jaimeappropriate institutional setting for public debt

TRANSCRIPT

Jaime Delgadillo Cortez

Revised 31 July 2007

DRAFT Paper prepared for UNCTAD

Appropriate Institutional Setting for Public Debt

Management

- 2 -

Executive Summary

External shocks as well as weak institutions dealing with public debt management can be major sources of debt distress in emerging economies. Shocks cannot be totally controlled, but the institutional setting for effective debt management can be strengthened. Effective debt management ensures that both the level - and growth - of debt are fiscally sustainable. It means clear objectives for public debt management are defined and debt management objectives and practices with macroeconomic policies are carefully coordinated. An appropriate institutional setting for debt management can contribute to achieving the objectives of effective debt management. These include governance arrangements, clarity of roles of institutions dealing with debt management, specified objectives for public debt management, coordination of public debt management with other public policies, organizational structure of Debt Management Offices and transparency and accountability. Many government institutions dealing with debt management face a number of challenges, ranging from lack of adequate governance arrangements,, to inappropriate organizational structures, and lack of professional staff and tools. Many of these constraints could be resolved by the creation of effective Debt Offices and strengthening of these offices’ ability to manage the debt portfolio more efficiently. In many cases this can be accomplished by reviewing the institutional and legal arrangements for these offices and if necessary introducing proper reforms. Public Debt is often the largest liability of low and middle-income countries. The management of these liabilities cannot be seen as isolated from the overall macroeconomic management of a country. An inadequate or risky debt structure can have an adverse impact on the stability of the financial sector often leading to debt crisis Debt offices can have an important role to play in preventing debt crisis, but in order for them to do so, they first need to develop their own capabilities and skills for the implementation of sound medium-term debt strategies, management of the debt portfolio and in order for them to contribute to the performance of debt sustainability analysis, including fiscal sustainability of debt, in coordination with other areas of the government. Debt management objectives must be clearly defined and published and the policies regarding risk and cost should be disclosed. The responsibilities and roles attached to each institution regarding debt management must be clearly spelled out. In the absence of clarity of responsibilities, lack of coordination can lead to uncertainties and higher transaction and borrowing costs. Consolidated authority for debt management in a single office, for example, and a well-structured DMO can contribute enormously to transparency and accountability. The objectives for debt management should encompass all types of government obligations, including domestic and external debt and contingent liabilities. The existence of a single institution in charge of implementing debt policies permits a greater attention and concentration to debt management issues and provides support to the idea of ensuring a clear separation between fiscal, monetary and debt management policies. The establishment of an appropriate structure for the DMO is crucial to perform management functions and control of public debt. These management functions would be performed according to strategies and policies elaborated by the authorities.

- 3 -

The DMO should have all the required personnel to respond efficiently to its mandates, and a policy of adequate remuneration to attract and retain qualified staff. Coordination across agencies and macroeconomic objectives is crucial for effective debt management. Consultations are indispensable especially if there are potential conflicts among debt management strategy, monetary and fiscal policies and exchange rate policies. A formal coordinating body in the form of an executive debt committee may aid in sharing information across policy makers and implementing agencies and in clarifying roles and responsibilities. Best practice suggests that the organizational structure of a DMO should be in the form of a front, middle, back office structure. The Back Office centralizes all the operations related to the registration of the operations of public debt and production of statistical information. The main function of the Middle Office is to conduct the analytical work required for assisting the executive debt management levels in designing a debt strategy and a framework for risk monitoring and control. The functions of the Front Office are related to the gathering of financial resources to cover the public sector needs. Therefore, comprises the use of various sources of funds, whether domestic or external, and all the processes involving the negotiation and contract of new borrowing. Ideally debt management functions should be consolidated in a single office, under the Ministry of Finance, the latter being ultimately accountable for incurring debt on behalf of the government.

- 4 -

Table of Contents INTRODUCTION...........................................................................................................................5

PART I THE CONTEXT OF THE INSTITUTIONAL SETTING FOR DMO’S ...................7

a) The need to prevent debt crisis. The challenges and constraints facing DMO’s. Obstacles to management....................................................................................................7

b) Public debt management as an integral part of the broad framework of macroeconomic policies ......................................................................................................9

PART II THE ROLE AND ORGANIZATION OF A DEBT MANAGEMENT OFFICE.....12

a) Governance issues. Legal framework. The need for clear mandates, role and jurisdiction. Clear designation of authority to incur and manage debt. Accountability and transparency.......................................................................................12

b) Policies and procedures, including operational aspects...................................................14

c) The separation of Executive Debt Management and Operational Debt Management ......................................................................................................................17

d) The need for an Executive Public Debt Management Committee. Functions. Designation of policy. Coordination issues.......................................................................19

e) The setting of a DMO in a Front, Middle, Back Office structure. ....................................21

f) Location of the DMO.........................................................................................................28

ANNEX I OPERATIONAL RISKS.......................................................................................29

ANNEX II A SEPARATE DMO, THE CASE OF NIGERIA ................................................30

LIST OF ABBREVIATIONS .......................................................................................................33

- 5 -

INTRODUCTION External shocks as well as weak institutions dealing with public debt management in transition and emerging economies can be major sources of debt distress. Shocks cannot be totally controlled, but the institutional setting for debt management can be strengthened. Literature on debt management 1 suggests that there is a strong relationship between the quality of institutions involved in debt management and the degree of debt distress in developing and emerging economies. It could therefore be deducted that debt intolerance could be reduced or better managed when solid institutions are in place. Institutions need to review periodically their arrangements and make adjustments to changing external and internal circumstances. Public debt management can be defined as the process of establishing and executing a strategy for managing the government’s debt portfolio in order to meet government funding requirements, achieve objectives with regard to costs and risks, and meet any other objectives related to debt, such as promoting investment for economic growth and to develop the domestic financial market for government securities. Effective debt management ensures that both the level - and growth - of debt are fiscally sustainable. It defines clear objectives for public debt management and carefully coordinates debt management objectives and practices with macroeconomic policies2. In emerging and transition economies emphasis in debt management is largely put on the production on the production of reliable debt data and improving the quality of the debt database , on market development, ensuring adequate financing for developmental and social needs, ensuring compliance with debt service, controlling contingent liabilities, negotiating agreements with creditors, performing cost/risk analysis, and designing strategies to attain a sustainable debt position. An appropriate institutional setting for debt management can contribute to achieving the objectives of effective debt management. Institutional arrangements would necessarily focus on a number of aspects:

• Governance arrangements • clarity of roles of institutions dealing with debt management • specified objectives for public debt management • coordination of public debt management with other public policies • organizational structure of DMOs • transparency and accountability

This document is divided in two parts. Part I refers briefly to the Context of Public Debt Management, including the challenges of DMOs and public debt management as an integral part of the broad framework of macroeconomic policies. Part II examines the different issues related to the institutional set up of debt management, including governance issues; mandates; accountability and transparency; the separation of executive debt management and operational debt management and the need for an executive debt management committee. The document focuses more extensively on the role, organization and functions of DMOs in low and middle-income countries from an institutional development perspective.

1 See IMF publications on debt management. 2 IMF World Bank Guidelines on Debt Management, 2002; and DMFAS Effective Debt Management a Revision, forthcoming.

- 6 -

DMOs need to develop their own capabilities and skills to implement medium-term debt strategies, manage the costs/risks of the debt portfolio and to conduct debt sustainability analysis, a task to be done in a concerted effort with other governmental organizations.

- 7 -

PART I THE CONTEXT FOR PUBLIC DEBT MANAGEMENT

a) The challenges and constraints facing institutions dealing with debt management .

Pro-active debt management is essential under changing market conditions. For example, DMOs must face the challenge of the globalization of capital markets, the volatility of capital flows, a more complex creditor’s portfolio. Furthermore, emerging market economies are obtaining substantial financing from private sources in the form of bonds or equity flows. There are external factors beyond the authority’s control, such as volatility in the price of export products, exchange rate and interest rate fluctuations, contagion effects, etc, but in normal circumstances DMOs can play a crucial role in crisis prevention and resolution. Inadequate legal arrangements or lack of clarity of designation, inappropriate organizational structures, inadequate staff, lack of clear definitions of functions, insufficient training, absence of strategic objectives and responsibilities are frequent in many DMOs. Absence of strong middle offices equipped to conduct analytical work often result in the absence of a debt strategy. Unclear debt management objectives, benchmarks, inability to conduct Debt Sustainability Analysis (DSA), lack of efficient tools available are also part of the problems in many debt management offices There are often deficiencies in implementation of strategies and lack of coordination with monetary and fiscal policies. There are also other factors beyond the scope of work of DMOs, which eventually impede their efficient performance such as structural deficiencies in the money markets, as well as in the primary and secondary markets, or inadequate management of quasii-fiscal deficits or international reserves. Some DMOs do not have the resources, a clear mandate, the means or the level to get a clear message to the authorities. It is not the intention of this document to address all of these issues. However many of the above referred constraints and challenges facing DMOs today, can be addressed by strengthening the ability of DMOs to manage their debt portfolio, by reviewing the present institutional and legal arrangements for debt management and if necessary by introducing appropriate reforms.

- 8 -

Figure 1

Figure 1 above illustrates the core activities typically performed by DMOs in low income and middle-income countries. In the first case, the basic role of debt management is described as concentrating mainly on dealing with captive markets for domestic debt and for a heavy reliance on concessional financing or grants. Government instruments are characterized by its short-term nature and high interest rates. DMOS in this case concentrate heavily on the development of the primary and secondary markets in an attempt to diversify the debt portfolio and eventually accessing the international capital markets. In the case of middle-income countries, debt management has a more expanded role. DMOs are engaged with managing cost/risk, conducting transactions in derivative markets, providing extended financial services to the government, and eventually participating in a wider integrated risk management with other areas of public financial management3.

3 For example see The Changing Role of the Public Debt Manager, presentation made by Phillip Anderson, World Bank, 2005 UNCTAD’s Fifth Inter-Regional Debt Management Conference.

Low-Income Countries

Debt Management

Expanded Role

Middle-Income Countries

Debt Management Basic Role

Integrated Risk Management Gov. Financial

Services. Financial Asset Mgt. Cost/Risk Management.

Transactions in Derivative Markets

Operational Risk Management.

Access Int. Capital Markets Diversify Debt Portfolio

Develop Domestic Primary & Secondary Markets

Issue Short Term Govt. Securities, Captive Sources

Reliance on ODA, IDA Grants

- 9 -

b) Public debt management as an integral part of the broad framework of macroeconomic policies

Figure 2 below explains the relationship between Public Debt and some key sectors of the economy such as the external and the real sectors. Public investment programs are financed with internal or external resources in the form of loans or grants, adding to the share of the country’s rate of social and economic growth. Debt flows are recorded in the Balance of Payments. Debt sustainability analysis basically relates public debt information with Balance of Payments data and macroeconomic variables, including growth objectives and economic and social programs. Information regarding debt stocks and flows (including debt service and disbursements), interest rates, exchange rates, capital account movements, etc are combined to determine the size of the financing gap, which needs to be filled with a combination of external and domestic financing, or if necessary with debt restructuring or debt relief operations. . Given the importance of domestic debt in many countries, its connotations with public finances and the necessity of incorporating it into the overall management of government’s liabilities, the concept of Total Public Debt is used in this paper, meaning the inclusion of both external as well as domestic debt.

Figure 2

EXTERNAL SECTOR

RE

AL

SE

CTO

R

PUBLIC FINANCIAL SECTOR

PUBLIC DEBTEXTERNAL

Flow chart for public debt management in developing economieswithin macroeconomic framework

Disburse

ment receipts

Debt servi

ce paym

ents

Principal &

interest

Financing projects

Imports - Exports

Loca

l cur

ren

cy

Internal FinancingRequirements

Tax and revenues

Local counterpart fundsP

ublic investment program

s

G.D.P. B.O.P.

BUDGET

DOMESTIC DEBT

External Financing requirementsLoans and grants

Growth Objectives

- 10 -

Public Debt is often the largest liability of low and middle-income countries. The management of these liabilities cannot be seen as isolated from the overall macroeconomic management of a country. There is a strong recognition of debt management linkages with macroeconomic and financial stability. An inadequate or risky debt structure can have an adverse impact on the stability of the financial sector. Therefore, the objectives for fiscal, monetary and public debt policy should be coordinated to achieve and maintain debt sustainability and fiscal discipline An effective public financial management system is essential for successful macroeconomic management and crucial to providing reliable financial information to deter fraud, waste and abuse of public resources. Public debt management, as part of public financial management can significantly contribute to the attainment of an efficient financial management system. Relevant information on debt management strategies, debt sustainability analysis, public debt stocks and flows, are essential ingredients for the development and implementation of public finances. This is particularly applicable in the context of budgeting and expenditure management. In this area governments want to improve planning and budget formulation; set realistic and achievable spending ceilings; improve spending prioritization; monitor commitments and disbursements; and ensure accurate and timely information flows among government institutions. As it is noted in the World Bank’s Public Expenditure Management Handbook, theory and practice show that a country’s institutions - both formal and informal - have a decisive influence on budgetary outcomes at three levels. At a first level, the introduction of institutional reforms in public financial management aims to improve aggregate fiscal discipline and planning and the traditional control functions of public expenditure management to establish budget parameters. At a second level, these reforms aim to improve the planning function of public expenditure management through improvements in the capacity to allocate resources in accordance with strategic priorities and baseline data from prior expenditures and revenue patterns. While budgeting can be seen as a technical exercise, ultimately it is the expression and platform for political decision-making over the utilization of scarce resources for selected priorities.

- 11 -

Figure 3

Integrated Debt Management Information Flows

Central Bank

InternationalOrganizations

Creditors

National Planning /Development Office

Debt Service

BOP InformationPrivate Debt

Public InvestmentSocial & Economic Projects

Grants

Marcoeconomic Objectives

Stocks & Flows

Records on Balances

DMO

- Budget

- Treasury

- Accounting

Debt Service Projections

Fiscal Targets

Debt Stocks & FlowsDebt Exchange Rates

Interest Rates

Disbursement Projections

Internal/External FinancingRequirements

Budget

CONGRESS

Public/Private Entities(guarantees)

Information on guarantees

Ministry of Finance :

The Figure above illustrates the flows of information between a consolidated DMO and its main stakeholders: the Ministry of Finance, the Central Bank, the National Planning Agency, and the creditors, including International Organizations. Incoming and outgoing information to and from the DMO contribute to maintaining a close and coordinated relationship regarding debt management among key institutions. This exchange in turn facilitates the implementation of debt management operations in a timely and appropriately way i.e. debt service payments; and enables the DMO to assist the government in conducting debt sustainability analysis.

- 12 -

PART II THE ROLE AND ORGANIZATION OF A DEBT MANAGEMENT OFFICE

a) Governance issues. Legal framework. The need for clear mandates, role and jurisdiction.

Clear designation of authority to incur and manage debt. Accountability and transparency.

The legal framework should clarify the authority to borrow and to issue new debt, invest, and undertake transactions on the government’s behalf .The organizational framework for debt management should be well specified, and ensure that mandates and roles are well articulated. Legal arrangements should be supported by delegation of appropriate authority to debt managers (IMF-World Bank Guidelines). Debt management objectives must be clearly defined and published and the policies regarding risk and cost should be disclosed. The responsibilities and roles attached to each institution regarding debt management must be clearly spelled out. In the absence of clarity of responsibilities, lack of coordination can lead to uncertainties and higher transaction and borrowing costs. Consolidated authority for debt management in a single office and a well-structured DMO can enormously contribute to transparency and accountability. The objectives for debt management should encompass all types of government obligations, including domestic and external debt and contingent liabilities. Legislation on fiscal responsibility can add to debt management regulations in order to foster fiscal discipline and bring the debt management objectives in line with the fiscal targets. This is particularly important when local government have a certain degree of independence to incur debts, both foreign and domestic, especially in federal countries. Delegation is the efficient allocation of powers to people with the appropriate ability and/or experience. Delegation is necessary in order for senior management to achieve all required tasks in a timely manner. An Act of Parliament usually stipulates that the Minister of Finance may delegate to the DMO specific powers, duties and functions that pertain to the management of public debt. This helps the DMO to conclude transactions in a timely manner, better take advantage of market opportunities, and ensure that projects are funded in the fiscal year in which they were budgeted for. These benefits could equally apply to concessional funding, inasmuch as loan negotiations may have concluded but projects not be implemented on time, due to decision-making delays caused by inadequate delegation. The degree of delegation may depend on the number of financial transactions the DMO undertakes every year. .Ministers of Finance therefore face decisions as to what borrowing and investment powers to delegate, whom to delegate these authorities to and how much decision-making authority to vest. These can be difficult decisions and governments tend to be cautious in making them.

- 13 -

Delegation implies accountability. Therefore, it is highly desirable that an Act of Parliament determine that the Minister of Finance file an annual or semi-annual report with Parliament on past activities related to public debt management, and on plans regarding public debt management in the next fiscal year. This helps promote transparency and accountability, and encourages a debate on these issues, inasmuch as civil society has a better understanding of the country’s debt situation. Investors, as well as international financial institutions, would also have a better knowledge of the government’s future funding plans, as well as its developmental priorities. Therefore, borrowing could be less donor driven, and more in line with government priorities.

BOX 1

DMOs Main Functions and Responsibilities

• To implement the debt strategy, debt management policies, procedures, benchmarks and guidelines prescribed in the regulations designed by the executive levels of debt management;

• To issue debt or to contract debt on behalf of the Minister of Finance while minimizing risk and to participate in debt sustainability analysis together with other areas of the government, to alert the authorities of any possible situation of unsustainable debt and to recommend timely adjustments when needed;

• To maintain a timely and reliable database on public debt and to conduct regular data validation;

• To minimize costs and risks associated with public borrowing and publicly issued guarantees;

• To order debt service payments to the financial agent of the central government through the Treasury and/or the Budget Department, for the loans borrowed and the bonds issued directly or on behalf of the central government.

• To generate and provide reliable and timely information on public debt policies and data to a variety of users and to the public in general on a periodic basis and/or through the internet;

• To eventually extend government guarantees through a risk analysis evaluation. The Congress on annual basis through the budget law normally authorizes the guarantee coverage. The DMO should monitor all forms of contingent liabilities;

• To monitor the loans borrowed and bonds issued by entities and enterprises pertaining the central government;

• To monitor sub national debt, including the loans borrowed and bonds issued by the local governments, as well as the loans and bonds borrowed or issued by local government’s entities;

• To monitor grants, private external debt and on-lending extended to public or private entities

- 14 -

Sound practice sovereigns usually implement regular auditing of the financial transactions undertaken by the debt managers to assess their compliance with generally accepted accounting practices and the government’s portfolio management policies and comprehensive reporting of financial performance to the Minister of Finance and/or Parliament. This reporting would review the financial transactions undertaken, assess the risks in the portfolio and the compliance with the risk management framework. Sometimes multiyear targets are established in the form of a preset limit or debt ceiling. If the government is undertaking many financial transactions it is inefficient to require all transactions or elements of transactions to be approved by the Minister of Finance. MEFMI, South African Debt Office and The World Bank, Sovereign Debt Management, Cash Management, & Domestic Market Development: Malawi, (2000).

b) Policies and procedures, including operational aspects Risks of government losses from inadequate operational controls should be managed according to sound business practices, including well-articulated responsibilities for staff, and clear monitoring and control policies and reporting arrangements. Debt management activities should be supported by an accurate and comprehensive management information system with proper safeguards. Staff involved in debt management should be subject to a code-of-conduct and conflict-of interest guidelines regarding the management of their personal financial affairs. A framework should be developed to enable debt managers to identify and manage the tradeoffs between expected cost and risk in the government debt portfolio. To assess risk, debt managers should regularly conduct stress tests of the debt portfolio on the basis of the economic and financial shocks to which the government – and the country more generally – are potentially exposed.(IMF-World Bank Guidelines)

BOX 2

Legal and Regulatory Processes for Debt Issuance

A Debt Management Office needs to be able to operate in a legal and regulatory environment, which ensures that debt issuance is consistent with specified borrowing limits, and where there is no legal uncertainty that might undermine the confidence of investors as to the obligation to service and repay government debt. The authority to borrow should be clear, as should delegation of authority, and subsequent accountability and reporting. Many governments have in place legislation relating to powers to borrow, invest, and enter into other financial obligations, as well as requirements to report those decisions to the parliament through budget documentation, and/or other government financial reporting. Usually this legislation authorizes the Minister of Finance to conduct all borrowing and related financial transactions on behalf of the government and establishes a maximum amount of new funding and guarantees that the Congress, Parliament, or the Minister of Finance can approve over a specified period (usually one year). This overcomes the need to request specific authorizations from Congress or Parliament for individual transactions, which may introduce a range of political factors into the decision making and considerably delay the execution of transactions.

- 15 -

BOX 3

Types of Risks Market Risk: The risk associated with changes in market prices, such as interest rates, exchange rates, commodity prices, on the cost of the government’s debt servicing. For both domestic and foreign currency debt, changes in interest rates affect debt-servicing costs on new issues when fixed rate debt is refinanced, and on floating rate debt at the rate-reset dates. Hence, short-duration debt (short-term or floating rate) is usually considered to be more risky than long-term, fixed rate debt. (Excessive concentration in very long-term, fixed rate debt also can be risky as future financing requirements are uncertain.) Debt denominated in or indexed to foreign currencies also adds volatility to debt servicing costs as measured in domestic currency owing to exchange rate movements. Bonds with embedded put options can exacerbate market and rollover risks. Rollover Risk: The risk that debt will have to be rolled over at an unusually high cost or, in extreme cases, cannot be rolled over at all. To the extent that rollover risk is limited to the risk that debt might have to be rolled over at higher interest rates, including changes in credit spreads, it may be considered a type of market risk. However, because the inability to roll over debt and/or exceptionally large increases in government funding costs can lead to, or exacerbate, a debt crisis and thereby cause real economic losses, in addition to the purely financial effects of higher interest rates, it is often treated separately. Managing this risk is particularly important for emerging market countries. Liquidity Risk: There are two types of liquidity risk. One refers to the cost or penalty investors face in trying to exit a position when the number of transactors has markedly decreased or because of the lack of depth of a particular market. This risk is particularly relevant in cases where debt management includes the management of liquid assets or the use of derivatives contracts. The other form of liquidity risk, for a borrower, refers to a situation where the volume of liquid assets can diminish quickly in the face of unanticipated cash flow obligations and/or a possible difficulty in raising cash through borrowing in a short period of time. Credit Risk: The risk of non-performance by borrowers on loans or other financial assets or by a counterparty on financial contracts. This risk is particularly relevant in cases where debt management includes the management of liquid assets. It may also be relevant in the acceptance of bids in auctions of securities issued by the government as well as in relation to contingent liabilities, and in derivative contracts entered into by the debt manager. Settlement Risk: The potential loss that the government, as a counterparty, could suffer as a result of failure to settle, for whatever reason other than default, by another counterparty. Operational Risk: This includes a range of different types of risks, including transaction errors in the various stages of executing and recording transactions; inadequacies or failures in internal controls, or in systems and services; reputation risk; legal risk; security breaches; or natural disasters that affect business activity Source: World Bank/IMF Guidelines

- 16 -

In order to help guide-borrowing decisions and reduce government’s risk, debt managers should consider the financial and other risk characteristics of the government’s cash flows. The risk management framework complements the debt portfolio management approach. The portfolio benchmarks reflect the level of risk that is acceptable to the DMO. Operational risks arise in the normal course of managing debt transactions ( see Annex I on Operational Risks). The responsibility for identifying and developing plans to manage them lies with management. A risk plan would describe procedures to minimize damages caused by risks. The New Zealand DMO’s internal operations are managed through an established risk culture, policies, ethical guidelines and codes of conduct, defined responsibilities and accountabilities, formal delegations, segregated duties, limits, reporting and performance management requirement, and established processes DMOs can implement a ‘Code of Conduct for Staff and Management’ that rests on a tripod of: professionalism and integrity; honesty. Faithfulness, efficiency, and staff courtesy in official conduct; and dignified conduct in private life.

• Professionalism and integrity: demands all staff to openly demonstrate professionalism and integrity in executing the policies and programs of the DMO;

• Honesty, faithfulness, efficiency, and courtesy in official conduct: demands staff to keep faith to their official responsibilities by not allowing personal considerations or activities to interfere with official duties, maintaining constancy and sincerity of purpose, being result-oriented, and respecting the people it deals with;

• Dignified conduct in private life: demands staff to exercise restraints in their private lives and in the conduct of private activities that could have bearing on their official engagements or individual personality.

Annual work plans should be tightly integrated with debt strategy work. There is a strategy hierarchy extending from the overall strategic debt management objectives, to annual debt management reviews and plans consistent with the overall objectives, to operational plans for individual work areas to give effect to the annual strategy. The Government of Canada provides annual plans for:

• Fixed-coupon marketable program

• Bond buyback program

• Real return bonds

• Treasury bill program

• Domestic market development

• Retail debt program

• Management of government’s cash balances

• Foreign reserve debt program

• Risk management

- 17 -

c) The separation of Executive Debt Management and Operational Debt Management The Executive Debt Management functions (that is the policy, regulatory and resourcing functions4) are the responsibility of the Minister of Finance and other high government officials, such as the Heads of the DMO, National Planning, Budget and Treasury Offices, in the form of a high level body which could be denominated as the Executive Debt Management Committee (EDMC). The role of the EDMC, is to approve debt management guidelines and the principles to implement them, and then meets at intervals to analyze the DMO’s performance and evaluate the compliance with established regulations and targets. The Governor of the Central Bank can be part of this Committee, basically for the coordination between monetary policy, debt management and fiscal policy, including the issuance program and aspects dealing with money, primary and secondary markets. The functions of this Committee are subsequently described in more detail in this chapter. The day-to-day operations are to be delegated by the EDMC to be conducted by the DMO, and then reported to and coordinated with the Minister of Finance. The DMO must have a clear medium term strategy (including strategic targets), performance indicators and strict monitoring and control functions in place. These functions should not be related to debt issuance and debt service only. They should also encompass effective management of the risks associated with the debt structure, and make them compatible with the fiscal targets, while reducing vulnerability to shocks of government finance. The development of an integrated financial management system would certainly contribute to improvements in debt management and overall financial management. Stronger accountability and transparency frameworks are also needed. Based on previous work on effective debt management developed by DMFAS/UNCTAD and other international organizations (World Bank, IMF, and others) and best practices in debt management implemented in several countries, the recommended Executive Debt Management (EDM) functions can be summarized as follows: EDM functions for external debt include the establishment of debt sustainability standards; determination of borrowing needs and limits, desired terms and borrowing sources; formulation of guidelines for debt operations such as debt conversions, buy-backs, on-lending, etc; policy framework for government guarantees and contingent liabilities; arrangements and regulations for borrowing, disbursements, and debt service. EDM functions for domestic debt deal with the formulation of debt management objectives and strategy; establishing borrowing ceilings according to budgetary and fiscal goals; development of a benchmark debt structure; determination of the volume, type of instruments, maturity, timing, frequency, and selling techniques; develop communication linkages with stakeholders.

4 Effective Debt Management, DMFAS/UNCTAD,1993, op.cit.

- 18 -

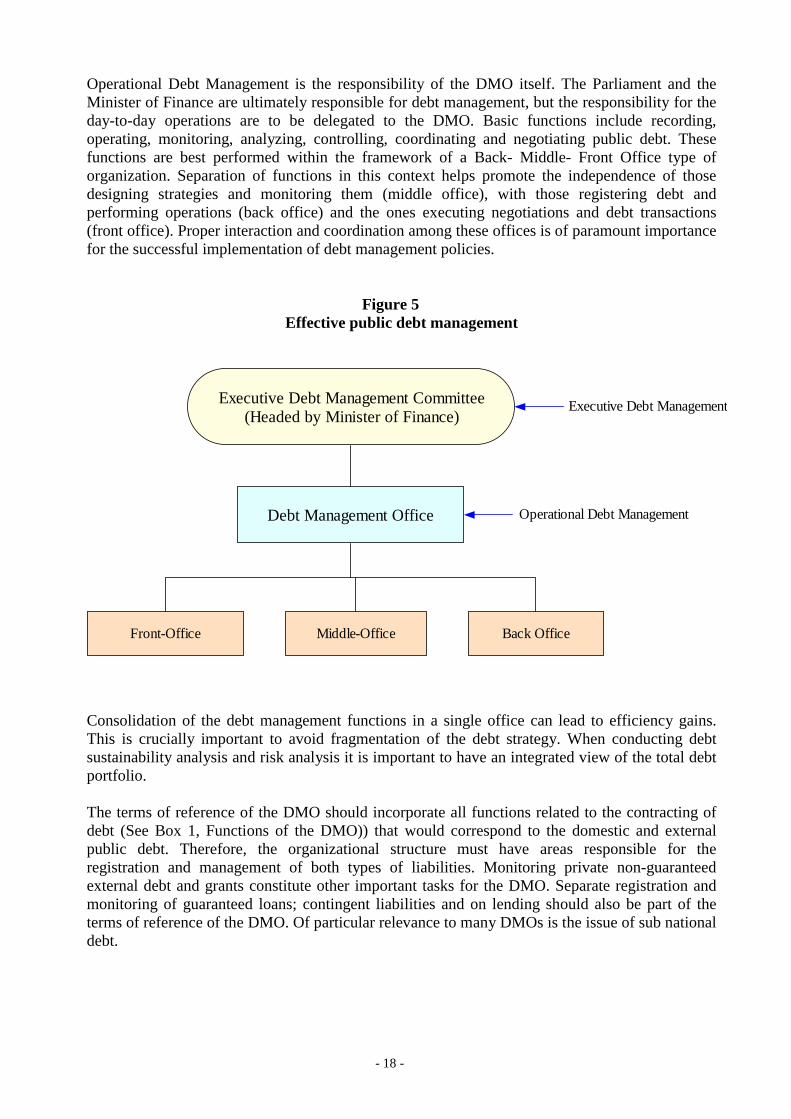

Operational Debt Management is the responsibility of the DMO itself. The Parliament and the Minister of Finance are ultimately responsible for debt management, but the responsibility for the day-to-day operations are to be delegated to the DMO. Basic functions include recording, operating, monitoring, analyzing, controlling, coordinating and negotiating public debt. These functions are best performed within the framework of a Back- Middle- Front Office type of organization. Separation of functions in this context helps promote the independence of those designing strategies and monitoring them (middle office), with those registering debt and performing operations (back office) and the ones executing negotiations and debt transactions (front office). Proper interaction and coordination among these offices is of paramount importance for the successful implementation of debt management policies. Figure 5

Effective public debt management

Executive Debt Management Committee(Headed by Minister of Finance)

Debt Management Office

Middle-OfficeFront-Office Back Office

Executive Debt Management

Operational Debt Management

Consolidation of the debt management functions in a single office can lead to efficiency gains. This is crucially important to avoid fragmentation of the debt strategy. When conducting debt sustainability analysis and risk analysis it is important to have an integrated view of the total debt portfolio. The terms of reference of the DMO should incorporate all functions related to the contracting of debt (See Box 1, Functions of the DMO)) that would correspond to the domestic and external public debt. Therefore, the organizational structure must have areas responsible for the registration and management of both types of liabilities. Monitoring private non-guaranteed external debt and grants constitute other important tasks for the DMO. Separate registration and monitoring of guaranteed loans; contingent liabilities and on lending should also be part of the terms of reference of the DMO. Of particular relevance to many DMOs is the issue of sub national debt.

- 19 -

The establishment of an appropriate structure for the DMO is crucial to perform management functions and control of public debt. Specifically, this refers to functions performed in the daily management of public debt. These management functions would be performed according to strategies and policies elaborated by the authorities. Therefore, the DMO should be equipped with the appropriate structure and functions, to implement the centralization of registration and management of public debt with a reliable registry. The organizational structure of the DMO should be based on a Functions Manual that will determine its role, responsibilities and functions, with supervision at intermediate level and the necessary qualified staff in permanent positions to execute all the tasks of the work program. The DMO should incorporate the terms of reference related with the centralization of responsibilities, in terms of registration, monitoring and operational functions. The functions of each element of the DMO structure should be clearly specified and there should be effective coordination and information sharing within the DMO. This requirement could be embodied in an internal communications strategy. The mandates of the respective staff should also be set in clear and unambiguous terms encapsulated within the job description and operationalized through performance plans. The DMO should have all the required personnel to respond efficiently to its mandates, and a policy of adequate remuneration to attract and retain qualified staff. This will depend on the assigned responsibilities in terms of management of public debt, both external and domestic. Job descriptions for every member of the staff are essential for the proper functioning of the DMO. d) The need for an Executive Public Debt Management Committee. Functions. Designation

of policy. Coordination issues. Coordination across agencies and macroeconomic objectives is crucial for effective debt management. Consultations are indispensable especially if there are potential conflicts between debt management strategy, monetary and fiscal policies and exchange rate policies. This is particularly important if there are multiple agencies dealing with public debt issues. A formal coordinating body in the form of a debt committee may aid in sharing information across policy makers and implementing agencies and in clarifying roles and responsibilities. (on this issue also see External Debt Statistics, Guide for Compilers and Users, BIS, ComSec, Eurostat, IMF, OECD, Paris Club Secretariat, UNCTAD, World Bank, 2003). On the other hand, public debt management activities are typically related to the responsibilities and the area of influence of the Ministry of Finance. Therefore, for practical reasons, it would be appropriate to establish an Executive Committee on Debt Management (EDMC), presided by the Minister of Finance in order to coordinate policies, establish debt strategies and direct the business of the DMO within the framework of the financial and economic policies of the Government. In addition to the Minister of Finance, other members of the Committee could include the Governor of the Central Bank, the head of the Planning Office, any other high ranking government official involved in macroeconomic policies and public finance management, and the head of the DMO as Secretary to the Committee. The Committee has executive debt management functions.

- 20 -

Executive debt management functions relate to the direction and organization of the DMO, including debt strategies, structure of the debt office and staffing and systems. The Committee would provide the DMO with the necessary guidelines, responsibilities, directives and instructions relating to all aspects of public debt management, to ensure that the DMO complies with the policies adopted by the EDMC within the framework of the economic program of the government. Based on these guidelines and instructions, the DMO will then perform its operational debt management functions, which have to do with the day-to-day activities of a debt management office. The functions of the DMO need to be defined clearly by the EDMC.

Figure 6 Possible Composition of the Executive Debt management Committee

Head of

Treasury

Head of Budget

Economic Adviser to the President

Head of Planning Office

Governor of Central Bank

Head of DMO Secretary

Minister of Finance

Chairman

The main function of the Committee on Debt Management is to define public debt management strategy, based on debt portfolio analysis and debt sustainability analysis, within the overall macroeconomic strategy. Determine overall borrowing needs in line with macroeconomic objectives and sustainable debt levels. The EDMC should define DMO’s legal, institutional and organizational frameworks. If needed, subsequently review these in light of variations in the overall macroeconomic strategy, or exogenous factors

- 21 -

e) The setting of a DMO in a Front, Middle, Back Office structure. The Back Office This office centralizes all the operations related to the registration, monitoring and control of disbursements/subscriptions, execution and management of public debt service operations, registration of the operations of public debt and production of statistical information. Therefore, the functions comprise the administration of the full cycle of the life of a contract/instrument, from the signature/issue to its full payment. Failure to properly perform these functions (i.e., delays in debt service, improper registration of debt contracts, maintenance of inexact and non updated debt information, etc) can have costly implications for the government. The accuracy and timeliness of information on public debt, both external and domestic are crucial for effective debt management. Development of internal controls and guidelines for data validation can avoid discrepancies in loan transactions and permit a sound database and accurate and timely debt servicing of the debt.

BOX 4

Functions of the Executive Debt Management Committee • Approve the debt management strategy over the medium-term

• Decide on sectors that will have access to external/domestic financing and in what terms

• Define level and characteristics of domestic debt issuing for fiscal purposes

• Establish borrowing ceilings by debtor/creditor categories

• Establish guidelines for extending government guarantees

• Define mix of external/domestic indebtedness and desired amortization profiles

• Decide on debt restructurings proposed by the DMO to conform with debt strategy

• Provide laws, guidelines and regulations for effective debt management

• Define institutional framework for DMO and each institution involved in debt management operations, including proper coordination of activities

• Provide the organizational framework for the DMO, including information flows, functions and schedule of duty

• Through the Budget Law, for each fiscal year, establish the debt service targets, and ceilings on indebtedness for foreign and domestic debt

• Eventually, establish benchmarks for certain debt indicators, such as debt service to exports, stock of public debt to GDP, debt service to government revenues, etc.

• Define policies for attracting and retaining DMO staff with relevant qualifications;

• Define salary policies, career perspectives, allowances

• Define training programmes and recycling of knowledge sessions for DMO staff

• Support improvements, maintenance and extensions in the debt database system

- 22 -

This office is responsible for the management of records of debt holders and for the administration of registration of government debt instruments. Forecasts of forthcoming debt service payments for domestic (as well as for external debt) need to be produced and sent to the financial agent of the government for debt service compliance. Grants, on lending, guaranteed debt and contingent liabilities should be registered and monitored closely. Private non-guaranteed debt needs to be monitored as well. Sub national debt needs to be given proper attention, given its connotations at the national level. The back office should ensure that budgetary provisions exist for public debt service (external and domestic), including contingent liabilities, and that sufficient reserves are planned for external debt service. This office should have the strong support of the IT/ IS group for the maintenance of the local area network, as well as the interface with other areas of the financial management system of the government. The back office performs the basic functions, which will permit that all other operational functions could be carried out. The distribution of tasks to comply with these functions could be divided in: the "Area of Registration", concerning the registry of debt information in the database; the "Area of Accounting Operations", mainly involved with the issue of the "Payment Order"; and the "Area of the Database Administrator " in charge of the system and network maintenance. These functions should be regulated by a Procedures Manual that norms the flow of information in the operative cycle. This involves: the reception of documentation and information of domestic and external financing; the registration of this information in the database; and, the steps to follow for the accounting and statistical registry of disbursements and public debt service. Therefore, this Manual should link the operative activities with the structure and functions established by the Functions Manual. Both manuals should establish the organizational framework that is required for an efficient operational debt management. The preparation of payment orders to service public debt can be performed by the Area of Accounting Operations, with payment schedules generated by the functional groups of the Area of Registration, although the actual accounting of debt service payments are not necessarily done inside the DMO. With a reliable debt database and a debt system, the preparation of the payment order should be rapid and efficient. The payment orders can be generated and printed directly from the database system, based on the debt system's information. The process of debt service payments to creditors is performed after the reconciliation of the creditors’ requests with the amounts scheduled in the debt system's database. This centralization of public debt registration and monitoring, and the operative process for the issue of the payment orders, represent important savings. The efficiency in the payment of obligations reduces processing time and produces financial savings by the elimination of penalties for late payments. A well-organized back office will have a structure with efficient flow of information, adequate business processes, good quality of information produced, high productivity of its personnel to handle its responsibilities. Therefore, the structure should be organized with a distribution of functions that clearly defines and establishes the sources of financing and the co-ordination and administration of the resources originating on public credit. An efficient model of back office structure integrates all the functions and operative processes in a more vertical manner, with necessary levels of managerial responsibilities.

- 23 -

The monitoring and control of public debt information should be based on a methodical centralization of public credit operations in the database of the DMO. The DMO should have a debt database with up-to-date information of domestic and external debt registered in the system. The registration of operations of domestic or external financing in the database system is initiated with the opening of loan files well classified by the source of origin, creditor, and debtor and executing agency. This registration will facilitate an adequate control of the management of disbursements and payments made during the fiscal year, as well as the projection of debt service . The processes of control and monitoring of the registration of new loans in the database should be made by the head of each functional group. These should have the responsibility of generating listings or reports of the loans incorporated to verify the consistency of the information entered. The work of validation of the information should be executed periodically and errors or inconsistencies corrected. The status of the database and its evolution should be evaluated in regular meetings among the heads of the functional groups who have the responsibility of executing the work programme. The procedure for the registration of financial inflows reflects the operative of disbursements by the government and the rest of the public sector. This is handled through the financial agent, (Central Bank) or other mechanisms, executing the credit that corresponds to the participating organizations, being these debtors, executors or final beneficiaries. Regularly, the DMO should receive from the Treasury, Central Bank, executing agencies, or creditor organizations, the information of the transfer of resources or disbursements in the name of the beneficiary. The input of loan’s information to the database should be monitored and controlled periodically by the head of unit of the Back Office of the DMO. The technicians of the units should have the responsibility to run lists of loans to verify the consistency of the information and to correct them if necessary. The Database Administrator should perform the validation of the consolidated debt information periodically. Errors and inconsistencies in the information could be detected through consolidated reports, and notified to the head of each group for correction. The status of the database and its consistency should be analyzed in periodic meetings with the heads of units who have the responsibility of executing the agreed work program. The database established would facilitate an adequate monitoring and control of disbursements and payments made during the budgetary period. It would also support the preparation of debt service projections and the evaluation of its impact in the debt profile. The confidence in the debt information processed and reported by the DMO has a direct relationship with the quality of data that is entered in the system. Therefore, it is necessary to ensure that the participants or beneficiaries of domestic and external financing report the information on time. It is important to control that the information is of good quality and that the flows comprise all the operations of public debt outstanding. In order to accomplish this, the process should be regulated by a resolution or legal norm that instruct all the entities of the public sector to respond to data requirements of the DMO. Normally, it should be one of the functions of the DMO to provide specific norms and mechanisms related to the mandatory registration of direct and guaranteed public debt.

- 24 -

The control and supervision functions of a DMO require that debt information be collected without obstacles. This will assure that the Government’s debt strategy is followed by all entities that participate in the area of public debt. It will also guarantee that the authorities have access at any time to up-to-date information at detailed and aggregated levels. Therefore it is important that the DMO establishes direct contact with the executing agencies or users of resources and creditors in order to have direct access to this information. This information will be reconciled with information received from other sources and with the Central Bank. It is also important that the institution in charge of monitoring the Public Investment Programme, provides all the information to the DMO, in particular information related to the amounts of disbursements that are estimated according to each project. This information will guarantee that the projections of debt service are compatible with these estimates. This is also applicable to the information on real disbursements so there is consistency between the information at the DMO, the executing agencies and the Central Bank. This is also important in order to have better estimates for the preparation of the budget. Accordingly the Treasury would be able to review its estimates for cash flows to avoid liquidity problems. Registration Function. This is the most relevant function of the Back Office. It can be disaggregated in different sub functions: Collecting, Storing, Processing, Validating and Disseminating debt data. The Back Office normally has to deal with a great demand of information on public debt. International organizations, different areas of the executive and legislative branches, researchers, media, etc do require to have reliable and updated debt information. Transparency and efficiency in generating information is a key task of the Back Office5. An important activity of this office is to conduct data validation at regular intervals in order to ensure the reliability of the database. Normally, this also requires regular reconciliations with creditors. The dissemination of public debt information should be closely coordinated with the Middle Office. Operating Function. The Back Office should monitor disbursements of registered loans keeping an updated database and generate accurate and timely projections to ensure correct and timely debt service. This would avoid default and/or unnecessary payment of penalty charges, commitment fees and other charges. The Back Office should coordinate its activities closely with the Front Office to ensure transparent and opportune flow of information and with the Middle Office, a recipient of disaggregated or consolidated debt information for analytical purposes.

5 For more details on this topic see presentation on Information and Transparency in Debt Management, Udaibir S. Das, IMF, UNCTAD’s Fifth Inter-Regional Debt Management Conference, 2005.

- 25 -

The Middle Office The main function of the Middle Office is to conduct the analytical work required for assisting the executive debt management levels in designing a debt strategy and a framework for risk monitoring and control. Regular debt portfolio review to ensure DMO’s control over the debt portfolio and public debt sustainability analysis should be part of the activities of this office, in coordination with other government offices. Another vital role of this office is the generation of managerial reports on public debt for internal users inside the DMO and the government; and the publication and dissemination of statistics, policies and reports on external and domestic debt on a periodic basis. A centralized public debt database should enable the DMO to provide at any time and to any governmental entity or institution, up-to-date information on the status stocks and flows of public debt. The distribution of information to the main users should be performed through a distribution program prepared for this purpose according to the type of report and its periodicity. The preparation of debt information and reports could respond to standard requirements and specific requests. It would involve internal users that participate in the management of public debt at the Ministry of Finance. These could be mainly the Budget, Treasury and the General Accountant. The Procedures Manual should specify the reports that are required by the various modules of the public financial administration. Internal users also include other entities as the Central Bank, the National Planning Office, the General Auditor, etc. It also includes external users, mainly the international organizations such as the World Bank, IMF, regional development banks, Paris Club creditors, civil society and private users. The work program for the production of reports should include the preparation of monthly and quarterly managerial reports for the Ministry of Finance. The reports would comprise the stock of debt outstanding and transactions that took place during specific periods. These reports are normally used by the authorities in the decision making process and the formulation of policies for domestic and external financing. This work program should also be supported by the preparation and distribution of a Statistical Bulletin of Public Debt. The work program of the DMO should also include the production of other information and reports mainly used for analytical purposes. These include estimates and projections of disbursements and public debt service with various assumptions of variable interest rates and exchange rates. It is the responsibility of the middle office to coordinate debt management with other public policy objectives. Once the group responsible for the elaboration of the analysis of the status of debt and its evolution is trained to incorporate into the analysis the Balance of Payments and macroeconomic information, will be able to develop debt strategies with the help of analytical tools. Then will be ready to support the efforts of the authorities to implement debt strategies. The analytical group at the middle office should provide strong support to the front office.

- 26 -

Analytical Function. The Analytical Function will perform portfolio analysis in a macroeconomic framework and long-term debt sustainability and cost-risk analysis on a regular basis, including external and domestic debt. Debt Sustainability Analysis (DSA) needs to include complete fiscal sustainability, including the medium and long term social and economic needs through scenario analysis. This can be accomplished by using different DSA analytical tools, such as the World Bank/IMF debt dynamics templates, Debt- Pro or DSM+6. Other kinds of analysis are performed by this function depending on the needs and strategy adopted. Performance of sensitivity analysis with varying scenarios of exchange rates and interest rates would allow the middle office to provide information about the impact of different debt service scenarios on fiscal and monetary variables. Distinct debt scenarios need to be evaluated for managing public debt and developing an appropriate medium-term debt strategy, including the costs and risks attached to it. Proposals on debt management targets, such as currency composition or amortization profiles are to be part of the middle office responsibilities. This will also permit the establishment of targets for the appropriate external-domestic debt mix. This function will provide a substantial feedback to the Minister or the Board through the head of the DMO in order to evaluate the global macroeconomic debt strategy and, eventually, amend it. This function would also allow DMO to adopt strategies, within the mandate given to it, and to propose strategy changes to the Minister of Finance. The appropriate performance of this function requires the establishment of strong working relationships with other governmental entities in charge of formulation of macroeconomic policies, planning, public investment, Millennium Development Goals (MDGs) costing, cash management, budgeting, monetary policies and balance of payments. A key function of the middle office is to ensure the internal compliance with the debt strategy approved at higher levels. Active participation with relevant internal and external stakeholders is also required. Risk Analysis Function. This function refers to the evaluation and establishment of the cost, risk limits of the debt portfolio. Funding strategies designed would not consider the risks associated with them, therefore it is the responsibility of the Middle Office to incorporate risk in a systematic and quantifiable manner. This can be accomplished by using techniques to construct risk scenarios under different assumptions of currency and interest rate volatility. The Front Office The functions of this office are related to the gathering of financial resources to cover the public sector needs. Therefore, it comprises the use of various sources of funds, whether domestic or external, and all the processes involving the negotiation and contract of new borrowing. The front office performs the functions that are really of the EDMC’s Secretariat, i.e. to ensure that the law, the rules and regulations, and the guidelines issued by the Committee are applied and followed. The front office applies the guidelines when negotiating new loans or issuing new instruments. 6 Information on these analytical tools can be obtained through the websites of Debt Relief International or the DMFAS/UNCTAD Programme.

- 27 -

The front office should have the proper legal advise to conduct its functions. Disclosure obligations in distinct markets must be analyzed in detail. Implementation/Monitoring/Negotiating Function. This set of functions is basically the follow up and enforcement of the decisions taken at the executive level, and are essential for the efficient implementation of the decided debt management strategy. This includes the debt conversion policies and directives established by the government. Attracting Official Development Assistance (ODA) and grants is an implicit function of the front office of DMOs in lower income countries. The Negotiating Function is an essential responsibility of the front office, and bears the responsibility of following closely all the guidelines that the executive has laid down for this purpose. The front office will also closely coordinate its activities with the middle office, and with other bodies of the government as well as with official and private institutions. In the area of domestic debt, the front office has numerous responsibilities, including the development of debt and liquid markets; management of debt operations including auctions, subscriptions, etc; organizing distribution channels and selling procedures; administration of delivery and redemption of securities; development of arrangements for intervention and contacts with markets; and management of government outstanding portfolio. Development of an Efficient Government Securities Market This is an essential function for the front office in less developed economies. These includes: the development of securities market regulation to support the issuance and trading of government securities; develop market infrastructure to help build market liquidity and reduce systemic risk; strengthening the demand for government instruments by building the potential investor base; and developing the supply of public instruments for the establishment of an efficient primary market, by projecting the government’s liquidity needs, creating efficient channels for the distribution of securities, progressively extending the maturity of government instruments and consolidating the number of debt issues, among others. The front office can also play a role in the development of the secondary market by enhancing the liquidity of government instruments, defining trading procedures and promoting an efficient trading system and market transparency. The front office, in conducting its role of promoter of the domestic debt market, should aim at the separation of instruments used for debt management and monetary policy. When the market is limited to short-term instruments, it is difficult to avoid conflicts between monetary and debt policies and objectives. In more sophisticated DMOs, the Front office has a distinctive role in managing a more diversified domestic debt portfolio, entering into derivative market operations, integrated risk management, accessing the international capital markets and providing financial services to the government.

- 28 -

f) Location of the DMO A unified DMO with consolidated functions regarding operational debt management appears to be the most appropriate setting for effective debt management7. The existence of a single institution in charge of implementing debt policies permits a greater attention and concentration to debt management issues and provides support to the idea of ensuring a clear separation between fiscal, monetary and debt management policies. Regarding the location of the DMO, present practices vary from country to country. Separate DMOs outside the government are more frequent in developed economies with sophisticated financial markets. Under this arrangement, DMOs implement the debt strategies determined by the Minister of Finance, as an agency of the government8. If the government is to remain in control of debt management, for example through the EDMC there is a need to establish monitoring controls to ensure that the DMO will comply with the objectives determined. This is usually accomplished by setting up strategic objectives and benchmarks for debt management. Clear governance, legal and institutional arrangements need to be in place for controlling and monitoring a separate DMO. The main advantages of separate DMOs9 can be summarized as follows:

• Greater efficiency in managing debt

• More independence from political influence

• Attracts qualified staff with better salaries

• Permits the application of private sector management practices and debt techniques

DMOs inside the Ministry of Finance (MOF) are more common in the case of less developed economies, where more coordination is needed between debt management and other policies. Debt management in low and middle-income countries is a strategic and vital component of economic policies. Sources of financing vary from official lending from multilateral or bilateral sources or from the domestic or international capital markets Debt portfolio management is not the only concern. Fiscal discipline, social and economic growth and debt sustainability are intertwined prominent matters10. Some advantages of these DMOs are:

• greater coordination of debt management with the core activities of the MOF, such as fiscal and budgetary policies

• more flexibility in managing contingent liabilities and on lending

• facilitates addressing fiscal sustainability of debt

7 See also Institutional Arrangements for Public Debt Management, Elizabeth Currie, Jean-Jacques Dethier, and Eriko Togo, World Bank 2003. 8 Recent Experiences in the Organization of Debt Management Offices, Fred Jensen, presentation made at UNCTAD’s Fifth Inter-regional Debt Management Conference 2005. 9 See Annex II for a case of Separate DMO in a developing country 10 More details on the subject can be found in Boressen, Pal and Cossio-Pascal Enrique, The role and Organization of a Debt Management Office, 2002.

- 29 -

ANNEX I OPERATIONAL RISKS

Operations risks usually arise in the areas that provide support services to the public debt organization. Auditors would recognize the following operations risks when they examine the organizational structure of the public debt management unit. i. Lack of separation of duties or functions. Public debt transactions must be independently

processed, confirmed, valued, and reviewed, and monitored by an independent administrative office.

ii. Inadequate staff expertise. Supervisors must have the proper expertise to avoid becoming a

“rubber stamp” to the debt traders. Support staff is usually the first line of defense to uncover errors and irregularities that may occur in processing debt transactions.

iii. Product risk. New debt instruments can be too complex or poorly understood. This could

lead to the inability of the support area to process, value, and control new debt instruments. iv. System and technology risks. These risks exist when the staff fails to stay up to date in

technological developments associated with new information systems or adopt computerized information systems without “re engineering” their debt management practices.

v. Procedures risks. These risks exist when the debt management functions do not have written

procedures and the work flow is not structured in a predictable and well- designed manner, with proper audit trails maintained. These written procedures become more important the more complex debt instruments are.

vi. Disaster recovery risks. These risks exist when the debt organization has not planned for

alternative sites, computer resources, communications, resources, trading facilities, and other support services in the case of a disaster. Debt market makers must have alternative remote trading and technology sites and be able to recover from “point-of-failure” with minimal disruptions.

vii. Documentation risks. These risks exist when debt transactions do not have well-designed

agreements that are legally authorized, properly executed and supported by appropriate confirmation in a timely manner. Legal departments and support staff must maintain master agreements and supporting confirmations.

viii. Valuation risks. These risks exist when the support staff cannot perform, at least on a regular

basis, an independent valuation of all debt instruments or if the valuation of the support staff differs from the valuation of the SAI or an independent third party.

Source: INTOSAI Guidance for Planning and Conducting an Audit of Public Debt

- 30 -

ANNEX II A SEPARATE DMO, THE CASE OF NIGERIA There are a few developing countries such as Nigeria, with a separate DMO. The Graph below shows the arrangements of the Nigerian DMO.

Figure 7

Separate DMO – The case of Nigeria

Supervisory Board

(Executive Debt Management)

DirectorGeneral (OPERATIONAL(Operational Debt Management)

Public debt committee headed byMinister of Finance

(Executive Debt Management)

Internal Audit

Front OfficeCorporate

AffairsDepartment

Back OfficeMiddle Office

In any case, it is the Minister of Finance who is finally accountable for incurring debt on behalf of the government and he delegates some of his authorities to the DMO for this purpose. When the debt management activities are consolidated in a single office, and there are appropriate institutional, organizational structure and governance arrangements there are no great dissimilarities between a separate DMO and a DMO inside the Ministry of Finance.

- 31 -

REFERENCES

1. Asiedu,Elizabeth (2003), Debt Relief and Institutional Reform: a focus on Heavily Indebted Poor Countries, The Quarterly Review of Economics and Finance, Kansas, May

2. Bank for International Settlements (2003), Sound Practices for the Management and

Supervision of Operational Risk, Basel, February 3. Borresen, Pal and Cosio-Pascal, Enrique, (2002), Role and Organization of a Debt Office,

DMFAS Programme Technical Paper Nº 1, United Nations, New York and Geneva, UNCTAD/GDS/DMFAS/2.

4. Cohen,Daniel; Phamtan Michele; Rampulla Cristina; Vellutini, Charles (2004), Beyond the

HIPC Initiative, Investment Development Consultancy, France, March 5. Commonwealth Business Forum (2003), Achieving Sustainable Development: Challenges for

Business and Governments, Abuja, December 6. Contaduria General de la Nacion,(2005) The Integrated System of Financial Information,

Buenos Aires, February 7. Currie, Elizabeth; Dethier, Jean-Jacques and Togo, Eriko, (2003), Institutional Arrangements

for Public Debt Management, Washington, World Bank Research Paper 3021. 8. Deredza, Cornilious, (2004), Conceptualising a Sovereign Foreign Borrowing Policy

Framework, in Forum, MEFMI, Harare, March. 9. DMFAS/UNCTAD (1989) Effective Debt Management, UNCTAD/RDP/DFP/ DMS/2,

Geneva. 10. DMFAS/UNCTAD (1993) Effective Debt Management, UNCTAD/GID/DMS/15, Geneva. 11. International Monetary Fund (IMF), Bank for International Settlements (BIS), the

Commonwealth Secretariat (Comsec), Eurostat, the Organization for Economic Co-operation and Development (OECD), the Paris Club Secretariat, the United Nations Conference on Trade and Development (UNCTAD) and the World Bank, (2003), External Debt Statistics: Guide for Compilers and Users, Washington.

12. International Monetary Fund (2003), Manual on Fiscal Transparency, Washington 13. International Monetary Fund and the Hong Kong Monetary Authority (2000), Sovereign

Assets and Liabilities Management, Washington, November 14. International Monetary Fund (2004), Sovereign Debt Structure for Crisis Prevention,

Washington, July 15. Kraay Aart and Vikram Nehru (2003), When is Debt Sustainable?, (unpublished, Washington,

World Bank)

- 32 -

16. Magnusson, Tomas (2001) The Institutional and Legal Base for Effective Debt Management, UNCTAD Third Inter-Regional Debt Management Conference, Geneva

17. Mehran, H. (ed.) (1985), External Debt Management, International Monetary Fund,

Washington. 18. MEFMI and World Bank, (2001), Public Debt Management, Cash Management and Domestic

Debt Market Development, Case Study Tanzania Washington, June 19. Noel, Michel (2000), Building Sub-national Debt Markets in Developing and Transition

Countries, a framework for Analysis, Policy Reform and Assistance Strategy, for the World Bank preparation of the Manual on Domestic Debt Markets Development-The Policy Issues, Washington, January.

20. UNCTAD, 2005, Presentations on Debt Management, UNCTAD’s Fifth Inter-Regional Debt

Management Conference, Geneva, June 21. UNCTAD, (2004), Economic Development in Africa – Debt Sustainability: Oasis or Mirage?,

New York and Geneva, August. 22. UNCTAD, (2003), Proceedings of the Third Inter-Regional Debt Management Conference,

Geneva 3-6 December 2001, United Nations, Geneva and New York. 23. UNDP, (1997), A Report on the Joint UNCTAD-World Bank Programme of Debt

Management, Management Development and Governance Division, Discussion Paper 4, UNDP, New York.

24. Wheeler, Graeme (2004), Sound Practice in Government Debt Management, World Bank,

Washington 25. World Bank and IMF, (2001), Guidelines for Public Debt Management, Washington, March. 26. World Bank and IMF, (2001a), Developing Government Bond Markets: A Handbook,

Washington. 27. World Bank and the IMF, (2002), Guidelines for Public Debt Management: Accompanying

Document, Washington, November. 28. World Bank and the IMF, (2003), Amendments to the Guidelines for Public Debt

Management, Washington, November 29. World Bank and the IMF, (2004), Debt Sustainability in Low-Income Countries-Proposal for

and Operational Framework and Policy Implications, Washington, February.

- 33 -