is your bank solvent? here’s how you can find …monthly... · is your bank solvent? here’s how...

TRANSCRIPT

www.sovereignman.com

IS YOUR BANK SOLVENT? HERE’S HOW YOU CAN FIND OUT.

It’s been an amazing month so far. Last week we held an exceptional event in Medellin, Colombia for members of our Total Access group.

My goal was to introduce people to the incredible city of Medellin, as well as the many lifestyle, business, and investment opportunities in Colombia.

Medellin is beautiful, vibrant, and quite tempting. Most of my staff had never been before, and by the end of the first day they were pressuring me to open a new office in the city.

I talk about Colombia a lot, and I’m constantly holding it up as an example of “risk arbitrage.”

Let’s be honest: the perceived risk about Colombia is very high. Most people still consider it a hotbed of narco-trafficking, kidnapping, murder, and chaos.

And while there are obviously still problems in Colombia, the ACTUAL risk in the country isn’t nowhere near what people think.

www.sovereignman.com2 SMX april 2016

If you tell your friends that you’re going to Colombia, they’ll think you’re crazy.

But it’s precisely these situations-- when the actual risk is much LOWER than the perceived risk—when you want to get in… when you want to invest.

Conversely, you want to get out when the actual risk is much HIGHER then the perceived risk; it’s when people think everything is perfectly fine, but there are serious problems just beneath the surface… that’s the time to head towards the exits.

This is very much the case with most western banking systems today.

It’s plagued by illiquidity and very low levels of capital. And yet most people don’t think twice when it comes to the safety of their bank.

The perceived risk is very low. The actual risk is quite a bit higher. Again—it’s time to hedge your bets and at least know where the exits are.

Now, the cornerstone of almost every Plan B is to protect your savings. And that makes the decision of WHERE you hold your savings critically important.

Traditionally we hold our savings in banks. And most of us grew up believing that banks were inherently safe. After all, they’re guaranteed by the government! The mere thought of a bank conjures images of conservative stewardship and rock solid responsibility.

The reality, however, is far different from this myth.

In fact, in the US alone, hundreds of banks have gone under in the last 15 years, sometimes taking their depositors’ or taxpayers’ money with them.

Banking systems in the West

Most banks in the West today are pitifully capitalized and highly illiquid.

They only hold a small portion of their customer deposits in reserve, while loaning the rest out and making risky bets with your money.

Most Western governments – which notionally provide a guarantee to entire banking systems and deposits – are themselves insolvent and drowning in debt.

And most of the biggest central banks in the world are borderline insolvent.

You wouldn’t just go to the first person you see on the street, hand them over your money, and say “Here, hang on to this for me, please.” That would be insane.

And yet that’s what most people do when it comes to choosing where they bank.

www.sovereignman.com3 SMX april 2016

They pick a bank to hold their money based on how cute and clever the advertisements are, whether the credit cards look swanky, or because the bank is close to the house (as if geography is still relevant in 2016).

No one considers the safety and prudence of their “financial partner,” which is what a bank actually is.

Of course, this willful ignorance extends to an entire nation’s banking system. It’s rarely just one bank that has bad practices. Often you’ll see the same weaknesses with most of the banks across the whole banking system.

Yet, still, no one questions the sanctity of this system. No one wants to admit that the Emperor has no clothes.

Jamie Dimon, the CEO of JP Morgan Chase, recently told Bloomberg News, “Despite all the turbulence so far this year, I don’t think anyone’s questioning our [banking] system. And that, obviously, is a good thing.”

Strange comment—it’s a ‘good thing’ that no one raises a hint of concern about a banking system that’s so illiquid.

Of course, this level of illiquidity is built into the system itself. It’s called fractional reserve banking, and it works basically like this:

www.sovereignman.com4 SMX april 2016

How fractional reserve banking can quickly collapse

As a customer, you deposit your savings in a bank.

The bank then turns around and lends out the vast majority of that deposited money… potentially in some idiotic no-money-down loan.

The bank keeps only a small fraction of OUR money in “reserve” to hand back to us in case we depositors have the audacity to make a withdrawal or transfer our money out of the system.

Often this liquidity reserve can be as low as 1% (or less) of the bank’s total deposits.

Banks therefore rely on the statistical probability that most of their depositors will not all show up one day and demand their money back at the same time.

And as a result of this presumption, the vast majority of your money simply isn’t there.

If there was a sudden rush of bank customers who wanted to withdraw their money, the bank would have to borrow emergency funds from the central bank… as well as start selling their investments and calling in loans in order to raise cash.

Now, if this only happened to ONE bank, it wouldn’t be a big deal.

But just imagine what would happen if ALL the banks (or even a handful of large banks) had to start selling investments and calling in loans-- it would be total chaos.

www.sovereignman.com5 SMX april 2016

Just imagine every bank in the banking system simultaneously dumping assets – stocks, bonds, etc. If everyone is a seller and no one is a buyer, asset prices collapse.

Concurrently, if banks started calling in loans, then many borrowers would also likely have to start dumping assets as well in order to raise the necessary cash.

This would cause an even further collapse of assets.

This is where things get really interesting.

Because in addition to having very limited liquidity, many Western banks also maintain very thin levels of capitalization (also known as solvency).

We frequently refer to this as a bank’s margin of safety.

Just like it’s a good idea for individuals to set aside a rainy day emergency fund, a bank with a strong margin of safety has set aside substantial reserves so that, even if the value of its assets decreases substantially, the bank will still have enough to cover customer deposits.

Many banks have a negligible margin of safety… and very few people even realize it until it’s too late.

So if there’s a scenario where banks across the financial system start dumping assets, asset prices will fall very quickly. And banks that have very thin margins of safety will go under.

As we showed earlier, banks can and do go bust.

Even today, the US financial system, as well as those of many other Western countries, especially in Europe, is very fragile.

It is therefore critical to be able to assess the financial health of your bank—and move at least a portion of your savings to a safer institution in a stable jurisdiction overseas.

Last week, we sent an alert to members of Sovereign Man: Confidential scrutinizing the banking systems in Singapore and Hong Kong to analyzing that banks there would be able to weather the storm in case of a wave of Chinese defaults.

This is important analysis. It’s critical to know how well your bank will hold up (or not hold up) in the event of a major financial crisis.

By the way, you don’t have to be wearing a tin foil hat to consider the possibility of crisis.

In the United States, there has hardly been a ten-year period without some sort of major recession, panic, crash, or other crisis.

So it’s a foolish course of action to simply presume that everything will be perfectly fine until the end of time.

www.sovereignman.com6 SMX april 2016

Today we want to show you how you can analyze at least the basic safety levels of your bank yourself.

This is something I have been writing about and talking about for years; in this edition, however, I’d like to make it as simple as possible, so please stick with me:

The four components of a strong, sound bank

If you want to maximize the chances that you never suffer the pain of losing any money in a banking crisis, choose a bank with as many of the following characteristics as possible.

1. A healthy bank maintains adequate (or even excess) reserves with the central bank.

And it can be instructive to look at an entire banking system’s statutory requirement for reserves.

The technical term for this is the “reserve ratio.” Some banking systems, like in Lebanon for example, impose very high reserve requirements on banks. Others are less conservative.

In the United States, reserve requirements can be as low as zero. In Canada, there is no statutory reserve requirement at all.

This means that Canadian and US banks essentially have no requirement to maintain a single penny of customer deposits on reserve. And that, ladies and gentlemen, requires having supreme trust in your bank.

2. A healthy bank holds a high percentage of its customer deposits in assets that can be redeemed instantly without major price fluctuations.

Liquidity is critical. A liquid bank is able to withstand a bank run and minor panic. A liquid bank is able to honor all withdrawal requests without delay because they have the available funds on hand.

www.sovereignman.com7 SMX april 2016

This requires that banks maintain strong reserves (see point #1). It also requires that the investments they make are liquid.

Generally speaking, loans (mortgages, car loans, etc.) are much less liquid than, say, 3-month government bonds.

It will take a bank about one second to liquidate government bonds (particularly US government bonds).

Loans and mortgages, on the other hand, need to be recalled or collateralized in complicated transactions.

They are NOT liquid… especially if everyone else is trying to sell their loans at the same time.

A liquid bank will have a fairly low “loan to deposit ratio”. The fewer loans outstanding relative to the total deposits, the more “liquid” a bank tends to be.

(We’ll show you how to determine this in a few minutes…)

Low loan to deposit ratios indicate that banks should have liquid assets to withstand a bank run.

3. A healthy bank holds strong capital reserves on its balance sheet, so that if some of its assets go bad and become irrecoverable, the bank still has enough funds to repay its depositors and creditors.

The technical measure we look at is called the “capital adequacy ratio.”

There are a number of ways to calculate these ratios, but in essence the idea is to determine how much capital (equity, reserves, etc.) the bank has when compared to its portfolio of assets.

Let’s assume that a bank has $99 in customer deposits.

That same bank has assets (cash, loans, bonds, etc.) totaling $100.

So in the most simplistic terms, the bank’s capital is $1 ($100 minus $99).

That $1 constitutes just 1% of its assets ($1/$100 = 1%). This means that if the value of the bank’s assets suddenly fell by just 1%, the bank would be wiped out and unable to repay its customers.

This is the margin of safety we referred to above. And the greater the capital adequacy, the safer the bank.

4. A healthy bank doesn’t engage in risky lending or investment behavior, so that the likelihood its assets will be impaired in the first place is low.

A good place to check this is to look at the bank’s “non performing loan (NPL) ratio”—both current and historical. And examine the bank’s business model.

For example: Bank A is a community credit union that specializes in making short-term loans backed by real estate in its own neighborhood at a very conservative 2:1 margin (i.e. every $1 loaned is backed by $2 in real estate).

www.sovereignman.com8 SMX april 2016

Bank B uses its depositors’ money to provide no-money-down loans for people with bad credit to buy new cars that will rapidly depreciate.

Clearly Bank A has much safer lending practices, and if you’re a depositor, you’d rather hold your money there.

You should be able to ask your banker (especially if it’s a small bank) about their loan portfolio, and how much is in auto loans, residential real estate, etc.

Find out what their lending conditions are. If the bank is making no-money-down loans with your money, it’s time to find a new bank.

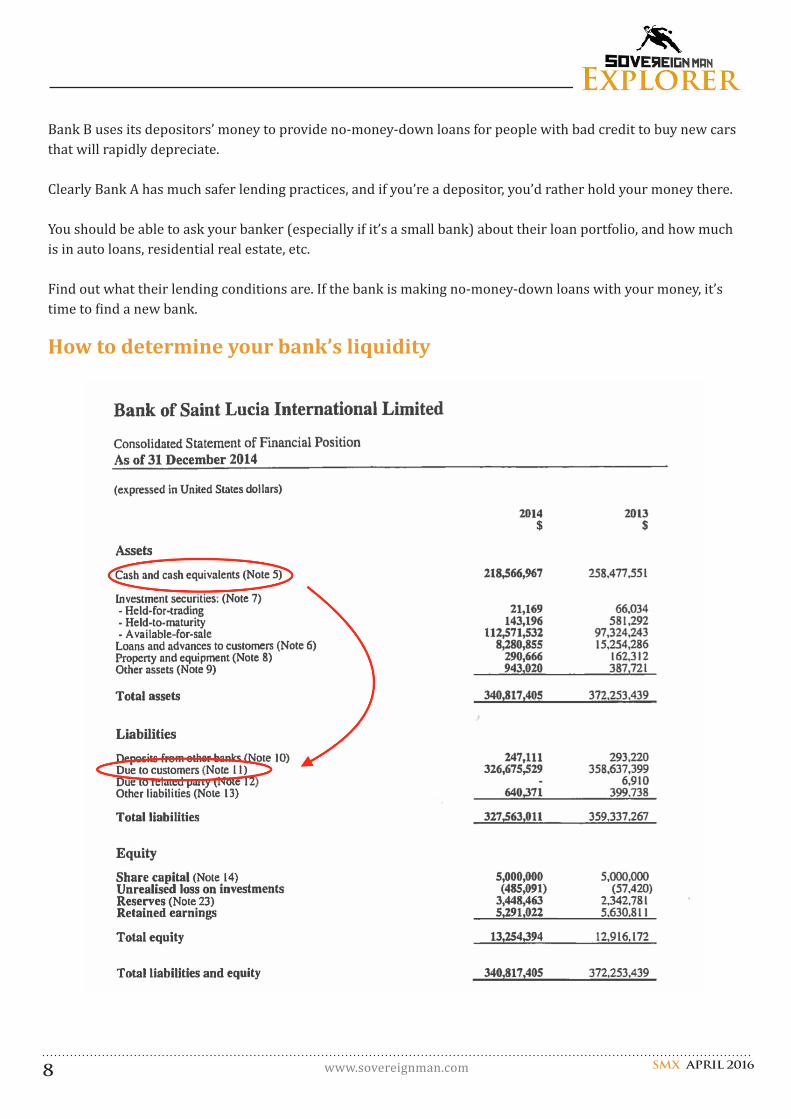

How to determine your bank’s liquidity

www.sovereignman.com9 SMX april 2016

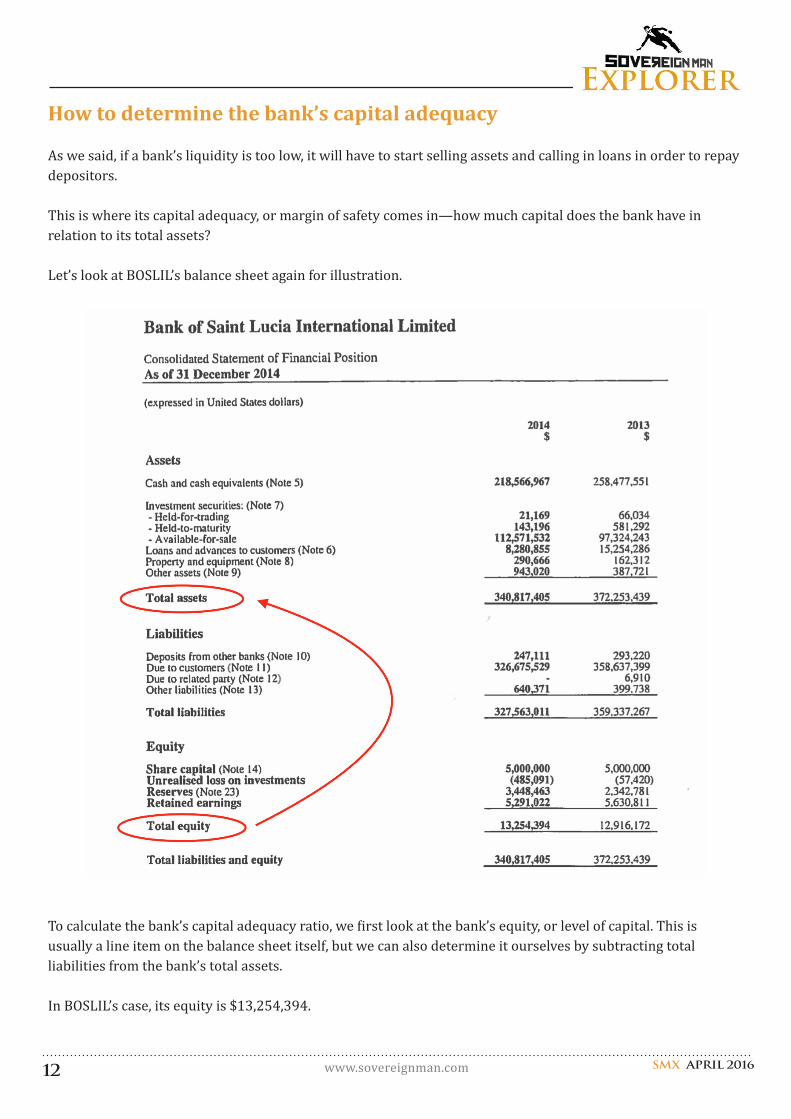

Above is the latest publicly available and audited balance sheet for Bank of St. Lucia International Limited (BOSLIL), which we have discussed with you before.

To broadly determine BOSLIL’s liquidity, let’s look at the following two items on its balance sheet:

• “Cash and cash equivalents” in the asset column. This can include physical cash, as well as government bonds like US Treasuries that can be sold in an instant.

• “Due to customers” in the liability column, which is the total amount that it owes to its retail depositors.

If we divide the two, we get the bank’s liquidity ratio:

$218,566,967 / $326,675,529 = 66.9%

BOSLIL’s liquidity ratio is a phenomenal 66.9%. This is very high.

BOSLIL, of course, doesn’t make any loans, that’s why their liquidity is so high.

(You’ll notice that there’s a “Loans and advances to customers” line on its balance sheet. BOSLIL does make secured loans—i.e. they’ll lend you your own money that’s otherwise tied up in a term deposit or other long-term instrument.)

Not every balance sheet uses the same terms. You might see some banks include things like “Deposits at Central Bank” under the asset column, for example. This should be included in liquidity as well in addition to “cash and cash equivalents.”

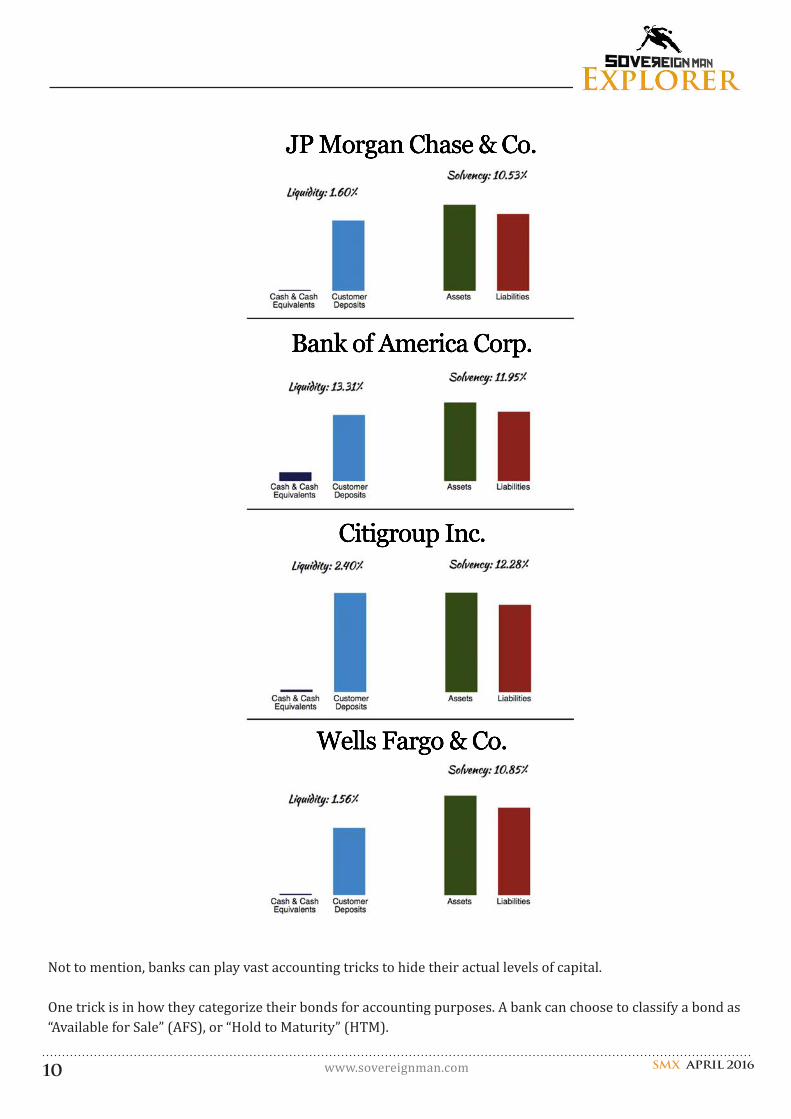

What about US banks?

By global standards, US banks are extremely illiquid, but reasonably solvent at the moment. Sort of.

Big behemoths like Bank of America, JP Morgan Chase, Citigroup, and so on, have become too large to manage. It’s very difficult to know what’s buried in their balance sheets.

Even official numbers, however, are appalling… JP Morgan’s balance sheet reveals that their liquidity ratio is only 1.6%, which is incredibly low.

In other words, if only 1.6% of JP Morgan’s depositors come and withdraw their cash, the bank will run out of money and will have to start selling its assets to honor its obligations.

www.sovereignman.com10 SMX april 2016

JP Morgan Chase & Co.

Bank of America Corp.

Citigroup Inc.

Wells Fargo & Co.

Not to mention, banks can play vast accounting tricks to hide their actual levels of capital.

One trick is in how they categorize their bonds for accounting purposes. A bank can choose to classify a bond as “Available for Sale” (AFS), or “Hold to Maturity” (HTM).

www.sovereignman.com11 SMX april 2016

AFS bonds are exactly that—they’re sitting on the shelf ready to be sold in a heartbeat if the bank needs to increase its liquidity.

But bond prices, just like stock prices, move up and down with great frequency. And accounting rules require banks to disclose the market value of their bond portfolios.

When bond prices fall, the banks’ capital (and profits) fall.

So what do they do? They reclassify their bonds as Hold to Maturity.

HTM basically means that the bond is tucked away forever, and that the bank will never sell it.

Since it will never be sold, an HTM bond doesn’t need to be marked up and down like an AFS bond does.

So when bond prices fall, its good for a bank to reclassify its bonds from AFS to HTM; that way they don’t need to report any losses.

US banking giant BB&T, for example, went from having 0% of its bond portfolio classified as HTM to more than 30% in just one year!

In fact there has been a grand rotation over the last few years among US banks that have reclassified their bonds as HTM (i.e. they don’t have to report losses).

It’s a common trick, and most of the banks do it in the US, which is one of the reasons I’m uncomfortable with the entire system.

Another challenge is with the Federal Reserve itself.

As of April 14, 2016, the Fed has capital of roughly $40 billion on a balance sheet that totals $4.5 trillion.

This means the Fed’s ‘margin of safety’ is just 0.89%, i.e. the central bank that issues the world’s biggest reserve currency is borderline insolvent.

This is an astonishingly low level of capital, and it sets the tone for the entire US banking system.

Then there’s the FDIC—the US deposit insurance scheme, which has very little capital backing up its “guarantee”.

And of course, backing up the entire system is the greatest debtor in the history of the world—the insolvent United States government.

So bottom line, the US banking system is supported by an insolvent government, a nearly insolvent central bank, and an undercapitalized insurance scheme.

Which brings us to…

www.sovereignman.com12 SMX april 2016

How to determine the bank’s capital adequacy

As we said, if a bank’s liquidity is too low, it will have to start selling assets and calling in loans in order to repay depositors.

This is where its capital adequacy, or margin of safety comes in—how much capital does the bank have in relation to its total assets?

Let’s look at BOSLIL’s balance sheet again for illustration.

To calculate the bank’s capital adequacy ratio, we first look at the bank’s equity, or level of capital. This is usually a line item on the balance sheet itself, but we can also determine it ourselves by subtracting total liabilities from the bank’s total assets.

In BOSLIL’s case, its equity is $13,254,394.

www.sovereignman.com13 SMX april 2016

We then take this number and divide it by the bank’s total assets.

The capital ratio the we get for BOSLIL is 3.89%.

This is a low capital ratio. But it’s important to look at the two numbers together (i.e. both capital AND liquidity).

A liquid bank in a well-capitalized jurisdiction doesn’t need as high of a margin of safety as a bank with very low liquidity in a country with an insolvent government.

As we calculated earlier, BOSLIL’s liquidity is 66.9%. So its low capital ratio (and the fact that the bank doesn’t loan money) isn’t as much of a concern.

Bottom line

Having a Plan B covers different components of your life. There’s a personal component. There’s a legal component. There’s a financial component.

We discuss all of them in this publication.

Part of the financial component is safeguarding your wealth from the dangers in the financial system.

We write about this often—a great way to reduce financial risks is to employ a three-part strategy:

1. Hold physical cash. This eliminates counterparty risk in the event of a banking crisis. If bank’s freeze accounts, or go under, you’ll still have cash. We recommend holding a few months’ worth of savings—but don’t go overboard.

2. Own physical gold. This eliminates risks in the monetary system. If entire central banks and currencies that they issue fall into turmoil, cash won’t help you much.

www.sovereignman.com14 SMX april 2016

But owning physical gold (preferably stored in a secure jurisdiction overseas) will uphold at least a portion of your wealth.

Again, don’t go overboard with gold either. Own as much as makes you comfortable.

If you’re worried about the price of gold, laying awake at night checking the Gold Price app on your mobile phone, it may be a good indicator that you own too much.

Listen to your instincts.

3. Have an account at a safe bank, preferably overseas.

Having a safe foreign account not only provides greater financial security for your savings, but it also creates an additional layer of asset protection.

No one ever expects it to happen, but if you ever find yourself being frivolously sued or wrongfully accused, any funds you have in your home country can be frozen in an instant.

Having a bank account overseas in a safe jurisdiction (as well as cash and gold) ensures that you will have some additional savings set aside if that rainy day ever comes.

The largest part of your savings is probably going to be in the banking system; banks are still currently the most convenient way to operate within the financial system.

But as you can probably see by now, not all banks are created equal.

Some banks are very safe, while others are terribly shaky.

And it’s important to distinguish between them, at least on a basic level.

So, make this part of your Plan B: be able to analyze your financial partner, so that when you deposit your savings, you can have a strong sense of comfort that’s backed by hard numbers.