ja solar corporate...

TRANSCRIPT

JA Solar Corporate Presentation June 2012

Protect the one Earth we all share, for this and future generations.

This presentation contains forward-looking statements. These statements relate to future

events or to future financial performance and involve known and unknown risks, uncertainties,

and other factors that may cause our actual results, levels of activity, performance, or

achievements to be materially different from any future results, levels of activity, performance,

or achievements expressed or implied by these forward-looking statements. In some cases,

you can identify forward-looking statements by the use of words such as “may,” “could,”

“expect,” “intend,” “plan,” “seek,” “anticipate,” “believe,” “estimate,” “predict,” “potential,”

or “continue” or the negative of these terms or other comparable terminology. You should not

place undue reliance on forward-looking statements because they involve known and

unknown risks, uncertainties and other factors that are, in some cases, beyond our control

and that could materially affect actual results, levels of activity, performance, or achievements.

Any forward-looking statement you see or hear during this presentation reflects our current

views with respect to future events and is subject to the risks, uncertainties, and assumptions

relating to our operations, results of operations, growth strategy, and liquidity. We assume no

obligation to publicly update or revise these forward-looking statements for any reason,

whether as a result of new information, future events, or otherwise.

Forward-looking Statements

2

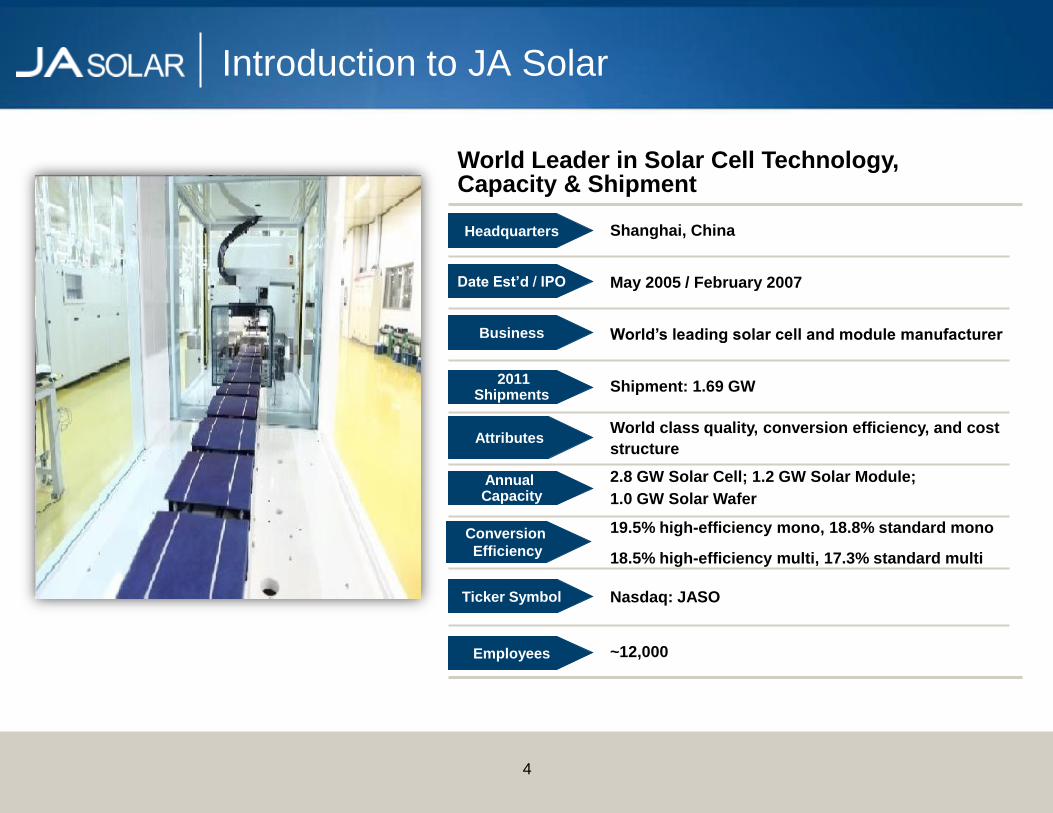

Introduction to JA Solar

Shanghai, China

May 2005 / February 2007

World’s leading solar cell and module manufacturer

Shipment: 1.69 GW

World class quality, conversion efficiency, and cost

structure

2.8 GW Solar Cell; 1.2 GW Solar Module;

1.0 GW Solar Wafer

19.5% high-efficiency mono, 18.8% standard mono

18.5% high-efficiency multi, 17.3% standard multi

Nasdaq: JASO

~12,000

World Leader in Solar Cell Technology, Capacity & Shipment Headquarters

2011 Shipments

Ticker Symbol

Date Est’d / IPO

Attributes

Annual Capacity

Conversion

Efficiency

Employees

Business

4

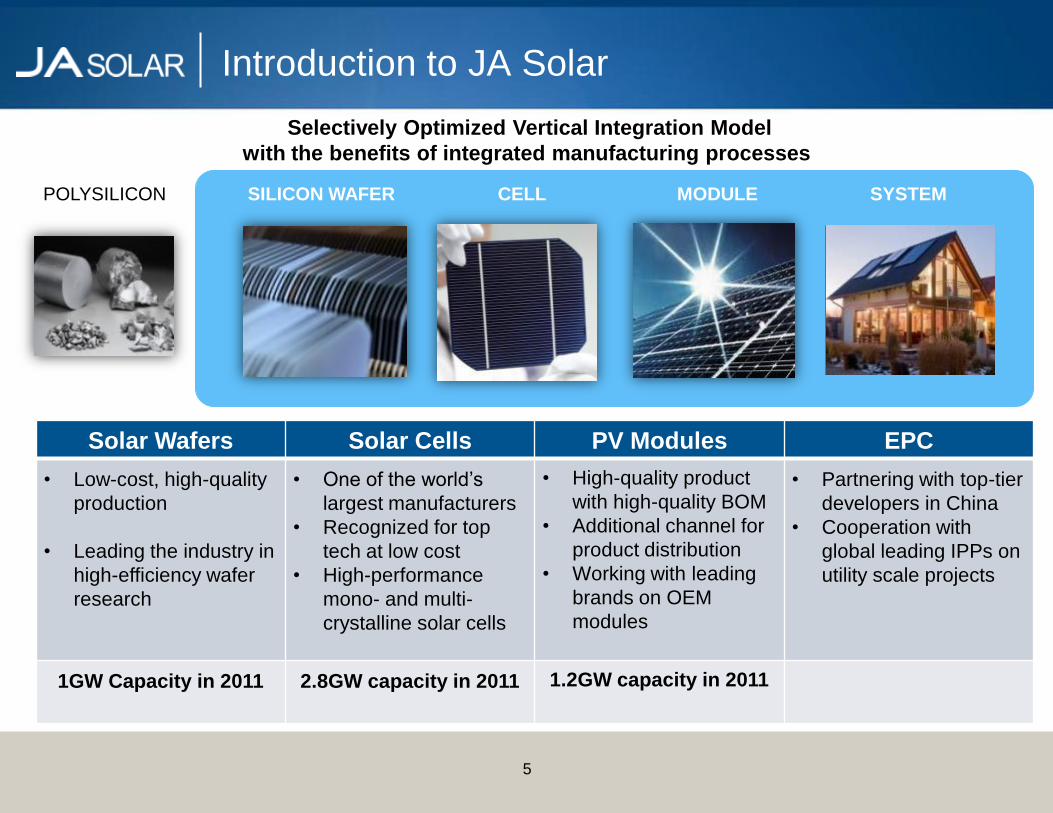

Introduction to JA Solar

POLYSILICON SILICON WAFER CELL MODULE SYSTEM

Introduction to JA Solar

Selectively Optimized Vertical Integration Model

with the benefits of integrated manufacturing processes

5

Solar Wafers Solar Cells PV Modules EPC

• Low-cost, high-quality

production

• Leading the industry in

high-efficiency wafer

research

• One of the world’s

largest manufacturers

• Recognized for top

tech at low cost

• High-performance

mono- and multi-

crystalline solar cells

• High-quality product

with high-quality BOM

• Additional channel for

product distribution

• Working with leading

brands on OEM

modules

• Partnering with top-tier

developers in China

• Cooperation with

global leading IPPs on

utility scale projects

1GW Capacity in 2011

2.8GW capacity in 2011

1.2GW capacity in 2011

Substantial Shipment & Market Share Growth

(MW)

Over 4.0 GW in cumulative PV product shipment since 2006

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2006 2007 2008 2009 2010 2011 2012E

26 132

277

509 1,246 1,210

1,800~2,000

217

485

Cell Module

1,463

1,695

6

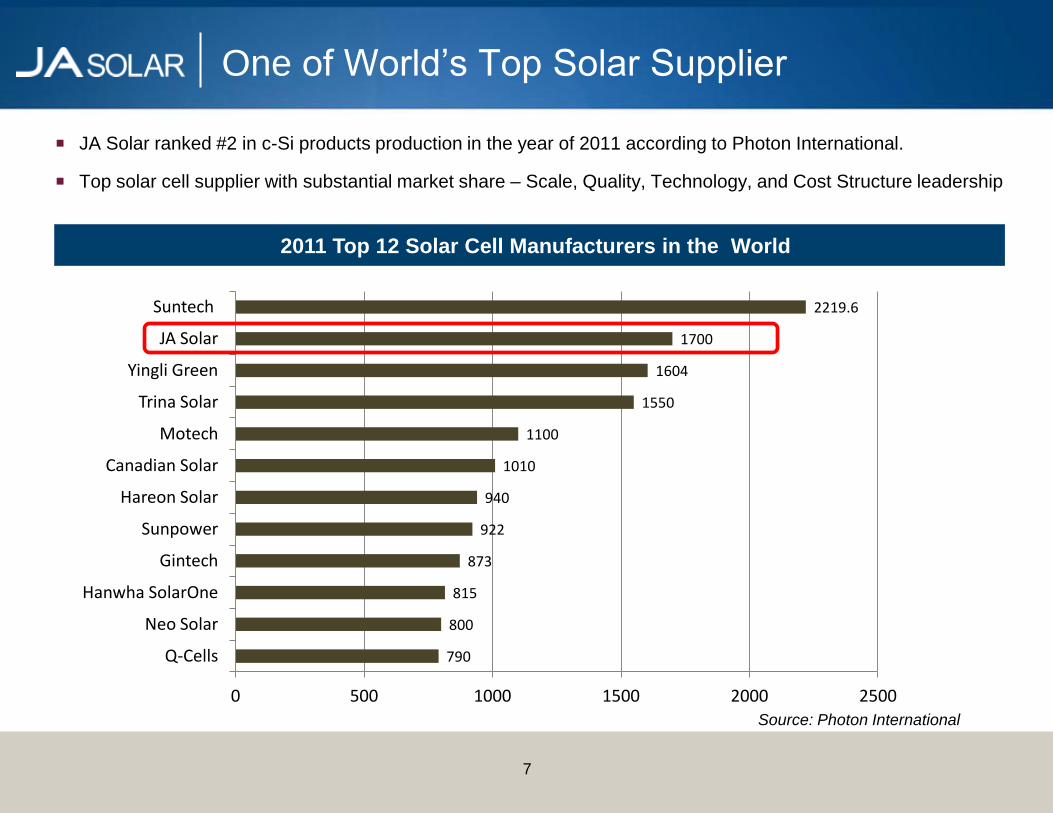

JA Solar ranked #2 in c-Si products production in the year of 2011 according to Photon International.

Top solar cell supplier with substantial market share – Scale, Quality, Technology, and Cost Structure leadership

7

2011 Top 12 Solar Cell Manufacturers in the World

One of World’s Top Solar Supplier

790

800

815

873

922

940

1010

1100

1550

1604

1700

2219.6

0 500 1000 1500 2000 2500

Q-Cells

Neo Solar

Hanwha SolarOne

Gintech

Sunpower

Hareon Solar

Canadian Solar

Motech

Trina Solar

Yingli Green

JA Solar

Suntech

Source: Photon International

JA Solar Milestones

8

May 2005

Ningjin Jinglong

Zhong’ao

Established

Apr 2006

1st Commercial

Production

Ningjin 25MW

Dec 2007

JA Corporate HQ

established in Shanghai

“JA PLAZA BUILDING”

Sept 2008

New Yangzhou

Fab Mass

Production

Achieved

Q4 2009

Established module

business in Shanghai

and wafer business in

Lianyungang

Feb 2007

NASDAQ IPO

Followed by a Secondary

Offering in Oct. 2007

Nov 2005

Renamed Jing Ao Solar Co.

Limited.

The name JA SOLAR is born

Q1 2010

Achieved Shipment

Run Rate of over 1GW

Q3 2010

Achieved

Cumulative

Shipment of

Over 1GW

Q4 2010

Achieved

Capacity

of Over 2GW

Q1 2011

Establishing

Hefei Facility

with 3GW

Planned

Capacity

Q4 2011

Revenue from

Module

Business

Exceeded 55%

May 2008

Convertible

Notes Offering

in May, 2008

2005 2006 2007 2008 2009 2010 2011

9

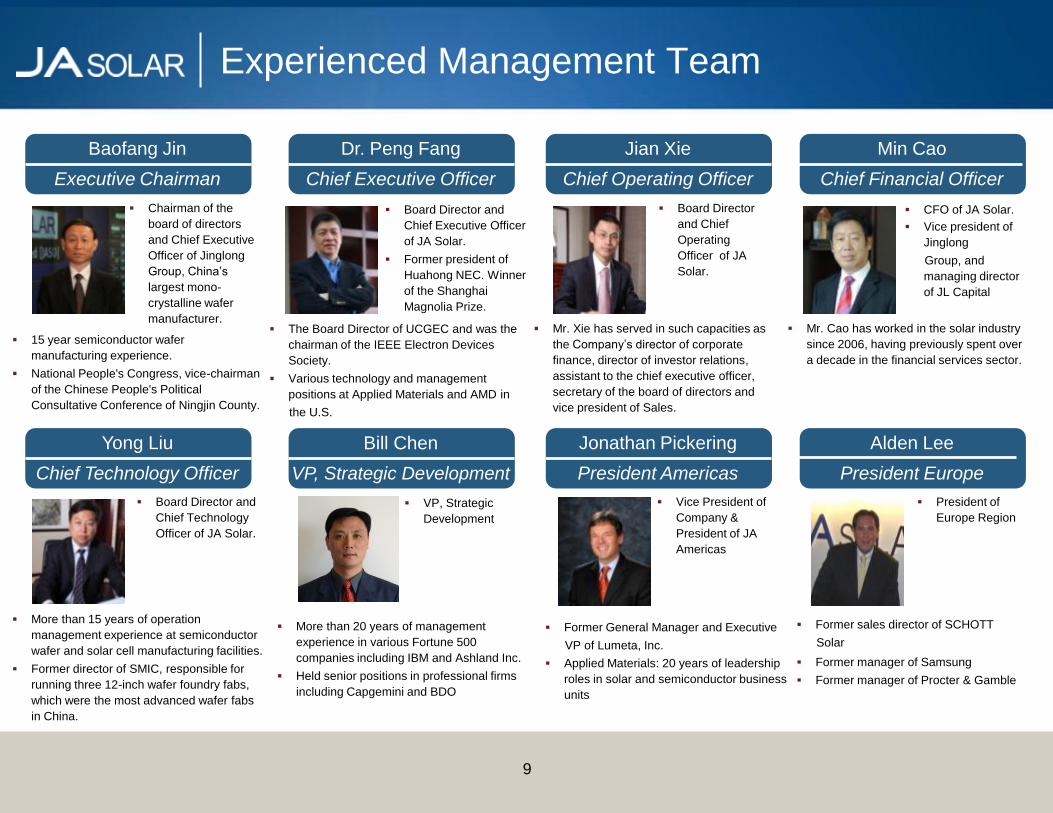

Experienced Management Team

Former General Manager and Executive

VP of Lumeta, Inc.

Applied Materials: 20 years of leadership

roles in solar and semiconductor business

units

Min Cao

Chief Financial Officer

Baofang Jin

Executive Chairman

Dr. Peng Fang

Chief Executive Officer

Jian Xie

Chief Operating Officer

Vice President of IR &

BD

15 year semiconductor wafer

manufacturing experience.

National People's Congress, vice-chairman

of the Chinese People's Political

Consultative Conference of Ningjin County.

The Board Director of UCGEC and was the

chairman of the IEEE Electron Devices

Society.

Various technology and management

positions at Applied Materials and AMD in

the U.S.

Mr. Xie has served in such capacities as

the Company’s director of corporate

finance, director of investor relations,

assistant to the chief executive officer,

secretary of the board of directors and

vice president of Sales.

More than 20 years of management

experience in various Fortune 500

companies including IBM and Ashland Inc.

Held senior positions in professional firms

including Capgemini and BDO

Chairman of the

board of directors

and Chief Executive

Officer of Jinglong

Group, China’s

largest mono-

crystalline wafer

manufacturer.

Board Director and

Chief Executive Officer

of JA Solar.

Former president of

Huahong NEC. Winner

of the Shanghai

Magnolia Prize.

Board Director

and Chief

Operating

Officer of JA

Solar.

Board Director and

Chief Technology

Officer of JA Solar.

VP, Strategic

Development

Yong Liu

Chief Technology Officer

Bill Chen

VP, Strategic Development

Jonathan Pickering

President Americas

More than 15 years of operation

management experience at semiconductor

wafer and solar cell manufacturing facilities.

Former director of SMIC, responsible for

running three 12-inch wafer foundry fabs,

which were the most advanced wafer fabs

in China.

Vice president of

Jinglong

Group, and

managing director

of JL Capital

Mr. Cao has worked in the solar industry

since 2006, having previously spent over

a decade in the financial services sector.

CFO of JA Solar.

Vice President of

Company &

President of JA

Americas

Alden Lee

President Europe

Former sales director of SCHOTT

Solar

Former manager of Samsung

Former manager of Procter & Gamble

President of

Europe Region

Customer Base

2010

JA Solar’s Modules Markets

Continuous and strong growth in module shipment

Substantial Geographic & Customer Diversification

61%

2%

15%

23%

Europ Oceania North America Asia

2011

MW

0

50

100

150

200

250

300

350

400

450

500

270 278

342 356 349 319 324

218 226

2 32

76

107 102

82 121

180 140

Cell Shipment Module Shipment

Europe

12

Substantial Geographic & Customer Diversification

Working with leading project developers, EPC companies and global OEMs. Customers include Solar-Fabrik,

MEMC/SunEdison, JABIL, Moser Baer, LANCO, CPI, China Guodian, and leading European Tier-1 solar OEMs.

We have close relationships with customers in Germany, Italy, France, Korea, Japan, India, and the US.

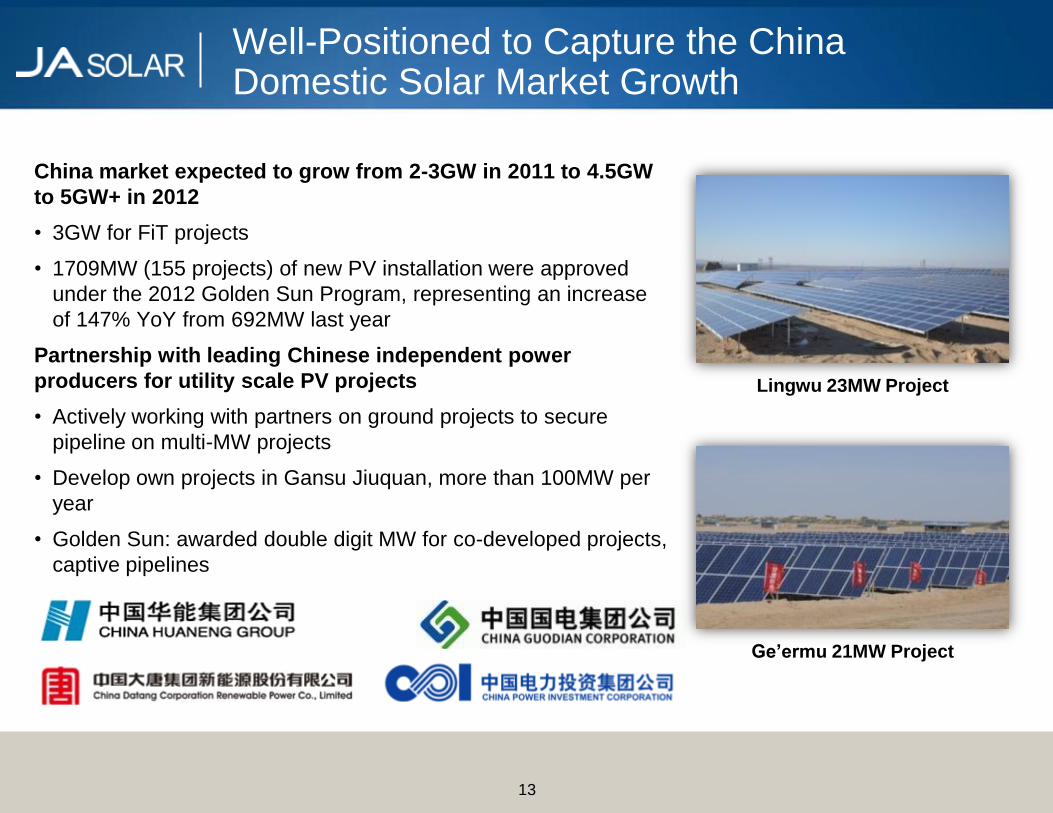

Well-Positioned to Capture the China Domestic Solar Market Growth

China market expected to grow from 2-3GW in 2011 to 4.5GW

to 5GW+ in 2012

• 3GW for FiT projects

• 1709MW (155 projects) of new PV installation were approved

under the 2012 Golden Sun Program, representing an increase

of 147% YoY from 692MW last year

Partnership with leading Chinese independent power

producers for utility scale PV projects

• Actively working with partners on ground projects to secure

pipeline on multi-MW projects

• Develop own projects in Gansu Jiuquan, more than 100MW per

year

• Golden Sun: awarded double digit MW for co-developed projects,

captive pipelines

13

Lingwu 23MW Project

Ge’ermu 21MW Project

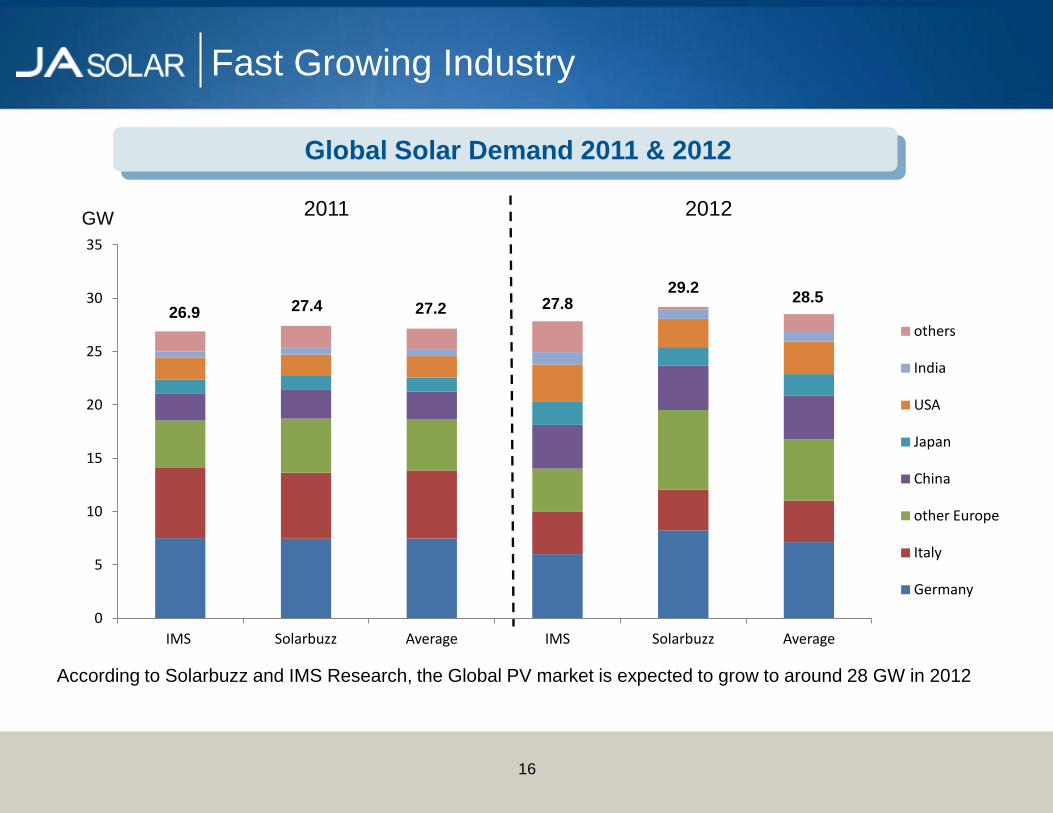

Global Solar Market

Source: Solarbuzz 2012

15

2001 - 2015 Global Solar Demand

Fast Growing Industry

0.4 0.4 0.6 1.1 1.5 1.8 2.8

6.1 7.6

18.2

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

27.4

47GW

Solarbuzz : 14.4% CAGR expected from 2011 to 2015, 47GW installations by 2015

IMS Research: 11.1% CAGR expected from 2010 – 2015, 45.5GW installations by 2015

0

5

10

15

20

25

30

35

IMS Solarbuzz Average IMS Solarbuzz Average

others

India

USA

Japan

China

other Europe

Italy

Germany

16

Global Solar Demand 2011 & 2012

Fast Growing Industry

According to Solarbuzz and IMS Research, the Global PV market is expected to grow to around 28 GW in 2012

26.9 27.4 28.5

27.2 27.8

2011 2012

29.2

GW

Manufacturing and Technology

Ningjin, Hebei province

1200MW capacity

Ningjin Cell Facility

Lianyungang, Jiangsu province

500MW capacity

Lianyungang Wafer Facility

Fengxian , Shanghai

1200MW capacity

Shanghai Module Facility

18

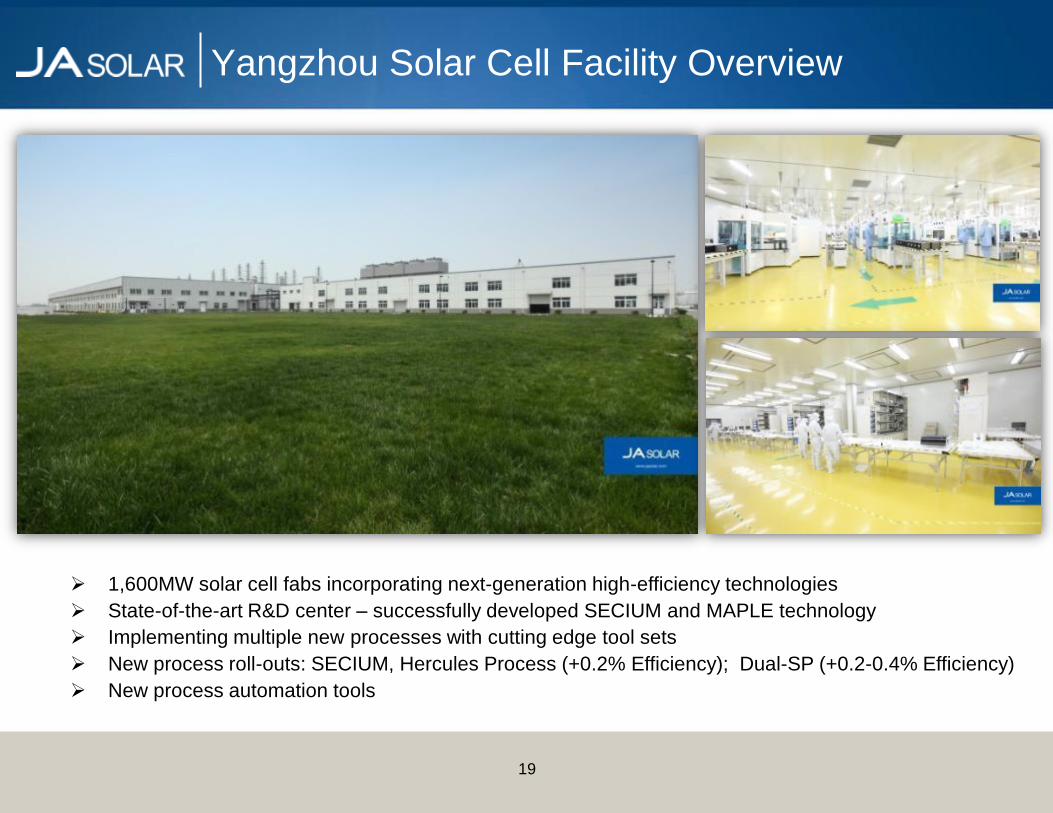

Yangzhou, Jiangsu province

1600MW capacity

State-of-the-art PV R&D Center

Yangzhou Cell Facility

Large Scale Operations

Hefei, Anhui province

3GW capacity planned by

2015

Hefei Solar Products Facility

Yanjiao, Hebei province

500MW capacity

Yanjiao Wafer Facility

1,600MW solar cell fabs incorporating next-generation high-efficiency technologies

State-of-the-art R&D center – successfully developed SECIUM and MAPLE technology

Implementing multiple new processes with cutting edge tool sets

New process roll-outs: SECIUM, Hercules Process (+0.2% Efficiency); Dual-SP (+0.2-0.4% Efficiency)

New process automation tools

19

Yangzhou Solar Cell Facility Overview

The world’s largest solar product manufacturing site with planned 3 GW solar products capacity;

500MW module production has commenced operation in February 2012

State-of-the-art facility utilizing newest automated equipment & technology

Vertical integration model – potential upstream and downstream partnerships with leading

international solar companies

Advanced R&D development – technology leadership and clear roadmap to achieve 20%+

conversion efficiency

Hefei Planned 3GW Solar Products Facility

20

1200MW module capacity by the end of 2011

World-class quality system

High quality materials

Module reliability lab partnering with TÜV and Intertek

OEM manufacturing for leading global OEMs with demonstrated quality control and assurance

21

Fengxian(Shanghai) Module Facility Overview

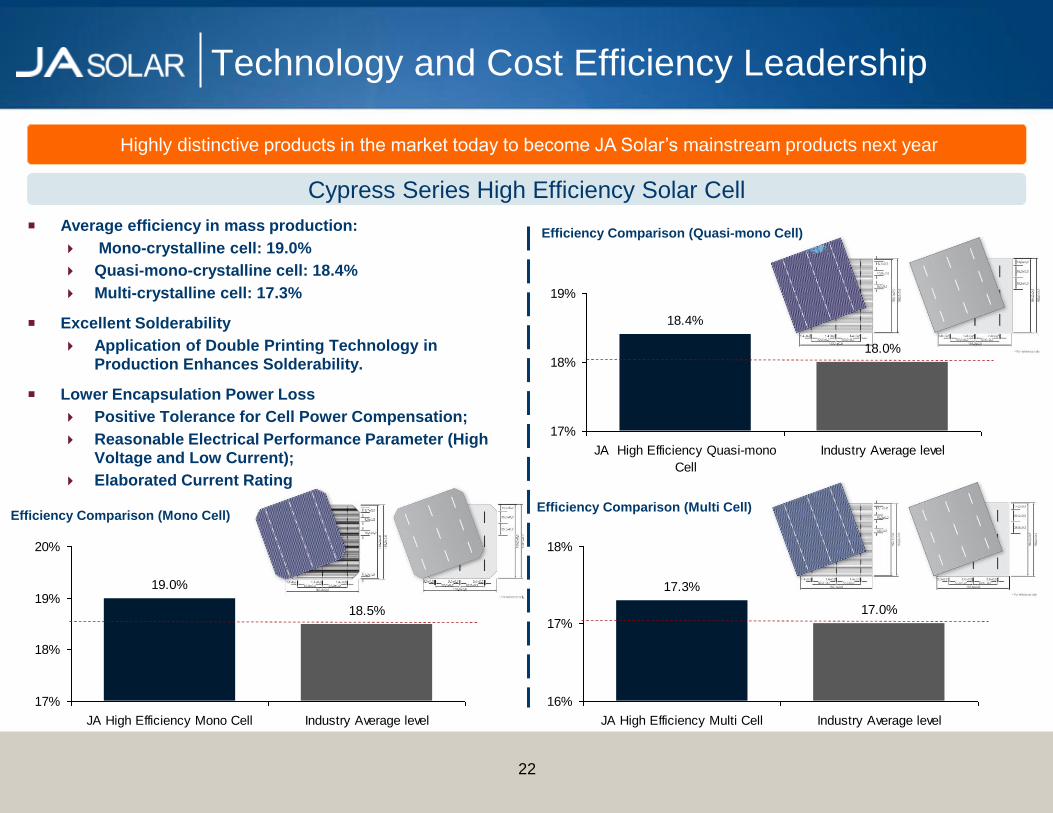

18.4%

18.0%

17%

18%

19%

JA High Efficiency Quasi-mono

Cell

Industry Average level

19.0%

18.5%

17%

18%

19%

20%

JA High Efficiency Mono Cell Industry Average level

17.3%

17.0%

16%

17%

18%

JA High Efficiency Multi Cell Industry Average level

22

Average efficiency in mass production:

Mono-crystalline cell: 19.0%

Quasi-mono-crystalline cell: 18.4%

Multi-crystalline cell: 17.3%

Excellent Solderability

Application of Double Printing Technology in Production Enhances Solderability.

Lower Encapsulation Power Loss

Positive Tolerance for Cell Power Compensation;

Reasonable Electrical Performance Parameter (High Voltage and Low Current);

Elaborated Current Rating

Cypress Series High Efficiency Solar Cell

Highly distinctive products in the market today to become JA Solar’s mainstream products next year

Technology and Cost Efficiency Leadership

Efficiency Comparison (Mono Cell)

Efficiency Comparison (Quasi-mono Cell)

Efficiency Comparison (Multi Cell)

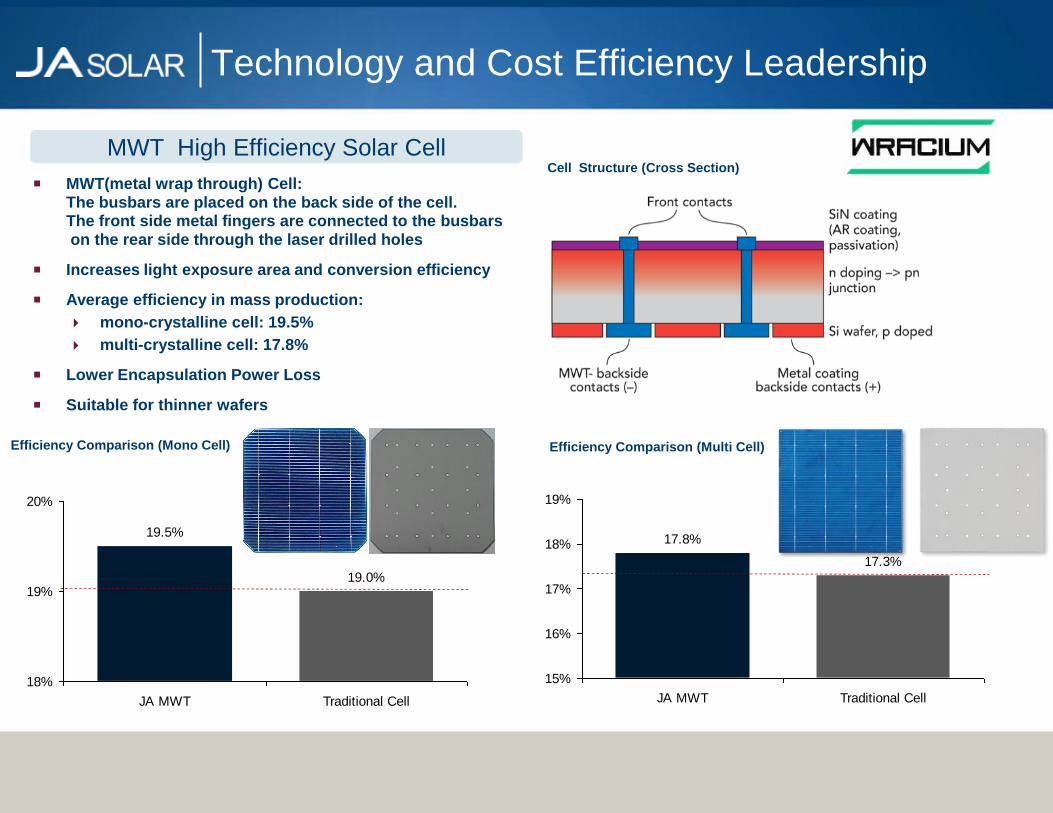

17.3%

17.8%

15%

16%

17%

18%

19%

JA MWT Traditional Cell

MWT High Efficiency Solar Cell

MWT(metal wrap through) Cell: The busbars are placed on the back side of the cell. The front side metal fingers are connected to the busbars on the rear side through the laser drilled holes

Increases light exposure area and conversion efficiency

Average efficiency in mass production:

mono-crystalline cell: 19.5%

multi-crystalline cell: 17.8%

Lower Encapsulation Power Loss

Suitable for thinner wafers

Efficiency Comparison (Mono Cell)

Technology and Cost Efficiency Leadership

19.0%

19.5%

18%

19%

20%

JA MWT Traditional Cell

Efficiency Comparison (Multi Cell)

Cell Structure (Cross Section)

Strategic Partnership with TÜV SÜD and Intertek

Cooperate with TÜV SÜD on a range of product and system testing and certification initiatives

Establish a world-class testing center to conduct IEC61215/61730 testing

TÜV SÜD has awarded Fengxian in-house laboratory TMP (Testing at Manufacturers' Premises)

certification, the only TMP laboratory of TÜV SÜD worldwide to date in the photovoltaic industry

Ability to perform in-house reliability and accelerated life time testing

Shorten the certification process duration and improve cost efficiencies

Manufacturing control recognized by TUV and Intertek

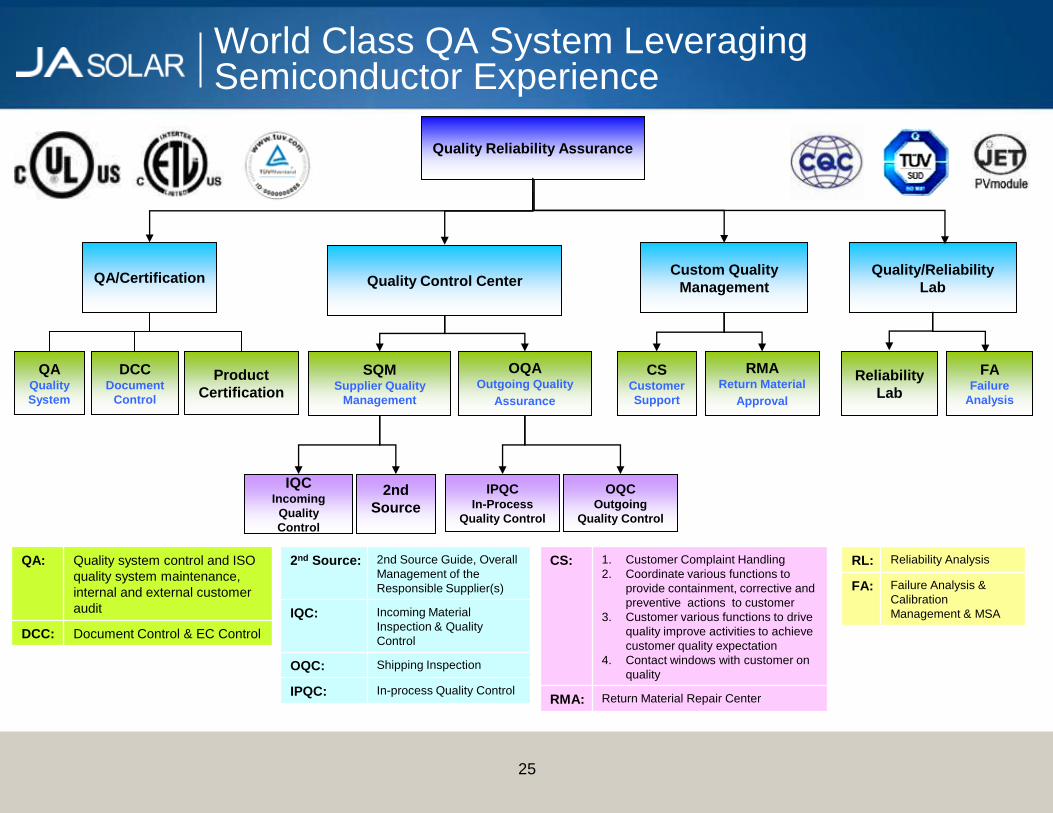

Quality Reliability Assurance

Custom Quality

Management

RMA Return Material

Approval

CS Customer

Support

OQA Outgoing Quality

Assurance

Quality Control Center

SQM Supplier Quality

Management

IQC Incoming

Quality

Control

2nd

Source

IPQC In-Process

Quality Control

QA/Certification

QA Quality

System

DCC Document

Control

Product

Certification

Quality/Reliability

Lab

Reliability

Lab

FA Failure

Analysis

OQC Outgoing

Quality Control

25

World Class QA System Leveraging Semiconductor Experience

QA: Quality system control and ISO

quality system maintenance,

internal and external customer

audit

DCC: Document Control & EC Control

2nd Source: 2nd Source Guide, Overall

Management of the

Responsible Supplier(s)

IQC: Incoming Material

Inspection & Quality

Control

OQC: Shipping Inspection

IPQC: In-process Quality Control

CS: 1. Customer Complaint Handling

2. Coordinate various functions to

provide containment, corrective and

preventive actions to customer

3. Customer various functions to drive

quality improve activities to achieve

customer quality expectation

4. Contact windows with customer on

quality

RMA: Return Material Repair Center

RL: Reliability Analysis

FA: Failure Analysis &

Calibration

Management & MSA

Financial Performance

Shipment and Revenue

Revenue (US$ mn)

Shipment (MW)

177 231

272 311

418 463 451

401 445

398 366

2009Q3 2009Q4 2010Q1 2010Q2 2010Q3 2010Q4 2011Q1 2011Q2 2011Q3 2011Q4 2012Q1

193 238

279 351

541 584 556

413 388 309

254

2009Q3 2009Q4 2010Q1 2010Q2 2010Q3 2010Q4 2011Q1 2011Q2 2011Q3 2011Q4 2012Q1

Source: 2012Q1 Company Earning Releases

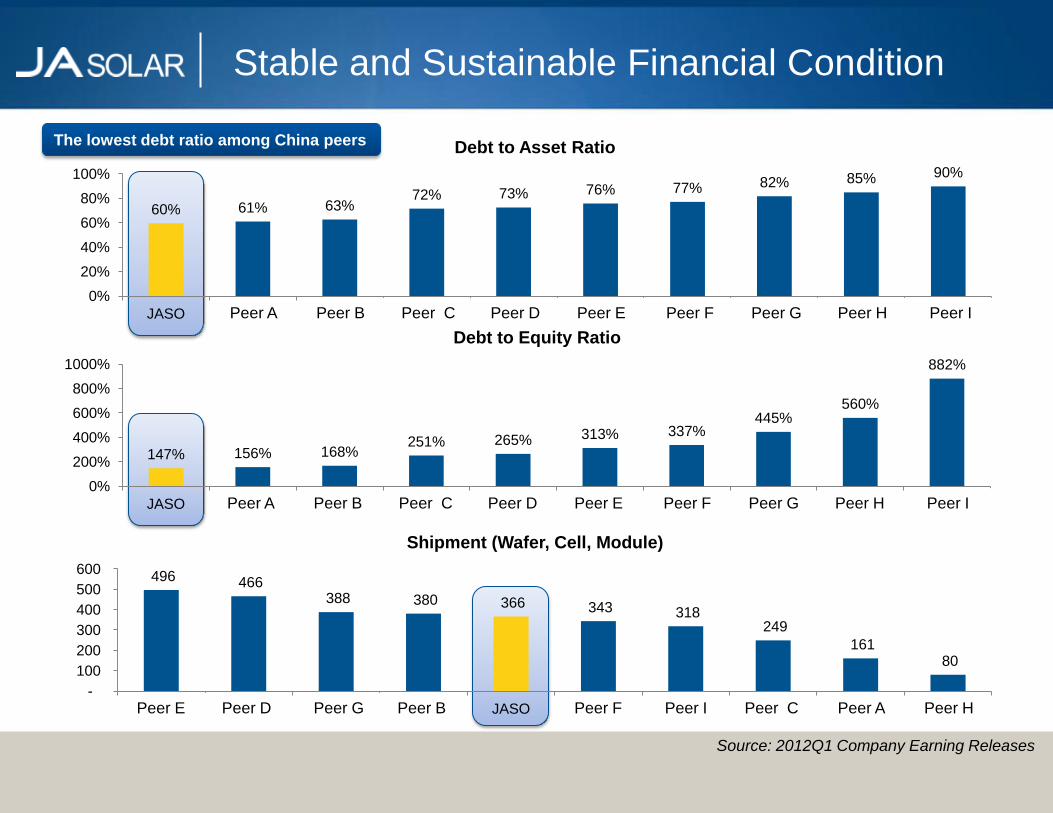

Stable and Sustainable Financial Condition

60% 61% 63% 72% 73% 76% 77% 82% 85% 90%

0%

20%

40%

60%

80%

100%

JASO HSOL TSL JKS SOL YGE CSIQ STP CSUN LDK

Debt to Asset Ratio

147% 156% 168% 251% 265% 313% 337%

445% 560%

882%

0%

200%

400%

600%

800%

1000%

JASO HSOL TSL JKS SOL YGE CSIQ STP CSUN LDK

Debt to Equity Ratio

496 466 388 380 366 343 318

249

161 80

-

100

200

300

400

500

600

YGE SOL STP TSL JASO CSIQ LDK JKS HSOL CSUN

Shipment (Wafer, Cell, Module)

The lowest debt ratio among China peers

Peer A Peer B Peer C Peer D Peer E Peer F Peer G Peer H Peer I

Peer A Peer B Peer C Peer D Peer E Peer F Peer G Peer H Peer I

Peer A Peer B Peer C Peer D Peer E Peer F Peer G Peer H Peer I

Strong Balance Sheet to Sustain Market Cycle

• Strong cash position and low liabilities ensure long-term

viability

Cash and cash equivalents of over 676.2 million as of the

end of 2012Q1

Among lowest debt-to-asset ratios in industry

• Long-term partnerships with the top domestic and international

banks as well as premier financial institutions

RMB 30 billion credit agreement with China Development

Bank

Strategic cooperation agreement with Wells Fargo

Supported by Leading Banks:

0.0

500.0

1000.0

1500.0

2000.0

2500.0

2011Q2 2011Q3 2011Q4 2012Q1

In m

illio

n U

SD

Liabilities and Stockholders’ Equity

Current Liabilities

Non-Current Liabilities

Stockholders' Equity

0.0

500.0

1000.0

1500.0

2000.0

2500.0

2011Q2 2011Q3 2011Q4 2012Q1

In m

illio

n U

SD

Assets

Cash & Cash Equivalents

Current Asset Excluding Cash & Cash Equivalents

Non-Current Asset

$676.2 million

in cash

Industry Leader with Stable Financial Position – Financial Times Deutschland

Financial Times Deutschland:

“Während die wenigsten Unternehmen im vergangenen Jahr eine hohe relative Marktperformance vorweisen konnten, verfügte jedoch zumindest die Hälfte über eine stabile Finanzkraft. Deutsche Vertreter dieser Gruppe sind Branchenprimus Solarworld sowie Aleo Solar, Payom Solar und die Solarfabrik. Aus den USA gehören First Solar und aus China Trina und JA Solar dazu.“

English translation:

“In the recent years, of the companies that performed relatively well, only few of them have a stable financial position. German representatives of this group are industry

leader SolarWorld, Aleo Solar, Payom Solar, and Solarfabrik. Other industry leaders with stable financial position are First Solar from the United States and Trina and JA Solar from China.”

- Die Solarbranche kann es noch schaffen, April 13, 2012. Financial Time Deutschland

Investment Thesis Summary

Growing customer base and geographic diversification

Strong management team with proven execution

Technology and cost leadership

Strong balance sheet for future growth

Clear R&D Roadmap to increase efficiency >20%

31

Thank you!