investor presentations2.q4cdn.com/.../2015/neff-q2-2015-investor-presentation-v08032015... · q2...

TRANSCRIPT

Q2 2015 Investor Presentation

2

Legal Disclaimer This presentation contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. All statements contained in this presentation that do not relate to matters of historical facts should be considered forward-looking statements, including statements regarding our expectations regarding growth of our end-markets; projected U.S. construction growth rate and spending and projected U.S. rental industry revenue growth rate; estimated exposure to oil and gas; our business strategy, including our plan to identify new customers, equipment demand opportunities, greenfield opportunities, and investment and divestiture opportunities; our 2015 outlook, including without limitation, statements regarding our forecasted revenue, Adjusted EBITDA, our expected rental rates, time utilization and net capital expenditures; and guidance regarding our 2016 target leverage ratio. We use words such as "will," "expect," "believe," "continue," "estimate," "intend," "target" and other similar expressions to identify some but not all forward-looking statements. Forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in the forward-looking statements. The forward-looking statements contained in this presentation are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other important factors we believe are appropriate under the circumstances. As you read and consider this presentation, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (many of which are beyond our control) and assumptions. Although we believe that these forward-looking statements are based on reasonable assumptions, you should be aware that many important factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance anticipated in the forward-looking statements. We believe these important factors include, but are not limited to, the important factors described under the captions "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" in the Company's annual report on Form 10-K for the fiscal year ended December 31, 2014 filed with the Securities and Exchange Commission ("SEC") on March 13, 2015 and similar disclosures in subsequent reports filed with the SEC, which could cause actual results to differ materially from those indicated by the forward-looking statements made in this presentation. Should one or more of these risks or uncertainties materialize, or should any of these assumptions prove incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this presentation to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances. New important factors that could cause our business not to develop as we expect emerge from time to time, and it is not possible for us to predict all of them. In addition to the financial measures prepared in accordance with U.S. generally accepted accounting principles (“US GAAP”), this presentation contains the non-US GAAP financial measures EBITDA and Adjusted EBITDA. The reasons for the use of these measures, a reconciliation of these measures to the most directly comparable US GAAP measures and other information relating to these measures are included in the appendix to this presentation.

Graham Hood Chief Executive Officer

Company At a Glance

4

Leading Regional Rental Equipment Provider

Sunbelt Region Focus area

+14,400 (1)

Customers served

Differentiated Emphasis on Earthmoving Equipment

~$775 million (2)

Original Equipment Cost (“OEC”) ~54% (2)

Of OEC focused on earthmoving category

Well Positioned in Key End-Markets

Key End-Markets Infrastructure, Non-Residential

Construction, Municipal, Oil & Gas and Residential Construction

~6% (3)

Expected weighted average CAGR of key end-markets through 2018

Compelling Financial Performance

~25% (4)

Adjusted EBITDA CAGR from 2011 to June 30, 2015

~50% (4) Adjusted EBITDA margin

Proven Management Team with Deep Roots in Rental

>1,070 full-time employees (2)

Located in 64 branches and the Company headquarters

~17 years Average tenure Regional VP’s have with

Neff Rental

Notes: (1) Company data for the last twelve months ending June 30, 2015 (2) As of June 30, 2015 (3) Includes infrastructure, non-residential construction, oil and gas, municipal and residential construction end-markets (4) For a reconciliation of net income to Adjusted EBITDA, see page 17

Business Strategy

5

Focus on Premium Customer Service

Continue to deliver best-in-class service and support to our long-standing customer base

Remain focused on our technical edge with respect to earthmoving equipment

Rigorous use of CRM and national account program to further penetrate our current customer base and identify new customer opportunities

Emphasis on Active Asset Management

Focus on Growing Markets

Capitalize on Operating Leverage

Ability to Generate Free Cash Flow

Remain committed to our focused position in the Sunbelt region of the United States

Continue to exploit and develop opportunities in the infrastructure, non-residential construction, residential construction, and oil and gas end markets

Maintain operational flexibility to generate significant cash flow through all types of business cycles

Rely on disciplined growth strategy to make feet investments that meet our stringent return criteria

Utilize real time data to improve rental rates and identify equipment demand opportunities

Maintain rigorous repair and maintenance program to increase time utilization and equipment longevity

Disciplined fleet investment and divestiture strategy driven by ROIC benchmarks and real time market dynamics

Remain committed to our focused position in the Sunbelt region of the United States

Continue to exploit and develop opportunities in the infrastructure, non-residential construction, oil and gas, municipal and residential construction end-markets

Take advantage of our current branch network and clustering strategy to add incremental fleet to our current footprint

Identify and evaluate one to three greenfield opportunities that meet our stringent return criteria and fit well within our current branch network. Announced opening of new Baltimore branch in January 2015.

Maintain operational flexibility to generate significant cash flow through various business cycles

Rely on our disciplined growth strategy and fleet investment criteria to make capital investment decisions

Divest fleet when deemed appropriate and when secondary equipment market demand is robust

Utilize real time data to improve rental rates and identify equipment demand opportunities

Maintain rigorous repair and maintenance program to increase time utilization and equipment longevity

Disciplined fleet investment and divestiture strategy driven by ROI benchmarks and real time market demand dynamics

6

632 689 745

803 840 848 891 991

1,104 1,167 1,152

1,068

903 806 788

861 911 960 1,012

1,072 1,138

1,218 1,304

17 18 22 24 25 25 26 28 31 35 37 36 28 27 29 31 33 36 38 41 44 48 51

$10

$30

$50

$70

$90

$500

$750

$1,000

$1,250

$1,500

1997A 1999A 2001A 2003A 2005A 2007A 2009A 2011A 2013A 2015E 2017E 2019E

Total U.S. Construction Spending U.S. Rental Industry Revenues

U.S. Construction Spending vs. U.S. Rental Industry Revenues Total U.S. Construction Spending $Bn

U.S. Rental Industry Revenues $Bn

Notes: (1) Architectural Billings Index (“ABI”) data as of June 2015 (2) 1997–2019 FMI Construction Outlook as of Q2 2015 (3) 1997–2019 Total U.S. Rental Market Revenue data from IHS Global Insights report as of July 2015

U.S. Equipment Rental Market Overview

ABI in Perspective (1)

30

40

50

60

70

Jun-97 Jun-00 Jun-03 Jun-06 Jun-09 Jun-12 Jun-15

Control expenses and conserve capital

Access to the right equipment for the job

24/7 Customer care

Eliminate the need for long-term maintenance

Minimize need for storage and transportation

Technical expertise and advice is available

Why Our Customers Choose to Rent vs. Own

Expansion Contraction

Expansion Expansion

Pent-up Demand

(2) (3)

7

Diversified Footprint and End-Markets

Sunbelt Region Overview

Key attributes of the Sunbelt region include:

Favorable climate conditions limit seasonality and facilitate year-round construction activity

Historically, higher than average equipment rental revenue growth rates when compared to other states outside of the Sunbelt region (3)

Forecasted U.S total construction growth rate for 2015 is 5.4%. Growth in Construction for states with Neff branch locations is estimated at 8.0% in 2015, which far exceeds the 2.5% estimated growth in Construction in States where Neff does not operate(4)

Branch proximity within the region allows Neff to deploy equipment seamlessly across different areas to drive rate and ROI Notes: (1) Forecasted 2015 Total U.S. Rental Industry Revenue growth rate data from IHS Global Insights report as of July 2015 (2) Company data for Q2 2015 (3) 1997–2014 Total U.S. Rental Industry Revenue data from IHS Global Insights report as of July 2015 (4) Forecasted 2015 Total Construction Industry growth rate data from IHS Global Insights data report as of June 2015

Neff Regions and Forecast Rental Industry Growth Rates (1) Rental Revenues by End-Market (2)

Infrastructure 28%

Non-Residential Construction

23%

Oil & Gas 8%

Residential Construction

12%

Municipal 10%

Other 19%

10%

15%

8%

9%

6%

5%

5%

7% 6%

10%

6%

9%

5% 6%

8

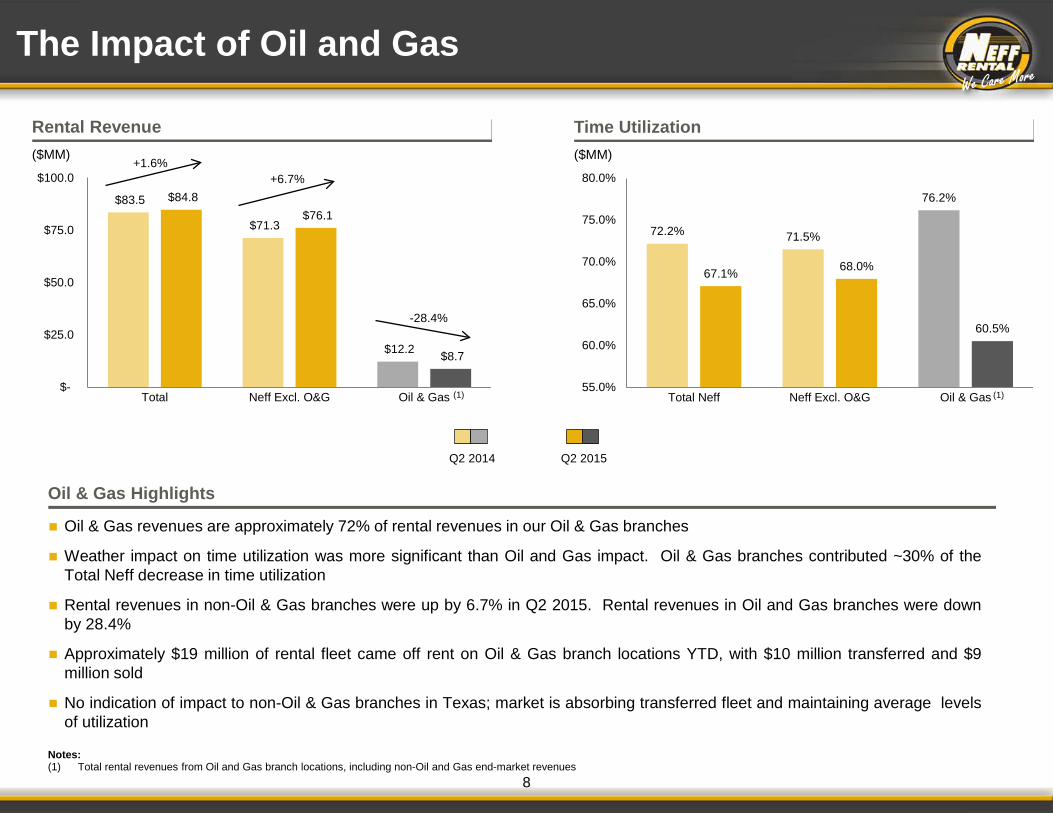

Notes: (1) Total rental revenues from Oil and Gas branch locations, including non-Oil and Gas end-market revenues

The Impact of Oil and Gas

Rental Revenue ($MM)

$83.5

$71.3

$12.2

$84.8 $76.1

$8.7

$-

$25.0

$50.0

$75.0

$100.0

Total Neff Excl. O&G Oil & Gas

Time Utilization ($MM)

72.2% 71.5%

76.2%

67.1% 68.0%

60.5%

55.0%

60.0%

65.0%

70.0%

75.0%

80.0%

Total Neff Neff Excl. O&G Oil & Gas (1) (1)

Oil & Gas Highlights

Oil & Gas revenues are approximately 72% of rental revenues in our Oil & Gas branches

Weather impact on time utilization was more significant than Oil and Gas impact. Oil & Gas branches contributed ~30% of the Total Neff decrease in time utilization

Rental revenues in non-Oil & Gas branches were up by 6.7% in Q2 2015. Rental revenues in Oil and Gas branches were down by 28.4%

Approximately $19 million of rental fleet came off rent on Oil & Gas branch locations YTD, with $10 million transferred and $9 million sold

No indication of impact to non-Oil & Gas branches in Texas; market is absorbing transferred fleet and maintaining average levels of utilization

+1.6% +6.7%

-28.4%

Q2 2014 Q2 2015

9

OEC of ~$775 million

Neff has invested over $670 million in its fleet since 2011 (1)

Average age of Neff’s fleet has been reduced from ~55 months in 2011 to ~44 months as of June 30, 2015

Average age of Earthmoving fleet: ~34 months

Fleet includes ~14,400 units of equipment, of which over 5,500 are earthmoving related

Neff’s Fleet in Focus as of June 30, 2015

Fleet Overview

Fleet Breakdown (% of OEC) as of June 30, 2015

Why Earthmoving?

Utilized at the initial stages of the construction process, and throughout the duration of most construction projects

Large and active end-markets (e.g., infrastructure, non-residential construction, residential construction, and oil & gas) and these customer bases require significant earthmoving assets

Customers value and want specialized earthmoving expertise – every project is different and requires the right combination of equipment, implements, and advice

Earthmoving penetration is relatively low at ~51%. With aerial and material handling at ~96% and ~84% rental penetration, respectively, we believe the future growth in industry penetration will likely come from the earthmoving category (2)

Earthmoving equipment retains a strong resale value and has a highly liquid secondary market

Earthmoving, 53.4%

Material Handling,

16.9%

Aerial, 12.8%

Trucks, 5.6%

Concrete / Compaction,

5.9%

Other, 5.4%

Note: (1) Defined as rental fleet purchases from January 2011 to June 2015 (2) Yengst Associates Market Machinery Research Report, dated June 2015

Mark Irion Chief Financial Officer

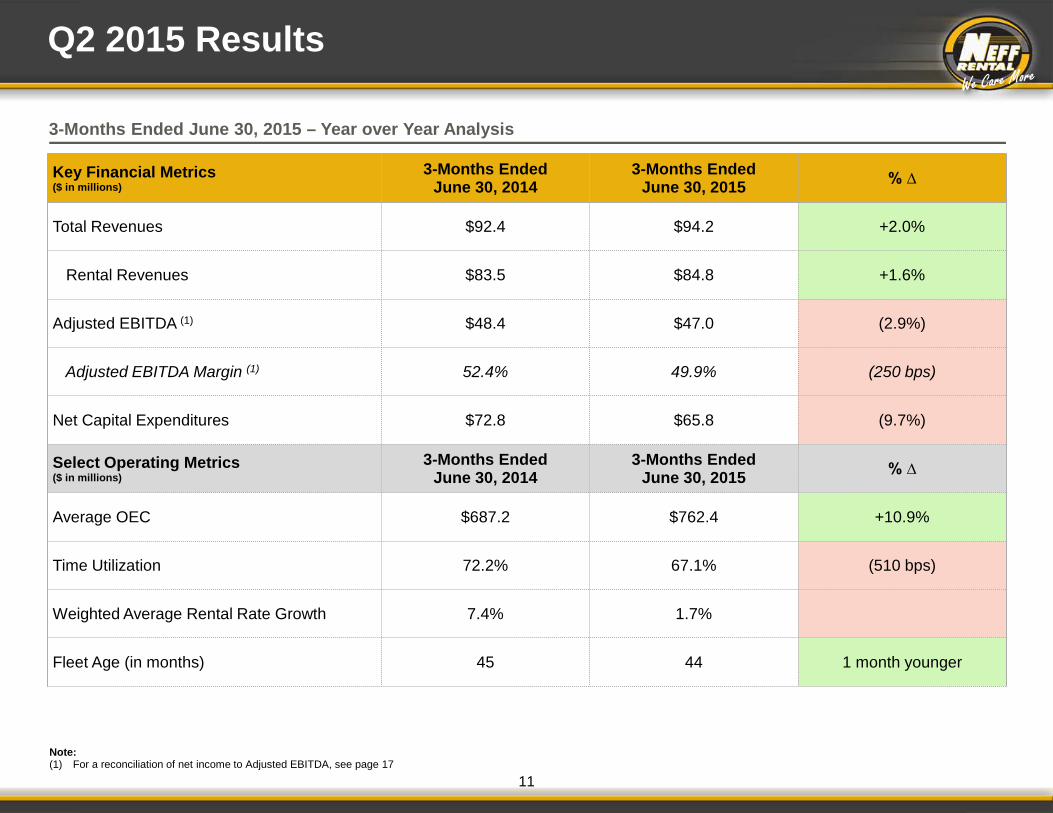

Q2 2015 Results

11

Key Financial Metrics ($ in millions)

3-Months Ended June 30, 2014

3-Months Ended June 30, 2015 % ∆

Total Revenues $92.4 $94.2 +2.0%

Rental Revenues $83.5 $84.8 +1.6%

Adjusted EBITDA (1) $48.4 $47.0 (2.9%)

Adjusted EBITDA Margin (1) 52.4% 49.9% (250 bps)

Net Capital Expenditures $72.8 $65.8 (9.7%)

Select Operating Metrics ($ in millions)

3-Months Ended June 30, 2014

3-Months Ended June 30, 2015 % ∆

Average OEC $687.2 $762.4 +10.9%

Time Utilization 72.2% 67.1% (510 bps)

Weighted Average Rental Rate Growth 7.4% 1.7%

Fleet Age (in months) 45 44 1 month younger

3-Months Ended June 30, 2015 – Year over Year Analysis

Note: (1) For a reconciliation of net income to Adjusted EBITDA, see page 17

YTD June 2015 Results

12

Key Financial Metrics ($ in millions)

6-Months Ended June 30, 2014

6-Months Ended June 30, 2015 % ∆

Total Revenues $170.1 $178.3 +4.8%

Rental Revenues $152.6 $159.0 +4.2%

Adjusted EBITDA (1) $83.2 $86.0 +3.4%

Adjusted EBITDA Margin (1) 48.9% 48.2% (70 bps)

Net Capital Expenditures $106.2 $108.2 1.9%

Select Operating Metrics ($ in millions)

6-Months Ended June 30, 2014

6-Months Ended June 30, 2015 % ∆

Average OEC $658.8 $742.3 +12.7%

Time Utilization 70.3% 65.4% (490 bps)

Weighted Average Rental Rate Growth 7.2% 2.7%

Fleet Age (in months) 45 44 1 month younger

6-Months Ended June 30, 2015 – Year over Year Analysis

Note: (1) For a reconciliation of net income to Adjusted EBITDA, see page 17

Debt and Liquidity Considerations

13

Summary Overview Current Debt Profile

Debt Maturity Profile

293.0

479.0

ABL @ L + 225 bps

Second Lien Term Loan @ L + 625 bps (1% LIBOR Floor)

$479.0

2015 2016 2017 2018 2019 2020 2021

$132 Unused

$293 Used

ABL 2nd Lien Term Loan

Total debt of $772.0MM as of June 30, 2015

Total debt net of $2.2MM OID is $769.8MM

Total leverage of 4.1x based on TTM Q2 2015 Adjusted EBITDA of $189.0MM

ABL leverage: 1.6x

Second lien leverage: 2.5x

Availability of $128.2MM on the ABL at June 30, 2015

No debt maturities prior to 2018

$772.0

$425.0

Net Capital Expenditures ($MM)

81.3

125.9 122.8 127.7 128.8

$50.0

$75.0

$100.0

$125.0

$150.0

2011 2012 2013 2014 TTM Q2 2015

Key Financial Metrics

14

197.4 234.6 281.0

324.1 330.4

36.9 44.8

33.5 34.5 36.6

10.5 11.5

12.7 13.4 13.1

244.8 291.0

327.2 372.0 380.2

$0.0

$100.0

$200.0

$300.0

$400.0

2011 2012 2013 2014 TTM Q2 2015

Rental Revenues Equipment Sales Parts & Service

86.7

119.9

150.8

186.1 189.0

$0.0

$45.0

$90.0

$135.0

$180.0

$225.0

2011 2012 2013 2014 TTM Q2 2015

Revenues ($MM)

Adj. EBITDA (1)

($MM)

Note: (1) For a reconciliation of net income to Adjusted EBITDA, see page 17

35.4

41.2

46.1 50.0 49.7

20.0

30.0

40.0

50.0

60.0

2011 2012 2013 2014 TTM Q2 2015

Adj. EBITDA Margin (1)

(%)

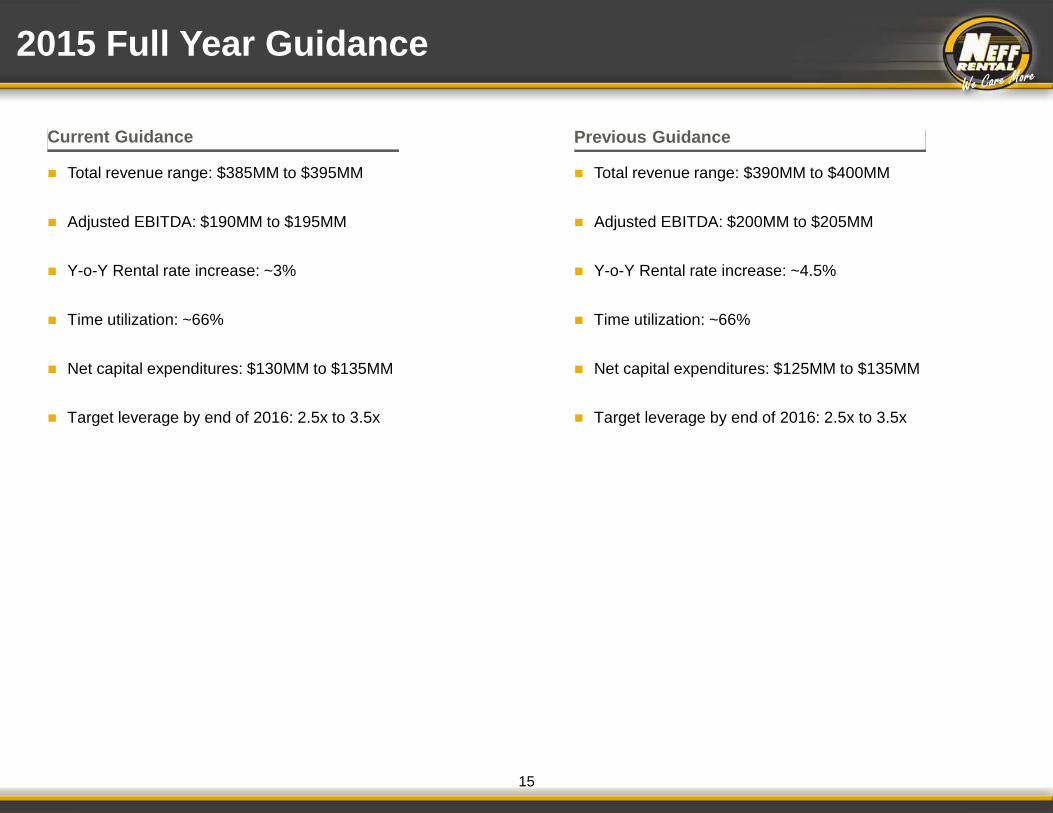

2015 Full Year Guidance

15

Current Guidance

Total revenue range: $385MM to $395MM

Adjusted EBITDA: $190MM to $195MM

Y-o-Y Rental rate increase: ~3%

Time utilization: ~66%

Net capital expenditures: $130MM to $135MM

Target leverage by end of 2016: 2.5x to 3.5x

Total revenue range: $390MM to $400MM

Adjusted EBITDA: $200MM to $205MM

Y-o-Y Rental rate increase: ~4.5%

Time utilization: ~66%

Net capital expenditures: $125MM to $135MM

Target leverage by end of 2016: 2.5x to 3.5x

Previous Guidance

Appendix

17

Reconciliation of Net Income to Adjusted EBITDA EBITDA represents net income plus interest expense, provision for taxes, depreciation of rental equipment, other depreciation and amortization and amortization of debt issue costs. Adjusted EBITDA represents EBITDA further adjusted to give effect to non-cash and other items that we do not consider to be indicative of future performance. Adjusted EBITDA is not a measure of performance in accordance with US GAAP and should not be considered as an alternative to net income or operating cash flows determined in accordance with US GAAP. Additionally, Adjusted EBITDA is not intended to be a measure of cash flow for management's discretionary use, as it excludes certain cash requirements such as interest payments, tax payments and debt service requirements. Management believes that EBITDA and Adjusted EBITDA in this presentation is appropriate because securities analysts, investors and other interested parties use these non-US GAAP financial measures as important measures of assessing our operating performance across periods on a consistent basis. Adjusted EBITDA has limitations as an analytical tool and should not be considered in isolation or as a substitute for analysis of our results as reported under US GAAP. The table below provides a reconciliation between net income and EBITDA and Adjusted EBITDA.

Notes: (1) Represents expenses and realized losses that were incurred in connection with the with the extinguishment of debt. (2) Represents the payments to certain members of management and independent members of the board of directors. (3) Represents cash payments made to suppliers of equipment in connection with rental splits, which payments are credited against the purchase price of the applicable equipment if Neff

Holdings elects to purchase that equipment. (4) Represents non-cash equity-based compensation expense recorded in the periods presented in accordance with US GAAP. (5) For 2011, represents expenses, realized gains and losses that were incurred in connection with the Chapter 11 Bankruptcy Proceedings. For 2012, represents (i) the adjustment of

certain interest rate swaps to fair value and (ii) loss on interest rate swaps. For, 2015, represents unrealized gain on interest rate swap.

Reconciliation of Net (loss) income to Adjusted EBITDA Year Ended December 31,

$ 000’s 2011 2012 2013 2014 2014 2015 2014 2015

Net (loss) income (36,783)$ 17,508$ 40,493$ 15,808$ (17,409)$ 18,022$ (22,867)$ 14,694$

Interest expense 16,524 23,221 24,598 40,481 15,119 21,267 8,316 10,753

Provision for income taxes 785 159 471 (5,359) 238 1,345 119 1,100

Depreciation of rental equipment 84,438 66,017 70,768 73,274 36,489 40,727 18,302 21,213

Other depreciation and amortization 11,937 9,041 8,968 9,591 4,708 5,118 2,462 2,657

Amortization of debt issue costs 1,164 1,461 1,929 3,061 2,339 752 1,012 381

EBITDA 78,065$ 117,407$ 147,227$ 136,856$ 41,484$ 87,231$ 7,344$ 50,798$

Loss on extinguishment of debt (1) - - - 20,241 15,896 - 15,896 -

Transaction bonus (2) - - - 24,506 24,506 - 24,506 -

Rental split expense (3) 1,750 932 2,343 3,658 745 1,103 395 299

Equity based compensation (4) 1,891 1,478 1,224 883 526 674 262 322

Adjustment to tax receivable agreement - - - - - (2,887) - (3,408)

Other (5) 4,957 102 - - - (119) - (1,007) Adjusted EBITDA 86,663$ 119,919$ 150,794$ 186,144$ 83,157$ 86,002$ 48,403$ 47,004$

Six Months Ended June 30,

Three Months Ended June 30,

18

Other Financial Data and Operating Data

Other Financial Data and Operating DataYear Ended December 31,

$ in 000's 2011 2012 2013 2014 2014 2015 2014 2015

Capital ExpendituresPurchases of rental equipment 108,606$ 159,192$ 144,483$ 149,174$ 105,938$ 111,095$ 74,980$ 65,207$ Purchases of non-rental equipment 9,592 11,556 11,852 13,018 11,020 10,068 3,287 6,723 Proceeds from sales of rental equipment (34,653) (41,731) (30,976) (31,620) (9,422) (11,765) (4,743) (5,476) Proceeds from sales of non-rental equipment (2,281) (3,097) (2,511) (2,859) (1,376) (1,196) (724) (698)

Net Capital Expenditures 81,264$ 125,920$ 122,848$ 127,713$ 106,160$ 108,202$ 72,800$ 65,756$

OEC of rental equipment sales 81,780 95,888 69,834 69,605 18,133 26,035 8,305 11,603 Growth rental equipment capex 26,826 63,304 74,649 79,569 87,805 85,060 66,675 53,604

Gross rental equipment capex 108,606$ 159,192$ 144,483$ 149,174$ 105,938$ 111,095$ 74,980$ 65,207$

Other Operating DataAverage OEC 470,638$ 527,266$ 606,624$ 688,733$ 658,764$ 742,319$ 687,228$ 762,423$ Fleet age in months (as of period end) 55 48 46 45 45 44 45 44Weighted average rental rate growth 8.3% 6.5% 6.4% 6.6% 7.2% 2.7% 7.4% 1.7%Time utilization 65.0% 68.7% 70.9% 69.7% 70.3% 65.4% 72.2% 67.1%

Three Months Ended June 30,

Six Months Ended June 30,

Net Capital Expenditures: Purchases of rental and non-rental equipment less proceeds from the sale of rental and non-rental equipment.

Time Utilization: The daily average OEC of equipment on rent, divided by the OEC of all equipment in the rental fleet during the relevant period.

EBITDA and Adjusted EBITDA: EBITDA represents net income plus interest expense, provision for taxes, depreciation of rental equipment, other depreciation and amortization and amortization of debt issue costs. Adjusted EBITDA represents EBITDA further adjusted to give effect to non-cash and other items that we do not consider to be indicative of future performance.

Fleet Age: The OEC weighted age of the entire fleet, excluding the benefit of refurbishments.

OEC: The first cost of acquiring the equipment, or in the case of used equipment purchases and rental splits, an estimate of the first cost that would have been paid to acquire the equipment if it had been purchased new in its year of manufacture, as the daily average OEC of equipment on rent, divided by the OEC of all equipment in the rental fleet during the relevant period.

Weighted Average Rental Rate Growth: The percentage change in the rate/price that is charged for equipment on rent. Overall company rental rates change based on a combination of pricing, fleet composition and term of rental. This metric is used to evaluate rate changes both year-over-year and sequentially (typically quarter-over-quarter). Rental rate changes are calculated based on the year-over-year or sequential variance in average contract rates, weighted by the prior period revenue mix.

Return on invested capital (ROIC): is a profitability ratio used to assess the company’s efficiency at allocating the capital under its control to profitable investments; calculated as annualized net operating profit after tax (NOPAT) divided by the year-over-year average of the invested capital accounts.

19

Glossary of Terms