investor september 2011 presentation - eurazeors... · gaz et eaux then azeo gas and water utility,...

TRANSCRIPT

Accelerating change

September 2011

Investor

Presentation

INVESTOR PRESENTATION

Disclaimer

This document has been prepared by Eurazeo SA (“Eurazeo”) solely for the use of

presentations made to investors or analysts.

Eurazeo makes no representations or warranties that the information contained herein

is accurate, correct or complete.

The information set out herein is provided as of the date of the presentation and

Eurazeo is under no obligation to keep current the information contained in this

presentation. However, this information is subject to completion and/or revision and

Eurazeo has the right to change the content hereof, in its sole discretion, at any time

without prior notice.

This document may contain information regarding current or future transactions as

well as “pro forma” information to show Eurazeo as it would be after said transactions

have been completed. These forward-looking statements are provided for information

purposes only and are not guarantees of future performance.

No information provided on this document constitutes, or should be used or

considered as, an offer to sell or a solicitation of any offer to buy the securities or

services of Eurazeo or any other issuer in any jurisdiction whatsoever.

- 2 -

INVESTOR PRESENTATION

Contents

- 3 -

Eurazeo: professional shareholder

1st Half 2011 results

Appendices

INVESTOR PRESENTATION

Eurazeo in a nutshell

Large stakes in leading companiesA long term French investor

130 years existence, strong shareholders

Deep network and strong track record

Led by Patrick Sayer since 2002

Investment cases built on a 4-6 year horizon,

no exit constraints

Active portfolio management

Active support to portfolio companies

Regular portfolio reviews

One new investment and one exit in 2010

19 acquisitions by portfolio companies

in 2010 and in H1 2011

3 new investments announced in H1-2011

- 4 -

ServicesElis, Edenred,

Fraikin, Foncia

Mobility

& leisureAccor, APCOA,

Europcar

Real estateANF, Colyzeo

Otherincluding OFI

21%

28%

20%

14%

9%

8%

LuxuryMoncler

BtoB distributionRexel

A balanced portfolio

NAV* as of August 29, 2011 : €4.0bn, €63.3/share

(*) Based on the update of listed securities, cash assets and treasury shares as of August 29, 2011,

private assets being valued as of June 30, 2011 (see details and valuation methodology on page 66)

INVESTOR PRESENTATION

130 years active investing

Significant outperformance vs. key indices over 10 years

+35% vs CAC40, +29% vs LPX

200119691881 20092003 2005 2007

GAZ ET EAUX then AZEOGas and water utility, later investment company

EURAFRANCEInvestment company

EURAZEOMerger of Eurafrance and Azeo

Fraikin

Eutelsat

Terreal

Lazard

Chargeurs réunis

Chaussures André

Viniprix

Danone

Sofina

Société Générale

de Belgique

Generali

UAP

Pearson

Sidel

Infogrames

Ipsos

Sogeti

Virata

Oberthur

Saint-Gobain

Accor

B&B Hotels

Air Liquide

Rexel

APCOA

Elis

Sirti

Intercos Fonroche

Colyzeo Banca Leonardo

Europcar Accor

Veolia

- 5 -

2011

OFI PE

Foncia

Moncler

INVESTOR PRESENTATION

A leading professional investor in France

DEEP EXPERIENCE OF PRIVATE INVESTMENT

– Strong deal flow

– Experience across categories: growth capital,

mid-caps and large buyouts

– Strong relationships with company managements drive

significant proprietary deal flow and early access to

companies that are put up for sale

– Institutional status drives access to deals with families,

large corporations and entrepreneurs

A PROVEN CAPACITY IN PUBLIC INVESTMENTS:

ACCOR, EDENRED, REXEL,...

– Deep sector knowledge and strategic impact

– Strong French network and capacity to earn the trust

and respect of key independent directors

– Capacity to absorb short term market movements:

strong balance sheet and flexible exit timeframe

– Long term value creation perspective

Largest European public investmentcompanies in the LPX Europe index(in €bn and by market cap as of Sept. 2, 2011)

Ratos

Partners Group

Wendel

Eurazeo

3i

Intermediate Capital

GIMV

Electra PE

Marfin Investment

SVG Capital

3.3

3.3

2.2

2.2

1.1

0.9

0.6

2.7

0.2

0.2

- 6 -

INVESTOR PRESENTATION

Eurazeo targets companies with the potential for significant change

1/ Projects of all sizes: €15m to €500m equity and more

- Eurazeo: focus on mid- to large size companies

- Eurazeo PME (former OFI Private Equity Capital): complementary market segment –

SMEs with enterprise value below €150/200m

- Eurazeo Croissance: focus on fast-growing SMEs with strong transformation potential

- Portfolio balance / diversification: a major consideration

2/ Clear criteria

- Market leaders

- Quality of management

- Barriers to entry

- Profitability and recurring cash-flows

- A step change / a new direction or a significant transformation to be accomplished (strong

organic growth or bolt-on acquisitions, potential for sector consolidation, etc.)

3/ Target IRR 15-25% depending on risk profile

- 7 -

INVESTOR PRESENTATION

A portfolio of market leaders

(1) Direct holding, excluding Colyzeo

Current % of interestheld by Eurazeo

- 8 -

Long-term truck rental with a fleet of more than 50,000 vehicles

Short-term car rentals with a fleet of ca.200,000 vehicles

Parking operator with approx. 6,300 parking facilities under management

Rental and cleaning of textiles and hygiene services

Professional distribution of electrical equipment with 2,300 branches

French real estate investment company with downtown trophy assets in major French cities

Hotel manager: Accor operates in 90 countries with 145,000 employees

Leading player in the creation, developmentand production of color cosmetic products

Prepaid services designed to enhance individual well-being and the performance of organizations

51.7%

8.9%

8.9%

81.2%

85.1%

81.7%

13.2%

21.6%

33.6%

#1 IN THE WORLD

#1 IN LYONS AND MARSEILLES

#1 IN EUROPE

#1 IN THE WORLD

#1 IN EUROPE

#1 IN EUROPE

#1 IN THE WORLD

#1 IN FRANCE

#1 IN THE WORLD

1

Major player in photovoltaic industry in France 28.4% SMALL AND GROWING

1

Leader in residential real estate in France 40.0% #1 IN FRANCE

INVESTOR PRESENTATION

Accelerating change

TRANSFORMING STRATEGIES

- The Accor / Edenred stock demerger resulted in two focused world leading companies

- Accor refocused on core business, accelerated the change to a franchise and management contract

centered business model, and sold non-core assets

- From a passive to a very active development of ANF Immobilier real estate portfolio

- Implementing social and environmental guidelines across our portfolio

ACCELERATING GROWTH

- Transforming acquisitions: Rexel / Hagemeyer, Europcar / Vanguard EMEA, APCOA / CPS, B&B

Hotels / Villages Hôtel,

- Driving organic growth: sales-force recruitment (Elis), accelerating redesign and renovation

(Accor, ANF Immobilier, B&B Hotels,), creating new products & services (Edenred, Rexel)

- Investing in the future: new business models (Europcar urban mobility), new geographies (B&B

Hotels, Elis), renewable energy (Fonroche)

PENETRATING EMERGING MARKETS

- Accor objectives in China and India, South East Asia and Brazil

- Targeted external growth for Edenred in South America

- Rexel strengthening its position in China and penetrating Brazil and India

- 9 -

INVESTOR PRESENTATION

A long-term shareholder base and a strong corporate governance

(1) Only concert as of January 31, 2011

(2) Including 3.58% of treasury shares

(*) Voting rights

A strong corporate Governance

Separation of the roles of Chairman

and CEO

Independence of the Supervisory Board:

6 independent members out of 12

Audit Committee, Finance Committee,

Compensation and Appointments

Committee

Existence of a shareholder agreement

between founding families (former

SCHP)

Sofina

5.70%

(9.07%*)

Free float(2)

56.44%

(47.65%*)

Foundingfamilies(1)

19.93%

(19.42%*)

CréditAgricole

17.93%

(23.86%*)

- 10 -

Shareholding structure

as of August 31, 2011

INVESTOR PRESENTATION

3.0

2.4

1.5

1.3

1.4 1.3

Significant NAV increase

- 11 -

(1) With ANF taken at its NAV on the basis of an independent valuation of its assets (€39.6)

(2) Cash and treasury shares net of tax

(3) Restated for FY2010 distribution (bonus share and special distribution of ANF Immobilier shares)

(4) Proforma NAV includes investment in Moncler – Private assets valued as of June 30, 2011,

update of listed securities, cash assets and treasury shares as of August 29, 2011.

NAV/share in €

Additional NAV

with ANF taken

at its NAV(1)

NAV/share

+ €22

+ ~50%

Non listed

Listed

Cash(2)

44%

14%

38%

62.0 70.3 70.1

06/30/2010(3) 12/31/2010(3) 06/30/201106/30/2009(3) 12/31/2009(3)12/31/2008(3)

47.7 42.5 57.3

INVESTOR PRESENTATION

A solid financial situation

- 12 -

• No structural debt at Eurazeo level

• New investments with moderate leverage

• Successful refinancing of the revolving credit line

• Cash position proforma of investments in Foncia and Moncler

and sale of LT participations (Ipsos) ~€200m

(*) Consolidated leverage = (consolidated net debt – value of assets which do not contribute to adjusted consolidated EBITDA) / adjusted consolidated EBITDA

(in €m) H1 2011 H1 2010 %

Eurazeo cash position (NAV) 769.4 722.4 6.5%

Consolidated net debt 5,953.1 6,269.1 -5.0%

Consolidated leverage* 2.6x 3.2x -19%

INVESTOR PRESENTATION

Contents

- 13 -

Eurazeo: professional shareholder

1st Half 2011 results

Appendices

INVESTOR PRESENTATION

Contents

Positive momentum in 1st Half 2011

OFI Private Equity, Foncia and Moncler

Outlook

- 14 -

15

21

46

INVESTOR PRESENTATION

POSITIVE MOMENTUM IN 1ST HALF 2011

- 15 -

INVESTOR PRESENTATION

Positive momentum in 1st Half 2011

Strong operational performance of portfolio companies

Solid financial position

- 16 -

3 promising investments with transformation potential

INVESTOR PRESENTATION

Investment company

SME segmentReal estate

servicesLuxury

outerwear

Sustained investment activity

- 17 -

3 acquisitions performed in H1 2011, all offering significant transformation

and value creation potential

• Significant potential for return on investment and recurring capital gains with target investment of €50 to 100m annually (1 to 3 companies per year)

• Consolidation of Eurazeo‟s position across France‟s private equity market

Transformation and value creation potential:

• Recurring revenues and strong cash flow generation

• Untapped organic growth potential and opportunities for synergies between complementary activities

• Sustainable cash flow generation notably supported by solid growth prospects

• Numerous growth levers: new geographies, retail expansion, product offering

• Multiple: 11x LTM 06/11

EBITDA

• Multiple: 11.6x LTM 06/11

EBITDA

• Price: fully paid in Eurazeo shares

• Acquired assets valued at €68/new Eurazeo share

INVESTOR PRESENTATION

1st Half 2011 key figures

(in €m) H1 2011 H1 2010(1) Change*

CONSOLIDATED REVENUES 1,907.7 1,810.9 +5.3%

ADJUSTED EBIT(2) 200.5 186.2 +7.7%

NET INCOME GROUP SHARE - 106.3 92.9 n.a.

June 30, 2011 December 31, 2010 Change

NAV 4,398 4,281(3) +2.7%

NAV / share (in €) 70.1 70.3(3) -0.3%

CASH ASSETS 769 909 -15.4%

* Excluding B&B Hotels for the 1st Half of 2010

(1) 1st Half 2010 restated for the exit of B&B Hotels from the perimeter as of June 30 (2) Fully consolidated companies only

(3) Restated for special distribution of ANF shares, number of shares restated for capital increase in remuneration for OFI shares

- 18 -

INVESTOR PRESENTATION

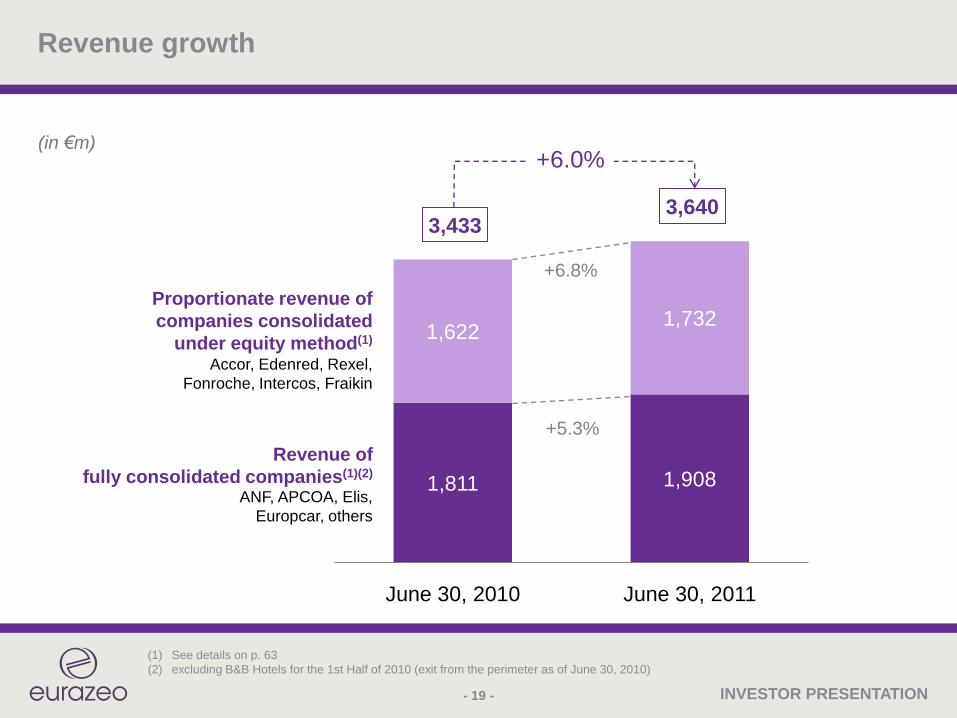

Revenue growth

- 19 -

1,811 1,908

1,6221,732

June 30, 2010 June 30, 2011

3,4333,640

Proportionate revenue of

companies consolidated

under equity method(1)

Revenue of

fully consolidated companies(1)(2)

+6.8%

+5.3%

Accor, Edenred, Rexel,

Fonroche, Intercos, Fraikin

ANF, APCOA, Elis,

Europcar, others

+6.0%(in €m)

(1) See details on p. 63

(2) excluding B&B Hotels for the 1st Half of 2010 (exit from the perimeter as of June 30, 2010)

INVESTOR PRESENTATION

Strong increase in companies‟ results

- 20 -

Fully consolidated

companies‟ adjusted EBIT

Profit from

equity affiliates

186.2200.5

9.5

35.2

H1 2010 H1 2011

195.8

235.7

+20.4%

(1) 2010 pro forma adjusted for exit of B&B Hotels

(1)

(in €m)

INVESTOR PRESENTATION

OFI PRIVATE EQUITY,

FONCIA AND MONCLER3 PROMISING INVESTMENTS

- 21 -

INVESTOR PRESENTATION

3 promising investments

+ Foncia + Moncler

- 22 -

Foncia: France‟s leader in residential real estate services,

recurring business and limited exposure to real estate cycle

Moncler: a unique luxury brand offering

significant growth potential, notably in emerging markets

OFI Private Equity:

a leading investment company targeting SME market

INVESTOR PRESENTATION- 23 -

becomes

3 promising investments:

INVESTOR PRESENTATION

OFI Private Equity is a natural complement for Eurazeo

An investment philosophy close to Eurazeo‟s A committed shareholder: majority position, solid governance, CSR approach

Similar investment criteria: quality of management, strong profitability and high growth potential, reliable and recurring cash flows, market leaders, portfolio diversification

Alignment of interests with portfolio company management teams

Recognized high quality management team Experience and track record of Olivier Millet and his team

Six-person investment team: Olivier Millet, 2 associate directors, 2 investment directors and 1 investment manager

Good track record since its creation in 2005 14 investments

4 divestitures with an overall multiple of 2.2x

1.4x current portfolio on the basis of June 30, 2011 NAV

Quality portfolio built around market leading companies

- 24 -

INVESTOR PRESENTATION

Attractive price and success of the public offer

Success of the simplified exchange public offer, Eurazeo now holds:

95.27%** of the capital and of the voting rights of OFI PEC

96.89% of the BSA 1 issued by OFI PEC

99.23% of the BSA 2 issued by OFI PEC

- 25 -

Eurazeo will proceed with a “squeeze out” procedure

on the OFI PEC residual shares, BSA1 and BSA2

The squeeze out should be effective before year‟s end

(*) Based on OFI PEC's June 2011 NAV and the announced valuation of the other acquired assets

(**) Not including OFI PEC treasury shares

Quality assets bought at attractive price:

- fully paid in Eurazeo shares

- acquired assets valued at €68/new Eurazeo share*

INVESTOR PRESENTATION

Eurazeo pme

- Ambition:

• Invest in companies with significant transformation potential, on the small and medium

entreprise market segment (investment size between €15m and €75m)

• Investment target of €50m to €100m per year (1 to 3 companies per year)

- In a dynamic market segment:

• LBO small-mid cap segment (EV between €15m and €200m)

• ~90 operations per year, 1 out of 3 being a secondary transaction

- 26 -

INVESTOR PRESENTATION

Diversified assets

- 27 -

8 investments,

6 majority(1)

Balanced between

Services and Industry

No single investment

more than 26% of

Gross Asset Value

(1) Dessange, FDS, Léon de Bruxelles, Mors Smitt, Gault & Frémont and Fondis. Minority Investments : IMV and BFR Groupe

Cash

26%

26%24%

7%

7%

2%3%

1%4%

€168.5mas at June 30, 2011

INVESTOR PRESENTATION

Solid growth across the portfolio

- 28 -

(*) Perimeter at June 30, 2011

Preliminary figures H1 2011 Actual H1 2010

In €m Nb. of companies Revenue EBITDA EBITDA Margin Revenue EBITDA EBITDA Margin

Majority* 6 175 27 15.4% 161 26 16.2%

Minority* 2 38 6 17.2% 48 7 15.6%

21.7

7.4

17.4

26.8

45.8

55.6

21.1

5.8

16

26.5

41.8

50.1 Openings of 7 new restaurants during the year 2011, 5 have been realised on the first semester

+1%

+11%

+27%

+3%

+9%

Change

+10%

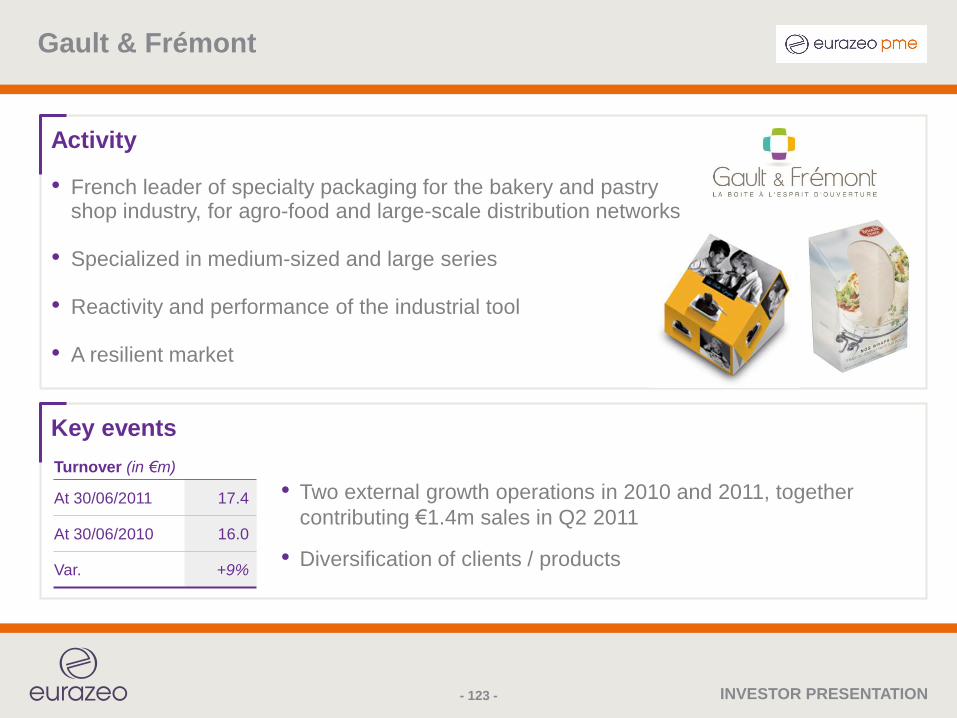

External growth, +1% on a same basis perimeter (2 external growth operations in 2010 and 2011, together contributing €1,4M€ sales in Q2 2011)

Redeployment of its business activity Development of the product portfolio with new suppliers

in order to accelerate the group development

Good performance for the Dessange and Camille Albane franchises

Further international development

Further international development (direct setting-up or external growth)

Revenue (€m)

External growth: acquisition of STS Rail Ltd (Turnover 2010 : € 3,2M) in the UK in April 2011

H1 2010

H1 2011

Dessange

Gault & Frémont

Fondis

Mors Smitt

Siem/Flexitallic

Léon de Bruxelles

INVESTOR PRESENTATION- 29 -

3 promising investments:

INVESTOR PRESENTATION

Transaction overview

Transaction Purchase of 98.11% of Foncia from BPCE for €711m

ConsortiumGovernance shared equally between Eurazeo and Bridgepoint

Equity investment (before employees) of €197m for Eurazeo and €39m for Eurazeo Partners

BPCE

• €80m of equity instruments

• €20m of junior equity with returns capped at 10%

• €100m of redeemable bonds in shares protecting investors‟ return on investment

(i.e. repayment profile triggers only after investors money multiple exceeds 2.7x)

Financing

Prudent all-senior bank financing of €395m (maturity: 2017/2018), including a bullet tranche

of €300m and additional available financing facilities of €90m to finance

the company‟s development

Valuation €1,017m / €917m net of redeemable bonds, 11x LTM EBITDA June 11

- 30 -

INVESTOR PRESENTATION

A very attractive investment opportunity (1/2)

1. France‟s leader in residential real estate services

– 1st in France in lease management/rentals (8%), joint property (13%) and 4th in transactions

– Very fragmented market: less than 27% of the market in joint property and 16% for lease

management held by the top 3 players

– Strong Foncia brand

– Network of 577 branches in France with national coverage and homogenous work practices

2. Recurring revenues generated from a large and loyal client base

– 84% of revenues generated through recurring activities little affected by economic cycles

– Very large client base: 1 million joint-property dwellings, 252,000 lease management

properties

– Very long-term client relationships: 95% retention rate

- 31 -

INVESTOR PRESENTATION

A very attractive investment opportunity (2/2)

3. Strong cash flow generation

– A 90% EBITDA to cash transformation rate

– Business generates working capital resources, not needs

– Limited maintenance investment

– Moderate acquisition debt

4. A primary LBO offering opportunities for significant transformation

– Untapped organic growth potential: improving quality of service, cross-selling

complementary products to existing customer base

– Extended, standardized network enables absorption of new offices

– International expansion started in Germany, Switzerland and Belgium

A recurring activity offering significant value creation potential

- 32 -

INVESTOR PRESENTATION

36%

31%

16%

1%8%

8%

French leader in residential real estate services

- Leader in residential real estate services

- 3 complementary activities:

– Lease management / rentals

#1 in France (8% market share) with

252,000 dwellings under management

– Joint property management

#1 in France (13% market share) with

1 million dwellings under management

– Property transactions

#4 with 12,000 sales agreements

signed in 2010

- A business with strong recurrent

revenues (84% of revenues)

- A network of 609 branches,

of which 577 in France

- 7,000 employees of which 6,500 in France

(1) Including renting business (95% captive)

Lease management(1)/

Rentals

Joint property

Transaction

Associated services

International

Client accounts

2010 revenue by activity

Revenue by country

92%

5%

2%

1%

France

Switzerland

Germany

Belgium

Recurring

revenue: 84%

- 33 -

INVESTOR PRESENTATION

A steadily growing property management market

Market size

Business description Revenue sourcesMarket growth

Lease

management/

Rentals

€2.5 bn

• Management activities (accounting, administration and legal) and research for new tenants

• Long-term customer relationships (renewal rate 95 %)

• Recurring revenues linked to fees invoiced to owners and tenants

• Interest earned on client account placements

+ 3-4 %

per year

Joint property

management€1.4 bn

• Joint-property owners association administers property on behalf of all owners

• Long-term customer relations (renewal rate: 95 %)

• Recurring revenues linked to fees invoiced to joint-property owners

• Interest earned on client accounts

Associated

servicesN/A

• Financial management (SCPI, etc.), technical diagnoses, insurance brokerage and financing

• Revenues linked essentially to recurring business

• Significant source of synergies

Transactions €4.0 bn• Property value estimation,

organization of visits, preparation of pre-contracts

• More cyclical business (dependent on property market)

• Revenue proportional to volume / price of transactions

Variable

~84% of

Foncia‟s

business

~16% of

Foncia‟s

business

- 34 -

INVESTOR PRESENTATION

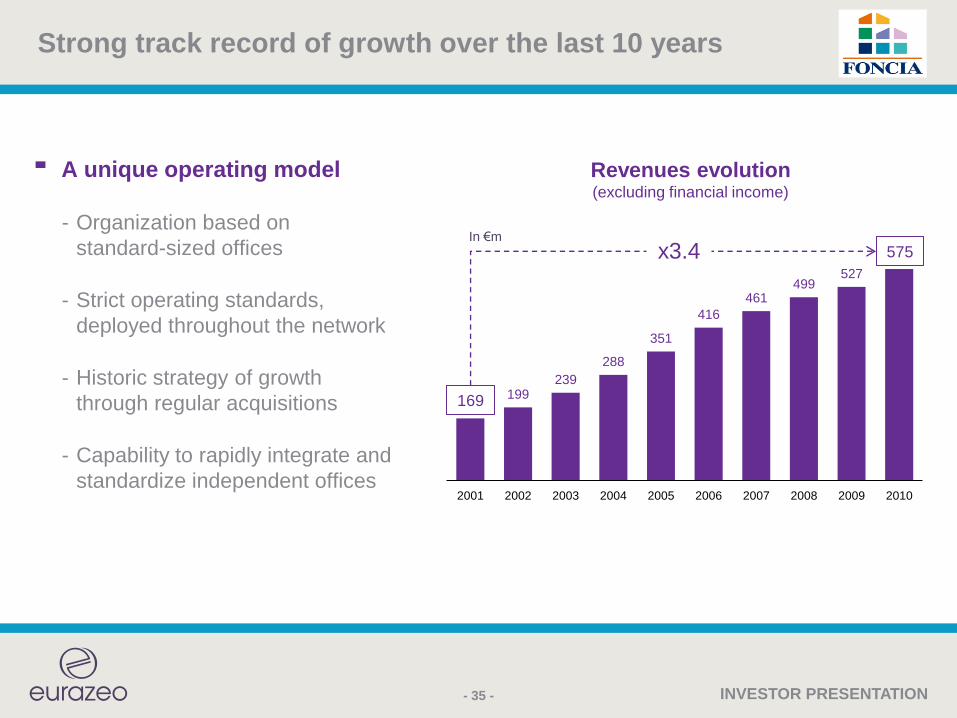

Strong track record of growth over the last 10 years

A unique operating model

Organization based on

standard-sized offices

Strict operating standards,

deployed throughout the network

Historic strategy of growth

through regular acquisitions

Capability to rapidly integrate and

standardize independent offices

169199

239

288

351

416

461499

527

575

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Revenues evolution(excluding financial income)

169

575x3.4In €m

- 35 -

INVESTOR PRESENTATION

Strong transformation potential

Ambition: make Foncia the benchmark reference

in residential real estate services

• Promote commercial synergies between

the different disciplines

• Develop new product offering

• Reinforce organic growth culture and quality

of joint-property management services

• Improve quality and perception of services

• Develop new product offering

• Develop operational efficiency sources

reinforcing leadership competitive advantages

• Secure synergies from acquisitions

Transactions

Lease

management/

Rentals

Associated

services

Joint-property management

(1 million dwellings in France)

Administrative and support functions

- 36 -

INVESTOR PRESENTATION

Financials

- 37 -

January – June (€m) H1-2011 H1-2010Reported

changeFull Year 2010

Revenue 297.7 285.2 +4.4% 580.4

Normalized EBITDA (1)

% margin

45.0

15.1%

42.4

14.9%+6.1%

80.1

13.8%

(1) EBITDA normalized for non recurring items accounting practices and other items as identifed in the due diligence process.

Reported numbers might differ

LTM Normalized EBITDA(1)

As of June 2011 = €82.8m

INVESTOR PRESENTATION- 38 -

3 promising investments:

INVESTOR PRESENTATION

Key elements of the transaction

- 39 -

Moncler Key figures€429m sales and €102m of EBITDA in 2010

50 operated stores* for the Moncler brand, as of today

Purchase Price Eurazeo is purchasing a 45%-stake in the Company for a price of €418m

Transaction value€1.2bn Entreprise Value

11.6x LTM June 2011 EBITDA

Shareholder structure

Governance

Mr. Remo Ruffini to remain Chairman of the Board

Eurazeo will appoint 5 board members, including the Vice-Chairman,

Mr. Remo Ruffini 3 board members, Carlyle and Mittel each 1 board member

CalendarExpected closing Q4 2011

Financing and equity syndication in progress

45%

32%

17.8%

5%

Eurazeo

R. Ruffini

0,3% S. Buongiovani

Carlyle

Mittel

38%

48%

13.5%

R. Ruffini

Carlyle

Mittel0,5% S. Buongiovani

(*) Operated stores include urban stores, ski resorts stores, shops in shops and outlets – excluding franchises (2) and corners (9)

INVESTOR PRESENTATION

Investment case

The luxury market presents attractive fundamentals and is complementary

to Eurazeo‟s portfolio

The luxury apparel & accessories market is estimated at €100bn and is forecasted to grow at 6-7% p.a.

Few companies with critical mass such as Moncler are available

Strong growth prospects supported notably by an increasing exposure to emerging markets

Moncler opened 4 stores in China, and expects to open 5 more in 2011

Strong potential in Korea and Russia

Roll-out geographical reach in the USA

High profitability levels and solid cash conversion rate

Seasoned and well regarded management team that has built Moncler‟s success story

Limited acquisition debt resulting in significant operating and financial flexibility (<2.5x leverage)

Exit options: sale to a strategic

- 40 -

Moncler is an attractive investment for Eurazeo

INVESTOR PRESENTATION

Moncler is pursuing its growth

and diversification strategy (1/2)

- 41 -

51%49%

Rest of the world

Italy

H1 2010

Sales

Moncler brand:

continued

geographical

diversification

41%

59%

Strong growth

for the group and

for the Moncler

brand in H1 2011

H1 2011

Sales

Sales growth Vs H1 2010

Group +19%

Moncler brand +35%

INVESTOR PRESENTATION

Moncler is pursuing its growth

and diversification strategy (2/2)

- 42 -

23%

77%

Wholesale

Operated stores

H1 2010

Sales

Moncler brand:

Continued shift

to retail

29%

71%

H1 2011

Sales

Moncler brand:

seasonal rebalancing

Spring-Summer 2011 collection sales in retail

and wholesale showing strong results

• H1 2011 like-for-like growth in Moncler stores at 12%

• 2012 Spring-Summer collection orders show a good trend

INVESTOR PRESENTATION

Pursuing expansion of retail network

- 43 -

2010 To date End 2011

Europe 24 29 34

Asia 13 17 24

North America 3 4 4

Total 40 50 62

Number of Operated Stores

Evolution of

retail network

• 22 openings expected in

2011, versus 15 openings

in 2010 and 11 in 2009

• Balanced focus on Europe

and Asia in 2011

Expand focus

Increase penetration

Strongly develop operated stores in top end locations

Intensify efforts on underpenetrated markets with strong potential

INVESTOR PRESENTATION

1st Half 2011 highlights

- 44 -

• Strong performance of Moncler Division (+35%), both in wholesale and retail and across key geographies

• Other Brands: +1.9%, mainly due to retail development which offsetsa lower performance in wholesale

January – June

(€m)H1 2011 H1 2010

Reportedchange

Revenue 189.3 158.7 +19.3%

EBITDA

% margin

30.4

16.0%

26.0

16.4%

+16.6%

INVESTOR PRESENTATION

Investment perspectives

Growth remains very strong in H1 and is expected to continue

• All openings for 2011 are well advanced and most of them secured

• Orders in the wholesale channel are above previous year

Preparation of the transaction‟s closing

• Antitrust

• Debt financing (limited leverage)

• Equity syndication

- 45 -

Expected closing in Q4 2011

INVESTOR PRESENTATION

OUTLOOK

- 46 -

INVESTOR PRESENTATION

Still seizing opportunities

Sale of stake in LT Participations (Ipsos) to Sofina SA

Increased stake in Intercos:

- from 25.1% to 33.6% following purchase of 50% of Euraleo

from Gruppo Banca Leonardo

Reinvestment of €10m in Fonroche to finance its growth

Banca Leonardo: successful disposal of DNCA

- 47 -

INVESTOR PRESENTATION

A well-balanced and diversified portfolio

- 48 -

(1) With ANF taken at its NAV on the basis of an independent valuation of its assets (€39.6)

(2) Cash and treasury shares net of tax

(3) Restated for FY2010 distribution (bonus share and special distribution of ANF Immobilier shares)

(4) Proforma NAV includes investment in Moncler – Private assets valued as of June 30, 2011, update of listed securities, cash assets and

treasury shares as of August 29, 2011,

NAV/share in €

1.3

1.4 1.3Additional NAV

with ANF taken

at its NAV(1)

NAV/share

62.0 70.3 70.1

+ €8

Non listed

Listed

Cash(2)

ServicesElis, Edenred,

Fraikin, Foncia

Mobility

& leisureAccor, APCOA,

Europcar

Real estateANF, Colyzeo

Otherincluding OFI

21%

28%

20%

14%

9%

8%

LuxuryMoncler

BtoB distributionRexel

Pro forma(4) NAV as of August 29, 2011

A further balanced portfolio

€4.0bn €63.3/share

June 30, 2010(3)

44%

42%

14%

34%

47%

19%

38%

47%

15%

December 31, 2010(3) June 30, 2011

INVESTOR PRESENTATION

To conclude

3 promising acquisitions

Strong operational performance of portfolio companies

- 49 -

Resilience of Eurazeo‟s model

and confirmed value creation potential

INVESTOR PRESENTATION

Contents

- 50 -

Eurazeo: professional shareholder

1st Half 2011 results

Appendices

INVESTOR PRESENTATION

APPENDICES

including Group Companies‟ detailed information

- 51 -

INVESTOR PRESENTATION

Appendices

- 52 -

Financial appendices

Group companies‟ detailed information

Other information

INVESTOR PRESENTATION

1ST HALF 2011 RESULTS

- 53 -

INVESTOR PRESENTATION

1st Half 2011 consolidated results

Operational performance in H1 2011

- 54 -

INVESTOR PRESENTATION

Consolidated scope as of June 30, 2011

- 55 -

06/2011

Consolidated companies 188

Fully consolidated 181

Equity method 7

INVESTOR PRESENTATION

Results analysis

- 56 -

* 06/2010 Proforma : deconsolidation of B&B Hotels as of January 1, 2010.

(1) Before changes in derivatives, fair value adjustments of investment properties, depreciation and amortization of intangibles, available for sale

securities and equity affiliates as well as amortization of allocated goodwill

(2) Excluding impact from derivatives

(3) Including restructuring charges of - €2.5m in 2011, €1.3m in 2010 and €24.0m in 2009

(4) Before depreciation and amortization of intangibles, available for sale securities and equity affiliates as well as amortization of allocated goodwill

ANF Immobilier 38.1 27.2 19.5 18.9

APCOA 13.8 12.6 12.6 15.3

Elis 87.2 84.2 84.2 81.2

Europcar 61.4 62.2 62.2 42.6

B&B Hotels - - 12.5 10.2

Adjusted EBIT (1) 200.5 186.2 191.0 168.2Net cost of financial debt of above companies (2) (238.2) (228.3) (235.4) (224.9)

Earnings for equity affiliates 35.2 9.5 9.5 (27.5)

Cost of net financial debt Accor/Edenred (LH19) (2) (17.7) (18.3) (18.3) (20.6)

Change in value of investment properties 18.1 9.6 6.3 (61.0)

Capital gains or losses - 217.2 217.2 44.9

Revenues of holding sector 34.4 25.3 25.3 40.9

Net cost of financial debt of holding sector (2) (24.4) (31.8) (31.8) (7.7)

Operating costs of holding sector (24.5) (30.8) (30.8) (25.8)

Change from derivatives (rates and shares) (49.5) (4.3) (4.3) (22.7)

Other incomes and expenses (3) (10.6) (15.3) (17.9) (49.0)

Income tax 7.5 (0.2) (0.6) 54.0

Income before depreciation and amortization (4) (69.2) 118.9 110.4 (131.2)

Group share (80.0) 122.8 118.4 (86.9)Minorities share 10.8 (3.9) (8.0) (44.2)

Depreciation and amortization (30.3) (33.8) (33.8) (46.6)

Consolidated income IFRS (99.5) 85.1 76.6 (177.8)

Group share (106.3) 92.9 88.5 (120.9)Minorities share 6.8 (7.8) (11.9) (56.9)

in € million 06/2011 06/2010* 06/2010 06/2009

INVESTOR PRESENTATION

Change in net income compared to Pro Forma* June 2010

- 57 -

85

14

269

29 -45-99

-217

IFRSNet income

06/2011

IFRSNet income

06/2010*

Other items**

Increase in companies‟results

consolidatedunder equity

method

Increase in companies‟ operating income

Change inderivatives

(in €m)

(*) Pro forma reflecting exit of scope of B&B Hotels

(**)Including increase in revenues of Holding activity (+€9m) and positive change of financing costs

and overheads of holding activity (+€14m).

Change in fair value of investment properties

Changein realized

capital gains

-217

INVESTOR PRESENTATION

A solid financial situation

- 58 -

(in €m) H1 2011 H1 2010 %

Eurazeo cash position (NAV) 769.4 722.4 6.5%

Consolidated net debt 5,953.1 6,269.1 -5.0%

Consolidated leverage* 2.6x 3.2x -19%

• New investments with moderate leverage

• Successful refinancing of the revolving credit line

• Cash position proforma of investments in Foncia and Moncler

and sale of LT participations (Ipsos) ~€200m

(*) Consolidated leverage = (consolidated net debt – value of assets which do not contribute to adjusted consolidated EBITDA) / adjusted consolidated EBITDA

Subsequent events:

INVESTOR PRESENTATION

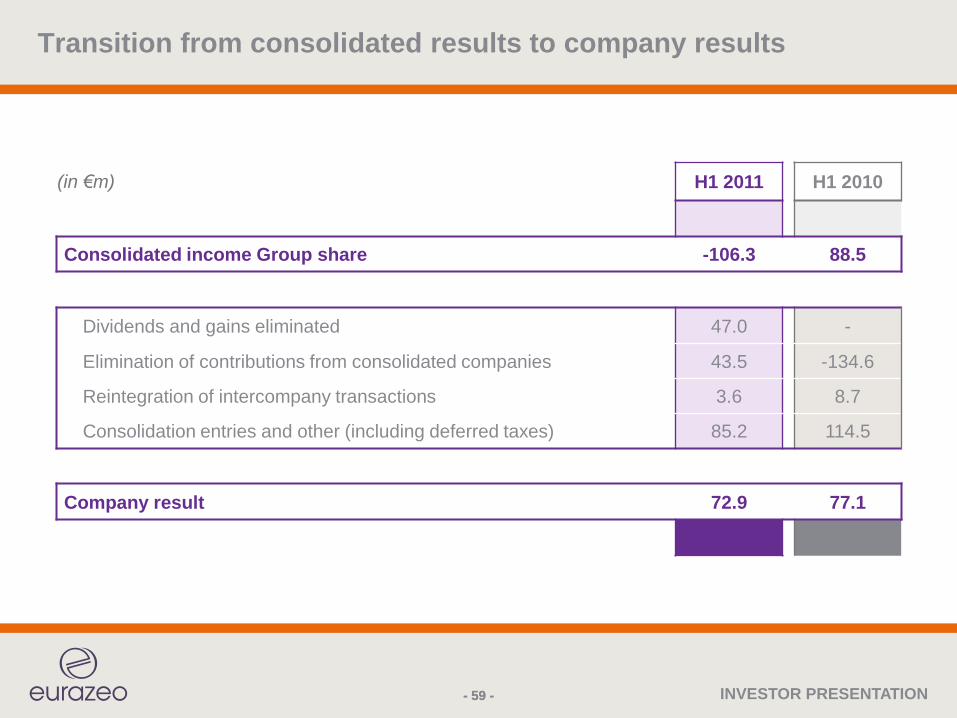

Transition from consolidated results to company results

- 59 -- 59 -

(in €m) H1 2011 H1 2010

Consolidated income Group share -106.3 88.5

Dividends and gains eliminated 47.0 -

Elimination of contributions from consolidated companies 43.5 -134.6

Reintegration of intercompany transactions 3.6 8.7

Consolidation entries and other (including deferred taxes) 85.2 114.5

Company result 72.9 77.1

INVESTOR PRESENTATION

Strong increase in companies‟ results

- 60 -

(1) 2010 pro forma adjusted for exit of B&B Hotels.

(in €m) H1 2011 H1 2010(1) %

Consolidated revenues 1,907.7 1,810.9 +5.3%

Europcar 61.4 62.2 -1.3%

Elis 87.2 84.2 +3.5%

APCOA 13.8 12.6 +9.6%

ANF 38.1 27.2 +40.1%

Adjusted EBIT 200.5 186.2 +7.7%

Profit from equity affiliates 35.2 9.5 +269.1%

Total 235.7 195.8 +20.4%

INVESTOR PRESENTATION

Use of cash

- 61 -

909

557

December 31,

2010

in €m

• Cash proforma of investment of Moncler ~€200m

• Successful refinancing of Eurazeo‟s syndicated credit line during summer 2011

(102)

(64)

(67)75

(154)

(40)

Dividends

received

Dividends

paidReimbursement

of Immobilière

Bingen‟s debtFinancial costs

Fonroche & Foncia

invest. & sale

of LT (Ipsos)

Other

August 29,

2011

Amount: €1bn Maturity: July 2016

INVESTOR PRESENTATION- 62 -

1st Half 2011 consolidated results

Operational performance in H1 2011

INVESTOR PRESENTATION

6,163

910

559

501

359

45

2,973

5,745

904

522

461

330

34

2,849

Rexel

Europcar

Elis

Edenred**

APCOA

ANF

Accor

Revenue growth across the board

- 63 -

REVENUES (€m)

Strong momentum in Latin America. Improvement in Europe, reflecting first signs of stabilization in Central Europe

Sustained growth of financial revenues: +16.0%

Strong growth led by steady rise in occupancy rates and a gradual recovery in average room rates

Continued volume recovery in the various segments, mainly airports, on-street and shopping centers, and solid commercial performance

Acceleration of Hotel and Health segments growth, recovery of Industry segment in France.International: growth in all geographies

Growth on a comparable basis in H1 2011 in all geographies (Europe +5.6%, North America +7.9%, Asia-Pacific +6.6%) supported by prices increases and accelerating growth in volume

H1 2010

H1 2011

+7.8%

+5.8%

+2.3%

+0.1%

+9.8%

+6.1%

(*) Change „2011/2010‟ at constant perimeter and exchange rates (**) Including Financial Revenues

Change lfl*

Market recovery limited to low-contributive segments and increased competition

Selective approach of business with sustained pricing strategy and exit from unprofitable contracts

+9.1%

+4.4%

+7.1%

+0.7%

+8.6%

+7.3%

Change

Like-for-like growth driven by the increase in city-center retail rents & residential vacancy reduction

Excluding one-off effect of litigation with PrintempsDepartment Store (+€7.8m): +12.3%

+36%+33%

INVESTOR PRESENTATION

334

61

174

167

24

31

199

257

62

167

155

21

27

156

Rexel

Europcar

Elis

Edenred

APCOA

ANF

Accor

Portfolio companies grew operating profit

- 64 -

Operating flow-through ratio before digital extra costsclose to 50%Operating EBIT (excl. Financial revenues): +10.8% lflFinancial EBIT: +16.0% lfl

Change lfl*

Significant growth as a result of volume effect and good drop-through ratio (49% at the group level, despite the impact of Ivory Coast and Egypt)

Profitability improvement driven by revenue growth combined with tight cost control, more selective commercial policy and successful contracts renegotiation in the UK

Negative mix effect due to lower profitability of international activities

2010 comparison basis is high due to non-recurring items. Excl. one-off effect: +5.7%

EBITDA margin up 90bps mainly thanks to increasein gross margin (+10bp) and good control over costs

+10.1%

+44.0%

+1.0%

-1.9%

+12.1%

+29.4%

(*) Change „2011/2010‟ at constant perimeter and exchange rates(1) EBIT for Accor and Edenred, EBIT restated for interest expense included in fleet operating lease rents for Europcar,

EBITDA for Rexel, recurring EBITDA for ANF, EBITDA for all other companies(2) Including Financial Revenues

OPERATING PROFIT (1) (€m)H1 2010

H1 2011

(2)

Reinvestment of productivity gains and pricing strategy into brand enhancement and new marketing initiatives

Stable operating margin on tight fleet management and cost control despite modest revenue growth

Profitability increase due to rise in rents+11.4%

Change

+10.8%

+27.6%

+4.0%

-1.3%

+8.0%

+29.7%

+11.4%

INVESTOR PRESENTATION

Rexel

Europcar

Elis

Edenred

APCOA

ANF

Accor

Net debt

- 65 -

NET DEBT*1 (€m)H1 2010

H1 2011LEVERAGE1,2

Quasi debt-clearing at year end. Impact of the asset disposal program.

Limited use of debt

Debt increase driven by a weak performance in H2-2010 and contract renegotiation in the UK. Stable leverage

Impact of demerger costs (€ 42m), dividend (€ 127m) and change in exchange rates (€ 79m)

Impact of international acquisitions (Spain, Switzerland, Italy) and IT investment

Slight increase of cost of vehicle per unit and refinancing cost impact

Strong cash flow generation2,364

3,528

1,940

338

634

489

559

2,535

3,358

1,857

320

602

472

964

Rexel

Europcar

Elis

Edenred

APCOA

ANF

Accor

%/pt Change „H1 2011/H1 2010‟

+6.4%

-0.0x

+0.2x

+9.0%

+0.0x

+0.0x

-0.9x

-42.0%

+3.7%

+5.3%

+5.6%

+4.5%

+5.1%

-6.7%

40%

31%

16.7%

23.1%

30%

30%

11.7x

11.9x

3.9x

3.0x

5.3x

5.3x

5.5x

5.5x

(*) End of June debt(1) Accor: excluding discontinued operations (Edenred, demerged during the period, and Groupe Lucien Barrière and the Onboard Train Services

business, reclassified in discontinued operations in accordance with IFRS 5). Ratio S&P – FFO/Net debt including fixed leasing.(2) Edenred: Ratio S&P – FFO/Net debt ANF: LTV ratioEuropcar : leverage calculated as Net debt including leasings/EBITDAAPCOA, Elis, Rexel: net debt / EBITDA

INVESTOR PRESENTATION

Eurazeo‟s NAV as of June 30, 2011

- 66 -

% held No. shares

Share price

in €

NAV as of

June 30, 2011 (in €m)

With ANF at NAV(1)

ANF @ €39.6

Private investments 1,521.3

Groupe OFI(1) 128.7

Public investments 1,512.9

Rexel 21.55% 57,923,503 16.60 961.6

LT (Ipsos) 24.98% 32.46 55.2

Accor 8.85% 20,101,821 29.17 586.3

Edenred 8.90% 20,101,821 20.13 404.7

Net debt Accor/Edenred -494.9

Accor/Edenred net*(2) 20,101,821 496.1

Real Estate 563.2 661,5

ANF net 51.72% 14,337,178 32.70 468.8 567,0

Colyzeo and Colyzeo 2(2) 94.4

Other public shares 0.0

Danone (pledged EB) 2.53% 16,433,370 42.60 700.0

Debt Danone (EB) -700.0

Danone net 0.0

Other assets 23.8

Eurazeo Partners 8.3

Other (SFGI, ...) 15.4

Cash 769.4

Non-affected debt -110.3

Tax on latent capital gains

and other tax assets-104.9 -124.2

Treasury shares 3.42% 2,145,140 94.0

TOTAL VALUE OF ASSETS AFTER TAX 4,398.0 4 ,477.0

NAV PER SHARE 70.1 71.4

NUMBER OF SHARES 62,743,286 62,743,286

(*) Net of allocated debt(1) OFI PEC shares are valued on the basis of the NAV communicated by OFI PEC. OFI PE Commandite shares and Eurazeo-PME shares

are valued at their acquisition price. The NAV presented here includes OFI PEC‟s holdings of 76.4%.(2) Accor/Edenred shares held indirectly through Colyzeo funds are included on the line for these funds.

Methodology: compliant

with IPEV guidelines

- Private investments:

valuation primarily based

on multiples of comparables

or of transactions. Values

retained were the subject

of a detailed review by an

independent professional

appraiser

- Public companies: average

over a 20-day period of the

volume-weighted share price

INVESTOR PRESENTATION

Eurazeo‟s NAV as of August 29, 2011

Methodology: compliant

with IPEV guidelines

- Private investments: based

on June 30, 2011 valuation

- Update of listed securities,

cash assets and treasury

shares as of August 29, 2011

(*) Net of allocated debt (1) OFI PEC shares are valued on the basis of the NAV communicated by OFI PEC. OFI PE Commandite shares and Eurazeo-PME shares

are valued at their acquisition price. The NAV presented here includes OFI PEC‟s holdings of 95.3%.(2) Accor/Edenred shares held indirectly through Colyzeo funds are included on the line for these funds.

% held No. shares

Share price

in €

NAV as of August 29,

2011 (in €m)

With ANF at NAV(1)

ANF @ €39.6

Private investments 1,732.7

Groupe OFI(1) 157.6

Public investments 1,101.7

Rexel 21.55% 57,923,503 13.74 735.9

Accor 8.85% 20,101,821 24.81 498.7

Edenred 8.90% 20,101,821 17.88 359.4

Net debt Accor/Edenred -492.2

Accor/Edenred net*(2) 20,101,821 365.8

Real Estate 541.8 669.9

ANF net 51.63% 14,337,178 30.61 439.9 567.0

Colyzeo and Colyzeo 2(2) 102.9

Other public shares 0

Danone (pledged EB) 2.53% 16,433,370 42.60 700.0

Debt Danone (EB) -700.0

Danone net 0

Other assets 21.4

Eurazeo Partners 7.0

Other (SFGI, ...) 14.4

Cash 557.1

Non-affected debt -110.3

Tax on latent capital gains

and other tax assets-85.0 -110.2

Treasury shares 3.58% 2,259,617 81.0

TOTAL VALUE OF ASSETS AFTER TAX 3,997.9 4,100.9

NAV PER SHARE 63.3 64.9

NUMBER OF SHARES 63,141,655 63,141,655

- 67 -

INVESTOR PRESENTATION

Appendices

- 68 -

Financial appendices

Group companies‟ detailed information

Other information

INVESTOR PRESENTATION

Strong 1st Half 2011 revenue performance,up 5.8% like-for-like to €2,973m, led by steady rise in occupancy rates and a gradual recovery in average room rates

Successful disposal of Le Nôtresold to Sodexo at an enterprise value of €75m; Closing expected by the end of September

Successful refinancing of existing facility, with €1.5 bn Syndicated Line of Credit

ECONOMIC INTEREST

8.85%EQUITY METHOD

- 69 -

INVESTOR PRESENTATION

1st Half 2011 highlights

- 70 -

H1 like-for-like Q2 2011

Hotels +5.9% +6.1%

Upscale and Midscale Hotels +6.0% +6.2%

Economy Hotels excluding the U.S. +6.4% +6.7%

Economy Hotels in the U.S. +3.7% +3.4%

Acceleration of the performance in the 2nd Quarter

France: strong performance in the 2nd

Quarter. Revenues up 7.4% like-for-like in Up & Midscale and 5.7% in the Economy also thanks to the Paris Airshow in June

H1 like-for-like Total

EBITDAR +9.7% €897m

EBIT +44% €199m

Robust growth of EBITDAR and EBIT

Good flow-through ratio standing at 49% at the group level, despite the impact of Ivory Coast and Egypt

Accor is on track to meet its full year target of 30,000 new rooms and the two-year target of €1.2bn impact on the net debt from asset disposal

- 13,700 rooms were opened in the period, 78% of which under management and franchise contracts, in line with the asset right strategy

- Two Sale & Management-Back agreements signed in July: Pullman Bercy (€105m - 6.5% yield) and Sofitel Paris Arc de Triomphe (€69m)

On May, Accor closed a €1.5bn syndicated line of credit with a group of leading banks

- Replacing the €2bn syndicated credit facility signed in June 2007, subsequently reduced to €1.7bn, expiring in June 2012

- This new five-year facility will lengthen the average maturity of Accor‟s financing at favorable conditions

INVESTOR PRESENTATION

Financials

Note: PF = Pro Forma = Excluding discontinued operations (Edenred, demerged during the period, and Groupe Lucien Barrière

and the Onboard Train Services business, reclassified in discontinued operations in accordance with IFRS 5).

January – June (€m) H1-2011 H1-2010Reported

change

Comparable

change

Revenue 2,973 2,849 +4.4% +5.8%

EBITDAR

% margin

897

30.2%

835

29.3%

+7.5%

+0.9pt

+9.7%

+1.1pt

EBIT

% margin

199

6.7%

156

5.5%

+27.6%

+1.2pt

+44.0%

+2.0pt

Net debt 559 964 -42.0%

IFRS

- 71 -

INVESTOR PRESENTATION

European leader in hospitality and world leader

in prepaid services

Key strengths Major global Hotels group

Global leader in vouchers, 30 million users per year

Successful implementation of a clear and ambitious strategy

Refocus on the hotel business and Services segment

“Asset-right” strategy decreasing volatility

Recognized brands covering every segment of the hotel sector, from luxury to budget

Hotels‟ EBITDAR margin in top quartile

Prepaid Services model: strong growth and highly cash flow generative

Strong expansion opportunity

Resilience of the budget hotel segment and prepaid services

The deal Date of initial investment: May 2005 through Colyzeo

Increased stake: May 2008 in concert with Colony (27.26% as of Feb. 01, 2011)

Eurazeo‟s investment: €489m in equity and €468m in initial gross debt

Eurazeo‟s direct share: 8.86% as of December 31, 2010,2 seats on a 11-members Board of Directors (in addition to the respective 2 seats granted to Colony)

Financing Eurazeo‟s pro-rated stake of nominal of debt on LH19: €488m (after refinancing)

Maturity: 2015 (extended in November 2010)

Covenants: LTV and Accor‟s/Edenred‟s share liquidity

Key figures Key value-added plans Effective demerger

Hotels: Development of franchise model and acceleration of asset disposals

(€m) 2008 2009 PF 2010

Consolidated data as reported

Revenues 6,776 5,490 5,948

EBITAR 1,872 1,518 1,814

EBIT 569 235 446

Net debt 750 1,321 730

- 72 -

Note: PF = Pro Forma = Excluding discontinued operations (Edenred, demerged during the period, and Groupe Lucien Barrière

and the Onboard Train Services business, reclassified in discontinued operations in accordance with IFRS 5).

INVESTOR PRESENTATION

Intense business activitywith strong financial results

Guidance reiterated

INTEREST

51.7%FULLY CONSOLIDATED

- 73 -

INVESTOR PRESENTATION

1st Half 2011 highlights

Strong financial results

- 2011 H1 Rents +36% ; like-for-like growth by 12% ; 23% on city-center portfolio

- 15% increase in recurring cash-flow

- Printemps (Lyons) renewal rent fixed by Court at €2.1m (vs. €0.4m)

One-off impact on revenues for €7.8m (June 2006- Dec 2010)

Appraisal = €1,607m

- NAV= €40.5 per share

- Low gearing, LTV= 30%

In market liquidity

- Integration of EPRA Index still an objective for March 2012

- 74 -

INVESTOR PRESENTATION

Financials

January – June (€m) H1-2011 H1-2010 Reported changeComparable

change

Rents 45.2 34.0 33.0% 35.8%*

City-center 28.8 17.7

B&B 16.5 16.2

EBITDA

Recurring EBITDA

% margin

38.3

30.5

81.6%

27.4

27.4

80.6%

40.0%

11.4%

1pts

Current cash flow

Recurring cash flow

Per share

29.6

21.7

0.80

18.9

18.9

0.69

56.8%

15.3%

15.1%

15.2%

NAV 40.5 38.5 5.2%

LTV 30% 30% -

IFRS

- 75 -

* Including one-off impact from Printemps; recurring rents: +12.3%

INVESTOR PRESENTATION

Lyons

- 76 -

INVESTOR PRESENTATION

Marseilles

- 77 -

INVESTOR PRESENTATION

Sustained growth in revenueon the back of continued traffic recovery in existing contracts

Recovery in EBITDA margin thanks to the successful renegotiation of UK contracts, a more selective approach on new business and a tight control on costs

Net debt under control,with continued improvement in liquidity management and working capital

INTEREST

81.2%FULLY CONSOLIDATED

- 78 -

INVESTOR PRESENTATION

1st Half 2011 highlights

H1 2011 revenues of €359.5m, up 9.1% vs. H1 2010 on a reported basis and +7.8% on a comparable basis

- Strong performance in the existing business, with rebound in all key segments

- Sustained commercial performance

H1 2011 EBITDA of €23.6m, up 10.8% vs. H1 2010 on a reported basis and +10.1% on a comparable basis

Clean-up of the legacy issues, which have affected the company in the past, and initiatives to enhance the quality of the business, which should both continue to benefit the company in H2 2011

- Successful renegotiation of main loss-making contracts in the UK, which should fully benefit

the company in H2 2011

- More selective approach on new business, to enhance the margin and the cash generation of the portfolio

- Continued control on costs

- 79 -

INVESTOR PRESENTATION

Financials

January – June (€m) H1-2011 H1-2010Reported

change

Change at constant

exchange rates

Revenue 359.5 329.6 +9.1% 7.8%

EBITDA

% margin

23.6

6.6%

21.3

6.5%+10.8% 10.1%

Net debt 634 602

- 80 -

INVESTOR PRESENTATION

European leader in the management of paid car parks

The deal Date of initial investment: April 2007

Purchase price multiple: 16.5x LTM* EBITDA

Enterprise value: €885m (€391m in equity)

Vendor: Investcorp

1st investment of Eurazeo in a non-French company

Eurazeo‟s share: 81.2% as of December - 5 seats on a 6-member Board of Directors

Key strengths Parking market growth driven by:

Growing population leading to increase in the number of cars

Substitution from unpaid to paid parkings

Outsourcing of parking management

Favorable price trend

Strong competitive position: #1 in Europe in terms of parking spaces (1.3 m)

Largest airport car park operator in Europe

Diversified client base and good visibility on contracts

Ongoing value creation initiatives (improvement of operational performance, procurement, yield management, new business,…)

Balanced portfolio: Multi-contract (80% lease, 20% management), multi-country (18), multi-segment (active on every market segment)

Financing Net debt as at December 31, 2010: €608m

Maturity: 2014

Senior and 2nd lien debt, 100% bullet financing

80% hedged until 2012

Key figures (as reported)Key value-added plans

3 key acquisitions:

CPS Europe (#2 on-street player in the UK) WPS (Germany) RPS (Sweden)

Major effort put on overhead optimization

Zero Base program on 3 items: Cost and quality efficiencies, yield management and procurement

(€m) 2006 2007 2008 2009 2010

Consolidated data German standards

Revenues 490 589 642 640 700

EBITDA 53 57 63 53 51

Net debt 596 555 591 608

* LTM: Last Twelve Months

- 81 -

INVESTOR PRESENTATION

Robust growth in H1 2011, with an acceleration in Q2:

Issue volume up 10% like-for-like,with 21% growth in Latin America

Funds from operations up 20% like-for-like,in line with the Group‟s guidance of normalized growth over 10% per year like-for-like

EBIT up 12.1% like-for-like, operating flow-through ratio of 49% before digital extra costs

FY 2011 EBIT target: €340m to €360m

INTEREST

8.90%EQUITY METHOD

- 82 -

INVESTOR PRESENTATION

1st Half 2011 highlights

- 83 -

LflIssue Volume France

Rest of Europe Europe

Latin America

H1 2011 +10.0% +2.3% -0.3% +0.6% +21.0%

o/w Q1 +9.0% +2.9% -2.0% -0.3% +20.5%

o/w Q2 +10.9% +1.7% +1.3% +1.4% +21.5%

Issue Volume: faster growth in Q2, reflecting robust business

in Latin America and first signs of stabilization in Central Europe

Robust business in Employee Benefits (+10% lfl in H1),

Expense Management (+19% lfl in H1) and Public Social

Programs (+17% lfl in H1)

Incentive & Reward negatively impacted by the B2C Kadéos

gift activity (-3% lfl in H1)

Europe: excluding CONSIP contract loss in Italy,

Q2 lfl growth would be up +3.7% (vs. +2.2% in Q1),

reflecting first signs of stabilization in Central Europe

Latin America: Strong momentum in Q2, thanks to job

creation and higher penetration rates and face value

Issue Volume:

Operating revenue (excluding financial revenue):

Operating EBIT (excluding financial revenue):

• Up +10.8% like-for-like, operating flow-through ratio of 49% before digital extra costs

• +1.8 pts lfl improvement before digital extra costs of operating EBIT as a % of operating revenue

LflOperating revenue France

Rest of Europe

Latin America

H1 2011 +9.2% -0.3% +3.0% +18.5%

o/w Q1 +6.6% -1.1% -1.1% +17.4%

o/w Q2 +11.7% +0.6% +7.5% +19.5%

France: Positive trends in meal vouchers: up +4.2% lfl in Q2 (vs. +2.9% lfl in Q1)

Still a difficult situation in the B2C gift segment, due to business disruption with the largest distributor FNAC (down -36.0% lfl in Q2)

Rest of Europe: Better trends in core business mainly driven by first signs of stabilization in Central Europe

INVESTOR PRESENTATION

Financials

January – June (€m) H1-2011 H1-2010 Reported changeComparable

change

Issue Volume 7,264 6,615 +9.8% +10.0%

Operating Revenue 456 422 +8.1% +9.2%

Financial Revenue 44 39 +14.8% +16.0%

Total Revenue 501 461 +8.6% +9.8%

Operating EBIT

% Op. EBIT/IV

123

1.7%

116

1.8%

+5.7% +10.8%

Total EBIT 167 155 +8.0% +12.1%

Net debt 338 320

IFRS

- 84 -

INVESTOR PRESENTATION

European leader in hospitality and world leader

in prepaid services

Key strengths Major global Hotels group

Global leader in vouchers, 30 million users per year

Successful implementation of a clear and ambitious strategy

Refocus on the hotel business and Services segment

“Asset-right” strategy decreasing volatility

Recognized brands covering every segment of the hotel sector, from luxury to budget

Hotels‟ EBITDAR margin in top quartile

Prepaid Services model: strong growth and highly cash flow generative

Strong expansion opportunity

Resilience of the budget hotel segment and prepaid services

The deal Date of initial investment: May 2005 through Colyzeo

Increased stake: May 2008 in concert with Colony (27.26% as of Feb. 01, 2011)

Eurazeo‟s investment: €489m in equity and €468m in initial gross debt

Eurazeo‟s direct share: 8.90% as of December 31, 2010,2 seats on a 12-members Board of Directors (in addition to the respective 2 seats granted to Colony)

Financing Eurazeo‟s pro-rated stake of nominal of debt on LH19: €488m (after refinancing)

Maturity: 2015 (extended in November 2010)

Covenants: LTV and Accor‟s/Edenred‟s share liquidity

Key figuresKey value-added plans Effective demerger

Services: Continuation of strong dynamic development (country/product) and resume acquisitions

(€m) 2007 2008 2009 2010

Consolidated data

Revenues 837 946 902 965

Operating EBIT 224 236 233 248

Net debt 429 323 303 25

- 85 -

INVESTOR PRESENTATION

Growth driven by acceleration of hotel and

health segments growth, recovery of industry

segment in France and international

development

Sales +7.1% and EBITDA +4.0%

INTEREST

81.7%FULLY CONSOLIDATED

- 86 -

INVESTOR PRESENTATION

Elis is a value-added service provider of textile and

hygiene services in 4 market segments

- 87 -

INVESTOR PRESENTATION

1st Half 2011 highlights

- 88 -

H1 2011 Like-for-like

Sales +7.1% +2.3%

France +2.1% +2.0%

Hotels & Restaurants +5.1% • Acceleration of the growth

Industry, Trade and Services +1.9% • Slight recovery

Health market +3.4% • Continued growth

International +38.2% +3.2%

Production +5.0% +5.1%

Sales

H1 2011 Like-for-like

EBITDA +4.0% +1.0%

EBITDASlight decrease in margin due to:

• Greater weight of international (margin

slightly lower than in France) in growth

• Excluding one-off effect,

H1 2011 EBITDA: +5.7%

INVESTOR PRESENTATION

Financials

- 89 -

January – June (€m) H1-2011 H1-2010Reported

change

Like-for-like

change

Revenue 559.0 522.0 +7.1% +2.3%

EBITDA

% margin

173.6

31.0%

166.9

32.0%

+4.0% +1.0%

Net debt 1,940 1,857

INVESTOR PRESENTATION

Launch of new products

Product innovation

- 90 -

Extremely promising start of Duo ‘duvet+bedding’ launched in February 2011

More than 50 customers have signed for a monthly revenue of €70k (or €840k on an annual basis)

Ramp-up of Range Exclusiv’ launched in 2010

(1) Rebased to 100

100129 130

166

287

396

469500

532

100

150

200

250

300

350

400

450

500

550

600

nov.-10 déc.-10 janv.-11 févr.-11 mars-11 avr.-11 mai-11 juin-11 juil.-11

Range Exclusiv'

Turnover Evolution (1) - Europe

INVESTOR PRESENTATION

Market opening:

First University Hospital (CHU) in France

- 91 -

• Elis continues to open the market

(defined as service of rental and

maintenance of textile)

• The conversion to outsourcing

of textile maintenance in public

hospitals represents a significant

market and may contribute to the

reduction of costs in the hospitals

This is a key achievementElis has just been selected to outsource

the laundry of Caen University

Hospital. Beyond the contract size,

it is essential to notice that this is

the first university hospital of France

outsourcing this activity.

This Hospital becomes the largest

Healthcare institution of Elis.

INVESTOR PRESENTATION

60

70

80

90

100

ID‟Elis continuous improvement

- 92 -

2010

2011

DecemberOctoberAugustJuneAprilFebruary

The ID‟Elis program continues to deliver

(*) Rebased to 100

An effort has been undertakento reduce the number of Service reps who don‟t develop their customers

60

70

80

90

100

DecemberOctoberAugustJuneAprilFebruary

Continued reduction of detergents per Kg Continued reduction of energy per Kg

20%

30%

40%

50%

60%

DecemberOctoberAugustJuneAprilFebruary

Rate of service reps who haven‟t signed new

contracts qualified as rate of non-signature

INVESTOR PRESENTATION

European policy for

Human Resources development

• Development of partnerships with

Engineering Schools (ex: ENSAM) and

Business Schools (ex: EUROMED) to attract

strong candidates with solid potential

• Start of a European recruitment policy

• Exchange program of middle managers

within the European countries

• Creation of new tools to improve visibility

of Elis brand Vs potential candidates

all over Europe

- 93 -

INVESTOR PRESENTATION

Acquisitions / strategic agreements

Status on integration of September 2010 acquired businesses in Spain

• 2 factories have been closed and production has been reallocated to reduce logistic costs

• Integration of acquired businesses (customer relationship, invoicing and accounting)

within Elis IT systems

• Reorganization of deliveries to optimize logistic costs under process (several routes already

saved but remaining potential identified)

• Overall reorganization costs slightly above expectations

Elis continues to expand in Spain and Switzerland:

• As a result of the acquisition of Blanchatel in H1 2011:

- More than 350 collaborators in Switzerland spread over 7 industrial sites

- Consolidated annual revenues exceeding 34 million Euros in Switzerland

- Reinforcement of leadership in Swiss Romandy in rental and cleaning of textiles for the hospitality and healthcare sectors

• Exclusive agreement with LHA laundry (Andalucia):

- An Elis service center will be created in the premises of the laundry. LHA will concentrate on the production

- With Seville and Archidona, improved coverage of Andalucia (area of more than 10 million inhabitants)

- 94 -

INVESTOR PRESENTATION

European leader in textile rental and cleaning

The deal Date of initial investment: October 2007

Purchase price multiple: 7.3x LTM* EBITDA

Enterprise value: €2,276m (€393m in equity)

Vendor: PAI partners

Eurazeo‟s share: 81.8% - 5 seats on a 7-member Board of Directors

Key strengths European leader with a market share of approx.12% and strong leader in France

Steady growth over the past 40 years and resilient business

Demonstrated capacity to withstand difficult market conditions (SARS, September 11,…)

Long term contracts (3 to 4 years on average)

Consolidation opportunities

Development of cross-selling

Key figures (as reported)

Key value-added plans 8 bolt-on acquisitions in 2010 (International: 4, mainly Switzerland and Spain, France: 4, 5 in 2009, 6 in 2008 and 2 in 2007 (CWS France and CWS Spain)

Significant improvement program launched beginning 2009 on three items:

Revenue growth Cost control Improvement of working capital

Numerous growth initiatives in 2010: Reinforcement of international sales force and of marketing and commercial structure in France

(€m) 2006 2007 2008 2009 2010

Consolidated data

Revenues 936 993 1 036 1 042 1 068

EBITDA 291 318 327 335 347

Net debt 1,842 1,878 1,868 1,920

* LTM: Last Twelve Months

Financing Debt as of december 31, 2010: €1,920m

Maturity : 2014-2017

- 95 -

INVESTOR PRESENTATION

Stable profit and new investments

despite adverse market conditions

3Y Plan initiatives underwayINTEREST

85.1%FULLY CONSOLIDATED

- 96 -

INVESTOR PRESENTATION

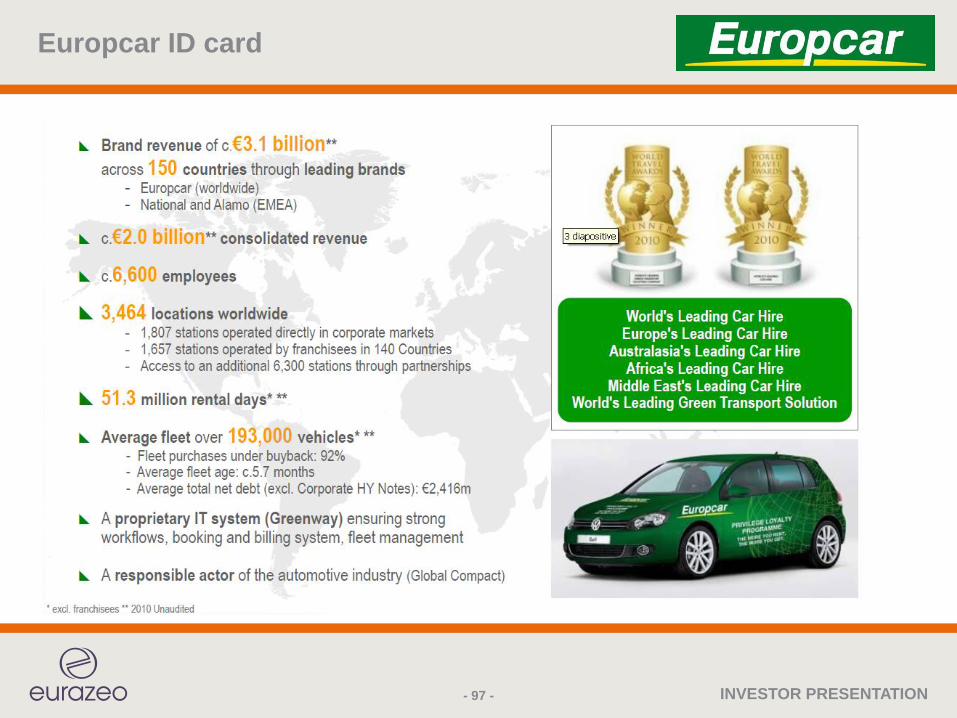

Europcar ID card

- 97 -

INVESTOR PRESENTATION

The European leader with global reach

- 98 -

INVESTOR PRESENTATION

1st Half 2011 highlights

Revenue and adjusted operating income stable vs H1 2010

- Market: recovery limited to low-contributive segments and increased competition

- Europcar: selective approach of business with sustained pricing strategy

(RPD improvement of 1.5% at constant exchange rates) and exit from unprofitable contracts

- Reinvestment of productivity gains and pricing strategy into brand enhancement

and new marketing initiatives

- Stable operating margin on tight fleet management and cost control despite modest revenue

growth

3Y Plan initiatives underway

- Systematic customer satisfaction assessment

- Advertising campaigns

- Sponsoring initiatives (Team Europcar)

- Innovation into new urban mobility solutions (car2go)

- 99 -

INVESTOR PRESENTATION

Financials

(1) Excluding acquisition-related and reorganization expenses, as well as non-recurring items, and after add-back of interest expense included in fleet operating lease rents

(2) Net debt at constant exchange rates including notional debt related to fleet operating lease agreements for €1,329m at end June 2011 (€1,104m at end June 2010)

At constant exchange rates Reported

January - June (€m) H1-2011 H1-2010

At 2011

exch. rates

Change H1-2011 H1-2010 Change

Revenue 909.6 908.4 +0.1% 909.6 903.5 +0.7%

Adjusted Operating Income(1)

% margin

61.4

6.7%

62.5

6.9%

-1.9% 61.4

6.7%

62.2

6.9%

-1.3%

Average net debt(2) 3,110 3,024 +2.8% 3,110 3,019 +3.0%

Average operating net debt(excluding corporate High Yield Notes)

2,285 2,224 +2.7% 2,285 2,219 +2.9%

- 100 -

INVESTOR PRESENTATION

European leading car rental company

The deal Date of initial investment: May 2006

Purchase price multiple: 16.5x 2006 EBIT

Enterprise value: €3,083m (€782m in equity, €663m post syndication)

Vendor/seller: Volkswagen

Eurazeo‟s share: 85.1% - 5 seats on a 6-member Board of Directors

Key strengths Growth perspective: market penetration lower in Europe versus U.S.

Leadership position in Europe + strengthening opportunities in U.S. and Australia/Asia through alliances and acquisitions

Operational excellence, notably through a performing IT system and an efficient fleet management

Long-term relationships with car manufacturers and >90% of fleet covered by buyback agreements

Diversification of fleet composition

Quality of teams and a strong corporate culture

Financing Net debt as at December 31, 2009: €2,849 m

Maturity:

Corporate debt: 2013-2018

Fleet debt: 2012-2017

Key figures (as reported)

(€m) 2006 2007 2008 2009 2010

Consolidated data

Revenues 1,469 2,047 2,091 1,851 1,973

Adjusted EBIT 168 276 253 213 243

Average net debt 2,461 3,178 3,532 3,088 3,220

Key value-added plans Acquisition of Vanguard in „07: Europcar became #1 in the UK and strengthened its leadership in Europe

Commercial strategic Alliance with Enterprise, #1 in the U.S.

Acquisition of master franchisee in Australia/New Zealand in 2008

Strong pricing discipline and improved operating and cash efficiency

Proven ability to adapt fleet and cost to lower demand over the crisis

Development of a mobility service (Hamburg, Germany)

- 101 -

INVESTOR PRESENTATION

Solid organic sales growth

Improved profitability

Strengthened financial structure

INTEREST

21.6%EQUITY METHOD

- 102 -

INVESTOR PRESENTATION

Q2 and 1st Half 2011 and highlights

- 103 -

+6.1%

+18.0%

+6.6%

+7.9%

+5.6%

Group

Latin America

Asia Pacific

North America

Europe

Group

(1)

Solid organic sales growth (+6.1%) in H1 2011

• 3rd consecutive quarter in growth in volumes

• Tougher comparable base: Q2 2010 marked the return of the growth

4.9%

5.7%

Q2 2010 Gross margin improvement

Opex reduction

Q2 2011

+10bps

+70bps

(2)

+80bps

• +10bps increase in gross margin in Q2

• EBITA(2) margin up 80bps to 5.7% in Q2

(2)

Improved profitability

Strengthened financial structure

• Free cash flow before interest & tax of €123m

• Indebtedness ratio at 3.0x EBITDA at June 30 (vs 3.19x at Dec 31, 2010)

• Enhanced financial flexibility and extended debt maturity through a €500m bond issue in May 2011

(1) Q2 2011 over Q2 2010 Growth

(2) At comparable scope of consolidation and exchange rates, excluding the non-recurring effect related

to changes in copper-based cables price and before amortization of purchase price allocation

INVESTOR PRESENTATION

Financials

January – June (€m) H1-2011 H1-2010Reported

change

Like-for-like and

same-day change

Revenue 6,163 5,745 +7.3% +6.1%

EBITA

% margin

334

5.4%

257

4.5%+29.7% +29.4%

Net debt 2,364 2,535

- 104 -

INVESTOR PRESENTATION

Worldwide leading distributor of electrical supplies

The deal Date of initial investment: March 2005

Purchase price multiple: 10.3x 2004 EBITDA

Enterprise value: €3,700m (€464m equity share of Eurazeo, co-investor alongside CD&R and MLPE)

Vendor: PPR

Eurazeo‟s share: 21.7% - 3 seats on a 10-member Board of Directors

Key strengths A world leader: #1 in North America, #1 in Asia-Pacific and #2 in Europe

Fragmented market with further potential for consolidation

Well-balanced portfolio of diversified countries and segments

Strong cash generation even in downturn

Sizeable organic growth opportunities: emerging markets prospects and extension of product range

Strong management team with considerable experience in business-to-business distribution

Reactivity in cost structure managementFinancing Debt as at December 31, 2010: €2,273m

3,2x Net debt/EBITDA

Key figures (as reported)

Key value-added plans 2 transforming acquisitions

Gexpro (US): Rexel becomes #1 in the US

Hagemeyer (Neth.): Expansion of European footprint

Development of promising markets: Renewable energies, energy savings, expertise in specific verticals (mining, oil & gas, utilities) and value-added supply chain services

Gross margin improvement through private label offering and supplier relationship management

Working capital optimization, logistics and capexmonitoring

Consolidated data 2005 2006 2007 2008 2009 2010

Revenues 7 377 9,299 10,704 12,862 11,307 11,960

EBITA 372 581 658 630 450 616

Net debt 2 191 2,861 1,607 2,932 2,401 2,273

- 105 -

INVESTOR PRESENTATION

Strong growth and good profitability

Promising international development

€10m additional investment to support international activities and development in other renewable energies

INTEREST

28.4%EQUITY METHOD

- 106 -

INVESTOR PRESENTATION

1st Half 2011 highlights

Strong financial performance

- EBITDA: up to €16.1m (6 months 2011) vs. €1.0m (6 months 2010)

- Consolidated sales: €66.4m (6 months 2011) vs. €13.0m sales (6 months 2010)

Very promising development in Puerto Rico

- Advanced discussions on a 40 MW contract in Puerto Rico

- Continued efforts to start activities in Africa, India and Brazil

- 107 -

Eurazeo has re-invested €10m in June 2011 to support Fonroche‟s

developments outside France and in other renewable energies

INVESTOR PRESENTATION

Financials

(€m)Jan-June 2011

(6 months)

Jan-June 2010

(6 months)

Revenue 66.4 13.0

EBITDA

% margin

16.1

24.3%

1.0

7.6%

Net debt 53.9 (6.2)

- 108 -

INVESTOR PRESENTATION

Long term rental activity still low but strong rebound in short term rental

Strong increase in profitability thanks to the continuing costs and organizational streamlining policy

INTEREST

13.2%EQUITY METHOD

- 109 -

INVESTOR PRESENTATION

1st Half 2011 highlights

Sales decrease limited to 2.0%, thanks to a balanced effect:

- Long term contract hire sales decrease by 4.6% versus H1 2010

- However, the commercial activity suggests an improvement in activity

in the coming months

- Short term rental sales, still very strong, increase by 12.9% versus H1 2011

Profitability

- Strict control over operations costs and overheads enables the company to further

improve its operational margin

- Further improvement expected in 2011 thanks to initiatives launched on purchases

and to the merger of the two French networks

- As during all the crisis, capital gains on resale of used trucks remain positive

- 110 -

INVESTOR PRESENTATION

Financials

January – June (€m) H1-2011 H1-2010

Revenue 338.1 345.1

EBITA Rental

% of sales

54.5

16.1%

54.3

15.8%

Capital Gains 2.7 1.9

EBITA

% of sales

57.4

17.0%

56.5

16.4%

- 111 -

INVESTOR PRESENTATION

Net revenues up 17% to €73.6m, net profit down 32% to €6.1m due to approximately €8m exceptional items affecting the yoy comparison

Wealth Management is stable after the 2010 impressive growth, while the Advisory business shows significant growth

Successful disposal of DNCA to TA Associates and brokerage activities to Kepler focusing on the core businesses

INTEREST

19.4%

- 112 -