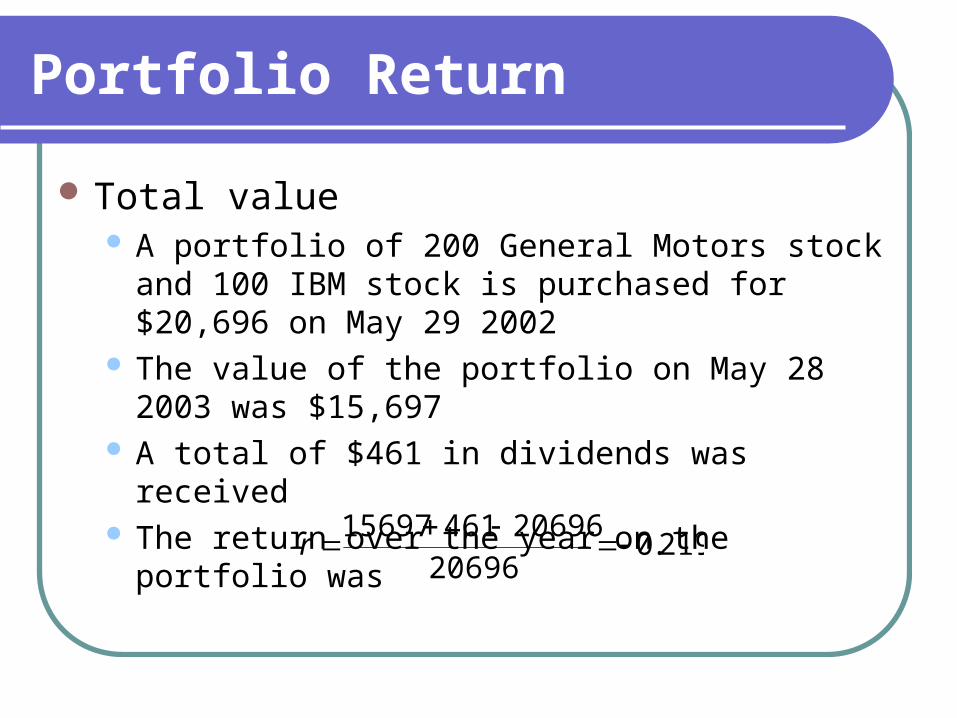

Portfolio Return

Total value A portfolio of 200 General Motors stock and 100 IBM

stock is purchased for $20,696 on May 29 2002 The value of the portfolio on May 28 2003 was

$15,697 A total of $461 in dividends was received The return over the year on the portfolio was

219.020696

2069646115697 r

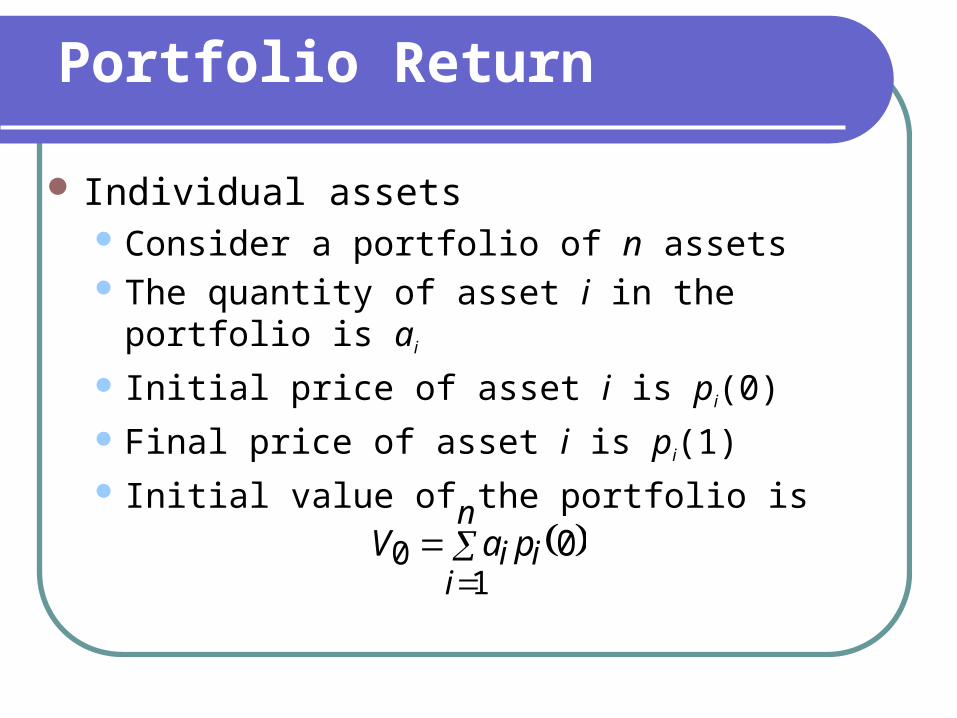

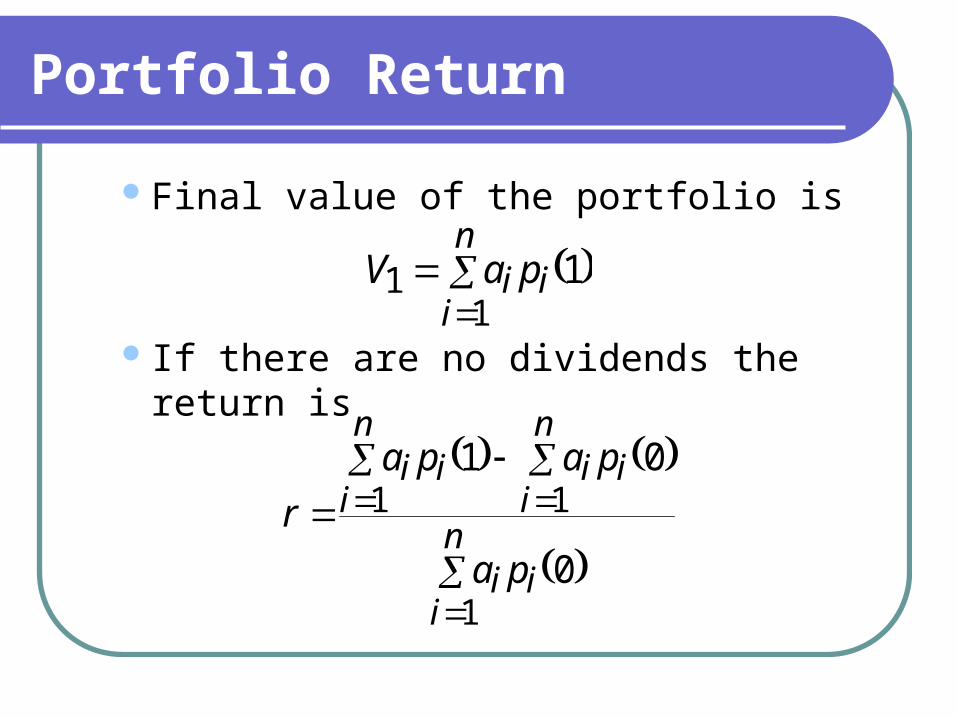

Portfolio Return

Individual assets Consider a portfolio of n assets The quantity of asset i in the portfolio is ai

Initial price of asset i is pi(0) Final price of asset i is pi(1) Initial value of the portfolio is

n

iii paV

10 0

Portfolio Return

Final value of the portfolio is

If there are no dividends the return is

n

iii paV

11 1

n

iii

n

iii

n

iii

pa

papa

r

1

11

0

01

Portfolio Return

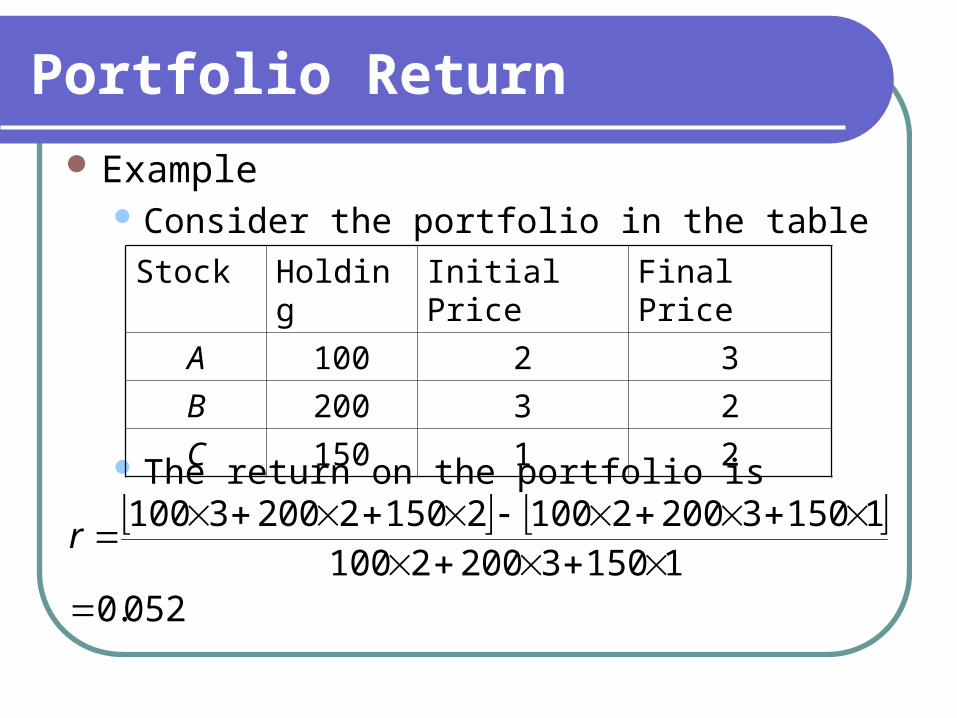

Example Consider the portfolio in the table

The return on the portfolio is

Stock Holding Initial Price Final Price

A 100 2 3

B 200 3 2

C 150 1 2

052.0115032002100

115032002100215022003100

r

Portfolio Return

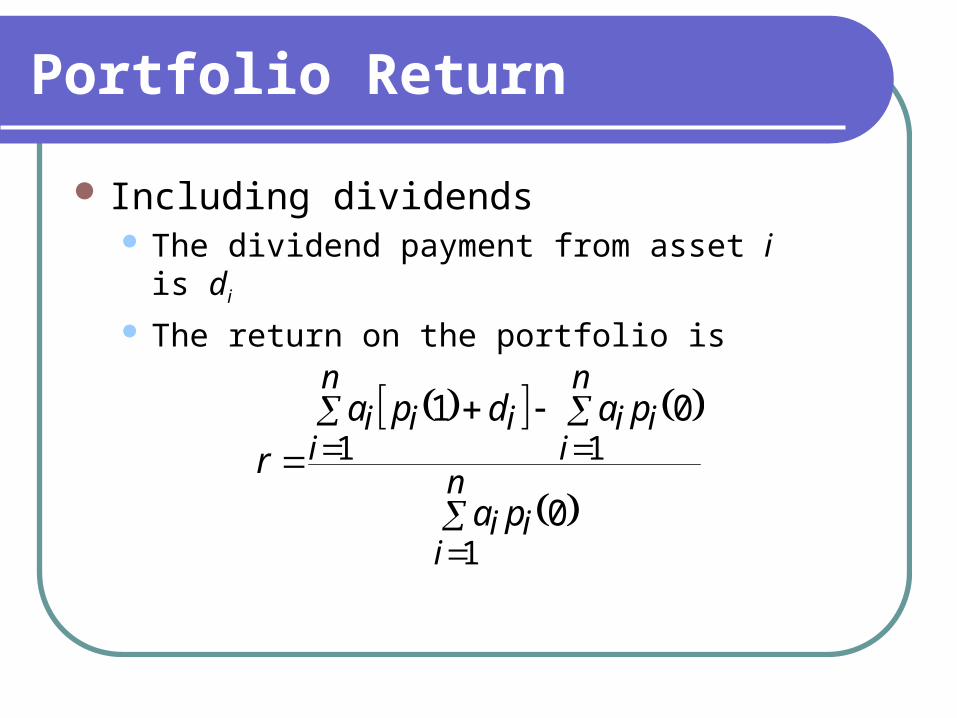

Including dividends The dividend payment from asset i is di

The return on the portfolio is

n

iii

n

iii

n

iiii

pa

padpa

r

1

11

0

01

Portfolio Return

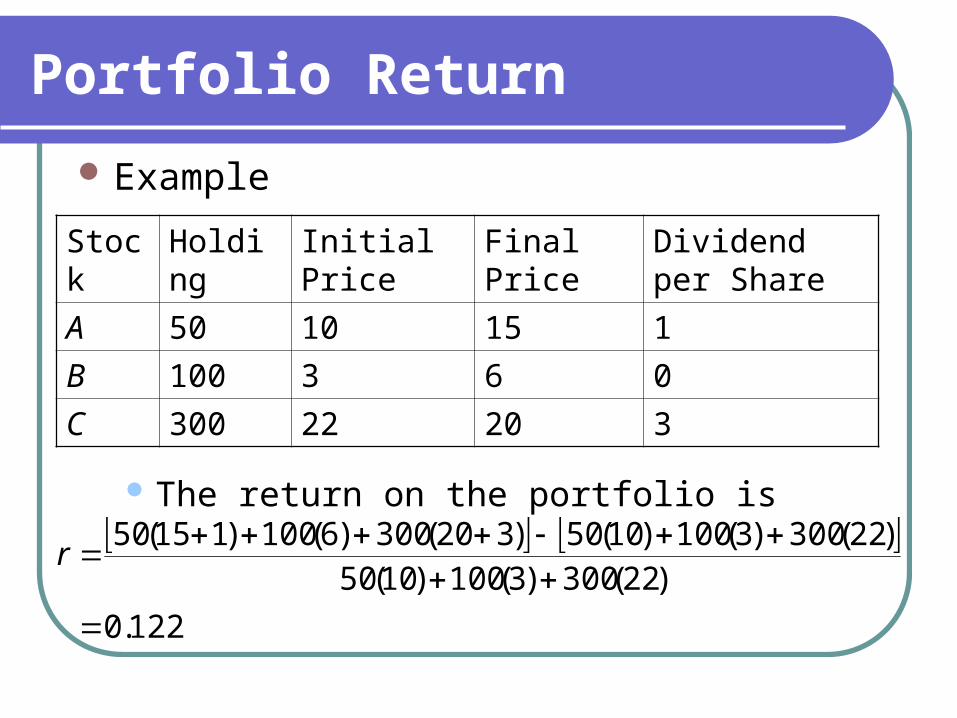

Example

The return on the portfolio is

Stock Holding Initial Price Final Price

Dividend per Share

A 50 10 15 1

B 100 3 6 0

C 300 22 20 3

122.0

)22(300)3(100)10(50)22(300)3(100)10(50)320(300)6(100)115(50

r

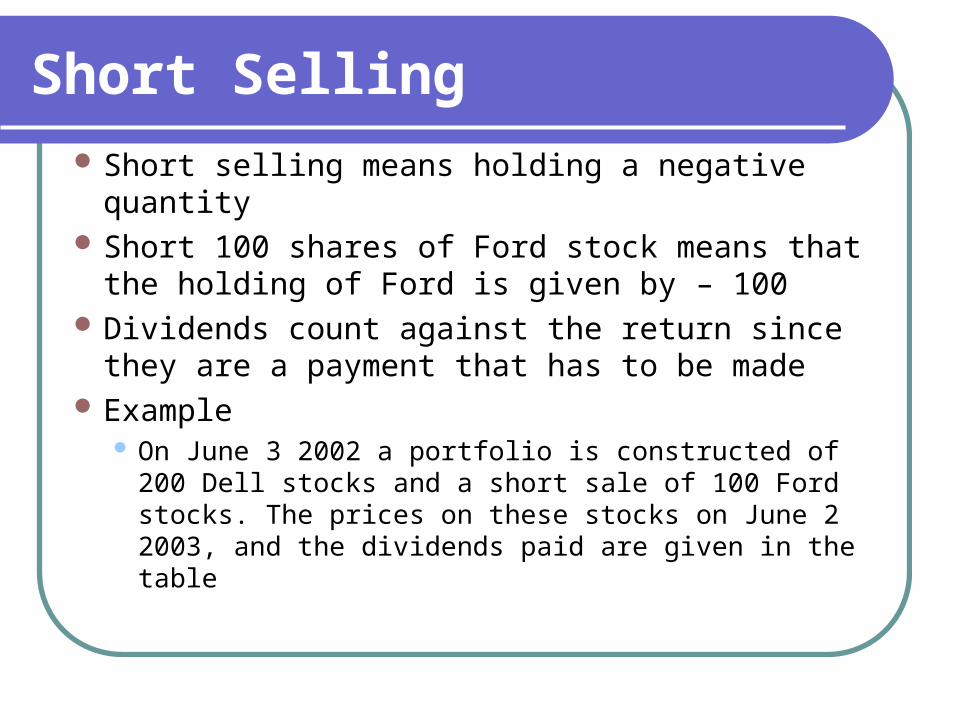

Short Selling

Short selling means holding a negative quantity Short 100 shares of Ford stock means that the

holding of Ford is given by – 100 Dividends count against the return since they

are a payment that has to be made Example

On June 3 2002 a portfolio is constructed of 200 Dell stocks and a short sale of 100 Ford stocks. The prices on these stocks on June 2 2003, and the dividends paid are given in the table

Short Selling

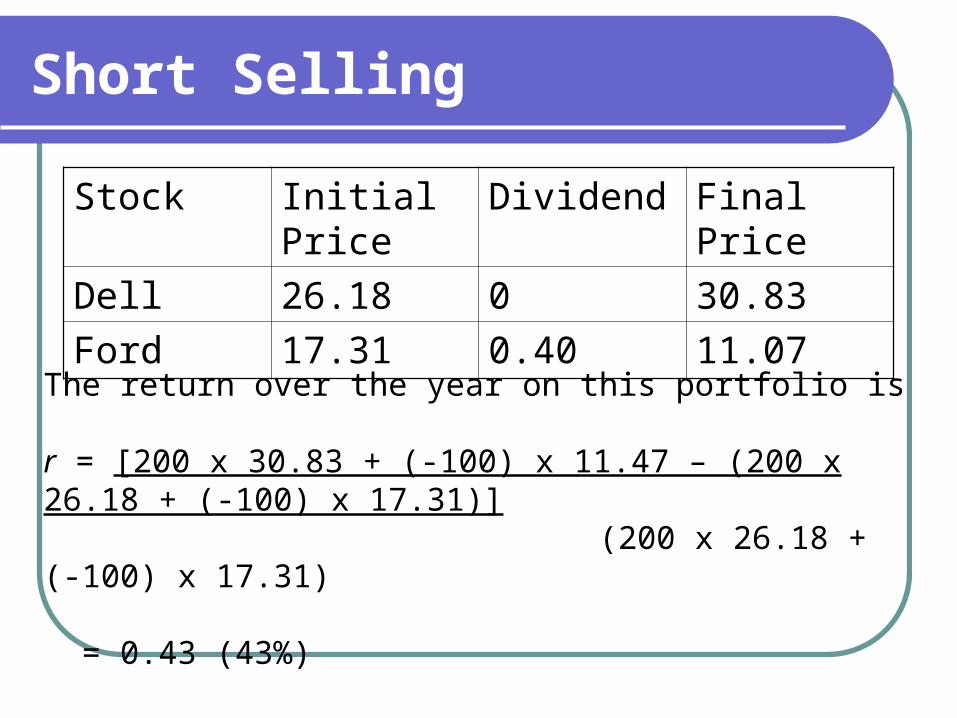

Stock Initial Price Dividend Final Price

Dell 26.18 0 30.83

Ford 17.31 0.40 11.07

The return over the year on this portfolio is

r = [200 x 30.83 + (-100) x 11.47 – (200 x 26.18 + (-100) x 17.31)] (200 x 26.18 + (-100) x 17.31)

= 0.43 (43%)

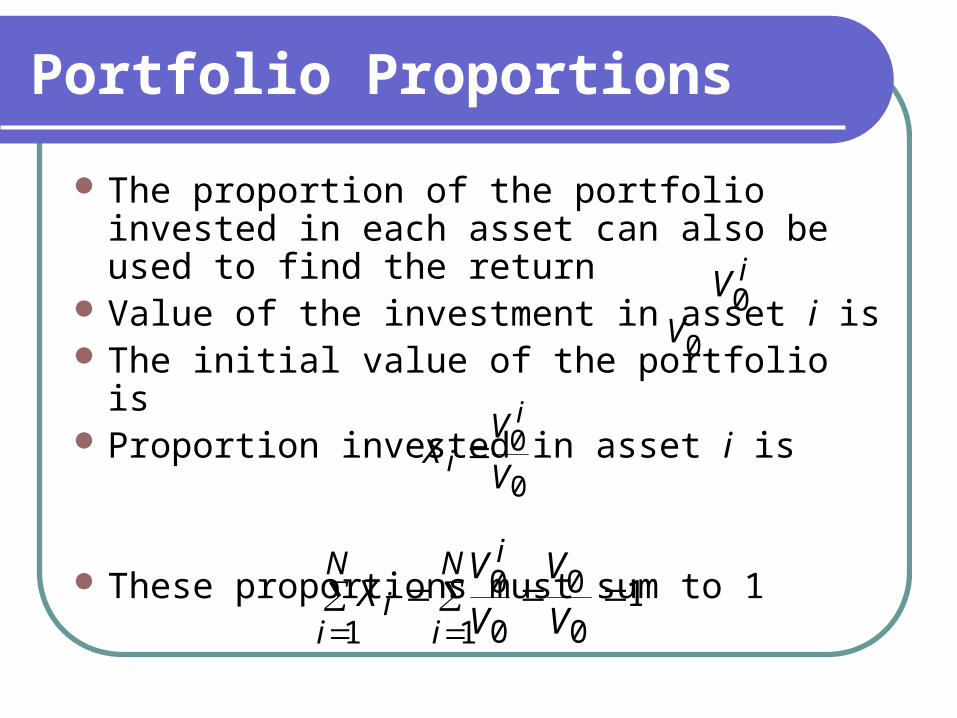

Portfolio Proportions

The proportion of the portfolio invested in each asset can also be used to find the return

Value of the investment in asset i is The initial value of the portfolio is Proportion invested in asset i is

These proportions must sum to 1

iV0

0V

0

0V

VX

i

i

10

0

1 0

0

1

V

V

V

VX

N

i

iN

ii

Portfolio Proportions

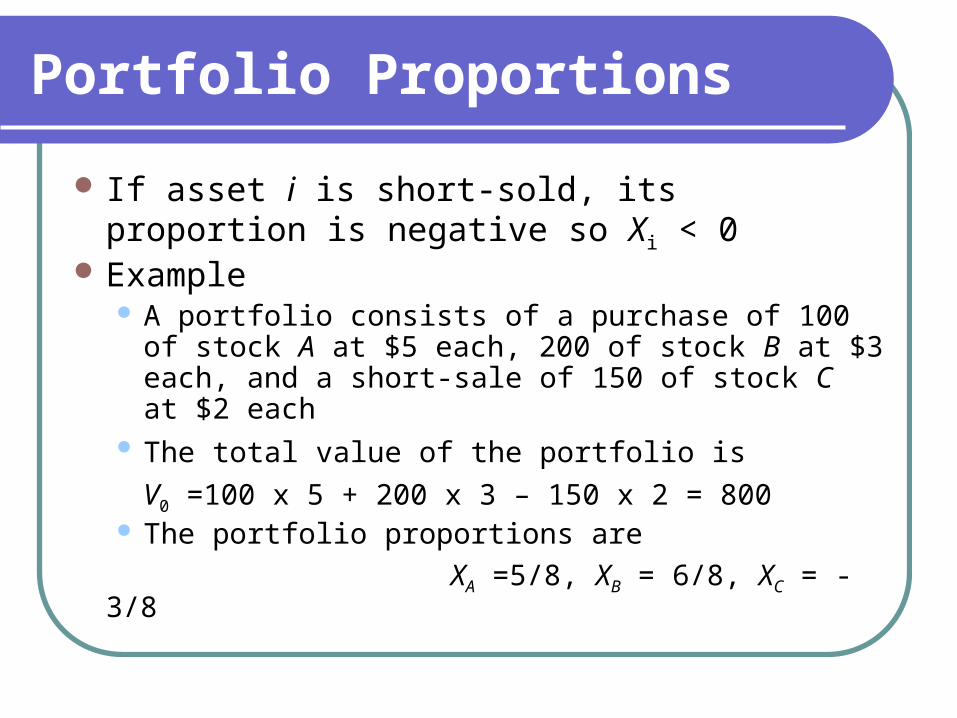

If asset i is short-sold, its proportion is negative so Xi < 0

Example A portfolio consists of a purchase of 100 of stock A

at $5 each, 200 of stock B at $3 each, and a short-sale of 150 of stock C at $2 each

The total value of the portfolio is V0 =100 x 5 + 200 x 3 – 150 x 2 = 800

The portfolio proportions are

XA =5/8, XB = 6/8, XC = -3/8

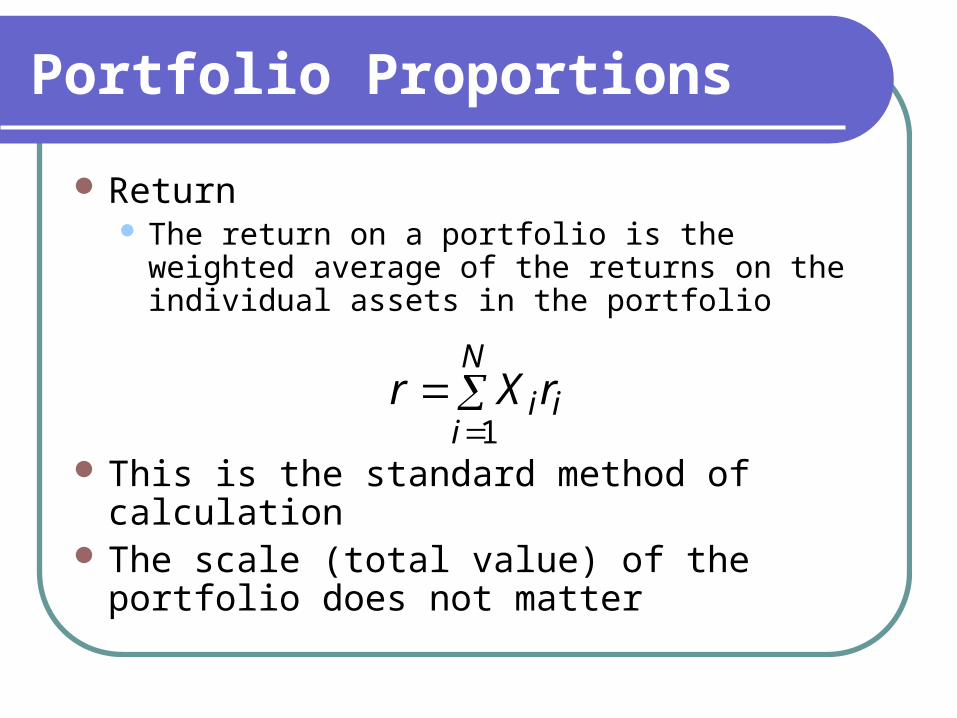

Portfolio Proportions

Return The return on a portfolio is the weighted average

of the returns on the individual assets in the portfolio

This is the standard method of calculation The scale (total value) of the portfolio does

not matter

N

iiirXr

1

Portfolio Proportions

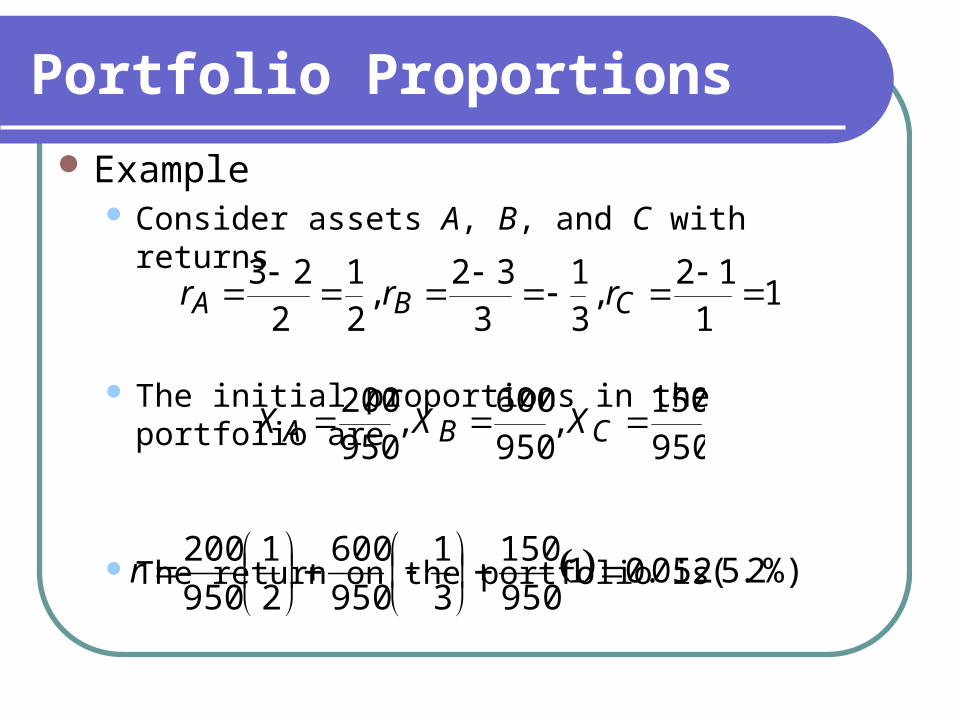

Example Consider assets A, B, and C with returns

The initial proportions in the portfolio are

The return on the portfolio is

11

12 ,

31

332

,21

223 CBA rrr

950150

,950600

,950200 CBA XXX

%)2.5( 052.01950

150

3

1

950

600

2

1

950

200

r

Portfolio Proportions

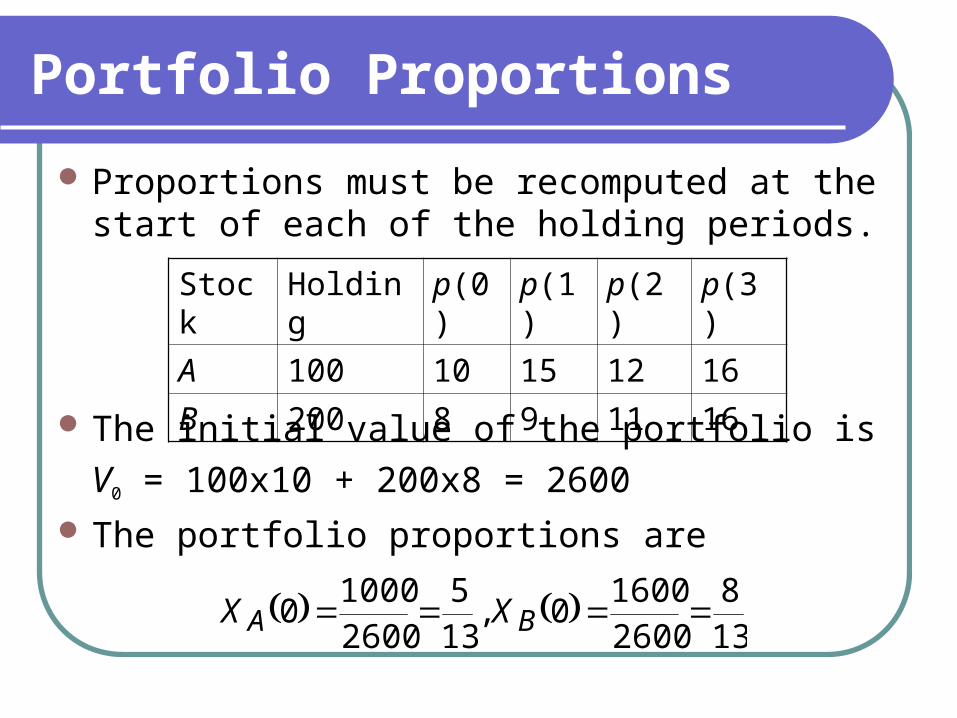

Proportions must be recomputed at the start of each of the holding periods.

The initial value of the portfolio is

V0 = 100x10 + 200x8 = 2600 The portfolio proportions are

Stock Holding p(0) p(1) p(2) p(3)

A 100 10 15 12 16

B 200 8 9 11 16

138

26001600

0,135

26001000

0 BA XX

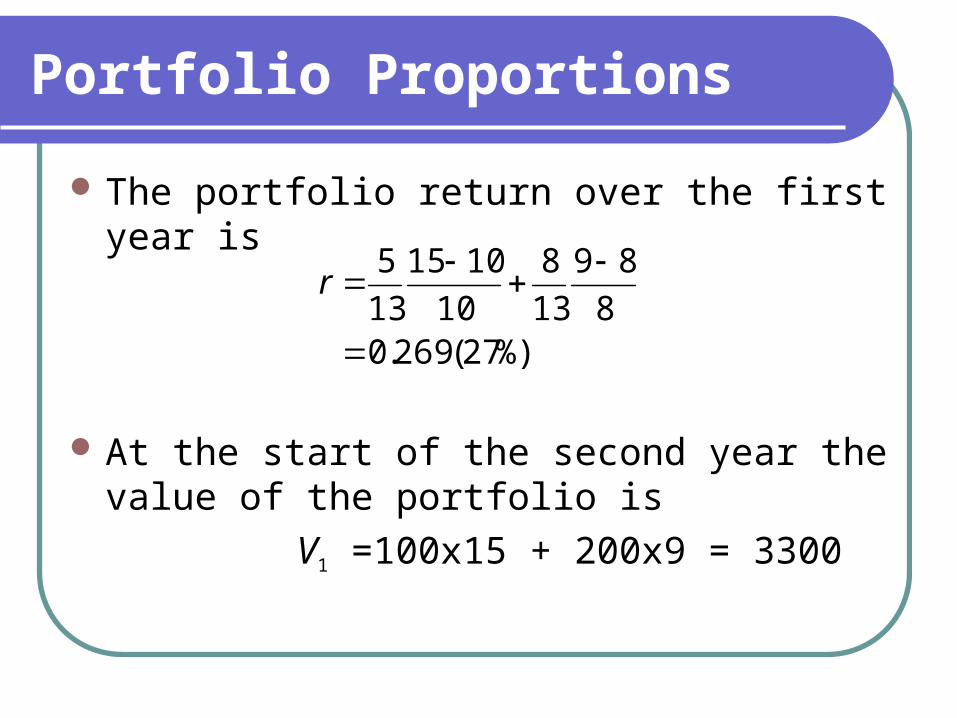

The portfolio return over the first year is

At the start of the second year the value of the portfolio is

V1 =100x15 + 200x9 = 3300

%)27( 269.08

89

13

8

10

1015

13

5

r

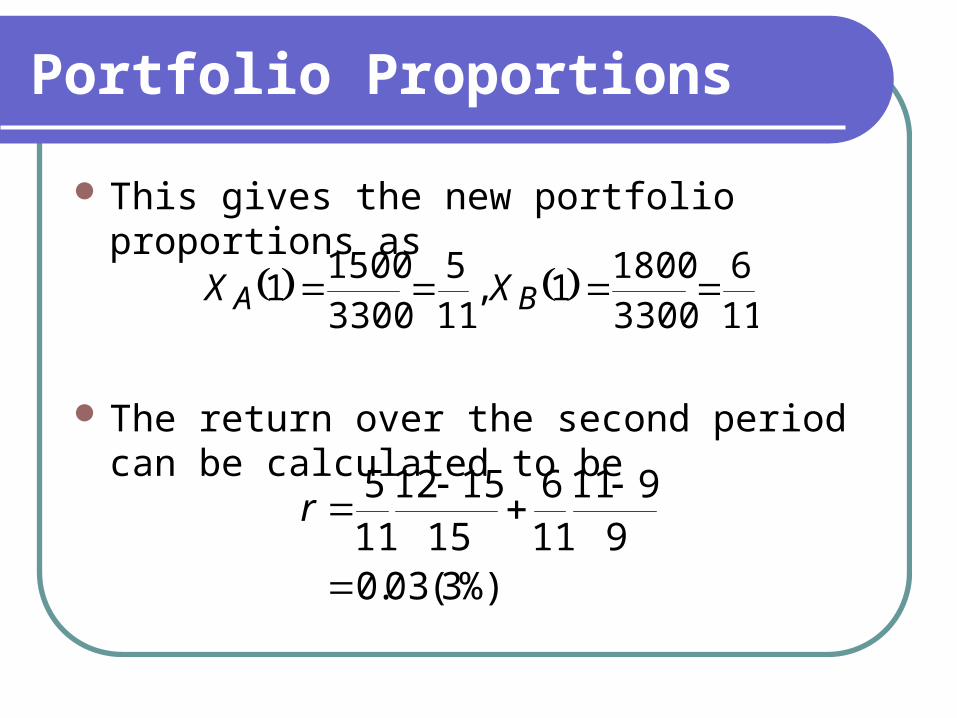

Portfolio Proportions

Portfolio Proportions

This gives the new portfolio proportions as

The return over the second period can be calculated to be

%)3( 03.09

911116

151512

115

r

116

33001800

1,115

33001500

1 BA XX

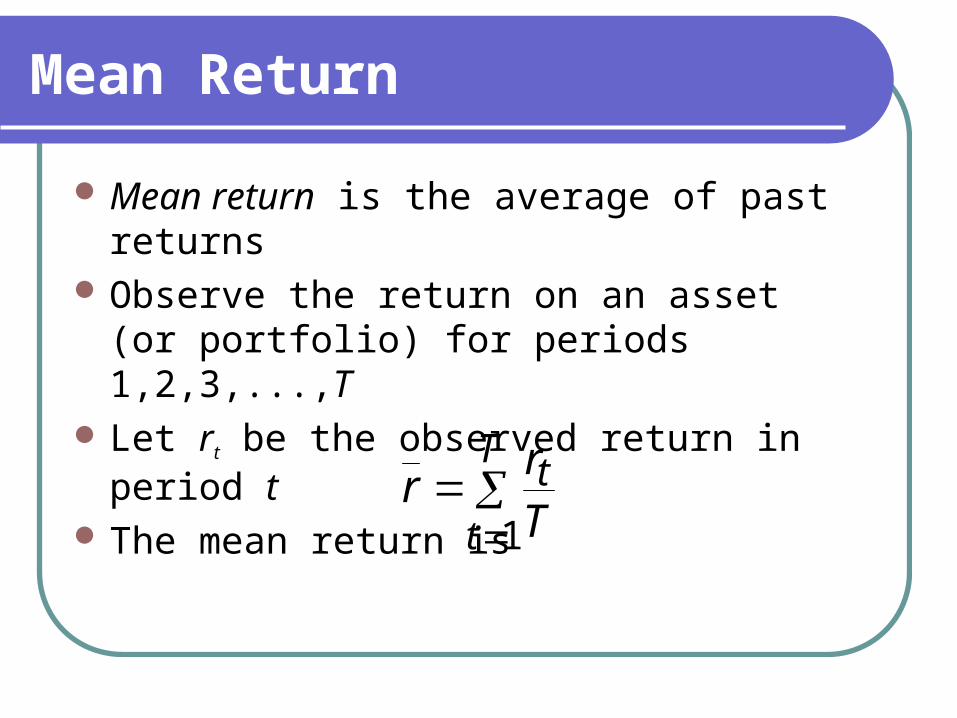

Mean Return

Mean return is the average of past returns Observe the return on an asset (or portfolio)

for periods 1,2,3,...,T Let rt be the observed return in period t The mean return is

T

t

tT

rr

1

Mean Return

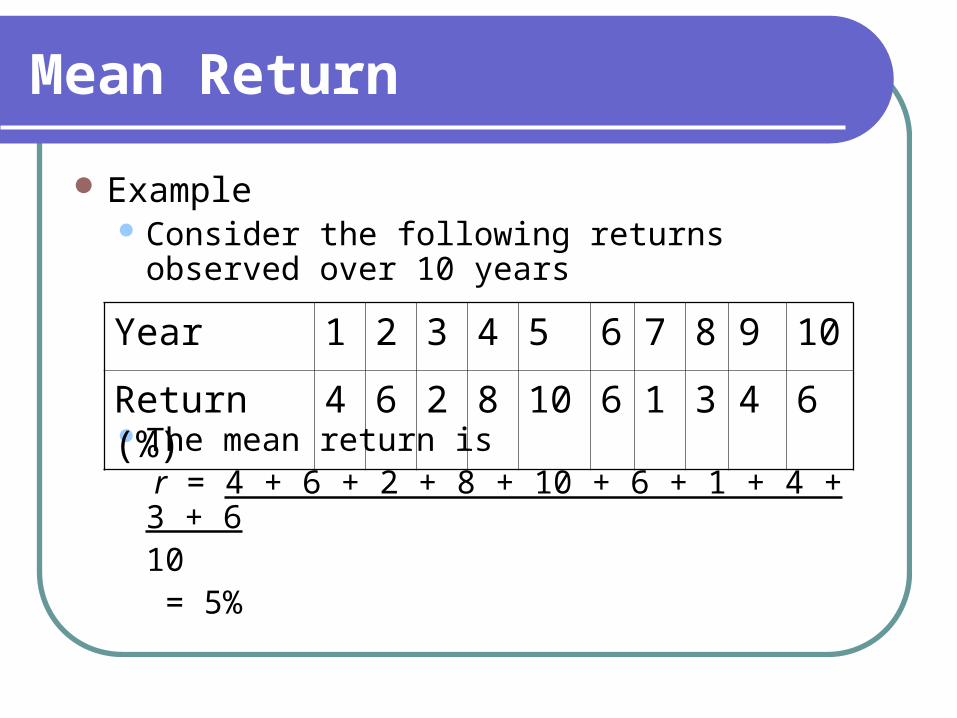

Example Consider the following returns observed over

10 years

The mean return is r = 4 + 6 + 2 + 8 + 10 + 6 + 1 + 4 + 3 + 6

10 = 5%

Year 1 2 3 4 5 6 7 8 9 10

Return (%) 4 6 2 8 10 6 1 3 4 6