investor presentation · 2017-10-02 · 3 fy2017 key performance indicators review group to focus...

TRANSCRIPT

0www.maybank.com

Investor Presentation

Financial Results2Q FY2017 and 1H FY2017 ended 30 June 2017

30 August 2017

Humanising Financial Services

1

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

2

Net profit surged

29.9% YoY for

1H FY2017

1H FY2017 OverviewNet income growth of 5.8% to RM11.4 billion, with net profit rising 29.9% to RM3.4 billion

• Net income growth of 5.8% YoY supported by growth in net fund based income of

10.9% YoY as Group loans grew 6.4% across home markets

• NIM improved by 13bps YoY to 2.41% from 2.28%, on the back of improved yields

for securities portfolio and cheaper funding source (Group CASA) growth of 10.4%

• PPOP growth of 5.0% YoY

• Net impairment losses reduced by 33.1% YoY

1

• Loan loss coverage (including regulatory reserve) of 92.6%

• Slower gross impaired loans formation of 4.3% QoQ, with Group GIL ratio at 2.53%

• Net credit charge off of 57 bps

Asset Quality

Indicators

• Strong Group LCR of 146% and lower Group LDR of 93.8% as at June 2017

• Total capital and CET1 ratios at 18.98%* and 13.56%* respectively as at June 2017

• Interim dividend of 23 sen per share

Maintained Robust

Liquidity and Capital

Positions

4

Strong PPOP growth

of 9.6% QoQ

(2Q’17 vs 1Q’17)

2 • PPOP growth was supported by improved net income growth of 4.6% QoQ and

lower overheads expenses

• Net income growth was supported by higher net fee based income of 15.9% QoQ

• Net profit was marginally down due to higher net impairment losses

3

Note:

*After proposed dividend and assumption of 85% reinvestment rate. Fully loaded Group CET1 capital ratio is at 13.37%.

3

FY2017 Key Performance Indicators ReviewGroup to focus on picking up momentum in key markets in 2H FY2017

Note:

* Normalised to exclude the effects for Singapore, Indonesia, Philippines, Greater China and Labuan(USD)

^ Restated following a BNM circular dated 21 June 2017 which excludes structured deposits

Key Performance IndicatorsFY2017

Guidance

1H FY2017 Achievement

Dec 2016 Mar 2017 Jun 2017 QoQ Annualised YoY

Headline KPI

Return on Equity 10%-11% - - - 9.7 -

Other Guidance

Group Loans Growth (reported)

(RM’ billion)6%-7% 485.7 486.1 480.1 (1.2)% (2.3)% 6.4%

Group Loans Growth (normalised)* - (0.4)% (1.3)% 4.4%

• Malaysia (RM’ billion) - 272.0 270.7 273.8 1.1% 1.3% 6.4%

• Singapore (SGD’ billion) - 38.9 39.1 38.5 (1.5)% (2.1)% 4.9%

• Indonesia (Rupiah’ trillion) - 124.7 122.6 123.1 0.3% (2.7)% 3.2%

Group Deposits Growth (reported)

(RM’ billion)6%-7% 517.1^ 508.1^ 511.7^ 0.7% (2.1)% 1.2%

Group Deposits Growth (normalised)* - 1.5% (1.3)% (0.6)%

4

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

5

P&L Summary: 1H FY2017 Revenue and PPOP up 5.8% and 5.0% respectively, with net profit increasing 29.9% YoY on lower net impairment losses

More

details on RM million1H

FY2017

1H

FY2016YoY

2Q

FY2017

1Q

FY2017QoQ

2Q

FY2016YoY

s.7 Net fund based income * 8,261.4 7,447.2 10.9% 4,143.5 4,117.9 0.6% 3,653.6 13.4%

s.7/8/

31 Net fee based income * 3,102.5 3,290.5 (5.7)% 1,665.8 1,436.8 15.9% 1,692.3 (1.6)%

s.6/30 Net operating income 11,363.9 10,737.7 5.8% 5,809.2 5,554.7 4.6% 5,345.9 8.7%

s.10 Overhead expenses (5,597.5) (5,243.9) 6.7% (2,793.4) (2,804.0) (0.4)% (2,623.7) 6.5%

s.6 Pre-provisioning operating profit (PPOP)¹ 5,766.4 5,493.8 5.0% 3,015.8 2,750.6 9.6% 2,722.2 10.8%

Net impairment losses (1,378.5) (2,059.7) (33.1)% (835.7) (542.8) 54.0% (1,181.2) (29.2)%

Operating profit 4,387.9 3,434.2 27.8% 2,180.1 2,207.9 (1.3)% 1,541.0 41.5%

s.30 Profit before taxation and zakat (PBT) 4,493.6 3,515.3 27.8% 2,244.5 2,249.1 (0.2)% 1,584.0 41.7%

Profit attributable to equity holders of

the Bank (Net Profit)3,361.2 2,586.7 29.9% 1,658.4 1,702.8 (2.6)% 1,159.9 43.0%

EPS - Basic (sen) 32.8 26.4 24.1% 16.1 16.7 (4.0)% 11.8 36.2%

Note:

* From consolidated Group numbers, Insurance and Takaful accounts for 6.6% of net fund based income and 8.9% of net fee-based income

¹ Pre-provisioning operating profit (PPOP) is equivalent to operating profit before impairment losses

6

10,738

6,117

3,848

726 51 646

11,363

6,607

3,762

675 142

812

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

1H FY2016

1H FY2017

5,494

2,719 2,942

171 (5)

317

5,766

3,017 2,774

86 64

460

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

1H FY2016

1H FY2017

Group Global Banking

Franchise-Led Growth: 1H FY2017 (1/2)Growth in net income and PPOP, mainly driven by rise in Group Community Financial Services income

Net Operating Income

RM

million

RM

million

PPOP

Note:

Net income & PPOP for group includes expenditures of “Head Office & Others” of RM650.0 million for 1H FY2016 and RM634.1 million for 1H FY2017

+25.6%

+5.8%

+8.0% +>100% (2.2)% (7.1)%

(1.0)%

1H FY2016: 4,625 1H FY2017: 4,579

Group Global Banking (5.9)%

1H FY2016: 3,108 1H FY2017: 2,923

+45.4%

+5.0%

+11.0% +>100% (5.7)% (50.0)%

7

7,447

4,662

2,343

143 (3) 491

8,261

5,062

2,508

148 (4)556

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

1H FY2016

1H FY2017

Franchise-Led Growth: 1H FY2017 (2/2)Net fund based income rose 10.9% YoY, supported by growth in all business pillars

Note:

Net fund based income includes expenditures of “Head Office & Others” of RM188.6 million for 1H FY2016 and RM10.0 million for 1H FY2017.

Net fee based income includes expenditures of “Head Office & Others” of RM461.3 million for 1H FY2016 and RM624.1 million for 1H FY2017.

Net Fund Based Income

3,291

1,455 1,505

583

53 155

3,103

1,545 1,253

527

146 256

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

1H FY2016

1H FY2017

Net Fee Based Income

RM

million

RM

million

Group Global Banking

+13.2%

+10.9%

+8.6% +36.4% +7.1% +3.9%

6.9%

1H FY2016: 2,483 1H FY2017: 2,653

Group Global Banking (10.1)%

1H FY2016: 2,142 1H FY2017: 1,926

+65.0%

(5.7)%

+6.2% >100% (16.7)% (9.7)%

8

3,291 3,254

202

2,233

(2,399)

3,103 2,982

219

2,510

(2,609)

Total Other operating income Fee Income from IslamicOperations

Net Earned InsurancePremiums

Net Insurance Benefits &Claims Incurred, Net Fee& Commission Expensesand Life & Takaful Fund

Tax

1H FY2016

1H FY2017

RM

million

RM million 1H FY2016 1H FY2017 YoY

Commission, service charges and fees 1,772 1,768 (0.2)%

Investment & Trading Income 484 533 10.1%

Unrealised gain/ (losses) on securities 201 319 58.8%

Unrealised gain/ (losses) on derivatives 397 (12) (102.9)%

Foreign Exchange Profit 127 124 (2.2)%

Other Income 273 250 (8.5)%

Net Fee Based Income: 1H FY2017Lower net fee based income, arising mainly from unrealised losses on derivatives

(5.7)% (8.4)% 8.4% +12.4% +8.7%

9

2.43

2.31 2.31

2.27

2.41

FY2013 FY2014 FY2015 FY2016 1H FY2017

NIM Trend: 1H FY2017NIM improved 14 bps YTD to 2.41%

Net Interest Margin (%)

5-Year Trend

10

RM million1H

FY2017

1H

FY2016YoY

2Q

FY2017

1Q

FY2017QoQ

2Q

FY2016YoY

Personnel Costs 3,050.9 2,832.5 7.7% 1,543.9 1,507.0 2.5% 1,418.4 8.9%

Establishment Costs 941.9 941.2 0.1% 459.6 482.3 (4.7)% 465.4 (1.2)%

Marketing Expenses 245.1 275.2 (10.9)% 109.8 135.3 (18.8)% 135.2 (18.8)%

Administration & General (A&G)

Expenses 1,359.5 1,195.0 13.8% 680.1 679.4 0.1% 604.9 12.4%

Total 5,597.5 5,243.9 6.7% 2,793.4 2,804.0 (0.4)% 2,623.7 6.5%

%1H

FY2017

1H

FY2016YoY

2Q

FY2017

1Q

FY2017QoQ

2Q

FY2016YoY

Total Cost to Income ¹ 49.1 48.7 0.4 47.9 50.3 (2.4) 48.9 (1.0)

Group JAW Position (0.9) 5.0 2.2

Overheads: 1H FY2017Overheads growth of 6.7% YoY from higher personnel costs and A&G expenses; QoQ, overheads remained flat

Note:

¹ Total cost excludes amortisation of intangible assets for Maybank Indonesia and Maybank Kim Eng

11

+24.7%

44.9 44.7

Jun 16 Jun 17

187.2 197.1

71.4 78.0

Jun 16 Jun 17

451.1 480.1

Jun 16 Jun 17

Balance Sheet Management Group loans growth of 6.4% YoY supported by Group CASA growth of 10.4%

19.8 21.1

16.6 17.2

Jun 16 Jun 17

Community Financial Services Global Banking

95.6 93.5

23.5 29.3

Jun 16 Jun 17

257.3

36.7

119.3

RM

billion

SG

D b

illion

IDR

tri

llio

n

Gross Loans (YoY)

6.4% 4.9% 3.2% 6.4 %

RM

billion

Group Malaysia Singapore Indonesia

38.5

273.8123.1

10.4 13.4

Jun 16 Jun 17

170.4188.2

Jun 16 Jun 17

5.2%

RM

billion

RM

billion

SG

D b

illion

IDR

tri

llio

n

CASA (YoY)

+5.3%

+9.3%

117.2 123.2

Jun 16 Jun 17

10.4% 28.4% (0.4)%

+6.2%

+3.4%

(2.1)%

12

70%

64%

49%

37%30%

Gross ImpairedLoans

IA+CA Expectedcashflow ofimpairedborrowers

30% discounton expected

cashflow

50% disount inexpectedcashflow

59% discountin expected

cashflow

981.7

370.3

615.7 542.5

830.3

1,846.8

1,372.8

2QFY2016

3QFY2016

4QFY2016

1QFY2017

2QFY2017

1HFY2016

1HFY2017

Allowances for losses on loans

70.5%

74.8%

72.0% 71.2%70.1%*

Loan loss coverage

Allowance for losses on loans

Asset QualityGroup loan loss coverage of 70.1% and 92.6% (including regulatory reserve)

RM

million

Note:

*Loan loss coverage including Regulatory Reserve is 92.6%

Cashflow Coverage for Gross Impaired Loans

Covered by

borrowers’

expected

cashflow

13

8,5559,337

10,568

Dec 15 Mar 16 Jun 16

11,055 11,658 12,158

Dec 16 Mar 17 Jun 17

Asset QualityDespite uptick in Group GIL ratio to 2.53%, formation of impaired loans growth further slowed to 4.3% QoQ

Group GIL Ratio CompositionR

M m

illion

10.0% YTD

4.3% QoQ

RM

million

GIL Ratio Components Jun 2017 Mar 2017 Dec 2016 Sep 2016 Jun 2016

Non Performing Loans (NPL) 1.79% 1.77% 1.64% 1.35% 1.32%

Restructured & Rescheduled (R&R) 0.37% 0.33% 0.39% 0.52% 0.67%

Performing Loans Impaired Due to

Judgmental/ Obligatory Triggers (IPL)0.37% 0.30% 0.25% 0.35% 0.35%

GIL Ratio 2.53% 2.40% 2.28% 2.22% 2.34%

Slower QoQ growth in Group GIL volume from a year ago

5.4% QoQ

23.5% YTD

13.2% QoQ 9.1% QoQ

14

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

Gross Impaired Loans

Net Impaired Loans

1.38%0.98%

1.30%1.68%

2.29%

1.16%0.76%

1.07%1.37%

1.83%

Asset Quality by MarketStable QoQ asset quality trends in Malaysia and Indonesia but continued weakness in Singapore

3.99% 4.06%

4.36% 4.55% 4.42%

2.99% 2.86%

3.44% 3.54% 3.51%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

2.23%2.14%

2.06% 2.13% 2.12%

1.78%1.63%

1.44% 1.51% 1.49%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

Malaysia Singapore Indonesia

15

Asset Quality by Line of BusinessAsset quality weakness mainly in retail SME and corporate banking in Singapore and Indonesia

Mortgage Auto Finance Credit Cards

Retail SME Business Banking Corporate Banking

Consumer

Business

Note:

In Malaysia, industry GIL ratio for mortgage is 1.1%, 0.9% for auto finance, and 1.3% for credit cards. In Singapore, industry GIL figure is only available for mortgage, which was

0.5% as at June 2017.

In Indonesia, Business Banking includes Commercial, SME and Micro loans. Maybank Indonesia’s GIL ratios are mapped in accordance to its local regulatory reporting requirements

and does not include R&R.

0.60% 0.61% 0.57% 0.60% 0.60%

0.42% 0.44% 0.45%0.58% 0.60%

0.95%1.27% 1.51% 1.76%

2.22%

-3.00%

-2.00%

-1.00%

0.0 0%

1.0 0%

2.0 0%

3.0 0%

4.0 0%

0.0 0%

0.5 0%

1.0 0%

1.5 0%

2.0 0%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

0.53% 0.55% 0.51% 0.53% 0.53%

0.29%0.38% 0.32% 0.34% 0.27%

1.51% 1.54%

1.32%1.23%

1.40%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

0.80% 0.79% 0.72% 0.77% 0.80%

2.32%2.13%

2.26%2.08%

1.95%

2.56%2.41% 2.35%

2.48%2.67%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

1.43%1.45%

1.70%

2.09% 2.39%

1.66%1.74%

1.57%

1.89%

2.18%1.92%2.08% 2.00% 2.06%

2.05%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

11.25% 10.60%11.92% 12.49% 12.50%

1.69%2.34% 2.42% 2.66% 2.67%

1.40% 1.52% 1.77% 1.96% 1.93%

-2.00%

0.0 0%

2.0 0%

4.0 0%

6.0 0%

8.0 0%

10. 00%

12. 00%

0.0 0%

2.0 0%

4.0 0%

6.0 0%

8.0 0%

10. 00%

12. 00%

14. 00%

16. 00%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

Malaysia Singapore Indonesia

13.67% 14.20%

10.51% 10.30%11.32%

2.53% 2.47%

1.85% 1.93% 1.97%2.24%1.21%

1.89%2.62%

4.06%

-2.00%

0.0 0%

2.0 0%

4.0 0%

6.0 0%

8.0 0%

10. 00%

12. 00%

0.0 0%

2.0 0%

4.0 0%

6.0 0%

8.0 0%

10. 00%

12. 00%

14. 00%

16. 00%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

16

88% comes

from

supporting

upstream

Commodities Exposure: 30 June 2017Maybank Group’s exposure to direct and indirect oil and gas borrowers as well as other commodities

Notes:

• Group exposure is for three home markets

Malaysia, Singapore and Indonesia, based on

Group gross loans as at end June 2017.

• Agriculture includes rubber, oil palm and

cocoa sectors

• Metals and mining includes coal, lignite,

peat, metal ores, tin, iron, steel and non-

ferrous metal sectors

Agriculture

Maybank Group 1.80%

Malaysia 1.32%

Singapore 0.06%

Indonesia 0.42%

Metals & Mining

Maybank Group 1.44%

Malaysia 1.09%

Singapore 0.10%

Indonesia 0.25%

Oil & GasMaybank

GroupMalaysia Singapore Indonesia Others

Loan exposure 3.89% 2.31% 1.24% 0.16% 0.18%

Borrowers’ Status:Segmental Exposure:

Direct & Indirect Oil & Gas:

Borrowers with O&G related exposure

Other Sectors

Group exposure of 3.89% includes funded

and non-funded

34%

36%

6%

24%

Upstream

Supporting Upstream

Downstream

Supporting Downstream

Notes:

Supporting upstream includes services activities incidental to crude oil and natural gas extraction

including surveying. This includes providers of services/ activities related to O&G industry

Excluding non-funded, exposure is 3.47%

37%

4%

43%16%

Normal

Special Mention Account

Watchlist

GIL

17

13.99% 13.77% 13.56%

15.66% 15.41% 15.20%

19.29% 19.19% 18.98%

Dec 16 Jun 17 Jun 17

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

Group

Bank

Strong Capital Position: 30 June 2017Total capital and CET1 ratios (assuming 85% dividend reinvestment rate) at 18.98% and 13.56% respectively

Before proposed

dividend

After proposed

dividend,

assuming 85%

reinvestment

rate 2017 2018Jan 2019

Onwards

Minimum Common Equity Tier

1 Capital4.5% 4.5% 4.5%

Minimum Tier 1 Capital 6.0% 6.0% 6.0%

Minimum Total Capital 8.0% 8.0% 8.0%

Capital Conservation Buffer

(Phase in)1.250% 1.875% 2.500%

Other Capital Buffers

D-SIB Buffer

Countercyclical Capital buffer

Regulatory Requirements

To be determined

0% - 2.5%

Note:

Based on 85% reinvestment rate under the DRP, the fully loaded CET1 Ratio would be at 13.37% (Group) and 12.79% (Bank) respectively.

15.88% 14.74% 14.43%

18.23% 17.09% 16.79%

19.43% 19.85% 19.55%

Dec 16 Jun 17 Jun 17

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

18

61.0%

76.5% 74.9%79.9%

74.7% 71.9%78.5% 76.3% 78.1%

72.2%

Gross Dividend (sen) and Payout Ratio (%)

DividendSingle-tier interim dividend of 23 sen consisting of 5 sen cash portion and 18 sen electable portion

11

2832

22.524 24

20 23

8

44

32

36

33

3133 30

32

FY09 FY10 FY11 FP11 FY12 FY13 FY14 FY15 FY16 1H FY17

Final

Interim

* Actual Reinvestment Rate for Dividend Reinvestment Plan.

# The Net Dividend is 28.5 sen of which 15 sen is single-tier dividend.

• Maybank adopted the single-tier dividend regime with effect from FYE 31 Dec 2012

85.9%*

85.7%*

88.2%*85.9%*

88.5%*

91.1%*

86.1%*

88.6%*

#

82.6%*

8.0

55.0

60.0

36.0

65.0

53.557.0

84.0%*

DividendPayout Ratio

83.7%*

54.0

87.5%*

89.1%*

52.0

83.5%*

19

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

20

MFRS 9 Preparation (1/3)Maybank Group’s implementation project timeline

Maybank Group has established a project team with the assistance from external consultants to plan and manage

the implementation of MFRS 9. This implementation project consists of three phases:

Completed Phases 1 and 2. Currently

undertaking parallel run of Phase 3.

Impact to the financial statements in the

areas of classification and measurement

for financial assets and impairment.

Classification and measurement

requirements will affect financial

statements presentation and disclosures.

Impairment requirements are expected to

result in higher impairment allowance

losses.

Initial findings from parallel run based on

actual June 2017 Group capital ratios

indicate potential reduction of between

60 bps and 90 bps for day 1 adjustment to

retained earnings on 1 January 2018.

If regulatory reserve can be utilised, the

net impact to Group capital ratios will be

mitigated.

Snapshot Progress Report:

This involves:

i) Parallel run and deployment of solution tools; and

ii) Reassessment of solution tools and conclusion

Phase 3:

Go live

Aims to:

i) Develop detailed implementation plan

ii) Determine accounting policies to be adopted by the Group and the Bank; and

iii) Identify optimal solutions for the Group and the Bank

Phase 2:

Build, test and deploy

Aims to:

i) Provide clear understanding of the new accounting requirements via training

ii) Perform gap and impact assessment

iii) Understand the interdependencies with other projects; and

iv) Develop MFRS 9 blue-print

Phase 1:

Impact assessment and solution development

Nov 2015 – Jul 2016Aug 2016 – Jun 2017 Jul 2017 - current

Note: Impact analysis is subject to further refinement on

methodology.

21

MFRS 9 Preparation (2/3)Key differences of impairment assessments under MFRS 9

*except for purchased or originated credit impaired assets.

• Impairment assessment is now based on expected credit loss model (ECL) instead of incurred loss model. ECL is an

estimate on losses expected from a credit event, such as a payment default.

• Banks will now have to assess if there has been a significant increase in credit risk since initial recognition for the

asset, taking into account relevant forward looking information. This assessment is applicable to the entire

exposure of the borrower, which includes drawn and undrawn commitments.

• To assess the impact of an undrawn commitment, a credit conversion factor (CCF) is applied. CCF is a modelled

assumption on the expected proportion of the undrawn exposure that will be drawn prior to a default occurring.

• Forward looking information includes macroeconomic conditions (e.g. unemployment rate, inflation, OPR, GDP, and

FX) and readily available information providing a fair idea about the borrower’s future circumstances, affecting its

creditworthiness. Forward looking assumptions are applied to probability of default (PD) and loss given default (LGD).

• 12-month ECL is the entire credit loss on a financial asset weighted by the probability that the loss will occur in the

next 12 months.

• Lifetime ECL is an ECL that results from all possible default events over the expected life of the financial assets. It is

estimated based on the present value of all cash shortfalls over the remaining expected life of the financial asset.

12-month ECL

Categories

ECL Recognition Lifetime ECL

Performing

(Initial recognition)*

Under Performing

(Assets with significant increase in

credit risk since initial recognition)*

Non Performing

(Credit impaired assets)

PerformingWatchlist and

Special Mention AccountsNPL, IPL, R&R

Maybank Group’s sub

classifications

22

MFRS 9 Preparation (3/3)Key differences between MFRS 9 and MFRS 139

1. Performing : 12-month ECL

Assessment

Done

Categories

1. Performing : 12-month Incurred Loss

Exposure at Default

(Drawn + Undrawn facility)

Outstanding Balance

(Drawn facility)

Forward looking assumptions applied

to Probability of Default (PD) &

Loss Given Default (LGD)

Incurred Loss PD & LGDProvisioning

Method

MFRS 9 MFRS 139

2. Non Performing :

2. Under Performing : Lifetime ECL

3. Non Performing :

Retail Lifetime ECL

PD = 100%

Non-Retail Impaired borrower

individually assessed

Retail Lifetime Incurred Loss

PD = 100%

Non-Retail Impaired borrower

individually assessed

23

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

24

89.3% 91.6% 93.9% 95.7% 93.8%

33.7% 34.8%36.0%

37.4% 36.8%

32.3% 33.2%34.6% 35.7% 35.1%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

LDR CASA CASA (without IA)

89.4%96.2% 91.5% 90.8% 90.9%

38.3% 40.3% 40.5% 41.2% 40.4%

36.0% 37.6% 38.0% 38.4% 37.6%20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

LDR and CASA RatioImproved Group LDR ratio of 93.8% QoQ as deposits grew ahead of loans; CASA for Singapore and Indonesia improved

SingaporeIndonesia

Group Malaysia

104.8% 102.8% 104.5% 103.9% 102.4%

39.3% 38.1% 38.6% 37.0% 37.2%

90.3% 88.0% 88.9% 88.4% 86.7%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

LDR (Bank Level)

81.3% 80.9%87.4%

92.4% 91.4%

23.0% 25.1% 28.1% 30.5% 31.7%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17Note:

LDR is based on gross loans over customer deposits. LDR excludes structured deposits as per BNM’s circular dated 21 June 2017 “Classification and Regulatory Treatment for

Structured Products under FSA 2013 and IFSA 2013”.

Group and Malaysia LDRs include investment accounts totaling RM27.79 billion for 30 June 2017, RM31.71 billion for 31 March 2017, RM31.54 billion for 31 Dec 2016, RM30.37

billion for 30 Sep 2016 and RM30.96 billion for 30 June 2016

25

Borrowings, 5%

Capital Instruments, 3%

Customer Funding, 75%

FI Deposits, 7%

Equity, 10%

USD, 37%

MYR, 30%

IDR, 9%

JPY, 8%

SGD, 6%

HKD, 5%

Others, 5%

Funding Composition and Utilisation: 30 June 2017Well-diversified funding sources with strong customer funding base and ample liquidity with Group LCR of 146%

Balance Sheet Management

RM685.2b RM56.0b

148136

152134

146

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

Group LCR (%)

BNM min

requirement

of 80%

Stock of high quality liquid assets

Net cash outflows over 30-day periodRatio

BNM Minimum

Requirement

Year LCR

1 Jan 2017 80%

1 Jan 2018 90%

1 Jan 2019 & thereafter 100%

Liquidity Coverage Ratio (LCR)

Funding Breakdown

Note:

Customer Funding comprises Deposits from Customers & Investment Accounts of Customers.

Securities comprises Financial Assets at FVTPL, Financial Investments AFS & Financial Investments HTM.

By maturity:

≤ 1 Year 26%

> 1 Year 74%

Borrowings and Capital

Instruments by CurrencyFrom Group’s Total Assets of RM752.1 billion

Funding Composition:

Customer Funding 68%

Equity 9%

Borrowings + Capital Instruments 7%

FI Deposits 6%

Asset Classes:

Loans, Advances & Financing 63%

Securities 20%

26

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

27

Market Outlook2017 industry outlook for our home markets

Key Indicators Industry Outlook

Singapore

Malaysia

Indonesia

• GDP (f) 5.1% (2016: 4.2%)

• System loan (f) 5.4% for 2017

• OPR(f) 3.00% (2016: 3.00%)

• USD/MYR average (f) 4.35 (2016: 4.14)

• Inflation (f) 3.5-4.0% (2016: 2.1%)

• GDP (f) 3.0% (2016: 2.0%)

• System loan (f) 6-7%

• System deposit (f) 6-7%

• 3M SIBOR (f) 1.20% (2016: 0.97%)

• USD/SGD average 1.35 (2016: 1.38)

• Inflation (f) 0.9% (2016: -0.5%)

• GDP(f) 5.1% (2016: 5.0%)

• System loan (f): 10.2%

• System deposit (f): 10.0%

• Reference Rate (f) 4.75% (2016: 4.75%)

• USD/IDR average (f) 13,325 (2016: 13,330)

• Inflation average (f) 4.1% (2016: 3.5%)

• Loans growth to be supported by government

spend on infrastructure projects.

• Relative stability in local currency expected.

• Loan growth supported by better economic

outlook and loan demand.

• NIMs expected to remain stable or potentially

improve slightly.

• Asset quality for O&G support services sector will

continue to deteriorate if oil prices stay low.

• Loans growth in 2H 2017 to be supported by

ongoing expansion in the non-household sector.

• NIM expected to contract in 2H 2017 from

deposits competition.

• Asset quality and capital positions stable.

28

Managed cost growth to maintain CIR of < 50%

NIM management through disciplined pricing

and continued CASA growth

Continued management of asset quality ahead of MFRS 9 adoption in 2018

Maybank Performance OutlookGroup performance in 2H 2017

3

5

Top line growth supported by selective loans growth

and fee income contribution1

4

Growth for loan and deposit to be in line with industry growth2

29

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

30

68.7%

9.7%

10.0%

11.6%

Malaysia Singapore Indonesia Others

57.5%19.1%

15.3%

8.1%

57.7%25.8%

8.3%8.2%

80.3%

6.1%

9.2%4.4%

62.2%15.7%

14.4%

7.7%

57.8%25.1%

8.2%

8.9%

International & Malaysia Portfolio Mix 1H FY2017

Overseas:

42.2%

1H FY2016

Net Operating Income Profit Before Tax

1H FY2017

Overseas:

37.8%

Overseas:

19.7%

Gross loans*

(Jan 16 – Jun 16)

Overseas:

42.3%

Overseas:

42.5%

Overseas:

31.3%

(Jan 17 – Jun 17)

RM3.52b

Note:

* Including Islamic loans sold to Cagamas and excludes unwinding of interest

RM451.1bRM10.74b

RM4.49b RM480.1bRM11.36b

31

1,437 1,430

131

1,254

(1,378)

1,666 1,552

88

1,256

(1,230)

Total Other operating income Fee Income from IslamicOperations

Net Earned InsurancePremiums

Net Insurance Benefits &Claims Incurred, Net Fee& Commission Expensesand Life & Takaful Fund

Tax

1Q FY2017

2Q FY2017

RM

million

RM million 1Q FY2017 2Q FY2017 QoQ

Commission, service charges and fees 860 908 5.6%

Investment & Trading Income 232 301 29.4%

Unrealised gain/ (losses) on securities 206 113 (45.1)%

Unrealised gain/ (losses) on derivatives (76) 65 >100%

Foreign Exchange Profit 76 48 (37.6)%

Other Income 132 118 (10.5)%

Net Fee Based Income: QoQ

+15.9% +8.5% (32.9)% +0.2% (10.8)%

32

Unaudited Income Statement for Insurance and Takaful Business

RM million1H

FY2017

1H

FY2016YoY

2Q

FY2017

1Q

FY2017QoQ

2Q

FY2016YoY

Net interest income 550.2 484.7 13.5% 299.1 251.1 19.1% 251.7 18.8%

Net earned premiums 2,509.7 2,233.2 12.4% 1,255.8 1,253.9 0.2% 1,064.6 18.0%

Other operating income 432.1 390.7 10.6% 172.3 259.8 (33.7)% 143.1 20.4%

Total operating income 3,491.9 3,108.5 12.3% 1,727.2 1,764.8 (2.1)% 1,459.3 18.4%

Net insurance benefits & claims

incurred, net fee & commission

expenses and life & takaful fund tax

(2,689.3) (2,474.4) 8.7% (1,265.3) (1,424.0) (11.1)% (1,108.5) 14.1%

Net operating income 802.6 634.1 26.6% 461.9 340.8 35.5% 350.8 31.7%

Overhead expenses (353.1) (328.4) 7.5% (186.8) (166.3) 12.3% (167.7) 11.4%

PPOP 449.5 305.7 47.0% 275.1 174.5 57.7% 183.1 50.3%

Net impairment losses (11.6) (33.4) (65.2)% (9.8) (1.8) >100% (14.0) (29.8)%

Operating profit 437.9 272.4 60.8% 265.3 172.6 53.6% 169.1 56.9%

RM million1H

FY2017

1H

FY2016YoY

2Q

FY2017

1Q

FY2017QoQ

2Q

FY2016YoY

Net insurance benefits & claims

incurred, net fee & commission

expenses and life & takaful fund tax

(2,689.3) (2,474.4) 8.7% (1,265.3) (1,424.0) (11.1)% (1,108.5) 14.1%

Less: intercompany elimination 80.7 74.9 7.7% 35.1 45.6 (22.9)% 32.9 6.9%

Total net insurance benefits & claims

incurred, net fee & commission

expenses and life & takaful fund tax

(2,608.6) (2,399.5) 8.7% (1,230.2) (1,378.4) (10.8)% (1,075.7) 14.4%

Reconciliation of net insurance benefits & claims incurred, net fee & commission expenses and life & takaful fund tax

33

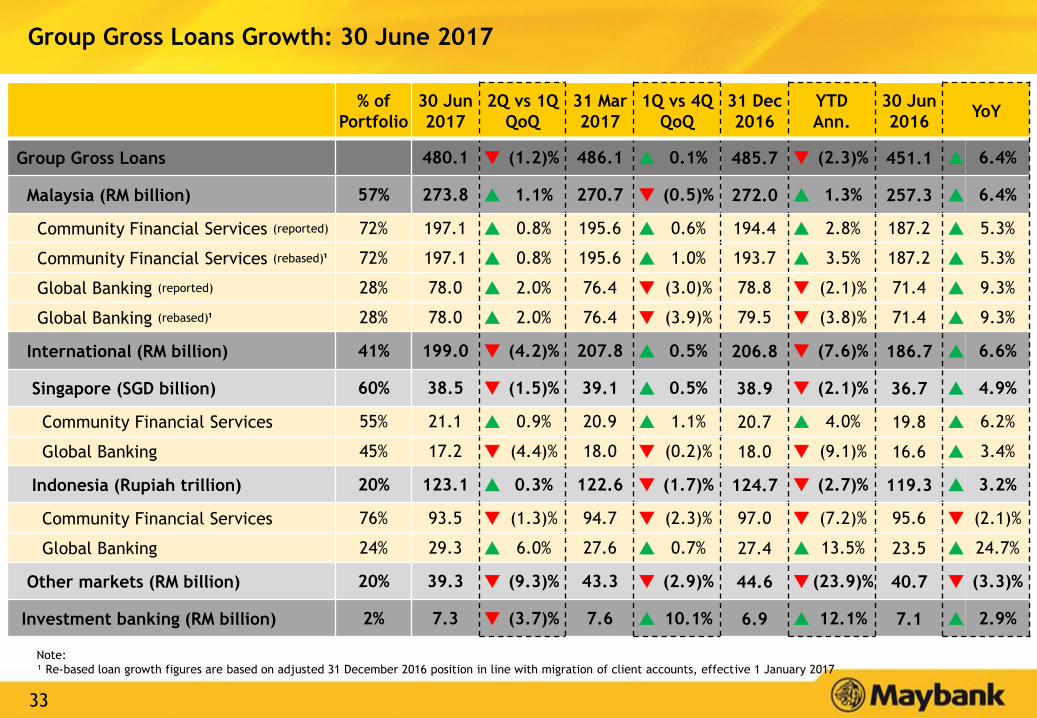

Group Gross Loans Growth: 30 June 2017

% of

Portfolio

30 Jun

2017

2Q vs 1Q

QoQ

31 Mar

2017

1Q vs 4Q

QoQ

31 Dec

2016

YTD

Ann.

30 Jun

2016YoY

Group Gross Loans 480.1 (1.2)% 486.1 0.1% 485.7 (2.3)% 451.1 6.4%

Malaysia (RM billion) 57% 273.8 1.1% 270.7 (0.5)% 272.0 1.3% 257.3 6.4%

Community Financial Services (reported) 72% 197.1 0.8% 195.6 0.6% 194.4 2.8% 187.2 5.3%

Community Financial Services (rebased)¹ 72% 197.1 0.8% 195.6 1.0% 193.7 3.5% 187.2 5.3%

Global Banking (reported) 28% 78.0 2.0% 76.4 (3.0)% 78.8 (2.1)% 71.4 9.3%

Global Banking (rebased)¹ 28% 78.0 2.0% 76.4 (3.9)% 79.5 (3.8)% 71.4 9.3%

International (RM billion) 41% 199.0 (4.2)% 207.8 0.5% 206.8 (7.6)% 186.7 6.6%

Singapore (SGD billion) 60% 38.5 (1.5)% 39.1 0.5% 38.9 (2.1)% 36.7 4.9%

Community Financial Services 55% 21.1 0.9% 20.9 1.1% 20.7 4.0% 19.8 6.2%

Global Banking 45% 17.2 (4.4)% 18.0 (0.2)% 18.0 (9.1)% 16.6 3.4%

Indonesia (Rupiah trillion) 20% 123.1 0.3% 122.6 (1.7)% 124.7 (2.7)% 119.3 3.2%

Community Financial Services 76% 93.5 (1.3)% 94.7 (2.3)% 97.0 (7.2)% 95.6 (2.1)%

Global Banking 24% 29.3 6.0% 27.6 0.7% 27.4 13.5% 23.5 24.7%

Other markets (RM billion) 20% 39.3 (9.3)% 43.3 (2.9)% 44.6 (23.9)% 40.7 (3.3)%

Investment banking (RM billion) 2% 7.3 (3.7)% 7.6 10.1% 6.9 12.1% 7.1 2.9%

Note:

¹ Re-based loan growth figures are based on adjusted 31 December 2016 position in line with migration of client accounts, effective 1 January 2017

34

RM billion% of

Portfolio

30 Jun

2017

2Q vs 1Q

QoQ

31 Mar

2017

1Q vs 4Q

QoQ

31 Dec

2016

YTD

Ann.

30 Jun

2016YoY

Community Financial Services (reported) 72% 197.1 0.8% 195.6 0.6% 194.4 2.8% 187.2 5.3%

Community Financial Services (rebased)¹ 72% 197.1 0.8% 195.6 1.0% 193.7 3.5% 187.2 5.3%

Consumer 58% 157.7 0.9% 156.3 0.6% 155.3 3.1% 149.3 5.7%

Total Mortgage 28% 77.6 1.8% 76.2 1.6% 75.0 7.0% 72.2 7.5%

Auto Finance 16% 44.6 0.9% 44.2 1.9% 43.4 5.7% 41.3 8.1%

Credit Cards 2% 6.6 2.2% 6.5 (4.3)% 6.7 (4.4)% 6.3 4.5%

Unit Trust 10% 26.2 (2.2)% 26.8 (2.7)% 27.6 (9.6)% 27.0 (2.6)%

Other Retail Loans 1% 2.6 3.1% 2.5 (2.7)% 2.6 0.6% 2.5 5.6%

Business Banking + SME (reported) 14% 39.4 0.2% 39.3 0.7% 39.1 1.7% 37.9 4.0%

Business Banking + SME (rebased)¹ 14% 39.4 0.2% 39.3 2.5% 38.4 5.3% 37.9 4.0%

SME (reported) 5% 13.8 4.2% 13.2 5.0% 12.6 18.9% 11.4 21.3%

SME (rebased)¹ 5% 13.8 4.2% 13.2 6.2% 12.4 21.4% 11.4 21.3%

Business Banking (reported) 9% 25.6 (1.9)% 26.1 (1.4)% 26.5 (6.4)% 26.6 (3.5)%

Business Banking (rebased)¹ 9% 25.6 (1.9)% 26.1 0.7% 25.9 (2.4)% 26.6 (3.5)%

Global Banking (Corporate) (reported) 28% 78.0 2.0% 76.4 (3.0)% 78.8 (2.1)% 71.4 9.3%

Global Banking (Corporate) (rebased)¹ 28% 78.0 2.0% 76.4 (3.9)% 79.5 (3.8)% 71.4 9.3%

Total Malaysia 273.8 1.1% 270.7 (0.5)% 272.0 1.3% 257.3 6.4%

Malaysia Loans Growth: 30 June 2017

Note:

¹ Re-based loan growth figures are based on adjusted 31 December 2016 position in line with migration of client accounts, effective 1 January 2017

35

Group Deposits Growth: 30 June 2017

% of

Portfolio

30 Jun

2017

2Q vs 1Q

QoQ

31 Mar

2017

1Q vs 4Q

QoQ

31 Dec

2016

YTD

Ann.

30 Jun

2016YoY

Group Gross Deposits 511.7 0.7% 508.1 (1.7)% 517.1 (2.1)% 505.6 1.2%

Malaysia (RM billion) 59% 304.9 1.0% 301.8 0.3% 300.9 2.7% 305.9 (0.3)%

Savings Deposits 13% 41.1 (0.3)% 41.2 6.4% 38.8 12.1% 42.0 (2.1)%

Current Accounts 27% 82.1 (1.3)% 83.2 0.0% 83.2 (2.5)% 75.2 9.2%

Fixed Deposits 52% 159.8 0.2% 159.5 (2.5)% 163.5 (4.6)% 173.6 (7.9)%

Others 7% 21.9 22.3% 17.9 15.9% 15.5 83.4% 15.2 44.8%

International 41% 208.8 0.3% 208.2 (4.4)% 217.7 (8.2)% 201.2 3.8%

Singapore (SGD billion) 63% 42.1 (0.5)% 42.3 (4.9)% 44.5 (10.7)% 45.1 (6.7)%

Savings Deposits 14% 5.8 (0.1)% 5.8 0.8% 5.7 1.4% 4.6 24.8%

Current Accounts 18% 7.6 6.6% 7.1 4.7% 6.8 23.2% 5.8 31.2%

Fixed Deposits 68% 28.8 (2.3)% 29.4 (7.9)% 32.0 (20.1)% 34.7 (17.2)%

Indonesia (Rupiah trillion) 19% 120.1 1.8% 118.0 (1.1)% 119.3 1.4% 114.4 5.0%

Savings Deposits 20% 24.5 (1.2)% 24.8 (3.1)% 25.6 (8.6)% 26.2 (6.6)%

Current Accounts 17% 20.2 7.0% 18.9 (7.5)% 20.4 (1.9)% 18.7 8.3%

Fixed Deposits 63% 75.4 1.5% 74.3 1.4% 73.3 5.8% 69.5 8.5%

Note:

• Deposits figures are restated following a BNM circular dated 21 June 2017 which excludes structured deposits

36

Key Operating Ratios

(%)1H

FY2017

1H

FY2016YoY

2Q

FY2017

1Q

FY2017QoQ

2Q

FY2016YoY

Return on Equity 9.7 8.3 1.4% 9.6 10.0 (0.4)% 7.5 2.1%

Net Interest Margin 2.41 2.28 13 bps 2.39 2.43 (4) bps 2.23 16 bps

Fee to Income Ratio 27.3 30.6 (3.3)% 28.7 25.9 2.8% 31.7 (3.0)%

Loans-to-Deposit Ratio 93.8 89.3 4.5% 93.8 95.7 (1.9)% 89.3 4.5%

Cost to Income Ratio1 49.1 48.7 0.4% 47.9 50.3 (2.4)% 48.9 (1.0)%

Asset Quality

Gross Impaired Loans Ratio 2.53 2.34 19 bps 2.53 2.40 13 bps 2.34 19 bps

Net Impaired Loans Ratio 1.73 1.72 1 bps 1.73 1.61 12 bps 1.72 1 bps

Loans Loss Coverage 70.1 70.5 (0.4)% 70.1 71.2 (1.1)% 70.5 (0.4)%

Net Charge off rate (bps) (57) (80) 23 bps (68) (45) (23) bps (85) 17 bps

Capital Adequacy (Group)2

CET1 Capital Ratio 13.56 13.59 (3) bps 13.56 13.02 54 bps 13.59 (3) bps

Total Capital Ratio 18.98 18.99 (1) bps 18.98 18.50 48 bps 18.99 (1) bps

Note:

¹ Total cost excludes amortisation of intangibles for Maybank Indonesia and Kim Eng.2 The capital ratios are adjusted based on the assumption of 85% reinvestment rate under the DRP for the period.

37

MFRS 9 Preparation (1/2)Credit loss provided under MFRS 9 standards (FOR ILLUSTRATION PURPOSES ONLY)

Under MFRS 9, there are three categories: Performing, Under Performing and Non Performing.

The ‘Performing’ category applies 12-mth expected credit loss (ECL). The ‘Under Performing’ and ‘Non Performing’

categories apply lifetime ECL.

Under the ‘Non Performing’ category, non-retail impaired borrowers are individually assessed. Shortfall will be provided

as individual allowance if exposure at default (EAD) > discounted cashflow.

Note: PD = Probability of Default. LGD = Loss Given Default. DF = Discount Factor.

: The example provided on this page is purely an illustration and does not reflect an actual situation to evaluate Maybank Group or its financial position

Timeline : Month 5 (PD1 x LGD x EAD1) / DF = ECL

(1.7% x 45% x RM8 mil) / 1.05

= RM58,286

Category : Performing

EAD : RM8 mil

Timeline : Month 7 [(PD1 x LGD x EAD1) / DF1 ] + [(PD2 x LGD x EAD2) / DF2 ] = ECL

[(1.7% x 45% x RM8 mil) / 1.05 ] + [(1.5% x 45% x RM5 mil) / 1.052 ]

= RM58,286 + RM30,612

= RM88,898

Category : Under Performing

(Status: Watchlist)

EAD : RM8 mil

Timeline : Month 9

Impaired borrower is individually assessedCategory : Non Performing

EAD : RM8 mil

Scenario: Corporate Borrower A has a drawn facility of RM10 million over a two year duration.

Assumptions:

PD1 = 1.7%

PD2 = 1.5%

LGD = 45%

EAD1 = RM8 mil

EAD2 = RM5 mil

DF = 5%

38

Timeline : Month 9

Impaired borrower is individually assessedCategory : Non Performing

Outstanding Balance : RM8 mil

MFRS 9 Preparation (2/2)Credit loss provided under MFRS 139 standards (FOR ILLUSTRATION PURPOSES ONLY)

Under MFRS 139, there are only two categories: Performing and Non Performing.

The ‘Performing’ category applies 12-mth incurred loss PD and LGD for performing, watchlist and special mention loans.

Under the ‘Non Performing’ category, non-retail impaired loans are individually assessed. Shortfall will be provided as

individual allowance if outstanding balance > discounted cashflow (DCF).

Note: PD = Probability of Default. LGD = Loss Given Default. DF = Discount Factor.

: The example provided on this page is purely an illustration and does not reflect an actual situation to evaluate Maybank Group or its financial position

Timeline : Month 5 (PD x LGD x outstanding balance) / DF = Incurred Loss

(1.5% x 40% x RM8 mil) / 1.05

= RM45,714

Category : Performing

Outstanding Balance : RM8 mil

Timeline : Month 7 (PD x LGD x outstanding balance) / DF = Incurred Loss

(1.5% x 40% x RM8 mil) / 1.05

= RM45,714

Category : Performing

(Status: Watchlist)

Outstanding Balance : RM8 mil

Scenario: Corporate Borrower A has a drawn facility of RM10 million over a two year duration.

Assumptions:

PD = 1.5%

LGD = 40%

DF = 5%

39

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

40

Community Financial Services: Overview of Market Share for Malaysia

*** Total bank deposits inclusive of investment asset (“IA”)

^ Without IA. With IA, the market share as at June’17 for Total Core Retail Deposits,

Retail CASA, Retail Savings, Demand Deposits and Retail Fixed Deposits are 19.1%, 25.8%,

28.3%, 21.9% and 16.5% respectively (against MBB retail IA).

* Refers to housing, shophouse and other mortgage loans

** Credit cards market share refer to receivables for commercial

^^ Excluding non-financial transactions as per BNM guidelines

^^^ Industry numbers only available half yearly

Loans

Total consumer (Household) 17.4% 17.5% 17.6% 17.5% 17.5% # 2

Auto (Purchase of transport vehicles) 24.1% 24.7% 25.4% 25.8% 25.7% # 2

Total mortgage * 13.4% 13.3% 13.3% 13.3% 13.2% # 2

Credit cards ** 17.6% 17.7% 18.0% 17.9% 17.9% # 1

Unit trust 52.3% 52.4% 51.6% 51.8% 51.8% # 1

Deposits

Total deposits *** 18.6% 17.3% 17.9% 17.6% 17.9% # 1

Total core retail deposits ^ 18.4% 18.3% 17.9% 18.0% 17.6% # 2

Retail CASA ^ 24.8% 24.7% 24.6% 25.1% 24.9% # 1

Retail savings ^ 30.7% 30.3% 30.3% 28.3% 28.3% # 1

Demand deposits ^ 15.1% 15.4% 15.3% 19.7% 19.4% # 1

Retail fixed deposits ^ 15.2% 15.0% 14.5% 14.3% 13.9% # 2

Channels

Internet banking - Subscriber base 44.1% 43.5% 44.6% 44.3% 43.6% # 1

Mobile banking - Subscriber base 28.2% 30.2% 31.4% 32.0% 31.7% # 1

Internet banking - Transaction Volume 51.9% 51.8% 52.2% 56.6% 56.6% # 1

Mobile banking - Transaction Volume 62.2% 63.0% 59.3% 42.7% 43.5% # 1

Branch network 19.3% 19.3% 18.8% 18.8% 18.6% # 1

Mar-17Sep-16Market share Jun-16

Mar-17

vs

Jun-17

Market

positionDec-16 Jun-17

^^ ^^ ^^

^^^

41

Business Banking + SME loans grew by 4.0% YoY to RM39.4

billion led by SME growth of 21.3% YoY

Community Financial Services: Overview of Malaysia Loans Portfolio

177.8 186.5 191.8

7.27 7.38 7.47

Jun 16 Dec 16 Jun 17

TFA Product per customer

102.8 103.8 103.8

3.25 3.36 3.46

Jun 16 Dec 16 Jun 17

TFA Product per customer

37.9 39.1 39.4

0

10

20

30

40

50

60

Jun 16 Dec 16 Jun 17

149.3 155.3 157.7

020406080

100120140160180200

Jun 16 Dec 16 Jun 17

+5.7% YoY

Consumer loans grew 5.7% YoY to RM157.7 billion led by

mortgage and auto finance growth

Note:

• Customer classification: HNW (IA>RM3m, TFA>RM4m); Affluent (IA between RM250k to RM3m, TFA between RM1m to <RM4m)

• TFA: Total Financial Assets (Deposits, Investments, Financing & Protection).

+3.1% YTD Ann.

HNW and Affluent customer TFA grew 7.9% YoY to

RM191.8 billion

Mass customer cross sell ratio improved to 3.46x

+4.0% YoY

+1.7% YTD Ann.

RM

billion

+1.0% YoY

RM

billion

+ 7.9 % YoY

RM

billion

RM

billion

+5.6% YTD Ann.

Note:

• Business Banking and SME figures are before migration of accounts.

42

Community Financial Services: Overview of Malaysia Deposits Portfolio

215.8 214.0 208.0

0.0

50.0

100.0

150.0

200.0

250.0

Jun 16 Dec 16 Jun 17

(5.6)% YTD Ann.

133.6 136.8 137.4

0.020.040.060.080.0

100.0120.0140.0160.0180.0200.0

Jun 16 Dec 16 Jun 17

+2.8% YoY

+0.9 % YTD Ann.

Our deposit strategy focused on growing CASA, which has

improved our NIM.

Consumer deposits show positive growth of +2.8% YoY

mainly driven by strong growth in CASA at 6.7% YoY.

82.2 77.2 70.6

0

20

40

60

80

100

120

Jun 16 Dec 16 Jun 17

(14.1)% YoY

(17.2)% YTD Ann.

RM

billion

Total CFS deposits contracted by -3.6% YoY, due to

reduction in costly fixed deposits

Business Banking + SME deposits contracted by -14.1%

YoY

Consumer deposits grew +2.8% YoY

(3.6)% YoY

RM

billion

RM

billion

Note:

• Business Banking and SME deposits figures are before migration of accounts.

43

Community Financial Services: Overview of CFS Malaysia Asset Quality

Total GIL ratio for consumer financing portfolio remain

stable at 0.5%, lower than industry average of 1.1%.

Combined GIL ratio for Business Banking + SME showed

a slight increase to 8.8%, due to impairments from

Business Banking.

736.3 739.0792.1

0.5 0.5 0.5

Jun 16 Dec 16 Jun 17

GIL (RM'm) GIL (%)

3,931.1 4,134.3 4,257.7

2.1 2.1 2.2

Jun 16 Dec 16 Jun 17

GIL (RM'm) GIL (%)

3,194.83,395.2 3,465.7

8.5 8.7 8.8

Jun 16 Dec 16 Jun 17

GIL (RM'm) GIL for SME + BB (%)

Total CFS GIL relatively stable at 2.2%

Slight uptick in Business Banking + SME GIL

Consumer GIL remained stable at 0.5%

44

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

45

11.6

23.2

36.6

11.7

27.9

39.2

11.2

28.0

38.8

Jun 17 Dec 16 Jun 16

RM billion

Note:

‘Term Loan’ now includes foreign currency denominated accounts, while ‘Trade

Finance and Others’, which previously included ‘Short Term Revolving Credit’, is now

combined with ‘Overdraft’.

Term Loan

Global Banking: Overview of Malaysia Corporate Banking Portfolio

Corporate Banking GIL ratio at 1.97% as at June 2017

Short Term

Revolving

Credit

Trade

Finance and

Others

+ 20.8% YoY

(3.3) % YoY

+6.0% YoY

25.3%25.5%

26.2%

25.1%24.7%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

2.53% 2.47%

1.85% 1.93% 1.97%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

Note: Market share of total trade products (On Balance Sheet items, Contingent

Liabilities and Others)

Trade Finance market share Total GB loans increased 9.3% YoY to RM78.0 billion

46

Group Securities Portfolio*:

38.2% Foreign Securities as at 1H FY2017

Group Securities Portfolio* grew 6.9% YoY

33% of GM PDS (Maybank Conventional Malaysia) rated

“AA” or above as at 1H FY2017

Global Banking: Overview of Group Global Markets Portfolio

1H FY20171H FY2016

21.1%

25.3%

28.3%

15.7%

9.6%

RM 139.0

billion

Government

Securities

- Domestic

Government

Securities

- Foreign

PDS/Corp

Bonds

- Domestic

PDS –

Foreign

Others

(NIDs, BA, etc)

25.5%

20.0%29.8%

18.2%

6.5%

RM 148.7

billion

Government

Securities

- Domestic

Government

Securities

- Foreign

PDS/Corp

Bonds

- Domestic

PDS –

Foreign

Others

(NIDs, BA, etc)

64.5 61.4 57.968.2 67.7

61.2 63.762.8

68.6 71.4

13.3 12.910.2

11.9 9.6

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

Govt. Securities PDS/Corp Bonds Others

+6.9%

RM

billion

139.0 138.0130.9

148.7

49.3%

19.1%

20.3%

1.9%

0.6% 8.8%

RM25.5

billion

A

<A

Commercial

Papers

Others

1H FY2016

AAA

AA

65.3%

16.1%

17.2%

0.3%

0.2%0.9%

RM24.8

billion

A

<ACommercial

Papers

Others

1H FY2017

AAA

AA

Note: * Group Securities Portfolio is inclusive of Financial assets designated upon initial

recognition (part of FVTPL)

148.7

Note: ‘Others’ category refers to Government Guaranteed bonds, partially Government

Guaranteed bonds and non rated bonds

47

Malaysia36%

Singapore26%

Thailand23%

Indonesia4%

Philippines2%

Hong Kong5%

Others4%

YTD June FY17 Brokerage Market Share by Country

1 Singapore & Vietnam’s YTD ranking data are not available.

Note: Maybank Kim Eng represents the combined business of Maybank IB and business segments under Maybank Kim Eng Holdings

Global Banking: Overview of Group Investment Banking Portfolio

Country RankMarket

Share

Trading Value

(USD’m)

Thailand 1 7.5% 22,260

Malaysia 2 10.9% 15,991

Philippines 9 4.2% 1,643

Indonesia >10 2.3% 2,947

Hong Kong Tier 2 0.7% 15,316

Singapore N/A1 3.9% 8,498

Vietnam N/A1 1.8% 876

1H FY2017 Fee-based Income for Malaysia

Brokerage Fees56.9%

Arranger Fees8.1%

Underwriting & Placement Fees3.1%

Advisory Fees11.8%

Agency/ Guarantee Fees

3.1%

Other Fee Income17.0%

1H FY2017 Total Income Breakdown by Country

RM674.7 mil

Total Income for Maybank Kim Eng

726.0

674.7

400.00

500.00

600.00

700.00

800.00

1H FY2016 1H FY2017

(7.1)%

RM

mil

48

Global Banking: Notable Deals for 1H FY2017

49

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

50

Maybank Singapore: P&L Summary

(SGD mil) 1H FY2017 1H FY2016* YoY

Net Fund Based income 334.27 270.23 +23.7%

Net Fee Based income 161.42 132.75 +21.6%

Net income 495.68 402.98 +23.0%

Overhead expenses (185.55) (179.33) +3.5%

Operating profit 310.13 223.65 +38.7%

Profit before taxation 150.63 147.83 +1.9%

Net fund-based income rose 23.7%, due to net interest margin improvement and loan growth of 4.9%.

Fee-based income increased 21.6%, led by higher wealth management, credit related and treasury income.

Overhead expenses rose 3.5% arising from higher revenue-related spend.

Buoyed by a combination of broad-based revenue growth and disciplined cost management, operating profit expanded

38.7%.

PBT rose by a smaller pace of 1.9% to reach SGD 150.63 million as additional loan loss allowances were set aside, mainly

for oil & gas related exposure.

Note:

* 1H FY2016 figures are the restated numbers to align the Islamic banking income re-classification adjustments made effective 2017.

51

5.2 6.1 6.8

15.0 14.9 14.1

5.2 6.4 6.6

19.8 17.1 14.8

Jun 16 Dec 16 Jun 17

Consumer -Time Deposits

Consumer CASA

Business TimeDeposits

Business CASA

4.6 5.7 5.85.8 6.8 7.6

34.8 32.0 28.8

Jun 16 Dec 16 Jun 17

Time Deposits

Demand Deposits

Savings

7.9 8.4 8.1

4.2 4.9 4.6

4.0 4.2 3.7

6.0 6.3 6.5

9.4 9.7 10.1

1.7 1.8 1.93.4 3.5 3.4

Jun 16 Dec 16 Jun 17

Other(Consumer)

Car Loan

Housing Loan

Others(Corporate)

Non-Bankfinancial Inst

GeneralCommerce

Building &Const

Maybank Singapore loans rose 4.9% YoY

Diversified Loan Portfolio

38.9

Consumer

40%

Corporate

60%

0.4%-1.9%

4.5%6.4%

4.9%

-3.6% -5.0%

0.5%

5.8%

6.4%

-10.0%

10.0%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

Maybank Singapore Growth Industry Growth

+4.9% YoY

Maybank Singapore: Overview of Loans and Deposits Portfolio

% YoY change

38.536.7

(6.7)% YoY

Consumer

51%

Corporate

49%

SG

D b

illion

Consumer deposits account for 51% of deposits

SG

D b

illion

CASA Ratio:

31.7%SG

D b

illion

Robust CASA growth of 28.4% YoY; CASA ratio also

improved to 31.7% in June 2017 from 23.0% a year ago

Lower consumer deposits at SGD21.4 billion from reduced FDs but

mitigated by CASA growth of 25.5% YoY

Higher business deposits at SGD20.9 billion as CASA grew 31.3% YoY

44.5 42.245.2

52

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

53

Maybank Indonesia: P&L Summary

(IDR bil) 1H FY2017 1H FY2016* YoY 2Q FY2017 1Q FY2017 QoQ

Net Fund Based income 3,836 3,585 7.0% 1,936 1,900 1.9%

Net Fee Based income 1,457 1,334 9.2% 890 567 57.0%

Net income 5,292 4,919 7.6% 2,826 2,467 14.6%

Overhead expenses (3,064) (2,770) 10.6% (1,621) (1,444) 12.3%

Personnel (1,234) (1,199) 2.9% (622) (612) 1.7%

General and Administrative (1,830) (1,571) 16.5% (999) (832) 20.1%

Operating profit 2,228 2,149 3.7% 1,205 1,023 17.8%

Provisions Expenses (836) (991) (15.7)% (478) (358) 33.5%

Non Operating (Expense) / Income (11) 4 (>100)% (3) (8) (59.4)%

Profit Before Tax and Non-Controlling Interest 1,381 1,162 18.8% 724 657 10.2%

Tax and Non-Controlling Interest (383) (304) 26.0% (216) (167) 29.1%

Profit After Tax and Non-Controlling Interest 998 858 16.3% 508 490 3.7%

EPS - Basic (IDR) 14.74 12.67 16.3% 7.50 7.23 3.7%

Note:

* FY2016 figures restated to reflect Indonesia long form report for consistency.

54

22,790

240

23,030 20,324

171

20,495

New Used Total

Jun 16 Jun 17

437

527

145175

Jun 16 Jun 17

Revenue Profit Before Tax

Financing – stand aloneIDR billion

(10.8)%

(28.8)%

(11.0)%

+20.4% +21.9%

Asset Quality Unit Financing (unit)

Revenue and Profit Before Tax IDR billion

Maybank Indonesia: Overview of Maybank Finance Operations

+20.4%

0.36%0.34%

0.32% 0.33% 0.32%

0.44%0.42%

0.39%0.41%

0.39%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

NPL Net NPL Gross

5,514

6,722

Jun 16 Jun 17

55

119

29

75

224

103

16

88

207

New Used Multipurpose Total

Jun 16 Jun 17

9371020

49 75

Jun 16 Jun 17

Revenue Profit Before Tax

Financing – stand aloneIDR billion

+8.8% +5.5%

Asset Quality Unit Financing (‘000 unit)

Revenue and Profit Before Tax IDR billion

+52.6%

1.18% 1.36% 1.25% 1.17% 1.24%

3.55%3.84%

3.32%2.96% 2.90%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

NPL Net NPL Gross

5,243 5,531

Jun 16 Jun 17

(13.8)% (46.7)%

(7.7)%

+17.1%

Maybank Indonesia: Overview of WOM Finance Operations

56

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

57

Maybank Islamic, 56.4%

Maybank Conventional,

Malaysia, 43.6%

Islamic Banking: Performance Overview

Group Islamic Banking Financial Performance

Maybank Islamic: Key Financial Ratios

Maybank Islamic: Total Gross Financing grew to RM154.5

billionRM million 1H FY2017 1H FY2016 YoY

Total Income 2,170.8 1,820.7 19.2%

Profit Before Tax 1,267.6 826.6 53.4%

Financing & Advances 165,004.6 144,466.2 14.2%

Deposits & Investment

Account:148,491.8 145,171.6 2.3%

Deposits from Customers 120,705.3 114,207.6 5.7%

Investment Account 27,786.6 30,964.0 (10.3)%

Key Financial Ratios 1H FY2017 1H FY2016

Net Profit Margin (YTD) 1.94% 1.85%

Total Capital Ratio (TCR) 17.77% 18.43%

Cost to Income Ratio (CIR) 36.32% 37.53%

Direct FDR1 96.4% 91.3%

Adjusted FDR with LTIF2 87.7% 84.5%

Maybank Islamic Contribution to Maybank Malaysia Loans

and Financing as at June 2017

Year Contribution

Jun 2016 53.1%

Sep 2016 53.2%

Dec 2016 54.5%

Mar 2017 54.9%

Jun 2017 56.4%

Note:

1) Direct Financing to Deposits Ratio (FDR) comprising gross financing against deposit

and Unrestricted Investment Account (exc. RPSIA assets and liabilities)

2) Adjusted FDR comprising adjusted financing against adjusted deposit (exc. RPSIA

assets and liabilities) including long term interbank funding (LTIF)

Cashline for retail has been reclassified from others to mortgage and term respectively

Group Islamic Banking’s performance has improved YoY, deriving from key markets in

Malaysia, Indonesia and Singapore

CFS:9% GB:20%

14%

7%

12%

24%

5%

16%

58

Maybank Islamic Market Share (Malaysia) as of June 2017

Maybank Islamic ranks No.1 by Asset Market Share

in Malaysia

Source: BNM monthly statistical bulletin and latest respective Bank’s Financial

Statements

MalaysiaAsset Market Share

Mar 17Rank

Maybank Islamic 30% 1

CIMB Islamic 12% 2

Public Islamic 9% 3

Source: Bloomberg

Sukuk League Table Ranking June 2017

Key Products Jun 17 Jun 16

Automobile Financing 44.7% 42.9%

Home 28.1% 28.0%

Term Financing 29.6% 29.9%

Source for industry numbers: BNM Monthly Statistical Bulletin

Islamic Banking: Market Share

Market Share by Product (Malaysia) as of June 2017

Source for industry numbers: BNM Monthly Statistical Bulletin

33.8% 33.9%34.4%

33.9% 33.9%

31.3%

30.3% 30.3%29.7% 29.5%

Jun 16 Sep 16 Dec 16 Mar 17 Jun 17

Financing Deposits & Investment Accounts

Market Share

(%)

Amount

(USD million)Issues

#5 Maybank 6.54% 2,151 49

Market Share

(%)

Amount

(USD million)Issues

#2 Maybank 22.66% 1,883 38

MYR Sukuk League Table

Ranking

Global Sukuk League Table

Ranking

59

8.0%

10.6%

12.1%

0.0% 5.0% 10.0% 15.0%

HL-MSIG Ins. & Tak.

Allianz Insurance

Etiqa Ins. & Tak.

7.6%

14.2%

14.8%

22.1%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Etiqa Ins. & Tak.

GE Ins. & Tak.

Prudential Ins. & Tak.

AIA Ins. & Tak.

304.5

472.4

1H FY2016 1H FY2017

Insurance and Takaful: Performance Overview

Total Assets (RM billion)

Gross Premium

Profit Before Tax (RM million)

Life / Family (New Business) Market Share

No. 4 in Life/Family

(New Business)

No. 1 in General

Insurance and

Takaful

General Insurance and Takaful Market Share

55.1% YoY

0 500 1,000 1,500 2,000 2,500 3,000 3,500

Total Life/Family & General

Total General

Misc

Personal Accident

MAT

Motor

Fire

Total Life/Family

Group Premium

Credit Premium

Regular Premium

Single Premium

RM Million

1H FY2017

1H FY2016

>100%

14.5%

23.5%

0.2%

21.5%

7.0%

8.3%

(1.7)%

(25.7)%

(15.6)%

(9.3)%

5.1%

32.6 31.9 33.1

Jun 16 Dec 16 Jun 17

1.5% YoY

Note :

PBT includes estimated transfer of RM48.8 million from Family Fund in 1H FY2017

Note: Market Share is for period Apr’16 – Mar’17 (Source: LIAM / ISM Statistics)

60

61,136.8 64,187.0

72,949.6 75,473.0

Dec 16 Jun 17

Gross Loans

CustomersDeposits

2,623.2 2,837.7

377.2

765.5

1H FY2016 1H FY2017

Revenue

PBT

Maybank Philippines: Performance Overview

Revenue increased by 8.2% YoY, led by higher net interest

income (NII).

Increase in NII contributed by higher interest income from

term loans.

PBT increased by 102.9% YoY driven by higher revenue,

coupled with lower overhead expenses and provisioning.

Gross loans rose by 10.0% YTD ann. driven by growth in term

loans.

Customer deposits rose by 6.9% YTD ann. supported by growth

in term deposit and saving account.

Gross impaired loans ratio improved to 2.32% due to lower

NPL.

+ 8.2% YoY

+>100% YoY

Revenue and PBT

Gross Loans and Deposits

Key Highlights

PESO

Mil

PESO

Mil

+10.0%*

+6.9%*

Key Ratios 1H FY2017 1H FY2016

Return on assets 1.55% 0.83%

Return on equity 13.56% 3.58%

Cost-to-income ratio 71.32% 72.33%

Loans to Deposit ratio 85.05% 92.44%

Gross Impaired Loans Ratio 2.32% 4.60%

No. of branches 74 80

Note: *Annualised growth

61

Table of Contents

Executive Summary 2

Results Overview 5

MFRS 9 Update 20

Liquidity Update 24

Prospects & Outlook 27

Appendix:

1. Financial Performance 30

2. Community Financial Services 40

3. Global Banking 45

4. Maybank Singapore 50

5. Maybank Indonesia 53

6. Other segments 57

7. Affiliates 62

Financial Results: 2Q FY2017 and 1H FY2017 ended 30 June 2017

62

943.7

1,252.0

103.5

265.8

1H FY2016 1H FY2017

Revenue

PBT

An Binh Bank: Performance Overview

Revenue increased by 32.7% YoY, mainly due to higher net

interest income and fee income.

PBT increased by 156.8% or VND162.3b YoY, mainly

contributed by higher revenue.

Gross loans expanded by 8.5.% YTD ann. mainly due to higher

retail lending.

Customer deposits increased by 13.8% YTD ann. mainly due to

growth in saving account.

Gross NPL ratio increased by 1.1%, mainly contributed by

higher NPL.

Key Ratios 1H FY2017 1H FY2016

Return on assets 0.70% 0.30%

Return on equity 9.10% 3.60%

Cost-to-income ratio 52.34% 54.86%

Loans to Deposit ratio 92.56% 91.58%

Gross NPL Ratio 2.60% 1.50%

VN

D B

ilVN

D B

il

+ 32.7 % YoY

+>100% YoY

49,555.2

51,665.0 52,227.5

55,818.5

Dec 16 Jun 17

Gross Loans

CustomersDeposits

+ 8.5 %*

+ 13.8% *

Gross Loans and Deposits

Revenue and PBTKey Highlights

Note: *Annualised growth

63

MCB Bank: Performance Overview

30.3 30.4

19.5 17.7

1H FY2016 1H FY2017

Revenue

PBT

+ 0.2 % YoY

(9.5)% YoY

384.0 432.5

776.0

891.2

Dec 16 Jun 17

Gross Loans

CustomersDeposits

+ 29.7 %*

+ 25.3%*

PKR B

ilPKR B

il

Key Ratios 1H FY2017 1H FY2016

Return on assets 2.31% 2.06%

Return on equity 22.82% 18.83%

Cost-to-income ratio 47.39% 38.88%

Loans to Deposit ratio 48.53% 50.35%

Gross NPL Ratio 5.20% 5.46%

Gross Loans and Deposits

Revenue increased marginally by 0.2% YoY, owing to better

Non-Interest Income (NOII).

Higher NOII was mainly attributed from gain on sale of

securities.

PBT decreased by 9.5% YoY, mainly attributed to higher

provisioning.

Gross loans increased by 25.3% YTD ann. arising from growth

in domestic loans and Islamic financing.

Customer deposits grew by 29.7% YTD ann. mainly led by

higher CASA growth.

Revenue and PBTKey Highlights

Note: *Annualised growth

64

Dato’ Amirul Feisal Wan Zahir

Group Chief Financial Officer

Contact: (6)03-2074 7703

Email: [email protected]

MALAYAN BANKING BERHAD

14th Floor, Menara Maybank

100, Jalan Tun Perak

50050 Kuala Lumpur, Malaysia

Tel : (6)03-2070 8833

www.maybank.com

Jeeva Arulampalam

Head, Group Investor Relations

Contact: (6)03-2074 8017

Email: [email protected]

Disclaimer. This presentation has been prepared by Malayan Banking Berhad (the “Company”) for information purposes only and does not purport to contain all the

information that may be required to evaluate the Company or its financial position. No representation or warranty, express or implied, is given by or on behalf of the

Company as to the accuracy or completeness of the information or opinions contained in this presentation.

The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of

it form the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever.

The Company does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in

connection therewith.

Investor Relations Contact

Humanising Financial Services