issue 28

DESCRIPTION

technicalTRANSCRIPT

Jun

e2

00

8

.technicalanalyst.co.ukwwwThe publication for trading and investment professionals

Markets StrategiesThe predictive power

of fund flows

Automated TradingOverview of

execution algorithmsSector performance

in the S&P500

Dealing with RiskJulian McCree of Erste Bank

presents

A premier event for trading and investment professionals

Speakers include:

Global Equities

200826 June 2008

Chandos House

London W1Outlook and investment

strategies for global stocks

Web: www.technicalanalyst.co.uk

Telephone: +44 (0)1483 573150

Register Today!

Email: [email protected]

Topics covered:Who should attend:

Delegate fee: £445 + VAT

+ Outlook for global stocks+ VIX and market direction+ Trend following strategies+ Momentum investing+ Issues in shorting stocks

+ Fund managers+ Hedge funds+ Traders+ Risk managers+ Analysts+ Brokers

Bringing together leading experts in the field oftechnical and quantitative trading, the confer-ence will look to assess the effectiveness of thevarious equity trading strategies such as trendfollowing and momentum investing in thecurrent market climate, as well as providing anin-depth assessment of the outlook for the majorstock markets. This is the essential event for theUK and Europe’s investment community.

Max KnudsenPIA First

Antonio ManziniUBS

Charles MorrisHSBC Investments

Laurens SwinkelsRobeco

Robin GriffithsCazenove Capital

Richard RamyarLipper

© 2008 Global Markets Media Limited. All rights reserved. Neither this publication nor any part of it may be

reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical,

photocopying, recording or otherwise, without the prior permission of Global Markets Media Limited. While the

publisher believes that all information contained in this publication was correct at the time of going to press, they

cannot accept liability for any errors or omissions that may appear or loss suffered directly or indirectly by any

reader as a result of any advertisement, editorial, photographs or other material published in The Technical

Analyst. No statement in this publication is to be considered as a recommendation or solicitation to buy or sell

securities or to provide investment, tax or legal advice. Readers should be aware that this publication is not

intended to replace the need to obtain professional advice in relation to any topic discussed.

CONTENTS 1 FEATURES

S&P500 OutlookKamran Sheikh of Informa Global Markets

breaks down the S&P500 and gives

his outlook for its various sectors.

Managing RiskJulian McCree of Erste Bank talks about

his approach to trade management.

Fund Flows Data We present a Deutsche Bank study that

looks to establish if weekly fund flows

data can be used to predict the markets.

JUNE

>36

>04

> 19

>

> >

WELCOMEAlthough a great deal is written in books and magazines (including this one) about

how to employ technical trading strategies, the subjects of risk and money man-

agement are often overlooked. As any successful trader will tell you, this is often

as important a subject as choosing a successful entry and exit strategy. In this

issue Julian McCree, a trader at Erste Bank, gives us his views on how trade man-

agement is best approached when combined with a technical trading strategy.

We also discuss the importance of funds flows and examine if data can be used to

predict market movements.

We hope you enjoy this edition of the magazine

Matthew Clements, Editor

June 2008 THE TECHNICAL ANALYST 1

Editor: Matthew Clements

Managing Editor: Jim Biss

Consultant Editor: Trevor Neil

Advertising & subscriptions:Louiza Charalambous

Marketing: Vanessa Green

Events: Adam Coole

Design & Production:Stuart Field

The Technical Analyst is published by

Global Markets Media Ltd

Jeffries House

1-5 Jeffries Passage

Guildford

GU1 4AP

UK

Tel: +44 (0)20 7833 1441

Web: www.technicalanalyst.co.uk

Email: [email protected]

SUBSCRIPTIONS

Subscription rates (6 issues)

UK: £160 per annum

Rest of world: £185 per annum

Electronic pdf: £49 per annum

For information, please contact:

ADVERTISING

For information, please contact:

PRODUCTION

Art, design and typesetting by

Stuart Field.

Printed by Goodman Baylis

ISSN(1742-8718)

MARKET VIEWS S&P500 - Divergence in sector performance

Emerging Markets Outlook

Outlook for Crude Oil

TECHNIQUES Volume - The voice of the market

The Predictive Power of Weekly Fund Flows

The ARMS Index

Trading Variations in Double Tops and Double Bottoms

INTERVIEWJulian McCree, Erste Bank

RESEARCH UPDATE

BOOKSThe Encyclopedia of Candlestick Charts

Top Ten Books

AUTOMATED TRADING SYSTEMSOverview of Today’s Algorithms:

Advanced Strategies for a Complex Marketplace

TRAINING DIARY

04

10

12

16

19

28

32

36

41

43

44

45

48

CONTENTS 2 REGULARS>

June 2008 THE TECHNICAL ANALYST 3

28 43

4 THE TECHNICAL ANALYST June 2008

Market Views

S&P500DIVERGENCE IN SECTOR PERFORMANCE By Kamran Sheikh

June 2008 THE TECHNICAL ANALYST 5

Market Views

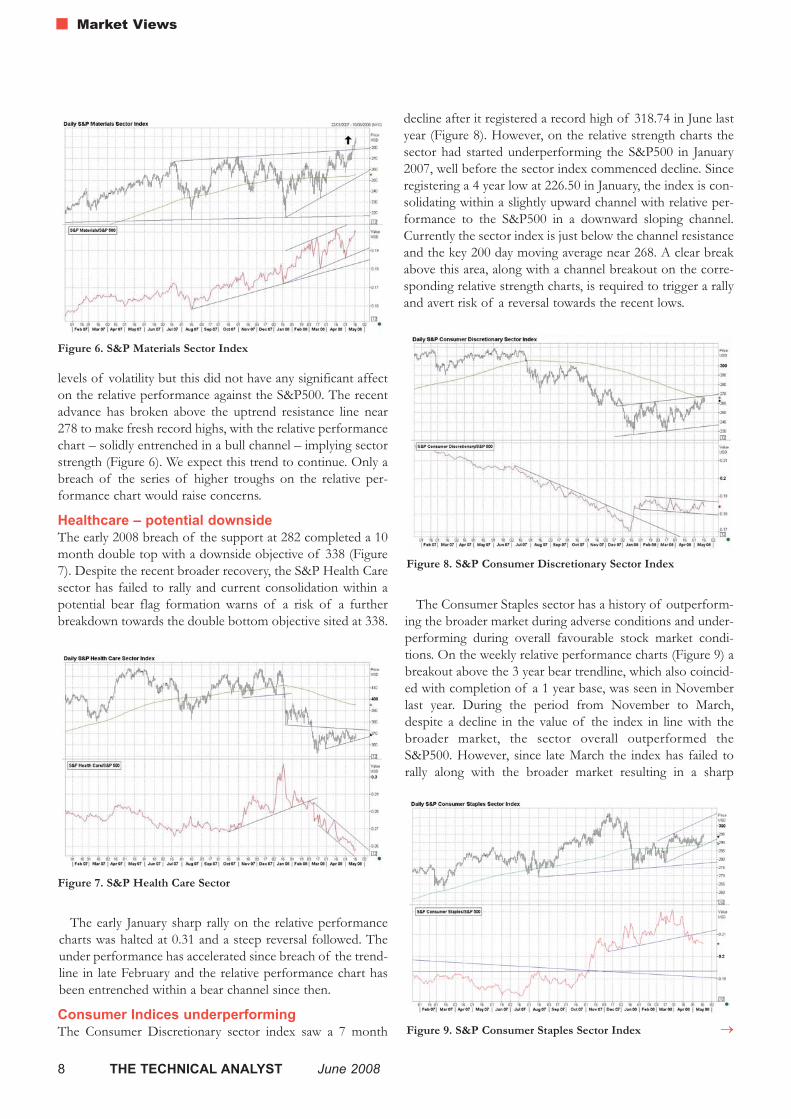

Sector performanceAfter a notably weak start to the year by the entire market,there has been a marked divergence in sector performance in2008. While the S&P500 has lost only 2.90% (by 16 May)after recovering from its early losses, sharp declines wereseen in sectors like Financials (-10.4%), Healthcare (-10.4%)and Telecommunication (-8.1%). See Figure 1. On the otherhand some sectors outperformed the broader market, such asMaterials (+10.0%), Energy (+9.0%) and ConsumerDiscretionary (+1.5%).

Historically out performance by the Energy Sector hascoincided with a decline in the broader market. The EnergySector also has a tendency to rally at the end of an expansionin the economic cycle. While weight of the Energy sector(and of course fuel prices) can be seen adversely affecting thestock market, out performance the Materials and ConsumerDiscretionary sectors is evidence of confidence in the econ-omy via strong manufacturing and high levels of spendingon the luxury goods and services, respectively, even in thecurrent market conditions.

Despite the fact that the S&P Information TechnologySector is still down 4% this year so far (16 May), the recentbreakouts on the Sector Index and the relative strength ofS&P500 charts is of significant importance as this sector hasan history of leading bull markets. Another positive develop-ment is the recent weakness of the Consumer Staples Indexrelative to the S&P500. Historically Consumer Staples sectoris considered resilient to overall bearish stock market condi-tions and outperforms S&P500 during times of poor confi-dence in the economy. By contrast, it usually underperformsduring times of confidence. The recent deterioration in theSector’s relative strength to the broader market, after a peri-od of out performance in Q4 2007 and Q1 2008, is a posi-tive signal for the stock market.

In this article we take a brief look at US stock market sec-tors. Since global stock markets are closely interconnected,similar trends can be observed in other markets around theglobe.

Bullish energy sector In light of rising fuel prices to fresh record highs (Figure 2),it is not surprising that the Energy sector is making new alltime highs. The current bull market commenced in mid-2002and regardless of a few corrective reactions, the overall trendhas been strong. The second half of 2007 witnessed high lev-els of volatility but the Index has held above the support

“DESPITE SOME OVERBOUGHT CONDITIONS [IN THEENERGY SECTOR] NEITHER INDICATORS NOR THE CHART

STRUCTURE SHOW SIGNS OF REVERSAL”

→

Figure 1. S&P500 sector performance

Figure 2. S&P Energy Sector

near 480 (2006 peak) during August and January dips. Theearly April break above the trendline resistance near 580 wasfollowed by fresh all time highs. Despite some overboughtconditions, neither indicators nor the chart structure showsany signs of reversal at this stage.

The Energy sector has been outperforming the S&P500since late 2003. However, the out-performance significantlyaccelerated following a break above the neckline of a doublebottom formation (Sep 2006-Jan 2007) in mid last year. Therelative strength chart is solidly entrenched within a bullchannel since early this year. We look for this trend to contin-ue for the time being. A break below the channel support onthe relative strength charts would warn of diminishing inter-est in the Energy Sector and may be a positive sign for therest of the stock market.

Technology – a leading indicatorThe Information Technology sector index is considered aleading sector. Historically this sector has led bull markets inpast years and generally outperformed the broader market.The index completed a classic text book head and shoulderformation in early January (Figure 3). This was followed by asharp decline to probe below the formation objective at 340within 3 weeks. Following a 3 month consolidation within atight 335-364 range, the index has completed a base, whichalso coincides with a 5 month bear trendline break on the rel-ative strength charts. The subsequent breaks above the trend-line near 381, and the 200 day moving average close to 385,corresponded with a rally on the relative strength charts. Wetake this advance as a positive sign for the stock market ingeneral and the Information sector in particular.

Industrials outperformFollowing a sharp decline in late January, the S&P Industrialssector has formed a series of consecutive rising troughs andpeaks. A break above the 6 month trendline resistance (con-necting October and December 2007 highs) near 341 and therecent clearance of the 200 day moving average close to 349exhibits underlying strength (Figure 4).

The sector has been outperforming the S&P500 sinceApril 2007. However, the recent formation of a potentialhead and shoulders top on the relative strength charts warnsof a possible reversal, though the outlook remains positivewhile the S&P Industrial & S&P500 ratio is above the neck-line at 0.24.

Telecoms face resistance The S&P Telecommunication Services sector advanced formost of 2006 and 2007, outperforming the rest of the mar-ket before the index completed a double top formation uponbreach of the neckline at 159 late last year. The subsequentdecline was worse than the rest of the market as reflected onthe relative strength charts (Figure 5). Following a 3 monthbasing, the index has shown some recovery, however thetrendline from the September peak and the 200 day movingaverage near 160 offer tough resistance. The relative perform-ance chart is exhibiting a fairly neutral outlook at this stage.

Materials see new highsThe Materials sector index has been in an uptrend since mid2006 and outperforming the broader market since late2006. The second half of 2007 and early 2008 saw high

June 2008 THE TECHNICAL ANALYST 7

Market Views

Figure 3. S&P Information Technology Index

Figure 4. S&P Industrials Sector

Figure 5. S&P Telecom Services Sector Index

→

levels of volatility but this did not have any significant affecton the relative performance against the S&P500. The recentadvance has broken above the uptrend resistance line near278 to make fresh record highs, with the relative performancechart – solidly entrenched in a bull channel – implying sectorstrength (Figure 6). We expect this trend to continue. Only abreach of the series of higher troughs on the relative per-formance chart would raise concerns.

Healthcare – potential downside The early 2008 breach of the support at 282 completed a 10month double top with a downside objective of 338 (Figure7). Despite the recent broader recovery, the S&P Health Caresector has failed to rally and current consolidation within apotential bear flag formation warns of a risk of a furtherbreakdown towards the double bottom objective sited at 338.

The early January sharp rally on the relative performancecharts was halted at 0.31 and a steep reversal followed. Theunder performance has accelerated since breach of the trend-line in late February and the relative performance chart hasbeen entrenched within a bear channel since then.

Consumer Indices underperformingThe Consumer Discretionary sector index saw a 7 month

decline after it registered a record high of 318.74 in June lastyear (Figure 8). However, on the relative strength charts thesector had started underperforming the S&P500 in January2007, well before the sector index commenced decline. Sinceregistering a 4 year low at 226.50 in January, the index is con-solidating within a slightly upward channel with relative per-formance to the S&P500 in a downward sloping channel.Currently the sector index is just below the channel resistanceand the key 200 day moving average near 268. A clear breakabove this area, along with a channel breakout on the corre-sponding relative strength charts, is required to trigger a rallyand avert risk of a reversal towards the recent lows.

The Consumer Staples sector has a history of outperform-ing the broader market during adverse conditions and under-performing during overall favourable stock market condi-tions. On the weekly relative performance charts (Figure 9) abreakout above the 3 year bear trendline, which also coincid-ed with completion of a 1 year base, was seen in Novemberlast year. During the period from November to March,despite a decline in the value of the index in line with thebroader market, the sector overall outperformed theS&P500. However, since late March the index has failed torally along with the broader market resulting in a sharp

Figure 6. S&P Materials Sector Index

Figure 7. S&P Health Care Sector

Figure 8. S&P Consumer Discretionary Sector Index

Figure 9. S&P Consumer Staples Sector Index →

Market Views

8 THE TECHNICAL ANALYST June 2008

decline on the relative performance charts. The outlook ofthe relative strength charts seems negative which may be aprecursor to a broader bull market.

Financials – no sign of recoveryThe S&P Financial sector index completed a double top for-mation in July 2007 (Figure 10). The relative performancechart had already shown signs of warning upon completionof a top area 4 months before the credit crunch started tak-ing its toll in March last year. A sharp decline followed onboth the sector and relative performance charts. Despiterecent basing on the Financial Sector charts following theMarch low at 302.82, the relative strength versus the S&P500,which is still declining within a bear channel, has shown nosigns of improvement so far.

Utilities – possible strength aheadThe Utilities sector has enjoyed an uptrend on the relativeperformance charts from mid 2004 (Figure 11). Despite thehigh volatility on the index chart in late 2007 and early 2008,the relative performance versus the S&P500 – on the longerterm charts – is still in an uptrend and above the key 4 year

bull trendline. Since establishing a high in January following arecord high at 225 on the sector index chart, the relativestrength to the S&P500 is within a bear channel. Currentlythe Utilities sector is forming a potential reverse head andshoulders formation. A clear break above the horizontalneckline near 209, along with a breakout from the bear chan-nel resistance on the relative strength charts, would signalcontinuation of the primary bull trend on both the index andthe relative performance chats.

Figure 10. S&P Financial Sector Index

Figure 11. S&P Utilities Sector

“AFTER A NOTABLY WEAK START TOTHE YEAR BY THE ENTIRE MARKET,

THERE HAS BEEN A MARKED DIVERGENCE IN SECTOR PERFORMANCE IN 2008”

Kamran Sheikh is technical analyst with InformaGlobal Markets in London.

June 2008 THE TECHNICAL ANALYST 9

Market Views

10 THE TECHNICAL ANALYST June 2008

Market Views

June 2008 THE TECHNICAL ANALYST 11

Market Views

TA: Do you believe there is a decoupling between USand Asian stocks and economies?

MH: You need to distinguish between macro decoupling andasset price decoupling. There is very clear evidence of eco-nomic decoupling between the US and the BRIC and Asianeconomies. In contrast asset prices are correlated. When theUS stock market falls, so do Asian stock markets. But thenegative hit is much smaller than it used to be.

TA: What is your view of the Chinese stock market?

MH: The Chinese market is oversold and investors areunderweight. We say trading buy. But a renewed secularupswing in the Chinese stock market requires a sustained fallin inflation.

TA: Do you think other markets apart from BRICs,such as the frontier markets of central Asia, will offerbetter opportunities?

MH: Frontier markets offer strong, uncorrelated returns.The markets are undercapitalized and under owned, offerstrong economic growth potential, and are underleveragedeconomies. Within Emerging Markets the BRIC markets willretain the leadership.

TA: Which emerging markets do you think are over-bought?

MH: Morocco, Egypt and Brazil are currently the most over-bought relative to their 200 day moving average.

TA: Do any recent dips in emerging markets offergood buying opportunities or are you expecting amore sustained correction?

MH: We've been buyers since the Bear Stearns event but webelieve it's a bear market rally.

TA: Will a decline in export competitiveness viz-a-viza fall in the USD have a major impact? Where will itits impact be felt most?

MH: Not for the commodity producers. They love a weaker

dollar. And the Asian markets are benefiting from the strongEuro. Indeed, while export growth from Asia to the US hasslowed over the past year, total Asian export growth has actu-ally risen.

TA: What other markets or data do you think are use-ful as leading indicators for emerging market equi-ties?

MH: Our best short term sentiment indicators are the MerrillLynch Fund Managers Survey and the EPFR fund flow data.Emerging Markets are of course also highly correlated withmany other market indicators, such as commodities, the USdollar, volatility and the S&P500.

TA: Re portfolio/country allocation, what are the keyfactors in your decision-making process?

MH: We are always overweight markets with attractive valu-ations (cheap PEs) and large current account surpluses. Thelatter implies high levels of savings and liquidity. If you canget that cheap then you are onto a winner.

TA: Can you give us an idea of how you use EPFRdata? Are you looking to follow trends or spot poten-tial reversals when the market is over-extended? Howgood is EPFR data in helping you to do this?

MH: EPFR flow data helps us to identify inflexion points inthe equity market. We use flow data to develop trading rulesand make directional calls on emerging markets. The data isvery useful.

TA: What techniques do you use to fine-tune/timeyour entries and exits? How and to what extent doyou use technical analysis?

MH: In addition to our flow and sentiment tools, we usetechnical indicators such as 200 day moving averages and soon to indicate breakouts and the extent to which markets areoverbought and oversold.

Emerging Markets OutlookUsing a mix of technical, fundamental and flow data, Michael Hartnett gives his outlook for the emerging markets.

Michael Hartnett is Chief Global Emerging Markets EquityStrategist at Merrill Lynch in New York.

12 THE TECHNICAL ANALYST June 2008

Market Views

Outlook forCrude Oil

On 23 April this year,Global Markets Mediaheld their first OilMarket seminar inLondon, covering allaspects of the oil mar-ket from explorationto changes in thedemand profile. Herewe summarise a few oftheir conclusions andask whether oil pricesare set to continue ontheir path upwards andfor how long. →

Do Current Oil PricesRepresent a Paradigm Shift?

Leo Drollas, Centre for Global Energy Studies

“We have probably seen the oil pricepeak for the time being, unless thereare further supply disruptions or thegeopolitical scene suddenly deterio-rates. Refinery margins are under somepressure from slowing oil demand andhigh crude prices amid worries aboutan impending recession. Oil prices arelikely to stay above $100/bbl until thethird quarter but will tend to weakenthereafter, requiring cuts by OPECearly next year. In the longer term, oildemand growth is likely to slow upconsiderably due to high oil prices andworries about the environment…OPEC will do its best to keep the oilprice above $60/bbl, but it will faceperiods of excess capacity that will testits cohesion and its resolution.”

Crude Towards $200:Fundamental and TechnicalDrivers

Lars Steffensen, Ebullio Capital Management

“The days of talking about demanddestruction are over. This myth hasbeen busted. On the supply side,OPEC won’t deliver and non-OPECcountries can’t, and there is no end insight. US and Europe are not growing,

but they are still driving their cars –accounting for 65 to 75% of globaldemand in the transport and petro-chemical sectors. Moreover, emergingeconomies don’t see the real price –OPEC, China, India, Indonesia andmany others subsidize domestic con-sumption and can’t stop for politicalreasons. OPEC now believe that highprices are needed to slow unrelentingdemand growth. Technically, there is afirm uptrend and dips are beingbought, which means any retracementis limited. One cannot be bearish untilsubsidies are removed, resourcenationalism goes away, project delaysend, new supplies come to market andsupply/demand transmission isrestored. The only thing guaranteed isvolatility.”

Oil as an Asset Class

Tim Guinness, Guinness Atkinson

“In the long-term, the demand fromemerging economies provides a nearirresistible force which means we areunlikely to see a real curbing ofdemand without a $150-200 spike.OPEC will seek to manage averageprice up by $5/10 barrel per year. Withregards to the equity markets, energyequities will return 50 – 150% overnext 5 years in a scenario which com-bines higher earnings from higher oil,gas & coal prices (even after highergovernment take) and multiple expan-sion. In the shorter-term, the oil priceis likely to correct to around $80 as oilinventories are about right. Above all,investment valuations remain attractivefor energy equities. The market is valu-ing stocks at $55-65 oil, well belowanalysts’ forecasts of $70-80 and theactual $102.5 year strip.”

The Changing Profile ofDemand

Eduardo Lopez, International Energy Agency

“High prices, coupled with worseningeconomic prospects and milder winterconditions are certainly affectingOECD demand. Yet, in non-OECDcountries, demand has actually turnedout to be much higher than expected.By 2012 non-OECD growth will beabout three times higher than theOECD’s. In general, when a manufac-turing sector emerges, income per capi-ta rises significantly and oil demandtakes off (as cars, flights, air condition-ing etc become part of everyday life).Empirically, the pace of demandgrowth becomes very brisk between$3000 and US$9,000 per capita. It’snotable that several non-OECDeconomies are in or about to reachthat stage.

“Our forecast is that transportationfuels will account for the bulk of oildemand and oil demand growth willcome from non-OECD countries.Within the OECD, demand is sus-tained by North America which willrepresent 53% of the total by 2012.With regard to non-OECD countries,Asian demand will account for 47%and the Middle East for 19% of thetotal. Biofuels are gaining much atten-tion and are seen as an alternative forexpensive and polluting oil-basedtransportation fuels. However, despitespeculator growth in a few countries –such as Brazil – biofuels are likely toaccount for less than 2% of globalproduct demand by 2012.”

June 2008 THE TECHNICAL ANALYST 13

→

Market Views

Oil Prices: Are capacity con-straints to blame?

Margaret Chadwick, Oxford Petroleum Research

“There are four key reasons to explainwhy oil prices are so high: Upstreamsupply rationing from OPEC, particu-larly in 2006-2007; strong demand fortransport fuels combined with a fully-utilised refinery upgrading capacity (inrelation to upgrading heating fuel totransport fuel); A Q1 surge in middledistillate demand caused by a cold snap(with reference to the 14 large oil-con-suming countries); and downstreamrefinery bottlenecks. As such, in2007/2008, Europe’s deficit soared andChina became a large importer. Tomake matters worse, non-OPEC pro-duction has also been below expecta-tions.”

We also summarise below a few of thekey points in relation to conventionaland non-conventional oil reserves:

Geological Uncertainty andRisk: Implications forHydrocarbon ResourceAssessment

Jonathan Redfern, University of Manchester

“The calculation and estimation ofreserves is complex and open to errorand interpretation. Generally for anydiscovered prospect or field, three

cases are calculated depending onincreasing geologic certainty: Possible(P3 – 10% probability); Probable (P2 –50% probability); and Proven (P1 –90% probability). It’s often not clearwhen numbers are quoted whetherthey are talking about STOIP(Standard Oil in Place, which includesthe sub-economic resources) orReserves/Resources (P1 to P3). Oftenhigh hopes are not rewarded, as in thecase of Kenya and Mautania.

“With regard to the calculation ofglobal resources, by using trends with-in mature basins it’s possible to esti-mate the ultimate recoverable reservesexpected (URR). It’s a typical trend fora basin to follow a fractal pattern, i.e.to have a few very large fields at firstand many more smaller fields towardsthe end of its life that produce fromsmaller complex structures and strati-graphic traps

“Convention oil and gas is definedas hydrocarbons that “flow freely”, arein accessible locations and do notrequire complex and expensive tech-nology to produce. Non conventionaloil and gas is everything else, includingdeepwater oil and gas (although thishas started to be considered conven-tional in the last 5 to 10 years), heavyoil, oil shale/sands, polar oil and gas,coal bed methane, tight oil and gasfields, biogenic gas, gas hydrates andsynthetic oil from gas. According toBP, total proved oil reserves (P1) equal1,208 thousand million barrels, enoughfor 40 years demand at current con-sumption of 84 million barrels a day.The Middle East accounts for 61.5%of total proved reserves. According tothe US National Petroleum Counsel(NPC), the mean estimate of remain-ing oil reserves (including mean esti-mates for new discoveries and growthof existing reserves, but not includingnon conventional oil) is 2,628 thou-sand million barrels, enough for 86years at current consumption levels. Asregards global in-place oil resources, astudy in 1998 estimated a most likelycase of 14,960 thousand million bar-rels, including conventional and somenon-conventional resources butexcluding oil sands/shales. The ques-

tion is now how much of this can berecovered?

“There are 350 ‘giant fields’ in theworld which hold 50-60% of currentworld oil reserves, each containingmore than 500 million barrels inreserves. The largest of which isGhawar in Saudi Arabia, discovered in1938, which has 489 thousand millionbarrels in place and 100 thousand mil-lion recoverable. With a reserve size of100 million barrels considered verygood in many basins, to replace justone Ghawar means we need to find1100 new fields. So where is theremaining big potential?

“There are several areas which offerpotentially big fields. These are theCanadian Oil Sands; Deepwater Gulfof Mexico; Deepwater West Africaand Brazil; Baltic/Russian Arctic; aswell as new exploration and produc-tion from the Middle East. The UnitedStates government recently declaredAlberta’s oil sands to be ‘proven oilreserves’. Consequently, the USupgraded its global oil estimates forCanada from five billion to 175 billionbarrels. Only Saudi Arabia has moreoil. The Tupi deepwater field in Brazilis the biggest discovery since 2000 andthe largest ever in deep waters.Petrogras believes Tupi may be Brazil’sfirst of several new “elephants”, fieldsof more than 1 billion barrels. InitiallyTupi will produce about 100,000 bar-rels a day but may ramp up to as muchas 1 million before 2020. “It’s mon-strous,” says Matthew Shaw, a LatinAmerican energy analyst at consultantWood Mackenzie.

“An NPC Global Oil & Gas Studyconcluded that global endowment is nota limiting factor in future supply in thenear term. Constraints will come fromother sources – technology, access,deliverability, economics, geopolitics etc.Small changes in recovery efficiency(percentage of oil in place that will ulti-mately be produced) will have a globallystrategic impact upon the oil budget,and the role of unconventionalresources will have a growing and pro-found impact as non conventional oil &gas becomes conventional.”

Market Views

14 THE TECHNICAL ANALYST June 2008

Techniques

16 THE TECHNICAL ANALYST June 2008

Ilike to think about volume as themost powerful indicator I have onmy trading screen. Volume is driv-

ing price, not the other way around. Sowho is actually moving the market? Thebig volume traders such as the largebanks, hedge funds and market makers,the so called smart money or profes-sionals. They have much more informa-tion than most other traders, withaccess to order books where they cansee stops, size of orders and who isselling and buying.

These institutions trade large tickettrades or a series of trades to engage inthe market and they have to pay moreattention to slippage and executionthan smaller players do. They get in andout of the market in the most cost effi-cient way by buying into down movesand selling into up moves. This oftengives them a better average entry pricesince they are trading against the shortterm momentum so they find it easierto scale in large trades without gettingtoo much slippage.

Trading tricksThese large institutional traders willalso use various techniques to “trick”other traders such as hunting for stopsand spiking the market up to makeother traders take bad long positionswhile they build up shorts to slam themarket down. News events are often agood time to play tricks and manipulatethe market and many times the market

will react unexpectedly when the actualdata is released. Keeping this in mind itis now easy to see why volume is animportant indicator. It gives an indica-tion of what price levels the largetraders get engaged at and how muchinterest they have in higher or lowerprices.

Since the large traders are the onesdriving the market it can be an advan-tage to try and follow their lead. Butvolume by itself is not really giving youmuch to go by so you need to be ableto read the price chart in relation tovolume to really understand what isgoing on. To be really effective one hasto pay attention to what the market hasbeen doing recently to put it all intoperspective.

High volume candlesYou will see plenty of signals by exam-ining the volume in relation to the priceaction. Are the professionals showingan interest in the up or down move orare they aware of something that isabout to change so they are backingaway or even turning around their posi-tions? One of the first things I look foron a chart in order to see where theprofessionals are showing interest isextremely high volume candles. This isimportant because the only way to getan extreme high volume day is if thereare both sellers and buyers heavilyinvolved in the market. This tends tohappen at market tops and bottoms.

The next thing is to look at what hap-pened on those specific days. The key isto try and figure out if the profession-als are accumulating or distributing andthen try to play along with them. Acommon misperception is that peoplethink weakness shows on down barsand strength on up bars. Weakness willalways show first in an up bar andstrength will always show itself first ona down bar. This is of course due to thefact that at certain levels professionalswill turn their positions around or shownew interest. This will eventually leadto a change in trend.

Reversals on extremely highvolumeA good example is the recent reversalin the S&P 500 E-mini futures on the17th of March (Figure 1). This was aclassic reversal formation and the chartactually gave several signals that a lowwas in the making. On 16th March thevolume was extremely high trading 3.87million contracts, 64% more than the20 day average at that time. The nextday it traded slightly less with 3.69 mil-lion contracts but still way above the 20day average of 2.46 million. The signif-icant clue was that the close on boththose days was some way off the lows.The only way this can happen is if pro-fessionals are buying into the sellingand therefore creating extreme volumeand forcing the market off the lows.

High volume up bars closing off

- the voice of the marketBy Per-Erik Karlsson

→

volume

June 2008 THE TECHNICAL ANALYST 17

Techniques

the highs represents selling. The nextbig clue was the following day, the 18thMarch, when the market rallied 52.50points to close right at the high, trading3.12 million contracts. For that to hap-pen the professionals had to be buyersthe previous few days removing mostsupply so the market could rise. Indeedthat is what happened as well with theS&P rising 174 points in 34 days.

Lack of interestAnother thing I like to look for is what

I call “lack of interest”. If professionalsthink prices are too high they will nolonger be interested in buying andtherefore volume could drop quite a loton up bars. I also want the bar to beshort because that further underlinesthe lack of buying power. Figure 2shows Dax futures where there are sev-eral signs of a lack of interest from pro-fessionals on the recent down trendfrom October 2007 to the low on the17th March 2008.

First you will notice several weakness

signs at the highs of October 2007showing high volume up bars closingoff the highs. This suggests the profes-sionals were lining up for a down moveselling into those highs. Then as itdrops lower at the beginning ofNovember you get the first confirma-tion that the market is weak because on6th November the first “lack of inter-est” bar appears. Notice how short thebar is and also the accompanying lowvolume which is lower than the recentbars and well below the 20 day averagevolume. Then another one on 14thJanuary and the market droppedsharply the next 7 trading sessions. On2nd April the last “lack of interest” barappears and the market drops another348 points in 3 days from that day’sclose to the low 3 days later.

The market will often react quitequickly to these “lacks of interest” barsand if you look at the Dax chart youwill see that the market moved lower onall three occasions following “lack ofinterest” during that down move fromOctober 07 to March 08. Failure by themarket to respond within a few bars isa warning signal that something is notright and the market might swing theopposite way.

Figure 1. S&P 500 Daily Continous Contract June 08

Figure 2. Dax continous futures contract June 08

18 THE TECHNICAL ANALYST June 2008

Techniques

Volume rising into low Huge volume

Low volume vs. recent bars

Reversal - Closing off the highs on extreme volumesignals buying

More buying by professionals the following day, high volume up bar closing right at the high, very wide bar.

More strength, ‘lack of interest’ byprofessionals to sell the market

Volume lower than resent bars

Again no interest to participare in the

up moveVolume is lower than resent bars

This reversal corresponds with theS&P reversal on the above chart

Lack ofinterest More selling, up bar closing off the high, high volume

Lack of interest on up bar

Weakness in the backgroundLack of interest on up bar

More selling

Selling, high volume up bars closing off the highs

Per-Erik Karlsson is head of tradingoperations at Advantage Financialin Switzerland.

The PredictivePower of WeeklyFund FlowsBy Bernd Meyer, Joelle Anamootoo and Ingo Schmitz

June 2008 THE TECHNICAL ANALYST 19

Techniques

As Keynes said, the stock market is comparable to abeauty contest whereby the person picking the mostpopular candidate wins a prize: “It is not a case of

choosing those [faces] which, to the best of one’s judgment,are really the prettiest… We have reached the third degreewhere we devote our intelligence to anticipating what averageopinion expects the average opinion to be.” As such, aninvestor is likely to gain by anticipating which assets, regionsor sectors will become the popular choices, which not neces-sarily reflect the best fundamentals. To the extent that thetrend in fund flows reflects investor action and behaviour,this is likely to shed more information on market expecta-tions regarding various asset classes as well as regions andsectors.

In August 2006, we (the Equity Strategy research team atDeutche Bank) looked at fund flow data in general and theEmerging Portfolio Fund Research (EPFR) data in particular(see Box 2), and analysed the predictive power of weeklyfund flow data, both for the direction of the equity marketand for the relative performance of regions. The key findingsfrom this research can be found in Box 1. The top line find-ing is that there is stronger evidence for predictive power

regarding the relative performance of regions than for themarket overall, but that there was no strong evidence thatflows lead performance in the following weeks. Simplestrategies that go long or short the asset based on the previ-ous week’s direction of flows do not generally work.Focusing on the changes in the direction of the flow ratherthan the direction of the flows does not improve the predic-tive power for the market direction either.

However, including the ‘Liquidity Pulse’ - a measure of ris-ing or contracting liquidity momentum – helps predict mar-ket direction. Extremely strong/weak readings of theLiquidity Pulse should be seen as a negative/positive signal.As such, we were able to develop profitable trading rules forthe market based on the combination of the direction of theweekly fund flows, the direction of the average 4-week flowand the Liquidity Pulse.

We also found that the relative strength of fund flows fordifferent regions contains explanatory power for subsequentrelative performance of the regions. Excluding transactioncosts, we find information ratios larger than 1. In our view,this suggests that the relative strength of fund flows doesadd value to models of regional equity allocation. →

Money flows are the ultimate drivers of asset prices.Against this backdrop it is not surprising to find thatdata on fund flows has increasingly gained populari-ty as it has become more widely available. But it isnot just that money flows drive performance; goodperformance of assets also tends to attract moneyflows. Due to this interplay, fund flows tend to showsome inertia and as such should contain somemomentum information.

“THE PROBABILITY THAT A POSITIVE INFLOW FOLLOWS A POSITIVE INFLOW IS AROUND 68%. A NEGATIVE INFLOW FOLLOWS A NEGATIVE INFLOW WITH 60% PROBABILITY.”

20 THE TECHNICAL ANALYST June 2008

Techniques

Box 1: Key findings about the predictive power of weekly fund flows

� We find no evidence of seasonal patterns in weekly fund flow, such as the rush in January, the sell off in the summer andtax loss selling. In our view fund flow data therefore do not require seasonal adjustment.

� Weekly fund flows show inertia as flows drive performance and performance leads flows. The average first-order autocor-relation coefficient is 0.27, with emerging market equity flows showing autocorrelation up to 0.54. The probability that apositive inflow follows a positive inflow is around 68%. A negative inflow follows a negative inflow with 60% probability.

� We observe a high (0.28) average contemporaneous correlation between weekly fund flows and equity market perform-ance (as measured by the respective MSCI indices). We also find a strong positive correlation between performance andlagged fund flows, providing clear evidence that performance leads flows. We do not find strong evidence that fund flowslead performance in the following weeks.

� In the bear market until March 2003 as well as in sideways markets the direction of fund flows in one week (or in 4weeks on average) carries predictive power for subsequent performance. In a rising market the direction of fund flowsdoes not seem helpful and actually gives wrong signals on average. Hence, simple strategies that go long or short basedon the previous week’s direction of flows do not generally work.

� Focusing on the changes in the direction of the flow rather than the direction of the flows does not improve theexplanatory power for the market direction.

� Including the Liquidity Pulse, a measure of rising or contracting liquidity momentum, proves helpful for predicting themarket direction. We were able to develop trading rules for the market based on the direction of the weekly fund flows,the direction of the average 4-week flow and the Liquidity Pulse that have worked for the regions for which we have thelongest history. Generally these strategies suggest to remain invested in the market unless all measures send a negative sig-nal. Extremely strong/weak readings of the Liquidity Pulse should be seen as negative/positive signal. The May 2006 cor-rection though was not predicted by these strategies.

� Our cross-sectional analysis shows that the relative strength of fund flows for different regions contains explanatorypower for subsequent relative performance of the regions. Excluding transaction costs we find information ratios largerthan 1. Even if results after transaction costs are unlikely to be that positive, this suggests in our view that the relativestrength of fund flows does add value to models of regional equity allocation.

� Finally a word of warning. One needs to be careful with any major conclusions as the earliest data available is fromJanuary 2000. All data available for developed markets lies in the positive part of the current market cycle. In this marketcycle cheap money was available globally due to low interest rates in Japan, Europe and the US, which lead to a strongappreciation in value of all asset classes. The data could be misleading and not reflect the true long-term fund flow pic-ture. As no other data is available we can neither prove our findings to be right nor wrong. We believe however the datacan among other things be used to confirm economic or equity performance trends.

* Based on Deutsche Bank report “Predictive power of weekly fund flows”, 10 August 2006.

June 2008 THE TECHNICAL ANALYST 21

Techniques

Liquidity Pulse – a measure of liquidity momentum

Our results suggested that neither the direction of flows inone week (or its 4-week average) nor the change in the direc-tion of flows, on their own, are sufficient to predict nextweek’s equity market performance. We therefore had to testmeasures that go beyond simply looking at the direction ofthe flows. Liquidity momentum, i.e. a measure of rising orcontracting liquidity might prove helpful. Flows might still bepositive (negative) but the size of the inflows (outflows)might already ease, indicating a declining (rising) investorconviction. To measure liquidity momentum we introducedthe liquidity pulse.

Calculation of the Liquidity PulseThe liquidity pulse compares the size of the current flow

(4-week average as % of NAV) with the average size of theflow in the last 13 weeks. The relative size is given in stan-dard deviation from the mean. As a momentum indicator itgauges investor’s confidence in certain regions and the move-ment of momentum in those regions. A high liquidity pulseindicates a liquidity momentum expansion as the asset classin question is experiencing net inflow for many consecutiveweeks. This is an indication of above-average investor confi-dence in a certain region and generally indicates a strong per-formance for equity markets in the respective region. A liq-uidity pulse which is steadily increasing indicates an increasein the amount of fund inflows into the region, and viceversa.

We illustrate the output such that the light blue data pointsare closely around the mean and show moderate changes inmomentum. The dark blue data points are more than onestandard deviation away from the mean and indicate periodsof strongly expanding or contracting liquidity momentum.

The charts in Figures 1 and 2 illustrate the DevelopedEquity Market Pulse (based on the fund flows for WesternEurope, the US and Japan) and the Risky Fund FlowsLiquidity Pulse (based on fund flows for Latin-American

equity funds, Asia-Ex Japan equity funds, EMEA equityfunds, emerging market bond funds and high yield bondfunds). Compared to the Emerging Markets Liquidity Pulse,the Risky Fund Flows Liquidity Pulse captures the addition-al effect of the emerging bond and high yield bond markets.Therefore the Risky Fund Flows Liquidity Pulse shows amore complete picture of risky fund flows than the emerg-ing markets equity liquidity pulse, and we believe that it is amore valuable measure of investor’s willingness to invest inrisky assets, i.e. risk appetite.

Liquidity Pulse and equity market performance When comparing the liquidity pulse data with equity perform-ance, we observe common trends. Figure 3 shows the US liq-uidity pulse versus the US MSCI equity index performancefrom April 2004 to July 2006. The trends of the liquidity pulseand equity performance are similar during periods of consis-tent liquidity momentum expansion and contraction. Thismakes the fund flows a reasonable momentum indicator.However, what we also observe is that if liquidity momentumis signaled to be very strong (or very weak) the subsequentperformance tends to be negative (or positive). This suggeststhat the liquidity pulse becomes a contra indicator whenmomentum has become too strong in either direction. Wefind comparable results for the other regions.

-3

-2

-1

0

1

2

3

Apr

-04

Jun-

0 4

Aug-

0 4

Oct

-04

Dec-

04

Feb-

05

Apr

-05

Jun-

0 5

Aug-

0 5

Oct

-05

Dec-

05

Feb-

06

Apr

- 06

Jun-

0 6

Liquidity M o mentum Expanding

Liquidity M o mentum Co ntracting

Source: Deutsche Bank Equity Strategy / EPFR

Figure 1. Developed Market Equity Liquidity Pulse

-3

-2

-1

0

1

2

3

Apr-0

4

Jun-

04

Aug-

04

Oct

-04

Dec-

04

Feb-

0 5

Apr-0

5

Jun-

05

Aug-

05

Oct

- 05

Dec-

05

Feb-

0 6

Apr-0

6

Jun-

06

Liquidity M o mentum Expanding

Liquidity M o mentum Co ntracting

Source: Deutsche Bank Equity Strategy / EPFR

Figure 2. Risky Fund Flows Liquidity Pulse

-3

-2

-1

0

1

2

3

Apr

-04

May

-04

Jun-

04

Jul-0

4

Au

g-04

Sep-

04

Oct

-04

No

v-04

Dec

-04

Jan-

05

Feb-

05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5

Au

g-05

Sep-

05

Oc t

-05

No

v-05

Dec

-05

Jan-

06

Feb-

06

Mar

-06

Apr

-06

May

-06

Jun-

06

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

US L iquidity P ulse (l.h.s.) Wee kly US MSCI Per formance (r .h.s .)

Source: Deutsche Bank Equity Strategy / EPFR, Factset

Figure 3. US Liquidity Pulse vs. weekly US MSCI Indexperformance

→

22 THE TECHNICAL ANALYST June 2008

Techniques

� Large universe. EPFR tracks a total of 8817 funds with adifferent geographical focus and across different assetclasses. 7725 of these funds are equity funds (as ofAugust 2006)

� Most of the funds under coverage are long only funds,and only a minority of the included hedge funds has shortpositions, but these are insignificant relative to totalinvestment value.

� All the funds included are pure plays – equity funds investonly in equities, and bond funds invest only in debt secu-rities, and not a mixture of both.

� The funds are not generally exchange traded. Data on theproportion of ETFs to non-exchange traded funds is lim-ited, but according to EPFR it is negligible.

� Investors are a mix of retail and institutional investors.EPFR estimates that 70% of them are institutional, thebiggest ones being pension funds and insurance compa-nies. Institutional investors account for most of thoseinvesting in emerging market funds, but we see a higherparticipation of retail investors for Western Europe andUS equity funds.

� EPFR tracks mutual funds on a global basis compared tosome other providers of flow data, and presents the flowof funds into geographical asset classes irrespective ofdomicile. For instance, the flows into Western Europeequity funds represent the amount deposited or with-drawn in funds investing in Western European equitiesirrespective of where the funds are located. We believethat this data is therefore more representative comparedto other data available which tend to only cover fundslocated in the US.

Calculation of flowsOn a weekly basis we obtain the raw data from EPFR, whoin turn obtain it each Wednesday from the respective fundmanagers. EPFR releases the data on Thursday night, hencethe Weekly fund flows note we publish each Friday containsvery timely information.

The calculation of the weekly net flow is as follows:

� Assets BoW = Total fund assets beginning of week(as of prior Wednesday's market close)

� Assets EoW = Total fund assets end of week(as of current Wednesday's market close)

� Weekly Portfolio Change = (Assets BoW) x (Weekly per-formance of fund)*

� Weekly net flow in local currency = Assets EoW – AssetsBoW – Weekly Portfolio Change

� Weekly net flow in $ = Weekly net flow in local currencyx Average weekly forex

� Weekly flow as % of NAV = Weekly net flows in dol-lars/Assets BoW in dollars using beginning of the weekexchange rate

The flow data table which features in our Weekly fund flowsnote contains information on weekly flows, the 4-week aver-age flow as well as the year-to-date net flow for all funds inour universe. The 4-week moving average of the flowssmoothes the data as the weekly flows can at times be quitevolatile. Flow information is provided in absolute dollarsand as a percentage of total assets. The latter improves thecomparability of the flows across regions.

Focus on fund flow as a proportion of total assetsWe recommend analysing fund flow data as a % of totalassets, rather than in dollar terms, because it provides a bet-ter comparison between regions:

� First, funds investing in emerging markets, for instance,tend to be smaller than those investing in developed mar-kets such that weekly flows in dollar terms do not accu-rately reflect the flow momentum across regions.

� Second, the size of net flows (in dollars) tends to changewith the development/index performance of the marketswhich they track.

� Third, EPFR has widened its coverage of fund flows overtime. For a better historical comparison, it is thereforenecessary to look at fund flows as a percentage of thecovered assets rather than in absolute terms.

� Fourth, it is worth noting that the flows are provided indollar terms and are therefore dependant on foreignexchange movements. As the dollar strengthens or weak-ens relative to the funds’ respective local currencies, wecould see some fluctuations in the overall funds which arenot the result of equity investor behaviour.

*change in NAV per share including any dividend distributions

Box 2: A brief guide to fund flow data

We use Emerging Portfolio Fund Research (EPFR) fund flow data for several reasons:

June 2008 THE TECHNICAL ANALYST 23

Techniques

Trading strategies including the Liquidity Pulse We now test trading strategies for individual regions based onthe direction of the 1-week flow in combination with thedirection of the average 4-week flow and the liquidity pulse.The general idea is to stay invested in the market unless allthree indicators send a negative signal.

Strategy with strong/weak liquidity pulse as a contra indicator The first strategy uses the liquidity pulse at the top and thebottom of the range as a contrarian indicator. This assumesfor example that if the momentum falls too much, it will hita lower boundary and rebound into positive territory, alongwith equity performance. The same principle applies to veryhigh momentum. If the liquidity pulse lies above 1, it is takenas a contrarian indicator and is a negative signal, if it liesbetween 1 and 0 it is a positive signal, if it lies between 0 and-1 it is a negative signal and if it is below -1 it is again a con-trarian indicator and hence a positive signal. The data andperformance charts for our strategy for the emerging marketsare shown in Figure 4.

The strategy outperformed the market from February 2001to July 2006 by 72pp (study conducted August 2006) with aninformation ratio of roughly 70% both based on annualisedweekly returns as well as on returns by calendar year. Thestrategy rose by 154%, compared to 83% for the benchmark,if all excess returns are reinvested. Note that the strategy hasin particular outperformed during a bear or sideways market.Between 2001 and 2003 the trading strategy tended to out-perform especially when the MSCI Index dropped, as itpicked up the signals and went short. It has non-negativeexcess returns in 97.5% of the weeks, mostly because it stayslong most of the time. The problem however is that it hasnot given many signals to trade since then and as a result didnot pick up the market correction in May 2006. The flow datasignals were not clear enough to be picked up by the tradingstrategy. This trading strategy therefore has not outper-formed the bull market since March 2003.

We increased the boundaries of the liquidity pulse to 1.5xstandard deviation in order for the contrarian indicators toreact at more extreme levels. This way the strategy increasedthe number of trades executed and for the emerging marketsincreased its performance to 184%. The information ratiothough did not improve.

We applied the same strategy to all other regions. With theLiquidity Pulse boundaries set to 1x standard deviation forthe Liquidity Pulse to become a contra indicator, a positiveexcess return is generated for the US, Japan and theEmerging Market with the information ratio ranging from0.3 to 0.7. The main problem with this strategy is that it hasnot worked well since 2003. While it seems to work well in abear market, it does not in a bull market. We believe the mainreason why the strategy does not work well for other regions,is because for most regions we only have data available forthe bull market. We cannot back test this strategy for the bearmarket period, and therefore cannot make any clear conclu-sions on its ability to outperform the bear market in anyregions other than the emerging markets.

Increasing the sensitivity of the strategy to the flow signalsdecreases its overall performance, as does the introduction ofadditional signals from flows into bond funds data or fromtaking the difference of weekly flows. We cannot draw anyclear conclusions from the results obtained.

Strategy with only weak liquidity pulse as a contra indicatorOur second strategy is similar to the one above but a liquidi-ty pulse above 0 is taken as a positive signal, if it is between0 and -1.5 it is taken as a negative signal and if it is below -1.5 it is taken as a contrarian indicator, and hence a positivesignal. Again we show the results for the emerging markets inFigure 5. This strategy also outperforms the market consider-ably, but has the same limitations as above.

Predictive power of fund flows for regional allocationAnother question we wanted to answer is whether the

50

100

150

200

250

300

350

400

Feb

-01

Ma

y-0 1

Au

g-01

Nov

-01

Feb

-02

Ma

y-0 2

Au

g-02

Nov

-02

Feb

-03

Ma

y-03

Au

g-03

Nov

- 03

Feb

-04

Ma

y-04

Au

g-04

Nov

- 04

Feb

-05

Ma

y-05

Au

g-05

Nov

-05

Feb

- 06

Ma

y-06

0. 90

1. 10

1. 30

1. 50

1. 70

1. 90

2. 10

B enchmark (MS CI Emer ging Mar kets Index) (l.h. s .)

Portfolio (Trading S trategy F or Eme rging Ma rkets) (l.h.s .)

Outperformance (r .h. s .)

Source: Deutsche Bank Equity Strategy / EPFR, Factset

Figure 4. Trading strategy vs. benchmark (liquidity pulse boundaries at 1x)

50

100

150

200

250

300

350

400

Feb

-01

Ma

y-01

Au

g-01

Nov

-01

Feb

-02

Ma

y-0 2

Au

g-0 2

Nov

-02

Feb

-03

Ma

y-03

Au

g-03

Nov

-03

Feb

-04

Ma

y-0 4

Au

g-04

Nov

-04

Feb

- 05

Ma

y-0 5

Au

g-05

Nov

-05

Feb

-06

Ma

y-0 6

0. 90

1. 10

1. 30

1. 50

1. 70

1. 90

2. 10

B enchmark (MS CI Emer ging Mar kets Index) (l.h. s .)

Portfolio (Trading S trategy F or Eme rging Ma rkets) (l.h.s .)

Outperformance (r .h. s .)

Source: Deutsche Bank Equity Strategy / EPFR, Factset

Figure 5. Trading strategy vs. benchmark (liquidity pulse boundaries at 1.5x)

→

June 2008 THE TECHNICAL ANALYST 25

Techniques

relative strength of flows for different regions contains anyexplanatory power for subsequent relative performance ofthe regions.

We look at the six main regions covered by the fund flowdata: Western Europe, the US, Latin-America, Asia ex Japan,Japan, and EMEA. The cross-sectional comparison of theflows is based on the 4-week average flow as % of NAV forthe six regions. Each week we normalise these 6 observationsby calculating the cross-sectional z-score. z-scores are cappedat 2 to reduce the noise in the data. It is ensured though, thatthe sum of the z-scores equals zero.

The benchmark is an equally weighted portfolio of the sixregions with weekly re-adjustment. The strategy takes activebets relative to the benchmark with the size and the directionof the active bet similar to the z-score of the flows times afixed multiplier. For example, if a region has a z-score of 1,we add one percentage point, times the multiplier, to the ini-tial weighting of 16.7% to that region. Therefore every weekwe readjust our positions in all 6 regions around their initialpositions of 16.7%, depending on their respective z-score

values. We use a multiplier 3, meaning that the absolute sizeof the maximal active bet equals 6pp.

Our strategy outperformed the market in 2003, 2004, 2005and marginally underperformed in 2006 (to 10 August 2006).57.5% of the weekly excess returns have been positive. Theaverage annualized excess at 0.94% compared to the bench-mark looks small, but with an even smaller tracking error of0.74% the information ratio is 1.28. Fund reallocations of151% of the portfolio size were needed annually, suggestingthat even including transaction costs an excess return can begenerated. The results suggest that the relative strength ofweekly fund flows can add value to models of regional equi-ty allocation.

Bernd Myer, Joelle Anamootoo and Ingo Schmitz areEquity Strategists at Deutsche Bank AG. This article isbased on their report “Predictive power of weekly fundflows” (2006). For information on EPFR data visitwww.epfr.com.

26 THE TECHNICAL ANALYST June 2008

Techniques

presents

A premier event for trading and investment professionals

Speakers include:

Automated Trading

200815 October 2008

Royal Society of Medicine

London W1

Backtesting andoptimisation

Web: www.technicalanalyst.co.uk

Telephone: +44 (0)1483 573150

Register Today!

Email: [email protected]

Topics include: Who should attend:

Delegate fee: £495 + VATRegister by 31 July for £100 early bird discount

+ Data integrity + Statistical analysis of test results + Correlation between asset classes+ Issues in data mining+ Monte Carlo techniques + Avoiding curve fitting

+ Traders + Fund managers + Hedge funds + Proprietary dealers + Quantitative analysts + Algorithmic trading managers

Automated Trading 2008 is a one day confer-ence for traders and investment managers involved in automated or systematic trading across all asset classes. Bringing together leading experts from the UK and US, this event will focus on backtesting and optimisation strategies for those looking to develop and build their own automated trading system.

David Aronson Baruch University

Gaurav Mangla Collage LLC

Daniel Jones Oxford University

Richard RamyarLipper

Woon WongCardiff Business School

Emmanuel Acar Directional Trading

The Arms Index, otherwise know as the TRIN (short forTrading Index), has traditionally been used as a short termindicator for US stocks that uses daily price and volume datato measure relative demand for rising and falling stocks. Byusing data from all 2250 or so stocks listed on the NYSE, theindex acts, in effect, as a volume weighted ratio of risingstocks versus falling stocks. This ratio can then be used as anindicator of how buying or selling pressure in the market ischanging.

Although the ARMS Index is calculated using data from allNYSE stocks, it can be refined to include just S&P or Dowstocks. However, Richard Arms warns that the effectivenessof the index is reduced when fewer stocks are used in its cal-culation. Moreover, despite its widespread use as a shortterm indicator, Arms insists that the TRIN can be used forlong term analysis and that many of his clients are tradition-al long term fund managers and not necessarily just shortterm intraday traders.

Arms today runs a consulting firm, ARMS Advisory, fromhis base in Albuquerque, New Mexico specialising in provid-ing TRIN based research to trading and investment houses.Richard spoke to the Technical Analyst for this feature andhis views on using and interpreting the TRIN are included.

The ARMS Index The ARMS Index is calculated using daily closing prices andvolume data from the New York Stock Exchange (NYSE).The formula is familiar enough:

Advances the number of NYSE listed stocks thatclose higher

Declines the number of NYSE listed stocks thatclose down

Advancing volume the volume of stocks closing higherDeclining volume the volume of stocks ending low

The TRIN calculation produces an index that centres around1.0, a value where the index is said to be neutral as advancingand declining volume is equally spread over rising and fallingissues. Because of the nature of the formula, the index pro-duced is counter-intuitive in nature in that if more volume isgoing into stocks that are rising in price, the index falls

The ARMS IndexWe take a look at the famous ARMS index and try to establish how best to use the indicator when trad-ing US stocks.

Figure 1.

ARMS Index =

Number ofadvancing stocks

Number ofdeclining stocks

Advancingvolume

Decliningvolume

÷

→

28 THE TECHNICAL ANALYST June 2008

Techniques

June 2008 THE TECHNICAL ANALYST 29

Techniques

30 THE TECHNICAL ANALYST June 2008

Techniques

below 1.0 and visa versa. So if the index is above 1.0 then itis said to be bearish for stocks and below 1.0 is bullish. Thisis because even if, for example, the number of rising stocksexceeds the number of declining stocks the index will rise ifthis occurs on low or declining volume.

Using the TRIN The index or line that this equation produces from daily datais often used smoothed using a moving average. Indeed,many references to using the TRIN are often made in termsof its moving average.

However, beyond that the index is open to a great deal ofinterpretation. Some users of TRIN tend to adopt their ownparameters as to which reading indicates a bullish or bearishsignal. Richard Arms himself recommends using the follow-ing moving averages for trading different time scales:

Short term: 4 day MA

Intermediate: 10 day MA

Medium term: 21 day MA

Long term: 55 day MA

(Note that 21 and 55 are both Fibonacci numbers).

Wall Street traders and investment managers have tradi-tionally used the 10 day moving average for TRIN. This is

probably because before the use of computers, it was an eas-ier figure to work with.

Despite the index being considered bullish when it is below1.0 and bearish when it is above 1.0, Richard Arms himselfconcedes that the index appears to be most effective whenused as an overbought/oversold indicator. However, there isno consensus on what constitutes overbought or oversoldconditions and furthermore, they depend on what movingaverage of the index is being used. John Murphy states thatthe TRIN can be used as a contrary indicator, especially inintraday trading. A very high figure (strongly bearish) is there-fore bullish as it indicates a turning point.

According to Katie Townshend chief market technician atMKM Partners, a proprietary trading and research firm basedin Greenwich, Connecticut, the real value of the TRIN lies inits application as a breadth indicator, as well as an over-bought/oversold oscillator. Furthermore, the TRIN shouldnot be used in isolation but only when other indicators con-firm it. “I publish the TRIN reading on a daily basis in anemail to clients but only heed it when it reaches extremes.Lately, a high extreme has been about >2.0 and a low extremehas been about <0.5.”

“When it reaches a high extreme, which usually happens onsharp down days, it can be considered an oversold readingthat suggests the next day or two will be more bullish.Conversely, when it reaches a low extreme, which usually isassociated with strong up days, it can be considered an over-bought reading that suggests the next day or two will be morebearish”, she says.

“WALL STREET TRADERS AND INVESTMENT MANAGERS HAVE TRADITIONALLY USED THE

10 DAY MOVING AVERAGE”

→

June 2008 THE TECHNICAL ANALYST 31

Techniques

Trading rulesRichard Arms recommended trading rules based on using theTRIN as an overbought/oversold oscillator are as follows:

Moving Average Overbought Oversold(sell) (buy)

Short term (4 to 10 day) <0.75 >1.25Medium term (21 day) <0.85 >1.10Long term (55 day) <0.90 >1.05

The TRIN suffers to some extent from a lack of consen-sus regarding not only which moving averages to use butwhat readings of the index indicate a buy and sell signal. Thisis a drawback because it suggests that the ideal parametersmay change as market conditions change so the optimal read-ings to use are likely to remain unknown at any particulartime.

In addition, there have been very few proper statisticalstudies on the TRIN which is surprising given how popularthe index is often said to be. What does appear to be agreedon is that using the index in its simplest form without a mov-ing average, (buy<1.0, sell>1.0) does not produce profitableresults.

Robert Colby, a US based analyst who has written aboutand backtested most (if not all) technical indicators* foundthat the ARMS index has little predictive power for readingsbetween 0.523 and 1.444. However, extreme readings beyondthese were profitable with a one year holding period to a 99%confidence level. Although Colby also cites the TRIN’s valueis being used as an overbought/oversold indicator, he alsosays that extreme readings of the index in either direction(above 1.444 and below 0.523) give a bullish reading.Backtesting showed this result had a 99% confidence levelfor a 1-year holding period although the number of signalsthis strategy has generated since 2000 has gone up consider-ably, which calls into question whether it is still valid. Thelow readings of the index are bullish because this usuallyindicates a (oversold) reversal after the end of a decline orbear market.

The problem with these findings is that TRIN is usuallythought of as a short term indicator and used as such whichmakes a one year holding period unrealistic. Colby states thatthe 10 day simple moving average above 1.266 is very bullishfor a one year holding period to a 99% confidence level.From this Colby proposes a “greater than 1.266 rule”. Itshould be noted that these results are based on data before2000.

Based on backtesting 16 years of data, for short term trad-ing Colby recommends the following rule:

Buy: 11 day exponential moving average (EMA) > 0.8

Sell: 11 day EMA < 0.8

This strategy according to Colby would have returned1640% for the S&P500 (with reinvested profits and no costs)during the test period from 1984 to 2000, more than 80%more than a buy and hold strategy (900% return).

Colby also cites the significance of a single day’s reading of2.65 for the index. If the S&P500 had been bought on theclose of every day when the index was 2.65 or above over inthe 35 years before 2000, it would have yielded a profit 11 outof the 12 instances it happened when held for one year.

Holding period Although Colby sites a one year holding period in all his test-ing of TRIN and doesn’t vary this, Kirkpatrick andDahlquist** insist that the holding period is crucial to theprofitability of the indicator. For example, with the >2.65rule, although the signal only occurs every couple of years, ifthe holding period is reduced from one year to two monthsor less, the returns are some 100 times greater than a buy andhold strategy. Kirkpatrick suggest the difficulty in establishingthese rules for the TRIN comes in applying short term indi-cators to long (one year) holding periods.

Other signalsAccording to other literature there are other signals that theTRIN can generate. As Richard Arms explains, “Apart fromthe well known use of the index moving averages, I haveworked a great deal with moving average crossovers. Thebest, I think, is the 21-day to 55-day. The 55 becomes thebaseline and the 21 indicates the extremes. Another simplestrategy is two consecutive days of the index over 2.0 whichhas a very good record of calling important bottoms.”

Richard ARMS’ new book, “Stop and Make Money: How to Profitin the Stock Market Using Volume and Stop Orders” has recentlybeen published by Wiley.

*The Encyclopaedia of Technical Market Indicators(McGraw Hill) by Robert Colby **Technical Analysis (FT Press) by Charles Kirkpatrick andJulie Dahlquist

“THE INDEX ACTS AS AVOLUME WEIGHTED

RATIO OF RISING AND

FALLING STOCKS”

Double Top and Double Bottom pat-terns are part of classic technical analy-sis. Double Top/Bottom patterns arevery common and form in all time-frames and in all instruments. Thesepatterns form when prices fail to makenew highs/new lows at significant pre-vious levels. Double Top and Bottompatterns are relatively reliable and easyto trade. When Double Bottoms/Topsfail, they may be signaling potentialTriple Top or Triple Bottoms patterns.Double Top/Bottom patterns have sev-eral variants and these variations involvedifferent trading rules and different pat-tern recognition methods.

Formation of Double Top/Bottom patternsIn active markets, Double Top/Bottompatterns are found as the market worksup rapidly in a peak or trough accompa-

nied by high volume in the first stage.Without any warning signs the marketreverses and retraces to a key supportlevel/resistance and stagnates for fewbars before rising/falling to the previ-ous peak/trough with lesser volume inthe second stage. These two sharpmoves create the Double Top/Bottompatterns and signal a potential reversalof prior trends. In most Double Top orDouble Bottom patterns the two swingpeaks or troughs need not be equal andthe first or second peak or trough canbe higher/lower.

The preceding movement prior to theDouble Top/Bottom pattern forma-tion signals whether the pattern is acontinuation or reversal pattern. If thepreceding movement is a long contin-ued up/down trend prior to the firstpeak/trough, the pattern may be signal-ing a reversal while if the preceding

movement is a short trend, it may besignaling a continuation pattern.Markets making new highs/lows (atleast 40-bar) in the first peak/troughmay signal reversal patterns.

The “size” of the pattern or durationof the interval between the twopeaks/troughs measures the success ofthe pattern. A long duration betweenthe two peaks/troughs signals a highpossibility of reversal. The “size” ofthe retracement (at least 15% from thefirst swing) between the twopeaks/troughs also indicates the likeli-hood of pattern success. High volumeduring the first peak/trough and lightervolume in the second peak/trough fol-lowed again by higher volume duringthe breakout/breakdown signalsgreater probability of pattern success.

Double Top Trading RulesDouble Top patterns are recognized bythe two peaks with an intermediatereaction swing low. After completion ofthe second peak, prices trade below thereaction low to signal a potential trade.

Trading RulesTrade: A Double top pattern confirma-tion occurs at the breakdown level ofthe swing low at the neckline. Enter ashort trade below the previous swinglow at the neckline (see Figure 3).Target: The Double Top offers a

Chart patterns like Double Tops and Head-and-Shoulders essentially convey thesame signal – that of a trend reversal at the end of the pattern. Given the poten-tially important long-term Double Tops forming in the FTSE and S&P (seeFigures 1 and 2), we ask Suri Duddella to discuss the many variants of DoubleTops and Double Bottoms and to highlight some of their different trading rules.

Figure 1. Figure 2.

Trading Variations in DoubleTops and Double Bottoms By Suri Duddella

→

32 THE TECHNICAL ANALYST June 2008

Techniques

good risk/reward ratio. Measure thedistance between the top of the patternto the neckline for potential target rangefrom the trade entry (see Figure 4).

Stop: Double tops also fail and formtriple or multiple top patterns. Usuallythe failure occurs when prices reverseand trade at the middle of the Doubletop pattern range. Enter a stop order atthe middle of the pattern range to pro-tect the trade.

Double Bottom Trading RulesThe Double Bottom pattern is a mirrorimage of the Double Top. An extendeddown trend results in new lows fol-lowed by a moderate rally from the firstbottom. After a brief rally the pricesattempt to test the first bottom again.Failure to trade below the first-bottomresults in a second-bottom as pricesrally and reverse the prior trend. Theintermediate swing-high between thetwo bottoms is called the ‘reactionswing-high’. When price trades abovethis ‘reaction swing-high’, it signals apotential long trade.

Trading RulesTrade: A Double Bottom can only betraded after confirmation of the patternbreakout. Confirmation of the patternoccurs when prices close above theneckline. Enter a long trade above thehigh of the breakout bar from the neck-line (see Figure 5).Target: The Double Bottom pattern

also has a good risk/reward ratio. Thefirst target would be 100% of the swingrange of the pattern. The second targetwould be 127% to 162% of the depthof the “double bottom” pattern (seeFigure 6).

Stop: Double Bottom patterns do fail.This pattern failure occurs if the pricecloses below the middle of the patternfor multiple bars. Trading below thebottom of the pattern could signal atriple bottom. Place a stop order belowthe middle of the pattern to protect thetrade.

Variations of Double Top/Bottom patternsKnowledge of the variations and theirtrading rules dramatically increases the

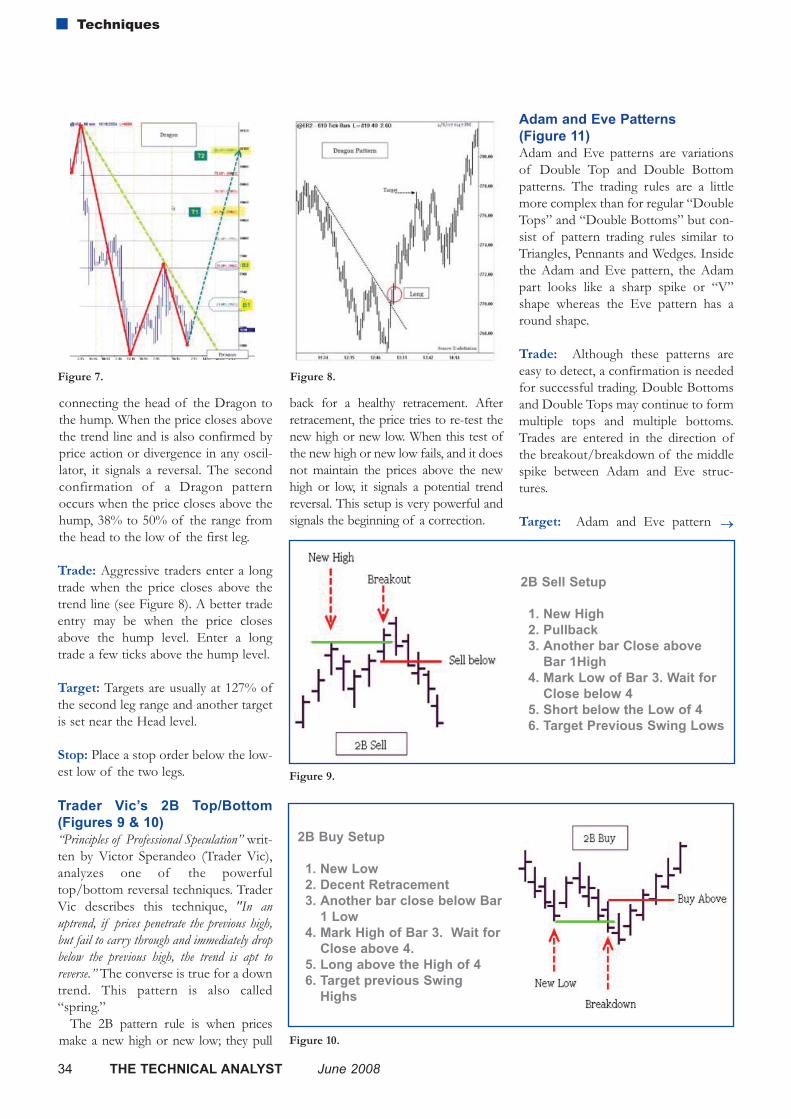

chance of trading Double Tops andBottoms successfully. Most patternshave some variation of their basicstructure (simple or complex) with dif-ferent trading rules to their cousins inthe same group, but have the samerequirements as to volume action, pricemovement and timing. Some examplesof Double Top and Bottom variantsare: Dragon Patterns, Trader Vics’ 2BTop/2B Bottom, and Adam and Evepatterns, which I briefly review here.

Dragon Pattern (Figure 7)Dragon patterns usually form at marketbottoms. Dragon patterns work in alltime-frames and in all market instru-ments. Like most Double bottom pat-terns, Dragon patterns present excellenttrading opportunities with low risk toreward ratios. The Dragon pattern issimilar to the “W” pattern and theInverse Dragon pattern is similar to the“M” pattern, albeit with different trad-ing rules.

The Dragon pattern starts with a“Head” formation and price declinesfrom the head level to form two legs ofthe Dragon. These two legs in aDragon pattern usually form within 5%to 10% of the price difference. The sec-ond leg gives a strong indication ofimminent reversal when it posts a key

reversal bar or a divergence in any oscil-lator indicators. The price rise in thesecond leg is usually followed by a spikein the volume. A trend line is drawn

Figure 3. Figure 4.

Figure 5. Figure 6.

→

June 2008 THE TECHNICAL ANALYST 33

Techniques

connecting the head of the Dragon tothe hump. When the price closes abovethe trend line and is also confirmed byprice action or divergence in any oscil-lator, it signals a reversal. The secondconfirmation of a Dragon patternoccurs when the price closes above thehump, 38% to 50% of the range fromthe head to the low of the first leg.