investors’ day

TRANSCRIPT

Investors’ Day Rüschlikon, 8 December 2015

Investors' Day | Rüschlikon, 8 December 2015

Time Content Management

10.00 – 10.30 Registration

10.30 – 12.00 Group strategic framework Michel M. Liès

Capital allocation at the core of our strategy David Cole

12.00 – 13.00 Lunch break

13.00 – 13.35 Life Capital Thierry Léger

13.35 – 14.10 Corporate Solutions Agostino Galvagni

14.10 – 14.30 Break

14.30 – 15.15 Reinsurance Christian Mumenthaler

15.15 – 15.30 Wrap-up Michel M. Liès

Agenda Investors’ Day 2015

2

Group strategic framework

Michel M. LièsGroup Chief Executive Officer

Investors' Day | Rüschlikon, 8 December 2015

Outperform our peers

• Reinsurance

• Asset Management

• Admin Re®

Smart expansion

• Corporate Solutions

• Longevity & Health

• High Growth Markets

Current position

The leading player in the wholesale

re/insuranceindustry

Strategic goal:

Swiss Re's current strategy has been successful

4

Investors' Day | Rüschlikon, 8 December 2015

Life Capital1

Reinsurance

• To be a focused, lean, global player in large commercial business

• To be a recognised force in the closed life book market

• To be the world's leading reinsurer

• The foundation of our strengths

• A key opportunity for growth

• Providing cash dividends

Corporate Solutions

Swiss Re Group

Admin Re®

Current position

Strategic goal

Current position

Strategic goal

Current position

Strategic goal

P&C L&H

Our business model has positioned Swiss Re as a leading player

5

1 As of 1 January 2016

Investors' Day | Rüschlikon, 8 December 2015

1 EPS CAGR of 10% has been adjusted to 5% for 2015 to account for the distribution of excess capital through the special dividend of USD 1.1bn in April 2015. Methodology is in line with the approach taken for the special dividend of USD 1.6bn paid in April 2014 and USD 1.5bn paid in April 2013

2 Assumes constant foreign exchange rate3 Excl. CPCI4 Cumulative dividends included in ENW per share were translated from CHF to USD using the fx rate of the dividend payment date; dividends included for 2011: USD

3.1 (CHF 2.75), 2012: USD 6.4 (CHF 3.00, or USD 3.3, in addition to the 2011 dividend), 2013: USD 14.5 (CHF 7.50, or USD 8.05, in addition to the 2011 and 2012 dividends), 2014: USD 23.5 (CHF 8.00, or USD 9.03, in addition to the 2011, 2012 and 2013 dividends), 2015: USD 31.1 (CHF 7.25, or USD 7.61 in addition to the 2011, 2012, 2013 and 2014 dividends)

Delivering on the 2011-2015 financial targets has been and remains Swiss Re's top priority

6

3

ROE 700 bps above risk free average over 5 years (2011-2015)

9.2 9.6

13.4 13.7

10.5

14.5

2010 2011 2012 2013 2014 9M2015

avg.2011-2015E

in %

= reported ROE

= 700 bps above US Gov 5 years

8.57.8 8.2 8.6 8.5

89.7 87.8

105.2

123.1

135.7140.9 144.5

2010 2011 2012 2013 2014 H12015

2015E

= reported ENWPS includingcumulative dividends in USD4

= ENWPS @ 10% avg. annual growth (base: 2010)

ENW per share growth plus dividends 10% avg. annual growth rate over 5 years

in USD

98.7

108.5119.4

131.3

3

6.6

7.7

11.913.0

10.210.7

9.2

2010 2011 2012 2013 2014 9M2015

2015E

in USD2

= reported EPS

= EPS @10% avg. annual growth (base: 2010), adjusted for special dividends1

EPS 10% average annual growth rate, adjusted for special dividends1

7.38.0 8.4 8.8

Investors' Day | Rüschlikon, 8 December 2015

We have delivered a market leading total return to our shareholders

7

Swiss Re had one of the highest annualised total returns to shareholders compared to samples of insurers and reinsurers and to reference indices over the period from 2011 to 2015

12%

11%

8%

5%

4% 12%

9%MSCI Index5

STOXX Europe600 Insurance 14%

Sample ofre/insurers4

10%2 22%

15%

Swiss Re

Sample ofreinsurers3

Annualised total return to shareholders (2011-2015)1

1 31 December 2010 to 30 November 2015, based on USD2 Includes special dividends3 Weighted average of Everest Re, Hannover Re, Munich Re, RGA, RenRe, SCOR4 Weighted average of ACE, Allianz, AIG, AXA, XL Group, Zurich, and reinsurers mentioned in footnote 35 MSCI Daily Total Return Gross World Index

Dividend driven returnShare price development

Investors' Day | Rüschlikon, 8 December 2015

Swiss Re faces various challenges and opportunities

8

Low margins

Evolution of primary players with rich

customer insights

Low yield, low growth environment;regulatory changes

Current

Future

Impact of technology

Industry consolidation

Volatility in High Growth Markets

Reshuffling of value chain

New and enlarging risk pools

Investors' Day | Rüschlikon, 8 December 2015

Closing the protection gap and providing solutions for emerging risks will improve global resilience

9

Nat Cat: USD 1.3 trillion 2005-20141

Mortality:USD 105 trillion globally2

Casualty accumulation:

e.g. estimated US asbestos litigation costs USD 85bn3

Connected car: EUR 50bn market of telematics-based car insurance by 2020?5

Connected health: 20% market share for

wearables-based health insurance

products by 2025?6

Emerging risk pools

Protection gap

Sources: 1 Swiss Re Sigma 5/2015 2 Swiss Re Economic Research & Consulting 3 Guy Carpenter September 20154 ABI Research and Swiss Re estimate 5 Ptolemus Consulting estimate 6 Roland Berger estimate

Cyber: USD 10bn market by 2020?4

Investors' Day | Rüschlikon, 8 December 2015

Today we introduce our strategic framework, which will enable us to achieve our new financial targets

10

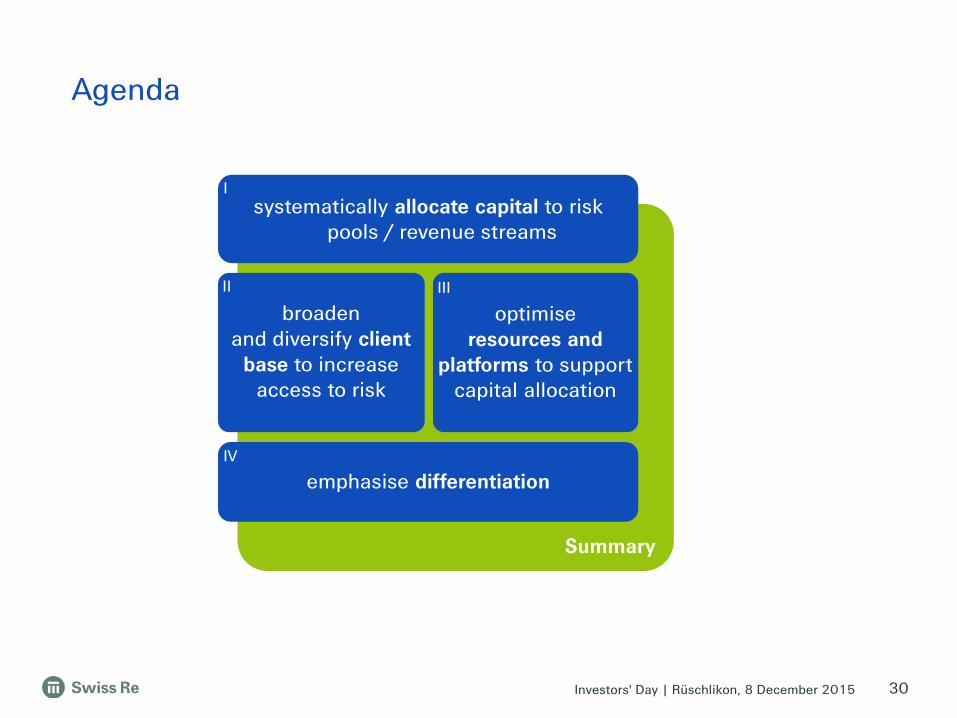

Areas of strategic action

broadenand diversify client

base to increase access to risk

optimise resources and platforms

to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Group financial targets

maintain capital management priorities

ROE ≥risk free + 700bps1

ENWper share

growth10% p.a.2

• Building upon our successful strategy introduced in 2011

• Moving to the next stage of our transformation into a capital allocator

• Emphasising four areas of strategic action going forward

1 700bps above risk free (10-year US Gov Bonds); Swiss Re management to monitor a basket of rates reflecting Swiss Re's business mix; over the cycle2 Year-end ENW + dividends from current year divided by previous year end ENW; all per share; over the cycle

Investors' Day | Rüschlikon, 8 December 2015

Successful aspects of our business model are affirmed under our strategic framework

11

Group strategic framework focuses on systematically allocating capital and resources to provide optionality for value creation

• Continued focus on wholesale re/insurance

• Pursue selected strategic initiatives to access attractive risk poolsWholesale

re/insurance

Global scale and

diversification

• Global reach enabling efficient capital allocation to achieve profitable growth

• Benefits from geographic, business mix and client segment diversification

• Superior balance sheet, credit rating and solvency position allowing flexibility

• Underwriting and asset management discipline with superior risk selectionBalance sheet

for risk

Premium brand

• A leading reinsurance franchise with over 150 years of history

• A preferred partner resulting in long and deep client relationships

Strategic controller

• Group focus on strategy, capital and talent while empowering Business Units to execute

• Business Unit structure benefits from flexibility and efficiency

Investors' Day | Rüschlikon, 8 December 2015

Agenda

12

broadenand diversify client

base to increase access to risk

optimise resources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Key drivers leading to outperformance in value creation

13

I

II III

IV

A multi-risk book provides numerous advantages in addition to capital related diversification benefits

1 EVM, US GAAP, cash flow

Risk selection

Capitalallocation

Portfoliomanagement

Extensive R&D providing a competitive advantage (requires economies of scale)

Active monitoring and hedging of liabilities and continued optimisation of the asset portfolio

Capital deployment based on expected return

Proprietary modelling capabilities to quickly adapt models based on lessons learnt and outlook

Maximise absolute economic profit subject to risk tolerance constraints

Optimal portfolio mix to meet different hurdle rates1

Investors' Day | Rüschlikon, 8 December 2015

Swiss Re actively manages liability and asset risk pools

14

Asset risk pools

Liability risk pools

Mortality

Longevity

Health

Property

Specialty

Casualty

• Swiss Re benefits from diversification through access to different pools of liability and asset risks

• Group has the flexibility to (re-)allocate capital between lines of business, asset classes and regions

Cash and short-term investments

Government bonds

Equities & alternatives

Credit investments

I

II III

IV

P&C Reinsurance L&H Reinsurance Corporate Solutions Life Capital1

1 Effective 1 January 2016Note: Bars illustrate current exposure to risk pools

Illustrative

Investors' Day | Rüschlikon, 8 December 2015

Swiss Re’s portfolio selection maximises value creation

15

Bubble size reflects asset allocation

• Asset risk selection is based on the requirement to match insurance liabilities within strict risk limits and the search for attractive risk-return patterns

• Liability risk selection balances Swiss Re’s profitability levels and attractiveness of markets

• Swiss Re targets an optimal portfolio of asset and liability risks to balance short-term targets with long-term shareholder value creation

I

II III

IV

Credit Investments

Equities & alternatives (incl. PrincipalInvestments)

Risk HighLowLow

Re

turn

Government bonds

Selected asset risks

High

Cash and short-term investments

High risk/return

Low risk/return

Bubble size reflects premium volume

Risk HighLowLow

Re

turn

High risk/return

Low risk/return

Selected liability risks

High

Property Re(incl. Nat Cat)

Health Re

Specialty Re

Property Commercial

Note: Return based on historic 3 year economic profitability. Risk based on standalone SST risk capital requirements.

Specialty Commercial

Investors' Day | Rüschlikon, 8 December 2015

Agenda

16

broadenand diversify client

base to increase access to risk

optimiseresources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Three ways to broaden and diversify our access to risk

17

I

II III

IV

Geographies

• Extend leadership in mature markets

• Maintain market leadership in High Growth Markets (HGM)

Clients Risks

• Offer tailored solutions

• Access new clients

• Develop innovative approaches

• Leverage Swiss Re’sknowledge and thought leadership

• Enhance capabilities and new products

Investors' Day | Rüschlikon, 8 December 2015

Geographies – Dedicated initiatives in place to maintain leading position in HGM

18

Dedicated strategic initiatives across Swiss Re in place to remain the leading wholesale re/insurer in HGM

Reinsurance

Expansion in focus countries

• Organic growth

• Partnerships

Corporate Solutions

Further broadening the footprint

• Organic growth

• New offices

• Acquisitions

Aspiration for 2020

30%

20202012 2014

27%15%

30% HGM premium share

Principal Investments Swiss Re Group

Optimise diversification

• Coordination and advisory for HGM

Investment in selected HGM countries

• Increase exposure

• Complement HGMfocus of Business Units

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Clients – Broadening our access through profitable growth initiatives

19

Corporate Solutions Life Capital

Large corporates Insurance companies

Mid-size corporates

New forms of exposure to client pools

Continued focus

• Dedicated growth initiatives targeting Regional & National companies in Reinsurance, mid-size corporates in Corporate Solutions, and distribution partners in Life Capital

• Innovative approaches to access new client pools, extending beyond the traditional business models

Dedicated growth initiatives

Global insurance companies

Large insurance companies

Regional and National insurance companies

Governments & supranationals

Reinsurance

Principal Investments

Distribution partners

I

II III

IV

Pension funds

20

I

II III

IV

VietnamAgriculture yield cover

Pacific Islands Earthquake and

tropical cyclone risk

UruguayEnergy

production shortfalls

due to drought

IndiaWeather insurance

for farmers

CaribbeanHurricane,

earthquake and excess rainfall risk

BeijingAgricultural risk

TurkeyEarthquake pool

Louisiana Hurricane risk

MexicoEarthquake/hurricane

and livestock risk

BangladeshFlood

insurance

African Risk CapacityGovernment drought

insurance pool

FloridaHurricane risk

United KingdomFlood risk

Shenzhen typhoon/rainfall Thailand

Crop insurance

• First dedicated public sector team in the reinsurance industry

• Over 200 closed transactions since 2006

• Develop insurance, reinsurance and capital markets solutions onall perils (natural disasters, weather risks, pandemics, etc.)

• Global footprint

• Pioneer in emerging and industrialised markets

Clients – Swiss Re Global Partnerships enables the Group to broaden our client base and address the protection gap

Investors' Day | Rüschlikon, 8 December 2015

Health lines are emerging as key markets

Risks – Selected access to additional risk pools

21

Focusing on product development leveraging aging, technology, and data to increase share in global medical reinsurance

Helping establish infrastructure debt as tradable asset class to strengthen long-term investors’ capacity to support the real economy

Investing significantly in the understanding of cyber risks, rolling out solutions prudently in the primary and reinsurance space

Building on excellent biometric data to develop innovative solutions in the primary insurance and reinsurance market

I

II III

IV

Infrastructure investment enhances economic growth

Expected % of GDP spending requirement in infrastructure vs

historicals

Required spending(to achieve 1.7% p.a. real GDP growth)

Historical average, 2002-11

Global health premiums,USD bn

Infrastructure investmentsHealth portfolio

USD 105tr mortality protection gap

Mortality gapCyber

USD 2bn premiums globally in 2014

Source: Swiss Re Economic Research & Consulting; Swiss Re estimates; McKinsey Global Institute

2.9

2.8

Continental Europe

Europe2.6

UK and Ireland 3.4

2.3

2.31 000

500

0

1 500

2 000

20

15

E

20

05

20

25

E

20

20

E

20

10

5-10

2015E

6-10

2025E

2.6

2020E

3

12-18

7-84-6

2-5

0.5

USRoW

Cyber market premiums (base case), USD bn

Mortality protection gap by region, USD trn

5823

17

7Europe

NorthAmerica

Latin America

Asia

Investors' Day | Rüschlikon, 8 December 2015

Agenda

22

broadenand diversify client

base to increase access to risk

optimiseresources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Swiss Re optimises resources and platforms to support capital allocation

23

Examples

Dynamic and forward-looking capital allocation supported by agile resources and platforms

• Use of smart analytics and cognitive computing to improve our underwriting capabilities (e.g. impact from 200 examples identified)

Smart analytics

• Alignment of the workforce to actively support our HGM strategy (e.g. increase of FTE in Latin America and Asia by 421% and 66% respectively since 2011)

Talent

• Leverage distribution platforms to maximise value from our wholesale model (e.g. distribution partnerships in Life Capital via elipsLife and iptiQ)

Distribution platforms

• Flexible access to funding for our businesses (e.g. access to external funding recently established for Swiss Re Ltd, Corporate Solutions and Life Capital)

Funding platform

• Simplification, modernisation, and integration of IT architecture (e.g. 20% net reduction of applications, consolidation to two main data centres)

IT platforms

• Continued development of our AM capabilities (e.g. first Swiss company to receive Renminbi Qualified Foreign Institutional Investor license)

Asset Management

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

`

Long-term focus Corporate SolutionsPrincipal Investments (PI)

Targeted by Reinsurance and Corporate SolutionsLong-term focus Reinsurance

HGM

Swiss Re has more than doubled its workforce in HGMsbetween 2011 and 2015

24

India2

China

Indonesia

Brazil

Mexico

1 Including Shared Service Centre of 430 FTEs in 2011 and 580 FTEs in 20152 Bangalore 41% of Asian FTEs in 2015

We successfully increased our workforce in HGMs and will continue in line with our 2020 aspiration

Latin America FTEs

~730

Jun 2015Jan 2011

~140

Asia FTEs

~1 4301

Jun 2015Jan 2011

~8601

Africa FTEs

~60

Jun 2015Jan 2011

~40

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015 25

Swiss Re adopts smart analytics and cognitive computing to further extend its competitive positioningSelected examples from over 200 delivered cases

Transparent motor China

Reinsurance

For China, we have built a sophisticated model predicting motor accident frequencies leveraging a wide range of data sources

Rapid sales analytics

Corporate Solutions

Improve sales effectiveness: binding likelihood increases by 20% when sales activities happen after quotes

Screening risk engineering reports

Through text analytics, we structure a large number of property risk reports, reducing the single risk report analysis time down from 4 hours to real time

Contract intelligence hub

Group

Client and market intelligence

Reinsurance

We have developed an advanced contract analytics solution covering all re/insurance contracts from all lines which allows us to analyse clauses

Analysing internal and external communication, we quantify Swiss Re client relationships and identify hot topics and market trends

• Competence centre for smart analytics (30 data scientists, 200 smart analytics affine re/insurance professionals)

• Cognitive computing competence centre which Swiss Re is jointly building with IBM

I

II III

IV

Corporate Solutions

Investors' Day | Rüschlikon, 8 December 2015

Agenda

26

broadenand diversify client

base to increase access to risk

optimiseresources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Active differentiation remains pivotal to extending our lead as a knowledge company and allocator of risk capital

27

'We’re smarter together'

Client relationships

• Preferred partner

• Decade-long relationships

• Global presence and broad product offering

Knowledge company

• Thought leadership

• Technical expertise

• Risk insights and modelling

• Proprietary data and research

Financial strength

• Capital strength

• Financial flexibility

• Integrated risk management and systematic ALM

• Distinctive access to contingent capital

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Swiss Re benefits from direct access to clients in all Business Units

28

• Swiss Re differentiation based on unique access to clients and development of tailored risk solutions

• Direct client interactions also for intermediated business

Percentage of premiums derived from non-intermediated business, 9M 2015

1 Reflects Admin Re®

I

II III

IV

P&C Reinsurance L&H Reinsurance Life Capital1Corporate Solutions

52% 11% 100%96%

Investors' Day | Rüschlikon, 8 December 2015

Delivering distinctive thought leadership, R&D and industry dialogue through unique channels

29

Industry-leading “sigma” publications

Distinctive thought leadership State-of-the art delivery

Large and highly educated pool of talents

• 300 FTEs working on research matters

• 30 FTEs in Economic Research & Consulting, 50 FTEs in nat cat modelling

Client and expert events

• 100+ client and expert events per year hosted at the Centre for Global dialogue for 1 000+ clients (15 000+ people)

• 50+ client training courses offered

On-the-go access to knowledge

Research and publications in

partnership with leading institutions

I

II III

IV

Our thought leadership is a true driver of business impact: highly informed decisions, access to world-class talents, state-of-the-art support for clients, impacting societal development

First-class client events

Acclaimed proprietary research into trends and products

Wide-ranging global database, covering all types of insurance markets and products

Investors' Day | Rüschlikon, 8 December 2015

Summary

broadenand diversify client

base to increase access to risk

optimiseresources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Agenda

30

Investors' Day | Rüschlikon, 8 December 2015

Current

Future

Our strategic framework positions us strongly vis-à-vis current and future challenges and opportunities

31

Growing tailored solutions

Broadening our access to client and risk pools

Optimised AM and funding

Agile capital (re-)allocation & wholesale approach

Investing to differentiate on knowledge leadership

Creating optio-nality through strategic partnerships

Embedding cognitive computing in our UW

Bringing new sustainable solutions to the market

Examples Examples

Low margins

Low yield, low growth environ-ment; regulatory

changes

Evolution of primary players

with rich customer insights

Impact of technology

Industry conso-lidation

Volatility in High Growth

Markets

Reshuffling of value chain

New and enlarging risk pools

Investors' Day | Rüschlikon, 8 December 2015

• P&C Reinsurance remains a key contributor through differentiation and underwriting discipline

• L&H Reinsurance benefits from increasing demand

• Corporate Solutions expands into Primary Lead and broadens the footprint

• Life Capital pursues growth opportunities

• Focus on attractive opportunities above our return hurdles

• Sustain long-term earnings through effective portfolio steering

• Deliver market leading returns

Our four areas of strategic action create long-term value for our shareholders

32

Profitability: ROE

Growth: ENW per share

broadenand diversify client

base to increase access to risk

optimise resources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Capital allocation at the core of our strategyDavid ColeGroup Chief Financial Officer

Investors' Day | Rüschlikon, 8 December 2015

Reinsurance

Life Capital4

Swiss Re Ltd

USD 2.2bn2USD 3.0bn2USD 8.0bn2 USD 1.4bn2

Reinsurance Corporate Solutions Admin Re®

1 Distribution to shareholders of approx. USD 10.6bn from 2012 to 2015 incl. USD 2.6bn dividends paid end of April 2015 and up to CHF 1.0bn for the public share buy-back

2 Internal dividend flows from January 2012 to September 20153 PI has paid to Group dividends of USD 0.4bn between 2012 and September 20154 As of 1 January 20165 Transaction completion expected early 2016

1.0

12

1.2

14 15

2.73.1

13 151312

0.30

1.0

1.8

14

0.2

13

0

14 15

0.7

12

0.5

1413

1.1

15

0.40.4

12

0.4

Inorganic Deleveraging Organic

P&C L&H

Swiss Re’s capital allocation aims to deliver sustainable shareholder value

34

Usage of funds

Capital return

USD 10.6bn1 distributionto shareholders

PI3

Agile use of funds to deliver shareholder value:

• Capital return of up to USD 10.6bn to shareholders since 2012

• Acquisitions, e.g. Sun Alliance China, Guardian5

• Significant deleveraging

• Organic growth through capital (re-) allocation

Investors' Day | Rüschlikon, 8 December 2015

We use a holistic capital management and performance framework to systematically allocate capital

35

Performance measurement

Evaluate performance and (re-)allocate capital

• Monitor performance based on an integrated KPI framework

• Relentlessly re-allocate capital (away from underperforming portfolios and towards best performing ones)

Generate sustainable shareholder value

• Close the protection gap and respond to emerging risk pools by delivering innovative solutions

• Leverage distinctive skills and capabilities of Swiss Re Group

Strategic ambition

Define capital allocation for liability and asset risk pools

• 45 liability portfolios and key asset classes considered for capital allocation

• Assess risk pools based on historic performance and future outlook

• Optimise financial metrics (EVM, US GAAP, cash flow) and risk appetite

Capital allocation

Execute capital allocation to portfolios

• Business Units proactively plan and execute on shared vision for the target liability portfolio to deliver sustainable shareholder value

• Capture attractive market opportunities accordingly

Business planning

II III

IV

I

1

2

3

4

Investors' Day | Rüschlikon, 8 December 2015

We allocate capital to risk portfolios in a consistent manner across the Group

36

US GAAP perfor-mancemetric

EVM perfor-mancemetric

• Developed single-year and multi-year view of performance on portfolio level

• Use key financial metrics as support for capital (re-) allocation decisions

• Break down Group targets to liability portfolios

Illustrative – performance per portfolio• Cash flows discounted and recognised at inception

• Capital costs recognised

• Cash flows recognised over lifetime of contract

• Capital costs not taken into account

Illustrative – performance per portfolio

Investors' Day | Rüschlikon, 8 December 2015 37

Swiss Re continues to maintain a high quality, well-balanced investment portfolio

• High-quality credit investments have been steadily added to the portfolio since the re-balancing in 2013

• Additional investments include a diversified mix of corporate bonds across various currencies, high quality loans, securitised products and credit ETFs

• Equities and alternative investments were reduced in 2014 through sales of equity securities and hedge fund redemptions

• Acquisition of Guardian is expected to increase the Group’s overall allocation to credit by approximately 6%pts. The quality of the credit portfolio remains high

23%17% 12% 11%

32% 39%41%

37%

33% 35% 38% 44%

11% 8% 8% 7%1% 1% 1% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

End FY 2013 End FY 2014 End Q3 2015 End Q3 2015(Estimated pro formaimpact of Guardian)

Other

Equities & alternatives (incl.Principal Investments)

Credit investments

Government bonds

Cash and short-terminvestments

Investors' Day | Rüschlikon, 8 December 2015

6.3%

5.0%5.3%

4.7%

1.8%

3.5%

4.4%4.0%

3.6% 3.7% 3.8%

0%

1%

2%

3%

4%

5%

6%

7%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 9M 2015

10-year avg US Treasury risk-free rates ROI Running yield

• Asset re-balancing helped mitigate the effect of low yields on the return on investments in recent years

• Decline in interest rates has only been partially reflected in the running yield development, demonstrating the impact of re-balancing on portfolio income

• Notwithstanding the recent performance, a prolonged low yield environment would likely represent a headwind to the investment result going forward

38

Steady investment performance through active asset re-balancing despite continued low yield environment

1 Historical ROIs as published; 2011 and later based on new calculation method, as initially disclosed at Investors' Day 2012

1

Investors' Day | Rüschlikon, 8 December 2015

2013 201420122011

We will maintain a dynamic allocation of capital under our strategic framework

39

1 Dividends based on year accrued2 Excludes BU-funded and debt-funded acquisitions

Acqui-sitions2

-

Divestments

0.2

0.9

Dividends1

2.6

Business reinvestmentsAcqui-

sitions2

-

Divestments

0.6

1.4

Dividends1

2.8

Business reinvestments

0.2

Dividends1

1.1

Divestments

Business reinvestments

1.5

Acqui-sitions2

1.1

Dividends1

3.1

Divestments

-

Business reinvestments

1.3

In 2015

• Share buy-back has started, for an amount up to CHF 1.0bn purchase value

• Announced acquisition of Guardian will absorb GBP 1.0bn in early 2016

• Group capitalisation remains very strong

Swiss Re Group view, end of year figures, USD bn

-

Acqui-sitions2

Net Income 2.6Shareholders’ equity 29.6

Net Income 4.2Shareholders’ equity 32.9

Net Income 4.4Shareholders’ equity 31.9

Net Income 3.5Shareholders’ equity 34.8

Investors' Day | Rüschlikon, 8 December 2015

Swiss Re's risk tolerance criteria are the basis for our capital management, risk steering and limit setting

After an extreme loss event (99% shortfall)

able to meet

Extreme loss criteria

Group

Rating AARespectability criteria

Liquidity

• Level reflects regulatory and client expectations

• To have sufficient capital to be in a position to continue to write new business, for all major entities

• Sufficient liquidity to fund subsidiary recapitalisations where needed and cover committed requirements in the year following the stress loss

Capital criteria Liquidity criteria

Swiss Solvency Test 100%

Swiss Solvency Test 185%

40

Risk tolerance represents the amount of risk Swiss Re is willing to accept within the constraints imposed by its capital and liquidity resources, its strategy, and the regulatory and rating agency environment

Risk tolerance objectives:

• Maintain capital and liquidity that are sufficiently attractive from a client perspective, and that meet regulatory requirements and client expectations ("respectability criteria")

• Be able to continue to operate following an extreme loss event ("extreme loss criteria")

• Avoid material operational risks that could subject the Group to large operational losses with corresponding consequences from an economic, reputational or regulatory perspective

Funding amounts required to be held at the Swiss Re Ltd level, as well as the external dividend proposals take into consideration both sets of constraints

Investors' Day | Rüschlikon, 8 December 2015

208% 213% 223%245% 241%

48.7

SST 1/2012SST 1/2011

18.5 19.819.1

40.7

SST 1/2013

38.552.2

21.6

SST 1/2015

52.6

23.6

SST 1/2014

Swiss Re's very strong capital position enables the capital allocator role for the Group

41

Swiss Re’s capitalisation remains very strong across multiple metrics

• Group SST ratio comfortably above respectability level; impact of the acquisition of Guardian is expected to be approximately 20-25%pts

• Swiss Re's excess capital is well above the capital required for a S&P AA rating

• Group accessible capital (after deduction of Principal Investments) amounted to USD 4.5bn at the end of Q3 2015

SST target capitalSST risk-bearing capital

185% Group SST respectability level

USD bn

SST ratio

Investors' Day | Rüschlikon, 8 December 2015

We ensure an integrated approach to managing current and future risks

42

Development since SST 1/2015

• Pre-Guardian, SST target capital decreased mainly due to higher interest rates reducing the market value margin, which forms part of the SST adjustments

• Guardian acquisition is expected to add market (credit spread) and credit (default & migration) risk, while the insurance risk of the transaction is expected to add to Swiss Re's insurance risk diversification

USD m, pre-tax1

Economic net worth +216 +411

Change in interest rates +50bps +100bps

Change in credit spreads +50bps +100bps

Economic net worth -3 754-1 944

Change in market values2 -10% -25%

Economic net worth -958 -2 394

SST 1/2015 in USD bn

1 All sensitivities are assumed to have taken effect on 31 December 2014 and no management actions are included in this analysis2 Equities and alternative investments, excl. real estate

Diversification benefit 13.3

2.9Credit (incl. credit UW)

19.2

SST target capital 23.6

SST adjustments 4.4

99% TailVar

Life and Health 8.0

Property and Casualty 9.5

Financial market 12.1

Group regulatory capital requirement Sensitivities on ENW

Investors' Day | Rüschlikon, 8 December 2015

One regime more conservative than the other

We have gained extensive experience in complying with economic solvency regimes

43

Swiss Re operates under a comprehensive economic and risk based solvency regime since 2008

• SST is a more conservative economic-based regime than Solvency II

• EU confirmed equivalence with Solvency II

• Swiss Re’s internal model serves both SST and Solvency II; both the Swiss regulator (FINMA) and Luxembourg’s regulator (CAA) have provided regulatory approval

• Initial application of Standard Formula approach under Solvency II

• Continued engagement with the PRA on future internal model approval

UK

• Swiss Re's internal model approved by the local regulator (CAA)

• External auditor issued an unqualified positive assurance opinion on the internal model for 2013, 2014 and 2015

Luxembourg Key differences: SST vs Solvency II (internal model)

SST Solvency II

Risk measure • Based on 99% TailVaR • Based on 99.5% VaR

Market value margin/

Risk margin

• Part of available and required capital

• Part of technical provisions

Deferred Tax• Not accounted for • Loss absorbing effect

on required capital

Operational risk • Qualitative treatment • Quantitative treatment

Valuation (discounting)

• Market consistent valuation based on replication

• Option for volatility or matching adjustments

Investors' Day | Rüschlikon, 8 December 2015

33.937.2 38.4 37.5

5.46.5 6.6 6.4

9.57.0 5.4 4.9

8.5 6.7 6.5 6.0

31%24%

21% 20%

14% 15% 15% 15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 H1 2015

Core capital Total hybrid incl. contingent capitalSenior debt LOCSenior leverage plus LOC ratio Subordinated leverage ratio

USD bn

Achieved USD 5.8bn of net deleveraging6 ahead of our 2016 target of more than USD 4bn7

4 5

1

2 3

Senior leverage plus LOC ratio target range: 15-25%

Subordinated leverage ratio target range: 15-20%

1 Core capital of Swiss Re Group is defined as economic net worth (ENW) 5 Subordinated debt divided by sum of subordinated debt and ENW 2 Senior debt excluding non-recourse positions 6 Total from end 2012 to Investors’ Day 2015, based on Q3 2015 carrying values3 Unsecured LOC capacity and related instruments (usage is lower) 7 Announced at Investors’ Day 20134 Senior debt plus LOCs divided by total capital

Our Group capital structure is well within our leverage ratio target range, providing further flexibility

44

Investors' Day | Rüschlikon, 8 December 2015

Letters of credit

Senior debt

Sub-ordinated debt

Further reduction in line with reducing requirements in Reinsurance

Support business growth in Life Capital in line with leverage targets

Further optimisation of capital structure and cost of capital

Innovative capital instruments to

strengthen Group capital base

Subject to FINMA approval

Significant progress or fully realised

Continue to implement contingent capital road-map focusing on Group Holding level

Outlook

Swiss Re’s target capital structure and financial flexibility is supported by strong funding platforms

45

Established access to external funding

in all Business Units to fund ongoing

capital and liquidity requirements

Contingent capital

Established funding platform at Swiss Re Ltd with the first pre-funded subordinated debt facility in November 2015

Corporate Solutions

Reinsurance

Group

Outlook

Life Capital

Change since 2012

Investors' Day | Rüschlikon, 8 December 2015

Group financial targets

Systematic capital allocation is essential for achieving our Group and Business Unit targets

46

• 10-15% ROE over the cycle

• 10-12% ROE over the cycle

• 10-15% ROE over the cycle

• 6-8% ROE mid-term

1 Management to monitor a basket of rates reflecting Swiss Re's business mix

L&H Reinsurance Corporate Solutions Life CapitalP&C Reinsurance

Rf+700bps

Over the cycle2016

10% per annum

2015 Over the cycle2016

700bps above risk free (10-year US Gov Bonds1)

ROE ENW per share growth

Year-end ENW + dividends from current year divided by previous year end ENW; all per share

Business Unit targets

Investors' Day | Rüschlikon, 8 December 2015

Aligning the measurement of our financial targets with underlying fundamentals

47

• Reflects the long-term ambition of the Group

• Encompasses both industry and economic cycles

Over the cycle

• Increases ambition of the Group

• Reflects shift towards longer duration business

10-year risk free rate

ROE

• USD remains Swiss Re’s largest currency exposure

• Management to monitor a basket of rates reflecting Swiss Re'sbusiness mix

Basket of rates

ROE

• Change to EVM methodology, including setting capital cost parameters

• Adjustments to be recorded in the opening balance of 2016 ENW

Economic growth

ENW

Investors' Day | Rüschlikon, 8 December 2015 48

Swiss Re’s capital allocation aims to deliver sustainable shareholder value

We confirm our capital management priorities

• Ensure superior capitalisation at all times and maximise financial flexibility

• Grow the regular dividend with long-term earnings, and at a minimum maintain it

• Deploy capital for business growth where it meets our strategy and profitability requirements

• Repatriate further excess capital to shareholders

We aim to deliver long-term shareholder value

• Strategic framework enabling systematic allocation of capital to risk pools

• Very strong capital position across multiple metrics

• Steady investment performance through active asset re-balancing despite continued low yield

• Capital structure comfortably within our leverage ratio target ranges, providing flexibility

• Swiss Re Ltd and all Business Units have established access to external funding

Life Capital

Thierry LégerCEO Life Capital (effective 1 January 2016)

Investors' Day | Rüschlikon, 8 December 2015

Life Capital combines primary Life & Health insurance expertise and businesses…

in USD bn in %

1 Share of Swiss Re Group’s Economic Net Worth deployed across Business Units (excl. Group Items), 30 June 20152 Transaction completion expected early 2016

9M 15

0.3

0.9

0.5

FY 14FY 13

1.2

FY 12

Gross cash generation Return on Equity

• Swiss Re’s Life Capital Business Unit will manage closed and open life and health books

• Composed of Admin Re® (plus Guardian2) and existing primary life and health activities

• Significant cash generation

10%

Economic Net Worth1

9M 15

6.1

FY 14

0.6

6.1

2.6

6.8

7.7

FY 13

3.8

6.8

FY 12

ROE excl. US exit impact

Admin Re®Admin Re®

50

Investors' Day | Rüschlikon, 8 December 2015

…with attractive growth opportunities based on a few key trends…

Trends in L&H

Aging societyIncrease in longevity, health, and care needs

Regulatory reformsComplex regulatory environment

Customer engagement

Fair treatment of legacy clients requires active management

TechnologySystem changes lead to costly investments in legacy platforms

Disruption in distribution channelsEfficient distribution is key

Protection gapMortality and morbidity gap in high growth and mature markets

Efficient capital allocationClients not willing to have capital tied-up in legacy operations

51

Investors' Day | Rüschlikon, 8 December 2015

…and expanded access to Life & Health risk pools

Closed book~ 4m policies

~ USD 40bn assets

Open book~ 0.5m policies

~ USD 0.3bn assets

• Leading closed life book consolidator: focus on UK; investigate opportunities outside the UK

• Create value through operational, capital and asset management synergies

• Selective growth in Admin Re®

Ambition:

• Diversify our L&H book to generate stable returns for shareholders

• Provide excellent service and positive experience to our policyholders

• Deliver 6-8% ROE in the mid-term

• Grow new business in individual and group L&H through partnerships

• Further establish elipsLife (group L&H) and iptiQ (white-labelling)

Note: Approximate number of policies and assets (excl. policyholder assets) as at December 2014, including assumption of closing Guardian

52

Investors' Day | Rüschlikon, 8 December 2015

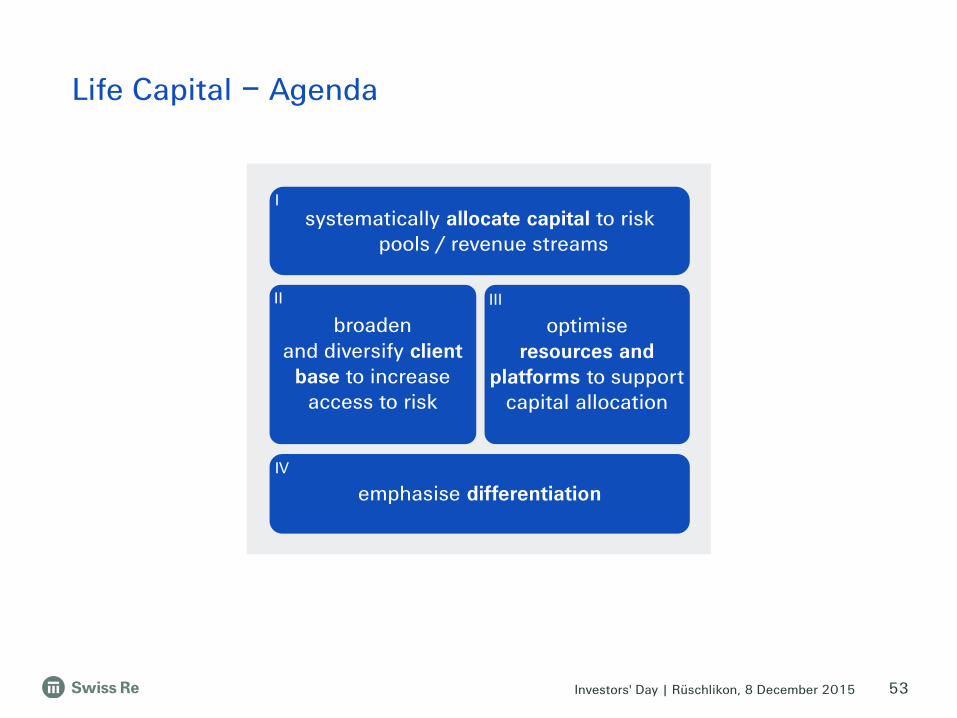

Life Capital – Agenda

53

broadenand diversify client

base to increase access to risk

optimise resources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

We will systematically allocate capital to attractive and growing Life & Health risk pools…

I

II III

IV

Aim is to build a balanced portfolio benefiting from diversity of risks

54

• Mortality & morbidity risk

• Persistency risk

• Indirect equity risk• Persistency risk

• Longevity risk• Credit/spread risk

Unit-linked policies Annuities Biometric protectionExample products

Health

Mortality

Closed book Open book

Longevity

Liability risk pools

Illustrative

Note: Bars illustrate current exposure to risk pools

Investors' Day | Rüschlikon, 8 December 2015

…and attractive revenue streams – Guardian acquisition as an example

Diversified product mix

In %

Enhanced investment portfolio

In %

Post Guardian

acquisition

32 20

60 71

6

111 0

8

• Demonstrates Admin Re®’s position as a leading closed life book consolidator in the UK

• Transaction in excess of Group’s 11% ROE hurdle rate

Acquisition diversifies Admin Re®’s portfolio

• Long-term dominance of pensions policies

• The Guardian acquisition is expected to rebalance the product mix, with a majority of annuity policies

Continued focus on quality investment portfolio

• Guardian brings approx. GBP 12.5bn of assets to the balance sheet

• Increased allocation to investment grade credit improves asset yields with acceptable risk exposures

Post Guardian

acquisition

End Q3 2015 pro forma

Term or protection

Policies administered for 3rd parties Annuities

Unit linked / savings

I

II III

IV

55

Equities & alternatives

Other

Cash and short-term investments

Credit investments

Government bonds

End Q3 2015

37 36

13 2112

13

38 30

End Q3 2015 pro formaEnd Q3 2015

Investors' Day | Rüschlikon, 8 December 2015

We actively manage in-force portfolios to enhance cash generation

Proven track record in extracting maximum value from closed books

0.7

1.0

2016-2018E

1.7

0.3

9M 15FY 14

0.8

FY 13

0.9

0.7

0.20.5

0.4

1.2

FY 12

Admin Re®

Sales proceeds

Guardianin USD bn

Operational integration

Asset optimisation

Risk diversification

Debt funding

• Driving economies of scale with system and operational standardisation

• Managing asset portfolio to optimise expected yield and capital required

• Harnessing diversity in risks to deliver balance in capital and surplus

• Accessing debt funding to provide efficient and appropriate leverage

Gross Cash Generation

56

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

In open books, Life Capital provides solutions to a broad client base

57

I

II III

IV

Working with our clients and partners to access and serve policyholders

Medical insurer

Our partner:

• Large medical health provider seeking to cross-sell into life insurance

Value proposition:

• Collaborating with partner to define products for the online and tele sales market

• Working closely with partner to continuously optimise customer journey to increase sale conversions

Group life business

Our clients:

• Several Fortune 500 and 10k SME clients in portfolio

Success stories:

• Preferred provider for largest brokers and benefit consultants in NL and CH; 2.5% share of wallet in both countries

• First holistic biometrical total solution with integrated end-to-end IT-platform

• Established in 2014• Primary white-labelling carriers that Swiss Re established to support

the development of primary L&H opportunities with distribution partners such as primary insurers

• Established in 2008• Focuses on (B2B) corporate

customer business in Europe• Licensed for direct L&H

insurance business

Direct distributor

Our partner:

• New UK distributor replicating past success with “direct TV + sales call centre” abroad

Value proposition:

• Fronting and full customer service through its end-to-end service platform

• Supporting entry to the UK and collaborated on developing new tailor-made products

Investors' Day | Rüschlikon, 8 December 2015

Life Capital has the ability to broaden its geographic presence

I

II III

IV

Closed book Open book

Selective European presence

• Market presence in several European countries, e.g. UK, Switzerland, Netherlands

Future opportunities

• Opportunities in other key insurance markets

UK and Ireland – “strong market presence”

• UK closed book market estimated at over GBP 400bn reserves

• Admin Re® has been involved in the processes for all material transactions during 2015

• Presence established in Ireland with acquisition of Guardian

Continental Europe – “future opportunities”

• Continental Europe with potential to develop functioning closed book markets

• Continental Europe demonstrates business trends similar to those that prompted closed book activity in the UK

58

Investors' Day | Rüschlikon, 8 December 2015

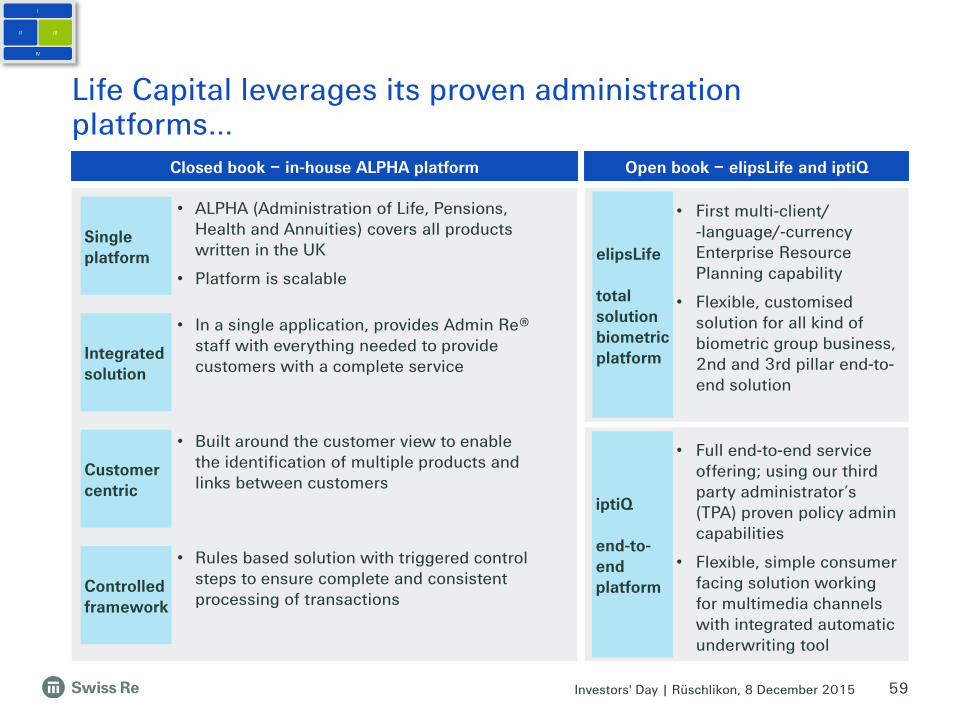

• First multi-client/-language/-currency Enterprise Resource Planning capability

• Flexible, customisedsolution for all kind of biometric group business, 2nd and 3rd pillar end-to-end solution

Life Capital leverages its proven administration platforms…

I

II III

IV

Closed book – in-house ALPHA platform Open book – elipsLife and iptiQ

• Full end-to-end service offering; using our third party administrator’s (TPA) proven policy admin capabilities

• Flexible, simple consumer facing solution working for multimedia channels with integrated automatic underwriting tool

Single platform

Integrated solution

Customer centric

Controlled framework

59

iptiQ

end-to-end platform

elipsLife

total solution biometric platform

• ALPHA (Administration of Life, Pensions, Health and Annuities) covers all products written in the UK

• Platform is scalable

• In a single application, provides Admin Re® staff with everything needed to provide customers with a complete service

• Built around the customer view to enable the identification of multiple products and links between customers

• Rules based solution with triggered control steps to ensure complete and consistent processing of transactions

Investors' Day | Rüschlikon, 8 December 2015

3.5

4.5

0.5

1.0

4.0

3.5

5.0

2.0

3.0

0

2.5

1.5

2006

1.5

0.2

2007

0.4

1.0

20082004

0.9

2.8

0.9

2014

in million

2015E

0.4

2013

3.3

20122011

3.63.1

3.9

2009

4.3

0.3

3.0

0.2

20052003

0.8

3.9

0.8

0

0.2

2010

Policy count

…and continues to support Swiss Re clients

Acquisitions Current closed books

Strong track record in successfully executing deals with long-term partners

AvivaHeritage

ZurichLife

BarclaysLife

MetLife

HSBC

ZurichLife

GELife

60

Guardian1 Growth in 2016

• 0.5m open book policies

• Future policy growth from open/closed books

I

II III

IV

Virgin Money

Life

1 Presented on a pro forma basis for 2015, transaction completion expected early 2016

Windsor Life

Investors' Day | Rüschlikon, 8 December 2015 61

• Important asset in acquiring closed books• Key element in developing new partnerships and sourcing distribution partners• Interaction and reputation with regulators

There are 4 key differentiators for Life Capital

• Superior client satisfaction and robust client response

• Offering client-centric products

• Exploring new propositions, e.g. Flexible Retirement Accounts; white-labelling life insurance solutions

Customer serviceIntegration & execution capabilities

Biometric data & knowledge

• Track record in acquiring closed books

• Demonstrated value extraction

• Operational excellence

• Integrated IT systems and service model which allow high speed to market

• Extensive granular biometric risk data

• Capability to make more accurate pricing decisions

• Provision of leading-edge automated and flexible underwriting engine

• Ability to design products tailored to clients’ needs

I

II III

IV

Trusted brand

Investors' Day | Rüschlikon, 8 December 2015

Summary and Q&A

broadenand diversify client

base to increase access to risk

optimiseresources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Life Capital – Agenda

62

Investors' Day | Rüschlikon, 8 December 2015

Life Capital expected to be a strong contributor to the Swiss Re Group

• Focus on successful integration of Guardian

• Continue to seek attractive acquisition targets in the UK closed books market and potentially in Continental Europe

• Accelerate growth in Europe and replicate the model in the US for open books

• Deliver 6-8% ROE in the mid-term

• Life Capital Business Unit builds on the Group’s strengths

• Attractive growth opportunities

• Differentiation through proven operating platforms, customer service, knowledge and trusted brand

• Building a balanced book of business

• Strong gross cash generation

Conclusion

Outlook & priorities

63

Corporate Solutions

Agostino GalvagniCEO Corporate Solutions

Investors' Day | Rüschlikon, 8 December 2015 65

On track to deliver against 2015 targets

in USD bn in %

1 Share of Swiss Re Group’s Economic Net Worth deployed across Business Units (excl. Group Items), 30 June 2015Note: Gross premiums written including premium for insurance in derivative form, net of internal fronting for the Reinsurance Business Unit; ROE shown from 2012 as Corporate Solutions has been reported as separate segment from Q1 2012; 9M 2015 ROE is annualised

3.9

2.7

4.2

2.6

3.4

Gross premiums written Return on Equity

• Commercial insurance Business Unit of the Swiss Re Group

• A key opportunity for growth10%

Economic Net Worth1

Target range 2015: 4-5

2012 2013 2014 9M 2015

~4

2012 2013 2014 2015E20112010

7.4

9.6

12.5

18.7

Target range 2015: 10-15

Baseline year

Investors' Day | Rüschlikon, 8 December 2015

2010Baseline year

2015 Achieved

Employees ~1 000 ~2 400

Offices 32 52

Operating platform

Operational sustainability

Sales

Underwriting

Harmonise and upgrade

Improve and maintain

Corporate Solutions has transformed itself since launch in 2010…

66

Maintain excellence

Segment and upgrade

Investors' Day | Rüschlikon, 8 December 2015 67

Liabilities

• Composition of funding changed with the introduction of subordinated debt

7.1

8.9

3.4

9.9

6.8

3.9

+26%Assets under management

Reinsurance recoverables

Other assets

-28%

2011 9M 2015

Assets

• Assets under management to gradually replace reinsurance recoverables which produce no investment income

2011 9M 2015

Equity

Subordinated debt

OtherLiabilities

2.3 2.4

17.817.0

…and so has our balance sheet, aligning with peers

0.5

Note: Corporate Solutions has been reported as separate segment from Q1 2012, with pro forma figures available for the prior year

in USD bn in USD bn

Investors' Day | Rüschlikon, 8 December 2015

Corporate Solutions – Agenda

68

broadenand diversify client

base to increase access to risk

optimise resources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015 69

Our portfolio is well diversified across lines of business, geographies and industries

By line of business By geography

By industry

Property

Casualty

Special Lines

GPW

29%

21%

36%

14%

Asia Pacific

EMEA

North America

Latin America

8%

GPW

Credit & Surety

9M 2015

57%

24%

11%

9M 2015

GPW

Note: Gross premiums written (GPW) including premium for insurance in derivative form, net of internal fronting; Special Lines includes Aviation & Space, Engineering, Marine and Energy Offshore; portfolio composition by industry relates to 9M 2015

14%

29%

21%

36%

5%4%

10%

16%

8%7%16%

4%3%

27%

Food & Tobacco

Retail & Trading

Life Sciences

Professional Services

Aviation

Transportation

Engineering & Construction

Credit, Agriculture, Weather

Energy & Utilities

Mining

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

We delivered strong profitable growth compared to peers since 2010…

70

Co

mb

ine

d r

ati

o 2

011

–2

01

4

Gross premiums growth 2010 – 2014 CAGR

80%

95%

110%13%

86%

16%-6% 5%

• Since 2010, continuously benchmarking ourselves against a selected set of 8 peers

Corporate Solutions

Insurers with global master policy capabilities

Insurers with multiregional focus

Insurers with wholesale focus

Source: Swiss Re Economic Research & Consulting Note: Peer group average weighted premium growth is in USD; Corporate Solutions combined ratio 2011-2013 is on basis of estimated total financial contribution to Swiss Re Group (ie Corporate Solutions business written, as shown at Investors' Day 2012, incl. development of historical loss reserves remaining in Reinsurance); combined ratio is shown starting 2011 as Corporate Solutions has been reported as separate segment from Q1 2012, with pro forma figures available for the prior year

Quadrants are determined based on average combined ratio and gross premiums compound annual growth rate (CAGR) over the years; bubble size = 2014 base

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

…but are very careful in the current market

71

Source: Swiss Re Economic Research & ConsultingNote: Peer group average weighted premium growth is in USD; due to consolidation in market number of peers reduced to 7 over the period

• Focused on maintaining underwriting discipline

Corporate Solutions

Insurers with global master policy capabilities

Insurers with multiregional focus

Insurers with wholesale focus

Gross premiums growth9M 2015 vs. 9M 2014

Co

mb

ine

d r

ati

o 9

M 2

01

5

92%

-19%

85%

104%

95%

-8% 15%-2%

Quadrants are determined based on average combined ratio and average gross premium growth rates; bubble size = 9M 2015 base where available, otherwise H1 2015

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

The commercial insurance market is very diverse and fragmented. Corporate Solutions ranks 25th overall...

72

Source: Swiss Re Economic Research & ConsultingNote: 2014 commercial insurance market premium: USD 740bn. In case of players writing business other than commercial insurance, only the commercial insurance premiums are shown

Players beyond top-30

Insurers with global master policy capabilities Insurers with regional focus

Insurers with wholesale focusInsurers with multiregional focus

Top 11-30 represent ~15% of market

Top-10 represent ~20% of market

Corporate Solutions

4.2

Top-30

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015 73

…but is a leader in the Excess Layer Market, and expandinginto the next segment

2014 commercial insurance market premium: USD 740bn

70

130

270

210

Wholesale

Retail

Granularity of distribution

Administrative load

Deal complexity

Main characteristics

Deal size

in USD bn

Primary Lead (mid-sized corporations)

Excess Layers(large corporations)

SMEs

Workers’ Compensation and Commercial Auto

Pe

ne

tra

tio

n

Source: Swiss Re Economic Research & Consulting

60Global Master Policies

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

We are on our way to become a Primary Lead insurer

74

Ambition: Generate additional premiums of USD 1.0bn – 1.5bn by 2020

Primary Lead capabilities (in place or to be rolled-out in 2016)

Latin America: • Colombia (Casualty; 2016: Property)• Brazil (Property, Marine; 2016:

Casualty)

North America: • Canada (P&C)• US (Property, FinPro; 2016: Casualty)

EMEA: • Italy (P&C, FinPro, Marine) • France (P&C, Marine)• Germany (P&C; 2016: FinPro)

• UK (2016: P&C, FinPro)• Netherlands (2016: P&C)• South Africa (2016: P&C)• Switzerland (2016: P&C, FinPro)

Asia Pacific: • China (P&C)• Singapore (Casualty, FinPro)• Australia (2016: Property)

Capabilities being developed:

• Products: Develop primary products in line with local standards; ability to price primary products

• Services: Establish local services (esp. Claims and Risk Engineering)

• Systems: Integrate management of co-insurance panels into current platforms and processes

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Our distribution footprint is global and growing…52 offices across 20 countries

Local presence & insurance license

Local insurance license

Local presence & reinsurance license

EMEA: 12 offices

North America: 23 offices

Note: Latin America includes Miami as hub for the region

75

Latin America: 7 offices

Asia Pacific: 10 offices

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

…and we strengthened our presence in our 12 key High Growth Markets

No local presenceAlready well covered Local presence to be strengthened

76

I

II III

IV

South AfricaOffice opened in 2015

SingaporeInsurance license obtained in 2013

IndiaTurkey UAEDubai office opened

in 2012

BrazilUBF acquisition in 2011

Chile

ColombiaSeguros Confianzaacquisition in 2014

Hong Kong

MalaysiaReinsurance license obtained in 2015, Origination/UW out of Singapore

ChinaSun Alliance China

acquisition in 2015

Mexico

Investors' Day | Rüschlikon, 8 December 2015

We hired ~2 000 new employees since launch in October 2010…

77

2010Baseline year

33

2015 Achieved

Nu

mb

er

of

em

plo

yee

s

~1 000

~2 400

~600 Inorganic growth

Organic growth

Intra Group shifts ~600

Attrition

~200 (~600) ~600

Replacements

~25%~7%

X%Share of High Growth Markets

• Tailor-made onboarding programme

• Employee engagement index 12% above global financial insurance industry

• Share of staff in High Growth Markets increased to ~25%

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015 78

• Productivity gains achieved through:

– Re-design and simplification of end-to-end underwriting process

– More efficient allocation of underwriting tasks, leveraging service centres

– Re-shaping of IT landscape

Work units per FTE Premiums per FTE

+23% productivity

increase

2013 H1 2015 2013 H1 2015

+10% productivity

increase

Note: Work units per FTE are transactional actions related to handling submissions, submitting quotes and binding transactions. FTE are weighted: underwriters/originators: 1, business support: 0.5, service centre support: 0.25; productivity metrics are rolling full-year views available since 2013; lower increase in Premium per FTE compared to Work units per FTE mainly reflects shift towards smaller deal size

~110~135

~2.9~3.2

in USD m

I

II III

IV

…and we significantly increased our productivity

Investors' Day | Rüschlikon, 8 December 2015 79

Three key factors differentiate us from competitors

Corporate Solutions' value proposition

~500 transactions with USD 100m capacity or more

in 2014

Opens doors and attracts talents• Leading brand

• Financial strength

• "We are here to stay“

• Large net capacity

• Innovation

Supported by

– Superior underwriting knowledge

– Disciplined cycle management

– Proactive claims management

~40 innovative transactions

in 2014

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Innovation capabilities in several areas, acknowledged by the market

80

Bespoke structures

• Multi-line/multi-yearsolutions

• Non-damage business interruption

• Parametric solutions

Derivative solutions

• Temperature and weather related derivatives

• Crop shortfall derivatives

New risks

• Cyber risk: Partnership with IBM

I

II III

IV

Awards

Innovative transaction of the year in Switzerland

2015

First solar radiation index transaction in China

2015

Energy Risk Weather House of the year

2012, 2013, 2014

Investors' Day | Rüschlikon, 8 December 2015

Summary and Q&A

broadenand diversify client

base to increase access to risk

optimise resources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Corporate Solutions – Agenda

81

Investors' Day | Rüschlikon, 8 December 2015

• Ambition to grow, further increasing Corporate Solutions’ relevance to the Swiss Re Group

• Key initiatives for growth beyond 2015 are

– Expanding into Primary Lead and

– Further broadening of the footprint

• Continue to carefully navigate the current market with unchanged focus on profitability

• On track to deliver against 2015 targets

• Transformed into a larger and more solid player, with a

– Distinct value proposition building on our leading brand, large net capacity and innovation capabilities

– Leadership position in the Excess Layer Market

– Distribution network of 52 offices in 20 countries

Key messages

82

Conclusion

Outlook & priorities

Christian MumenthalerCEO Reinsurance

Reinsurance

Investors' Day | Rüschlikon, 8 December 2015 84

Swiss Re’s largest Business Unit delivers strong results

1 Share of Swiss Re Group’s Economic Net Worth deployed across Business Units (excl. Group Items), 30 June 2015

Combined ratio and operating margin Return on Equity

• Wholesale reinsurance leader offering products and related services in property and casualty, as well as in life and health

• Foundation of Swiss Re Group’s strength

• Strong performance over the last years and YTD

L&H

P&C49%

31%

Economic Net Worth1

in %

80.7 84.883.8 83.7

P&C: Combined ratio

8.6

FY 14 9M 15FY 13FY 12

5.8

2.6

10.7

L&H: Operating margin

17.0

23.3

9M 15FY 12 FY 14FY 13

-7.9

26.026.7 26.7

6.4

8.9

in %

P&C L&H

Investors' Day | Rüschlikon, 8 December 2015

Reinsurance – Agenda

85

broadenand diversify client

base to increase access to risk

optimise resources and

platforms to support capital allocation

systematically allocate capital to risk pools / revenue streams

emphasise differentiation

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015

Key success factors:

• Integrated economic framework to steer both P&C and L&H Reinsurance businesses, including planning, pricing and reserving

• Active portfolio steering between and within P&C and L&H Reinsurance businesses

• Separation of pricing and costing to enable transparent decision making

• Feedback loop allows to optimise costing

Swiss Re - Steering Framework

86

Since 2006 we have a Group-wide process for business steering and underwriting which is successfully applied in Reinsurance

StrategyLearning

Capitalallocation

&Target

setting

Decision making

Portfolio-& perform-

ancemeasure-

ment

EVM

1

2

3

4

I

II III

IV

1

2

3

4

Investors' Day | Rüschlikon, 8 December 2015

We shifted the portfolios in line with our underwriting framework and growth strategy

P&C Reinsurance portfolio composition1

1 Data before external retro and other items; average Q3 2015 FX rates used for all years; Line of business split does not include High Growth Markets business

L&H Reinsurance portfolio composition1

US GAAP Gross Earned Premiums US GAAP Gross Earned Premiums

22% 24% 22% 22% 19% 16%

18% 17% 18% 17%15%

15%

15% 13% 10% 9%10% 10%

17%11%

13% 14%15% 17%

9%

9% 11% 10%8% 11%

11% 12% 9%14% 10%

14% 15% 15% 18% 20% 21%

9M 201520142013201220112010

4%

Property Non-Prop

Property Prop / Fac

Specialty

Casualty (excl. Motor)

Motor

HGM (Motor China only)

HGM (excl. Motor China)

74% 73% 70% 67% 64% 60%

19% 20% 23% 25% 28%31%

7% 7% 7% 7% 8% 9%

9M 201520142013201220112010

LifeHGM Health

I

II III

IV

87

• P&C: High Growth Markets driver for growth; reduction of Property since 2013 due to price developments

• L&H: continuous growth of Health and business in High Growth Markets

Investors' Day | Rüschlikon, 8 December 2015

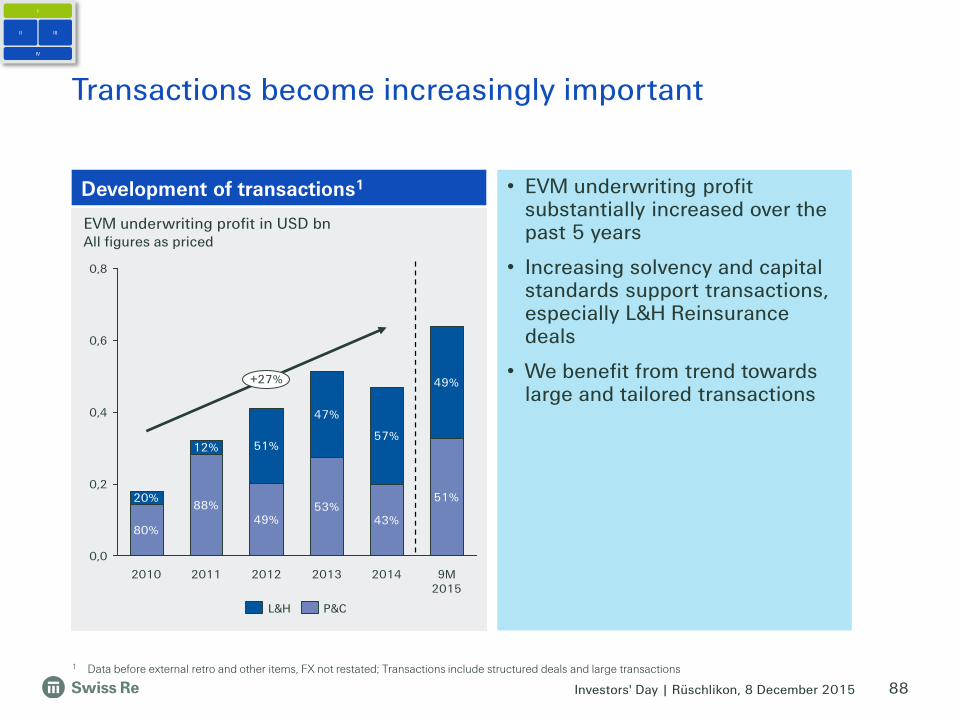

Transactions become increasingly important

88

0,4

0,6

0,2

0,0

0,8

9M 2015

49%

51%

+27%

2014

43%

57%

2013

53%

47%

2012

49%

51%

2011

88%

12%

2010

80%

20%

Development of transactions1

EVM underwriting profit in USD bnAll figures as priced

L&H P&C

1 Data before external retro and other items, FX not restated; Transactions include structured deals and large transactions

I

II III

IV

• EVM underwriting profit substantially increased over the past 5 years

• Increasing solvency and capital standards support transactions, especially L&H Reinsurance deals

• We benefit from trend towards large and tailored transactions

Investors' Day | Rüschlikon, 8 December 2015

0%

10%

20%

30%

40%

50%

9M 201520122010 2014201320112009

Operating income2Revenues1

P&C – Swiss Re has been consistently outperforming the market with regards to profitability

89

• Average revenue share of 21%

• Average profit share of 30%

Swiss Re P&C Reinsurance revenues and operating income2 share vs other reinsurers 40%

Market share of top 7 reinsurers

In 2011, the industry experienced extraordinary high natural catastrophe losses. Swiss Re was hit to a lesser extent than peers.

I

II III

IV

1 Revenues exclude net realised investment gains 2 Operating income is income before tax and before interest for financial debt, excluding net realised investment gains (losses) Top 7 reinsurers include: Swiss Re, Munich Re, Hannover Re, PartnerRe, SCOR, Everest Re, AlleghanySource: Swiss Re Economic Research and Consulting

Investors' Day | Rüschlikon, 8 December 2015

-10%

0%

10%

20%

30%

40%

9M 201520122010 2014201320112009

90

L&H – Swiss Re with significant portion of profit pool

1 Revenues exclude net realised investment gains; limited comparability due to different accounting standards of peer group; Top 6 reinsurers include Swiss Re, Munich Re, Hannover Re, PartnerRe, SCOR, RGA

2 Operating income is income before tax and before interest for financial debt, excluding net realised investment gains (losses) Source: Swiss Re Economic Research and Consulting

• Average revenue share of 23%

• Average profit share of 25%

Swiss Re L&H Reinsurance revenues and operating income2 share vs other reinsurers

70%

Market share of top 6 reinsurers

I

II III

IV

2014 was impacted by Swiss Re’s decisive management actions in respect of pre-2004 US YRT business and the unwind of a funding structure.

Operating income2Revenues1

Investors' Day | Rüschlikon, 8 December 2015 91

L&H Reinsurance shows strong underlying results – well on track to achieve 2015 ROE target

• L&H Reinsurance well on track to achieve its ROE target of 10-12%

• Management of in-force blocks of business continues to be a key priority

• 2014 results impacted by decisive management actions, setting the foundation for profitable growth

• 9M 2015 operating income and margins have developed within expected range

• Mortality/morbidity experience vs. expected is also tracking within our expected volatility

Return on Equity

1 Model/assumption changes in relation to VA/GMDB/B36 are shown as part of “Model/assumption changes”2 Adjusted for realised gains/losses and model-/assumption-updates, and large one offs, net of tax3 Same as described in footnote 2 and for USD 5.5bn equity capital base, announced in the June 2013 Investors’ Day

Operating income adjustments

• Mortality/morbidity experience vs. expected 138 -16

• Model/assumption changes1 -87 81

• VA/GMDB/B361 -1 12

• Other one-offs -623 0

Operating margin, % 2.6 10.7

FY 2014 9M 2015

Operating income of which approximately 331 986

I

II III

IV

in USD m

-7.9

17.0

5.7

11.8

6.5

12.6

FY 2014 9M 2015

ROE, reported

ROE, adjusted

ROE, adjusted on USD5.5bn equity

2

3

in %

Investors' Day | Rüschlikon, 8 December 2015 92

Four focus areas to broaden and diversify client base to increase access to risk

High Growth MarketsContinue to expand geographically, and be the global leader

Regionals & Nationals (R&N)Significant growth in volume and number of clients since start of initiative

CasualtyWe actively manage the Casualty business according to the pricing cycle

HealthAddressing the health-protection need of the ageing population

I

II III

IV

Investors' Day | Rüschlikon, 8 December 2015 93

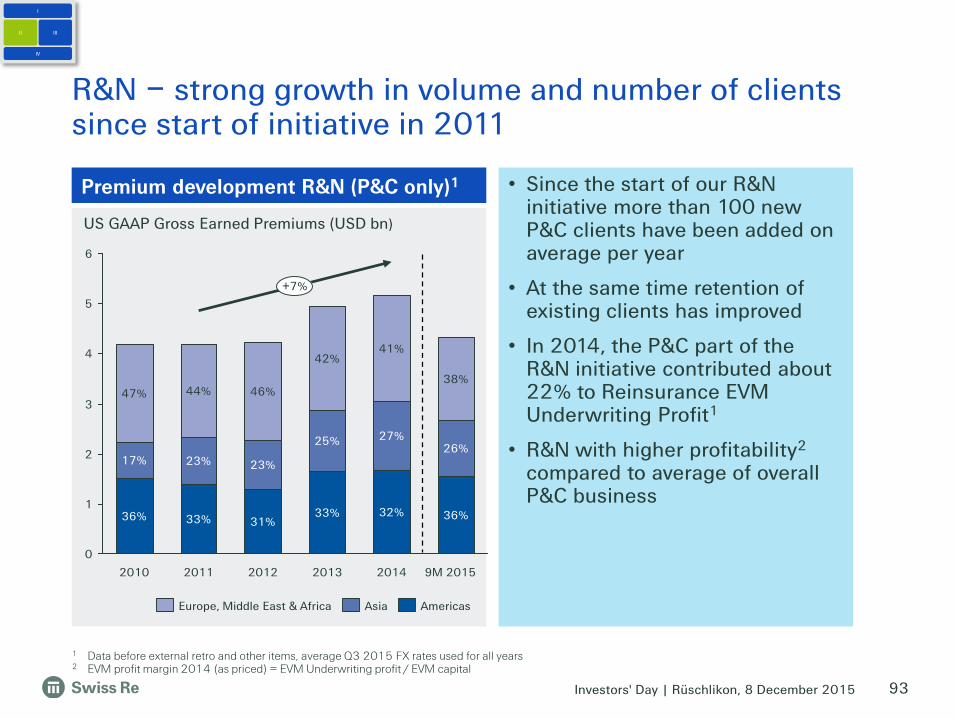

R&N – strong growth in volume and number of clients since start of initiative in 2011

Premium development R&N (P&C only)1

2

1

5

0

6

4

344%

2014

38%

26%27%

41%

2013

32%

2012

31%

46%

23%

2011

33%

2010

36%

17%

47%

23%

42%

33%

25%

36%

+7%