irs whistleblower program

TRANSCRIPT

S

The IRS

Whistleblower

Program

Kevan P. McLaughlin, Esq., LL.M

Background

• 1867 – An Act to Amend Existing Laws

Relating to Internal Revenue and for

other Purposes, ch. 169, § 7, 14 Stat.

471, 473 (1867)

• 1996 – Taxpayer Bill of Rights 2, Pub.

L. No. 104-168, 110 Stat. 1452 (1996)

Tax Relief and Healthcare Act

of 2006

• Discretionary Awards – IRC § 7623(a)

• Mandatory Awards – IRC § 7623(b)

Mandatory Awards

If the Secretary proceeds with any administrative or judicial

action … based on information brought to the Secretary’s

attention by an individual, such individual shall, … receive as

an award at least 15 percent but not more than 30 percent of

the collected proceeds (including

penalties, interest, additions to tax, and additional amounts)

resulting from the action (including any related actions) or

from any settlement in response to such action. The

determination of the amount of such award by the

Whistleblower Office shall depend upon the extent to which

the individual substantially contributed to such action.

IRC § 7623(b)(1)

Limitations

IRC § 7623(b) applies to any action:

(A) against any taxpayer, but in the case of any

individual, only if such individual’s gross

income exceeds $200,000 for any taxable year

subject to such action, and

(B) if the tax, penalties, interest, additions to tax,

and additional amounts in dispute exceed

$2,000,000.

Key Provisions

• “Administrative” or “Judicial Action”

• “Proceeds Based On”

• “Related Action”

• “Collected Proceeds”

• “Amount in Dispute” and “Gross Income”

Filing a Claim

• Notice 2008-4

• Form 211

• Proposed Treas. Reg. § 301.7623-

1(c)

IRS Whistleblower Office

• Formation

• Staffing

• Responsibilities

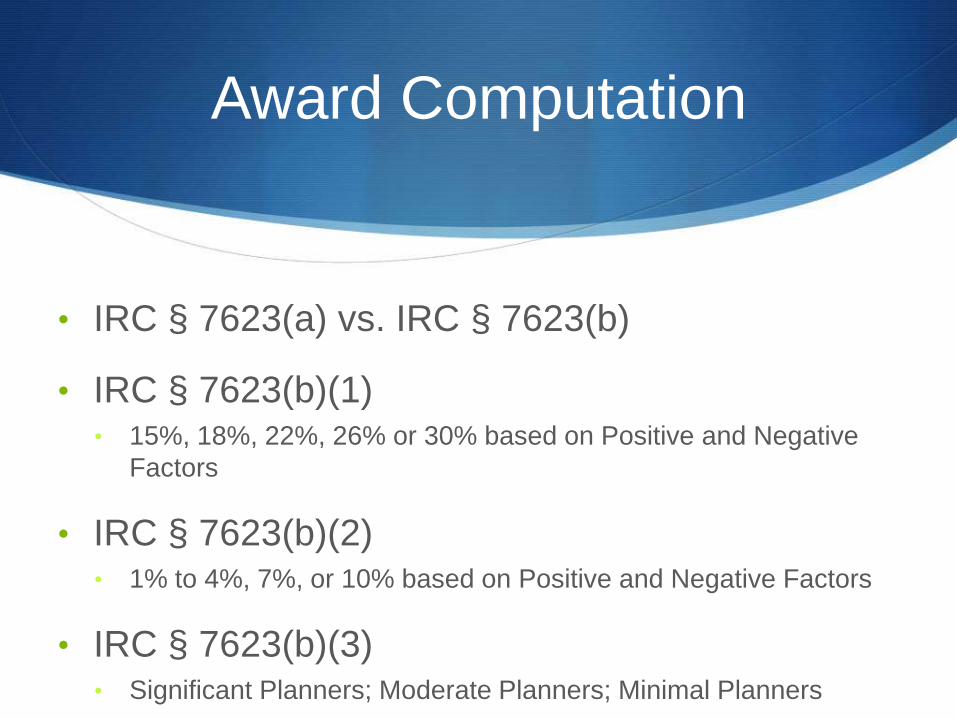

Award Computation

• IRC § 7623(a) vs. IRC § 7623(b)

• IRC § 7623(b)(1)• 15%, 18%, 22%, 26% or 30% based on Positive and Negative

Factors

• IRC § 7623(b)(2)• 1% to 4%, 7%, or 10% based on Positive and Negative Factors

• IRC § 7623(b)(3)• Significant Planners; Moderate Planners; Minimal Planners

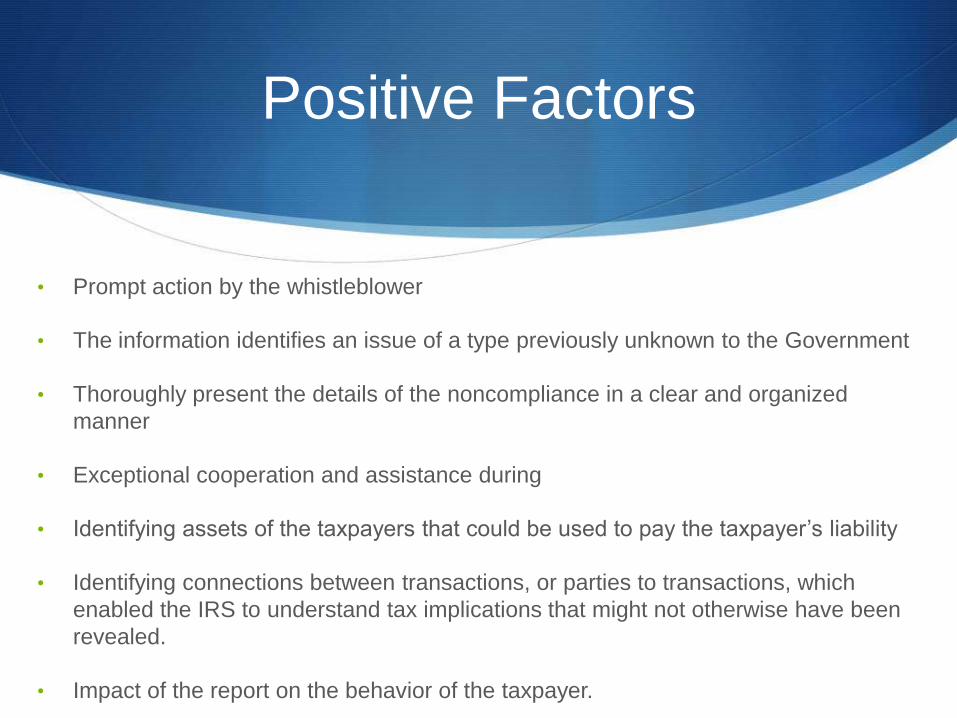

Positive Factors

• Prompt action by the whistleblower

• The information identifies an issue of a type previously unknown to the Government

• Thoroughly present the details of the noncompliance in a clear and organized

manner

• Exceptional cooperation and assistance during

• Identifying assets of the taxpayers that could be used to pay the taxpayer’s liability

• Identifying connections between transactions, or parties to transactions, which

enabled the IRS to understand tax implications that might not otherwise have been

revealed.

• Impact of the report on the behavior of the taxpayer.

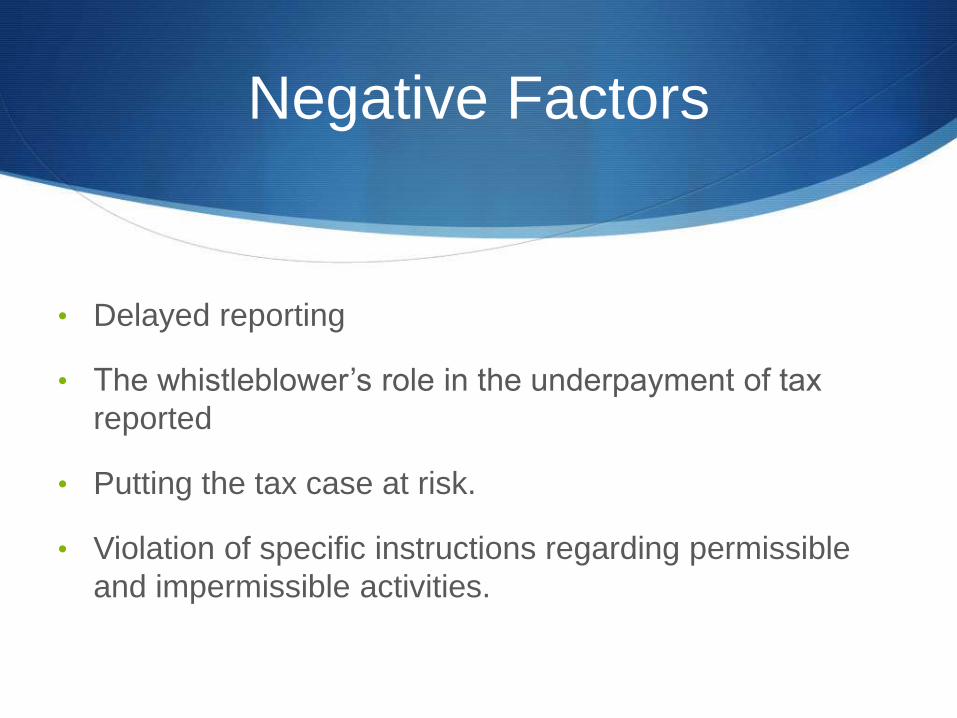

Negative Factors

• Delayed reporting

• The whistleblower’s role in the underpayment of tax

reported

• Putting the tax case at risk.

• Violation of specific instructions regarding permissible

and impermissible activities.

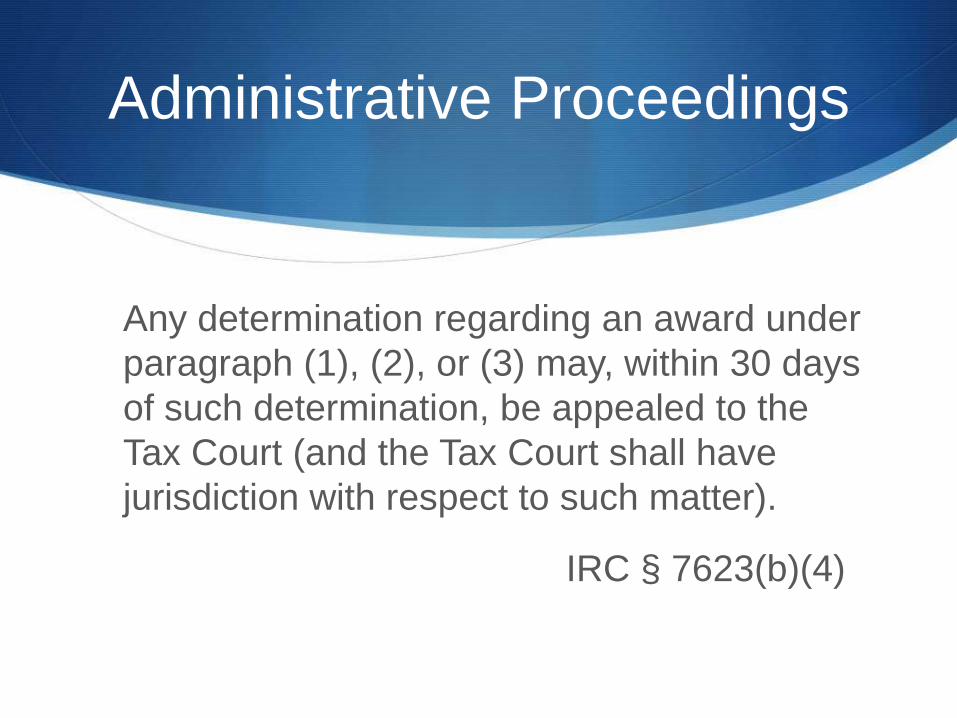

Administrative Proceedings

Any determination regarding an award under

paragraph (1), (2), or (3) may, within 30 days

of such determination, be appealed to the

Tax Court (and the Tax Court shall have

jurisdiction with respect to such matter).

IRC § 7623(b)(4)

Recent Cases

• Cooper v. Commissioner, 135

T.C. 4 (2010)

• Friedlandv. Commissioner,

T.C. Memo. 2011-90

• Cooper v. Commissioner, 136

T.C. 30 (2011)

• Kasper v. Commissioner, 137

T.C. 37 (2011)

• Friedlandv. Commissioner,

T.C. Memo. 2011-217

• Whistleblower 14106-10W v.

Commissioner, 137 T.C. 15

(2011)

• Cohen v. Commissioner, 139

T.C. 12 (2012)

• Insignav. Commissioner,

Docket 4609-12W

Cooper v. Commissioner

(Cooper I)

• Facts

• Challenge – Lack of Jurisdiction

• Issue (case of first impression) – what is a

“determination” for purposes of IRC §

7623(b)(4)?

• “we find that our jurisdiction is not limited to

the amount of an award determination but

includes any determination to deny an award.”

Friedlandv. Commissioner

(Friedland I)

• Facts

• Challenge – Lack of Jurisdiction

• Issues:

• Is a letter a “determination” under IRC § 7623(b)(4)?

• “Any determination regarding an award from the

Whistleblower Office may be appealed to the Tax Court.”

• “We held that the letter constituted a determination because it

was a final administrative decision regarding the taxpayer’s

whistleblower claims.”

• If so, is petition timely?

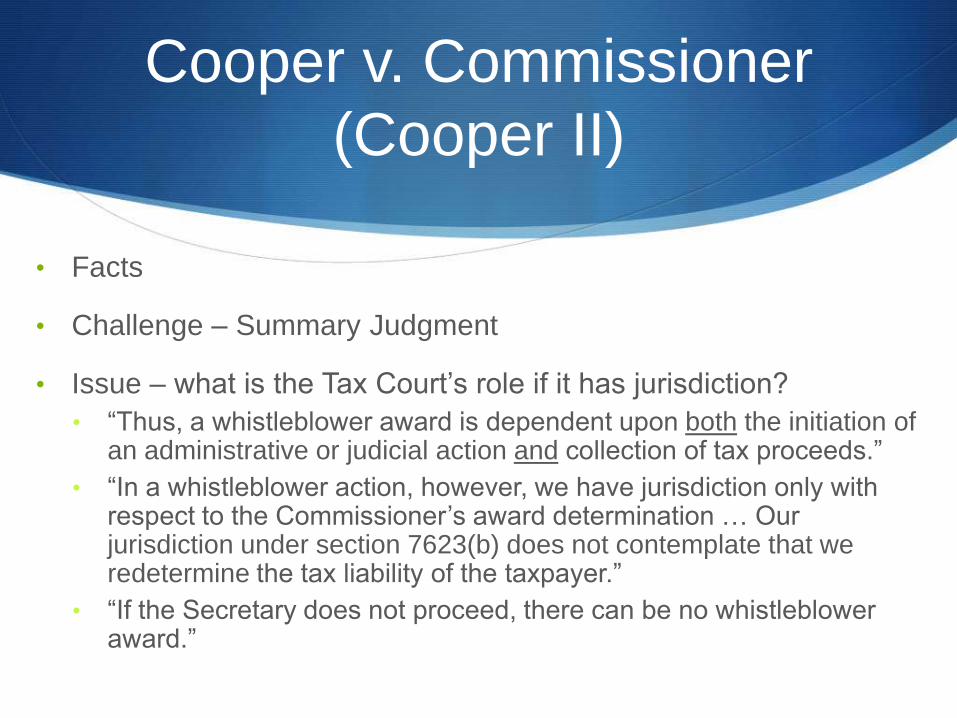

Cooper v. Commissioner

(Cooper II)

• Facts

• Challenge – Summary Judgment

• Issue – what is the Tax Court’s role if it has jurisdiction?

• “Thus, a whistleblower award is dependent upon both the initiation of an administrative or judicial action and collection of tax proceeds.”

• “In a whistleblower action, however, we have jurisdiction only with respect to the Commissioner’s award determination … Our jurisdiction under section 7623(b) does not contemplate that we redetermine the tax liability of the taxpayer.”

• “If the Secretary does not proceed, there can be no whistleblower award.”

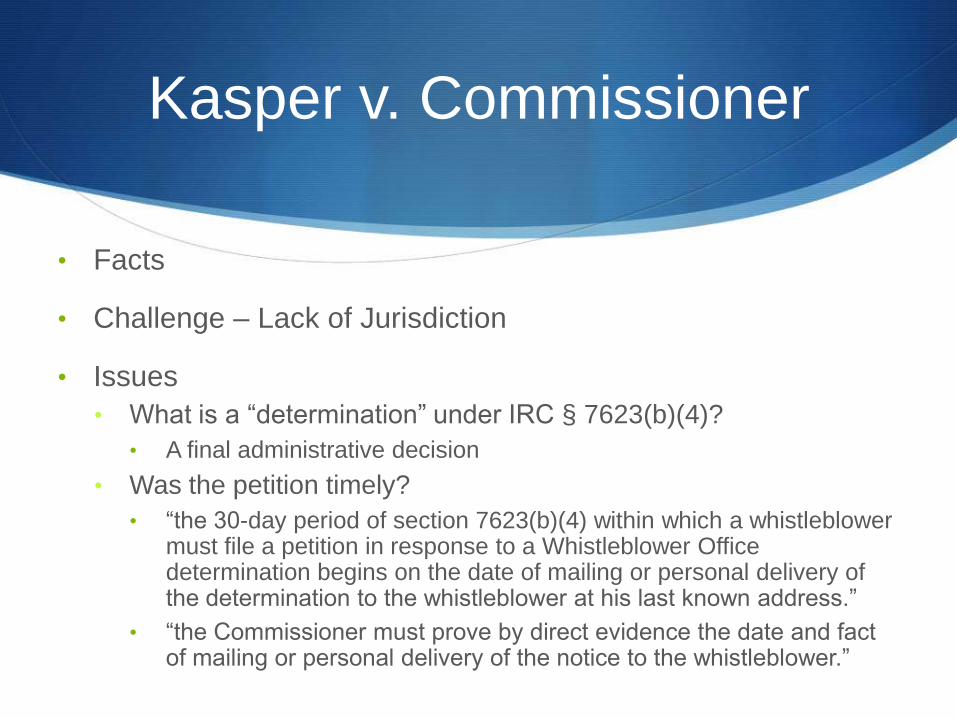

Kasper v. Commissioner

• Facts

• Challenge – Lack of Jurisdiction

• Issues

• What is a “determination” under IRC § 7623(b)(4)?

• A final administrative decision

• Was the petition timely?

• “the 30-day period of section 7623(b)(4) within which a whistleblower must file a petition in response to a Whistleblower Office determination begins on the date of mailing or personal delivery of the determination to the whistleblower at his last known address.”

• “the Commissioner must prove by direct evidence the date and fact of mailing or personal delivery of the notice to the whistleblower.”

Friedlandv. Commissioner

(Friedland II)

• Facts

• Challenge – Lack of Jurisdiction

• Issues

• Was petition timely?

• “Where a taxpayer receives actual notice without

prejudicial delay and with sufficient time to file a

petition, the Court has found that the notice is

effective.”

• If timely, does claim meet monetary thresholds?

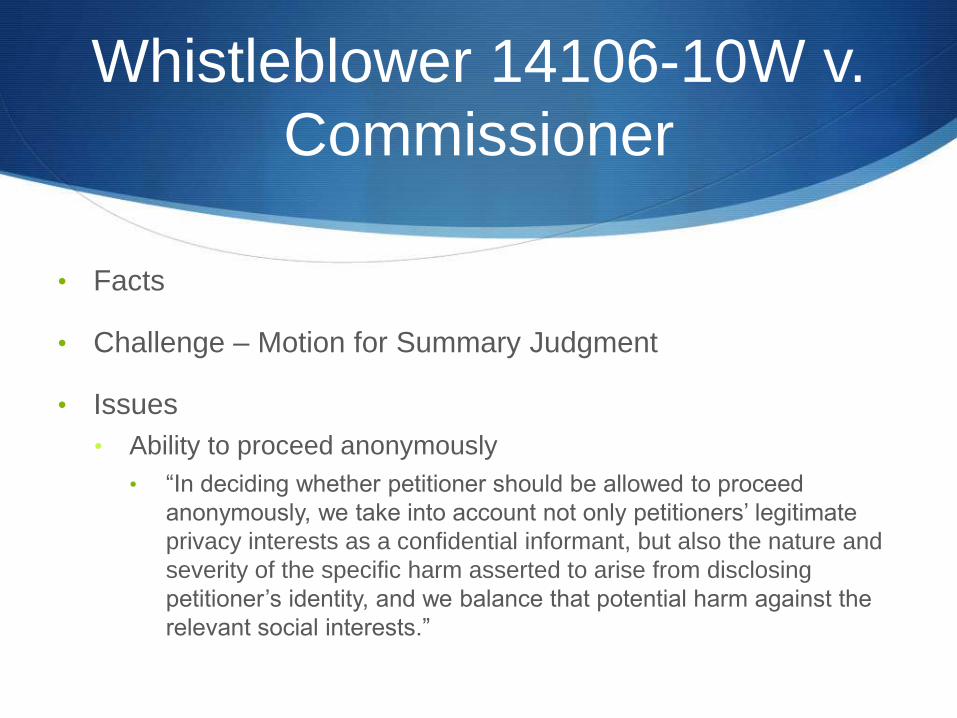

Whistleblower 14106-10W v.

Commissioner

• Facts

• Challenge – Motion for Summary Judgment

• Issues

• Ability to proceed anonymously

• “In deciding whether petitioner should be allowed to proceed

anonymously, we take into account not only petitioners’ legitimate

privacy interests as a confidential informant, but also the nature and

severity of the specific harm asserted to arise from disclosing

petitioner’s identity, and we balance that potential harm against the

relevant social interests.”

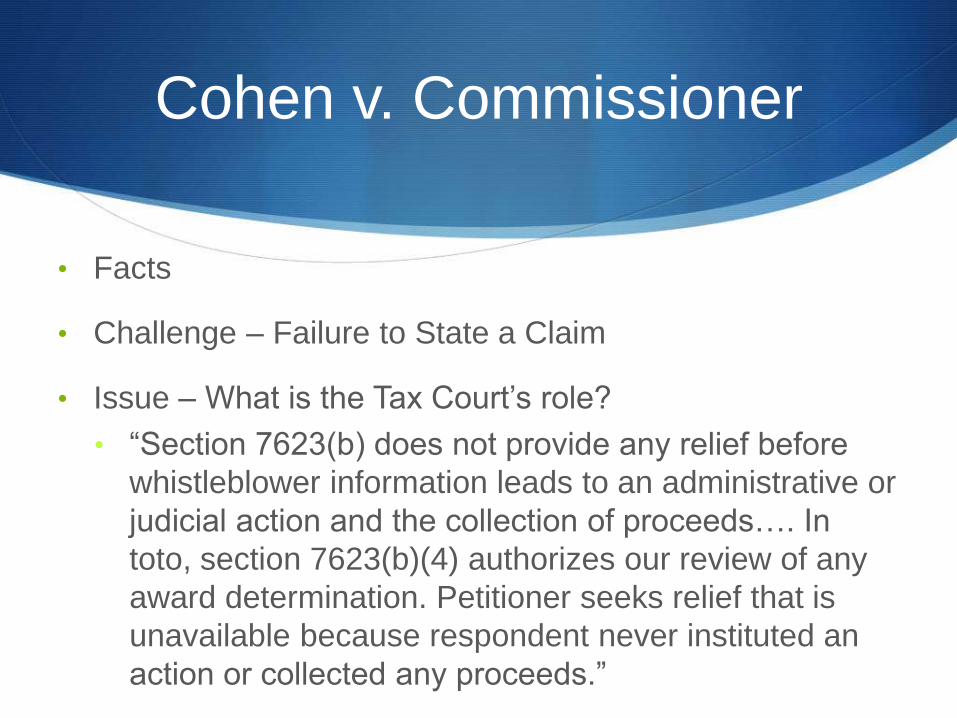

Cohen v. Commissioner

• Facts

• Challenge – Failure to State a Claim

• Issue – What is the Tax Court’s role?

• “Section 7623(b) does not provide any relief before

whistleblower information leads to an administrative or

judicial action and the collection of proceeds…. In

toto, section 7623(b)(4) authorizes our review of any

award determination. Petitioner seeks relief that is

unavailable because respondent never instituted an

action or collected any proceeds.”

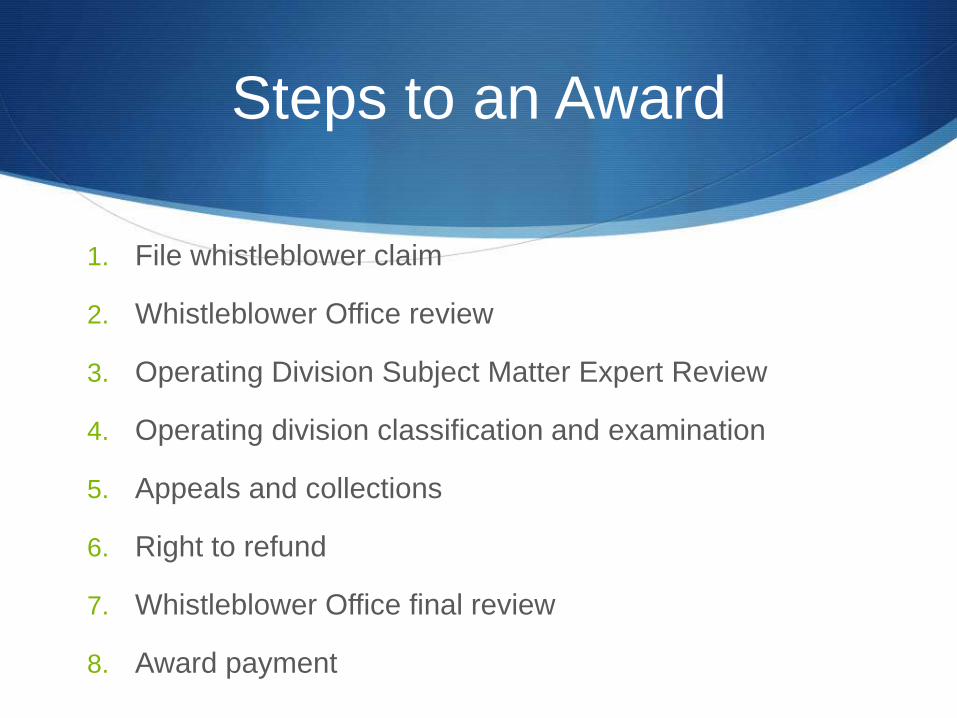

Steps to an Award

1. File whistleblower claim

2. Whistleblower Office review

3. Operating Division Subject Matter Expert Review

4. Operating division classification and examination

5. Appeals and collections

6. Right to refund

7. Whistleblower Office final review

8. Award payment

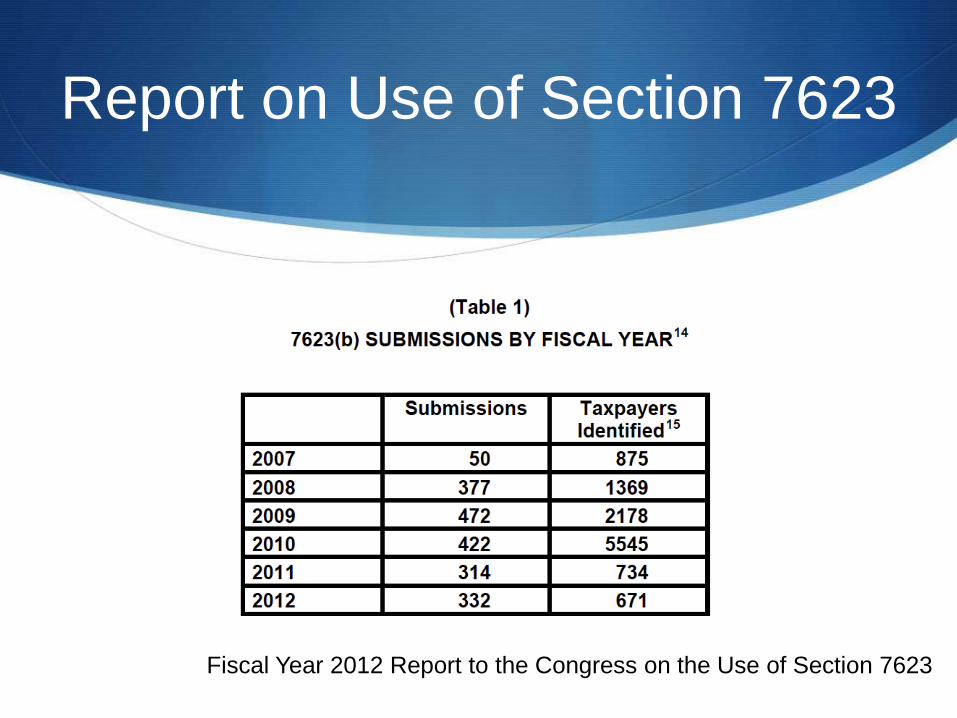

Report on Use of Section 7623

Fiscal Year 2012 Report to the Congress on the Use of Section 7623

Report on Use of Section 7623

Fiscal Year 2012 Report to the Congress on the Use of Section 7623