islamic finance bulletin

DESCRIPTION

November 2012TRANSCRIPT

Islamic Finance Bulletin

November 2012

www.lums.lancs.ac.uk/research/centres/golcer/

Gulf One Lancaster Centre For Economic Research

Page 2

From the TeamThere is probably more to feature in terms of institutional change this month than in respect of any strength in market direction.

Stocks and bonds have tended relatively speaking to tread water, considering the uncertainty arising from political impasse on budgetary and financial affairs in both the US and Europe. Likewise, political tran-sition in China has not left any sense of dynamism overcoming inertia. As weather vanes of the global economy, commodities have not inspired confidence either.

More notable then, are further signs of Islamic finance’s progress in Malaysia, where merger and consoli-dation may build upon the sector’s advances so far, and the potential for the industry’s breakthrough in the mass market that is India.

Frankly, we may wait considerably longer for the kinds of market-oriented structural reform that might stand a chance of kickstarting economic growth in the Western world, still operating a fairly one-di-mensional approach to reigniting demand. And it is that missing factor which may be necessary to give conventional assets the prompting necessary to restore self-sustaining confidence. Tending still to be governed ultimately by much the same global influences, Islamic indices are likely to be similarly affected.

In the meantime, the likes of copper, gold and oil prices have shown a distinctly soft side, reflecting the weakness in economic activity and outlook. If inflation picks up, however, as some policy makers appear to have noticed it might, then markets will have another cue to reckon with.

ContentsHIGHLIGHTS (p.3)

RECENT DEVELOPMENTS (p.4)

STOCK MARKETS (p.6)

COMMODITIES (p.9)

BOND AND CDS MARKETS (p.11)

ACCOUNTANCY ISSUES (p.14)

PERSPECTIVE (p.15)

DIARY OF EVENTS (p.16)

Page 3

Malaysia: As a foremost centre in Islamic finance, Malaysia appears to be sustaining its momentum. Although the sector has shown a reluctance to pursue mergers between its in-stitutions, and a shifting attitude appears to be geared to coping with cost structures, talk of tie-ups in the industry may lead to greater criti-cal mass to compete with conventional banks. In the meantime, significant IPOs are helping to cement the country’s emerging reputation. (Recent Developments)

Oil & Gas: Conditions specific to the US economy sparked oil and gas prices in different directions within the past month. Weak economic data and the accumulation of crude oil stockpiles added to the existing level of inventory restraint on the WTI benchmark, as well as the development of shale. At the same time the devastation brought by Hur-ricane Sandy applied the opposite pressure to prices already elevated by the onset of the winter season. (Commodities)

India: Discussions between the government and central bank, following other meetings between and reports by national bodies, suggest that In-dia is making steps towards accommodating the Islamic model within its general banking sys-tem. Investigations so far seem to suggest that decisive steps towards such a breakthrough in financial provision would involve adjustment to taxation rather than banking laws themselves. (Accountancy Issues)

Highlights

Recent Developments in the Islamic Finance Industry

Malaysia’s Islamic banks seek consolidation

While Islamic banks since their inception have shown reluctance towards merging, recently it has become clear that they are now ready for that evolution in Malaysia, one of the big-gest hubs of Islamic finance. For example, Bank Muamalat Malaysia Bhd is in the process of approving an M&A deal for US$143.6bn. Islamic finance in Malaysia has shown sub-stantial growth, now accounting for 23.7% of total banking assets. The current calls for M&A in Islamic banking result from the need to cope with rising operational costs, and the insufficient professional experience of some Islamic bank managers for running operations successfully in compliance with Shariah. Islamic banks in the past have opposed the idea of M&A, fearing a loss of control, as the sector discourages risk-taking.

From GOLCER’s point of view, we find this step a remarkable initiative that will tend to create conglomerates of Islamic banks, with the pros-pect of matching or outperforming conventional banks, given the current fierce competition between the two banking sectors.

Source: Arabian Business News.Com, October 18th

ADIB promotes global ethical business

Abu Dhabi Islamic Bank (ADIB), a top-tier Islamic financial institution, has engaged in marketing Islamic finance as an ethical and sus-tainable business model worldwide. The bank was exclusive sponsor at the inaugural episode of ‘Faith in Finance’, a new six-part series launched by Bloomberg TV. The programme emphasized the view of Islamic banking as not only an ethical business model but one which

will eventually be more profitable to shareholders and investors in the medium and long terms. That idea taps into the fear and experience of inves-tors and depositors losing capital, as well as the substantial demand for ethical banking. Islamic finance principles are essentially identified with their ethical and moral dimensions. Source: AMEinfo.com, October 28th

World Bank and IDB sign Islamic finance deal

A three-year agreement between the World Bank and the Jeddah-based Islamic Development Bank (IDB) has been signed to share expertise in Islamic finance as well as study its impact on developing economies. The IDB comprises 56 member coun-tries. The bank seeks to provide financing, loans and technical assistance promoting developmental paths which are consistent with Shariah. Under this deal the two bodies will cooperate to investigate issues in Islamic finance related to areas such as financial stability as well as promote best practices in the industry. GOLCER takes the view that, since Islamic finance and banking is expanding tremendously nowa-days, studying this phenomenon in terms of its stability and its financial as well as social contribu-tions to the public has become essential. We also consider that this collaboration is likely to have a massive impact on industry practice in the near

Page 4

future, given the recent trend toward adopting Islamic finance in many countries like Egypt, Libya and Tunisia.

Source EIN news, October 18th

Islamic finance struggling in Azerbaijan

Existing policies in Azerbaijan towards Islamic finance, particularly by the government, show an obvious fear from the political perspective about expanding this sector. Over recent years sever-al banks in Azerbaijan have offered a limited range of services along Islamic principles. The coun-try’s largest bank, considered a public bank, has opened an “Islamic window” providing finance to small companies. A limited number of conventional banks are allowed Islamic windows. There are no banks operating purely as Islamic institutions.The Azerbaijan government is reluctant to take the critical step of stipulating legislation to regulate the industry and aid its expansion, as well as enable the issuance of Sukuk (Islamic bonds). That stance is attributable to fears that Islamic finance could en-courage Islamist politics in a country in which 93% of the population are Muslims.Source: Reuters, October 16th

Dubai’s Emicool signs $216 million Islamic loan

A joint venture between Dubai Investments and Union Properties, Dubai-based Emirates District Cooling (Emicool), has signed a 793 million dirham ($216 million) Islamic loan guaranteed by both par-ents. The 10-year credit facility has been structured according to Shariah requirements. Its purpose is to refinance a 668 million dirham bridge loan and other facilities to finance the construction of cooling plants within the emirate.

GOLCER finds that this substantial loan is likely to set an obvious lead in increasing demand for Islam-

ic banking instruments. It is also likely to convey positive signals to different parties as stakeholders in the banking sector.

Source: Reuters, October 21st

IILM hires new chief executive

The International Islamic Liquidity Management Corp (IILM), backed by central banks located mainly in Asia and the Middle East, has ap-pointed a new CEO ahead of its first issuance of Sukuk of $300 to $500 million within the next few months. The main rationale of this company is to help Islamic banks in managing their liquidity, as well as facilitate liquidity across the industry’s Islamic instruments. IILM has faced a challenge in promoting compliance with Islamic laws among members in the participating countries. The members include monetary authorities in Indone-sia, Iran, Kuwait, Luxembourg, Malaysia, Mauri-tius, Nigeria, Qatar, Saudi Arabia, Sudan, Turkey and the United Arab Emirates, as well as the Islamic Development bank and the Islamic Corpo-ration for the Development of the Private Sector.

Source: Reuters, October 19th

Page 5

Page 6

With sentiment preoccupied with worries over the US fiscal cliff and continuing recession and tensions in the Eurozone, markets worldwide were fairly gloomy in October. The US has little time to solve its budgetary dilemma. As the Financial Times explained, if by this year-end the US government doesn’t come up with a resolution, then the economy will be hit by a USD 600 bn tax increase and USD 100 bn spending cut which would threaten another recession in the first half of next year, GDP projected to contract by 4%. Taxes would penalize dividends and capital gains, and spending cuts would affect those companies which depend on the state sector the most, namely health care and defence contracting.

GCC

Markets in the GCC region were mixed. Saudi Arabia, Kuwait and Bahrain closed in the red while Oman, UAE and Qatar showed positive returns. With trading being very thin owing to the religious holi-days, much of the stock movements were based on global headlines, tending to the negative. Moreover, the IMF has warned the GCC countries to cut back on their state spending, predicting deficits in the next five years. Should a deep recession hit the world econo-my, oil prices would plunge and oil producers would be the most affected. The UAE’s index rose by 4.2% after HSBC’s PMI index climbed through the 50 mark, reflecting non-oil sectors, and Fitch Ratings suggested a strong start for the retail and hospitality industry in Dubai in 2013. However, the Kuwaiti index fell by

2.6% owing to more country specific factors. A tense socio-political situation and related pro-tests damaged investor sentiment. The Oman index rose by 4.8% on the month upon increased oil production and rising demand from the Asian market.

MENA

The Centamin verdict in Egypt outweighed the hopes of foreign investors as to the long awaited billion dollar loan from the IMF. The Egyptian court suspended the operations of the foreign company, which ran a gold mine in Egypt, citing irregularities in the renewal of its contract. The Egyptian index dipped by 5.2%, while the Leba-nese index fell by 2.6% as a result of a sluggish economy over the past several months. Figures showed the country’s trade deficit expanding by 13.9% year on year during the first nine months of the year.

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct65.5

66

66.5

67

67.5

68

68.5

Isla

mic

In

de

x

93

93.5

94

94.5

95

95.5

96

96.5

97

Co

nv

en

tio

na

l In

de

x

GCC

0.976836Correlation (1 mth)

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct800

820

840

860

880

900

920

Eg

yp

t Is

lam

ic I

nd

ex

310

320

330

340

350

360

ME

NA

Ag

gre

ga

te I

nd

ex

MENA

0.2244Correlation (1 mth)

Stock Markets

Page 6

Page 7

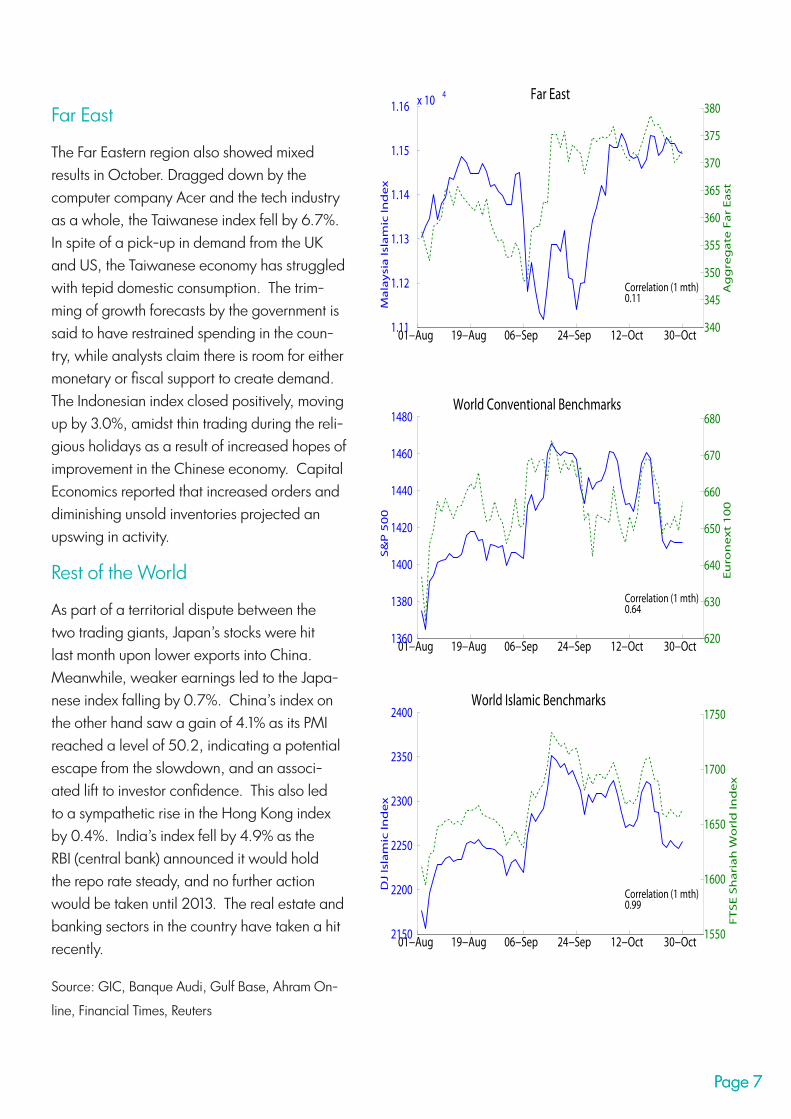

Far East

The Far Eastern region also showed mixed results in October. Dragged down by the computer company Acer and the tech industry as a whole, the Taiwanese index fell by 6.7%. In spite of a pick-up in demand from the UK and US, the Taiwanese economy has struggled with tepid domestic consumption. The trim-ming of growth forecasts by the government is said to have restrained spending in the coun-try, while analysts claim there is room for either monetary or fiscal support to create demand. The Indonesian index closed positively, moving up by 3.0%, amidst thin trading during the reli-gious holidays as a result of increased hopes of improvement in the Chinese economy. Capital Economics reported that increased orders and diminishing unsold inventories projected an upswing in activity.

Rest of the World

As part of a territorial dispute between the two trading giants, Japan’s stocks were hit last month upon lower exports into China. Meanwhile, weaker earnings led to the Japa-nese index falling by 0.7%. China’s index on the other hand saw a gain of 4.1% as its PMI reached a level of 50.2, indicating a potential escape from the slowdown, and an associ-ated lift to investor confidence. This also led to a sympathetic rise in the Hong Kong index by 0.4%. India’s index fell by 4.9% as the RBI (central bank) announced it would hold the repo rate steady, and no further action would be taken until 2013. The real estate and banking sectors in the country have taken a hit recently.

Source: GIC, Banque Audi, Gulf Base, Ahram On-

line, Financial Times, Reuters

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct1.11

1.12

1.13

1.14

1.15

1.16 x 10 4

Ma

lay

sia

Isla

mic

Ind

ex

340

345

350

355

360

365

370

375

380

Ag

gre

ga

te F

ar

Ea

st

Far East

0.117483Correlation (1 mth)

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct1360

1380

1400

1420

1440

1460

1480

S&

P 5

00

620

630

640

650

660

670

680

Eu

ron

ex

t 1

00

World Conventional Benchmarks

0.64223Correlation (1 mth)

Page 7

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct2150

2200

2250

2300

2350

2400

DJ

Isla

mic

Ind

ex

1550

1600

1650

1700

1750World Islamic Benchmarks

FT

SE

Sh

ari

ah

Wo

rld

Ind

ex

0.991131Correlation (1 mth)

Islamic or Shariah compli-ant indices exclude indus-tries whose lines of busi-

ness incorporate forbidden goods or where debts/

assets ratios exceed 33%. The increasing popular-ity of Islamic finance has

led to the establishment of Shariah compliant stock

indices in many stock markets across the world, even where local Muslim populations are relatively

small, such as in China and Japan.

Volatility is a measure of un-certaincy of market returns. It is calculated as the standard deviation of the returns in the reported month. The formula for the standard deviation is:

σ=E[(X-μ)2]1/2

Page 8

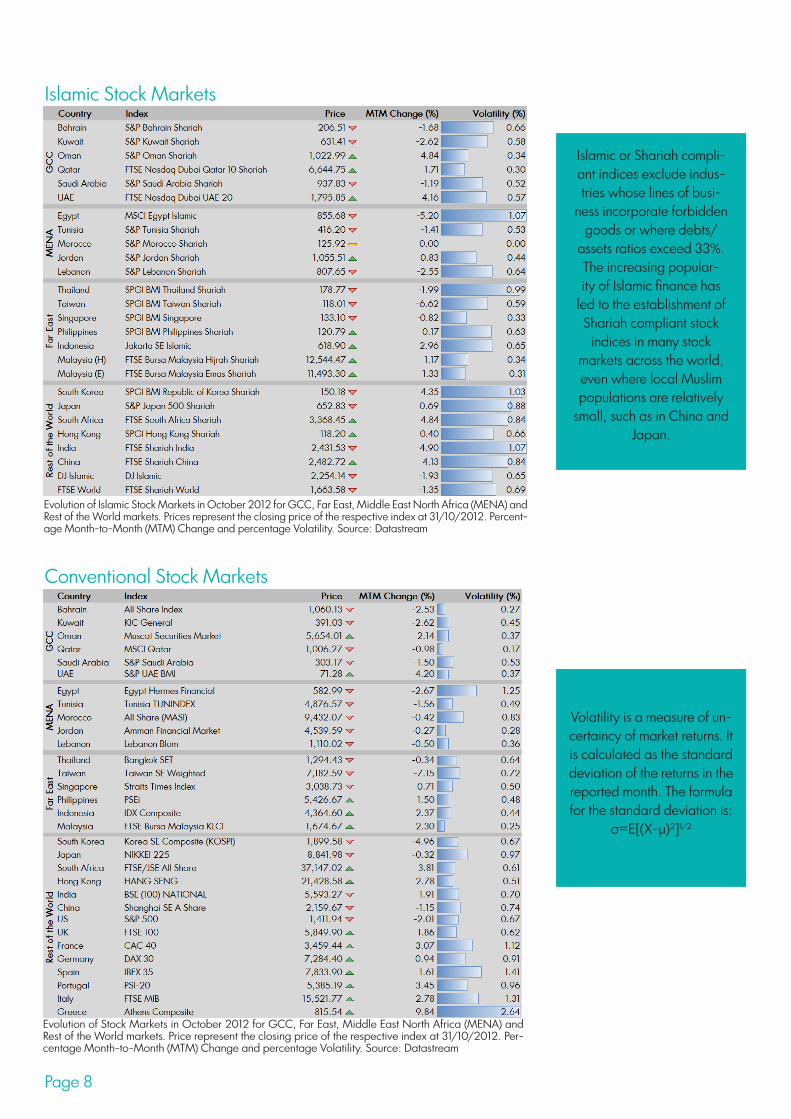

Islamic Stock Markets

Conventional Stock Markets

Evolution of Islamic Stock Markets in October 2012 for GCC, Far East, Middle East North Africa (MENA) and Rest of the World markets. Prices represent the closing price of the respective index at 31/10/2012. Percent-age Month-to-Month (MTM) Change and percentage Volatility. Source: Datastream

Evolution of Stock Markets in October 2012 for GCC, Far East, Middle East North Africa (MENA) and Rest of the World markets. Price represent the closing price of the respective index at 31/10/2012. Per-centage Month-to-Month (MTM) Change and percentage Volatility. Source: Datastream

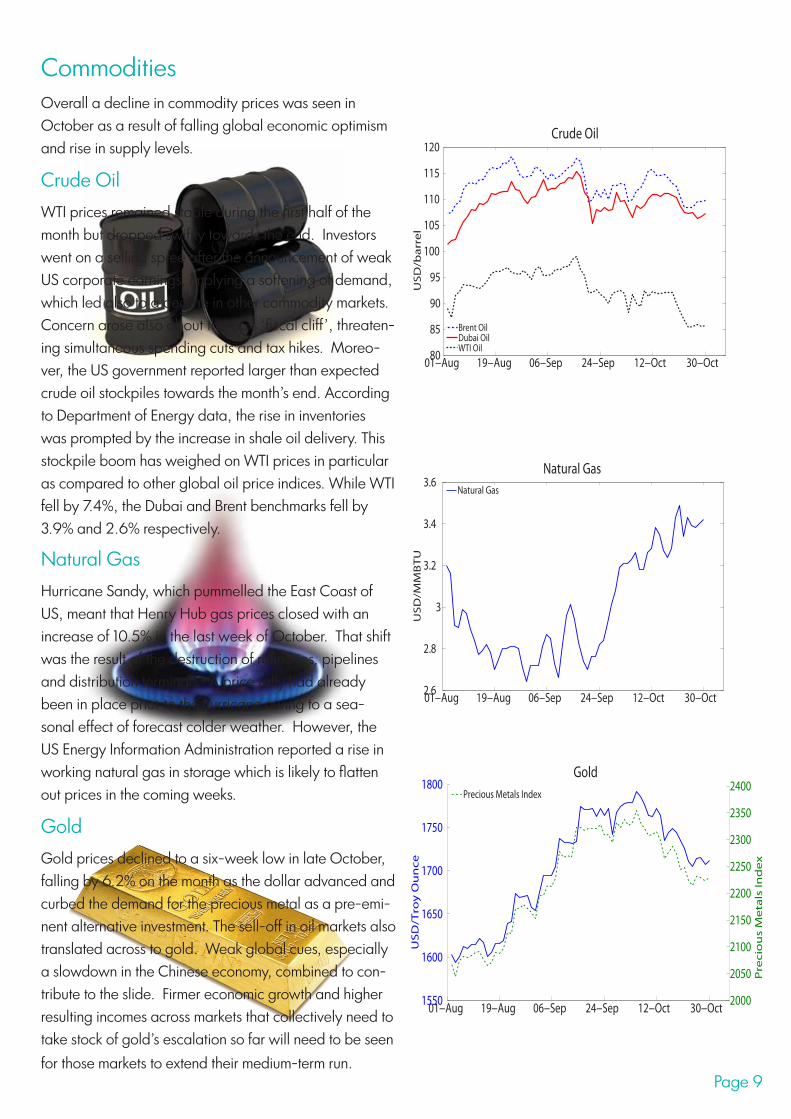

CommoditiesOverall a decline in commodity prices was seen in October as a result of falling global economic optimism and rise in supply levels.

Crude OilWTI prices remained stable during the first half of the month but dropped swiftly towards the end. Investors went on a selling spree after the announcement of weak US corporate earnings, implying a softening of demand, which led also to a decline in other commodity markets. Concern arose also about the US’s ‘fiscal cliff’, threaten-ing simultaneous spending cuts and tax hikes. Moreo-ver, the US government reported larger than expected crude oil stockpiles towards the month’s end. According to Department of Energy data, the rise in inventories was prompted by the increase in shale oil delivery. This stockpile boom has weighed on WTI prices in particular as compared to other global oil price indices. While WTI fell by 7.4%, the Dubai and Brent benchmarks fell by 3.9% and 2.6% respectively.

Natural GasHurricane Sandy, which pummelled the East Coast of US, meant that Henry Hub gas prices closed with an increase of 10.5% in the last week of October. That shift was the result of the destruction of refineries, pipelines and distribution terminals. A price rally had already been in place prior to the hurricane owing to a sea-sonal effect of forecast colder weather. However, the US Energy Information Administration reported a rise in working natural gas in storage which is likely to flatten out prices in the coming weeks.

GoldGold prices declined to a six-week low in late October, falling by 6.2% on the month as the dollar advanced and curbed the demand for the precious metal as a pre-emi-nent alternative investment. The sell-off in oil markets also translated across to gold. Weak global cues, especially a slowdown in the Chinese economy, combined to con-tribute to the slide. Firmer economic growth and higher resulting incomes across markets that collectively need to take stock of gold’s escalation so far will need to be seen for those markets to extend their medium-term run.

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct2.6

2.8

3

3.2

3.4

3.6Natural Gas

US

D/M

MB

TU

Natural Gas

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct80

85

90

95

100

105

110

115

120Crude Oil

US

D/b

arr

el

Brent OilDubai OilWTI Oil

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct1550

1600

1650

1700

1750

1800

US

D/T

roy

Ou

nce

2000

2050

2100

2150

2200

2250

2300

2350

2400

Pre

cio

us

Me

tals

Ind

ex

Gold

Precious Metals Index

Page 9

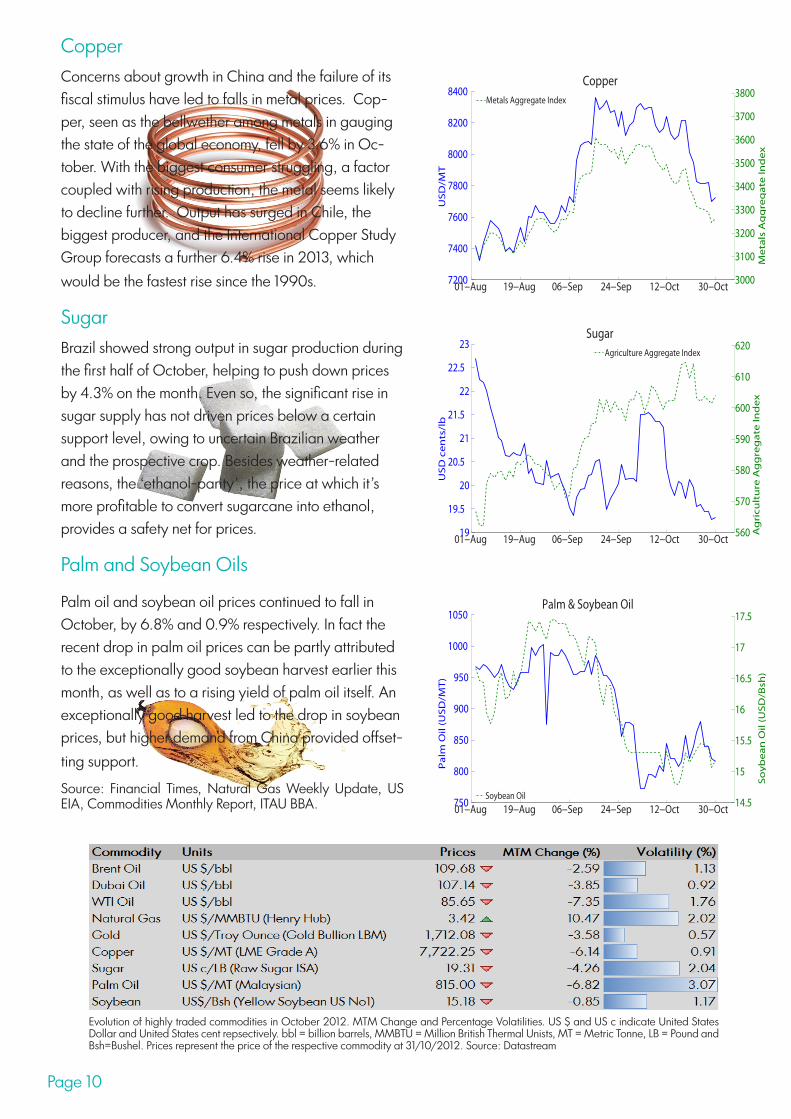

CopperConcerns about growth in China and the failure of its fiscal stimulus have led to falls in metal prices. Cop-per, seen as the bellwether among metals in gauging the state of the global economy, fell by 3.6% in Oc-tober. With the biggest consumer struggling, a factor coupled with rising production, the metal seems likely to decline further. Output has surged in Chile, the biggest producer, and the International Copper Study Group forecasts a further 6.4% rise in 2013, which would be the fastest rise since the 1990s.

SugarBrazil showed strong output in sugar production during the first half of October, helping to push down prices by 4.3% on the month. Even so, the significant rise in sugar supply has not driven prices below a certain support level, owing to uncertain Brazilian weather and the prospective crop. Besides weather-related reasons, the ‘ethanol-parity’, the price at which it’s more profitable to convert sugarcane into ethanol, provides a safety net for prices.

Palm and Soybean Oils

Palm oil and soybean oil prices continued to fall in October, by 6.8% and 0.9% respectively. In fact the recent drop in palm oil prices can be partly attributed to the exceptionally good soybean harvest earlier this month, as well as to a rising yield of palm oil itself. An exceptionally good harvest led to the drop in soybean prices, but higher demand from China provided offset-ting support.

Source: Financial Times, Natural Gas Weekly Update, US EIA, Commodities Monthly Report, ITAU BBA.

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct7200

7400

7600

7800

8000

8200

8400

US

D/M

T

3000

3100

3200

3300

3400

3500

3600

3700

3800

Me

tals

Ag

gre

gat

e In

de

x

Copper

Metals Aggregate Index

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct19

19.5

20

20.5

21

21.5

22

22.5

23

US

D c

en

ts/l

b

560

570

580

590

600

610

620

Ag

ricu

ltu

re A

gg

reg

ate

Ind

ex

Sugar

Agriculture Aggregate Index

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct750

800

850

900

950

1000

1050

Pal

m O

il (U

SD

/MT

)

14.5

15

15.5

16

16.5

17

17.5

So

ybe

an O

il (U

SD

/Bsh

)

Palm & Soybean Oil

Soybean Oil

Evolution of highly traded commodities in October 2012. MTM Change and Percentage Volatilities. US $ and US c indicate United States Dollar and United States cent repsectively. bbl = billion barrels, MMBTU = Million British Thermal Unists, MT = Metric Tonne, LB = Pound and Bsh=Bushel. Prices represent the price of the respective commodity at 31/10/2012. Source: Datastream

Page 10

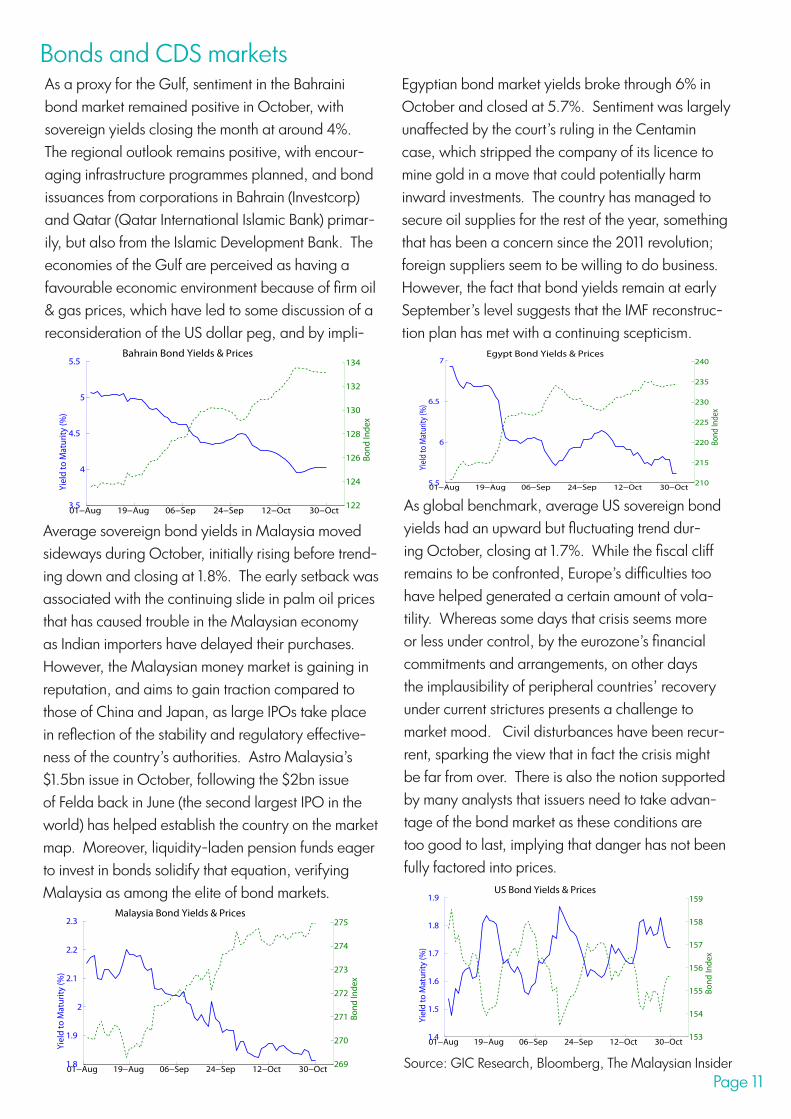

As a proxy for the Gulf, sentiment in the Bahraini bond market remained positive in October, with sovereign yields closing the month at around 4%. The regional outlook remains positive, with encour-aging infrastructure programmes planned, and bond issuances from corporations in Bahrain (Investcorp) and Qatar (Qatar International Islamic Bank) primar-ily, but also from the Islamic Development Bank. The economies of the Gulf are perceived as having a favourable economic environment because of firm oil & gas prices, which have led to some discussion of a reconsideration of the US dollar peg, and by impli-

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct3.5

4

4.5

5

5.5

Yiel

d to

Mat

urity

(%)

122

124

126

128

130

132

134Bo

nd In

dex

Bahrain Bond Yields & Prices

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct5.5

6

6.5

7

Yiel

d to

Mat

urity

(%)

210

215

220

225

230

235

240Egypt Bond Yields & Prices

Bond

Inde

x

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct1.4

1.5

1.6

1.7

1.8

1.9

Yiel

d to

Mat

urity

(%)

153

154

155

156

157

158

159US Bond Yields & Prices

Bond

Inde

x

01−Aug 19−Aug 06−Sep 24−Sep 12−Oct 30−Oct1.8

1.9

2

2.1

2.2

2.3

Yiel

d to

Mat

urity

(%)

269

270

271

272

273

274

275Malaysia Bond Yields & Prices

Bond

Inde

x

Source: GIC Research, Bloomberg, The Malaysian Insider

Egyptian bond market yields broke through 6% in October and closed at 5.7%. Sentiment was largely unaffected by the court’s ruling in the Centamin case, which stripped the company of its licence to mine gold in a move that could potentially harm inward investments. The country has managed to secure oil supplies for the rest of the year, something that has been a concern since the 2011 revolution; foreign suppliers seem to be willing to do business. However, the fact that bond yields remain at early September’s level suggests that the IMF reconstruc-tion plan has met with a continuing scepticism.

Average sovereign bond yields in Malaysia moved sideways during October, initially rising before trend-ing down and closing at 1.8%. The early setback was associated with the continuing slide in palm oil prices that has caused trouble in the Malaysian economy as Indian importers have delayed their purchases. However, the Malaysian money market is gaining in reputation, and aims to gain traction compared to those of China and Japan, as large IPOs take place in reflection of the stability and regulatory effective-ness of the country’s authorities. Astro Malaysia’s $1.5bn issue in October, following the $2bn issue of Felda back in June (the second largest IPO in the world) has helped establish the country on the market map. Moreover, liquidity-laden pension funds eager to invest in bonds solidify that equation, verifying Malaysia as among the elite of bond markets.

As global benchmark, average US sovereign bond yields had an upward but fluctuating trend dur-ing October, closing at 1.7%. While the fiscal cliff remains to be confronted, Europe’s difficulties too have helped generated a certain amount of vola-tility. Whereas some days that crisis seems more or less under control, by the eurozone’s financial commitments and arrangements, on other days the implausibility of peripheral countries’ recovery under current strictures presents a challenge to market mood. Civil disturbances have been recur-rent, sparking the view that in fact the crisis might be far from over. There is also the notion supported by many analysts that issuers need to take advan-tage of the bond market as these conditions are too good to last, implying that danger has not been fully factored into prices.

Bonds and CDS markets

Page 11

A Credit Default Swap (CDS) is de-signed to transfer the credit exposure of fixed income products between parties.

A CDS is also referred to as a credit derivative contract, where the purchaser of the swap makes payments up until the maturity date of a contract. The buyer of the CDS makes a series of payments (the CDS “fee” or “spread” quoted in basis points) to the seller and, in exchange, receives a payoff if the loan defaults.

Riskier economies will have higher CDS “spreads”. The CDS spread can be more informative on the risk of the country as the CDS market is more liquid than the

bond market.

Page 12

Credit Default Swap Markets

Sovereign Bond Markets

Evolution of Bond Markets in October 2012 relative to the previous month. The table reports the price index on which the MTM Change is calculated (month-to-month) and the Yield of sovereign bond maturities typically between 6 months and 25 years. Data as at 31/10/2012.

Evolution of CDS Spreads in October 2012 relative to the previ-ous month. The index reported here represents the average ba-sis points (bp) of a 5-year CDS for protection against sovereign bonds. Data as at 31/10/2012. MTM Change refers to the change relative to the previous month.

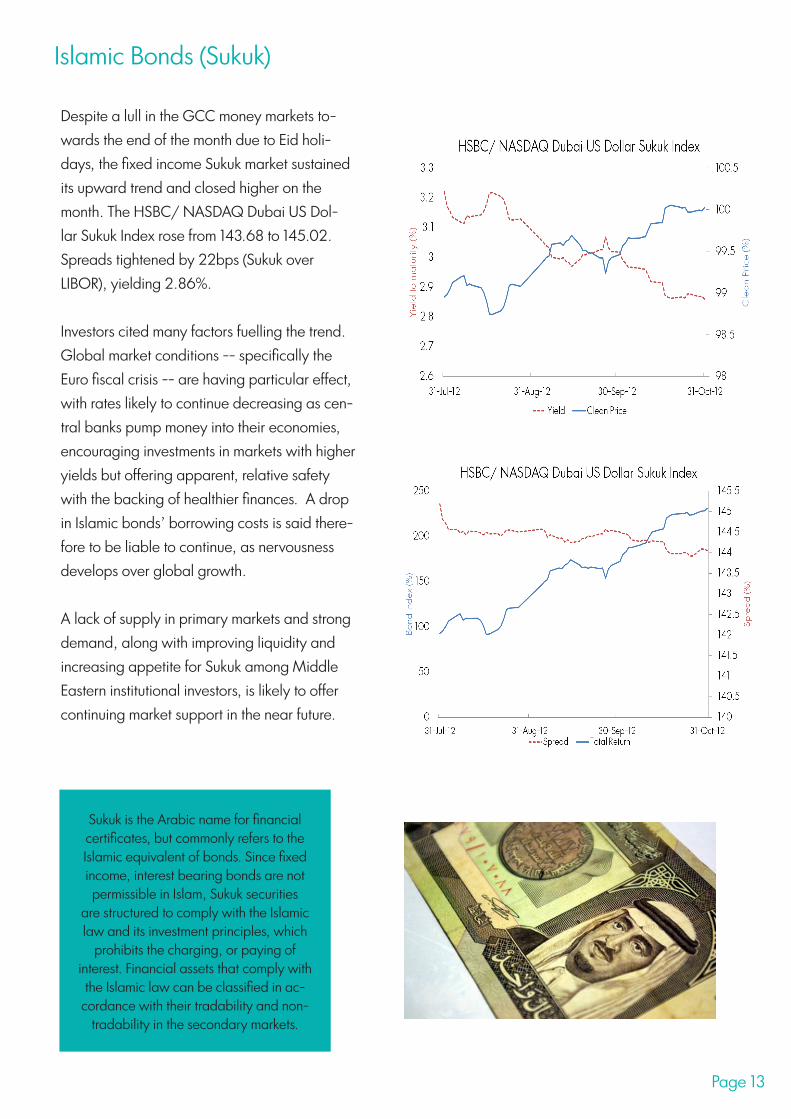

Islamic Bonds (Sukuk)

Despite a lull in the GCC money markets to-wards the end of the month due to Eid holi-days, the fixed income Sukuk market sustained its upward trend and closed higher on the month. The HSBC/ NASDAQ Dubai US Dol-lar Sukuk Index rose from 143.68 to 145.02. Spreads tightened by 22bps (Sukuk over LIBOR), yielding 2.86%.

Investors cited many factors fuelling the trend. Global market conditions -- specifically the Euro fiscal crisis -- are having particular effect, with rates likely to continue decreasing as cen-tral banks pump money into their economies, encouraging investments in markets with higher yields but offering apparent, relative safety with the backing of healthier finances. A drop in Islamic bonds’ borrowing costs is said there-fore to be liable to continue, as nervousness develops over global growth. A lack of supply in primary markets and strong demand, along with improving liquidity and increasing appetite for Sukuk among Middle Eastern institutional investors, is likely to offer continuing market support in the near future.

Page 13

Sukuk is the Arabic name for financial certificates, but commonly refers to the Islamic equivalent of bonds. Since fixed income, interest bearing bonds are not permissible in Islam, Sukuk securities

are structured to comply with the Islamic law and its investment principles, which

prohibits the charging, or paying of interest. Financial assets that comply with the Islamic law can be classified in ac-

cordance with their tradability and non-tradability in the secondary markets.

Accountancy Issues Rules and Regulations

IFSB revises capital adequacy standard

The Islamic Financial Services Board (IFSB) has issued new draft guidelines on capital adequacy for Islamic banks and the risk management prac-tices of takaful (Islamic insurance) companies. The original standard was issued in December 2005, based on Basel II regulations currently applying to banks around the world. In line with the future adoption of the Basel III standard, the IFSB’s new guidance aims to elaborate on the issue of the composition of capital in relation to Sukuk. A draft of the IFSB’s new guidelines was due to be issued in the first week of November for public consultation.

Source: Reuters, October 30th

RBI looks at encouraging Islamic banking

Discussion and debate around the issue of apply-ing an Islamic banking model have been raised by the central bank and the finance ministry, seeking to identify the rules needed to converge to practices in line with Shariah law. The Reserve Bank of India (RBI) governor has been engaged with the government on how existing laws can be restructured or amended. The finance ministry recently requested the RBI to examine the pos-sibility of making the interest-free model part of India’s Rs 75 trillion banking system. That was followed by an RBI meeting with the National Commission for Minorities (NCM) to study the proposition of Islamic banking. A National Com-mittee on Islamic Banking (NCIB) report has indi-cated that it is not necessary to change banking laws to implement interest-free products, but that tax laws would need to be changed.

GOLCER believes that India is closer to applying

the Islamic banking model than ever before.

Source: EIN News, October 16th

Tunisia’s calls for Islamic finance have political echoes

Following several attempts, and prolonged secular rule, Tunisia’s government aims to develop Islamic banking in the country. However, concerns have been raised that it might have political rather than economic motives behind this initiative. With re-cent interest targeted at accessing the huge pool of Islamic investment funds from the Gulf, the contro-versy in Tunisia has some political complications. Delays in developing the basis for Islamic finance in Tunisia are attributable to the severe competi-tion from conventional banks. At the same time, the accusation has arisen that this development is designed to attract support and head off any challenge from Islamists in parliamentary elections expected next year.

Source: Reuters, October 10th

Page 14

Perspective

Any view of international financial and commodity mar-kets, as we carry in this bulletin, comes face to face with the fact of global interconnectedness.

Just as developing Islamic indices remain related to conventional counterparts which have already reached maturity -- visibly both in stock and bond markets, so the traditional instruments around the world in those categories still relate back to the default benchmarks.

Although market behaviour in recent years has been distorted by the experience of the financial crisis, and its inducement of risk-on/risk-off patterns, what happens in the dominant US dollar and euro markets still provides a critical lead to the rest of the world, especially when the news in those crucial arenas is of fundamental impor-tance.

So America’s so-called ‘fiscal cliff’ budget challenge, and Europe’s own damaging budget rift, and especially its laboured but hugely significant steps towards fis-cal and banking union, have overshadowed markets’ mood, particularly as the prospect of any convincing upturn in the global economy appears to be lacking.

Many would prefer to draw upon more promising signs from the East, rather than be subdued by the West’s growing sense of inertia, and resulting slow growth. The trouble, however, is that much of Asia’s dynamism has followed the recycling of its payments surpluses into its’ customers’ debt load, limiting, at least according to that mercantilist model, its own ability henceforth to continue to grow at its relatively breakneck pace.

China is the prime example, of course, and our refer-ence to the weakened state of the copper market, for example, is a direct reflection of a slowdown in world growth that is responding as much to the difficulties of the emerging economies as to the well-established lo-comotive blocs of the past.The latest Chinese economic data – indicating whether the juggernaut is slowing

down further or speeding up again -- have taken on an unprecedented degree of importance to the rest of the planet.

Indeed the country’s claim on resources and every-one’s attention is likely only to be accentuated, as a simple function of population trends, let alone devel-opmental surge.

Among other things, it is regrettable, therefore, that China’s growth impetus hitherto has been unsustain-ably imbalanced towards overinvestment, leading inevitably to booms and busts that will, also unavoid-ably, cast doubt over the momentum in international trade.

Key regions of relevance to this publication, such as the Arabian Gulf, will be highly dependent on such overarching international trends for as long as their economic output is export-oriented and their indig-enous consumption and investment are underde-veloped by comparison, even though that’s been a natural product of historic development based on an overwhelming resource endowment in oil and gas.

Indeed, in current circumstances it may be that oil prices might actually need to be lower precisely to get the world economy moving faster again -- the clearest demonstration of the state of interdependence.

It may also be that without some policy reinvention in both hemispheres, markets will reflect only moderate outlooks for rates of economic activity, while, it seems, having to worry more about inflation than a high pro-portion of mainstream economists had imagined.

Just as the Gulf states should probably not re-live the 1970s in terms of recycling their petrodollars unpro-ductively abroad, equally, reacquainting with the stagflation of that era is not the most promising future for sustained market performance in any asset class.

Markets struggle with a dysfunctionally integrated world

by Andrew Shouler

Page 15

Diary of Events

February: 14-15, 2013Kuala Lumpur, MalaysiaICIBFC 2013: International Conference on Islamic Banking, Finance and Commerce

The XXXIV International Conference on Islamic Banking, Finance and Commerce aims to bring together lead-ing academic scientists, researchers and scholars to exchange and share their experiences and research results about all aspects of Islamic Banking, Finance and Commerce, and discuss the practical challenges encountered and the solutions adopted.

More Information: http://www.waset.org/conferences/2013/kualalumpur/icibfc/

March: 11-12, 2013Lahore, PakistanGlobal Forum on Islamic Finance (GFIF) 2013:

COMSATS Institute of Information Technology Lahore, Pakistan is hosting Global Forum on Islamic Finance with the collaboration of Lancaster University UK to provide an opportunity to share latest developments among scholars from around the globe in the field of Islamic finance. The theme of the Conference is “Islamic Finance: New Realities, New Challenges”. The GFIF will consider the political and socio-economic developments and their likely effects on Islamic financial institutions.

Contact: Dr. Yahya Rashid COMSATS Institute of Information Technology, Lahore, [email protected]

More Information: http://www.inomics.com/economics/conferences/2012/9/6/global-forum-islamic-finance-gfif-2013

March: 17-18, 2013Muscat, OmanOman Second Islamic Banking and Finance Conference:

Oman Second Islamic Banking & Finance Conference is to take place on the 17th & 18th of March 2013 at the Al Bustan Hotel in Muscat, to shed light on latest developments in the banking industry of the Sultanate and explore outlook and challenges of implementing Islamic banking.

Contact: [email protected] Information: http://www.iktissadevents.com/events/OIBF/2

Training Courses:GOLCER Training Courses in Finance, Management and Statistics:More Information: http://www.lums.lancs.ac.uk/files/coursesnew.pdf

Page 16

Research TeamGerry Steele

Vasileios [email protected]

Rhea [email protected]

Marwa El [email protected]

Andrew [email protected]

Marwan IzzeldinDirector

DISCLAIMER

This report was prepared by Gulf One Lancaster Centre for Economic Research (GOLCER) and is of a general nature and is not intended to provide specific advice on any matter, nor is it intended to be comprehensive or to address the circumstances of any particular individual or entity. This material is based on current public information that we consider reliable at the time of publication, but it does not provide tailored investment advice or recommendations. It has been prepared without regard to the financial circumstances and objectives of persons and/or organisations who receive it. The GOLCER and/or its members shall not be liable for any losses or damages incurred or suffered in connection with this report including, without limitation, any direct, indirect, incidental, special, or consequential damages. The views expressed in this report do not necessarily represent the views of Gulf One or Lancaster University. Redistribution, reprinting or sale of this report without the prior consent of GOLCER is strictly forbidden.