investor presentation - rostelecom.ru investor... · investor presentation . 0 170 231 240 78 35...

TRANSCRIPT

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

Investor Presentation

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Today’s Presenters

2

Sergey

Kalugin

President, CEO

Ekaterina

Ustinova

Head of Investor Relations

Kai-Uwe

Mehlhorn

Senior Vice-President,

CFO

Maria

Florentieva

Vice-President,

Strategy and Investor

Relations

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

51.1%

20.1%

28.8%

Rostelecom at a Glance

3

Strong Subscriber Base &

Market Share3

Financial Results 1H14

Broadband

10.9 mln

41%

Shareholder Structure 1

Other Shareholders

Treasury shares2

Strengthened Positions

in Mobile Business

Rostelecom holds 45% in T2-RTK (Tele2

Russia), a national mobile player

Combined mobile market share3 (by subs)

156.4*

RUB bln

-2% YoY

REVENUES

+3% YoY

fixed

24.8

RUB bln

15.9%

to Sales

CAPEX

-24% YoY

54.1*

RUB bln

34.6%

margin

OIBDA

35.4%

margin fixed

176.2

RUB bln

1.6x

to OIBDA

NET DEBT

RUB 41.1 bln

improvement

State Property

Agency 47%

4.1%

State stake

B2C 50%

B2B 23%

B2G 14%

B2O 13%

Revenue Mix by Segments 1H14

MTS 32%

Megafon 28%

Vimpelcom 23%

T2-RTK 15%

Other 2%

* Including effect of RUB 11.1 bln on revenue and effect of RUB 2.8 bln on OIBDA from

discontinued operations.

Pay-TV

7.7 mln

22%

Fixed Voice

25.6 mln

69%

1 As of October 1, 2014

2 Including shares owned by Mobitel

3 As of the end of 2Q2014

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Content

4

Investment Highlights

1

Rostelecom Strategic Priorities

2

Financial Results & Outlook

3

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

1. Investment Highlights

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Investment Highlights

6

2

3

4

5

6

1

Exposure to

attractive markets

with strong growth

profiles

Leading positions

in most Russian

telecom segments

Unique and largest

fixed-line network

in Russia

Significant upside

potential from

operational

efficiencies

Robust financial

profile

Management team

with significant TMT

experience

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

2.3

4.9 7.2

9.5 11.8

14.1

2013 2014F 2015F 2016F 2017F 2018F

Exposure to Attractive Markets with Strong

Growth Profiles

7

1

Pay TV and IPTV penetration in Russia3

Fixed Broadband Penetration1 (2013)

VoD Market Volume4 (RUB bln) Mobile Data Market Volume4 (RUB bln)

ARPU CAGR 2013-2017 = 3%

5.5 6.6 8.0

9.5 10.8 12.0 13.1 14.0

1.1 2.1

3.4

4.4

5.2

6.1 6.9

7.5

0.4

0.7

0.9

1.1

1.4

1.6

1.9

6.7

9.1

12.1

14.8

17.2

19.5

21.6

23.4

2012 2013 2014F 2015F 2016F 2017F 2018F 2019F

2Play (BB & Voice) 3Play (BB, TV & Voice) 4Play (BB, TV, Voice & Mobile)

Bundle subscribers in Russia2 (mln)

102 129

157 183

203 222

237

2012 2013 2014F 2015F 2016F 2017F 2018F

Source:

1 Company estimates, iKS-Consulting, Pordata.pt, ITU

2 Ovum

3 J’Son & Partners Consulting

4 iKS-Consulting

40% 44% 47% 49% 50% 50% 53%

60% 61% 63% 64% 65% 66% 67% 69% 71%

82% 83% 89% 89%

97%

5%

7%

9%

11% 12%

13% 14%

58%

64%

70%

75% 78%

81% 83%

2012 2013 2014F 2015F 2016F 2017F 2018F

IPTV Pay TV

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

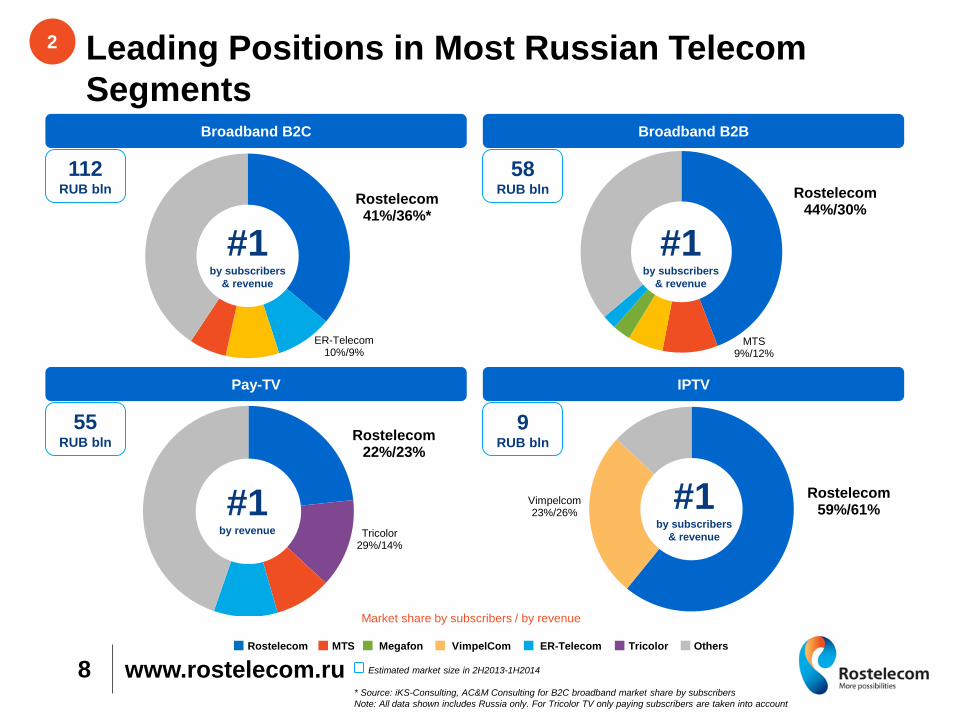

Rostelecom 41%/36%*

ER-Telecom 10%/9%

Rostelecom 22%/23%

Tricolor 29%/14%

Leading Positions in Most Russian Telecom

Segments

8

2

IPTV

Broadband B2C

Pay-TV

Broadband B2B

Rostelecom 44%/30%

MTS 9%/12%

#1 by subscribers

& revenue

#1 by revenue

Market share by subscribers / by revenue

Rostelecom 59%/61%

Vimpelcom 23%/26%

Estimated market size in 2H2013-1H2014

* Source: iKS-Consulting, AC&M Consulting for B2C broadband market share by subscribers

Note: All data shown includes Russia only. For Tricolor TV only paying subscribers are taken into account

VimpelCom Others Tricolor Megafon ER-Telecom MTS Rostelecom

112 RUB bln

55 RUB bln

58 RUB bln

9 RUB bln

#1 by subscribers

& revenue

#1 by subscribers

& revenue

www.rostelecom.ru

Largest Fixed-Line Network in Russia to Support

Growth

9

Growing Demand for Speed and Capacity

IP Traffic Growth2

3x

2013

2018

Rostelecom is well positioned to support

this demand….

500,000 km of backbone

Total footprint ~ 55 mln

Total homes passed ~ 34 mln

Total households upgraded to fiber by the

end of 2016 ~ 33 mln

… and monetize its network competitive

advantages

• Upselling B2C and B2B customers to

fiber for higher speeds and video products

• Reliable and secure nation-wide

solutions for B2B and B2G clients

• Implementation of Bridging Digital

Divide program

Total capacity required

in 20151

> 100 Mb/s

3

1 Average capacity required in metropolis area. Source: Company estimates

2 Source: Cisco

Fixed Internet Traffic,

PB per month2

12 18

22 28

35 40

Average BB Speed

in CEE, Mbps2

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Significant Upside Potential from Operational

Efficiencies

10

COST EFFECT

Network Modernization

Network

Maintenance

Cost

REVENUE EFFECT

High End Tariffs & Value

Added Services

Personnel Efficiency

Improvement

Optimization of Retail Chain

& Real Estate Portfolio

Customer Care

Improvement

Procurement Optimization

Excessive

Functions

Eliminations Productivity

Property

Maintenance

Cost Income from

Disposals

Customer

Service Cost Customer

Satisfaction

Prices Vendor

compe-

tition

Stable

4

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

32.7

24.8

1H13

1H14

28.8

21.2

1H13

1H14

9.0%

10.8% 2Q14

2Q13

7.2

8.2 2Q14

2Q13

4.1

4.9 2013

2012

2.4

3.1 2013

2012

71.0

72.6 2Q14

2Q13

79.9

76.0 2Q14

2Q13

Robust Financial Profile

1 Consolidated P&L data for 2013 and 1Q14 include the entire mobile business of

Rostelecom, while the data for 2Q14 exclude mobile subsidiaries transferred to JV with

Tele2 Russia.

2 OIBDA = Operating Profit excl. Long-term motivation program accrual expenses plus

Depreciation & Amortization 11

Revenue

Revenue

fixed-line

Capex

Ordinary

share

Preferred

share

27.5

26.2 2Q14

2Q13

29.1

27.6 2Q14

2Q13 OIBDA

OIBDA

fixed-line Cap

ex

(R

UB

bln

)

Reve

nu

e 1 (

RU

B b

ln)

Capex

fixed-line OIB

DA

2 (

RU

B b

ln)

Div

ide

nd

s (

RU

B)

OIB

DA

ma

rgin

(%

)

Net

Inc

om

e &

ma

rgin

38.7%

36.0% 2Q14

2Q13

36.5%

36.3% 2Q14

2Q13 OIBDA margin

OIBDA margin

fixed-line

-5% YoY due to demerger of

mobile subsidiaries

+2% YoY

-5% YoY due to demerger of

mobile subsidiaries

-5% YoY

stable YoY

-2.7pp YoY

Net Income

Net Income

margin

+28% YoY

+18% YoY

-26% YoY

+14% YoY

+1.8pp YoY

-24% YoY

5

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Management Team with Significant TMT

Experience

12

Sergey

Kalugin • President, CEO

• Joined the Company in March,

2013

• 12 years experience in Telecom

& Media

• Previously CEO of National

Telecommunications, largest

cable TV & IS provider in Russia

Maria

Florentieva

• Vice President, Strategy &

Investor Relations

• Joined the Company in May,

2013

• 7 years experience in Telecom

& Media

• Previously Deputy CEO of

National Telecommunications

Kai-Uwe

Mehlhorn • Senior Vice President, CFO

• Joined the Company in May, 2013

• Over 21 years of TMT

experience, 11 years at CFO

position

• Previously CFO of Megafon and

Tele2 Russia.

Larisa

Tkachuk

• Senior Vice President, Sales &

Marketing

• Joined the Company in April,

2013

• Over 10 years of Telecom &

Media experience

• Previously Sales & Marketing

Director at Megafon

Mikhail

Irzhevsky

• Vice President, Legal Affairs

& Corporate Governance

• Joined the Company in

October, 2013

• Over 20 years of consulting in

international law firms

• Previously Partner at

Freshfields Bruckhaus Deringer

LLP

Alexander

Maslov

• Vice President, GR

• Joined the Company in June,

2013

• Over 7 years experience in IT,

Telecom & Media and over 20

years of Government experience

• Previously Deputy Minister of

Communications and Mass

Media of Russia

Dmitriy

Sadkov

• Vice President, IT

• Joined the Company in June,

2013

• Over 13 years of experience in

IT

• Previously Director of

Management Consulting

Department at IBS and at

McKinsey & Company

Alexander

Tseitlin

• Senior Vice President,

Network

Joined the Company in May,

2013

• Over 30 years of Telecom

experience

• Previously CEO at Mostelecom,

Moscow incumbent cable TV

company

6

Galina

Rysakova • Senior Vice President, HR

• Joined the Company in 2001

• Over 13 years experience in

Organizational Development

and Human Resources

• Previously worked as HR

Manager at Sheremetyevo

International Airport

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

2. Rostelecom Strategic

Priorities

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Rostelecom Strategic Priorities

14

Revenue CAPEX /

Revenue

OIBDA

margin

Technological

leadership in IP

networks

1

Differentiated

offerings

2 Best-in-class

customer

service

3

Organisational &

corporate culture

transformation

4

Efficiency

improvement

5

SH

AR

EH

OL

DE

R R

ET

UR

N

Proven track-

record of cost

control

Effective

utilization of 3G /

4G licenses &

network roll-out

Data growth

opportunity

45% STAKE in T2-RTK

Dividends Fundamental

value

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Technological Leadership in IP Networks

15

Projects Multiservice Network Capacity

IP/MPLS, Tb/s

Households Passed by Fiber, mln

Submarine cable Sakhalin - Magadan – Kamchatka

Modernization of multiservice network

Digital divide bridging

Сеть агрегации РФ

AS 1

2389

(КЦ

)AS

РФ

Единая сетьAS 12389

CR CR

RGR RGR

CG-NAT

BRAS

DR DR

BPE

• Capex and opex decrease as a result of network hops

optimization

• Simplification and speeding up network development, including

the new services launch

• Increasing competition between vendors

Core (CR) Service level

(BPE, BRAS, CG-NAT)

2014 2014-2016

Backbone

(RGR)

Aggregation

Level (DR)

Test completed Test launched

Project’s stages

Project’s target

Fiber

Broadband

10 Мb/s • Construction contract is signed with “INTER RAO UES Power

efficiency centre” to connect 13.6k rural settlements to fiber optic

• OJSC “Hyprosvyaz” was appointed as a major Project Office

• Testing of wireless broadband equipment is completed

• Construction is in process according to schedule

• Maximum capacity: up to 8Тb

• Project cost: ≈ RUB 3 bln

• Status: contracts with vendors are signed

• Construction start: Q3 2014

• Operations start: June 2016

3.5 4.5

3.5

7.4

9.7

2012 2013 7M2014Load Capacity

+111% +31%

2.8

5.6

2.6

7.9

2012 2013 7M2014 2014F

+100% YoY

+41% YoY

1

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Differentiated Offerings – Subscriber Base

16

Subscribers (mln)

Subscribers (mln) Video-on-Demand

transactions (mln)

Technology Breakdown (%)

ARPU

Fiber Subscribers (mln)

IPTV Subscribers (mln)

7.1 7.2 7.3 7.5 7.6 7.7

129 131 132 140

143 147

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

+7.1% YoY

3.3 3.5

3.8 4.0

4.3 4.5

422 418 402

418

441 421

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

+27.3% YoY

0.9 1.0

1.2

1.5

1.7 1.6

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

+65.9% YoY Seasonality

effect

PA

Y T

V

BR

OA

DB

AN

D

2a

10.0 10.1

10.3 10.6

10.8 10.9

460 450

437 448

459 446

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

+7.4% YoY

1.7 1.9

2.0 2.2

2.3 2.4

180 182 182 201 210 206

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

+28.9% YoY

33% 35% 36% 38% 40% 41%

67% 65% 64% 62% 60% 59%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

FTTx xDSL

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Differentiated Offerings – Triple Play

17

2b

“Three-in-one”

Launch of a national triple play promotion

campaign “Three-in-one”: savings on monthly

charges for customers who simultaneously

subscribe to the Home Internet, IPTV and Home

Telephone

Home Internet ~ 450

RUB/month VS.

Home Telephone ~ 180

RUB/month

IPTV ~ 200

RUB/month 3-in-1

from 499 RUB/month*

for new clients or clients with 1 service

(for promo-period only – 4 months)

Extra package of TV channels

“Karaoke”

Multiroom

3Play service and the promotional “Three-in-one” campaign aim is retention of fixed voice subscribers and increase in

subscriber bases for broadband and pay TV.

from 685 RUB/month*

for customers using 2 services

* Minimal tariff. Prices and specifications of the services may differ across the regions.

Promotional period is 4 months.

or

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Transformation into Digital Services Provider

18

B2C

B2B

&

B2G

• Triple Play

• Enhanced self-services

features

• SaaS (SAP, Microsoft)

• Vertical Solutions for

government sectors

• OTT Box with best in the

market offering of linear

& VOD programming

• Online video-portal with

free access major TV

channels shows and

series catch up

• Integrated online portal

with e-commerce and

financial services

• Data Centers with Tier 3

standards

• National CDN solution

• Private clouds enabled

by best in class

connectivity standards,

VPNs, security protocols,

etc.

TODAY NEXT STEPS FURTHER ON….

New product ecosystem

• Focus on development of

virtualized products

within core capabilities

area and partnering for

the rest through

collaboration alliances

and open platform

2c

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Best-in-Class Customer Service First Results

19

3a

Based on the TOP 35 “Quick wins” project analysis

September 2013 June 2014 KPIs

2015-2016

Repeated calls 1 19% 11% 5%

Calls resolved within target

time 2 14% 54,3% 90% (2+3 lines)

3rd line of

technical

support

Repeated calls 1 15-25% 12-20% 10%

Customer issues average

handle time 2 50-20 h 13 h 2,5 h 2nd line of

technical

support Tickets resolved remotely 3 25-40% 52% 70%

Plan Achieved so far

The first results of customer calls and repeated calls reduction

(3rd line of technical support)

28 738

15 714 12 507 11 896 11 582

11,3%

June 2014

103 707

May 2014

10,9% 11,4%

13,8%

104 296

April 2014

110 199

February 2014

113 978

October 2013

18,7%

153 682 Repeated calls

Total calls

10%

70% (2+3 lines)

14%

6 h

60%

KPIs

2014 KPIs for

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

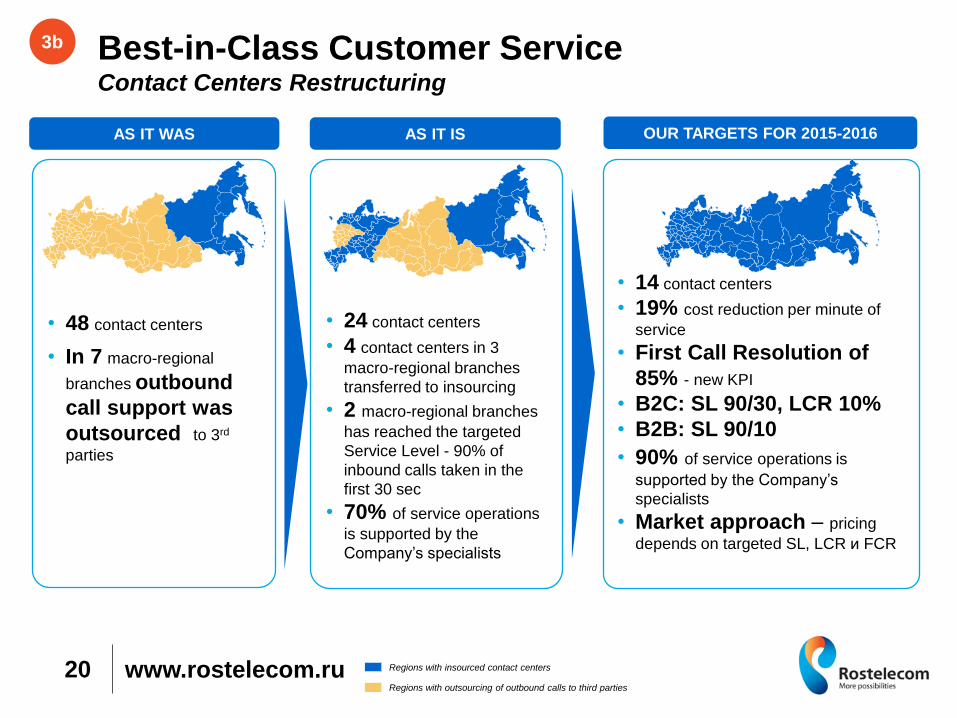

• 24 contact centers

• 4 contact centers in 3

macro-regional branches

transferred to insourcing

• 2 macro-regional branches

has reached the targeted

Service Level - 90% of

inbound calls taken in the

first 30 sec

• 70% of service operations

is supported by the

Company‟s specialists

• 14 contact centers

• 19% cost reduction per minute of

service

• First Call Resolution of

85% - new KPI

• B2C: SL 90/30, LCR 10%

• B2B: SL 90/10

• 90% of service operations is

supported by the Company‟s

specialists

• Market approach – pricing

depends on targeted SL, LCR и FCR

• 48 contact centers

• In 7 macro-regional

branches outbound

call support was

outsourced to 3rd

parties

Best-in-Class Customer Service Contact Centers Restructuring

20

3b

AS IT WAS AS IT IS OUR TARGETS FOR 2015-2016

Regions with outsourcing of outbound calls to third parties

Regions with insourced contact centers

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Organizational & Corporate Culture

Transformation

21

4

Key Initiatives

“Ideal Branch” Model

Corporate Culture

& Sustainability

Centralization of support functions

(IT, backoffice, etc.)

Creation of competence centers at macro branches level

Outsourcing of certain business functions and related optimization of organizational structure

Development of „ideal‟ operational model with solid scalability potential on the base of some pre-selected local branch

Replication of developed operational model at regional branches level

„Ideal branch‟ project is expected to be instrumental for the whole organizational transformation and should also set the ground for CRM and other IT systems improvements

Management efficiency: lead by example, mentorship, commitment, encouragement and staff training

Customer-oriented approach, continuous improvement

Motivate to action and evaluate on real achievements

Simplicity and delegation: facilitate accomplishment of the objectives and empowerment

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru 22

5

Personnel productivity

Total savings breakdown Project result: +1-2% OIBDA margin increase by 2017

26%

22%

7% 6%

5%

4%

2% 2%

26%

Points of sale

Personnel efficiency

Network modernization

Consolidation of controlcenters

Contact-centers

Rent of channels

Real estate in use

Bills printing and delivery

Other

RUB

15 bln of savings

Efficiency Improvement

2.9

4.24.6

2.9

1.8

Data for foreign operators include mobile business data (Source: companies’ data, World Bank)

Revenue per employee, RUB mln/person

CAGR

+10%

Orange DT/T-Mobile AT&T RTK

2018

RTK

2013

>2.5

Inflation

Str

uctu

ral

Busin

ess

Changes

OIB

DA

2017

OIB

DA

2013

Com

petition

Negative Effect Positive Effect

Pro

cure

ment

OE

I

Pro

gra

m

Pers

onnel

Optim

ization

Procurement savings, RUB bln

3.5

16.1

8.5

>12.0

2012 2013 1H2014 2014F

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

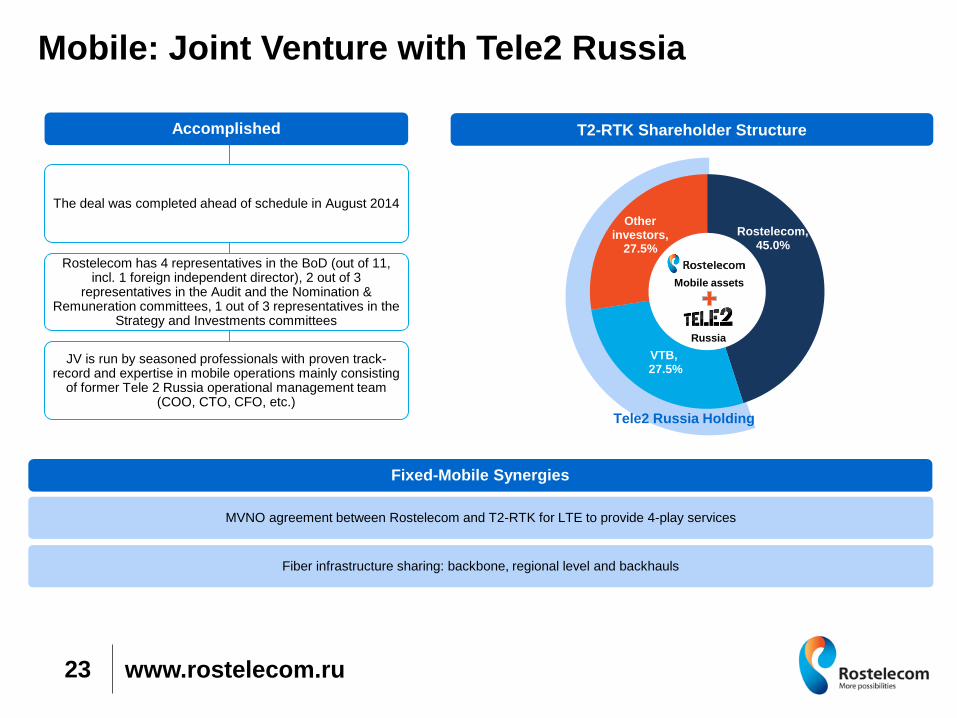

Rostelecom, 45.0%

VTB, 27.5%

Other investors,

27.5%

Mobile: Joint Venture with Tele2 Russia

23

Russia

Mobile assets

T2-RTK Shareholder Structure

The deal was completed ahead of schedule in August 2014

Rostelecom has 4 representatives in the BoD (out of 11, incl. 1 foreign independent director), 2 out of 3

representatives in the Audit and the Nomination & Remuneration committees, 1 out of 3 representatives in the

Strategy and Investments committees

JV is run by seasoned professionals with proven track-record and expertise in mobile operations mainly consisting

of former Tele 2 Russia operational management team (COO, CTO, CFO, etc.)

Accomplished

Fixed-Mobile Synergies

MVNO agreement between Rostelecom and T2-RTK for LTE to provide 4-play services

Fiber infrastructure sharing: backbone, regional level and backhauls

Tele2 Russia Holding

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

3. Financial Results & Outlook

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

= 𝐑𝐔𝐁 𝟏𝟖𝟓. 𝟓 𝐛𝐥𝐧

CAPEX (RUB bln)

and CAPEX / Revenue (%)

OIBDA2 (RUB bln)

and OIBDA Margin (%) Revenue 1 (RUB bln)

Key Consolidated Financial Results

25

79.6

73.6

81.0 85.3

80.4 76.0

71.0 72.6

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

Total Fixed-line

+2.3% YoY Effect from

mobile

subsidiaries

79.9

29.4 29.1 29.6 25.2 26.5 27.6

37.0% 36.5% 36.5%

29.5% 33.0%

36.3%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

1 Consolidated P&L data for 2013 and 1Q14 include the entire mobile business of

Rostelecom, while the data for 2Q14 exclude mobile subsidiaries transferred to JV with

Tele2 Russia.

2 OIBDA = Operating Profit excl. Long-term motivation program accrual expenses +

Depreciation & Amortization

3 Free Cash Flow = net cash provided by operating activities less CAPEX

Net Debt/OIBDA

203.2 180.7

207.2 217.3 184.0 176.2

1.8

1.6

1.8 1.9 1.7 1.6

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

Net Debt Analysis (RUB bln) FCF3 Analysis (RUB bln) Total Debt Structure (RUB bln)

20.5

37.2 43.6 45.5

37.5

2H2014 2018 and

onwards 2016 2017 2015

by Maturity

by Rate by Currency

25.1

7.6

14.4

21.4

10.0 14.8

31.6%

9.5%

17.8%

25.1%

12.4%

19.5%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14

S&P / Fitch ratings BB+ stable / BBB- stable

Fixed rate

Floating rate

1%

99%

RUB Other

1%

99% 1H14

-3.1

3.0

17.2

10.7

2011 2012 2013 1H14

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

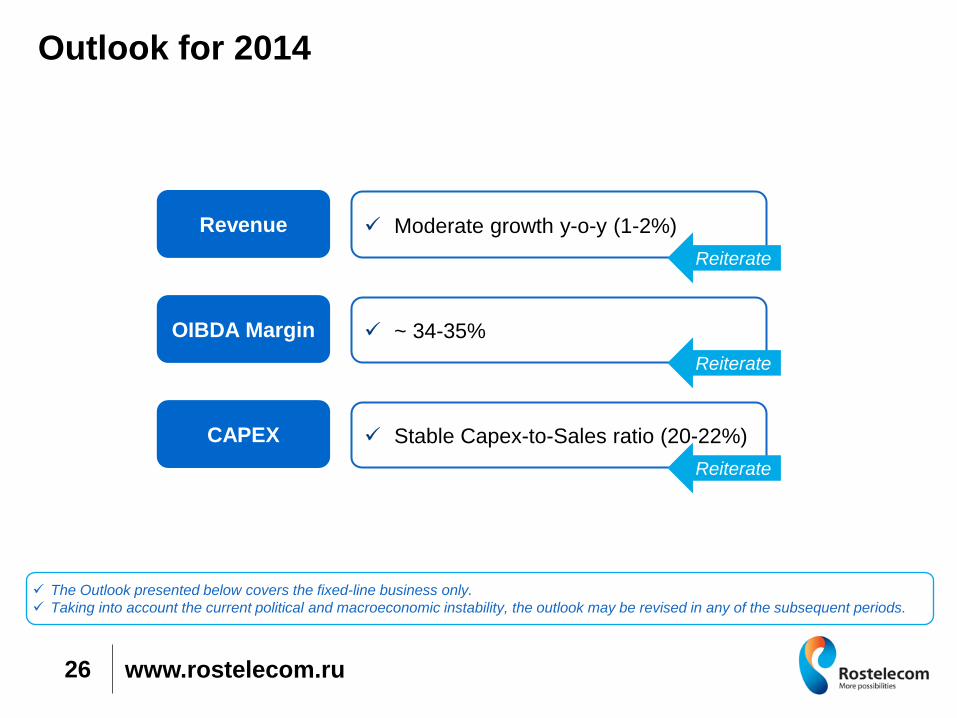

Outlook for 2014

26

The Outlook presented below covers the fixed-line business only.

Taking into account the current political and macroeconomic instability, the outlook may be revised in any of the subsequent periods.

Revenue Moderate growth y-o-y (1-2%)

OIBDA Margin ~ 34-35%

CAPEX Stable Capex-to-Sales ratio (20-22%)

Reiterate

Reiterate

Reiterate

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

Appendices

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

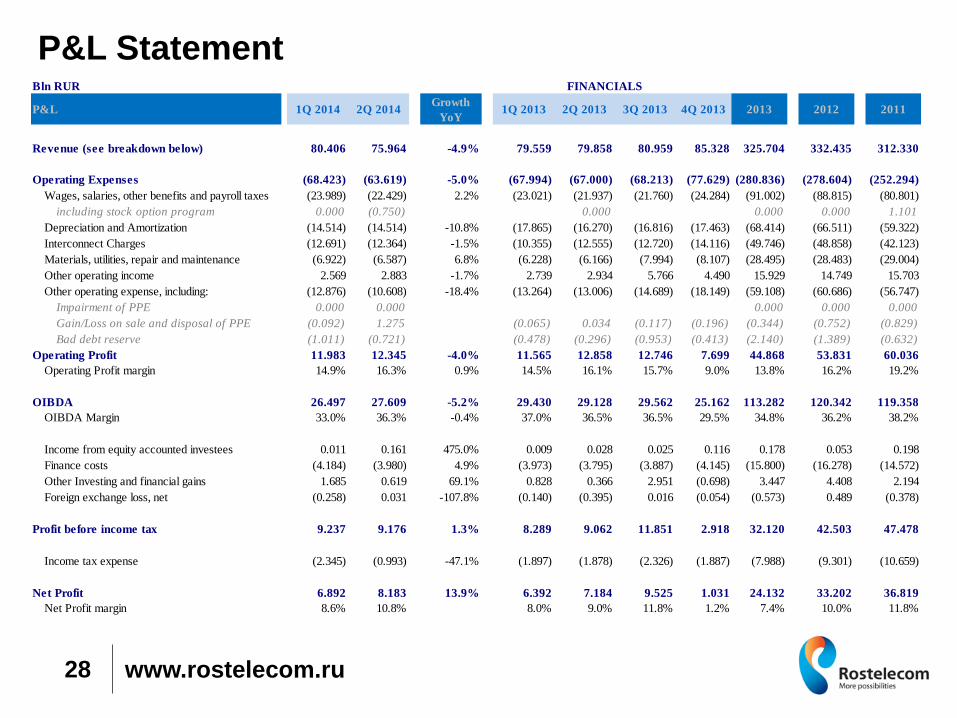

P&L Statement

28

Bln RUR

P&L 1Q 2014 2Q 2014Growth

YoY1Q 2013 2Q 2013 3Q 2013 4Q 2013 2013 2012 2011

Revenue (see breakdown below) 80.406 75.964 -4.9% 79.559 79.858 80.959 85.328 325.704 332.435 312.330

Operating Expenses (68.423) (63.619) -5.0% (67.994) (67.000) (68.213) (77.629) (280.836) (278.604) (252.294)

Wages, salaries, other benefits and payroll taxes (23.989) (22.429) 2.2% (23.021) (21.937) (21.760) (24.284) (91.002) (88.815) (80.801)

including stock option program 0.000 (0.750) 0.000 0.000 0.000 1.101

Depreciation and Amortization (14.514) (14.514) -10.8% (17.865) (16.270) (16.816) (17.463) (68.414) (66.511) (59.322)

Interconnect Charges (12.691) (12.364) -1.5% (10.355) (12.555) (12.720) (14.116) (49.746) (48.858) (42.123)

Materials, utilities, repair and maintenance (6.922) (6.587) 6.8% (6.228) (6.166) (7.994) (8.107) (28.495) (28.483) (29.004)

Other operating income 2.569 2.883 -1.7% 2.739 2.934 5.766 4.490 15.929 14.749 15.703

Other operating expense, including: (12.876) (10.608) -18.4% (13.264) (13.006) (14.689) (18.149) (59.108) (60.686) (56.747)

Impairment of PPE 0.000 0.000 0.000 0.000 0.000

Gain/Loss on sale and disposal of PPE (0.092) 1.275 3650.0% (0.065) 0.034 (0.117) (0.196) (0.344) (0.752) (0.829)

Bad debt reserve (1.011) (0.721) 143.6% (0.478) (0.296) (0.953) (0.413) (2.140) (1.389) (0.632)

Operating Profit 11.983 12.345 -4.0% 11.565 12.858 12.746 7.699 44.868 53.831 60.036

Operating Profit margin 14.9% 16.3% 0.9% 14.5% 16.1% 15.7% 9.0% 13.8% 16.2% 19.2%

OIBDA 26.497 27.609 -5.2% 29.430 29.128 29.562 25.162 113.282 120.342 119.358

OIBDA Margin 33.0% 36.3% -0.4% 37.0% 36.5% 36.5% 29.5% 34.8% 36.2% 38.2%

Income from equity accounted investees 0.011 0.161 475.0% 0.009 0.028 0.025 0.116 0.178 0.053 0.198

Finance costs (4.184) (3.980) 4.9% (3.973) (3.795) (3.887) (4.145) (15.800) (16.278) (14.572)

Other Investing and financial gains 1.685 0.619 69.1% 0.828 0.366 2.951 (0.698) 3.447 4.408 2.194

Foreign exchange loss, net (0.258) 0.031 -107.8% (0.140) (0.395) 0.016 (0.054) (0.573) 0.489 (0.378)

Profit before income tax 9.237 9.176 1.3% 8.289 9.062 11.851 2.918 32.120 42.503 47.478

Income tax expense (2.345) (0.993) -47.1% (1.897) (1.878) (2.326) (1.887) (7.988) (9.301) (10.659)

Net Profit 6.892 8.183 13.9% 6.392 7.184 9.525 1.031 24.132 33.202 36.819

Net Profit margin 8.6% 10.8% 8.0% 9.0% 11.8% 1.2% 7.4% 10.0% 11.8%

FINANCIALS

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Revenue Structure

29

Bln RUR

Revenue / Breakdown 1Q 2014 2Q 2014Growth

YoY1Q 2013 2Q 2013 3Q 2013 4Q 2013 2013 2012 2011

By services:

Local Telephone services 20.992 20.084 -10.4% 21.730 22.403 21.734 21.568 87.436 89.504 91.526

Intra-Zonal 3.762 3.684 -12.0% 4.231 4.184 4.525 4.230 17.171 19.634 22.439

DLD / ILD 3.969 3.609 -15.0% 4.695 4.248 4.147 4.011 17.101 20.562 24.236

Interconnect and traffic transit 6.325 7.044 22.4% 5.554 5.754 7.010 6.546 24.864 21.991 20.444

Mobile communication services 9.239 3.583 -64.0% 9.503 9.939 9.576 9.884 38.902 41.161 40.660

Rent of channels 2.527 2.881 -12.4% 3.335 3.290 1.119 1.742 9.486 11.433 10.782

Broadband Internet 14.991 14.811 9.8% 13.520 13.487 14.402 14.529 55.938 51.619 47.984

Pay-TV 3.425 3.534 30.9% 2.787 2.700 3.145 3.274 11.906 9.208 6.748

Data services 5.853 5.619 0.0% 5.349 5.617 5.575 6.485 23.025 20.872 19.227

Other 9.324 11.115 34.9% 8.855 8.237 9.726 13.059 39.876 46.451 28.284

% of total Revenues

Local Telephone services 26.1% 26.4% 27.3% 28.1% 26.8% 25.3% 26.8% 26.9% 29.3%

Intra-Zonal 4.7% 4.8% 5.3% 5.2% 5.6% 5.0% 5.3% 5.9% 7.2%

DLD / ILD 4.9% 4.8% 5.9% 5.3% 5.1% 4.7% 5.3% 6.2% 7.8%

Interconnect and traffic transit 7.9% 9.3% 7.0% 7.2% 8.7% 7.7% 7.6% 6.6% 6.5%

Mobile communication services 11.5% 4.7% 11.9% 12.4% 11.8% 11.6% 11.9% 12.4% 13.0%

Rent of channels 3.1% 3.8% 4.2% 4.1% 1.4% 2.0% 2.9% 3.4% 3.5%

Broadband Internet 18.6% 19.5% 17.0% 16.9% 17.8% 17.0% 17.2% 15.5% 15.4%

Pay-TV 4.3% 4.7% 3.5% 3.4% 3.9% 3.8% 3.7% 2.8% 2.2%

Data services 7.3% 7.4% 6.7% 7.0% 6.9% 7.6% 7.1% 6.3% 6.2%

Other 11.6% 14.6% 11.1% 10.3% 12.0% 15.3% 12.2% 14.0% 9.1%

By customers:

B2C 41.570 36.598 -11.7% 41.958 41.434 40.955 41.537 165.884 167.330 170.373

B2B 18.235 17.931 -1.2% 17.949 18.147 19.477 18.253 73.827 70.794 72.437

B2G 10.408 11.163 11.0% 10.607 10.061 10.881 14.055 45.604 54.159 35.212

B2O 10.193 10.271 0.5% 9.045 10.216 9.645 11.483 40.389 40.152 34.308

B2C 51.7% 48.2% 52.7% 51.9% 50.6% 48.7% 50.9% 50.3% 54.5%

B2B 22.7% 23.6% 22.6% 22.7% 24.1% 21.4% 22.7% 21.3% 23.2%

B2G 12.9% 14.7% 13.3% 12.6% 13.4% 16.5% 14.0% 16.3% 11.3%

B2O 12.7% 13.5% 11.4% 12.8% 11.9% 13.5% 12.4% 12.1% 11.0%

FINANCIALS

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Balance Sheet

30

Bln RUR

BALANCE SHEET 3/31/2014 6/30/2014 3/31/2013 6/30/2013 9/30/2013 12/31/2013 12/31/2012 12/31/2011

Assets

Current assets

Cash & cash equivalents 6.250 7.249 7.287 14.891 7.416 7.960 13.629 9.634

Other investments 24.387 0.504 4.137 4.547 10.862 1.966 3.492 4.609

Prepayments 3.818 3.454 3.661 3.708 3.917 3.508 4.416 2.945

Prepaid income tax 4.802 3.902 3.635 3.381 2.701 4.894 2.951 3.384

Inventories 4.511 4.614 4.692 4.561 4.233 3.941 4.990 5.172

Trade and other accounts receivable 46.383 43.489 40.513 42.217 43.594 39.824 35.882 30.512

Other current assets 0.720 0.708 1.537 1.528 1.704 0.609 0.908 1.109

Total current assets 90.871 63.920 65.462 74.833 74.427 62.702 66.268 57.365

Assets held for sale 31.365 33.962 93.048 0.401 0.261

Non-current assets

PPE & Intangible assets 327.111 323.050 396.995 393.840 389.140 335.059 399.917 348.493

Investment property 0.114 0.121 0.254 0.216 0.229 0.113 0.274 0.259

Goodwill and other intangible assets 59.278 59.489 85.724 84.672 83.196 64.346 88.329 89.340

Investment in associates 27.802 27.955 0.785 0.807 0.830 0.918 0.775 0.773

Other investments 0.700 0.254 0.112 0.147 0.138 0.520 3.035 1.829

Other non-current assets 4.024 4.342 8.325 7.752 9.430 4.266 8.191 15.061

Total non-current assets 419.029 415.211 492.195 487.434 482.963 405.222 500.521 455.755

Total assets 541.265 513.093 557.657 562.267 557.390 560.972 567.190 513.381

Liabilities

Current liabilities

Accounts payable 51.150 49.858 51.222 95.220 49.838 73.635 61.839 41.279

Short-term loans and borrowings 37.123 26.883 56.698 47.639 59.432 33.209 65.016 82.453

Other current liabilities 6.803 7.045 9.001 8.987 8.843 9.419 10.287 8.863

Total current liabilities 95.076 83.786 116.921 151.846 118.113 116.263 137.142 132.595

Liabilities held for sale 6.399 8.936 17.647

Equity

Shareholders equity 0.097 0.096 0.097 0.097 0.096 0.097 0.097 0.097

Treasury shares (81.311) (81.382) (36.472) (31.194) (58.898) (68.325) (34.822) (18.388)

Additional paid in capital 1.624 1.622 4.322 4.320 4.579 1.658 4.344 4.743

Retained earnings and other reserves 293.156 294.346 272.927 243.334 283.788 262.967 266.607 235.158

Non-controlling interest 3.350 3.125 2.664 2.429 3.201 3.359 2.606 9.588

Total equity 216.916 217.807 243.538 218.986 232.766 199.756 238.832 231.198

Non-current liabilities

Long-term loans 177.528 158.577 157.941 152.454 166.017 184.600 152.874 94.640

Employee benefits 9.855 9.882 10.909 10.946 10.919 9.774 10.861 11.046

Deferred tax liabilities 27.802 26.836 23.322 22.927 24.626 26.728 23.107 20.518

Other non-current liabilities 7.689 7.270 5.026 5.108 4.949 6.204 4.374 23.384

Total non-current liabilities 222.874 202.565 197.198 191.435 206.511 227.306 191.216 149.588

Total equity & liabilities 541.265 513.094 557.657 562.267 557.390 560.972 567.190 513.381

Net Debt 184.014 176.159 203.215 180.655 207.171 217.309 200.769 162.850

Net Debt / OIBDA LTM x 1.7 x 1.6 x 1.8 x 1.6 x 1.8 x 1.9 x 1.7 x 1.4

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

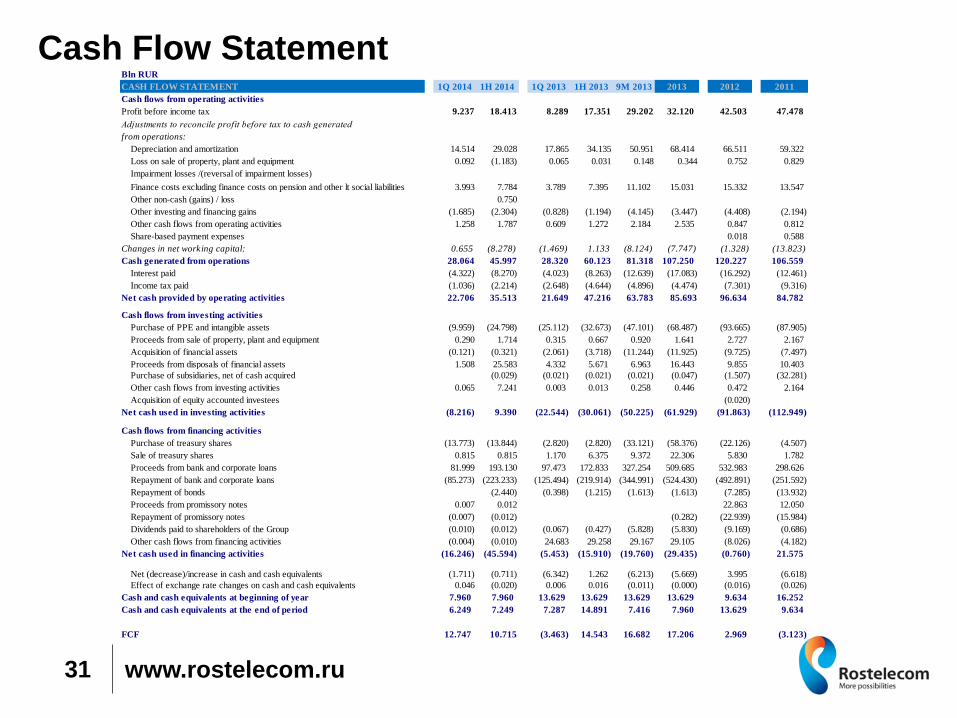

Cash Flow Statement

31

Bln RUR

CASH FLOW STATEMENT 1Q 2014 1H 2014 1Q 2013 1H 2013 9M 2013 2013 2012 2011

Cash flows from operating activities

Profit before income tax 9.237 18.413 8.289 17.351 29.202 32.120 42.503 47.478

Adjustments to reconcile profit before taх to cash generated

from operations:

Depreciation and amortization 14.514 29.028 17.865 34.135 50.951 68.414 66.511 59.322

Loss on sale of property, plant and equipment 0.092 (1.183) 0.065 0.031 0.148 0.344 0.752 0.829

Impairment losses /(reversal of impairment losses)

Finance costs excluding finance costs on pension and other lt social liabilities 3.993 7.784 3.789 7.395 11.102 15.031 15.332 13.547

Other non-cash (gains) / loss 0.750

Other investing and financing gains (1.685) (2.304) (0.828) (1.194) (4.145) (3.447) (4.408) (2.194)

Other cash flows from operating activities 1.258 1.787 0.609 1.272 2.184 2.535 0.847 0.812

Share-based payment expenses 0.018 0.588

Changes in net working capital: 0.655 (8.278) (1.469) 1.133 (8.124) (7.747) (1.328) (13.823)

Cash generated from operations 28.064 45.997 28.320 60.123 81.318 107.250 120.227 106.559

Interest paid (4.322) (8.270) (4.023) (8.263) (12.639) (17.083) (16.292) (12.461)

Income tax paid (1.036) (2.214) (2.648) (4.644) (4.896) (4.474) (7.301) (9.316)

Net cash provided by operating activities 22.706 35.513 21.649 47.216 63.783 85.693 96.634 84.782

Cash flows from investing activities

Purchase of PPE and intangible assets (9.959) (24.798) (25.112) (32.673) (47.101) (68.487) (93.665) (87.905)

Proceeds from sale of property, plant and equipment 0.290 1.714 0.315 0.667 0.920 1.641 2.727 2.167

Acquisition of financial assets (0.121) (0.321) (2.061) (3.718) (11.244) (11.925) (9.725) (7.497)

Proceeds from disposals of financial assets 1.508 25.583 4.332 5.671 6.963 16.443 9.855 10.403

Purchase of subsidiaries, net of cash acquired (0.029) (0.021) (0.021) (0.021) (0.047) (1.507) (32.281)

Other cash flows from investing activities 0.065 7.241 0.003 0.013 0.258 0.446 0.472 2.164

Acquisition of equity accounted investees (0.020)

Net cash used in investing activities (8.216) 9.390 (22.544) (30.061) (50.225) (61.929) (91.863) (112.949)

Cash flows from financing activities

Purchase of treasury shares (13.773) (13.844) (2.820) (2.820) (33.121) (58.376) (22.126) (4.507)

Sale of treasury shares 0.815 0.815 1.170 6.375 9.372 22.306 5.830 1.782

Proceeds from bank and corporate loans 81.999 193.130 97.473 172.833 327.254 509.685 532.983 298.626

Repayment of bank and corporate loans (85.273) (223.233) (125.494) (219.914) (344.991) (524.430) (492.891) (251.592)

Repayment of bonds (2.440) (0.398) (1.215) (1.613) (1.613) (7.285) (13.932)

Proceeds from promissory notes 0.007 0.012 22.863 12.050

Repayment of promissory notes (0.007) (0.012) (0.282) (22.939) (15.984)

Dividends paid to shareholders of the Group (0.010) (0.012) (0.067) (0.427) (5.828) (5.830) (9.169) (0.686)

Other cash flows from financing activities (0.004) (0.010) 24.683 29.258 29.167 29.105 (8.026) (4.182)

Net cash used in financing activities (16.246) (45.594) (5.453) (15.910) (19.760) (29.435) (0.760) 21.575

Net (decrease)/increase in cash and cash equivalents (1.711) (0.711) (6.342) 1.262 (6.213) (5.669) 3.995 (6.618)

Effect of exchange rate changes on cash and cash equivalents 0.046 (0.020) 0.006 0.016 (0.011) (0.000) (0.016) (0.026)

Cash and cash equivalents at beginning of year 7.960 7.960 13.629 13.629 13.629 13.629 9.634 16.252

Cash and cash equivalents at the end of period 6.249 7.249 7.287 14.891 7.416 7.960 13.629 9.634

FCF 12.747 10.715 (3.463) 14.543 16.682 17.206 2.969 (3.123)

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

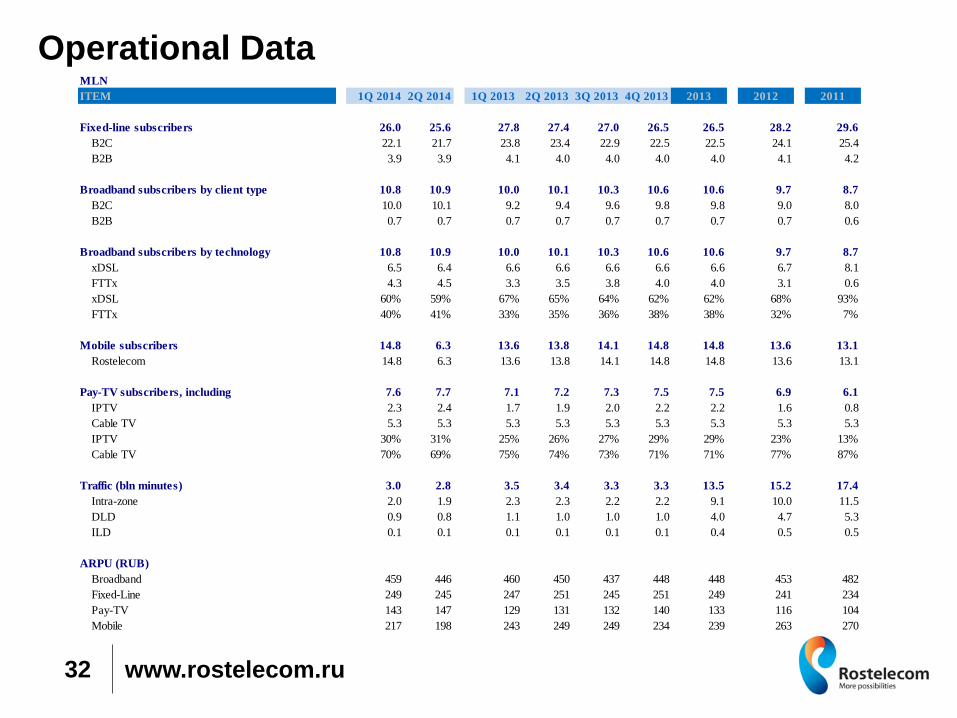

Operational Data

32

MLN

ITEM 1Q 2014 2Q 2014 1Q 2013 2Q 2013 3Q 2013 4Q 2013 2013 2012 2011

Fixed-line subscribers 26.0 25.6 27.8 27.4 27.0 26.5 26.5 28.2 29.6

B2C 22.1 21.7 23.8 23.4 22.9 22.5 22.5 24.1 25.4

B2B 3.9 3.9 4.1 4.0 4.0 4.0 4.0 4.1 4.2

Broadband subscribers by client type 10.8 10.9 10.0 10.1 10.3 10.6 10.6 9.7 8.7

B2C 10.0 10.1 9.2 9.4 9.6 9.8 9.8 9.0 8.0

B2B 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.6

Broadband subscribers by technology 10.8 10.9 10.0 10.1 10.3 10.6 10.6 9.7 8.7

xDSL 6.5 6.4 6.6 6.6 6.6 6.6 6.6 6.7 8.1

FTTx 4.3 4.5 3.3 3.5 3.8 4.0 4.0 3.1 0.6

xDSL 60% 59% 67% 65% 64% 62% 62% 68% 93%

FTTx 40% 41% 33% 35% 36% 38% 38% 32% 7%

Mobile subscribers 14.8 6.3 13.6 13.8 14.1 14.8 14.8 13.6 13.1

Rostelecom 14.8 6.3 13.6 13.8 14.1 14.8 14.8 13.6 13.1

Pay-TV subscribers, including 7.6 7.7 7.1 7.2 7.3 7.5 7.5 6.9 6.1

IPTV 2.3 2.4 1.7 1.9 2.0 2.2 2.2 1.6 0.8

Cable TV 5.3 5.3 5.3 5.3 5.3 5.3 5.3 5.3 5.3

IPTV 30% 31% 25% 26% 27% 29% 29% 23% 13%

Cable TV 70% 69% 75% 74% 73% 71% 71% 77% 87%

Traffic (bln minutes) 3.0 2.8 3.5 3.4 3.3 3.3 13.5 15.2 17.4

Intra-zone 2.0 1.9 2.3 2.3 2.2 2.2 9.1 10.0 11.5

DLD 0.9 0.8 1.1 1.0 1.0 1.0 4.0 4.7 5.3

ILD 0.1 0.1 0.1 0.1 0.1 0.1 0.4 0.5 0.5

ARPU (RUB)

Broadband 459 446 460 450 437 448 448 453 482

Fixed-Line 249 245 247 251 245 251 249 241 234

Pay-TV 143 147 129 131 132 140 133 116 104

Mobile 217 198 243 249 249 234 239 263 270

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

www.rostelecom.ru

Disclaimer

By attending any meeting where this presentation is made, or by reading any part of this presentation, you acknowledge and agree to be bound by the following:

• This presentation has been prepared by OJSC Rostelecom (the “Company”). This presentation is strictly confidential to the recipient, may not be distributed to the

press or any other person, and may not be reproduced in any form, in whole or in part.

• The Company has included its own estimates, assessments, adjustments and judgments in preparing certain market information herein, which have not been

verified by an independent third party. Market information included herein is, therefore, unless otherwise attributed exclusively to a third party source, to a certain

degree subjective. While the Company believes that its own estimates, assessments, adjustments and judgments are reasonable and that the market information

prepared by the Company appropriately reflects the industry and the markets in which it operates, there is no assurance that the Company’s own estimates,

assessments, adjustments and judgments are the most appropriate for making determinations relating to market information.

• Neither the Company nor any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever

arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.

• This presentation is confidential and does not constitute or form part of, and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy

or acquire securities of the Company or any of its subsidiaries in any jurisdiction or an inducement to enter into investment activity in any jurisdiction. Neither this

presentation nor any part thereof, nor the fact of its distribution, shall form the basis of, or be relied on in connection with, any contract or commitment or investment

decision whatsoever.

• This presentation is not intended for publication or circulation in the United States. This presentation does not constitute and should not be construed as an offer to

sell or the solicitation of an offer to buy securities in the United States or to any U.S. person (as defined in Regulation S under the US Securities Act of 1933 (the

“Securities Act”)). No securities of the Company have been, nor will be, registered under the Securities Act or the securities laws of any state of the United States,

and unless so registered may not be offered or sold except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the

Securities Act and applicable state securities laws. This presentation does not constitute a public offering or an advertisement of securities in the Russian

Federation and does not constitute an offer or a proposal to make offers or to acquire any securities in the Russian Federation.

• In any member state of the European Economic Area, this Presentation is made to and directed only at persons who are qualified investors within the meaning of

article 2(1)(e) of the Prospectus Directive (2003/71/EC) (“Qualified Investors”). In addition, in the United Kingdom, this Presentation is made to and directed at: (i)

investment professionals falling within article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) and (ii) high net

worth individuals, and other persons to whom it may lawfully be communicated, falling within article 49(2)(A) to (D) of the Order (such persons together with

Qualified Investors, being “Relevant Persons”). In these jurisdictions, persons who are not Relevant Persons must not rely on or act upon the information contained

in this presentation or any of its contents. Any investment or investment activity to which this Presentation relates is only available to Relevant Persons and will be

engaged in only with Relevant Persons. The recipients of the information contained herein should not base any behavior that would amount to market abuse for the

purposes of the Financial Services and Markets Act 2000 (“FSMA”) and the Code of Market Conduct made pursuant to the FSMA on the information in this

Presentation or any information provided or discussed in connection with it.

• This presentation is not directed at, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country

or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing

within such jurisdiction. Persons into whose possession this presentation comes should inform themselves about, and observe, any such restrictions

33

0 170 231

240 78 35

6 58 123

253 188 95

120 172 56

128 71 144

191 162 155

0 102 204

182 213 251

Contact Information

Investor Relations

Office +7 (499) 995 9780

E-mail: [email protected]

Web: http://www.rostelecom.ru/en/ir/