italian mses: when and how they gro · ¡staying power over the long period: fourth capitalism...

TRANSCRIPT

Italian MSEs: when and how they grow

A route for Italian medium-sized enterprise to grow

Fulvio Coltorti (Mediobanca Research Area)

11 November 2013

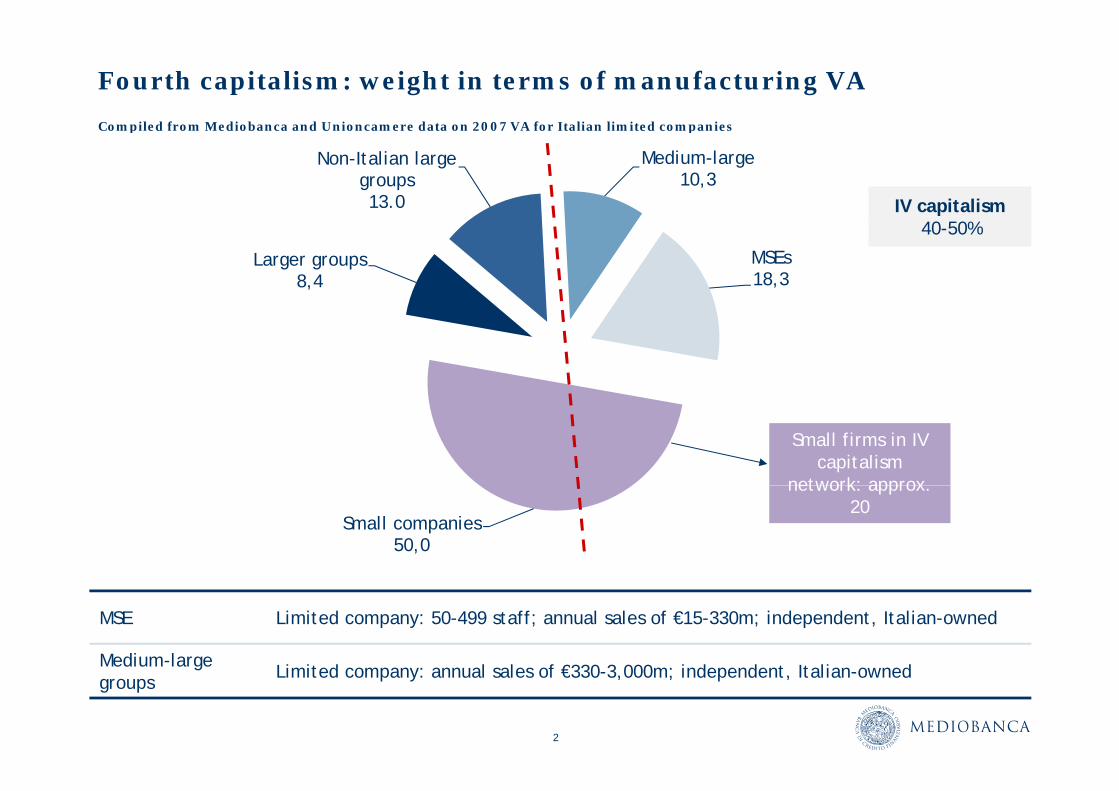

Fourth capitalism: weight in terms of manufacturing VA

Compiled from Mediobanca and Unioncamere data on 2007 VA for Italian limited companiesCompiled from Mediobanca and Unioncamere data on 2007 VA for Italian limited companies

Non-Italian large groups13.0

Medium-large 10,3

IV capitalism

Larger groups8,4

MSEs18,3

40-50%

Small firms in IV capitalism

network: approx

Small companies50,0

network: approx. 20

MSE Limited company: 50-499 staff; annual sales of €15-330m; independent, Italian-owned

Medium-large Li i d l l f €330 3 000 i d d I li d

2

Medium large groups Limited company: annual sales of €330-3,000m; independent, Italian-owned

Fourth capitalism on the stock market

Compiled from Mediobanca and Unioncamere data

Listed MSEs14

Compiled from Mediobanca and Unioncamere data

14 Listed medium-large groups

66

Unlisted medium-large groups

546

Fourth capitalism companies in 2011:Fourth capitalism companies in 2011:only 80 out of 4,200 are listed (2%):

why is this?

Unlisted MSEs3580

3

3580

Company model

Concentrated ownership: normally family-owned

in 70% of cases the founder and his/her descendents own and manage the company* in 70% of cases, the founder and his/her descendents own and manage the company*

in 20% of cases, externals are brought in by the family to help run the company*

in 10% of cases, the founder’s family do not control or run the company*

Specialized production: carried out by activating a filière across the territory; on average 36 most relevant suppliers (located “in proximity”), chosen for their quality, reliability and price*

Commercial strategy: aim at market niches and close relations with customers, who are generally prepared to pay a price premium for the perceived qualityprepared to pay a price premium for the perceived quality

Financial capital comes from shareholders and banks; with the former meeting the need for fixed assets, and the latter providing the working capital

4

* Unioncamere data

Demographic trends, 2002-11: from 4,027 to 3,594 MSEs

Changes in MSE universe Mediobanca Unioncamere survey 2013Changes in MSE universe – Mediobanca-Unioncamere survey, 2013

Cumulative flows, 2003-11, and % of stock at end-2002

A i iti ( ) Incorporations Mergers and Threshold

effect

Acquisition (+) loss (-) of Italian

ownership

Incorporations(+), liquidations

and compositionswith creditors (-)

Mergers and other

transactions (+/-)

Total

Entries 3,472 37 125 - 3,634

Exits 3,268 129 -396 * 274 4,067

Balance +204 -92 -271 -274 -433

Balance as % vs 2002 5.1 -2.3 -6.7 -6.8 -10.7

5

* Di cui fallimenti e altre procedure 189; tasso medio annuo di default 0,5%

Capital solidity indicators: net equity as % of fixed assets

Mediobanca data: leading 100 Italian companies as at 2012 MSEs as at 2011Mediobanca – data: leading 100 Italian companies as at 2012, MSEs as at 2011

108 4 110 7

Net equity as % of fixed assets

97,0

108,4 110,7

31,0 28,221,7

-1,4

,

Top 100 Italian

companies -

Top 100 Italian

companies: i t

Top 100 Italian

companies: bli

Top 100 Italian

companies -di

MSEs -average

MSEs - Made in Italy

MSEs -districts

6

average private public median

Financial needs for investment purposes, and how they are metCompiled based on Mediobanca-Unioncamere 2013 data – Closed set – Self-financed = retained earnings + depreciation/amortization + changes to post-retirement provisions

130

109,3

114,0115,5 114,2

116,1

111,1 111,8 111,7

110

120

106,7,

110,7

100

110

90

80

702002 2003 2004 2005 2006 2007 2008 2009 2010 2011

7

Technical investments Self-financed Net equity/tangible fixed assets

Wrong analysis obstructs understanding …

The Italian productive system is notable for its innovation gap … The timelag compared to the leading industrial nations is affected by the Italian productive system being fragmented into a large number of small companies … (Bank of Italy, QEF 121, April 2012)p ( y, Q , p )

The predominance of small and medium-sized companies shows the difficulties encountered by Italian enterprise in growing to become international players. (EU Commission, April 2013)

An increasing body of research based on corporate data suggests that there is a strong, positive correlation between the size of a company, its productivity and performance in terms of export … (EU Commission April 2013)Commission, April 2013)

Why does no-one actually go and look at the factories?

8

Innovation gap? an example of robotized islands replacing manual machinery

Tecnomeccanica S.p.A., Novara

Sales: €20m (90% of which exports); 114 staff

Value added per staff member in 2012: net per capita VA €60,400; cost of labour €41,900

Investment to replace manual machinery:

Cost of machinery: +50%

Labour savings: -67%

Actual productivity: +25%Actual productivity: +25%

Unit production cost: -20%

Reduced costs pay for robot in six years

9

No international players? Exports up 5.6% per annum on average

Compiled based on Mediobanca Unioncamere data Closed setCompiled based on Mediobanca-Unioncamere data – Closed set

Classes of exporter(share exported in No. of companies

Rate of % change in

exports 2002-

Financial solidity 2011

(net % of total exports in

2002) exports, 2002-2011 equity/fixed

assets )2011

In 2002 Change in 2011

> 85% 83 +44 20.2 119.6 17.7

40 – 85% 616 +87 51.7 123.1 63.0

15 – 40% 417 -34 88.4 107.6 15.7

0 – 15% 337 -18 169.5 110.4 3.6

No exports 283 -79 - 95.7 -

Total 1,736 15.4 63.0 111.7 100.0

In 2002, 40% of MSEs were large exporters; by 2011 this had increased to 48%

10

Productivity improves if size increases? €’000 per employee

Compiled from MSE database 2004 2011 Coltorti & Venanzi Artimino 2013Compiled from MSE database, 2004-2011 – Coltorti & Venanzi, Artimino 2013

606053

50

191913 11

50-99 100-249 250-499

Net VA EBITNet V

As size increases, so productivity and profit per staff member declines; the same trend is witnessed in

11

s s e c eases, so p oduct v ty a d p o t pe sta e be decl es; t e sa e t e d s w t essed Germany, France and Spain

The essence of the fourth capitalism

Social driver: the firm may be seen as a capital investment or as a life project on which the person stakes their reputation and network of social relations; Fourth capitalism companies are life projects which are mostly conceived in district environmentsy

Economic driver: entrepreneurs are linked to their companies for as long as the latter provide them with an adequate return which incorporates compensation for industrial risk; if this compensation declines or disappears entirely the demands for returns become more insistent whereas if the compensation disappears entirely, the demands for returns become more insistent, whereas if the compensation increases disproportionately, there tends to be pressure to invest outside their own area of professional expertise (with serious risks of losing capital in the process)

Staying power over the long period: Fourth capitalism companies tend to endure for an intermediate time horizon; some 80% of MSEs fall within this bracket (in the last decade the average duration for firms in the universe was eight years)

Given these premises, the stock market is an option that is chosen by only a few, select MSEs

12

What is the optimal company size for the markets served? Entrepreneurs’ answers (as %)Sample survey by Unioncamere (March 2013)Sample survey by Unioncamere (March 2013)

5,2

80,2,

14,6

Too large Right size Looking to grow

13

Fourth capitalism and the stock market, from 2003 to date: 54 listings, 52 delistings …g , g

Compiled based on Mediobanca data (Indici e Dati) – industrial MSEs and medium-large companies

6 6

1517

02

6 63

0

1 1 2 1

-5

-2 -2-1

-3-1

-4

-1 -2

-2 -2-1

-1-3

1

-2 -1-1-25

-7-6

-3

-1-2

-1

-3

-2

3

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 novListings Delisted due to PTOs Delisted due to crisis Delisted due to mergers

14

Listings Delisted due to PTOs Delisted due to crisis Delisted due to mergers

When is the stock market useful?

When substantial outlays are necessary in short timeframes (e.g. to fund acquisitions)

When needing to finance extensive distribution networks or major, long-term research programmes

When there is an opportunity to leverage a “window” effect for a brand, or to obtain certification/accreditation with international institutional customerscertification/accreditation with international institutional customers

When the entrepreneur has the objective of reaching a large size for the company over the long periodlong period

When an entrepreneur needs to valorize their capitalWhen an entrepreneur needs to valorize their capital

15

Fourth capitalism: most recent research

M di b U i L di i i d t i li it li (2002 2011) b it Mil d R 2013Mediobanca, Unioncamere, Le medie imprese industriali italiane (2002-2011); www.mbres.it; Milan and Rome, 2013

G. Barbaresco, “Le medie imprese industriali italiane”, presentation, Rome, 7 November 2013; www.mbres.it

D. Mauriello, Le medie imprese, protagoniste di un modello di sviluppo che abbina innovazione e benessere alla coesione sociale, Rome, 7 November 2013; www.mbres.it

Confindustria, R&S, Unioncamere, Medium-Sized Enterprises in Europe (2013), www.mbres.it, Milan, 2013.

F. Coltorti, D. Venanzi, “Produttività, competitività e territori delle medie imprese italiane”, paper presented at XXIII Artimino meeting on local development, 7 October 2013.

F. Coltorti, R. Resciniti, A. Tunisini, R. Varaldo (eds), Mid-sized manufacturing companies: the new driver of Italian , , , ( ), f g p fcompetitiveness, Milan, Springer, 2013.

F. Coltorti, “Italian industry, decline or transformation? A framework”, European Planning Studies, iFirst, October 2012; “L’industria italiana tra declino e trasformazione: un quadro di riferimento”, QA-Rivista dell’Associazione Rossi Doria 2 (2012); revised versions of paper presented at 52nd meeting of the Society of Italian Economists held in Rome on 15 October 20112011

F. Coltorti, “I sistemi di imprese alla guida dell’internazionalizzazione dell’industria Italiana”, Economia Italiana 2 (2012)

G. Barbaresco, F. Coltorti, “Dinamiche evolutive del ‘Quarto capitalismo’ in Emilia-Romagna”, in La metamorfosi del “modello emiliano”. L’Emilia-Romagna e i distretti industriali che cambiano, Bologna, Il Mulino, 2012

F. Coltorti, G. Garofoli, “Le medie imprese in Europa”, Economia Italiana 1 (2011); “Medium-Sized Enterprises in Europe”, Review of Economic Conditions in Italy 1 (2011)

Mediobanca Research Area, window on Fourth capitalism at http://www.mbres.it/it/publications/fourth-capitalism

16

Mediobanca Research Area

www.mbres.it