investment opportunities in nigeria and the diasporaand...

TRANSCRIPT

InvestmentInvestment opportunities in Nigeria and the Diasporaand the Diaspora

Ni i i th S MilNigerians in the Square Mile (NISM). London

Table of content

1 Overview of Nigerian macroeconomic environment / 21 investment climate 2

Assessment of key sectors2 6

- Financial services industry 6

- Energy & Natural Resources 10

C G d 17- Consumer Goods 17

- Telecommunication industry 21- Telecommunication industry 21

3 Market Entry Options 23

1© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

Overview of Nigerian macroeconomic environment / Investment ClimateInvestment Climate

Nigeria……a quick glance

US$169 billionUS$289 3 billion US$169 billion Annual disposable income in 2012

US$6 2 billion

US$289.3 billionNigeria’s nominal GDP in 2012, makes it the

second largest economy in Sub-Saharan Africa in 2012 US$6.2 billion

FDI inflows in 2012

US$835 86.8%

Nigeria’s projected GDP growth for 2013 one of the US$835.8Consumer spending capital in 2012

3 2%

g p j gfastest growing economies

167 million 3.2%External debt to GDP ratio in 2012

12 81 million

Nigeria’s population in 2012 with average growth of 2.6%

5% 12.81 millionActive internet connections with 30.1%

penetration rate

5%CAGR of consumer spending between 2007 and

2012

113 millionMobile phone subscribers with 67.8%

penetration rate

51%Nigeria’s population are urban dwellers in 2012

3© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

penetration rate1. Economist Intelligence Unit2. National Bureau of Statistics (NBS) revised 2010 and estimates for Q4 2011 GDP report3. MPC Communique – January 2012

Nigeria’s economic growth is expected to remain strongstrong…

9%700Historical and forecast GDP and annual growth

32%35%

Key sector growth (2011 - 2012)

639

6.0%7.0%

7.9%7.5%

6.7%6.7%

7.2%6.8%

7.1%7.0%

4%5%6%7%8%

300

400

500

600

'bill

ion

13% 13% 12% 10% 10% 10% 8%5% 4% 4%

5%

15%

25%

35%

208 169 196 244 289 334 382 443530

0%1%2%3%4%

0

100

200

300

8 9 0 2 3 4 5 6 7

US

$

-0.90%-5%

5%

Tele

com

s

min

eral

s

uild

ing

&

nstru

ctio

n

Res

tura

nt

le&

Ret

ai;

eal e

stat

e

s se

rvic

es

nufa

ctui

rn

Oth

ers

gric

ultu

re

FSI

Oil&

Gas

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

GDP GDP growth

Source: Economist Intelligent Unit: Data & statistics Source: Central Bank of Nigeria: GDP Report Q1 2013

T

Sol

id Bu

Con

Hot

els

& R

Who

lesa R

e

Bus

ines

s

Man A

g

Key factors that will drive growth include increasedprivate consumption and higher crude oil production

Growth will be driven primarily by non-oil sectors23% 17% 18% 20% 23% 17% 19% 21%

25% 26% 24% 27% 27% 28% 25% 28%

60%

80%

100%

Sector contribution to GDP

including agriculture, trade & commerce,telecommunications, building & construction

Successful completion of key reforms such asf f

35% 42% 44% 39% 34% 41% 43% 38%

17%15% 14%

14% 16%14% 13%

13%

23% 20% 23% 17% 21%

20%

40%

60%

privatization of the power sector, enactment of thepetroleum industry bill, will also contribute to thegrowth of the economy

0%Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2011 2012

Agriculture Oil & Gas Wholesale & retail Others

4© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

Source: Central Bank of Nigeria: GDP Report Q1 2013

Agriculture Oil & Gas Wholesale & retail Others

Key drivers of the Nigerian investment climate…

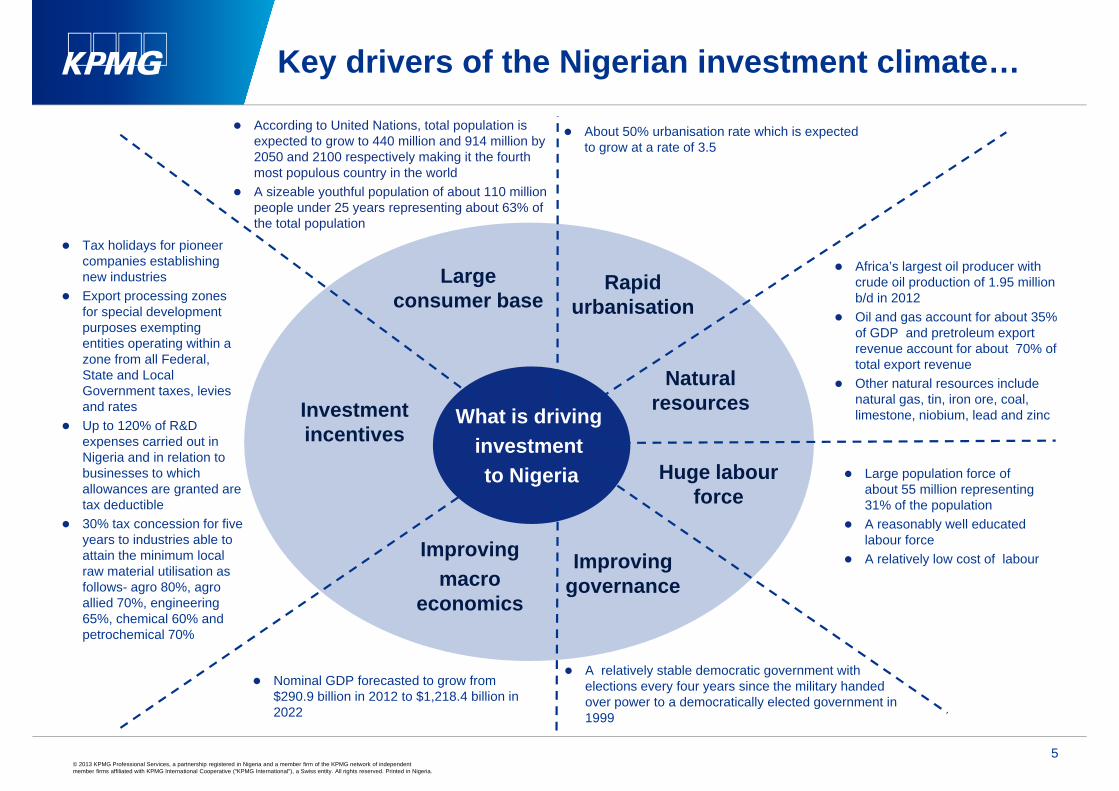

According to United Nations, total population is expected to grow to 440 million and 914 million by 2050 and 2100 respectively making it the fourth most populous country in the world

About 50% urbanisation rate which is expected to grow at a rate of 3.5

most populous country in the world A sizeable youthful population of about 110 million

people under 25 years representing about 63% of the total population

Tax holidays for pioneer companies establishing Af i ’ l t il d ith

Rapid urbanisation

Large consumer base

companies establishing new industries

Export processing zones for special development purposes exempting entities operating within a

Africa’s largest oil producer with crude oil production of 1.95 million b/d in 2012

Oil and gas account for about 35% of GDP and pretroleum export revenue account for about 70% of

Natural resourcesInvestment

incentivesWhat is driving

i t t

zone from all Federal, State and Local Government taxes, levies and rates

Up to 120% of R&D expenses carried out in

revenue account for about 70% of total export revenue

Other natural resources include natural gas, tin, iron ore, coal, limestone, niobium, lead and zinc

Huge labour force

incentives investment to Nigeria

expenses carried out in Nigeria and in relation to businesses to which allowances are granted are tax deductible

30% tax concession for five

Large population force of about 55 million representing 31% of the population

A reasonably well educated

Improving governance

30% tax concession for five years to industries able to attain the minimum local raw material utilisation as follows- agro 80%, agro allied 70%, engineering 65% h i l 60% d

A reasonably well educated labour force

A relatively low cost of labourImproving macro

economics

Nominal GDP forecasted to grow from $290.9 billion in 2012 to $1,218.4 billion in

A relatively stable democratic government with elections every four years since the military handed over power to a democratically elected government in

65%, chemical 60% and petrochemical 70%

5© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

2022 over power to a democratically elected government in 1999

Assessment of key sectors:

Financial servicesFinancial services industry

On-going reforms are changing the Nigerian financial services landscape…financial services landscape…

R i lNew StructureOld Structure

Regional

National

International

Commercial Banks

Commercial Banks

D l t International

Non Interest

Merchant Banking

Development Finance Institutions

Bureaux de-changeNon–Interest

Specialised Banking

Microfinance

Development

Universal Banking Finance Companies

Di t H

Finance Houses

BankingMortgage

Primary Mortgage Institutions

Discount Houses

Discount HousesOthers

BDCMicrofinance Banks

Key Regulatory Bodies: CBN and NDIC Key Regulatory Bodies: CBN and NDIC

Source: KPMG Analysis

Payments: Interswitch, ValuCard, NIBBS, Chams

Key Regulatory Bodies: CBN and NDIC

Payments: Interswitch, ValuCard, NIBBS, Chams

Key Regulatory Bodies: CBN and NDIC

7© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

These changes have created banks stratified into six main categoriesmain categories…

Top Tier Emerging Mid Tier Regional/ Foreign RescuedTop Tier Banks

Emerging ‘Big’ Banks

Mid Tier Banks Specialised

BanksBanks’

Subsidiaries

Rescued Banks

Predominantly Acquisitions and Considerable Players focused on Foreign owned Banks that failed Predominantly Nigerian-owned

Dominant share of domestic and regional markets, visible presence in

Acquisitions and recapitalization of rescued banks by mid-tier players

Considerable market presence and reach

Potential candidates for foreign technical alliance or

Players focused on defined market segment, products and geography

Currently obtained and operate

Foreign owned subsidiaries operating in the industry

Relatively moderate market presence

Banks that failed the CBN/NDIC stress test and were bailed out

Management Banks taken over by

West and Central Africa, international financial centers

Significant total assets

acquisition Includes players

focused on defined markets segment, products and geographic scope

regional and national commercial banking licences

and reach Appropriate

corporate governance structures

AMCON and renamed

Very strong likelihood to be sold off to foreign/ other investorsassets,

shareholders’ funds and channel infrastructure

geographic scope Some of the players

are characterised by innovation

Culture of proper risk management practices imbued from the parent companies

investors

8© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

Nigerian banking industry: Recent developmentsg g y p

Bank Charges The CBN recently introduced

Integration There has been increased

Tier II capital drive

new guidelines in relation to various charges levy by banks on customers (effective April 2013).

Electronic

Bank chargesIntegration

Ti II it l

closure of branches among industry players which is largely attributable to branch overlap arising from the recently concluded merger and acquisition

Electronic banking channels Increased usage of electronic

channels among Nigerian banks is largely due to the cashless policy initiatives

Cap on NPL at 5%

There has been increased drive towards raising of tier 2 capital among Nigerian Banks.

Electronic banking channels

Tier II capital drive

acquisition

cashless policy initiatives introduced by the CBN

Increase in AMCON Levy

The CBN recently announced that it will target a maximum non performing loan ratio of 5% across the industry. Recent

developmentsCash reserve

ratioCap on NPL

at 5%

Cash reserve ratio In line with its contractionary

monetary policy, the CBN Increase in AMCON Levy Effective 2013, banks were

required to contribute 0.5% (initially 0.3%) of their preceding year total assets to the sinking fund.

Agency banking As part of its ongoing financial

inclusion drive the CBN in

pratio at 5%introduced 50% CRR on public sector deposits

Toxic loans In a bid to discourage

excessive risk taking, AMCON has discontinued the purchase

f b d l f i l

ginclusion drive, the CBN in 2012 approved the use of agency banking model by commercial banks. This policy is expected to be actively operational by 2014.

Increase in AMCON

Levy

Agency banking

Nationalised banks AMCON has commenced the disposal

process of the three nationalised banks with appointment of financial advisers to manage the disposal of its 100%

of bad loans from commercial banks.

Toxic loansNationalised banks

9© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

g pequity stake in Enterprise Bank.

Energy & Natural Resources – Oil &Resources – Oil & gas, Power

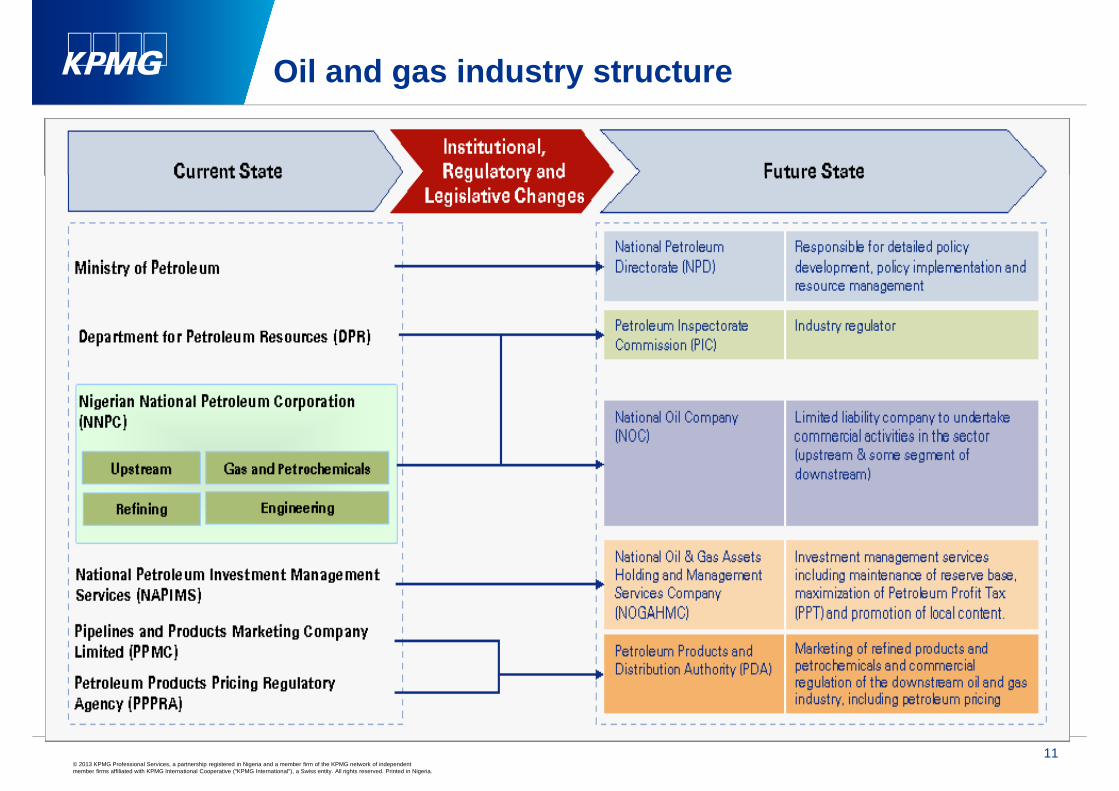

Oil and gas industry structureg y

11© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

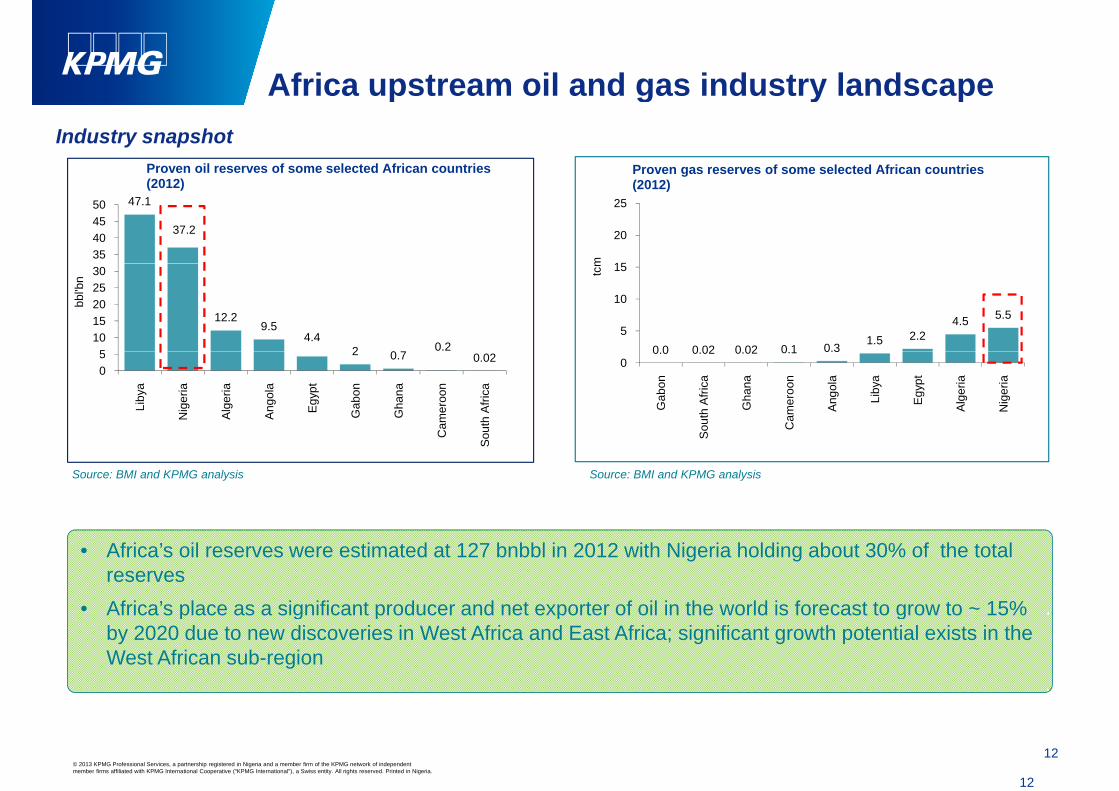

Africa upstream oil and gas industry landscape

Proven gas reserves of some selected African countries Proven oil reserves of some selected African countries

Africa upstream oil and gas industry landscape Industry snapshot

15

20

25

m

g(2012)

47.1

37.2

35404550

(2012)

0 0 0 02 0 02 0 1 0.3 1.5 2.24.5 5.5

5

10

15tcm

12.29.5

4.42 0 7

0.251015202530

bbl'b

n

0.0 0.02 0.02 0.1 0.30

Gab

on

Sou

th A

frica

Gha

na

Cam

eroo

n

Ang

ola

Liby

a

Egy

pt

Alg

eria

Nig

eria

2 0.7 0.0205

Liby

a

Nig

eria

Alg

eria

Ang

ola

Egy

pt

Gab

on

Gha

na

Cam

eroo

n

outh

Afri

caS

Source: BMI and KPMG analysis Source: BMI and KPMG analysis

• Africa’s oil reserves were estimated at 127 bnbbl in 2012 with Nigeria holding about 30% of the total reserves

• Africa’s place as a significant producer and net exporter of oil in the world is forecast to grow to ~ 15%Africa s place as a significant producer and net exporter of oil in the world is forecast to grow to 15% by 2020 due to new discoveries in West Africa and East Africa; significant growth potential exists in the West African sub-region

12© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

12

Key Developments in the Nigerian Upstream sector

Local content actDivestment of onshore oil blocks

Key Developments in the Nigerian Upstream sector

• Increased focus on International Oil Companies (IOCs’) deepwater developments and offshore production

Contin ed di estment of oil blocks b IOCs d e to

• Framework to promote active participation of

Nigerians in oil & gas activities

• Continued divestment of oil blocks by IOCs due to uncertainties around PIB, maturing onshore fields & lack of any significant onshore discoveries

• Offshore projects afford a high degree of

• Policy seeks to promote value addition & growth of

indigenous capacity

• Entry of new indigenous players through asset protection from sabotage and host community crisis Key

Developments

acquisition & strategic partnerships

Outlook

• Increased number of indigenous oil and gas players

Draft Petroleum Industry Bill (PIB)

• PIB is an omnibus legislation to regulate all activities in the Nigerian oil & gas industry p y

• Expected increase in production by 17% between 2012 and 2030

• Increased domestic consumption due to domestic refining

activities in the Nigerian oil & gas industry• Uncertainty exists about when the Bill will be

passed and in what form• Passage of the Bill is expected to bring about:

i fi l f k th t refining• Expected significant investment in gas gathering &

development facilities for local gas to power utilisationImpact of shale gas on oil demand

- a progressive fiscal framework that encourages further investment in the industry while optimising government revenues

- increase efficiency due to the unbundling of NNPC

13© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

13

• Impact of shale gas on oil demandNNPC- a comprehensive review of oil tax regimes

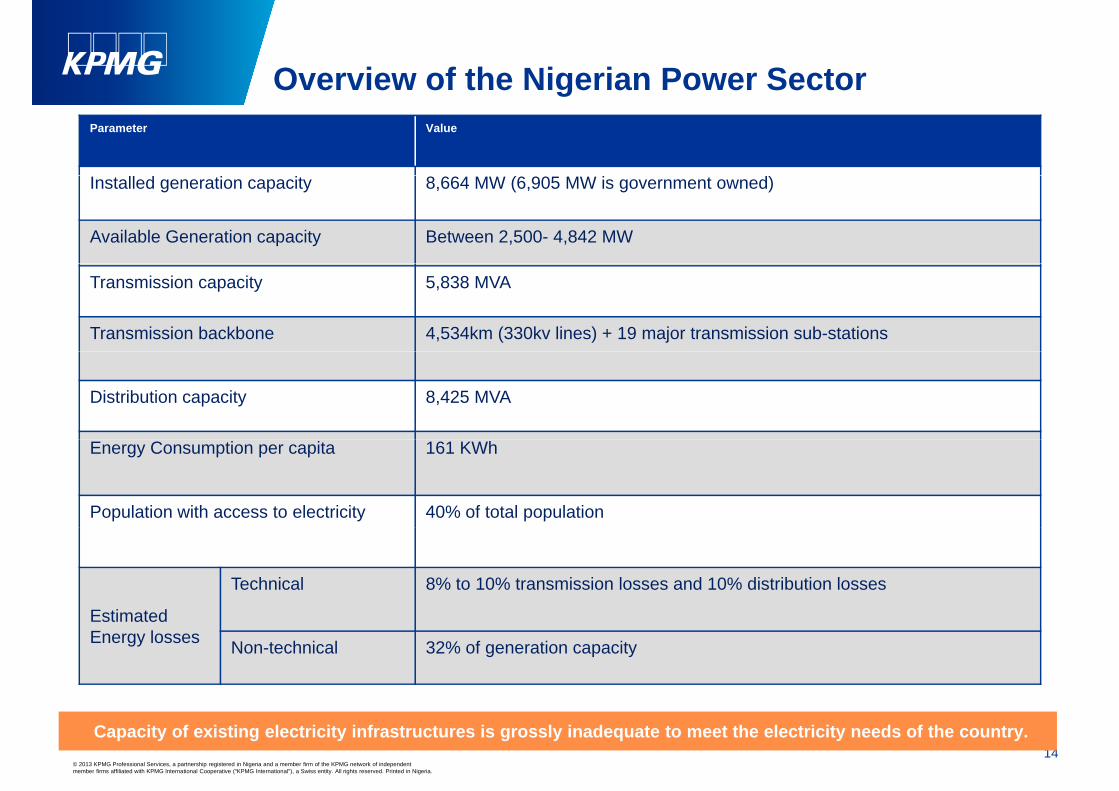

Overview of the Nigerian Power SectorOverview of the Nigerian Power SectorParameter Value

Installed generation capacity 8,664 MW (6,905 MW is government owned)

Available Generation capacity Between 2,500- 4,842 MW

Transmission capacity 5,838 MVA

Transmission backbone 4,534km (330kv lines) + 19 major transmission sub-stations

Distribution capacity 8,425 MVA

Energy Consumption per capita 161 KWh

Population with access to electricity 40% of total population

Estimated

Technical 8% to 10% transmission losses and 10% distribution losses

Estimated Energy losses Non-technical 32% of generation capacity

14© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

Capacity of existing electricity infrastructures is grossly inadequate to meet the electricity needs of the country.

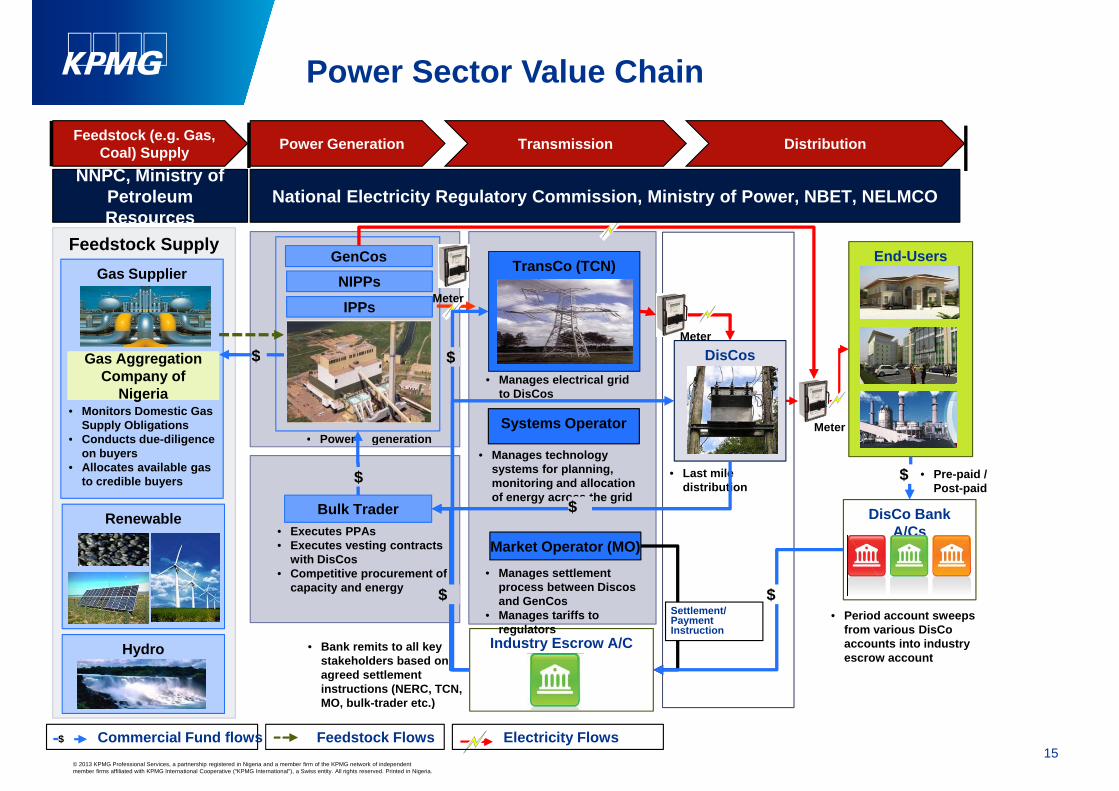

Power Sector Value Chain

Power Generation Transmission DistributionFeedstock (e.g. Gas, Coal) Supply

NNPC Ministry of

GenCos TransCo (TCN) End-UsersFeedstock Supply

National Electricity Regulatory Commission, Ministry of Power, NBET, NELMCONNPC, Ministry of

Petroleum Resources

TransCo (TCN)NIPPs

IPPs

Di C

Gas Supplier

$Meter

Meter

$

• Power generation

• Manages electrical grid to DisCos

Systems Operator

DisCos$

Meter

$Gas AggregationCompany of

Nigeria

Gas AggregationCompany of

Nigeria• Monitors Domestic Gas

Supply Obligations• Conducts due-diligence • Power generation

• Last mile distribution

Bulk TraderE t PPA

• Manages technology systems for planning, monitoring and allocation of energy across the grid

$

DisCo Bank A/C

$ • Pre-paid / Post-paid

• Conducts due-diligence on buyers

• Allocates available gas to credible buyers

$Renewable

Market Operator (MO)• Manages settlement

process between Discos and GenCos

• Manages tariffs to

• Executes PPAs• Executes vesting contracts

with DisCos• Competitive procurement of

capacity and energy

A/Cs

Settlement/ • Period account sweeps$$

Industry Escrow A/C

• Manages tariffs to regulators

Payment Instruction

• Period account sweeps from various DisCoaccounts into industry escrow account Hydro • Bank remits to all key

stakeholders based on agreed settlement instructions (NERC, TCN, MO bulk trader etc )

15© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

Feedstock FlowsCommercial Fund flows$ Electricity Flows

MO, bulk-trader etc.)

Key Reforms in the Nigerian Power SectorKey Reforms in the Nigerian Power Sector

Integrated Government-Owned Utility Company

Unbundled Government-Owned Utility Company

Privatisation Model/ Structure Incentives for private investors in Nigerian power sector

Post - 2005Pre - 2005 Post - 2012

IPP ProjectsPrivate Sector

Greenfield Initiatives

Nigerian power sector

• Liquidation of PHCN paved the way for privatization.

Generation NIPP Generation Assets

Thermal Power Plants6 GENCOs

Operations and Maintenance

ContractsNIPP Projects

• World bank PRG to support private sector participation

• Establishment of the Bulk Trader and planned

3 Hydro Power Plants

3 Thermal Power

Concessions

70% Equity Sale to

Trader and planned improvement of existing Multi-Year-Tariff Order

• Establishment of Gas NEPA Plants

Transmission

Core Investors

3-year

Aggregation Company to manage local demand and supply of gas.

Transmission Transmission Company of NigeriaTransCo

yManagement

Contract+ • Approval of N300 billion

Power and Aviation Fund to support investment in the sector

Distribution 11 Discos 60% Equity Sale to Core InvestorsNDPHCPHCN

11Discos

NDPHCPHCN

sector• US$3.5 billion investment for

the construction of a 700KV super grid to improve

16© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

NDPHCPHCN transmission capacity to 7,000MW

Consumer Goods

Industry structure

Nigerian FMCG I d t

Food and Beverages

Industry

Personal Care

Household goods

Industrial goods

Food processing

Meat/ seafood

Dairy products & Food services/

Distribution

Beverages Care goods goods

processing product beverages

Wheat Product Meat Milk and ice

creamFast Foods & Restaurants

C i

Distribution

Pharmaceutical & health

Personal / body care

Soaps and detergents

Fabricare/ liquids

Flour

Agricultural produce

Pasta/ noodles

Baked goods/ P t i

Fish & Seafood

Other meat & seafood

Butter/Cheese

Yogurt

Convenience foods/catering

servicesLeisure/

h it lit

& health

Others

liquids p oduce

Cement

B ildi

Home care

Pastries & seafood variants

Yogurt hospitality

Biscuits/ Confectionaries Alcoholic Mass grocery/

Retail

Oth f d

Building materials

ElectronicsNon-

alcoholicSeasonings & Condiments

Other food establishments/

Tobacco

18© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

Source: Euromonitor, Business Monitor International and Economic Intelligence Unit

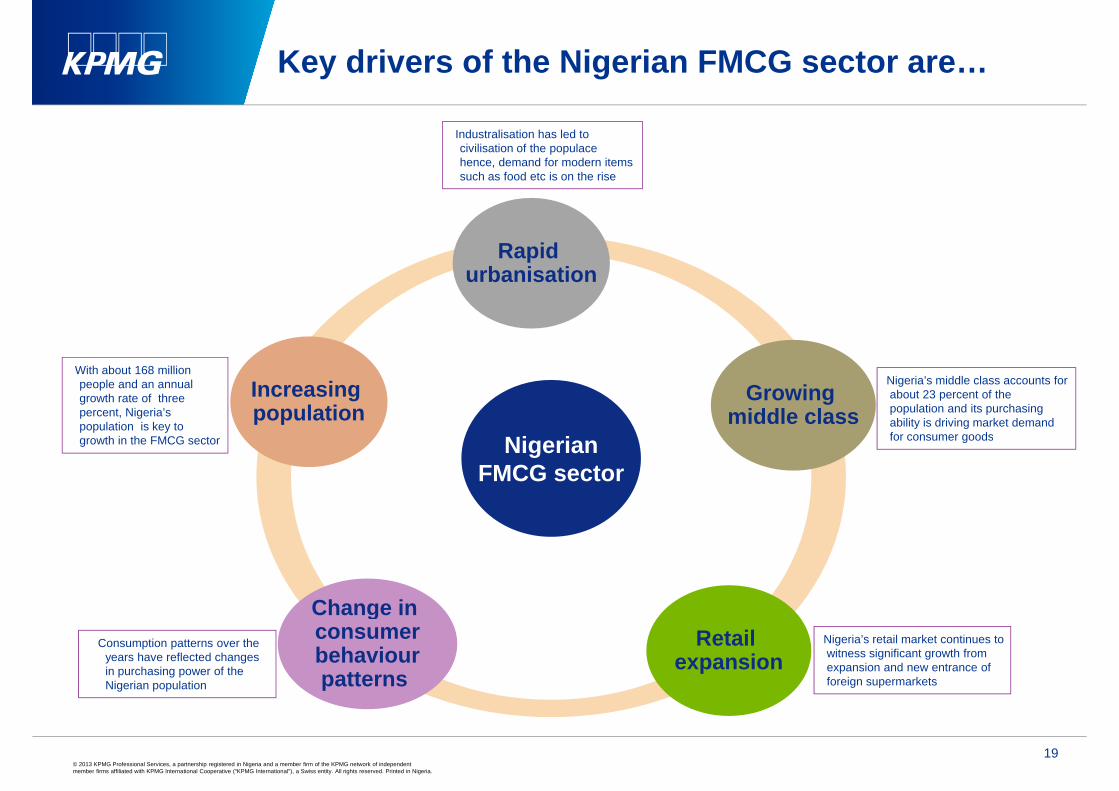

Key drivers of the Nigerian FMCG sector are…

Industralisation has led to civilisation of the populace hence, demand for modern items such as food etc is on the risesuch as food etc is on the rise

Rapid urbanisation

With about 168 million people and an annual growth rate of three percent, Nigeria’s population is key to growth in the FMCG sector

Nigeria’s middle class accounts for about 23 percent of the population and its purchasing ability is driving market demand for consumer goodsNi i

Increasing population

Growing middle class

growth in the FMCG sector for consumer goodsNigerian FMCG sector

Change inConsumption patterns over the

years have reflected changes in purchasing power of the Nigerian population

Nigeria’s retail market continues to witness significant growth from expansion and new entrance of foreign supermarkets

Change in consumerbehaviour patterns

Retail expansion

19© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

M&A & Capacity Expansion - expected to increase...

Consumer Behaviour

p y p p

Consumer Behaviourand Business

Model Innovation M&A & Expansion Regulatory/Policy Development

Increasing demand for healthier food options Shift from informal to formal retail

outlets

Nestle completed US$77 million Flowergate factory P&G completedUS$250 million plant De United completed US$20 million

Pioneer status for new plants and other tax incentives IFRS adoption Cash-liteoutlets

Shift from local to western products Internet retailing fast gaining

l it

De United completed US$20 million factory in Kaduna De United Foods constructed a flour

milling plant in Port-Harcourt Flour Mills acquired Thai Farms

Pending draft industrial policy Push for reforms in various

sectors e.g. ports, power, agriculture etcpopularity

New products and packaging Supply chain optimisation and

use of third-party logistics

Flour Mills acquired Thai Farms SABMiller Plc acquired stake in

Castel Group

agriculture, etc. Restrictions on street trading

20© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

Telecommunication industry

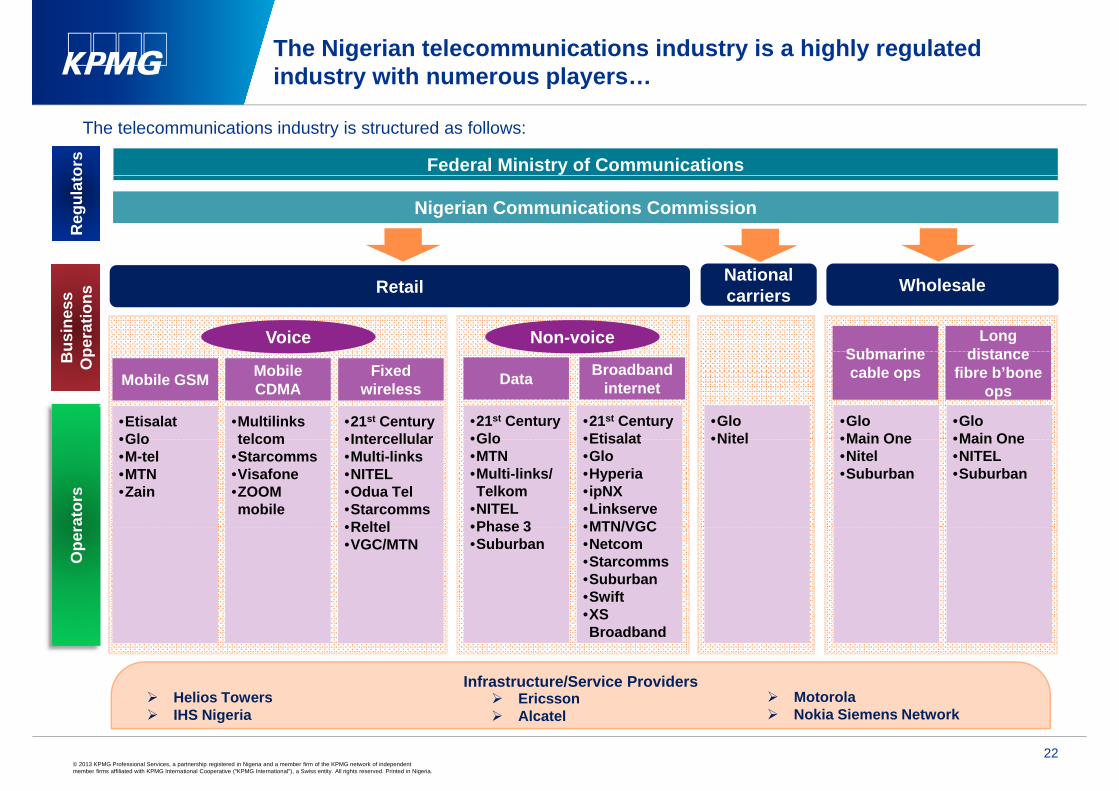

The Nigerian telecommunications industry is a highly regulated industry with numerous players…y p y

Federal Ministry of Communications

The telecommunications industry is structured as follows:

ors

ors

Nigerian Communications Commission

Reg

ulat

oR

egul

ato

Retail National carriers Wholesale

Voice Non-voiceSubmarine

Long distanceus

ines

s pe

ratio

nsus

ines

s pe

ratio

ns

•Glo•Main One

•Glo•Main One

•Glo•Nitel

•21st Century•Glo

•21st Century•Etisalat

•Multilinks telcom

•21st Century•Intercellular

•Etisalat•Glo

Mobile CDMA

Fixed wirelessMobile GSM Data Broadband

internet

Submarine cable ops

distance fibre b’bone

ops

B OpB Op

•Main One•Nitel•Suburban

•Main One•NITEL•Suburban

•Nitel•Glo•MTN•Multi-links/ Telkom

•NITEL•Phase 3

•Etisalat•Glo•Hyperia•ipNX•Linkserve•MTN/VGC

telcom•Starcomms•Visafone•ZOOM mobile

•Intercellular•Multi-links•NITEL•Odua Tel•Starcomms•Reltel

•Glo•M-tel•MTN•Zain

rato

rs

•Phase 3•Suburban

•MTN/VGC•Netcom•Starcomms•Suburban•Swift•XS

•Reltel•VGC/MTN

Ope

r

•XS Broadband

Infrastructure/Service Providers Helios Towers Ericsson Motorola

22© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

IHS Nigeria Ericsson Alcatel Nokia Siemens Network

Market Entry Options

Market Entry Options…

Joint Venture / Partnerships

Local Production &

Export

Mergers and acquisition

EXAMPLE

Export MARKETENTRY

MODELSPPP Greenfield

MODELS

LicensingFranchising

24© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.

Key contacts

Dapo OkubadejoPartner & Africa Head, M&A, PE and Transaction AdvisoryPartner & Africa Head, M&A, PE and Transaction AdvisoryKPMG NigeriaBishop Aboyade Cole StreetVictoria IslandVictoria IslandLagosMobile: +234 803 402 0964T l 234 1 280 9268Tel: + 234 1 280 [email protected]

25© 2013 KPMG Professional Services, a partnership registered in Nigeria and a member firm of the KPMG network of independentmember firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Nigeria.