investor presentation - kimberly-clark€¦ · leading the world in essentials for a better life...

TRANSCRIPT

Leading the World in Essentials for a Better Life

Investor

Presentation Financial Information

as of December 31, 2014

www.kimberly-clark.com

• $20 billion global company founded in 1872

• Products used by one-quarter of world’s population

• Strong legacy of innovation – created 5 of the 8 major product

categories in which we compete

• Products sold in more than 175 countries

• #1 or #2 position in 80 countries

• Strong global brands, including five billion-dollar brands:

2

Highlights

3

Our Values

Authentic: Our heritage is one of honesty, integrity and doing

the right thing

Accountable: We take ownership for our business and our future

Innovative: Our commitment is to new ideas that add value

Caring: We respect each other and care for the communities

where we live and work

• Sustainability 2015 vision built around a framework of People,

Planet and Products

– Engage with people to build enduring relationships

– Respect our planet and conserve its resources

– Deliver quality products today and for generations to come

• Visit www.kimberly-clark.com/sustainability for information on

our sustainability strategy and performance

4

Commitment to Sustainability

A Trusted Brand…Yesterday, Today and Tomorrow

5

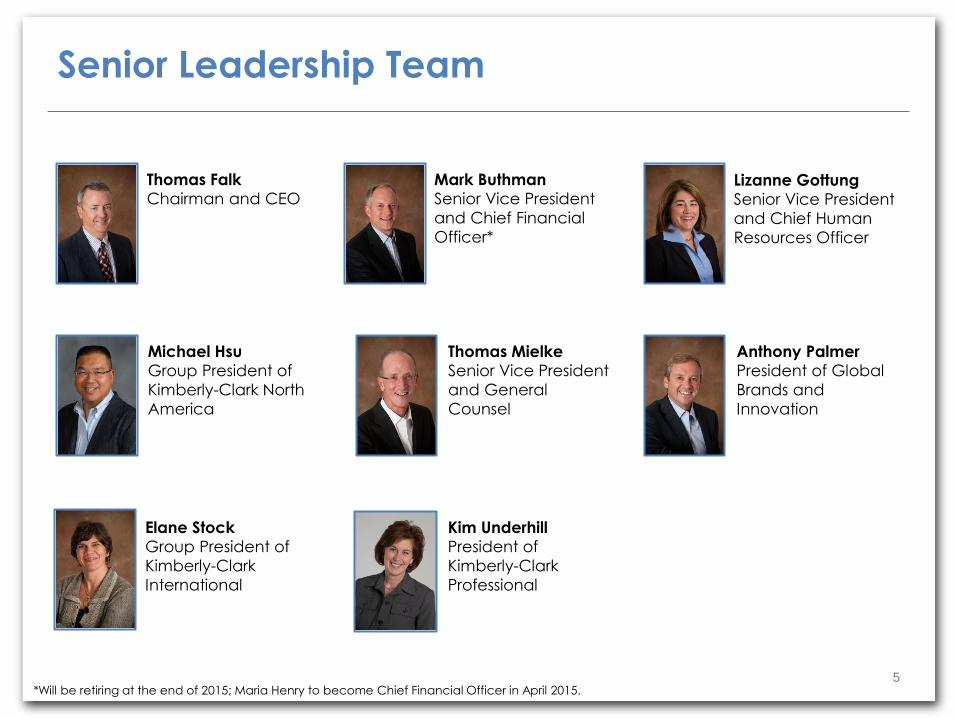

Senior Leadership Team

Mark Buthman

Senior Vice President

and Chief Financial

Officer*

Anthony Palmer

President of Global

Brands and

Innovation

Lizanne Gottung

Senior Vice President

and Chief Human

Resources Officer

Thomas Mielke

Senior Vice President

and General

Counsel

Thomas Falk

Chairman and CEO

Kim Underhill

President of

Kimberly-Clark

Professional

Michael Hsu

Group President of

Kimberly-Clark North

America

Elane Stock

Group President of

Kimberly-Clark

International

*Will be retiring at the end of 2015; Maria Henry to become Chief Financial Officer in April 2015.

6

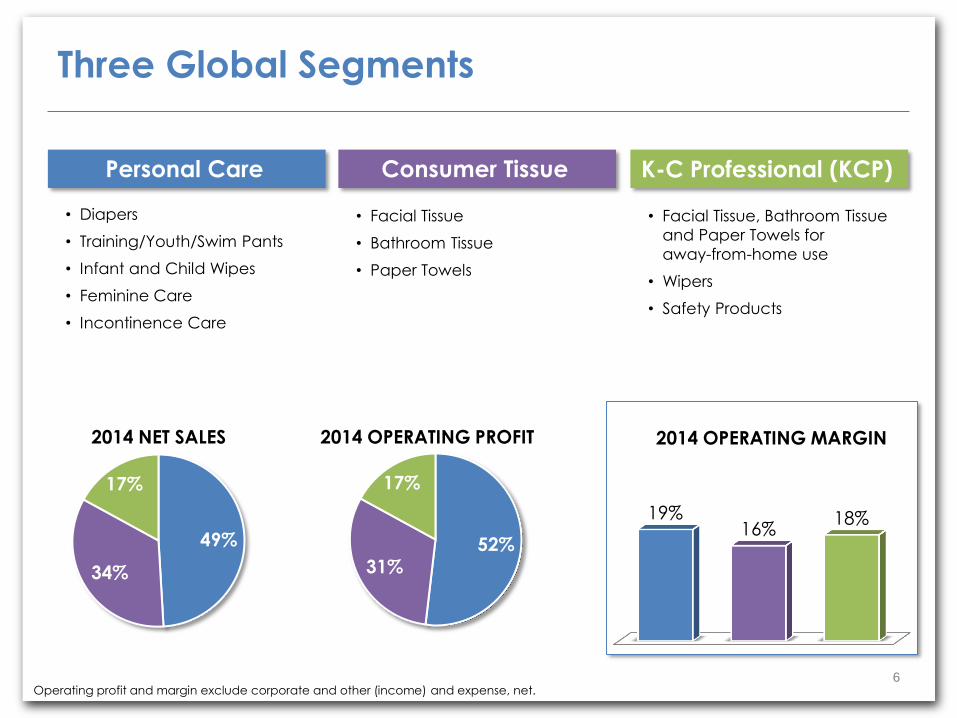

Three Global Segments

49%

34%

17%

2014 NET SALES

52% 31%

17%

2014 OPERATING PROFIT

Operating profit and margin exclude corporate and other (income) and expense, net.

Personal Care Consumer Tissue K-C Professional (KCP)

• Diapers

• Training/Youth/Swim Pants

• Infant and Child Wipes

• Feminine Care

• Incontinence Care

• Facial Tissue

• Bathroom Tissue

• Paper Towels

• Facial Tissue, Bathroom Tissue

and Paper Towels for

away-from-home use

• Wipers

• Safety Products

19% 16%

18%

2014 OPERATING MARGIN

7

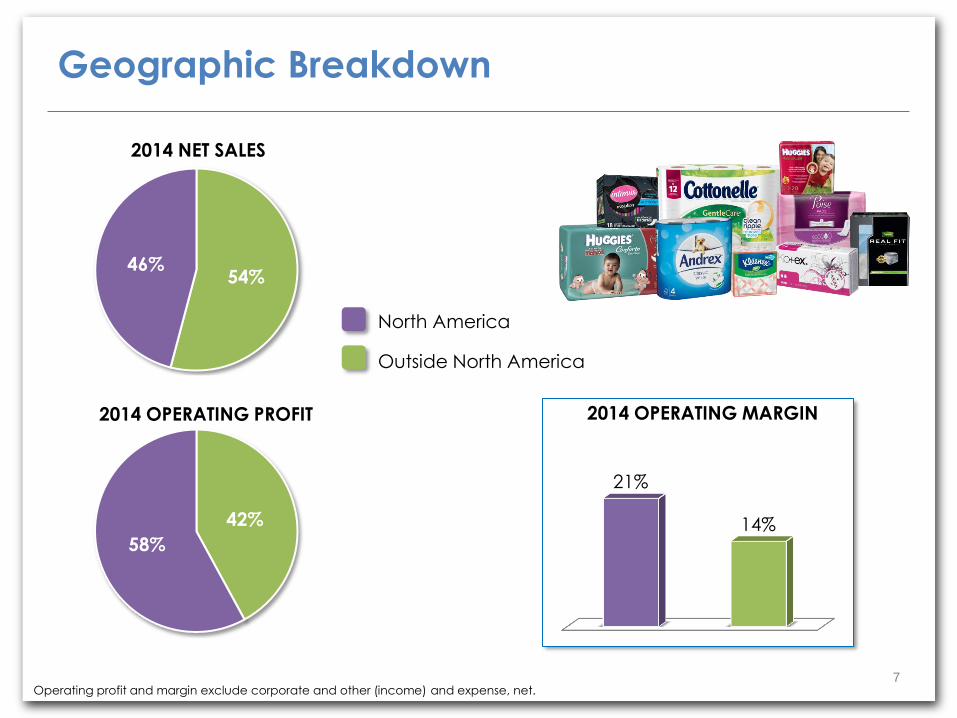

Geographic Breakdown

54% 46%

2014 NET SALES

42%

58%

2014 OPERATING PROFIT

Operating profit and margin exclude corporate and other (income) and expense, net.

21%

14%

2014 OPERATING MARGIN

North America

Outside North America

• GBP is our strategic plan that prioritizes growth opportunities

and applies greater financial discipline to our operations

– Launched in mid-2003 and designed to generate sustainable

growth and improved shareholder returns

• GBP strategies

– Manage portfolio to balance growth, profitability, cash flow

– Invest in brands, innovation, growth initiatives

– Deliver sustainable cost reduction

– Disciplined capital management to improve

ROIC and return cash to shareholders

8

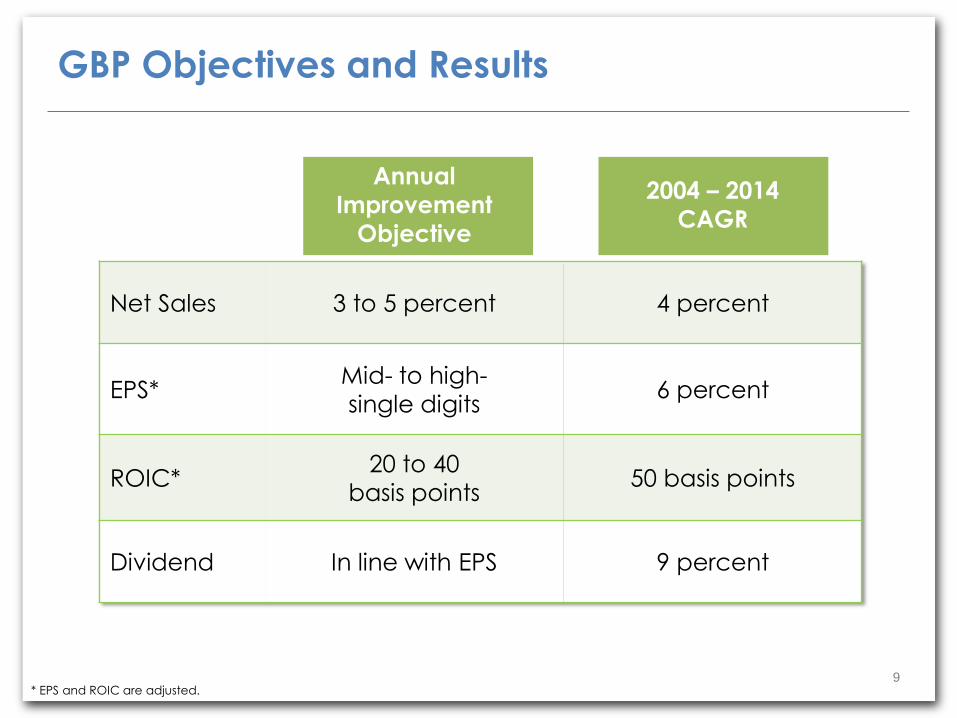

Global Business Plan (GBP)

Annual

Improvement

Objective

2004 – 2014

CAGR

Net Sales 3 to 5 percent 4 percent

EPS* Mid- to high-

single digits 6 percent

ROIC* 20 to 40

basis points 50 basis points

Dividend In line with EPS 9 percent

9

GBP Objectives and Results

* EPS and ROIC are adjusted.

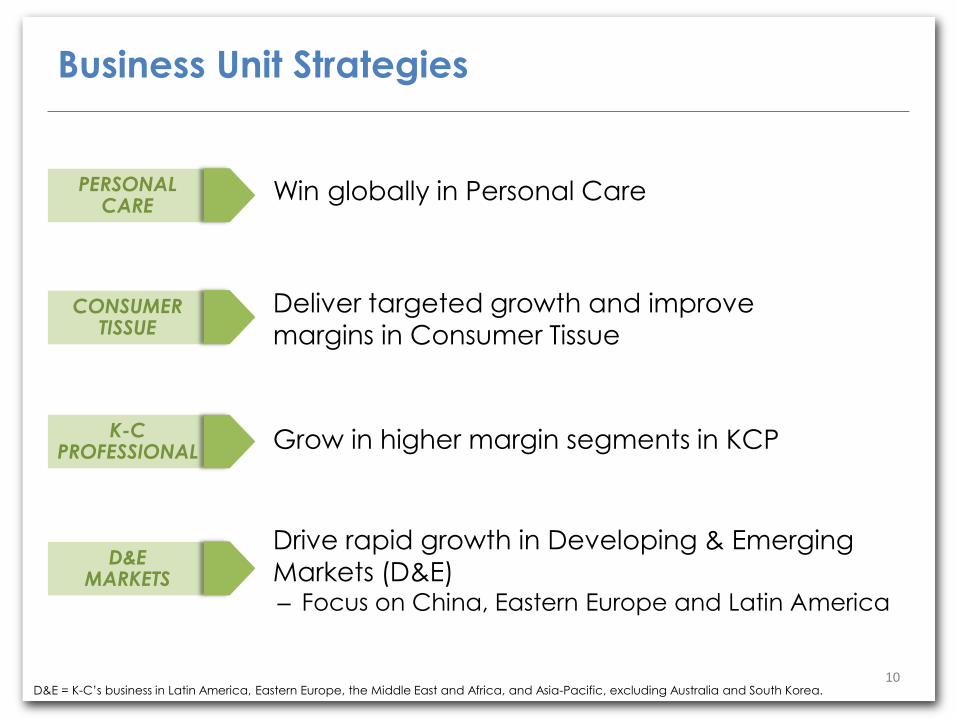

Drive rapid growth in Developing & Emerging

Markets (D&E) – Focus on China, Eastern Europe and Latin America

D&E MARKETS

Deliver targeted growth and improve margins in Consumer Tissue

10

Business Unit Strategies

Win globally in Personal Care

Grow in higher margin segments in KCP K-C PROFESSIONAL

CONSUMER TISSUE

PERSONAL CARE

D&E = K-C’s business in Latin America, Eastern Europe, the Middle East and Africa, and Asia-Pacific, excluding Australia and South Korea.

• Leverage strong brands

• Win with consumers by providing superior innovation supported by integrated marketing campaigns

• Long track record of success

– 11-year organic net sales CAGR: +6 percent

11

Win Globally in Personal Care

2003 2014

39%

49%

PERSONAL CARE NET SALES % OF TOTAL COMPANY

12

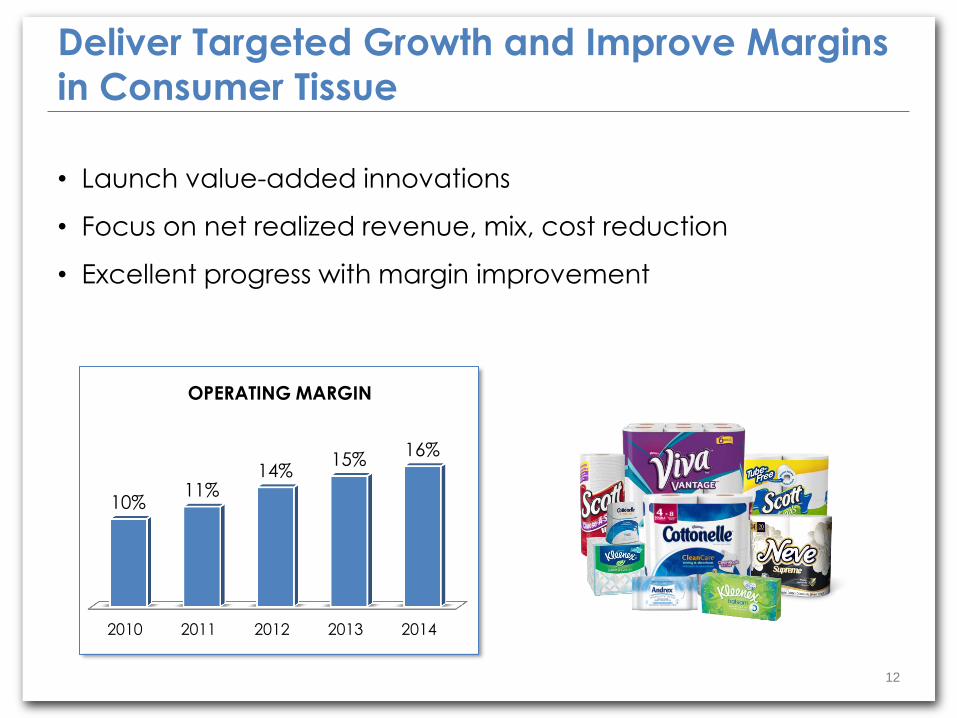

Deliver Targeted Growth and Improve Margins

in Consumer Tissue

• Launch value-added innovations

• Focus on net realized revenue, mix, cost reduction

• Excellent progress with margin improvement

2010 2011 2012 2013 2014

10% 11%

14% 15%

16%

OPERATING MARGIN

13

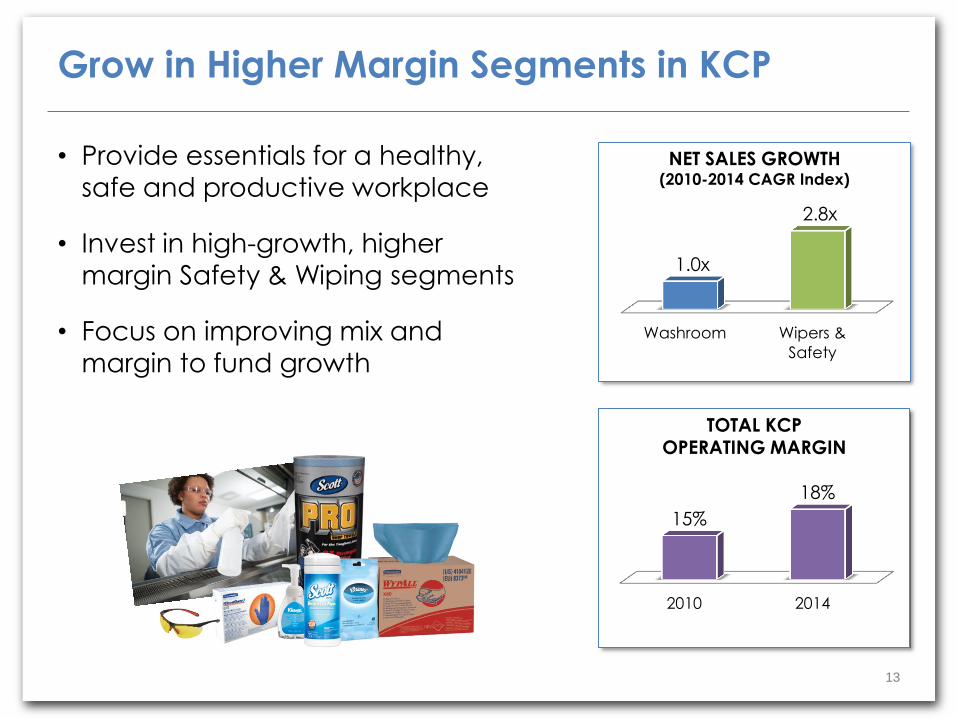

Grow in Higher Margin Segments in KCP

• Provide essentials for a healthy,

safe and productive workplace

• Invest in high-growth, higher

margin Safety & Wiping segments

• Focus on improving mix and margin to fund growth

Washroom Wipers &

Safety

1.0x

2.8x

NET SALES GROWTH (2010-2014 CAGR Index)

2010 2014

15%

18%

TOTAL KCP OPERATING MARGIN

14

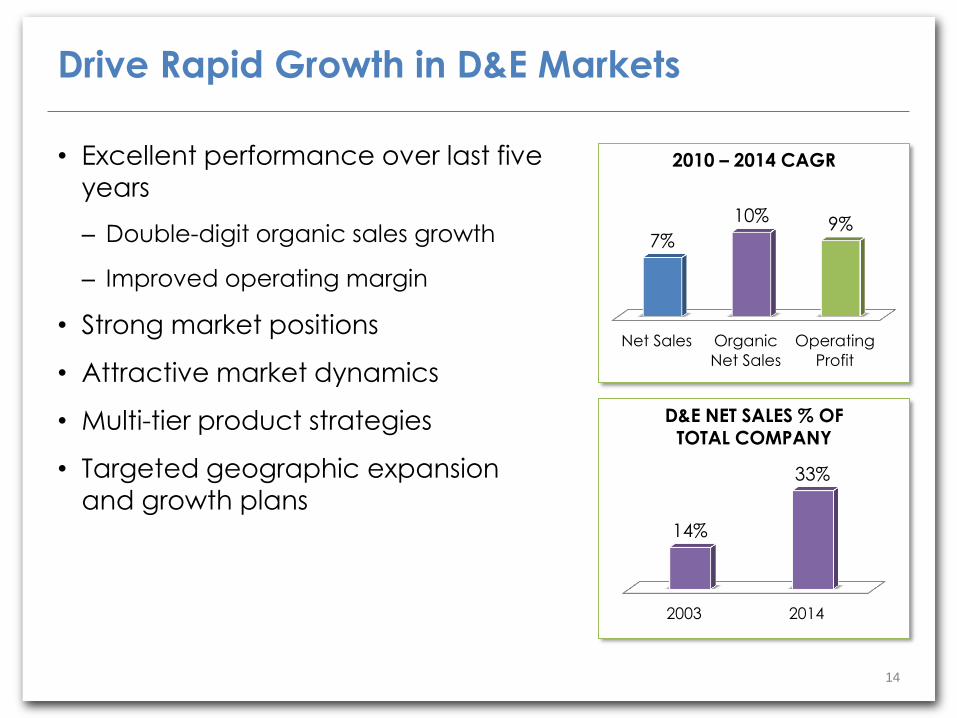

Drive Rapid Growth in D&E Markets

• Excellent performance over last five

years

– Double-digit organic sales growth

– Improved operating margin

• Strong market positions

• Attractive market dynamics

• Multi-tier product strategies

• Targeted geographic expansion

and growth plans

Net Sales Organic

Net Sales

Operating

Profit

7%

10% 9%

2003 2014

14%

33%

2010 – 2014 CAGR

D&E NET SALES % OF TOTAL COMPANY

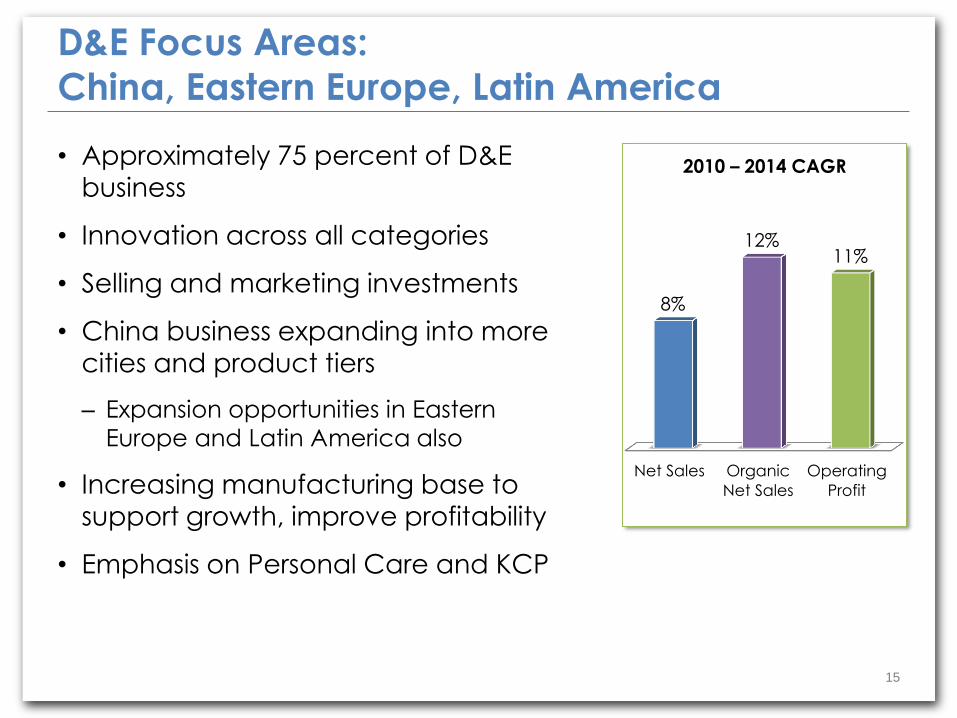

• Approximately 75 percent of D&E

business

• Innovation across all categories

• Selling and marketing investments

• China business expanding into more cities and product tiers

– Expansion opportunities in Eastern

Europe and Latin America also

• Increasing manufacturing base to

support growth, improve profitability

• Emphasis on Personal Care and KCP

15

D&E Focus Areas:

China, Eastern Europe, Latin America

Net Sales Organic

Net Sales

Operating

Profit

8%

12% 11%

2010 – 2014 CAGR

2003 2014

18%

41%

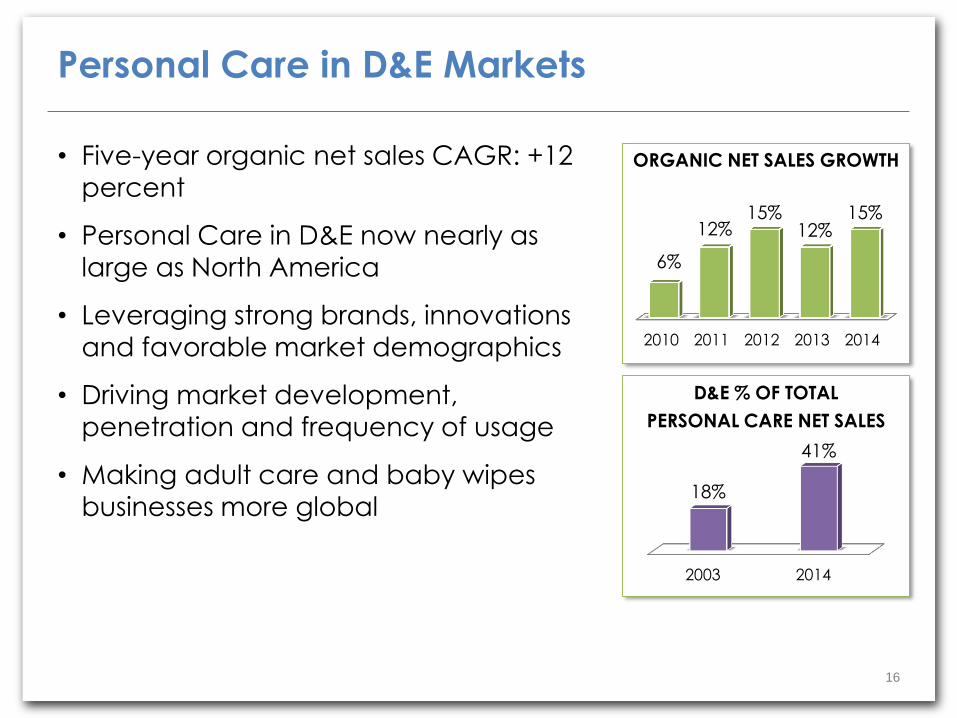

• Five-year organic net sales CAGR: +12

percent

• Personal Care in D&E now nearly as

large as North America

• Leveraging strong brands, innovations and favorable market demographics

• Driving market development,

penetration and frequency of usage

• Making adult care and baby wipes

businesses more global

16

Personal Care in D&E Markets

D&E % OF TOTAL

PERSONAL CARE NET SALES

2010 2011 2012 2013 2014

6%

12% 15%

12% 15%

ORGANIC NET SALES GROWTH

17

KCP in D&E Markets

• Approaching $1 billion in annual net

sales; excellent margins and growth opportunities

• Double-digit growth in organic net

sales and operating profit over last

five years

• Expanding where industrialization and

economic development are

occurring

– Including Latin America, Eastern Europe

and China

• Leveraging global brands, go-to-

market capabilities and sustainability leadership

Net Sales Organic

Net Sales

Operating

Profit

9%

12%

10%

2010 – 2014 CAGR

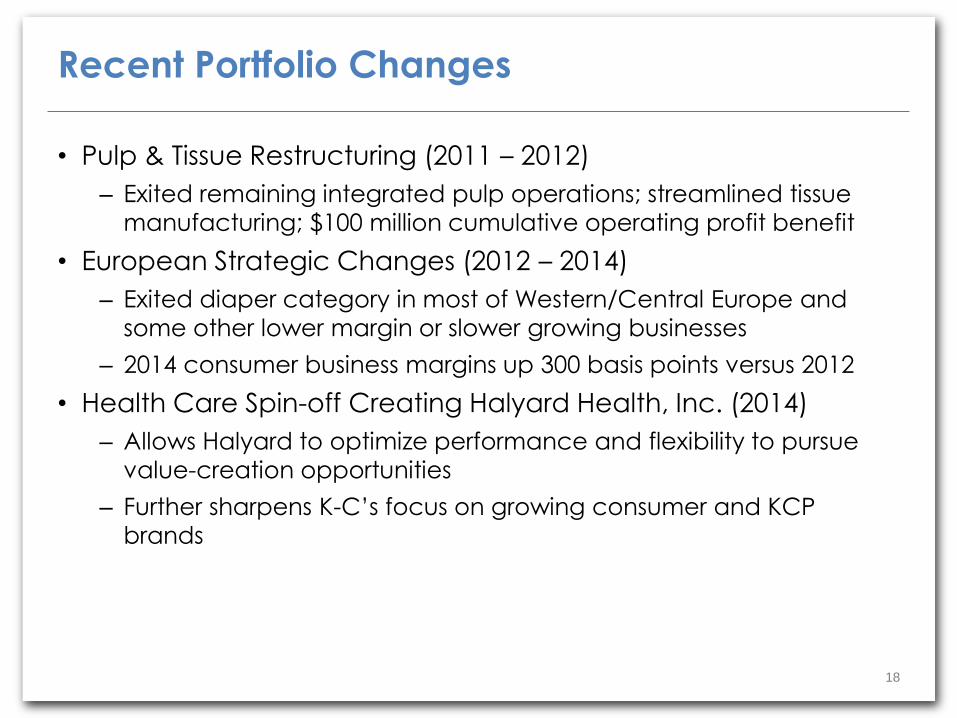

• Pulp & Tissue Restructuring (2011 – 2012)

– Exited remaining integrated pulp operations; streamlined tissue

manufacturing; $100 million cumulative operating profit benefit

• European Strategic Changes (2012 – 2014)

– Exited diaper category in most of Western/Central Europe and

some other lower margin or slower growing businesses

– 2014 consumer business margins up 300 basis points versus 2012

• Health Care Spin-off Creating Halyard Health, Inc. (2014)

– Allows Halyard to optimize performance and flexibility to pursue

value-creation opportunities

– Further sharpens K-C’s focus on growing consumer and KCP

brands

18

Recent Portfolio Changes

• Announced October 2014

• Will offset impact of stranded overhead costs from health care business spin-off and improve efficiency

• More flexibility to invest in brands, targeted growth initiatives,

capabilities

• Anticipated workforce reductions 1,100 to 1,300

• Expected financial impacts

– After-tax costs $130 to $160 million by end of 2016

– Pre-tax savings $120 to $140 million by end of 2017

• Further evidence of financial and cost discipline

19

2014 Organization Restructuring

• Supporting innovation and building brand equity

• Increasing use of non-traditional channels and programs

• Improving efficiencies

• Significant increase in spending in last five years

20

Investing For Growth – Advertising

2009 2014

$559

$767

2.9%

NSV

3.9%

NSV

ADVERTISING SPENDING ($ MILLIONS)

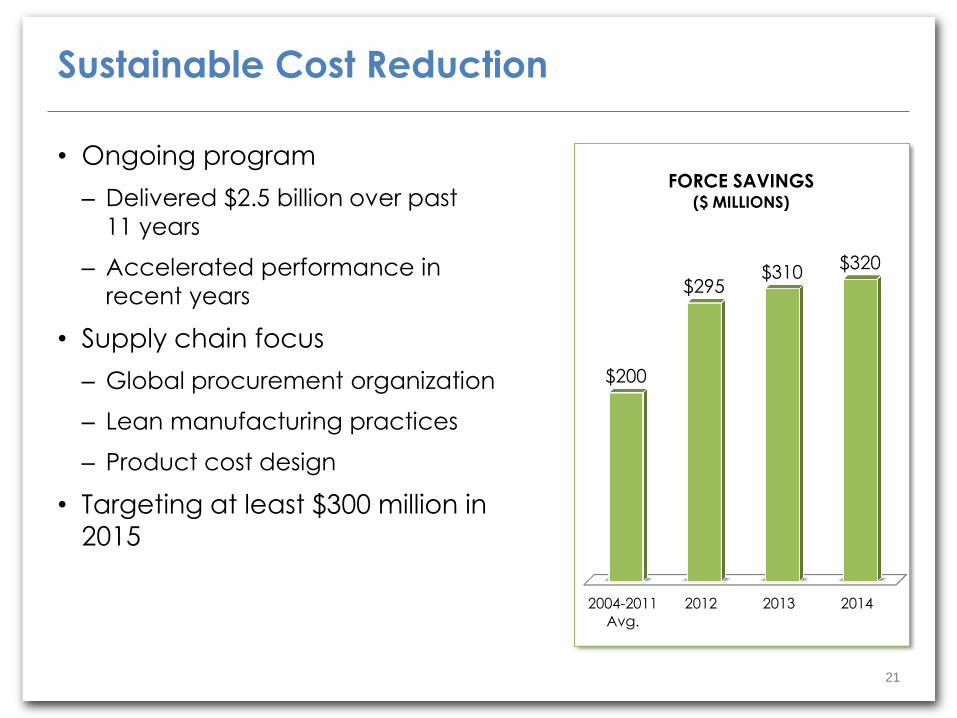

• Ongoing program

– Delivered $2.5 billion over past

11 years

– Accelerated performance in

recent years

• Supply chain focus

– Global procurement organization

– Lean manufacturing practices

– Product cost design

• Targeting at least $300 million in

2015

21

Sustainable Cost Reduction

2004-2011

Avg.

2012 2013 2014

$200

$295 $310

$320

FORCE SAVINGS ($ MILLIONS)

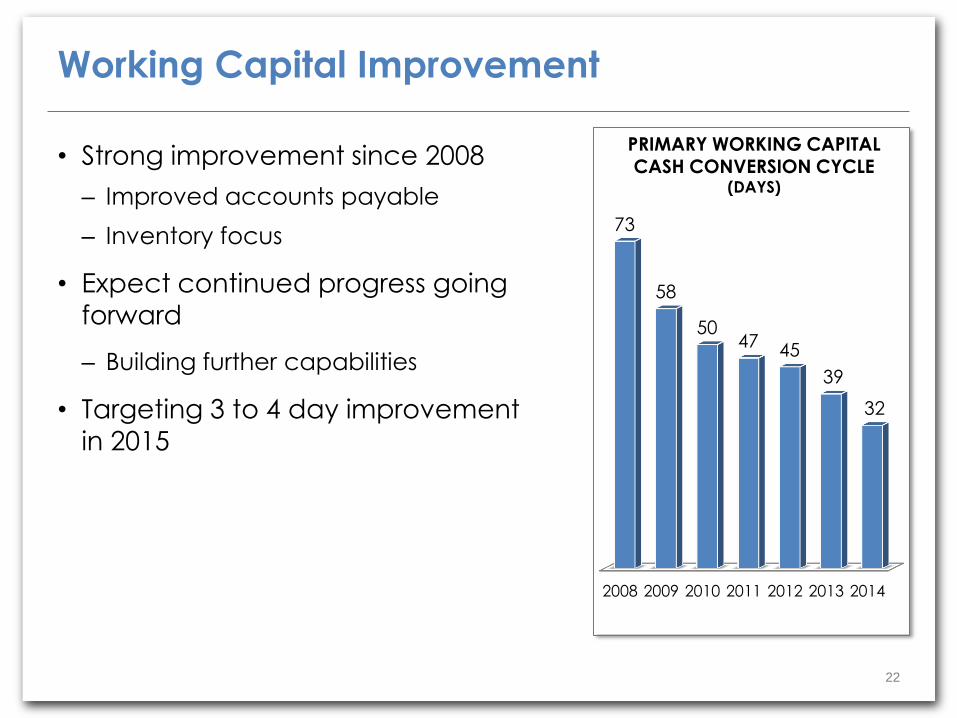

• Strong improvement since 2008

– Improved accounts payable

– Inventory focus

• Expect continued progress going

forward

– Building further capabilities

• Targeting 3 to 4 day improvement

in 2015

22

Working Capital Improvement

2008 2009 2010 2011 2012 2013 2014

73

58

50 47

45

39

32

PRIMARY WORKING CAPITAL CASH CONVERSION CYCLE

(DAYS)

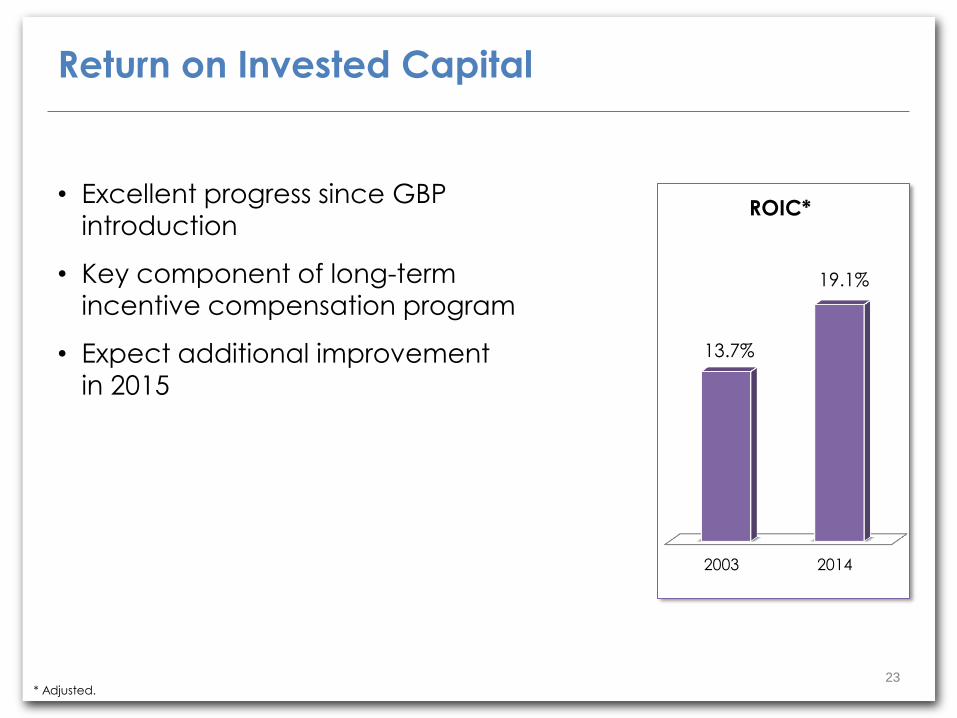

• Excellent progress since GBP introduction

• Key component of long-term

incentive compensation program

• Expect additional improvement

in 2015

23

Return on Invested Capital

* Adjusted.

2003 2014

ROIC*

19.1%

13.7%

• Maintain ‘A’ credit rating and balance sheet flexibility

• Fund business needs (growth, innovation, cost savings)

– Capital spending 4.5 to 5.5 percent of net sales

• Grow dividend

– Top-tier payout in Consumer Packaged Goods industry

• Consider M&A

– Not core part of growth strategy

• Return excess cash to shareholders via

share repurchases

24

Capital Allocation Strategy

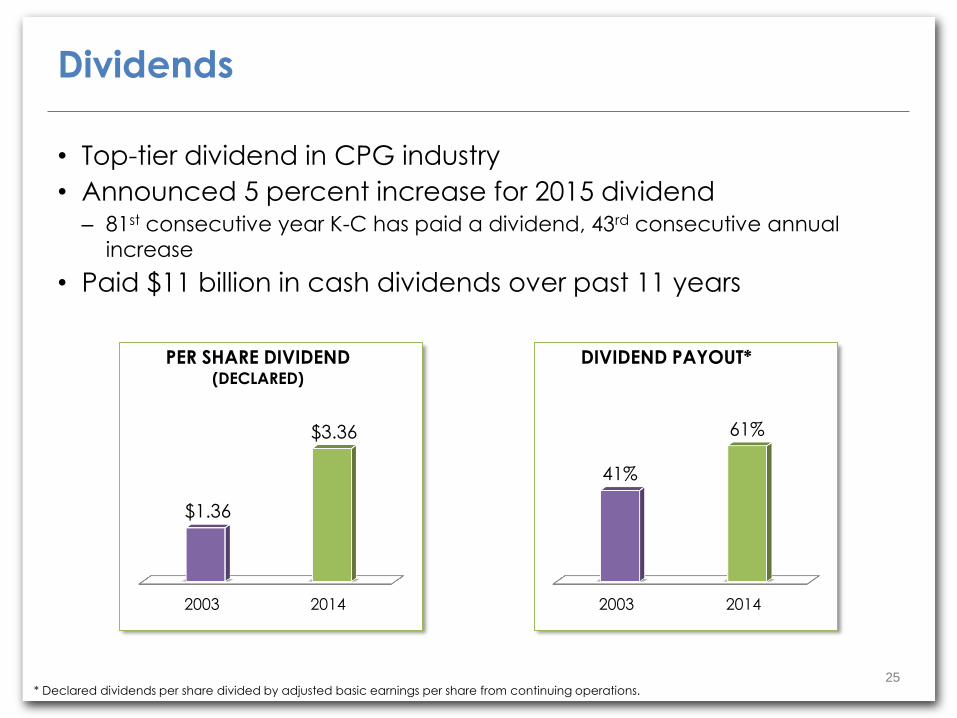

• Top-tier dividend in CPG industry

• Announced 5 percent increase for 2015 dividend – 81st consecutive year K-C has paid a dividend, 43rd consecutive annual

increase

• Paid $11 billion in cash dividends over past 11 years

25

Dividends

* Declared dividends per share divided by adjusted basic earnings per share from continuing operations.

2003 2014

41%

61%

DIVIDEND PAYOUT*

2003 2014

$1.36

$3.36

PER SHARE DIVIDEND (DECLARED)

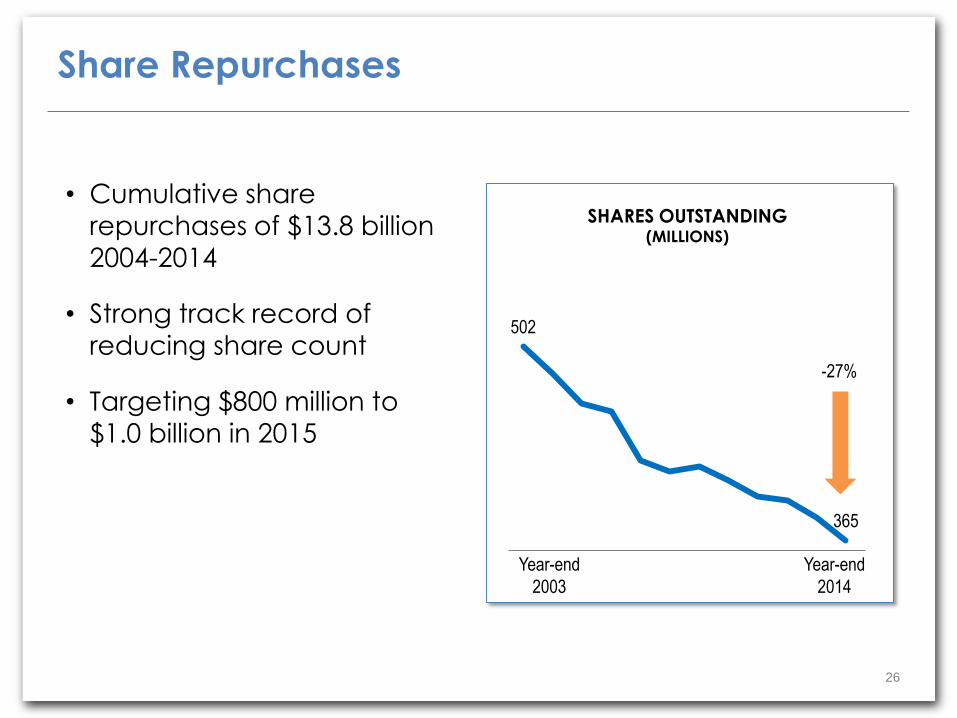

• Cumulative share repurchases of $13.8 billion

2004-2014

• Strong track record of reducing share count

• Targeting $800 million to

$1.0 billion in 2015

26

Share Repurchases

502

365

SHARES OUTSTANDING (MILLIONS)

-27%

Year-end

2014

Year-end

2003

27

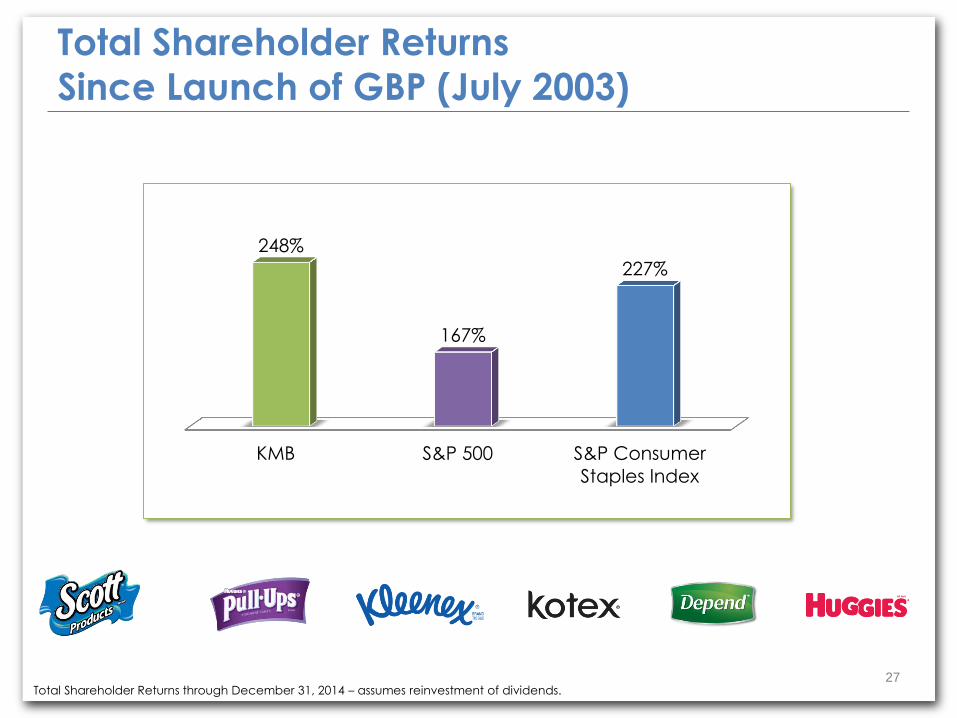

Total Shareholder Returns

Since Launch of GBP (July 2003)

Total Shareholder Returns through December 31, 2014 – assumes reinvestment of dividends.

KMB S&P 500 S&P Consumer

Staples Index

248%

167%

227%

• Contact Investor Relations with your questions

– Paul Alexander, Vice President at (972) 281-1440

• Visit www.kimberly-clark.com/investors to view our annual

report, SEC filings or news releases

• To obtain copies of our 2014 Annual Report on Form 10-K, SEC

filings or news releases, call (800) 639-1352

28

To Learn More About Kimberly-Clark

Forward-Looking Information

Certain matters in this presentation, including our 2015 outlook, expectations and planning assumptions,

and any estimates, projections, and statements relating to our business plans, strategies or objectives,

constitute forward-looking statements and are based upon management’s expectations and beliefs

concerning future events impacting the company. These statements are subject to risks and

uncertainties, including currency rates and exchange risks, cost savings and reductions, raw material,

energy, and other input costs, competition, market demand and economic and political conditions and

the anticipated costs, scope, timing and financial and other effects of the 2014 organization

restructuring. There can be no assurance that these future events will occur as anticipated or that the

company’s results will be as estimated. Furthermore, unless otherwise specifically indicated, forward-

looking statements contained in this presentation are based on our fourth quarter 2014 earnings

communication which occurred on January 23, 2015. Forward-looking statements speak only as of the

date they were made, and we undertake no obligation to publicly update any of these statements. For

a description of certain factors that could cause the company’s future results to differ materially from

those expressed in any such forward-looking statements, see Item 1A of the company’s Annual Report

on Form 10-K for the year ended December 31, 2014 entitled “Risk Factors.”

Non-GAAP Financial Measures

This presentation contains some financial measures that have been adjusted to exclude certain items

and differ from reported results using Generally Accepted Accounting Principles (GAAP). Management

believes that reporting in this manner enhances investors’ understanding and analysis of the company’s

performance. Organic net sales exclude the impact of changes in foreign currency exchange rates and

lower sales as a result of portfolio changes. For additional information on why we make these

adjustments and reconciliations to comparable measures under GAAP, see the supplemental

information posted to the Investors section of our website (www.kimberly-clark.com/investors).

29

Safe Harbor Statement