issue 38 april 2016 | quarterly publication | compiled by

TRANSCRIPT

Issue 38 – April 2016 | Quarterly Publication | Compiled by Graeme Holt

2

Page 2 – The Rand and what you need to do to safeguard your wealth

Page 7 – Safeguarding your wealth in times of uncertainty

Page 9 – Diversify your risk and invest offshore

Page 10 – Update on Pension tax laws amendment bill

Page 11 – Market Overview

Page 14 & 15 – VPFP Contact Details and Services

The Rand and what you need to do to safeguard your wealth

In the wake of “Nene gate” and subsequent blow out of the Rand it is natural that we as South Africans

have a lot to be concerned about both in the short term and the longer term. In this issue we felt it important to firstly, revisit and understand what factors influence exchange rates and secondly, what

you need to do as an investor to remain on track to achieving your long term financial goals in times of uncertainty.

The Rand Before we look at these forces, we should sketch out how exchange rate movements affect a nation's

trading relationships with other nations. A higher currency (strong currency) makes a country's exports more expensive and imports cheaper in foreign markets; a lower currency (weak currency)

makes a country's exports cheaper and its imports more expensive in foreign markets. A higher exchange rate can be expected to lower the country's balance of trade, while a lower exchange rate

would increase it.

Aside from factors such as interest rates and inflation, the exchange rate is one of the most important

determinants of a country's relative level of economic health. Exchange rates play a vital role in a country's level of trade, which is critical to every free market economy in the world. For this reason,

exchange rates are among the most watched, analysed and governmentally manipulated economic measures. But exchange rates matter on a smaller scale as well: they impact the real return of an

investor's portfolio. Here we look at some of the major forces behind exchange rate movements.

Note: Numerous factors determine exchange rates, and all are related to the trading relationship between two countries. Remember, exchange rates are relative, and are expressed as a comparison

of the currencies of two countries. The following are some of the principal determinants of the

exchange rate between two countries. Note that these factors are in no particular order; like many aspects of economics, the relative importance of these factors is subject to much debate.

1. Differentials in Inflation

As a general rule, a country with a consistently lower inflation rate exhibits a rising currency value, as

its purchasing power increases relative to other currencies. During the last half of the twentieth century, the countries with low inflation included Japan, Germany and Switzerland, while the U.S. and

Canada achieved low inflation only later. Those countries with higher inflation typically see depreciation in their currency in relation to the currencies of their trading partners. This is also usually

accompanied by higher interest rates.

Over time, ignoring all other factors, a currency should appreciate/depreciate in line with the inflation differential of its trading partner.

On the Table this Quarter

3

Example:

US inflation 1% vs SA inflation 7% - The Rand will depreciate by roughly 6% versus the US dollar on

a basket of goods – purchasing power.

The chart below illustrates the fair value of the Rand – based on inflation differentials – against the US Dollar, using 1999 as a starting point. Based on this analysis the Rand should be trading around

R/$10.42, which indicates roughly a 60% undervaluation. In real terms, it is the second most

undervalued it has been in nearly half a century, perhaps justifiable given the collapse of dollar-based commodity prices.

When commodity prices do recover, the Rand will strengthen, especially from its current level, muting the impact of imported inflation. In addition, should the low growth/low interest rate environment

persist in developed economies, and volatility settles, then yield seekers will eventually return to emerging markets. It goes without saying that calling currency moves is difficult, but at such extreme

fundamental levels (strong US$ and low priced oil & commodities), maybe a contrarian view is prudent.

The chart below illustrates how the Rand responds positively to commodity price rises and vice versa.

4

The Rands real effective change rate (REER) determined by the commodity cycle.

2. Differentials in Interest Rates

Interest rates, inflation and exchange rates are all highly correlated. By manipulating interest rates, central banks exert influence over both inflation and exchange rates, and changing interest

rates impact inflation and currency values. Higher interest rates offer lenders in an economy a higher return relative to other countries. Therefore, higher interest rates attract foreign capital and cause the

exchange rate to rise (stronger currency). The impact of higher interest rates is mitigated, however, if inflation in the country is much higher than in others, or if additional factors serve to drive the

currency down. The opposite relationship exists for decreasing interest rates - that is, lower interest

rates tend to decrease exchange rates (weak currency).

3. Current-Account Deficits The current account is the balance of trade between a country and its trading partners, reflecting all

payments between countries for goods and services. A deficit in the current account shows the country is spending more on foreign trade than it is earning (imports are higher than exports), and that it is

borrowing or relying on capital inflows (stocks, bonds, FDI) from foreign sources to make up the

deficit. In other words, the country requires more foreign currency than it receives through sales of exports, and it supplies more of its own currency than foreigners demand for its products. The excess

demand for foreign currency (imports) lowers the country's exchange rate until domestic goods and services are cheap enough for foreigners, and foreign assets are too expensive to generate sales for

domestic interests.

5

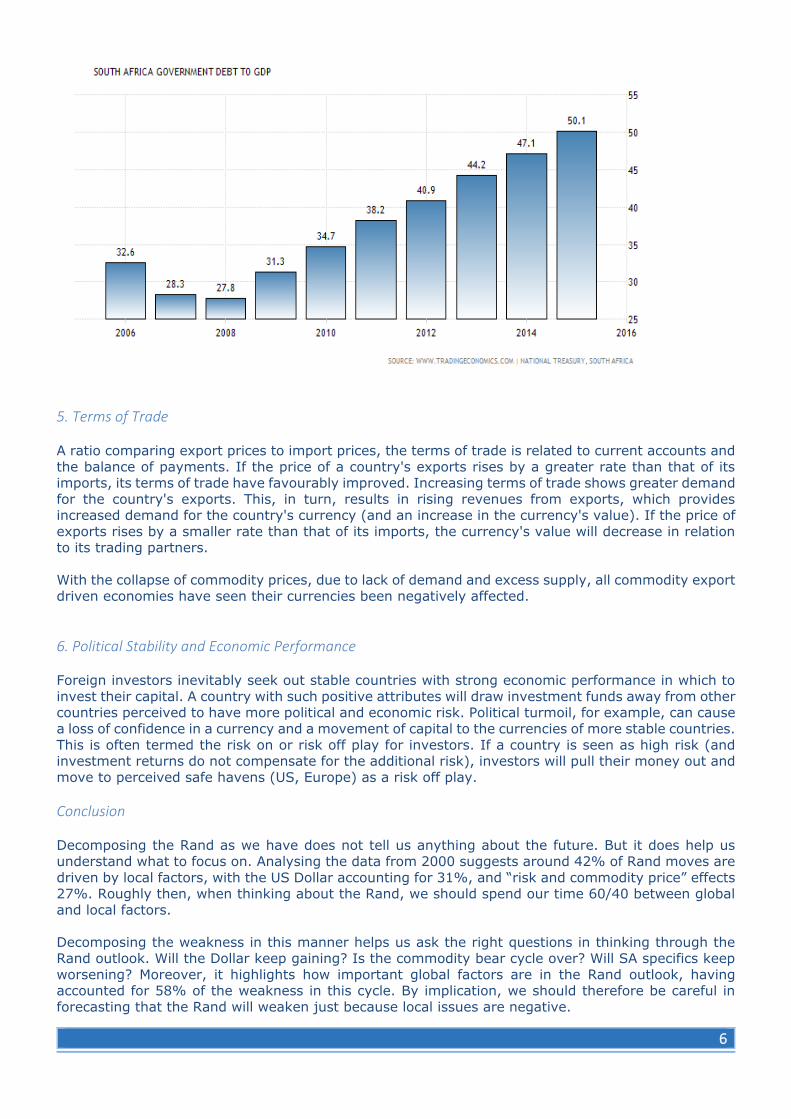

4. Public Debt Countries will engage in large-scale deficit financing to pay for public sector projects and government

funding. While such activity stimulates the domestic economy, nations with large public deficits and

debts are less attractive to foreign investors. The reason? A large debt encourages inflation, and if inflation is high, the debt will be serviced and ultimately paid off with cheaper currency in the future,

making it harder to service.

In the worst case scenario, a government may print money to pay part of a large debt, but increasing the money supply inevitably causes inflation. Moreover, if a government is not able to service its deficit

through domestic means (selling domestic bonds, increasing the money supply), then it must increase the supply of securities for sale to foreigners, thereby lowering their prices and offering a higher yield,

which again increases the government’s debt obligation. Finally, a large debt may prove worrisome to

foreigners if they believe the country risks defaulting on its obligations. Foreigners will be less willing to own securities denominated in that currency if the risk of default is great. For this reason, the

country's debt rating (as determined by rating agencies such as Moody's or Standard and Poors) is a crucial determinant of its exchange rate.

In a scenario of high inflation (cannot afford to print money) and insufficient bond purchases the

government will turn to higher taxation to service the public debt.

6

5. Terms of Trade

A ratio comparing export prices to import prices, the terms of trade is related to current accounts and

the balance of payments. If the price of a country's exports rises by a greater rate than that of its imports, its terms of trade have favourably improved. Increasing terms of trade shows greater demand

for the country's exports. This, in turn, results in rising revenues from exports, which provides increased demand for the country's currency (and an increase in the currency's value). If the price of

exports rises by a smaller rate than that of its imports, the currency's value will decrease in relation to its trading partners.

With the collapse of commodity prices, due to lack of demand and excess supply, all commodity export

driven economies have seen their currencies been negatively affected.

6. Political Stability and Economic Performance Foreign investors inevitably seek out stable countries with strong economic performance in which to

invest their capital. A country with such positive attributes will draw investment funds away from other countries perceived to have more political and economic risk. Political turmoil, for example, can cause

a loss of confidence in a currency and a movement of capital to the currencies of more stable countries.

This is often termed the risk on or risk off play for investors. If a country is seen as high risk (and investment returns do not compensate for the additional risk), investors will pull their money out and

move to perceived safe havens (US, Europe) as a risk off play.

Conclusion Decomposing the Rand as we have does not tell us anything about the future. But it does help us

understand what to focus on. Analysing the data from 2000 suggests around 42% of Rand moves are

driven by local factors, with the US Dollar accounting for 31%, and “risk and commodity price” effects 27%. Roughly then, when thinking about the Rand, we should spend our time 60/40 between global

and local factors.

Decomposing the weakness in this manner helps us ask the right questions in thinking through the Rand outlook. Will the Dollar keep gaining? Is the commodity bear cycle over? Will SA specifics keep

worsening? Moreover, it highlights how important global factors are in the Rand outlook, having accounted for 58% of the weakness in this cycle. By implication, we should therefore be careful in

forecasting that the Rand will weaken just because local issues are negative.

7

Safeguarding your wealth in times of uncertainty

Our job, as custodians of your wealth, need to protect you from many risks not just market and

currency volatility. We also have to ensure that you are making the most rational decisions that will

help you obtain your financial objectives in the long run.

It’s very easy to be emotionally driven by short term news flow, especially when its sensationalised

and hyped up to generate the biggest audience and social network following. It’s not necessarily the

content of the news flow but how we interpret the information and use it in our decision making that’s

most important.

History shows that people are generally not good at making rational long-term financial decisions in

times of duress. According to studies by Dalbar, “Quantitative Analysis of Investor Behaviour 2015”

investors lose as much as 66% of their potential returns over long periods of time due to poor investor

decision-making. This means that if you invest R100 000 over 30 years, you could end with R2 326

645 if you achieve the normal, average returns. However most investors actually only receive R305

257! The difference is not explained by fees because the normal average returns include fees.

Therefore it can only be explained by investors selling quality investments at the wrong time (when

they are losing money) and buying them when they are already too expensive.

So, how do you make rational financial decisions in difficult times?

Firstly, you have to resist the temptation to think short term. The markets always move in long cycles

and it would be a mistake to believe that a trend that started in 2011 will continue forever. In this

instance, the commodity cycle started its decline in 2011 and this caused emerging market currencies

to decline along this path. It is important to remember that every month the downturn continues is

also a step closer to the end of the cycle. Towards the end of any cycle, the markets become

increasingly irrational and this often scares the investors who had been holding on. It is always worth

remembering that markets can be irrational for longer than you think but if you are able to temper

your emotions and ignore the noise this will afford the opportunity to be buying quality assets at a

discount.

Secondly, try stay away from the doomsayers and forecasters. The truth is no one knows what the

future might or might not bring, but pinning your hopes on speculative outcomes does come at a

price. All the predictions that we are seeing from “experts” about “obvious” events often won’t happen

or they take longer to materialise than what we planned for – all at a price. Do you remember how

inflation was going to be out of control in the US because of the Federal Reserve’s Quantitative Easing

policy (QE1, 2 and 3)? This “obvious” event still has not materialised after seven years and making

the decision to be invested in cash over this period has certainly not been rewarding.

What are VPFP doing to safeguard your future?

At VPFP we made the decision to align the advisory and asset management skills in order for the client

to obtain the best possible outcome regardless of the multitude of financial complexities.

We avoid “all or nothing” decisions and strive for consistency, both in application and investment

returns. We avoid big investment decisions that are based on predictions. This is usually the cause of

serious financial losses for investors. Rather than following conventional ideas and speculative

8

thought, we “look through” the noise to identify and purchase quality assets that hold a value bias

with a high probability of a positive outcome for our clients.

We believe the best way to safeguard your assets is to diversify your investment portfolio across a

range of asset types, time and countries. Proper diversification will ensure that regardless of political

ignominy, what the news is reporting or where the currency is headed, your portfolio is positioned to

weather the storm and achieve its target return objective.

9

Diversify your risk and invest offshore

While the case for offshore investing is always topical, it has been even more so over the past two

years as the local market stalls and the Rand sustained its slide against major currencies.

But investing offshore is a long-term, “through-the-cycle” decision and shouldn’t be guided by isolated

factors like Rand weakness, the slowdown in China or the online blog from the emotional expat. The decision to invest offshore goes hand in hand with a realisation that as an investor, you need to

diversify your portfolio across geographies, sectors, companies and currencies.

Investing offshore widens the opportunity set to an investable universe not available to investors with exposure to the local market. Going offshore also offers investors a chance to access international

investment managers with different investment processes and ideas. All these factors can help

diversify your asset exposure and reduce overall risk on your balance sheet.

When to go offshore? Whilst it’s never a bad time to invest in offshore markets there should be a few factors to consider

and strategies to employ to make sure you get the most from your investment and your expectations are met.

Currency diversification and earnings growth The depreciation of the Rand and the earnings growth have been by far the most significant sources

of return. With the Rand depreciating significantly over the last year, it is no surprise that the bulk of the offshore return in Rand was related to the currency. With the typical sources of equity returns

being earnings growth, dividend yield and share rating, it is interesting to note that the contribution

of the earnings growth over the same period was still relatively high at 49% (of returns in US Dollars).

The SA market is extremely concentrated Currently 20 stocks on the JSE All Share Index represent between 70% and 80% of the overall market

capitalisation which illustrates how concentrated our local market is. Considering the Rand diversification and growth offered by offshore investing and the fact that the South African equity

market is highly concentrated, the decision is not whether investors should have offshore exposure

but how much it should be?

Financial planning A good starting point would be to identify what percentage of your balance sheet you would like to

peg in hard currency? This will be highly dependent on personal circumstances like current lifestyle, future needs and current exposure through assets such as Pension Funds. Regulation 28 compliant

funds (funds that are allowed to manage pension fund assets) may have up to 25% of their assets

offshore plus a 5% exposure to Africa.

While decisions about the extent of offshore exposure should be taken with care, in general, studies around the optimal level of offshore exposure (depending on the return objective and considering the

economic cycle), suggest that an optimal offshore allocation is probably somewhere between 20% and 40% of your balance sheet.

A target return objective and investment term should be set up with your planner to gauge future performance. When to move should not be an all or nothing approach but rather planned entry points

and the money allocated in tranches.

If you would like to set up an offshore investment please contact your financial advisor for further information.

10

Update on Pension tax laws amendment bill

The following changes have been introduced through an urgent tax amendment bill, and will NOT continue as scheduled from 1 March 2016:

1. The bill will propose to Parliament to postpone the annuitisation requirement for provident

funds for two years, until 1 March 2018.

2. Provident fund members will not be required to annuitise contributions to their funds that

were made before 1 March 2018.

3. To ensure the integrity of the retirement system, the ability to transfer tax-free from pension fund to provident fund will also be delayed until 1 March 2018. Clarity on possible

misinterpretations will also be provided in the bill, to ensure that payroll administrators apply the law in line with original intentions.

The following amendments will continue as scheduled from 1 March 2016:

1. The tax deduction for contributions to all retirement funds (including provident funds) will

increase to 27.5 per cent of the greater of taxable or remuneration, up to a cap of R350 000

per year, from 1 March 2016.

2. The minimum threshold required for annuitisation for pension and retirement annuity funds

will still be increased from R75 000 to R247 500.

3. Aside from the issues covered in the urgent tax amendment bill, all other provisions

legislated in the 2015 Tax Laws Amendment Act (and all other tax laws) will come into force on 1 March 2016.

11

Market Overview

After the “Nenegate” tornado that hit in the fourth quarter of 2015, 2016 has continued to serve up

significant surprises, both locally and abroad.

Market volatility combined with geopolitical uncertainty caused material losses in all risk assets in January 2016. This was extremely evident in global developed market equities, global listed property

and most emerging market assets. Oil was again under pressure, hitting a low of US$26/barrel, while most industrial commodities like Iron Ore and Steel also continued to fall.

Yet, on 22 January 2016, an entirely new narrative began, leading to one of the strongest recoveries

seen in risk assets over the past 80 years. The US Equity market managed to recoup a 10% loss from

the start of the year to the middle of January 2016, ending the first quarter marginally better. Most assets followed suit and ended the quarter up strongly.

Global central banks continued to provide support to the market with the European Central Bank

(“ECB”) increasing its direct market action by increasing its bond buying program in February. The Bank of Japan (“BoJ”) continued its buying spree and has managed to persuade the Japanese

Government Pension Fund to provide even more market support through both bond and equity index purchases. After the US Federal Reserve Bank (“Fed”) raised interest rates in December 2015,

communication turned significantly more dovish during the first quarter and ended with Fed

Chairperson, Janet Yellen, indicating a less aggressive interest rate hiking path than the market expected.

On the emerging market front both Chinese and Indian central banks have continued to provide

support to their economies either by direct foreign exchange transaction (specifically China), or by lowering interest rates and bank lending requirements.

Domestically, the SARB Monetary Policy Committee continued to increase interest rates in line with

expectations to ward off possible rating agency downgrades. The local economy remained under

pressure which has reflected in the latest SA Business Confidence Index. The index came in at the lowest level since Q2 2010. Private sector credit extension demonstrated a small improvement but

remained well below the previous peak. SA assets did however perform extremely well in both USD and ZAR terms on the back of rand strength and the risk asset recovery.

Performance – what added and what detracted?

As mentioned earlier, Q1 has been a very volatile quarter for risk assets. The JSE All Share Index

returned nearly 3.9% for the quarter (on a Total Return basis) but remains below the high achieved on 4 November 2015. Resource stocks were by far the best performing sector returning 18.1%,

Industrials returned 7.6% and Financials returned 6.2%. The biggest laggards in the local market were the large cap rand hedge shares which underperformed on the back of ZAR strength.

Globally, most assets struggled in ZAR terms as the rand strengthened against the USD (+5.1%),

GBP (+7.4%) and the yen (+1.6%), but weakened slightly against the euro (-0.7%). Rand strength combined with low returns in hard currency terms resulted in most global risk assets generating

negative returns for Q1, which is in stark contrast to what has been happening over the past 6 to 12

months.

Global equities lost 4.8% as developed markets struggled. Global property staged a material comeback from the January lows but still ended the quarter down 0.7%. Global bonds did provide some relief

12

returning 1.3% on the back of the dovish outlook from the US Fed and accommodative actions from

the ECB and BoJ.

Overall the portfolios had a reasonably difficult quarter on the back of lacklustre global performance as a result of ZAR strength, while our preference for cyclical and attractively valued assets in SA added

value in SA Equity.

The portfolios managed to eke out positive returns but lagged the market. This came on the back of

strong outperformance during the latter parts of 2015. The Ampersand Momentum CPI+2% Fund of Funds (“CPI 2”) generated a return of 0.7%, the Ampersand Momentum CPI+4% Fund of Funds (“CPI

4”) generated 0.3% and the Ampersand Momentum CPI+6% Fund of Funds (“CPI 6”) generated 0.2%.

Source: MoneyMate 31 March 2016

If we go back to the latest high achieved on the market on 4 November 2015, the robust nature of

our investment approach is clearly visible. The CPI 2 generated a return of 2.3%, the CPI 4 was up

1.4% and the CPI 6 was up 0.8% versus the JSE All Share Index that was down -3.3% (on a Total Return basis), over this period.

13

Cumulative Fund Performance for the Period Ending 31 March 2016

Source: MoneyMate, Ampersand AM 31 March 2016 (A Class, ZAR) (CPI Benchmark as at 28 February 2016)

Over the longer term the portfolios have performed in line with expectations although only the CPI 2 managed to outperform its CPI Plus Objective while the CPI 4 and CPI 6 marginally underperformed

as at 31 March 2016. Looking at the performance over the relevant time frames, the CPI 2 managed to outperform 12/12 months versus its SA CPI Plus 2% p.a. objective over all 24 month rolling periods.

The CPI 4 managed to outperform 10/12 months versus its CPI Plus 4% p.a. objective over all 36 month rolling periods, while the CPI 6 also managed to outperform 10/12 months versus its CPI Plus

6% p.a. objective over all 48 month rolling periods.

Position going forward

We remain cautiously optimistic and for now we feel that conditions continue to favour risk assets. In our local portfolios we continue to prefer growth-orientated assets, especially SA listed property and

offshore equities. After a 7year bull market, downside risks to performance are on the rise, especially in more defensive stocks which have performed exceptionally well over this period.

The portfolios remain well diversified and we have included low-risk exposure through enhanced cash instruments, both locally and offshore. Although we have seen the first move on monetary tightening

in the US, we are of the opinion that interest rates will remain on a lower trajectory than the US Fed has indicated. We also see actions from other central banks as positive for the global risk environment

although these actions could have long term unintended consequences as central bank actions continue in uncharted waters.

We have to caution that the current environment could result in a slight increase in volatility over the

short term, as we expect market volatility and yields to remain unpredictable and prone to surprise.

We believe it is in our clients’ best interests to remain focused on the long term and seek to invest in

assets that have the highest probability of achieving positive real returns. Our philosophy and investment approach has proven to be robust and effective in these challenging times and we believe

our investors will continue to reap the benefits going forward.

14

Disclosures

Performance is calculated for a portfolio/portfolio class. Individual investor returns may differ as a result of fees, actual date(s)

of investment, date(s) of reinvestment of income and withholding tax. Annualised returns, also known as Compound Annualised

Growth Rates (CAGR), are calculated from cumulative returns; they provide an indication of the average annual return achieved

from an investment that was held for the stated time period. Actual annual figures are available from the Manager on request.

Performance figures quoted are from MoneyMate, as at 31/03/2016, for a lump sum investment, using NAV-NAV prices with

income distributions reinvested on the ex-dividend date. CPI/Inflation figures are lagged by one month.

Collective investment schemes in securities are generally medium- to long-term investments. The value of participatory

interests or the investment may go down as well as up. Past performance is not necessarily a guide to future performance. The

manager does not provide any guarantee, either with respect to the capital or the return of a portfolio. For certain portfolios

the manager has the right to close these portfolios to new investors to manage them more efficiently, in accordance with their

mandates. Collective investment schemes are traded at ruling prices and can engage in borrowing and scrip lending. The

collective investment scheme may borrow up to 10% of the market value of the portfolio to bridge insufficient liquidity.

Different classes of participatory interests apply to these portfolios and are subject to different fees and charges. A schedule of

fees, charges and maximum commissions is available on request from the manager, or is available on the website

(www.momentum.co.za/assetmanagement). Forward pricing is used. The portfolio valuation time is 08h00 for fund of funds,

and 15h00 for all other portfolios. The transaction cut-off time for non-fund of funds is 14h00 on the pricing date, and for fund

of funds it is 14h00 on the business day prior to the pricing date. MMI Holdings Limited is a full member of the Association for

Savings and Investment SA.

Associates of the manager may be invested within certain portfolios and the details thereof are available from the manager.

Foreign securities within portfolios may have additional material risks, depending on the specific risks affecting that country,

such as: potential constraints on liquidity and the repatriation of funds; macroeconomic risks; political risks; foreign exchange

risks; tax risks; settlement risks; and potential limitations on the availability of market information. Fluctuations or movements

in exchange rates may cause the value of underlying international investments to go up or down. Investors are reminded that

an investment in a currency other than their own may expose them to a foreign exchange risk.

A fund of funds is a portfolio that invests in portfolios of collective investment schemes that levy their own charges, which could

result in a higher fee structure for the fund of funds. The manager retains full legal responsibility for the third-party-named

portfolio.

The investment manager of the funds pertaining to this application form is Ampersand Asset Management (Pty) Ltd, registration

number 2007/006571/07, and is an authorised financial services provider, FSP license number 33676. The above investment

manager is an authorised financial services provider under the Financial Advisory and Intermediary Services Act (No. 37 of

2002), to act in the capacity as investment manager. The address is 1 Tuscany Office Park 6 Coombe Place Rivonia

Johannesburg. This information is not advice, as defined in the Financial Advisory and Intermediary Services Act (No. 37 of

2002). Please be advised that there may be representatives acting under supervision.

___________________________________________

Ampersand Asset Management | Ampersand Momentum CPI FoF | Class A | Market Review as at 31 March 2016 | Published: April 2016

15

Financial Planning

James Vickers Ian Peters +27 11 803 8105 +27 11 803 8158

[email protected] [email protected]

Graeme Holt Jacqui Nolan +27 11 803 7642 +27 11 803 7782

[email protected] [email protected]

Marinda Combrink Tracy van der Merwe +27 11 803 7399 +27 11 803 7393

[email protected] [email protected]

Yolandi Perold Tinks Hichert +27 11 803 6519 +27 11 803 7689

[email protected] [email protected]

Roxy Geel Notizi Dike +27 11 234 2902 +27 11 803 7399

[email protected] [email protected]

Employee Benefits

Chris Ellis Guy Peters +27 11 803 3663 +27 11 803 7379

[email protected] [email protected]

Mark Lumley Peliswa Mzondo +27 11 803 7379 +27 11 234 6682

[email protected] [email protected]

Tselane Mafatle +27 10 595 1340

16

Tom Barlow Tarryn Keogh +27 11 803 6597 +27 11 803 6597

[email protected] [email protected]

Tiaan Fourie Monique Boshoff +27 11 803 6597 +27 11 803 6597

17