j ohn hancock variable insurance trust - … prospectus.pdf · j ohn hancock variable insurance...

TRANSCRIPT

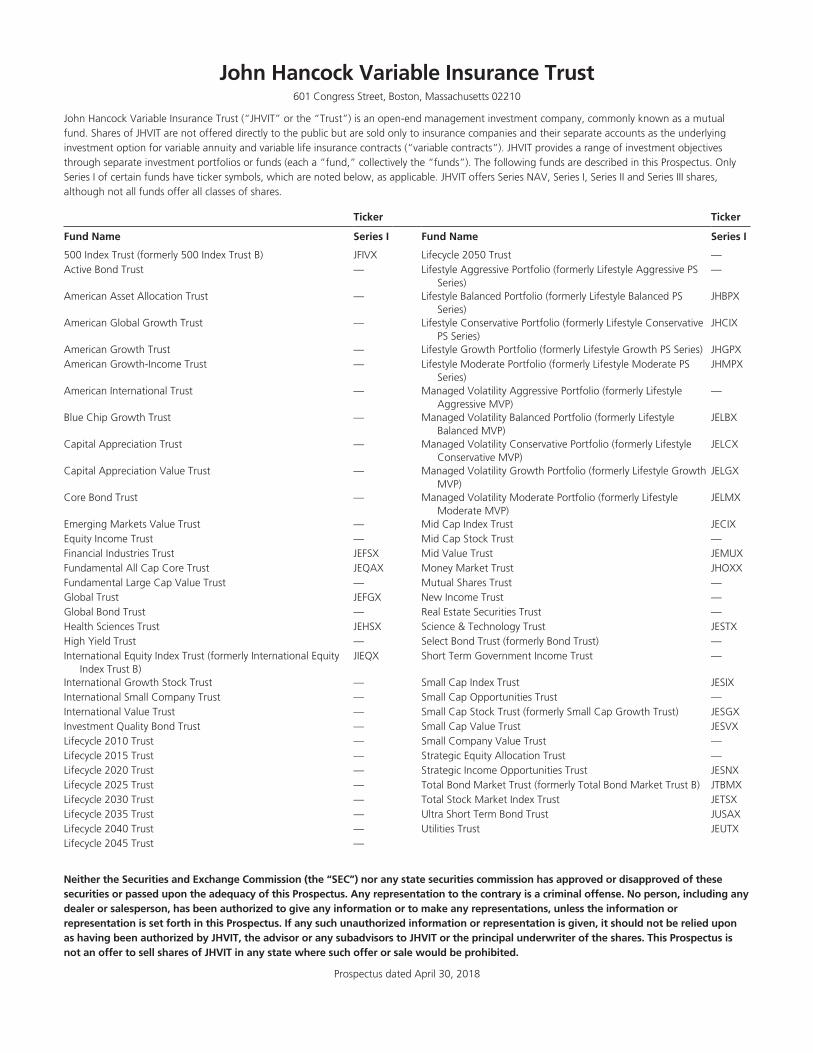

John Hancock Variable Insurance Trust601 Congress Street, Boston, Massachusetts 02210

John Hancock Variable Insurance Trust (“JHVIT” or the “Trust”) is an open-end management investment company, commonly known as a mutualfund. Shares of JHVIT are not offered directly to the public but are sold only to insurance companies and their separate accounts as the underlyinginvestment option for variable annuity and variable life insurance contracts (“variable contracts”). JHVIT provides a range of investment objectivesthrough separate investment portfolios or funds (each a “fund,” collectively the “funds”). The following funds are described in this Prospectus. OnlySeries I of certain funds have ticker symbols, which are noted below, as applicable. JHVIT offers Series NAV, Series I, Series II and Series III shares,although not all funds offer all classes of shares.

Ticker Ticker

Fund Name Series I Fund Name Series I

500 Index Trust (formerly 500 Index Trust B) JFIVX Lifecycle 2050 Trust —Active Bond Trust — Lifestyle Aggressive Portfolio (formerly Lifestyle Aggressive PS

Series)—

American Asset Allocation Trust — Lifestyle Balanced Portfolio (formerly Lifestyle Balanced PSSeries)

JHBPX

American Global Growth Trust — Lifestyle Conservative Portfolio (formerly Lifestyle ConservativePS Series)

JHCIX

American Growth Trust — Lifestyle Growth Portfolio (formerly Lifestyle Growth PS Series) JHGPXAmerican Growth-Income Trust — Lifestyle Moderate Portfolio (formerly Lifestyle Moderate PS

Series)JHMPX

American International Trust — Managed Volatility Aggressive Portfolio (formerly LifestyleAggressive MVP)

—

Blue Chip Growth Trust — Managed Volatility Balanced Portfolio (formerly LifestyleBalanced MVP)

JELBX

Capital Appreciation Trust — Managed Volatility Conservative Portfolio (formerly LifestyleConservative MVP)

JELCX

Capital Appreciation Value Trust — Managed Volatility Growth Portfolio (formerly Lifestyle GrowthMVP)

JELGX

Core Bond Trust — Managed Volatility Moderate Portfolio (formerly LifestyleModerate MVP)

JELMX

Emerging Markets Value Trust — Mid Cap Index Trust JECIXEquity Income Trust — Mid Cap Stock Trust —Financial Industries Trust JEFSX Mid Value Trust JEMUXFundamental All Cap Core Trust JEQAX Money Market Trust JHOXXFundamental Large Cap Value Trust — Mutual Shares Trust —Global Trust JEFGX New Income Trust —Global Bond Trust — Real Estate Securities Trust —Health Sciences Trust JEHSX Science & Technology Trust JESTXHigh Yield Trust — Select Bond Trust (formerly Bond Trust) —International Equity Index Trust (formerly International Equity

Index Trust B)JIEQX Short Term Government Income Trust —

International Growth Stock Trust — Small Cap Index Trust JESIXInternational Small Company Trust — Small Cap Opportunities Trust —International Value Trust — Small Cap Stock Trust (formerly Small Cap Growth Trust) JESGXInvestment Quality Bond Trust — Small Cap Value Trust JESVXLifecycle 2010 Trust — Small Company Value Trust —Lifecycle 2015 Trust — Strategic Equity Allocation Trust —Lifecycle 2020 Trust — Strategic Income Opportunities Trust JESNXLifecycle 2025 Trust — Total Bond Market Trust (formerly Total Bond Market Trust B) JTBMXLifecycle 2030 Trust — Total Stock Market Index Trust JETSXLifecycle 2035 Trust — Ultra Short Term Bond Trust JUSAXLifecycle 2040 Trust — Utilities Trust JEUTXLifecycle 2045 Trust —

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of thesesecurities or passed upon the adequacy of this Prospectus. Any representation to the contrary is a criminal offense. No person, including anydealer or salesperson, has been authorized to give any information or to make any representations, unless the information orrepresentation is set forth in this Prospectus. If any such unauthorized information or representation is given, it should not be relied uponas having been authorized by JHVIT, the advisor or any subadvisors to JHVIT or the principal underwriter of the shares. This Prospectus isnot an offer to sell shares of JHVIT in any state where such offer or sale would be prohibited.

Prospectus dated April 30, 2018

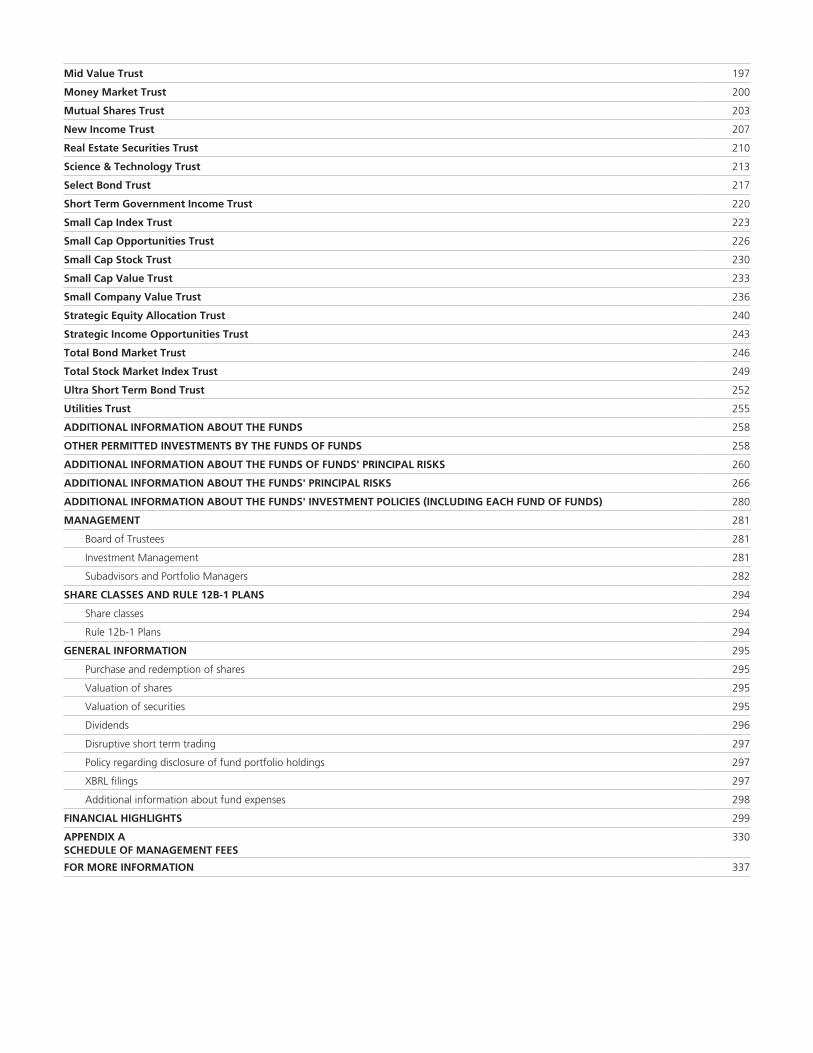

John Hancock Variable Insurance TrustTable of contents500 Index Trust

Active Bond Trust

American Asset Allocation Trust

American Global Growth Trust

American Growth Trust

American Growth-Income Trust

American International Trust

Blue Chip Growth Trust

Capital Appreciation Trust

Capital Appreciation Value Trust

Core Bond Trust

Emerging Markets Value Trust

Equity Income Trust

Financial Industries Trust

Fundamental All Cap Core Trust

Fundamental Large Cap Value Trust

Global Trust

Global Bond Trust

Health Sciences Trust

High Yield Trust

International Equity Index Trust

International Growth Stock Trust

International Small Company Trust

International Value Trust

Investment Quality Bond Trust

Lifecycle 2010 Trust

Lifecycle 2015 Trust

Lifecycle 2020 Trust

Lifecycle 2025 Trust

Lifecycle 2030 Trust

Lifecycle 2035 Trust

Lifecycle 2040 Trust

Lifecycle 2045 Trust

Lifecycle 2050 Trust

Lifestyle Aggressive Portfolio

Lifestyle Balanced Portfolio

Lifestyle Conservative Portfolio

Lifestyle Growth Portfolio

Lifestyle Moderate Portfolio

Managed Volatility Aggressive Portfolio

Managed Volatility Balanced Portfolio

Managed Volatility Conservative Portfolio

Managed Volatility Growth Portfolio

Managed Volatility Moderate Portfolio

Mid Cap Index Trust

Mid Cap Stock Trust

1

1

4

8

11

14

17

20

23

27

31

35

38

42

46

50

53

56

59

63

66

69

72

75

79

82

86

91

96

101

106

111

116

121

126

131

136

141

146

151

156

163

170

177

184

191

194

Mid Value Trust

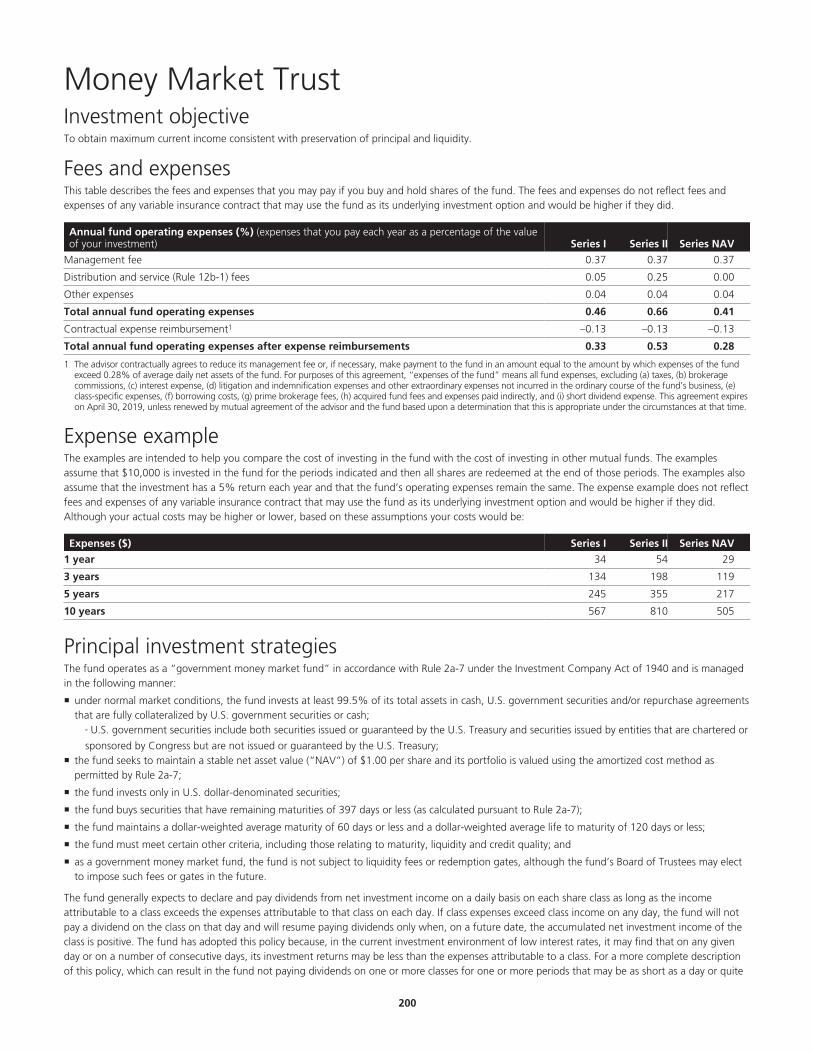

Money Market Trust

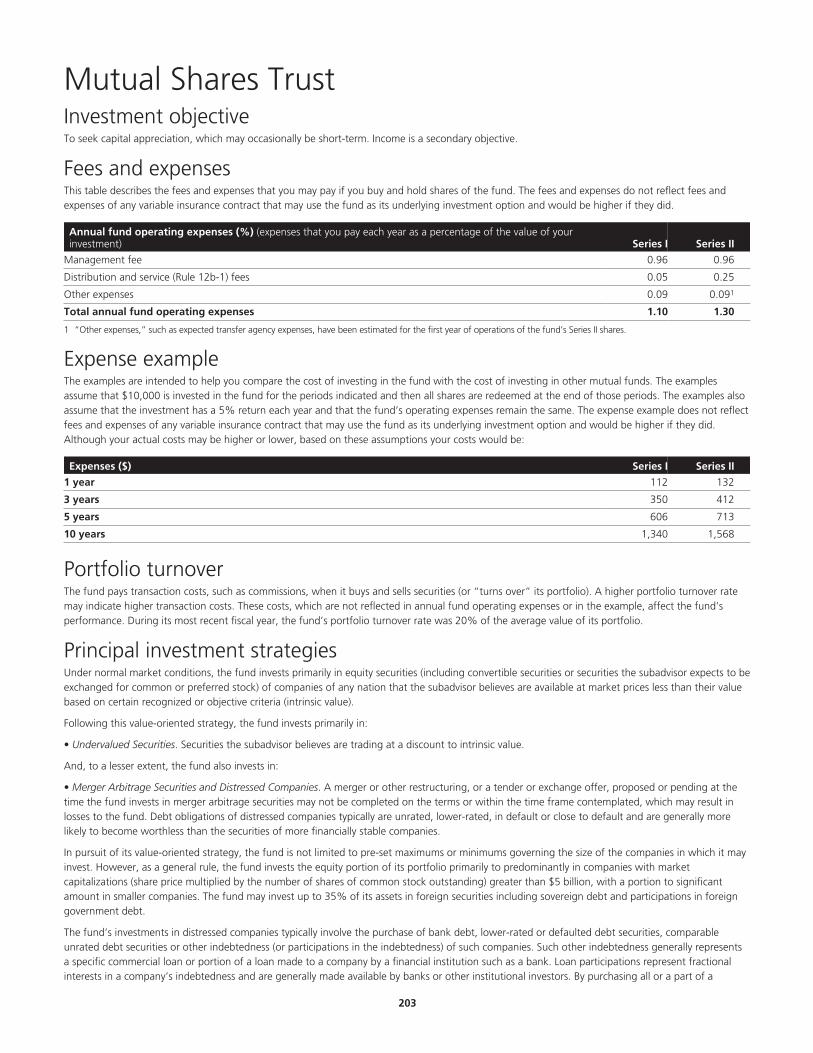

Mutual Shares Trust

New Income Trust

Real Estate Securities Trust

Science & Technology Trust

Select Bond Trust

Short Term Government Income Trust

Small Cap Index Trust

Small Cap Opportunities Trust

Small Cap Stock Trust

Small Cap Value Trust

Small Company Value Trust

Strategic Equity Allocation Trust

Strategic Income Opportunities Trust

Total Bond Market Trust

Total Stock Market Index Trust

Ultra Short Term Bond Trust

Utilities Trust

ADDITIONAL INFORMATION ABOUT THE FUNDS

OTHER PERMITTED INVESTMENTS BY THE FUNDS OF FUNDS

ADDITIONAL INFORMATION ABOUT THE FUNDS OF FUNDS' PRINCIPAL RISKS

ADDITIONAL INFORMATION ABOUT THE FUNDS' PRINCIPAL RISKS

ADDITIONAL INFORMATION ABOUT THE FUNDS' INVESTMENT POLICIES (INCLUDING EACH FUND OF FUNDS)

MANAGEMENT

Board of Trustees

Investment Management

Subadvisors and Portfolio Managers

SHARE CLASSES AND RULE 12B-1 PLANS

Share classes

Rule 12b-1 Plans

GENERAL INFORMATION

Purchase and redemption of shares

Valuation of shares

Valuation of securities

Dividends

Disruptive short term trading

Policy regarding disclosure of fund portfolio holdings

XBRL filings

Additional information about fund expenses

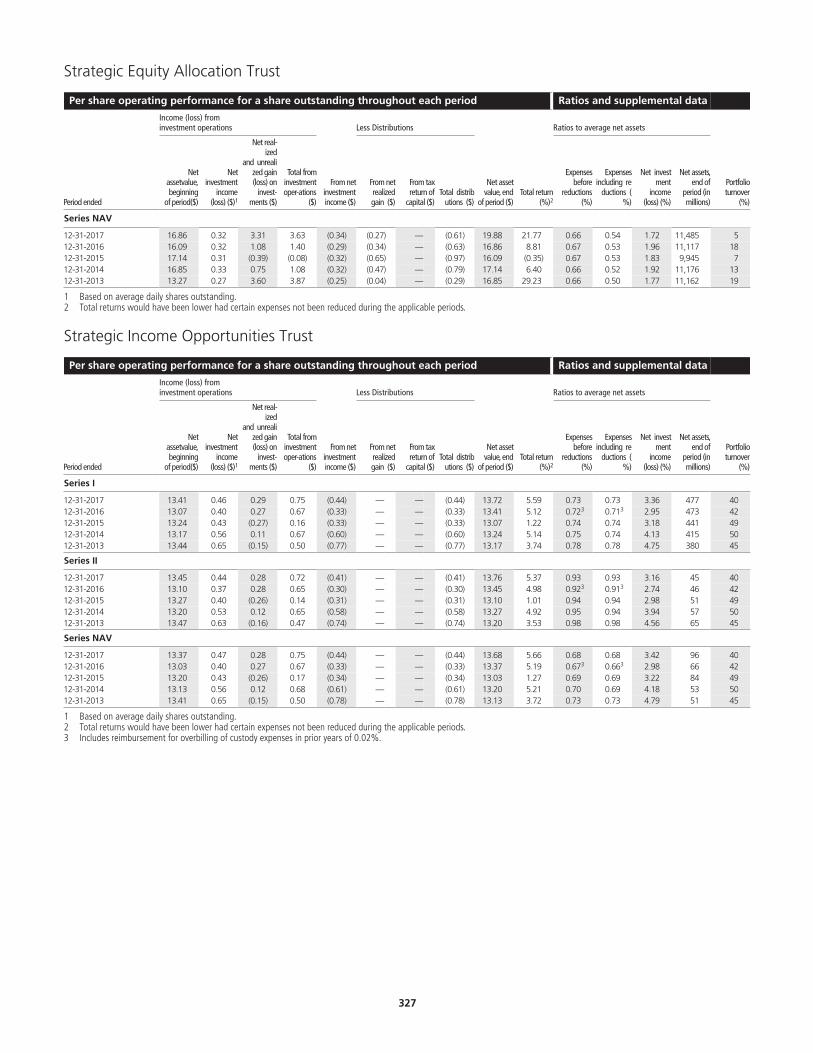

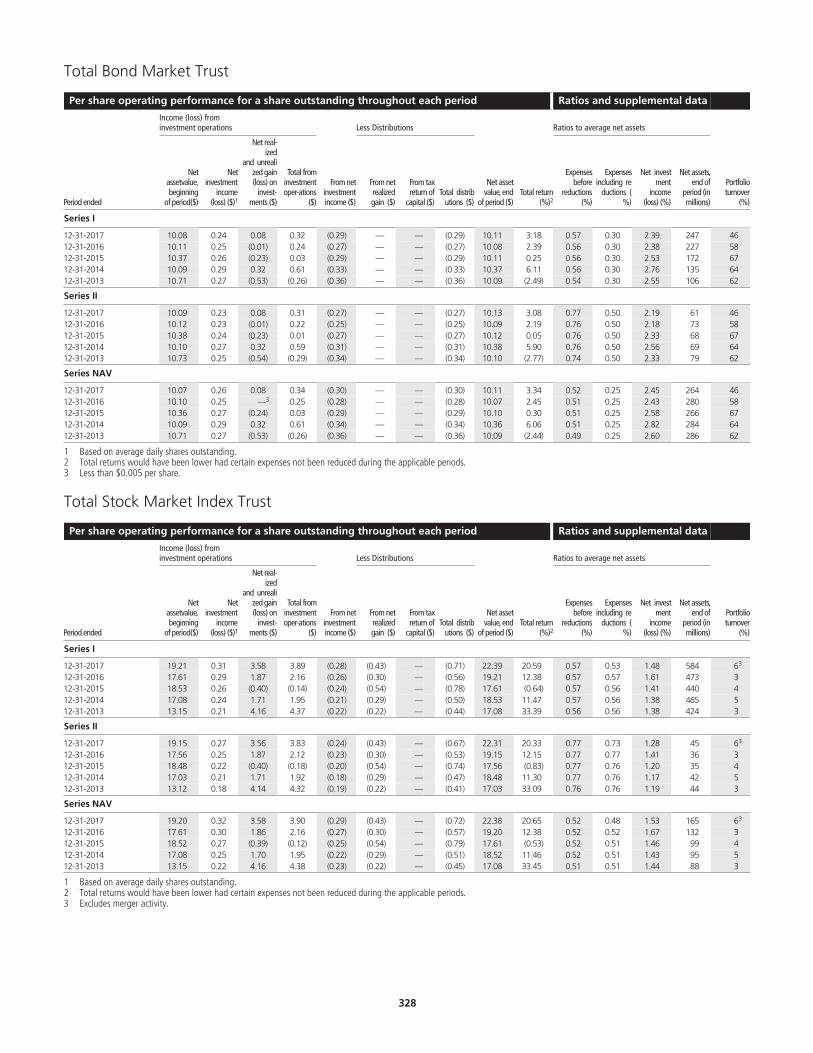

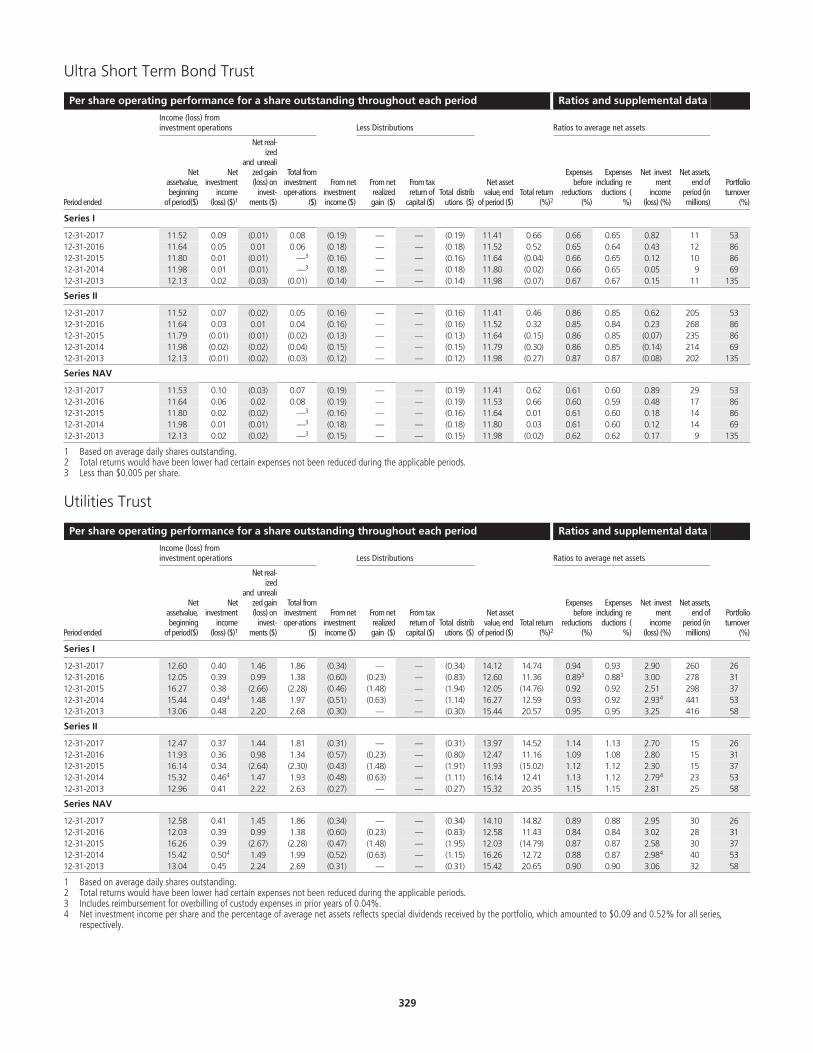

FINANCIAL HIGHLIGHTS

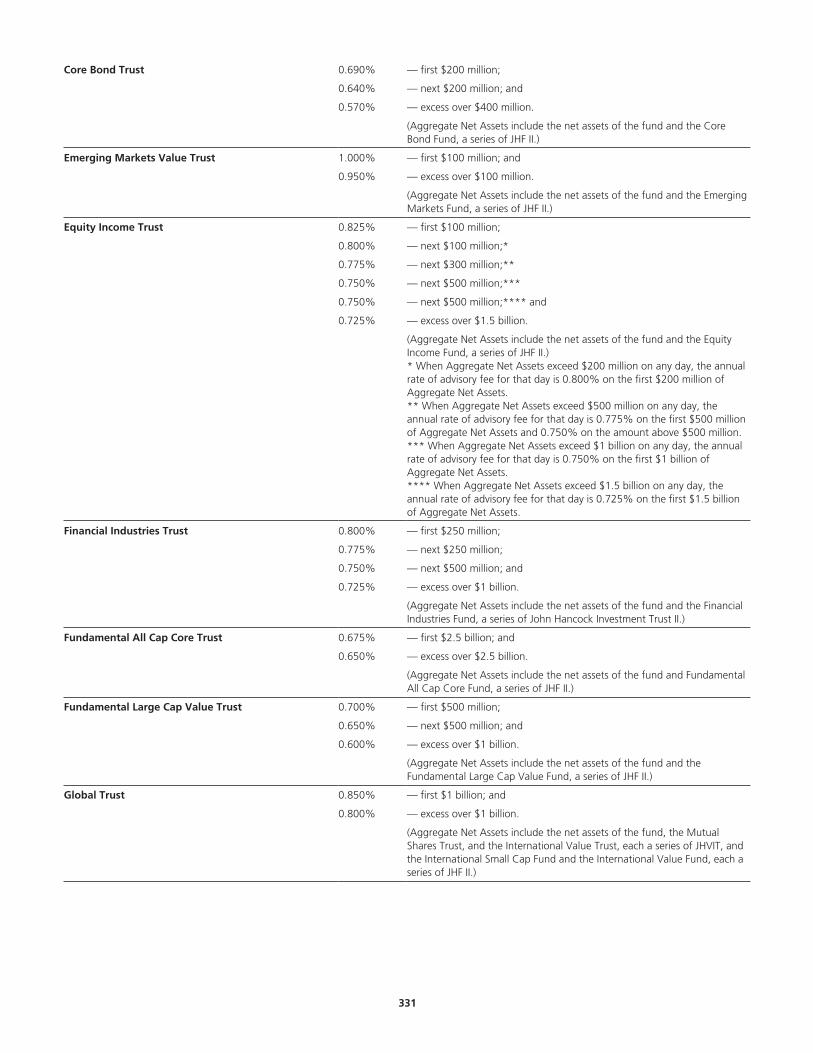

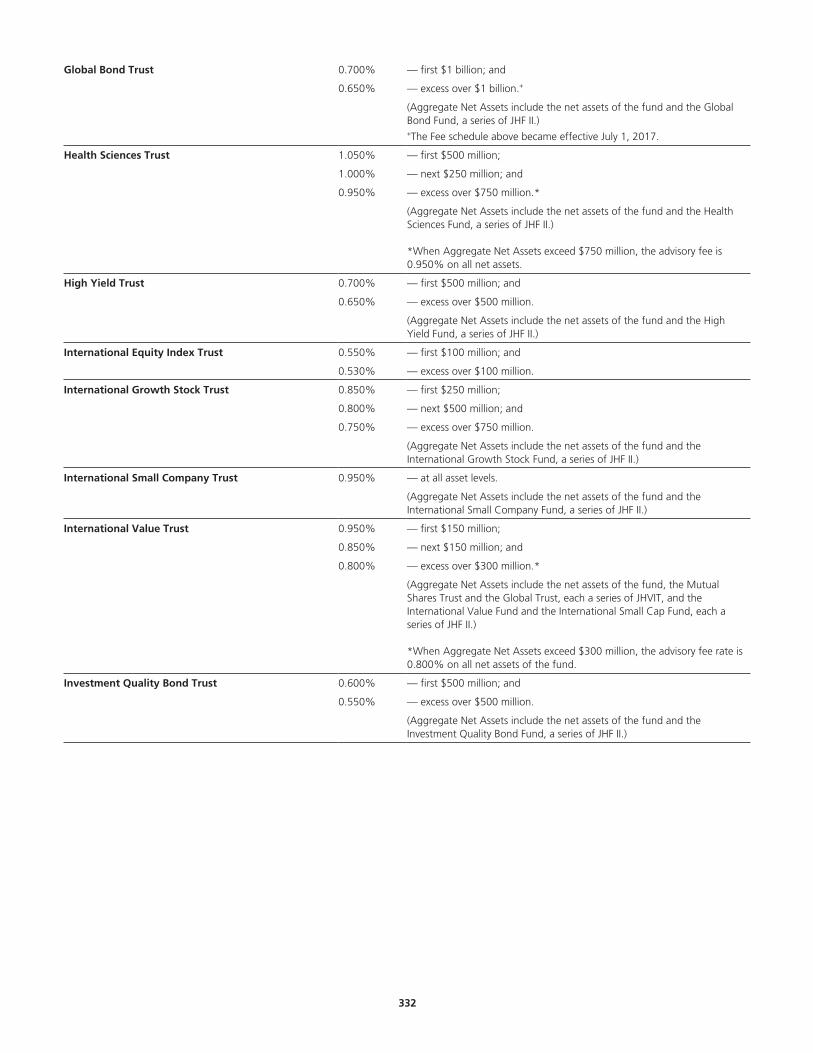

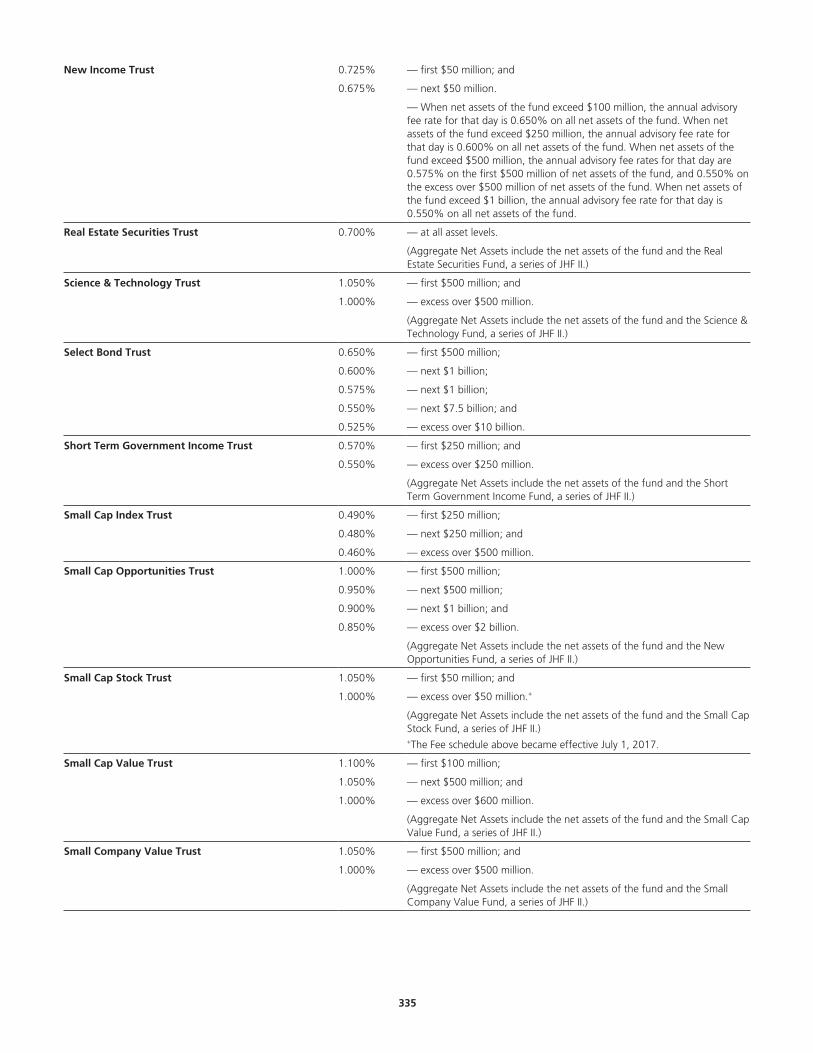

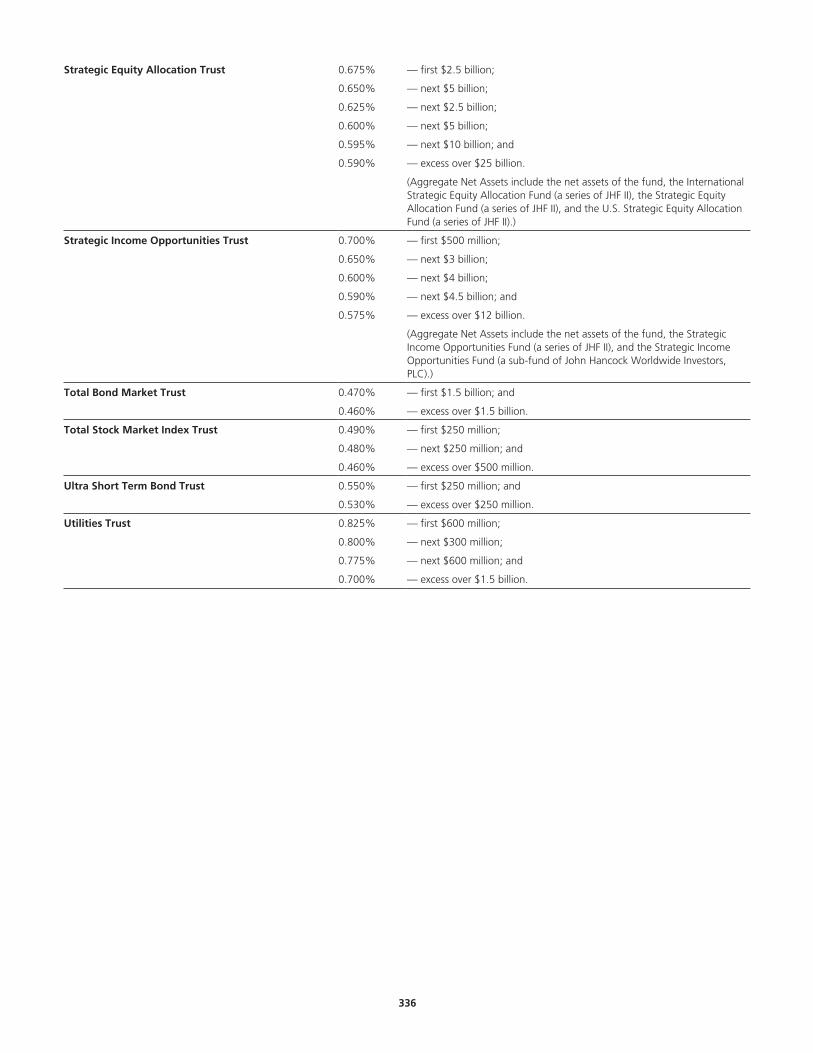

APPENDIX ASCHEDULE OF MANAGEMENT FEES

FOR MORE INFORMATION

2

197

200

203

207

210

213

217

220

223

226

230

233

236

240

243

246

249

252

255

258

258

260

266

280

281

281

281

282

294

294

294

295

295

295

295

296

297

297

297

298

299

330

337

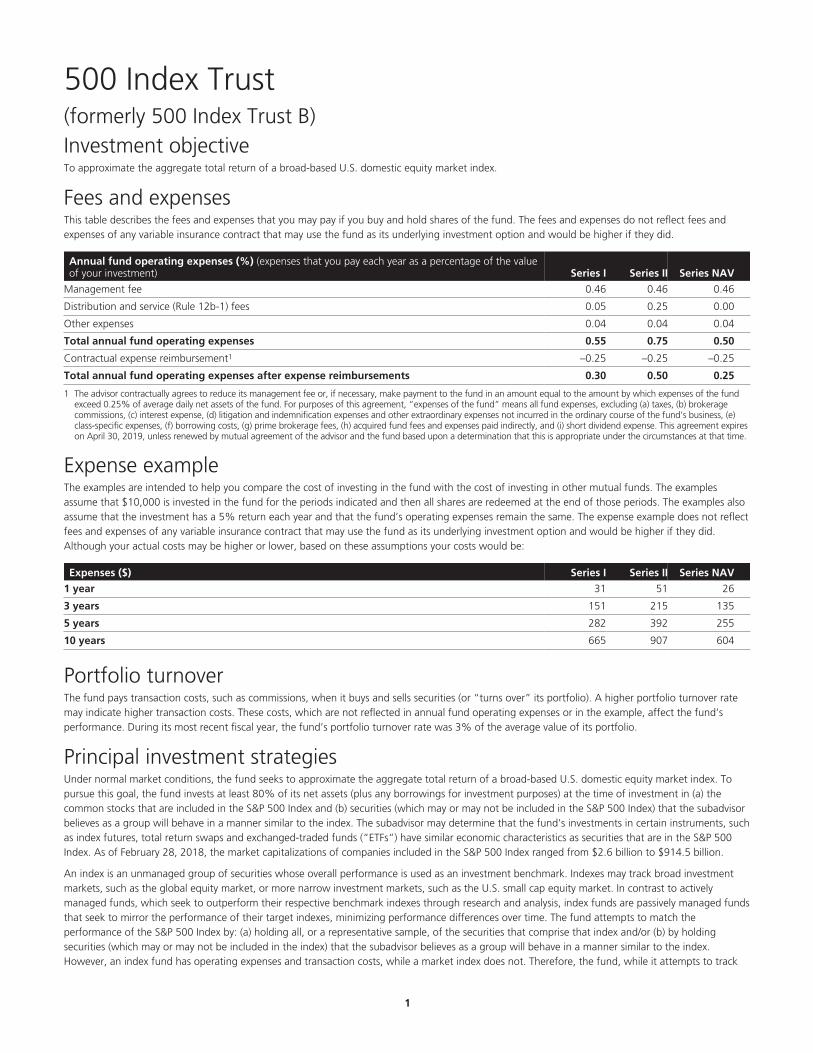

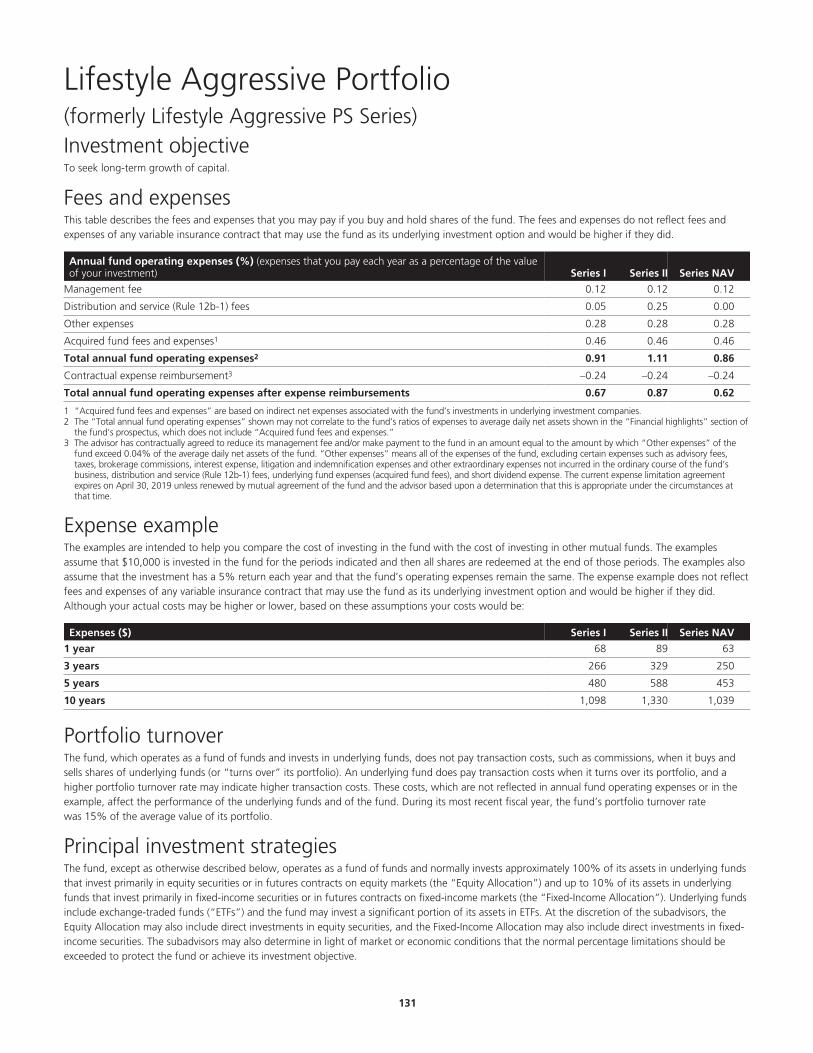

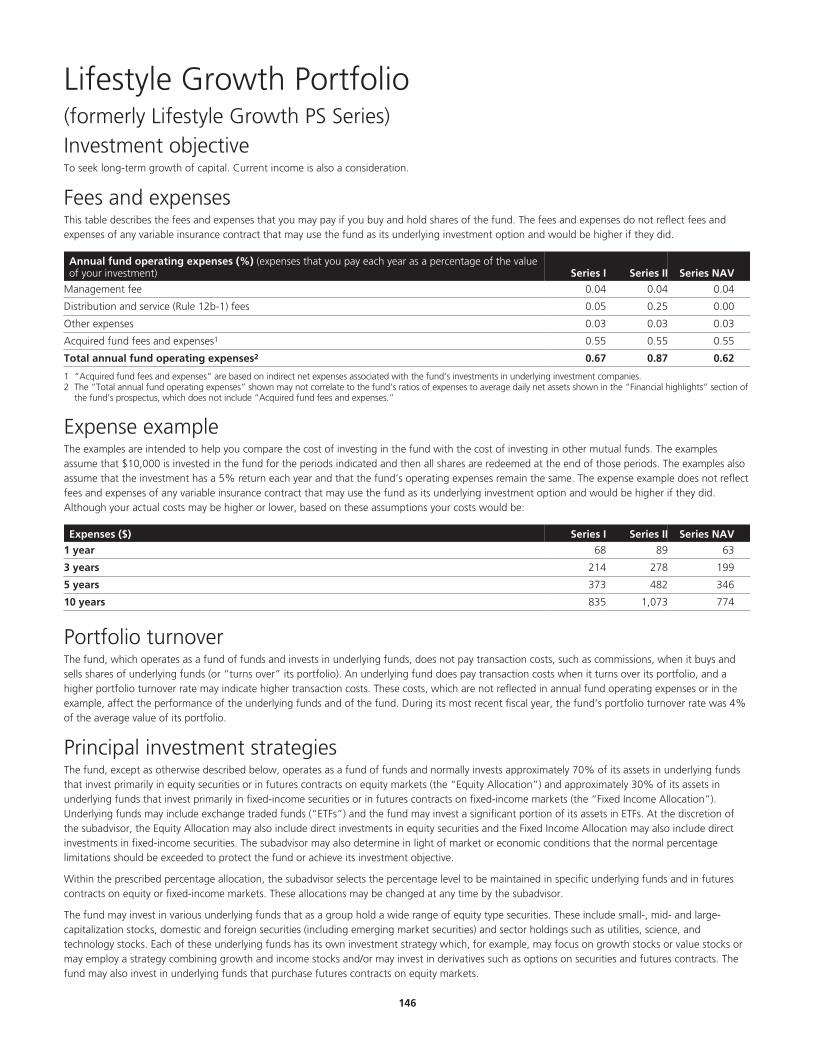

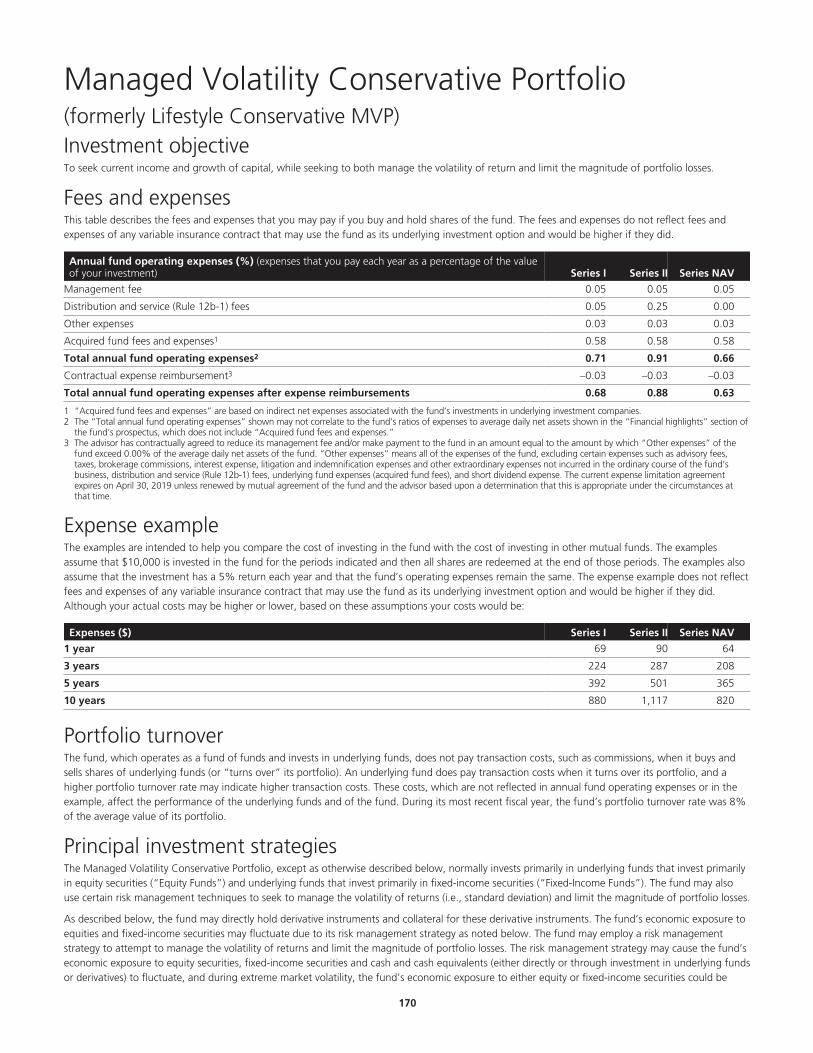

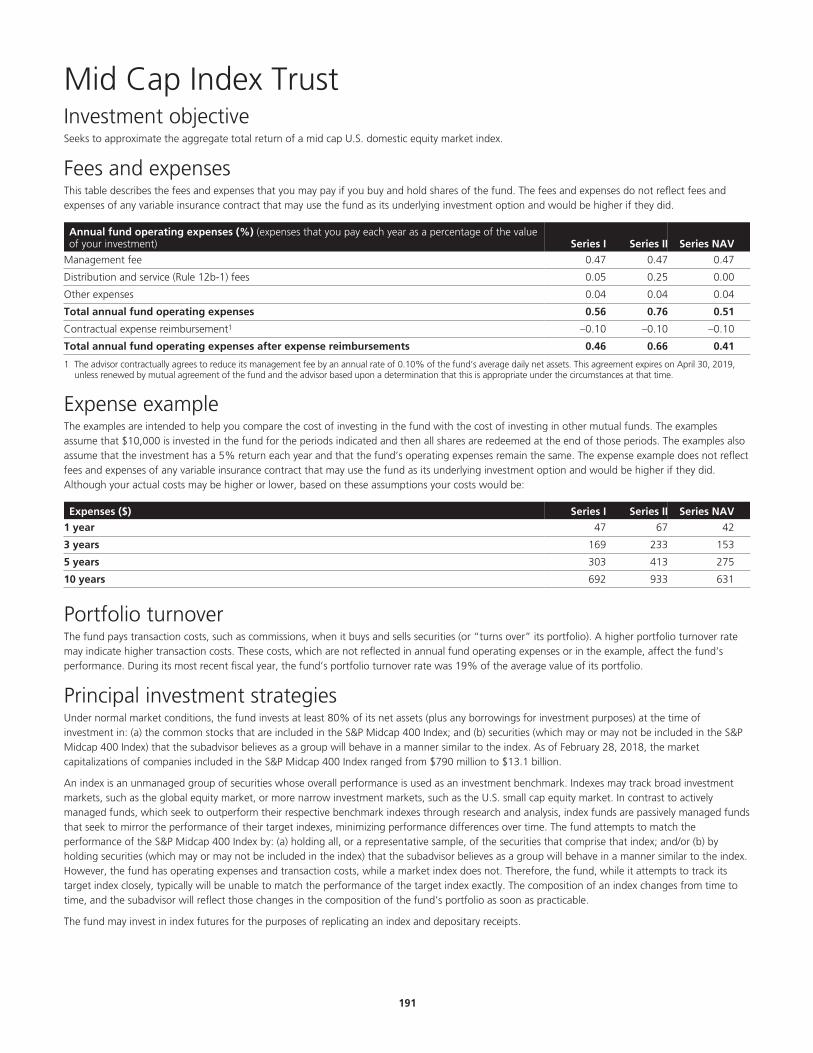

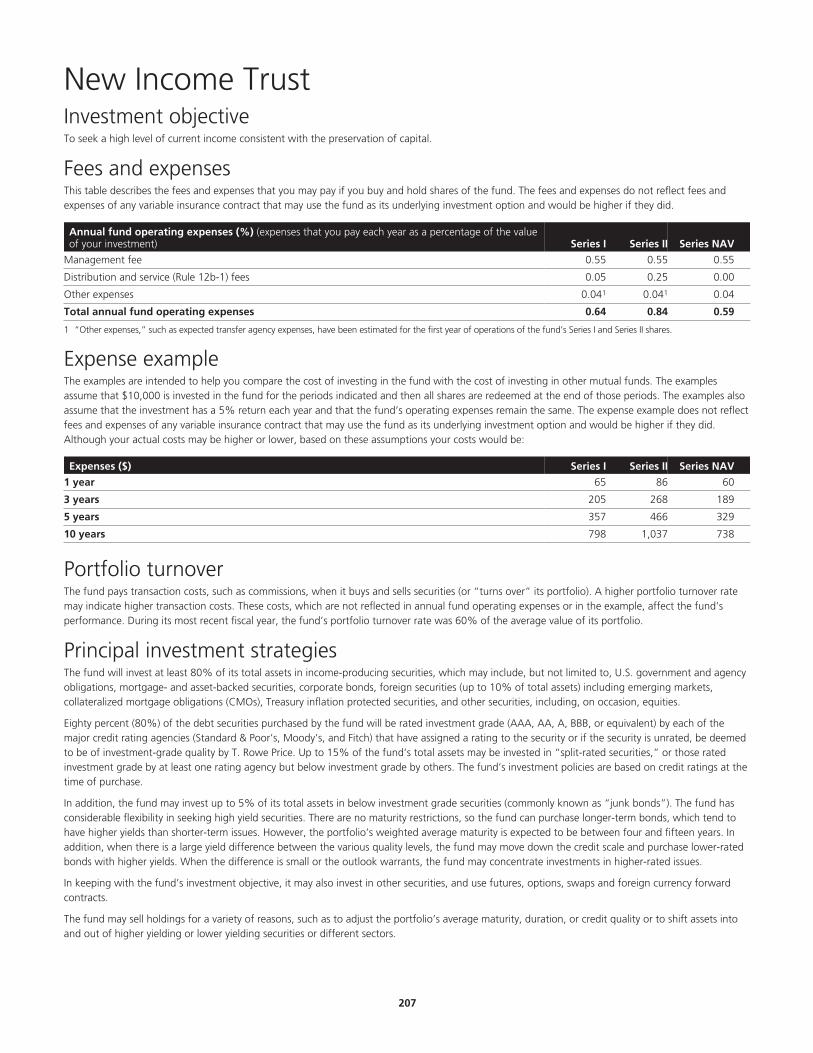

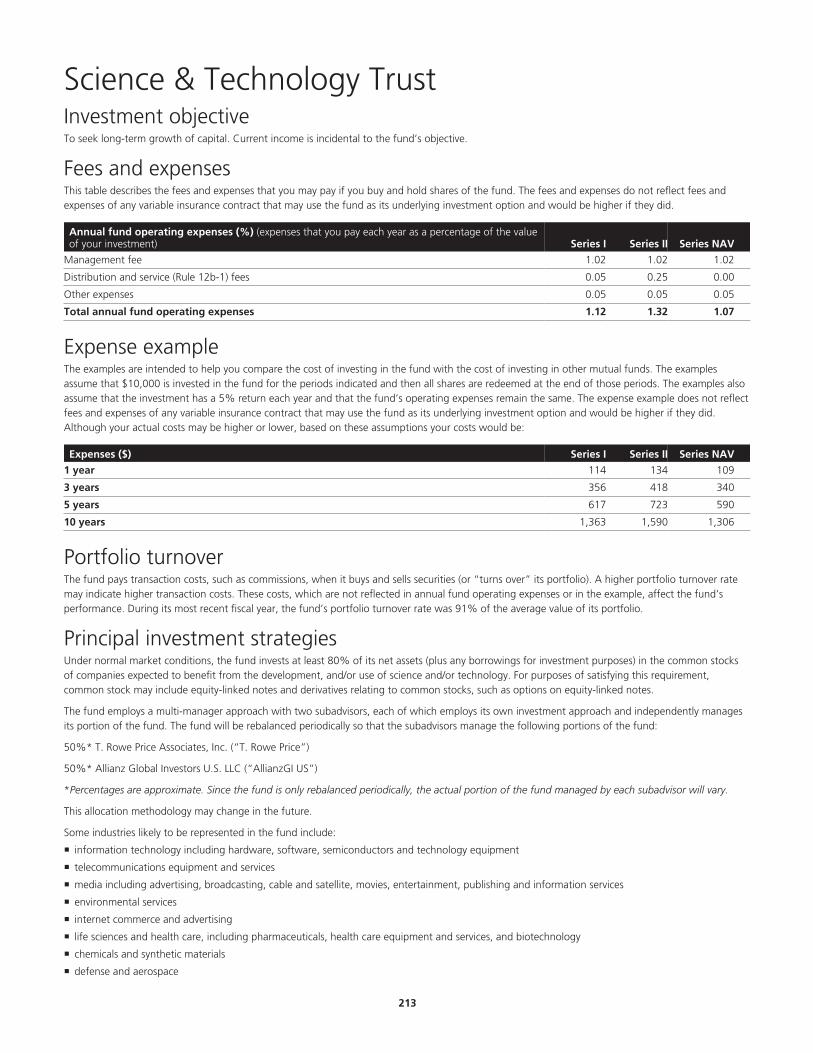

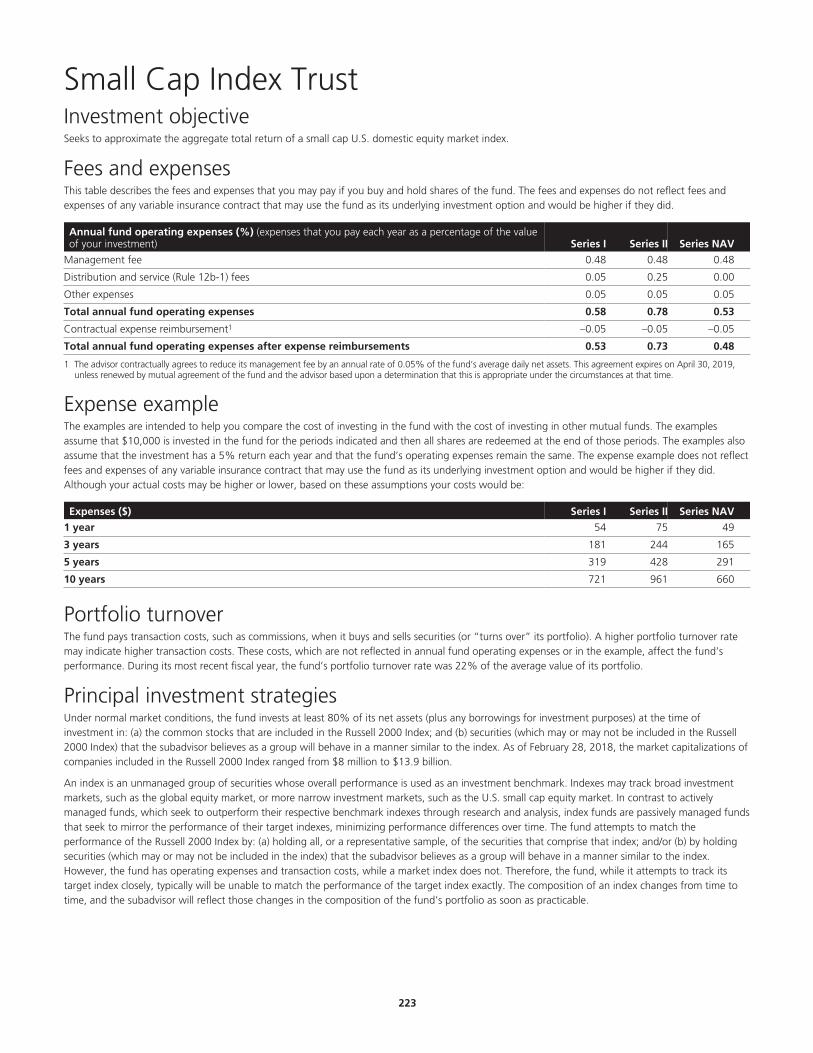

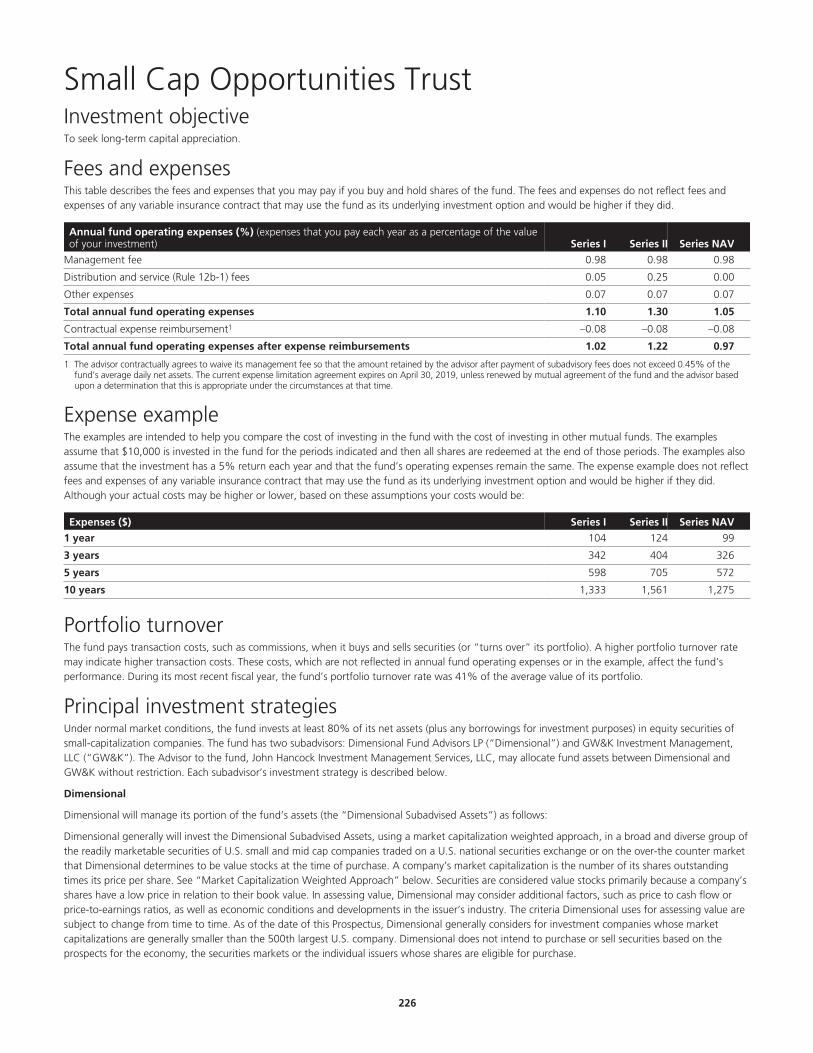

500 Index Trust (formerly 500 Index Trust B)Investment objectiveTo approximate the aggregate total return of a broad-based U.S. domestic equity market index.

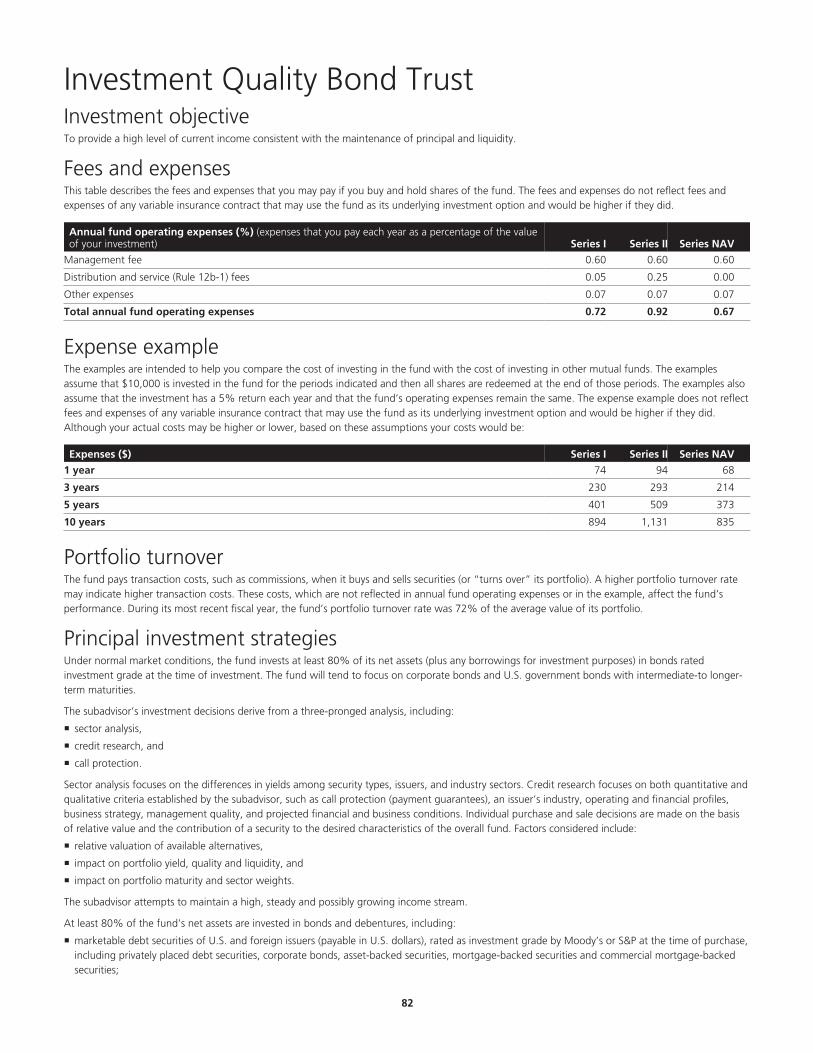

Fees and expensesThis table describes the fees and expenses that you may pay if you buy and hold shares of the fund. The fees and expenses do not reflect fees andexpenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.

Annual fund operating expenses (%) (expenses that you pay each year as a percentage of the valueof your investment) Series I Series II Series NAV

Management fee 0.46 0.46 0.46

Distribution and service (Rule 12b-1) fees 0.05 0.25 0.00

Other expenses 0.04 0.04 0.04

Total annual fund operating expenses 0.55 0.75 0.50

Contractual expense reimbursement1 –0.25 –0.25 –0.25

Total annual fund operating expenses after expense reimbursements 0.30 0.50 0.25

1 The advisor contractually agrees to reduce its management fee or, if necessary, make payment to the fund in an amount equal to the amount by which expenses of the fundexceed 0.25% of average daily net assets of the fund. For purposes of this agreement, “expenses of the fund” means all fund expenses, excluding (a) taxes, (b) brokeragecommissions, (c) interest expense, (d) litigation and indemnification expenses and other extraordinary expenses not incurred in the ordinary course of the fund’s business, (e)class-specific expenses, (f) borrowing costs, (g) prime brokerage fees, (h) acquired fund fees and expenses paid indirectly, and (i) short dividend expense. This agreement expireson April 30, 2019, unless renewed by mutual agreement of the advisor and the fund based upon a determination that this is appropriate under the circumstances at that time.

Expense exampleThe examples are intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The examplesassume that $10,000 is invested in the fund for the periods indicated and then all shares are redeemed at the end of those periods. The examples alsoassume that the investment has a 5% return each year and that the fund’s operating expenses remain the same. The expense example does not reflectfees and expenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Expenses ($) Series I Series II Series NAV

1 year 31 51 26

3 years 151 215 135

5 years 282 392 255

10 years 665 907 604

Portfolio turnoverThe fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover ratemay indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect the fund’sperformance. During its most recent fiscal year, the fund’s portfolio turnover rate was 3% of the average value of its portfolio.

Principal investment strategiesUnder normal market conditions, the fund seeks to approximate the aggregate total return of a broad-based U.S. domestic equity market index. Topursue this goal, the fund invests at least 80% of its net assets (plus any borrowings for investment purposes) at the time of investment in (a) thecommon stocks that are included in the S&P 500 Index and (b) securities (which may or may not be included in the S&P 500 Index) that the subadvisorbelieves as a group will behave in a manner similar to the index. The subadvisor may determine that the fund’s investments in certain instruments, suchas index futures, total return swaps and exchanged-traded funds (“ETFs”) have similar economic characteristics as securities that are in the S&P 500Index. As of February 28, 2018, the market capitalizations of companies included in the S&P 500 Index ranged from $2.6 billion to $914.5 billion.

An index is an unmanaged group of securities whose overall performance is used as an investment benchmark. Indexes may track broad investmentmarkets, such as the global equity market, or more narrow investment markets, such as the U.S. small cap equity market. In contrast to activelymanaged funds, which seek to outperform their respective benchmark indexes through research and analysis, index funds are passively managed fundsthat seek to mirror the performance of their target indexes, minimizing performance differences over time. The fund attempts to match theperformance of the S&P 500 Index by: (a) holding all, or a representative sample, of the securities that comprise that index and/or (b) by holdingsecurities (which may or may not be included in the index) that the subadvisor believes as a group will behave in a manner similar to the index.However, an index fund has operating expenses and transaction costs, while a market index does not. Therefore, the fund, while it attempts to track

.1

its target index closely, typically will be unable to match the performance of the index exactly. The composition of an index changes from time to time,and the subadvisor will reflect those changes in the composition of the fund’s portfolio as soon as practicable.

Use of Hedging and Other Strategic Transactions. The fund may invest in futures contracts, swaps, and depositary receipts. The fund may invest inderivatives (investments whose value is based on securities, indexes or currencies).

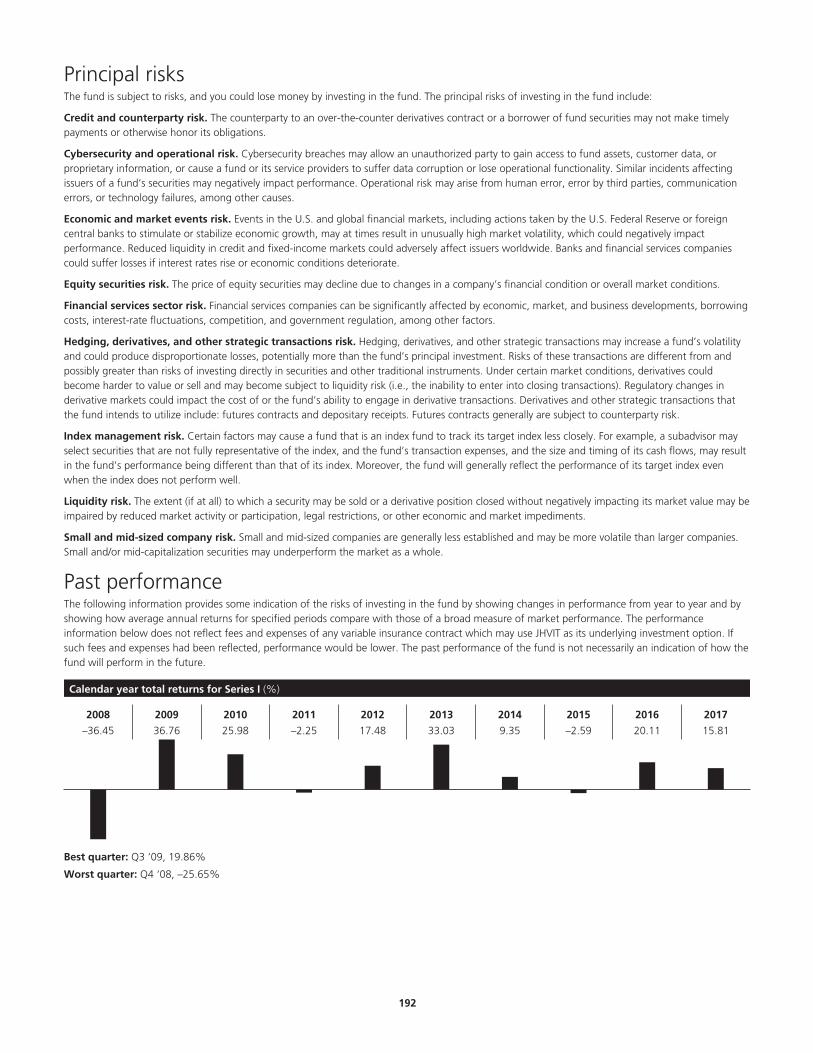

Principal risksThe fund is subject to risks, and you could lose money by investing in the fund. The principal risks of investing in the fund include:

Credit and counterparty risk. The counterparty to an over-the-counter derivatives contract or a borrower of fund securities may not make timelypayments or otherwise honor its obligations.

Cybersecurity and operational risk. Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, orproprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affectingissuers of a fund’s securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communicationerrors, or technology failures, among other causes.

Economic and market events risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreigncentral banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impactperformance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companiescould suffer losses if interest rates rise or economic conditions deteriorate.

Equity securities risk. The price of equity securities may decline due to changes in a company’s financial condition or overall market conditions.

Exchange-traded funds risk. An ETF generally reflects the risks of the underlying securities it is designed to track. A fund bears ETF fees and expensesindirectly.

Hedging, derivatives, and other strategic transactions risk. Hedging, derivatives, and other strategic transactions may increase a fund’s volatilityand could produce disproportionate losses, potentially more than the fund’s principal investment. Risks of these transactions are different from andpossibly greater than risks of investing directly in securities and other traditional instruments. Under certain market conditions, derivatives couldbecome harder to value or sell and may become subject to liquidity risk (i.e., the inability to enter into closing transactions). Regulatory changes inderivative markets could impact the cost of or the fund’s ability to engage in derivatives transactions. Derivatives and other strategic transactions thatthe fund intends to utilize include: futures contracts, depositary receipts, total return swaps, and swaps. Futures contracts and swaps generally aresubject to counterparty risk. In addition, swaps may be subject to interest-rate and settlement risk, and the risk of default of the underlying referenceobligation.

Index management risk. Certain factors may cause a fund that is an index fund to track its target index less closely. For example, a subadvisor mayselect securities that are not fully representative of the index, and the fund’s transaction expenses, and the size and timing of its cash flows, may resultin the fund’s performance being different than that of its index. Moreover, the fund will generally reflect the performance of its target index evenwhen the index does not perform well.

Liquidity risk. The extent (if at all) to which a security may be sold or a derivative position closed without negatively impacting its market value may beimpaired by reduced market activity or participation, legal restrictions, or other economic and market impediments.

Sector risk. When a fund focuses its investments in certain sectors of the economy, its performance may be driven largely by sector performance andcould fluctuate more widely than if the fund were invested more evenly across sectors.

S&P 500 Index risk An investment in the fund involves risks similar to the risks of investing directly in the equity securities included in the S&P 500Index.

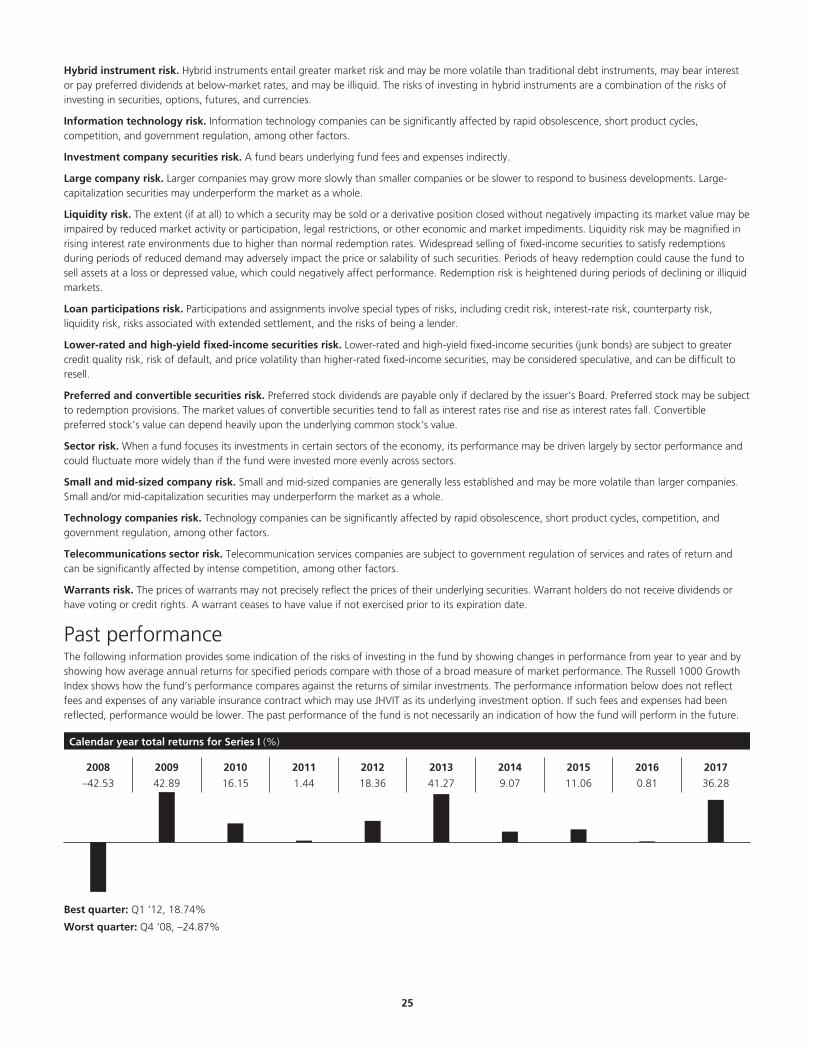

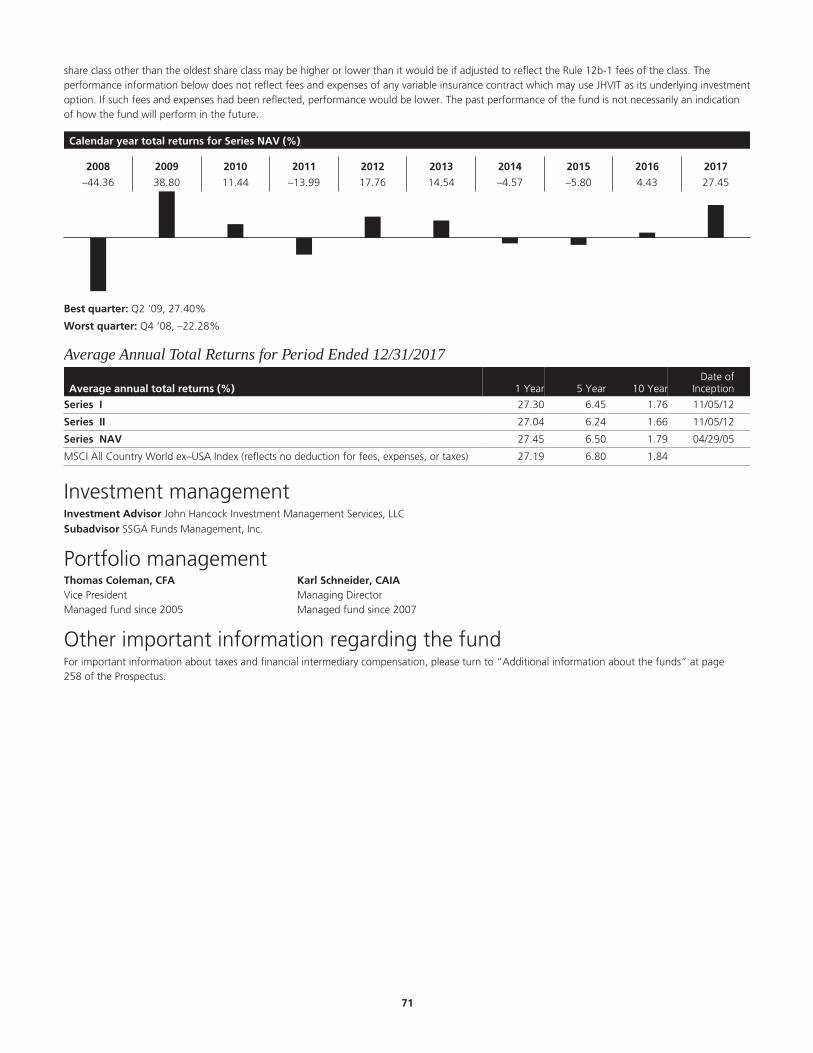

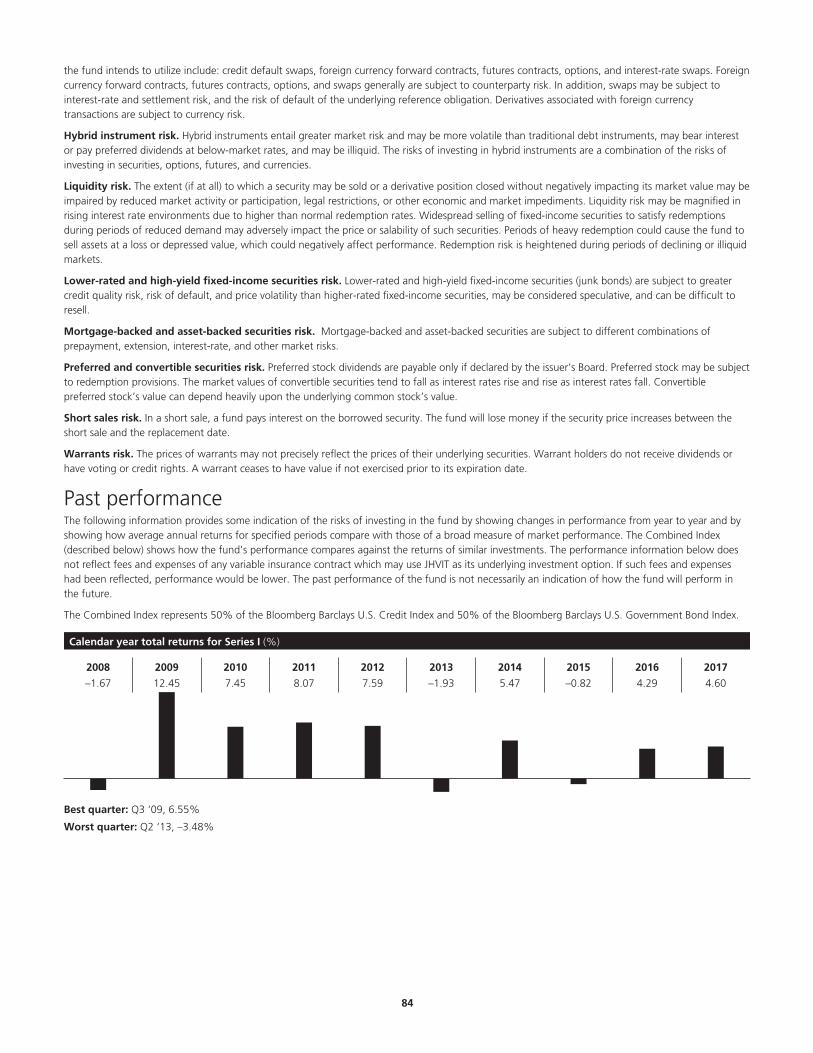

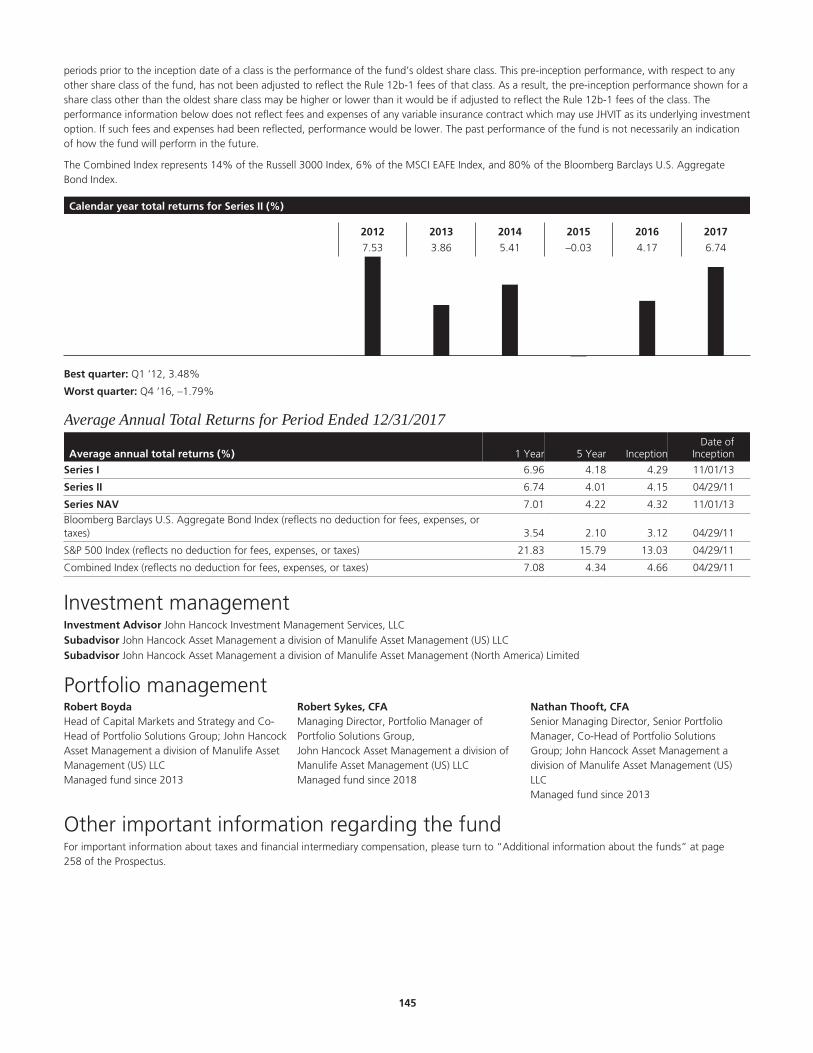

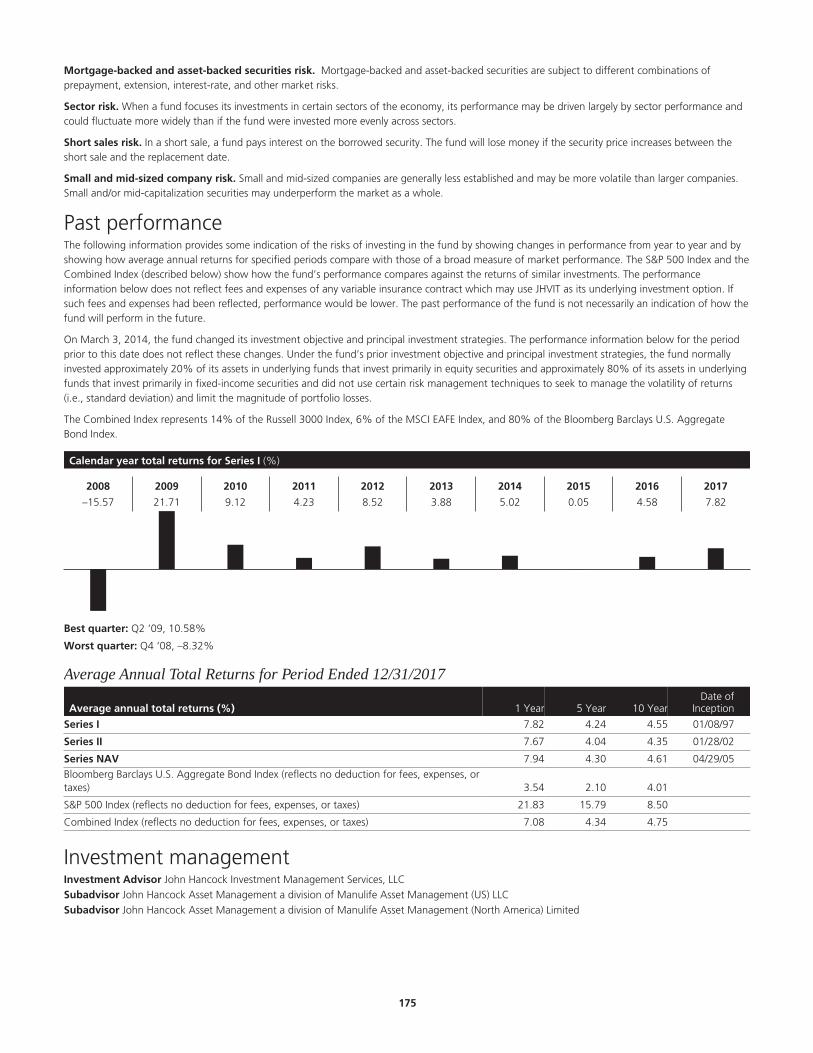

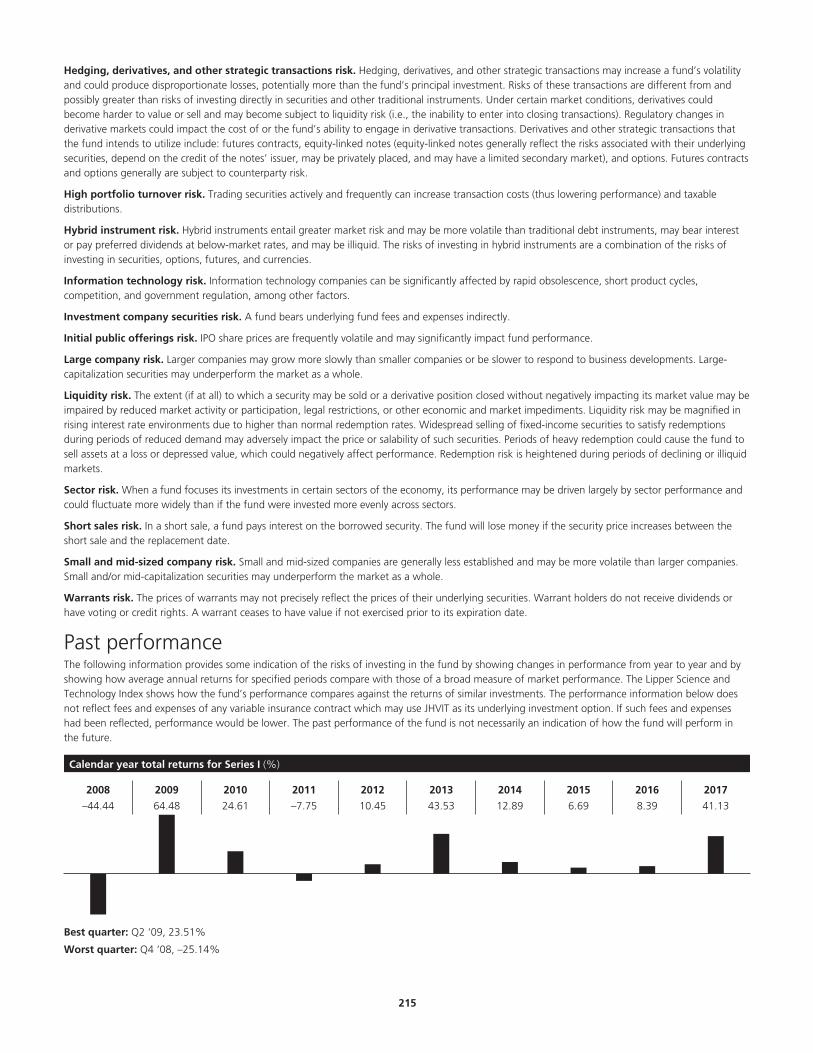

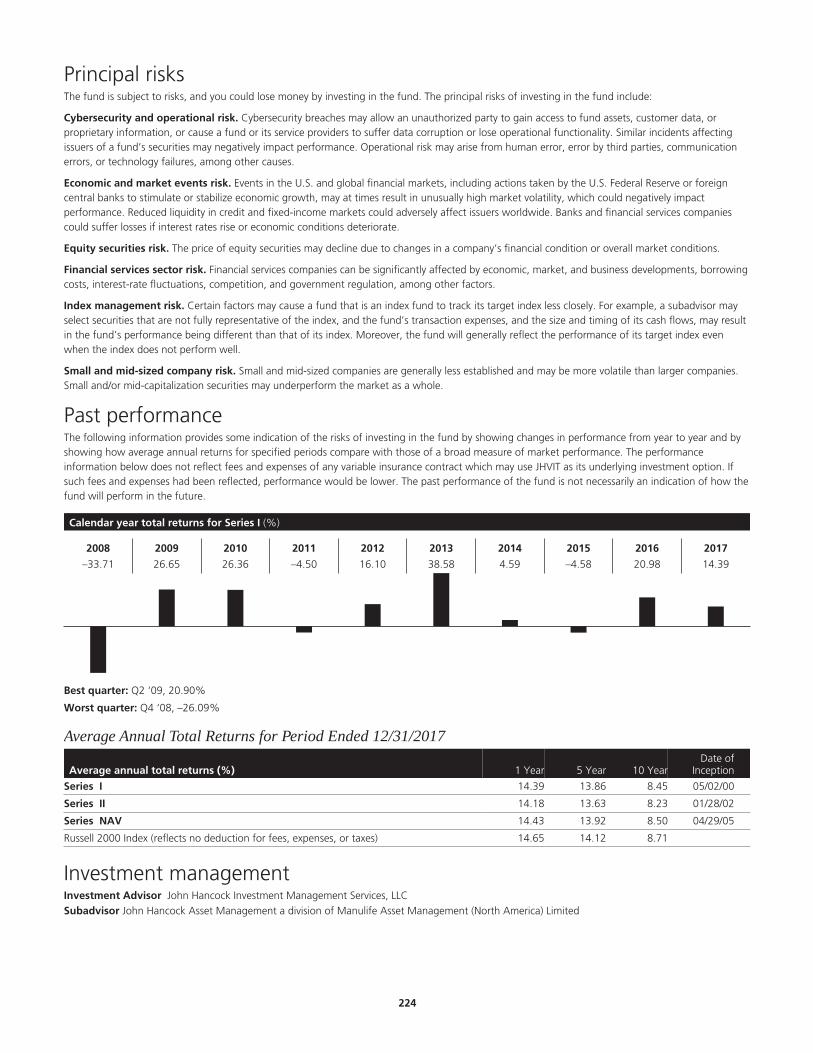

Past performanceThe following information provides some indication of the risks of investing in the fund by showing changes in performance from year to year and byshowing how average annual returns for specified periods compare with those of a broad measure of market performance. Performance shown forperiods prior to the inception date of a class is the performance of the fund’s oldest share class. This pre-inception performance, with respect to anyother share class of the fund, has not been adjusted to reflect the Rule 12b-1 fees of that class. As a result, the pre-inception performance shown for ashare class other than the oldest share class may be higher or lower than it would be if adjusted to reflect the Rule 12b-1 fees of the class. Theperformance information below does not reflect fees and expenses of any variable insurance contract which may use JHVIT as its underlying investmentoption. If such fees and expenses had been reflected, performance would be lower. The past performance of the fund is not necessarily an indicationof how the fund will perform in the future.

.2

Calendar year total returns for Series NAV (%)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

–37.19 26.35 14.86 1.87 15.80 32.03 13.43 1.15 11.64 21.54

Best quarter: Q2 ‘09, 15.85%

Worst quarter: Q4 ‘08, –22.11%

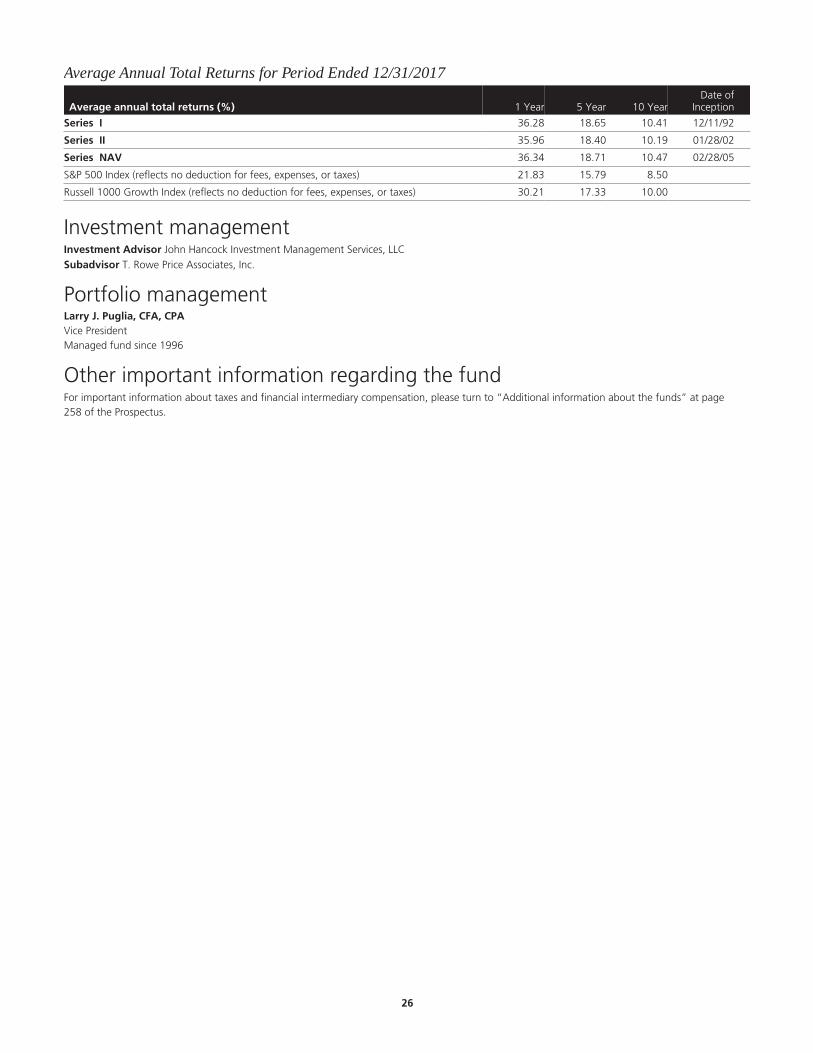

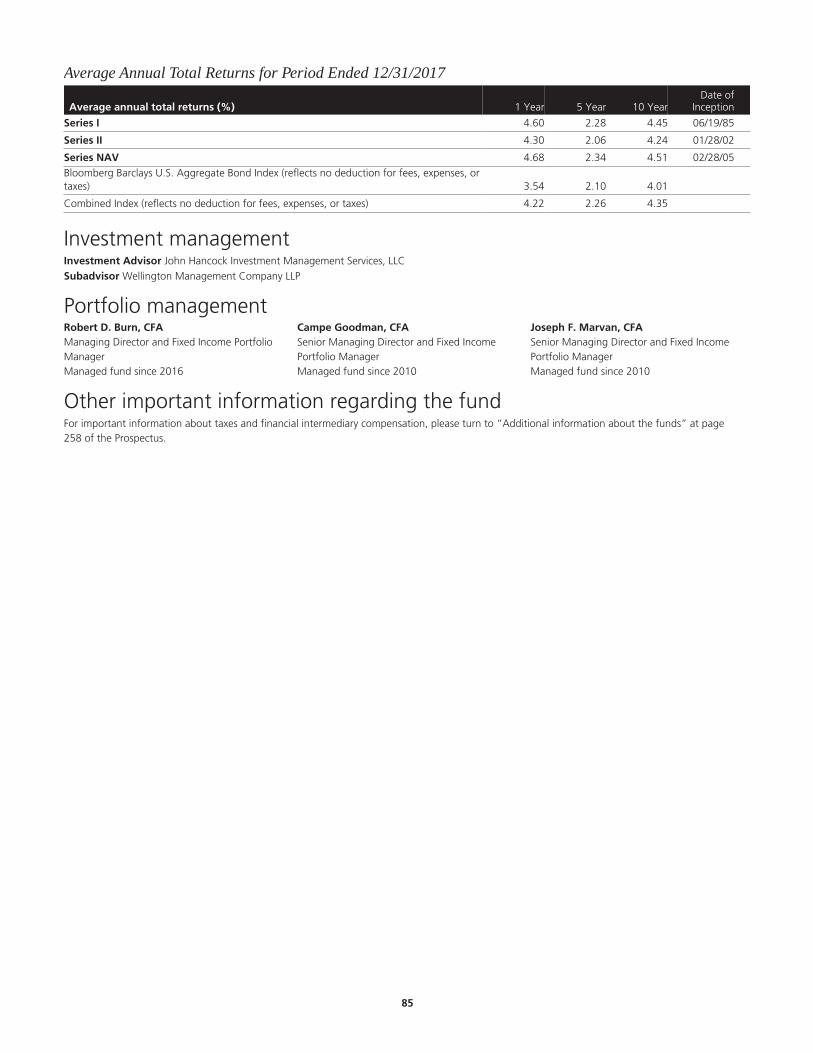

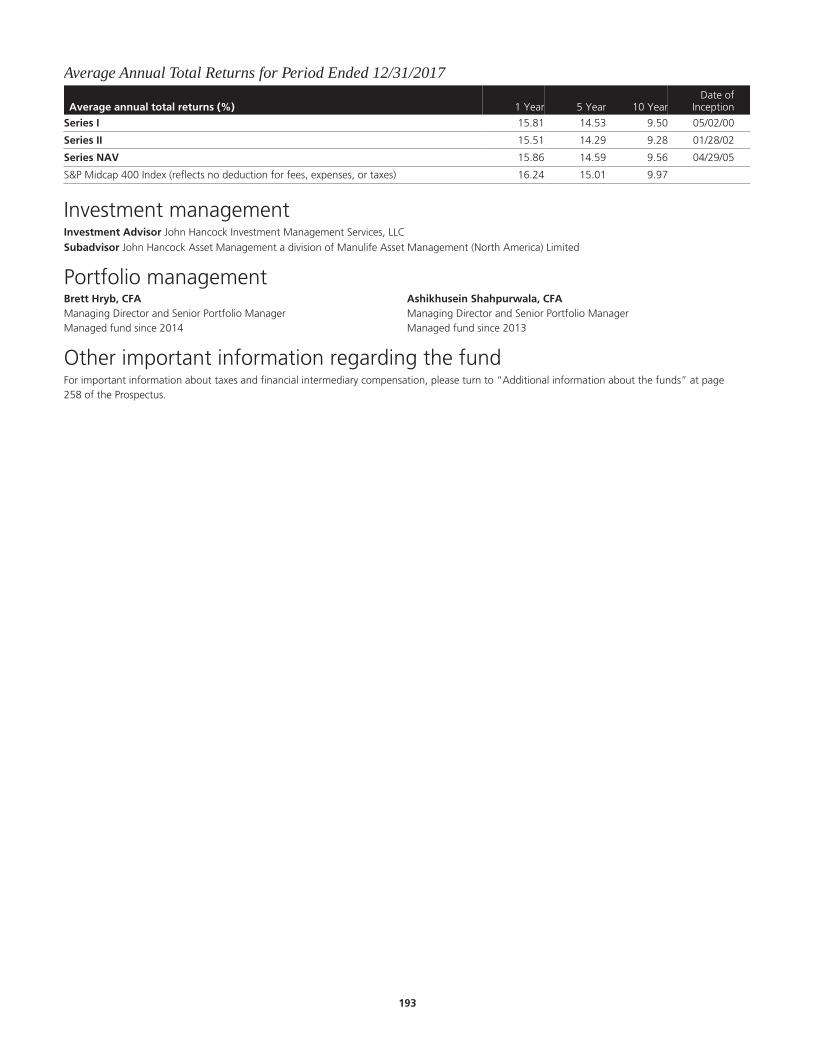

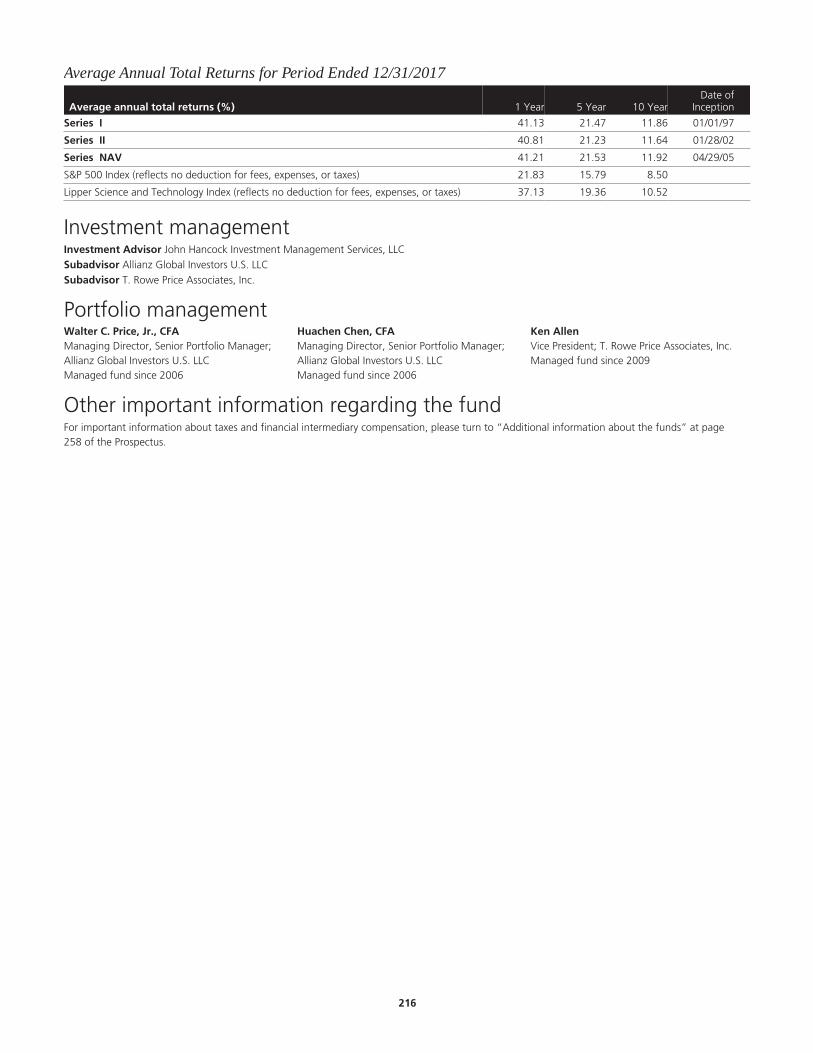

Average Annual Total Returns for Period Ended 12/31/2017

Average annual total returns (%) 1 Year 5 Year 10 YearDate of

Inception

Series I 21.52 15.45 8.23 11/05/12

Series II 21.28 15.23 8.12 11/05/12

Series NAV 21.54 15.50 8.25 05/01/96

S&P 500 Index (reflects no deduction for fees, expenses, or taxes) 21.83 15.79 8.50

Investment managementInvestment Advisor John Hancock Investment Management Services, LLC§

Subadvisor John Hancock Asset Management a division of Manulife Asset Management (North America) Limited

Portfolio managementBrett Hryb, CFAManaging Director and Senior Portfolio ManagerManaged fund since 2014

Ashikhusein Shahpurwala, CFAManaging Director and Senior Portfolio ManagerManaged fund since 2013

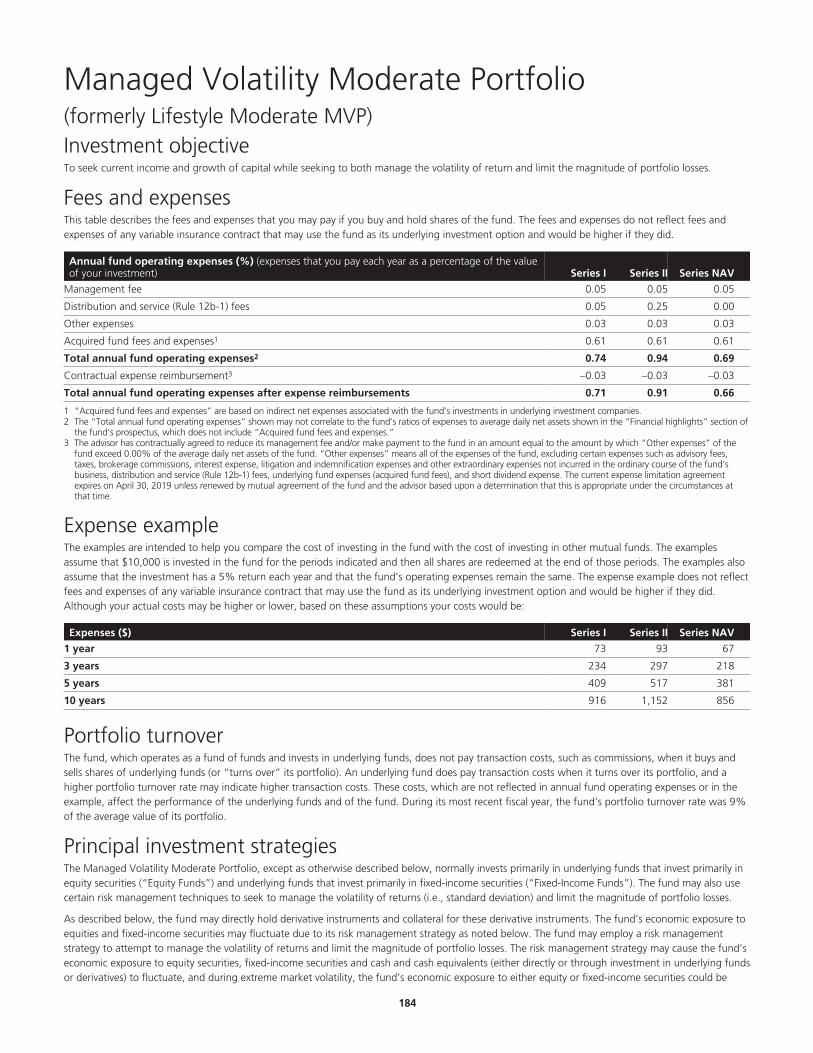

Other important information regarding the fundFor important information about taxes and financial intermediary compensation, please turn to “Additional information about the funds” at page258 of the Prospectus.

.3

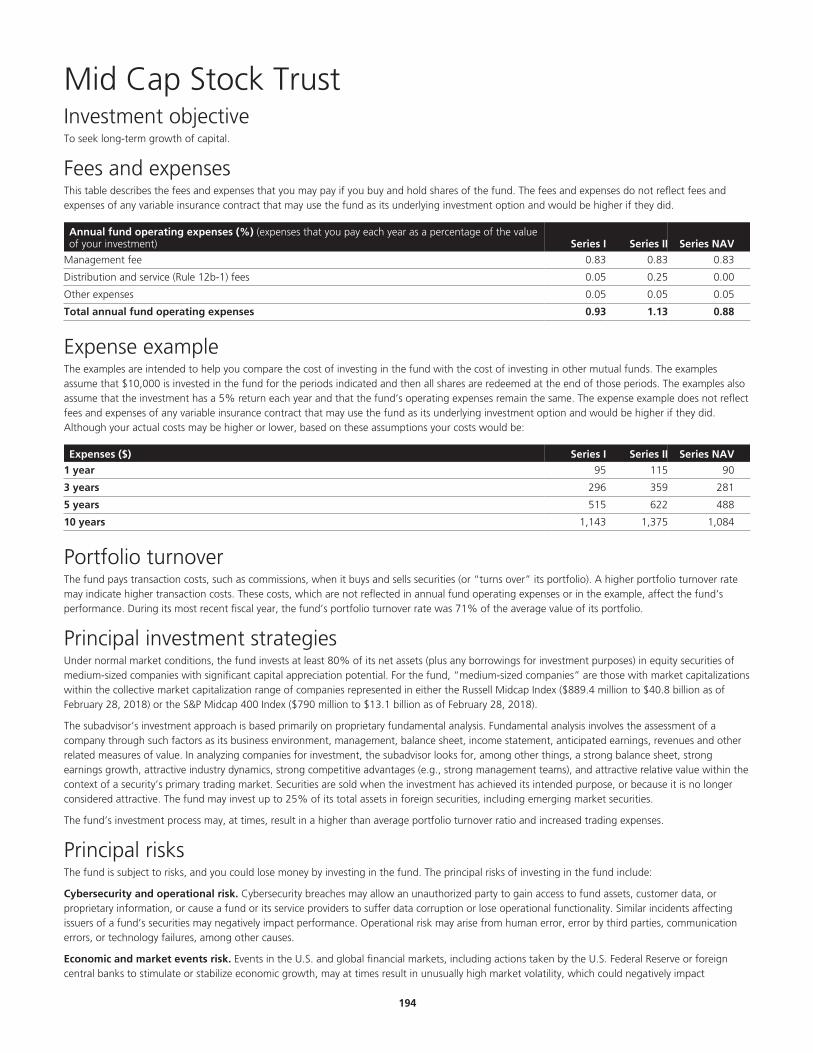

Active Bond Trust Investment objectiveTo seek income and capital appreciation.

Fees and expensesThis table describes the fees and expenses that you may pay if you buy and hold shares of the fund. The fees and expenses do not reflect fees andexpenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.

Annual fund operating expenses (%) (expenses that you pay each year as a percentage of the valueof your investment) Series I Series II Series NAV

Management fee 0.60 0.60 0.60

Distribution and service (Rule 12b-1) fees 0.05 0.25 0.00

Other expenses 0.05 0.05 0.05

Acquired fund fees and expenses1 0.01 0.01 0.01

Total annual fund operating expenses2 0.71 0.91 0.66

1 “Acquired fund fees and expenses” are based on indirect net expenses associated with the fund’s investments in underlying investment companies.2 The “Total annual fund operating expenses” shown may not correlate to the fund’s ratios of expenses to average daily net assets shown in the “Financial highlights” section of

the fund’s prospectus, which does not include “Acquired fund fees and expenses.”

Expense exampleThe examples are intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The examplesassume that $10,000 is invested in the fund for the periods indicated and then all shares are redeemed at the end of those periods. The examples alsoassume that the investment has a 5% return each year and that the fund’s operating expenses remain the same. The expense example does not reflectfees and expenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Expenses ($) Series I Series II Series NAV

1 year 73 93 67

3 years 227 290 211

5 years 395 504 368

10 years 883 1,120 822

Portfolio turnoverThe fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover ratemay indicate higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect the fund’sperformance. During its most recent fiscal year, the fund’s portfolio turnover rate was 86% of the average value of its portfolio.

Principal investment strategiesUnder normal market conditions, the fund invests at least 80% of its net assets (plus any borrowings for investment purposes) in a diversified mix ofdebt securities and instruments. The fund seeks to invest its assets in debt securities and instruments with an average duration of between 4 to 6 years,however, there is no limit on the fund’s average maturity. As part of its investment strategy, the fund may invest in mortgage-backed securities to asignificant extent.

Eligible investments include, but are not limited to:

U.S. Treasury and agency securities;

Asset-backed securities and mortgage-backed securities, both investment grade and below-investment grade, including mortgage pass-throughsecurities, commercial mortgage-backed securities (“CMBS”) and collateralized mortgage obligations (“CMOs”);

Corporate bonds, both U.S. and foreign, and without any limit on credit quality; and

Foreign government and agency securities.

The fund may invest in asset-backed securities rated, at the time of purchase, less than A (but not rated lower than B by Standard & Poor’s RatingsServices (“S&P”) or Moody’s Investors Service (“Moody’s”). The subadvisor uses proprietary research and economic and industry analysis to identifyspecific bonds, bond sectors and industries that are attractively priced. Due to this process, the fund may have a higher than average portfolio turnoverratio, which may increase expenses and affect performance results.

The foreign securities in which the fund invests may be denominated in U.S. dollars or foreign currency.

.4

John Hancock Asset Management manages the fund with two investment teams, each of which employs its own investment approach andindependently manages its portion of the fund. The fund will be rebalanced periodically so that each team manages the following portions of thefund:

50%* Securitized Asset Team

50%* Core / Core Plus Team

*Percentages are approximate. Since the fund is only rebalanced periodically, the actual portion of the fund managed by each team will vary.

This allocation methodology may change in the future.

Securitized Asset Team

The Securitized Asset Team uses a combination of proprietary research and quantitative tools and seeks to identify bonds and bond sectors that areattractively priced based upon market fundamentals and technical factors. The Securitized Asset Team opportunistically emphasizes bonds with yieldsin excess of U.S. Treasury securities.

This portion of the fund normally has no more than 10% of its total assets in high yield bonds (“junk bonds”) and normally invests in foreign securitiesonly if U.S. dollar-denominated. This portion of the fund normally has an average credit rating of “A” or “AA.”

The Core / Core Plus Team

The Core / Core Plus Team uses proprietary research to identify specific bond sectors, industries and bonds that are attractively priced. The team seeksto anticipate shifts in the business cycle, using economic and industry analysis to determine which sectors and industries might benefit over the next 12months.

This portion of the fund normally has no more than 25% of its total assets in high yield bonds (sometimes referred to as “junk bonds”) and may investin both U.S. dollar-denominated and foreign currency-denominated foreign securities. This portion of the fund normally has an average credit rating of“A” or “AA.”

Under normal circumstances, no more than 15% of the total assets of the portion of the fund managed by the Core / Core Plus Team will be investedin asset-backed securities rated lower than A by both rating agencies. The fund’s investment policies are based on credit ratings at the time ofpurchase.

Use of Hedging and Other Strategic Transactions. The fund is authorized to use all of the various investment strategies referred to under “AdditionalInformation About the Funds’ Principal Risks — Hedging, derivatives and other strategic transactions risk” including, but not limited to, U.S. Treasuryfutures and options, index derivatives, credit default swaps and forwards.

Principal risksThe fund is subject to risks, and you could lose money by investing in the fund. The principal risks of investing in the fund include:

Changing distribution levels risk. The fund may cease or reduce the level of its distribution or make a greater return of capital if income ordividends paid from its investments declines.

Credit and counterparty risk. The issuer or guarantor of a fixed-income security, the counterparty to an over-the-counter derivatives contract, or aborrower of fund securities may not make timely payments or otherwise honor its obligations. U.S. government securities are subject to varyingdegrees of credit risk depending upon the nature of their support. A downgrade or default affecting any of the fund’s securities could affect the fund’sperformance.

Cybersecurity and operational risk. Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, orproprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affectingissuers of a fund’s securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communicationerrors, or technology failures, among other causes.

Economic and market events risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreigncentral banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impactperformance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companiescould suffer losses if interest rates rise or economic conditions deteriorate.

Fixed-income securities risk. A rise in interest rates typically causes bond prices to fall. The longer the average maturity or duration of the bonds heldby a fund, the more sensitive it will likely be to interest-rate fluctuations. An issuer may not make all interest payments or repay all or any of theprincipal borrowed. Changes in a security’s credit quality may adversely affect fund performance.

Foreign securities risk. Less information may be publicly available regarding foreign issuers. Foreign securities may be subject to foreign taxes andmay be more volatile than U.S. securities. Currency fluctuations and political and economic developments may adversely impact the value of foreignsecurities.

Hedging, derivatives, and other strategic transactions risk. Hedging, derivatives, and other strategic transactions may increase a fund’s volatilityand could produce disproportionate losses, potentially more than the fund’s principal investment. Risks of these transactions are different from andpossibly greater than risks of investing directly in securities and other traditional instruments. Under certain market conditions, derivatives couldbecome harder to value or sell and may become subject to liquidity risk (i.e., the inability to enter into closing transactions). Regulatory changes in

.5

derivative markets could impact the cost of or the fund’s ability to engage in derivatives transactions. Derivatives and other strategic transactions thatthe fund intends to utilize include: foreign currency forward contracts, futures contracts, options, and credit default swaps. Foreign currency forwardcontracts, futures contracts, options, and swaps generally are subject to counterparty risk. In addition, swaps may be subject to interest-rate andsettlement risk, and the risk of default of the underlying reference obligation.

High portfolio turnover risk. Trading securities actively and frequently can increase transaction costs (thus lowering performance) and taxabledistributions.

Liquidity risk. The extent (if at all) to which a security may be sold or a derivative position closed without negatively impacting its market value may beimpaired by reduced market activity or participation, legal restrictions, or other economic and market impediments. Liquidity risk may be magnified inrising interest rate environments due to higher than normal redemption rates. Widespread selling of fixed-income securities to satisfy redemptionsduring periods of reduced demand may adversely impact the price or salability of such securities. Periods of heavy redemption could cause the fund tosell assets at a loss or depressed value, which could negatively affect performance. Redemption risk is heightened during periods of declining or illiquidmarkets.

Lower-rated and high-yield fixed-income securities risk. Lower-rated and high-yield fixed-income securities (junk bonds) are subject to greatercredit quality risk, risk of default, and price volatility than higher-rated fixed-income securities, may be considered speculative, and can be difficult toresell.

Mortgage-backed and asset-backed securities risk. Mortgage-backed and asset-backed securities are subject to different combinations ofprepayment, extension, interest-rate, and other market risks.

Inverse interest-only securities Inverse interest-only securities that are mortgage-backed securities are subject to the same risks as othermortgage-backed securities. In addition, the coupon on an inverse interest-only security can be extremely sensitive to changes in prevailing interestrates.

Sector risk. When a fund focuses its investments in certain sectors of the economy, its performance may be driven largely by sector performance andcould fluctuate more widely than if the fund were invested more evenly across sectors.

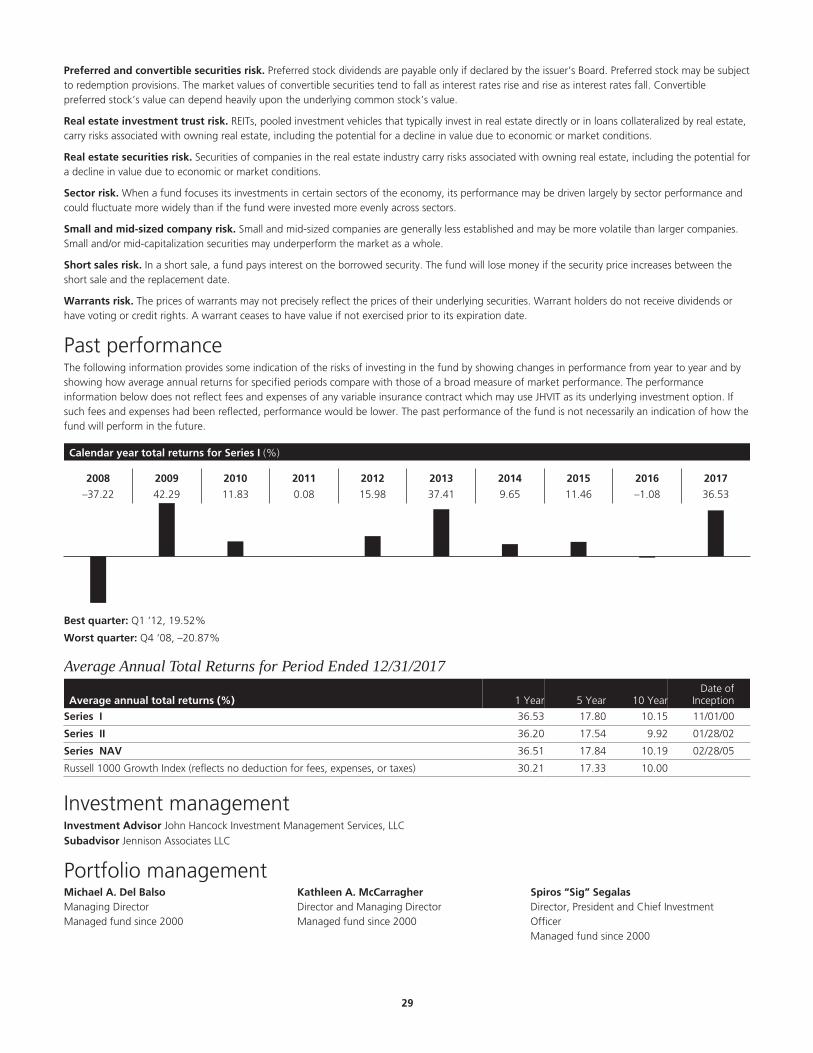

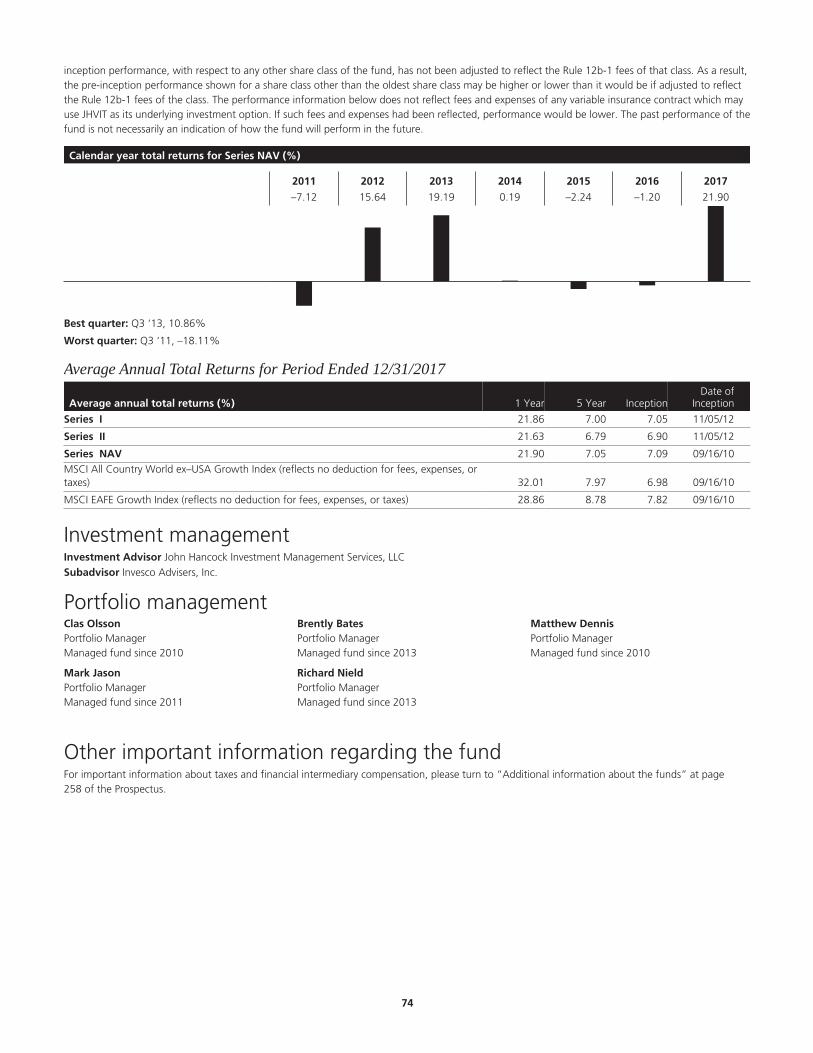

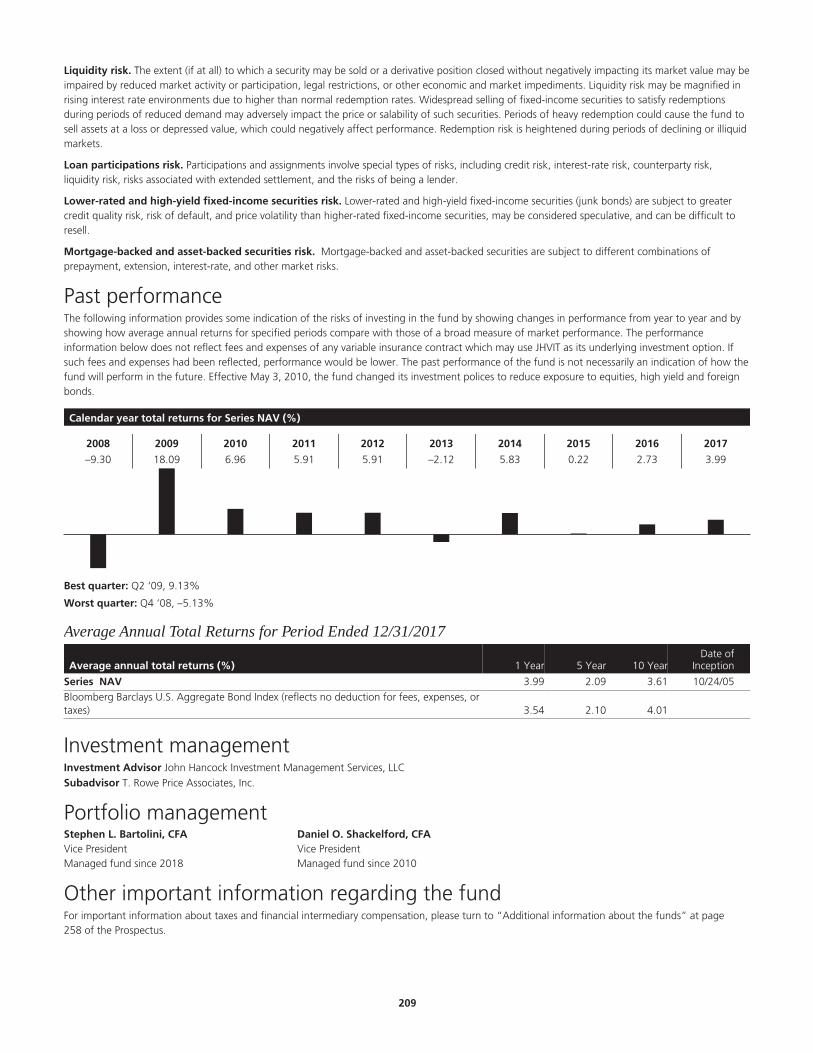

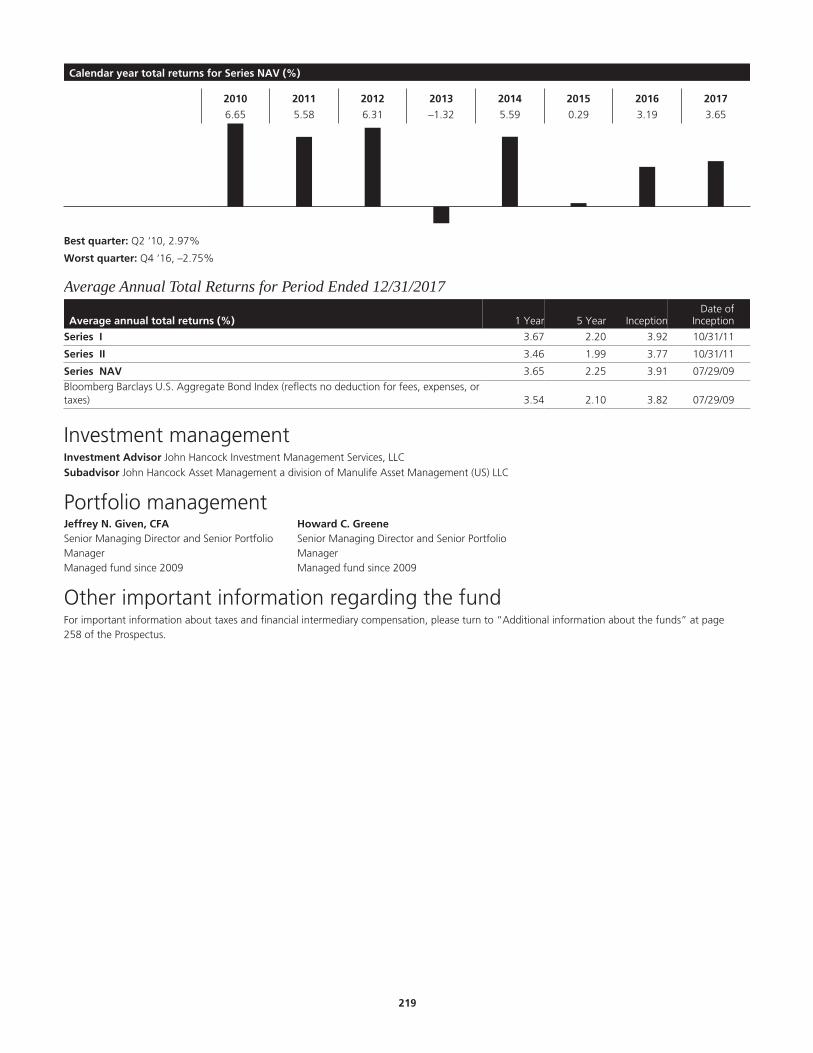

Past performanceThe following information provides some indication of the risks of investing in the fund by showing changes in performance from year to year and byshowing how average annual returns for specified periods compare with those of a broad measure of market performance. The performanceinformation below does not reflect fees and expenses of any variable insurance contract which may use JHVIT as its underlying investment option. Ifsuch fees and expenses had been reflected, performance would be lower. The past performance of the fund is not necessarily an indication of how thefund will perform in the future.

Calendar year total returns for Series NAV (%)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

–10.48 24.86 13.91 5.97 9.76 0.19 6.97 0.12 4.50 4.89

Best quarter: Q3 ‘09, 9.91%

Worst quarter: Q4 ‘08, –5.91%

Average Annual Total Returns for Period Ended 12/31/2017

Average annual total returns (%) 1 Year 5 Year 10 YearDate of

Inception

Series I 4.84 3.25 5.64 05/02/05

Series II 4.63 3.04 5.44 05/02/05

Series NAV 4.89 3.30 5.71 03/28/86Bloomberg Barclays U.S. Aggregate Bond Index (reflects no deduction for fees, expenses, ortaxes) 3.54 2.10 4.01

Investment managementInvestment Advisor John Hancock Investment Management Services, LLC§

Subadvisor John Hancock Asset Management a division of Manulife Asset Management (US) LLC

.6

Portfolio managementPeter M. Farley, CFASenior Managing Director and Senior Portfolio Manager; John HancockAsset Management a division of Manulife Asset Management (US) LLCManaged fund since 2005

Jeffrey N. Given, CFASenior Managing Director and Senior Portfolio Manager; John HancockAsset Management a division of Manulife Asset Management(US) LLCManaged fund since 2006

Howard C. GreeneSenior Managing Director and Senior Portfolio Manager; John HancockAsset Management a division of Manulife Asset Management (US) LLCManaged fund since 2005

Other important information regarding the fundFor important information about taxes and financial intermediary compensation, please turn to “Additional information about the funds” at page258 of the Prospectus.

.7

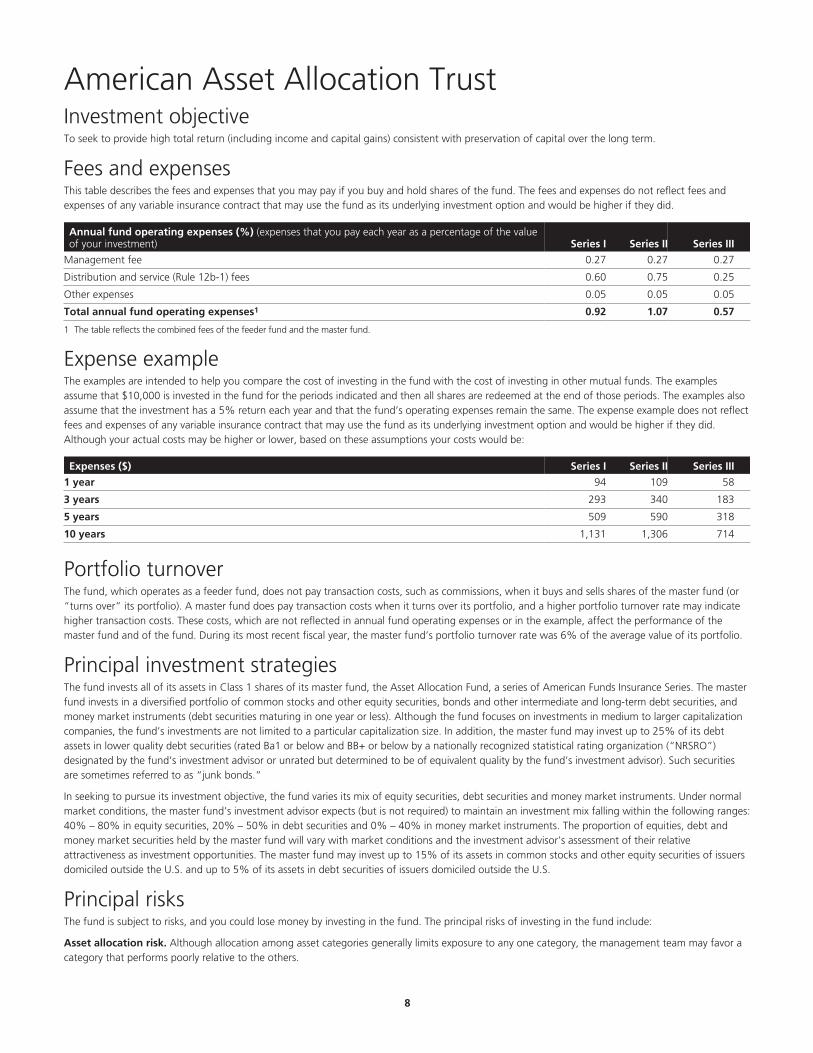

American Asset Allocation Trust Investment objectiveTo seek to provide high total return (including income and capital gains) consistent with preservation of capital over the long term.

Fees and expensesThis table describes the fees and expenses that you may pay if you buy and hold shares of the fund. The fees and expenses do not reflect fees andexpenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.

Annual fund operating expenses (%) (expenses that you pay each year as a percentage of the valueof your investment) Series I Series II Series III

Management fee 0.27 0.27 0.27

Distribution and service (Rule 12b-1) fees 0.60 0.75 0.25

Other expenses 0.05 0.05 0.05

Total annual fund operating expenses1 0.92 1.07 0.57

1 The table reflects the combined fees of the feeder fund and the master fund.

Expense exampleThe examples are intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The examplesassume that $10,000 is invested in the fund for the periods indicated and then all shares are redeemed at the end of those periods. The examples alsoassume that the investment has a 5% return each year and that the fund’s operating expenses remain the same. The expense example does not reflectfees and expenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Expenses ($) Series I Series II Series III

1 year 94 109 58

3 years 293 340 183

5 years 509 590 318

10 years 1,131 1,306 714

Portfolio turnoverThe fund, which operates as a feeder fund, does not pay transaction costs, such as commissions, when it buys and sells shares of the master fund (or“turns over” its portfolio). A master fund does pay transaction costs when it turns over its portfolio, and a higher portfolio turnover rate may indicatehigher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect the performance of themaster fund and of the fund. During its most recent fiscal year, the master fund’s portfolio turnover rate was 6% of the average value of its portfolio.

Principal investment strategiesThe fund invests all of its assets in Class 1 shares of its master fund, the Asset Allocation Fund, a series of American Funds Insurance Series. The masterfund invests in a diversified portfolio of common stocks and other equity securities, bonds and other intermediate and long-term debt securities, andmoney market instruments (debt securities maturing in one year or less). Although the fund focuses on investments in medium to larger capitalizationcompanies, the fund’s investments are not limited to a particular capitalization size. In addition, the master fund may invest up to 25% of its debtassets in lower quality debt securities (rated Ba1 or below and BB+ or below by a nationally recognized statistical rating organization (“NRSRO”)designated by the fund’s investment advisor or unrated but determined to be of equivalent quality by the fund’s investment advisor). Such securitiesare sometimes referred to as “junk bonds.”

In seeking to pursue its investment objective, the fund varies its mix of equity securities, debt securities and money market instruments. Under normalmarket conditions, the master fund’s investment advisor expects (but is not required) to maintain an investment mix falling within the following ranges:40% – 80% in equity securities, 20% – 50% in debt securities and 0% – 40% in money market instruments. The proportion of equities, debt andmoney market securities held by the master fund will vary with market conditions and the investment advisor’s assessment of their relativeattractiveness as investment opportunities. The master fund may invest up to 15% of its assets in common stocks and other equity securities of issuersdomiciled outside the U.S. and up to 5% of its assets in debt securities of issuers domiciled outside the U.S.

Principal risksThe fund is subject to risks, and you could lose money by investing in the fund. The principal risks of investing in the fund include:

Asset allocation risk. Although allocation among asset categories generally limits exposure to any one category, the management team may favor acategory that performs poorly relative to the others.

.8

Credit and counterparty risk. The issuer or guarantor of a fixed-income security or a borrower of fund securities may not make timely payments orotherwise honor its obligations. U.S. government securities are subject to varying degrees of credit risk depending upon the nature of their support. Adowngrade or default affecting any of the fund’s securities could affect the fund’s performance.

Cybersecurity and operational risk. Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, orproprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affectingissuers of a fund’s securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communicationerrors, or technology failures, among other causes.

Economic and market events risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreigncentral banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impactperformance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companiescould suffer losses if interest rates rise or economic conditions deteriorate.

Equity securities risk. The price of equity securities may decline due to changes in a company’s financial condition or overall market conditions.

Fixed-income securities risk. A rise in interest rates typically causes bond prices to fall. The longer the average maturity or duration of the bonds heldby a fund, the more sensitive it will likely be to interest-rate fluctuations. An issuer may not make all interest payments or repay all or any of theprincipal borrowed. Changes in a security’s credit quality may adversely affect fund performance.

Foreign securities risk. Less information may be publicly available regarding foreign issuers. Foreign securities may be subject to foreign taxes andmay be more volatile than U.S. securities. Currency fluctuations and political and economic developments may adversely impact the value of foreignsecurities.

Income stock risk. Income provided by the fund may be affected by changes in the dividend polices of the companies in which the fund invests andthe capital resources available for such payments at such companies.

Large company risk. Larger companies may grow more slowly than smaller companies or be slower to respond to business developments. Large-capitalization securities may underperform the market as a whole.

Liquidity risk. The extent (if at all) to which a security may be sold without negatively impacting its market value may be impaired by reduced marketactivity or participation, legal restrictions, or other economic and market impediments. Liquidity risk may be magnified in rising interest rateenvironments due to higher than normal redemption rates. Widespread selling of fixed-income securities to satisfy redemptions during periods ofreduced demand may adversely impact the price or salability of such securities. Periods of heavy redemption could cause the fund to sell assets at a lossor depressed value, which could negatively affect performance. Redemption risk is heightened during periods of declining or illiquid markets.

Lower-rated and high-yield fixed-income securities risk. Lower-rated and high-yield fixed-income securities (junk bonds) are subject to greatercredit quality risk, risk of default, and price volatility than higher-rated fixed-income securities, may be considered speculative, and can be difficult toresell.

Small and mid-sized company risk. Small and mid-sized companies are generally less established and may be more volatile than larger companies.Small and/or mid-capitalization securities may underperform the market as a whole.

Past performanceThe following information provides some indication of the risks of investing in the fund by showing changes in performance from year to year and byshowing how average annual returns for specified periods compare with those of a broad measure of market performance. The Bloomberg BarclaysU.S. Aggregate Bond Index and the Combined Index (described below) show how the fund’s performance compares against the returns of similarinvestments. Unless all share classes shown in the table have the same inception date, performance shown for periods prior to the inception date of aclass is the performance of the fund’s oldest share class. The performance of the fund’s oldest share class, for periods prior to its inception, is theperformance of the master fund share class in which the fund invests, adjusted to reflect the expenses of the fund’s oldest class. This pre-inceptionperformance, with respect to any other share class of the fund, has not been adjusted to reflect the Rule 12b-1 fees of that class. As a result, the pre-inception performance shown for a share class other than the oldest share class may be higher or lower than it would be if adjusted to reflect the Rule12b-1 fees of the class. The performance information below does not reflect fees and expenses of any variable insurance contract which may use JHVITas its underlying investment option. If such fees and expenses had been reflected, performance would be lower. The past performance of the fund isnot necessarily an indication of how the fund will perform in the future.

The Combined Index represents 60% of the S&P 500 Index and 40% of the Bloomberg Barclays U.S. Aggregate Bond Index.

.9

Calendar year total returns for Series II (%)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

–29.83 23.27 11.90 0.86 15.49 23.13 4.89 0.91 8.92 15.69

Best quarter: Q3 ‘09, 11.42%

Worst quarter: Q4 ‘08, –16.41%

Average Annual Total Returns for Period Ended 12/31/2017

Average annual total returns (%) 1 Year 5 Year 10 YearDate of

Inception

Series I 15.79 10.56 6.50 04/28/08

Series II 15.69 10.43 6.35 05/01/07

Series III 16.25 10.96 6.92 01/03/08

S&P 500 Index (reflects no deduction for fees, expenses, or taxes) 21.83 15.79 8.50 Bloomberg Barclays U.S. Aggregate Bond Index (reflects no deduction for fees, expenses, ortaxes) 3.54 2.10 4.01

Combined Index (reflects no deduction for fees, expenses, or taxes) 14.21 10.25 6.98

Investment managementInvestment Advisor of the Master Fund: Capital Research and Management Company

Portfolio managementAlan N. BerroPresident; Partner - Capital World InvestorsManaged the fund since 2000

David A. DaiglePartner - Capital Fixed Income Investors, CapitalResearch and Management CompanyManaged the fund since 2009

Jeffrey T. LagerPartner - Capital World InvestorsManaged the fund since 2007

James R. MulallyPartner - Capital Fixed Income Investors, CapitalResearch and Management CompanyManaged the fund since 2006

John R. QueenVice President - Capital Fixed Income Investors,Capital Research and Management CompanyManaged the fund since 2015

Other important information regarding the fundFor important information about taxes and financial intermediary compensation, please turn to “Additional information about the funds” at page258 of the Prospectus.

.10

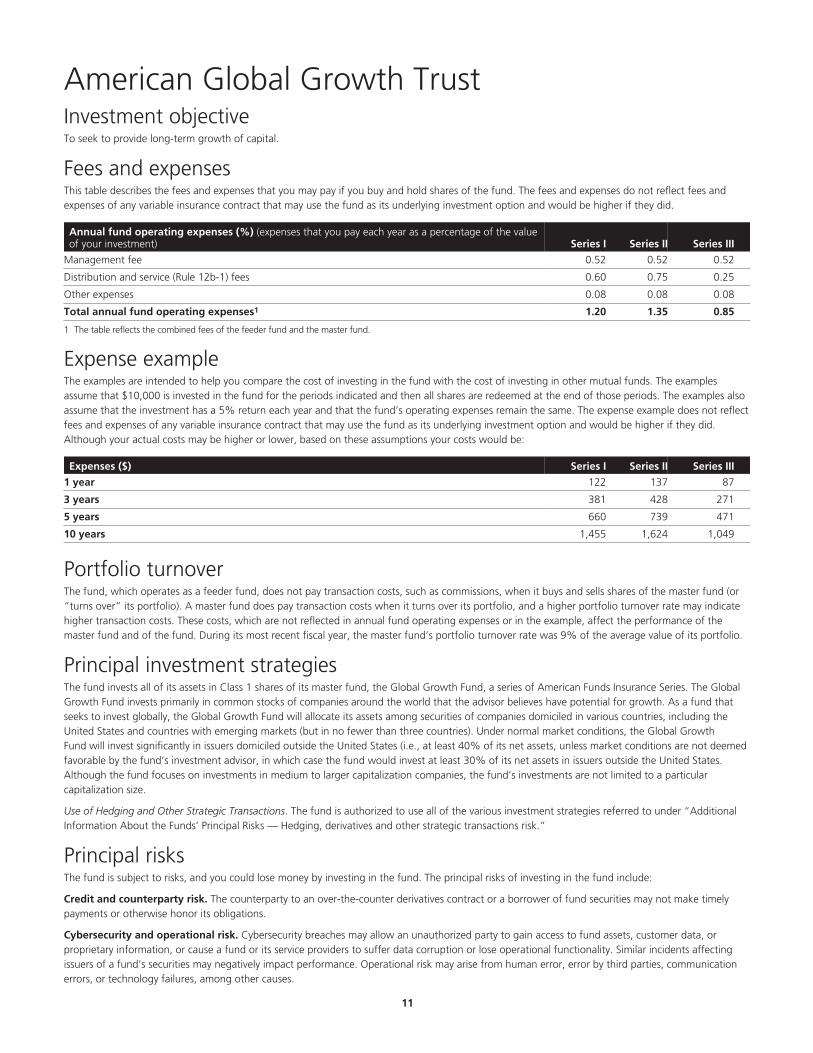

American Global Growth Trust Investment objectiveTo seek to provide long-term growth of capital.

Fees and expensesThis table describes the fees and expenses that you may pay if you buy and hold shares of the fund. The fees and expenses do not reflect fees andexpenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.

Annual fund operating expenses (%) (expenses that you pay each year as a percentage of the valueof your investment) Series I Series II Series III

Management fee 0.52 0.52 0.52

Distribution and service (Rule 12b-1) fees 0.60 0.75 0.25

Other expenses 0.08 0.08 0.08

Total annual fund operating expenses1 1.20 1.35 0.85

1 The table reflects the combined fees of the feeder fund and the master fund.

Expense exampleThe examples are intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The examplesassume that $10,000 is invested in the fund for the periods indicated and then all shares are redeemed at the end of those periods. The examples alsoassume that the investment has a 5% return each year and that the fund’s operating expenses remain the same. The expense example does not reflectfees and expenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Expenses ($) Series I Series II Series III

1 year 122 137 87

3 years 381 428 271

5 years 660 739 471

10 years 1,455 1,624 1,049

Portfolio turnoverThe fund, which operates as a feeder fund, does not pay transaction costs, such as commissions, when it buys and sells shares of the master fund (or“turns over” its portfolio). A master fund does pay transaction costs when it turns over its portfolio, and a higher portfolio turnover rate may indicatehigher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect the performance of themaster fund and of the fund. During its most recent fiscal year, the master fund’s portfolio turnover rate was 9% of the average value of its portfolio.

Principal investment strategiesThe fund invests all of its assets in Class 1 shares of its master fund, the Global Growth Fund, a series of American Funds Insurance Series. The GlobalGrowth Fund invests primarily in common stocks of companies around the world that the advisor believes have potential for growth. As a fund thatseeks to invest globally, the Global Growth Fund will allocate its assets among securities of companies domiciled in various countries, including theUnited States and countries with emerging markets (but in no fewer than three countries). Under normal market conditions, the Global GrowthFund will invest significantly in issuers domiciled outside the United States (i.e., at least 40% of its net assets, unless market conditions are not deemedfavorable by the fund’s investment advisor, in which case the fund would invest at least 30% of its net assets in issuers outside the United States.Although the fund focuses on investments in medium to larger capitalization companies, the fund’s investments are not limited to a particularcapitalization size.

Use of Hedging and Other Strategic Transactions. The fund is authorized to use all of the various investment strategies referred to under “AdditionalInformation About the Funds’ Principal Risks — Hedging, derivatives and other strategic transactions risk.”

Principal risksThe fund is subject to risks, and you could lose money by investing in the fund. The principal risks of investing in the fund include:

Credit and counterparty risk. The counterparty to an over-the-counter derivatives contract or a borrower of fund securities may not make timelypayments or otherwise honor its obligations.

Cybersecurity and operational risk. Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, orproprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affectingissuers of a fund’s securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communicationerrors, or technology failures, among other causes.

.11

Economic and market events risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreigncentral banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impactperformance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companiescould suffer losses if interest rates rise or economic conditions deteriorate.

Equity securities risk. The price of equity securities may decline due to changes in a company’s financial condition or overall market conditions.Growth company securities may fluctuate more in price than other securities because of the greater emphasis on earnings expectations.

Foreign securities risk. Less information may be publicly available regarding foreign issuers. Foreign securities may be subject to foreign taxes andmay be more volatile than U.S. securities. Currency fluctuations and political and economic developments may adversely impact the value of foreignsecurities. The risks of investing in foreign securities are magnified in emerging markets.

Hedging, derivatives, and other strategic transactions risk. Hedging, derivatives, and other strategic transactions may increase a fund’s volatilityand could produce disproportionate losses, potentially more than the fund’s principal investment. Risks of these transactions are different from andpossibly greater than risks of investing directly in securities and other traditional instruments. Under certain market conditions, derivatives couldbecome harder to value or sell and may become subject to liquidity risk (i.e., the inability to enter into closing transactions). Regulatory changes inderivative markets could impact the cost of or the fund’s ability to engage in derivatives transactions. Derivatives and other strategic transactions thatthe fund intends to utilize include: credit default swaps, foreign currency forward contracts, foreign currency swaps, futures contracts, futures onoptions, swaptions, interest-rate swaps, and options. Foreign currency forward contracts, futures contracts, options, and swaps generally are subject tocounterparty risk. In addition, swaps may be subject to interest-rate and settlement risk, and the risk of default of the underlying reference instrument.

Large company risk. Larger companies may grow more slowly than smaller companies or be slower to respond to business developments. Large-capitalization securities may underperform the market as a whole.

Liquidity risk. The extent (if at all) to which a security may be sold or a derivative position closed without negatively impacting its market value may beimpaired by reduced market activity or participation, legal restrictions, or other economic and market impediments.

Sector risk. When a fund focuses its investments in certain sectors of the economy, its performance may be driven largely by sector performance andcould fluctuate more widely than if the fund were invested more evenly across sectors.

Small and mid-sized company risk. Small and mid-sized companies are generally less established and may be more volatile than larger companies.Small and/or mid-capitalization securities may underperform the market as a whole.

Past performanceThe following information provides some indication of the risks of investing in the fund by showing changes in performance from year to year and byshowing how average annual returns for specified periods compare with those of a broad measure of market performance. The Lipper Global FundIndex shows how the fund’s performance compares against the returns of similar investments. Unless all share classes shown in the table have thesame inception date, performance shown for periods prior to the inception date of a class is the performance of the fund’s oldest share class. Theperformance of the fund’s oldest share class, for periods prior to its inception, is the performance of the master fund share class in which the fundinvests, adjusted to reflect the expenses of the fund’s oldest class. This pre-inception performance, with respect to any other share class of the fund,has not been adjusted to reflect the Rule 12b-1 fees of that class. As a result, the pre-inception performance shown for a share class other than theoldest share class may be higher or lower than it would be if adjusted to reflect the Rule 12b-1 fees of the class. The performance information belowdoes not reflect fees and expenses of any variable insurance contract which may use JHVIT as its underlying investment option. If such fees andexpenses had been reflected, performance would be lower. The past performance of the fund is not necessarily an indication of how the fund willperform in the future.

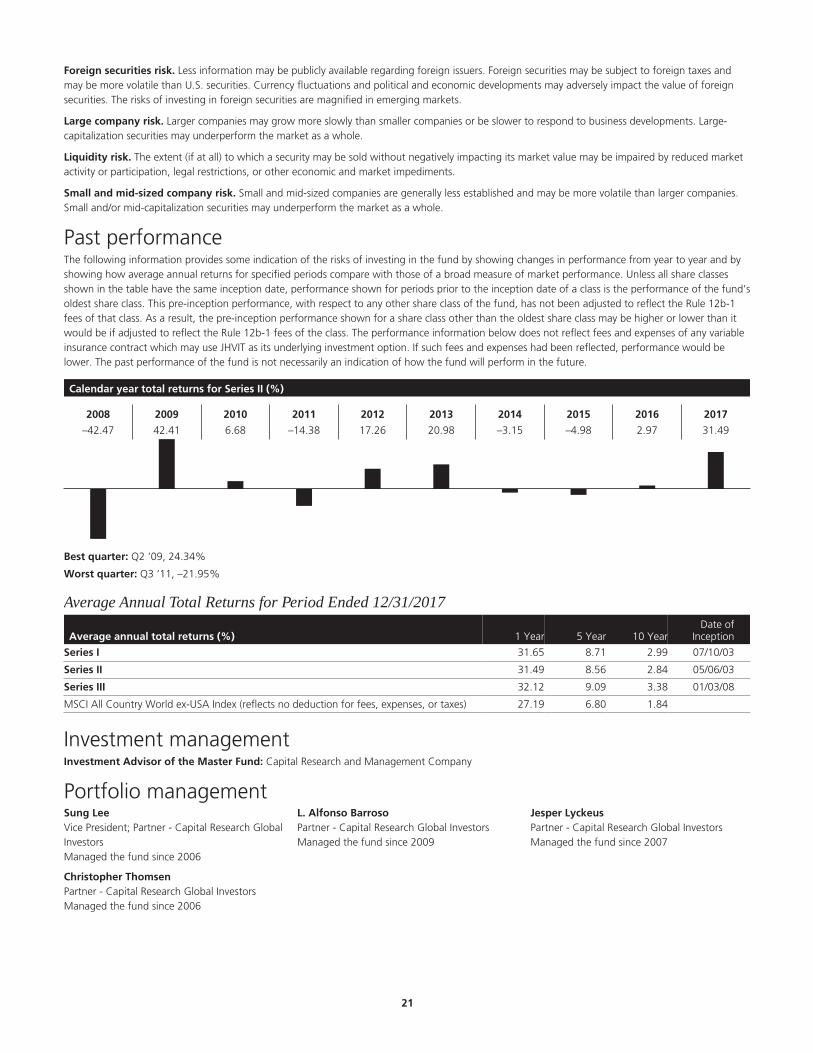

Calendar year total returns for Series II (%)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

–38.68 41.42 11.17 –9.40 22.00 28.43 1.82 6.50 0.10 30.92

Best quarter: Q2 ‘09, 22.00%

Worst quarter: Q4 ‘08, –20.17%

.12

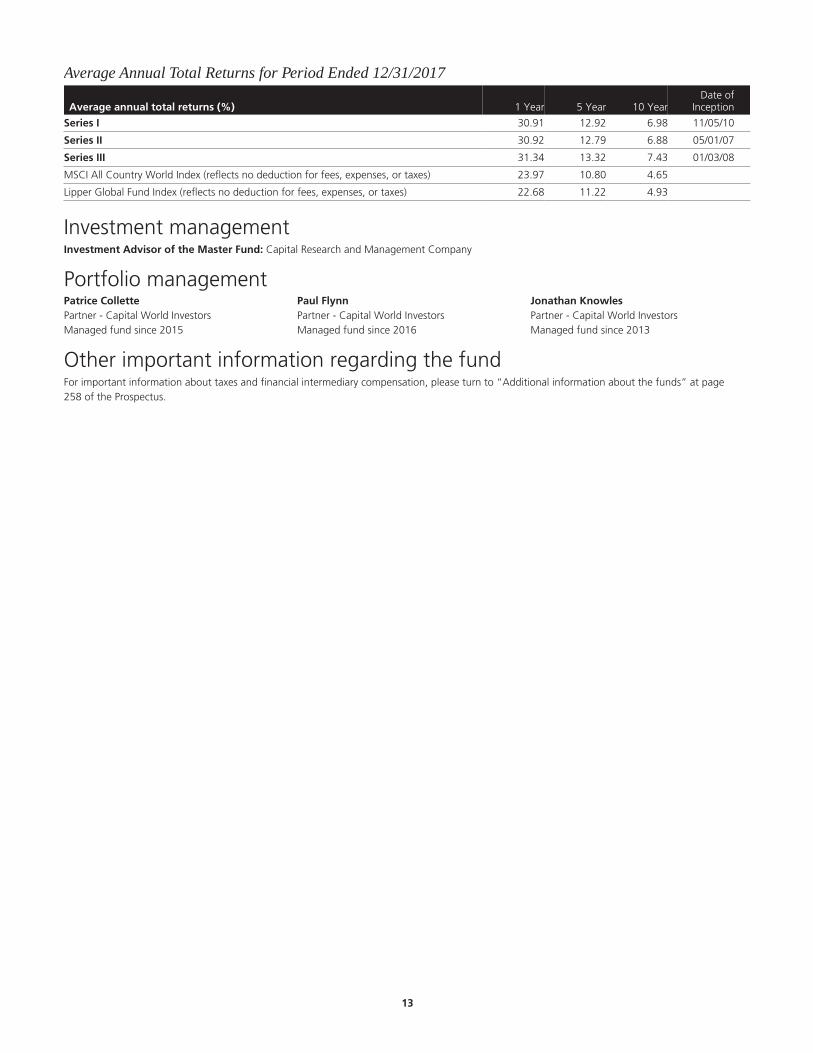

Average Annual Total Returns for Period Ended 12/31/2017

Average annual total returns (%) 1 Year 5 Year 10 YearDate of

Inception

Series I 30.91 12.92 6.98 11/05/10

Series II 30.92 12.79 6.88 05/01/07

Series III 31.34 13.32 7.43 01/03/08

MSCI All Country World Index (reflects no deduction for fees, expenses, or taxes) 23.97 10.80 4.65

Lipper Global Fund Index (reflects no deduction for fees, expenses, or taxes) 22.68 11.22 4.93

Investment managementInvestment Advisor of the Master Fund: Capital Research and Management Company

Portfolio managementPatrice CollettePartner - Capital World InvestorsManaged fund since 2015

Paul FlynnPartner - Capital World InvestorsManaged fund since 2016

Jonathan KnowlesPartner - Capital World InvestorsManaged fund since 2013

Other important information regarding the fundFor important information about taxes and financial intermediary compensation, please turn to “Additional information about the funds” at page258 of the Prospectus.

.13

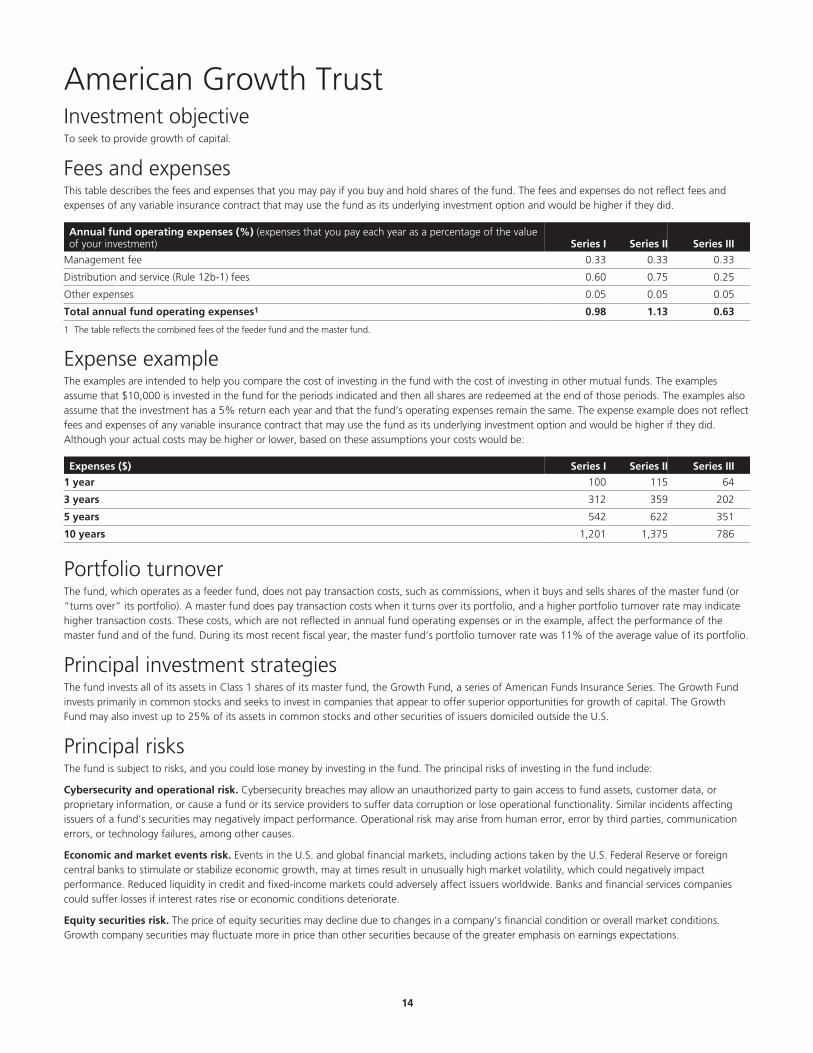

American Growth Trust Investment objectiveTo seek to provide growth of capital.

Fees and expensesThis table describes the fees and expenses that you may pay if you buy and hold shares of the fund. The fees and expenses do not reflect fees andexpenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.

Annual fund operating expenses (%) (expenses that you pay each year as a percentage of the valueof your investment) Series I Series II Series III

Management fee 0.33 0.33 0.33

Distribution and service (Rule 12b-1) fees 0.60 0.75 0.25

Other expenses 0.05 0.05 0.05

Total annual fund operating expenses1 0.98 1.13 0.63

1 The table reflects the combined fees of the feeder fund and the master fund.

Expense exampleThe examples are intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The examplesassume that $10,000 is invested in the fund for the periods indicated and then all shares are redeemed at the end of those periods. The examples alsoassume that the investment has a 5% return each year and that the fund’s operating expenses remain the same. The expense example does not reflectfees and expenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Expenses ($) Series I Series II Series III

1 year 100 115 64

3 years 312 359 202

5 years 542 622 351

10 years 1,201 1,375 786

Portfolio turnoverThe fund, which operates as a feeder fund, does not pay transaction costs, such as commissions, when it buys and sells shares of the master fund (or“turns over” its portfolio). A master fund does pay transaction costs when it turns over its portfolio, and a higher portfolio turnover rate may indicatehigher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect the performance of themaster fund and of the fund. During its most recent fiscal year, the master fund’s portfolio turnover rate was 11% of the average value of its portfolio.

Principal investment strategiesThe fund invests all of its assets in Class 1 shares of its master fund, the Growth Fund, a series of American Funds Insurance Series. The Growth Fundinvests primarily in common stocks and seeks to invest in companies that appear to offer superior opportunities for growth of capital. The GrowthFund may also invest up to 25% of its assets in common stocks and other securities of issuers domiciled outside the U.S.

Principal risksThe fund is subject to risks, and you could lose money by investing in the fund. The principal risks of investing in the fund include:

Cybersecurity and operational risk. Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, orproprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affectingissuers of a fund’s securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communicationerrors, or technology failures, among other causes.

Economic and market events risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreigncentral banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impactperformance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companiescould suffer losses if interest rates rise or economic conditions deteriorate.

Equity securities risk. The price of equity securities may decline due to changes in a company’s financial condition or overall market conditions.Growth company securities may fluctuate more in price than other securities because of the greater emphasis on earnings expectations.

.14

Foreign securities risk. Less information may be publicly available regarding foreign issuers. Foreign securities may be subject to foreign taxes andmay be more volatile than U.S. securities. Currency fluctuations and political and economic developments may adversely impact the value of foreignsecurities.

Large company risk. Larger companies may grow more slowly than smaller companies or be slower to respond to business developments. Large-capitalization securities may underperform the market as a whole.

Liquidity risk. The extent (if at all) to which a security may be sold without negatively impacting its market value may be impaired by reduced marketactivity or participation, legal restrictions, or other economic and market impediments.

Sector risk. When a fund focuses its investments in certain sectors of the economy, its performance may be driven largely by sector performance andcould fluctuate more widely than if the fund were invested more evenly across sectors.

Small and mid-sized company risk. Small and mid-sized companies are generally less established and may be more volatile than larger companies.Small and/or mid-capitalization securities may underperform the market as a whole.

Past performanceThe following information provides some indication of the risks of investing in the fund by showing changes in performance from year to year and byshowing how average annual returns for specified periods compare with those of a broad measure of market performance. Unless all share classesshown in the table have the same inception date, performance shown for periods prior to the inception date of a class is the performance of the fund’soldest share class. This pre-inception performance, with respect to any other share class of the fund, has not been adjusted to reflect the Rule 12b-1fees of that class. As a result, the pre-inception performance shown for a share class other than the oldest share class may be higher or lower than itwould be if adjusted to reflect the Rule 12b-1 fees of the class. The performance information below does not reflect fees and expenses of any variableinsurance contract which may use JHVIT as its underlying investment option. If such fees and expenses had been reflected, performance would belower. The past performance of the fund is not necessarily an indication of how the fund will perform in the future.

Calendar year total returns for Series II (%)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

–44.28 38.68 18.14 –4.79 17.23 29.48 7.96 6.35 9.03 27.74

Best quarter: Q2 ‘09, 18.33%

Worst quarter: Q4 ‘08, –26.20%

Average Annual Total Returns for Period Ended 12/31/2017

Average annual total returns (%) 1 Year 5 Year 10 YearDate of

Inception

Series I 27.87 15.78 7.89 07/10/03

Series II 27.74 15.67 7.75 05/05/03

Series III 28.22 16.18 8.31 01/03/08

S&P 500 Index (reflects no deduction for fees, expenses, or taxes) 21.83 15.79 8.50

Investment managementInvestment Advisor of the Master Fund: Capital Research and Management Company

Portfolio managementMark L. CaseyPartner - Capital World InvestorsManaged the fund since 2017

Michael T. KerrPartner - Capital World InvestorsManaged the fund since 2005

Andraz RazenVice President - Capital World InvestorsManaged the fund since 2013

Martin RomoPartner - Capital World InvestorsManaged the fund since 2016

Alan J. WilsonPartner - Capital World InvestorsManaged the fund since 2014

.15

Other important information regarding the fundFor important information about taxes and financial intermediary compensation, please turn to “Additional information about the funds” at page258 of the Prospectus.

.16

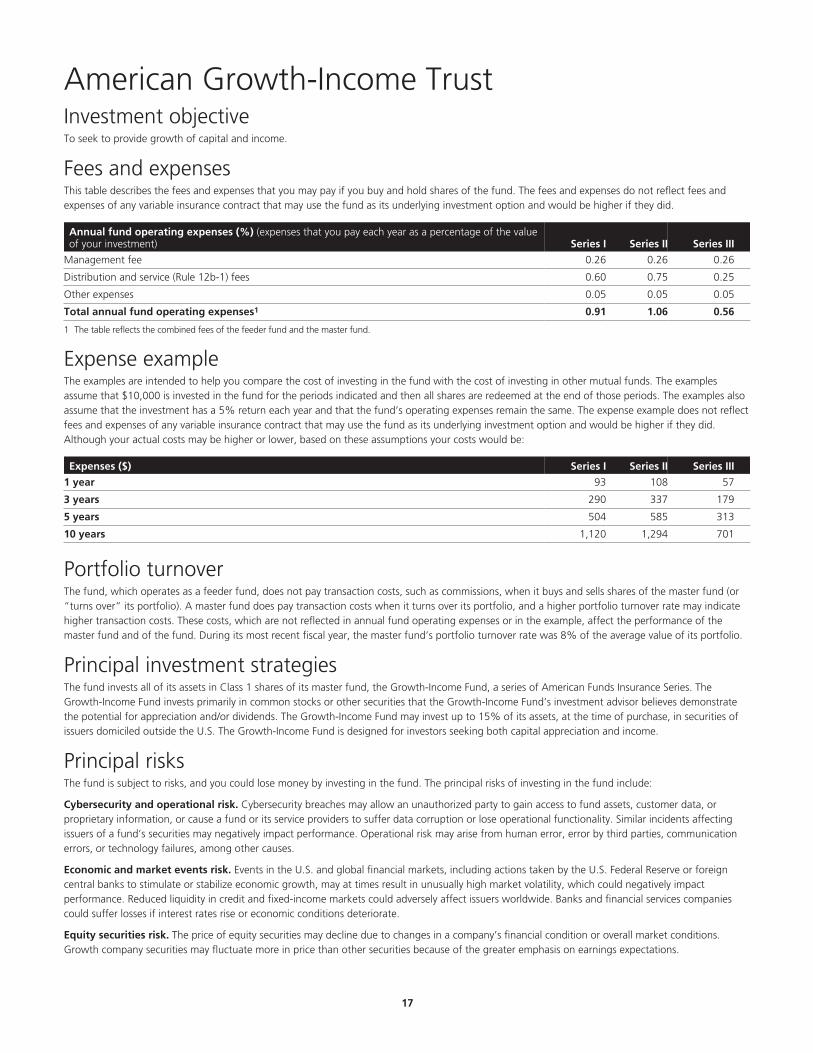

American Growth-Income Trust Investment objectiveTo seek to provide growth of capital and income.

Fees and expensesThis table describes the fees and expenses that you may pay if you buy and hold shares of the fund. The fees and expenses do not reflect fees andexpenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.

Annual fund operating expenses (%) (expenses that you pay each year as a percentage of the valueof your investment) Series I Series II Series III

Management fee 0.26 0.26 0.26

Distribution and service (Rule 12b-1) fees 0.60 0.75 0.25

Other expenses 0.05 0.05 0.05

Total annual fund operating expenses1 0.91 1.06 0.56

1 The table reflects the combined fees of the feeder fund and the master fund.

Expense exampleThe examples are intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The examplesassume that $10,000 is invested in the fund for the periods indicated and then all shares are redeemed at the end of those periods. The examples alsoassume that the investment has a 5% return each year and that the fund’s operating expenses remain the same. The expense example does not reflectfees and expenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Expenses ($) Series I Series II Series III

1 year 93 108 57

3 years 290 337 179

5 years 504 585 313

10 years 1,120 1,294 701

Portfolio turnoverThe fund, which operates as a feeder fund, does not pay transaction costs, such as commissions, when it buys and sells shares of the master fund (or“turns over” its portfolio). A master fund does pay transaction costs when it turns over its portfolio, and a higher portfolio turnover rate may indicatehigher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect the performance of themaster fund and of the fund. During its most recent fiscal year, the master fund’s portfolio turnover rate was 8% of the average value of its portfolio.

Principal investment strategiesThe fund invests all of its assets in Class 1 shares of its master fund, the Growth-Income Fund, a series of American Funds Insurance Series. TheGrowth-Income Fund invests primarily in common stocks or other securities that the Growth-Income Fund’s investment advisor believes demonstratethe potential for appreciation and/or dividends. The Growth-Income Fund may invest up to 15% of its assets, at the time of purchase, in securities ofissuers domiciled outside the U.S. The Growth-Income Fund is designed for investors seeking both capital appreciation and income.

Principal risksThe fund is subject to risks, and you could lose money by investing in the fund. The principal risks of investing in the fund include:

Cybersecurity and operational risk. Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, orproprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affectingissuers of a fund’s securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communicationerrors, or technology failures, among other causes.

Economic and market events risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreigncentral banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impactperformance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companiescould suffer losses if interest rates rise or economic conditions deteriorate.

Equity securities risk. The price of equity securities may decline due to changes in a company’s financial condition or overall market conditions.Growth company securities may fluctuate more in price than other securities because of the greater emphasis on earnings expectations.

.17

Foreign securities risk. Less information may be publicly available regarding foreign issuers. Foreign securities may be subject to foreign taxes andmay be more volatile than U.S. securities. Currency fluctuations and political and economic developments may adversely impact the value of foreignsecurities.

Income stock risk. Income provided by the fund may be affected by changes in the dividend polices of the companies in which the fund invests andthe capital resources available for such payments at such companies.

Large company risk. Larger companies may grow more slowly than smaller companies or be slower to respond to business developments. Large-capitalization securities may underperform the market as a whole.

Liquidity risk. The extent (if at all) to which a security may be sold without negatively impacting its market value may be impaired by reduced marketactivity or participation, legal restrictions, or other economic and market impediments.

Small and mid-sized company risk. Small and mid-sized companies are generally less established and may be more volatile than larger companies.Small and/or mid-capitalization securities may underperform the market as a whole.

Past performanceThe following information provides some indication of the risks of investing in the fund by showing changes in performance from year to year and byshowing how average annual returns for specified periods compare with those of a broad measure of market performance. Unless all share classesshown in the table have the same inception date, performance shown for periods prior to the inception date of a class is the performance of the fund’soldest share class. This pre-inception performance, with respect to any other share class of the fund, has not been adjusted to reflect the Rule 12b-1fees of that class. As a result, the pre-inception performance shown for a share class other than the oldest share class may be higher or lower than itwould be if adjusted to reflect the Rule 12b-1 fees of the class. The performance information below does not reflect fees and expenses of any variableinsurance contract which may use JHVIT as its underlying investment option. If such fees and expenses had been reflected, performance would belower. The past performance of the fund is not necessarily an indication of how the fund will perform in the future.

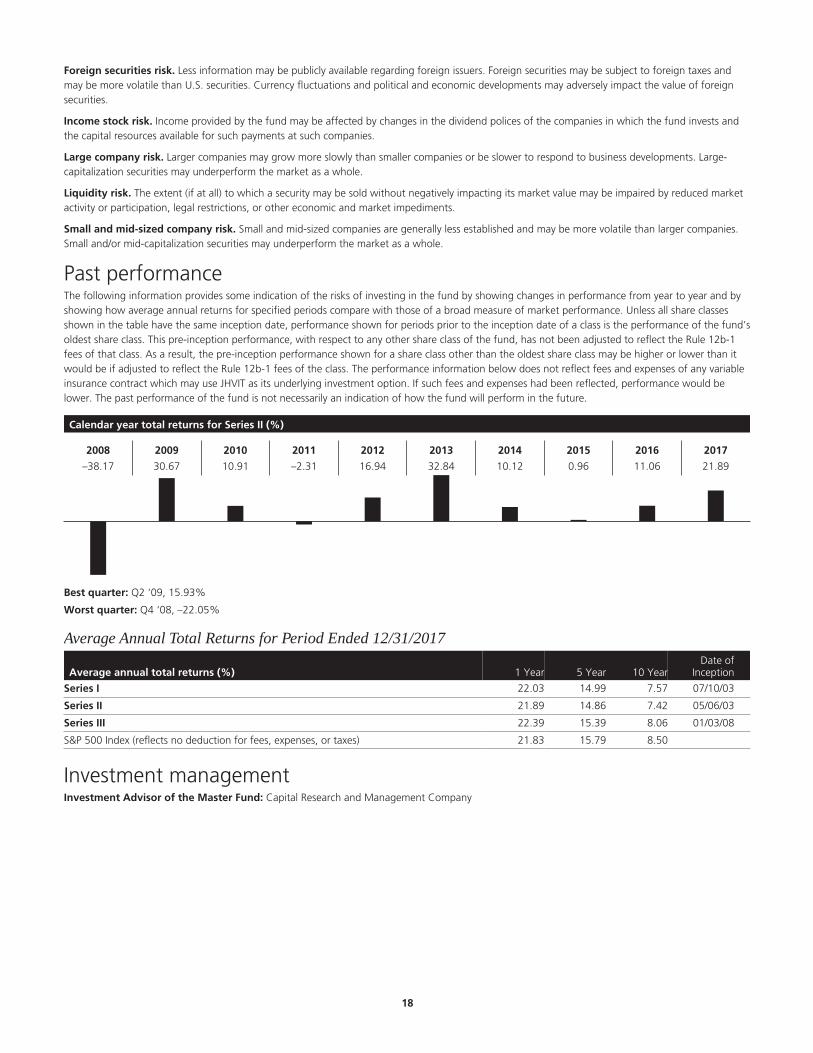

Calendar year total returns for Series II (%)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

–38.17 30.67 10.91 –2.31 16.94 32.84 10.12 0.96 11.06 21.89

Best quarter: Q2 ‘09, 15.93%

Worst quarter: Q4 ‘08, –22.05%

Average Annual Total Returns for Period Ended 12/31/2017

Average annual total returns (%) 1 Year 5 Year 10 YearDate of

Inception

Series I 22.03 14.99 7.57 07/10/03

Series II 21.89 14.86 7.42 05/06/03

Series III 22.39 15.39 8.06 01/03/08

S&P 500 Index (reflects no deduction for fees, expenses, or taxes) 21.83 15.79 8.50

Investment managementInvestment Advisor of the Master Fund: Capital Research and Management Company

.18

Portfolio managementDonald D. O’NealVice Chairman of the Board;Partner - Capital ResearchGlobal InvestorsManaged the fund since2005

J. Blair FrankPartner - Capital ResearchGlobal InvestorsManaged the fund since2006

Claudia P. HuntingtonPartner - Capital ResearchGlobal InvestorsManaged the fund since1994

Dylan YollesVice President; Partner -Capital InternationalInvestorsManaged the fund since2005

William L. RobbinsPartner - CapitalInternational InvestorsManaged fund since 2012

Other important information regarding the fundFor important information about taxes and financial intermediary compensation, please turn to “Additional information about the funds” at page258 of the Prospectus.

.19

American International Trust Investment objectiveTo seek to provide long-term growth of capital.

Fees and expensesThis table describes the fees and expenses that you may pay if you buy and hold shares of the fund. The fees and expenses do not reflect fees andexpenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.

Annual fund operating expenses (%) (expenses that you pay each year as a percentage of the valueof your investment) Series I Series II Series III

Management fee 0.50 0.50 0.50

Distribution and service (Rule 12b-1) fees 0.60 0.75 0.25

Other expenses 0.07 0.07 0.07

Total annual fund operating expenses1 1.17 1.32 0.82

1 The table reflects the combined fees of the feeder fund and the master fund.

Expense exampleThe examples are intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The examplesassume that $10,000 is invested in the fund for the periods indicated and then all shares are redeemed at the end of those periods. The examples alsoassume that the investment has a 5% return each year and that the fund’s operating expenses remain the same. The expense example does not reflectfees and expenses of any variable insurance contract that may use the fund as its underlying investment option and would be higher if they did.Although your actual costs may be higher or lower, based on these assumptions your costs would be:

Expenses ($) Series I Series II Series III

1 year 119 134 84

3 years 372 418 262

5 years 644 723 455

10 years 1,420 1,590 1,014

Portfolio turnoverThe fund, which operates as a feeder fund, does not pay transaction costs, such as commissions, when it buys and sells shares of the master fund (or“turns over” its portfolio). A master fund does pay transaction costs when it turns over its portfolio, and a higher portfolio turnover rate may indicatehigher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the example, affect the performance of themaster fund and of the fund. During its most recent fiscal year, the master fund’s portfolio turnover rate was 9% of the average value of its portfolio.

Principal investment strategiesThe fund invests all of its assets in Class 1 shares of its master fund, the International Fund, a series of American Funds Insurance Series. TheInternational Fund invests primarily in common stocks of companies domiciled outside the United States, including companies domiciled in developingcountries, that the advisor believes have the potential for growth.

Principal risksThe fund is subject to risks, and you could lose money by investing in the fund. The principal risks of investing in the fund include:

Cybersecurity and operational risk. Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, orproprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affectingissuers of a fund’s securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communicationerrors, or technology failures, among other causes.

Economic and market events risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreigncentral banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impactperformance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companiescould suffer losses if interest rates rise or economic conditions deteriorate.

Equity securities risk. The price of equity securities may decline due to changes in a company’s financial condition or overall market conditions.Growth company securities may fluctuate more in price than other securities because of the greater emphasis on earnings expectations.

.20

Foreign securities risk. Less information may be publicly available regarding foreign issuers. Foreign securities may be subject to foreign taxes andmay be more volatile than U.S. securities. Currency fluctuations and political and economic developments may adversely impact the value of foreignsecurities. The risks of investing in foreign securities are magnified in emerging markets.

Large company risk. Larger companies may grow more slowly than smaller companies or be slower to respond to business developments. Large-capitalization securities may underperform the market as a whole.

Liquidity risk. The extent (if at all) to which a security may be sold without negatively impacting its market value may be impaired by reduced marketactivity or participation, legal restrictions, or other economic and market impediments.

Small and mid-sized company risk. Small and mid-sized companies are generally less established and may be more volatile than larger companies.Small and/or mid-capitalization securities may underperform the market as a whole.