is it ifrs adoption or convergence to ifrs that matters? tija symposium 2012 2/1/12 is it ifrs...

TRANSCRIPT

060 TIJA Symposium 2012

2/1/12

Is it IFRS Adoption or Convergence to IFRS that Matters?

Lei Cai

Asheq Rahman

Stephen Courtenay

School of Accountancy

Massey University

Auckland

New Zealand

Draft Date: 31 Jan 2012

1

060 TIJA Symposium 2012

2/1/12

Is it IFRS Adoption or Convergence to IFRS that Matters?

Abstract

Prior Studies find that International Financial Reporting Standards (IFRS) adoption improves

earnings quality. Some studies also introduce enforcement variables to show the added

benefits of enforcement. However, we note that some of the countries that have adopted IFRS

had accounting standards similar to IFRS prior to adopting IFRS while others had accounting

standards less similar to IFRS. We contend that the latter group benefit more from IFRS

adoption because their accounting standards undergo greater improvements. We examine the

effect of IFRS adoption by taking into account the prior dissimilarities a country’s accounting

standards had with IFRS. We use data from 31 countries and we take into account the effects

of legal enforcement. We find that when IFRS is adopted or when accounting standards are

more similar to IFRS, countries have lower levels of earnings management. Also, countries

with accounting standards less similar to IFRS prior to IFRS adoption have a greater drop in

earnings management after IFRS adoption. Our results support the contention that countries

with lower quality accounting standards would benefit more from IFRS adoption.

2

060 TIJA Symposium 2012

2/1/12

1. Introduction

Many countries have begun mandatory adoption of International Financial Reporting

Standards (IFRS) issued by the International Accounting Standards Board (IASB). IFRS

removes many allowable accounting alternatives, and some initial evidences show that IFRS

limit managerial discretion to manipulate earnings, thereby improving earnings quality.

Research investigating the usefulness of IFRS adoption has shown that countries that adopt

IFRS have lower earnings management (Jeanjean and Stolowy, 2008; Callao and Jarne 2010;

Hoque et al. 2012). We contend that the term ‘adoption’ does not to carry the same meaning

across countries because the effect of adoption is formed by a country’s distinctive regulatory,

capital market, accounting, and auditing features. This has been partially studied by recent

studies through an examination of the effects of enforcement on the adoption of IFRS

(Jeanjean and Stolowy, 2008; Hoque et al. 2012). These studies, however, do not take into

consideration the fact that some of the IFRS adopting countries already had accounting

standards similar to IFRS prior to adopting IFRS. We contend that the benefit of IFRS

adoption is reaped more by countries whose accounting standards are less similar to IFRS.

We examine the effect of IFRS adoption by taking into account the prior dissimilarities a

country’s accounting standards had with IFRS. We take into account the effects of legal

enforcement as recent studies have done. We also find that when IFRS is adopted or when

accounting standards are more similar to IFRS, countries have lower levels of earnings

management. Also, countries with standards less similar to IFRS prior to IFRS adoption have

a greater reduction in earnings management after IFRS adoption. Our results support the

contention that countries, in general, benefit from IFRS adoption, and countries that achieve

greater ‘convergence’ to IFRS by adopting IFRS benefit more than those countries that

already had accounting standards similar to IFRS. However, in this milieu, while we find

legal enforcement to be a significant player in reducing earnings management, its influence

on enhancing the effects of IFRS on earnings management reduction is not consistently

significant. The likely cause of this is that countries that had standards dissimilar to IFRS had

weaker legal enforcement arrangements. Therefore, their reduction in their earnings

management is primarily due to IFRS adoption and less due to the legal enforcement

arrangements complementing IFRS.

A strength of our study is that we have been able to study the effects of IFRS adoption more

effectively. Previous studies (Jeanjean and Stolowy, 2008; Hoque et al, 2012) were unable to

3

060 TIJA Symposium 2012

2/1/12

obtain data for large-sample tests because their studies were conducted too soon after IFRS

adoption by their sample countries. Regulations take years to unfold and take effect. As

mandatory IFRS adoption has been use for some years in many countries, it is now possible

to empirically test how IFRS plays a role in establishing earnings quality. In this regard, we

note that the effects of IFRS adoption take about three to four years to take effect.

Our sample covers data from 2000 to 2009 across 31 countries. We use the theory

frameworks of Soderstrom and Sun (2007), Leuz et al. (2003), and Hope (2003). Our results

show that firm reporting incentives are shaped by the institutional environments of countries

(Ball et al., 2000; Hope, 2003; Bhattacharya et al. 2003; Beneish and Yohn, 2008; Jeanjean

and Stolowy, 2008), and IFRS has the strongest effect on earnings quality when

‘convergence’ is large due to IFRS adoption.

Our paper contributes to the accounting literature in three ways. First, most IFRS adoption

papers (Callao and Jarne, 2010; Houqe et al. 2011) do not consider the differences between

local GAAP and IFRS. Simply coding IFRS adoption as an indicator variable to measure the

quality of accounting standards is not sufficient because it does not capture how much IFRS

adoption affects the state of accounting policies in a country. In this paper, we capture the

degree of variation in GAAP differences to get a better measurement of IFRS adoption.

Second, previous studies only provide preliminary evidence on the effect of IFRS adoption

because their data cover only one or two years after mandatory adoption of IFRS, or cover

fewer countries. We use a large sample that covers data up to five years after mandatory

adoption of IFRS. Third, our study focuses on the issue of which countries benefit more from

IFRS adoption. Currently, much attention is being placed on the convergence between IFRS

and the US accounting standards. The question that arises from this focus is whether this

should be the main direction of the IASB’s efforts or should the IASB provide more attention

to those countries that need assistance in improving the quality of their accounting standards?

The remainder of the paper is organized as follows. Section 2 provides the literature review

and leads to the hypothesis. Section 3 describes the research design, including the measures

for the dependent, independent, and control variables, the model specifications, and the

sample selection process. Section 4 presents the descriptive statistics and empirical analysis.

Finally, the conclusion of this study is drawn in Section 5.

4

060 TIJA Symposium 2012

2/1/12

2. Literature review and hypotheses development

Adopting a common set of high quality accounting standards can improve earnings quality

through the ease of monitoring and comparison of financial reports across borders, which

puts pressure on management to report faithfully and truthfully and engage less in earnings

management activities (Soderstrom and Sun 2007). Daske and Gebhardt (2006) find

significant increases in disclosure quality under IFRS in three European countries (namely,

Austria, Germany, and Switzerland) scored by independent academic accounting scholars.

Using a sample in 21 countries, Barth, Landsman, and Lang (2008) show that international

accounting standards (IAS) adopting firms have less earnings management, more timely loss

recognition, and more value relevant earnings than non-adopting firms in post-adoption

period. They suggest that adopting IAS improves accounting quality and potentially reduces

the cost of equity capital. More recently, Chen et al. (2010) find that accounting quality has

marginally improved after IFRS adoption in the 15 European Union countries. They suggest

that the improvement in accounting quality is due to IFRS restricting alternative accounting

choices, reducing the ambiguity in local standards, and changing the managerial incentives.

In contrast, opponents argue that adopting high quality accounting standards per se does not

necessarily improve accounting quality. For example, Ball, Robin, and Wu (2003) find that

the accounting quality is low in four Asian countries/regions (Hong Kong, Malaysia,

Singapore, and Thailand), even though their accounting standards are derived from common

law countries. Lin and Paananen (2006) examine changes in the patterns of earnings

management activities over time, and suggest that IASB has not been effective in decreasing

overall earnings management activities. Callao and Jarne (2010) compare discretionary

accruals in periods preceding and immediately after IFRS adoption for firms listed on 11

European stock markets. Their findings suggest that IFRS encourages discretionary

accounting and opportunistic behaviour.

Besides accounting standards, accounting quality is also determined by a country’s overall

institutional system and firms’ incentives for financial reporting (Ball et al., 2000; Ball et al.,

2003; Boonlert-U-Thai, Meek, and Nabar, 2006; Jeanjean and Stolowy, 2008). Leuz et al.

(2003) use cluster analysis with La Porta et al’s (1998) nine institutional variables to identify

systematic differences in earnings management across 31 countries. They report lower

earnings management in countries with stronger investor protection, since strong protection

limits insiders’ ability to acquire private control benefits, and reduces their incentives to mask

5

060 TIJA Symposium 2012

2/1/12

firm performance. Similarly, Burgstahler, Hail, and Leuz (2006) examine the relation

between earnings management and the interaction among ownership structure, capital market

structure and development, the tax system, accounting standards, and investor protection.

They document that strong legal systems are associated with lower earnings management.

Boonlert-U-Thai et al. (2006) explore the effects of investor protection on reported earnings

quality, and find that earning smoothness is less prevalent in strong investor protection

countries. Ding, et al. (2007) examine how a country’s legal system, economic development,

importance of stock markets, and ownership concentration shape the country’s accounting

standards, which in turn affect the country’s quality of financial reporting. Soderstrom and

Sun (2007) argue that cross-country differences in accounting quality are likely to remain

following IFRS adoption, because accounting quality is a function of the institutional setting

in which firms operate. Although conversion to IFRS is likely to improve earnings quality, it

is only one of several determinants. Even after mandatory IFRS adoption, country-level

institutional variables continue to vary across countries.

Many researchers argue that the enforcement of accounting standards is as important as the

accounting standards (e.g. Shleifer and Vishny, 1997). “Strong IFRS enforcement puts

pressure on management and auditors to act faithfully and truthfully to comply with the

standards, and contributes to comparability of financial statements across countries” (FEE,

2002, 29). Enforcement of standards also helps investors perceive that financial reports

reflect a firm’s fundamentals, which can increase the relevance of the accounting information.

Ewert and Wagenhofer (2005) find that tightening enforcement of accounting standards

reduces earnings management and improves reporting quality.

Ball et al. (2003) and Holthausen (2003) predict that IFRS adoption by countries with weak

enforcement mechanisms will lead to lower perceived quality of the standards, and suggests

that it would be useful for the literature to begin to structure and quantify the country

descriptions by developing more informative tests. Similarly, Leuz et al. (2003) and Beneish

and Yohn (2008) argue that countries with strong outsider1 protection are expected to enact

and enforce accounting and securities laws that limit the manipulation of accounting

information. Jeanjean and Stolowy (2008) provide early evidence of the importance of the

institutional environment in reducing earnings management after IFRS adoption. They find

that earnings management did not decline in Australia and the UK after the introduction of 1 Outsiders are distinguished from those insiders such as managers and controlling shareholders, who have

incentives to conceal their private control benefits from outsiders (See Leuz et al. 2003).

6

060 TIJA Symposium 2012

2/1/12

IFRS, and in fact increased in France. In a pre-IFRS setting Hope (2003) had found that

accounting standards enforcement is needed to encourage or forces managers to follow the

rules. In a more recent study, Hoque et al (2012) find that legal enforcement (a proxy for

accounting enforcement) had a positive influence on the effects of IFRS adoption on the

reduction of earnings management.

The studies on the influence of IFRS adoption and enforcement often simply assume that all

countries adopting IFRS will benefit from IFRS adoption and that enforcement along with

IFRS adoption will provide further accounting quality improvements. These studies do not

take into account that among the countries that have adopted IFRS there is a large proportion

that already had accounting standards similar to IFRS and had strong enforcement

arrangements, in particular, with regards to securities law disclosure requirements and

auditing. We contend that countries that had accounting standards divergent2 from IFRS are

likely to have more significant effects from the adoption of IFRS. Also, countries that have

not adopted IFRS but have standards relatively similar to IFRS will enjoy lower levels of

earnings management. In this respect, two countries, USA and Canada, stand out. These two

countries have more extensive standards than IFRS. Likewise, we hypothesize that

H1 Earnings management is negatively associated with IFRS adoption and greater

convergence of local standards to IFRS.

As discussed above, legal enforcement arrangements are likely to have a direct positive

influence on earnings quality. Legal enforcement is also likely to enhance the influence of

IFRS and convergence to IFRS. Therefore, we hypothesise that

H2 Earnings management is negatively associated with legal enforcement.

H3 The stronger the legal enforcement the greater will be the influence of IFRS adoption and

convergence of local standards to IFRS on the reduction of earnings management.

IFRS adoption is not simply the replacement of local accounting standards. Most countries

that have adopted IFRS have also enhanced their securities laws and auditing requirements.

For example, to adopt IFRS, EU countries, Australia, New Zealand, and Singapore are

providing legislative support to accounting standards and adopting better auditing standards.

2 Of lower quality as the proponents of IFRS suggest.

7

060 TIJA Symposium 2012

2/1/12

Because of better accounting standards and better enforcement support, we predict that

countries that had standards that were less convergent with IFRS are likely to experience

higher reduction in earnings management. Therefore, we hypothesize that:

H4 For IFRS adoption countries, the reduction of earnings management is higher for those

countries that had local standards less convergent to IFRS prior to IFRS adoption.

3. Research design

3.1. Dependent variable: earnings management

We use earnings management as the dependent variable to represent accounting quality that is

particularly responsive to reporting incentives (Burgstahler et al., 2006). Following Leuz et al.

(2003)3 we use two country-level measures of earnings management to capture the two

different dimensions along which insiders exercise the discretion to manipulate earnings,

namely, 1) the variation of accruals, and 2) the magnitude of accruals. The first captures the

degree of earnings smoothing, while the second measures the managerial discretion in

reported earnings. The measures are further explained below:

1) Smoothing measure: the variation of accruals

Earnings smoothing is defined as “an attempt on the part of the firm’s management to reduce

abnormal variations in earnings to the extent allowed under sound accounting and

management principles” (Beidleman, 1973, 653). To capture the degree of earnings

smoothing, the first earnings management measure (EM1) in formula (1) is a country’s

median ratio4 of the firm-level standard deviation of operating earnings divided by the

firm-level standard deviation of cash flow from operations. The scaling by cash flow from

operations controls for differences in the variability of economic performance across firms. A

low value indicates that management exercises accounting discretion to smooth reported

earnings.

3 Leuz et al. (2003) use two measures: the correlation between changes in accounting accruals and operating

cash flows, and the small loss avoidance. We find that these two measures are not suitable for our study, because

one year’s change in accruals may relate to changes in operating cash flows in several subsequent years, and the

small loss avoidance cannot be used for a country in a given year that has a small number of firms in the sample.

These two measures only suit the analysis when pooling the firm-level data in a relatively long time period, and

with a large sample size. We test the correlation between the aggregate earnings management score calculated

by Leuz et al.’s (2003) four measures and the aggregate score based on our two measures, and find a positive

Spearman’s correlation (p<0.01). 4 We use the median ratio to allow direct firm size comparisons across countries, and to avoid extreme values.

8

060 TIJA Symposium 2012

2/1/12

EM1 = Median (StdDev (Operating Income) / StdDev (Cash Flow from Operations)) (1)

Cash flow from operations is computed by subtracting the accruals from operating income

because cash flow information of firms is not available in some countries, especially prior to

2001, as in formula (2):

Cash Flow from Operations = Operating Income – Accruals (2)

Following Dechow, Sloan, and Sweeney (1995) accruals are calculated as in formula (3):

Accrualsit = (ΔCAit – ΔCashit) – (ΔCLit - ΔSTDit - ΔTPit) – Depit (3)

Where:

ΔCAit = change in total current assets,

ΔCashit = change in cash & short-term investments;

ΔCLit = change in total current liabilities,

ΔSTDit = change in short-term debt included in current liabilities,

ΔTPit = change in income taxes payable, and

Depit = depreciation and amortization expense, for firm i in year t.

2) Discretion measure: the magnitude of accruals

The second earnings management measure (EM2) captures the magnitude of accruals. It is

used as a proxy for management discretion in reported earnings. It is computed as a country’s

median ratio of the absolute value of firms’ accruals divided by the absolute value of firms’

cash flows from operations in a fiscal year. A larger value is interpreted as higher earnings

management.

EM2 = Median (|Accruals|/|Cash Flow from Operations|) (4)

Finally, to reduce measurement error, we combine EM1 and EM2 into an aggregate earnings

management measure (EM12)5. High values of EM12 suggest high levels of earnings

management.

5 This aggregate measure is positively and significantly correlated with the component extracted from a

principal component analysis of EM1 and EM2 (not tabulated).

9

060 TIJA Symposium 2012

2/1/12

EM12 = (- 1) * EM1 + EM2 (5)

We reverse the direction of EM1 by multiplying it by -1, to make higher values represent

higher earnings management.

[Insert Table 1 here]

3.2. Independent variables: accounting standards and enforcement

3.2.1. Accounting standards

To measure the extent of IFRS adoption, we include Bae, Tan, and Welker’s (2008)6

summary score of difference between local GAAP and IFRS (GAAPDiff) to indicate how

each country’s local accounting standards differ from IFRS. This measure ranges from 0 to 21,

with higher values for more discrepancies between each country’s local GAAP and IFRS.

We use a dummy variable for mandatory IFRS adoption. ‘Mandatory adoption’ takes the

value of 1 for a given country in years ending on or after the mandatory IFRS adoption year,

and 0 otherwise (see Table 4 for mandatory adoption Year).

Alternatively, by considering the effect of discrepancy of accounting standards and IFRS

adoption together, we create a variable by multiplying GAAPDiff and a non-adoption dummy.

The non-adoption dummy variable takes the value of 1 for non-adoption countries or for

countries in years prior to mandatory IFRS adoption and 0 for otherwise. For example, high

values stand for more discrepancies between local GAAP and IFRS for non-adoption

countries or for adoption countries in pre-IFRS periods, while 0 indicates the countries in

years after mandatory IFRS adoption or the countries have 0 score of GAAPDiff (such as

Singapore and South Africa).

3.2.2. Enforcement

Ball et al. (2003) and Soderstrom and Sun (2007) argue that accounting standards alone do

not determine the quality of financial reporting. Country-level enforcement factors are likely

to have a powerful influence on earnings management, especially after mandatory IFRS

6 Bae et al. (2008) develop two measures of differences in accounting standards for 1,176 country pairs based

on an international survey of generally accepted accounting principles in 2001. We use their first measure that

involves identifying a list of 21 important accounting rules.

10

060 TIJA Symposium 2012

2/1/12

adoption. However, the enforcement of accounting standards is difficult to measure and

quantify, as it takes different forms in different countries. To develop a good measure of

enforcement, we start from the following definitions:

“Enforcement” is defined by the European Federation of Accountants (FEE) as “...a system to

whenever possible prevent, and hereafter identify and correct, material errors or omissions in

the application of IFRS in financial information and other regulatory statements issued to the

public...” (FEE, 2002, 31). The Committee of European Securities Regulators (CESR)

defines “enforcement” as “...the combination of supervision and sanctioning in cases of

non-compliance with the rules...” (FEE, 2002, 31).

An enforcement system for accounting standards has internal and external effects. Internally,

IFRS are enforced by accountants through preparing the financial reports, internal auditors

through internal audits, and audit committee/board/AGM through corporate governance.

Externally, IFRS are enforced by external auditors, national IFRS enforcement bodies,

financial market regulators and the press. An efficient and effective enforcement has six

aspects: 1) self-enforcement through the preparation of financial statements; 2) a statutory

audit of financial statements; 3) approval of financial statements; 4) an institutional oversight

system; 5) litigation and legal sanctions; and 6) public and press reactions (FEE, 2001). FEE

(2001) argues that large differences in legal environments can explain part of the differences

in enforcement mechanisms, which relate to the institutional oversight systems. Further, FEE

(2001) observes that the enforcement of accounting standards differs significantly across

countries, and is even nonexistent in some countries.

The above statements indicate that the country-level measure of enforcement can be based on

legal factors and the institutional oversight system. To capture these factors, we slightly

modify Hope’s (2003) comprehensive measure of enforcement7 by using four country-level

factors: 1) insider trading laws, 2) judicial efficiency, 3) rule of law, and 4) shareholder

protection. First, we aggregate these four measures by assigning equal weights to each

variable. We also conduct a principal component analysis to avoid the problem of

multicollinearity.

7 We exclude audit spending in Hope’s (2003) measure for two reasons. First, Hope (2003, 242) realizes that

audit spending is not a perfect measure of the audit quality, as it covers only the top 10 audit firms. Second,

although audit spending contributes to part of the country-level enforcement, including it or not does not affect

the result of analysis.

11

060 TIJA Symposium 2012

2/1/12

The first element of enforcement, insider trading laws, may deter insiders from manipulating

earnings to profit from trading in the firm’s stock (Hope, 2003). Beneish and Vargus (2002)

show that insider trading is associated with earnings management. Aboody, Hughes, and Liu

(2005) find that privately informed traders earn greater profits when trading stocks with high

earnings quality risk factors. In our study, we use the aggregate insider trading law index

developed by Beny (2005), which equals the sum of sections of the statute as follows: (1)

tipping, (2) tippee, (3) damages, and (4) criminal or the sum of scope and sanction. It ranges

from 0 to 4, with 0 indicating the least restrictive insider trading legal regime and 4 indicating

the most restrictive insider trading legal regime.

The second and third elements, judicial efficiency and rule of law, are from La Porta et al.

(1998). Judicial efficiency indicates the efficiency and integrity of the legal environment as it

affects business, while rule of law assesses a country’s law and order tradition. As explained

by Hope (2003), although a country’s judicial system might be functioning well without

enforcement of accounting standards, generally standards enforcement is strongly associated

with a strong judicial system, and accounting regulations tend to be effective in countries

with strict rules of law. Both judicial efficiency and rule of law range from 0 to 10, with

lower scores for less efficiency and less tradition for law and order.

The inclusion of the above legal variables8 is consistent with Schipper’s (2005) argument

that enforcement power resides in the security exchanges and courts where firms are listed.

However, because the security exchanges in most IFRS adoption countries require audit

reports compliant with IFRS or have similar requirements such as compliance with “IFRS as

adopted by EU”, “NZ FRS”, or “Hong Kong FRS” (Deloitte’s IAS Plus Website, 2011), we

do not code this basic requirement into the measure of a country’s IFRS enforcement

mechanisms.

Finally, Hung (2001), Ball et al. (2000), and Leuz et al. (2003) infer that countries with strong

shareholder protection are expected to enact and enforce accounting rules and securities laws

that limit earnings manipulation. Thus, in weak shareholder protection environments,

managers are more likely to violate accounting standards to manipulate earnings. Hence, we

use La Porta et al.’s (1998) anti-director rights index as the fourth enforcement variable. It is

8 The four legal variables represent the legal and political system factors identified by Soderstrom and Sun

(2007). Even though accounting enforcement is conceptually different to legal enforcement, they are strongly

connected.

12

060 TIJA Symposium 2012

2/1/12

an aggregate measure of minority shareholder rights, ranging from 0 to 6, where 0 (6)

indicates the weakest (strongest) investor protection.

3.3. Control variables

To isolate the relation between earnings management, IFRS adoption and enforcement

mechanisms, we control for other country-level institutional factors such as ownership

structure, financial market development, capital structure and tax system identified by

Soderstrom and Sun (2007). These factors also affect the quality of financial reporting.

Rahman, Yammeesri, and Perera (2010) show that institutional variables such as ownership

structure, nature of debt, and regulations vary systematically between countries affecting the

levels of accruals based earnings quality.

3.3.1. Ownership structure

We control for ownership structure by using an ownership concentration measure. La Porta et

al. (1998) show that firms in countries with concentrated ownership have less demand for

financial reporting and more earnings management. Soderstrom and Sun (2007) provide that

controlling shareholders have incentives to smooth earnings, as they not only have access to

inside information, but also have incentives to hide their exploitation of the wealth of

minority shareholders. Both theory (Shleifer and Wolfenzon, 2002) and prior evidence (La

Porta et al., 1998; La Porta, Lopez-De-Silanes, Shleifer, and Vishny, 1999) show that

ownership concentration is lower in countries with better investor protection. Leuz et al.

(2003) find that firms in countries with relatively dispersed ownership, strong investor

protection and large stock markets exhibit lower levels of earnings management than

countries with relatively concentrated ownership, weak investor protection, and less

developed stock markets.

3.3.2. Financial market development

We control for financial market development because the demand for financial information

from market participants may provide incentives for firms to improve the quality of financial

reporting. Many (e.g., Leuz et al., 2003; Burgstahler et al., 2006; Djankov, La Porta,

Lopez-de-Silanes, and Shleifer, 2008) find that firms in countries with large and highly

developed equity markets engage in less earnings management, as financial markets can

13

060 TIJA Symposium 2012

2/1/12

screen out firms with less informative earnings. We use market liquidity9 as our market

development variable because Levine and Zervos (1998) and Atje and Jovanovic (1993) find

that market liquidity is positively associated with economic growth, and Huddart, Hughes,

and Brunnermeier (1999) find that high liquidity lowers the costs of capital, motivating firms

to make earnings more informative.

3.3.3. Capital structure

Capital structure can affect the level of earnings management in two ways. First, an important

incentive for earnings management is to reduce the likelihood of violating debt covenants

(Healy and Wahlen, 1999). In theory, when firms have more debt, managers have more

incentives to engage in earnings manipulation to maintain the contractual covenants (Watts

and Zimmerman, 1978). Ali and Hwang (2000) and Soderstrom and Sun (2007) argue that

banks demand less financial reporting than do shareholders because banks have private

access to firm management.

Incentives to manage earnings also exist in countries with high levels of equity finance. For

example, the presence of bonuses and executive stock options can motivate managers to

enhance accruals to increase accounting earnings. However, this is countered by better

investor protection arrangements in such countries.

In contrast, firms in countries with more public debt tend to have less earnings management,

because creditors such as bond holders have more monitoring power, especially in countries

with high creditor protection.

We use a country’s median ratio of total long-term debt and total assets (LT Debt / TA) as the

proxy of the capital structure (bank debt is not available in Global Vantage) where total

long-term debt in Global Vantage represents all interest-bearing obligations due after the

current operating cycle.

3.3.4. Tax system

In countries with close conformity between tax and financial accounting rules, firms are

likely to choose conservative accounting methods to keep earnings down. However, some

9 We also use stock market capitalization as the market development variable and have similar results (not

reported).

14

060 TIJA Symposium 2012

2/1/12

studies find that firms in countries with high tax-book conformity along with high tax rates

have less scope to decrease earnings (Guenther and Young, 2000; Burgstahler et al., 2006).

While it is unclear what effect taxation has on earnings management, we feel that it is

important to control for the effect of taxation as an additional influence on accounting

practice. High tax rates increase the incentive to reduce taxable earnings and hide profits in

financial reporting (Soderstrom and Sun, 2007). Since the actual tax rates are not easy to

compare across countries, we use a country’s median ratio of total income taxes to total assets

(Total taxes / TA) obtained from Global Vantage database to reflect the tax burden of the

country.

3.4 Regression models

We employ the following models to test our hypothesis that earnings management is

negatively associated with IFRS adoption and stronger legal enforcement. In Models (1) to

(6), we test the effects of mandatory adoption by using a mandatory adoption dummy

variable and GAAPDiff separately, with the alternative measure of IFRS adoption

(GAAPDiff_NA) tested in models (7) and (8). In model (8), we use Generalized Linear

Model (GLM) for the interactions between GAAPDiff_NA and the principal components of

legal enforcement.

Model (1) – (6):

EM12 = β0+ β1GAAPDiff + β2 Mandatory Adoption + β3 Legal Enforcement + β4 Ownership Concentration + β5

Market Liquidity + β6LT Debt/TA + β7TotalTaxes/TA + Year Dummies + ε

Model (7):

EM12 = β0+ β1GAAPDiff_NA + β2Enforcement_PC1 + β3Enforcement_PC2 + β4Enforcement_PC3 + β5

Ownership Concentration + β6 Market Liquidity + β7LT Debt/TA + β8TotalTaxes/TA + Year Dummies +

ε

Model (8):

EM12 = β0+ β1GAAPDiff_NA + β2Enforcement_PC1 + β3GAAPDiff_NA*Enforcement_PC1 +

β4Enforcement_PC2 + β5GAAPDiff_NA*Enforcement_PC2 + β6Enforcement_PC3 +

β7GAAPDiff_NA*Enforcement_PC3 + β8 Ownership Concentration + β9 Market Liquidity + β10LT

Debt/TA + β11TotalTaxes/TA + Year Dummies + ε

Where EM12 is the aggregate score that is equal to magnitude of accruals (EM2) minus

smoothing (EM1). GAAPDiff is the summary score of how domestic GAAP differs from IAS

15

060 TIJA Symposium 2012

2/1/12

on 21 key accounting dimensions; Mandatory Adoption is a dummy that takes 1 for the

period after mandatory adoption and 0 otherwise; GAAPDiff_NA is a combined measure for

the effect of both mandatory IFRS adoption and the differences of accounting standards, by

multiplying GAAPDiff and a non-adoption dummy10

, high values stand for more

discrepancies between local GAAP and IFRS, and 0 indicates no difference between

domestic GAAP and IFRS, or the countries have already mandatorily adopted IFRS; The

legal enforcement variables are introduced one at a time in model (1) to (4), the aggregate

enforcement measure is used in model (5), and the principal components are employed in

model (7); Ownership Concentration is measured as the median percentage of common

shares owned by the top 3 shareholders in the ten largest privately owned non-financial firms

in a given country; Market Liquidity is the total value of market trading as a percentage of the

country's GDP; LT Debt/TA is the country's median ratio of total long-term debt and total

assets; Total Taxes/TA is the country's median ratio of total income taxes and total assets.

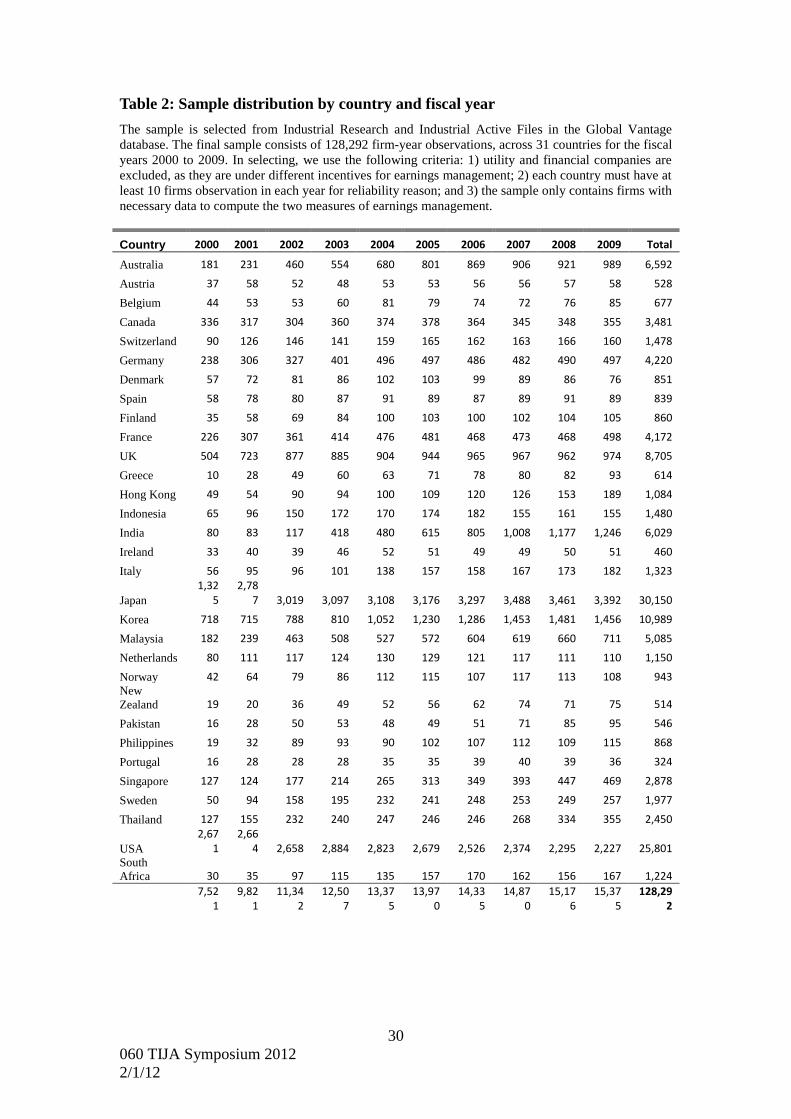

3.5. Sample selection

The sample is obtained from the Global Vantage: Industrial Research and Industrial Active

datasets. Following previous research (Leuz et al. 2003; Lin and Paananen, 2006), we

exclude financial service firms such as banks and financial institutions because it is difficult

and problematic to compute their discretionary accruals. We also exclude utility companies

because they are regulated and have different incentives to manage earnings from companies

in unregulated industries. To ensure sufficient observations in any given country and year for

computing EM1 and EM2, each country must have at least 10 firm observations in each year.

We also exclude firm-year observations with missing financial data that is necessary for

computing EM1 and EM2. For example, because EM1 requires calculation of the standard

deviation of operating earnings and standard deviation of cash flow, each firm must have

income statement and balance sheet information for at least five consecutive years. We obtain

data from 1996 for computing the consecutive five-yearly standard deviations of EM1 in year

2000. To extend the work of Leuz et al. (2003), the sample period for the analyses is from

2000 to 2009.

Table 2 shows the sample distribution by country and fiscal year. The final sample consists of

128,292 firm-year observations, across 31 countries for the fiscal years 2000 to 2009.

10

The non-adoption dummy is simply one less adoption dummy, representing the non-adoption countries and

adoption countries in years prior to mandatory IFRS adoption.

16

060 TIJA Symposium 2012

2/1/12

[Insert Table 2 here]

4. Descriptive statistics and empirical analysis

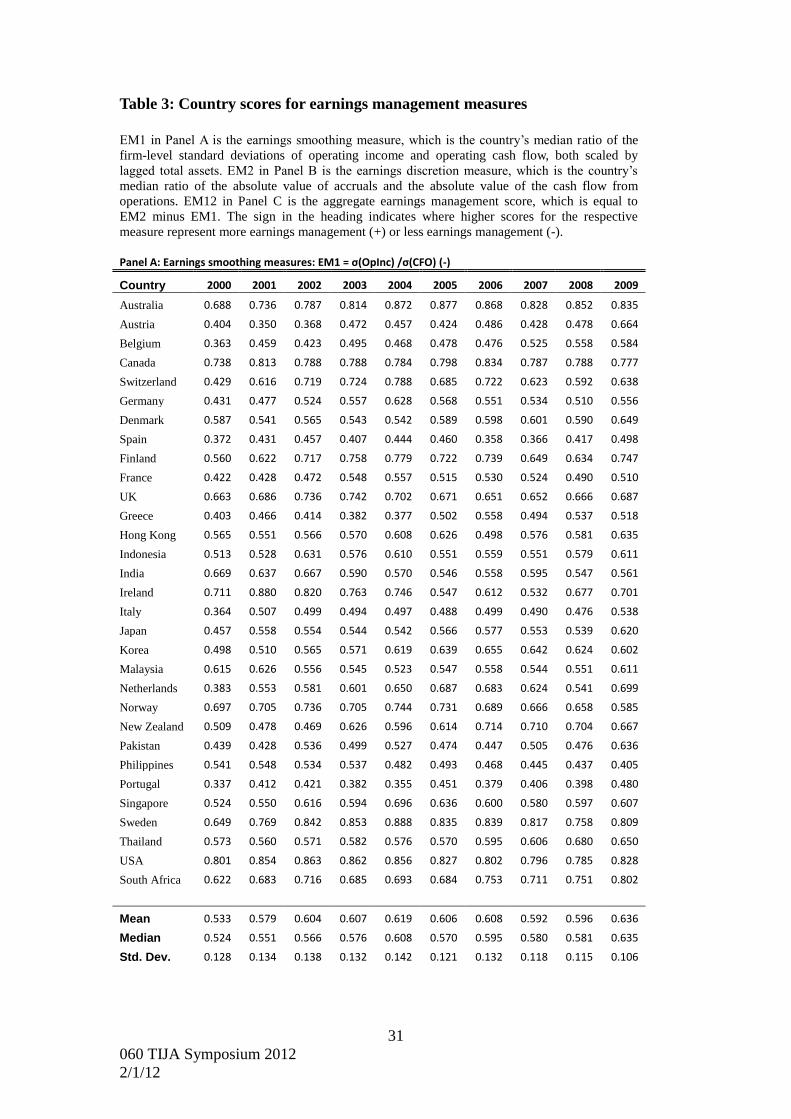

4.1. Descriptive statistics for earnings management

Table 3 provides descriptive statistics for the two individual earnings management measures

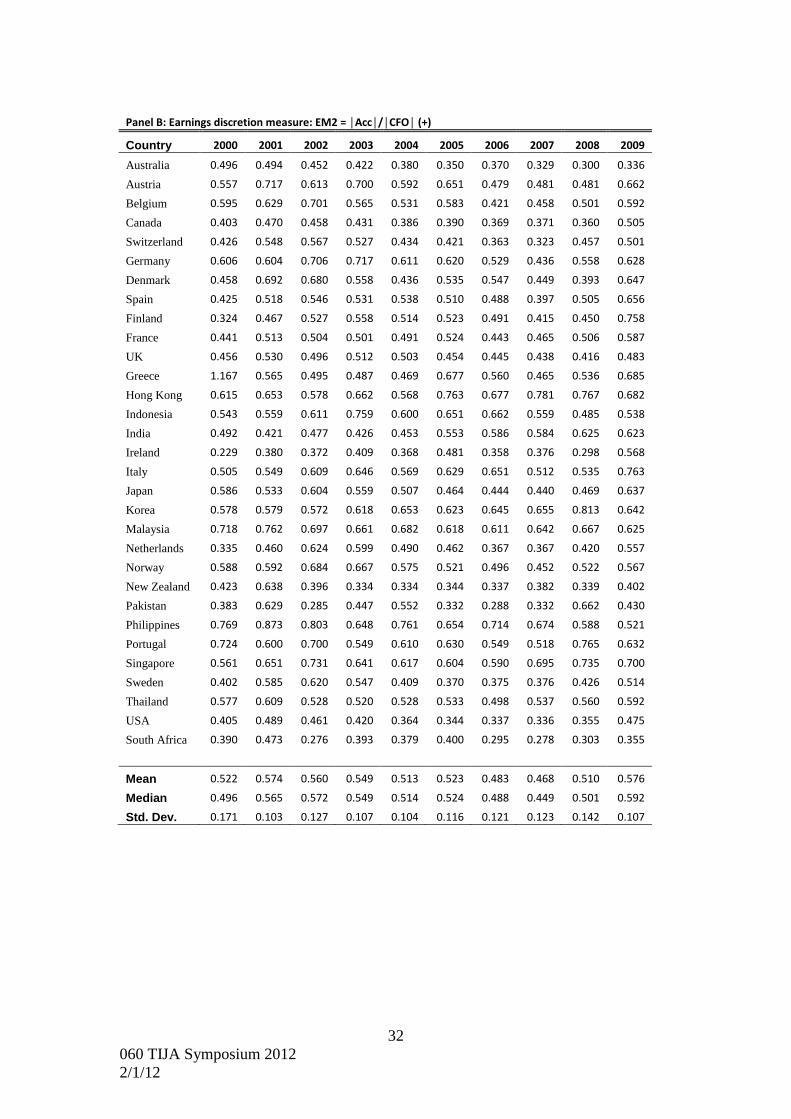

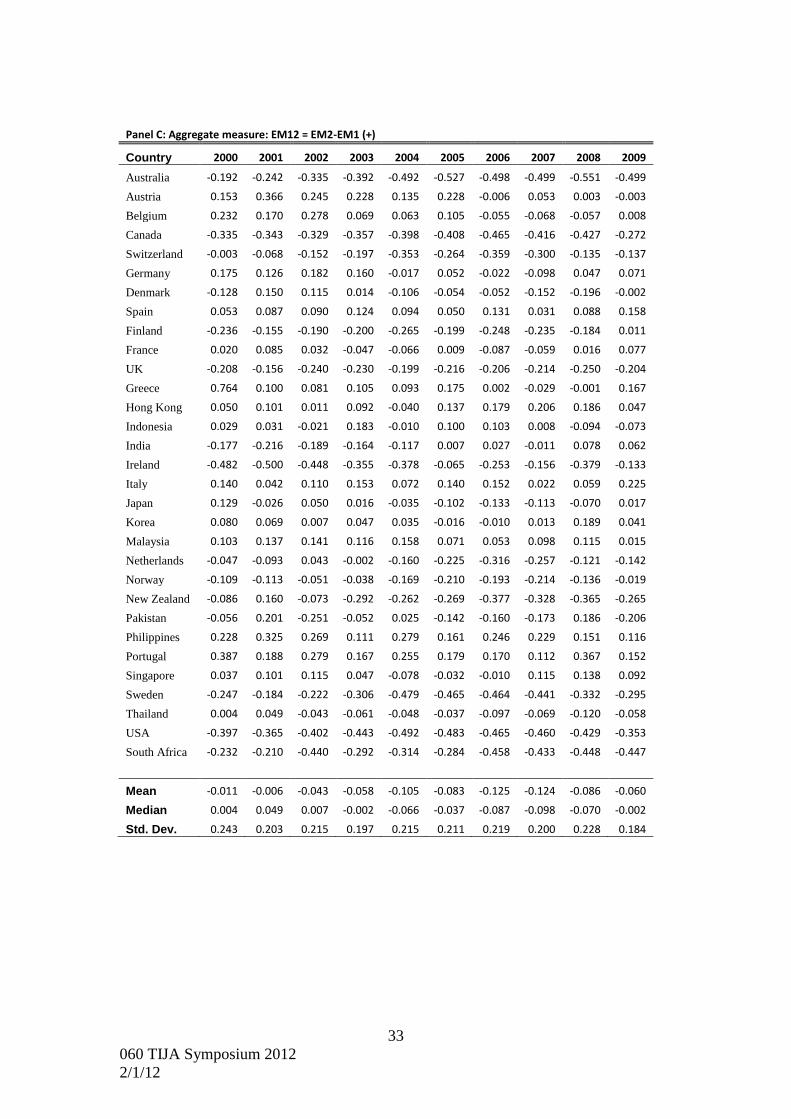

in Panel A and Panel B respectively, as well as their aggregate measure in Panel C. The signs

in the heading of the panels indicate whether higher values imply more earnings management

(+) or less earnings management (-). While the U.S. is yet to adopt IFRS, prior studies have

found high quality earnings due to high quality accounting standards and strong regulatory

and institutional arrangements. Furthermore, our data show that Canada also has a low level

of earnings management and strong institutions similar to the U.S. Therefore, we use the

average earnings management of the U.S. and Canada as a benchmark11

.

[Insert Table 3 here]

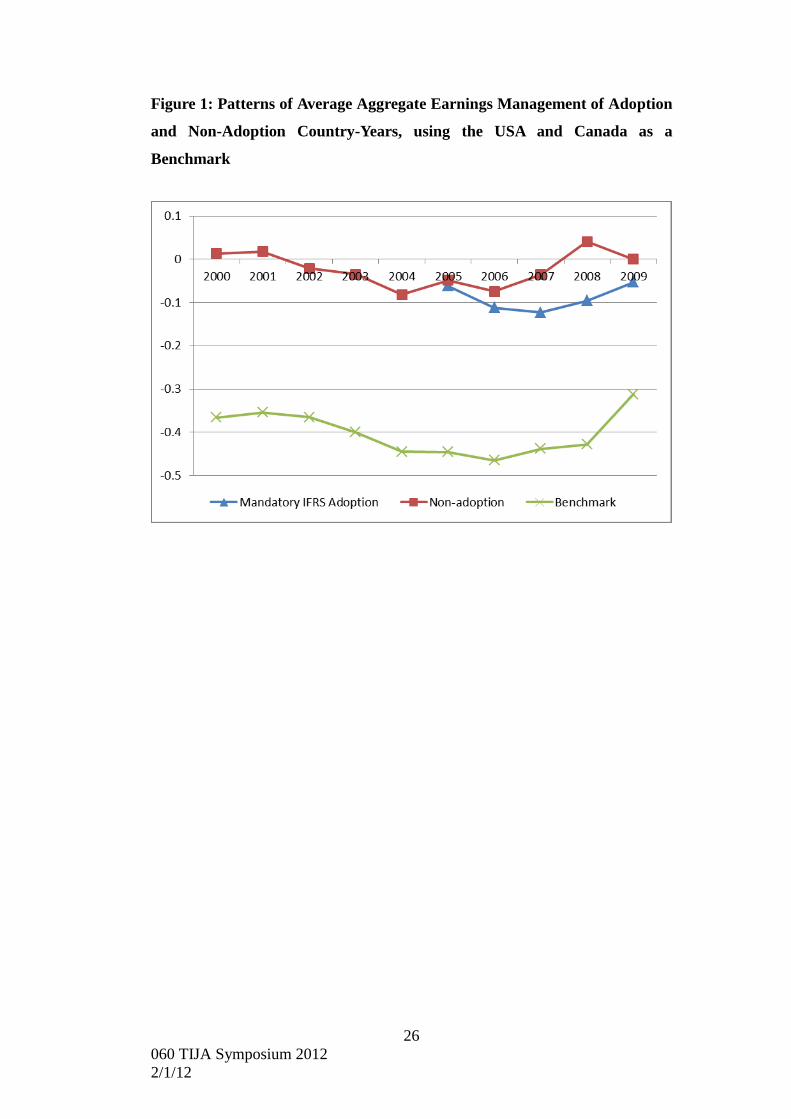

Figure 1 provides a comparison of the average earnings management of the IFRS adoption

group, non-adoption group, and the benchmark of U.S. and Canada. It shows that there is no

particular trend for the level of earnings management over the years. On average, the IFRS

adoption group has a slightly lower level of earnings management than the non-adoption

group, while the benchmark of the U.S. and Canada has the lowest level of earnings

management. However, a selection bias may exist in this study because the number of

non-adoption countries is much less than the adoption countries.

[Insert Figure 1 here]

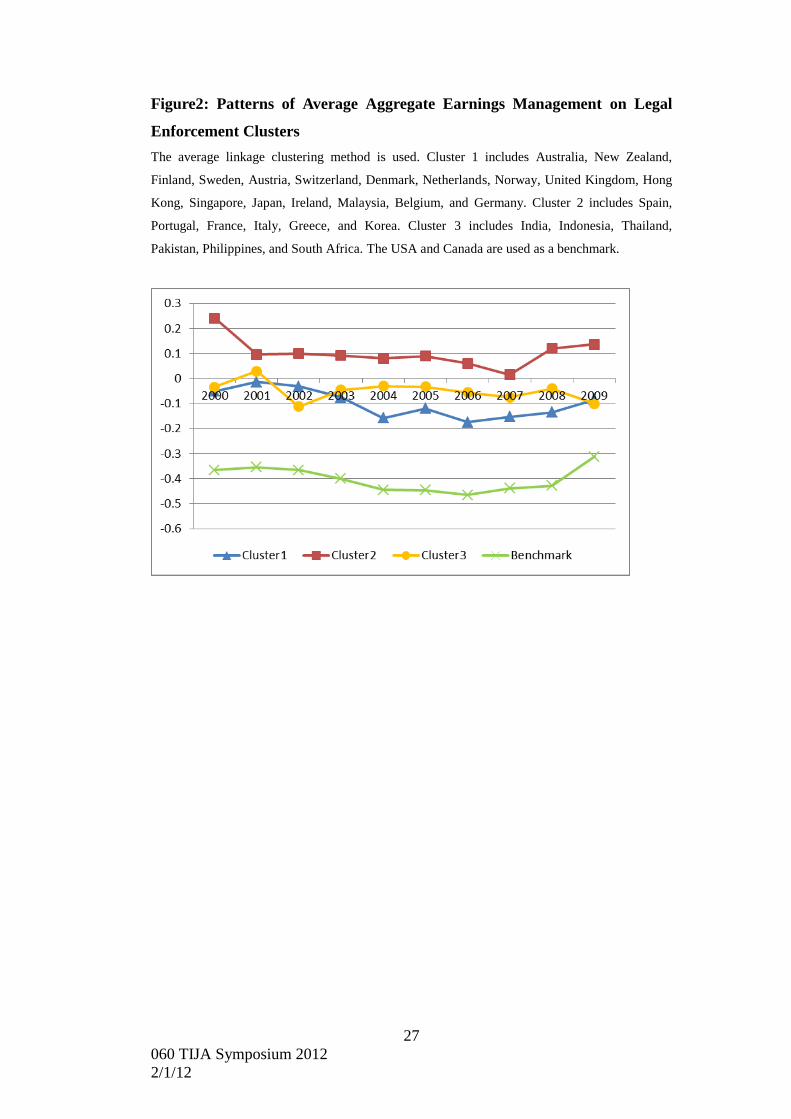

Based on the four legal enforcement variables, we use a cluster analysis12

to segment the

countries into three major groups. Cluster one includes Australia, New Zealand, Finland,

Sweden, Austria, Switzerland, Denmark, Netherlands, Norway, United Kingdom, Hong Kong,

Singapore, Japan, Ireland, Malaysia, Belgium, and Germany. Cluster two includes Spain,

Portugal, France, Italy, Greece, and Korea. Cluster three includes India, Indonesia, Thailand,

Pakistan, Philippines, and South Africa. By using the U.S. and Canada benchmark, we

compare the average earnings management between the three clusters. Figure 2 shows that

11

The result is similar, when we only use U.S. data as the benchmark (not tabulated). 12

The U.S. and Canada used as a benchmark are excluded from the cluster analysis.

17

060 TIJA Symposium 2012

2/1/12

cluster one with stronger legal enforcement on average has a lower level of earnings

management than cluster two and three, the weaker legal enforcement clusters. Cluster three

has the highest level of earning management. Again, the benchmark group of the U.S. and

Canada has the lowest level of earnings management.

[Insert Figure 2 here]

4.2. Institutional characteristics

Table 4 presents the country-by-country data for institutional variables used in this study. The

four legal enforcement factors and their aggregate measure show that countries such as the

U.S., Canada, New Zealand, Australia and the United Kingdom have the highest enforcement

scores, while Indonesia, Philippines, Pakistan, and Thailand have the lowest.

For ownership, the U.S., Taiwan, and UK show the smallest ownership concentration, while

Greece, Belgium, and Indonesia have the largest ownership concentration. The accounting

standards difference index shows that Singapore, South Africa and the United Kingdom have

the smallest number of differences from IFRS, while Greece, Spain, Finland and Portugal

have the largest number of differences. The mandatory adoption year is used for coding the

IFRS adoption and non-adoption year dummies.

[Insert Table 4 here]

4.3. Bivariate correlations

Table 5 reports the Pearson and Spearman correlation coefficients for the correlations

between pooled earnings management measures13

and various country-level institutional

variables.

As expected, the pooled smoothing measure (EM1) and the pooled magnitude of accruals

(EM2) are negatively correlated with a Pearson coefficient of -0.611 (p < 0.01) or a Spearman

coefficient of -0.628 (p < 0.01), suggesting that EM1 and EM2 capture somewhat distinct

aspects of earnings management.

The proxy for accounting standards (GAAPDiff) is positively correlated with pooled

13

The pooled measure is the average over the sample period of 2000 to 2009.

18

060 TIJA Symposium 2012

2/1/12

AggregateEM (0.458) at a highly significant level (p < 0.01), suggesting that the quality of

accounting standards is an important factor affecting accounting quality.

Consistent with our hypothesis, the four legal enforcement factors are all negatively

correlated with pooled AggregateEM. Aggregate Enforcement is also negatively correlated

with pooled AggregateEM (-0.498) at a highly significant level (p < 0.01), showing that

countries with stronger legal enforcement generally have less earnings management.

The control variable Ownership Concentration is positively correlated with pooled

AggregateEM (0.616) at a highly significant level (p < 0.01), suggesting that countries with

concentrated ownership generally have high levels of earnings management.

[Insert Table 5 here]

4.4. Principal component analysis

Since the above correlation table shows that the four enforcement variables are somewhat

correlated, we conduct a principal component analysis (PCA) (see Table 6) to identify the

underlying components. Four principal components are identified. The first three components

together explain 96.7% of the total variation. We ignore the last principal component for the

regressions in the next two sub-sessions.

The first principal component (Enforcement_PC1) explains 50.7% of the variations. We

interpret this first principal component as total law enforcement, because three of the four

enforcement variables have strong loadings in the component. Their loadings are: judicial

efficiency (0.597), rule of law (0.666), and insider trading law (0.442).

The second principal component (Enforcement_PC2) explains 28% of the variations. It

mainly represents anti-director rights, which has a loading of 0.872.

The third principal component (Enforcement_PC3) explains 18.1% of the variations. It

mainly represents insider trading laws, which has a loading of 0.818.

[Insert Table 6 here]

19

060 TIJA Symposium 2012

2/1/12

4.5. Regressions

Consistent with the results of the bivariate correlations, Table 7 shows that the results of

country-year level linear regressions with aggregate earnings management as the dependent

variable. We control for serial/auto correlation across years using year dummies14

. The

adjusted R-squares for the regressions range from 42.4% to 45.9%.

Models 1 to 6 show that GAAPDiff is positively and significantly associated with earnings

management (β1 ranges from 0.014 to 0.016 with all p < 0.01), suggesting that the quality of

accounting standards is relevant to earnings quality. The mandatory adoption dummy is

negatively associated with earnings management, suggesting that the IFRS adoption countries

have lower levels of earnings management in post-adoption periods, compared with the

non-adoption countries and adoption countries in pre-adoption periods.

In models 7 and 8, GAAPDiff_NA (i.e. the combination of mandatory adoption of IFRS and

GAAPDiff) is positively and significantly associated with earnings management, suggesting

that countries with lower accounting standards quality have higher levels of earnings

management. Putting together the results of models 1 to 8, our results indicate that earnings

management is lower for countries that have adopted IFRS or have local standards that

converge with IFRS. This result supports hypothesis H1.

Similar to previous studies, we also find a reduction in earnings management for the

enforcement variables. In OLS models 1 to 4, individually all four legal enforcement factors

are negatively associated with earnings management. Except for the Anti-director rights index,

the other legal enforcement variables are negative at highly significant levels. In OLS models

5 to 7, both the aggregate measure and the principal components of legal enforcement are

negatively and significantly associated with earnings management, indicating that strong

legal enforcement reduces earnings management. Therefore, our results support hypothesis

H2, i.e., earnings management is negatively associated with legal enforcement.

Using General Linear Model (GLM) in 8, the coefficient on the interactions between

GAAPDiff_NA and Enforcment_PC1 is negative and marginally significant at a significance

level of p<0.10, suggesting that stronger legal enforcement can overcome the GAAP

differences to reduce a country’s overall level of earnings management. However, this result

14

The coefficients for year dummies are not tabulated for brevity.

20

060 TIJA Symposium 2012

2/1/12

is not as significant as those of Hoque et al (2012). The main reasons for this are that when

countries are adopting IFRS they are also making additional securities law arrangement for

enforcing IFRS and for auditing, and several countries, such as Australia, New Zealand,

Singapore and South Africa already had local standards similar to IFRS prior to the official

adoption of IFRS. Note that the coefficient of GAAPDiff_NA in models 7 and 8 are not as

strong as those of Mandatory adoption of IFRS in models 1 to 3. While we do find support

for hypothesis H3, the support is not very significant.

Ownership concentration is significantly and positively associated with earnings management

across various models, suggesting that countries with higher ownership concentration have

higher levels of earnings management. The coefficients for market liquidity15

are close to

zero and not significant. The long-term debt to total assets ratio is negatively associated with

earnings management, suggesting that the monitoring power of the debt holders reduces

earnings management. The total taxes to total assets ratio is also negatively associated with

earning management. Consistent with Guenther and Young (2000) and Burgstahler et al.

(2006), the countries with high tax rates have less scope to decrease earnings.

[Insert Table 7 here]

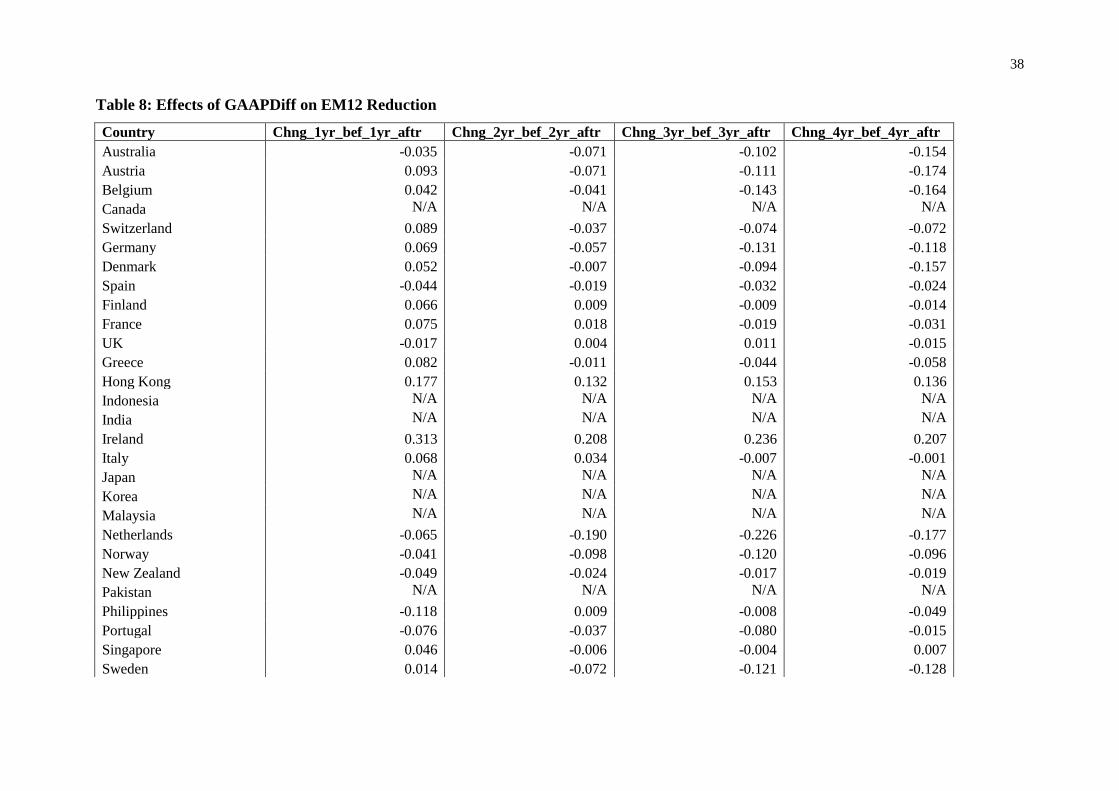

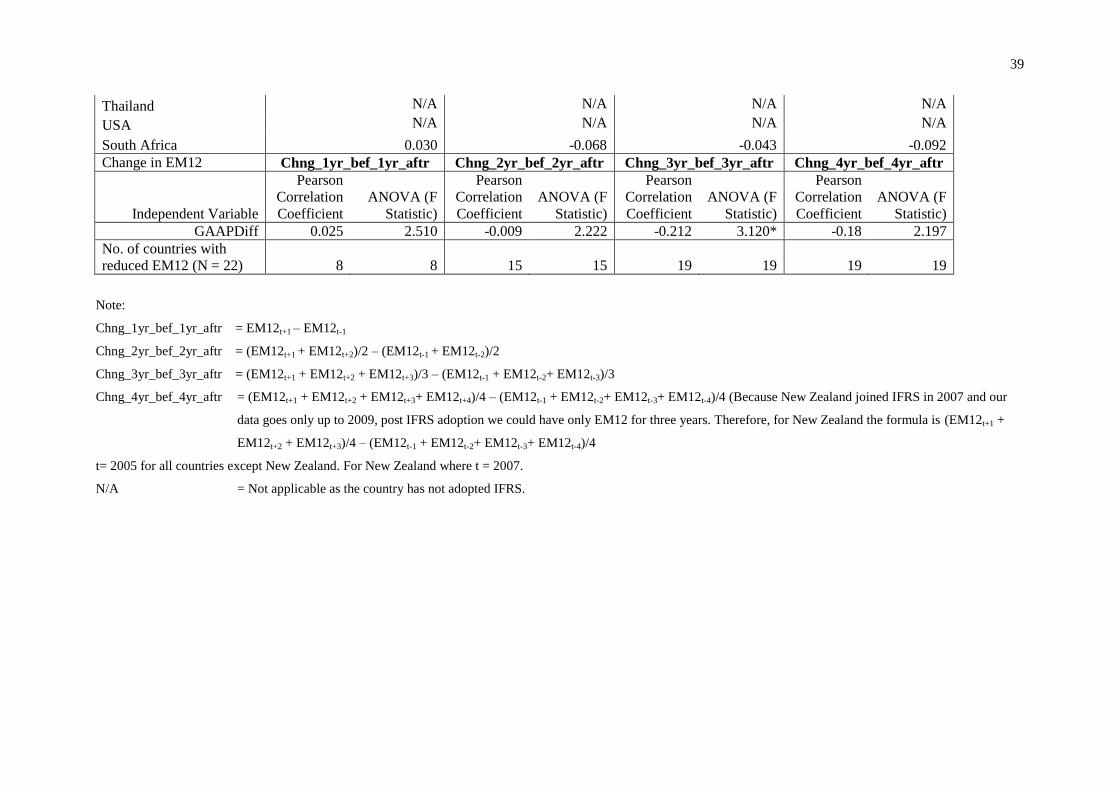

For hypothesis H4, we conduct tests to ascertain whether or not for IFRS adoption countries,

the reduction of earnings management is higher for those countries that had local standards

less convergent to IFRS prior to IFRS adoption. The results for these tests are presented in

Table 8. The results show that out of the 22 countries in our sample that adopted IFRS, the

number of countries with reductions in earnings management increased from 8 to 19 within a

period of three years after IFRS adoption. We also find a negative correlation between

GAAPDiff immediately prior IFRS adoption and earnings management change. The results

show that while the initial two years after IFRS adoption the association between GAAPDiff

and EM12 was minimal, but by the third year this association had become quite large (-0.212)

and in the fourth year the trend of EM12 reducing continued (-0.180). Because GAAPDiff is

a categorical variable, we conducted ANOVA and found the third year F-statistic 3.120 to be

significant at p <0.10. Although the results are not very strong, there is a clear indication that

the countries with higher GAAPDiff are enjoying reductions in earnings management.

[Insert Table 8 here]

15

When we replace market liquidity with market capitalization, the results are similar.

21

060 TIJA Symposium 2012

2/1/12

4.7. Sensitivity tests

Our results are robust across several sensitivity tests (not tabulated). (1) We examine the

minimum sample size of 10 firm observations in each country-year by changing this

requirement to at least 30 firm observations in each country-year, and find similar results. (2)

The results remain similar, when we use a principal component of EM1 and EM2 to replace

the aggregate earnings management as the dependent variable in the regressions. (3) The

mandatory adoption dummy remains significant, when we use an additional dummy variable

for indicating countries during the period of voluntary adoption IFRS, which is also

negatively associated with the aggregate earnings management. (4) Some of our enforcement

variables and ownership concentration are drawn from studies conducted several years ago16

,

and may have changed over time. The results are not affected by using an alternative time

variant measure of rule of law drawn from World Bank Worldwide Governance Indicators17

to replace the time-invariant rule of law drawn from La Porta et al. (2008). Here, the rule of

law reflects perceptions of the extent to which agents have confidence in and abide by the

rules of society, and in particular the quality of contract enforcement, property rights, the

police, and the courts, as well as the likelihood of crime and violence (Kaufmann, Kraay, and

Mastruzzi, 2010). It is estimated annually, and available from 1996 to 2010. (5) We have

multi-year data for the earnings management variables, which are positively correlated,

because our smoothing measure is calculated using the standard deviation of data from the

previous five years and moves for every five-year period. Another reason is that the firms

with high accruals in a certain year are also likely to have high accruals in following years.

We conduct autoregressive regressions to control for the potential autocorrelation problem.

All estimated coefficients from the time series method are consistent with the results of linear

regressions. (6) We acknowledge that many institutional factors link and interact with each

other, adding noise to the models. Also, because we have two measures of earnings

management, we conduct additional tests, such as canonical correlation analysis to control for

the correlations between the two earnings management measures, and between the various

institutional factors. The results from the alternative multivariate methods are consistent with

16

We assume that the changes of these institutions are costly and time consuming and the changes are gradual,

although these variables are slowly changing over time. For example, some countries have renewed their

enforcement systems to support the adoption of IFRS. 17

The Worldwide Governance Indicators (WGI) including the alternative rule of law measure is downloaded

from http://info.worldbank.org/governance/wgi/pdf/wgidataset.xls.

22

060 TIJA Symposium 2012

2/1/12

our regressions.

In summary, the results of the bivariate correlations, OLS regressions, GLM, and robustness

tests support our hypothesis that both good accounting standards quality and strong legal

enforcement are necessary to reduce earnings management.

5. Conclusion

Although accounting standards are now harmonized in many countries, the lack of uniformity

and comparability in the enforcement of accounting standards across borders reduces the

benefits of IFRS adoption to improve accounting quality, which is of concern to accounting

standard setters, regulators, and investors. We examine this concern by investigating the

effects of IFRS adoption and legal enforcement on the differences in earnings management

across 31 countries. A unique step we take in this study is to take into account the level of

convergence that had already taken place in a country prior to IFRS adoption. We took this

because countries that have had large changes in their accounting standards and policies

would enjoy the benefits of IFRS adoption more than the countries that already had higher

quality accounting standards and policies.

The findings show that mandatory adoption of IFRS and strong enforcement reduce earnings

management. However, the effects of legal enforcement are not as strong as ascertained in

previous studies when the difference between pre-IFRS accounting standards and IFRS are

taken into account. Also, we find that countries with less convergent standards to IFRS

benefit more from IFRS adoption. These findings highlight the importance of IFRS adoption

in countries with lower quality accounting standards and institutional settings than for those

with better accounting arrangements. Currently, the International Accounting Standards

Board (IASB) is focused on aligning IFRS with the US accounting standards. Our results

suggest that alignment with US standards would have lower benefits than the effort to

encourage countries with less developed accounting institutional arrangements to adopt IFRS.

23

060 TIJA Symposium 2012

2/1/12

References

Aboody, D., Hughes, J. & Liu, J. (2005). Earnings quality, insider trading, and cost of capital.

Journal of Accounting Research, 43(5), 651-673.

Ali, A. & Hwang, L. (2000). Country-specific factors related to financial reporting and the

value relevance of accounting data. Journal of Accounting Research, 38(1), 1-21.

Atje, R. & Jovanovic, B. (1993). Stock market and development. European Economic Review,

37, 632-640.

Bae, K. -H., Tan, H. & Welker, M. (2008). International GAAP differences: The impact on

foreign analysts. The Accounting Review, 83(3), 593–628.

Ball, R., Kothari, S. & Robin, A. (2000). The effect of international institutional factors on

properties of accounting earnings. Journal of Accounting and Economics, 29, 1-52.

Ball, R., Robin, A. & Wu, J. S. (2003). Incentives versus Standards: Properties of Accounting

Income in Four East Asian Countries, and Implications for Acceptance of IAS. Journal

of Accounting and Economics, 36, 235–270.

Barth, M., Landsman, W. & Lang, M. (2008). International accounting standards and

accounting quality. Journal of Accounting Research, 46(3), 467-498.

Beidleman, C. (1973). Income smoothing: the role of management. The Accounting Review,

48(4), 653-667.

Beneish, M. D. & Vargus, M. E. (2002). Insider trading, earnings quality, and accrual

mispricing. The Accounting Review, 77(4), 755-791. M.D.

Beneish, M. D. & Yohn, T. L. (2008). Information friction and investor home bias: A

perspective on the effect of global IFRS adoption on the extent of equity home bias,

Journal of Accounting and Public Policy, 27, 433–443.

Beny, L. N. (2005). Do insider trading laws matter? Some preliminary comparative evidence.

American Law and Economics Review, 7(1), 144-183.

Bhattacharya, U., Daouk, H. & Welker, M. (2003). The world price of earnings opacity. The

Accounting Review, 78(3), 641-678.

Boonlert-U-Thai, K., Meek, G. K. & Nabar, S. (2006). Earnings attributes and

invetor-protection: International evidence. The International Journal of Accounting,

41(4), 327-357.

Burgstahler, D., Hail, L. & Leuz. C. (2006). The importance of reporting incentives: Earnings

management in European private and public firms. The Accounting Review, 81(5),

983–1016.

Callao, S. & Jarne, J. I. (2010) Have IFRS affected earnings management in the European

Union? Accounting in Europe, 7(2), 159-189.

Chen, H., Tang, Q., Jiang, Y. & Lin, Z. (2010). The role of international financial reporting

standards in accounting quality: evidence from the European Union. Journal of

International Financial Management and Accounting, 21(3), 220-278.

Daske, H. & Gebhardt, G. (2006). International financial reporting standards and experts’

perceptions of disclosure quality. Abacus, 42(3-4), 461-498.

Daske, H., Hail, L., Leuz, C. & Verdi, R. (2008), Mandatory IFRS reporting around the world:

early evidence on the economic consequences. Journal of Accounting Research, 46(5),

1085-142.

Dechow, P., Sloan, R. & Sweeney, A. (1995). Detecting earnings management. The

Accounting Review, 70, 193-225.

Deloitte’s IAS Plus Website. (2011). Use of IFRSs by jurisdiction. Retrieved September 1,

2011, from http://www.iasplus.com/country/useias.htm .

24

060 TIJA Symposium 2012

2/1/12

Ding, Y., Hope, O., Jeanjean, T. & Stolowy, H. (2007). Differences between domestic

accounting standards and IAS: measurement, determinants and implications. Journal of

Accounting and Public Policy, 26(1), 1-38.

Djankov, S., La Porta, R., Lopez-de-Silanes, F. & Shleifer, A. (2008). The law and economics

of self-dealing. Journal of Financial Economics, 88, 430-465.

Ewert, R. & Wagenhofer, A. (2005). Economic effects of tightening accounting standards to

restrict earnings management. The Accounting Review, 80, 1101-1124.

FEE. (2001). Enforcement mechanisms in Europe: A preliminary investigation of oversight

systems. Retrieved June 2, 2008, from http://www.fee.be/fileupload/upload/

Enforcement MechanismsinEurope153200520952.pdf.

FEE. (2002). Discussion paper on enforcement of IFRS within Europe. Retrieved June 5,

2008, from http://www.iasplus.com/resource/feenforc.pdf.

Guenther, D. & Young, D. (2000). The association between financial accounting measures

and real economic activity: a multinational study. Journal of Accounting and

Economics, 29(1), 53-72.

Healy, P. & Wahlen, J. (1999). A review of the earnings management literature and its

implication for standard setting. Accounting Horizons, 13, 365-383.

Holthausen, R. W. (2003). Testing the relative power of accounting standards versus

incentives and other institutional features to influence the outcome of financial

reporting in an international setting, Journal of Accounting and Economics, 36,

271-283.

Hope. O. -K. (2003). Disclosure practices, enforcement of accounting standards, and analysts’

forecast accuracy: an international study. Journal of Accounting Research, 41(2),

235-272.

Hoque, M., Zijl, T., Dunstan, K. & Karim, W. (2011). The effect of IFRS Adoption and

investor protection on earnings quality around the world. International Journal of

Accounting, Forthcoming.

Huddart, S., Hughes, J. & Brunnermeier, M. (1999). Disclosure requirements and stock

exchange listing choices in an international context. Journal of Accounting and

Economics, 26, 237-269.

Hung, M. (2001). Accounting standards and value relevance of financial statement: An

international analysis. Journal of Accounting and Economics, 30 (3), 401-420.

Jeanjean, T. & Stolowy, H. (2008). Do accounting standards matter? An exploratory analysis

of earnings management before and after IFRS adoption. Journal of Accounting and

Public Policy, 27, 480–494.

Kaufmann, D., Kraay, A. & Mastruzzi, M. (2010). The Worldwide Governance Indicators : A

summary of methodology, data and analytical issues. World Bank Policy Research

Working Paper No.543. Retrieved December 1, 2011, from

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1682130.

La Porta, R., Lopez-De-Silanes, F., Shleifer, A. & Vishny, R. (1998). Law and finance.

Journal of Political Economy, 106(6), 1113-55

La Porta, R., Lopez-De-Silanes, F., Shleifer, A. & Vishny, R. (1999). The quality of

government. Journal of Law, Economics and Organization, 15, 222-279.

Leuz, C., Nanda, D. & Wysocki, P. D. (2003). Earnings management and investor protection:

an international comparison. Journal of Financial Economics, 69, 505-527.

Levine, R. & Zervos, S. (1998). Stock markets, banks and economic growth. American

Economic Review, 88, 537-558.

Lin, H. & Paananen, M. (2006). The effect of financial systems on earnings management

among firms reporting under IFRS. Business School Working Papers UHBS 2006-2.

Retrieved 20/5/08 from https://uhra.herts.ac.uk/dspace/bitstream/2299/714/1/S61.pdf.

25

060 TIJA Symposium 2012

2/1/12

Pope, P. F. & Walker, M. (1999). International differences in the timeliness, conservatism,

and classification of earnings. Journal of Accounting Research, 37(Supplement), 53-87.

Rahman, A., Yammeesri, J. & Perera, H. (2010). Financial reporting quality in international

settings: A comparative study of the USA, Japan, Thailand, France and Germany. The

International Journal of Accounting, 45(1), 1-34.

Schipper, K. (2005). The introduction of International Accounting Standards in Europe:

implications for international convergence. European Accounting Review, 14(1),

101-126.

Shleifer, A. & Vishny, R. (1997), A survey of corporate governance, The Journal of Finance,

52 (2), 737-783.

Shleifer, A. & Wolfenzon, D. (2002). Investor protection and equity markets. Journal of

Financial Economics, 66(1), 3–27.

Soderstrom, N. S. & Sun, K. J. (2007). IFRS adoption and accounting quality: a review.

European Accounting Review, 16(4), 675-702.

Watts, R. L. & Zimmerman, J. L. (1978). Towards a positive theory of the determination of

accounting standards. The Accounting Review, 53, 112-134.

Barth, M., Landsman, W. & Lang, M. (2008). International accounting standards and

accounting quality. Journal of Accounting Research, 46(3), 467-498.

Callao, S. & Jarne, J. I. (2010) Have IFRS affected earnings management in the European

Union? Accounting in Europe, 7(2), 159-189.

Chen, H., Tang, Q., Jiang, Y. & Lin, Z. (2010). The role of international financial reporting

standards in accounting quality: evidence from the European Union. Journal of

International Financial Management and Accounting, 21(3), 220-278.

Daske, H., Hail, L., Leuz, C. & Verdi, R. (2008), Mandatory IFRS reporting around the world:

early evidence on the economic consequences. Journal of Accounting Research, 46(5),

1085-142.

Jeanjean, T. & Stolowy, H. (2008). Do accounting standards matter? An exploratory analysis

of earnings management before and after IFRS adoption. Journal of Accounting and

Public Policy, 27, 480–494.

26

060 TIJA Symposium 2012

2/1/12

Figure 1: Patterns of Average Aggregate Earnings Management of Adoption

and Non-Adoption Country-Years, using the USA and Canada as a

Benchmark

27

060 TIJA Symposium 2012

2/1/12

Figure2: Patterns of Average Aggregate Earnings Management on Legal

Enforcement Clusters

The average linkage clustering method is used. Cluster 1 includes Australia, New Zealand,

Finland, Sweden, Austria, Switzerland, Denmark, Netherlands, Norway, United Kingdom, Hong

Kong, Singapore, Japan, Ireland, Malaysia, Belgium, and Germany. Cluster 2 includes Spain,

Portugal, France, Italy, Greece, and Korea. Cluster 3 includes India, Indonesia, Thailand,

Pakistan, Philippines, and South Africa. The USA and Canada are used as a benchmark.

28

060 TIJA Symposium 2012

2/1/12

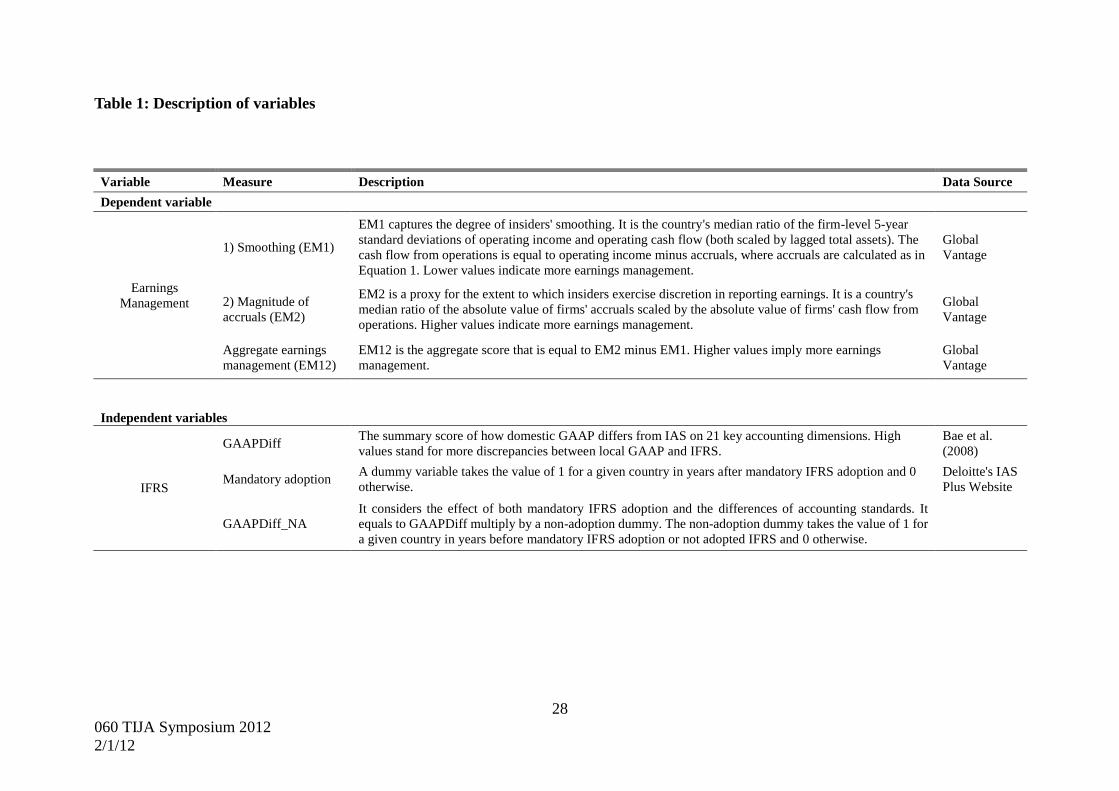

Table 1: Description of variables

Variable Measure Description Data Source

Dependent variable

Earnings

Management

1) Smoothing (EM1)

EM1 captures the degree of insiders' smoothing. It is the country's median ratio of the firm-level 5-year

standard deviations of operating income and operating cash flow (both scaled by lagged total assets). The

cash flow from operations is equal to operating income minus accruals, where accruals are calculated as in

Equation 1. Lower values indicate more earnings management.

Global

Vantage

2) Magnitude of

accruals (EM2)

EM2 is a proxy for the extent to which insiders exercise discretion in reporting earnings. It is a country's

median ratio of the absolute value of firms' accruals scaled by the absolute value of firms' cash flow from

operations. Higher values indicate more earnings management.

Global

Vantage

Aggregate earnings

management (EM12)

EM12 is the aggregate score that is equal to EM2 minus EM1. Higher values imply more earnings

management.

Global

Vantage

Independent variables

IFRS

GAAPDiff The summary score of how domestic GAAP differs from IAS on 21 key accounting dimensions. High

values stand for more discrepancies between local GAAP and IFRS.

Bae et al.

(2008)

Mandatory adoption A dummy variable takes the value of 1 for a given country in years after mandatory IFRS adoption and 0

otherwise.

Deloitte's IAS

Plus Website

GAAPDiff_NA

It considers the effect of both mandatory IFRS adoption and the differences of accounting standards. It

equals to GAAPDiff multiply by a non-adoption dummy. The non-adoption dummy takes the value of 1 for

a given country in years before mandatory IFRS adoption or not adopted IFRS and 0 otherwise.

29

060 TIJA Symposium 2012

2/1/12

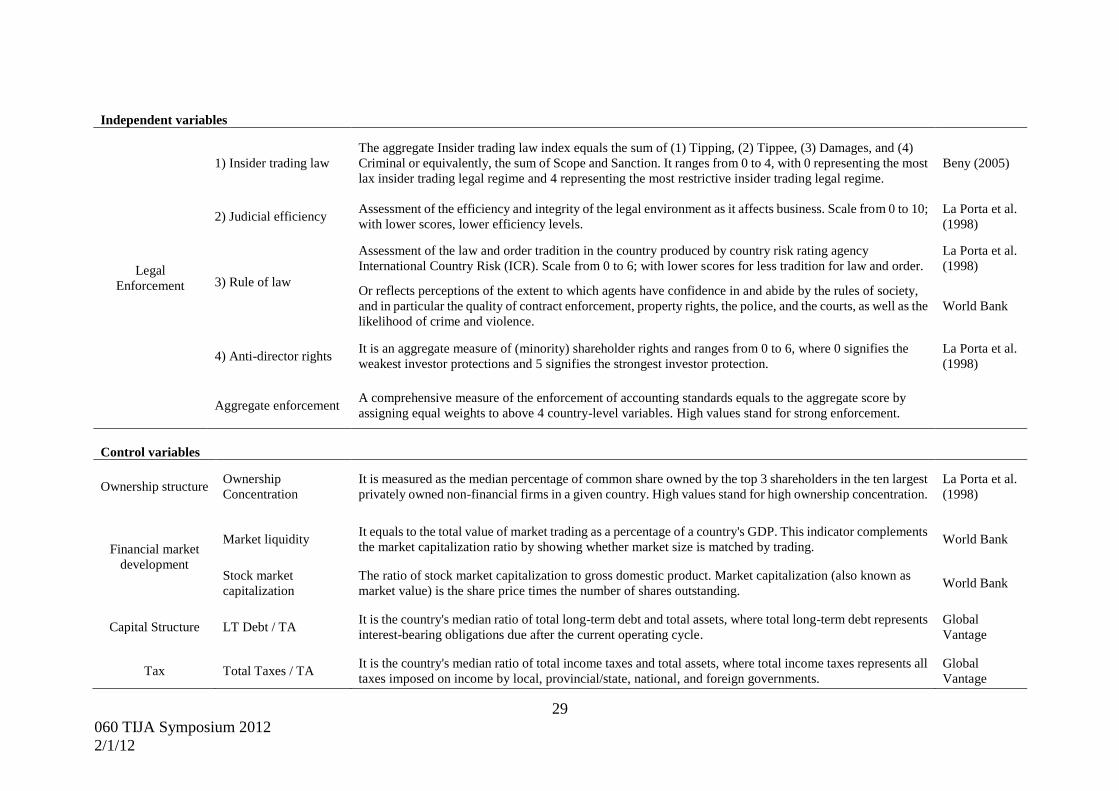

Independent variables

Legal

Enforcement

1) Insider trading law

The aggregate Insider trading law index equals the sum of (1) Tipping, (2) Tippee, (3) Damages, and (4)

Criminal or equivalently, the sum of Scope and Sanction. It ranges from 0 to 4, with 0 representing the most

lax insider trading legal regime and 4 representing the most restrictive insider trading legal regime.

Beny (2005)

2) Judicial efficiency Assessment of the efficiency and integrity of the legal environment as it affects business. Scale from 0 to 10;

with lower scores, lower efficiency levels.

La Porta et al.

(1998)

3) Rule of law

Assessment of the law and order tradition in the country produced by country risk rating agency

International Country Risk (ICR). Scale from 0 to 6; with lower scores for less tradition for law and order.

La Porta et al.

(1998)

Or reflects perceptions of the extent to which agents have confidence in and abide by the rules of society,

and in particular the quality of contract enforcement, property rights, the police, and the courts, as well as the

likelihood of crime and violence.

World Bank

4) Anti-director rights It is an aggregate measure of (minority) shareholder rights and ranges from 0 to 6, where 0 signifies the

weakest investor protections and 5 signifies the strongest investor protection.

La Porta et al.

(1998)

Aggregate enforcement A comprehensive measure of the enforcement of accounting standards equals to the aggregate score by

assigning equal weights to above 4 country-level variables. High values stand for strong enforcement.

Control variables

Ownership structure Ownership

Concentration

It is measured as the median percentage of common share owned by the top 3 shareholders in the ten largest

privately owned non-financial firms in a given country. High values stand for high ownership concentration.

La Porta et al.

(1998)

Financial market

development

Market liquidity It equals to the total value of market trading as a percentage of a country's GDP. This indicator complements

the market capitalization ratio by showing whether market size is matched by trading. World Bank

Stock market

capitalization

The ratio of stock market capitalization to gross domestic product. Market capitalization (also known as

market value) is the share price times the number of shares outstanding. World Bank

Capital Structure LT Debt / TA It is the country's median ratio of total long-term debt and total assets, where total long-term debt represents

interest-bearing obligations due after the current operating cycle.

Global

Vantage

Tax Total Taxes / TA It is the country's median ratio of total income taxes and total assets, where total income taxes represents all

taxes imposed on income by local, provincial/state, national, and foreign governments.

Global

Vantage

30

060 TIJA Symposium 2012

2/1/12

Table 2: Sample distribution by country and fiscal year

The sample is selected from Industrial Research and Industrial Active Files in the Global Vantage

database. The final sample consists of 128,292 firm-year observations, across 31 countries for the fiscal

years 2000 to 2009. In selecting, we use the following criteria: 1) utility and financial companies are

excluded, as they are under different incentives for earnings management; 2) each country must have at

least 10 firms observation in each year for reliability reason; and 3) the sample only contains firms with

necessary data to compute the two measures of earnings management.

Country 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Total

Australia 181 231 460 554 680 801 869 906 921 989 6,592

Austria 37 58 52 48 53 53 56 56 57 58 528

Belgium 44 53 53 60 81 79 74 72 76 85 677

Canada 336 317 304 360 374 378 364 345 348 355 3,481

Switzerland 90 126 146 141 159 165 162 163 166 160 1,478

Germany 238 306 327 401 496 497 486 482 490 497 4,220

Denmark 57 72 81 86 102 103 99 89 86 76 851

Spain 58 78 80 87 91 89 87 89 91 89 839

Finland 35 58 69 84 100 103 100 102 104 105 860

France 226 307 361 414 476 481 468 473 468 498 4,172

UK 504 723 877 885 904 944 965 967 962 974 8,705

Greece 10 28 49 60 63 71 78 80 82 93 614

Hong Kong 49 54 90 94 100 109 120 126 153 189 1,084

Indonesia 65 96 150 172 170 174 182 155 161 155 1,480

India 80 83 117 418 480 615 805 1,008 1,177 1,246 6,029

Ireland 33 40 39 46 52 51 49 49 50 51 460

Italy 56 95 96 101 138 157 158 167 173 182 1,323

Japan

1,325

2,787 3,019 3,097 3,108 3,176 3,297 3,488 3,461 3,392 30,150

Korea 718 715 788 810 1,052 1,230 1,286 1,453 1,481 1,456 10,989

Malaysia 182 239 463 508 527 572 604 619 660 711 5,085

Netherlands 80 111 117 124 130 129 121 117 111 110 1,150

Norway 42 64 79 86 112 115 107 117 113 108 943 New

Zealand 19 20 36 49 52 56 62 74 71 75 514

Pakistan 16 28 50 53 48 49 51 71 85 95 546

Philippines 19 32 89 93 90 102 107 112 109 115 868

Portugal 16 28 28 28 35 35 39 40 39 36 324

Singapore 127 124 177 214 265 313 349 393 447 469 2,878

Sweden 50 94 158 195 232 241 248 253 249 257 1,977

Thailand 127 155 232 240 247 246 246 268 334 355 2,450

USA

2,671

2,664 2,658 2,884 2,823 2,679 2,526 2,374 2,295 2,227 25,801

South

Africa 30 35 97 115 135 157 170 162 156 167 1,224

7,521

9,821

11,342

12,507

13,375

13,970

14,335

14,870

15,176

15,375

128,292

31

060 TIJA Symposium 2012

2/1/12

Table 3: Country scores for earnings management measures

EM1 in Panel A is the earnings smoothing measure, which is the country’s median ratio of the

firm-level standard deviations of operating income and operating cash flow, both scaled by

lagged total assets. EM2 in Panel B is the earnings discretion measure, which is the country’s

median ratio of the absolute value of accruals and the absolute value of the cash flow from

operations. EM12 in Panel C is the aggregate earnings management score, which is equal to

EM2 minus EM1. The sign in the heading indicates where higher scores for the respective

measure represent more earnings management (+) or less earnings management (-).

Panel A: Earnings smoothing measures: EM1 = σ(OpInc) /σ(CFO) (-)

Country 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Australia 0.688 0.736 0.787 0.814 0.872 0.877 0.868 0.828 0.852 0.835

Austria 0.404 0.350 0.368 0.472 0.457 0.424 0.486 0.428 0.478 0.664

Belgium 0.363 0.459 0.423 0.495 0.468 0.478 0.476 0.525 0.558 0.584

Canada 0.738 0.813 0.788 0.788 0.784 0.798 0.834 0.787 0.788 0.777

Switzerland 0.429 0.616 0.719 0.724 0.788 0.685 0.722 0.623 0.592 0.638

Germany 0.431 0.477 0.524 0.557 0.628 0.568 0.551 0.534 0.510 0.556

Denmark 0.587 0.541 0.565 0.543 0.542 0.589 0.598 0.601 0.590 0.649

Spain 0.372 0.431 0.457 0.407 0.444 0.460 0.358 0.366 0.417 0.498

Finland 0.560 0.622 0.717 0.758 0.779 0.722 0.739 0.649 0.634 0.747

France 0.422 0.428 0.472 0.548 0.557 0.515 0.530 0.524 0.490 0.510

UK 0.663 0.686 0.736 0.742 0.702 0.671 0.651 0.652 0.666 0.687

Greece 0.403 0.466 0.414 0.382 0.377 0.502 0.558 0.494 0.537 0.518

Hong Kong 0.565 0.551 0.566 0.570 0.608 0.626 0.498 0.576 0.581 0.635

Indonesia 0.513 0.528 0.631 0.576 0.610 0.551 0.559 0.551 0.579 0.611

India 0.669 0.637 0.667 0.590 0.570 0.546 0.558 0.595 0.547 0.561

Ireland 0.711 0.880 0.820 0.763 0.746 0.547 0.612 0.532 0.677 0.701

Italy 0.364 0.507 0.499 0.494 0.497 0.488 0.499 0.490 0.476 0.538

Japan 0.457 0.558 0.554 0.544 0.542 0.566 0.577 0.553 0.539 0.620

Korea 0.498 0.510 0.565 0.571 0.619 0.639 0.655 0.642 0.624 0.602

Malaysia 0.615 0.626 0.556 0.545 0.523 0.547 0.558 0.544 0.551 0.611

Netherlands 0.383 0.553 0.581 0.601 0.650 0.687 0.683 0.624 0.541 0.699

Norway 0.697 0.705 0.736 0.705 0.744 0.731 0.689 0.666 0.658 0.585

New Zealand 0.509 0.478 0.469 0.626 0.596 0.614 0.714 0.710 0.704 0.667

Pakistan 0.439 0.428 0.536 0.499 0.527 0.474 0.447 0.505 0.476 0.636

Philippines 0.541 0.548 0.534 0.537 0.482 0.493 0.468 0.445 0.437 0.405

Portugal 0.337 0.412 0.421 0.382 0.355 0.451 0.379 0.406 0.398 0.480

Singapore 0.524 0.550 0.616 0.594 0.696 0.636 0.600 0.580 0.597 0.607

Sweden 0.649 0.769 0.842 0.853 0.888 0.835 0.839 0.817 0.758 0.809

Thailand 0.573 0.560 0.571 0.582 0.576 0.570 0.595 0.606 0.680 0.650

USA 0.801 0.854 0.863 0.862 0.856 0.827 0.802 0.796 0.785 0.828

South Africa 0.622 0.683 0.716 0.685 0.693 0.684 0.753 0.711 0.751 0.802

Mean 0.533 0.579 0.604 0.607 0.619 0.606 0.608 0.592 0.596 0.636

Median 0.524 0.551 0.566 0.576 0.608 0.570 0.595 0.580 0.581 0.635

Std. Dev. 0.128 0.134 0.138 0.132 0.142 0.121 0.132 0.118 0.115 0.106

32

060 TIJA Symposium 2012

2/1/12

Panel B: Earnings discretion measure: EM2 = │Acc│/│CFO│ (+)

Country 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Australia 0.496 0.494 0.452 0.422 0.380 0.350 0.370 0.329 0.300 0.336

Austria 0.557 0.717 0.613 0.700 0.592 0.651 0.479 0.481 0.481 0.662

Belgium 0.595 0.629 0.701 0.565 0.531 0.583 0.421 0.458 0.501 0.592

Canada 0.403 0.470 0.458 0.431 0.386 0.390 0.369 0.371 0.360 0.505

Switzerland 0.426 0.548 0.567 0.527 0.434 0.421 0.363 0.323 0.457 0.501

Germany 0.606 0.604 0.706 0.717 0.611 0.620 0.529 0.436 0.558 0.628

Denmark 0.458 0.692 0.680 0.558 0.436 0.535 0.547 0.449 0.393 0.647

Spain 0.425 0.518 0.546 0.531 0.538 0.510 0.488 0.397 0.505 0.656