investor presentation q2 13 - bmo 2013 investor presentation.pdfpcl 0.11 0.15 net income 1.0 1.0 eps...

TRANSCRIPT

Investor PresentationJune 6, 2013

Q2 13

2Investor Presentation | Q2 2013

Forward Looking Statements & Non-GAAP Measures

Caution Regarding Forward-Looking Statements

Bank of Montreal’s public communications often include written or oral forward-looking statements. Statements of this type are included in this document, and may be included in other filings with Canadian securities regulators or the U.S. Securities and Exchange Commission, or in other communications. All such statements are made pursuant to the “safe harbor” provisions of, and are intended to be forward-looking statements under, the United States Private Securities Litigation Reform Act of 1995 and any applicable Canadian securities legislation. Forward-looking statements may involve, but are not limited to, comments with respect to our objectives and priorities for 2013 and beyond, our strategies or future actions, our targets, expectations for our financial condition or share price, and the results of or outlook for our operations or for the Canadian and U.S. economies.

By their nature, forward-looking statements require us to make assumptions and are subject to inherent risks and uncertainties. There is significant risk that predictions, forecasts, conclusions or projections will not prove to be accurate, that our assumptions may not be correct and that actual results may differ materially from such predictions, forecasts, conclusions or projections. We caution readers of this document not to place undue reliance on our forward-looking statements as a number of factors could cause actual future results, conditions, actions or events to differ materially from the targets, expectations, estimates or intentions expressed in the forward-looking statements.

The future outcomes that relate to forward-looking statements may be influenced by many factors, including but not limited to: general economic and market conditions in the countries in which we operate; weak, volatile or illiquid capital and/or credit markets; interest rate and currency value fluctuations; changes in monetary, fiscal or economic policy; the degree of competition in the geographic and business areas in which we operate; changes in laws or in supervisory expectations or requirements, including capital, interest rate and liquidity requirements and guidance; judicial or regulatory proceedings; the accuracy and completeness of the information we obtain with respect to our customers and counterparties; our ability to execute our strategic plans and to complete and integrate acquisitions; critical accounting estimates and the effect of changes to accounting standards, rules and interpretations on these estimates; operational and infrastructure risks; changes to our credit ratings; general political conditions; global capital markets activities; the possible effects on our business of war or terrorist activities; disease or illness that affects local, national or international economies; natural disasters and disruptions to public infrastructure, such as transportation, communications, power or water supply; technological changes; and our ability to anticipate and effectively manage risks associated with all of the foregoing factors.

We caution that the foregoing list is not exhaustive of all possible factors. Other factors could adversely affect our results. For more information, please see the discussion below, which outlines in detail certain key factors that may affect Bank of Montreal’s future results. When relying on forward-looking statements to make decisions with respect to Bank of Montreal, investors and others should carefully consider these factors, as well as other uncertainties and potential events, and the inherent uncertainty of forward-looking statements. Bank of Montreal does not undertake to update any forward-looking statements, whether written or oral, that may be made from time to time by the organization or on its behalf, except as required by law. The forward-looking information contained in this document is presented for the purpose of assisting our shareholders in understanding our financial position as at and for the periods ended on the dates presented, as well as our strategic priorities and objectives, and may not be appropriate for other purposes.

Effective the first quarter of 2013, our regulatory capital, risk-weighted assets and regulatory capital ratios have been calculated pursuant to the Capital Adequacy Requirement (CAR) Guideline released by the Office of the Superintendent of Financial Institutions (OSFI) in December 2012 to implement the Basel III Accord in Canada. When calculating the pro-forma impact of Basel III on our regulatory capital (including capital deductions and qualifying and grandfathered ineligible capital), risk-weighted assets and regulatory capital ratios in prior periods, we assumed that our interpretation of OSFI’s draft implementation guideline of rules and amendments announced by the Basel Committee on Banking Supervision (BCBS), and our models used to assess those requirements, were consistent with the final requirements that would be promulgated by OSFI. We have not recalculated our pro-forma Basel III regulatory capital, risk-weighted assets or capital ratios based on the CAR Guideline and references to Basel III pro-forma items refer to these items as previously estimated.

Assumptions about the level of asset sales, expected asset sale prices, net funding cost, credit quality, risk of default and losses on default of the underlying assets of the structured investment vehicle were material factors we considered when establishing our expectations regarding the structured investment vehicle, including the adequacy of first-loss protection. Key assumptions included that assets will continue to be sold with a view to reducing the size of the structured investment vehicle, under various asset price scenarios, and that the level of default and losses will be consistent with the credit quality of the underlying assets and our current expectations regarding continuing difficult market conditions.

Assumptions about the level of default and losses on default were material factors we considered when establishing our expectations regarding the future performance of the transactions into which our credit protection vehicle has entered. Among the key assumptions were that the level of default and losses on default will be consistent with historical experience. Material factors that were taken into account when establishing our expectations regarding the future risk of credit losses in our credit protection vehicle and risk of loss to Bank of Montreal included industry diversification in the portfolio, initial credit quality by portfolio, the first-loss protection incorporated into the structure and the hedges into which Bank of Montreal has entered.

Assumptions about the performance of the Canadian and U.S. economies, as well as overall market conditions and their combined effect on our business, are material factors we consider when determining our strategic priorities, objectives and expectations for our business. In determining our expectations for economic growth, both broadly and in the financial services sector, we primarily consider historical economic data provided by the Canadian and U.S. governments and their agencies. See the Economic Review and Outlook section in Bank of Montreal’s Second Quarter 2013 Report to Shareholders.

Non-GAAP Measures

Bank of Montreal uses both GAAP and non-GAAP measures to assess performance. Readers are cautioned that earnings and other measures adjusted to a basis other than GAAP do not have standardized meanings under GAAP and are unlikely to be comparable to similar measures used by other companies. Reconciliations of GAAP to non-GAAP measures as well as the rationale for their use can be found in Bank of Montreal’s Second Quarter 2013 Report to Shareholders and Bank of Montreal’s 2012 Management’s Discussion and Analysis, all of which are available on our website at www.bmo.com/investorrelations.

Examples of non-GAAP amounts or measures include: efficiency and leverage ratios; revenue and other measures presented on a taxable equivalent basis (teb); amounts presented net of applicable taxes; adjusted net income, revenues, provision for credit losses, specific provision for credit losses, expenses, earnings per share, effective tax rate, ROE, efficiency ratio and other adjusted measures which exclude the impact of certain items such as credit-related items on the acquired M&I performing loans, run-off structured credit activities, M&I integration costs, amortization of acquisition-related intangibles, decrease (increase) in collective allowance for credit losses and restructuring costs.

Bank of Montreal provides supplemental information on combined business segments to facilitate comparisons to peers.

3Investor Presentation | Q2 2013

Other Information

Quarterly Dividend $0.74

Listings NYSE, TSX (Ticker: BMO)

Share Price (April 30, 2013)

TSX C$63.19

NYSE US$62.71

Market Cap (April 30, 2013) C$41 billion

Employees 46,580

Q2 13 Results (C$ billions) Adjusted2 Reported

Revenue 3.8 3.9

PCL 0.11 0.15

Net Income 1.0 1.0

EPS ($) 1.46 1.42

ROE (%) 14.5 14.2

Average Assets 555 555

Basel III Common Equity Tier 1 Ratio (%)3 9.7% 9.7%

BMO Financial Group8th largest bank in North America1; 2nd largest Canadian bank by retail branches in Canada and the U.S.

2 Adjusted measures are non-GAAP measures. See slides 2 and 33 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders

Who we areEstablished in 1817, BMO Financial Group is a highly diversified financial services provider based in North America. With total assets of $555 billion and 46,580 employees (as at April 30, 2013), BMO provides a broad range of retail banking, wealth management and investment banking products and services to more than 12 million customers. BMO Financial Group conducts business through three operating groups: Personal and Commercial Banking, Private Client Group and BMO Capital Markets.

3 OSFI’s decision to delay the effective date for the imposition of the Credit Valuation Adjustment (CVA) risk capital charge until January 2014 improved our CET1 ratio at April 30, 2013, by approximately 35 basis points.

1 As measured by assets as at April 30, 2013; ranking published by Bloomberg

4Investor Presentation | Q2 2013

Expand strategically in select global markets to create future growth

Strategic PrioritiesA Clear Vision: to be the bank that defines great customer experience

1

2

3

4

5

Achieve industry-leading customer loyalty by delivering on our brand promise

Enhance productivity to drive performance and shareholder value

Leverage our consolidated North American platform to deliver quality earnings growth

Ensure our strength in risk management underpins everything we do for our customers

5Investor Presentation | Q2 2013

Strategic FootprintBMO’s strategic footprint is anchored by our core business in the heartland of the continental economy

* BMO has retail banking branches across Canada and in the U.S. Midwest states of Illinois, Wisconsin, Indiana, Minnesota, Missouri and Kansas, as well as in Arizona and Florida

BMO facilitates financing, investmentand wholesale banking activitiesbetween our North American baseand strategically located offices in therapidly growing economies of Asia.

Our significant and long-establishedpresence throughout Canada and theU.S. includes regional economies fuelledby natural resources and agriculture.BMO’s deep connections and historicalpresence in the energy sector extendfrom the oilfields of Western Canadasouthward through to Texas.

Offices in four European countries anda regional representative office in theMiddle East provide us with a strongdistribution platform for our wholesalebanking activities as well as a presencein key markets for institutional assetmanagement and investment banking.

BMO’s enlarged continental footprint is centred in the vital Great Lakes economy that connects six key U.S. Midwest states and the two largest Canadian provinces.

6Investor Presentation | Q2 2013

BMO – A Strong FoundationWe have the business platform, balance sheet and expertise to generate quality growth

Diversified business mix with retail focus 78% of Q2 F2013 operating group revenue from retail businesses Commercial banking is a strength in Canada (#2 in lending) and the U.S. Top-tier deposit market share in key U.S. Midwest markets

Strong national presence in Canada, as well as strategic positioning in select high-growth U.S. and emerging wealth management markets

North American Capital Markets business operating as bulge bracket firm in Canada with mid-cap focus in the U.S.

Strong capital position Basel III Common Equity Tier 1 Ratio of 9.7%1 as at April 30th, 2013

Disciplined and balanced approach to capital management

Proactive risk management Independent risk oversight across the enterprise Disciplined credit risk management capabilities and processes

Commitment to stakeholders Quarterly dividend of $0.74; longest-running dividend payout record of any company in Canada at 184 years Clear brand promise that delivers real benefit for customers Sound corporate governance

1 OSFI’s decision to delay the effective date for the imposition of the Credit Valuation Adjustment (CVA) risk capital charge until January 2014 improved our CET1 ratio at April 30, 2013, by approximately 35 basis points

7Investor Presentation | Q2 2013

Economic Outlook

Canada

United States

Outlook as at May 31, 2013; Source: BMO Economics

The U.S. economy is growing moderately, with strength in housing markets and business investment and a pickup in consumer spending partly offset by government cutbacks

Aggressive fiscal restraint will keep economic growth moderate at 2.2% in 2013, though improved household finances and housing markets should support a stronger expansion in the second half of the year

The unemployment rate will likely decline slowly to 7.2% in late 2013

The Federal Reserve is expected to keep interest rates near zero until 2015

The U.S. dollar is expected to remain firm this year

The Canadian economy continues to grow at a modest pace, held back by the strong Canadian dollar, weak global demand, elevated household debt and fiscal consolidation, but supported by low interest rates

Modest GDP growth of 1.7% is expected in 2013, with strength in business investment and in the resource-producing provinces partly offset by weakness in consumer spending, government cutbacks and a moderation in housing markets

The unemployment rate is forecast to decline to 6.9% in late 2013

The Bank of Canada is expected to keep interest rates steady until the second half of 2014

The Canadian dollar should remain near parity against the U.S. dollar in 2013, supported by firm commodity prices and higher interest rates than in the U.S

8Investor Presentation | Q2 2013

Economic Indicators

Sources: BMO Economics, Haver Analytics1Annual average*Estimates as of May 31, 2013; Eurozone estimates provided by OECD

Canada United States Eurozone

Economic Indicators (%)1 2012 2013E 2014E 2012 2013E 2014E 2012 2013E 2014E

GDP Growth 1.7 1.7 2.3 2.2 2.2 3.2 -0.5 -0.7 0.7

Inflation 1.5 1.0 1.7 2.1 1.4 1.7 2.5 1.4 1.6

Interest Rate (3mth Tbills) 0.9 1.0 1.2 0.1 0.1 0.1 0.5 0.1 0.5

Unemployment Rate 7.3 7.0 6.7 8.1 7.4 6.7 11.4 12.0 11.3

Current Account Balance / GDP* (3.4) (2.9) (2.6) (3.0) (2.9) (2.8) 1.4 1.9 2.2

Budget Surplus / GDP* (1.4) (1.0) (0.3) (7.0) (4.0) (3.4) (3.3) (2.8) (2.6)

9Investor Presentation | Q2 2013

Operating Group Overview

Personal and Commercial Banking - Canada Over 7 million customers Over 900 branches and access to 2,680 automated banking machines

Expanded our branch network by opening or upgrading 27 locations and adding 84 ABMs YTD Strong personal lending growth1 in Q2’13 with balances up 10% Y/Y and 1.3% Q/Q Continued strong momentum in commercial lending with growth2 of 12% Y/Y and 4.6% Q/Q

#2 market share position in small and medium sized loans

Personal and Commercial Banking – U.S. Over 2 million customers Over 600 branches and access to 1,369 automated banking machines; headquartered in Chicago branch footprint spans across the

U.S. Midwest states of Illinois, Wisconsin, Indiana, Minnesota, Missouri and Kansas, as well as Arizona and Florida Strong core C&I loan growth up 17% Y/Y and 4% Q/Q, in Q2’13; 6th straight sequential quarter of growth

Private Client Group (PCG) Broad offering of wealth management products and solutions including Insurance products Full range of client segments from mainstream to ultra-high net worth, as well as select institutional markets Operates in Canada and the United States, as well as in China and the United Kingdom AUA / AUM $522B as at April 30, 2013

BMO Capital Markets (BMO CM) Provides a full range of products and services to help corporate, institutional and government clients achieve their ambitions Expertise in areas including equity and debt underwriting, corporate lending and project financing, mergers and acquisitions advisory

services, merchant banking, securitization, treasury and market risk management, foreign exchange, derivatives, debt and equity research and institutional sales and trading

29 locations around the world, including 16 in North America

Operating Group Overview

1 Personal lending includes mortgages and consumer loans but excludes credit cards. Personal Cards balances approximately 83% of total credit card portfolio in each of Q2’12, Q1’13 and Q2’132 Commercial lending growth excludes commercial credit cards. Commercial cards balances approximately 17% of total credit card portfolio in each of Q2’12, Q1’13 and Q2’13

10Investor Presentation | Q2 2013

Q2 2013 Financial Highlights

Adjusted1

Q2 12 Q1 13 Q2 13

Net Income (C$MM) 982 1,041 997

EPS ($) 1.44 1.52 1.46

ROE (%)2 15.4 14.8 14.5

Reported

Net Income (C$MM) 1,028 1,048 975

EPS ($) 1.51 1.53 1.42

Basel III Common Equity Tier 1 Ratio (%)3 7.6 9.4 9.7

Adjusted EPS of $1.46, up 1% Y/Y

Adjusted net income up 2% Y/Y

Strong Y/Y net income growth in PCG excluding Insurance, up 14% and BMO CM up 19%

Insurance results reduced by $34MM after-tax ($0.05/share) due to negative impact of lower long-term interest rates

P&C US net income up 3%

P&C Canada essentially unchanged

Continued good Y/Y growth in Commercial banking

In Canada, both loan and deposit balances up 12%

In U.S., core C&I loans up 17%

Adjusted provisions4 for credit losses of $110MM compared to $151MM a year ago

Adjusted ROE of 14.5% on strong capital position

In Q2’13 purchased 4MM shares under buyback program

Adjusted effective tax rate5 of 20.0% compared to 19.9% in Q1’13 and 19.5% in Q2’12

1 See slide 33 for adjustments to reported results2 Reported ROE: Q2’12 16.2%; Q1’13 14.9%; Q2’13 14.2% 3 Q2’13 Common Equity Tier 1 Ratio based on Basel III. Q2’12 based on pro forma Basel III4 Reported PCL $145MM, compared to $195MM a year ago5 Reported effective tax rate of 20.8%

Adjusted measures are non-GAAP measures. See slide 2 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders

11Investor Presentation | Q2 2013

P&C US730

PCG765

Trading Products

550Inv. & Corp

Banking 300

Canada -Personal

964

Canada -Commercial

568

Diversified Business Mix with Retail Focus78% of Q2 operating group adjusted revenue from retail businesses

PCG (Wealth

Management) 20%

P&C (Personal & Commercial)

58%

Q2 F2013 Adjusted Revenue by Operating Group (C$MM) - $3,877MM

P&C (Personal & Commercial)

59%

Q2 F2013 Adjusted Net Income by Operating Group (C$MM) -

$1,023MM

PCG (Wealth

Management) 14%

BMO CM (Investment Banking)

27%Excludes Corporate Services adjusted net loss of $26MM

Excludes Corporate Services adjusted revenue $(118)MM

Adjusted measures are non-GAAP measures. See slide 2 and 33 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders

BMO CM (Investment Banking)

22%

P&C Canada

431

P&C US 168

PCG 148

BMO CM 276

12Investor Presentation | Q2 2013

RevenueY/Y Revenue driven by good growth in PCG (excluding Insurance) and BMO CM

1,758 1,857 1,836

1,969 2,004 1,923

Q2'12 Q1'13 Q2'13

Y/Y adjusted revenue up 1%

NII down 2% as volume growth across all Groups, particularly commercial, was more than offset by lower NIM

NIR up 4% driven by PCG and BMO CM

Good growth in mutual funds

Higher trading revenues primarily due to increased revenue from interest rate activities

Q/Q adjusted revenue down 3%

NII down 4% due to fewer days and lower NIM

NIR down 1% reflecting lower underwriting, lending and advisory fees from high levels in Q1

Adjusted NIM of 164 bps, down 3bps Q/Q. Adjusted NIM (excluding trading) of 200 bps, down 3 bps Q/Q

Reported Revenue – Q2’12 $3,959MM; Q1’13 $4,081MM; Q2’13 $3,944MM, Reported NII – Q2’12 $2,120MM; Q1’13 $2,216MM Q2’13 $2,098MM, Reported NIR – Q2’12 $1,839MM; Q1’13 $1,865MM; Q2’13 $1,846MMReported NIM - 179 bps, down 6 bps Q/Q

Total Bank Adjusted1 Revenue (C$MM)

NIR

NII

3,727 3,861 3,759

1 Adjusted measures are non-GAAP measures. See slide 2 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders. See slide 33 for adjustments to reported results

13Investor Presentation | Q2 2013

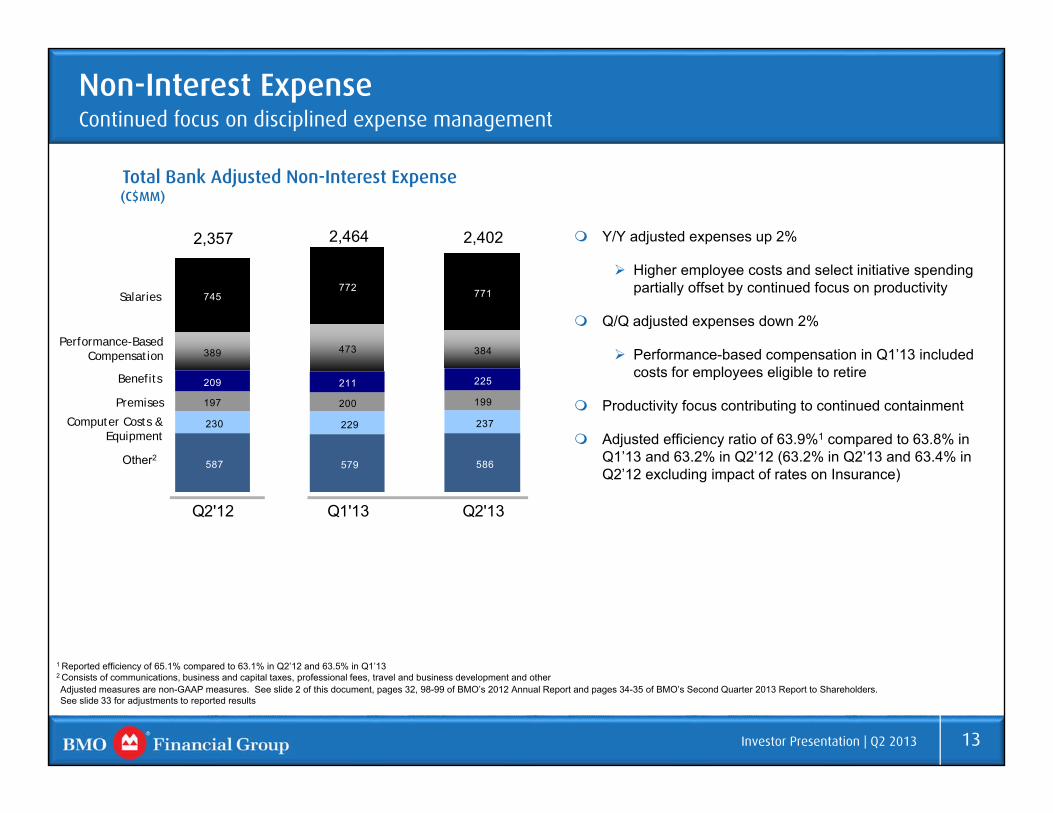

Non-Interest ExpenseContinued focus on disciplined expense management

587 579 586

230 229 237

197 200 199

209 211 225

389 473 384

745772 771

Q2'12 Q1'13 Q2'13

Y/Y adjusted expenses up 2%

Higher employee costs and select initiative spending partially offset by continued focus on productivity

Q/Q adjusted expenses down 2%

Performance-based compensation in Q1’13 included costs for employees eligible to retire

Productivity focus contributing to continued containment

Adjusted efficiency ratio of 63.9%1 compared to 63.8% in Q1’13 and 63.2% in Q2’12 (63.2% in Q2’13 and 63.4% in Q2’12 excluding impact of rates on Insurance)

2,357

Total Bank Adjusted Non-Interest Expense(C$MM)

Computer Costs & Equipment

Performance-Based Compensation

Benefits

Premises

Salaries

Other2

2,4022,464

1 Reported efficiency of 65.1% compared to 63.1% in Q2’12 and 63.5% in Q1’132 Consists of communications, business and capital taxes, professional fees, travel and business development and otherAdjusted measures are non-GAAP measures. See slide 2 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders. See slide 33 for adjustments to reported results

14Investor Presentation | Q2 2013

Capital & Risk Weighted AssetsCapital position is strong

Basel III Q1 13 Q2 13

Common Equity Tier 1 Ratio (CET1) (%)1 9.4 9.7

Tier 1 Capital Ratio (%) 11.1 11.3

Total Capital Ratio (%) 13.4 13.7

RWA ($B) 211 208

Assets to Capital Multiple2 16.1 16.3

Basel III CET1 Ratio is 9.7%, up from 9.4% at Q1’13

Basel III RWA decreased from last quarter due mainly to lower risk in certain portfolios and better risk assessments

Capital increased from last quarter due largely to retained earnings growth

4 million common shares were repurchased in Q2F2012

Common Shareholders’ Equity ($B)

F2013

1 OSFI’s decision to delay the effective date for the imposition of the Credit Valuation Adjustment (CVA) risk capital charge until January 2014 improved our CET1 ratio at April 30, 2013, by approximately 35 basis points 2 The Assets-to-Capital Multiple is calculated by dividing total assets, including specified off-balance sheet items, by total capital calculated on a transitional basis, as set out in OSFI's 2013 CAR Guideline.

15Investor Presentation | Q2 2013

436 462

444461

431

283 276 268 265 259

Q2 Q3 Q4 Q1 Q2

Q2 adjusted net income $431MM

Robust loan growth of $15B or 10% Y/Y and $3B or 2% Q/Q Personal loan growth 10% Y/Y and 1.3% Q/Q Commercial loan growth 12% Y/Y and 4.6% Q/Q

#2 market share1 position in small and medium sized loans Deposit growth of 7% Y/Y and 2% Q/Q

Personal deposit growth 4.0% Y/Y and 1.2% Q/Q Commercial deposit growth 12% Y/Y and 2.9% Q/Q

Expenses up 3% Y/Y due to continued business investment; efficiency ratio 51.9% Continue to manage core operating expenses tightly while re-tooling our

workforce Expanded branch network by opening or upgrading 18 locations across the

country in Q2’13 Increased front-line resources across a number of roles Focus on sales force productivity paying off Two technology projects underway:

Commercial Lending Redesign: to increase the front line capacity to sell while reducing operational costs

Credit Card enhancements, including a consistent and scalable North American credit card payments platform that supports future growth and enhancements

Strong top-tier customer loyalty scores are being translated into strong balance growth

Adjusted Net Income* and

Net Interest Margin

(1)%

Adjusted Net Income* ($MM)

Net Interest Margin (bps)

F2013F2012

Y/YGrowth

1 Business loan share (Banks) issued by CBA (one calendar quarter lag basis (Q1 F13: Dec 2012))* Adjusted measures are non-GAAP measures. See slide 2 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders.

See slide 33 for adjustments to reported results. Reported Net Income: Q2’12 $433MM; Q3’12 $459MM, Q4’12 $442MM; Q1’13 $458MM; Q2’13 $430MM

Personal & Commercial Banking CanadaFocused on growing high quality assets and attracting new customers

16Investor Presentation | Q2 2013

Personal & Commercial Banking U.S. Continued momentum in core Commercial and Industrial

Adjusted Net Income* and

Net Interest Margin

Adjusted net income $163MM, up 3% Y/Y; down from a very strong Q1

YTD adjusted earnings up 9%

Expenses down Y/Y and Q/Q primarily due to synergy related savings net of selective investments in the business In our Commercial business we have invested in growth opportunities by both

expanding our geographic footprint and adding to our capabilities in certain sectors Added loan offices in Omaha and Atlanta Expanded our Dealer Finance footprint to Washington DC and Ohio Added large Corporate and airplane expertise to our Equipment

Finance team Launched a new Franchise Finance specialty Expanded our ABL team

In our Personal business we have invested in additional personnel to capitalize on the growth in the mortgage sector and premier banking services

Adjusted efficiency ratio 59.6%1

Positive trend in total loan portfolio Strong commercial loan growth driven by continued momentum in core C&I

balances up 17% Y/Y and 4% Q/Q

Brand awareness has increased significantly for BMO Harris Bank across our footprint, with particularly strong gains in Indiana and Minnesota

3%158 153 156 197

163

439 442 430 421 417

Q2 Q3 Q4 Q1 Q2

Adjusted Net Income (US$MM)

Net Interest Margin (bps)

F2013F2012

Y/YGrowth

* Adjusted measures are non-GAAP measures. See slide 2 of this document, page 32, 98-99 of BMO’s 2012 Annual Report and page 34-35 of BMO’s Second Quarter 2013 Report to Shareholders. For details on adjustments refer to slide 33

1 Reported net income up 6% Y/Y, down 17% Q/Q; reported efficiency ratio of 62.2%. Reported net income (US): Q2’12 $143MM, Q3’12 $137MM, Q4’12 141MM, Q1’13 $183MM , Q2’13 $152MM

17Investor Presentation | Q2 2013

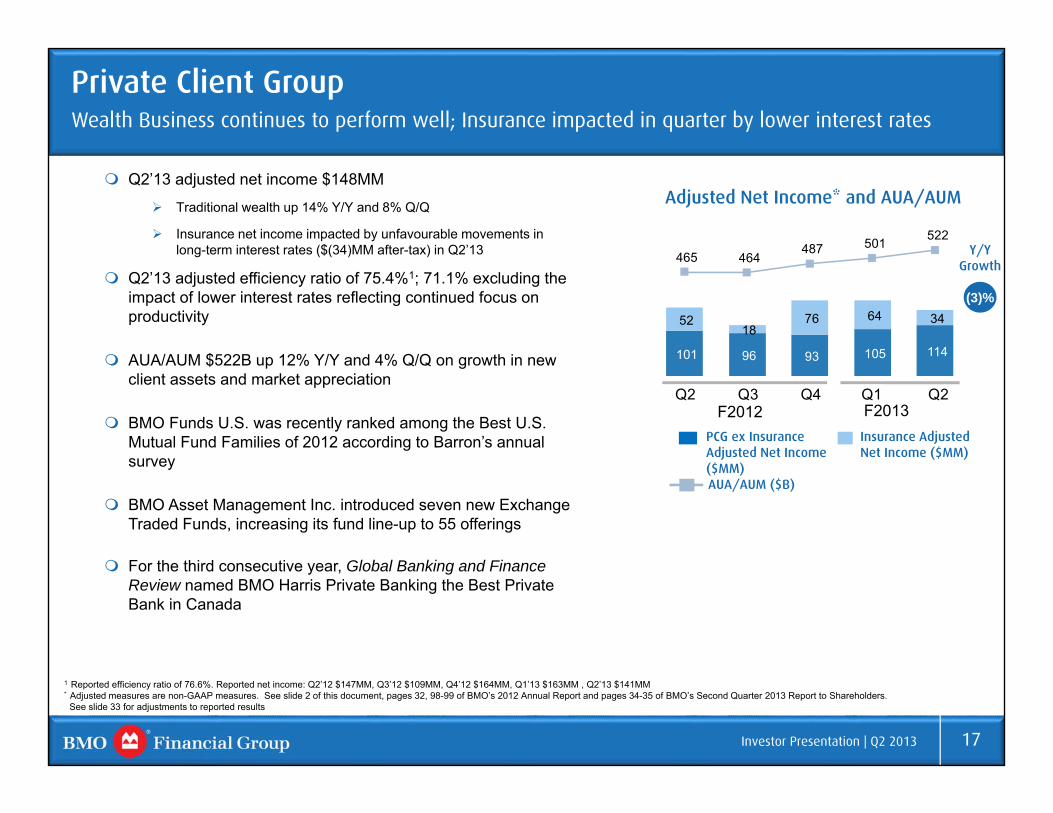

Private Client GroupWealth Business continues to perform well; Insurance impacted in quarter by lower interest rates

Adjusted Net Income* and AUA/AUM Q2’13 adjusted net income $148MM

Traditional wealth up 14% Y/Y and 8% Q/Q

Insurance net income impacted by unfavourable movements in long-term interest rates ($(34)MM after-tax) in Q2’13

Q2’13 adjusted efficiency ratio of 75.4%1; 71.1% excluding the impact of lower interest rates reflecting continued focus on productivity

AUA/AUM $522B up 12% Y/Y and 4% Q/Q on growth in new client assets and market appreciation

BMO Funds U.S. was recently ranked among the Best U.S. Mutual Fund Families of 2012 according to Barron’s annual survey

BMO Asset Management Inc. introduced seven new Exchange Traded Funds, increasing its fund line-up to 55 offerings

For the third consecutive year, Global Banking and Finance Review named BMO Harris Private Banking the Best Private Bank in Canada

(3)%

101 96 93 105 114

52 18

76 64 34

465 464 487 501 522

Q2 Q3 Q4 Q1 Q2

Insurance Adjusted Net Income ($MM)

PCG ex InsuranceAdjusted Net Income ($MM)

F2013F2012

AUA/AUM ($B)

Y/YGrowth

1 Reported efficiency ratio of 76.6%. Reported net income: Q2’12 $147MM, Q3’12 $109MM, Q4’12 $164MM, Q1’13 $163MM , Q2’13 $141MM* Adjusted measures are non-GAAP measures. See slide 2 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders.

See slide 33 for adjustments to reported results

18Investor Presentation | Q2 2013

BMO Capital MarketsAdjusted results up Y/Y and down Q/Q from a very strong Q1

Adjusted Net Income1 and Return on Equity

Q2’13 adjusted net income $276MM and ROE of 19.4%

Y/Y adjusted net income up 19%; down from a very strong Q1

Good Y/Y revenue growth driven by higher trading and corporate banking revenues

Net income from US operations increased to US$47MM; YTD earnings have doubled

Efficiency ratio of 59.3%

Strong market position and commitment to focusing on clients

BMO Capital Markets named Canada’s Best Investment Bank for the third time and World’s Best Metals and Mining Investment Bank for the fourth consecutive year by Global Finance

YTD, rank 1st in Equity Capital Markets in the Canadian League tables

BMO Capital Markets participated in 129 new issues in Q2’13

19%233 250

315 310 276

19.2 20.9

27.2

21.3 19.4

Q2 Q3 Q4 Q1 Q2

Adjusted Net Income ($MM)

Return on Equity (%)

F2013F2012

Y/YGrowth

1 Adjusted measures are non-GAAP measures. See slide 2 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders. See slide 33 for adjustments to reported results

19Investor Presentation | Q2 2013

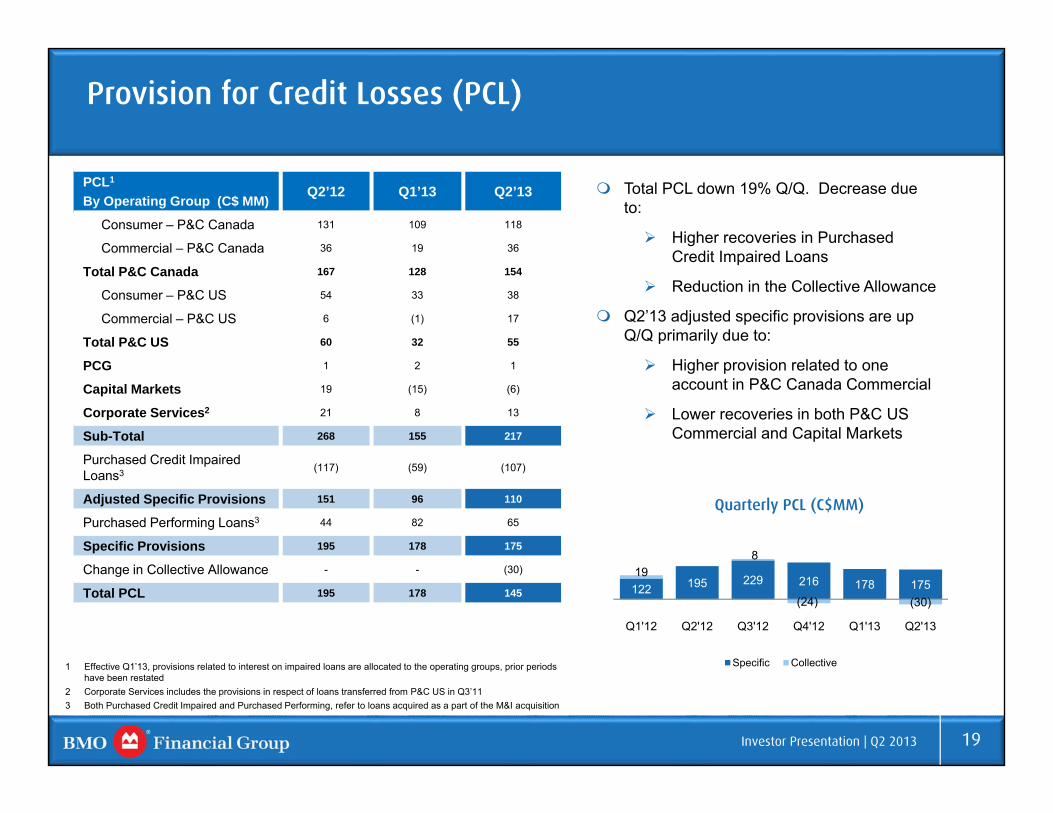

Provision for Credit Losses (PCL)

PCL1

By Operating Group (C$ MM) Q2’12 Q1’13 Q2’13

Consumer – P&C Canada 131 109 118

Commercial – P&C Canada 36 19 36

Total P&C Canada 167 128 154

Consumer – P&C US 54 33 38

Commercial – P&C US 6 (1) 17

Total P&C US 60 32 55

PCG 1 2 1

Capital Markets 19 (15) (6)

Corporate Services2 21 8 13

Sub-Total 268 155 217

Purchased Credit Impaired Loans3 (117) (59) (107)

Adjusted Specific Provisions 151 96 110

Purchased Performing Loans3 44 82 65

Specific Provisions 195 178 175

Change in Collective Allowance - - (30)

Total PCL 195 178 145 122 195 229 216 178 17519

8

(24) (30)

Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

Quarterly PCL (C$MM)

Specific Collective

Total PCL down 19% Q/Q. Decrease due to:

Higher recoveries in Purchased Credit Impaired Loans

Reduction in the Collective Allowance

Q2’13 adjusted specific provisions are up Q/Q primarily due to:

Higher provision related to one account in P&C Canada Commercial

Lower recoveries in both P&C US Commercial and Capital Markets

1 Effective Q1’13, provisions related to interest on impaired loans are allocated to the operating groups, prior periods have been restated

2 Corporate Services includes the provisions in respect of loans transferred from P&C US in Q3’113 Both Purchased Credit Impaired and Purchased Performing, refer to loans acquired as a part of the M&I acquisition

20Investor Presentation | Q2 2013

Liquidity and Funding Strategy

BMO’s Cash and Securities to Total Assets Ratio reflects a strong liquidity position

BMO’s large base of customer deposits, along with our strong capital base, reduces reliance on wholesale funding

* Core Deposits are comprised of customer operating and saving deposits and smaller fixed-date deposits (less than or equal to $100,000)

** Customer Deposits are core deposits plus large fixed-date deposits excluding wholesale customer deposits

Core and Customer Deposits ($B)Cash and Securities to Total Assets Ratio (%) (1)

(1) The decline in the ratio in 2011 from 2010 is the result of including securitized loans and mortgages previously reported off balance sheet under Canadian GAAP on balance sheet under IFRS

29.1%

31.9%

35.0%

29.5% 29.4%30.1%

Q4 2008 Q4 2009 Q4 2010 Q4 2011 Q4 2012 Q2 2013

125.4 125.3135.3

177.3190.7

202.4

145.3 147.9 152.9

194.4203.5

215.7

0

50

100

150

200

250

Q4 2008 Q4 2009 Q4 2010 Q4 2011 Q4 2012 Q2 2013

Core Deposits* Customer Deposits**

21Investor Presentation | Q2 2013

Diversified Wholesale Term Funding Mix

0

2

4

6

8

10

12

14

16

F2013 F2014 F2015 F2016 F2017 F2018 ≥ F2019

Mat

uriti

es C

DE

($B)

Term Debt Tier 1 Capital Tier 2 Capital Securitization

Wholesale Capital Market (1)

Term Funding Composition (Total $77.0B) As at April 30, 2013

Wholesale Capital Market (1)(2)

Term Funding Maturity Profile(Total $77.0B) As at April 30, 2013

BMO's wholesale funding principles seek to match the term of assets with the term of funding. Loans for example are funded with customer deposits and capital, with any difference provided by longer-term wholesale funding

BMO has a well diversified wholesale funding platform across markets, products, terms, currencies and maturities

Credit Ratings

Moody’s S&P Fitch DBRS

Aa3 A+ AA- AA

(1) Wholesale capital market term funding includes non-structured funding for terms greater than or equal to two years.(2) Securitization includes Covered Bond maturities.

Covered Bonds10%

C$ Mortgage & C$ and US$ Credit Card Securitization

32%

C$ Senior Debt24%

Senior Debt (Global Issuance)

22%

Tier 1 Capital5%

Tier 2 Capital7%

22Investor Presentation | Q2 2013

Corporate Governance

Comprehensive code of business conduct and ethics, FirstPrinciples,guides conduct and ethical decision-making by our directors, officers and employees

Governance practices reflect emerging best practices and BMO meets or exceeds legal, regulatory, TSX and NYSE requirements

We have share ownership requirements to ensure directors’ and executives’ compensation is aligned with shareholder interests

The Globe and Mail’s Board Games 2012 annual review of corporate governance practices in Canada ranked BMO 7th overall among 244 Canadian reporting issuers

23Investor Presentation | Q2 2013

Sustainability at BMO

We view Sustainability as creating value for our shareholders while acting in the long-term interest of our various stakeholders and have programs and commitments in place to achieve this.

We are transparent about our progress. Our recently published 2012 Environmental, Social and Governance (ESG) Report provides details on how we are managing the ESG impacts of our business while creating value for our customers, investors, the economy and society.

We are innovative in our approach to ESG reporting. Our ESG scorecard, found in the report, contains year over year metrics for the items most important to our stakeholders

• a talented and diverse workforce, • community investment, • board diversity, • ethical conduct and; • consideration for the environment.

We are recognized for our efforts by inclusion in investor based indices:

24Investor Presentation | Q2 2013

Reasons to invest in BMOWell positioned to leverage our North American platform and deliver sustained earnings growth

R

Proven strength in commercial banking across our large North American platform

Operating leverage from our expanded U.S. platform

Strong capital position

Advantaged business mix in the current environment

Enhancing productivity to drive performance

Focused on generating revenue growth by achieving industry-leading customer experience and loyalty

25Investor Presentation | Q2 2013

APPENDIX

26Investor Presentation | Q2 2013

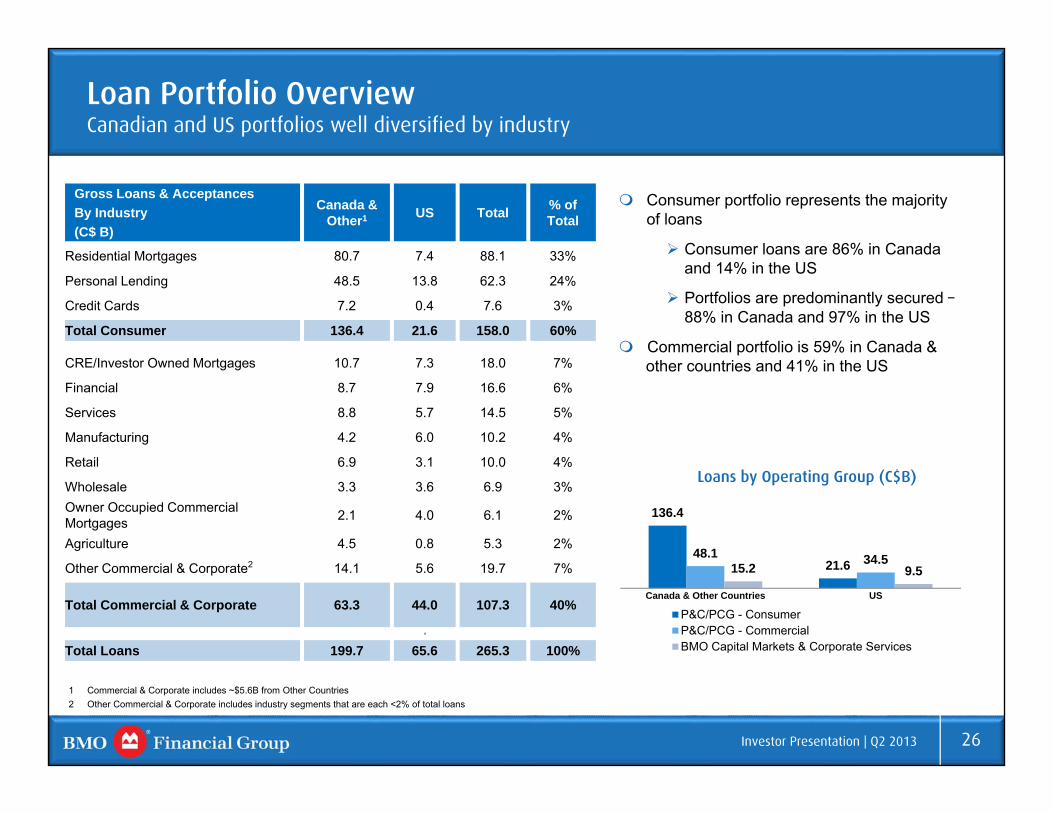

Loan Portfolio OverviewCanadian and US portfolios well diversified by industry

Consumer portfolio represents the majority of loans

Consumer loans are 86% in Canada and 14% in the US

Portfolios are predominantly secured –88% in Canada and 97% in the US

Commercial portfolio is 59% in Canada & other countries and 41% in the US

Gross Loans & Acceptances By Industry(C$ B)

Canada & Other1 US Total % of

Total

Residential Mortgages 80.7 7.4 88.1 33%

Personal Lending 48.5 13.8 62.3 24%

Credit Cards 7.2 0.4 7.6 3%

Total Consumer 136.4 21.6 158.0 60%

CRE/Investor Owned Mortgages 10.7 7.3 18.0 7%

Financial 8.7 7.9 16.6 6%

Services 8.8 5.7 14.5 5%

Manufacturing 4.2 6.0 10.2 4%

Retail 6.9 3.1 10.0 4%

Wholesale 3.3 3.6 6.9 3%Owner Occupied Commercial Mortgages 2.1 4.0 6.1 2%

Agriculture 4.5 0.8 5.3 2%

Other Commercial & Corporate2 14.1 5.6 19.7 7%

Total Commercial & Corporate 63.3 44.0 107.3 40%

.8

Total Loans 199.7 65.6 265.3 100%

1 Commercial & Corporate includes ~$5.6B from Other Countries2 Other Commercial & Corporate includes industry segments that are each <2% of total loans

136.4

21.648.1 34.5

15.2 9.5

Canada & Other Countries US

Loans by Operating Group (C$B)

P&C/PCG - ConsumerP&C/PCG - CommercialBMO Capital Markets & Corporate Services

27Investor Presentation | Q2 2013

Personal & Commercial Banking Canada – Loan Balances

39.2 41.7 43.7

8.9 8.9 8.6

41.3 43.0 43.1

67.275.0 76.4

Q2'12 Q1'13 Q2'13

156.6 168.6 171.8

Average Loans & Acceptances1

(C$B)

1 Column totals may not equal sum of the components due to rounding 2 Personal lending includes mortgages and consumer loans but excludes credit cards. Personal Cards balances approximately 83% of total credit card portfolio in each of Q2’12, Q1’13 and Q2’13

10%

Y/Y Growth

Residential MortgagesConsumer Loans

Credit CardsCommercial Loans & Acceptances

Personal

Strong lending growth2 with balances up 10.0% Y/Y and 1.3% Q/Q

Mortgage balances up 13.7% Y/Y. Balances up 1.9% Q/Q reflecting softer market

Total personal lending2 market share3 up 5 bps Q/Q despite impact from a recent acquisition by a competitor

Commercial

Continued strong momentum in commercial lending with growth4 of 12% Y/Y and 4.6% Q/Q.

Strong Commercial pipeline

#2 market share5 position in small and medium sized loans

3 Personal share issued by OSFI (one month lag basis (Q2 F13: Mar 2013)) ; Market share data sources: Consumer Loans and Residential Mortgages – OSFI4 Commercial lending growth excludes commercial credit cards. Commercial cards balances approximately 17% of total credit card portfolio in each of Q2’12, Q1’13 and Q2’135 Business loan share (Banks) issued by CBA (one calendar quarter lag basis (Q1 F13: Dec 2012))

28Investor Presentation | Q2 2013

Personal & Commercial Banking Canada – Deposit Balances

Average Deposits1

(C$B)

104.7109.9 111.8 7%

Y/Y Growth

Commercial DepositsPersonal Deposits

Personal

Deposit balances up 4.0% Y/Y and 1.2% Q/Q

Strong Y/Y growth of 9.0% in retail operating deposits

Commercial

Strong momentum in commercial deposit growth, up 12% Y/Y and 2.9% Q/Q

Commercial deposit market share2 up 43 bps Q/Q

Strategy to grow commercial deposits performing well

1 Column totals may not equal the sum of the components due to rounding 2 Business deposit share (Banks) issued by CBA (one calendar quarter lag basis (Q1 F13: Dec 2012))

29Investor Presentation | Q2 2013

Personal & Commercial Banking U.S. – Commercial Balances

18.8 19.1 19.9 21.3 22.1

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Core C&I ($B) - Average

All amounts in U.S. $B

Strong core C&I loan growth up 17% Y/Y, with Q2’13 being the 6th straight sequential quarter of growth

Growth in core C&I reflects increases across a number of businesses including Diversified Industries, Dealer Finance, Equipment Finance, Financial Institutions and Food and Consumer

Strong growth in the pipeline during the quarter

CRE fundamentals and valuations continue to recover; adding to pipeline and commitments at a moderate pace in a competitive environment

Deposits declined slightly Q/Q, but increased $2B or 11% Y/Y

3.0 3.0 2.9 2.9 2.9

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Core Commercial Real Estate ($B) - Average

3.4 3.1 2.7 2.4 2.1

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Run-off Loans ($B) - Average

17.7 17.7 18.7 19.9 19.7

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Commercial Deposits ($B) - Average

30Investor Presentation | Q2 2013

Personal & Commercial Banking U.S. – Personal Balances

6.6 6.4 6.3 6.0 5.8

4.0 4.1 4.2 4.3 4.5

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Mortgages ($B) - AverageMortgages Serviced Mortgage

5.0 5.2 5.4 5.6 5.8

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Indirect Auto ($B) - Average

All amounts in U.S. $B

5.8 5.7 5.6 5.6 5.5

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Home Equity ($B) - Average

5.5 5.4 5.3 5.1 5.0

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Business Banking / Small Business Loans ($B) -Average

4.2 3.9 3.7 3.7 3.6

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Other Loans ($B) - Average

41.5 41.3 40.6 39.9 39.9

Q2 12 Q3 12 Q4 12 Q1 13 Q2 13

Personal Deposits ($B) - Average

Mortgage portfolio declined as new originations of long term fixed rate loans are largely sold into the secondary market. Serviced portfolio is up 12% Y/Y and 3% Q/Q

Home Equity portfolio continues to reflect consumer deleveraging

Indirect Auto portfolio continues to grow. New originations increased 15% Y/Y and 5% Q/Q

Business Banking environment remains cautious for new borrowings. Increased emphasis on calling activities is driving an increase in pipeline

Deposit balances remained stable Q/Q and declined Y/Y as continued growth of core checking and savings balances partially offset by planned reductions in money market and higher cost CD portfolios

Other loans include non-strategic portfolios such as wholesale mortgages, purchased home equity, and certain small business CRE, as well as credit card balances and other personal loans

31Investor Presentation | Q2 2013

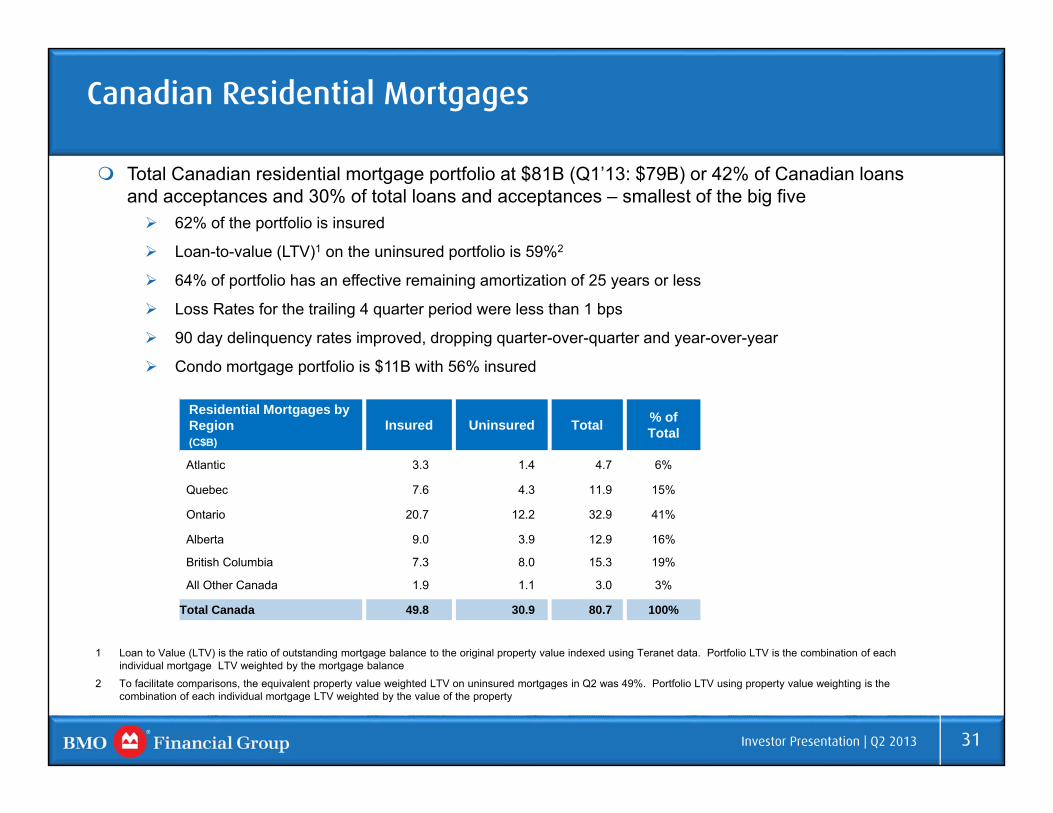

Canadian Residential Mortgages

Total Canadian residential mortgage portfolio at $81B (Q1’13: $79B) or 42% of Canadian loans and acceptances and 30% of total loans and acceptances – smallest of the big five 62% of the portfolio is insured

Loan-to-value (LTV)1 on the uninsured portfolio is 59%2

64% of portfolio has an effective remaining amortization of 25 years or less

Loss Rates for the trailing 4 quarter period were less than 1 bps

90 day delinquency rates improved, dropping quarter-over-quarter and year-over-year

Condo mortgage portfolio is $11B with 56% insured

Residential Mortgages by Region (C$B)

Insured Uninsured Total % of Total

Atlantic 3.3 1.4 4.7 6%

Quebec 7.6 4.3 11.9 15%

Ontario 20.7 12.2 32.9 41%

Alberta 9.0 3.9 12.9 16%

British Columbia 7.3 8.0 15.3 19%

All Other Canada 1.9 1.1 3.0 3%

Total Canada 49.8 30.9 80.7 100%

1 Loan to Value (LTV) is the ratio of outstanding mortgage balance to the original property value indexed using Teranet data. Portfolio LTV is the combination of each individual mortgage LTV weighted by the mortgage balance

2 To facilitate comparisons, the equivalent property value weighted LTV on uninsured mortgages in Q2 was 49%. Portfolio LTV using property value weighting is the combination of each individual mortgage LTV weighted by the value of the property

32Investor Presentation | Q2 2013

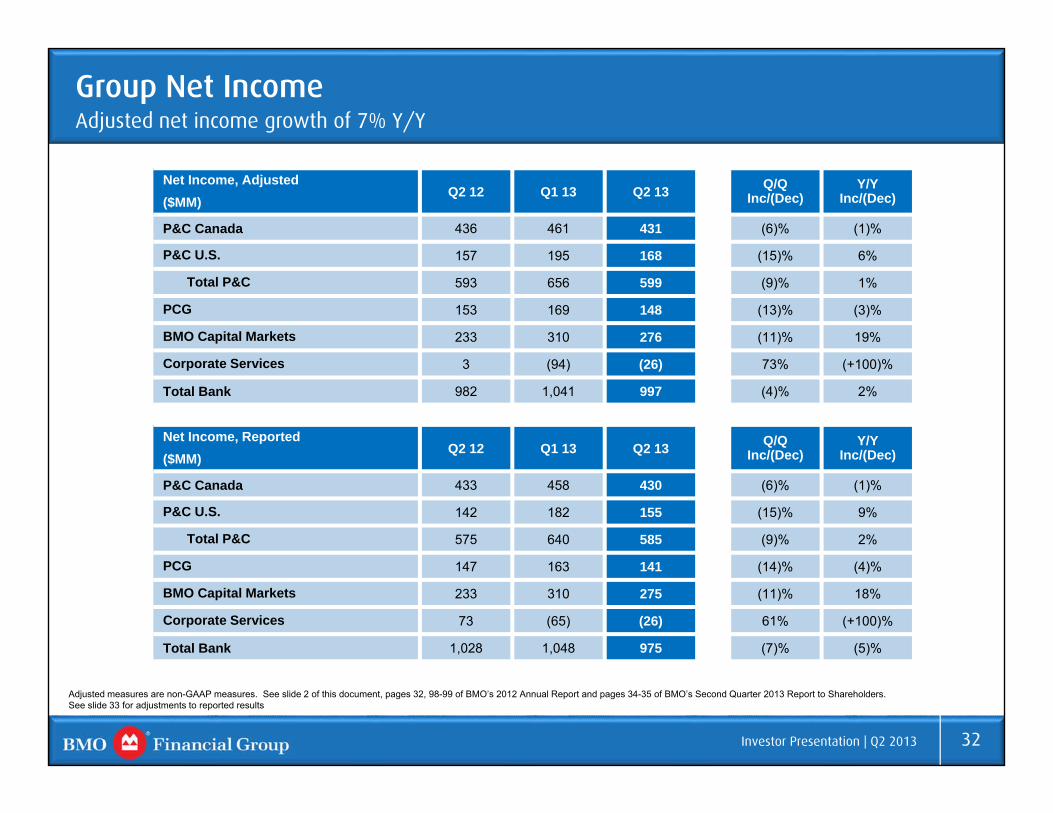

Net Income, Adjusted($MM)

Q2 12 Q1 13 Q2 13 Q/Q Inc/(Dec)

Y/Y Inc/(Dec)

P&C Canada 436 461 431 (6)% (1)%

P&C U.S. 157 195 168 (15)% 6%

Total P&C 593 656 599 (9)% 1%

PCG 153 169 148 (13)% (3)%

BMO Capital Markets 233 310 276 (11)% 19%

Corporate Services 3 (94) (26) 73% (+100)%

Total Bank 982 1,041 997 (4)% 2%

Net Income, Reported($MM)

Q2 12 Q1 13 Q2 13 Q/Q Inc/(Dec)

Y/Y Inc/(Dec)

P&C Canada 433 458 430 (6)% (1)%

P&C U.S. 142 182 155 (15)% 9%

Total P&C 575 640 585 (9)% 2%

PCG 147 163 141 (14)% (4)%

BMO Capital Markets 233 310 275 (11)% 18%

Corporate Services 73 (65) (26) 61% (+100)%

Total Bank 1,028 1,048 975 (7)% (5)%

Group Net IncomeAdjusted net income growth of 7% Y/Y

Adjusted measures are non-GAAP measures. See slide 2 of this document, pages 32, 98-99 of BMO’s 2012 Annual Report and pages 34-35 of BMO’s Second Quarter 2013 Report to Shareholders.See slide 33 for adjustments to reported results

33Investor Presentation | Q2 2013

Adjusting Items

Adjusting1 items – Pre-tax ($MM) Q2 12 Q1 13 Q2 13

Credit-related items on the M&I purchased performing loan portfolio 90 128 119

M&I integration costs (74) (92) (50)

Amortization of acquisition-related intangible assets (33) (31) (31)

Decrease/(increase) in the collective allowance for credit losses 18 - 22

Run-off structured credit activities 76 7 6

Restructuring costs (31) - (82)

Adjusting items included in reported pre-tax income 46 12 (16)

Adjusting1 items – After-tax ($MM) Q2 12 Q1 13 Q2 13

Credit-related items on the M&I purchased performing loan portfolio 55 79 73

M&I integration costs (47) (57) (31)

Amortization of acquisition-related intangible assets (24) (22) (22)

Decrease/(increase) in the collective allowance for credit losses 12 - 11

Run-off structured credit activities 73 7 6

Restructuring costs (23) - (59)

Adjusting items included in reported after-tax net income 46 7 (22)

EPS ($) 0.07 0.01 (0.04)

1 All adjusting items are reflected in Corporate Services with the exception of the amortization of acquisition-related intangible assets, which is reflected across the Operating Groups

Investor Relations Contact Information

E-mail: [email protected]

www.bmo.com/investorrelations

Fax: 416.867.3367

ANDREW CHINDirector, Investor [email protected]

SHARON HAWARD-LAIRDHead, Investor [email protected]