irvine unified school district - iusd

TRANSCRIPT

IRVINE UNIFIEDSCHOOL DISTRICT

2015-16 Adopted Budget

June 23, 2015

Agenda

2

Discussion and recommendation for approval of 2015-16 Local Control

Accountability Plan (LCAP)

Overview of 2015-16 Final State Education Budget

Discussion and recommendation for approval of IUSD 2015-16 Budget

2015-16 Budget Development Process

Estimated Local Control Funding Formula (LCFF) allocations

Detailed Budget Assumptions

2015-16 “Initial” Budget Financial Projections

Multiyear Projections

Updates to the LCAP

3

Since the June 2 public hearing, cabinet has made several minor revisions to the

Local Control Accountability Plan (LCAP):

Increased funding to support professional learning for classified

instructional staff

Up to eight hours of training beyond regular working hours

Additional administrative assistant support at the district level

.25 FTE Math and Science

.50 FTE Student Support Services

LCAP revisions to enhance readability

Renumbering of LCAP actions

Incorporating an index summarizing LCAP actions

4

Updates to the LCAP

This past May the State significantly revised its budget projections providing

IUSD with approximately $13 million of additional one-time funding and $10

million of ongoing funding. Throughout the summer of 2015, staff will continue

to plan actions to support LCAP goals and to prioritize proposed actions

received in 2014-15 from stakeholder feedback.

Planned actions for summer 2015:

Continue to build on our five focus areas

Direct Student Instructional Support

Mental Health Support

Increase School Site Funding

California Standards Aligned Materials and Support

Equity and Safety

Seek feedback from stakeholders on additional actions

Update School Board throughout summer

Overview of 2015-16

State Education Budget

5

On June 16, the Governor announced an agreement with the Legislature on a

2015-16 State Budget

The central area of contention remains the availability of additional state

revenues based on differences between the Department of Finance (DOF)

and the Legislative Analyst’s Office (LAO)

In May the Legislative Analyst’s Office (LAO) forecast state revenues of

approximately $3 billion more than the Governor’s May Revised 2015-16

State Budget Proposal

Legislative Budget Conference Committee reached a compromise with

Governor’s Administration, agreeing to stay within the limits of the

Department of Finance’s lower revenue projections

California General Fund Revenues

6

$106,000

$108,000

$110,000

$112,000

$114,000

$116,000

$118,000

$120,000

$122,000

$124,000

$126,000

2015-16 2016-17 2017-18

LAO Administration

$120.5

$113.3

$118.5

$124.4

$122.2

$116.3

State General Fund Revenues(In Billions)

Highlights of 2015-16

State Education Budget

7

The 2015-16 Final State Budget includes increases of approximately:

$100 million to augment State funded Preschool

$165 million to augment State funded Childcare

$500 million in one-time funding for a teacher effectiveness block grant

Although very few details have been provided, these allocations may reduce

the May Revise allocations for the one-time mandate reimbursement and may

reduce the LCFF allocation

2015-16 Budget Development

Process

8

On May 14, 2015, the Governor released the May Revision to his 2015-16

January Budget proposal

Due to timing constraints and in the absence of a Final State Adopted Budget,

Districts typically build Budgets based on the Governor’s May Revision

Budgets are updated throughout the year

First Interim – December

Second Interim – March

Budget assumptions are developed with guidance from:

The Orange County Department of Education (OCDE)

School Services of California (SSC)

The California Association of School Business Officials (CASBO)

A variety of other sources…

9

Recap of 2015-16 May Revise Assumptions

included in IUSD’s Budget

Over $6 billion added to 2014-15 and 2015-16 due to increases in State revenues

Additional $3.3 billion in education funding for 2013-14 and 2014-15 – treated as “one-time”Ongoing increase in Proposition 98 of $2.7 billion in 2015-16

Governor’s proposal allocates $2.4 billion of prior years “one time” revenues to the repayment of prior years mandate reimbursement, bringing the total for 2015-16 to $3.5 billion or $601/per ADA

For IUSD this represents approximately $18.4 million (increase of approximately $13 million from January State Budget Proposal)

Governor’s proposal allocates $2.1 billion of the ongoing increase to the continued implementation of the Local Control Funding Formula (LCFF)

Sufficient to eliminate approximately 53% of the remaining gap in LCFF funding statewideFor IUSD represents $28.9 million in 2015-16 “gap” LCFF funding (increase of approximately $10 million from January State Budget Proposal)

Estimated LCFF Gap Funding per

ADA

$6,702

$7,604

$7,707

$7,883

$5,600

$6,100

$6,600

$7,100

$7,600

$8,100

$8,600

2014-15 2015-16 2016-17 2017-18

Est Funding - DOF Est. Funding - SSC

53.08% of Gap$28.9M Increase 12.62% of Gap

$4.0M Increase

$8,229

29.97% of Gap$21.4M Increase

37.40% of Gap$11.8M Increase

$7,944

18.24% of Gap$6.7M Increase

36.74% of Gap$10.5M Increase

10

IUSD Estimated LCFF Funding

2015-16 thru 2017-18

IUSD LCFF2015-16

Projection

2016-17

Projection

2017-18

Projection

LCFF Target(Actual Target to be Reached in 2020-21)

$265,945,160 $282,042,200 $302,861,823

LCFF Floor(2012-13 Actual Funding Adjusted for ADA Growth &

any LCFF Funding Received)

$211,442,034 $250,468,540 $266,102,914

LCFF Gap =(Difference Between Target & Floor)

$54,503,126 $31,573,660 $36,758,909

Gap Funding Rate =(% of Gap to be Funded)

53.08% 12.62% 18.24%

Gap Funding Amount =(Anticipated Additional Funds)

$28,930,259 $3,984,596 $6,704,825

Total LCFF Funding = $240,372,293 $254,453,136 $272,807,739

11

$0

$50

$100

$150

$200

$250

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15Projected

2015-16Projected

2016-17Projected

2017-18Projected

Millions

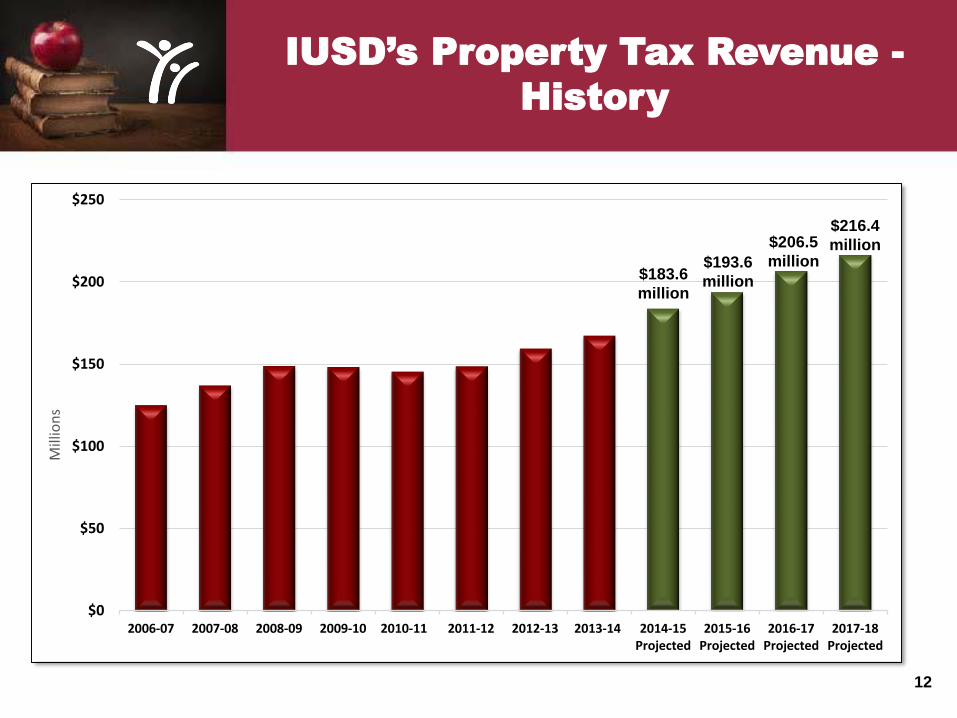

IUSD’s Property Tax Revenue -

History

$183.6

million

$193.6

million

$206.5

million

$216.4

million

12

2015-16 Revenue Budget

Assumptions

Description 2015-16 2016-17 2017-18

ADA Growth 976 1403 1592

COLA 1.02% 1.60% 2.48%

GAP Funding Rate 53.08% 12.62% 18.24%

Property Tax Growth 7% 7% 5%

RIMD Revenues $4,854,939 $4,952,038 $5,051,079

Redevelopment Revenues $750,000 $750,000 $750,000

13

2015-16 Expenditure Budget

Assumptions

Description 2015-16 2016-17 2017-18

Step and Column Increases 2% 2% 2%

Additional Teacher FTE – Growth 30 50 53

Average New Teacher Cost $75,208 $76,712 $78,246

PERS Rate 11.847% 13.050% 16.600%

STRS Rate 10.73% 12.58% 14.43%

Health Insurance Contribution $10,143 $10,143 $10,143

Workers Compensation Rate 3.00% 3.00% 3.00%

Utility Increases 5% 5% 5%

Special Education Underfunding $28,843,468 $30,073,049 $31,644,776

Deferred Maintenance Transfer $1,500,000 $0 $0

14

15

Updated Budget Prioritization Process

(Utilization of Ongoing and One-Time Resources)

April 2015

Study Session

Description $ in millions $ in millions

Ongoing Available Funding $5.1 $15.1

One-Time Available Funding

2014-15 Projected Unrestricted EFB: $28.4 $34.1

State Mandated Reserves @ 2% <$6.3> <$6.1>

Contingency Reserve (approved in 2014-15 LCAP) <$5.0> <$5.0>

2014-15 Deferred LCAP Allocation <$2.0> -------

2014-15 Site and Department Carryover <$4.0>

One-Time Available Reserves in 2015-16 $15.1 $19.0

One-Time Mandate Reimbursement $5.1 $18.4

Updated

May Revise

Updated Projections based on 2015-16 May Revise

2015-16 Expenditure Budget

Assumptions – LCAP Prioritization

Summary

DescriptionOngoing

AllocationOne-Time Allocation

2015-16 2015-16 2016-17

Summary by Major Category:

Direct Student Instructional Support: $2,190,000 $496,760

Mental Health Support: $565,457

School-Site Funding: $365,000 $610,000

Standards Aligned Materials: $307,027 $5,169,191 $3,250,000

Equity and Safety: $1,283,211 $3,903,991

Totals: $4,710,695 $10,179,942 $3,250,000

Unallocated: $10,389,305 $23,970,059

16

2015-16 Adopted Budget & Multiyear

Projected Unrestricted General Fund

Description2014-15

Estimated

2015-16

Projected

2016-17

Projected

2017-18

Projected

Total Revenues $218,091,489 $271,824,806 $268,694,412 $287,201,944

Total Expenditures ($193,274,909) ($210,346,986) ($217,803,779) ($229,012,437)

EXCESS (DEFICIENCY) $24,816,580 $61,477,820 $50,890,633 $58,189,507

Other Sources/Uses ($36,059,880) ($41,251,545) ($39,921,288) ($41,618,423)

Net Increase/(Decrease) ($11,243,300) $20,226,275 $10,969,345 $16,571,084

Beginning Balance $45,702,340 $34,459,040 $54,685,315 $65,654,660

Projected Ending Balance $34,459,040 $54,685,315 $65,654,660 $82,225,744

17

2015-16 Adopted Budget & Multiyear

Components of Ending Fund Balance

Description2014-15

Projected

2015-16

Projected

2016-17

Projected

2017-18

Projected

Estimated Ending Fund

Balance$34,459,040 $54,685,315 $65,654,660 $82,225,744

Components of Ending Fund

Balance:

Revolving Cash/Stores $525,000 $525,000 $525,000 $525,000

State Recommended

Minimum DEU$5,537,564 $5,651,945 $5,939,785 $6,023,843

Contingency Reserve $5,000,000 $5,000,000 $5,000,000 $5,000,000

Deferred LCAP Allocation $3,250,000

Site Carryover $4,000,000 $4,000,000 $4,000,000 $4,000,000

Other Assigned $19,396,476 $36,258,370 $50,189,875 $66,676,901

18

2015-16 Adopted Budget & Multiyear

Unrestricted General Fund

With Unallocated Allocations

Description2014-15

Estimated

2015-16

Projected

2016-17

Projected

2017-18

Projected

Total Revenues $218,091,489 $271,824,806 $268,694,412 $287,201,944

Total Expenditures ($193,274,909) ($210,346,986) ($217,803,779) ($229,012,437)

Currently Unallocated Ongoing ----------------- $10,389,305 $10,389,305 $10,389,305

Currently Unallocated One-Time ----------------- $27,970,059* $3,250,000

Revised Total Expenditures ($193,616,910) ($248,706,350) ($231,443,084) ($239,401,742)

EXCESS (DEFFICIENCY) $24,816,580 $23,118,456 $37,251,328 $47,800,202

Total Other Sources/Uses ($36,059,880) ($41,251,545) ($39,921,288) ($41,618,423)

NET INCREASE (DECREASE) ($11,243,300) ($18,133,089) ($2,669,960) $6,181,779

Beginning Balance $45,702,340 $34,459,040 $16,325,951 $13,655,991

Ending Balance $34,459,040 $16,325,951 $13,655,991 $19,837,770

* Unallocated amount in 2015-16 includes $4 million in site carryover from 2014-15 19

2015-16 Adopted Budget & Multiyear

Components of Ending Fund Balance

With Unallocated Allocations

Description2014-15

Projected

2015-16

Projected

2016-17

Projected

2017-18

Projected

Estimated Ending Fund

Balance$34,459,040 $16,325,951 $13,655,991 $19,837,770

Components of Ending Fund

Balance:

Revolving Cash/Stores $525,000 $525,000 $525,000 $525,000

State Recommended

Minimum DEU$5,537,564 $6,419,132* $6,212,571* $6,231,629*

Contingency Reserve $5,000,000 $5,000,000 $5,000,000 $5,000,000

Deferred LCAP Allocation $3,250,000

Site Carryover $4,000,000

Other Assigned $19,396,476 $1,131,819 $1,918,420 $8,081,141

* State minimum reserves increased due to proposed expenditure increases 20

Unknowns/Challenges

21

Proposition 30 continues to be a “temporary” tax generating approximately

$7- 8 billion in revenue annually

Recent gains in Proposition 98 have been largely driven by the repayment of

the maintenance factor

At its peak, maintenance factor reached $11.2 billion

Maintenance factor likely eliminated by 2016-17

Annual growth in Proposition 98 likely reduced to 2% - 4%

CalPERS and CalSTRS increases

LCFF was intended to restore 2007-08 purchasing power by 2020-21

By full implementation $4.5 billion in pension cost increases funded by

districts out of LCFF…..

Increasing pressure to increase funding for non-Proposition 98 programs

Questions/Discussion

22