investment in ireland and the eu - european … · investment in ireland and the eu . debora...

TRANSCRIPT

Investment in Ireland and the EU

Debora Revoltella Director

Economics Department

Dublin

April 10, 2017

20/04/2017 1

Real investment: IE v EU country groupings

20/04/2017 European Investment Bank Group 2

Real investment (2008 = 100)

Source: EIB, based on Eurostat National Accounts

40

60

80

100

120

140

160

180

IE Core Cohesion Periphery

-35.00

-15.00

5.00

25.00

45.00

65.00

1Q05 3Q06 1Q08 3Q09 1Q11 3Q12 1Q14 3Q15

Financial corporations Government HH NFC Total

-35.00

-15.00

5.00

25.00

45.00

65.00

1Q05 3Q06 1Q08 3Q09 1Q11 3Q12 1Q14 3Q15

Financial corporations Government HH NFC Total

Real investment: Sector-level

20/04/2017 European Investment Bank Group 3

Note: Includes 2016 revisions Source: EIB, based on Eurostat Sectoral Accounts

Real GFCF by institutional sector (4Q 2008 = 100)

IE EU28

-40

-20

0

20

40

60

80

100

1Q05

1Q06

1Q07

1Q08

1Q09

1Q10

1Q11

1Q12

1Q13

1Q14

1Q15

1Q16

IPP DwellingsOther structures Machinery & EquipmentOther Total

Real investment by asset

20/04/2017 European Investment Bank Group 4

Source: EIB, based on National Accounts and Eurostat

Real GFCF by asset class (1Q 2008 = 100) EU28 IE

-40

-20

0

20

40

60

80

100

IPP DwellingsOther structures Machinery & EquipmentOther Total

Infrastructure investment

20/04/2017 European Investment Bank Group 5

Source: EIB, based on Eurostat National Accounts

0

0.5

1

1.5

2

2.5

3

3.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

% o

f GD

P

Government Corporate PPP Non-PPP Proejct

0

0.5

1

1.5

2

2.5

3

3.5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

% o

f GD

P

Utilities Transport Communication Education Health

Infrastructure investment in per cent of GDP

EIB Investment Survey (EIBIS)

• Annual survey commenced 2Q 2016

• Some 12,500 firms surveyed across EU28 (of which 400 in Ireland)

• NFCs with 5+ employees operating in manufacturing, services, construction &

infrastructure

• Qualitative and quantitative information on: • firm characteristics and performance • Investment needs and constraints • past investment activities and future focus • sources of finance

• Representative of the economy (firms weighted by value-added)

20/04/2017 European Investment Bank Group 6

20/04/2017 European Investment Bank Group 7

The share of Irish firms investing is already high and, on balance, these expect to mildly expand investment

Investment cycle

Medium/Large

Micro/Small Infrastructure

Services

Construction

Manufacturing IE

EU

IT

LV

LT

LU

MT

NL PL PT

RO

SK

SI

ES

SE UK AT

BE

BG

HR

CY

CZ

DK EE

FI

FR

DE GR

HU

-0.150

-0.100

-0.050

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.600 0.650 0.700 0.750 0.800 0.850 0.900 0.950 1.000

Low investment expanding High investment expanding

Low investment contracting High investment contracting

This graphs plots the average share of firms that invested in the previous financial year (x-axis) against the net difference between those intending to expand and those expecting to contract investment in coming year .

0%

20%

40%

60%

80%

100%

EU

Irela

nd

Man

ufac

turin

g

Con

stru

ctio

n

Serv

ices

Infra

stru

ctur

e

Mic

ro/S

mal

l

Med

ium

/Lar

ge

Organisation/business processes

Training of employees

Software, data, IT,website

R&D

Machinery andequipment

Land, business buildingsand infrastructure

Investment areas

Q. In the last financial year, how much did your business invest in each of the following with the intention of maintaining or increasing your company’s future earnings?

**The blue bars indicate the proportion of firms who have invested in the last financial year. A firm is considered to have invested if it spent at least EUR 500 per employee on investment activities. Investment intensity is the median investment per employee of investing firms.

0%

2%

4%

6%

8%

10%

12%

EL ES IT SK DE

HU PT AT CZ

EU18 SI DK

UK NL

US FI FR BE IE SE

Investment into intangibles

Share of Irish firms’ investment into intangibles highest in the EU, with machinery further crowded out by property

20/04/2017 European Investment Bank Group 8

Source: INTAN invest

%

20%

40%

60%

80%

100%

Irela

nd

Man

ufac

turin

g

Con

stru

ctio

n

Serv

ices

Infra

stru

ctur

e

Mic

ro/S

mal

l

Med

ium

/Lar

ge

At or above capacity EU average

Share of firms operating at or above capacity

9

%

20%

40%

60%

80%

100%

Luxe

mbo

urg

Mal

taAu

stria

Esto

nia

Rom

ania

Den

mar

kPo

rtuga

lPo

land

Ger

man

yN

ethe

rland

sU

KC

ypru

sH

unga

ryC

zech

Rep

Irela

ndBu

lgar

iaC

roat

iaSl

ovak

iaBe

lgiu

mIta

lySl

oven

iaSw

eden

Spai

nFi

nlan

dG

reec

eLa

tvia

Fran

ceLi

thua

nia

Full capacity is the maximum capacity attainable under normal conditions e.g., company’s general practices regarding the utilization of machines and equipment, overtime, work shifts, holidays etc. Q. In the last financial year, was your company operating above or at maximum capacity attainable under normal circumstances?

Share of firms at or above full capacity

%

20%

40%

60%

Mal

taSp

ain

Aust

riaG

erm

any

Italy

Slov

akia

Irela

ndH

unga

ryC

roat

iaN

ethe

rland

sSl

oven

iaBu

lgar

iaD

enm

ark

Belg

ium

Latv

ia UK

Rom

ania

Esto

nia

Luxe

mbo

urg

Swed

enPo

rtuga

lC

zech

Rep

Fran

ceFi

nlan

dPo

land

Lith

uani

a

Energy efficient building stock

Base: All firms Q. What proportion, if any, of your commercial building stock satisfies high or highest energy efficiency standards? Data not shown for Greece and Cyprus, as the Greek translation may have influenced interpretation of the question. This will be addressed in the next round of interviews.

%

20%

40%

60%

Ger

man

yAu

stria

Hun

gary

Mal

taSl

oven

iaIta

lySp

ain

Net

herla

nds

Luxe

mbo

urg

Esto

nia

Latv

iaBe

lgiu

mIre

land

Den

mar

kC

roat

iaSl

ovak

iaPo

rtuga

lFi

nlan

dC

zech

Rep

Rom

ania

Swed

enFr

ance

Lith

uani

aU

KPo

land

Bulg

aria

State-of-the-art machinery & equipment

Base: All firms Q. What proportion, if any, of your machinery and equipment, including ICT, would you say is state-of-the-art? Data not shown for Greece and Cyprus, as the Greek translation may have influenced interpretation of the question. This will be addressed in the next round of interviews.

Perceived investment gap

20/04/2017 European Investment Bank Group 10

0%

20%

40%

60%

80%

100%

Cyp

rus

Lith

uani

aSl

oven

iaG

reec

eC

roat

iaLa

tvia

Hun

gary

Den

mar

kR

oman

iaEs

toni

aPo

land

Slov

akia

Bulg

aria

Spai

nC

zech

Rep

Ger

man

yU

KIre

land

Portu

gal

Fran

ceM

alta

Swed

enLu

xem

bour

gN

ethe

rland

sFi

nlan

dBe

lgiu

mIta

lyAu

stria

Too much About the right amount Too little Don’t know

Perceived investment gap by country

Q. Looking back at your investment over the last 3 years, was it too much, too little, or about the right amount to ensure the success of your business going forward?

Quality of capital stock

0%

20%

40%

60%

80%

100%

EU

Irela

nd

Man

ufac

turin

g

Con

stru

ctio

n

Serv

ices

Infra

stru

ctur

e

Mic

ro/S

mal

l

Med

ium

/Lar

ge

Q. Looking ahead to the next 3 years, which of the following is your investment priority (a) replacing existing buildings, machinery, equipment, IT (b) expanding capacity for existing products/services (c) developing or introducing new products, processes, services?

0%

20%

40%

60%

80%

100%

Cro

atia

Rom

ania

Den

mar

kSl

ovak

iaN

ethe

rland

sC

ypru

sC

zech

Rep

Pola

nd UK

Ger

man

yAu

stria

Latv

iaG

reec

eLi

thua

nia

Swed

enBu

lgar

iaSp

ain

Hun

gary

Esto

nia

Luxe

mbo

urg

Italy

Slov

enia

Belg

ium

Irela

ndM

alta

Finl

and

Portu

gal

Fran

ce

Capacity expansion Replacement New products/services No investment planned

Investment focus over coming three years

11

Future investment priorities by country Irish firms’ future investment priorities by sector

Technology: Investment to modernise stock

20/04/2017 European Investment Bank Group 12

0%

20%

40%

60%

80%

100%

CZ DK FI IT SK ES UK HR PL IE SE CY BE HU NL PT DE FR MT LU LV LT RO BG EL SI AT EE

Investment in new products, processes or services that are new to the company, new to the country or new to the global market?

Did not invest in new products New to the company New to the country New to the global market

Base: All firms that invested in the last financial year (excluding don’t know/refused responses) Q. Were the new products, process or services (a) new to the company; (b) new to the country; (c) new to the global market?

0% 20% 40% 60% 80% 100%

Uncertainty about the future

Availability of finance

Adequate transport infrastructure

Business regulations

Labour market regulations

Access to digital infrastructure

Energy costs

Availability of staff with right skills

Demand for products or services

A major obstacle A minor obstacle

0% 20% 40% 60% 80% 100%

Uncertainty about the future

Availability of external finance

Adequate transport infrastructure

Business regulations

Labour market regulations

Access to digital infrastructure

Energy costs

Availability of staff with right skills

Demand for products or services

Firms that invested sufficiently Firms that invested too little

Long-term barriers to investment

Long-term barriers to investment: uncertainty & skilled labour

20/04/2017 European Investment Bank Group 13

Q. Thinking about your investment activities in Ireland, to what extent is each of the following an obstacle? Is a major obstacle, a minor obstacle or not an obstacle at all?

Long-term barriers by investment sufficiency

0%

20%

40%

60%

80%

100%

EU

Man

ufac

turin

g

Con

stru

ctio

n

Serv

ices

Infra

stru

ctur

e

SME

Larg

e

Bank loan

Other bank finance

Bonds

Equity

Leasing

Factoring

Loans fromfamily/friends

Grants

Other

Very high reliance on internal finance

20/04/2017 European Investment Bank Group 14

0%

20%

40%

60%

80%

100%

EU

Irela

nd

Man

ufac

turin

g

Con

stru

ctio

n

Serv

ices

Infra

stru

ctur

e

Mic

ro/S

mal

l

Med

ium

/Lar

ge

External Internal Intra-group

Q. Approximately what proportion of your investment in the last financial year was financed by each of the following?

Type of financing used for investment

Q. Approximately what proportion of your external finance does each of the following represent?

Access to finance: a story of two worlds

20/04/2017 European Investment Bank Group 15

PT

EL

HU

HR CY

IE

MT

BG LT

RO

SL IT

LV

NL

SK

ES

UK

AT

DE

PL

BE

DK

FR

EE FI

CZ

LU

SE

0%

5%

10%

15%

20%

25%

30%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Shar

e of

inve

stin

g fir

ms

that

are

hap

py to

rely

ex

cl. o

n in

tern

al fu

nds

Share of investing firms that are external finance constrained

High availability of internal sources; high external barriers

little availability of internal sources; high external barriers

high availability of internal sources; low external barriers

little availability of internal sources; low external barriers

Base: All firms

Finance constrained firms include: those that invested which dissatisfied with the amount of finance obtained (received less), firms that sought external finance but did not receive it (rejected) and those who did not seek external finance because they thought borrowing costs would be too high (too expensive) or they would be turned down (discouraged) Firms happy to use internal funds are those that invested using exclusively internal funds and who stated that they did not seek any external finance because they were satisfied with their internal funds.

Internally financed vs. financially constrained

0% 20% 40% 60% 80% 100%

Amount obtained

Cost of finance

Maturity

Collateral

Type of finance

Very satisfied Fairly satisfied NeitherFairly dissatisfied Very dissatisfied

0%

5%

10%

15%

20%

Portu

gal

Cyp

rus

Gre

ece

Mal

taBu

lgar

iaC

roat

iaH

unga

ryIre

land

Rom

ania

Lith

uani

aSl

oven

iaLa

tvia

Italy

Net

herla

nds

Slov

akia

Spai

nAu

stria

Belg

ium

Ger

man

yU

KD

enm

ark

Esto

nia

Fran

cePo

land

Finl

and

Cze

ch R

epLu

xem

bour

gSw

eden

Rejected Received less Too expensive Discouraged

Share of financially constrained firms

Financially constrained firms

20/04/2017 European Investment Bank Group 16

Base: All firms; Finance constrained firms include: those dissatisfied with the amount of finance obtained (received less), firms that sought external finance but did not receive it (rejected) and those who did not seek external finance because they thought borrowing costs would be too high (too expensive) or they would be turned down (discouraged)

Satisfaction with external finance

Q. How satisfied or dissatisfied are you with …?

Brexit

20/04/2017 European Investment Bank Group 17

0%

20%

40%

60%

80%

100%

positive negative no impact Don't know/refused

Expected effect of outcome of Brexit referendum on investment activities

Q. How do you expect the outcome of the UK referendum on EU membership to affect your investment activities in the coming year?

Summary Survey findings for Ireland

• Investment continues to recover, though data and accounting particularities

related to multinationals blur the picture.

• Infrastructure investment severely hit and continued to suffer through 2015,

with the impact of fiscal constraints on public sector capital investment driving;

• High private sector propensity to invest ongoing, with rotation toward catch-

up in construction and services; elevated share of smaller firms not investing;

• Main barriers to investment are uncertainty, lack of skills, energy costs, and

digital infrastructure; external finance a limiting factor for firms that underinvested.

• Polarised world of financing needs, with a high share of firms relying on

internal finance, including intra-group, and most of the remainder on banking, with

an elevated share of firms experiencing constraints, especially smaller and

younger firms; cost and collateral requirements are important.

20/04/2017 European Investment Bank Group 18

Thank you!

19

Annex

20/04/2017 European Investment Bank Group 20

0%

20%

40%

60%

80%

100%

EU

Irela

nd

Man

ufac

turin

g

Con

stru

ctio

n

Serv

ices

Infra

stru

ctur

e

Mic

ro/S

mal

l

Med

ium

/Lar

ge

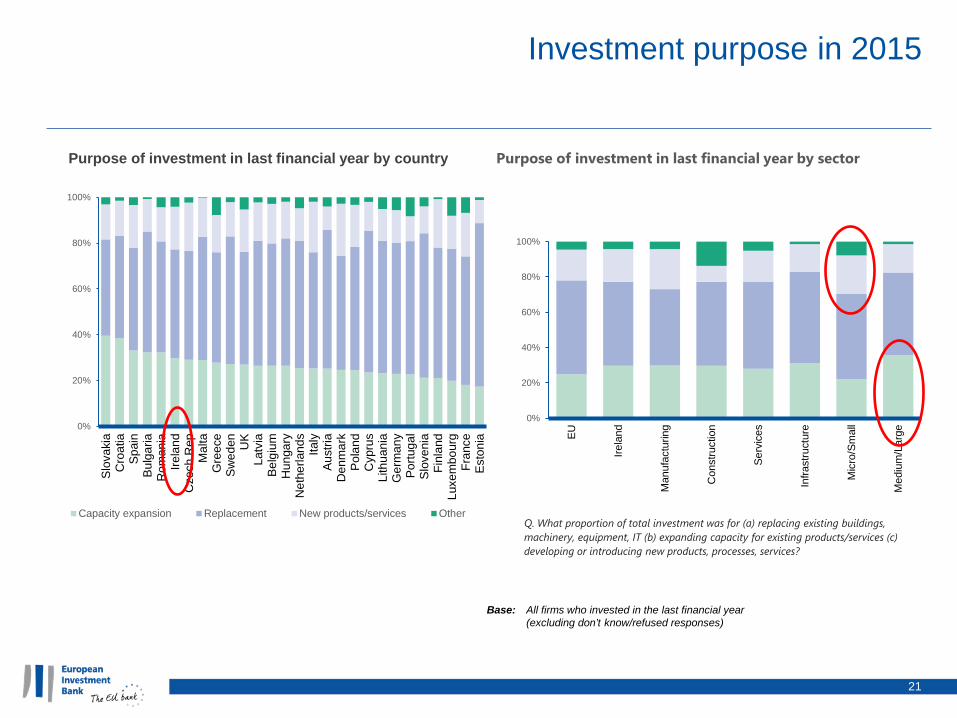

Purpose of investment in last financial year by sector

0%

20%

40%

60%

80%

100%

Slov

akia

Cro

atia

Spai

nBu

lgar

iaR

oman

iaIre

land

Cze

ch R

epM

alta

Gre

ece

Swed

en UK

Latv

iaBe

lgiu

mH

unga

ryN

ethe

rland

sIta

lyAu

stria

Den

mar

kPo

land

Cyp

rus

Lith

uani

aG

erm

any

Portu

gal

Slov

enia

Finl

and

Luxe

mbo

urg

Fran

ceEs

toni

a

Capacity expansion Replacement New products/services Other

Investment purpose in 2015

21

Purpose of investment in last financial year by country

Base: All firms who invested in the last financial year (excluding don’t know/refused responses)

Q. What proportion of total investment was for (a) replacing existing buildings, machinery, equipment, IT (b) expanding capacity for existing products/services (c) developing or introducing new products, processes, services?

External finance

20/04/2017 European Investment Bank Group 22

Satisfaction with external finance

0% 20% 40% 60% 80% 100%

Amount obtained

Cost of finance

Maturity

Collateral

Type of finance

Very satisfied Fairly satisfied Neither Fairly dissatisfied Very dissatisfied

Q. How satisfied or dissatisfied are you with …?

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Received Less Rejected Too Expensive Discouraged

Base: All firms; Finance constrained firms include: those dissatisfied with the amount of finance obtained (received less), firms that sought external finance but did not receive it (rejected) and those who did not seek external finance because they thought borrowing costs would be too high (too expensive) or they would be turned down (discouraged)

Productivity On average, Irish firms are more productive than their EU counterparts

Average firm-level TFP growth is falling in IE but the growth rate is higher than in the EU

70

80

90

100

110

120

130

2006-2008 2009-2011 2012-2014Inde

x (1

00 =

med

ian

TFP

for t

he E

U in

200

6-20

08)

Distribution of firm-level TFP in Ireland

p10 p50 p90 mean

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

EU IE Core Periphery Cohesion

2006-2008 2009-2011 2012-2014

Note: Core: AT BE DE DK FI FR SE UK; Periphery: EL ES IE IT PT SI; Cohesion: BG CZ EE HU PL RO SK. Source: ECON calculations based on the Bureau Van Dijk’s Orbis database.