investor booklet -...

TRANSCRIPT

November 2017

Investor

Booklet

Legal Disclaimer

This presentation includes forward-looking statements within the meaning of Section 27A of theSecurities Act of 1933 and Section 21E of the Securities and Exchange Act of 1934. All statementsother than statements of historical facts included in this presentation regarding, among other things,our prospects, plans, financial position and business strategy, may constitute forward lookingstatements. These statements are based on the beliefs and assumptions of our management andon the information currently available to our management at the time of such statements. Forward-looking statements generally include discussions and descriptions other than historical information.These forward-looking statements can generally be identified as such because the context of thestatement will include words such as "trend," "may," "annualized," "should," "outlook," "project,""intend," "seek," "plan," "believe, "anticipate," "expect," "estimate," "potential," "continue," "goal," or"opportunity," the negatives of these words, or similar words or expressions. The forward-lookingstatements made herein are only made as of the date of this presentation and we undertake noobligation to publicly update such forward looking statements to reflect subsequent events orcircumstances. Although we believe that the expectations reflected in these forward-lookingstatements are reasonable, these expectations may not prove to be correct. All subsequent writtenand oral forward-looking statements attributable to us or persons acting on our behalf are expresslyqualified in their entirety by the cautionary statements included in this document. These forward-looking statements are subject to risks and uncertainties that are discussed in greater detail in theCompany’s filings with the Securities and Exchange Commission, including our Annual Reports onForm 10-K and Quarterly Reports on Form 10-Q, that may cause actual results to differ materially.

1

Continental is a leading, high margin manufacturer of

gypsum wallboard and complementary finishing products

• Market position: Leader in core geographic regions

• Plants: 3 drywall manufacturing facilities (owned)

2 joint compound facilities (owned)

1 joint venture paperboard liner facility

• Manufacturing: 3.3 billion square feet; operated at

79% capacity utilization YTD 2016

• Key financials: Total revenue of $476 mm

(LTM 9/30/2017) Adj. EBITDA of $133 mm (27.9% margin)

• Headquarters: Herndon, Virginia

Company Overview

2016 Sales Breakdown by Country

Geographic Footprint

Canada North Central North East South East

Corporate Wallboard Plants Joint Compound

Paperboard Liner

2 Source: Company filings.

United States93%

Canada7%

3

Company Highlights

Focused on Operational Excellence with New, Low-Cost Production1

Well Positioned to Capitalize on Construction Recovery2

Favorable Industry Dynamics3

Strong Margins and Cash Flow Drive Value Enhancing Opportunities4

• Among the newest capacity in the industry results in higher operating efficiency and lower capex needs

• Strategic locations near raw material sources and customer end markets drive lower material and freight costs

• Strong positions in markets growing faster than the national average, but still well below peak

• U.S housing starts recovering but remain well below 50-year average of 1.4 million

• Repair and remodel provides stable demand base; housing and commercial embed significant potential upside

• Market leader in key geographic regions with an estimated 30-35% average market share in key major markets

• As of 2016, industry capacity 16% below prior peak level.

• Significant EBITDA and margin growth through low-cost, efficient operating structure

• Strong cash flow generation and low capex drives deleveraging and other value enhancing opportunities

• Stock repurchase program of up to $200 million through December 2018.

Sustainable

Platform for

EBITDA and

Cash Flow

Generation

4

Solid Platform for EBITDA and Cash Flow Generation

Attractive Market Position Low-Cost, Efficient Capacity

Strategic Raw Material Supply Strict Capital Deployment

• Over 55% of US wallboard demand in

CBPX addressable markets

• Plants strategically located close to

end markets

• Strong customer relationships in

growing markets

• Seven Hills JV provides captive paper

supply

• Natural gas hedges in place for ~50%

of energy needs

• Primary and secondary synthetic

gypsum supply contracts provide

ample gypsum for long term horizon

• One of lowest industry costs per unit

• Invested over $587mm in state-of-the-art

capacity from 2000 to 2016, creating

some of the fastest industry line-speeds

• Energy consumption per MSF reduced

by 18% since 2007

• New ERP system implemented below

budget and ahead of schedule in 2014

• Low sustaining capital needs given

recent investments

• Strategic capex program focused on high

return projects with <3 year paybacks

• Repurchased $98M of shares through the

company’s $200M stock repurchase

program as of September 30, 2017.

• Net debt / LTM Adjusted EBITDA ratio

improved to 1.6x as of September 2017

Springfield

Nashville

Knoxville

Richmond

Charlottesville

HuntingtonCincinnati

Columbus

Cleveland

Detroit

GrandRapidsMilwaukee

Chicago

De Moines

Kansas City

St. Louis

Memphis

Louisville

Indianapolis

Toronto

Silver Grove

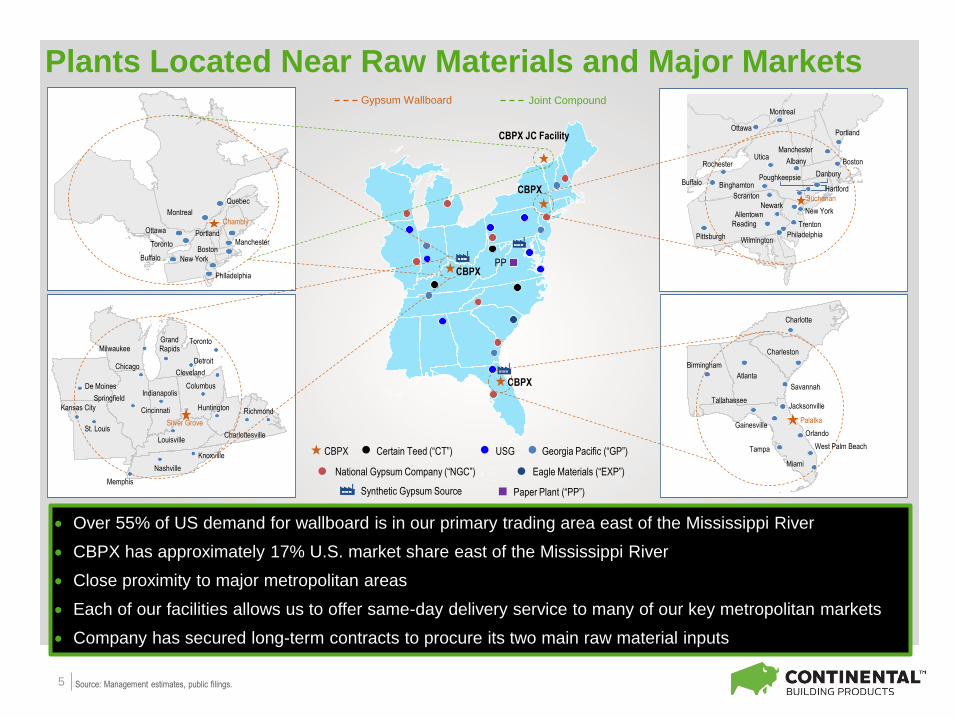

Source: Management estimates, public filings.5

Over 55% of US demand for wallboard is in our primary trading area east of the Mississippi River

CBPX has approximately 17% U.S. market share east of the Mississippi River

Close proximity to major metropolitan areas

Each of our facilities allows us to offer same-day delivery service to many of our key metropolitan markets

Company has secured long-term contracts to procure its two main raw material inputs

Plants Located Near Raw Materials and Major Markets

PortlandManchester

Philadelphia

Buffalo New York

Ottawa

Montreal

Quebec

Toronto

Chambly

Boston

Pittsburgh

Reading

Ottawa

Montreal

Portland

ManchesterUtica

Albany

Buchanan

New YorkNewark

Binghamton

ScrantonHartford

Allentown

Trenton

PhiladelphiaWilmington

Poughkeepsie Danbury

Boston

Buffalo

Rochester

Charlotte

Charleston

Birmingham

Atlanta

Savannah

JacksonvilleTallahassee

Gainesville

Tampa

Orlando

West Palm Beach

Miami

Palatka

CBPX

CBPX

CBPX

CBPX JC Facility

Eagle Materials (“EXP”)National Gypsum Company (“NGC”)

USGCertain Teed (“CT”) Georgia Pacific (“GP”)CBPX

PP

Paper Plant (“PP”)Synthetic Gypsum Source

Gypsum Wallboard Joint Compound

6

Attractive market opportunity with favorable demand trends Housing starts rebounding off all-time lows

US Population

(mm)179.3 203.2 226.5 248.7 281.4 320.1

Long Term Average Housing

Starts at 1.4mm per Annum

Period

Housing Starts

(in thousands)

Housing Starts 2016(1)

(in thousands)

Percentage

Difference

Peak (2) 2,357 1,174 101%

Long-Term Average (3) 1,439 1,174 23%

Average Cyclical Low (4) 1,131 1,174 (4%)

Source: US Census Bureau.

(1) Average of monthly seasonally-adjusted housing starts, as reported by the US Census Bureau through December 2016.

(2) Peak occurred in 1972.

(3) Average housing starts from 1959 through 2016.

(4) Calculated as the average of the 1960, 1966, 1975, 1982 and 1991 housing starts.

Hou

sin

g s

tart

s (

00

0’s

)

0

500

1000

1500

2000

2500

0.0

500

1,000

1,500

2,000

0

5

10

15

20

25

30

35

40

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

(BS

F)

(th

ou

sa

nd

s)

Source: Gypsum Association (wallboard demand) and U.S. Census Bureau (housing starts).

Upside to Wallboard Demand Highly Correlated To

Improving Housing Starts

7

New Housing Starts

Wallboard Demand

New Housing Starts Correlation = 91%

8

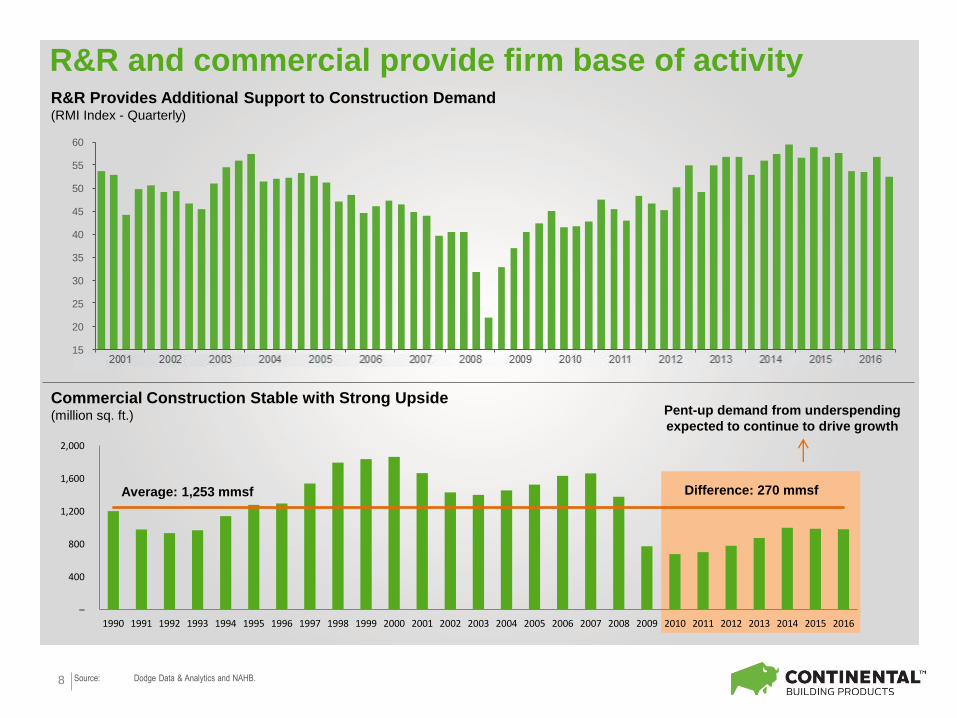

R&R and commercial provide firm base of activityR&R Provides Additional Support to Construction Demand(RMI Index - Quarterly)

Commercial Construction Stable with Strong Upside(million sq. ft.)

Average: 1,253 mmsf Difference: 270 mmsf

Pent-up demand from underspending

expected to continue to drive growth

Source: Dodge Data & Analytics and NAHB.

15

20

25

30

35

40

45

50

55

60

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

–

400

800

1,200

1,600

2,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

39.6

33.4

2008 2017

187

129

96 104 99 98

124

146 155 154

144

87%

65% 60%

54% 53% 55% 58% 63% 66% 67% 79%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

9

Industry dynamics remain favorable

Industry Capacity Rationalized

(Billions of sq. ft.)

CBPX Capacity Utilization and Mill-Net Price Still Below Peak

(CBPX Mill-Net price per thousand sq. ft., MSF)

1997 2016

(Capacity Share) (Capacity Share)

Briar

26%

21%16%

13%

10%

10%

4%

31%

22%19%

5%

5%

4%

4%

3% 2%

Source: Management estimates, Gypsum Association and public corporate presentations.

10

Wallboard volume growth expected as construction recovery continues

New, low-cost production generates high margins and operating leverage

Positive Pricing Actions

Generating strong cash flow

• Housing cycle viewed as having a longer recovery as starts remain at trough levels seen in previous cycles

• Repair and remodel has provided consistent base demand

• New commercial recovering from historical lows

• Substantially improved cost structure with a strong commitment to operational excellence

• Significant past capex investments drive strong operating leverage and EBITDA growth

• Average mill-net price up approximately 50% from 2011 to 2016 and remains well below previous peak levels

• Strong cash flow generation with near term focus on balance sheet strength and value enhancing opportunities

• Solid track record of disciplined deployment of cash flows to maximize shareholder value

2

1

4

3

Financial and Operational Overview

Source: Company filings.

Volume(millions of square feet, mmsf)

Mill-Net Price Per MSF

Total Net Sales($ in millions)

11

Capacity Utilization

Total Capacity: 3,300 mmsf 740 mmsf of head room

Improving Top Line with Plenty of Headroom for Growth

$124

$146 $155 $154

$144

2012 2013 2014 2015 2016

1903

2161 2180 2199

2560

58%

65% 66% 67%

79%

2012 2013 2014 2015 2016

$311

$402 $425 $422

$461

2012 2013 2014 2015 2016

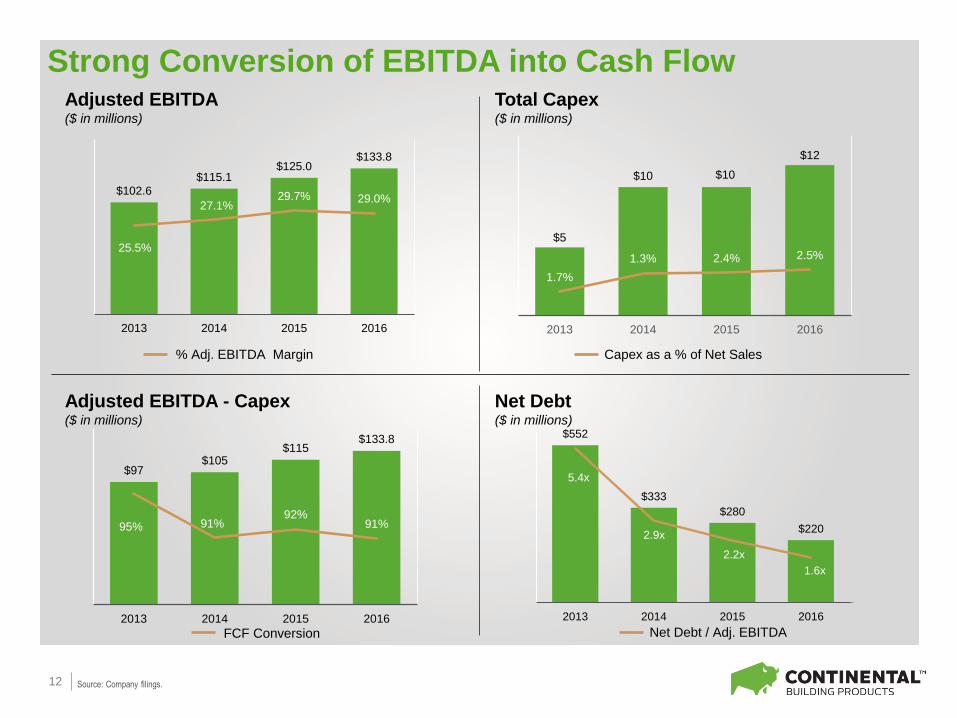

Adjusted EBITDA($ in millions)

Total Capex($ in millions)

Adjusted EBITDA - Capex($ in millions)

12

Capex as a % of Net Sales% Adj. EBITDA Margin

Strong Conversion of EBITDA into Cash Flow

Source: Company filings.

Net Debt($ in millions)

Net Debt / Adj. EBITDAFCF Conversion

$102.6

$115.1 $125.0

$133.8

25.5%

27.1% 29.7% 29.0%

2013 2014 2015 2016

$5

$10 $10

$12

1.7%

1.3% 2.4% 2.5%

2013 2014 2015 2016

$97 $105

$115 $133.8

95% 91%92%

91%

2013 2014 2015 2016

$552

$333

$280

$220

5.4x

2.9x

2.2x

1.6x

0

1

2

3

4

5

6

2013 2014 2015 2016

Strong Cash Flows Driving Deleveraging and Other

Value Enhancing Opportunities

13

($ in millions) 9/30/2016 9/30/2017

Cash $35 $60

Revolver -- --

1st lien term loan due 2021 274 272

Original issue discount (2) (2)

Total debt $272 $270

Book equity 302 299

Total capitalization $574 $568

Net Debt $238 $210

LTM Adjusted EBITDA $133 $133

Credit Statistics

Net debt / LTM Adj. EBITDA 1.8x 1.6x

Liquidity $108 $133

Source: Company filings.

Since 2015, the Company has repurchased a total of approximately 4.7 million shares for

$97.8 million as of September 30, 2017.

14

Recent Operating and Financial Performance

Source: Company filings.

Q3 2017

Vs

($ in millions) 2015 2016 Q3 2016 Q3 2017 Q3 2016

Mill-Net Price ($/MSF) $153.70 $143.83 $144.34 $144.90 +0.4%

Wallboard Volume (MMSF) 2,199 2,560 634 644 +1.6%

Total Net Sales $422 $461 $115 $117 +1.7%

Operating Income $44 $87 $19 $20 +5.3%

EBITDA $125 $134 $30 $32 +6.7%

% Margin 29.7% 29.0% 26.6% 27.3% +2.6%

Depreciation and Amortization $51 $47 $12 $12 NM

Capital Expenditures $10 $12 $3 $6 +100.0%

15

Jay Bachmann

President, CEO

13 years of experience with the Company

Prior positions

– Chief Financial Officer, USA (Lafarge NA)

– Senior Vice President Finance - Investor Relations (Lafarge SA)

Dennis Schemm

Senior VP, CFO

Joined the Company in 2015 with over 20 years of industry experience

Prior positions

– Vice President of Global Finance for Armstrong Flooring (Armstrong Worldwide)

– Director of Global Financial Planning and Analysis at Gilbarco, a Danaher

Company

– Senior Financial Roles at Monsanto Company

Tim Power

Senior VP, General

Counsel

16 years of experience with the Company

Prior positions

– Vice President and Associate General Counsel (Lafarge NA)

– Assistant General Counsel (Lafarge NA)

Bruce Major

Senior VP,

Manufacturing and

Strategic Sourcing

Joined the Company in 2016 with 17 years in Gypsum Operations Management

Prior positions

– VP – Manufacturing, Lafarge Cement U.S.

– SVP – Manufacturing, Lafarge Gypsum Division

Experienced and Highly Aligned Management Team

Appendix

17

Non-GAAP Reconciliations

Reconciliation of Net Income to Adjusted EBITDA ($ in Thousands)

Source: Company filings.

(a) Represents expense recognized pursuant to the LTIP funded by LSF8, an affiliate of Lone Star.

September 30, 2017 September 30, 2016

Net Income 10,987$ 6,210$

Adjustments:

Other expense/(income), net (146) 5,900

Interest expense, net 2,988 3,146

Losses from equity method investment 204 291

Income tax expense 5,674 3,014

Depreciation and amortization 12,057 11,868

EBITDA—Non-GAAP Measure 31,764 30,429

Long Term Incentive Plan Funded by Lone Star (a) — —

Adjusted EBITDA—Non-GAAP Measure 31,764 30,429

Adjusted EBITDA Margin - Adjusted EBITDA as a percentage of net sales -

Non-GAAP Measure 27.3% 26.6%

For the Three Months Ended

(in thousands)

18

Non-GAAP Reconciliations (cont’d)

Reconciliation of Operating Income to Adjusted EBITDA ($ in Thousands)

Source: Company filings.

September 30, 2016 December 31, 2016 March 31, 2017 June 30, 2017 September 30, 2017

Operating Income - GAAP Measure $ 18,561 $ 22,801 $ 21,687 $ 21,620 $ 19,707

Depreciation and Amortization 11,868 10,990 11,286 12,474 12,057

EBITDA - Non-GAAP Measure $ 30,429 $ 33,791 $ 32,973 $ 34,094 $ 31,764

Long Term Incentive Plan funded by Lone Star - - - - -

Adjusted EBITDA - Non-GAAP Measure $ 30,429 $ 33,791 $ 32,973 $ 34,094 $ 31,764

Adjusted EBITDA Margin - Adjusted EBITDA as a

percentage of net sales - Non-GAAP Measure 26.6% 28.6% 27.3% 28.3% 27.3%

For the Quarter Ended