investor update - s3.amazonaws.com€¦ · 3 ep energy today oil-focused growth company with four...

TRANSCRIPT

Investor Update June 2014

2

Cautionary Statement Regarding Forward-Looking Statements

This presentation includes certain forward-looking statements and projections of EP Energy. EP Energy has made every reasonable effort to ensure that the information and assumptions on which these statements and projections are based are current, reasonable, and complete. However, a variety of factors could cause actual results to differ materially from the projections, anticipated results or other expectations expressed, including, without limitation, the supply and demand for oil, natural gas and NGLs; EP Energy’s ability to meet production volume targets; the uncertainty of estimating proved reserves and unproved resources; the future level of service and capital costs; the availability and cost of financing to fund future exploration and production operations; the success of drilling programs with regard to proved undeveloped reserves and unproved resources; EP Energy’s ability to comply with the covenants in various financing documents; EP Energy’s ability to obtain necessary governmental approvals for proposed E&P projects and to successfully construct and operate such projects; actions by the credit rating agencies; credit and performance risk of EP Energy’s lenders, trading counterparties, customers, vendors and suppliers; changes in commodity prices and basis differentials for oil and natural gas; general economic and weather conditions in geographic regions or markets served by EP Energy, or where operations of EP Energy are located, including the risk of a global recession and negative impact on oil and natural gas demand; the uncertainties associated with governmental regulation, including any potential changes in federal and state tax laws and regulation; political and currency risks associated with international operations of EP Energy; competition; and other factors described in EP Energy’s Securities and Exchange Commission filings. While EP Energy makes these statements and projections in good faith, neither EP Energy nor its management can guarantee that anticipated future results will be achieved. Reference must be made to those filings for additional important factors that may affect actual results. EP Energy assumes no obligation to publicly update or revise any forward-looking statements made herein or any other forward-looking statements made by EP Energy, whether as a result of new information, future events, or otherwise. This presentation presents certain production and reserves-related information on an "equivalency" basis. Equivalent volumes are computed with natural gas converted to barrels at a ratio of six Mcf to one Bbl. These conversions are based on energy equivalency conversion methods primarily applicable at the burner tip and do not represent value equivalencies at the wellhead. Although these conversion factors are industry accepted norms, they are not reflective of price or market value differentials between product types. This presentation refers to certain non-GAAP financial measures such as “Adjusted EBITDAX“ and “Adjusted Cash Operating Costs Per Unit”. Definitions of these measures and reconciliation between U.S. GAAP and non-GAAP financial measures are included in the Appendix and EP Energy’s First Quarter 2014 Financial and Operational Reporting Package at epenergy.com.

3

EP Energy Today Oil-focused growth

company with four core assets in leading U.S basins

~477,000 total net acres1

~5,644 risked drilling locations1

1Q’14 Results

49.1 MBbls/d oil production

94.7 MBoe/d total production

$357 MM Adjusted EBITDAX

13 rig average

66 completed wells 1 Pro forma for April 2014 acquisition. Notes: See Appendix and 1Q’14 Financial and Operational Reporting Package, available at epenergy.com for the company’s non-GAAP reconciliation and definitions. Acreage and gross drilling locations as 12/31/13.

Net Acres: 91,675 1Q 2014 Net Daily Production (MBoe/d): 46.5 Gross Drilling Locations: 946

EAGLE FORD SHALE

EP Energy Acreage

Net Acres: 175,1731 1Q 2014 Net Daily Production (MBoe/d): 11.9 Gross Drilling Locations: 3,3751

HAYNESVILLE SHALE Net Acres: 36,865 1Q 2014 Net Daily Production (MMcfe/d): 112.2 Gross Drilling Locations: 197

ALTAMONT Net Acres: 173,110 1Q 2014 Net Daily Production (MBoe/d): 13.4 Gross Drilling Locations: 1,126

WOLFCAMP SHALE

TX

UT

TX Acquired acreage

EPE acreage

4

Proven Management Team Name Position

Industry Yrs.

EP/EPE Yrs. Experience

Brent Smolik Chairman, President & CEO 29 7

Clay Carrell EVP & COO 25 6

Dane Whitehead EVP & CFO 29 7

Marguerite Woung-Chapman

SVP, General Counsel 22 22

Joan Gallagher SVP, HR & Admin. Services 20 8

Frank Falleri SVP, Central 28 26

Greg Givens VP, Eagle Ford 17 17

Richard Little VP, Southern 17 11

Scott Anderson VP, Business Development 29 3

Kyle McCuen VP, Planning & Treasury 17 15

Dennis Price VP, Marketing 20 18

Frank Olmsted VP, Controller 23 14

Delaney Bellinger VP, Info. Tech. 30 2

Energy

5

Performance Highlights

Execution Growth

Note: All amounts pro forma for completed and pending asset sales.

Focused execution delivering high-return growth

Concentrated asset base with high degree of operating control

Record well completions

66 wells in 1Q’14

Expect 265 – 290 in FY’14

All programs performed above type curve

Solid multi-year hedges

Significant liquidity

Accelerating oil and equivalent production growth

Expect YOY oil volumes up > 45%

Expect YOY equivalent volumes up 19%1

20+ year of drilling inventory now

~5,644 risked drilling locations

Continued EBITDAX growth

Higher unit margins

1 Year-over-year growth rate 2013 continuing production volumes compared with 2014 continuing production volumes.

6

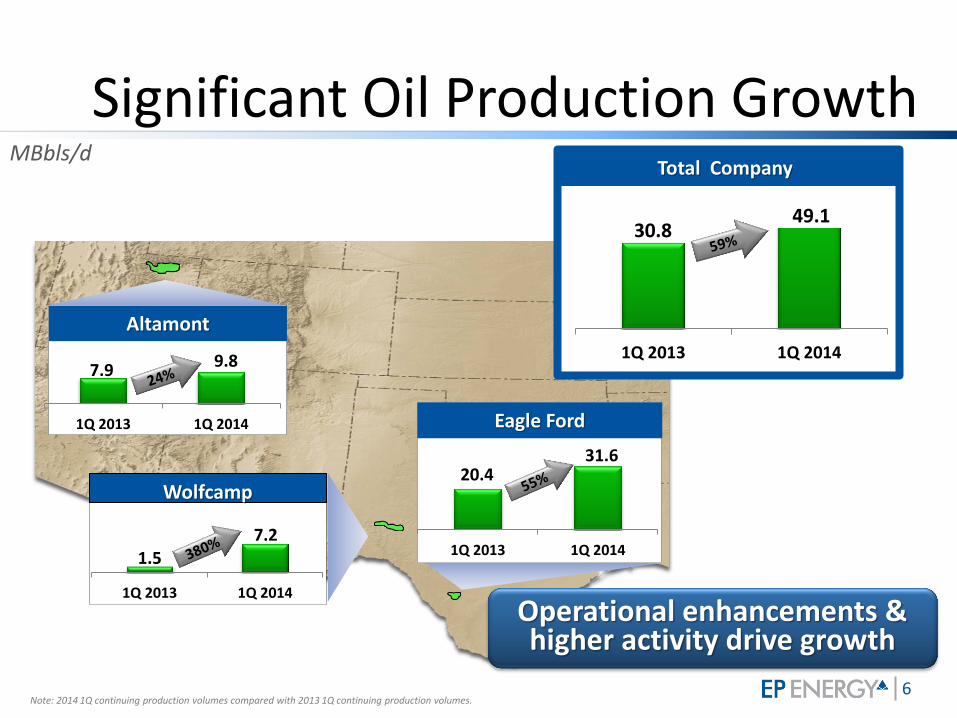

Significant Oil Production Growth

Wolfcamp

1Q 2013 1Q 2014

1.5 7.2

Altamont

9.8 7.9

Eagle Ford

31.6 20.4

Operational enhancements & higher activity drive growth

MBbls/d Total Company1

1Q 2013 1Q 2014

49.1 30.8

Note: 2014 1Q continuing production volumes compared with 2013 1Q continuing production volumes.

1Q 2013 1Q 2014

1Q 2013 1Q 2014

7

High-Quality, Concentrated Asset Portfolio

Wolfcamp Eagle Ford

Altamont Haynesville

A Leading Operator in Each Basin

8

Eagle Ford: Franchise Program Continued growth and improvement in

high-return assets

Six rigs running

Improved run time and reducing unit lifting cost

Record quarterly production in 1Q’14 of 46.5 MBoe/d (31.6 MBbls/d of oil)

135–145 well completions (‘14E)

35 wells completed in 1Q’14

Further upside

Additional efficiencies gains

Testing 40-acre spacing

Testing shorter stage spacing and higher proppant volumes

Significant high-quality oil volume growth

Oil Production (MBbls/d)

2.0 2.5

5.3

8.8 9.8

10.9

15.7

18.5

20.4

22.2

26.1 27.3

1.1

31.6

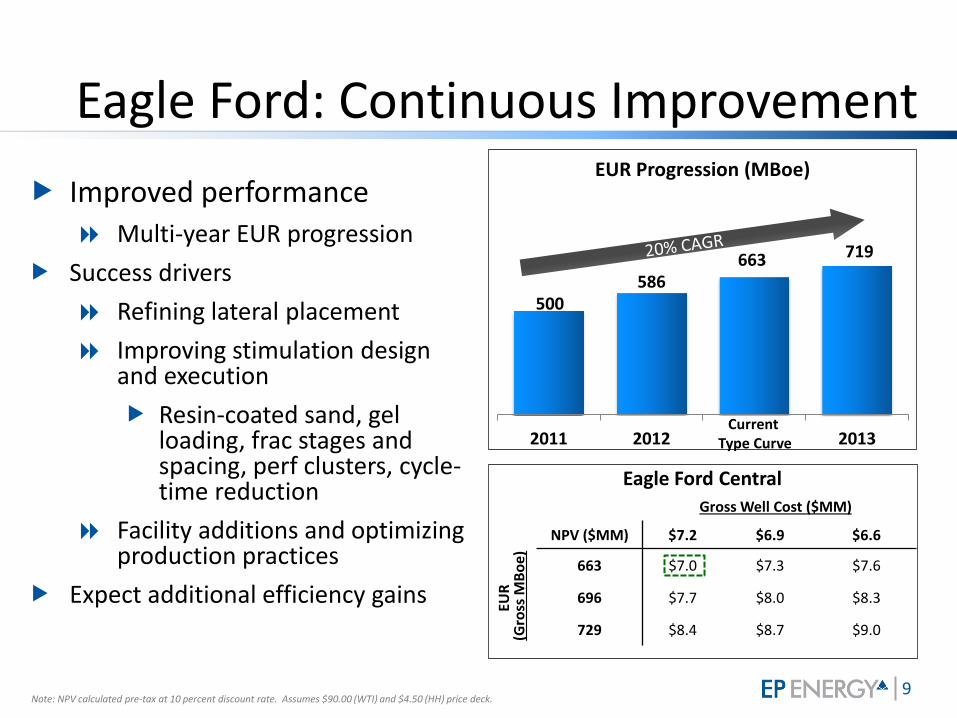

9

500 586

663 719

2011 2012 Current Type Curve 2013

Eagle Ford: Continuous Improvement

Improved performance

Multi-year EUR progression

Success drivers

Refining lateral placement

Improving stimulation design and execution

Resin-coated sand, gel loading, frac stages and spacing, perf clusters, cycle-time reduction

Facility additions and optimizing production practices

Expect additional efficiency gains

EUR Progression (MBoe)

Current Type Curve

Note: NPV calculated pre-tax at 10 percent discount rate. Assumes $90.00 (WTI) and $4.50 (HH) price deck.

Eagle Ford Central

Gross Well Cost ($MM)

E

UR

(G

ross

MB

oe

) NPV ($MM) $7.2 $6.9 $6.6

663 $7.0 $7.3 $7.6

696 $7.7 $8.0 $8.3

729 $8.4 $8.7 $9.0

10

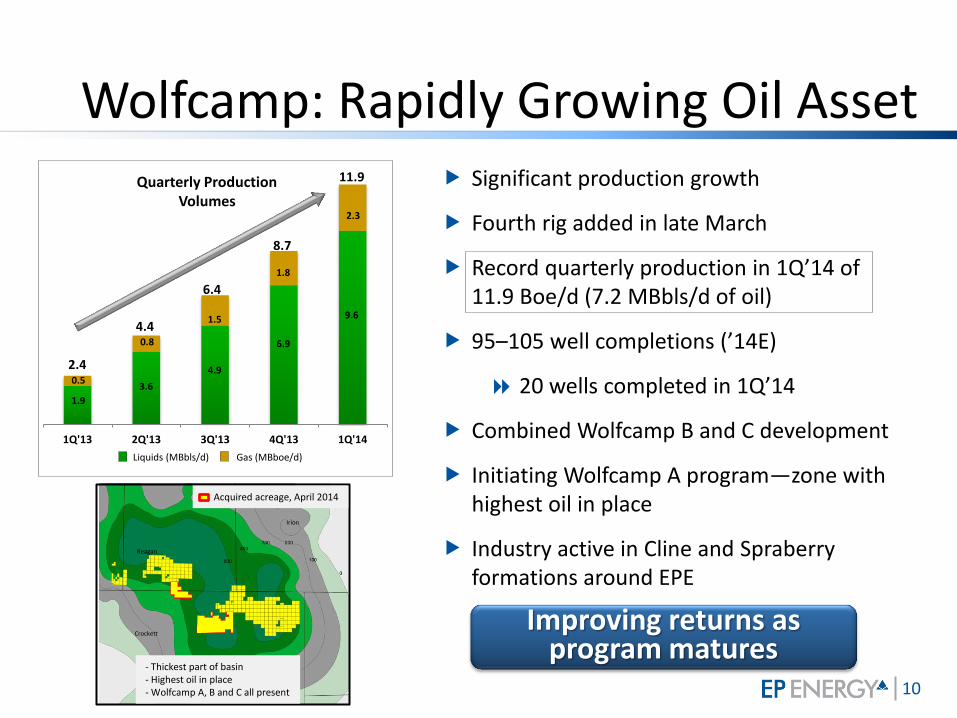

Wolfcamp: Rapidly Growing Oil Asset Significant production growth

Fourth rig added in late March

Record quarterly production in 1Q’14 of 11.9 Boe/d (7.2 MBbls/d of oil)

95–105 well completions (’14E)

20 wells completed in 1Q’14

Combined Wolfcamp B and C development

Initiating Wolfcamp A program—zone with highest oil in place

Industry active in Cline and Spraberry formations around EPE

Improving returns as program matures

1Q'13 2Q'13 3Q'13 4Q'13 1Q'14

Reagan

Crockett

Irion

Quarterly Production Volumes

8.7

6.4

4.4

2.4

11.9

6.9

4.9

3.6

1.9

9.6

1.8

1.5

0.8

0.5

2.3

Liquids (MBbls/d) Gas (MBboe/d)

Acquired acreage, April 2014

- Thickest part of basin - Highest oil in place - Wolfcamp A, B and C all present

11

Wolfcamp: Current Development Concept

Expanding development across acreage position

2014 primarily combined B/C development

Adding A wells

770' between wells in each zone

Completing all wells on a pad prior to producing

12 Page 12

Wolfcamp: Improving Results 23

Development plan focused on combined B/C development

Well results above type curve

Average initial 30-day production rates:

Equiv: 549 Boe/d vs. 367 Boe/d type curve

Oil: 351 Bbls/d vs. 240 Bbls/d type curve

Wolfcamp Long

Gross Well Cost ($MM)

Gro

ss E

UR

(M

Bo

e)

NPV ($MM) $5.8 $5.3 $4.8

400 $2.8 $3.2 $3.7

425 $3.3 $3.8 $4.2

450 $3.8 $4.3 $4.8

Note: NPV calculated pre-tax at 10% discount rate. Assumes $90.00 (WTI) and $4.50 (HH) price deck

29-well average includes EP Energy production data for wells utilizing current completion design of combined Wolfcamp B and C completions. Wells 43-22-3H, 43-22-5H, 43-22-7H, 40EP25-01H, 40EP 25-03H, 40EP25-04H, 40EP25-05H, 40EP25-06H, 44-17-HH, 44-17-IH, 44-17-JH, 44-17-PH, 44-17-KH, 44-17-LH, 44-17-MH, 44-12-JH, 44-12-KH, 44-12-NH, 44-12-OH, 44-12-RH, 44-12-SH,44-12-VH, 44-12-WH, 44-13-HH, 44-13-IH, 44-13-JH, 44-13-KH, 44-13-LH, 44-13-MH.

0

20

40

60

80

100

120

140

1

15

29

43

57

71

85

99

11

3

12

7

14

1

15

5

16

9

18

3

19

7

21

1

22

5

23

9

25

3

26

7

28

1

29

5

30

9

32

3

33

7

35

1

36

5

37

9

39

3

40

7

Cu

mu

lati

ve P

rod

uct

ion

, MB

OE

Days

Individual Wells Well Average (up to 29) Current Type Curve

Number of wells online for:

30 days 29

60 days 22

90 days 15

B/C Development Wells Cumulative Production (Mboe)

Current Type Curve EUR: 400 Mboe

13 Page 13

Wolfcamp: Expanding Development

Region derisked by industry activity and tests

1,300+ horizontal wells in four county area1

~220 A and C Bench wells offsetting EPE acreage

Expanding our development in 2014 while maintaining efficiencies

~3,375 drilling locations2

1Wells drilled below 5,000’ in Crockett, Reagan, Irion, and Upton counties between January 2009 and March 2014. 2 As of December 31, 2013 pro forma for 475 drilling locations from the April 2014 acquisition.

2013 Wells

2014 Wells

2014 Wolfcamp A –bench wells

2014 Wells A Bench – ~5 B Bench – 45-50 C Bench – 45-50 Total = 95-105

2013 Wells WCB – 61 WCC – 5 Total = 66

Recently Acquired Acreage

14

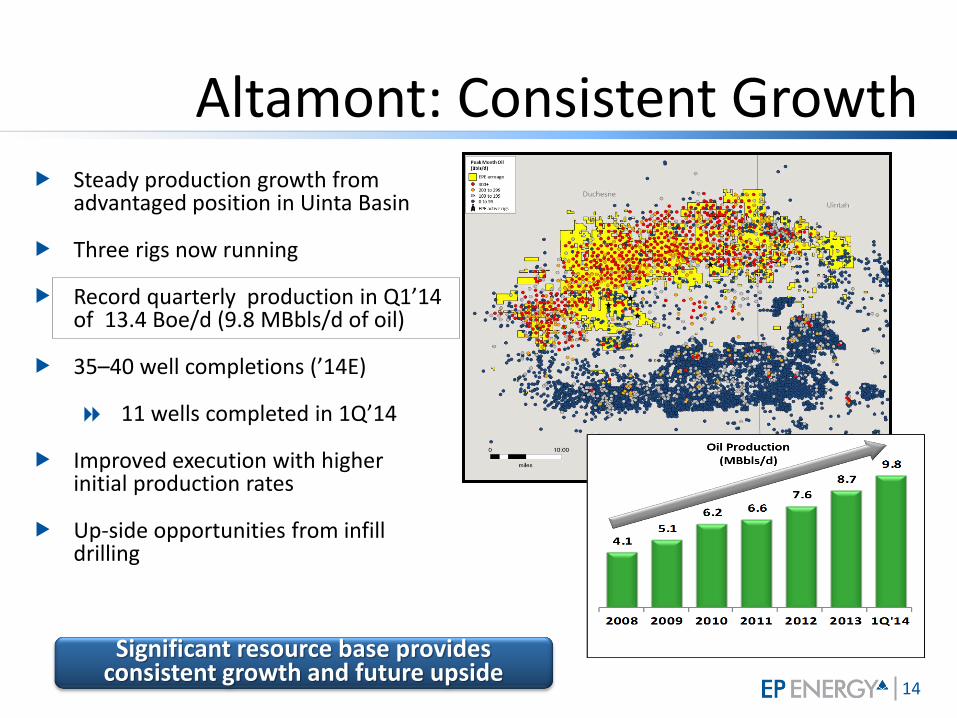

Altamont: Consistent Growth Steady production growth from

advantaged position in Uinta Basin

Three rigs now running

Record quarterly production in Q1’14 of 13.4 Boe/d (9.8 MBbls/d of oil)

35–40 well completions (’14E)

11 wells completed in 1Q’14

Improved execution with higher initial production rates

Up-side opportunities from infill drilling

Significant resource base provides consistent growth and future upside

15

Haynesville – Premier Shale Gas Resource

~37,000 net acres in core of De Soto Parish in NE Louisiana

Acreage 100% HBP

No current drilling activity

197 drilling locations1

Able to quickly commence program with commodity price improvement

Attractive economics with gas prices of $4.00 − $4.50, yielding single-well IRRs of 33% − 47%2

Access to growing Gulf Coast markets

Source: DI Desktop and EP Energy estimates 1 As of 12/31/2013. 2 Type well economics for Holly area wells

Peak Month Gas (Mcf/d)

10,000+

7,500 to 9,999

5,000 to 7,499

0 to 4,999

EPE acreage

Fairway

Haynesville: Premier Shale Gas Resource

16

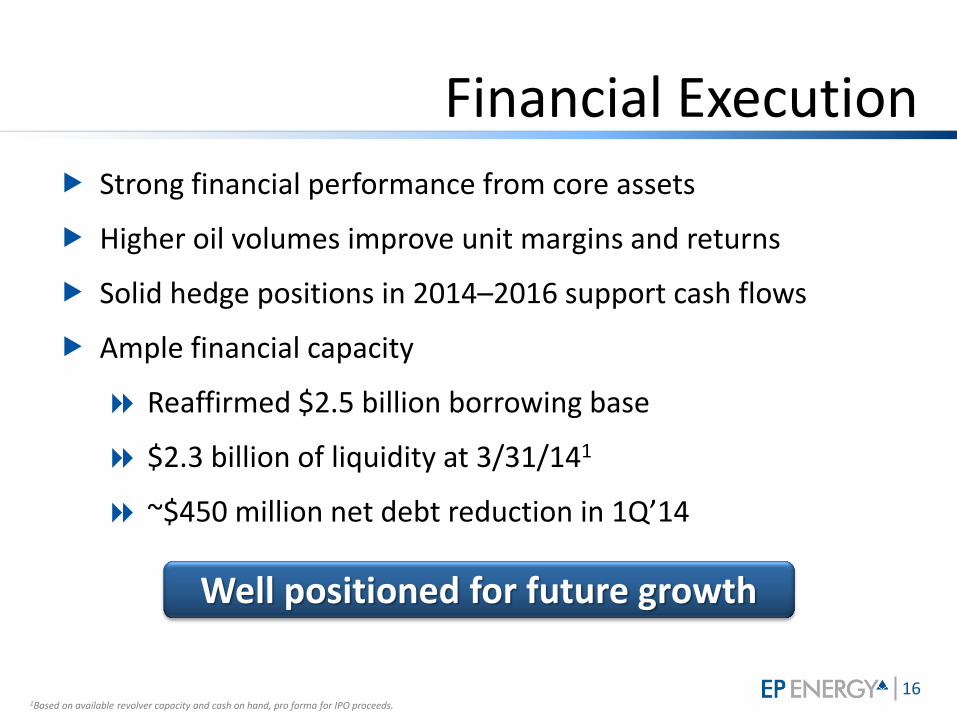

Financial Execution

Strong financial performance from core assets

Higher oil volumes improve unit margins and returns

Solid hedge positions in 2014–2016 support cash flows

Ample financial capacity

Reaffirmed $2.5 billion borrowing base

$2.3 billion of liquidity at 3/31/141

~$450 million net debt reduction in 1Q’14

Well positioned for future growth

1Based on available revolver capacity and cash on hand, pro forma for IPO proceeds.

17

Efficient Capital

1 IRRs based on $90.00/Bbl (WTI) and $4.50/MMBtu (Henry Hub) price deck. Weighted average well level IRR weighted by 2014E capital.

2014E Capital: $2.0 Billion – Project level IRR > 45%1

1Q’13 Total: $428 43 completions

1Q’14 Total: $475 66 Completions

Wolfcamp $132

Altamont $64

Eagle Ford $276

35 well completions

11 well completions

20 well completions

Wolfcamp $104

Altamont $49

Eagle Ford $271

30 well completions

7 well completions

6 well completions

Other $4 Other $3

18

Exciting 2014 Growth Outlook

Focused on execution and operational improvements

Improving LOE per barrel in core oil programs

Significant EBITDAX margin expansion

Improve operational efficiency

$2 billion capital program

$1.73 billion drilling and completion capital – 87 percent drill-bit focused

Directed entirely to Eagle Ford, Wolfcamp and Altamont – 45%+ avg. well level IRR3

Growing cash flows narrow capex funding gap

Programs well positioned for growth

45+ percent increase in oil volumes now

19 percent increase in total equivalent production now2

Continued production

growth1

Eagle Ford down spacing

Wolfcamp A program initiated

Altamont infill wells

Successful acquisition and divestiture enhanced portfolio

Enhancing drilling inventory

1 Pro forma for completed and pending divestitures. 2 Year-over-year growth rate 2013 continuing production volumes compared with 2014 continuing production volumes 3IRR represents before tax rate of return per internal estimates. IRR based on $90.00/Bbl (WTI) and $4.50/MMBtu (Henry Hub) price deck. Weighted average well level IRR weighed by 2014E capital.

18

Investor Update June 2014

20

Non-GAAP Disclosures

Disclosure of Non-GAAP Financial Measures

The Securities and Exchange Commission’s Regulation G applies to any public disclosure or release of material information that includes a non-GAAP financial measure. In the event of such a disclosure or release, Regulation G requires (i) the presentation of the most directly comparable financial measure calculated and presented in accordance with GAAP and (ii) a reconciliation of the differences between the non-GAAP financial measure presented and the most directly comparable financial measure calculated and presented in accordance with GAAP.

The company uses the terms EBITDAX , Adjusted EBITDAX and adjusted cash operating costs per unit.

EBITDAX is defined as income (loss) from continuing operations plus interest and debt expense, income taxes, depreciation, depletion and amortization and exploration expense. Adjusted EBITDAX is defined as EBITDAX, adjusted as applicable in the relevant period, for the net change in the fair value of derivatives (mark to market effects of financial derivatives, cash settlements and premiums paid or received related to these derivatives), impairment charges, equity earnings from our investment in Four Star (sold in September 2013), non-cash compensation expense, transition and restructuring costs, losses on extinguishment of debt, fees paid to our Sponsors, and costs associated with our initial public offering. The company believes that the presentation of EBITDAX and Adjusted EBITDAX is important to provide management and investors with (i) additional information to evaluate our ability to service debt, adjusting for items required or permitted in calculating covenant compliance under our debt agreements, (ii) an important supplemental indicator of the operational performance of our business, (iii) an additional criterion for evaluating our performance relative to our peers, (iv) additional information to measure our liquidity (before cash capital requirements and working capital needs) (v) and supplemental information to investors about certain material non-cash and/or other items that may not continue at the same level in the future. EBITDAX and Adjusted EBITDAX have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of our results as reported under U.S. GAAP or as an alternative to net income, income (loss) from continuing operations, operating income, net cash provided by operating activities or any other measure of financial performance or liquidity presented in accordance with GAAP. For example, our presentation of EBITDAX may not be comparable to similarly titled measures used by other companies in our industry.

We monitor cash operating costs required to produce our oil and natural gas. Cash operating costs is a non-GAAP measure calculated on a per Boe basis and includes total operating expenses less depreciation, depletion and amortization expense, transportation costs, exploration expense, natural gas purchases, impairment charges and other expenses. Adjusted cash operating costs is a non-GAAP measure and is defined as cash operating costs less transition and restructuring costs, management, transaction and other fees paid to the Sponsors, non-cash compensation expense, and costs associated with our initial public offering. We believe cash operating costs and adjusted cash operating costs per unit are valuable measures of operating performance and efficiency; however, these measures may not be comparable to similarly titled measures used by other companies and are subject to several of the same limitations as analytical tools as noted in the paragraphs above.

21

Raising 2014 Production Growth Original 2/10/14 Year/Year

Growth Rate Updated 5/7/14 Year/Year

Growth Rate Oil production (MBbls/d) 50 - 54 40% 52- 55 46% Total production (MBoe/d) 94.5 – 102.5 15% 93.5 – 99.51 19%2

Capital program ($ billion) Drilling and completion $1.73 $1.73 Facilities, lease and seismic $0.20 $0.20 G&A, interest and other $0.07 $0.07 Total3 $2.00 $2.00

Average drilling rigs Eagle Ford 5 – 6 5 – 6 Wolfcamp 3 – 4 3 – 4 Altamont 3 – 4 3 – 4 Wells completed Eagle Ford 135 – 145 135 – 145 Wolfcamp 95 – 105 95 – 105 Altamont 35 – 40 35 – 40 Total 265 – 290 265 – 290

Per-unit adjusted cash cost (per Boe) $12.25 - $14.25 $12.25 - $14.25 Transportation cost (per Boe) $3.00 - $3.50 $3.00 - $3.50 DD&A rate (per Boe) $24.00 - $26.00 $24.00 - $26.00

1. The equivalent volume estimate and growth rate includes the impact of the Q2 2014 divestiture of non-core gas assets, which will be treated as discontinued operations beginning in Q2 2014. As a result, full year 2014 annual average production of approximately 3.5 Mboe/d (85 percent gas) from these assets will be excluded from reported volumes and guidance, and full year 2013 reported volumes will be reduced by approximately 4.9 Mboe/d. The impact on reported oil production from discontinued operations is expected to be minimal. ² Growth rate compares mid-point of 2014 estimated production range with 2013 actual results from continuing operations. 3Excludes $150 million capital for April 30, 2014 acquisition.

22

Type Well Economics

Note: IRR and NPV metrics per internal EPE estimates and assume $90.00/$4.50 price deck. NPV calculated at 10% discount rate, before income tax, and stated in ($MM). 1 13,320’ total vertical depth. ² Wolfcamp Long based 1.5 sections (960 acres) due to 7,500’ laterals. 3 Break-even oil price is price required to generate a 10% pre-tax IRR. Break-even prices on Eagle Ford, Wolfcamp and Altamont assume $4.50/MMBtu (Henry Hub). 4 As of December 31, 2013 pro forma for 475 drilling locations from the April 2014 acquisition. 5 The gross EUR estimates are more speculative than estimates of proved reserves and are thus subject to substantially greater risk of being recovered by EP Energy. In

addition, lower gross EUR estimates and /or higher gross well costs will result in lower NPV estimates than those presented.

Single-Well Sensitivities ⁵

NPV $7.2 $6.9 $6.6

663 $7.0 $7.3 $7.6

696 $7.7 $8.0 $8.3

729 $8.4 $8.7 $9.0

Gross Well Cost ($MM)

Gro

ss E

UR

(M

bo

e)

NPV $6.3 $5.7 $5.1

455 $3.6 $4.0 $4.5

478 $4.0 $4.4 $4.9

501 $4.5 $4.9 $5.3

Gross Well Cost ($MM)G

ross

EU

R (

Mb

oe

)

NPV $5.8 $5.3 $4.8

400 $2.8 $3.2 $3.7

425 $3.3 $3.8 $4.2

450 $3.8 $4.3 $4.8

Gross Well Cost ($MM)

Gro

ss E

UR

(M

bo

e)

NPV $7.9 $7.4 $6.9

5.8 $3.8 $4.2 $4.7

6.1 $4.5 $4.9 $5.3

6.4 $5.2 $5.6 $6.0

Gross Well Cost ($MM)

Gro

ss E

UR

(B

cfe

)

Haynesville Holly Eagle Ford Central Wolfcamp Long Altamont Vertical

Central North Long Short Vertical ¹ Horizontal Holly Non-Holly

Lateral Length (ft) 5,600 5,600 7,500 4,500 N/A 3,960 4,500 4,500

Well Spacing ²

(Distance between wells)

60 acres

(500 ft)

60 acres

(500 ft)

140 acres

(770 ft)

90 acres

(770 ft)

160 acres 160 acres 107 acres

(880 ft)

107 acres

(880 ft)

Gross EUR (Mboe) 663 311 400 241 455 310 967 694

% Liquids 77% 96% 75% 75% 73% 68% 0% 0%

Gross Well Costs ($MM) $7.2 $6.7 $5.8 $4.5 $6.3 $7.1 $7.9 $7.9

Net F&D Costs ($/Boe) $14.59 $28.78 $19.19 $24.91 $18.90 $27.97 $10.02 $14.83

Average WI % 89% 93% 95% 99% 73% 71% 81% 76%

Average NRI % 67% 70% 71% 74% 61% 58% 66% 58%

NRI Pre-Tax NPV - 10% ($MM) $7.0 $2.7 $2.8 $1.3 $3.6 $1.4 $3.8 $1.0

Break-Even Oil Price ($/Bbl or $/MCF) ³ $37.50 $65.00 $56.30 $69.80 $52.85 $71.68 $2.95 $3.88

Pre-Tax IRR 58% 26% 30% 21% 36% 24% 47% 21%

Gross Undrilled Locations (12/31/2013) ⁴ 800 146 2,780 595 776 350 104 93

Eagle Ford Wolfcamp Altamont Haynesville

23

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Eagle Ford: High-quality Oil Production

Average API Gravity1

1Based on monthly pipeline delivered sales

Month

41.0

42.0

43.0

44.0

45.0

46.0

47.0

No gravity adjustments for oil with gravity of 45 degrees or below

Percent

Gas

NGL

Oil

Month

Monthly Sales Volumes by Product

24

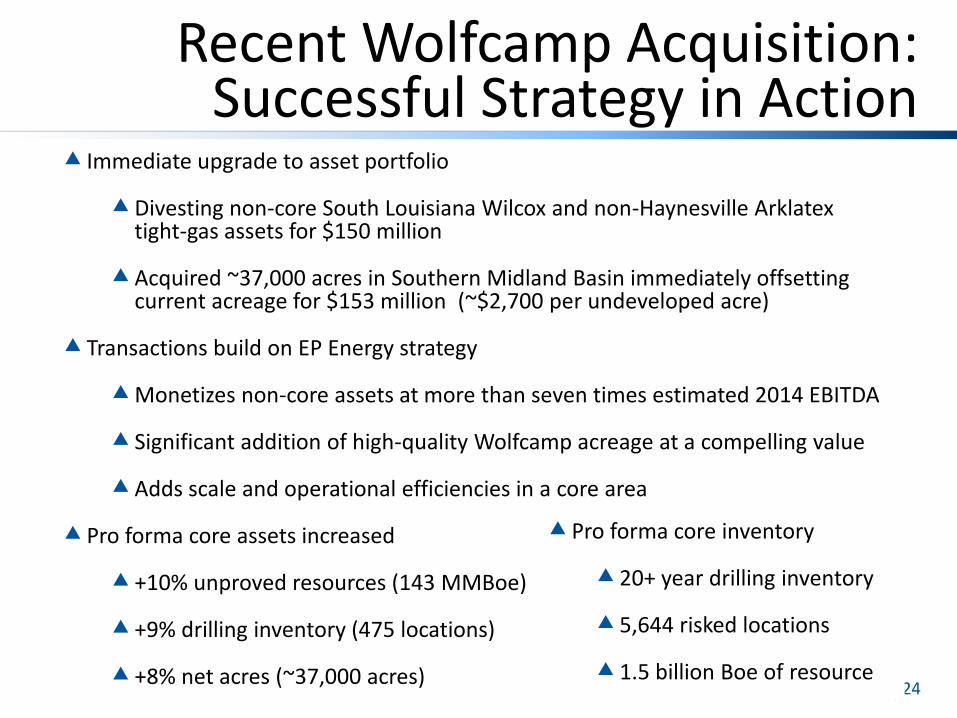

Recent Wolfcamp Acquisition: Successful Strategy in Action

Immediate upgrade to asset portfolio

Divesting non-core South Louisiana Wilcox and non-Haynesville Arklatex tight-gas assets for $150 million

Acquired ~37,000 acres in Southern Midland Basin immediately offsetting current acreage for $153 million (~$2,700 per undeveloped acre)

Transactions build on EP Energy strategy

Monetizes non-core assets at more than seven times estimated 2014 EBITDA

Significant addition of high-quality Wolfcamp acreage at a compelling value

Adds scale and operational efficiencies in a core area

Pro forma core assets increased

+10% unproved resources (143 MMBoe)

+9% drilling inventory (475 locations)

+8% net acres (~37,000 acres)

Pro forma core inventory

20+ year drilling inventory

5,644 risked locations

1.5 billion Boe of resource

25

Successful Wolfcamp Offset Activity

Sources: Texas RRC, HIS, and EP Energy Sources: Texas RRC, IHS, EP Energy

26

Solid Hedge Program

2014 2015 2016

Fixed Price Hedges1

Oil volumes (MMBbls) 14.6 21.0 11.8

Average floor price ($/Bbl) $ 97.79 $ 91.19 $ 90.47

Percent hedged – based on updated 2014 guidance ~100% +100% ~60%

Natural Gas (TBtu) 57.3 58.4 7.3

Average floor price ($/MMBtu) $ 4.02 $ 4.26 $ 4.20

Percent hedged – based on updated 2014 guidance ~100% ~85% ~10%

Eagle Ford Hedges2

Oil volumes (MMBbls) 5.4 3.7 4.6

Effective floor price ($/Bbl) $ 100.70 $ 96.24 $ 93.40

Note: Positions are as of March 31, 2014 (Contract months: April 2014 – Forward). 1 Oil fixed price hedges include WTI, Brent and LLS fixed price swaps and floors 2 Reflects combination of oil fixed prices and basis hedges that effectively floor Eagle Ford oil prices. Floor prices do not include customary refinery and contract deductions.