itc's methodologies in market analysis - world...

TRANSCRIPT

ITC's methodologies in market analysis:

How to identify a country’s strengths & weaknesses and export opportunities of sectors, products and

markets?

Thierry Paulmier ([email protected])

Market Analysis and Research Section (MAR)

What Is ITC?

• Mission– ITC enables small business export success in developing

countriesby providing trade development solutionsto the private sector, trade support institutions and policy-makers

• Strategic objectives– Enterprises: strengthen their international competitiveness.– Trade support institutions: develop their capacity to support

businesses.– Policy-makers: support them integrating the business sector into the

global economy.

Export Impact for Good

ITC Activities

ITC Organizational Chart

TradeMap

Market Access Map

Investment Map

Trade CompetitivenessProfiles

Product Map (TIS/MAS)

Customised tools

Tools

Trade CompetitivenessAssessment

Export PotentialAssessment (EPA)

Export opportunityScan

Market News Serviceand Market Briefs

Customised studies

Studies

Introduction toMarket Analysis

Market Access CapacityBuilding

Mentoring forEPA

Preparation ofMarket Profiles

Customised training

Capacity Building

MAR Products and Services

Product and Market Concentration in Africa

Nigeria

South Africa

Angola Congo Equatorial Guinea

Côte d'Ivoire

GabonBotswana

Zambia

GhanaCameroon

Namibia

Kenya

Chad

Mozambique

Mauritius

Zimbabwe

United Republic of Tanzania

Liberia

Senegal

DR Congo Ethiopia

Guinea

Madagascar

Uganda

Swaziland

Malawi

Lesotho

Mali

Seychelles

Niger

Togo

Benin

Burkina Faso

Sierra Leone

Central African Republic

Cape Verde

Rwanda

Guinea-Bissau

Burundi

Comoros

Eritrea

Saint Helena

Gambia

Mayotte

Sao Tome and Principe

Western Sahara

0

10

20

30

40

50

60

70

80

90

100020406080100

Share of top three export markets (%), 2006

Shar

e of

top

thre

e ex

porte

d pr

oduc

ts (%

), 20

06

Source: ITC TradeMap. The size of the bubbles is proportional to total country exports in 2006.

High product concentrationLow market concentration

Low product and market concentration

High product and market concentration

Low product concentrationHigh market concentration

Product and Market Concentration in Latin America

GrenadaSaint Vincent and the

Grenadines

Saint Kitts and Nevis

Dominica

Antigua and Barbuda

Saint Lucia

Belize

Barbados

Guyana

Haiti

Nicaragua

Panama

Suriname

Honduras

El Salvador

Paraguay

Jamaica

BahamasCuba

Guatemala Uruguay

Bolivia

Dominican Republic

Costa Rica

Ecuador

Trinidad and Tobago

PeruColombia

Argentina

Chile

Venezuela

Brazil

Mexico

0

10

20

30

40

50

60

70

80

90

1000102030405060708090100

Share of top three export markets (%), 2006

Shar

e of

top

thre

e ex

port

ed p

rodu

cts

(%),

2006

Source: ITC TradeMap. The size of the bubbles is proportional to total country exports in 2006.

High product concentrationLow market concentration

Low product and market concentration

High product and market concentration

Low product concentrationHigh market concentration

Product and Market Concentration in Asia

Tuvalu

NauruKiribati

Tonga

Timor-Leste

Micronesia

Palau

Samoa

MaldivesBhutan

Afghanistan

Vanuatu

Solomon Islands

Nepal

Fiji

Marshall Islands

Lao PDRMongolia

DPR of KoreaMacau

Cambodia

Papua New Guinea

Myanmar

Sri Lanka

Brunei Darussalam

Bangladesh

Pakistan

Viet NamPhilippines

Iran

IndonesiaIndia

Thailand

Malaysia

Singapore

Hong Kong (SARC)

Republic of Korea

China

0

10

20

30

40

50

60

70

80

90

100020406080100

Share of top three export markets (%), 2006

Shar

e of

top

thre

e ex

port

ed p

rodu

cts

(%),

2006

Source: ITC TradeMap. The size of the bubbles is proportional to total country exports in 2006.

High product concentrationLow market concentration

Low product and market concentration

High product and market concentration

Low product concentrationHigh market concentration

?

In the area of trade or investment strategy,the business community, trade supporting institutions and

policy makers need to know…

• What are my country’s strengths and weaknesses,overall or for a particular sector?

• What are promising industries or productsfor export development?

• What are attractive markets?

• What are my competitors?

ITC services to contribute totrade development strategies

1. Trade Competitiveness Assessments:Benchmark a country’s strengths and weaknesses

2. Export Potential Assessments:Identify promising industries/products and attractive markets

3. Export Opportunity Scans:Identify export opportunities for countries and regions;(can be done bilaterally)

1.Trade Competitiveness Assessments:Benchmark a country’s strengths and weaknesses

Trade Competitiveness Assessment

• What?– ITC report benchmarking your country’s performance in terms of production factors

and business environment.• Who would use it and why

– Trade Support Institutions and trade policy makers to identify the drivers and / or obstacles to their country’s export competitivenessin order to formulate a broader national export strategy

• Includes– An ITC report that draws on quantitative and qualitative information to rank a

country’s performance against a group of benchmark (similar) countries in terms of Factors of Production (land, capital, labour and infrastructure)Business Environment (political environment, legal framework, market efficiency)

– A national seminar where findings and recommendations of the report are discussed with national stakeholders

– Takes 2 to 3 months to deliver

How to identify potential benchmarking countries:Example Export structure for Pakistan (1)

Bangladesh (13.6)Viet Nam (10.7)10

United States (14.5)Indonesia (11.0)9

France (15.2)Cambodia (12.0)8

Germany (15.5)Sri Lanka (12.2)7

Thailand (16.4)Macau (12.6)6

Turkey (18.0)Turkmenistan (12.8)5

Italy (21.0)Turkey (14.4)4

Hong Kong (SARC) (22.4)Bangladesh (15.0)3

India (31.8)Egypt (15.1)2

China (41.0)India (19.8)1

Main competitorsin same products and markets

(Minimum of exports in value of each product and market as a % of

Pakistan’s total exports)

Countries withmost similar export structure

(Minimum of share in exports of each product and market as a % of

Pakistan’s total exports )

Rank

Similar export structurebut little direct competition:

Egypt, Cambodia, Sri Lanka, Macao, El Salvador, Guatemala, Mauritius,

Madagascar, Nepal, Turkmenistan

Different export structureand little direct competition:

All other countries (…)

Not direct competitors(not in top 20 of absolute index)

Strong direct competitors with similar export structure

(= potential benchmarks):India, Turkey, Bangladesh, China,

Thailand, Indonesia, Viet Nam, Italy, Hong Kong (SARC), Portugal

Strong direct competitorsbut with different export structure:

France, Germany, Mexico, Spain, Netherlands, Belgium, United States,

United Kingdom,Taiwan (PoC), Rep. of Korea

Main direct competitors(in top 20 of absolute index)

Similar export structure(in top 20 of the relative index)

Different export structure(not in top 20 of the relative index)

How to identify potential benchmarking countries:Example Export structure for Pakistan (2)

Jordan’s benchmarking countries: Export Similarity Index (ESI)

8214030Morocco

35175522Egypt

15195025Tunisia

14202939UAE

9217211Lebanon

5221255Turkey

Rank ESI (absolute)

ESI (absolute)Rank ESI (relative)

ESI (relative) Country

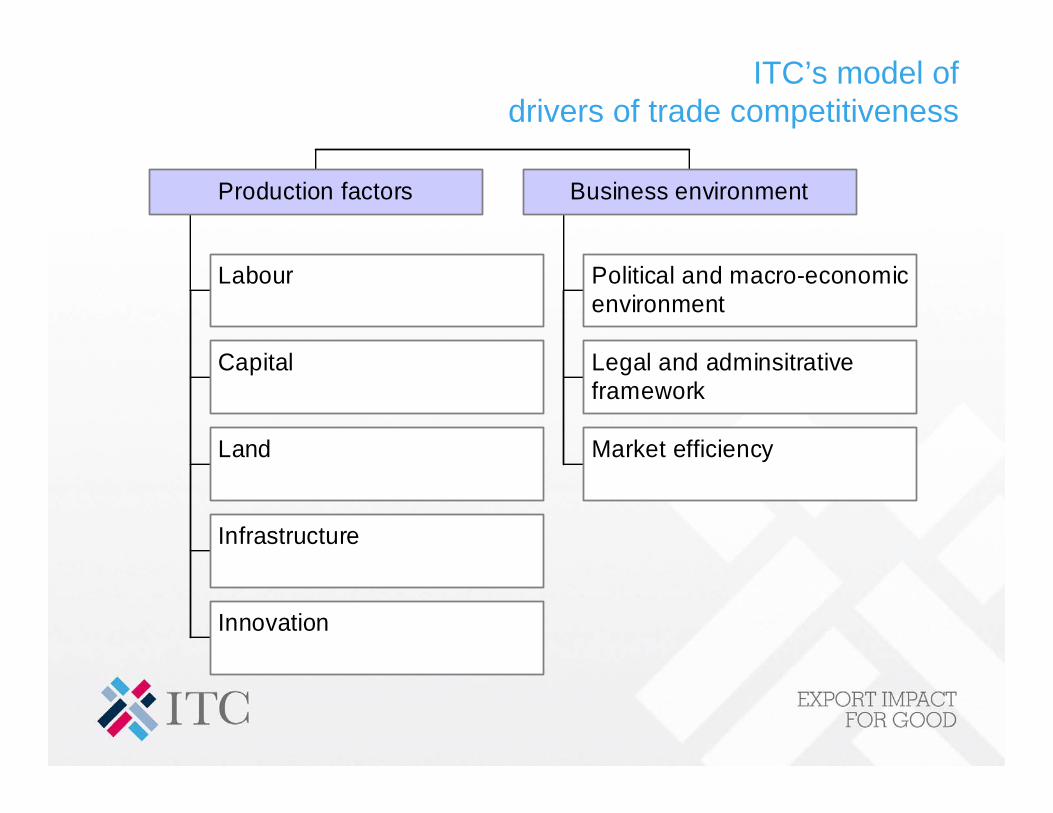

ITC’s model ofdrivers of trade competitiveness

Labour

Capital

Land

Infrastructure

Innovation

Production factors

Political and macro-economicenvironment

Legal and adminsitrativeframework

Market efficiency

Business environment

Production Factors

Labour supply

Healthinputs

Healthperformance

Educationinputs

EducationPerformance

Labour

Savings/investment

Bankingfinancing

Bondmarkets

Foreigndirectinvestment

Capital

Availability

Technology

Land

Availability

Cost

Quality

Infrastructure

R&D Expenditure

Technology Transfer

Public Sector Links

Technological Change(R&D)

Production Factors

Business Environment

Macro-economicstability

Social andgeopoliticalpeace

Political andmacro-economic

environment

Administrativeservices(trade-related)

Administrativeservices(business-related)

Judicial system

Tax system

Property rights

Legal andadministrative

framework

Capital market

Labour market

Domesticcompetition

Supportingindustries

Market efficiency& inter-industry

linkages

Business environment

How to benchmark a country against its competitors

148(1.44)

81(0.68)

101(0.83)

40(0.43)

45(0.45)

30/149(0.38)

1/6Pump price for diesel fuel

(USD per litre)

Rank in world / number of countries(vlue of indicator)

Rank in groupKAZ KAZ RUS CHN AUS CAN NOR

17(6.58)

5(6.76)

8(6.70)

123(3.84)

116(4.41)

79/125(5.22)

4/6Soundness of banks(index)

8(7)

10(7)

21(9)

64(18)

139(39)

170/171(93)

6/6Time for exporting(days)

Jordan’s Labour / Human CapitalOverview:

Supply Inputs Performance

Population ages 65 and above (% of total) (2/7)

School enrolment, tertiary(% gross) (2/7)Quality of educational system (2/6)School enrolment, secondary (% net) (2/6)Quality of math and science education (2/6)

Expenditure per student, tertiary (% of GDP per capita) (3/6)Expenditure on education (% of GNI) (3/6)

Labour force, total (million) (6/7)Population growth(annual %) (7/7)Unemployment, total (% of total labour force) (4/5)Unemployment, female (% of female labour force) (3/4)

Quality of management and business schools (5/6)Brain drain (5/6)School enrolment, primary(% net) (5/7)

Jordan’s Labour / Human CapitalStrengths:

• Young population• Rapid growth of workforce• High expenditure on education (students enter universities

well-prepared; good universities)• High quality of educational system, especially math and

science education• High health expenditure (good health system).

Jordan’s Labour / Human CapitalWeaknesses:

• High dependency ratio

• High unemployment affecting highly-qualified people and more women than men

• Brain drain of high skilled people

• Quality of management and business schools

Jordan’s Labour / Human CapitalChallenges:

• Improve the infant mortality rate• Improve quality of management and business schools• Relatively high unit labour cost (Increasing wages –

outpacing productivity growth)

• Create jobs: an annual need of approx. 60,000 new jobs, especially high skilled jobs.

• Create female jobs, especially in the private sector• Strengthen link between university and private sector to

better meet its needs

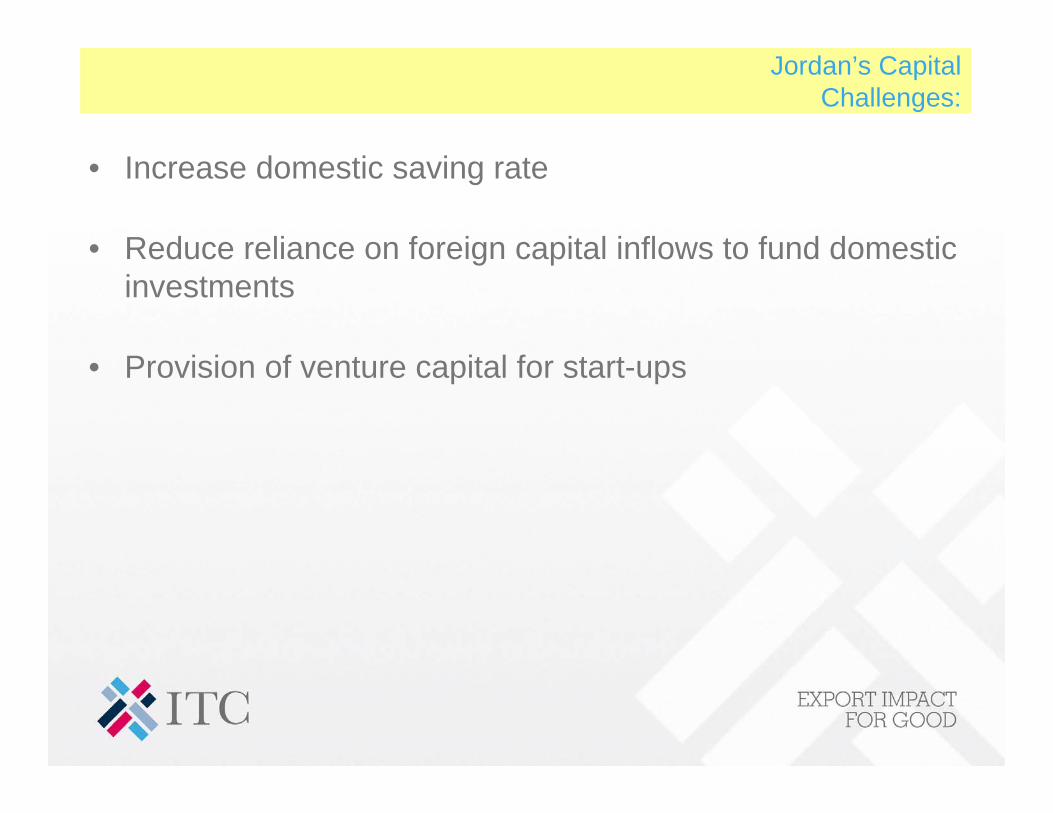

Jordan’s CapitalOverview:

Saving/Investment Banking/Financing Bond markets FDI

Gross fixed capital formation (% of GDP)(1/7)

Domestic credit to private sector (% of GDP) (1/7)Domestic credit by banking sector (% of GDP) (2/7)

Market capitalization of listed companies (% of GDP) (1/7)

Inward FDI stock (% of GDP) (1/7)Inward FDI flow (% of Gross Fixed Capital Formation) (1/7)

Non-performing loans (% of total loans) (3/7)

Venture capital availability (3/6)Stock market turnover ratio (3/7)

Gross savings(% GDP) (5/6)

Jordan’s CapitalStrengths:

• Strong investment (continued high FDI inflows)• Functioning Amman Stock Exchange (high market

capitalisation)• High foreign ownership of market capital at Amman Stock

Exchange• Healthy banking sector• Strong increases in provision of domestic credit• Low rate of non-performing loans and strongly decreasing

Jordan’s CapitalWeaknesses:

• Low gross savings

Jordan’s CapitalChallenges:

• Increase domestic saving rate

• Reduce reliance on foreign capital inflows to fund domestic investments

• Provision of venture capital for start-ups

Benchmarking Kazakhstan: Example Infrastructure

General infrastructure5/6 – 66/125

Air transport5/6 – 72/125

Railroads6/6 – 46/125

Port facilities & inland waterways

6/6 – 90/125

Telephone mainlines4/4 – 73/149

Mobile phones6/6 – 102/166

Internet users6/6 – 139/190

Internet monthly price6/6 – 120/181

Electric power consumption

5/6 – 46/123Energy use per PPP GDP

6/6 – 115/120

Below average

Electricity supply4/6 – 66/125

Average

Pump price for diesel fuel1/6 – 30/149

Pump price for gasoline 2/6–29/149

Above average

QualityAvailabilityCost

Kazakhstan’s main strengths

Good shareholder protection

Low costs for contract enforcement

Flexible hiring and firing regulations

Low overall tax level

Relatively balanced population growthand age-structure

High saving rate

High investment rate(gross fixed capital formation)

Availability of land, including irrigated land

Strong performance in attracting foreign direct investment

Business environmentProduction factors

Kazakhstan’s main weaknesses

High corruptionReliability of the policeLimited independency of judiciaryRising inflation (danger of “Dutch-Disease”)Legal and administrative framework (time, cost and number of procedures) inhibits specifically cross-border tradeHigh costs for starting and closing businessesRegistering of property demandingUnsatisfactory intellectual property rights protectionLack of local competitionLimited quantity and quality of local suppliers

Small labour forceLow life expectancyLow spending on health service provisionLow public investment in educationLow quality of educational trainingBrain drainSmall and shallow stock marketLow dissemination of agricultural technologiesLimited dissemination of information and communication technologies (ICT)Very high Internet price, low useLow quality of infrastructure (general, air, railroad, inland waterways)

Business environmentProduction factors

2. Export Potential Assessments Identify promising sectors, products and markets

?

Export Potential Assessment

• What?– ITC report that identifies promising export sectors and markets and makes industry specific

recommendations for future growth. It bridges the gap between macro-economic competitiveness studies and sector specific reports.

• Who would use it and why– Trade Support Institutions and trade policy makers

to identify their country’s opportunities in terms of export sectors and marketsas components of a broader national export strategy

• Includes– An ITC report that combines quantitative data and qualitative information

(interviews with enterprises and private sector industry groups) to identify:Industries with export potential among 10-20 industries.attractive markets for industries and productsindustry-specific strengths, weaknesses, opportunities and threats (SWOT)

– A capacity building workshop with public and private sector representatives– A national seminar where findings and recommendations of the report are discussed with

national stakeholders– Takes 6 to 9 months to deliver

Selection of sectors

Export performance

World markets

Coffee, tea, spices (09)

All sectors (HS2)

Fruit and nuts (08)

Live plants (06)

Pr. of animal origin (05)

Dairy prod. (04)

Seafood (03)

Meat (02)

(...)

Vegetables (07)

Animals (01)

Priority sectors

8. Precious stones

5. Iron and steel

5. Cotton

4. Cocoa

3. Ships

2. Ores

(…)

10. Rubber

9. Machinery

7. Fruits and nuts

1. Coffee

Domestic supply conditions

Socio-economic impact

Export Potential Assessment

Utilization of composite indicesto combine indicators with different units

• Standardisedto range between0 (low) and 100 (high)

• Averaged to obtain an overall index

Upper threshold

Lower threshold

100

0

How to identify promising industries?

Export value

Export growth

World marketshare

Relativetrade balance

Exportperformance

World importgrowth

Share of attractivemarketsin world imports

Tariff Advantage

World marketProspects

Worldmarkets

Product qualityUnit labour costsProduction costProcess technology

Product and process

Infrastructure costUp-/down-streamlinkages

Supporting industries

CompetitivenessProspects

Domestic supplyconditions

Export potential index

Full-time employmentequivalent

Job creation

Rural development

Poverty reduction

Industrialisation

Foreign currencygeneration

Environmentalsustainability

Socio-economic impact

Priority for export promotion

Index 1: Nepal’s Export Performance

-10000.00 01.2 (Low)14. Mandarin oranges

4-560.0491.5 (Low)13. Honey

100-60.03502.2 (Low)10. Wooden handicrafts

5630.11,9792.3 (Low)8. Medicinal plants and essential oils

30490.01692.3 (Low)12. Coffee

1340.111,4772.8 (Medium)3. Pulses

82180.07,3932.9 (Medium)4. Gems and jewellery

812690.02112.9 (Medium)11. Cut flowers

99240.05,6972.9 (Medium)5. Leather

63-190.322,1313.1 (Medium)1. Silk and pashmina products

25351.09443.2 (High)9. Hand made paper

87190.82,5183.3 (High)7. Ginger

83830.15,1693.5 (High)6. Tea

90210.511,6944.2 (High)2. Cardamom

Relative trade balance (%)

Export growth (% p.a.)

Share in world export (%)

Exports in value

(USD'000)

Index 1:Export

Performance

Index 1: Cambodia’s Export Performance

1

4*

9

13*

19*

25*

34*

50*

100*

157

200*

2,611

Exports*

Low (1.0)

Low (1.1)

Low (1.2)

Low 1.2)

Low (1.4)

Low (1.5)

Low (1.7)

Low (2.0)

Medium (3.0)

High (4.1)

High (5.0)

High (5.0)

Assessment(Index 1)

Beer

Silk

Rubber

Cassava

Livestock

Corn

Soybeans

Cashew nuts

Fishery

Footwear

Rice

Garments

Sector

Index 2: World markets for Cambodia’s Exported Products

Low (1.2)

Low (1.2)

Medium (2.7)

Medium (2.7)

Medium (2.7)

Medium (2.8)

Medium (3.1)

Medium (3.1)

High (3.4)

High (3.5)

High (3.9)

High (5.0)

Assessment(Index 2)

-3.4%23 5 Rice

-4.0%5 7 Corn

0.2%19 14Cashew nuts

1.5%28 8Fishery

2.8%30 5Silk

0.9%25 11 Beer

3.0%27 9 Footwear

0.4%50 5 Livestock

-0.3%42 12Soybeans

3.3%36 9Garments

0.0%40 25 Rubber

7.0%68 18 Cassava

Tariff advantage (+) or disadvantage (-)

compared to top 5 competitors

Share of attractive markets in world

imports (%)

World import growth

(% p.a.)

Sector

Index 3: Nepal’s Domestic Supply Conditions

2.82.53.13.13.42.92.83.42.6Leather

2.12.31.93.23.42.33.04.02.8Hand made paper

2.32.22.43.34.02.43.04.02.8Medicinal plants

3.53.03.92.51.33.31.83.52.9Ginger

3.23.43.03.02.43.13.03.43.0Wooden handicrafts

3.02.04.03.23.03.03.03.83.0Pulses

2.93.12.83.32.42.73.84.23.0Cut flowers

3.13.32.93.22.83.03.33.93.1Gems & jewellery

3.12.43.82.51.03.32.83.03.1Mandarin oranges

3.12.63.62.92.43.02.53.63.1Honey

2.52.72.43.23.81.93.04.23.1Tea

3.13.72.43.12.23.23.04.03.1Silk & pashmina

3.02.83.23.33.43.32.83.63.1Coffee

3.22.34.13.02.43.33.03.23.2Cardamom

Average

Upstream anddown-stream

linkages

Average infrastruc-ture cost

AverageProcess techno-

logy

Average produc-

tion costs

Unit Labour costs

Product quality

Index : Domestic

supply conditions(Survey)

Supporting IndustriesProduct and Process

Index 3: Nepal’s Domestic Supply Conditions

5

5

5

6

5

5

5

10

5

5

5

5

5

5

Number of interviewed firms

2.5 (Low)2.03.05. Leather

2.6 (Low)2.52.69. Hand made paper

2.9 (Med.)3.02.88. Medicinal plants & essential oils

3.0 (Med.)3.03.07. Ginger

3.0 (Med.)3.03.110. Wooden handicrafts

3.1 (Med.)3.03.13. Pulses

3.1 (Med.)3.03.111. Cut flowers

3.1 (Med.)3.03.24. Gems & jewellery

3.2 (High)3.52.814. Mandarin oranges

3.2 (High)3.53.013. Honey

3.4 (High)4.02.96. Tea

3.5 (High)4.03.11. Silk & pashmina

3.6 (High)4.03.112. Coffee

3.8 (High)4.53.12. Cardamom

Index 3: Domesticsupply conditions

Competitiveness prospect (expert

evaluation)

Index: Domestic supply

conditions (survey)

Index 3: Cambodia’s Domestic supply conditions

1.0

1.0

2.5

3.0

3.5

3.5

3.5

4.0

3.5

2.5

2.5

5.0

Prospective conditions

1.0

1.5

2.0

2.0

2.5

2.5

2.5

3.0

3.5

4.5

5.0

4.0

Current conditions

Medium (3.0)Rice

Low (2.5)Corn

Low (2.25)Silk

Low (1.25)Livestock

Medium (3.0)Soya beans

Low (1.0)Beer

Medium (3.0)Cashew nuts

High (3.5)Cassava

High (3.5)Fishery

High (3.5)Footwear

High (3.75)Garments

High (4.5)Rubber

Assessment(Index 3)

Sector

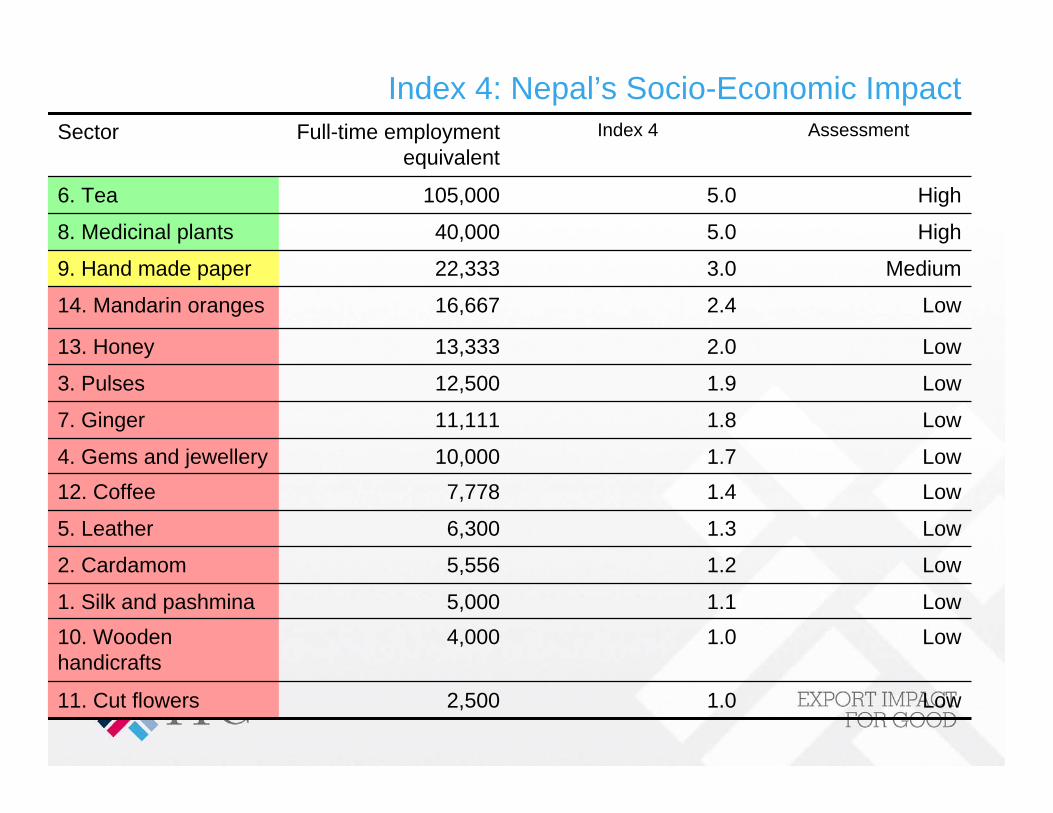

Index 4: Nepal’s Socio-Economic Impact

n.a.3.43.02.03.03.43.63.1Hand Made Paper

2.83.02.43.83.43.64.03.3Leather

3.03.23.02.84.04.04.23.5Pulses

4.03.33.03.03.33.84.03.5Tea

4.03.33.0n.a.3.33.83.53.5Medicinal Plants

3.04.24.81.24.24.44.03.7Mandarine Orange

3.23.33.51.84.84.74.53.7Ginger

2.83.24.62.45.04.83.83.8Cardamoms

3.63.85.02.64.44.23.63.9Honey

4.34.04.03.44.44.63.64.0Coffee

4.54.23.73.44.24.84.84.2Gems and Jewellery

4.64.23.64.03.84.84.84.3Wooden Handicrafts

4.35.03.83.84.65.05.04.5Silk and Pashmina

4.54.65.03.44.64.84.84.5Cut Flowers

Human capital

Gender equality

Environ-mental sustain-ability

Industrial-isation

Rural development

Poverty reduction

Job creation

Index 4: Socio-

economic impact

Index 4: Nepal’s Socio-Economic Impact

Low1.02,50011. Cut flowers

Low1.04,00010. Wooden handicrafts

Low1.15,0001. Silk and pashmina

Low1.25,5562. Cardamom

Low1.36,3005. Leather

Low1.47,77812. CoffeeLow1.710,0004. Gems and jewellery

Low1.811,1117. Ginger

Low1.912,5003. Pulses

Low2.013,33313. Honey

Low2.416,66714. Mandarin oranges

Medium3.022,3339. Hand made paper

High5.040,0008. Medicinal plants

High5.0105,0006. Tea

AssessmentIndex 4Full-time employment equivalent

Sector

Index 4: Socio-economic impact in Lao PDR

2.72.72.9

2.8

3.0

3.6

3.23.34.0

4.0

Women employ-

ment

2.72.72.9

2.8

3.0

3.6

3.23.34.0

4.0

Rural develop-

ment

2.72.72.9

2.8

3.0

3.6

3.23.34.0

4.0

Poverty reduc-tion

3.12.63.6Clothing

3.23.03.2Rattan

3.03.33.0Medicinal herbs

2.82.72.7Wood

2.82.72.7Wood products

2.93.02.9Coffee

2.93.22.8Beer

3.53.83.3Tea

3.93.74.0Rice

4.24.54.0Handicrafts

Index socio-economic

impact

Environ-mental sustain-ability

Employment creation

Index 4: Socio-economic impact in Cambodia

MediumLow (1.0)4,500MediumFootwear

Medium-HighHigh (4.6)360,000HighGarments

Medium-HighHigh (5.0)2,940,000Medium-HighRice

Medium-HighHigh (3.6)260,000Medium-HighFishery

HighMedium (1.2)20,500Medium-HighSilk

LowLow (1.0)3,000LowBeer

LowLow (1.0)4,000LowCassava

Low-MediumMedium (1.1)12,500Low-MediumCornLow-MediumMedium (1.1)16,500Low-MediumSoya beans

Medium-HighMedium (1.1)12,000MediumCashew nuts

MediumMedium (1.4)40,000MediumRubber

MediumHigh (5.0)400,000MediumLivestock

Partial assessmentbased on other criteria*

Partial assessmentbased on employment

Employment estimate

Overall assessmentIndustry

* Female employment, wages, rural development, linkages, environmental sustainability.

Domestic supply conditions:Example of SWOT for rubber in Cambodia

Many smallholdings use mediocre or poor quality trees.

Relatively low yield.

No high value-added down-stream industry (e.g. for tires).

Inefficiencies in SOEs, which still have to undergo privatization process.

Difficult to adapt production level on world demand and price level in the short-run.

Many countries such as EU, USA, Japan, Thailand, India, and China require certification by internationally accredited laboratories.

Lower labour costs than in major producing countries.

Modern processing facilities.

Capacity reserves in processing plants.

Quality of raw product is good.

High potential for growth of planted area.

Potential of future development of value-added rubber industry.

Privatization might help improving productivity.

Weaknesses and threatsStrengths and opportunities

Export potential versus human development index: Cambodia

HighMediumLow

GarmentsTourism------High

---SoybeansCornLow-Medium

Cassava---Beer

Web-based servicesTransport services

Low

FootwearWood products

Light manufacturingLabour services

LivestockCashew nutsMedium

RubberFishery

RiceFruits and vegetables

SilkMedium-High

Export potentialHumandevelopment index

Coffee Wood products

Coal

Vegetables

Processed fruits and vegetables

Tea

Rice

Handicrafts

Beer

2.0

2.5

3.0

3.5

4.0

4.5

2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6

Export potential index

Socio-economic impact index

Low potentialHigh socio-economic impact

High potential andsocio-economic impact

Low potential andsocio-economic impact

High potentialLow socio-economic impact

Export potential versus socio-economic impact: Lao PDR

Findings and actions for Viet Nam

Key points Priority actions

Fishery

- Strong impact onemployment and poverty. - Among the top ten world exporters. - Strong export performance.

- Develop aquaculture to avoid depletion of stocks; -Upgrade products and processing; - Improve packaging and branding.

Coffee

- Highly competitive producer, - High yields - Low production costs. - Poor storage and processing technology.

- Upgrade quality of green coffee beans through investments in research, storage and processing. - Shift to the Arabica variety. - Shift to organic coffee.

Identify interesting markets for a given product/industry

5. Russia

6. Brazil

Most interesting markets

(…)

4. Indonesia

1. China

Current markets

Market opportunities

3. UK

2. India3. Openness of markets

1. Size of markets

2. Dynamism of markets

4. Tariff advantage in markets

All markets

Hungary

France

Egypt

Denmark

Cambodia

Brazil

(…)

Indonesia

Germany

Argentina

5. Other criteria possible: Distance, NTBs, …

How to identify attractive markets?

Share of marketin world exports

Size ofimport markets

Growth differential:market growthminus world growth

Dynamismof markets

Tariff appliedto country

Opennessof markets

Average tariffapplied to 5 top competitorsin the marketminus tariff applied to country

Tariff advantagein markets

Market attractiveness index

Top 5 attractive markets in the world and the regionfor Cambodian Shrimps and prawns (HS 160520)

Cambodia’s main competitorsTariff advantage

TariffGrowth Rate

World share

(%)(%)(% p.a.)(%)

Markets(Rank in world)

Singapore, Japan, Indonesia0.05.01640.027. Philippines

Viet Nam, Netherlands, India0.40.0600.117. Malaysia

China, Japan, Thailand0.00.0260.515. Hong Kong

Singapore, China5.00.0510.013. Indonesia

China, USA, Malaysia38.610.01191.09. Viet Nam

Thailand, China, Viet Nam1.20.0731.45. United StatesThailand, Viet Nam, China3.20.0616.64. Japan

Greenland, Canada, Iceland0.50.0127.63. Denmark

Thailand, China, Viet Nam0.00.0233.62. Canada

China, Denmark, Belgium4.30.0623.21. Spain

Most attractive markets forCambodia’s most promising fishery products

1. Spain, 2. Canada, 3. Denmark, 4. Japan, 5.United States

1. Netherlands, 2. Japan, 3. UK, 4. France,5. United States

1. France, 2. Sweden, 3. UK, 4. Italy,5. Belgium

Most attractive marketsin the world

2.48

2.65

2.68

Export potential

index

12. Viet Nam, 32. Tajikistan, 34. Kazakhstan, 39. Singapore, 42. Thailand

Fish fillets, dried, salted (030420)

10. Viet Nam, 27. Malaysia,45. Georgia, 49. Maldives,

Fish fillets, fresh or chilled (030410)

Attractive markets in the region(rank in the world)

Product

9. Viet Nam, 13. Indonesia,15. Hong Kong (SARC),17. Malaysia,27. Philippines

Shrimps and prawns, prepared (160520)

*Markets in green indicate new markets for Cambodia.

Attractive markets for Cambodia

Rep. of Korea, Canada, China, Australia, Hong Kong

United States, France, United Kingdom, Italy, Japan Fishery

Germany, United States, United Kingdom, Japan, France

Germany, United States, Italy, Singapore, Brazil

China, Malaysia, Finland, Spain, Indonesia

Italy, France, United Kingdom, Germany, Spain

United Kingdom, France, Italy ,Spain, Germany

Most interesting markets

Belgium, Spain, Austria, Australia, Singapore

Turkey, Malaysia, Slovenia, Viet Nam, Mexico

South Africa, Viet Nam, Angola, Gambia

Rep. of Korea, Turkey, Australia, Canada, New Zealand

Thailand, Indonesia, Singapore, Australia, United Arab Emirates

Other markets

Tourism

Rubber

Cassava

Footwear

Garments

Sector

Cambodia’s tariff advantages or disadvantages

6768Neither an advantage nor a disadvantage (-5%<D<5%)

100100Total

24A Tariff disadvantage(D<=-5%)

3027A tariff advantage(D>=5%)

Share in world imports (%)Share in Cambodia’s exports

(%)Markets where Cambodia has…

D: Difference between the (weighted) tariff applied the top five competitors in each market and the tariff applied to Cambodia.

3. Export Opportunity Scan

Export Opportunity Scan

• What?– ITC report analysing quantitative data about your country’s export performance in

order to identify promising sectors for export promotion or import substitution• Who would use it and why

– Trade Support Institutions and trade policy makersAs a point of departure for a more detailed analysis of their country’spotential export sectors, products and markets

• Includes– An ITC report that draws on trade, market access and production data to analyse a

country’s current export performance and current production* compared with world demand and world production to identify sectors that have potential for:

Export development and / orImport substitution

– The report is based on statistics and therefore needs to be validated further at the country level using additional qualitative information

– Takes 1 to 2 months to deliver

* Production data covers agricultural commodities only

Selection of sectors

Export performance

World markets

Coffee, tea and spices (09)

All sectors (HS2)

Fruit and nuts (08)

Live plants (06)

Prod. of animal origin (05)

Dairy prod. (04)

Seafood (03)

Meat (02)

(...)

Vegetables (07)

Animals (01)

Priority sectors

8. Precious stones

5. Iron and steel

5. Cotton

4. Cocoa

3. Ships

2. Ores

(…)

10. Rubber

9. Machinery

7. Fruits and nuts

1. Fuel

Domestic supply conditions

Socio-economic impact

Export Opportunity Scan

Export Potential Asessment

Model for regional Trade Opportunity Scan (for agricultural commodities)

Tariff applied to the region & Tariff advantage for the regionMarket Access

Growth of world imports & Absolute change in world importsDynamism

World importsSizeWorld market index

Number of importing countries in the regionDiversification

Growth of regional imports from World & Absolute change in regional importsDynamism

Regional imports from world & Share of region in world importsSizeImport index

Net exports (excluding intra-regional trade)Relative trade balance

Trade balance

Number of exporting countries in the regionShare of top exporting country in the region

Diversification

Growth of region’s exports to worldAbsolute change in region’s exports

Dynamism

Region’s exports to worldShare of region’s exports in world exports

SizeExport index

Ratio of regional yield to world yieldYield

Number of producing countries & Share of top producing country in the regionDiversification

Growth of regional productionDynamism

Share of region in world productionSizeProduction index

IndicatorsDimensionIndices

Utilization of composite indicesto combine indicators with different units

• Standardisedto range between0 (low) and 100 (high)

• Averaged to obtain an overall index

Upper threshold

Lower threshold

100

0

Index 1 Production: Size

1007442,863,2891. Other roots and tubers

Index%MT

4325354,3007. Other vegetable products

342011,649,5798. Sorghum

3219440,5009. Cashew nuts

26155,457,92210. Groundnuts in shell

100632,455,5001. Cocoa beans

100593,576,0001. Citrus fruit nes

714211,475,2705. Millet

46

100

2856,048,9606. Cassava

853,107,1821. Cow peas, dry

Share of Western Africain world production

For information:ProductionTop 10 products

Index 1 Production: Dynamism

8846. Cassava

8846. Beans, dry

8238. Maize

8139. Dates

100171. Watermelons

100111. Broad beans, dry

10051. Eggplants

10071. Wheat

69310. Sorghum

9445. Cocoa beans

Index% p.a.

Growth of Western Africa productionTop 10 products

Index 1 Production: Diversification

64

71

93

71

100

71

79

100

100

100

Index

857054 (Nigeria )156. Groundnuts in shell

839637 (Ghana )117. Coconuts

816955 (Nigeria )148. Millet

768048 (Nigeria )119. Sesame seed

10010019 (Burkina Faso )151. Other pulses

918147 (Nigeria )152. Rice, paddy

897749 (Nigeria )153. Maize

8910025 (Mali )123. Cotton

88

100

Index

7642 (Nigeria )109. Pimento, allspice

8634 (Ghana )115. Bananas, plantains

% (top producer)0 to 16

Averageindex

Share of top producerin Western Africa’s production

Number of producing countries in Western Africa

Top 10 products

Index 1 Production: Yield

941.026. Other roots and tubers

931.017. Millet

921.008. Pimento, allspice

900.999. Cocoa beans

860.9510. Coconuts

1001.921. Nutmeg, mace, cardamons

1001.221. Cucumbers and gherkins

1001.111. Other spices

1001.071. Sesame seed

860.9510. Onions

991.075. Grapefruit and pomelos

IndexRatio

Ratio of Western Africa’s yieldto world yield

Top 10 products

Index 1 Production: Overall

21151086. Sorghum

1933177. Sesame seed

25171398. Cashew nuts

23618108. Groundnuts in shell

925511. Cocoa beans

781452. Millet

6222413. Other roots and tubers

1412664. Cassava

1

34

Rankdiversification

1922198. Other pulses

122615. Cow peas, dry

Rankrelative yield

Rankdynamism

Ranksize

Index 2 Export: Size

21384511,76810. Ginger

84,902

94,166

99,208

9,597

13,726

47,913

119,338

830,882

261,228

2,868,638

USD 1,000

Western Africa exportsto world

3361656. Other roots and tubers

2955547. Other oil crops

27172388. Bananas, plantains

2391369. Coffee, green

100100671001. Cocoa beans

100100151001. Cashew nuts

928581003. Cotton

7310010464. Pineapples

9

60

Index

2113210. Oil palm

396185. Sesame seed

%Index

Average Index

Share of Western Africain world exports

Top 10 products

Index 2 Export :Dynamism

5111,9731001626. Other fruits

5112,140100946. Cassava

5235,992100724. Other vegetable products

5259,4901002094. Other oil crops

791001,394,96059163. Cocoa beans

80100359,50460172. Cotton

85

54

% p.a

Growth of Western Africa exports to world

100100229,0021001. Cashew nuts

5111,8071006. Sorghum

IndexUSD 1,000Index

Average Index

Absolute change in Western Africa exports

Top 10 products

Index 2 Export :Diversification

7010034 (Niger)4057. Beans, dry

727451 (Côte d'Ivoire )7086. Cocoa beans

828445 (Côte d'Ivoire )8095. Tea

848842 (Côte d'Ivoire )8094. Other nuts

879438 (Côte d'Ivoire )8093. Cashew nuts

9010029 (Côte d'Ivoire )8092. Mangoes

632683 (Ghana )1001110. Other vegetables

5

6

11

0 to 16

Number of exporting countries

10010029 (Burkina Faso )1001. Cotton

698942 (Ghana)508. Groundnuts in shell

679438 (Niger)409. Cow peas, dry

Index % (top exporter)Index

Average Index

Share of top exporter in Western African exports

Top 10 products

Index 2 Export: Trade Balance

651001003047,8357. Sesame seed

7298974592,5105. Coffee, green

721001004592,3495. Bananas, plantains

7710010054119,2174. Pineapples

100100100100261,1561. Cashew nuts

100100100100826,0091. Cotton

5910099179,0828. Other oil crops

11,709

13,665

2,868,449

USD 1,000

Absolute trade balance

1001001001001. Cocoa beans

59100100198. Other roots and tubers

5910099188. Ginger

Index %Index

Average Index

Relative trade balanceTop 10 products

Index 2 Export: Overall

7143457. Sesame seed

1389218. Groundnuts in shell

5114799. Coffee, green

204392110. Other nuts

11232. Cotton

16313. Cocoa beans

4173944. Pineapples

11233125. Mangoes

12

3

Rankdiversification

8475. Other oil crops

1111. Cashew nuts

Ranktrade balance

Rankdynamism

Ranksize

Index 3 Import : Size

54902178,7547. Rice, paddy

561005136,6346. Jute and other bast fibres

571709649,3905. Maize

96912100200,7224. Oil palm

1001004100848,0581. Wheat

100100210072,6231. Tea

34511168,13710. Sorghum

5,464

24,753

51,439

USD 1,000

Western Africa imports from world

10010031001. Onions

52561488. Potatoes

47842119. Cow peas, dry

Index%Index

Average index

Share of Western Africain world imports

Top 10 products

Index 3 Import : Dynamism

51211100High9. Broad beans, dry*

51212100High9. Castor beans*

51258100989. Citrus fruit nes

597518,12944127. Onions

61235,2621002466. Soybeans

67347,9661001635. Sorghum

7110024,47843114. Tea

75100363,37850153. Wheat

7610077,18453182. Oil palm

512 31100High9. Oats*

79

83

33

% p.a.

Growth of Western Africa imports from World

8810031,518761. Maize

5245761008. Other pulses

5121291009. Almonds

IndexUSD 1,000Index

Average Index

Absolute change in Western Africa imports

Top 10 products

Index 3 Import : Diversification

819135 (Niger )71118. Cow peas, dry

796553 (Liberia )931410. Tomatoes

8610028 (Mali )71117. Other vegetables

899234 (Senegal )86136. Maize

938738 (Ghana )100155. Tea

9610015 (Liberia )93144. Peas, dry

999730 (Senegal )100162. Potatoes

999830 (Ghana )100162. Oil palm

10

14

15

0 to 16

Number of importing countries in Western Africa

10010026 (Senegal )1001. Onions

816951 (Senegal )938. Garlic

799432 (Senegal )6410. Dates

Index% (top importer)Index

Average Index

Share of top importer in Western Africa exports

Top 10 products

Index 3 Import: Overall

84297. Cow peas, dry

431198. Peas, dry

335109. Sorghum

8381410. Garlic

5412. Tea1713. Onions

14314. Wheat

6155. Maize

10

2

2

Rankdiversification

421310. Dates

1986. Potatoes

241. Oil palm

Rankgrowth

Ranksize

Index 4 World market: Size

959,9226. Cotton

848,7437. Bananas, plantains

505,2538. Tomatoes

454,7459. Cocoa beans

10021,3811. Wheat

10018,9161. Soybeans

10013,2501. Maize

10010,4411. Oil palm

394,11910. Barley

9710,1545. Coffee, green

IndexUSD million

World importsTop 10 products

Index 4 World market: Dynamism

59712,70447109. Bananas, plantains

58165741002410. Avocados

60271,00093217. Cashew nuts

61572,16865146. Tomatoes

651004,1673164. Wheat

65572,15273164. Cocoa beans

781006,91857123. Soybeans

791003,82659132. Coffee, green

7

23

% p.a.

Growth of world imports

1001005,8071001. Oil palm

60833,180377. Maize

IndexUSD millionIndex

Average Index

Absolute change in world importsTop 10 products

Index 4 World Market: Access conditions

6327898110. Cantaloupes & other melons

6437119139. Oats

6330996110. Cabbages

6843139326. Tang. mand. clement. satsma

6842139426. Lettuce

7554169615. Tomatoes

8289277484. Garlic

831004266103. Maize

87100457382. Cassava

5

1

6

%

Tariff applied to Western Africa

9010061811. Sesame seed

65319988. Beans

6344138210. Pimento, allspice

Index%Index

Average Index

Tariff advantage for Western Africa

Top 10 products

Index 4 World market: Overall

54977. Bananas, plantains

581568. Cotton

29499. Cocoa beans

1273010. Sesame seed

32252. Coffee, green

58112. Oil palm

41414. Wheat

62315. Soybeans

6

5

3

RankMarket access conditions

181410. Tang. mand. clement. satsma

686. Tomatoes

711. Maize

Rankgrowth

Ranksize

1. Cashew nuts1. Cocoa beans3. Cotton4. Pineapples5. Sesame seed6. Other roots and tubers7. Other oil crops8. Bananas, plantains9. Coffee, green10. Ginger10. Oil palm

Export index

1. Cocoa beans2. Millet3. Other roots and tubers 4. Cassava5. Cow peas, dry6. Sorghum7. Sesame seed8. Cashew nuts8. Groundnuts in shell 8. Other pulses

Production index

1. Oil palm2. Tea3. Onions1. Wheat5. Maize6. Potatoes7. Cow peas, dry8. Peas, dry9. Sorghum10. Dates10. Garlic

53. Cocoa beans

Import index World market index

1. Maize1. Wheat1. Oil palm1. Soybeans5. Coffee, green6. Cotton7. Bananas, plantains8. Tomatoes9. Cocoa beans10. Barley

Top 10 commodities for ACP West Africain each of the four indices

ACP Western African countries: Mapping the top 20 commodities in each index

---Millet, CassavaCitrus fruit Pimento, allspiceCoconuts…

Chillies & peppers, green Tang. mand. clement. Soybeans…

Eggplants Nutmeg, mace, cardamons Watermelons Grapefruit and pomelos ….

Low Export,Low Import indices

MaizeCow peas, dry Sorghum Onions

Wheat Tomatoes Oil palm Garlic

Rice, paddy; Dates Potatoes Tea …

Low Export,High Import indices

Cocoa beans Sesame seedCashew nuts Bananas, plantains

Other roots and tubers Groundnuts in shell

BeansCotton PineapplesCoffee, green

Mangoes Papayas Ginger Broad beans, green Cantaloupes & other melons

High Export,Low Import indices

------------High Export,High Import indices

High Production,High World markets indices

High Production,Low World markets indices

Low Production,High World market indices

Low Production,Low World market indices

Pimento, allspice

Cassava

Coconuts

Beans, dryBroad beans, dryMillet

No apparent potential

Other roots and tubers

Sesame seedGroundnuts in shell

Cashew nuts

Bananas, plantains

Cocoa beans

Export developmentHight rank in World markets or Exports

Import substitution and Export development

High rank in Imports and (Exports or World Markets)

Import substitutionHigh rank in

import

Product sectors

Spices

Roots and tubers

Oil crops

Nuts

Fruits and vegetables

Coffee, cocoa, tea

Cereals, grains, beans, peas and pulses

Onions

Cow peas, dry Sorghum Maize

ACP Western African countries: Commodities with high ranks (top 20) in production:

import substitution and/or export development

ACP Western African countries: Commodities with medium ranks (Top 21 to 40) in production:

import substitution and/or export development

Oil palm Oil crops

PotatoesRoots & tubers

Nutmeg, mace, cardamons

WatermelonsCucumbers & gherkinsEggplants Grapefruit & pomelos

Chick-peas

No apparent potential

BeansPineapplesMangoes

Cotton

Export development

Import substitution and Export

development

Import substitution

Product sectors

Spices

Nuts

Fruits and vegetables

Cotton

Cereals, grains, beans, peas and pulses

Pepper, white / long / black

Dates

Rice, paddy

Tomatoes

Wheat

ACP Western African countries: Commodities with low ranks in production:

import substitution and/or export development

SoybeansCastor beansOil crops

PotatoesSweet potatoes Roots & tubers

Almonds

CauliflowerOranges

Jute and other bastfibres Sisal & other textile fibres of agave

Oats

No apparent potential

Barley

Ginger

Avocados Tang. mand. clement.Chillies & peppers, greenLettuce Broad beans, green Cantaloupes & melons Papayas

Coffee, green

Export development Import substitution and

Export development

Import substitution

Product sectors

Spices

Nuts

Fruits and vegetables

Fibre crops

Coffee, tea

Cereals, grains, beans, peas & pulses

CabbagesCarrots

Tea

Peas, dry

Garlic

Exportvalue

Worldmarketshare

Size

Exportgrowth

Absolutechange

Dynamism

Net exports

Relativetradebalance

Trade Balance

Jordan Exports

Worldimports

Size

Worldimportgrowth

Absolutechange

Dynamism

Applied tariffsto Jordan

Tariffadvantage

Marketaccess

conditions

European imports

Exportvalue

Worldmarketshare

Size

Exportgrowth

Absolutechange

Dynamism

Jordan ExportsTo Europe

TradeOpportunity Scan

Trade Opportunity Scan for Jordan-EU

Jordan export index vs Europe import index

Low Europe market index,but high Jordan export index:

Fertilizers (2, 87)Salt/ sulphur/ earth/ stone/ plaster/ lime and cement (3, 66)Inorganic chemicals (5, 72)Vegetables (6, 69)Lead (8, 33)Pearls/ precious stones (8, 33)Fats and oils (10, 66)Nickel (13, 45)Copper (15, 49)Silk (15, 80)(…)

Low Europe marketand Jordan export indices:

Remaining product groups

Low Europeimport index

High Europe market and Jordan exportindices:

Garments (knit) (1, 15)Garments (not knit) (3, 9)Pharmaceutical prod. (7, 1)Aluminium (11, 24)Dairy prod. (12, 24)Ores/ slag/ ash (13, 17)Floating structures (Ships/boats) (15, 12)Other base metals (15, 19)Organic chemicals (21, 11)Prod. of animal origin (21, 19)(…)

High Europe market index,but low Jordan export:

Electronic equipment (35, 5)Meat and fish prep. (38, 15)Cereal and flour prod. (41, 19)Fruits and nuts (46, 19)Plastics (50, 5)Cocoa prod. (63, 17)Essential oils (66, 24)Paper (66, 12)Apparatus (72, 7)Art. of iron or steel (72, 10)(…)

High (top 30)

Europe import index

High (top 30) Jordan’s export indexLow Jordan’s export index

Rank of Europe import Index

Rank of Jordan Export Index

*Product groups in red indicates Jordan exports to Europe.

Jordan-Europe export index vs Europe import index

Low Europe market index,but high Jordan export – Europe index:

Inorganic chemicals (1, 72)Salt/ sulphur/ earth/ stone/ plaster/ lime and cement (2, 66)Fertilizers (3, 87)Pearls/ precious stones (6, 33)Lead (8, 33)Fats and oils (9, 66)Vegetables (10, 69)Copper (15, 49)Misc. Manuf. (15, 62)Wadding/ felt/ nonwovens/yarns/ twine/ cordage (17, 53)(…)

Low Europe marketand Jordan –Europe export indices:

Remaining product groups

Low Europe import index

High Europe market and Jordan – Europe export indices:

Rubber (4, 24)Mechanical appliances (5, 4)Aircraft/ spacecraft (7, 19)Fruits and nuts (11, 19)Other base metals (12, 19)Apparatus (12, 7)Iron and steel (14, 7)Organic chemicals (17, 11)Garments (knit) (20, 15)Vehicles (20, 3)(…)

High Europe market index,but low Jordan – Europe export:

Dairy prod. (34, 24)Cereal and flour prod. (34, 19)Cocoa prod. (34, 17)Footwear (34, 24)Essential oils (56, 24)Garments (not knit) (58, 9)Electronic equipment (58, 5)Plastics (60, 5)Pharmaceutical prod. (61, 1)Aluminium (62, 24)(…)

High Europe import index

High Jordan-Europe export indexLow Jordan-Europe export index

Rank of European import Index

Rank of Jordan-Europe Export Index

Viet Nam

Trade Competitiveness AssessmentExport Potential Assessment

Studies of the Market Analysis and Research Team

Lao PDR

Kazakhstan

Nepal

Romania

Uruguay Botswana

Zambia

Cambodia

Mongolia

Ghana

Jordan

Oman

Studies 2005 - 2008

Ghana (2006)Uruguay (2006) Kazakhstan (2006) Romania (2007)

Trade Competitiveness Assessment

Malawi (2006) Guinea Conakry (2006) Lao PDR (2007)Romania (2007-08)

Mentoring for Export Potential Assessment

CBI (2003, 2007)COMESA, ECCAS, ECOWAS (2007-08)6 ACP regionsJordan (2008)Oman-Sudan (2008)

Export/Trade Opportunity Scan

Zambia (2004) Botswana (2004) Lao PDR (2005)Viet Nam (2005)Mongolia (2005) Nepal (2007)DTIS Cambodia (2007)

Export potential assessment

Thank you for your attention