iqe plc · enabling advanced technologies financial dashboard s s s * before exceptional items 112...

TRANSCRIPT

Enabling Advanced Technologies

IQE Plc

H1 2017 Results, September 2017

Drew Nelson, CEOPhil Rasmussen, CFO

Enabling Advanced Technologies

Safe harbour statement

No accountant, lawyer or broker has reviewed this presentation or commented on its merits. No representation or warranty is made by the Company or any of its officers, employees or agents as to the contents of this presentation.

This presentation does not constitute an offer or solicitation of an offer of or invitation by or on behalf of the Company to acquire any shares in the capital of the Company.

This presentation contains forward looking information of a financial and other nature that is speculative and that is based on a variety of assumptions that may or may not be realised. Such information is subject to risks and uncertainties that could cause actual results to differ materially. Such risks and uncertainties include, but are not limited to, those related to the business conditions and financial strengths of the various markets served by the Company, the level of spending by the Company's customers on its products and the ability of the Company to successfully manufacture and market its products. Given these risks and uncertainties, investors and prospective investors should not place any undue reliance on such forward looking information.

This presentation does not purport to be all-inclusive or to contain all the information that an investor or a potential investor in the Company may desire.

Enabling Advanced Technologies

H1 2017 Overview – Positioning for growth

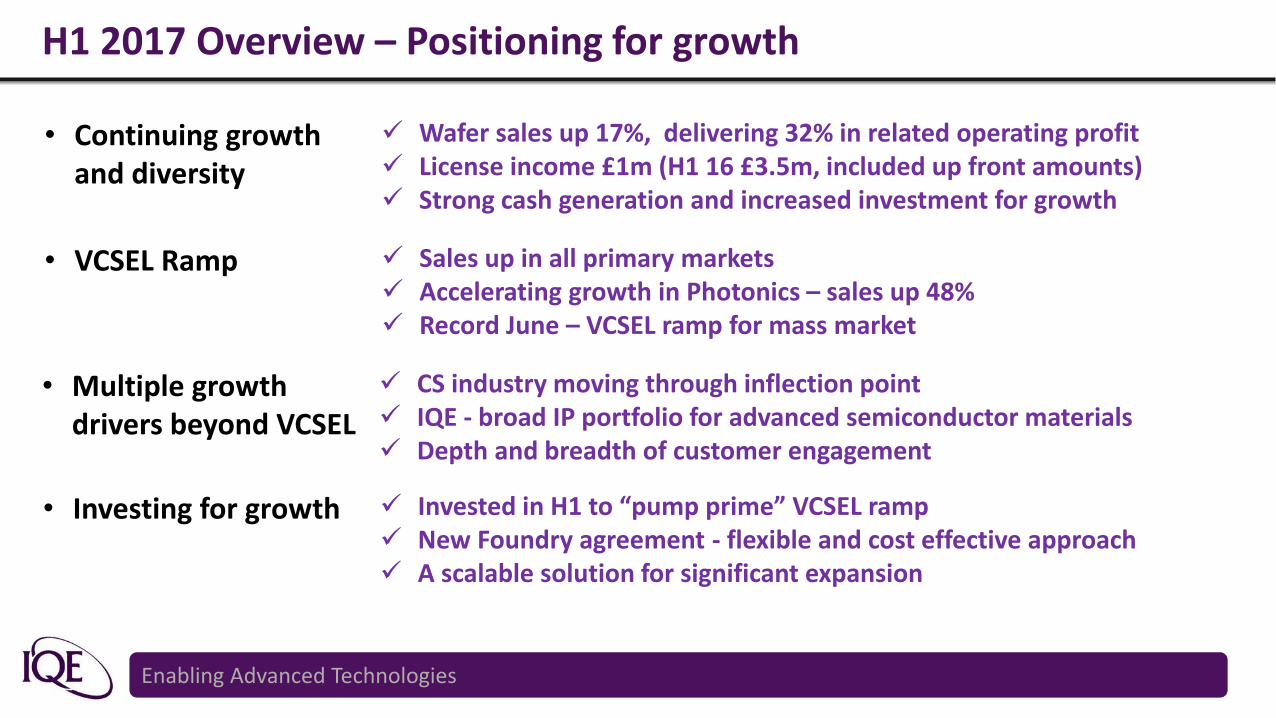

• Continuing growth and diversity

Wafer sales up 17%, delivering 32% in related operating profit License income £1m (H1 16 £3.5m, included up front amounts) Strong cash generation and increased investment for growth

• Investing for growth Invested in H1 to “pump prime” VCSEL ramp New Foundry agreement - flexible and cost effective approach A scalable solution for significant expansion

• Multiple growth drivers beyond VCSEL

CS industry moving through inflection point IQE - broad IP portfolio for advanced semiconductor materials Depth and breadth of customer engagement

• VCSEL Ramp Sales up in all primary markets Accelerating growth in Photonics – sales up 48% Record June – VCSEL ramp for mass market

Enabling Advanced Technologies

H1 2017 Financial Summary

£’million 30 June 2017 30 June 2016 Change

RevenuesWafersLicensing

70.469.4

1.0

63.059.5

3.5

+12%+17%-71%

Operating ProfitWafersLicensing

10.69.61.0

10.87.33.5

-2%+32%-71%

PBT 9.6 10.1 -5%

Fully Diluted EPS (pence) 1.35p 1.46p -8%

Cash Generated from Ops 11.2 12.4 -10%

Capital Investment 15.4 7.6 102%

Leverage 41.9 35.4 18%

Enabling Advanced Technologies

Growth and diversification of revenues

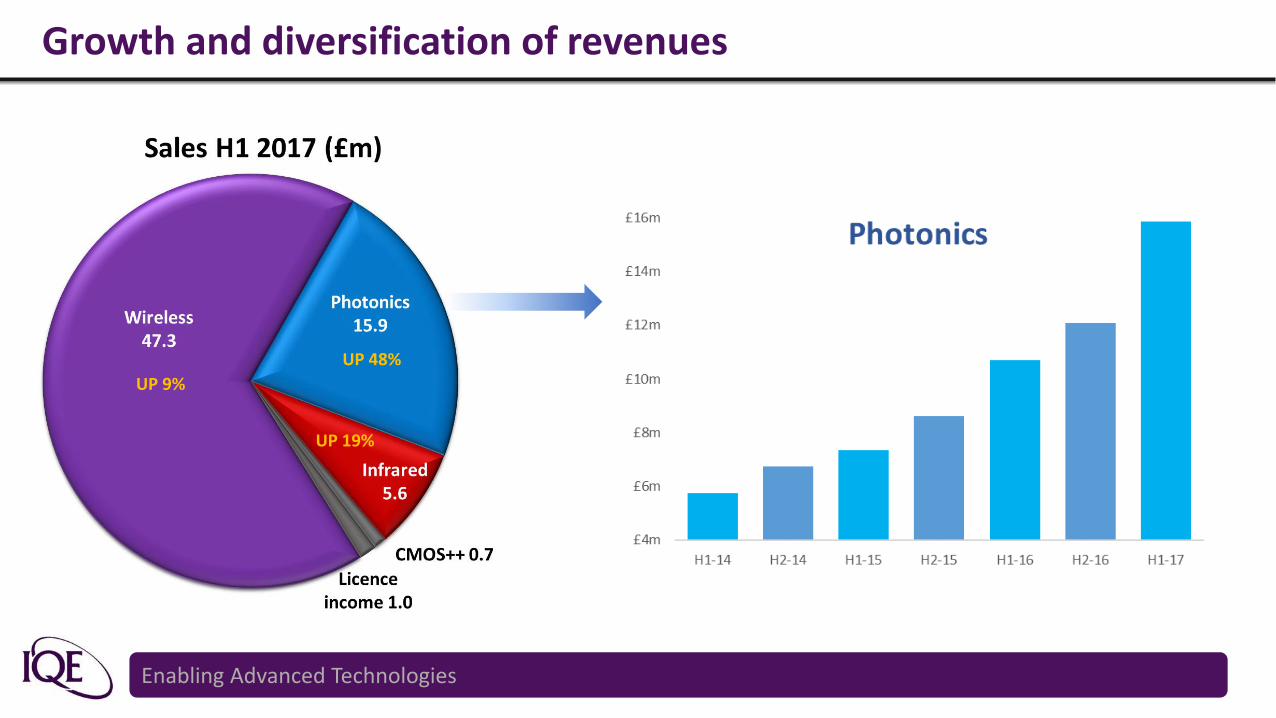

UP 9%

UP 48%

UP 19%

Enabling Advanced Technologies

£'m

Wafers License Total

H1 15

Wafers License Total

H1 16

Wafers License Total

H1 17

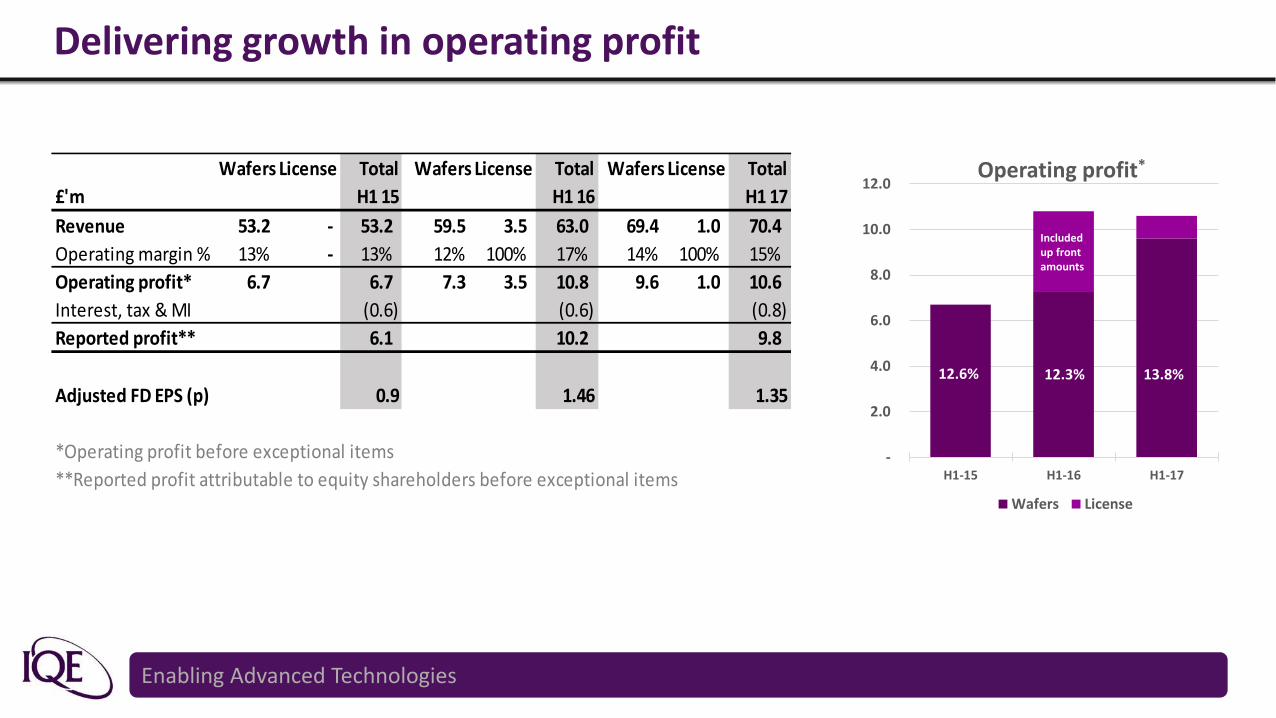

Revenue 53.2 - 53.2 59.5 3.5 63.0 69.4 1.0 70.4

Operating margin % 13% - 13% 12% 100% 17% 14% 100% 15%

Operating profit* 6.7 6.7 7.3 3.5 10.8 9.6 1.0 10.6

Interest, tax & MI (0.6) (0.6) (0.8)

Reported profit** 6.1 10.2 9.8

Adjusted FD EPS (p) 0.9 1.46 1.35

*Operating profit before exceptional items

**Reported profit attributable to equity shareholders before exceptional items

Delivering growth in operating profit

-

2.0

4.0

6.0

8.0

10.0

12.0

H1-15 H1-16 H1-17

Operating profit*

Wafers License

12.6% 12.3% 13.8%

Included up frontamounts

Enabling Advanced Technologies

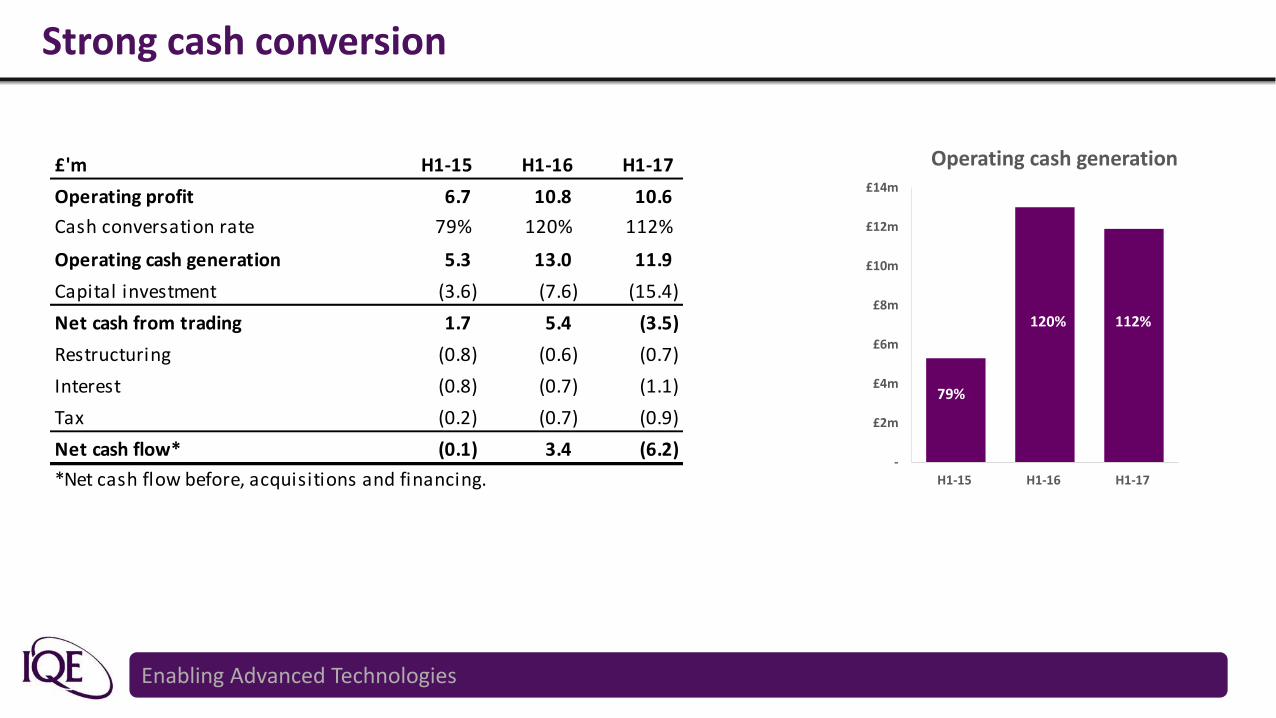

Strong cash conversion

-

£2m

£4m

£6m

£8m

£10m

£12m

£14m

H1-15 H1-16 H1-17

Operating cash generation£'m H1-15 H1-16 H1-17

Operating profit 6.7 10.8 10.6

Cash conversation rate 79% 120% 112%

Operating cash generation 5.3 13.0 11.9

Capital investment (3.6) (7.6) (15.4)

Net cash from trading 1.7 5.4 (3.5)

Restructuring (0.8) (0.6) (0.7)

Interest (0.8) (0.7) (1.1)

Tax (0.2) (0.7) (0.9)

Net cash flow* (0.1) 3.4 (6.2)

*Net cash flow before, acquisitions and financing.

79%

120% 112%

Enabling Advanced Technologies

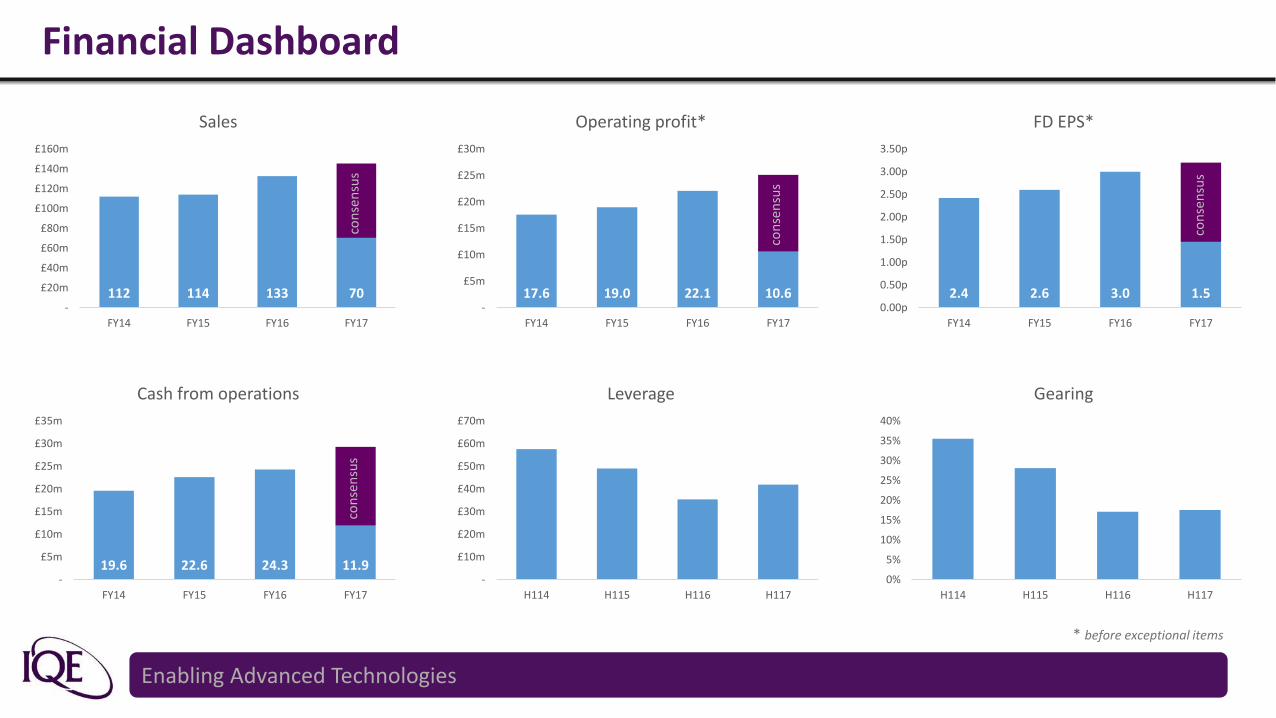

Financial Dashboard

con

sen

sus

con

sen

sus

con

sen

sus

con

sen

sus

* before exceptional items

112 114 133 70

0 0

0

-

£20m

£40m

£60m

£80m

£100m

£120m

£140m

£160m

FY14 FY15 FY16 FY17

Sales

17.6 19.0 22.1 10.6

00

0

-

£5m

£10m

£15m

£20m

£25m

£30m

FY14 FY15 FY16 FY17

Operating profit*

2.4 2.6 3.0 1.5

00

0

0.00p

0.50p

1.00p

1.50p

2.00p

2.50p

3.00p

3.50p

FY14 FY15 FY16 FY17

FD EPS*

19.6 22.6 24.3 11.9

0

-

£5m

£10m

£15m

£20m

£25m

£30m

£35m

FY14 FY15 FY16 FY17

Cash from operations

-

£10m

£20m

£30m

£40m

£50m

£60m

£70m

H114 H115 H116 H117

Leverage

0%

5%

10%

15%

20%

25%

30%

35%

40%

H114 H115 H116 H117

Gearing

con

sen

sus

con

sen

sus

con

sen

sus

con

sen

sus

Enabling Advanced Technologies

An Intro to Semiconductor Technology …

Enabling Advanced Technologies

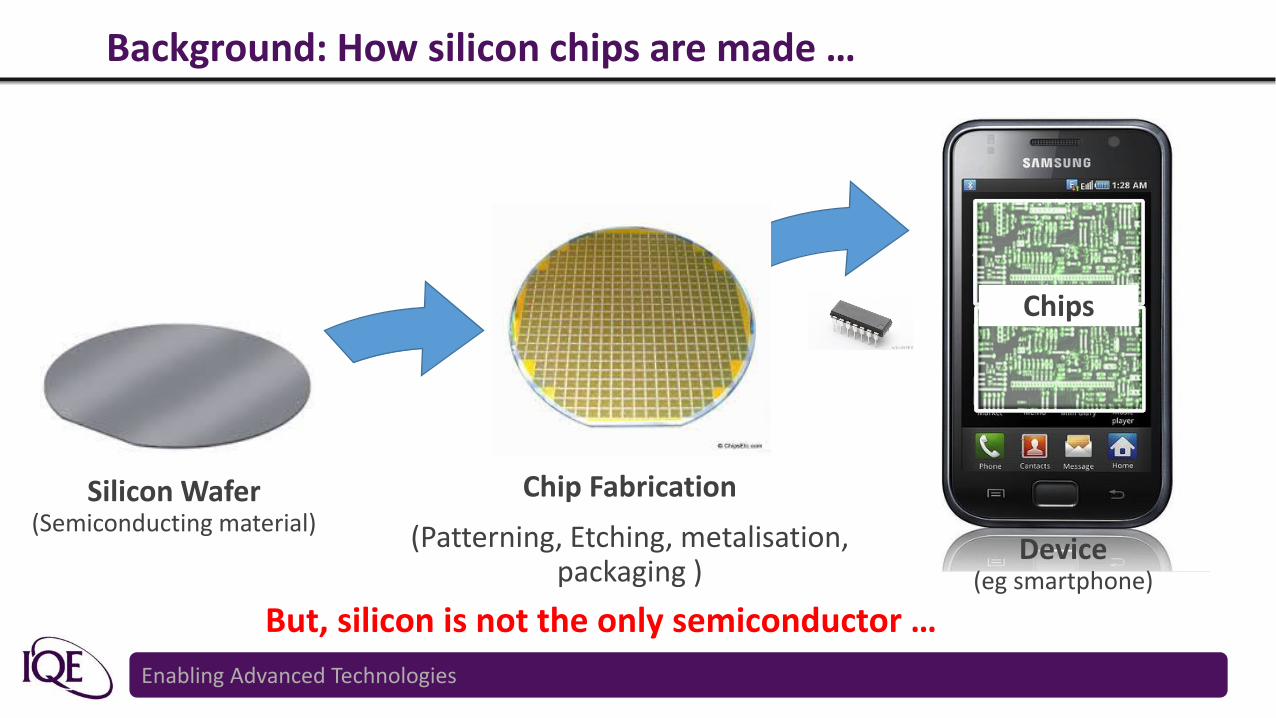

Background: How silicon chips are made …

Silicon Wafer(Semiconducting material)

Chip Fabrication

(Patterning, Etching, metalisation, packaging )

Device(eg smartphone)

Chips

But, silicon is not the only semiconductor …

Enabling Advanced Technologies

Compound semi chips

Silicon chips

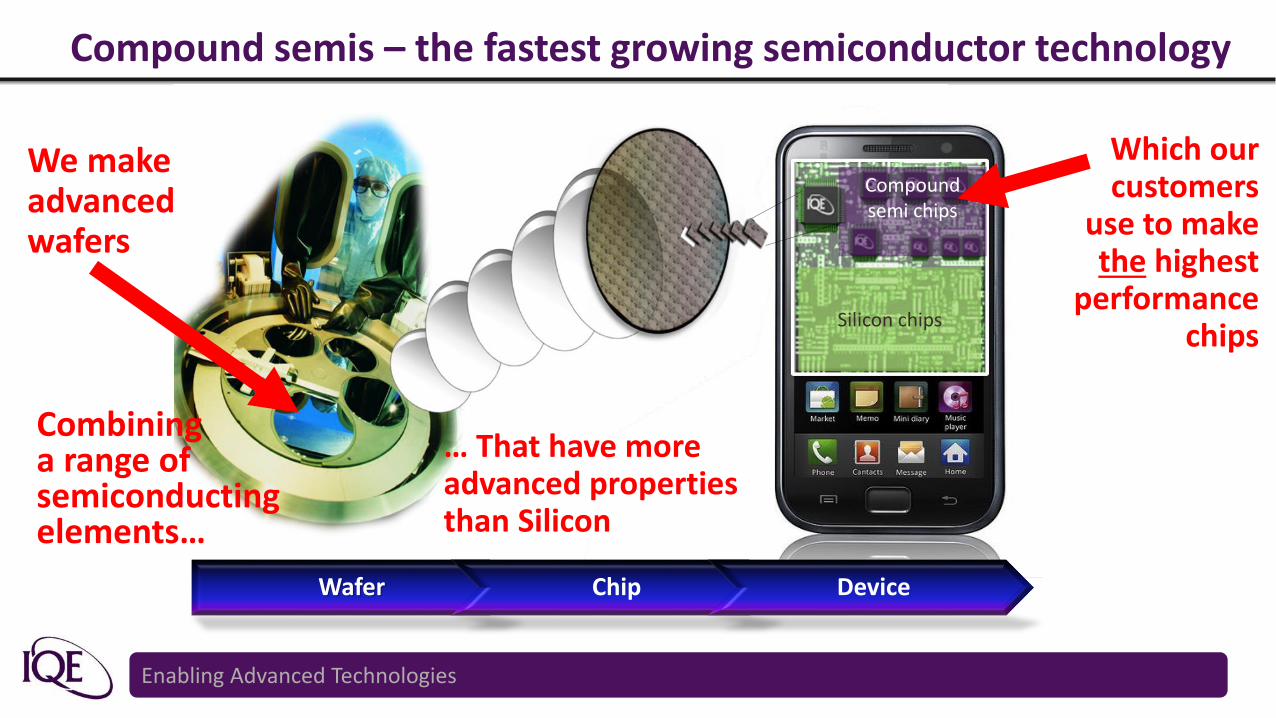

Compound semis – the fastest growing semiconductor technology

Wafer Chip Device

We make advanced wafers

Which our customers

use to make the highest

performance chips

Combining a range of semiconducting elements…

… That have more advanced properties than Silicon

Enabling Advanced Technologies

How we make compound semiconductor wafers …

Epitaxy – engineering advanced materials

• Atomically engineered films (up to >400 individual films)

• Leading edge crystal growth technology

• Bespoke to each application

• Extensive qualification requirements

• Large barriers to entry

Enabling Advanced Technologies

The markets for Compound Semiconductors…

Enabling Advanced Technologies

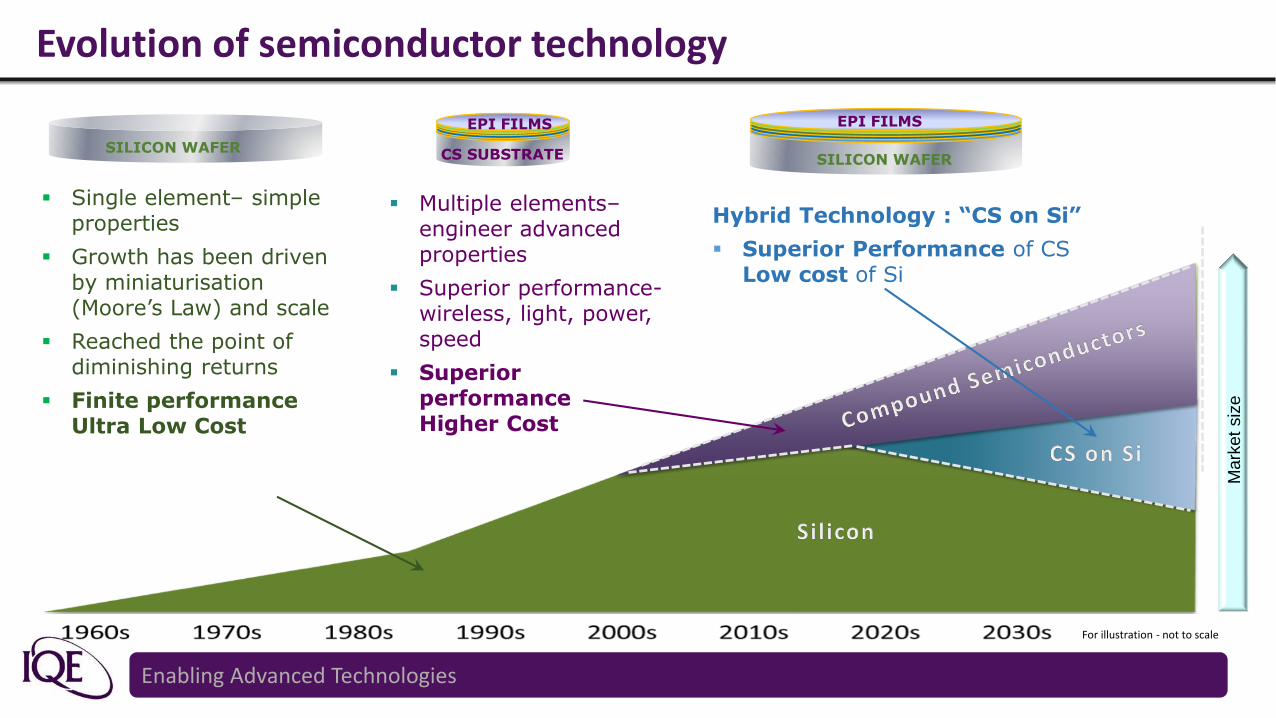

Evolution of semiconductor technology

Internet

Ma

rket

siz

e

For illustration - not to scale

Single element– simple properties

Growth has been driven by miniaturisation (Moore’s Law) and scale

Reached the point of diminishing returns

Finite performance Ultra Low Cost

Multiple elements–engineer advanced properties

Superior performance-wireless, light, power, speed

Superior performanceHigher Cost

Hybrid Technology : “CS on Si”

Superior Performance of CS Low cost of Si

SILICON WAFER CS SUBSTRATE

EPI FILMS

SILICON WAFER

EPI FILMS

Enabling Advanced Technologies

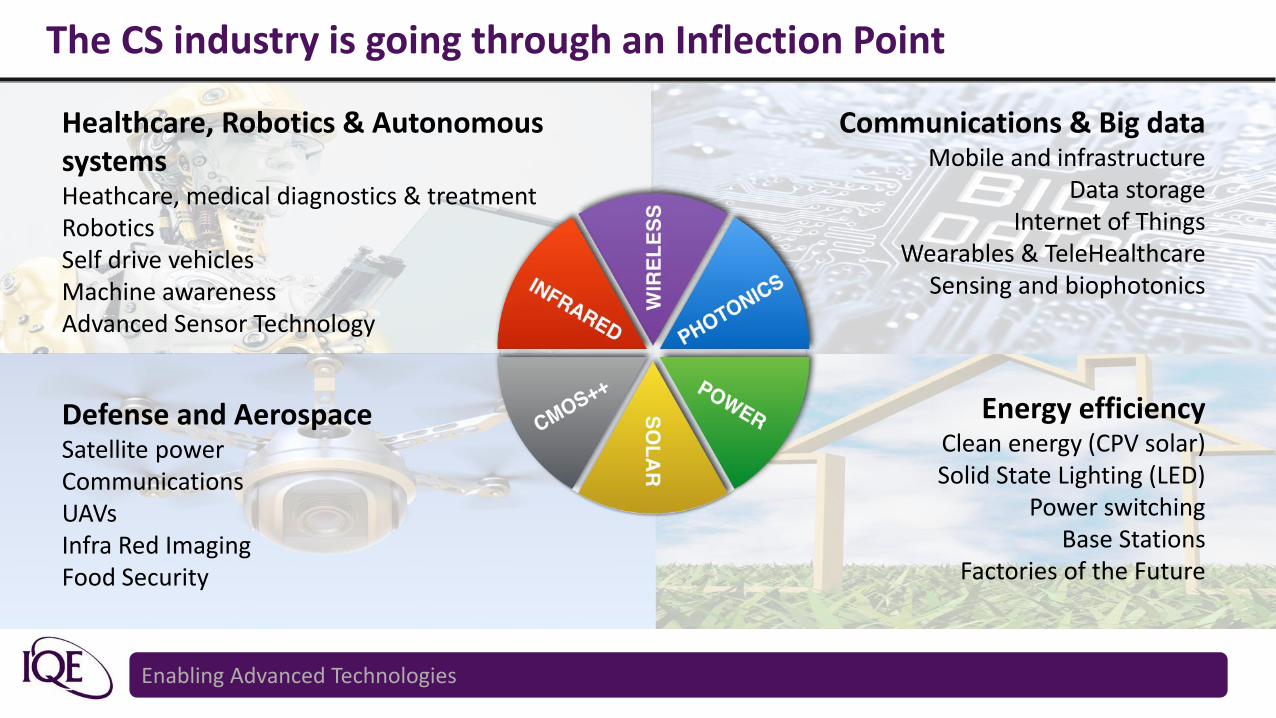

The CS industry is going through an Inflection Point

Healthcare, Robotics & Autonomous systemsHeathcare, medical diagnostics & treatmentRoboticsSelf drive vehiclesMachine awarenessAdvanced Sensor Technology

Communications & Big dataMobile and infrastructure

Data storageInternet of Things

Wearables & TeleHealthcareSensing and biophotonics

Energy efficiencyClean energy (CPV solar)Solid State Lighting (LED)

Power switchingBase Stations

Factories of the Future

Defense and AerospaceSatellite powerCommunicationsUAVsInfra Red ImagingFood Security

Enabling Advanced Technologies

Preparing for inflection

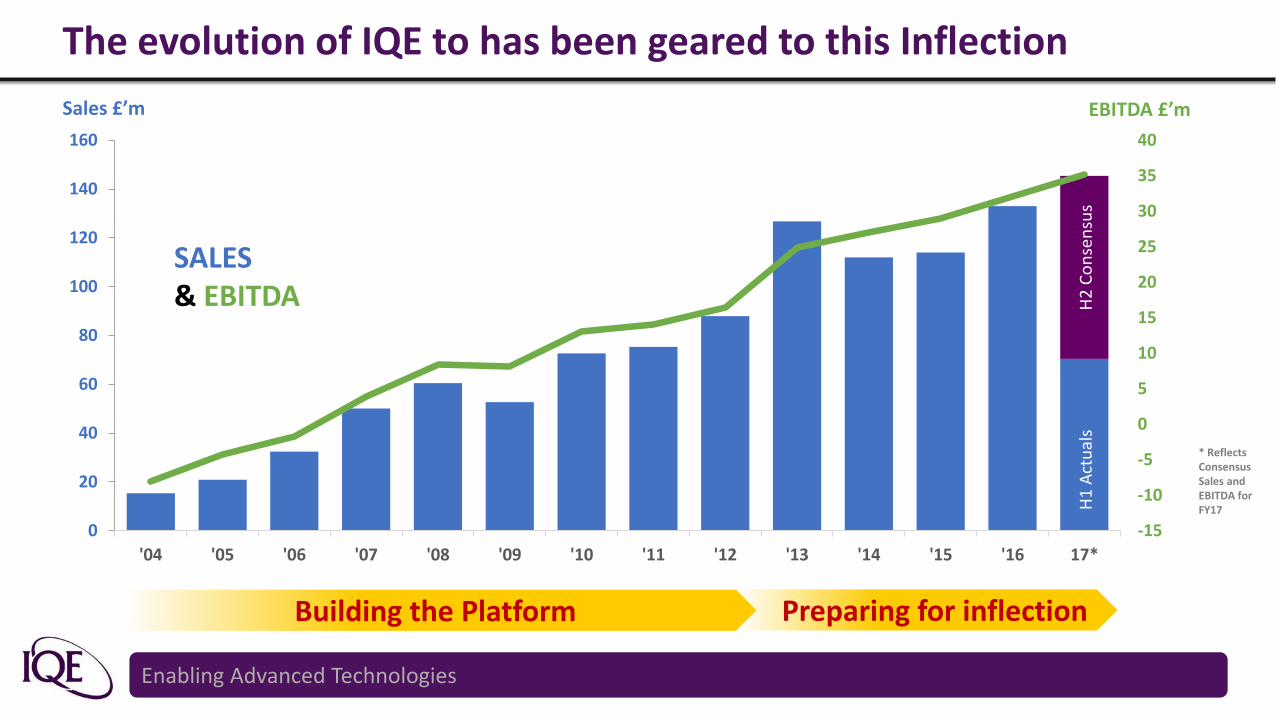

The evolution of IQE to has been geared to this Inflection

Co

nse

nsu

s

-15

-10

-5

0

5

10

15

20

25

30

35

40

0

20

40

60

80

100

120

140

160

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 17*

H2

Co

nse

nsu

s

Sales £’m EBITDA £’m

SALES& EBITDA

* Reflects Consensus Sales and EBITDA for FY17H

1 A

ctu

als

Building the Platform

Enabling Advanced Technologies

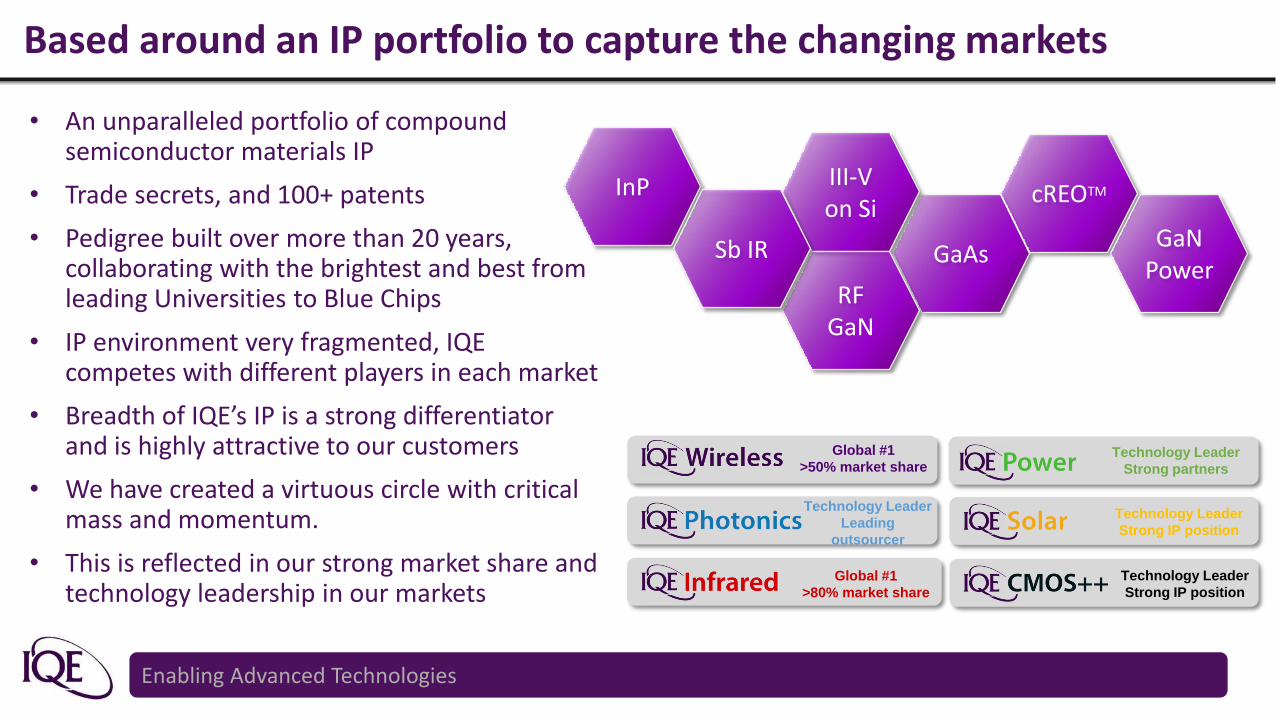

Based around an IP portfolio to capture the changing markets

Global #1

>80% market share

Global #1

>50% market share

Technology Leader

Leading

outsourcer

Technology Leader

Strong IP position

Technology Leader

Strong partners

Technology Leader

Strong IP position

• An unparalleled portfolio of compound semiconductor materials IP

• Trade secrets, and 100+ patents

• Pedigree built over more than 20 years, collaborating with the brightest and best from leading Universities to Blue Chips

• IP environment very fragmented, IQE competes with different players in each market

• Breadth of IQE’s IP is a strong differentiator and is highly attractive to our customers

• We have created a virtuous circle with critical mass and momentum.

• This is reflected in our strong market share and technology leadership in our markets

InP

GaAs

cREOTMIII-V on Si

RF GaN

GaNPower

Sb IR

Enabling Advanced Technologies

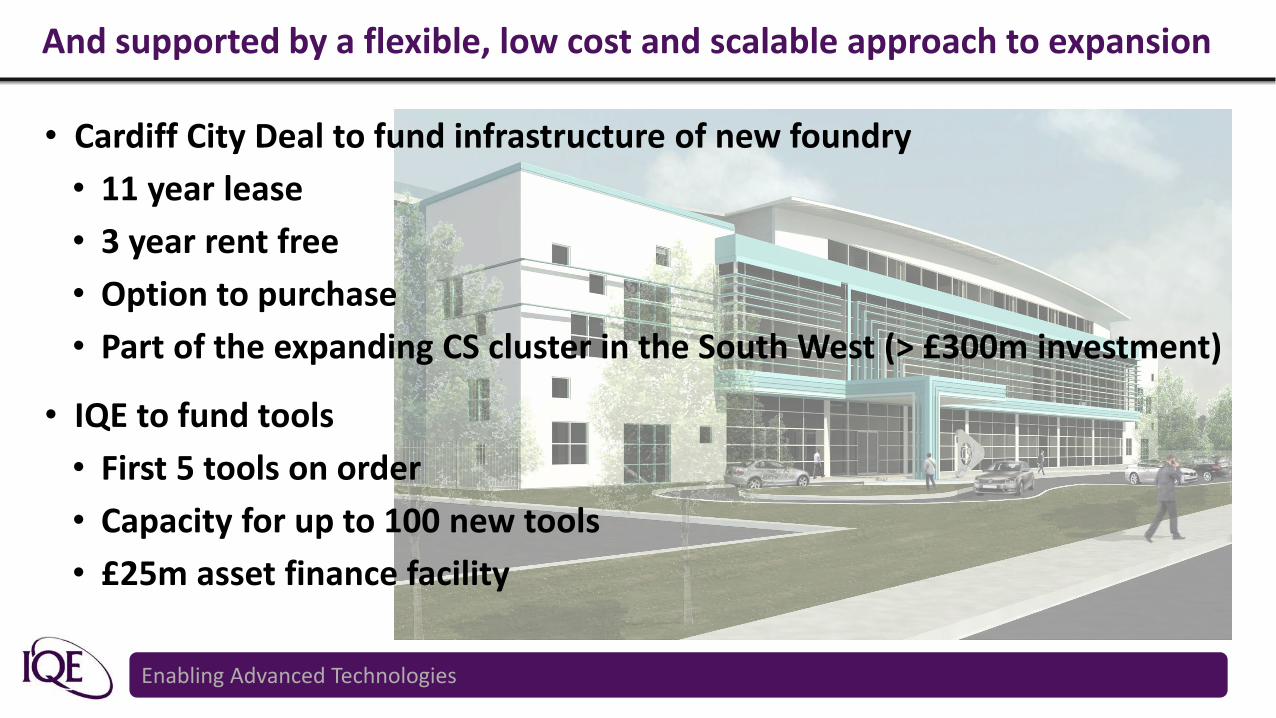

And supported by a flexible, low cost and scalable approach to expansion

• Cardiff City Deal to fund infrastructure of new foundry

• 11 year lease

• 3 year rent free

• Option to purchase

• Part of the expanding CS cluster in the South West (> £300m investment)

• IQE to fund tools

• First 5 tools on order

• Capacity for up to 100 new tools

• £25m asset finance facility

Enabling Advanced Technologies

IQE’s Outlook – its market engagement

Enabling Advanced Technologies

Basecase Outlook : Continuing the trend in growth and diversity

Growth

approx10%

Growth ~ low to

mid single digit

Strong double

digit growth

Enabling Advanced Technologies

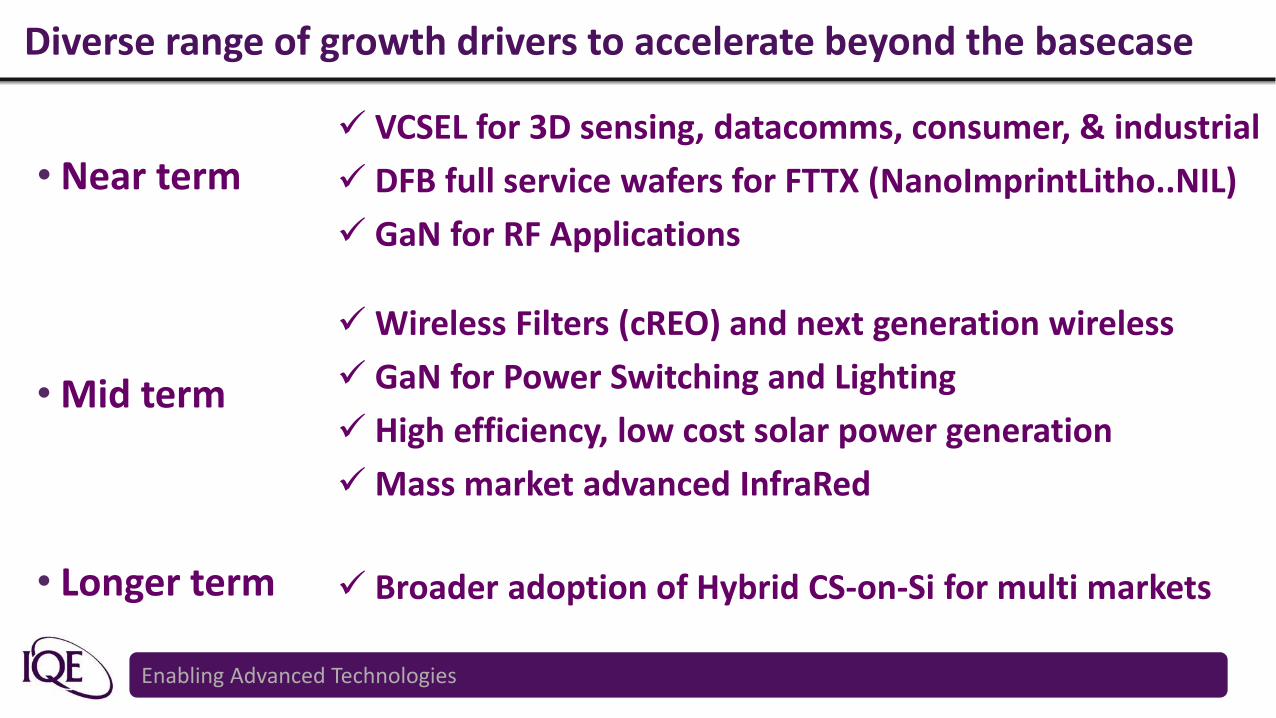

Diverse range of growth drivers to accelerate beyond the basecase

• Near term VCSEL for 3D sensing, datacomms, consumer, & industrial

DFB full service wafers for FTTX (NanoImprintLitho..NIL)

GaN for RF Applications

• Mid term

• Longer term

Wireless Filters (cREO) and next generation wireless

GaN for Power Switching and Lighting

High efficiency, low cost solar power generation

Mass market advanced InfraRed

Broader adoption of Hybrid CS-on-Si for multi markets

Enabling Advanced Technologies

Near Term Drivers to Accelerate Growth

Enabling Advanced Technologies

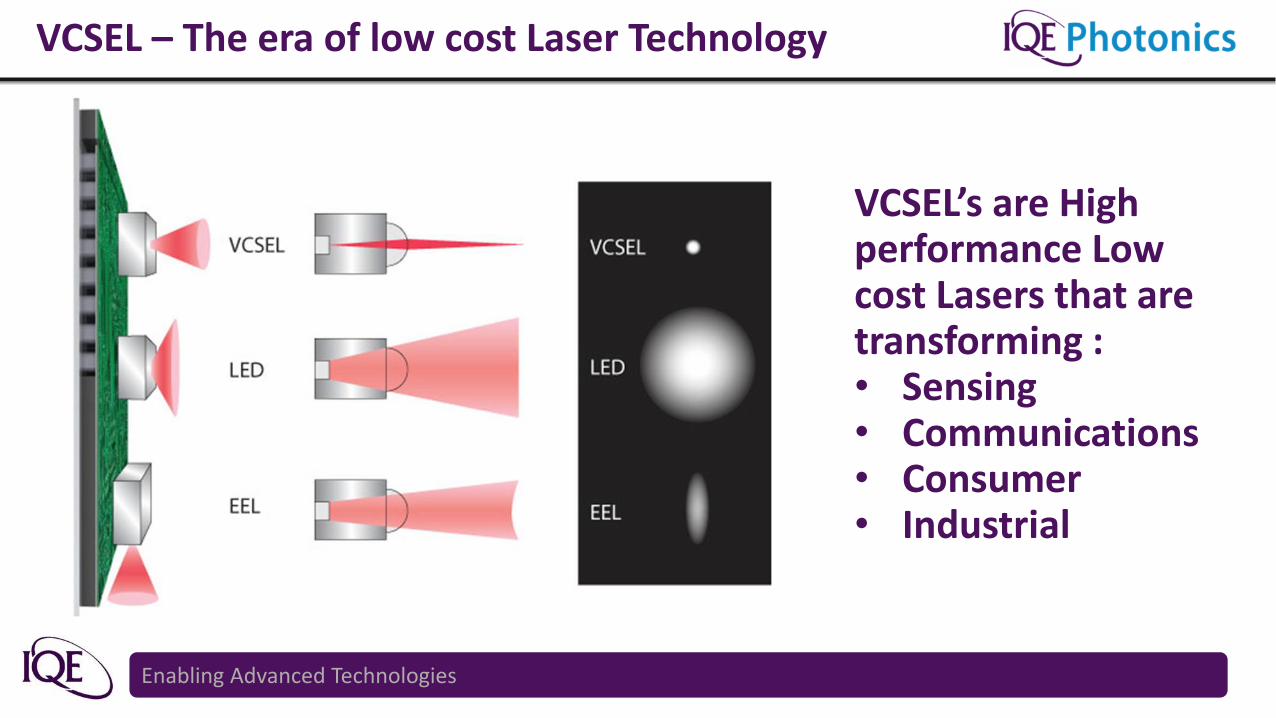

VCSEL – The era of low cost Laser Technology

VCSEL’s are High performance Low cost Lasers that are transforming :• Sensing• Communications• Consumer• Industrial

Enabling Advanced Technologies

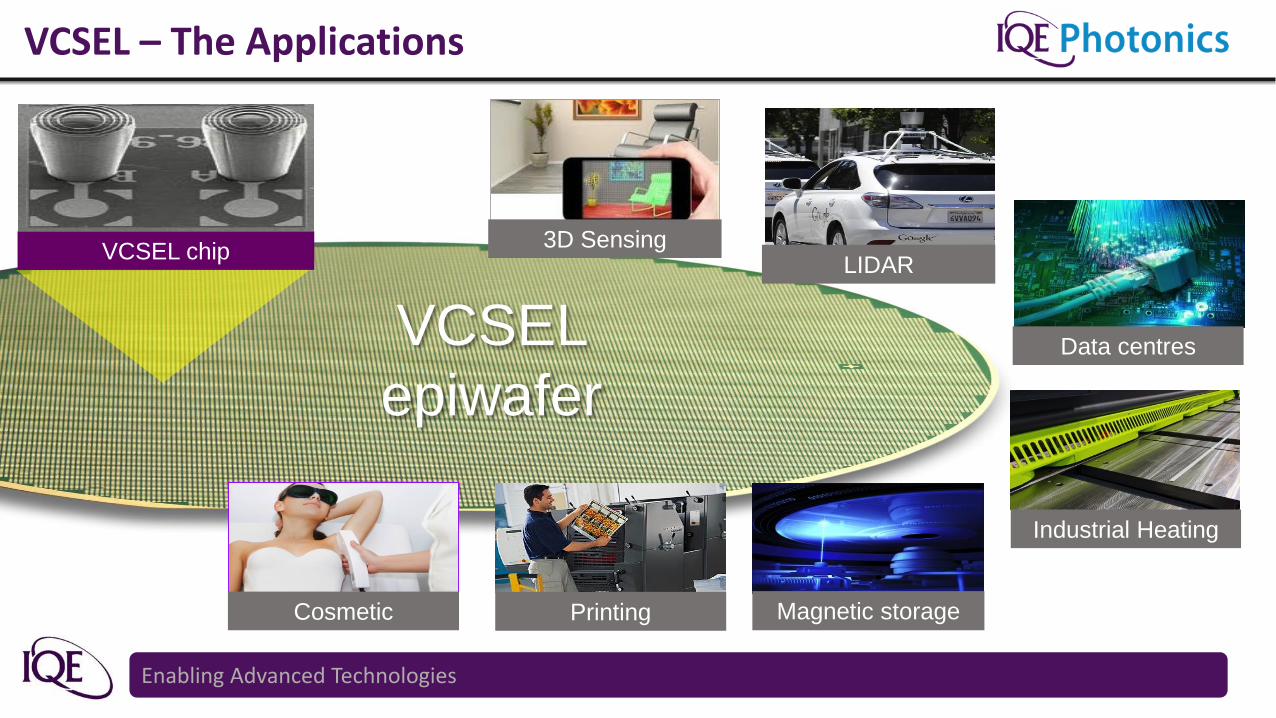

VCSEL

epiwafer

VCSEL chip

Magnetic storagePrinting

Data centres

Cosmetic

3D Sensing

Industrial Heating

VCSEL – The Applications

LIDAR

Enabling Advanced Technologies

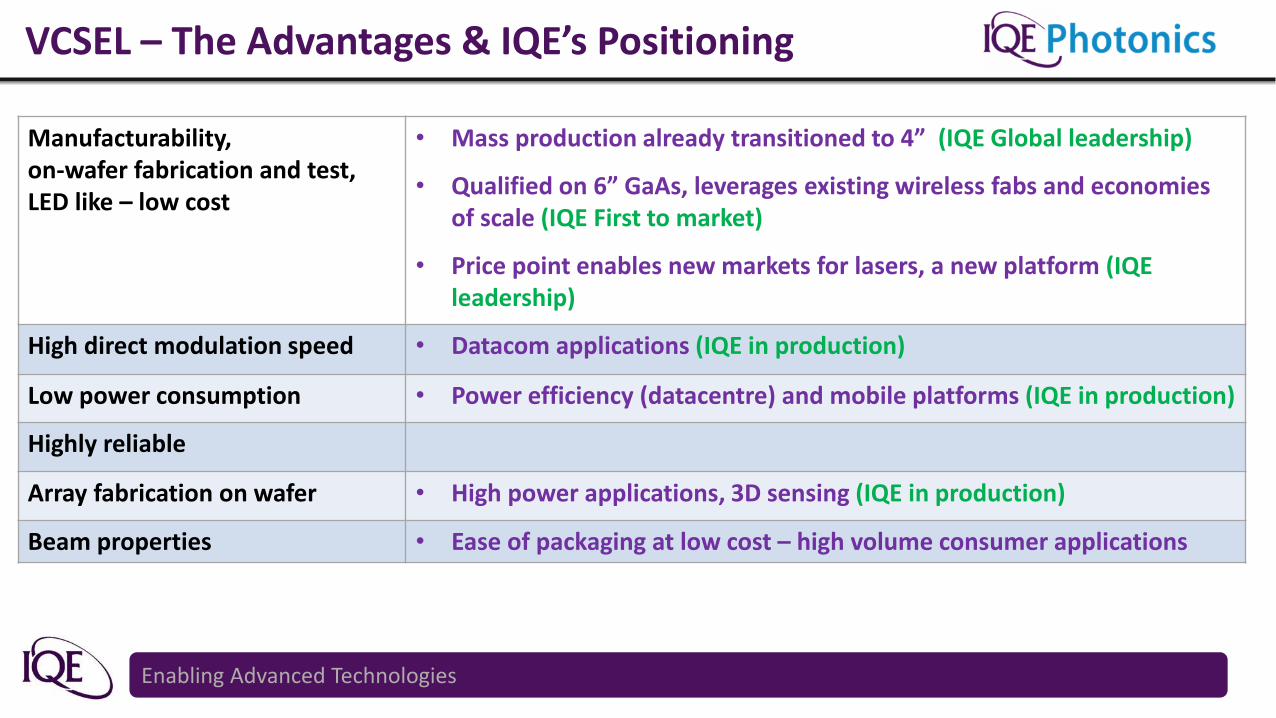

VCSEL – The Advantages & IQE’s Positioning

Manufacturability, on-wafer fabrication and test, LED like – low cost

• Mass production already transitioned to 4” (IQE Global leadership)

• Qualified on 6” GaAs, leverages existing wireless fabs and economies of scale (IQE First to market)

• Price point enables new markets for lasers, a new platform (IQE leadership)

High direct modulation speed • Datacom applications (IQE in production)

Low power consumption • Power efficiency (datacentre) and mobile platforms (IQE in production)

Highly reliable

Array fabrication on wafer • High power applications, 3D sensing (IQE in production)

Beam properties • Ease of packaging at low cost – high volume consumer applications

Enabling Advanced Technologies

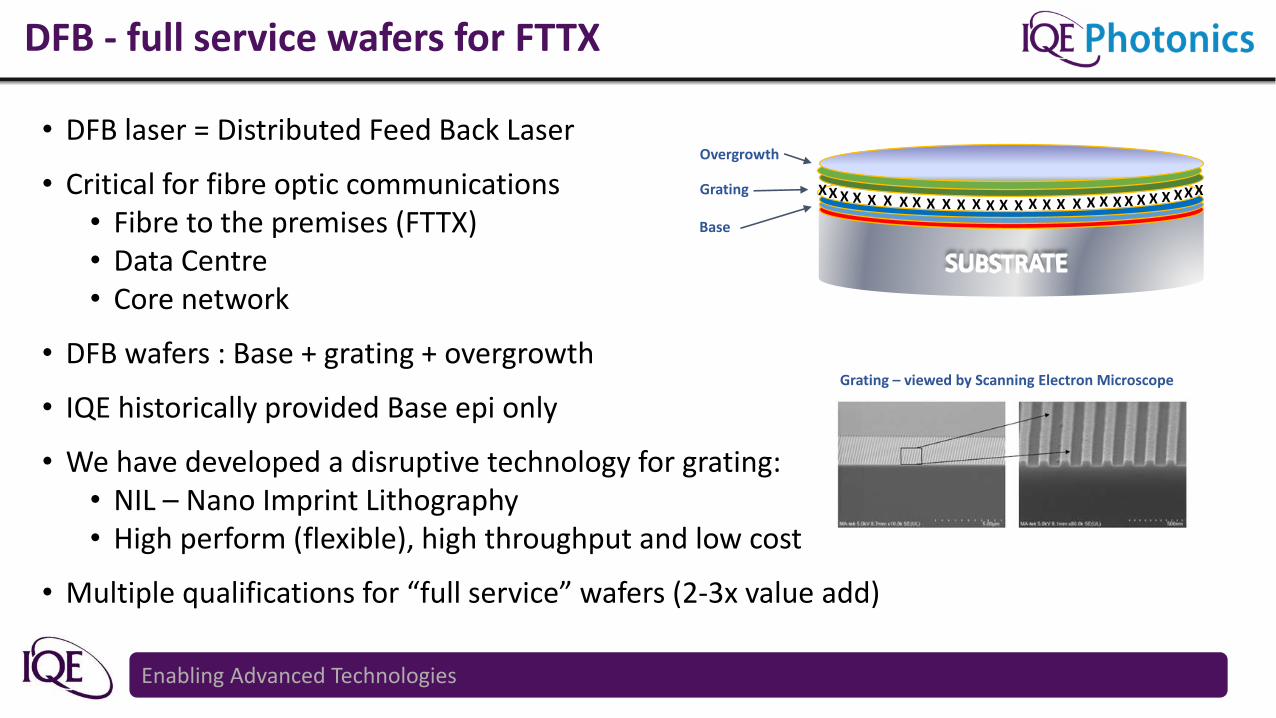

DFB - full service wafers for FTTX

• DFB laser = Distributed Feed Back Laser

• Critical for fibre optic communications• Fibre to the premises (FTTX)• Data Centre• Core network

• DFB wafers : Base + grating + overgrowth

• IQE historically provided Base epi only

• We have developed a disruptive technology for grating:• NIL – Nano Imprint Lithography• High perform (flexible), high throughput and low cost

• Multiple qualifications for “full service” wafers (2-3x value add)

Grating – viewed by Scanning Electron Microscope

XX X X X X X X X X X X X X X X X XXX XX XXX X XXX

Overgrowth

Grating

Base

Enabling Advanced Technologies

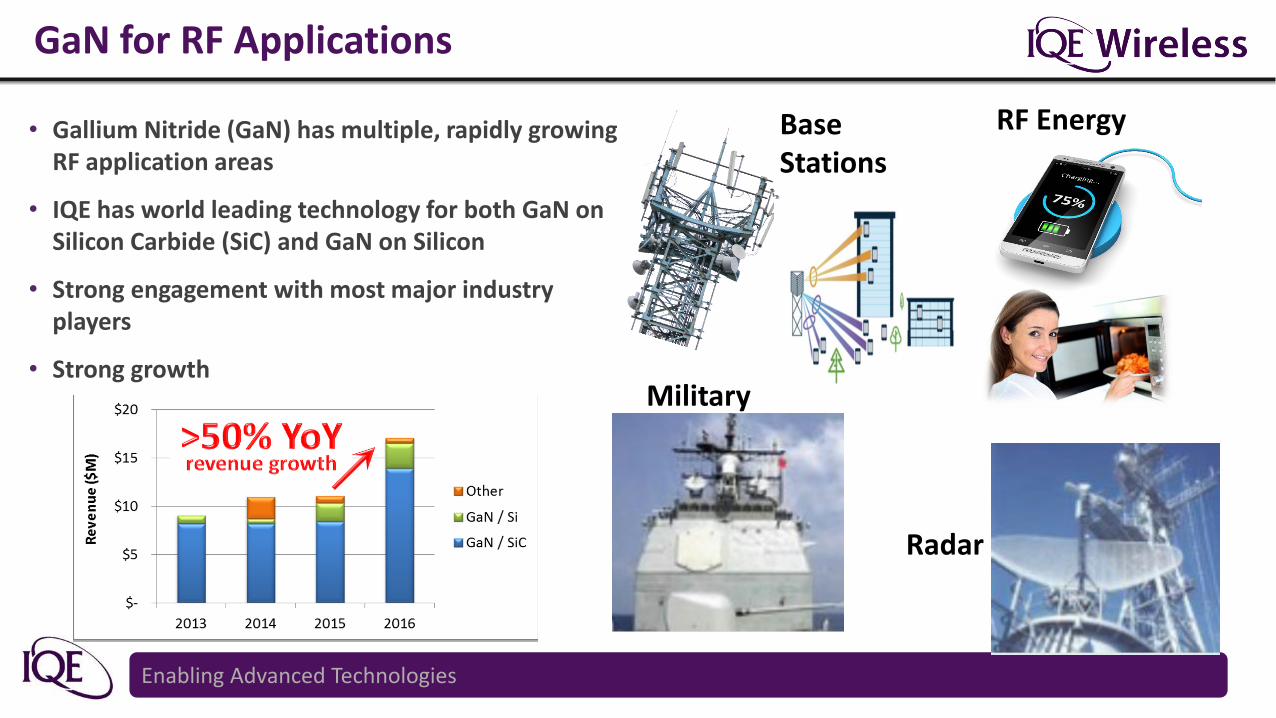

GaN for RF Applications

• Gallium Nitride (GaN) has multiple, rapidly growing RF application areas

• IQE has world leading technology for both GaN on Silicon Carbide (SiC) and GaN on Silicon

• Strong engagement with most major industry players

• Strong growth

RF EnergyBase Stations

Military

Radar

Enabling Advanced Technologies

Mid Term Drivers to Accelerate Growth

Enabling Advanced Technologies

Wireless filters (cREO)

$0.0b

$2.5b

$5.0b

$7.5b

$10.0b

$12.5b

$15.0b

2013 2014 2015 2016 2017

Mobile Device RF TAM

~15% CAGR

Filter Content $0.25 $1.25 $4.00 $7.25

Switching / Tuning $0.00 $0.25 $1.50 $2.25

Power Amplifiers $0.30 $1.25 $2.00 $3.25

Other $0.00 $0.00 $0.50 $0.50

Total RF content $0.55 $2.75 $8.00 $13.25 +

Typical2G

Typical3G

RegionalLTE

GlobalLTE

Potential routes to access using cREOTM

technology

Enabling Advanced Technologies

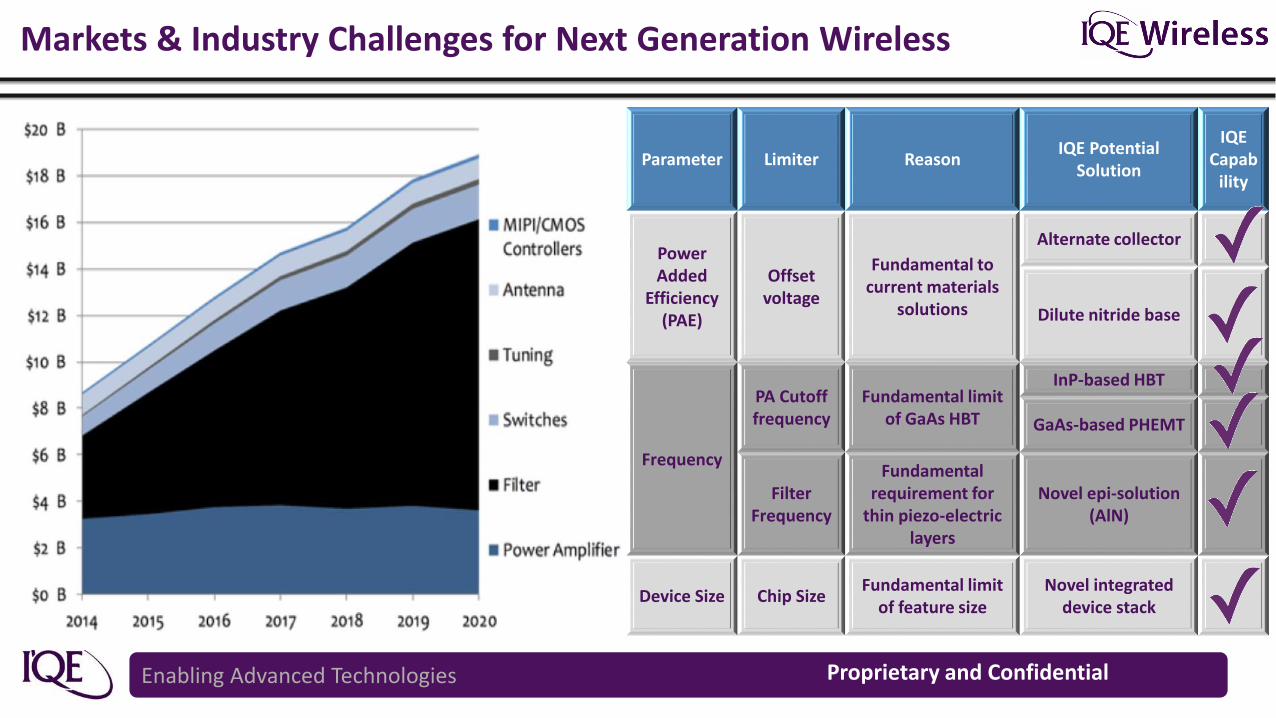

Markets & Industry Challenges for Next Generation Wireless

Parameter Limiter ReasonIQE Potential

Solution

IQE Capab

ility

Power Added

Efficiency(PAE)

Offset voltage

Fundamental to current materials

solutions

Alternate collector

Dilute nitride base

Frequency

PA Cutoff frequency

Fundamental limit of GaAs HBT

InP-based HBT

GaAs-based PHEMT

Filter Frequency

Fundamentalrequirement for

thin piezo-electric layers

Novel epi-solution (AlN)

Device Size Chip SizeFundamental limit

of feature sizeNovel integrated

device stack

Proprietary and Confidential

Enabling Advanced Technologies

Compound semiconductors for Power, RF and Lighting

10 100 1K 10K 100K 1M 10M

10

100

1K

10K

100K

1M

10MSiC

GaN

Silicon

Operating frequency (Hz)

Ou

tpu

t Po

wer

(V

A)

High Speed

High Power

Power inverters

EV/HEV

Micro InvertersPC (DC-DC)

Data Centre

Power Inverters

Enabling Advanced Technologies

Applications for IQE Solar Technology

• High efficiency solar cells

• 44% efficiency (Silicon ~18%)

• Power Generation Markets

• Satellites

• LEO’s

• Drones

• Terrestrial

Enabling Advanced Technologies

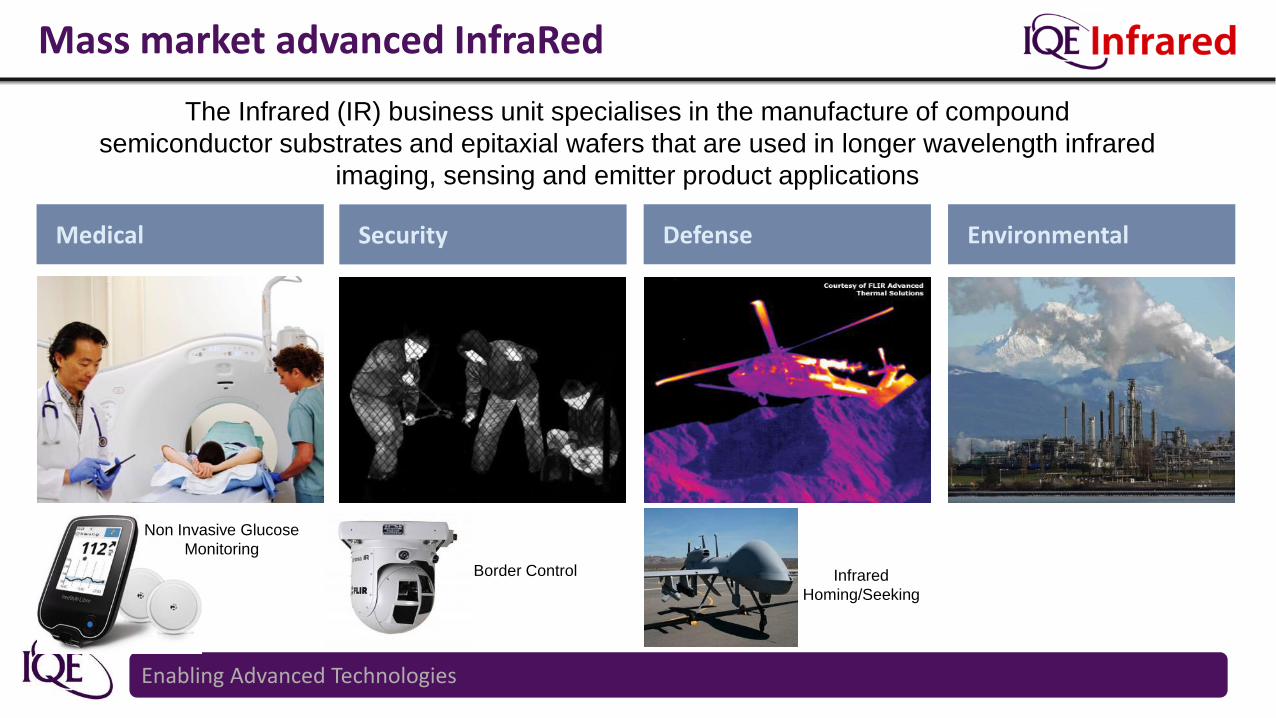

Mass market advanced InfraRed

The Infrared (IR) business unit specialises in the manufacture of compound

semiconductor substrates and epitaxial wafers that are used in longer wavelength infrared

imaging, sensing and emitter product applications

Medical DefenseSecurity Environmental

Non Invasive Glucose

Monitoring

Border Control Infrared

Homing/Seeking

Enabling Advanced Technologies

Longer Term Drivers to Accelerate Growth

Enabling Advanced Technologies

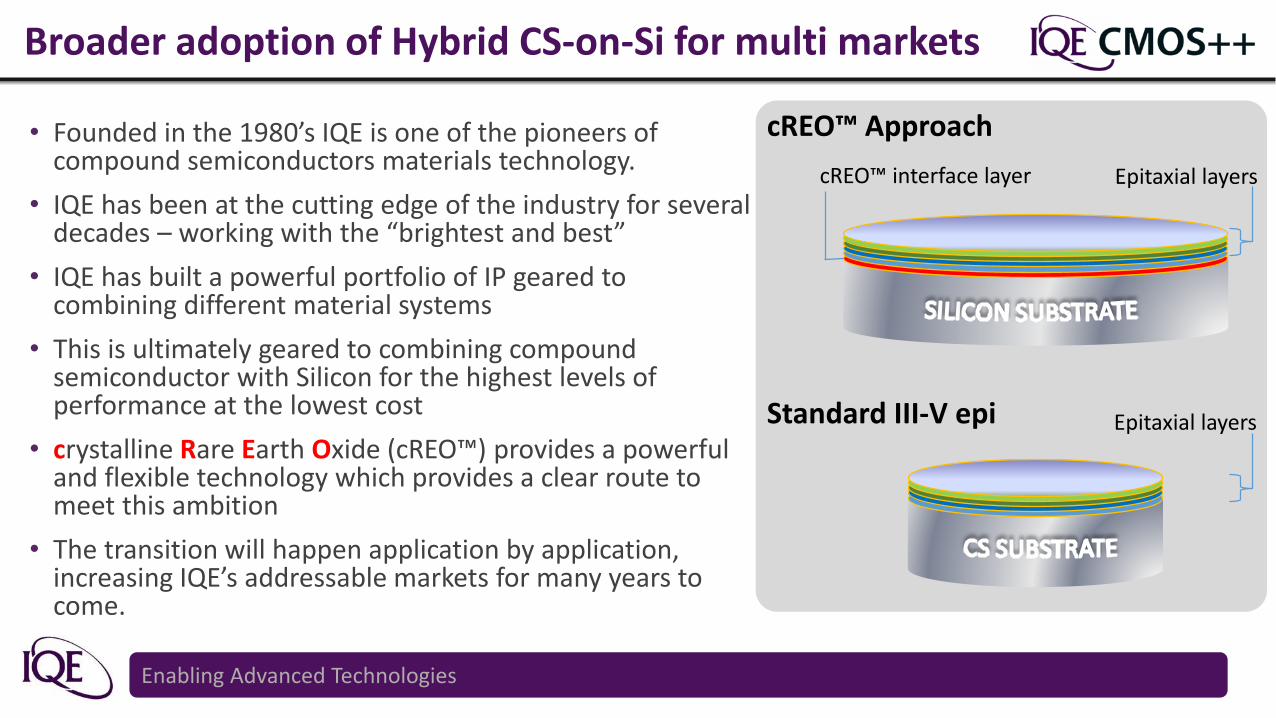

Broader adoption of Hybrid CS-on-Si for multi markets

• Founded in the 1980’s IQE is one of the pioneers of compound semiconductors materials technology.

• IQE has been at the cutting edge of the industry for several decades – working with the “brightest and best”

• IQE has built a powerful portfolio of IP geared to combining different material systems

• This is ultimately geared to combining compound semiconductor with Silicon for the highest levels of performance at the lowest cost

• crystalline Rare Earth Oxide (cREO™) provides a powerful and flexible technology which provides a clear route to meet this ambition

• The transition will happen application by application, increasing IQE’s addressable markets for many years to come.

Epitaxial layerscREO™ interface layer

Epitaxial layers

cREO™ Approach

Standard III-V epi

Enabling Advanced Technologies

Summary

• The CS Industry is moving through an Inflection Point

• IQE has geared its strategy and evolution to capture this opportunity

• At the heart of its strategy IQE’s IP portfolio is a key differentiator

• This is supported by a flexible and cost effective route to scaling the business

• This has translated into market leadership for IQE, with a sound “Basecase” for continuing growth

• However, the breadth and depth of IQE’s engagement in a broad range of near, mid and long term opportunities provide strong upside to the Basecase

• The start of the VCSEL ramp in H1 provides a key milestone on this journey

Enabling Advanced Technologies

Q&A