isa implementation support module prepared by iaasb staff october 2010 materiality, misstatements...

TRANSCRIPT

ISA Implementation Support Module

Prepared by IAASB Staff

October 2010

Materiality, Misstatements and Reporting − Part II

2

(Old) ISA 320

(Revised) ISA 320

(New) ISA 450

(Amended) ISA 700

(Old) ISA 700

Overview of Module

• Significant Features of New Standard

– Definition of Misstatement

– Judgments Involved

– Communication and Correction of Misstatements

– Evaluation of Uncorrected Misstatements

– Written Representations

– Documentation

Overview of ISA 450

3

• Misstatement = difference between what is reported and what is expected by the FRF or needed for true and fair view/fair presentation

• Misstatements include

– Factual misstatements

– Judgmental misstatements

– Projected misstatements

• Clearly trivial misstatements are not considered in evaluation of identified misstatements

Definition of Misstatement

4

Judgments Involved

5

Overall audit strategy and audit plan

Accumulate misstatements other than those that are clearly trivial as audit progresses

If nature of misstatements indicate others may exist, or aggregate approaches materiality

Revision needed?

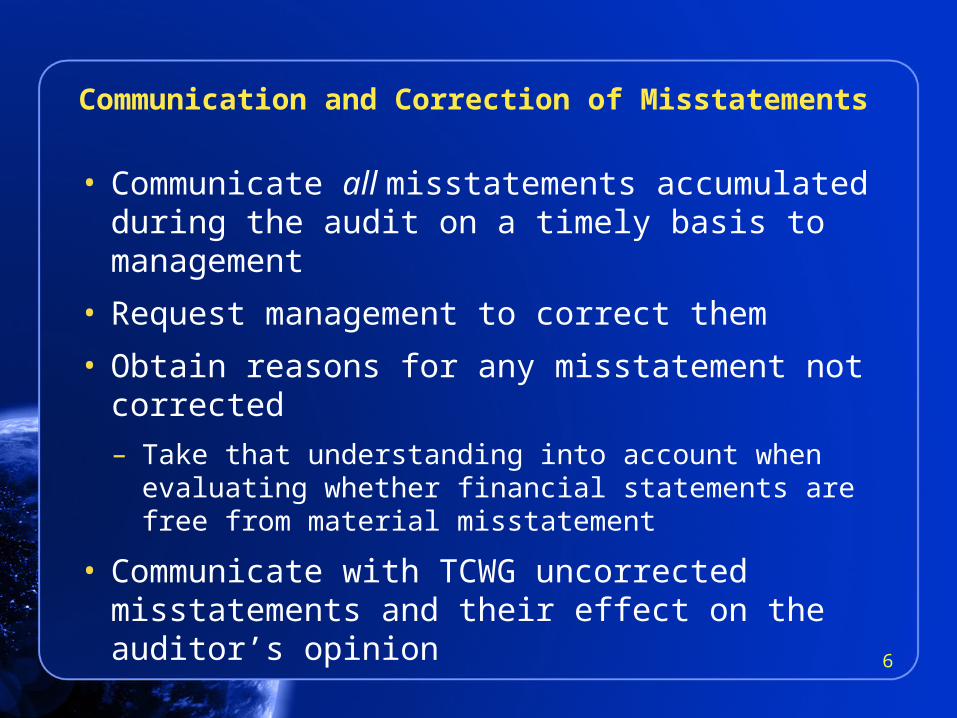

• Communicate all misstatements accumulated during the audit on a timely basis to management

• Request management to correct them

• Obtain reasons for any misstatement not corrected

– Take that understanding into account when evaluating whether financial statements are free from material misstatement

• Communicate with TCWG uncorrected misstatements and their effect on the auditor’s opinion

Communication and Correction of Misstatements

6

• Before evaluation, reassess materiality levels for financial statements as a whole and specific amounts

• Evaluate effect on financial statements, both individually and in aggregate

– Consider size and nature

– Circumstances of occurrence

– Effect of uncorrected prior-period misstatements

Evaluation of Uncorrected Misstatements

7

• Obtain written representation from management and, where appropriate, TCWG whether they believe effects of uncorrected misstatements are, individually and in aggregate, immaterial to financial statements as a whole

• Include or attach a summary of the uncorrected items to the written representation

Written Representations

8

• Document

– The amount below which misstatements would be regarded as clearly trivial

– All misstatements accumulated and whether they have been corrected

– Conclusion as to whether uncorrected misstatements are material, individually and in aggregate, and basis for that conclusion

Documentation

9

Note

This set of support slides does not amend or override the ISAs, the texts of which alone are authoritative. Reading the slides is not a substitute for reading the ISAs. The slides are not meant to be exhaustive and reference to the ISAs themselves should always be made. In conducting an audit in accordance with ISAs, the auditor is required to comply with all the ISAs that are relevant to the engagement.

10

Copyright © October 2010 by the International Federation of Accountants (IFAC). All rights reserved. Permission is granted to make copies of this work provided that such copies are for use in academic classrooms or for personal use and are not sold or disseminated and provided that each copy bears the following credit line: “Copyright © October 2010 by the International Federation of Accountants (IFAC). All rights reserved. Used with permission of IFAC. Contact [email protected] for permission to reproduce, store, or transmit this work.” Otherwise, written permission from IFAC is required to reproduce, store, or transmit, or to make other similar uses of, this work, except as permitted by law. Contact [email protected].

International Federationof Accountants

ISBN: 978-1-60815-077-9

www.ifac.org