ira hot topics

TRANSCRIPT

Hot IRA Topics Hot IRA Topics Hot IRA Topics Hot IRA Topics

Presented by:Robert L. Wolff,

Esq.P.O. Box 381

Dumaguete City, Negros OrientalPhilippines 6200

NY (518) 325-6015PH 09266485273

Fax: (518) 677-1600

DisclaimerDisclaimerI am not an attorney admitted to practice law in the I am not an attorney admitted to practice law in the Philippines. Philippines. I am admitted to practice law in New York.I am admitted to practice law in New York.The following is not a legal advice, but rather The following is not a legal advice, but rather comments and observations.comments and observations.For answers to legal issues raised by this For answers to legal issues raised by this presentation, you need to consult an attorney presentation, you need to consult an attorney admitted to practice law in the Philippines.admitted to practice law in the Philippines.

Problems to be Problems to be Aware of Aware of

and and Planning Planning

OpportunitiesOpportunities

Problems to be Problems to be Aware of Aware of

and and Planning Planning

OpportunitiesOpportunities

Not understanding how Not understanding how your assetsyour assets

will be distributed at death will be distributed at death can result in an estate can result in an estate

catastrophe. catastrophe. The Three Main Ways

Your Estate is Distributed:

ProbateRight of SurvivorshipContract

Problems with Doing a Problems with Doing a Rollover to an IRARollover to an IRA

Rollover from a 401(k) is subject to Rollover from a 401(k) is subject to an automatic 20% income tax an automatic 20% income tax withholdingwithholding

IRA to IRA rollover, only have 60 IRA to IRA rollover, only have 60 days to complete a rolloverdays to complete a rollover

Only the property distributed or Only the property distributed or cash can be rollovercash can be rollover

Required minimum distributions Required minimum distributions cannot be rolled overcannot be rolled over

One IRA to IRA rollover a year ruleOne IRA to IRA rollover a year rule

Required Minimum Required Minimum Distributions from Distributions from

Multiple Retirement Multiple Retirement PlansPlans

The total required minimum distributions from multiple IRAs can be taken from all or any one of the IRAs – except for an inherited IRAs

401(k)s do not have this rule, the required distribution has to be from each 401(k)

Problems with Problems with Pre-Nuptial AgreementsPre-Nuptial Agreements

The qualified joint and survivor The qualified joint and survivor annuity and qualified pre-annuity and qualified pre-retirement survivor annuity rulesretirement survivor annuity rules

Only a spouse can waive QJSD or Only a spouse can waive QJSD or QPSA rulesQPSA rules

This rule does not apply to IRAs.This rule does not apply to IRAs.

It is important to keep It is important to keep your designation of your designation of

beneficiary form up to beneficiary form up to date.date.As we age, often the As we age, often the

beneficiaries of our estate beneficiaries of our estate change. It is important that change. It is important that as the beneficiaries of our as the beneficiaries of our estate change, we update our estate change, we update our designated beneficiary designated beneficiary selection selection

The problem of having named The problem of having named an ex-spouse, a deceased an ex-spouse, a deceased spouse or a spouse in a spouse or a spouse in a nursing home as a beneficiary.nursing home as a beneficiary.

Kennedy v. DuPontKennedy v. DuPont Kennedy v. Plan Administrator for DuPont Savings and Investment

Plan, (No. 07-636, Decided January 26, 2009)

In a court battle that has been ongoing since 2001, Kari Kennedy lost a $402,000 inheritance because the beneficiary form did not name her as the beneficiary, even though that is what her father wanted. The United State Supreme Court UNANIMOUSLY ruled that the ex-spouse receives the retirement plan money because she was named on the beneficiary form – even though she waived her rights to that money in a divorce decree.

The Supreme Court ruling is the law of the land and there are no more appeals.

The beneficiary form controls who inherits the money and all of the Justices agree.

You need to understand You need to understand who can be who can be

a designated beneficiarya designated beneficiaryOnly an individual or an Only an individual or an

individual who is a individual who is a beneficiary of a Qualified beneficiary of a Qualified IRA Trust can be a IRA Trust can be a designated beneficiary.designated beneficiary.

Your designated beneficiary Your designated beneficiary is important if you want to is important if you want to create a Stretch-Out-IRA, create a Stretch-Out-IRA, the gift that keeps on giving.the gift that keeps on giving.

Why use separate accounts Why use separate accounts for IRAs for multiple IRA for IRAs for multiple IRA

beneficiariesbeneficiaries Oldest beneficiary rule.Oldest beneficiary rule.

The problem of naming an The problem of naming an entity, such as your estate, entity, such as your estate, as one of the beneficiaries as one of the beneficiaries of an IRA.of an IRA.

Using separate accounts Using separate accounts avoids the oldest avoids the oldest beneficiary rule.beneficiary rule.

Spouse and Non-Spouse and Non-Spouse RolloversSpouse Rollovers

Non-spouse can transfer a 401(k) to an Inherited IRA (can also convert to a Roth IRA), but can not rollover an inherited IRA.

Only a spouse can rollover a 401(k) or an IRA.

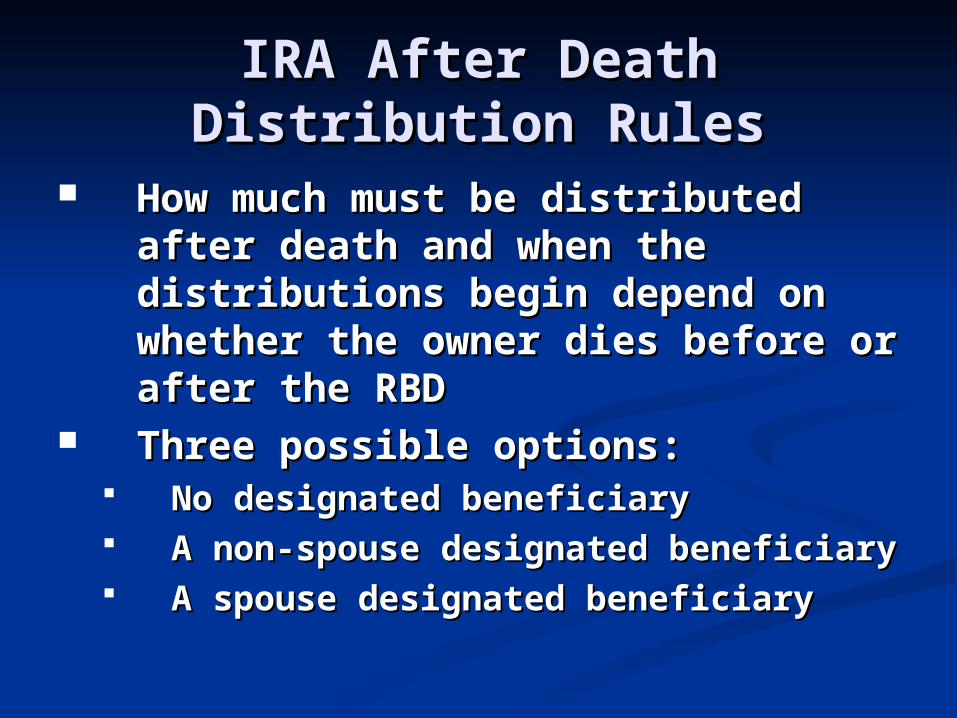

IRA After Death IRA After Death Distribution RulesDistribution Rules

How much must be distributed How much must be distributed after death and when the after death and when the distributions begin depend on distributions begin depend on whether the owner dies before or whether the owner dies before or after the RBDafter the RBD

Three possible options:Three possible options: No designated beneficiaryNo designated beneficiary A non-spouse designated beneficiaryA non-spouse designated beneficiary A spouse designated beneficiaryA spouse designated beneficiary

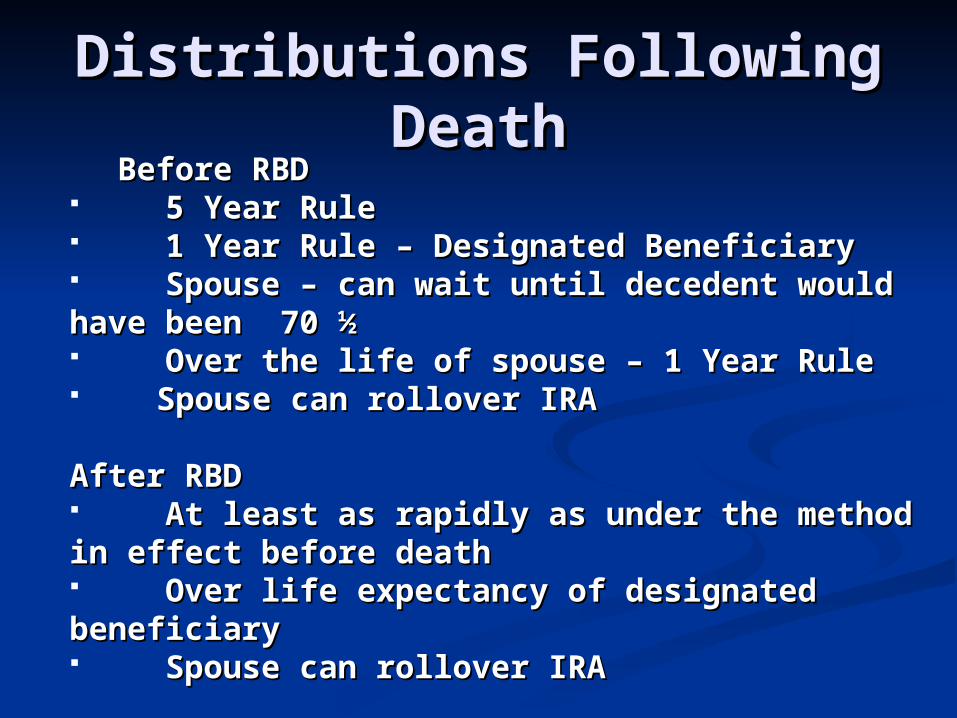

Distributions Following Distributions Following DeathDeath

Before RBDBefore RBD 5 Year Rule5 Year Rule 1 Year Rule – Designated Beneficiary1 Year Rule – Designated Beneficiary Spouse – can wait until decedent would Spouse – can wait until decedent would have been 70 ½ have been 70 ½ Over the life of spouse – 1 Year RuleOver the life of spouse – 1 Year Rule Spouse can rollover IRASpouse can rollover IRA

After RBDAfter RBD At least as rapidly as under the method in At least as rapidly as under the method in effect before deatheffect before death Over life expectancy of designated Over life expectancy of designated beneficiarybeneficiary Spouse can rollover IRASpouse can rollover IRA

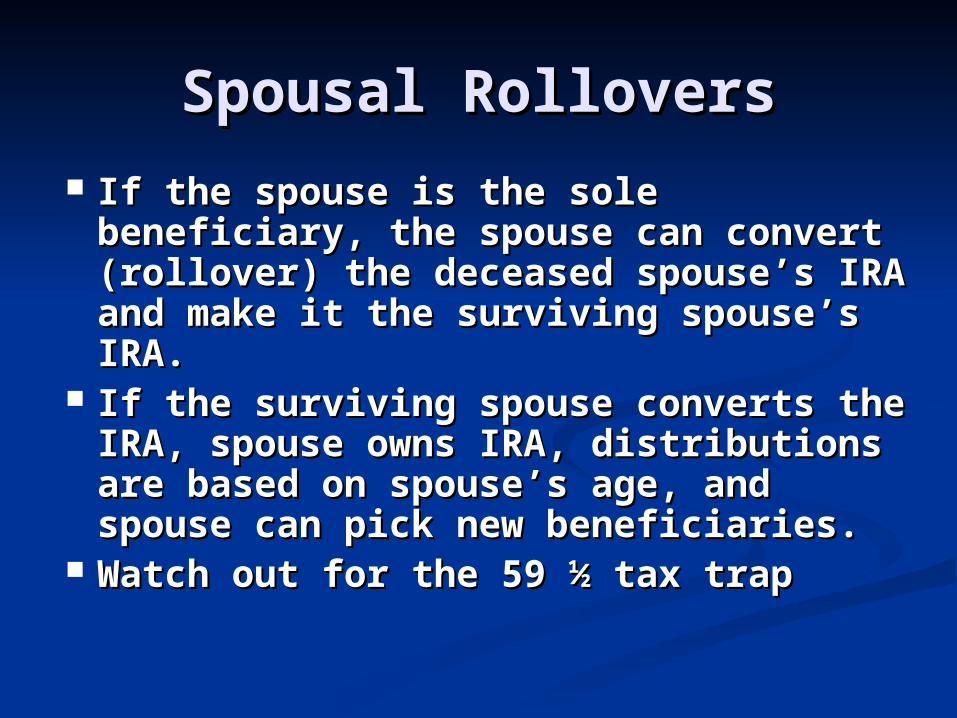

Spousal RolloversSpousal Rollovers

If the spouse is the sole beneficiary, If the spouse is the sole beneficiary, the spouse can convert (rollover) the spouse can convert (rollover) the deceased spouse’s IRA and the deceased spouse’s IRA and make it the surviving spouse’s IRA.make it the surviving spouse’s IRA.

If the surviving spouse converts the If the surviving spouse converts the IRA, spouse owns IRA, distributions IRA, spouse owns IRA, distributions are based on spouse’s age, and are based on spouse’s age, and spouse can pick new beneficiaries.spouse can pick new beneficiaries.

Watch out for the 59 ½ tax trapWatch out for the 59 ½ tax trap

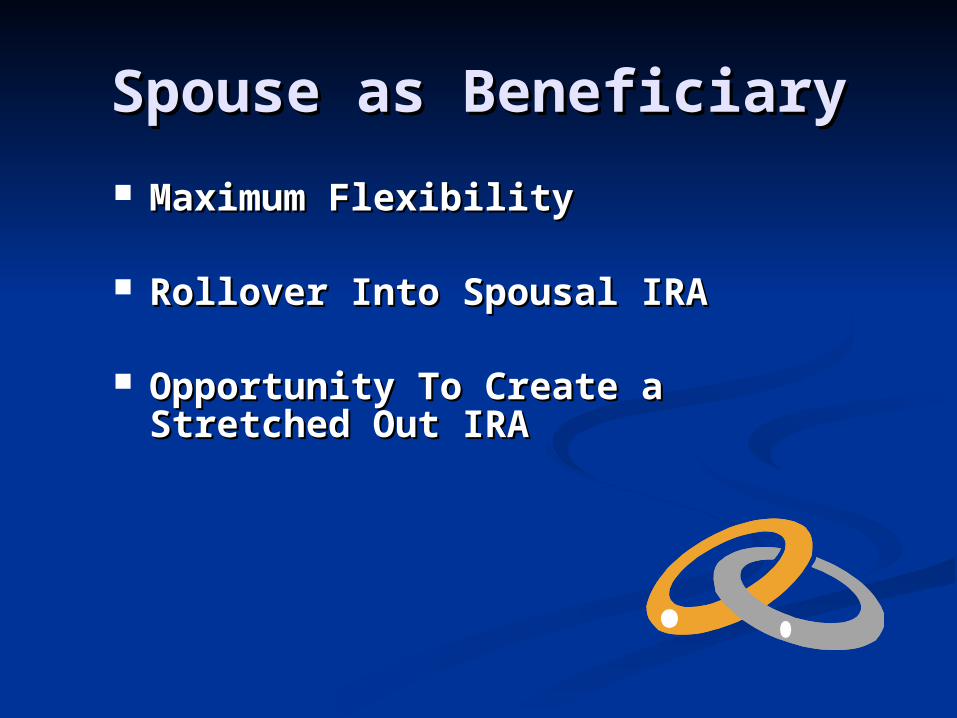

Spouse as BeneficiarySpouse as Beneficiary

Maximum FlexibilityMaximum Flexibility

Rollover Into Spousal IRARollover Into Spousal IRA

Opportunity To Create a Opportunity To Create a Stretched Out IRAStretched Out IRA

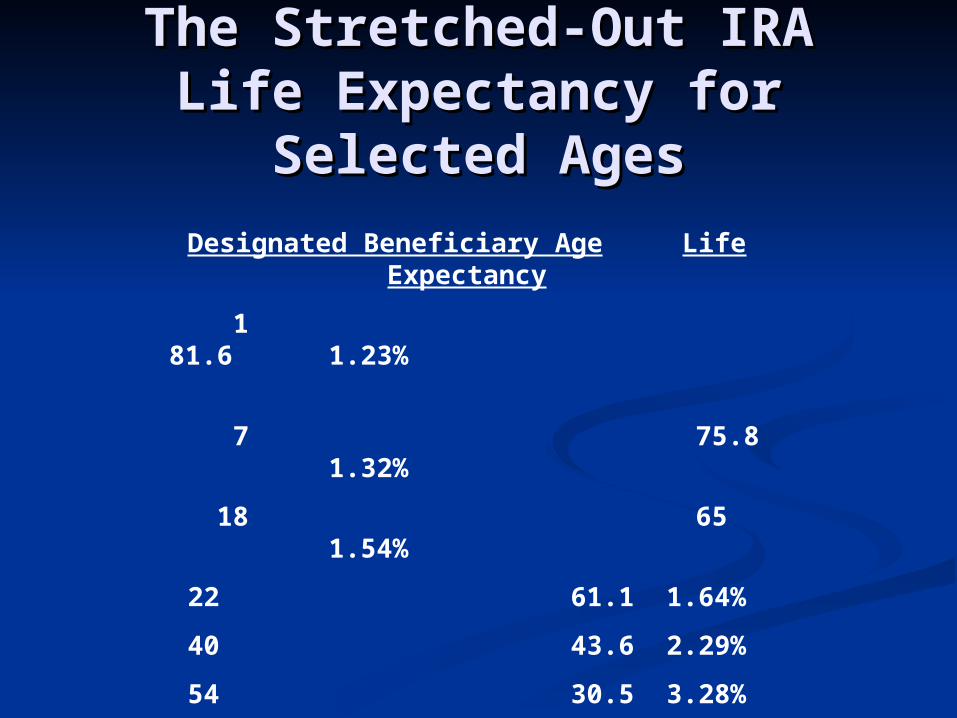

The Stretched-Out IRAThe Stretched-Out IRALife Expectancy for Life Expectancy for

Selected AgesSelected Ages

Designated Beneficiary Age Life Expectancy

1 81.6 1.23%

7 75.8 1.32%

18 65 1.54%

22 61.1 1.64%

40 43.6 2.29%

54 30.5 3.28%

80 10.2 9.80%

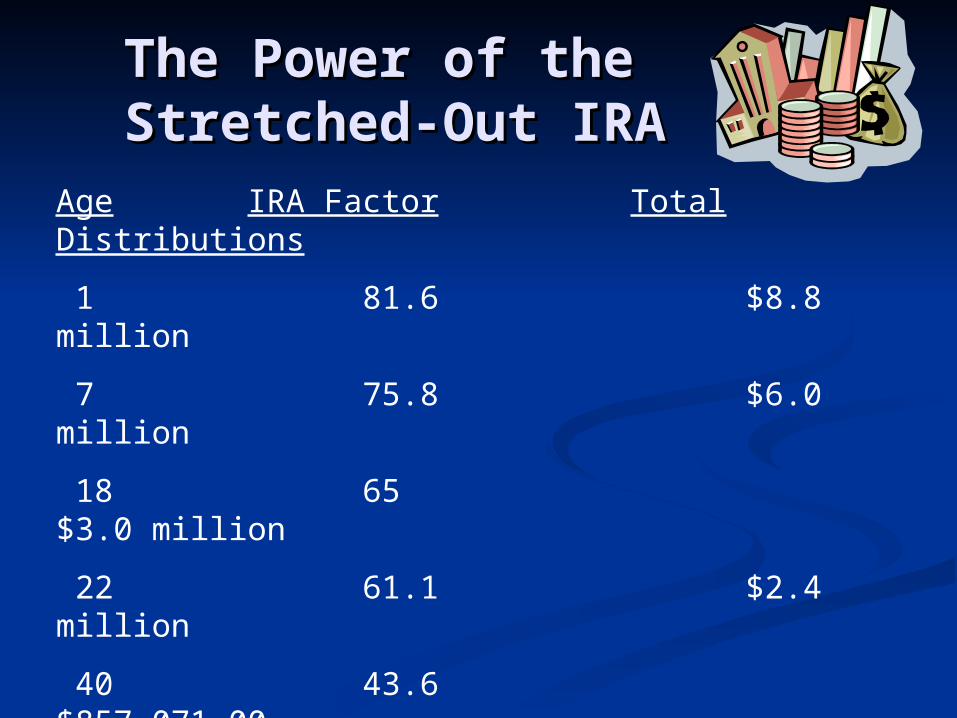

The Power of the The Power of the Stretched-Out IRAStretched-Out IRA

Age IRA Factor Total Distributions

1 81.6 $8.8 million

7 75.8 $6.0 million

18 65 $3.0 million

22 61.1 $2.4 million

40 43.6 $857,071.00

54 30.5 $415,949.00

80 10.2 $157,958.00

Assume $100,000.00 was invested at 8%

The Stretched- Out- IRAThe Stretched- Out- IRA

Give a Tax Shelter Piggy Bank to Your Give a Tax Shelter Piggy Bank to Your HeirsHeirs

Minimum Distribution

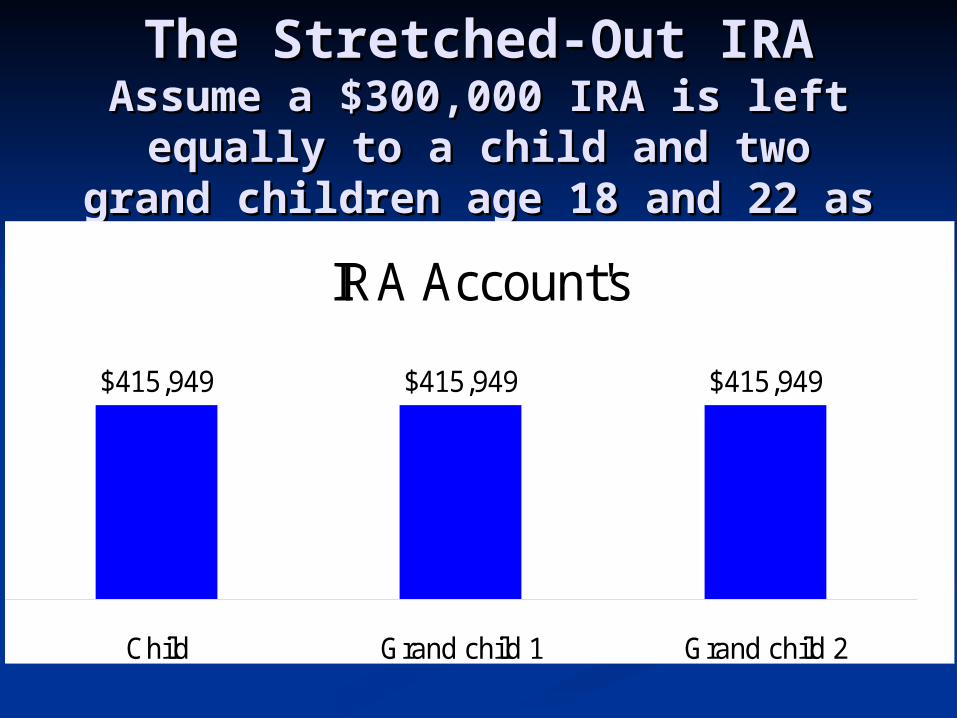

The Stretched-Out IRAThe Stretched-Out IRAAssume a $300,000 IRA is left Assume a $300,000 IRA is left

equally to a child and two grand equally to a child and two grand children age 18 and 22 as one children age 18 and 22 as one

account Invested at eight account Invested at eight percentpercent

IR A Account's

$415,949 $415,949 $415,949

C hild G rand child 1 G rand child 2

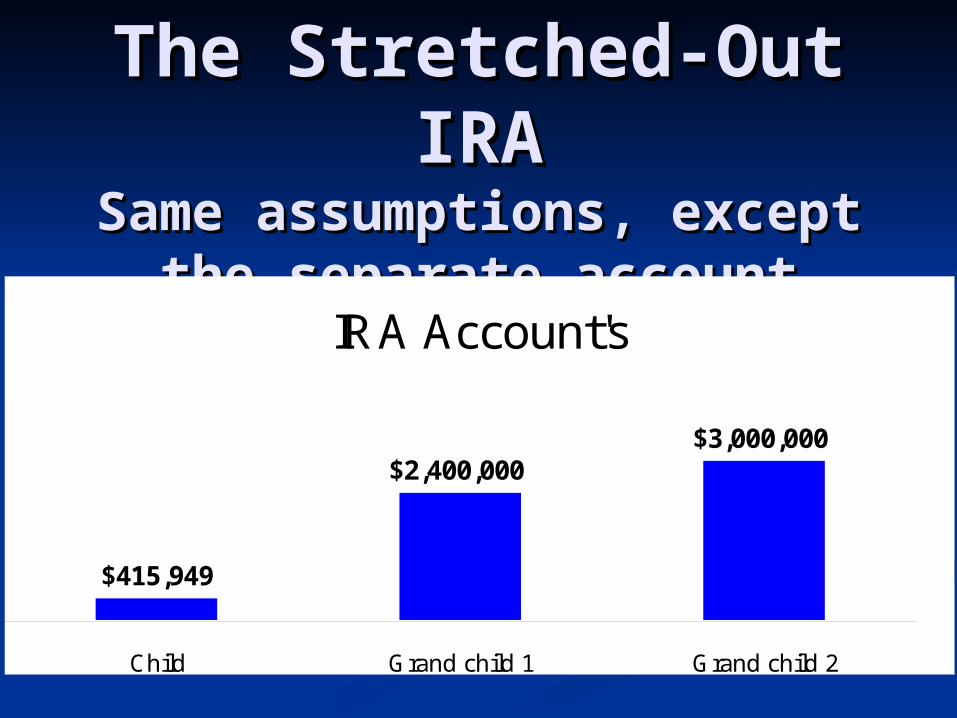

The Stretched-Out The Stretched-Out IRAIRA

Same assumptions, except Same assumptions, except the separate account the separate account

method is used.method is used.IR A Account's

$2,400,000$3,000,000

$415,949

C hild G rand child 1 G rand child 2

Why Name a Trust as a Why Name a Trust as a Beneficiary of an IRA?Beneficiary of an IRA?

Control and Asset Control and Asset Protection Protection

Planning for the Planning for the Trust BeneficiaryTrust Beneficiary

Benefits of Naming a Benefits of Naming a Trust as IRA BeneficiaryTrust as IRA Beneficiary Spendthrift protectionSpendthrift protection Creditor (asset) Creditor (asset) protectionprotection

Divorce protectionDivorce protection Estate planningEstate planning ““Dead-hand” controlDead-hand” control

DisclaimersDisclaimers General RuleGeneral Rule for for Qualified Qualified

DisclaimerDisclaimerMust be:Must be: In writingIn writing Within 9 monthsWithin 9 months No acceptance of the interest No acceptance of the interest

or any of its benefitsor any of its benefits Interest passes without any Interest passes without any

direction on the part of the direction on the part of the person making the person making the disclaimerdisclaimer

DisclaimersDisclaimers Assume a $300,000 IRA is left to a child age Assume a $300,000 IRA is left to a child age 54 with two grand children, age 18 and 22 54 with two grand children, age 18 and 22

as successor beneficiaries. Account as successor beneficiaries. Account Invested at eight percent, total distribution Invested at eight percent, total distribution

to all three is $1,247,847.to all three is $1,247,847.

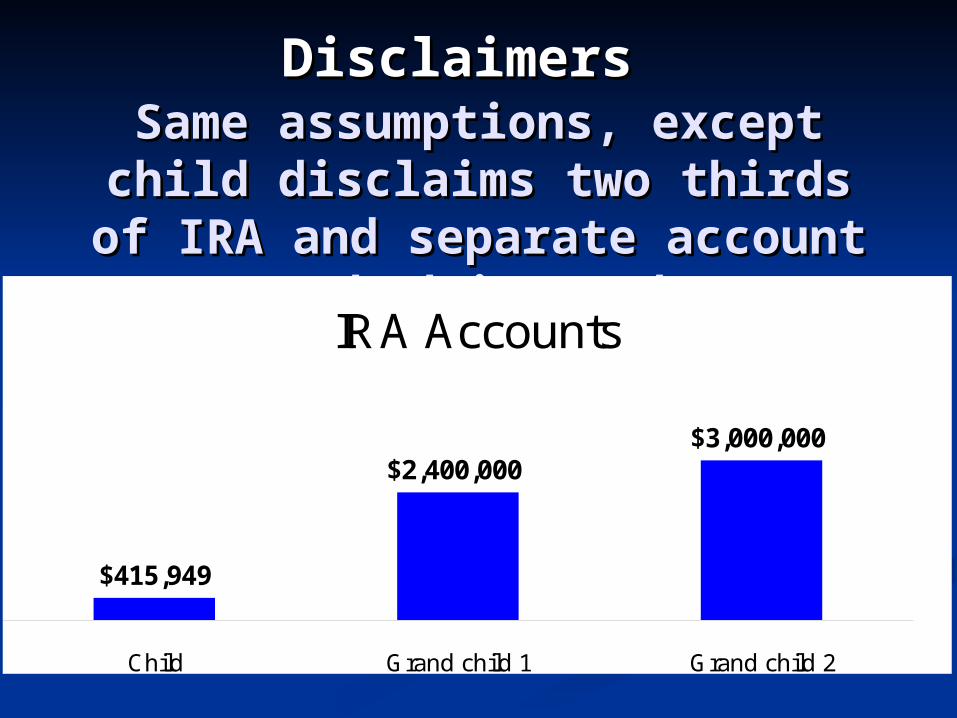

DisclaimersDisclaimers Same assumptions, except Same assumptions, except

child disclaims two thirds of child disclaims two thirds of IRA and separate account IRA and separate account

method is used.method is used.IR A Accounts

$2,400,000$3,000,000

$415,949

C hild G rand child 1 G rand child 2

Taking advantage of the Taking advantage of the Income Tax deduction for Income Tax deduction for

an individual IRAan individual IRA

Income in respect of a Income in respect of a decedent.decedent.

IRA are subject to double IRA are subject to double taxation.taxation.

Estate tax paid on the IRA Estate tax paid on the IRA death benefits can be used as death benefits can be used as a deduction to off-set income a deduction to off-set income taxes on distributions from taxes on distributions from the inherited IRA.the inherited IRA.

Net Unrealized Net Unrealized AppreciationAppreciation Contribution basis of stock or employer Contribution basis of stock or employer

security is taxable, but not the NUA.security is taxable, but not the NUA.

Rollover of employer securities to an IRA, the Rollover of employer securities to an IRA, the NUA exception is lost. The exception only NUA exception is lost. The exception only applies to qualified plans. There is no NUA applies to qualified plans. There is no NUA exception for IRAs.exception for IRAs.

Must be a lump sum distribution--with one Must be a lump sum distribution--with one taxable year. On account of:taxable year. On account of:

Employee’s separation from service;Employee’s separation from service;

Death of employee;Death of employee;

After employee attains 59 ½; andAfter employee attains 59 ½; and

Disability of employee.Disability of employee.

Charitable Remainder Trust Charitable Remainder Trust as Beneficiaries of an IRAas Beneficiaries of an IRA

Creates an Estate Tax Charitable Deduction

CRT-Pays no income tax on distribution

Creates a stream of income for the beneficiary

Benefits the charity

The Skinny on Charitable GivingThe Skinny on Charitable Giving

What is in it for me?

The Internal Revenue Code has a matching program which basically states- If you make a charitable donation, we will give you a tax deduction

What does this mean to the typical taxpayer? You can give to your favorite charity the tax dollars that would otherwise be pay in taxes to the IRS and New York State!

The Roth Do-OverThe Roth Do-Over

Taxpayers may recharacterize Taxpayers may recharacterize (i.e. “undo”or “redo”) the Roth (i.e. “undo”or “redo”) the Roth IRA conversion in current year or IRA conversion in current year or by the filing date of the current by the filing date of the current year’s tax returnyear’s tax return

Recharacterization can take Recharacterization can take place as late as 10/15 in the year place as late as 10/15 in the year following the year of conversionfollowing the year of conversion

Recharacterization in a Recharacterization in a Down MarketDown Market

Mary, in January, 2015 converts her Mary, in January, 2015 converts her $100,000 Traditional IRA to a Roth $100,000 Traditional IRA to a Roth IRAIRA

By September, 2016, Roth account By September, 2016, Roth account value is $60,000value is $60,000

Mary will pay income taxes on Mary will pay income taxes on $40,000 that is not in her Roth $40,000 that is not in her Roth account, unless Mary recharacterizes account, unless Mary recharacterizes her Roth account by October 15, her Roth account by October 15, 20162016

Roth IRAsRoth IRAs Contributions are non-tax deductibleContributions are non-tax deductible

100% of growth is income free, 100% of growth is income free, as opposed as opposed to merely tax deferred.to merely tax deferred.

Qualified distributions can be withdrawn Qualified distributions can be withdrawn income tax freeincome tax free

Roth IRAs are not subject to the minimum Roth IRAs are not subject to the minimum distributions rule (RMD) at age 70 ½distributions rule (RMD) at age 70 ½

Key Points To Consider Key Points To Consider When Considering a Roth When Considering a Roth

conversionconversion TTax free income is for your life and your ax free income is for your life and your

heirs.heirs. The income tax liability paid when you The income tax liability paid when you

convert is convert is NOTNOT an additional tax liability – an additional tax liability – the income tax liability is already built the income tax liability is already built into the tax due on Traditional IRA into the tax due on Traditional IRA distribution. distribution.

TAX POINT - Some one is going to pay TAX POINT - Some one is going to pay income taxes, either now or later. The income taxes, either now or later. The only question is when.only question is when.

The Roth IRA is a POWERFUL WEALTH The Roth IRA is a POWERFUL WEALTH TRANSFER VEHICLE because it is not TRANSFER VEHICLE because it is not subject to RMDs and offers tax free subject to RMDs and offers tax free growth, not tax just deferred growth. growth, not tax just deferred growth.

Hedge against increasing Income Tax Rates

Historically, income tax rates Historically, income tax rates are low. are low.

If income rates go up, qualified If income rates go up, qualified distributions from a Roth IRA distributions from a Roth IRA are not subject to income taxes.are not subject to income taxes.

Investment Diversification

The two main sources of tax-The two main sources of tax-exempt income are Municipal exempt income are Municipal Bonds and Roth IRA.Bonds and Roth IRA.

When planning to generate tax-When planning to generate tax-exempt income – Roth offer exempt income – Roth offer greater diversification.greater diversification.

Social Security Tax Reduction Planning

If your income is too high– 50% to 85% of If your income is too high– 50% to 85% of your social security benefits are taxable.your social security benefits are taxable.

When calculating income for social When calculating income for social security purposes– tax exempt income is security purposes– tax exempt income is included – Roth IRA distributions are not.included – Roth IRA distributions are not.

Roth IRA distributions can be used to Roth IRA distributions can be used to supplement retirement without increasing supplement retirement without increasing income for social security purposes.income for social security purposes.

To Reduce Tax On Social To Reduce Tax On Social Security IncomeThink Roth Security IncomeThink Roth

IRA or AnnuityIRA or Annuity QQualified income from a Roth IRA is ualified income from a Roth IRA is tax free, which will reduce your tax free, which will reduce your Provisional Income.Provisional Income.

A deferred Annuity will defer A deferred Annuity will defer income, reducing Provisional income, reducing Provisional Income.Income.

An immediate Annuity payment is An immediate Annuity payment is part return of capital, part income. part return of capital, part income. The return of capital part is not The return of capital part is not taxable, reducing Provisional taxable, reducing Provisional income.income.

The Tax-Free Stretch Roth IRA

A compelling reason to convert A compelling reason to convert to a Roth IRA – the beneficiary to a Roth IRA – the beneficiary can stretch tax-free can stretch tax-free distributions over his or her life distributions over his or her life time.time.

Assets inside the Roth IRA can Assets inside the Roth IRA can continue to grow tax free, as continue to grow tax free, as opposed to merely tax deferred.opposed to merely tax deferred.

Roth IRA PlanningRoth IRA PlanningPre Death ConsiderationsPre Death Considerations

A $100,000 IRA left to an 18 year old invested A $100,000 IRA left to an 18 year old invested at 8% over the beneficiary’s life will distribute at 8% over the beneficiary’s life will distribute approximately 3 million. If the beneficiary’s approximately 3 million. If the beneficiary’s average tax rate was 30%, $900,000 in income average tax rate was 30%, $900,000 in income taxes would be paid, leaving a net of 2.1 taxes would be paid, leaving a net of 2.1 million.million.

If the IRA owner’s income tax rate was 30% and If the IRA owner’s income tax rate was 30% and converted the $100,000 to a Roth IRA, $30,000 converted the $100,000 to a Roth IRA, $30,000 would be income taxe liability.would be income taxe liability.

By the IRA owner paying $30,000 in income By the IRA owner paying $30,000 in income taxes, the beneficiary would receive an taxes, the beneficiary would receive an additional net income tax free income of additional net income tax free income of $900,000, plus remove the $30,000 from the $900,000, plus remove the $30,000 from the IRA owner’s taxable estate, reducing estate IRA owner’s taxable estate, reducing estate taxes. taxes.

Trust Planning

A trust in 2014 reaches the A trust in 2014 reaches the highest marginal rate of 39.6% highest marginal rate of 39.6% when income exceeds $12,150when income exceeds $12,150

With a Roth IRA – no trust With a Roth IRA – no trust income tax on distributions from income tax on distributions from the Roth IRA to a trust.the Roth IRA to a trust.

Long-Term PlanningLong-Term Planning

Most retirees should have part of Most retirees should have part of their retirement assets in a Roth IRA.their retirement assets in a Roth IRA. Not having to take required minimum Not having to take required minimum

distributions at age 70 ½ is a big distributions at age 70 ½ is a big PLUSPLUS.. Qualified distributions are income tax Qualified distributions are income tax

free.free. It acts as a back-up tax shelter piggy It acts as a back-up tax shelter piggy

bank.bank. The Roth is a great asset to leave to The Roth is a great asset to leave to

heirs.heirs.

If you are thinking about taking If you are thinking about taking retiring, you should also be retiring, you should also be

thinking about estate planning thinking about estate planning and such documents as:and such documents as: Power-of-Attorney Health Care Proxy Living Will Last Will and Testament Living Trust

You should also be thinking about You should also be thinking about protecting your estate from protecting your estate from

catastrophic illness.catastrophic illness.

HOW TO PLAN FOR A FUTURE

YOU CAN’T PREDICT

THE WOLFF

YOU need to make a YOU need to make a PLAN PLAN

then WORK the planthen WORK the plan

We Offer a We Offer a FREEFREE Consultation to Review Consultation to Review

Your Your IRA Designation of IRA Designation of Beneficiary FormBeneficiary Form

Pursuant to Internal Revenue Service Circular 230, we hereby inform you that the advice set forth herein with respect to U.S. federal tax issues was not intended or written by the law firm of Robert L. Wolff to used, and cannot be used, by you or any taxpayer, for the purpose of (i) avoiding any penalties that may be imposed on you or any other person under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein. Taxpayers should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

IRS Circular 230