investment idea - canara bank - buy

DESCRIPTION

TRANSCRIPT

November 8, 2010

www.fullertonsecurities.co.in Page | 1

CANARA BANK BUY Canara Bank started its operations in 1906. The bank is one of the largest nationalized

banks in India. It has completed more than 100 years in the Indian banking industry and

gone through many changes in its operations especially since nationalization program

undertaken by government of India.

• Canara bank has strong geographical presence with a total of 3066 branches spread

across all geographical areas.This will augment profitability of the business. The

management expects to reach total business to Rs. 5lac cr by the end of FY11.

• The Credit-Deposit ratio (CD) of bank stands at 71% and Capital Adequacy Ratio of 13.

88% well above the regulatory norms of 9%. This can allow bank to undertake more

risky advances and better profitability with higher yield on funds.

• CASA deposits stand at Rs.72000cr with a share of CASA deposit out of domestic

deposit at 30%. Management targets at around 32% for FY11.

• We estimate that Canara Bank`s Net Interest Income (NII) to grow at a CAGR of 40%

over FY2010-12E to Rs 112.4bn by FY2012. We also expect the PAT to grow at CAGR of

27% over FY10-FY12E to Rs.48.2bn.

Based on a consolidated FY12 P/B multiple of 1.75, the fair value for the

company works out to Rs. 899.

-20

0

20

40

60

80

100

120Canara Bank.

Sensex

STOCK DATABSE / NSE Code

Bloomberg Code

No. of Shares (Mn)

Sensex / Nifty

PRICE DATA

CMP Rs (5th Nov. 2010)

Beta

Market Cap ( Rs mn)

52 Week High-low

Average Daily Volume

STOCK RETURN (%)

30D 3M 6M 1Y

Canara Bank 22% 59% 75% 112%

Sensex 3% 16% 23% 31%

Nifty 3% 16% 23% 32%

SHARE HOLDING PATTERN (%)

Promoter

Institution

Non Institution

Total

1 Year Price Performance (Rel. to Sensex)

100.0

313,240

746.25 / 345

102,597

73.2

9.7

17.2

0.86

532483 / CANBK

CBK IN EQUITY

410

21,004 / 6,311

764.0

Recommendations <= 1 year 1 - 2 yrs 2 - 5 yrs

Strong Buy

Buy

Hold

Reduce

SellStrong Buy – Expected Returns > 20% p.a.

Buy – Expected Returns from 10 to 20% p.a.

Hold – Expected Returns from 0 % to 10% p.a.

Reduce – Expected Returns from 0 % to 10% p.a. with possible downside risk

Sell – Returns < 0 %

Projections (Rs Mn) FY2008 FY2009 FY2010 FY2011E FY2012E

Net Interest Income 35,377 47,106 56,750 92,808 112,409

Y-o-Y Growth % 33% 20% 64% 21%

Non-Interest Income 26,441 24,681 30,716 37,473 46,467

Y-o-Y Growth % -7% 24% 22% 24%

Total Income 168,713 195,966 218,274 294,516 367,475

Y-o-Y Growth % 16% 11% 35% 25%

PAT After MI 17,948 20,421 29,973 41,725 48,242

Y-o-Y Growth % 14% 47% 39% 16%

EPS Rs 43.8 49.8 73.1 101.8 117.7

Adj Book Value Rs 239.5 270.1 322.5 411.1 513.9

NIM % 2.18% 2.50% 2.45% 3.25% 3.19%

RoE % 16.64% 17.53% 21.72% 24.39% 22.33%

PER x 7.5 6.5

Price/ BV 1.6 1.3

Price/Adjusted BV 1.9 1.5

Financial Snapshot

November 8, 2010

www.fullertonsecurities.co.in Page | 2

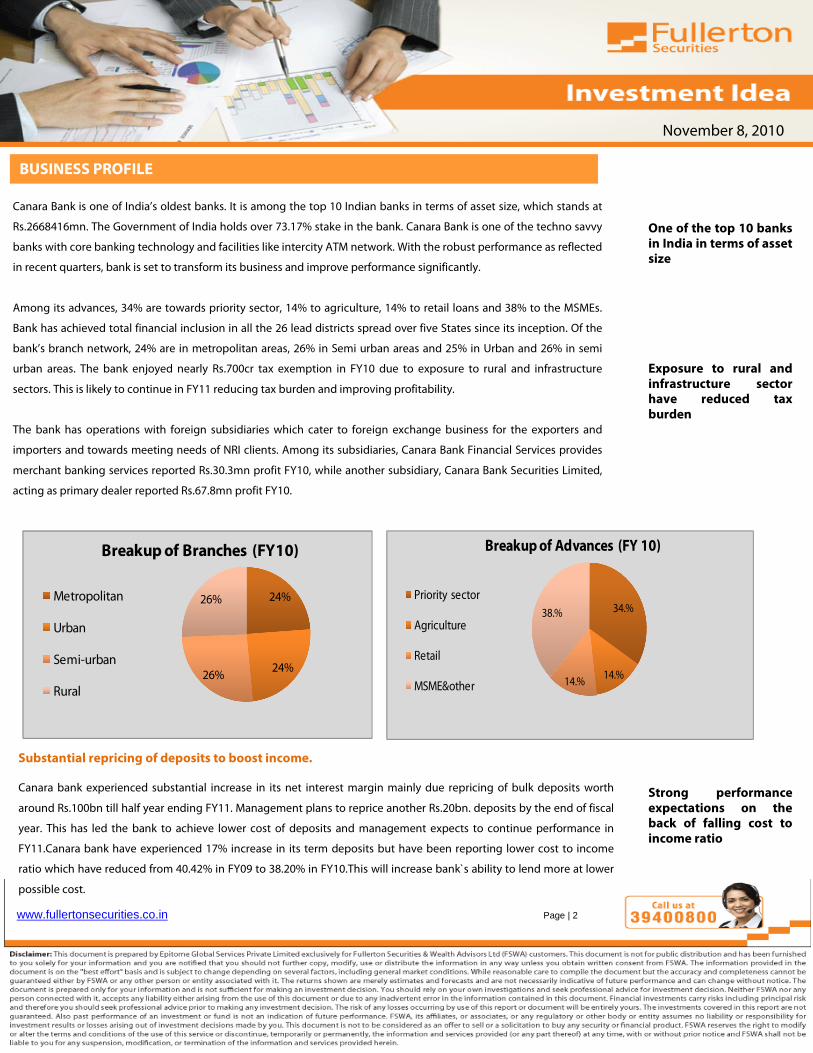

Canara Bank is one of India’s oldest banks. It is among the top 10 Indian banks in terms of asset size, which stands at

Rs.2668416mn. The Government of India holds over 73.17% stake in the bank. Canara Bank is one of the techno savvy

banks with core banking technology and facilities like intercity ATM network. With the robust performance as reflected

in recent quarters, bank is set to transform its business and improve performance significantly.

Among its advances, 34% are towards priority sector, 14% to agriculture, 14% to retail loans and 38% to the MSMEs.

Bank has achieved total financial inclusion in all the 26 lead districts spread over five States since its inception. Of the

bank’s branch network, 24% are in metropolitan areas, 26% in Semi urban areas and 25% in Urban and 26% in semi

urban areas. The bank enjoyed nearly Rs.700cr tax exemption in FY10 due to exposure to rural and infrastructure

sectors. This is likely to continue in FY11 reducing tax burden and improving profitability.

The bank has operations with foreign subsidiaries which cater to foreign exchange business for the exporters and

importers and towards meeting needs of NRI clients. Among its subsidiaries, Canara Bank Financial Services provides

merchant banking services reported Rs.30.3mn profit FY10, while another subsidiary, Canara Bank Securities Limited,

acting as primary dealer reported Rs.67.8mn profit FY10.

One of the top 10 banks in India in terms of asset size

Exposure to rural and infrastructure sector have reduced tax burden

Strong performance expectations on the back of falling cost to income ratio

Substantial repricing of deposits to boost income. Canara bank experienced substantial increase in its net interest margin mainly due repricing of bulk deposits worth

around Rs.100bn till half year ending FY11. Management plans to reprice another Rs.20bn. deposits by the end of fiscal

year. This has led the bank to achieve lower cost of deposits and management expects to continue performance in

FY11.Canara bank have experienced 17% increase in its term deposits but have been reporting lower cost to income

ratio which have reduced from 40.42% in FY09 to 38.20% in FY10.This will increase bank`s ability to lend more at lower

possible cost.

BUSINESS PROFILE

24%

24%26%

26%

Breakup of Branches (FY10)

Metropolitan

Urban

Semi-urban

Rural

34.%

14.%14.%

38.%

Breakup of Advances (FY 10)

Priority sector

Agriculture

Retail

MSME&other

November 8, 2010

www.fullertonsecurities.co.in Page | 3

Strong yearly performance along with good quarterly results augers well. Canara Bank`s interest income grown to Rs.187558million in FY10, registering YOY growth of 9% compared to last fiscal

year. Non interest income also rose to Rs.30716milion in FY10 showing growth of 24% since last financial year. Ability to

attract low cost deposit and strong resistance to high cost deposits reduced the cost of deposits to 6% in FY10. Bank

however experienced dip in yield on funds to 9.81% in FY10 against 10.79% in FY09. The bank could maintain net

interest margin of 2.45% in FY10.

The Bank reported 3.16% net interest margin for the Q2 FY11 as the cost of funds fell to 5.69%. It has increased thrust on

fee based income like cross selling of insurance, mutual funds, online trading services which resulted in increase in fee

based income during Q2FY11 to Rs.3520mn.

Strong results recording impressive growth in NII and non interest income

Reported NIM of 3.16% in Q2 FY11.

Strong income growth and improving margins to boost profitability.

BUSINESS PERFORMANCE

Peer Comparison

Compared to its peers, Canara Bank is operating at 2.45% NIM, whereas market leader SBI, also posted 2.45% NIM in

FY10. However PNB reported 3% NIM for FY10, on the back of reduced cost of deposits and higher yield on funds than

that of Canara Bank. As far as asset quality is concerned, Canara Bank`s Net NPA ratio to net advances stands at 1.09%

on account of its high exposure to rural and agriculture Sectors. Canara Bank have been able to maintain 21.72% ROE

on the back of effective cost cutting measures undertaken during FY10.

0.0%

1.0%

2.0%

3.0%

4.0%

0.00

50.00

100.00

150.00

200.00

FY08 FY09 FY10 FY11E FY12E

Rs

Bn

.

Strong Income Growth & Improving

Margins

Operating Income Net Interest Income NIM

0

1000

2000

3000

4000

FY08 FY09 FY10 FY11E FY12E

Advances & Deposits (Rs. Bn)

Advances Deposits

Peer Group Comparsion

CompaniesTotal

Income

NIM

Margins

%

Net NPA

Ratio %RoE % ROA % P/Adj BV (x) CMP FV

Canara Bank 218,274 2.45% 1.09% 21.7% 1.2% 2.36 764 10

PNB 255,220 3.0% 0.5% 21.0% 1.3% 2.50 1369 10

SBI 1,352,160 2.5% 1.7% 14.0% 0.8% 2.62 3441 10

BOB 206,240 2.4% 0.3% 20.0% 1.1% 2.40 1036 10

* FY10 figures

November 8, 2010

www.fullertonsecurities.co.in Page | 4

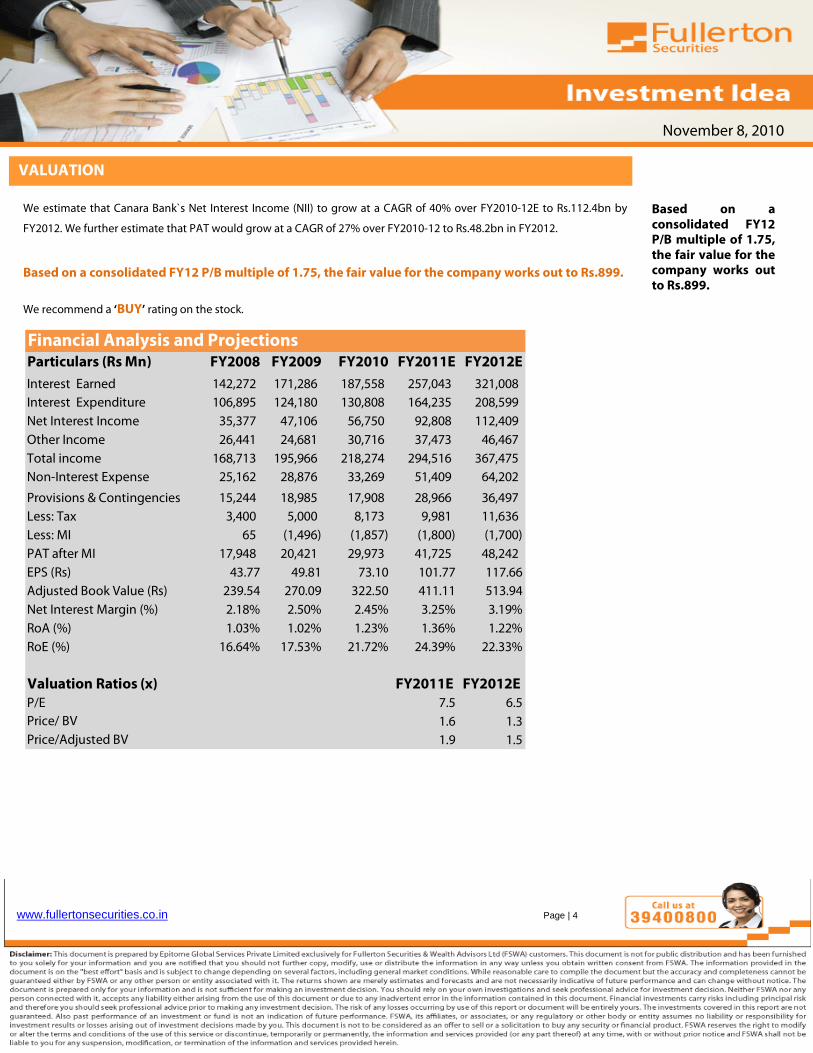

Based on a consolidated FY12 P/B multiple of 1.75, the fair value for the company works out to Rs.899.

VALUATION We estimate that Canara Bank`s Net Interest Income (NII) to grow at a CAGR of 40% over FY2010-12E to Rs.112.4bn by

FY2012. We further estimate that PAT would grow at a CAGR of 27% over FY2010-12 to Rs.48.2bn in FY2012.

Based on a consolidated FY12 P/B multiple of 1.75, the fair value for the company works out to Rs.899.

We recommend a ‘BUY’ rating on the stock.

Particulars (Rs Mn) FY2008 FY2009 FY2010 FY2011E FY2012E

Interest Earned 142,272 171,286 187,558 257,043 321,008

Interest Expenditure 106,895 124,180 130,808 164,235 208,599

Net Interest Income 35,377 47,106 56,750 92,808 112,409

Other Income 26,441 24,681 30,716 37,473 46,467

Total income 168,713 195,966 218,274 294,516 367,475

Non-Interest Expense 25,162 28,876 33,269 51,409 64,202

Provisions & Contingencies 15,244 18,985 17,908 28,966 36,497

Less: Tax 3,400 5,000 8,173 9,981 11,636

Less: MI 65 (1,496) (1,857) (1,800) (1,700)

PAT after MI 17,948 20,421 29,973 41,725 48,242

EPS (Rs) 43.77 49.81 73.10 101.77 117.66

Adjusted Book Value (Rs) 239.54 270.09 322.50 411.11 513.94

Net Interest Margin (%) 2.18% 2.50% 2.45% 3.25% 3.19%

RoA (%) 1.03% 1.02% 1.23% 1.36% 1.22%

RoE (%) 16.64% 17.53% 21.72% 24.39% 22.33%

Valuation Ratios (x) FY2011E FY2012E

P/E 7.5 6.5

Price/ BV 1.6 1.3

Price/Adjusted BV 1.9 1.5

Financial Analysis and Projections

November 8, 2010

www.fullertonsecurities.co.in Page | 5

Board of Directors

Director Name Current Position Description

S. Raman.Chairman &Managing

Director.

S. Raman is the new chairman and managing director of Canara bank. Raman joined Bank of India in 1974.

He also had two stints overseas when he was serving Bank of India - at Jersey (UK) Raman was elevated as

Executive Director of Union Bank of India in October 2008 where he oversaw treasury, corporate credit and

transaction banking, among others. He worked in different parts of the country, including Nagpur,

Hyderabad, New Delhi, Pune, Ahmedabad, Mumbai and Bhubaneshwar. His assignments included being

Zonal Manager in Gujarat and Orissa. A Post Graduate in Economics, Raman holds a Diploma in Business

Management and a Senior Diploma in German Language, besides CAIIB from the Indian Institute of

Bankers and ACIB from the Chartered Institute of Bankers, London from 1983 to 1987 and as Chief

Executive of Bank of India's US Operations from June 2005 to October 2008, a press statement issued here

stated.

K.L. Jagdish Pai. Executive Director.Jagadish Pai K L, who was functioning as the general manager in the Human Resources Development

wing of Bank of India, has taken over charge as the executive director.

H.S. Upendra Kamath. Executive Director.Shri. H. S. Upendra Kamath is Executive Director of Canara Bank with effect from March 26, 2009. He is

General Manager of Union Bank of India.

G. Padmanabhan. Director. He is working as an Executive Director on the board of Canara Bank.

Thomas Mathew Director. Dr. Thomas Mathew has been appointed as Director of Canara Bank. He is a Nominee of Central

Government.Yogendra Pati Tripati.

Non official part time

director.He Represents as non official part time director on the board of Canara Bank.

Devendra das Rastogi. Employee director. He works as a representative of employee on board of director.

Sunil Gupta Director. He represents shareholders on the board of Canara bank.

Babu Nagesh Company secretary He is working as a company secretary in Canara Bank.

Pasha Shabeer. Non executive director. He is working as non executive director on the board of Canara Bank.