investors, mutual funds & returns trend analysis report · performance* of equity-oriented...

TRANSCRIPT

Investors, Mutual

Funds & Returns –

Trend Analysis

Report

July 2018

Industry Size

Investor Trends

Inflow Outflow Analysis

Sector Update

Category Performance

Industry Insights

Regulatory Update

Mutual Fund Screener – What’s Inside

Industry Size

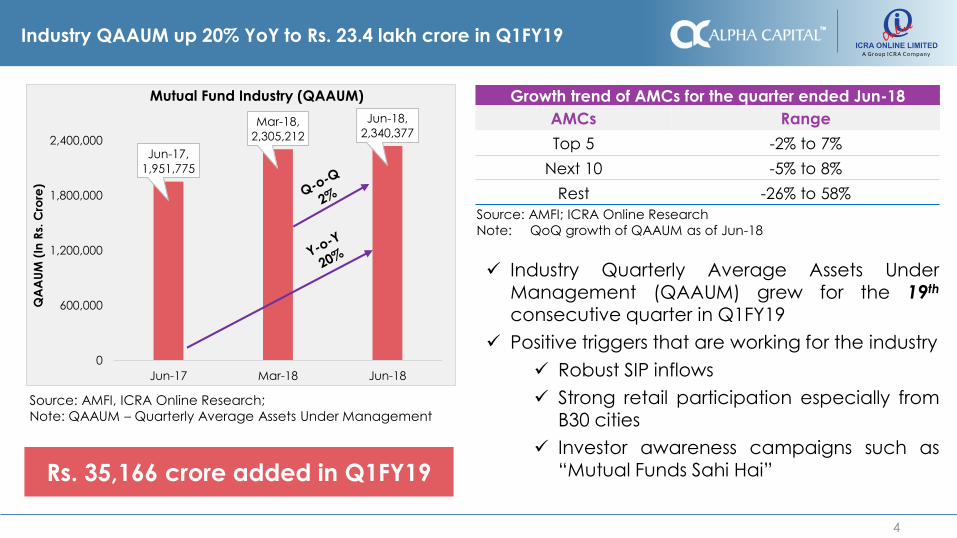

Industry QAAUM up 20% YoY to Rs. 23.4 lakh crore in Q1FY19

Growth trend of AMCs for the quarter ended Jun-18

AMCs Range

Top 5 -2% to 7%

Next 10 -5% to 8%

Rest -26% to 58%

Source: AMFI; ICRA Online Research

Note: QoQ growth of QAAUM as of Jun-18

4

Rs. 35,166 crore added in Q1FY19

Jun-17,

1,951,775

Mar-18,

2,305,212

Jun-18,

2,340,377

0

600,000

1,200,000

1,800,000

2,400,000

Jun-17 Mar-18 Jun-18

QA

AU

M (

In R

s. C

rore

)

Mutual Fund Industry (QAAUM)

Source: AMFI, ICRA Online Research;

Note: QAAUM – Quarterly Average Assets Under Management

✓ Industry Quarterly Average Assets UnderManagement (QAAUM) grew for the 19th

consecutive quarter in Q1FY19

✓ Positive triggers that are working for the industry

✓ Robust SIP inflows

✓ Strong retail participation especially fromB30 cities

✓ Investor awareness campaigns such as“Mutual Funds Sahi Hai”

Top 10 AMCs account for ~81% of QAAUM

5

Source: AMFI, ICRA Online Research

-2%

0%

2%

4%

6%

8%

0

70,000

140,000

210,000

280,000

350,000

ICICI

Prudential

Mutual Fund

HDFC Mutual

Fund

Aditya Birla

Sun Life

Mutual Fund

Reliance

Mutual Fund

SBI Mutual

Fund

UTI Mutual

Fund

Kotak

Mahindra

Mutual Fund

Franklin

Templeton

Mutual Fund

DSP

BlackRock

Mutual Fund

Axis Mutual

Fund

Q-o

-Q G

row

th (

In %

)

QA

AU

M (

In R

s. C

rore

)

Top 10 AMCs

Jun-18 Mar-18 % Change QoQ

QAAUM ≥ Rs. 3 lakh crore QAAUM ≥ Rs. 2 lakh

crore and < Rs. 3 lakh crore

QAAUM ≥ Rs. 1 lakh crore and < Rs. 2 lakh crore

0%

25%

50%

75%

100%

125%

0

20,000

40,000

60,000

80,000

Mira

e A

sse

t M

F

Ma

hin

dra

MF

Mo

tila

l Osw

al

MF

Ed

elw

eis

s M

F

L&T

MF

IIFL

MF

PP

FA

S M

F

IDB

I M

F

BO

I A

XA

MF

IL&

FS M

F (

IDF)

Yo

Y G

row

th (

In %

)

QA

AU

M (

In R

s. C

rore

)

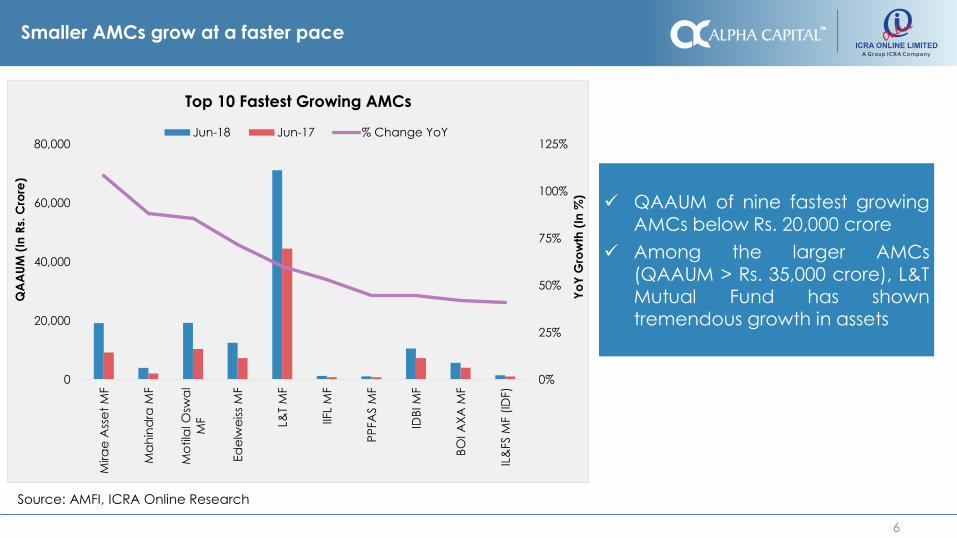

Top 10 Fastest Growing AMCs

Jun-18 Jun-17 % Change YoY

Source: AMFI, ICRA Online Research

Smaller AMCs grow at a faster pace

6

✓ QAAUM of nine fastest growingAMCs below Rs. 20,000 crore

✓ Among the larger AMCs

(QAAUM > Rs. 35,000 crore), L&TMutual Fund has showntremendous growth in assets

Private sector JVs (predominantly Indian) manage 54% of Q1FY19 QAAUM

7

Category

As a % of

Q1FY19

QAAUM

QAAUM (In Rs. Crore) Growth

Q1FY19 Q4FY18 Q1FY18 QoQ YoY

Bank Sponsored

Joint Ventures - Predominantly Indian 10.9% 255,479 240,779 187,361 6.1% 36.4%

Joint Ventures - Predominantly Foreign 0.5% 10,540 10,760 7,296 -2.0% 44.5%

Others 6.9% 161,176 165,653 155,411 -2.7% 3.7%

Institutions Indian 0.9% 21,057 20,768 24,373 1.4% -13.6%

Private Sector

Indian 17.8% 416,337 408,322 327,390 2.0% 27.2%

Joint Ventures - Predominantly Indian 54.5% 1,275,327 1,262,372 1,076,539 1.0% 18.5%

Foreign 6.7% 156,572 153,271 130,555 2.2% 19.9%

Joint Ventures - Predominantly Foreign 0.9% 20,752 19,692 16,175 5.4% 28.3%

Joint Ventures – Others 1.0% 23,137 23,595 25,720 -1.9% -10.0%

Source: AMFI, ICRA Online Research

Note: QoQ – Q1FY19 vs Q4FY18; YoY – Q1FY19 vs Q1FY18

Investor Trends

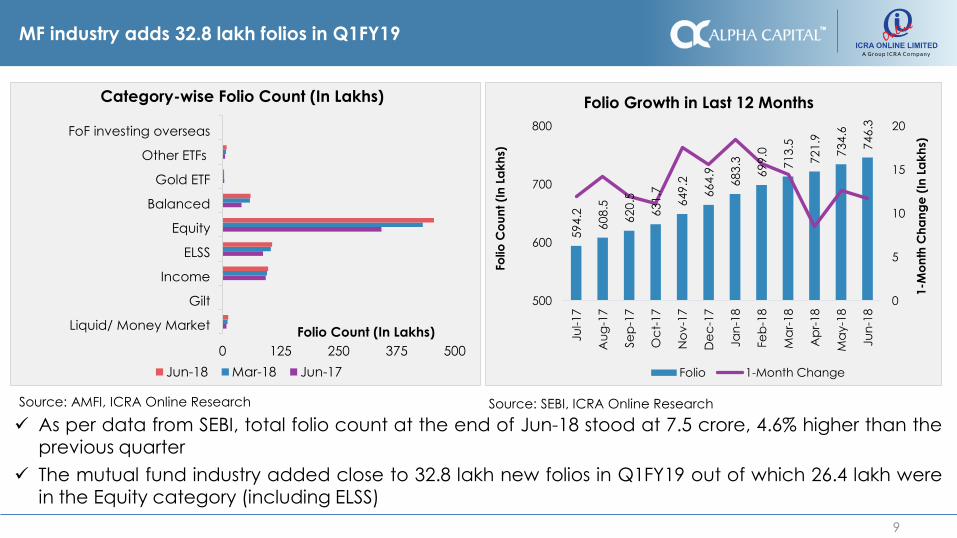

MF industry adds 32.8 lakh folios in Q1FY19

9

0 125 250 375 500

Liquid/ Money Market

Gilt

Income

ELSS

Equity

Balanced

Gold ETF

Other ETFs

FoF investing overseas

Folio Count (In Lakhs)

Category-wise Folio Count (In Lakhs)

Jun-18 Mar-18 Jun-17

Source: AMFI, ICRA Online Research

59

4.2

60

8.5

62

0.5

63

1.7

64

9.2

66

4.9

68

3.3

69

9.0

71

3.5

72

1.9

73

4.6

74

6.3

0

5

10

15

20

500

600

700

800

Ju

l-17

Au

g-1

7

Se

p-1

7

Oc

t-1

7

No

v-1

7

De

c-1

7

Ja

n-1

8

Fe

b-1

8

Ma

r-18

Ap

r-1

8

Ma

y-1

8

Ju

n-1

8

1-M

on

th C

ha

ng

e (

In L

ak

hs)

Fo

lio

Co

un

t (I

n L

ak

hs)

Folio Growth in Last 12 Months

Folio 1-Month Change

Source: SEBI, ICRA Online Research

✓ As per data from SEBI, total folio count at the end of Jun-18 stood at 7.5 crore, 4.6% higher than theprevious quarter

✓ The mutual fund industry added close to 32.8 lakh new folios in Q1FY19 out of which 26.4 lakh werein the Equity category (including ELSS)

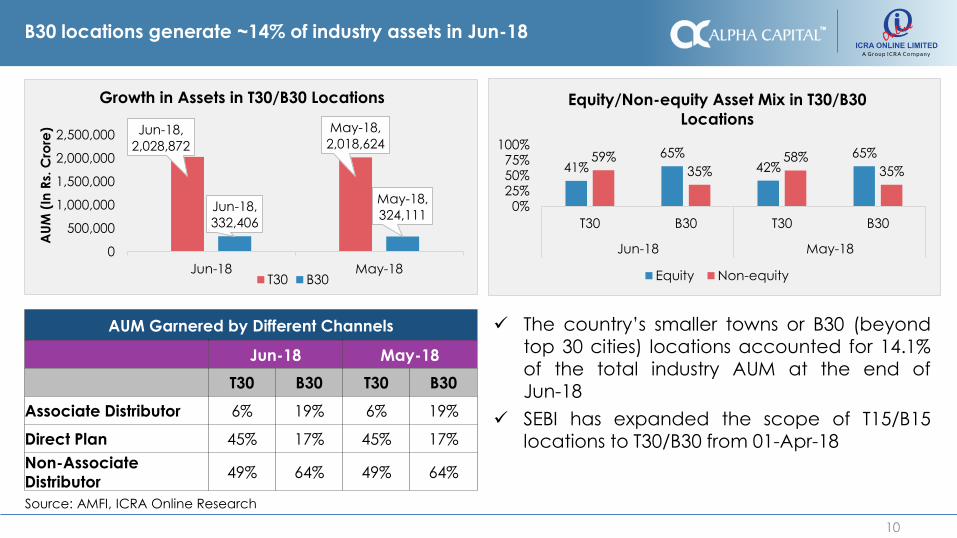

B30 locations generate ~14% of industry assets in Jun-18

10

Source: AMFI, ICRA Online Research

Jun-18,

2,028,872

May-18,

2,018,624

Jun-18,

332,406

May-18,

324,111

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Jun-18 May-18

AU

M (

In R

s. C

rore

)

Growth in Assets in T30/B30 Locations

T30 B30

41%65%

42%65%59%

35%58%

35%

0%25%50%75%

100%

T30 B30 T30 B30

Jun-18 May-18

Equity/Non-equity Asset Mix in T30/B30

Locations

Equity Non-equity

✓ The country’s smaller towns or B30 (beyondtop 30 cities) locations accounted for 14.1%of the total industry AUM at the end ofJun-18

✓ SEBI has expanded the scope of T15/B15locations to T30/B30 from 01-Apr-18

AUM Garnered by Different Channels

Jun-18 May-18

T30 B30 T30 B30

Associate Distributor 6% 19% 6% 19%

Direct Plan 45% 17% 45% 17%

Non-Associate

Distributor49% 64% 49% 64%

Inflow Outflow Analysis

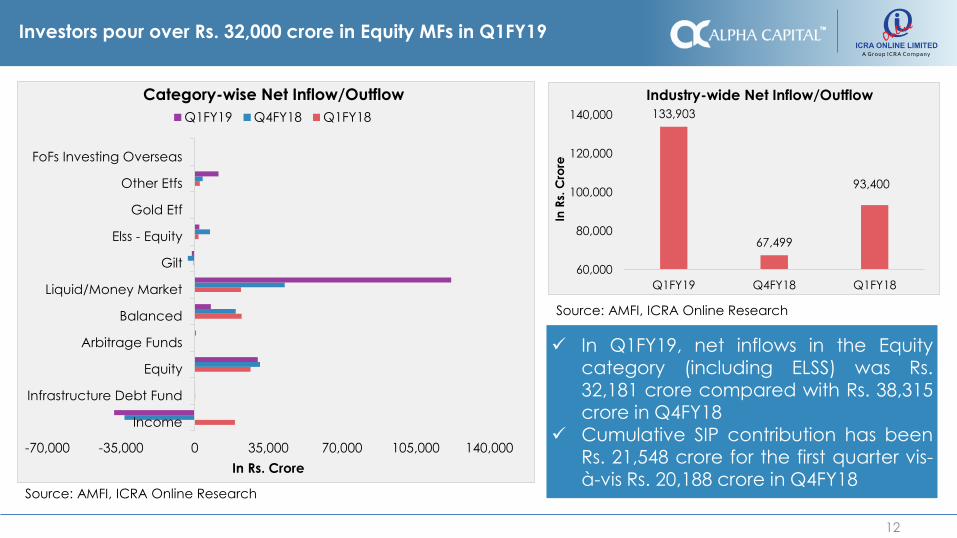

Investors pour over Rs. 32,000 crore in Equity MFs in Q1FY19

12

✓ In Q1FY19, net inflows in the Equity

category (including ELSS) was Rs.32,181 crore compared with Rs. 38,315crore in Q4FY18

✓ Cumulative SIP contribution has beenRs. 21,548 crore for the first quarter vis-à-vis Rs. 20,188 crore in Q4FY18

-70,000 -35,000 0 35,000 70,000 105,000 140,000

Income

Infrastructure Debt Fund

Equity

Arbitrage Funds

Balanced

Liquid/Money Market

Gilt

Elss - Equity

Gold Etf

Other Etfs

FoFs Investing Overseas

In Rs. Crore

Category-wise Net Inflow/Outflow

Q1FY19 Q4FY18 Q1FY18

Source: AMFI, ICRA Online Research

133,903

67,499

93,400

60,000

80,000

100,000

120,000

140,000

Q1FY19 Q4FY18 Q1FY18

In R

s. C

rore

Industry-wide Net Inflow/Outflow

Source: AMFI, ICRA Online Research

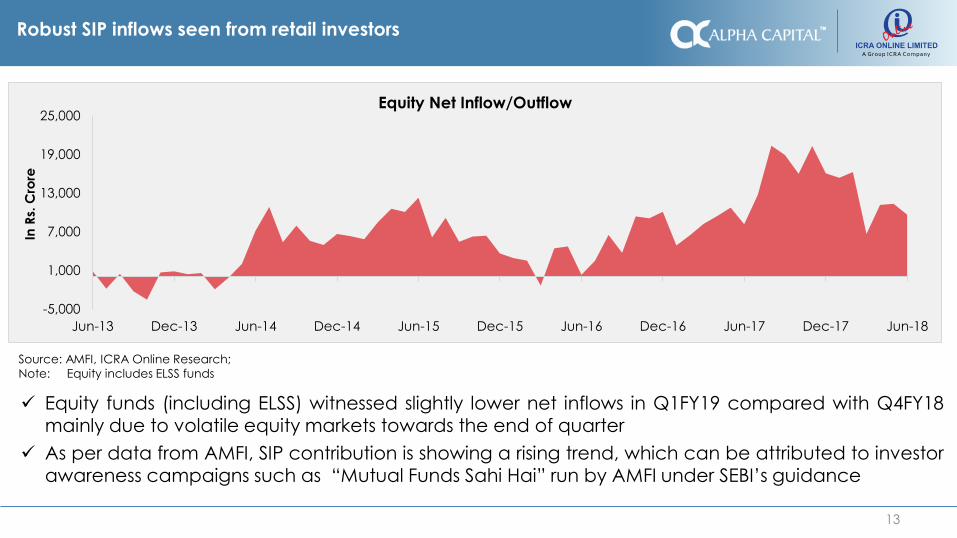

Robust SIP inflows seen from retail investors

13

-5,000

1,000

7,000

13,000

19,000

25,000

Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18

In R

s. C

rore

Equity Net Inflow/Outflow

Source: AMFI, ICRA Online Research;

Note: Equity includes ELSS funds

✓ Equity funds (including ELSS) witnessed slightly lower net inflows in Q1FY19 compared with Q4FY18mainly due to volatile equity markets towards the end of quarter

✓ As per data from AMFI, SIP contribution is showing a rising trend, which can be attributed to investor

awareness campaigns such as “Mutual Funds Sahi Hai” run by AMFI under SEBI’s guidance

Sector Update

Top 5 sectors constitute about 52% of the total equity AUM

15

✓ AMCs continue to bet on Bank and Finance sectors with ~ 31% of the total equity AUM

✓ Pharmaceuticals made it to the top five due to higher allocation compared with previous quarter

30,5

17

8,4

30

13,5

83

4,2

09

5,9

38

28,0

71

13,3

80

10,9

84

11,0

76

6,2

91

18,3

08

6,2

05 1

0,1

63

10,0

30

7,4

07

16,5

79

8,1

44

3,5

78

3,3

47

5,5

19

13,7

79

10,6

18

6,2

09

7,5

17

5,4

33

0

8,000

16,000

24,000

32,000

Banks Finance Software Consumer Non Durables Pharmaceuticals

Eq

uity

AU

M (

In R

s. C

rore

)

Equity exposure of Top 5 AMCs in Top 5 sectors (Jun-18)

HDFC Mutual Fund SBI Mutual Fund ICICI Prudential Mutual Fund Reliance Mutual Fund Aditya Birla Sun Life Mutual Fund

Source: AMFI, ICRA Online Research

Software sector sees the highest growth in inflow in percentage terms

16

-10.0%

10.0%

30.0%

50.0%

70.0%

0

45,000

90,000

135,000

180,000B

an

ks

Fin

an

ce

So

ftw

are

Co

nsu

me

r

No

n

Du

rab

les

Ph

arm

ac

eu

ti

ca

ls Au

to

Co

nst

ruc

tio

n

Pro

jec

t

Pe

tro

leu

m

Pro

du

cts

Po

we

r

Au

to

An

cill

arie

s

% C

ha

ng

e Y

oY

In R

s. C

rore

Sector wise Inflow in Jun-18 Vis-a-vis Mar-18 and Jun-17Jun-18 Mar-18 Jul-17 % change - QoQ % change - YoY

Source: AMFI, ICRA Online Research

Note: Only top-10 sectors considered

Category Performance

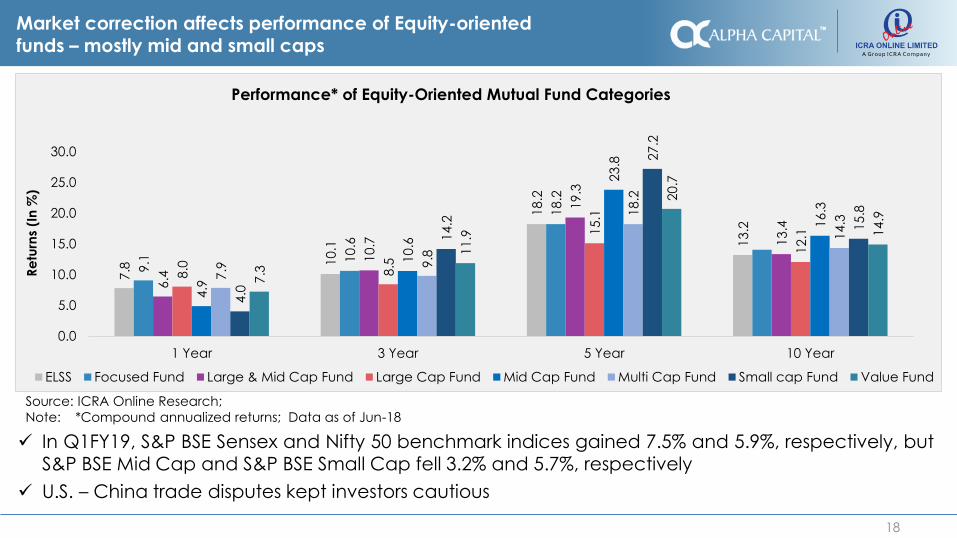

Market correction affects performance of Equity-oriented funds – mostly mid and small caps

18

7.8

10.1

18.2

13.2

9.1 1

0.6

18.2

6.4

10.7

19.3

13.4

8.0 8.5

15.1

12.1

4.9

10.6

23.8

16.3

7.9 9

.8

18.2

14.3

4.0

14.2

27.2

15.8

7.3

11.9

20.7

14

.9

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1 Year 3 Year 5 Year 10 Year

Re

turn

s (I

n %

)

Performance* of Equity-Oriented Mutual Fund Categories

ELSS Focused Fund Large & Mid Cap Fund Large Cap Fund Mid Cap Fund Multi Cap Fund Small cap Fund Value Fund

Source: ICRA Online Research;

Note: *Compound annualized returns; Data as of Jun-18

✓ In Q1FY19, S&P BSE Sensex and Nifty 50 benchmark indices gained 7.5% and 5.9%, respectively, butS&P BSE Mid Cap and S&P BSE Small Cap fell 3.2% and 5.7%, respectively

✓ U.S. – China trade disputes kept investors cautious

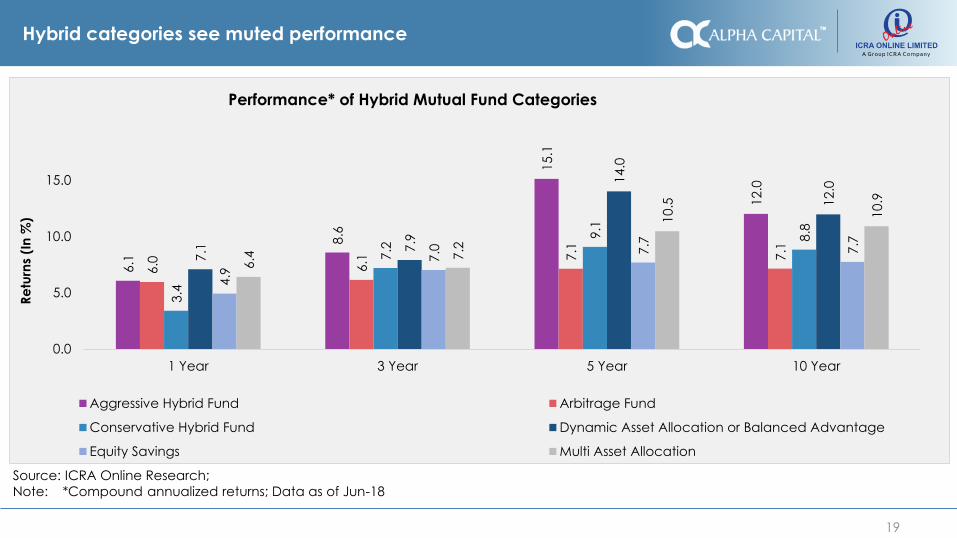

Hybrid categories see muted performance

19

6.1

8.6

15.1

12.0

6.0 6.1 7

.1

7.1

3.4

7.2

9.1

8.8

7.1 7

.9

14.0

12.0

4.9

7.0 7

.7

7.7

6.4 7

.2

10.5

10.9

0.0

5.0

10.0

15.0

1 Year 3 Year 5 Year 10 Year

Re

turn

s (I

n %

)

Performance* of Hybrid Mutual Fund Categories

Aggressive Hybrid Fund Arbitrage Fund

Conservative Hybrid Fund Dynamic Asset Allocation or Balanced Advantage

Equity Savings Multi Asset Allocation

Source: ICRA Online Research;

Note: *Compound annualized returns; Data as of Jun-18

20

Debt-oriented categories post muted returns

Key drivers:

✓ Bond yields continued to rise in Q1FY19 over concerns of widening fiscal deficit and tightening ofmonetary policy

✓ Medium- to long-term debt funds posted poor returns in the short-term periods

-3.0

5.3

2.4

2.3

1.1

-0.8

7.0

6.1

0.2

6.3

4.5 4.8

3.7

1.6

7.0

6.6

-1.2

6.3

4.7 5

.4

3.9

1.2

6.9

6.57.1 7.4

7.0 7.2

7.1

7.1 7.4

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Gilt Fund Low Duration

Fund

Short Duration

Fund

Credit Risk

Fund

Corporate

Bond Fund

Dynamic Bond Liquid Fund Ultra Short

Duration Fund

Re

turn

s (I

n %

)

Performance* of debt funds

3 Months 6 Months 1 Year 3 YearsSource: ICRA Online Research

Note: *Compound annualised returns for periods ≥1 year; Simple annualised returns for <1 year; Data as of Jun-18

Long Term Medium Term Short Term

Industry Insights

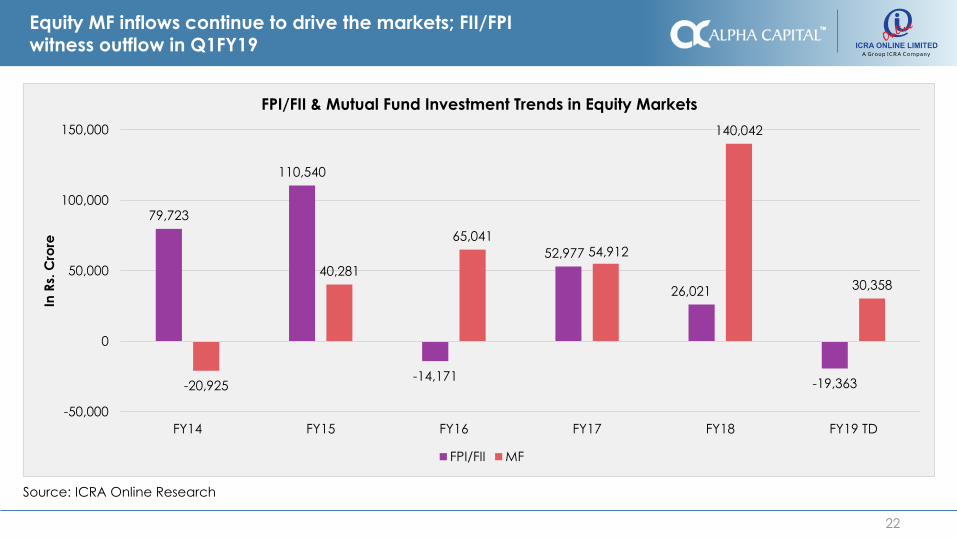

Equity MF inflows continue to drive the markets; FII/FPI witness outflow in Q1FY19

22

79,723

110,540

-14,171

52,977

26,021

-19,363-20,925

40,281

65,04154,912

140,042

30,358

-50,000

0

50,000

100,000

150,000

FY14 FY15 FY16 FY17 FY18 FY19 TD

In R

s. C

rore

FPI/FII & Mutual Fund Investment Trends in Equity Markets

FPI/FII MF

Source: ICRA Online Research

Instrument allocation pattern in debt segment

23

0%

25%

50%

Bond/

Debenture

CP CD Gilt SDL T Bill Others REITs & InvITs Cash &

Equivalents

In %

Jun-18 Mar-18 Dec-17

Source: ICRA Online Research

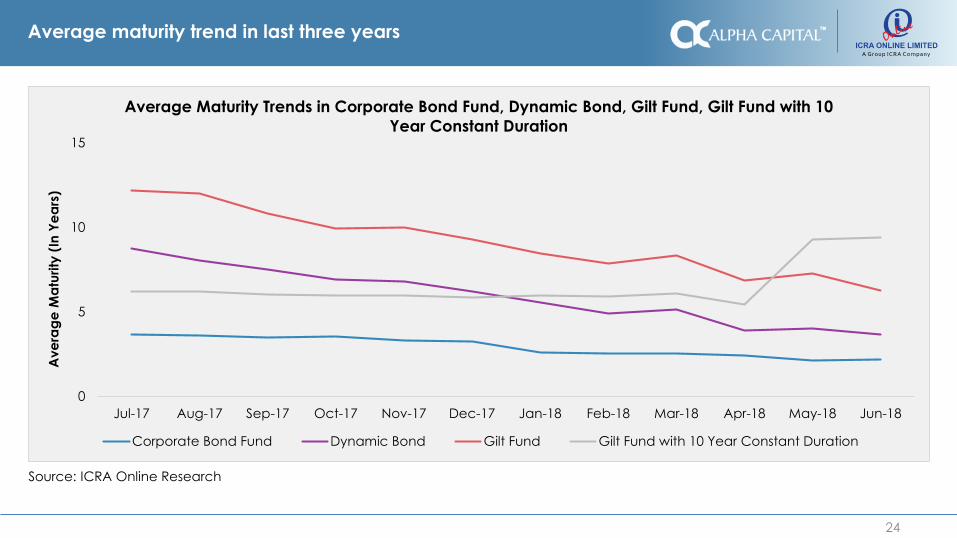

Average maturity trend in last three years

24

0

5

10

15

Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18

Ave

rag

e M

atu

rity

(In

Ye

ars

)

Average Maturity Trends in Corporate Bond Fund, Dynamic Bond, Gilt Fund, Gilt Fund with 10

Year Constant Duration

Corporate Bond Fund Dynamic Bond Gilt Fund Gilt Fund with 10 Year Constant Duration

Source: ICRA Online Research

Regulatory Update

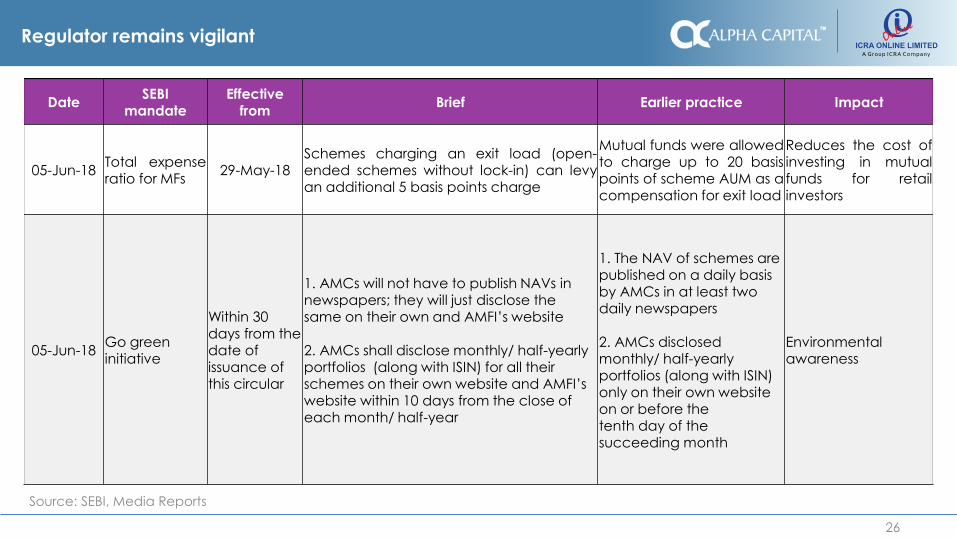

Regulator remains vigilant

26

DateSEBI

mandateEffective

fromBrief Earlier practice Impact

05-Jun-18Total expenseratio for MFs

29-May-18Schemes charging an exit load (open-ended schemes without lock-in) can levyan additional 5 basis points charge

Mutual funds were allowedto charge up to 20 basispoints of scheme AUM as acompensation for exit load

Reduces the cost ofinvesting in mutualfunds for retailinvestors

05-Jun-18Go green initiative

Within 30 days from the date of issuance of this circular

1. AMCs will not have to publish NAVs in newspapers; they will just disclose the same on their own and AMFI’s website

2. AMCs shall disclose monthly/ half-yearly portfolios (along with ISIN) for all their schemes on their own website and AMFI’s website within 10 days from the close of each month/ half-year

1. The NAV of schemes are published on a daily basis by AMCs in at least two daily newspapers

2. AMCs disclosed monthly/ half-yearly portfolios (along with ISIN) only on their own website on or before thetenth day of the succeeding month

Environmental awareness

Source: SEBI, Media Reports

MUMBAI

15, Ground Floor, Dosti shoppe

Link Dosti Acres, Antop Hill,

Wadala (East)

Mumbai - 400 037 Maharashtra,

Ph : 022 -2414 8864.

Contact Us

GURGAON

1154, 11th Floor Tower B, Spaze

Techpark, Sohna Road

Gurgaon - 122001

Haryana, Ph : 0124-4246036/8

Fax : 0124-4246037.

KOLKATA

Malancha, 4A, Elgin Road,

Kolkata - 700020 West Bengal,

Ph : 033 - 4003 4585,

Ph : 033 - 4006 8556

Fax : 033- 2280 8557.

COIMBATORE

207, 3rd Floor, Tulsi Complex,

1334 Thadagam Road, RS Puram,

Coimbatore - 641 002,

Tamil Nadu,

Ph : +91 422 4367 309.

SILIGURI

Himadri Bhawan Opp.

Gurudwara, Sevoke Road

Siliguri - 734401

West Bengal,

Ph : 0353 -2430 273.

Contact us

All information contained herein is obtained by ICRA Online Limited (“ICRON”) from sources believed by it to be accurate and reliable.

Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS”

without warranty of any kind. ICRON adopts all necessary measures so that the information it uses is of sufficient quality and from sources

ICRON considers to be reliable including, when appropriate, independent third-party sources. However, ICRON is not an auditor and cannot

in every instance independently verify or validate information received in preparing this document.

All information contained herein must be construed solely as statements of opinion, and ICRA Online Limited or its affiliates or group

companies and its respective and any of its officers, directors, personnel and employees, disclaim liability to any loss, damage of any nature,

including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the

use of this document or its contents in any manner or for any contingency within or beyond the control of, ICRON or any of its directors,

officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the

use of or inability to use any such information. Opinions expressed in the document are not the opinions of our holding company, ICRA Limited

(ICRA), and should not be construed as any indication of credit rating or grading of ICRA for any instruments that have been issued or are to

be issued by any entity. The recipient alone shall be fully responsible and/or are liable for any decision taken on the basis of this document

and/or the information contained herein.

Readers are requested to click here for ICRON disclaimer - http://www.icraonline.com/legal/standard-disclaimer.html

Disclaimer