investor information february 2018 - oebfa.at relations/republic of... · investor information,...

TRANSCRIPT

Republic of Austria

Republic of Austria

Investor Information – April 2018

Austrian Treasury

Republic of Austria

Agenda

2

1. General Overview – Austria‘s favourable fundamentals 3

2. Funding Strategy Republic of Austria 26

Investor Information, April 2018

Republic of Austria

Euro-Zone (EU19)

Austria – Key Data and Facts

3

Austria Euro-Zone

Area (sq. km ‘000) 84 2.758

Population 2017 (Mio.) 8.8 341.0

Population growth

(2013 – 2017e, average

yearly change)

+0.9% +0.3%

GDP per capita 2017 (EUR) 41.970 32.700

Net financial assets

per private household as of

Q3 2017 (EUR)

118.276 108.726

1. Austria‘s favourable fundamentals

EU28

Source: Statistics Austria, Eurostat, OECD

Investor Information, April 2018

Republic of Austria

Austria – Key Data and Facts

4 1. Austria‘s favourable fundamentals

in % Austria Euro-Zone

Real GDP growth 2.9 3.2 2.2 2.4 2.3 2.0

Inflation (HICP) 2.2 2.0 1.9 1.5 1.5 1.6

Unemployment 5.5 5.2 5.0 9.1 8.5 7.9

Current Account Balance 2.2 2.9 3.7 3.0 3.0 3.0

Budget Balance (Maastricht) -0.7 -0.4 0.0 -1.1 -0.9 -0.8

Structural Budget Balance -0.1 -0.5 -0.5 -1.0 -1.1 -1.1

Debt to GDP 78.4 74.5 70.9 89.3 87.2 85.2

Year 2017 2018 2019 2017 2018 2019

Investor Information, April 2018

Source: Data on Austria: EC – Autumn Economic Forecast, November 2017 / WIFO, March 2018 / Federal Ministry of Finance, March 2018 / Statistics Austria, April 2018

Data on Euro-Zone: EC – Autumn Economic Forecast, November 2017 & Interim Winter Forecast, February 2018

Note: Structural budget balance Austria excludes additional expenditures on refugees and asylum seekers

Republic of Austria

EU-28 70%

EU- Others 10%

Africa 1%

America 10%

Asia 9%

Australia 1%

Top-10 Export Partners 2017

Country Share in %

Germany 30.1

USA 6.8

Italy 6.4

France 5.0

Switzerland 4.9

Czech Republic 3.7

Hungary 3.4

Poland 3.1

United Kingdom 2.8

China 2.6

Austria – GDP and external trade

5

Composition of Austrian GDP

2017

EUR 369.2 bn

Consumption 72%

Investments 25%

Net exports 3%

Exports 54%

Imports 51%

Eurozone: 52.2%

Europe: 79.3%

1. Austria‘s favourable fundamentals

Note: Totals might not add up due to rounding

Distribution of Austrian Exports

Investor Information, April 2018

Source: Statistics Austria (GDP as of February 2018, Exports as of March 2018)

Republic of Austria

Agriculture, forestry and fishing: 1.1%

Mining and quarrying;

manufacturing: 16.8%

Electricity; water supply; sewerage

and waste manage- ment: 2.6%

Construction: 5.8%

Wholesale and retail trade: 10.9%

Transportation: 4.9%

Accommodation and food service

activities: 4.8%

Information and communi-

cation: 3.1%

Financial and insurance

activities:3.7%

Real estate activities: 8.8%

Other administra- tive and support service activities:

8.6%

Public administra- tion: 4.5%

Education; human health and social

work activities:11.0%

Other service activities: 2.5%

Composition of the Austrian GDP -

Low exposure to financial sector (3.7% of GDP)

6

Source: Statistics Austria as of February 2018

1. Austria‘s favourable fundamentals Investor Information, April 2018

Republic of Austria

Credit Ratings Overview

7

Long Term Short Term Outlook

Moody‘s Aa1 P-1 Stable

Standard & Poors AA+ A-1+ Stable

Fitch AA+ F1+ Stable

DBRS AAA R-1 (high) Stable

• All rating reports available online at www.oebfa.at

1. Austria‘s favourable fundamentals Investor Information, April 2018

Republic of Austria

Austria: Leader in Sustainability

8

Sustainability Country Ranking1

Sustainalytics Ranked 5th out of 172 countries worldwide

oekom research Ranked 9th out of 57 countries worldwide

1) Reports available online at www.oebfa.at

2) Eurostat, February 2017 (no data available for Germany, Netherlands, Italy, Ireland, Greece)

3) Eurostat, Employment in the environmental goods and services sector; May 2017

4) Eurostat, Sustainable Development in the European Union 2016

1. Austria‘s favourable fundamentals

• Highest environmental protection

expenditure per capita 2 and highest

share of green jobs in the EU3

• Share of renewable energy sources (in

total gross final energy consumption) is

over 32%. That is twice

the EU average (16%) and puts Austria

in 4th place in Europe4

• Austria has the 2nd highest recycling

rate of waste in the EU4

• With over 20% of its agricultural area

utilised under organic farming, Austria

ranks 1st among all EU member states4

0

200

400

600

800

1.000

1.200

1.400

in EUR

Environmental protection expenditure per inhabitant2

Investor Information, April 2018

Republic of Austria

0

0,5

1

1,5

2

2,5

Rule of Law Control of Corruption Government Effectiveness

Regulatory Quality Voice and Accountability

Austria’s High Institutional Strength

Worldbank Governance Indicators

9

Note: Values range from -2.5 (weak) to +2.5 (strong) / data as of October 2017

1. Austria‘s favourable fundamentals

• Rule of Law:

ranked 10 out of 214 countries

worldwide

• Voice and Accountability:

ranked 15 out of 214 countries

worldwide

• Government Effectiveness:

ranked 18 out of 214 countries

worldwide

• Control of Corruption

ranked 19 out of 214 countries

worldwide

• Regulatory Quality

ranked 19 out of 214 countries

worldwide

Investor Information, April 2018

Republic of Austria

10

Austria’s Favourable Fiscal Position Government Debt Ratio and Budget Deficit on a clearly declining path

• Excluding liabilities of government-owned wind-down units, Austria‘s general government debt was 76.5% as of

GDP (Q3-2017)

1. Austria‘s favourable fundamentals Investor Information, April 2018

Forecast

-1,5

-5,3

-4,4

-2,6 -2,2

-2,0

-2,7

-1,0

-1,6

-0,7 -0,4

+0,0 +0,1 +0,2 +0,4 68,7

79,9

82,7 82,4 81,9

81,3

84,0 84,6

83,6

78,4 74,5

70,9

67,7

65,0

62,2

-6

-4

-2

0

2

4

6

55

60

65

70

75

80

85

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

in % of GDP

Deficit / Surplus (rhs) Government Debt (lhs)

Source: Federal Ministry of Finance, March 2018 / Statistics Austria, April 2018

Republic of Austria

9,1

23,0

35,5

37,9

49,9

51,6

54,9

61,2

62,1

69,1

74,1

74,5

87,2

96,9

96,9

98,3

102,5

124,1

130,8

177,8

4,5

14,9

18,2

14,6

28,5

62,6

54,7

65,1

32,7

42,4

21,8

68,4

68,6

68,0

39,5

45,1

92,5

71,7

102,4

109,4

020406080100120140160180200

Estonia

Luxembourg

Latvia

Lithuania

Slovakia

Malta

Netherlands

Germany

Finland

Ireland

Slovenia

Austria

Euro area

France

Spain

Cyprus

Belgium

Portugal

Italy

Greece

2008

2018e

Euro area

% of GDP

24,3

33,3

35,5

36,6

39,1

53,0

71,5

77,4

81,6

85,3

108,4

239,1

13,0

28,3

33,3

37,8

13,2

46,3

71,0

39,6

60,7

49,9

72,8

184,6

04080120160200240

Bulgaria

Czech Republic

Denmark

Sweden

Romania

Poland

Hungary

Croatia

EU-28

United Kingdom

United States

Japan

2008

2018e

Non-euro area and others

% of GDP

Public Debt/GDP in Austria

Increase since 2008 substantially below Eurozone-average

11

Source: EC – Autumn Economic Forecast, November 2017 / Statistics Austria, February 2018 / Federal Ministry of Finance, March 2018

1. Austria‘s favourable fundamentals Investor Information, April 2018

Republic of Austria

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

6500

7000

7500

8000

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8e

201

9e

in Mil EUR in % of GDP

in % of GDP 3.4%

in Mil EUR in % of GDP

1.5%

Interest payments 2018: Forecast as of March 2018, GDP: WIFO, March 2018

• Absolute level of interest payments relatively stable

• Relative to GDP interest payments are below 2% and well beneath peak levels in 1996

Federal government - Interest payments 1990-2019

12 1. Austria‘s favourable fundamentals Investor Information, April 2018

Republic of Austria

45

50

55

60

65

70

75

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

AT: % of GDP EA: % of GDP

Household Debt in % of GDP

80

85

90

95

100

105

110

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

AT: % of GDP EA: % of GDP

Corporate Debt1 in % of GDP

1 Short- and long-term loans, money and capital market

instruments.

Source: European Central Bank, Austrian National Bank, October 2017

Level of corporate and household indebtedness substantially below Euro-Zone average

Indebtedness of households and corporates

13 1. Austria‘s favourable fundamentals Investor Information, April 2018

Republic of Austria

0 50 100 150 200 250 300 350 400 450 500

Cyprus

Ireland

Luxembourg

Greece

Portugal

Netherlands

Belgium

Italy

Spain

France

Finland

Austria

Estonia

Malta

Germany

Slovenia

Slovakia

Latvia

Lithuania

Euro Area: Total debt in % of GDP

Government Debt

Corporate Debt

Household Debt

Total indebtedness of the real economy

1. Austria‘s favourable fundamentals 14

Level of total indebtedness in Austria relatively low

Source: ECB / ESRB, May 2017 (data as of Q4 2016)

Investor Information, April 2018

Republic of Austria

Government debt and household assets

15

High domestic wealth

• Growth in net financial assets of households exceeds increase in government debt

• GDP per capita is 38% higher than EU-average

• Sustainable current account surplus

Source: Statistics Austria, March 2018 / Austrian National Bank, April 2018

1. Austria‘s favourable fundamentals Investor Information, April 2018

0

2

4

6

8

10

12

14

16

18

20

0

100

200

300

400

500

600

700

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

in % in bn EUR

Household financial assets (Gross) in bn EUR

Household financial assets (Net) in bn EUR

Government debt in bn EUR

Savings rate in % (rhs)

Republic of Austria

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

5,0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Austria Euro area EU

% of GDP

Forecast

Austria’s strong competitive position

16

Source: EC – Autumn Economic Forecast, November 2017

1. Austria‘s favourable fundamentals

Current Account Balance

Austria’s sustainable current account surplus

reflects strong international competitiveness

Investor Information, April 2018

Republic of Austria

Netherlands

Germany

Japan

Austria

Belgium

Finland

Euro area

European Union

Italy

Ireland

France

Spain

United States

UK

Portugal

Greece

-8 -6 -4 -2 0 2 4 6 8 10

in % of GDP (average 2005 - 2018e)

Net lending (+) / net borrowing (-) of the nation in % of GDP

net capital import net capital export

1. Austria‘s favourable fundamentals

Source: European Commission (AMECO) as of May 2017

1) OeNB, April 2018

Austria is an International Net Lender

17

Furthermore Austria has a

positive net international investment position

(Q4 2017: 6.0% of GDP)1

Investor Information, April 2018

Republic of Austria

-4

-3

-2

-1

0

1

2

3

4

5

Slo

ve

nia

Belg

ium

Luxem

bo

urg

Germ

an

y

Lithuan

ia

Neth

erland

s

Fin

land

Malta

Irela

nd

Austr

ia

Euro

zone (

EU

-19)

Slo

va

kia

Po

rtugal

Itla

y

Gre

ece

Fra

nce

Spain

Latv

ia

Cypru

s

Esto

nia

Source: European Commission Ageing Report, May 2015 (baseline scenario)

Pursuing further structural pension reforms is one of the key goals of the federal government.

Total Age-related expenditure in the euro area (projected change in pp of GDP, 2013-2040)

1. Austria‘s favourable fundamentals

Age-related expenditure under control

18 Investor Information, April 2018

Republic of Austria

80

85

90

95

100

105

110

115

120 Austria

Belgium

Netherlands

France

Spain

Finland

EU-28

Germany

Italy

Portugal

Greece

Austria‘s population growth outperforms European average

19

Source: Eurostat, data extracted in April 2017

Population Projections (main scenario): Assumptions related to fertility, mortality, net international migration as well as the approximated values of life expectancy at birth

2015 = 100 in %

1. Austria‘s favourable fundamentals Investor Information, April 2018

Republic of Austria

0,20

0,25

0,30

0,35

0,40

0,45

0,50

Gini Coefficient

Source: OECD Income Distribution Database, no data for Japan and Russia available / Gini coefficient 2015 or latest available, November 2017

Austria’s low Gini coefficient indicates a relatively equal income distribution

1. Austria‘s favourable fundamentals

High Social Stability

20 Investor Information, April 2018

Republic of Austria

100

110

120

130

140

150

160

170

180

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Ireland Austria NetherlandsSweden Germany BelgiumFinland France EU 19

in % of EU-28 average

Source: European Commission, Eurostat as of November 2017

1) in purchasing power standards

1. Austria‘s favourable fundamentals

Austria’s unemployment rate:

4th lowest in the Eurozone

Austria’s GDP per capita1:

4th highest in the EU

Austria’s favourable fundamentals

High GDP per capita and low unemployment

21

• GDP per capita since 2007 up

from 5th to 4th rank in the EU

• Unemployment rate nearly half of the

Eurozone-average

• 3rd lowest long-term unemployment

and 3rd lowest youth unemployment

rate in the Eurozone

Luxembourg: 267

Investor Information, April 2018

0

2

4

6

8

10

12

14

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

in %

Austria Euro area EU

Republic of Austria

1

1,5

2

2,5

3

3,5

4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

in % of GDP

Finland

Austria

Germany

Belgium

OECD

France

Netherlands

EU-28

UK

Luxembourg

Source: OECD (2017), Gross domestic spending on R&D (indicator). doi: 10.1787/d8b068b4-en (Accessed on 24 November 2017)

1. Austria‘s favourable fundamentals

Strong Innovation Performance

Austria’s R&D expenditure above peers

22

Research and Development expenditure

Investor Information, April 2018

Republic of Austria

Source: MIP Scoreboard, European Commission as of November 2017

1. Austria‘s favourable fundamentals

EU Macroeconomic Imbalance Procedure

Austria with no major imbalances

23

External Imbalances Internal Imbalances New employment indicators

Current Account

Balance as % of GDP,

3 year average

Net International Investment

Position as % of GDP

Real Effective Exchange Rate (42 trading partners,

based on HICP/CPI), %

change (3 years)

Export Market

Shares, % change

(5 years)

Nominal ULC, % change (3 years)

Deflated House Price

Index (1-year % change)

Private Sector Credit Flow as % of

GDP, consolidated

Private Sector

Debt as % of GDP, consoli-dated

General Govern-

ment Sector

Debt as % of GDP

Unemployment Rate,

3 year average

Total Financial

Sector Liabilities (1-year % change)

Activity rate in % of total population

aged 15 - 64 (3 years change)

Long-term unemployment

rate in % of active population aged 15-74 (3 years

change)

Youth unemployment

rate in % of active

population aged 15-24 (3 years

change)

# of indicators

beyond threshold

Threshold -4/+6% -35% +/- 5% (EA)

+/- 11% (Non-EA)

-6% 9% (EA)

12% (Non-EA)

6% 14% 133% 60% 10% 16.5% -0.2 0.5 2.0

Belgium -0.3 51.2 -0.4 -2.3 -0.6 1.0 13.3 190.1 105.7 8.3 1.2 0.1 0.1 -3.6 2

Germany 8.1 54.4 -2.6 2.9 5.2 5.4 3.8 99.3 68.1 4.6 5.2 0.3 -0.6 -0.7 2

Luxembourg 5.0 34.7 -1.5 26.2 2.5 5.9 1.5 343.6 20.8 6.3 7.5 0.1 0.4 2.2 2

Denmark 8.4 54.8 -1.5 -4.2 3.4 4.2 -10.4 210.7 37.7 6.3 3.3 1.9 -0.4 -1.0 2

Austria 2.2 5.6 1.0 -4.0 5.8 7.2 3.2 124.0 83.6 5.8 -2.4 0.7 0.6 1.5 3

France -0.7 -15.7 -3.1 -2.4 1.4 1.0 6.2 146.9 96.5 10.3 4.3 0.7 0.2 -0.3 3

Netherlands 8.8 69.1 -2.3 0.1 -1.1 4.4 1.5 221.5 61.8 6.8 5.3 0.3 0.0 -2.4 3

Sweden 4.6 11.2 -9.2 -7.9 2.0 7.6 7.6 188.5 42.2 7.4 9.0 1.0 -0.1 -4.7 3

UK -5.5 -1.1 0.2 -0.1 3.1 5.5 5.8 168.1 88.3 5.4 9.8 0.9 -1.4 -7.7 3

Finland -1.2 -2.3 0.5 -14.1 2.1 -0.3 2.2 149.3 63.1 9.0 4.5 0.7 0.6 0.2 4

Ireland 5.5 -176.2 -6.6 59.8 -20.5 6.6 -19.0 278.1 72.8 9.5 *9,5 0.7 -3.6 -9.6 5

Investor Information, April 2018

Republic of Austria

0

0,5

1

1,5

2

2,5

3

3,5

Ire

land

Ma

lta

Lu

xe

mbo

urg

Cypru

s

Sw

itzerl

and

Belg

ium

Ne

therl

and

s

Spain

No

rwa

y

Sw

ede

n

Fra

nce

Germ

any

De

nm

ark

Lithu

ania

La

tvia

Ca

nad

a

Fin

land

Hu

nga

ry

Ita

ly

Austr

ia

Migration Factor Foreign Direct Investment Factor

Financial Factor Export factor

Austria: Least exposed to Brexit scenario

24

S&P‘s Brexit Sensitivity Index

Source: S&P, “Who has the most to lose from Brexit?” Brexit Sensitivity Index (June 9, 2016)

1. Austria‘s favourable fundamentals Investor Information, April 2018

Republic of Austria

• Diversified and competitive economy

• No major macroeconomic imbalances, low private sector indebtedness

• High level of innovation

- R&D expenditure 2017e: above 3% of GDP / among Top-10 worldwide1

• Strong exports and tourism

- 2nd most diversified export structure in the world (out of 217 countries)2

• 4th lowest unemployment in Eurozone

• Sustainable current account surplus

• Net capital exporting country and positive net international investment position

• High savings ratio / Top-10 savers worldwide3

• 4th richest country in the EU4

• 4th most peaceful country in the world (out of 163)5

• Very low vulnerability to climate change / ranked 3 out of 116 countries worldwide6

Austria

A Safe Haven Core-Eurozone Economy

25

1) Statistics Austria, March 2018 / Research and Development Expenditures in % of GDP, February 2018 (UNESCO)

2) UNCTAD Statistics, Concentration and diversification indices of merchandise exports, February 2018

3) World Bank Global Financial Inclusion Database, (% aged 15+) saved any money in the past year

4) 2017 GDP in Euro per capita, Eurostat, March 2018

5) Institute for Economics and Peace, Global Peace Index 2017

6) S&P, May 2014

1. Austria‘s favourable fundamentals Investor Information, April 2018

Republic of Austria

0

5

10

15

20

25

30

35

40

45

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018e

in b

n E

UR

Redemptions

Net funding volume

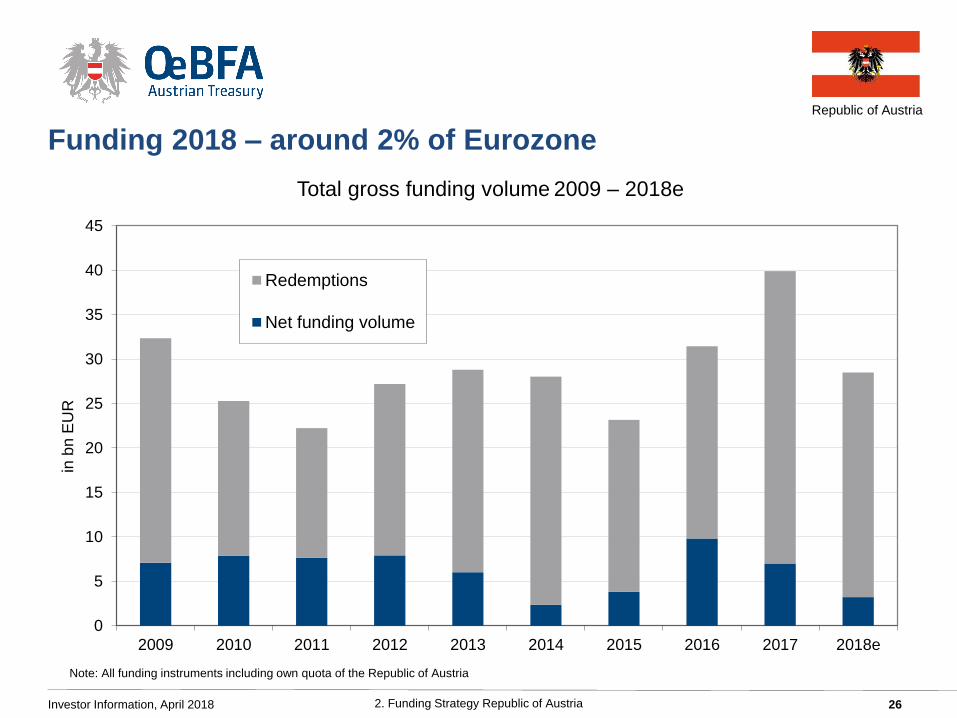

Funding 2018 – around 2% of Eurozone

26 2. Funding Strategy Republic of Austria Investor Information, April 2018

Total gross funding volume 2009 – 2018e

Note: All funding instruments including own quota of the Republic of Austria

Republic of Austria

Funding Outlook 2018

27 2. Funding Strategy Republic of Austria Investor Information, April 2018

Total issuance including all instruments (RAGB, T-bills, EMTN, loans):

2018: 27-30 bn EUR 2017: 39.9 bn EUR (updated forecast from Sept 7, 2017: 38–41bn EUR)

RAGB issuance 2018: 20–23 bn EUR RAGB issuance 2017: 24-26bn EUR (updated forecast from Sept 7, 2017)

outcome: 26.1 bn EUR

2018: one or two syndicated EUR issues

Total portfolio tenor (end-2018): 9.6-10.2 years (end-2017: 10.0 years)

Total portfolio interest fixing period (end-2018): 10.2-10.8 years (end-2017: 10.8 years)

As of April 11, 2018: around 45% of total funding programme completed

Republic of Austria

10.0 y

4.04%

2.47%

3.33

2.88 2.90

2.17

1.53

0.91

0.49 0.30

0.43

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013 2014 2015 2016 2017

in % in years

Total Annual Funding: Avg. Maturity Years (lhs) Federal Debt Portfolio: Avg. Maturity Years (lhs)

Federal Debt Portfolio: Avg. Effective Interest Rate % (rhs) Total Annual Funding: Avg. Yield % (rhs)

Key metrics of Federal Debt Portfolio 2009-2017

28 2. Funding Strategy Republic of Austria Investor Information, April 2018

Republic of Austria

29

Auction Calendar & Issuance 2018

• Volume and tenors are announced one week prior to the issue date at www.oebfa.at

• A re-opening of existing issues is regularly done in order to enhance liquidity.

2. Funding Strategy Republic of Austria

Announcement Issue date Value date

Jan 2 Jan 9 Jan 11 EUR 0.52 bn increase of 1.50% RAGB 2016-2047

EUR 0.86 bn increase of 0.50% RAGB 2017-2027

Jan 17 Jan 18 Jan 25 EUR 4.0 bn syndication of 0.75% RAGB 2018-2028

Jan 30 Feb 6 Feb 8 EUR 0.58 bn increase of 0.75% RAGB 2018-2028

EUR 0.83 bn increase of 0.00% RAGB 2016-2023

Feb 27 Mar 6 Mar 8 EUR 0.46 bn increase of 0.75% RAGB 2018-2028

EUR 0.69 bn increase of 0.00% RAGB 2017-2022

Apr 3 Apr 10 Apr 12 EUR 0.40 bn increase of 4.15% RAGB 2007-2037

EUR 0.75 bn increase of 0.75% RAGB 2018-2028

Apr 30 May 8 May 11

May 29 Jun 5 Jun 7

Jun 26 Jul 3 Jul 5

Jul 31 Aug 7

(reserve date)

Aug 9

Aug 28 Sep 4 Sep 6

Sept 25 Oct 2 Oct 4

Oct 30 Nov 6 Nov 8

Dec 4 Dec 11 Dec 13

Investor Information, April 2018

• The average tenor of the outstanding debt is 10.32 years (as of March 31, 2018).

Republic of Austria

Cornerstones of Funding Strategy

30 2. Funding Strategy Republic of Austria

• Diversity of funding sources (geographically and by instruments)

• Financial flexibility (e.g. to address specific investor demand)

• Capitalizing on scarcity value and strong fundamentals

• Secondary market liquidity

• Monthly auctions

• 21 RAGB primary dealers, 9 ATB dealers

• One of the lowest debt rollover ratios

• Conservative debt management strategy

• over 95% fixed rate

• less than 10% short term debt

• No foreign currency risk

• Well-balanced maturity profile

• Reliability, Transparency, stability-oriented approach

• Rigorous Investor Relations Programme

Investor Information, April 2018

Republic of Austria

Financing Instruments Republic of Austria

• Government bonds RAGB

• Debt issuance programme (DIP 144A)

• EMTN-Programme (Euro Medium Term Notes)

• Australian Dollar MTN-Programme – „Kangaroo Programme“

• Online retail savings product (bundesschatz.at)

• Loans and Schuldschein-Format

• Austrian Treasury Bills (ATB-Programme)

31 2. Funding Strategy Republic of Austria Investor Information, April 2018

Republic of Austria

Primary Dealer Panel Republic of Austria

32 2. Funding Strategy Republic of Austria

• Barclays Bank PLC

• BAWAG P.S.K. Bank für Arbeit und Wirtschaft und

Österreichische Postsparkasse AG

• BNP Paribas

• Citigroup Global Markets Limited

• Commerzbank AG

• Deutsche Bank Aktiengesellschaft

• Erste Group Bank AG

• Goldman Sachs International Bank

• HSBC France

• J.P. Morgan Securities plc

• Landesbank Baden-Württemberg

• Merrill Lynch International

• Morgan Stanley & Co. International plc

• Natixis

• NatWest Markets

• Nomura International plc

• Oberbank AG

• Raiffeisen Bank International AG

• Société Générale

• UniCredit Bank AG

• Volksbank Wien AG

• Bank of America Merrill Lynch International

Limited

• Barclays Bank PLC

• BAWAG P.S.K. Bank für Arbeit und Wirtschaft und

Österreichische Postsparkasse AG

• Citigroup Global Markets Limited

• Credit Suisse Securities (Europe) Limited

• Goldman Sachs International

• Raiffeisen Bank International AG

• UBS Limited

• UniCredit Bank AG

21 Primary Dealers for Austrian Government Bonds

9 Dealers for Austrian Treasury Bills

Investor Information, April 2018

Republic of Austria

• defined as short-term debt stock of the previous year plus maturing medium- and long-term debt in % of GDP - indicator for refinancing-risk

• Austria: very low refinancing-risk

• Conservative strategy

Source: S&P Global Sovereign Debt Report 2018, February 2018

Debt Rollover Ratio among lowest worldwide

33 2. Funding Strategy Republic of Austria Investor Information, April 2018

EU 19 2015 2016 2017 2018e

Italy 20,2 18,0 19,0 16,5

Belgium 16,3 15,9 16,2 14,6

Portugal 15,8 20,1 16,4 14,3

Spain 15,7 14,9 14,7 13,2

Greece 17,4 18,3 13,7 10,6

France 13,5 17,1 11,0 10,3

Netherlands 9,3 6,0 8,7 7,5

Finland 5,6 6,9 8,0 6,6

Ireland 6,9 4,9 5,1 6,0

Slovenia 6,1 9,0 6,7 5,4

Germany 6,2 6,1 5,2 5,3

Cyprus 11,4 13,2 3,9 5,3

Malta 6,1 7,9 6,5 5,2

Austria 5,4 6,2 6,1 5,2

Lithuania 4,5 4,3 3,0 5,1

Latvia 7,6 2,6 5,5 4,5

Slovakia 3,3 4,9 5,9 3,7

Luxembourg 0,0 0,0 0,4 1,2

Estonia 0,1 0,1 0,1 0,1

Average 9,0 9,3 8,2 7,4

Others 2015 2016 2017 2018e

Japan 75 70,2 65,6 58,1

USA 16,1 18,1 19,0 19,0

UK 6,9 14,8 7,6 6

Sweden 11,6 7,6 7,3 6,8

Norway 4,3 2,6 3,9 2,8

Turkey 4,1 3,4 3,0 3,0

Switzerland 2,3 2,5 1,9 2,1

Republic of Austria

Source: ECB, Austrian Treasury / data as of 31 March 2018

34

* Public Sector Puchase Programme of the Eurosystem (more details: PSPP Q&A on ECB website)

• Austria‘s capital key: 2.7%

• Weighted avg. maturity of holdings: 8.82 yrs

• Purchases will run at least until September 2018

2. Funding Strategy Republic of Austria

PSPP* holdings of RAGBs as % of outstanding stock

Investor Information, April 2018

0%

5%

10%

15%

20%

25%

30%

35%

Mar

20

15

Apr

20

15

May 2

01

5

Jun

201

5

Jul 20

15

Aug 2

01

5

Sep 2

01

5

Oct 20

15

No

v 2

01

5

De

c 2

01

5

Jan

201

6

Feb

20

16

Mar

20

16

Apr

20

16

May 2

01

6

Jun

201

6

Jul 20

16

Aug 2

01

6

Sep 2

01

6

Oct 20

16

No

v 2

01

6

De

c 2

01

6

Jan

201

7

Feb

20

17

Mar

20

17

Apr

20

17

May 2

01

7

Jun

201

7

Jul 20

17

Aug 2

01

7

Sep 2

01

7

Oct 20

17

No

v 2

01

7

De

c 2

01

7

Jan

201

8

Feb

20

18

Mar

20

18

Apr

20

18

May 2

01

8

Jun

201

8

Jul 20

18

Aug 2

01

8

Sep 2

01

8

0

10

20

30

40

50

in % EUR bn Estimated OeNB holdings of RAGBs % of RAGB stock - projected (rhs)

Republic of Austria

• Over 90% of debt held by investors domiciled in Europe

• Over 80% within the Eurozone1

Diversified investor base with Eurozone as home market (and strong overweight by Austrian investors)

Domestic Non-domestic

Prior to introduction of EUR around 70% (=ATS) 30%

After introduction of EUR around 80% (=EUR) 20%

Distribution by region2

Europe (incl. Austria) 87%

Americas 7%

Asia 3%

Middle East 2%

Africa 1%

Distribution by category2

Banks 38%

Asset managers 30%

Insurance & pension funds 16%

Central banks & int. org. 12%

Retail 3%

Others 1%

Overview: Investors in Austrian Government Bonds

35

Source: 1) IMF (CPIS) / Austrian National Bank

2) Austrian Treasury estimates: syndicated RAGB issues 2012-2018

2. Funding Strategy Republic of Austria Investor Information, April 2018

Republic of Austria

Austria’s stable Investor Base

36 2. Funding Strategy Republic of Austria

Investors by type and region (syndicated RAGB issues)*

Source: Austrian Treasury

* Primary market: 10-year maturities only (excluding PSPP purchases)

Investor Information, April 2018

00%

10%

20%

30%

40%

50%

60%

70%

80%

Central Banks &Official Institutions

Asset Managers Banks Insurance & PensionFunds

Retail Other

2012 2013 2014 2015 2016 2017 2018

00%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Austria Europe excl. Austria Africa Asia Middle East America

2012 2013 2014 2015 2016 2017 2018

Republic of Austria

0

5

10

15

20

25

30

201

82

01

92

02

02

02

12

02

22

02

32

02

42

02

52

02

62

02

72

02

82

02

92

03

02

03

12

03

22

03

32

03

42

03

52

03

62

03

72

03

82

03

92

04

02

04

12

04

22

04

32

04

42

04

52

04

62

04

72

04

82

04

92

05

02

05

12

05

22

05

32

05

42

06

22

06

32

06

42

06

92

07

02

07

12

07

22

07

32

07

42

08

62

08

72

11

62

11

7in

bn

. E

UR

Redemptions as of 31.03.2018

Redemptions as of 31.12.2017

Conservative debt portfolio:

• over 10yrs average maturity

• over 95% fixed rate

• among the lowest rollover ratios

worldwide

2. Funding Strategy Republic of Austria

Debt Portfolio – Redemption Profile

Well Diversified

37 Investor Information, April 2018

Republic of Austria

10y Yields - Austria vs. Germany

38

Source: Bloomberg

2. Funding Strategy Republic of Austria Investor Information, April 2018

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

01

.04

.08

01

.07

.08

01

.10

.08

01

.01

.09

01

.04

.09

01

.07

.09

01

.10

.09

01

.01

.10

01

.04

.10

01

.07

.10

01

.10

.10

01

.01

.11

01

.04

.11

01

.07

.11

01

.10

.11

01

.01

.12

01

.04

.12

01

.07

.12

01

.10

.12

01

.01

.13

01

.04

.13

01

.07

.13

01

.10

.13

01

.01

.14

01

.04

.14

01

.07

.14

01

.10

.14

01

.01

.15

01

.04

.15

01

.07

.15

01

.10

.15

01

.01

.16

01

.04

.16

01

.07

.16

01

.10

.16

01

.01

.17

01

.04

.17

01

.07

.17

01

.10

.17

01

.01

.18

01

.04

.18

Yield in %

10y Austria benchmark yield

10y Germany benchmark yield

Republic of Austria

• Strong credit fundamentals, diversified and competitive economy

• No major macroeconomic imbalances

• Sound financial policies (e.g. falling debt/GDP ratio)

• High institutional strength

• Low unemployment rate

• Strong exports and tourism

• Sustainable current account surplus

• Conservative funding strategy

• Net capital exporting country and positive net international investment position

Summary

39 Investor Information, April 2018

Republic of Austria

• www.oebfa.at (Austrian Treasury): auction calendar, debt portfolio, rating reports, etc.

• www.bundesschatz.at (Online retail savings product Republic of Austria)

• www.bmf.gv.at (Federal Ministry of Finance): details on the Austrian budget and Financial Stability Measures

• www.statistik.at (Statistics Austria)

• www.rechnungshof.gv.at/berichte/bundesrechnungsabschluss.html (Austrian Court of Audit): Reports on the Federal Financial Statements (in German only)

• www.oenb.at (Austrian National Bank)

• www.fiskalrat.at (Austrian Fiscal Advisory Council)

• http://ec.europa.eu/eurostat (Eurostat)

• http://europa.eu/efc/about-sub-committee_en (EFC Sub-Committee on EU Sovereign Debt Markets)

• www.oekb.at/en/capital-market/government-bonds/pages/default.aspx (OeKB / Austrian Government Bonds page)

Further Information

40 Investor Information, April 2018

Republic of Austria

Austrian Treasury

Austria – 1010 Vienna, Seilerstaette 24

Phone: (+43 1) 512 25 11- 0

Web: www.oebfa.at

Reuters: AFFA01…07 Bloomberg: RAGB, AUST

Managing Director

Markus Stix, [email protected]

Capital Markets Contact:

Christian Schreckeis, CFA (Head), [email protected], ext. 48

Martin Dymkowski, [email protected], ext. 46

Christoph Frömel, CFA, [email protected], ext. 44

Anja Tritremmel, CFA, [email protected], ext. 37

Money Markets Contact:

Günther Wahl (Head), [email protected], ext. 16

Sabine Denk, CFA, [email protected], ext. 14

Stefan Girsch, MA, FRM, [email protected], ext. 33

Pia Zivanovic-Amann, MBA, [email protected], ext. 47

Contact

41 Investor Information, April 2018