it-update revised on 206c 2016 - nirc@icai (revised) on 206c (2016).pdf · persons who take...

TRANSCRIPT

Revised update on provisions relating to

Tax Collection at Source u/s 206C of Income Tax Act, 1961

with special reference to amendments made by the Finance Act, 2012

and the Finance Act, 2016

Evolution and history of TCS

1. Before we dwell upon the contemporary TCS, it is imperative to look into the “evolution

and history of TCS.” It will help to understand and appreciate the spirit of the legislative intent in amending the provisions relating to TCS vide the Finance Act, 2016.

Chapter XVII-BB was inserted in the Income Tax Act, 1961 {hereinafter referred to

the Act} by the Finance Act, 1988 w.e.f. 1.6.1988. Originally only Section 206C {Profits and gains from the business of trading in

alcoholic liquor, forest produce, scrap etc.} was incorporated and introduced in the aforesaid Chapter by the Finance Act, 1988 w.e.f. 1.6.1988, which has been amended from time to time in accordance with the policies of the Government.

Presently section 206C runs from section (1) to Section (11), which provides a

complete code in relation to “collection of tax at source”. Thereafter section 206CA and 206CB were inserted. Section 206CA {Tax-collection account number} was inserted by the Finance Act,

2002 w.e.f 1.6.2002, requiring every person collecting tax in accordance with the provisions of section 206C to apply for allotment of “tax collection account number”.

o However, vide proviso to sub-section (2) the provisions of section 206CA were made non-applicable w.e.f. 1.10.2004 by the Finance (No.2) Act, 2004.

o Simultaneously, Section 203A of the Act was amended by substitution vide

the Finance (No. 2) Act, 2004 w.e.f. 1.10.2004, and under sub-section (1) thereof, mechanism of common “tax-deduction and collection-account number” was provided.

Section 206CB {Processing of statement of tax collected at source} was inserted by

the Finance Act, 2015 w.e.f. 1.6.2015 providing the mechanism of processing of “statement of TCS”. Cont…..2

: 2 : 2. CBDT Circular No. 525 dated 24.11.1988 on insertion of section 206C

In the budget speech on the union Budget and Finance Bill of 1988, the then Minister

of Finance Sh. N. D. Tiwari, vide para 101 of his speech, had quoted as follows:

“as an anti-evasion measure, I propose to provide for assessment of income of persons engaged in certain trades like liquor and forest contracts, at a reasonably fixed percentage of the amount payable by them while purchasing the goods. The tax shall be collected at source.

Keeping in view the “memorandum explaining the aforesaid proposals, CBDT had

issued Circular No. 525 dated 24.11.1988 explaining the legislative intent and objective in introducing the concept and provision of “tax collection at source” (TCS), the relevant part of which as follows;

“Instructions regarding deduction of tax at source on profits and gains from the business of trading in alcoholic liquor, forest produce, etc.

i. Considerable difficulty has been felt in the past in assessing income of

persons who take contracts for sale of liquor, forest produce, etc. It has been the Department’s experience that for taking such contracts, firms or associations of persons are specifically constituted and very often no trace is left of them or their members after the contract has been executed.

ii. Persons have also been found to have taken contracts in ‘benami’ names by floating undertakings or associations for short periods. Since tax is payable in the assessment years on the incomes of the previous years, the time by which the incomes from such sources become assessable, such persons become untraceable.

iii. Moreover, at the time of assessment years in these cases, either the accounts are not available or they are mostly incorrect or incomplete.

iv. Thus, even if assessments could be made on ex parte basis, it becomes almost impossible to collect the tax found due, either because it becomes difficult to establish the identity of the persons and trace them or because of the fact the persons in whose names contracts were taken are men of no means.

v. With a view to combating large scale tax evasion by persons deriving incomes from such business, the Finance Act, 1988 has inserted a new section 44AC {since omitted by the Finance Act, 1992 w.e.f. 1.4.1993} to provide for determination of income in such cases.

vi. Further, with a view to facilitating collection of taxes from such assessees, the Finance Act, 1988 has inserted a new section 206C to provide for collection of such tax at source.”

Cont…..3

: 3 : 3. Insertion of sub-section (1C) by the Finance (No. 2) Act 2004 w.e.f. 1.10.2004

Finance (No. 2) Act, 2004 had inserted sub-section (1C) w.e.f. 1.10.2004 to extend

the provisions of collection of tax at source in respect of parking and toll auctions and mining or quarrying leases with an objective to widen the tax base.

Therefore, it was provided that every person who grants a lease or a licence or enters into a contract or otherwise transfers any right or interest in any parking lot or toll plaza or a mine or a quarry to another person, other than a public sector company, for the use of such parking lot or toll plaza or mine or quarry for the purposes of business shall collect tax from the licensee or lessee of any such licence, contract or lease of the specified nature at the rate of two per cent, at the time of debiting of the amount payable by the licencee or lessee to his account or at the time of receipt of such amount from him in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier.

4. Legislative intent and thrust of the Government

From the above it is evident that the legislative intent and the trust of the Government

at that point of time was - o to combat large scale tax evasion in the trade of aforesaid goods by way of

tenders and contracts.

o to charge tax in respect of income of such business on presumption and special case at fixed percentage on the value of purchases.

o to collect the tax from the buyer at the time of purchase itself.

o to widen the tax base.

5. Business vs. Profession

The marginal head of section 206C is “Profits and gains from the business of

trading in alcoholic liquor, forest produce, scrap etc”. The title of the aforesaid circular also comprise word “business”. It is so because this section was introduced with the intention to compute income from the business of aforesaid commodities/goods and to collect tax at source in relation to the amounts received from the buyer of such commodities/goods.

Now, vide sub-section (1D) any amount received in cash for as consideration for sale

of service exceeding Rs. 2 lakh has also been roped in the ambit of the provisions of TCS. It means that w.e.f. 1.6.2016 the provisions of section 206C, 206CA and 206CB shall apply to TCS on such services. Cont…..4

: 4 : Word “Service” is neither defined in section 206C nor under the Act. “service”

includes - o services rendered as business o services rendered as profession

In sub-section (1D), services in the nature of profession have not been excluded.

On the contrary, the definition of “seller” provided in clause (c) of the Explanation to section 206C clarifies, wherein for the purposes of sub-section (1D) individual and HUF who are liable for audit under clause (b) of section 44AB have been included in the definition of “seller”. Clause (b) of section 44AB applies to “profession”, with threshold of Rs. 25 lakh up to AY 2016-17 and Rs. 50 lakh from AY 2017-18. In the definition of “seller” profession has not been excluded for other entities viz. company, firm or co-operative societies

Only because the marginal head of section 206C does not include the word

“profession”, it does not mean that the amended sub-section (1D) is not applicable to “profession” or the “professional services”.

In this regards it may be pertinent to mention that it is the settled law that -

o Headings’, o `Marginal Notes’ and o `Marginal Headings’

can be referred to while interpreting the particular provision of the act. However, Headings etc. do not decide the construction of the section, but Headings etc. are indicative of the meaning and purpose of the section

In the aforesaid “Heading” word “business” is used in relation to “profits and gains from trading of alcoholic liquor, forest produce, scrap, etc., which was introduced w.e.f. 1.6.1988, when it was intended to be used strictly for the business of aforesaid commodities.

Now, in 2016, sub-section (1D) has been made applicable to services also, which shall include “services in the nature of business” as well as “services in the nature of profession”, the “ Heading” has not been amended. Nevertheless, sub-section (1D) shall also apply to the services in the nature of profession”.

Relevance of Finance Minister’s Speech in interpreting tax laws

6. Normally the speeches made in the Parliament by the Finance Minister are not admissible

for the purposes of interpretation of a provision on statute.

7. However as held by courts, such speech can be relied upon to understand the purpose of the provision sought to be amended or brought on statute and in that background to interpret that particular provision. Cont…..5

: 5 : 8. In this regards in the case of K.P. Varghese vs. ITO (1981) 131 ITR 597, 609 (SC), the

Apex Court held that -

“The Finance Minster’s speech can be relied upon to throw light on the object and purpose of the particular provisions introduced by the Finance Bill.”

“Now, it is true that the speeches made by the members of the Legislature on the floor of the House when a Bill for enacting a statutory provision is being debated are inadmissible for the purpose of interpreting the statutory provision but the speech made by the mover of the Bill explaining the reason for the introduction of the Bill can certainly be referred to for the purpose of ascertaining- the mischief sought to be remedied by the legislation and the object and the purpose for which the legislation was enacted. This is in accord with the recent trend in juristic though not only in Western countries but also in India that interpretation of a statute being an exercise in the ascertainment of meaning, everything which is logically relevant should be admissible. In fact there are at least three decisions of this court, - the one in Loka Shikshana Trust vs. CIT (1975) 101 ITR 234 (SC) the other in Indian Chamber of Commerce vs. CIT (1975) 101 ITR 796 (SC) the third in Addl. CIT vs. Surat Art Silk Cloth Manufactures Association

(1980) 121 ITR 1 (SC) where the speech made by the Finance Minister while introducing the exclusionary clause in section 2, clause (15), of the Act was relied upon by the court for the purpose of ascertaining what was the reason for introducing that clause”.

Relevance of the Statement of Objects and Reasons

9. Courts have held that if the language of the statute is unambiguous, it is not required to consider the history of Parliament in making or amending a particular statutory provision.

10. However, the Statement of Objects and Reasons has been referred to by the Courts

where the words used in statute do not have clarity.

11. In this regard the case of S.C. Prashar v. Vasantsen Dwarkadas 49 ITR 1 (SC) is relevant - Cont…..6

: 6 : “Per Hidayatullah and Raghubar Dayal, JJ. : Where the language of an enactment is clear there is hardly any need to go to the marginal note or the history of the law before the amendment.

Per Das, J. : It is indeed true that the Statement of Objects and Reasons for introducing a particular piece of legislation cannot be used for interpreting the legislation if the words used therein are clear enough. But the Statement of Objects and Reasons can be referred to for the purpose of ascertaining the circumstances which led to the legislation in order to find out what was the mischief which the legislation aimed at.

Per Kapur, J. : In construing an enactment and determining its true scope it is permissible to have regard to all such factors as can legitimately be taken into account to ascertain the intention of the Legislature such as -

i. the history of the Act, ii. the reason which led to its being passed,

iii. the mischief which had to be cured iv. as well as the other provisions of the statute.”

12. Article 141 of the Constitution of India provides that “the law declared by the Supreme

Court shall be binding on all courts within the territory of India.

From the speech of Hon’ble Minister of Finance Sh. Pranab Mukharjee (as he was then)

on Union Budget, 2012

13. Section 206C was inserted in the statute book under Chapter XVII-BB by the Finance Act, 1988 w.e.f. 1.6.1988, however, in the Union Budget of 2012 the then Minister of Finance Sh. Pranab Mukarjee proposed amendment in section 206C to achieve different and specific objectives, which are spelled in his budget speech, as follows . 155. I propose a series of measures to deter generation and use of unaccounted money.

To this end, I propose –

(i) …………….. (ii) …………….. (iii) Tax collection at source on purchase in cash of bullion or jewellery in excess of

Rs. 2 lakh.

Memorandum explaining the proposed amendment vide Finance Act, 2012 {Tax Collection at Source (TCS) on cash sale of bullion and jewellery}

This amendment will take effect from 1st July, 2012.

Cont…..7

: 7 : 14. The memorandum explaining the amendment is as follows:

Under the existing provisions of the Income-tax Act, tax is required to be collected at source by the seller at the specified rate on certain goods like alcoholic liquor, tendu leaves, scrap etc. at the time of sale.

In order to -

reduce the quantum of cash transaction in bullion and jewellery sector and for curbing the flow of unaccounted money in the trading system of

bullion and jewellery,

it is proposed to provide that the seller of bullion and jewellery shall collect tax at the rate of 1% of sale consideration from every buyer of bullion and jewellery if sale consideration exceeds two lakh rupees and the sale is in cash. This would be irrespective of the fact whether buyer is a manufacturer, trader or purchase is for personal use.

CBDT Circular No. 3/2012, dated 12.6.2012 {Tax Collection at Source (TCS) on cash sale of bullion and jewellery}

This amendment will take effect from 1st July, 2012.

15. CBDT clarified the said amendment in circular No. 3/2012 dated 12.6.2012:

The Finance Bill, 2012, proposed to provide that the seller of bullion or jewellery shall collect tax at source (TCS) at the rate of 1 % of sale consideration from every buyer of bullion and jewellery in cash if the sale consideration exceeds Rs. 2 lakh. In order to reduce the compliance burden, the threshold limit for TCS on cash purchase of jewellery has been increased to Rs. 5 lakh from the proposed Rs. 2 lakh. The threshold limit for TCS on cash purchase of bullion is retained at Rs. 2 lakh. Further, it has also been provided that bullion shall not include any coin or any other article weighing 10 grams or less.

Section 206C(1D) as amended by Finance Act, 2012 {w.e.f 1.7.2012}

16. Finally, the aforesaid law was brought on the statute book as follows:

(1D) Every person, being a seller, who receives any amount in cash as consideration for sale of bullion (excluding any coin or any article weighing ten grams of less) or jewellery, shall at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration as income-tax, if such consideration,— (i) for bullion, exceeds two hundred thousand rupees; or (ii) for jewellery, exceeds two hundred thousand rupees. Cont…..8

: 8 : Section 206C(1D) as amended by Finance Act, 2013

{w.e.f 1.6.2013}

17. However, w.e.f. 1.6.2013, the Finance Act, 2013 amended the sub-section (1D) of section 206C as follows:

(1D) Every person, being a seller, who receives any amount in cash as consideration for sale of bullion {*omission} or jewellery, shall at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration as income-tax, if such consideration,— (i) for bullion, exceeds two hundred thousand rupees; or (ii) for jewellery, exceeds five hundred thousand rupees. {* omitted - excluding any coin or any article weighing ten grams of less}

From the speech of

Hon’ble Minister of Finance Sh. Arun Jaitly on Union Budget, 2016

18. Now, w.e.f. 1.6.2016, the Finance Act, 2016 has again amended to enlarge the scope of

TCS, the objectives of which are spelled out as follows: 149. I also propose to collect tax at source at the rate of 1% on purchase of luxury cars exceeding value of Rs. ten lakh and purchase of goods and services in cash exceeding Rs. two lakh. For compliant tax payers with resources, -

this levy not only advances collection of tax when the expenditure is

incurred,

but it provides data to the tax authorities to identify the persons who incur such expenditure, but may be missing from the tax base.

Farmers and notified class of persons will have an option of giving a form by which TCS will not be charged.

Comments

Through these measures the Government intends to advance the collection

and also to keep trail of non files involved in high value the transactions.

Memorandum explaining the proposed amendment vide Finance Bill, 2016 C. Widening of Tax Base and Anti Abuse Measures

{Tax Collection at Source (TCS) on sale of vehicles; goods or services}

Cont…..9

: 9 : 19. The memorandum explaining the amendment is as follows:

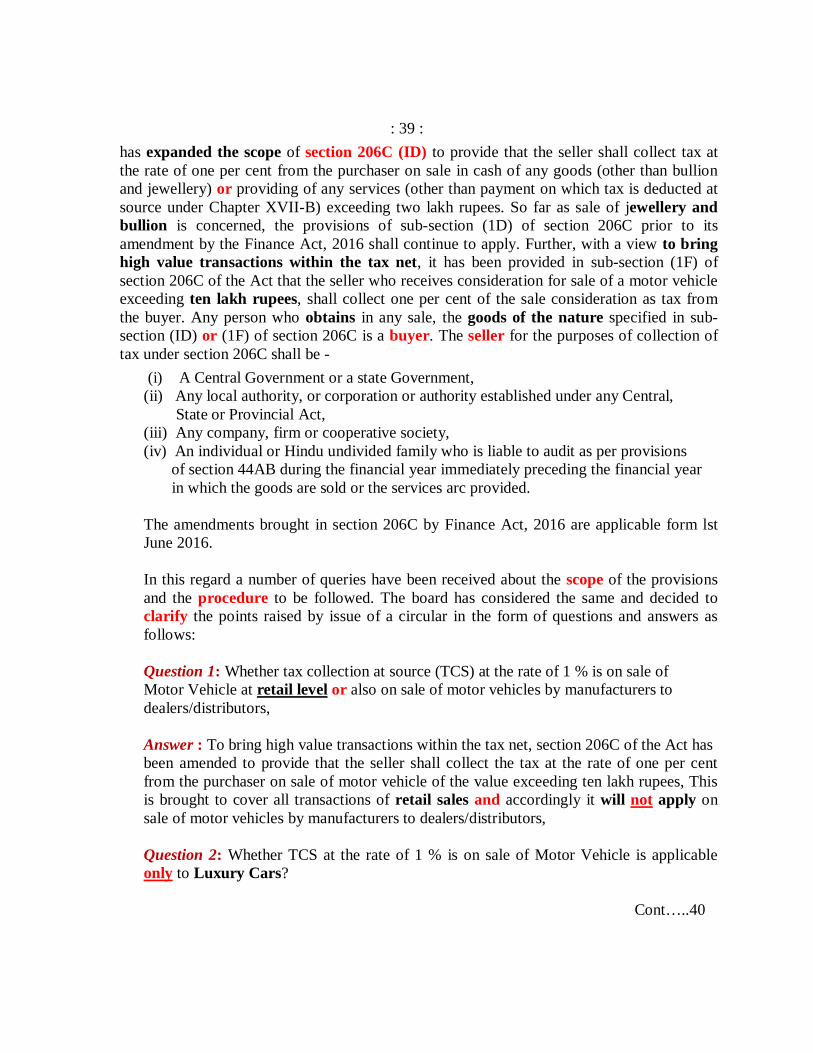

The existing provision of section 206C of the Act, inter alia, provides that the seller shall collect tax at source at specified rate from the buyer at the time of sale of specified items such as – alcoholic liquor for human consumption, tendu leaves, scrap, mineral being coal or lignite or iron ore, bullion etc. in cash exceeding two lakh rupees. In order to reduce the quantum of cash transaction in sale of any goods and services and for curbing the flow of unaccounted money in the trading system and to bring high value transactions within the tax net, it is proposed to amend the aforesaid section to provide that - the seller shall collect the tax at the rate of one per cent from the purchaser on sale of motor vehicle of the value exceeding ten lakh rupees and sale in cash of any goods (other than bullion and jewellery), or providing of any services (other than payments on which tax is deducted at source

under Chapter XVII-B) exceeding two lakh rupees.

It is also proposed to provide that the sub-section (1D) relating to TCS in relation to sale of any goods (other than bullion and jewellery) or services shall not apply to certain class of buyers who fulfill such conditions as may be prescribed.

This amendment will take effect from 1st June, 2016.

Section 206C(1D) as amended by Finance Act, 2016 Section 206C(1E) and (IF) inserted by the Finance Act, 2016

{w.e.f 1.6.2016}

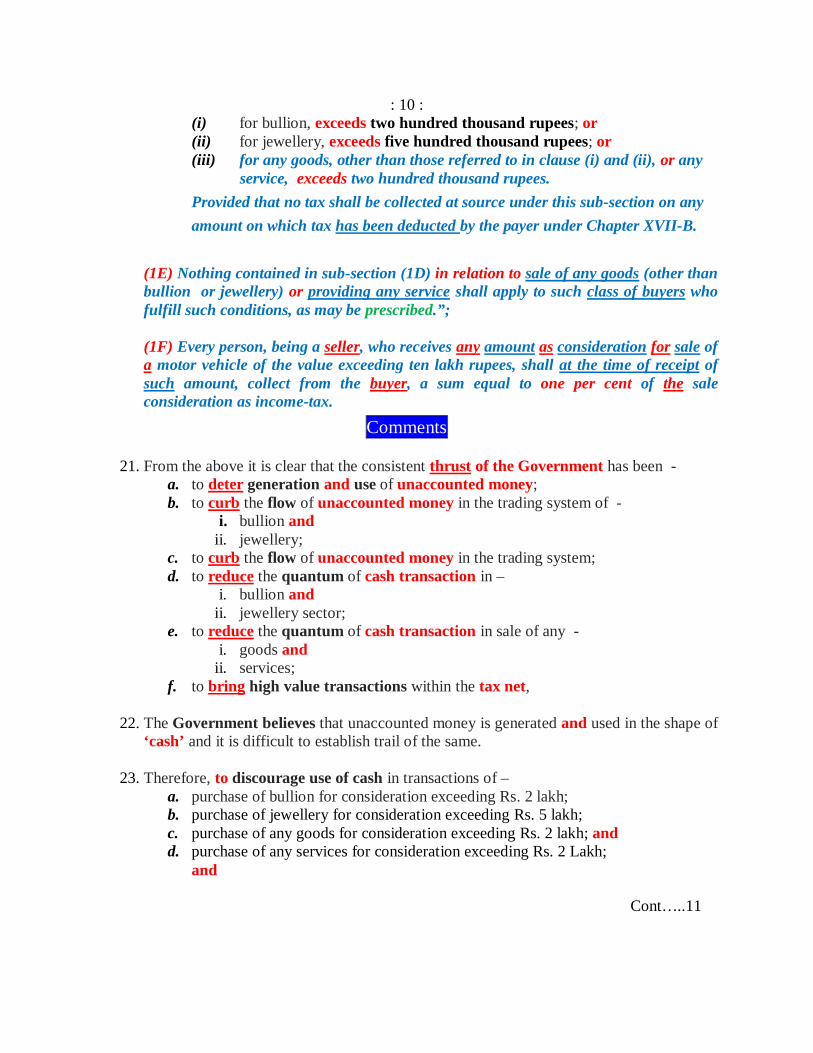

20. Thus, w.e.f. 1.6.2016, the Finance Act, 2016 has amended the sub-section (1D) of section 206C as follows and has inserted two new sub-section (1E) and (1F) as follows, besides other amendments in section 206C:

(1D) Every person, being a seller, who receives any amount in cash as consideration for sale of bullion or jewellery or any other goods (other than bullion or jewellery) or providing any service, shall, at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration as income-tax, if such consideration,— Cont…..10

: 10 : (i) for bullion, exceeds two hundred thousand rupees; or (ii) for jewellery, exceeds five hundred thousand rupees; or (iii) for any goods, other than those referred to in clause (i) and (ii), or any service, exceeds two hundred thousand rupees.

Provided that no tax shall be collected at source under this sub-section on any amount on which tax has been deducted by the payer under Chapter XVII-B.

(1E) Nothing contained in sub-section (1D) in relation to sale of any goods (other than bullion or jewellery) or providing any service shall apply to such class of buyers who fulfill such conditions, as may be prescribed.”;

(1F) Every person, being a seller, who receives any amount as consideration for sale of a motor vehicle of the value exceeding ten lakh rupees, shall at the time of receipt of such amount, collect from the buyer, a sum equal to one per cent of the sale consideration as income-tax.

Comments

21. From the above it is clear that the consistent thrust of the Government has been - a. to deter generation and use of unaccounted money; b. to curb the flow of unaccounted money in the trading system of -

i. bullion and ii. jewellery;

c. to curb the flow of unaccounted money in the trading system; d. to reduce the quantum of cash transaction in –

i. bullion and ii. jewellery sector;

e. to reduce the quantum of cash transaction in sale of any - i. goods and

ii. services; f. to bring high value transactions within the tax net,

22. The Government believes that unaccounted money is generated and used in the shape of

‘cash’ and it is difficult to establish trail of the same.

23. Therefore, to discourage use of cash in transactions of – a. purchase of bullion for consideration exceeding Rs. 2 lakh; b. purchase of jewellery for consideration exceeding Rs. 5 lakh; c. purchase of any goods for consideration exceeding Rs. 2 lakh; and d. purchase of any services for consideration exceeding Rs. 2 Lakh;

and

Cont…..11

: 11 : e. to mobalize additional resources from effluent class of the society, e.g. TCS on

purchase and sale of vehicle of value exceeding Rs. 10 Lakh; and f. to gather information regarding high value purchases of certain goods and

services, including luxury motor vehicle so that the same is matched with their sources of income

section 206C has been amended in the aforesaid manner.

24. It means that the Government wants to have details of aforesaid high value transactions and the transactions in which cash is involved. Through this measure the Government shall not only mop up additional revenue by ‘TCS’ but shall also be able to gather information and details of the buyers who are involved in such transactions, to verify whether they are using accounted money or unaccounted money for such transactions.

25. Section 206C under Chapter XVII-BB of the Income Tax Act, 1961 provides such mechanism.

26. Section 206C which was introduced by the Finance Act, 1988 w.e.f 1.6.1988 has been amended from time to time in accordance with the policies of the Government. It runs from section (1) to Section (11), which provides a complete code.

27. Text of section 206C {as amended by the Finance Act, 2016 w.e.f 1.6.2016} is as follows:

Chapter XVII-BB - Collection at source Section : 206C

Profits and gains from the business of trading in alcoholic liquor, forest produce, scrap, etc. 206C. {As amended by the Finance Act, 2016 w.e.f 1.6.2016} TCS in relation to goods specified in the ‘Table’ in sub-section (1) {the entries are seven in No(s) and goods are nine in No(s)} (1) Every person, being a seller shall, at the time of debiting of the amount payable by the buyer to the account of the buyer or at the time of receipt of such amount from the said buyer in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, collect from the buyer of any goods of the nature specified in column (2) of the Table below, a sum equal to the percentage, specified in the corresponding entry in column (3) of the said Table, of such amount as income-tax:

Cont…..12

: 12 :

Table .Sl. No.

Nature of goods Percentage

(i) Alcoholic Liquor for human consumption One per cent (ii) Tendu leaves Five per cent (iii) Timber obtained under a forest lease Two and one-half per cent (iv) Timber obtained by any mode other than under a forest lease Two and one-half per cent (v) Any other forest produce not being timber or tendu leaves Two and one-half per cent (vi) Scrap One per cent (vii) Minerals, being coal or lignite or iron ore One per cent

Provided that every person, being a seller shall at the time, during the period beginning on the 1st day of June, 2003 and ending on the day immediately preceding the date on which the Taxation Laws (Amendment) Act, 2003 comes into force {8.9.2003}, of debiting of the amount payable by the buyer to the account of the buyer or of receipt of such amount from the said buyer in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, collect from the buyer of any goods of the nature specified in column (2) of the Table as it stood immediately before the 1st day of June, 2003, a sum equal to the percentage, specified in the corresponding entry in column (3) of the said Table, of such amount as income-tax in accordance with the provisions of this section as they stood immediately before the 1st day of June, 2003. Declaration for ‘nil’ TCS {Rule 37C, Form No. 27C} (1A) Notwithstanding anything contained in sub-section (1), no collection of tax shall be made in the case of a buyer, who is resident in India, if such buyer furnishes to the person responsible for collecting tax, a declaration in writing in duplicate in the prescribed form and verified in the prescribed manner to the effect that the goods referred to in column (2) of the aforesaid Table are to be utilised for the purposes of manufacturing, processing or producing articles or things or for the purposes of generation of power and not for trading purposes. (1B) The person responsible for collecting tax under this section shall deliver or cause to be delivered to the Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner one copy of the declaration referred to in sub-section (1A) on or before the seventh day of the month next following the month in which the declaration is furnished to him.

Cont…..13

: 13 : Comment A declaration may be filed by a buyer, who is resident in India. Such declaration is to be filed in under rule 37C in Form No. 27C. Such declaration is to be filed for claiming ‘nil’ TCS under sub-section (1). Such declaration can be filed only in respect of goods mentioned in the ‘table’

provided in sub-section (1), which are seven in serial No(s) and nine in No(s). Such declaration cannot be filed if the buyer obtains such goods for trading

purposes. Such declaration can be filed if the buyer obtains such goods either of the following

purposes: o manufacturing of articles of things, or o processing of articles or things, or o producing articles of things, or o generation of power.

It means that such declaration cannot be filed for the purposes of – o sub-section (1C) o sub-section (1D) o sub-section (1F)

TCS in relation to parking lot, toll plaza, mine and quarry {the entries are three in No(s) and facilities are four in No(s)} (1C) Every person, who grants a lease or a licence or enters into a contract or otherwise transfers any right or interest either in whole or in part in any parking lot or toll plaza or mine or quarry, to another person, other than a public sector company (hereafter in this section referred to as "licensee or lessee") for the use of such parking lot or toll plaza or mine or quarry for the purpose of business shall, at the time of debiting of the amount payable by the licensee or lessee to the account of the licensee or lessee or at the time of receipt of such amount from the licensee or lessee in cash or by the issue of a cheque or draft or by any other mode, whichever is earlier, collect from the licensee or lessee of any such licence, contract or lease of the nature specified in column (2) of the Table below, a sum equal to the percentage, specified in the corresponding entry in column (3) of the said Table, of such amount as income-tax:

Table Sl. No. Nature of goods Percentage (i) Parking lot Two per cent (ii) Toll Plaza Two per cent (iii) Mining and quarrying Two per cent

Cont…..14

: 14 :

Explanation 1.— For the purposes of this sub-section, "mining and quarrying" shall not include mining and quarrying of mineral oil. Explanation 2.— For the purposes of Explanation 1, "mineral oil" includes petroleum and natural gas. TCS on purchase & sale of specified goods or services of consideration exceeding Rs. 2,00,000/- if any part of such consideration is paid in cash {A move to discourage use of cash to deter generation and use of unaccounted money} (1D) Every person, being a seller, who receives any amount in cash as consideration for sale of bullion or jewellery or any other goods (other than bullion or jewellery) or providing any service, shall, at the time of receipt of such amount in cash, collect from the buyer, a sum equal to one per cent of sale consideration as income-tax, if such consideration,—

(i) for bullion, exceeds two hundred thousand rupees; or (ii) for jewellery, exceeds five hundred thousand rupees; or (iii) for any goods, other than those referred to in clause (i) and (ii), or any service,

exceeds two hundred thousand rupees. Provided that no tax shall be collected at source under this sub-section on any amount on which tax has been deducted by the payer under Chapter XVIIB.

Enabling CBDT to make rules for granting exemption for sub-section (1D) {A move to provide relief from TCS to specified class of buyers} (1E) Nothing contained in sub-section (1D) in relation to sale of any goods (other than bullion or jewellery) or providing any service shall apply to such class of buyers who fulfill such conditions, as may be prescribed.; TCS on Motor Vehicles of value exceeding Rs. 10,00,000/- {A move to mobilize the resources and advancing the tax collection and collecting data} (1F) Every person, being a seller, who receives any amount as consideration for sale of a motor vehicle of the value exceeding ten lakh rupees, shall at the time of receipt of such amount, collect from the buyer, a sum equal to one per cent of the sale consideration as income-tax.

Cont…..15

: 15 : Mode of recovery (2) The power to recover tax by collection under sub-section (1) or sub-section (1C) or sub-section (1D) shall be without prejudice to any other mode of recovery.

28. It may be noted that sub-section (1F) is missing in the aforesaid sub-section (2), which relates to powers to recover TCS without prejudice to any other mode of recovery. This omission seems to be unintentional, because TCS under sub-section (1F) also can be collected without prejudice to any other mode of recovery.

29. This omission needs to be addressed to competent authorities for necessary correction.

Payment of TCS and furnishing of quarterly statement of TCS {Rule 37CA(1) & (2) - Payment} {Rule 31AA(1), Form No. 27EQ - Statement} {Rule 31AA(3)(i)(c), Form No. 27A - Statement} (3) Any person collecting any amount under sub-section (1) or sub-section (1C) or sub-section (1D) shall pay within the prescribed time the amount so collected to the credit of the Central Government or as the Board directs: Provided that the person collecting tax on or after the 1st day of April, 2005 in accordance with the foregoing provisions of this section shall, after paying the tax collected to the credit of the Central Government within the prescribed time, prepare such statements for such period as may be prescribed and deliver or cause to be delivered to the prescribed income-tax authority, or the person authorised by such authority, such statement in such form and verified in such manner and setting forth such particulars and within such time as may be prescribed. Comment

30. It may be noted that sub-section (1F) is missing in the main provision of aforesaid sub-section (3), which relates to time of payment of TCS collected. This omission seems to be unintentional, because TCS once collected has to be paid.

31. This omission needs to be addressed to competent authorities for necessary correction. TCS quarterly statement where the collector is an office of the Government (3A) In case of an office of the Government, where the amount collected under sub-section (1) or sub-section (1C) or sub-section (1D) has been paid to the credit of the Central Government without the production of a challan, the Pay and Accounts Officer or the Treasury Officer or the Cheque Drawing and Disbursing Officer or any other person, by whatever name called, who is

Cont…..16

: 16 :

responsible for crediting such tax to the credit of the Central Government, shall deliver or cause to be delivered to the prescribed income-tax authority, or to the person authorised by such authority, a statement in such form, verified in such manner, setting forth such particulars and within such time as may be prescribed. TCS correction statement (3B) The person referred to in the proviso to sub-section (3) may also deliver to the prescribed authority under the said proviso, a correction statement for rectification of any mistake or to add, delete or update the information furnished in the statement delivered under the said proviso in such form and verified in such manner, as may be specified by the authority. Credit of TCS {Rule 37-I} (4) Any amount collected in accordance with the provisions of this section and paid to the credit of the Central Government shall be deemed to be a payment of tax on behalf of the person from whom the amount has been collected and credit shall be given to such person for the amount so collected in a particular assessment year in accordance with the rules as may be prescribed by the Board from time to time.

Issue of TCS certificate and statement in Form No. 26AS {Rule 37D, Form No. 27D - Certificate} {Rule 31AB, Form No. 26AS – Statement of Tax to be maintained by AO} (5) Every person collecting tax in accordance with the provisions of this section shall within such period as may be prescribed from the time of debit or receipt of the amount furnish to the buyer or licensee or lessee to whose account such amount is debited or from whom such payment is received, a certificate to the effect that tax has been collected, and specifying the sum so collected, the rate at which the tax has been collected and such other particulars as may be prescribed. Provided that the prescribed income-tax authority or the person authorised by such authority referred to in sub-section (3) shall, within the prescribed time after the end of each financial year beginning on or after the 1st day of April, 2008, prepare and deliver to the buyer referred to in sub-section (1) or, as the case may be, to the licensee or lessee referred to in sub-section (1C), a statement in the prescribed form specifying the amount of tax collected and such other particulars as may be prescribed.

Cont…..17

: 17 : Comment

32. It may be noted that sub-section (1D) and (1F) are missing in the proviso to aforesaid sub-section (5). These omissions seems to be unintentional, because like other amounts of TCS collected and paid. TCS collected under sub-sections (1D) and (1F) needs to be reported in Form No. 26AS .

33. This omission needs to be addressed to competent authorities for necessary correction. TCS return where tax collected before 1.4.2005 (5A) Every person collecting tax before the 1st day of April, 2005 in accordance with the provisions of this section shall prepare within the prescribed time after the end of each financial year, and deliver or cause to be delivered to the prescribed income-tax authority or such other authority or agency as may be prescribed such returns in such form and verified in such manner and setting forth such particulars and within such time as may be prescribed : Provided that the Board may, if it considers necessary or expedient so to do, frame a scheme for the purposes of filing such returns with such other authority or agency referred to in this sub-section. (5B) Without prejudice to the provisions of sub-section (5A), any person collecting tax, other than in a case where the seller is a company, the Central Government or a State Government, may at his option, deliver or cause to be delivered such return to the prescribed income-tax authority in accordance with such scheme as may be specified by the Board in this behalf, by notification in the Official Gazette, and subject to such conditions as may be specified therein, on or before the prescribed time after the end of each financial year, on a floppy, diskette, magnetic cartridge tape, CD-ROM or any other computer readable media (hereinafter referred to as the computer media) and in the manner as may be specified in that scheme: Provided that where the person collecting tax is a company or the Central Government or a State Government, such person shall, in accordance with the provisions of this section, deliver or cause to be delivered, within the prescribed time after the end of each financial year, such returns on computer media under the said scheme. (5C) Notwithstanding anything contained in any other law for the time being in force, a return filed on computer media shall be deemed to be a return for the purposes of sub-section (5A) and the rules made there under and shall be admissible in any proceedings made there-under, without further proof of production of the original, as evidence of any contents of the original or of any facts stated therein. (5D) Where the Assessing Officer considers that the return delivered or caused to be delivered under sub-section (5B) is defective, he may intimate the defect to the person collecting tax and

Cont…..18

: 18 : give him an opportunity of rectifying the defect within a period of fifteen days from the date of such intimation or within such further period which, on an application made in this behalf, the Assessing Officer may, in his discretion, allow; and if the defect is not rectified within the said period of fifteen days or, as the case may be, the further period so allowed, then, notwithstanding anything contained in any other provision of this Act, such return shall be treated as an invalid return and the provisions of this Act shall apply as if such person had failed to deliver the return. Person responsible shall remain liable towards the Central Government (6) Any person responsible for collecting the tax who fails to collect the tax in accordance with the provisions of this section, shall, notwithstanding such failure, be liable to pay the tax to the credit of the Central Government in accordance with the provisions of sub-section (3). Defaulting Collector shall be deemed to be in default {Rule 37, Form 27BA – Certificate by CA} (6A) If any person responsible for collecting tax in accordance with the provisions of this section does not collect the whole or any part of the tax or after collecting, fails to pay the tax as required by or under this Act, he shall, without prejudice to any other consequences which he may incur, be deemed to be an assessee in default in respect of the tax: Provided that any person, other than a person referred to in sub-section (1D), responsible for collecting tax in accordance with the provisions of this section, who fails to collect the whole or any part of the tax on the amount received from a buyer or licensee or lessee or on the amount debited to the account of the buyer or licensee or lessee shall not be deemed to be an assessee in default in respect of such tax if such buyer or licensee or lessee —

(i) has furnished his return of income under section 139; (ii) has taken into account such amount for computing income in such return of income; and (iii) has paid the tax due on the income declared by him in such return of income,

and the person furnishes a certificate to this effect from an accountant in such form as may be prescribed: Provided further that no penalty shall be charged under section 221 from such person unless the Assessing Officer is satisfied that the person has without good and sufficient reasons failed to collect and pay the tax.

Comment 34. The provisions of the first proviso to sub-section (6A) are similar to the provisions of the

proviso to section 201(1) {as inserted by the Finance Act, 212 w.e.f 1.7.2012}. Cont…..19

: 19 : 35. However, the provisions of the first proviso to sub-section (6A) are not applicable to any

person who is a collector (person responsible to collect tax) for the purposes of sub-section (1D).

Simple interest on TCS (7) Without prejudice to the provisions of sub-section (6), if the person responsible for collecting tax does not collect the tax or after collecting the tax fails to pay it as required under this section, he shall be liable to pay simple interest at the rate of one per cent per month or part thereof on the amount of such tax from the date on which such tax was collectible to the date on which the tax was actually paid and such interest shall be paid before furnishing the quarterly statement for each quarter in accordance with the provisions of sub-section (3): Provided that in case any person, other than a person referred to in sub-section (1D), responsible for collecting tax in accordance with the provisions of this section, fails to collect the whole or any part of the tax on the amount received from a buyer or licensee or lessee or on the amount debited to the account of the buyer or licensee or lessee but is not deemed to be an assessee in default under the first proviso of sub-section (6A), the interest shall be payable from the date on which such tax was collectible to the date of furnishing of return of income by such buyer or licensee or lessee. TCS collected but not paid has charge on all assets of the Collector (8) Where the tax has not been paid as aforesaid, after it is collected, the amount of the tax together with the amount of simple interest thereon referred to in sub-section (7) shall be a charge upon all the assets of the person responsible for collecting tax.

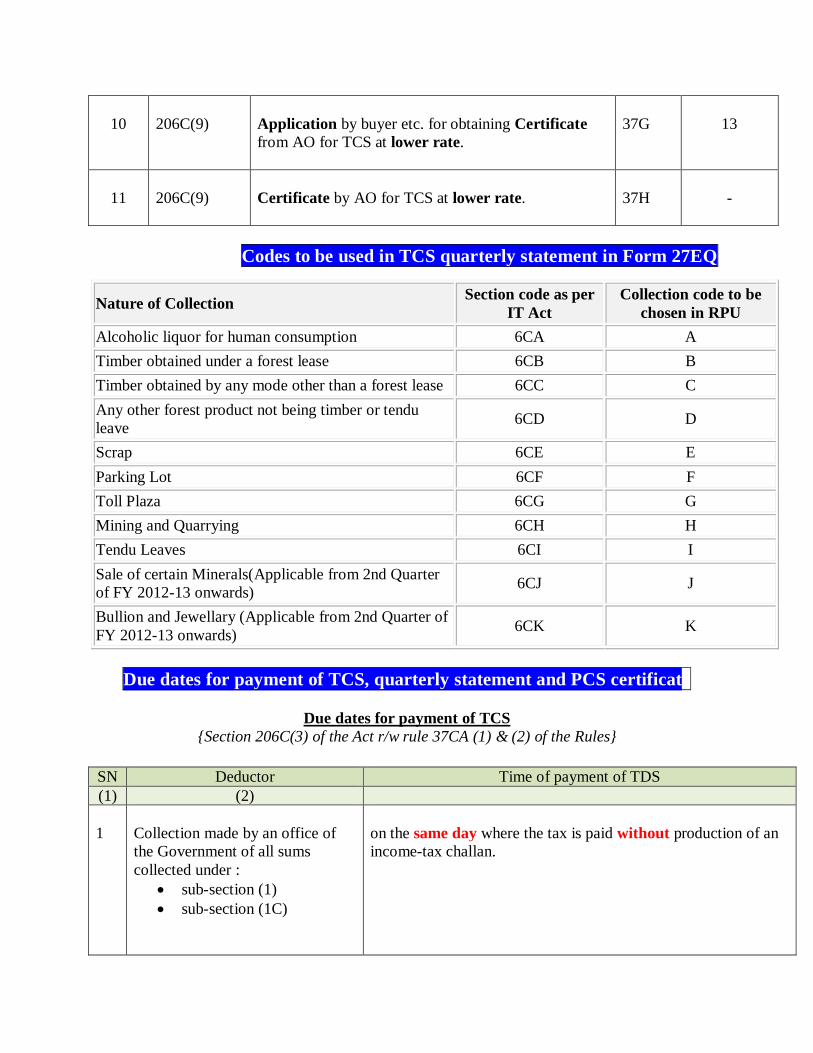

Certificate by AO for TCS at lower rate {Rule 37G, Form No. 13 - Application} {Rule 37H- Certificate} (9) Where the Assessing Officer is satisfied that the total income of the buyer or licensee or lessee justifies the collection of the tax at any lower rate than the relevant rate specified in sub-section (1) or sub-section (1C) or sub-section (1D), the Assessing Officer shall, on an application made by the buyer or licensee or lessee in this behalf, give to him a certificate for collection of tax at such lower rate than the relevant rate specified in sub-section (1) or sub-section (1C) or sub-section (1D). (10) Where a certificate under sub-section (9) is given, the person responsible for collecting the tax shall, until such certificate is cancelled by the Assessing Officer, collect the tax at the rates specified in such certificate.

Cont…..20

: 20 : (11) The Board may, having regard to the convenience of assessees and the interests of revenue, by notification in the Official Gazette, make rules specifying the cases in which, and the circumstances under which, an application may be made for the grant of a certificate under sub-section (9) and the conditions subject to which such certificate may be granted and providing for all other matters connected therewith.

Comment 36. An application for obtaining a certificate u/s 206C(9)/(10)/(11) can be filed and such

certificate can be obtained by a buyer covered under- a. sub-section (1) b. sub-section (1C) c. sub-section (1D)

37. Such application cannot be filed by a buyer covered under sub-section (1F) and no such

certificate be issued by AO for the buyer covered under sub-section (1F).

Explanation.— For the purposes of this section,— (a) "accountant" shall have the meaning assigned to it in the Explanation to sub-section (2)

of section 288;

(aa) "buyer" with respect to — (i) sub-section (1) means a person who obtains in any sale, by way of auction,

tender or any other mode, goods of the nature specified in the Table in sub-section (1) or the right to receive any such goods but does not include,— (A) a public sector company, the Central Government, a State Government,

and an embassy, a High Commission, legation, commission, consulate and the trade representation, of a foreign State and a club; or

(B) a buyer in the retail sale of such goods purchased by him for personal

consumption; (ii) sub-section (1D) or sub-section (1F) means a person who obtains in any sale,

goods of the nature specified in the said sub-section;

(ab) "jewellery" shall have the meaning assigned to it in the Explanation to sub-clause (ii) of clause (14) of section 2;

Cont…..21

: 21 :

(b) "scrap" means waste and scrap from the manufacture or mechanical working of materials which is definitely not usable as such because of breakage, cutting up, wear and other reasons;

(c) "seller" means the Central Government, a State Government or any local authority or

corporation or authority established by or under a Central, State or Provincial Act, or any company or firm or co-operative society and also includes an individual or a Hindu undivided family whose total sales, gross receipts or turnover from the business or profession carried on by him exceed the monetary limits specified under clause (a) or clause (b) of section 44AB during the financial year immediately preceding the financial year in which the goods of the nature specified in the Table in sub-section (1) or sub-section (1D) are sold or services referred to in sub-section (ID) are provided.

Comments with regards to Section 206C(1D) & (1F)

{Applicable w.e.f 1.6.2016} Seller

38. As per sub-section (1D) and (1F) tax is to be collected by the “seller”. It means that the “seller” is the person who is responsible for collecting tax at source.

39. As per clause (c) of the Explanation "seller" means - a. the Central Government, b. a State Government or c. any local authority or d. any corporation or e. any authority established by or under a Central, State or Provincial Act, or f. any company or g. any firm or h. any co-operative society and also includes i. an individual or a Hindu undivided family whose total sales, gross receipts or

turnover from the business or profession carried on by him exceed the monetary limits specified under clause (a) or clause (b) of section 44AB during the financial year immediately preceding the financial year in which the goods of the nature specified in the Table in sub-section (1) or sub-section (1D) are sold or services referred to in sub-section (ID) are provided.

40. For the purpose of section 206C, in clause (c) of the Explanation, “seller” is defined to comprise in its domain the aforesaid specific entities. If any entity is not mentioned therein, it is outside the definition of “seller”, therefore, outside the scope of section 206C.

Cont…..22

: 22 :

41. It means that for the purposes of section 206C(1) and 206C(1D) – a. a company; b. a firm; c. a co-operative society are obliged to collect tax even if they are not liable for audit u/s 44AB(a) or 44AB(b).

42. However, in the case of –

a. Individual or b. HUF they shall be obliged to collect tax if they are liable for audit u/s 44AB(a) or 44AB(b) during the financial year immediately preceding the financial year in which the goods of the nature specified in the Table in sub-section (1) or sub-section (1D) are sold or services referred to in sub-section (ID) are provided.

43. It means that for collecting tax at source u/s 206C(1) and 206C(1D) after 1.6.2016 and for financial year 2016-17 the status of the ‘Individual’ and ‘HUF’ “seller” qua liability for audit u/s 44AB(a) and 44AB(b) is to be tested for financial year 2015-16, i.e.

a. in the case of purchase and sale of goods (business) section 44AB(a) shall apply and it is to be seen whether “total sales, gross receipts or turnover in such business” exceeds Rs. One crore.

b. in the case of provision of service in the nature of business e.g. ‘business of commissions agency’, ‘business of repairs and maintenance’ or any other activity of providing services which are not in the nature of “profession”, section 44AB(a) shall apply and it is to be seen whether “total sales, gross receipts or turnover from in business” exceeds Rs. One crore.

c. in the case of provision of service in the nature of “profession”, section

44AB(b) shall apply and it is to be seen whether “gross receipts” in such profession exceeds Rs. Twenty five lakh {Rs. Fifty Lakh for FY 2016-17 relevant for AY 2017-18}

44. It may be pertinent to note that for the purpose of TCS u/s 206C(1F) on sale of “motor

vehicle” w.e.f. 1.6.2016 “seller” does not include ‘Individual’ and ‘HUF’, since as per clause (c) of Explanation to section 206C ‘Individual’ and ‘HUF’ are included in the definition of “seller” only for the purpose of TCS u/s 206C(1) and 206C(1D), and not for the purposes of section 206C(1F), wherein TCS on sale of “motor vehicle” is to be made. Cont…..23

: 23 :

45. In the above definition of “seller” besides company and firm “co-operative societies” have also been included, which is defined u/s 2(19) of the Act to mean a co-operative society registered under the Co-operative Societies Act, 1912 or any other law for the time being in force in any State for the registration of co-operative societies. The aforesaid definition of “seller” does not include – Trust Societies registered under Societies Registration Act, 1860. Association of Persons (AOP) Body of Individuals (BOI) Therefore, it appears that aforesaid entities are not required to collect tax u/s 206C. Buyer

46. Explanation to section 206C provides that - For the purposes of this section - (aa) "buyer" with respect to —

(i) sub-section (1) means a person who obtains in any sale, by way of auction, tender or any other mode, goods of the nature specified in the Table in sub-section (1) or the right to receive any such goods but does not include,-

(A) a public sector company, the Central Government, a State Government, and an embassy, a High Commission, legation, commission, consulate and the trade representation, of a foreign State and a club; or

(B) a buyer in the retail sale of such goods purchased by him for

personal consumption;

(ii) sub-section (1D) or sub-section (1F) means a person who obtains in any sale, goods of the nature specified in the said sub-section;

47. As per sub-section (1D) and (1F) tax is to be collected from the buyer.

48. As per clause (aa) of the Explanation, for the purpose of sub-section (1D) and sub-section (1F) “buyer” means a person who obtains in any sale, goods of the nature specified in the said sub-section;

49. It may be noted that in aforesaid sub-clause (ii) expression “goods of the nature specified in the said sub-section” is used. Cont…..24

: 24 :

50. There seems to be drafting error in using “said sub-section” while referring to sub-section (1D) and (1F). This expression should have been “said sub-sections”

51. As per above definition “buyer” is a person who - Obtains any goods of the nature specified in sub-section (1D) in any sale.

52. Use of word any before sale means ‘sale’ in any manner viz. – by way of direct sale; by way of auction; by way of tender; by way of e’commerce etc.

53. It is also significant to note that in contrast to ‘a buyer in the retail sale of goods

mentioned in sub-section (1) purchased by a person for personal consumption’ vide exclusionary sub-clause (ii) of clause (aa) of the Explanation, for the purposes of sub-section (1D) and (1F), “buyer” would include a ‘a person who purchases any goods in the retail sale of goods mentioned in sub-section (1D) and (1F) even for personal consumption’.

54. As per above definition “buyer” is a person who “obtains” such goods in any sale. Word “obtain” is neither defined in section 206C nor in the Income Tax Act, 1961. dictionary meaning of the same is – to acquire; to procure; to get hold of; to take possession of; to secure

55. It may be relevant to refer to the definition of “buyer” u/s 2(1) of Sales of Goods Act, 1930, according to which “buyer means a person who buys or agrees to buy goods”.

56. The ‘converse’ of the “buyer” means a person who sells or agrees to sell goods”. Cont…..25

: 25 :

57. The above is supported by section 2(13) the Sales of Goods Act, 1930 according to which “seller” means a person who sells or agrees to sell goods;

58. In the above definition the expression “agrees to buy” goes with the word “secure”. It means that when a buyer enters into a ‘contract of sale’ with a seller and ‘agree to buy goods’ he becomes “buyer”, and if he makes any advance to the seller under such contract of sale, such advance takes the colour of “consideration” for such sale as the same is paid by such person as “buyer” to the “seller”. On the other hand the expression “agrees to sell” indicates an undertaking from the seller to the buyer to perform the contract of sale.

59. As per clause sub-clause (ii) of clause (aa) of the Explanation, defining “buyer” with respect to sub-section (1F), TCS is to be made from a person who purchases the goods of the nature specified in sub-section (1F), i.e. “motor vehicle”.

60. It means that no TCS is to be made under sub-section (1F) with respect to any goods other then “motor vehicle”.

61. The word “value” used before exceeding Rs. 1000000/- refers to the “value of the motor vehicle” and not of anything else e.g. accessories loaded on the vehicle, body installed on the chassis of a ‘bus’ or ‘truck’ etc.

62. However, such accessories loaded on the vehicle or body installed on the chassis of a

‘bus’ or ‘truck’ etc. shall be covered by sub-section (1D), if its consideration exceeds Rs. 200000/- and any part of it is received/paid in cash. TCS u/s 206C(ID) Single transaction

63. Tax is to be collected u/s 206C(1D) in relation to transaction of – a. sale of bullion for amount exceeding Rs. 200000/-; b. sale of jewellery for amount exceeding Rs. 500000/-; c. sale of any goods for amount exceeding Rs. 200000/- d. provision of any service for amount exceeding Rs. 200000/-; e. sale of any goods and provision of any service for amount exceeding Rs. 200000/-

64. Section 206C(1D) applies in respect of single transaction of purchase/sale and service

because “consideration” refers to “sale” of (1) bullion, (2) jewellery, (3) any other goods, (4) providing any service, where “sale” has been mentioned as ‘singular’. Cont…..26

: 26 : Incidence of TCS

65. The incidence which reasons TCS is the – a. sale of any goods, or b. provision of any service

66. The provisions of sub-section (1D) shall apply only when a seller receives any amount in

cash from buyer as consideration for sale of bullion, jewellery, any other goods or services.

67. Before making TCS it is necessary to understand the meaning of following words for the purpose of following words used in sub-section (1D), which are neither defined in the said sub-section (1D) nor in the Income Tax Act, 1961:-

a. Sale; b. Goods; c. Service; and d. Consideration

Sale

68. For making a sale a person must intend to buy goods and the other person must intend to sell the same goods to such person, and for this they enter into “contract of sale”.

69. As per section 4(1) of the Sales of Goods Act, 1930 “a contract of sale of goods” is a contract whereby the seller transfers or agrees to transfer the property in goods to the buyer for a price.

70. Such price is in fact the consideration for sale.

71. As per section 2(10) of the Sales of Goods Act, 1930 “price” means the money consideration for a sale of goods

72. As per section 4(3) of the Sales of Goods Act, 1930 when under a “contract of sale” the property in the goods is transferred from the seller to the buyer, the contract is called a sale.

73. But where the transfer of the property in the goods is to take place at a future time or subject to some condition thereafter to be fulfilled, the contract is called an “agreement to sell”.

74. As per section 4(3) of the Sales of Goods Act, 1930 an “agreement to sell” becomes a sale when the time elapses or the conditions are fulfilled subject to which the property in the goods is to be transferred. Cont…..27

: 27 :

75. “Property in goods” means ownership of goods. Ownership of goods is different from possession of goods, which means custody of goods When “property in goods” passes from seller to buyer, it is called passing of property in goods.

76. As per the language employed in sub-section (1D) the ‘seller’ is obliged to collect tax

from ‘buyer’ at the time of receipt of such amount in cash.

77. “Such amount” refers to receipt of any amount in cash as consideration for sale.

78. Here “consideration” is used with the word “as” and expression “for sale”, which is different from “of sale”.

79. Here, the use of the words “as” means “by way of”, which means that the amount received by the seller in cash must be towards consideration for sale of –

a. bullion, b. jewellery, c. any goods d. any service and not otherwise. If any amount is received in cash or otherwise not as consideration for sale e.g. loan, deposit, gift, capital or for any other obligation, then the provisions of sub-section (1D) as well as sub-section (1F) {as similar words and expressions have been used therein – except sans of cash} shall not apply.

80. Here, the words “for” as against “of” suggest the future sale. Therefore, such

consideration can be for sale which has taken place or which is yet to take place, but the relationship between the payer and payee must be of ‘buyer’ and ‘seller’ under a “contract of sale”.

81. Therefore, the incidence is sale of any goods or provision of any service. If any amount is paid otherwise than as consideration for sale of any goods or provision of any service, the provisions of sub-section (1D) shall not apply, e.g. receipt of any amount as loan, deposit, capital, advance other than for sale or provision for service etc.

82. It is pertinent to note that the amendment in sub-section (1D) vide the Finance Act, 2016 is effective from 1.6.2016, therefore, the provisions of TCS shall apply to the transaction of purchase and sale of any other goods (other than bullion and jeweler) and any service where the “contract of sale” is entered into on or after 1.6.2016, because the tax is to be collected when any amount of consideration is received in cash and such consideration Cont…..28

: 28 : must be for sale of goods or services. Therefore, before any such amount is received, consideration must be present, and before consideration is decided there must be “contract of sale” of goods and such consideration must be for sale of such goods or services. Goods

83. As per section 2(7) the Sales of Goods Act, 1930 “goods” means every kind of movable property other than actionable claims and money; and includes stock and shares, growing crops, grass, and things attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale;

84. Therefore, sub-section (1D) shall not apply to any amount received in cash which is received as consideration for sale other than of goods e.g. –

a. immovable property being land or buildings; b. actionable claims; c. money.

85. It may not be out of place to mention that “motor vehicle” is a movable property and

“motor vehicle” of the value exceeding Rs. 10,00,000/- is covered by the provisions of sub-section (1F). Therefore, “motor vehicle” of value exceeding Rs. 2,00,000/- and of Rs. 10,00,000/- or less shall be covered by the provisions of sub-section (1D) if any part of the consideration for its sale is received in cash.

86. As per clause (ab) of Explanation to section 206C for the purpose of section 206C "jewellery" shall have the meaning assigned to it in the Explanation to sub-clause (ii) of clause (14) of section 2. The same is as follows:

“Explanation 1.— For the purposes of this sub-clause, "jewellery" includes — (a) ornaments made of gold, silver, platinum or any other precious metal or

any alloy containing one or more of such precious metals, whether or not containing any precious or semi-precious stone, and whether or not worked or sewn into any wearing apparel;

(b) precious or semi-precious stones, whether or not set in any furniture, utensil or other article or worked or sewn into any wearing apparel.”

87. As per clause (b) of Explanation to section 206C for the purpose of section 206C

"scrap" means - waste and scrap Cont…..29

: 29 : from the

manufacture or mechanical working of materials

which is definitely not usable as such because of breakage, cutting up, wear and other reasons.

88. TCS on “scrap” is provided in sub-section (1) of section 206C, and for the purpose of section 206C “scrap” is defined as above. Therefore, any waste or scrap generated from the manufacture or mechanical working of materials and which is definitely usable as such for aforesaid reasons would attract TCS under sub-section (1).

89. However, any waste or scrap, which is not covered by the above definition, shall be covered by the general meaning of “goods”, and thus would be covered under sub-section (1D), subject to applicability other conditions provided therein.

90. Immovable property being land or buildings; actionable claims; money shall also not be

covered by the general meaning of “goods”, and thus would be outside the preview of sub-section(1D). Point (time) of TCS

91. In view of above interpretation the “Point of TCS” is the date when any amount of such consideration is received by the seller from the buyer in cash if it is agreed between them that such consideration would be more than the respective thresholds.

92. The expression “such amount” used between “shall, at the time of receipt of” and “in cash” refers to “receives any amount in cash as consideration for sale”.

93. Therefore, the point of TCS shall be the time of receipt of any amount in cash as consideration for sale, i.e. any amount out of the agreed consideration for sale.

94. No tax is to be collected u/s 206C(1D) in relation to any of the above transactions if whole of the sale consideration is received by the seller by any mode otherwise than in cash.

95. Tax is to be collected u/s 206C(1D) in relation to the above transactions if whole of the sale consideration is received by the seller in cash. Cont…..30

: 30 :

96. Tax is also to be collected u/s 206C(1D) in relation to the above transactions if - the seller receives any amount in cash as consideration for sale of –

o bullion or o jewellery or o any other goods (other than bullion or jewellery) or o providing any service.

97. It means that if any amount out of such agreed consideration is received by the seller

from the buyer in advance in cash before the actual sale of such goods, i.e. before the raising of sale invoice and delivery of such goods, the incidence and point of TCS would arise under sub-section (1D) and accordingly tax shall be required to be deducted at that point of time.

98. If any part of such consideration is received in cash prior to the actual sale/delivery of goods, then tax to be collected on the entire sale consideration at the point of receipt of such amount in cash.

99. If any part of such consideration is received otherwise than in cash prior to the actual sale/delivery of goods, then no tax to be collected at that point of time.

100. If any part of such consideration is received in cash at the time of actual

sale/delivery of goods, then tax is to be collected at that point of time @ 1% of the entire such consideration and not only of such cash component because the legislative intent is to deter generation and use of unaccounted money being used in such transactions and to keep trail of such high value transactions.

101. In this regards it may be pertinent to refer to the provisions of section 194-IA {TDS on payment on transfer of certain immovable property other than agricultural land} of the Act, wherein similar language is employed, the relevant part of which reads as follows: “any person, being a transferee, responsible for paying (other than the person referred to in section 194LA) to a resident transferor any sum by way of consideration for transfer of any immovable property (other than agricultural land) shall, at the time of credit of such sum to the account of the transferor or at

Cont…..31

: 31 :

the time of payment of such sum in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct an amount equal to one per cent of such sum as income-tax thereon.”

102. It is the settled law of section 194-IA that wherever consideration for transfer of

any immovable property (other than agricultural land) exceeds Rs. 50 lakh, the transferee is obliged to collect tax at source @ 1% of any sum received against such consideration irrespective of the fact that transfer of such property has not yet taken place. It means that tax is required to be deducted in respect of all and any sum received even before the actual transfer of such property. TDS @ 1% is to be made from such sum and from the entire consideration of transfer of immovable property.

103. In both the provisions of section 206C(1D) and 194-IA following expressions are

common with variation as per context: o buyer and seller vs. transferee and transferor; o any amount in cash as consideration for sale vs. any sum by way of

consideration for transfer; o such amount refers to any amount received in cash vs. such sum refers to

any sum paid or credited; o consideration for sale vs. consideration for transfer.

104. Therefore, the point of collection of tax is the point of time when “such amount”

is received in cash. “Such amount” refers to “any amount” received in cash as consideration for sale of such goods or any service.

Other aspects of section 206C(1D)

105. Tax is to be collected u/s 206C(1D) in relation to the above transactions – o at the rate of 1% o of o sale consideration o as income tax, o if o such consideration –

(i) for bullion, exceeds Rs. 200000/-; or (ii) for jewellery, exceeds Rs. 500000/-; or (iii) for any goods, other than those referred to in clause (i) and (ii), or any

service, exceeds Rs. 200000/-. Cont…..32

: 32 : 106. Tax is to be collected @ 1% of sale consideration. The expression “a sum

equal to one per cent of sale consideration” neither refers to “such consideration” nor “consideration in cash”. It refers to “sale consideration”, which means the entire agreed sale consideration. Therefore, it appears that tax is to be collected by applying the rate of 1% to the entire sale consideration.

107. It may be clarified that “such consideration” used after the word “if” refers to

the entire agreed consideration, and it further refers to the respective threshold.

Consideration

108. Since word “consideration” has been used repeatedly in sub-section (1D) as well as in sub-section (1F), it is imperative to understand its meaning for the purpose of these sub-sections.

109. In sub-section (1D) word “consideration” has been used in following manner: o receives any amount in cash as consideration for sale; o 1% of sale consideration; o if such consideration

for bullion, exceeds Rs. 200000/-; or for jewellery, exceeds Rs. 500000/-; or for any goods, other than those referred to in clause (i) and (ii), or any service, exceeds Rs. 200000/-.

110. In sub-section (1F) word “consideration” has been used in following manner:

o receives any amount as consideration for sale of a motor vehicle; o 1% of the sale consideration;

111. To illustrate, even in section 194-IA word “consideration” has been used in following manner:

o wherever consideration for transfer of any immovable property (other than agricultural land)

o 1% of any sum paid against such sum (consideration)

112. Word “consideration” is neither defined in section 206C nor in section 194-IA and nor in the Income Tax Act, 1961.

113. In the context of purchase and sale of goods the provisions of the Sales of Goods

Act, 1930 are relevant. As per section 4(1) of “a contract of sale of goods” is a contract whereby the seller transfers or agrees to transfer the property in goods to the buyer for a price. Such price is in fact the consideration for sale. As per

Cont…..33

: 33 : section 2(10) of the Sales of Goods Act, 1930 “price” means the money consideration for a sale of goods. Since price has been used in relation to sale of goods, therefore, it may also be relevant to refer to the definition of “sale price” mentioned in laws relating to Tax/VAT/CST on sale of goods.

114. As per section 2(zd) of Delhi Value Added Tax Act, 2004 “sale price” means

the amount paid or payable as valuable consideration for any sale, including -

o (i) the amount of tax, if any, for which the dealer is liable under this Act; o (v) amount of duties levied or leviable on the goods under the Central Excise Act, 1944 or Customs Act, 1962 or the Delhi Excise Act, 2009 whether such duties are payable by the seller or any other person.

115. As per section 2(h) of Central Sales Tax Act, 1956 “sale price” means the

amount payable to a dealer as consideration for the sale of any goods………. As per section 8A of the CST Act, for the purpose of determination of ‘turnover’ of a dealer for the purpose of CST Act, CST is required to be deducted from the ‘sale price’ in accordance with the formula provided therein.

116. From the above provisions it is clear that “consideration” means any amount

paid or payable as price for the sale of goods, which would include all sort of taxes levied or leviable in relation to such price. Therefore, for the purposes of threshold for invoking

117. the provisions of TCS and for the purposes of collecting tax at source @ 1% such

price is to be considered being consideration. It may not also be out of place mention that in sub-section (1F) tax is to be collected if value of motor vehicle exceeds Rs. 1000000/-. Here the threshold of Rs. 1000000/- has been linked to ‘value’, which means the ‘price’ as explained above. Thus, here value, price and consideration are synonymous.

TCS @ 1% of which consideration – significance of the word “the”

118. In sub-section (1D) tax is to be collected @ 1% of sale consideration and in sub-section (1F) tax is to be collected @ 1% of the sale consideration. The use of word “the” in sub-section (1F) makes the difference. “The” is s definite article which is used, especially before a noun, with a specifying effect. In sub-section (1F) use of “the” before sale consideration means “sales consideration” mentioned before in the said sub-section (1F), which is, “any amount received as consideration for sale of motor vehicle of value exceeding Rs. 1000000/-“. It means that if any amount has been received in advance towards such consideration, it shall be subjected to TCS. In sub-section (1D) absence of

Cont…..34

: 34 : the word “the” in expression “@ 1% of sale consideration” means that it is not referring to any specific consideration or previously mentioned consideration. It is simply referring to consideration for sale of goods etc., i.e. the entire agreed consideration. Therefore, it appears that under sub-section (1D) TCS is to be made on the entire consideration for sale whenever any part of such consideration is received in cash.

119. Keeping in view the objectives sought to be achieved through this provision, it appears that tax is to be collected u/s 206C(1D) in relation to the above transactions if following conditions are fulfilled –

o sale consideration of “a” transaction of sale of such goods or provision of

service exceeds the respective threshold provided; and {such consideration in relation to the thresholds refers to the sale consideration of a transaction of sale of such goods or provision of service}

o any part of such sale consideration is received in cash; and

{any amount as consideration refers to part of the sale consideration of a transaction of sale of such goods or provision of service}

120. Again keeping in view the objectives sought to be achieved through this

provision, it appears that tax is to be collected u/s 206C(1D) in relation to the above transactions on whole of the “sale consideration” if any amount of such consideration is received in cash. The sub-section does not speak of TCS on the cash component of the sale consideration. It simply says “1% of sale consideration”, subject to the condition that any amount of the consideration is received in cash. This has been so provided perhaps to discourage involvement of cash in high value transactions of purchase and sale of bullion, jewellery and goods, and provision of services.

121. Logically, TCS should be made only on cash component of the sale consideration,

but the intention of the Government is to deter the use of cash in such transactions and to gather information of such high value transactions in which to any extent cash is involved. o This law will apply to medical/hospital services also where payments are

largely made in cash. In such case it is advisable if w.e.f. 1.6.2016 payments are made through ‘Debit Card’ or ‘Credit Card’ or ECS (RTGS / NEFT etc.).

122. But it may not be out of place to mention that u/s 285BA r/w rule 114E {Serial

No. 4} payments made by any person of an amount aggregating to Rs. 10 lakh or more by any mode other than in cash against bills raised in respect of one or more credit cards issued to that person in a financial year are obliged to be reported by the person issuing such credit cards in “annual statement of financial transactions” {earlier it was known as AIR}.

Cont…..35

: 35 : 123. Similarly u/s 285BA r/w rule 114E {Serial No. 11} receipt of cash payment

exceeding Rs. 2 lakh for sale by any person {who is liable for audit u/s 44AB of the Act} of goods or services of any nature (other than those specified at serial No. 1 to 10 of Rule 114E, if any) is to be reported by the person receiving such payment in “annual statement of financial transactions” {earlier it was known as AIR}. As per sub-rule (3) of rule 114E the reporting person mentioned in column (3) of the Table under sub-rule (2) (other than the person at Sl. No. 9) shall, while aggregating the amounts for determining the threshold amount for reporting in respect of any person as specified in column (2) of the said Table,-

(a) ………. (b) aggregate all the transactions of the same nature as specified in column (2)

of the said Table recorded in respect of that person during the financial year;

124. It may also not be out of place to mention that u/s 139A(5)(c) r/w rule 114B

Permanent Account Number (PAN) of buyer and seller are required to be quoted in all documents pertaining to purchase and sale of any goods or services of an amount exceeding Rs. 2 lakh and u/r 114C the seller is obliged to verify the PAN of both the parties.

125. It means that under the law, wherever the consideration in transaction of purchase

and sale or provision of any service exceeds Rs. 2 lakh, the parties to the transaction are obliged to intimate, provide and quote their so received PAN in the documents pertaining to such transactions, which may be used for the purpose of compliance u/s 206C.

126. No tax shall be collected at source u/s 206C(1D) on any amount on which tax has

been deducted by the payer under Chapter XVII-B, e.g. – a. TDS u/s 194J on professional services; b. TDS u/s 194J on technical services; c. TDS u/s 194J on any remuneration or fees or commission by whatever name

called, other than those on which tax is deductible u/s 192, to a director of a company;

d. TDS u/s 194H on services in the nature of commission; e. TDS u/s 194H on services in the nature of brokerage; f. TDS u/s 194C on services in the nature of -

1. carrying out any work in pursuance of a contract; 2. supply of labour for carrying out any work in pursuance of a

contract; 3. carriage of goods by any mode of transport other than by railways

in pursuance of a contract; Cont…..36

: 36 : 4. advertising in pursuance of a contract; 5. broadcasting in pursuance of a contract; 6. telecasting in pursuance of a contract; 7. production of programmes for such broadcasting in pursuance of a

contract; 8. production of programmes for such telecasting in pursuance of a

contract; 9. carriage of passengers by any mode of transport other than by

railways in pursuance of a contract; 10. catering in pursuance of a contract; 11. manufacturing or supplying a product according to the requirement

or specification of customer by using material purchased from such customer

12. in pursuance of a contract (but does not include manufacturing or supplying a product according to the requirement or specification of customer by using material purchased from a person, other than such customer)

g. TDS u/s 194-IA on consideration for transfer of any immovable property (other than agricultural land).

h. TDS u/s 195 in the case of deductee being no-resident and foreign companies.

TCS u/s 206C(IF)

127. Tax is to be collected u/s 206C(1F) in relation to the transaction of – o sale of “a” motor vehicle of the value exceeding Rs. 1000000/-.

128. Tax is to be collected u/s 206C(1F) in relation to the above transactions at the

time of receipt of any amount as consideration for sale.

129. Tax is to be collected u/s 206C(1F) in relation to the above transactions – o at the rate of 1% o of o sale consideration o as income tax,

130. It is important to note that tax is to be collected u/s 206C(1F) at the time when

any amount is received as consideration for sale of such motor vehicle. It means that if such amount of consideration is received in part, then tax is to be collected at the time of receipt of such part consideration.

Cont…..37

: 37 : 131. If any amount is received as advance before raising of sale invoice for the sale of