investor presentation park city group: vision randy fields · pdf fileinvestor presentation...

TRANSCRIPT

Park City Group: VisionConsumer Driven Sales Optimization™

Investor Presentation

Randy Fields

November 2009

OTCBB: PCYGwww.parkcitygroup.com

2

Specializes in Unique Supply Chain Solutions for Retailers and Suppliers

Reasons To Invest in Park City Group

Recurring revenue model with multiple year visibility Only scan based trading platform in the world Marquis customer list Beneficiary of the current economic backdrop Patent protected technology solution

3

Impactful Board of Directors

Randy Fields, Chairman & CEO - Co-founder, Mrs. Fields CookiesRobert Allen – former CEO of Southern Belle DairyPeter Brennan – private brand authority and Vice Chairman of

Daymon Worldwide James Gillis - Co-CEO of Source Interlink Companies, Inc., a

marketing and fulfillment company of entertainment productsBob Hermanns, SVP – Former CEO of Associated GrocersRichard Jacobsen – CEO, Time Inc. Retail Sales and MarketingRichard Krause –CEO of New England Confectionery Company

Industry Experts & Access to Customers

4

Our Target Market

All Major Retail Channels– Grocery, specialty, home

improvement, office supply, arts & crafts, sporting goods, electronics, etc…

All Consumer Goods Suppliers

- Clorox, Crayola, Warner Lambert, Johnson & Johnson, Titleist, Adidas, Kraft Foods, 3M, etc…

5

Select Retail CustomersGROCERYGROCERY DRUG & DRUG &

CONVENIENCECONVENIENCEMASS &MASS &

SPECIALTYSPECIALTY

6

Select Supplier CustomersBREAD &BREAD &BAKERYBAKERY

PRODUCEPRODUCE

JUICEJUICE

DAIRY &DAIRY &SNACKSSNACKS

CENTER CENTER STORESTORE

CONFECTIONCONFECTION

7

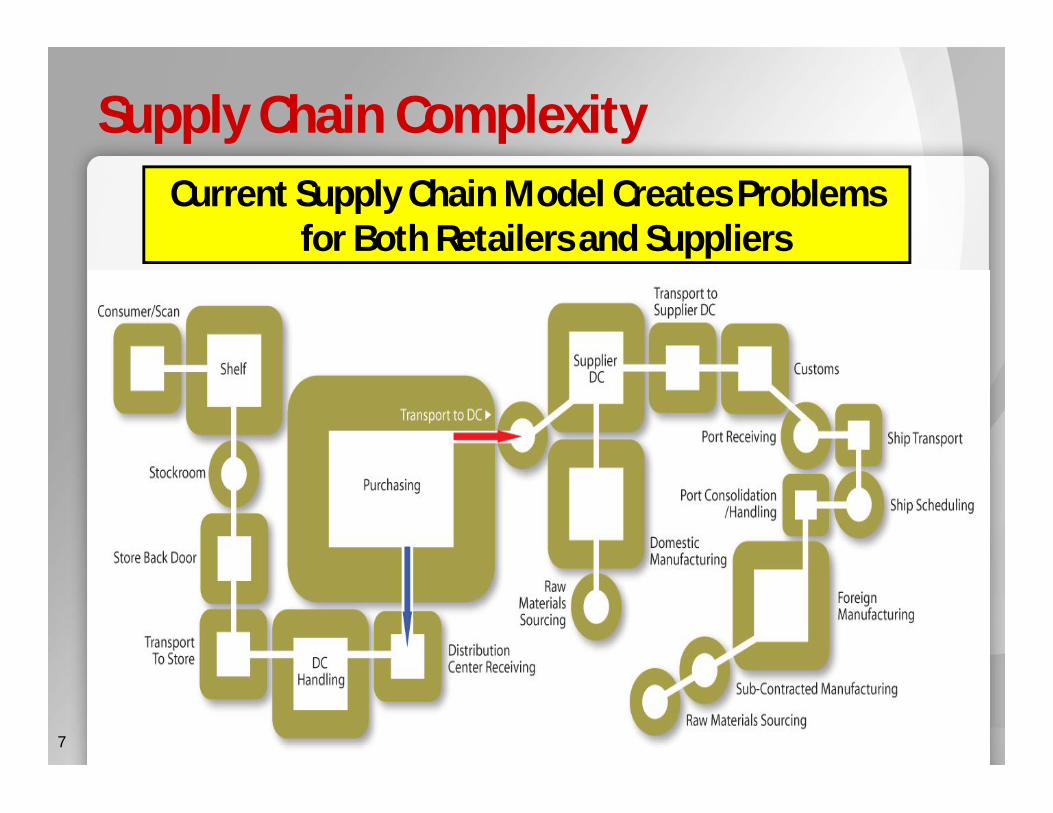

Supply Chain ComplexityCurrent Supply Chain Model Creates Problems

for Both Retailers and Suppliers

8

Retailer Concerns

Balance sheets are highly leveraged

Pressure to reduce inventory– Out-of-stocks

– Lost sales

– Reduced consumer loyalty

Consumer behavior is changing

Increasingly adversarial relationships with suppliers

Wal-Mart factor

9

Supplier Concerns

Sell to Retailers – not consumers– Paid at the retailer’s discretion

Increased private label penetration– Impacting shelf space allocation

– Reducing brand loyalty

Promotional spending effectiveness

Increasingly adversarial relationships with retailers

Supply chain visibility & complexity

10

Consumer Driven Sales OptimizationTM

Retailer and supplier data synchronization

Scan based trading

Visibility and analytics

Store level replenishment

Vendor managed inventory

Demand planning

Production planning

We Convert Information into CA$H!

Suite of Technology and Services That Tame the Supply Chain Beast

11

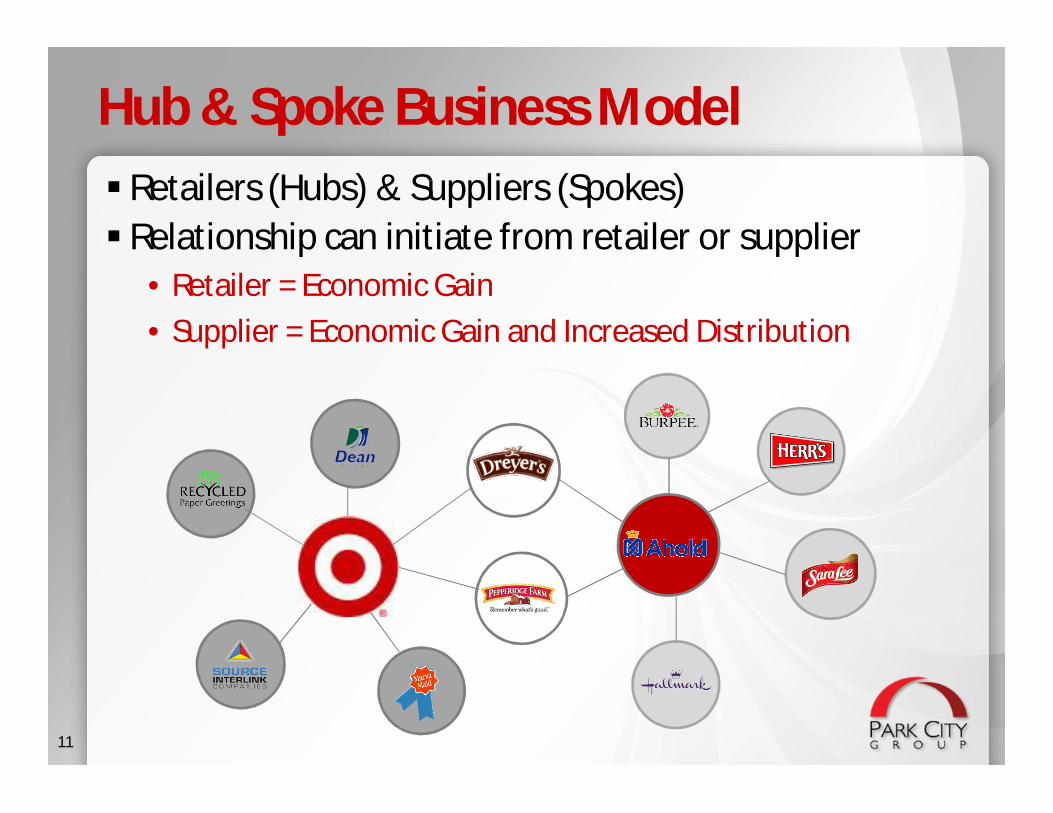

Retailers (Hubs) & Suppliers (Spokes) Relationship can initiate from retailer or supplier

• Retailer = Economic Gain• Supplier = Economic Gain and Increased Distribution

Hub & Spoke Business Model

12

Our Model

13

How The Retailer (Hub) Benefits

Increased Sales

Reduced Out-of-Stocks

Lower Inventories

Labor Savings

Improved Customer Experience

14

How The Supplier (Spoke) Benefits

Improved Sales

Reduced Financial Risk

Promotional Spending Efficiency

Reduced Slotting Fees

Better Demand and Production Planning

Provide Information Much like Wal-Mart

15

Benefits of Consumer Drives Sales Optimization

Area of Measure Impact*

Sales Increased 3% - 10%

Inventory Reduced 10% - 30%

Working Capital Decreased 10% - 15%

Shrink Reduced .2% - 2%

*Based on 15 years experience and hundreds of implementations

16

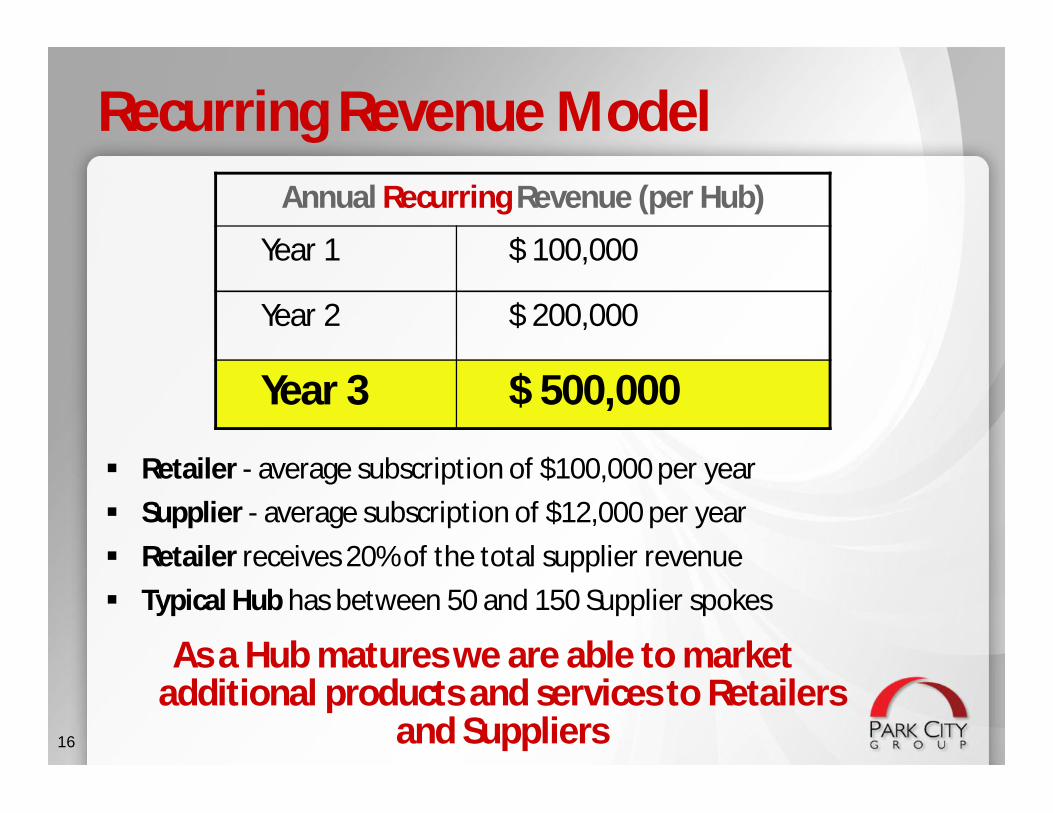

Recurring Revenue Model

Retailer - average subscription of $100,000 per year Supplier - average subscription of $12,000 per year Retailer receives 20% of the total supplier revenue Typical Hub has between 50 and 150 Supplier spokes

As a Hub matures we are able to market additional products and services to Retailers

and Suppliers

Annual Recurring Revenue (per Hub)

Year 1 $ 100,000

Year 2 $ 200,000

Year 3 $ 500,000

17

Basic Retailer & Supplier Matrix

18

Penetration of Additional Services Drives Exponential Revenue Growth

19

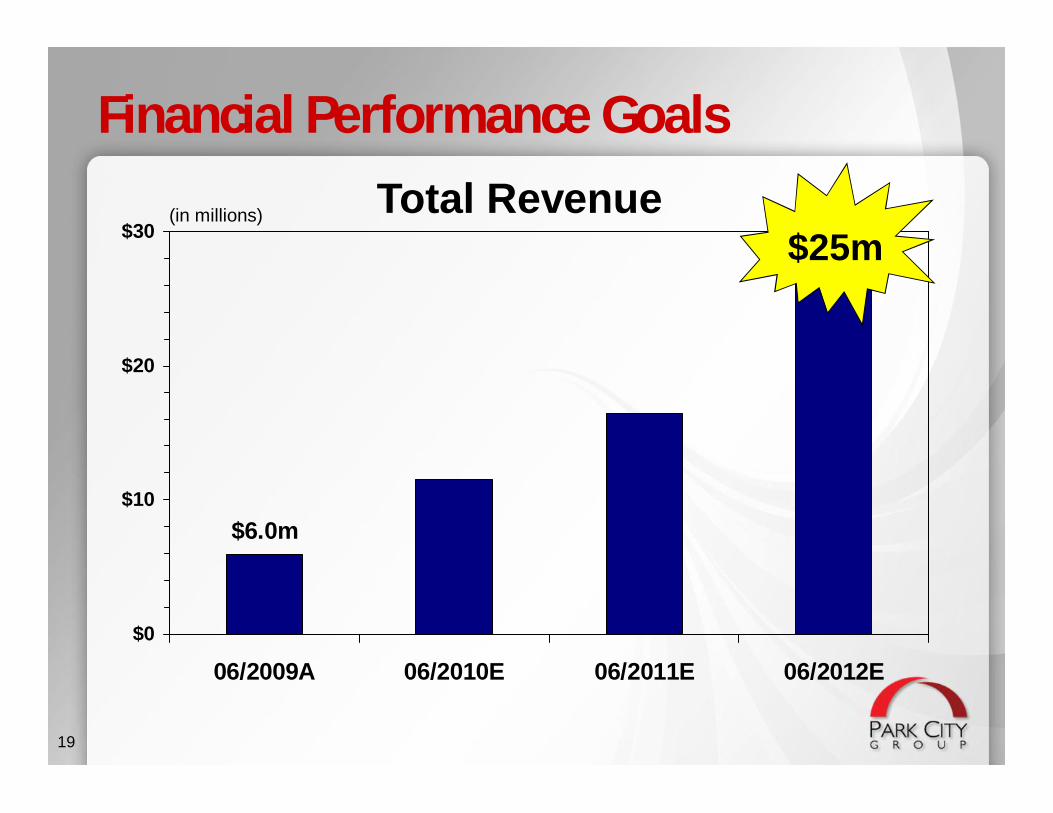

$6.0m

$0

$10

$20

$30

06/2009A 06/2010E 06/2011E 06/2012E

$25m(in millions) Total Revenue

Financial Performance Goals

20

$357,000$0

$5

$10

$15

$20

06/2009A 06/2010E 06/2011E 06/2012E

$13m

(1) Earnings before interest, taxes, depreciation and amortization

(2)

(2) On an adjusted pro-forma basis

(in millions)EBITDA(1)

Fiscal 2010 Will Be the Breakout Year

Financial Performance Goals

21

-$0.48

-$0.75

-$0.25

$0.25

$0.75

$1.25

06/2009A 06/2010E 06/2011E 06/2012E

$1.00Earnings Per Share

Financial Performance Goals

22

Patented, One-of-a-Kind Technology Platform

Market Credibility and Experience Through Our Founder, Randy Fields of Mrs. Fields Cookies

Superior Sales and Operational Management Team

Deep Consumer Packaged Goods and Retailer Experience

Access to Many Global C-Level Decision Makers

22

Summary: Our Competitive Advantage

23

Traditional Supply Chain Model

24

Our Model

25

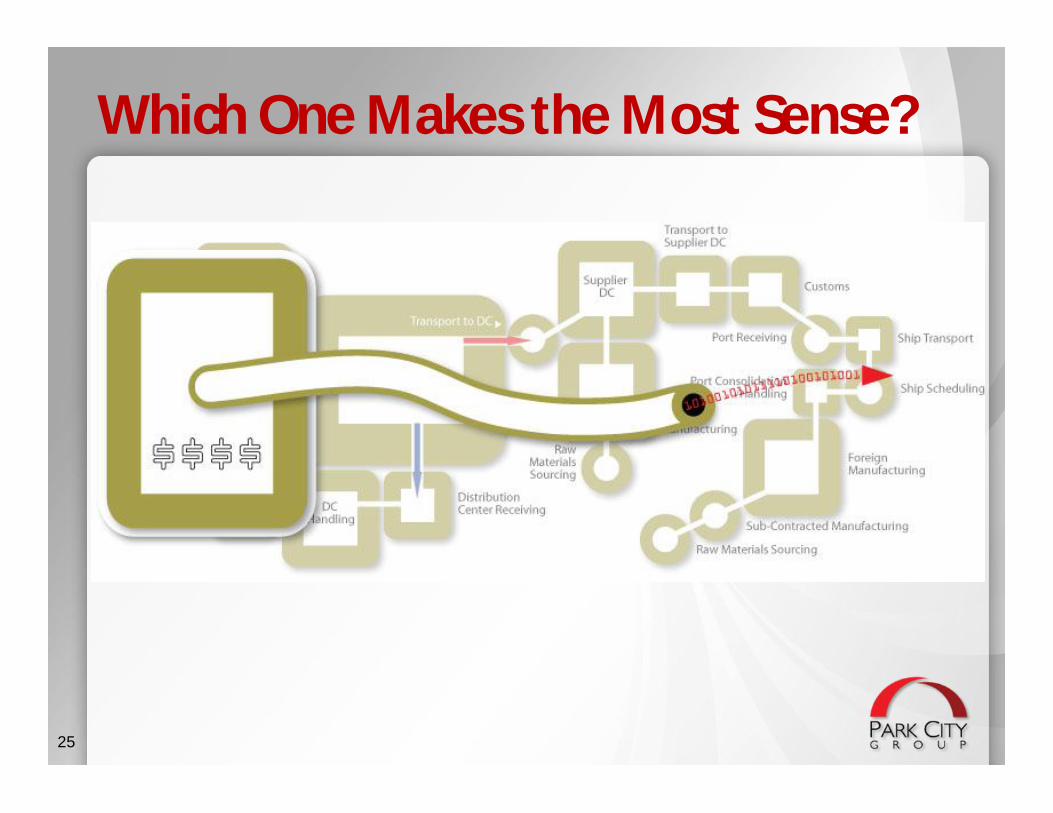

Which One Makes the Most Sense?

26

Forward-Looking StatementStatements in this presentation that relate to Park City Group's future plans, objectives,expectations, performance, events and the like are "forward-looking statements" within themeaning of the Private Securities Litigation Reform Act of 1995 and the Securities ExchangeAct of 1934. Future events, risks and uncertainties, individually or in the aggregate, couldcause actual results to differ materially from those expressed or implied in these statements.Those factors could include changes in economic conditions that may change demand for theCompany's products and services and other factors discussed in the "forward-lookinginformation" section and the "risk factor" section of the management's discussion andanalysis included in the Company's report on Form 10-K for the year ended June 30, 2009 orcurrent reports on Form 8-K filed with the Securities and Exchange Commission. Thispresentation is comprised of interrelated information that must be interpreted in the context ofall of the information provided and care should be exercised not to consider portions of thisrelease out of context. Park City Group uses paid services of investor relations organizationsto promote the Company to the investment community. Investments in any company shouldbe considered speculative and prior to acquisition, should be thoroughly researched. ParkCity Group does not intend to update these forward-looking statements prior toannouncement of quarterly or annual results.

Randy FieldsT: (435) 645-2100