investors presentation bpifrance financement, bond issuer · investors presentation bpifrance...

TRANSCRIPT

Investors Presentation Bpifrance Financement, Bond Issuer May 2014

Formerly

* Serving the Future

*

2013 Figures

Appendices

16/05/2014

2 Titre de la présentation

05.

Bpifrance Financement, Financials & Risk Management 04.

Bpifrance Financement, Key Facts & Figures

03. Bpifrance Financement, Funding Strategy

02.

Overview of Bpifrance 01.

01.

3

Overview of Bpifrance

16/05/2014

4 Titre de la présentation

EPIC

BPI-Groupe¹

BPI-Groupe SA²

50 % 50 %

Bpifrance

Participations Bpifrance

Financement³

(formerly OSEO SA)

100 %

Other (private

commercial

banks)

90 % 100 %

10 %

Direct

guarantee

on bond

issues

100 %

Bpifrance

Investissement

Asset

Management 100%

Bpifrance was created on July 12th, 2013

• Strongest possible ownership in

France

• EPIC BPI-Groupe and CDC

ratings considered by Moody’s as

aligned with those of French

Government (Aa1 (negative)/P1)

(AA+/F1+, Stable Outlook) Fitch

• 21 bn€ equity capital for BPI-

Groupe SA

• Full banking regulation (Basel III)

• Strict compartmentalization of

financial resources (statutory for

Bpifrance Financement)

¹ EPIC OSEO renamed EPIC BPI-Groupe, ² BPI-Groupe to be renamed Bpifrance SA, ³OSEO SA renamed Bpifrance Financement

16/05/2014

5 Titre de la présentation

Bpifrance : Legal Framework & Governance

● Act 2012-1559 (31 December 2012)

● Changes the name of EPIC OSEO to EPIC BPI-Groupe

● Defines the governance of BPI-Groupe SA (to be renamed Bpifrance SA)

● Describes how Bpifrance SA is Bpifrance Financement’s majority shareholder (90%)

● Confers legal continuity to all of Bpifrance Financement’s (ex-OSEO SA) debt bonds and

undertakings and those of its affiliates

● EPIC BPI-Groupe is under the supervision of both the Ministry for the

Economy, Industry and Employment, and the Ministry for Higher

Education and Research. The six members of the EPIC Board are

appointed by the State.

● Bpifrance Financement (ex-OSEO SA) and BPI-Groupe SA are :

● Under the permanent control of a Government Commissioner (with the power to veto some of

the Board of Directors’ decisions)

● Duly supervised by the French Banking Authority (ACPR) and the Financial Markets Authority

(AMF)

16/05/2014

6 Titre de la présentation

Permanence of BPI-Groupe’s Legal Status As A Public Institution

EPIC STATUS Applicable to BPI-Groupe

Set up by a specific Law or Decree

- Law required for the creation of a new category of EPIC

- Decree for an EPIC belonging to an existing category

The missions and organization of the EPIC BPI-Groupe are defined

under Act 2005-722 dated 29 June 2005, as amended and ratified, and

which refer to (i) the creation of the EPIC and (ii) the transformation of

the National Agency for Research Promotion (ANVAR) from a public

corporation into a limited company. This Act, together with Act 2013-

529 of 21 June 2013 and Act 2012-1559 of 31 December 2012, confirm

the creation of France’s Public Investment Bank (BPI).

General interest missions defined by law

- With a specific purpose (specialty principle)

- With some public law prerogatives

- To promote and support innovation, particularly technological, and to

contribute to technology transfer;

- To promote the development and financing of small and medium-sized

companies.

Control by public authorities

- Members of the Board of Directors appointed in whole or in part by

public authorities

- Supervision by public authorities

- Control of accounts made by the “Court of Auditors” (“Cour des

Comptes”)

- The 6 members of BPI-Groupe’s Board of Directors are appointed by

the State

- The Government Commissioner has the power to veto some decisions

of the Board of Directors

- The EPIC BPI-Groupe is under the supervision of both the Ministry for

the Economy, Industry and Employment, and the Ministry for Higher

Education and Research.

Implicit but automatic guarantee of the State

- No recovery or judicial liquidation proceedings for an EPIC

- If an EPIC is unable to comply with its obligations, the State is legally

bound to fulfill them

- BPI-Groupe is one of the rare EPICs to be classified as a central

government body or ODAC (Organisme Divers d’Administration

Centrale) like an EPA (Etablissement Public d’Administration), which

means that its debt is consolidated with that of the State (under

Maastricht’s Rules).

- Bpifrance Financement SA benefits, as a subsidiary, from an explicit

guarantee from EPIC BPI-Groupe for its bond issues. And, likewise,

BPI-Groupe benefits from an implicit guarantee from the State.

Transformation and dissolution only possible by law (Act or

Decree)

The June 2005 Act was amended in 2010 and 2012 to stipulate the

missions and governance of Bpifrance, and to give specific

empowerment to State representatives being members of the Board.

16/05/2014

7 Titre de la présentation

Moody’s : Aa1 (Negative) / P1

Moody’s rationale:

EPIC BPI-Groupe (ex-EPIC OSEO) is intrinsically linked to the

French Government

• High level of government involvement in its business plan

and budget

• Essential role in the development and implementation of

government policies favoring companies

• Public establishment with specific legal status

EPIC BPI-Groupe is not subject to liquidation laws thanks to

its legal status of EPIC

Given Bpifrance’s (ex-OSEO) important role in government

policy concerning SMEs, the French State would timely

extend its support, in case of stress at Bpifrance

Financement

Moody’s rationale on Bpifrance Financement (ex-OSEO) EMTN Program

* Now renamed EPIC BPI-Groupe

“From a credit-risk profile perspective, Moody’s considers CDC and

OSEO* to be intrinsically tied to the French State through their

operational and financial ties with the government. As such, CDC’s

deposit and senior debt ratings and OSEO’s issuer rating derive

from the application of a credit-substitution approach, whereby

their ratings are aligned with those of the French government.

Fitch’s rationale:

EPIC BPI-Groupe is strongly supported by the French government

- Its missions are defined by the French government

- Benefits from a strong administrative, legal and financial oversight

- Strong probability of support from the French State, given its legal

status

EPIC BPI-Groupe’s asset and liabilities cannot be liquidated or

transferred to entities other than the French State thanks to its

legal status

Bpifrance is a strategic tool for French economic policy

Fitch’s rationale on Bpifrance Financement (ex-OSEO) EMTN Program

Fitch : AA+ (Stable) / F1+

“The ratings are aligned with those of the French State due to

expected very strong support in case of need, strong oversight from

the state government and its strategic role in government policy

concerning SMEs”.

“The bonds issued under these programs benefit from an

unconditional and irrevocable first-call guarantee from EPIC BPI-

Groupe”.

EPIC BPI-Groupe Ratings

“The rating reflects the unconditional and irrevocable guarantee

from EPICBPI-Groupe (Aa1, negative/Prime-1) for full and timely

payments under this Program.”

16/05/2014

8 Titre de la présentation

Progression of Aggregated Balance Sheets of 10.45% (+5.1 bn€) (Figures audited but not yet approved by the general shareholders meeting)

Assets (bn€) Liabilities (bn€)

53.9

2,8

10.7

48.8

21.3

5.7

48.8

3.7

3

53.9

4.4

3,2

21.1

+20,6%

-6%

+20%

+180%

+0,9%

+16.3%

+28%

+6,7%

2013 / 2012 2013 / 2012

4.9

2.8

-6,7%

18,9%

Note**: Includes repo operations of securities portfolios and uncalled capital.

1 2,8

10 10,7

14 14

2 2,4

5 4,7

16

19,3

2012 2013

Cash Other Assets**

Equity Participations Innovation

Guarantee Financing

+20%

+180%

+7%

3,7 4,4

3 2,8

3,0 3,2

12,9

16,5

4,9

5,7

21,1

21,3

2012 2013

Cash Other Assets**

Equity Participations Innovation

Guarantee Financing

Other liabilities

FGI/FGA

ST/Financial

Provisions

MLT Financial Res.

Equity

16/05/2014

9 Titre de la présentation

Prudential Ratios

Bpifrance Consolidated

17,6

18,4

14,0

37,6% Solvency Ratio

Tier 1 Ratio 33,7%

2012

31,38%

29,12%

2013

Note: Credit risk encompasses all outstanding operations relating to financing, guarantee and innovation projects

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

35,00%

40,00%

2012 2013

TIER 1

Ratio desolvabilité

16/05/2014

10 Titre de la présentation

General Framework of Our Bond Issues

Issuer: Bpifrance Financement

Guarantor: BPI-Groupe EPIC

Bloomberg ticker OSEOFI + Gouv (F2)

Status: Senior Unsecured

Rating: Aa1 (negative) by Moody’s and AA+ (stable) by Fitch

Guarantee: Irrevocable, first-demand, unconditional and

autonomous

Maturity: TBC

Amount: Benchmark size

Risk Weighting: 20%, level 2A liquid asset under LCRV2

Permanent dealers: HSBC (Arranger), BNP Paribas, Crédit Agricole CIB,

Natixis

Legal Framework: French Law

Listing: Paris

02. Bpifrance Financement (Bond Issuer), Key Facts & Figures

11

2.1 Historical Background & Activity

2.2 Financials

2.3 Risk Management

16/05/2014

12 Titre de la présentation

Business Model

● Our aim is to finance and stimulate small & medium businesses’ growth:

● Soft loans for innovation : provide financing and expertise to companies with

innovative, technology-based, business-focused projects.

● Guarantees : risk-sharing in support of bank financing and private equity investments.

● Co-financing loans : partnership with commercial banks and financial institutions for

business investments and operations.

● An Aa1-rated bond and CD issuer:

● Tight links with French government at strategic

and operational levels

● 90% held by public establishment EPIC BPI-

Groupe (formerly EPIC OSEO) and Caisse

des Dépôts et Consignations (CDC)

● Bonds guaranteed by EPIC BPI-Groupe

● Conservative risk management

● A bank driven by solvability

and liquidity:

● Resilient financial performance

Banks Entrepreneurs

More than 90,000

companies financed

in 2013

1 972 employees

42 local agencies

Partnerships with all banks

in the business market

financement

16/05/2014

13 Titre de la présentation

An Ongoing Process of Rationalization and Investment by the

French State

€850m

Reserve

Guarantee

Fund(1)

€438 m

(Merger)

€120 m

(CEPME/

SOFARIS)

€300 m

(Crisis)

€100 m

(BDPME)

€150 m

(OSEO)

1980 1992-

1994 1996 2005 2009 2010

€539 m(2)

(OSEO industrie)

2012

(1) : The reserve guarantee fund is a buffer created to protect shareholders equity from the risks taken on the guarantee line of business.

(2) : Of which €365m from the French State

2013

€766 m

Bpifrance

● Equity Contributions

● Ex-ante provisioning against loans to customers on a statistical

basis: €533m as of 31 December 2013

● Written in diminution of results (with Board’s approval)

● In accordance with internal guidelines and adjusted on a yearly basis

14

The mission of Bpifrance Financement is to finance and stimulate French SMEs’ growth and innovation

Loans

Pari-passu with banks

+ Specific unsecured loans1

Soft Loans2

Subsidies

Loans

Innovation Guarantee

Risk sharing

Up to 70%

Risk Sharing & Partnership with Commercial Banks

Public Allocations

1. With public guarantee backing

2. Redeemable in case of success

3. Investment co-financing: €3.7 bn and Development loans: €1,3 bn

~33,9006

SMEs financed

Bpifrance

€5.0 bn3 loans

4,0€ bn ST financing4 Banks

Bpifrance

€3.8 bn risks

~ 60,400

SMEs financed

Banks

> €8 bn loans

Bpifrance

~€750 m5

~3,100

SMEs financed

Co-Financing

4. o.w CICE: €0,8

5. o.w. Innovation Aids: €634 m and Development loans: € 113m

Source: DCG (Bilan du 14/02/2013)

6. Includes PCE, CICE, short -term financing

2,9 3,3 3,7

1,1 1,3

1,4

5,1

6,5

7,6

2,0

2,7

3,6

11,1

13,8

16,2

2011 2012 2013

Leasing of real property Equipment Leasing LMT loans Development loans

15

Co-Financing

1. Excluding short-term financing

Activity Outstandings

Investment, co-financing and development loans

Annual Commitments - €m

1 358 1 284

2 128 2 412

1 197 1 264

4 683 4 960

2012 2013

Leasing Long and medium-term loans Development loans

Short-term financing - Annual Authorizations - €m

2 950 3 250

2012 2013

ST CICE

795

2012 2013

Average outstanding1 - €bn

16

Guarantee

Activity Activity

3 377 3 230

182 224 385

3 569 3 839

2012 2013

Classical guarantee Regions guarantee Cash guarantee*

Annual Authorizations - €m

1. Including CICE (€57m in 2013 - The Competitiveness and Employment Tax Credit)

Source : Bpifrance’s Financial Control Department (based on the Board of Director’s meeting of 14 Feb 2014)

10,6 11,2 12

2011 2012 2013

Average outstanding1 - €bn

Innovation

328 295

122 104

109 92

119 75

67

69

745

635

2012 2013

AI FUI ISI Investing in the Future Prog Partners financing

Innovation Aids - Annual Authorizations - €m

Development loans - Annual Commitments - €m

18 19

58

35

18

112

2012 2013Research Tax Credit (CIR) Pre-financing Innovation loans Priming loans

Compounded annual Turnover growth rate

over 3 years after origination year (%)

17

Economic Impact Significant Impact on the Development of Companies financed by Bpifrance

1. Classical guarantee / 2. Innovation Aids / 3. Assuming by convention three years from origination year to end of project.

Source: Bpifrance’s Assessment Department (« Evaluation des actions en financement de Bpifrance 2012 »)

Co-Financing

Guarantee1

Innovation2

5,5 7,2

12,5 10,3

2,5 1,4 1,1 4,0 5,3 6,2 5,2

0,8

-0,1

0,3

2002 2003 2004 2005 2006 2007 2008

2,7 4,1

3,1 3,3

1,5 0,1 0,6 0,0 0,1

0,8 0,9 0,1

-0,8 -0,7

2002 2003 2004 2005 2006 2007 2008

5,6 6,9 7,2 7,6

3,4

0,8

3,2 4,0

5,4 6,1 6,0

0,8 0,3 1,5

2002 2003 2004 2005 2006 2007 2008

1,5 2,2 2,1

2,8 2,9

0,5 1,2

-0,1

0,3 0,6 1,0 0,2

-0,8 -0,4

2002 2003 2004 2005 2006 2007 2008

Companies assisted by Bpifrance

Origination

year

Non-assisted comparable companies

6,0 8,8

4,7

-3,3 -0,6

7,8 5,3 6,5

5,0

-4,2 -3,1

7,1

2004 2005 2006 2007 2008 2009

1,6 3,0

2,3

0,6

-0,9

1,8

-0,6

0,6 0,2

-1,9 -2,3

-0,6

2004 2005 2006 2007 2008 2009

Origination

year

End of project

year

+2,7 p.

+1,5 p.

+ x p. Average difference vs. comparable

companies

Compounded annual Employment growth rate

over 3 years after origination (%)

+2,1 p.

+1,8 p.

Compounded annual Turnover growth rate

over 2 years after end of project3 (%)

Compounded annual Employment growth rate

over 2 years after end of project3 (%)

+1,1 p. +2,2 p.

02. Bpifrance Financement (Bond Issuer), Key Facts & Figures

18

2.1 Historical Background & Activity

2.2 Financials

2.3 Risk Management

16/05/2014

19 Titre de la présentation

Bpifrance Financement : Key Financials

(€ million) 2011 2012 2013

Net banking

Income 437 506 481

Operating

charges1 262 290 297

Cost of risk 6

(6bp)

33

(24bp)

40

(25bp)

Operating

profit2 168 183 144

NET INCOME3 120 130 96

December

2012

December

2013

Shareholders equity1 2 665 m€ 2 712 m€

Basel II ratio 15.03% 12,89%

Core tier 1 ratio 10.48 % 9,22%

Equity buffers

- Reserve guarantee fund 888 m€ 875 m€

- Ex-ante provision 465 m€3 533 m€4

Basel III Liquidity

ratios2

- LCR Estimate 534% 575%

- NSFR Estimate 102% 136%

Income Statement Solvability & Liquidity

1 Group share

2 Subject to calculation adjustments

3 Including 98m€ of provision from Innovation and 367m€ from co-financing

4 Including 129m€ of provision from Innovation and 404m€ from co-financing

1 Excl. income taxes

2 Incl. taxes & amortization, before income taxes & minority interests

3 After income taxes and minority interests; before ex-ante provisioning

16/05/2014

20 Titre de la présentation

(€ millions) ASSETS LIABILITIES

Co-Financing

Activity

• Customer Credit: 19,576

• Portfolio of securities3: 6 328

• Fixed assets & Others: 825

26,729

• MLT financial resources: 16,520

• ST financial resources2: 5,673

• Commercial resources: 561

• Equity & Other Liabilities: 3,975

26,729

Guarantee

• Cash & short-term instruments 95

• Portfolio of Securities/Deposits: 4,507

• Allocations to be received: 163

4,765

• Guarantee allocations: 4,765

4,765

Innovation • Liquidity reserve: 457

• Repayable advance: 1,651

2,108

• Intervention allocations: 2,108

2,108

TOTAL 33,602 33,602

1 Sources: Bpifrance’s ALM Committee of 31 December 2013

2 Including REPO on Securities Portfolio

3 95% of French Treasury Bonds (OAT)

Financial sources and uses1 (as of 31 December 2013)

Breakdown by line of business for Bpifrance Financement SA’s individual statements

02. Bpifrance Financement (Bond Issuer), Key Facts & Figures

21

2.1 Historical Background & Activity

2.2 Financials

2.3 Risk Management

16/05/2014

22 Titre de la présentation

Loan Portfolio : Credit Risk Management

*

Economic capital

Losses

Lo

sses F

req

uen

cy

Expected

Loss (EL)

Unexpected

Loss (UL)

Recourse of

State

Prudential model Economic vision

Bpifrance Financement

Commercial

margin

Ex-ante

Prov.

Shareholders

Equity Co

-fin

an

t

FdG FdG – Fair Value Shareholders

Equity

Gu

ara

nte

e

FdG FdG – Fair Value Shareholders

Equity

Inn

ov

ati

on

Financial prudential resources

Bpifrance Financement

The Fair value of guarantee funds

For innovation and guarantee-related activities, the fair value of guarantee funds (the IFRS fair value of such funds) corresponds to the surplus coverage applied beyond the Expected Losses (EL) of such funds. These capital resources, which are not recognized under any regulation, are indeed explicitly subordinated to equity funds.

The collective excess provision of the financing activity (ex-ante provision)

This equity buffer plays the same role for the financing activity as the fair value does for innovation and guarantee-related operations.

Tier 1 (only Common Equity Tier 1)

Industry & Transport

42%

PW & CE 12%

Trade 18%

Tourism & Health 12%

Other 16%

Exposure by Product Exposure by Activity

As at Dec. 2013 As at Dec. 2013

PLMT 44%

CBI-CBE 21%

CBM 9%

Dvlpt loans 6%

FCT 20%

The breakdown of exposures by

product and by sector is diversified

both in terms of exposure and

number of counterparties.

16/05/2014

23 Titre de la présentation

Investment Portfolio : Counterparties Risk Management

2%1%

96%

December 2013 - Ratings

P-1

Aaa

Aa1 - Aa3

A1 - A3

Unlisted

Short-term

P-1 Aaa Aa1 - Aa3 A1 - A3 Unlisted

French govies (OAT) 6 031 127 5 904 6 031 55,7%

AFT 3 726 3 726 0 3 726 34,4%

Other bonds 99 455 239 0 422 371 793 7,3%

Agencies 30 294 7 0 105 226 331 3,05%

Covered bonds legal 70 12 0 0 20 62 81 0,75%

Eurozone banks 103 0 0 92 11 103 0,95%

French banks 39 232 199 72 271 2,50%

Other banks 7 0 0 7 0 7 0,06%

Corporates 0 0,00%

BMTN 92 92 92 0,8%

Certificates of Deposit 187 128 60 187 1,7%

French banks CD's 187 128 60 187 1,73%

TOTAL 187 99 10 304 239 0 4 496 6 335 10 830 100%

Déc 2013

(€ millions)

Breakdown by rating Breakdown by portfolio TOTAL

Long-term Guarantee

fundsFinancing Amount %

16/05/2014

24 Titre de la présentation

Liquidity Risk Management

Liquidity Risk LT Refinancing Requirement

● Bpifrance Financement follows a strict liquidity containment policy by line of business. A funding gap

is monitored for financing activities.

● Nevertheless, the portfolio of guarantee funds is a source of mobilizable liquid assets.

NB : As enforced by its legal status, no cross-financing is possible between Bpifrance Financement and

the equity investment arm of Bpifrance (Bpifrance Participations).

Asset Liability Run-Off

260%

182%

149%

183% 166%

205% 207%

180%

150% 143% 149% 136%

0%

50%

100%

150%

200%

250%

300%

Evolution of Liquidity Ratio

Liquidity ratio to one month Estim. the ratio of permanent resources to 5 years

Limit = 100%

03. Bpifrance Financement (Bond Issuer), Funding Strategy

25

0

0,5

1

1,5

2

2,5

0

5

10

15

20

25

juin-12 déc.-12 juin-13 déc.-13

Crédits aux SNF accordés par OSEO (Ech. gauche)

Part OSEO dans le total des crédits accordés en France (Ech. droite)

Loans Outstandings to NFC &

Bpifrance Financement’s market share

Characteristics of Extended Credits Funding Stategy

FUNDING STRATEGY

€bn %

- Mostly of medium and long term duration

- Fixed or variable rates

- Partnership with commercial banks

- Generally pari-passu with commercial banks

in the co-financing activities

Loans granted to NFC by Bpifrance Financement (left-hand scale)

Bpifrance Financement market share (right-hand scale)

26

0

2 000

4 000

6 000

8 000

10 000

2013 2014 2015 2016 2017 2018

CICE pre-financing

Development loans

Investment co-financing

€m

Activity

- Regular bond market issues

- Public resources for specific missions

- Access to LDD resources to cope with the

lack of deposits

- Diversification with bilateral borrowings

- Liquidity advance to prevent market

disruptions

Banque de France figures 2014, budget figures, 2015 to 2018 Mid-term plan figures, as of Dec. 2013

Funding Strategy

16/05/2014

27 Titre de la présentation

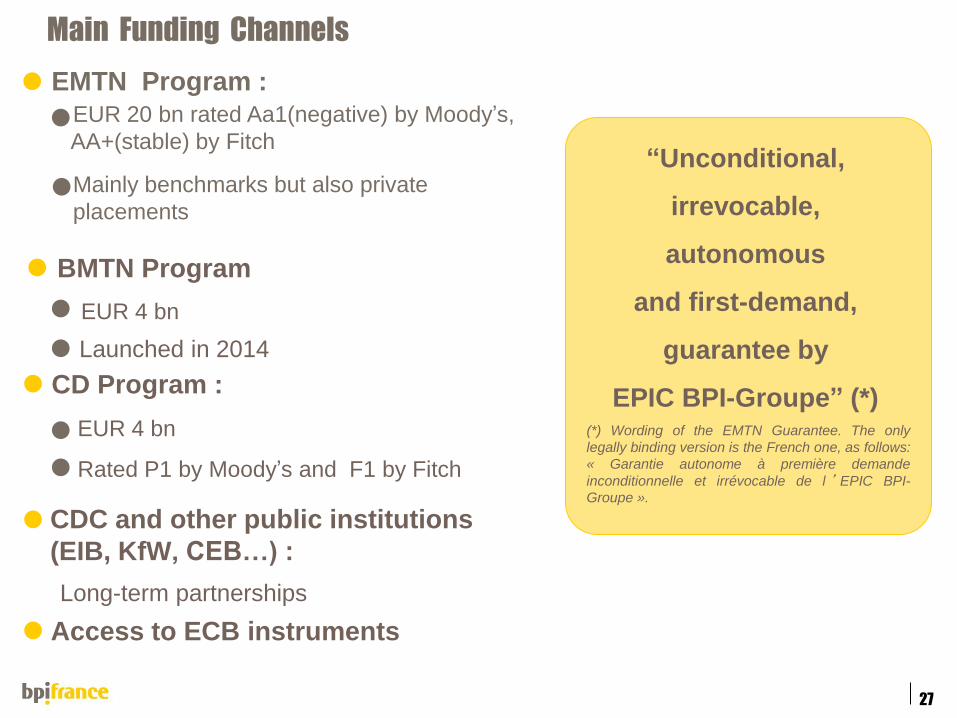

Main Funding Channels

EMTN Program :

EUR 20 bn rated Aa1(negative) by Moody’s,

AA+(stable) by Fitch

Mainly benchmarks but also private

placements

“Unconditional,

irrevocable,

autonomous

and first-demand,

guarantee by

EPIC BPI-Groupe” (*) (*) Wording of the EMTN Guarantee. The only

legally binding version is the French one, as follows:

« Garantie autonome à première demande

inconditionnelle et irrévocable de l ’ EPIC BPI-

Groupe ».

EUR 4 bn

Rated P1 by Moody’s and F1 by Fitch

CD Program :

CDC and other public institutions

(EIB, KfW, CEB…) :

Long-term partnerships

Access to ECB instruments

BMTN Program

EUR 4 bn

Launched in 2014

28

A Long-Term Oriented, Diversified Refinancing Structure

A limited ST refinancing (< 15%, excluding repo)

11%

29%

14%

15%

3%

19%

8%

Equity

Market funding > 1 year

Bilateral loans > 1 year

Savings account deposits loans(LDD) > 1 year

Commercial resources

Repo backed by securities > 1 year

ST refinancing (Deposit certificates& loans < 1 year)

31/12/2013

10%

37%

12%

13%

2%

11%

15%

Expected

31/12/2014

16/05/2014

29 Titre de la présentation

28%

11%

10%

51%

Breakdown by Investor type (EMTN issues)

Asset Manager

Banks

Central Banks

Insurance

16/05/2014

30 Titre de la présentation

Bpifrance Financement’s Bond Issues under the EMTN Program Bond Issues Issues Date

OBL OSEO-SA E3M+10 BP ECH 27/03/2015

Banks 47%

Asset Manager 42%

Banks 5%

Insurance 5%

Asset Manager 1%

OBL BPIFRANCE FINANCEMENT E3M+7 BP ECH 17/09/2015 (pp)

First issue 10/09/2013 500 M€ Private Placement Asset Manager 100%

OBL BPIFRANCE FINANCEMENT E3M+10BP ECH 07/02/2016

First issue 07/02/2014 500M€ Benchmark Banks 63%

Asset Manager 37%

OBL OSEO-SA 2,00% ECH 25/07/2017

Insurance 62%

Asset Manager 33%

Banks 5%

Second issue 05/07/2012 250 M€ Retap Central Banks 100%

Third issue 25/02/2013 200 M€ Private Placement Central Banks 100%

Banks 63%

Asset Manager 32%

Insurance 5%

OBL BPIFRANCE FINANCEMENT1% ECH 25/05/2019

First issue 13/05/2014 500M€ Retap Banks 100%

OBL OSEO-SA 2,375% ECH 25/04/2022

Insurance 78%

Banks 12%

Central Banks 4%

Asset Manager 4%

Asset Manager 2%

OBL OSEO-SA 3,125% ECH 26/09/2023

Insurance 89%

Central Banks 10%

Asset Manager 1%

Second issue 04/11/2011 200 M€ Private Placement Insurance 100%

OBL BPIFF 2,50% ECH 25/05/2024

Asset Manager 38%

Insurance 36%

Central Banks 20%

Banks 6%

OBL OSEO-SA 2,75% ECH 25/10/2025

Insurance 80%

Asset Manager 11%

Banks 7%

Central Banks 2%

Second issue 04/03/2013 300 M€ Private Placement Asset Manager 100%

Third issue 05/03/2013 125 M€ Private Placement Insurance 100%

OBL OSEO-SA 3,625% ECH 25/04/2026 (pp)

First issue 15/02/2012 110 M€ Private Placement Asset Manager 100%

OBL BPIFF 2,917% ECH 25/10/2027 (pp)

First issue 29/10/2013 125 M€ Private Placement Insurance 100%

OBL OSEO-SA E3M+115 BP ECH 27/07/2029 (pp)

First issue 05/07/2012 104 M€ Private Placement Insurance 100%

First issue 06/02/2013 750 M€ Benchmark

First issue 16/09/2011 1 000 M€ Benchmark

First issue 03/12/2013 800 M€ Benchmark

First issue 22/05/2012 900 M€ Benchmark

First issue 05/09/2012 1 250 M€ Benchmark

Fourth issue 13/02/2014 400M€ Retap

Book size Distribution By Investor Type

First issue 20/03/2013 1 000 M€ Benchmark

16/05/2014

31 Titre de la présentation

Contacts

Headquarters

27-31, avenue du Général Leclerc

94 710 Maisons-Alfort Cedex

Website: www.bpifrance.fr

Arnaud CAUDOUX

Chief Financial Officer and Executive Director

Tel: +33 1 41 79 83 07

Jean-Michel ARNOULT

Chief Treasurer, Head of Capital Markets

and Operations Settlement

Tel: +33 1 41 79 89 77

Eric de LA CHAISE

Head of Financial Engineering & Management

Tel: + 33 1 41 79 80 68

Christophe JACQUILLAT

Head of Market Operations

Tel: + 33 1 41 79 87 39

To access financial information directly, please go to:

http://www.bpifrance.fr/bpifrance/espace_investisseurs/

regulated_financial_information

05. Appendices

32

1. Entrepreneur is a French word…

2. Bpifrance Investissement

Government

backing and

financing

Powerful public

infra-structures

French Tech

Welcome Pack for

foreign startup

15M€ funded by the

government to

promote « French

Tech » startups

abroad

€5Bn tax credits for

R&D per year

~€20Bn yearly

invested by Bpifrance

in debt and equity, out

of which >€1Bn in

innovation

~€1Bn yearly invested

by VC funds, out of

which 50% funded by

Bpifrance

200M€ to be invested

by Bpifrance in

accelerators

Successful French entrepreneurs actively

supporting the community

Strong networks of accelerators, incubators

gathered in French Tech hubs

Among the best engineers in the

world, CTOs of the most famous

groups

50% cheaper and more loyal than in

the US

Strong CAC 40

Strong media

coverage of

innovation

A startup-friendly country, land of R&D, talents and investments

Global

players

France

Startup

Republic

Talents

Ecosystem

Money

Public

support

Inter-

national

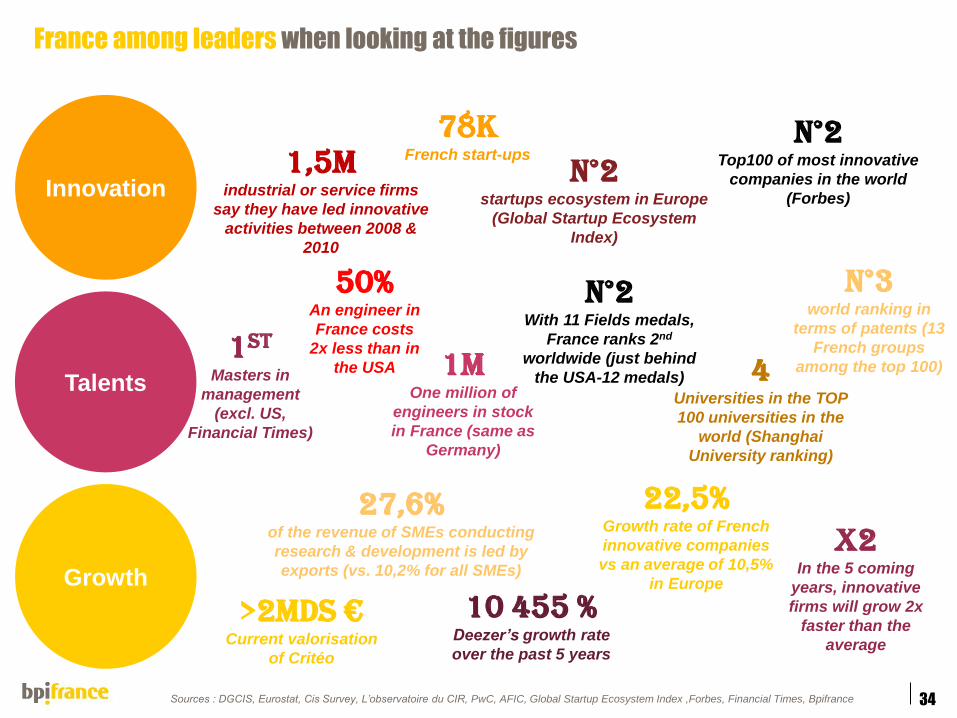

33

1,5M industrial or service firms

say they have led innovative

activities between 2008 &

2010

78K

French start-ups

27,6% of the revenue of SMEs conducting

research & development is led by

exports (vs. 10,2% for all SMEs)

Sources : DGCIS, Eurostat, Cis Survey, L’observatoire du CIR, PwC, AFIC, Global Startup Ecosystem Index ,Forbes, Financial Times, Bpifrance

X2 In the 5 coming

years, innovative

firms will grow 2x

faster than the

average

50% An engineer in

France costs

2x less than in

the USA

>2Mds € Current valorisation

of Critéo

10 455 % Deezer’s growth rate

over the past 5 years

22,5% Growth rate of French

innovative companies

vs an average of 10,5%

in Europe

N°3 world ranking in

terms of patents (13

French groups

among the top 100)

N°2 Top100 of most innovative

companies in the world

(Forbes)

4 Universities in the TOP

100 universities in the

world (Shanghai

University ranking)

1st

Masters in

management

(excl. US,

Financial Times)

France among leaders when looking at the figures

Innovation

Talents

Growth

N°2 startups ecosystem in Europe

(Global Startup Ecosystem

Index)

34

N°2 With 11 Fields medals,

France ranks 2nd

worldwide (just behind

the USA-12 medals) 1M

One million of

engineers in stock

in France (same as

Germany)

One of the most

friendly tax system

for R&D in the

world

France is #2 in

Europe for Venture

Capital

Legal 6-month trial

period allows firms

to fire employees

instantly

English is widely

spoken in France (but we do have an

accent…)

Far away from the clichés…

35

Already many successful serial entrepreneurs, “giving back” to startups

Xavier Niel Founder of Iliad – Free,

Kima Ventures

Marc Simoncini Founder of Meetic, sold to

Match.com

Jacques-Antoine Granjon Founder of Vente-Privée

Founded together :

• “101projets” : 101 startups founded by young entrepreneurs

received a 25k€ investment offer

• EEMI: a school to educate for Internet-specific jobs: web

developpers, web designers and web marketers.

Xavier created 42, a school offering for free a master in

computer science to high-potential and motivated students.

Pierre Kosciusko-Morizet, co-founder of PriceMinister

Jean-David Chamboredon CEO of ISAI

Olivier & Pierre founded PriceMinister, which was later

sold to Rakuten Group for €200M

Pierre founded ISAI with Jean-David, a VC firm

investing in early stage startups

Olivier is a very active business angel in France and

President of France Digitale

Olivier Mathiot co-founder of PriceMinister Cecile Real

Founder of Bioprofile,

Fluotpics, Endodiag

Cecile founded a VC firm

in Med Tech : Medevice

Ludovic Le Moan Founder of

Sigfox and ScoopIt

Ludovic created the TIC

Valley, a cluster of innovative

startups in the south of France

36

2013 – 2014 Highlights

37

France is a Start-up

Republic!

Enters Nasdaq with an initial

valuation of $2 billion

Raises $44M

Won awards at the CES 2014

Raises $137M

Raises $100M Raises $22M

Reaches 1M monthly users

and expends worldwide

Is sold for $600M

to Adobe

Celebrated by Forbes as 4th most

influential innovator for his robots

37

Supported

by

Supported

by

Bpifran e at the heart of the ecosystem

38

Supported

by Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by Supported

by

Supported

by Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Supported

by

Credit and equity from

05. Appendices

39

1. Entrepreneur is a French word…

2. Bpifrance Investissement

16/05/2014

40 Titre de la présentation

Guiding Principles for Equity Investments

Bpifrance Participations & Bpifrance Investissement

▪ Systematic search for joint investments with

private investors (both as a LP and as a GP)

▪ Investment in all sectors except

infrastructure, property and real estate,

banking industry

▪ Focus on :

– Growth sectors, particularly

biotechnology, digital technology and

energetic and ecological transition.

– Build-up operations

▪ From small (SME size) to large caps.

▪ Limited stakes in funds involving company

restructuring processes

▪ Minority Investments

▪ Patient investments (average

horizon of up to 8 - 10 years)

▪ Search for profitable operations

(positive return expected on

Bpifrance’s equity capital)

▪ General-interest criteria

(employment, competitiveness

and innovation) taken into account

in the decision-making process

▪ No stakes in high-leveraged

deals or transactions

Prudent

Investors

General Interest

Long Term

Socially

Responsible

Targeted Sectors and Companies

Systematic Partnership with Private

Investors

41

Overview of the Equity Investments Division

Bpifrance Participations (LP) / Bpifrance Investissement (GP)

Direct Stakes Holdings through Investment Funds

Third-party Asset

Management

Mid-Caps / LC €12 bn*

in direct stakes and via 3

direct funds

SMEs €0,6 bn* via 7 direct funds

Fund of Funds €1,3 bn* via 11 funds and a

pool of « affiliated » funds

€0,6 bn** via 1 fund

Innovation €0,2 bn* via 2 funds

€0,2 bn** managed under the

« Investing in the Future »

Programme via 3 funds

Funds Raised in 2014

Mid-Caps 2020 AEM2, Mode et finance2,

Bois 2, OC+A2, FDEN Averroès Finance III Large Ventures, FBIMR

Equity Investment

*By end of 2013

** Funds size of the Investing in the Future Programme

16/05/2014

42 Titre de la présentation

Disclaimer

This presentation has been prepared and is available on the web site of Bpifrance Financement. This presentation does not constitute an offer or

invitation by or on behalf of Bpifrance Financement to subscribe or purchase any notes issued or to be issued by Bpifrance Financement.

This presentation is not intended to provide any valuation of the financial situation of Bpifrance Financement nor any valuation of the notes issued or

to be issued by Bpifrance Financement and should not be considered as a recommendation to purchase any notes issued or to be issued by

Bpifrance Financement. Any projection, forecast, estimate or other ‘forward-looking’ statement in this document only illustrates hypothetical

performance under specified assumptions of events and/or conditions, which may include (but are not limited to) prepayment expectations, interest

rates, collateral and volatility. Such projections, forecasts, estimates or other ‘forward-looking’ statements are not reliable indicators of future

performance.

Any person having read this presentation shall independently judge of the relevance of the information contained herein; shall make its own

independent assessment of Bpifrance Financement and determine whether to participate in any potential transaction; and shall consult its own

advisors as to legal, tax or other aspects, as deemed necessary. The French “Autorité des Marchés Financiers” granted its visa under number 13-256

dated June 3rd, 2013 with respect to a base prospectus (the “Base Prospectus”). You are invited to report to the Base Prospectus as supplemented

by the supplements to the base prospectus before taking any decision with respect to the implementation of any potential transaction.

This presentation should not be reproduced, distributed or transmitted to any third party nor published in whole or in part, including by e-mail, on the

Internet, intranet or otherwise.

In some countries, the publication of this presentation and the offer or sale of notes issued or to be issued by Bpifrance Financement may be subject

to legal restrictions and/or regulations. In particular, this document and the information contained herein do not constitute an offer of securities for sale

in the United States and are not for publication or distribution, directly or indirectly, in the United States (within the meaning of Regulations under the

United States Securities Act of 1933, as amended, i.e. the “Securities Act”). No offer or sale of securities in the United States or to US persons may

take place, except pursuant to an exemption from the registration requirements of the Securities Act. The Issuer invites those reading this presentation

to inform themselves and comply with such restrictions and/or regulations.