jaiprakash associate ltd

TRANSCRIPT

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 1/10

Page | 1

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

CMP: ` 86.503 month Target - ` 102.00SL: ` 79.00

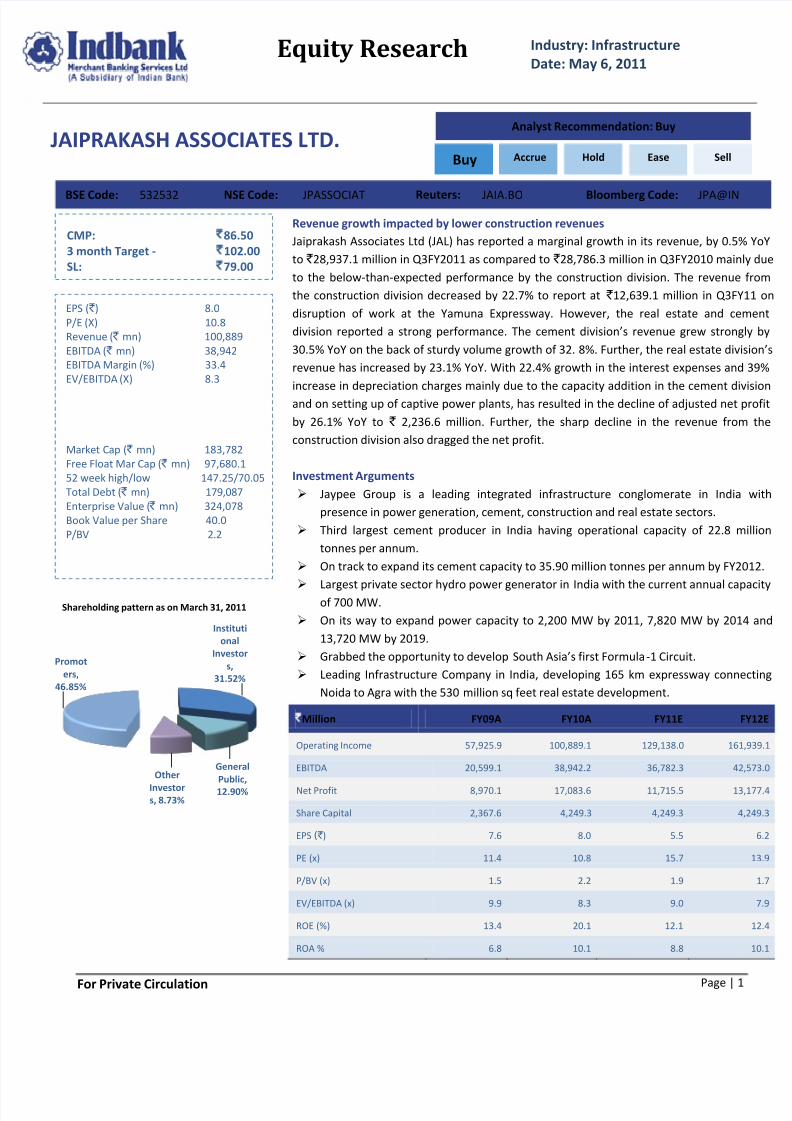

Shareholding pattern as on March 31, 2011

Promoters,

46.85%

Institutional

Investors,

31.52%

GeneralPublic,12.90%

Other

Investors, 8.73%

JAIPRAKASH ASSOCIATES LTD.

BSE Code: 532532 NSE Code: JPASSOCIAT Reuters: JAIA.BO Bloomberg Code: JPA@IN

EPS ( ` ) 8.0P/E (X) 10.8Revenue ( ` mn) 100,889EBITDA ( ` mn) 38,942EBITDA Margin (%) 33.4EV/EBITDA (X) 8.3

Market Cap ( ` mn) 183,782Free Float Mar Cap ( ` mn) 97,680.152 week high/low 147.25/70.05Total Debt ( ` mn) 179,087Enterprise Value ( ` mn) 324,078Book Value per Share 40.0P/BV 2.2

Revenue growth impacted by lower construction revenuesJaiprakash Associates Ltd (JAL) has reported a marginal growth in its revenue, by 0.5% YoYto ` 28,937.1 million in Q3FY2011 as compared to ` 28,786.3 million in Q3FY2010 mainlyto the below-than-expected performance by the construction division. The revenue fromthe construction division decreased by 22.7% to report at ` 12,639.1 million in Q3FYdisruption of work at the Yamuna Expressway. However, the real estate and cementdivision reported a strong performance. The cement division’s revenue grew strongly by30.5% YoY on the back of sturdy volume growth of 32. 8%. Further, the real estate divisiorevenue has increased by 23.1% YoY. With 22.4% growth in the interest expenses and 39%increase in depreciation charges mainly due to the capacity addition in the cement divisionand on setting up of captive power plants, has resulted in the decline of adjusted net profitby 26.1% YoY to ` 2,236.6 million. Further, the sharp decline in the revenue from theconstruction division also dragged the net profit.

Investment Arguments Jaypee Group is a leading integrated infrastructure conglomerate in India with

presence in power generation, cement, construction and real estate sectors. Third largest cement producer in India having operational capacity of 22.8 million

tonnes per annum. On track to expand its cement capacity to 35.90 million tonnes per annum by FY2012.

Largest private sector hydro power generator in India with the current annual capacityof 700 MW. On its way to expand power capacity to 2,200 MW by 2011, 7,820 MW by 2014 and

13,720 MW by 2019. Grabbed the opportunity to develop South Asia’s first Formula -1 Circuit. Leading Infrastructure Company in India, developing 165 km expressway connecting

Noida to Agra with the 530 million sq feet real estate development.

Analyst Recommendation: Buy

Buy Accrue Hold Ease Sell

` Million FY09A FY10A FY11E

Operating Income 57,925.9 100,889.1 129,138.0 161,939

EBITDA 20,599.1 38,942.2 36,782.3 42,

Net Profit 8,970.1 17,083.6 11,715.5 13,17

Share Capital 2,367.6 4,249.3 4,249.3 4,24

EPS (` ) 7.6 8.0 5.5

PE (x) 11.4 10.8 15.7

P/BV (x) 1.5 2.2 1.9

EV/EBITDA (x) 9.9 8.3 9.0

ROE (%) 13.4 20.1 12.1

ROA % 6.8 10.1 8.8

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 2/10

Page | 2

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

No Jaiprakash Associates to ramp its cement capacity

India on track with first ever F1 race

India is due to host Formula One race on October 30 this year. The organizers – Jaypee Sports International Ltd (JSIL) has namedthe Indian F1 track as Buddh International Circuit (BIC). This track covers around 5.14km and the circuit are expected to behomologated by July 2011. The circuit facility is able to accommodate 100,000 spectators and main grandstand is capable toaccommodate 30,000 viewers. The company invested ` 17 billion to construct the BIC and is expcetd to breakeven in the next 4years. Jaypee Sports International, a subsidiary of Jaiprakash Associates Ltd, is expected to garner ` 1,500 million from ticket salesof the race. BIC is a part of Jaypee Sports City spread across 2,500 acres. The sports city also has a cricket stadium, a hockey arenaand sports training academy.

Jaypee Group has marked its presence in the edible oil business. The company is in process of setting up soya and mustardprocessing plant at Rewa, Madhya Pradesh. The plant will mainly cater towards processing of 1 lakh tonne each of soya andmustard a year and will also produce oil cakes. The company has floated a separate company namely, Jaiprakash Agri InitiativesCompany in this regard. It will procure oil seeds from the farmers in Rewa and neighbouring areas and get these processed at itsplant and finally marketed the final product with its own brand.

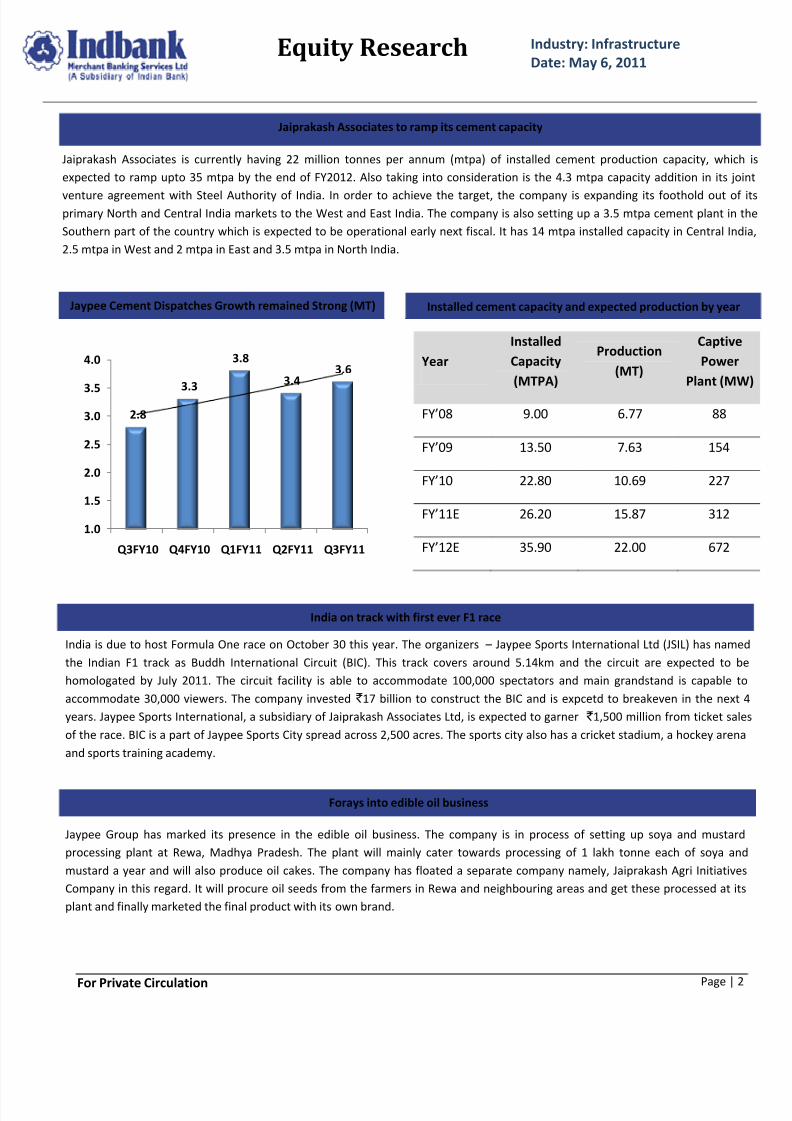

Jaiprakash Associates is currently having 22 million tonnes per annum (mtpa) of installed cement production capacity, which isexpected to ramp upto 35 mtpa by the end of FY2012. Also taking into consideration is the 4.3 mtpa capacity addition in its joint

venture agreement with Steel Authority of India. In order to achieve the target, the company is expanding its foothold out of itsprimary North and Central India markets to the West and East India. The company is also setting up a 3.5 mtpa cement plant in theSouthern part of the country which is expected to be operational early next fiscal. It has 14 mtpa installed capacity in Central India,2.5 mtpa in West and 2 mtpa in East and 3.5 mtpa in North India.

2.8

3.3

3.8

3.43.6

1.0

1.5

2.0

2.5

3.03.5

4.0

Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

YearInstalledCapacity(MTPA)

Production(MT)

CaptivePower

Plant (MW

FY’08 9.00 6.77 88

FY’09 13.50 7.63 154

FY’10 22.80 10.69 227

FY’11E 26.20 15.87 312

FY’12E 35.90 22.00 672

Jaypee Cement Dispatches Growth remained Strong (MT) Installed cement capacity and expected production by year

Forays into edible oil business

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 3/10

Page | 3

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

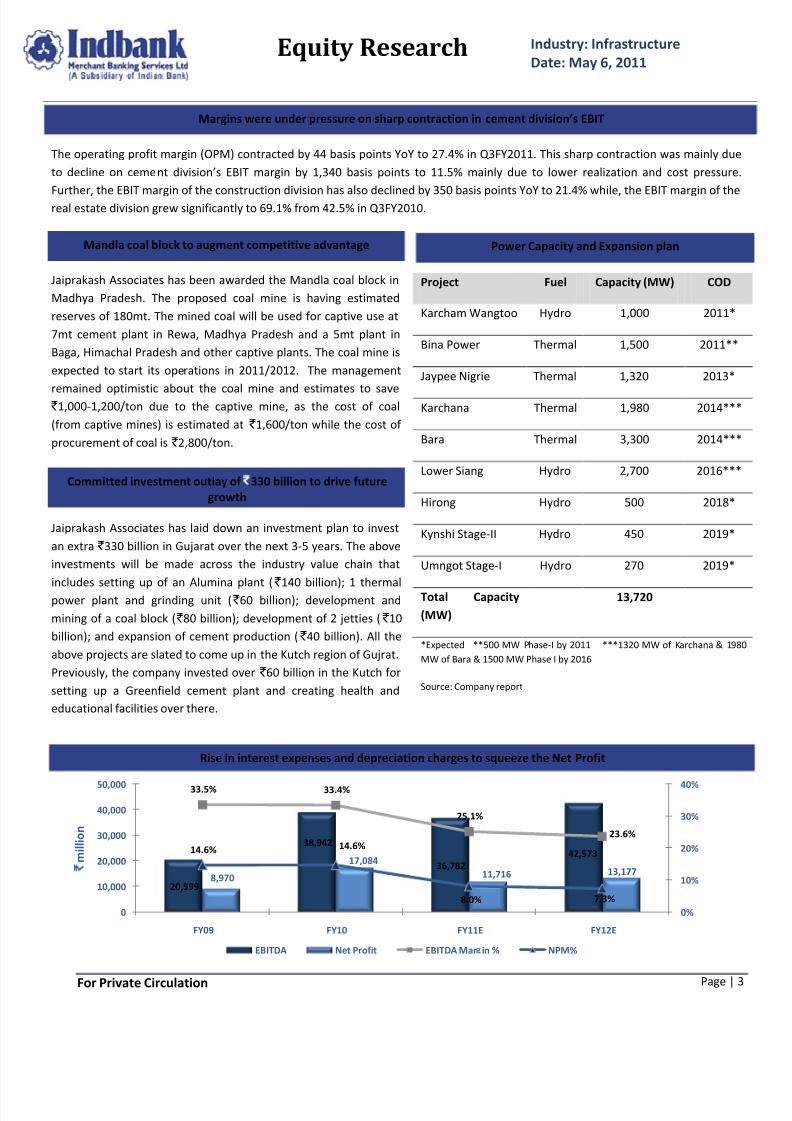

Power Capacity and Expansion planMandla coal block to augment competitive advantage

Rise in interest expenses and depreciation charges to squeeze the Net Profit

20,599

38,942

36,78242,573

8,970

17,08411,716 13,177

33.5% 33.4%

25.1%

23.6%

14.6% 14.6%

8.0% 7.3%0%

10%

20%

30%

40%

0

10,000

20,000

30,000

40,000

50,000

FY09 FY10 FY11E FY12E

` m i l l i o n

EBITDA Net Profit EBITDA Mar in % NPM%

Jaiprakash Associates has been awarded the Mandla coal block inMadhya Pradesh. The proposed coal mine is having estimatedreserves of 180mt. The mined coal will be used for captive use at7mt cement plant in Rewa, Madhya Pradesh and a 5mt plant inBaga, Himachal Pradesh and other captive plants. The coal mine isexpected to start its operations in 2011/2012. The management

remained optimistic about the coal mine and estimates to save ` 1,000-1,200/ton due to the captive mine, as the cost of coal(from captive mines) is estimated at ` 1,600/ton while the cost of procurement of coal is ` 2,800/ton.

Project Fuel Capacity (MW) COD

Karcham Wangtoo Hydro 1,000 2011*

Bina Power Thermal 1,500 2011**

Jaypee Nigrie Thermal 1,320 2013*

Karchana Thermal 1,980 2014***

Bara Thermal 3,300 2014***

Lower Siang Hydro 2,700 2016***

Hirong Hydro 500 2018*

Kynshi Stage-II Hydro 450 2019*

Umngot Stage-I Hydro 270 2019*

Total Capacity(MW)

13,720

*Expected **500 MW Phase-I by 2011 ***1320 MW of Karchana & 1980MW of Bara & 1500 MW Phase I by 2016

Source: Company report

Committed investment outlay of ` 330 billion to drive futuregrowth

Jaiprakash Associates has laid down an investment plan to investan extra ` 330 billion in Gujarat over the next 3-5 years. The aboveinvestments will be made across the industry value chain thatincludes setting up of an Alumina plant ( ` 140 billion); 1 thermalpower plant and grinding unit ( ` 60 billion); development andmining of a coal block ( ` 80 billion); development of 2 jetties ( ` 10billion); and expansion of cement production ( ` 40 billion). All theabove projects are slated to come up in the Kutch region of Gujrat.Previously, the company invested over ` 60 billion in the Kutch forsetting up a Greenfield cement plant and creating health andeducational facilities over there.

Margins were under pressure on sharp contraction in cement division’s EBIT

The operating profit margin (OPM) contracted by 44 basis points YoY to 27.4% in Q3FY2011. This sharp contraction was mainly dueto decline on ceme nt division’s EBIT margin by 1,340 basis points to 11.5% mainly due to lower realization and cost pressure.

Further, the EBIT margin of the construction division has also declined by 350 basis points YoY to 21.4% while, the EBIT margin of thereal estate division grew significantly to 69.1% from 42.5% in Q3FY2010.

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 4/10

Page | 4

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

Coal India Ltd (CIL), established in 1973 as a wholly- owned subsidiary of the Government of India, is the world’s largest coalproducing company both in terms of production as well as reserves with a total coal production of ~445.9 Mtn in FY10. In terms of reserves also, it is the world’s largest coal company with bgeilugref ~18.9 Btn and resources of ~64.3 Btn. It has over three and a half decades of core competence across the entire coal business values chain starting from exploration, planning and design, operations,beneficiation and marketing. As of March 31, 2010, CIL operated 471 mines in 21 major coalfields across eight states in India. Out of the total mines operated, the number of open cast mines, underground mines and mixed mines remained 163, 273 and 35,respectively. The principal product of CIL is raw coal, primarily non-coking. CIL is in the process of implementing a plan forbeneficiation of coal supplies to consumers, other than those at pithead, in a phased manner. CIL is also looking for diversificationopportunities in the areas of Coal Bed Methane, Coal Gasification, Coal Liquefaction and Power Generation. CIL has also madeprogress in acquiring metallurgical and high grade thermal coal resources abroad to enhance energy security of the nation.

97,592

75,304

154,689 188,025227,865

52,433

20,787

96,224 118,302145,269

25.3%

16.4%

29.4% 29.8% 30.0%

13.6%

4.5%

18.3% 18.7% 19.2%

0%

5%

10%

15%

20%

25%

30%

35%

0

50,000

100,000

150,000

200,000

250,000

FY08 FY09 FY10 FY11E FY12E

EBITDA Net Profit EBITDA Margin % NPM%

Bottomline Likely to Grow on the Back of Rise in Topline

Company Profile

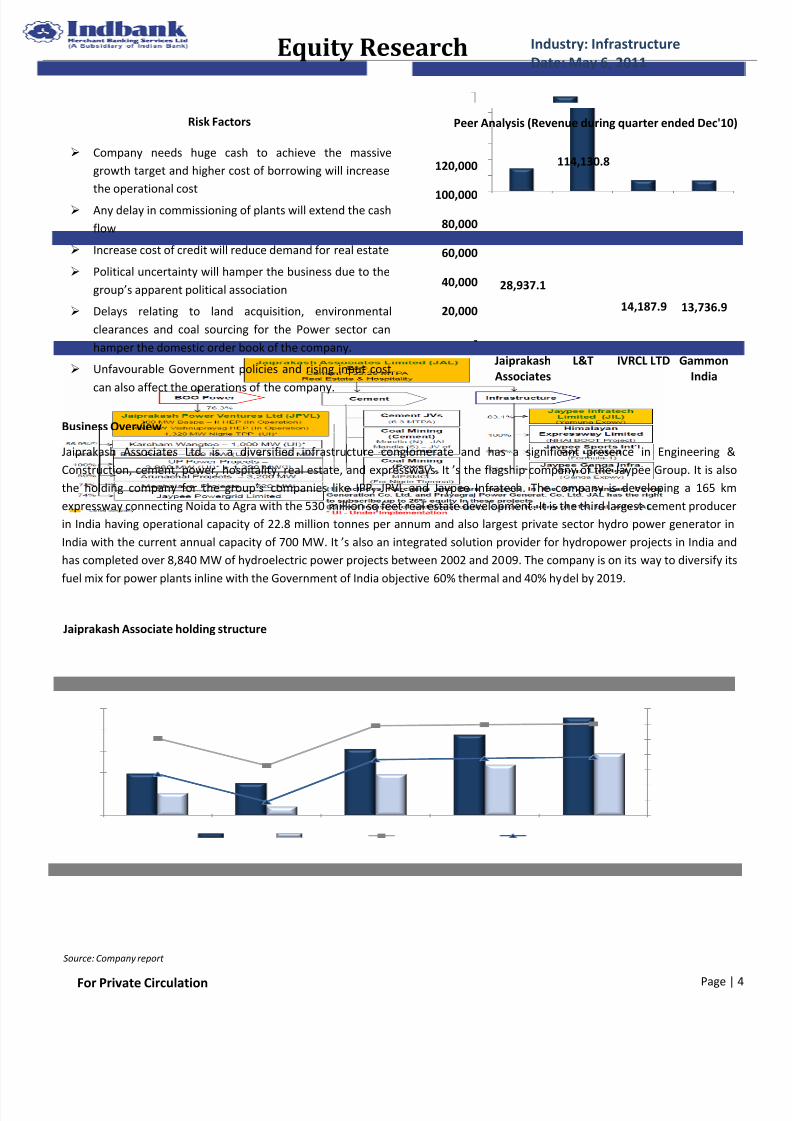

Risk Factors

Company needs huge cash to achieve the massivegrowth target and higher cost of borrowing will increasethe operational cost

Any delay in commissioning of plants will extend the cashflow

Increase cost of credit will reduce demand for real estate

Political uncertainty will hamper the business due to thegroup’s apparent political association

Delays relating to land acquisition, environmentalclearances and coal sourcing for the Power sector canhamper the domestic order book of the company.

Unfavourable Government policies and rising input cost

can also affect the operations of the company.

Business Overview

Jaiprakash Associates Ltd. is a diversified infrastructure conglomerate and has a significant presence in Engineering &Construction, cement, power, hospitality, real estate, and expressways. It ’s the flagship company of the Jaypee Group. It is alsothe holding company for the group’s companies like IPP, JPVL and Jaypee Infratech. The company is developing a 165 kmexpressway connecting Noida to Agra with the 530 million sq feet real estate development. It is the third largest cement producerin India having operational capacity of 22.8 million tonnes per annum and also largest private sector hydro power generator inIndia with the current annual capacity of 700 MW. It ’s also an integrated solution provider for hydropower projects in India andhas completed over 8,840 MW of hydroelectric power projects between 2002 and 2009. The company is on its way to diversify itsfuel mix for power plants inline with the Government of India objective 60% thermal and 40% hydel by 2019.

28,937.1

114,130.8

14,187.9 13,736.9

-

20,000

40,000

60,000

80,000

100,000

120,000

JaiprakashAssociates

L&T IVRCL LTD GammonIndia

Peer Analysis (Revenue during quarter ended Dec'10)

Jaiprakash Associate holding structure

Source: Company report

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 5/10

Page | 5

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

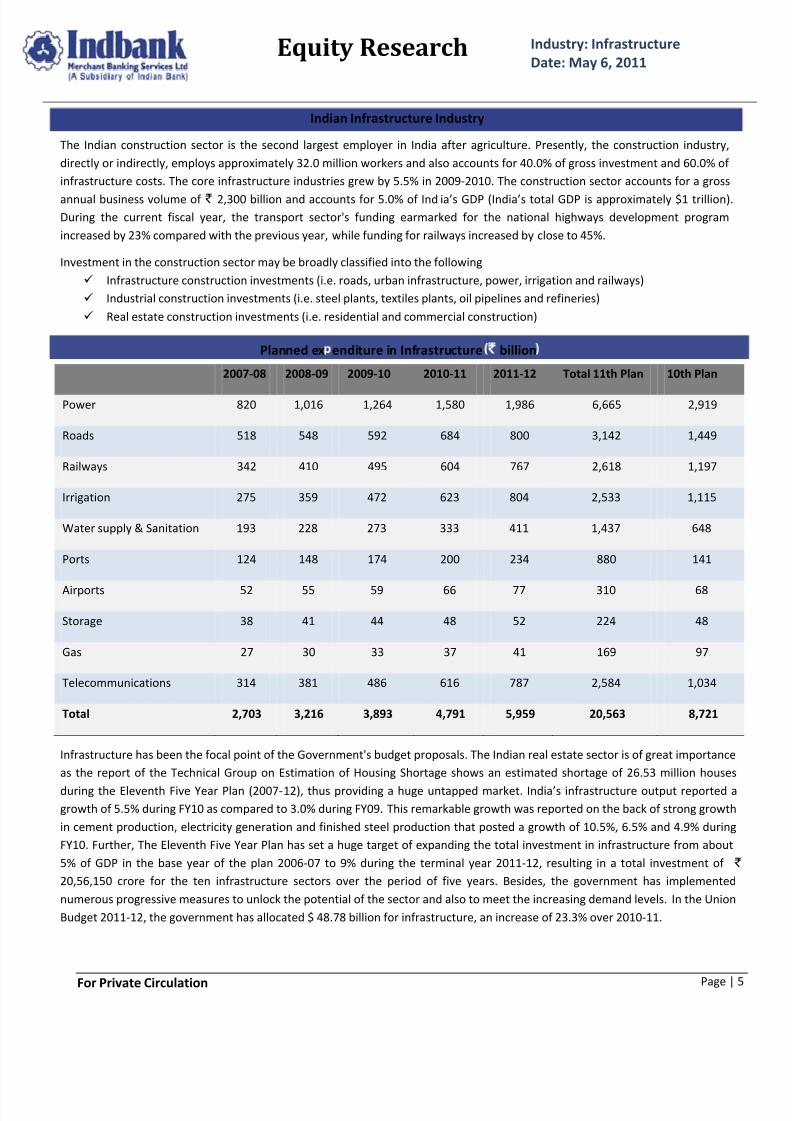

Indian Infrastructure Industry

The Indian construction sector is the second largest employer in India after agriculture. Presently, the construction industry,directly or indirectly, employs approximately 32.0 million workers and also accounts for 40.0% of gross investment and 60.0% of infrastructure costs. The core infrastructure industries grew by 5.5% in 2009-2010. The construction sector accounts for a gross

annual business volume of ` 2,300 billion and accounts for 5.0% of Ind ia’s GDP (India’s total GDP is approximately $1 trillion).During the current fiscal year, the transport sector's funding earmarked for the national highways development programincreased by 23% compared with the previous year, while funding for railways increased by close to 45%.

Investment in the construction sector may be broadly classified into the following Infrastructure construction investments (i.e. roads, urban infrastructure, power, irrigation and railways) Industrial construction investments (i.e. steel plants, textiles plants, oil pipelines and refineries) Real estate construction investments (i.e. residential and commercial construction)

Planned ex enditure in Infrastructure ` billion

Infrastructure has been the focal point of the Government's budget proposals. The Indian real estate sector is of great importanceas the report of the Technical Group on Estimation of Housing Shortage shows an estimated shortage of 26.53 million housesduring the Eleventh Five Year Plan (2007- 12), thus providing a huge untapped market. India’s infrastructure output reported agrowth of 5.5% during FY10 as compared to 3.0% during FY09. This remarkable growth was reported on the back of strong growthin cement production, electricity generation and finished steel production that posted a growth of 10.5%, 6.5% and 4.9% duringFY10. Further, The Eleventh Five Year Plan has set a huge target of expanding the total investment in infrastructure from about5% of GDP in the base year of the plan 2006-07 to 9% during the terminal year 2011-12, resulting in a total investment of `

20,56,150 crore for the ten infrastructure sectors over the period of five years. Besides, the government has implementednumerous progressive measures to unlock the potential of the sector and also to meet the increasing demand levels. In the UnionBudget 2011-12, the government has allocated $ 48.78 billion for infrastructure, an increase of 23.3% over 2010-11.

2007-08 2008-09 2009-10 2010-11 2011-12 Total 11th Plan 10th Plan

Power 820 1,016 1,264 1,580 1,986 6,665 2,919

Roads 518 548 592 684 800 3,142 1,449

Railways 342 410 495 604 767 2,618 1,197

Irrigation 275 359 472 623 804 2,533 1,115

Water supply & Sanitation 193 228 273 333 411 1,437 648

Ports 124 148 174 200 234 880 141

Airports 52 55 59 66 77 310 68

Storage 38 41 44 48 52 224 48

Gas 27 30 33 37 41 169 97

Telecommunications 314 381 486 616 787 2,584 1,034

Total 2,703 3,216 3,893 4,791 5,959 20,563 8,721

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 6/10

Page | 6

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

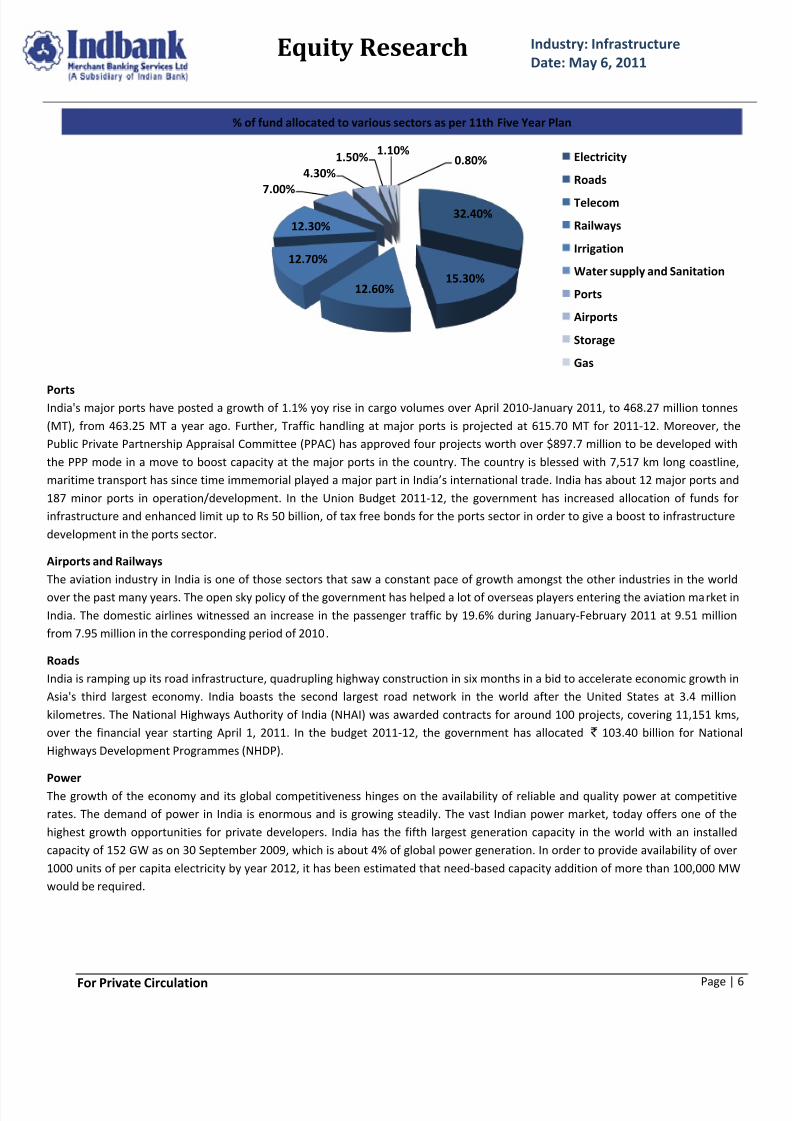

32.40%

15.30%12.60%

12.70%

12.30%

7.00%4.30%

1.50% 1.10%0.80% Electricity

Roads

Telecom

Railways

Irrigation

Water supply and Sanitation

Ports

Airports

Storage

Gas

% of fund allocated to various sectors as per 11th Five Year Plan

PortsIndia's major ports have posted a growth of 1.1% yoy rise in cargo volumes over April 2010-January 2011, to 468.27 million tonnes(MT), from 463.25 MT a year ago. Further, Traffic handling at major ports is projected at 615.70 MT for 2011-12. Moreover, thePublic Private Partnership Appraisal Committee (PPAC) has approved four projects worth over $897.7 million to be developed withthe PPP mode in a move to boost capacity at the major ports in the country. The country is blessed with 7,517 km long coastline,maritime t ransport has since time immemorial played a major part in India’s international trade. India has about 12 major ports and187 minor ports in operation/development. In the Union Budget 2011-12, the government has increased allocation of funds forinfrastructure and enhanced limit up to Rs 50 billion, of tax free bonds for the ports sector in order to give a boost to infrastructuredevelopment in the ports sector.

Airports and RailwaysThe aviation industry in India is one of those sectors that saw a constant pace of growth amongst the other industries in the worldover the past many years. The open sky policy of the government has helped a lot of overseas players entering the aviation market inIndia. The domestic airlines witnessed an increase in the passenger traffic by 19.6% during January-February 2011 at 9.51 millionfrom 7.95 million in the corresponding period of 2010.

RoadsIndia is ramping up its road infrastructure, quadrupling highway construction in six months in a bid to accelerate economic growth inAsia's third largest economy. India boasts the second largest road network in the world after the United States at 3.4 millionkilometres. The National Highways Authority of India (NHAI) was awarded contracts for around 100 projects, covering 11,151 kms,over the financial year starting April 1, 2011. In the budget 2011-12, the government has allocated ` 103.40 billion for NationalHighways Development Programmes (NHDP).

PowerThe growth of the economy and its global competitiveness hinges on the availability of reliable and quality power at competitiverates. The demand of power in India is enormous and is growing steadily. The vast Indian power market, today offers one of thehighest growth opportunities for private developers. India has the fifth largest generation capacity in the world with an installedcapacity of 152 GW as on 30 September 2009, which is about 4% of global power generation. In order to provide availability of over1000 units of per capita electricity by year 2012, it has been estimated that need-based capacity addition of more than 100,000 MWwould be required.

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 7/10

Page | 7

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

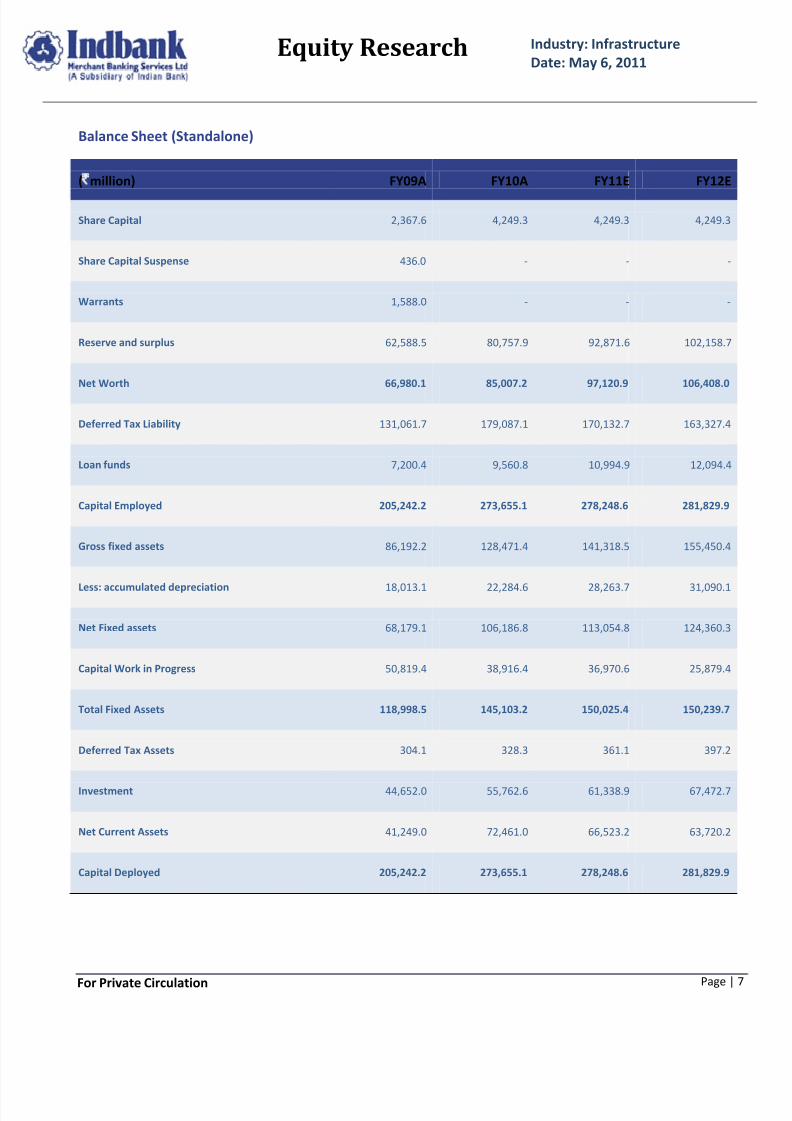

Balance Sheet (Standalone)

(` million) FY09A FY10A FY11E FY12E

Share Capital 2,367.6 4,249.3 4,249.3 4,249.3

Share Capital Suspense 436.0 - - -

Warrants 1,588.0 - - -

Reserve and surplus 62,588.5 80,757.9 92,871.6 102,158.7

Net Worth 66,980.1 85,007.2 97,120.9 106,408.0

Deferred Tax Liability 131,061.7 179,087.1 170,132.7 163,327.4

Loan funds 7,200.4 9,560.8 10,994.9 12,094.4

Capital Employed 205,242.2 273,655.1 278,248.6 281,829.9

Gross fixed assets 86,192.2 128,471.4 141,318.5 155,450.4

Less: accumulated depreciation 18,013.1 22,284.6 28,263.7 31,090.1

Net Fixed assets 68,179.1 106,186.8 113,054.8 124,360.3

Capital Work in Progress 50,819.4 38,916.4 36,970.6 25,879.4

Total Fixed Assets 118,998.5 145,103.2 150,025.4 150,239.7

Deferred Tax Assets 304.1 328.3 361.1 397.2

Investment 44,652.0 55,762.6 61,338.9 67,472.7

Net Current Assets 41,249.0 72,461.0 66,523.2 63,720.2

Capital Deployed 205,242.2 273,655.1 278,248.6 281,829.9

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 8/10

Page | 8

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

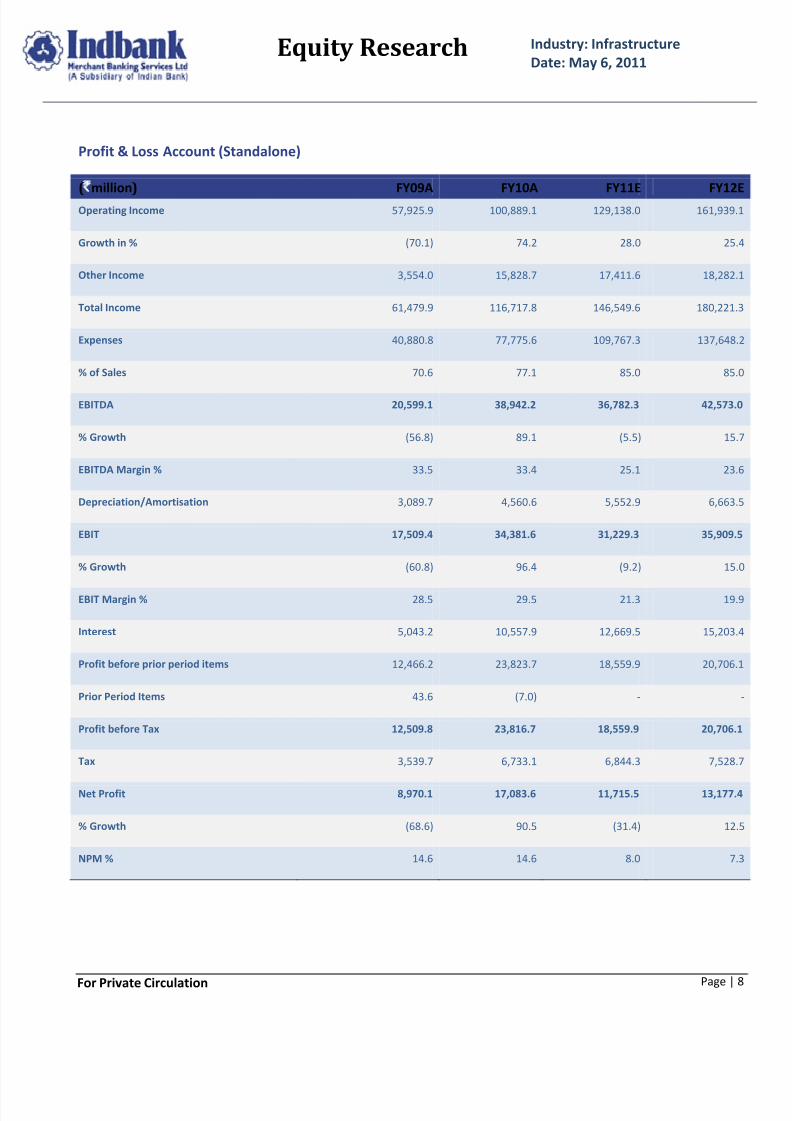

Profit & Loss Account (Standalone)

( ` million ) FY09A FY10A FY11E FY12

Operating Income 57,925.9 100,889.1 129,138.0 161,939.1

Growth in % (70.1) 74.2 28.0 25.4

Other Income 3,554.0 15,828.7 17,411.6 18,282.1

Total Income 61,479.9 116,717.8 146,549.6 180,221.3

Expenses 40,880.8 77,775.6 109,767.3 137,648.2

% of Sales 70.6 77.1 85.0 85.0

EBITDA 20,599.1 38,942.2 36,782.3 42,573.0

% Growth (56.8) 89.1 (5.5) 15.7

EBITDA Margin % 33.5 33.4 25.1 23.6

Depreciation/Amortisation 3,089.7 4,560.6 5,552.9 6,663.5

EBIT 17,509.4 34,381.6 31,229.3 35,909.5

% Growth (60.8) 96.4 (9.2) 15.0

EBIT Margin % 28.5 29.5 21.3 19.9

Interest 5,043.2 10,557.9 12,669.5 15,203.4

Profit before prior period items 12,466.2 23,823.7 18,559.9 20,706.1

Prior Period Items 43.6 (7.0) - -

Profit before Tax 12,509.8 23,816.7 18,559.9 20,706.1

Tax 3,539.7 6,733.1 6,844.3 7,528.7

Net Profit 8,970.1 17,083.6 11,715.5 13,177.4

% Growth (68.6) 90.5 (31.4) 12.5

NPM % 14.6 14.6 8.0 7.3

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 9/10

Page | 9

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

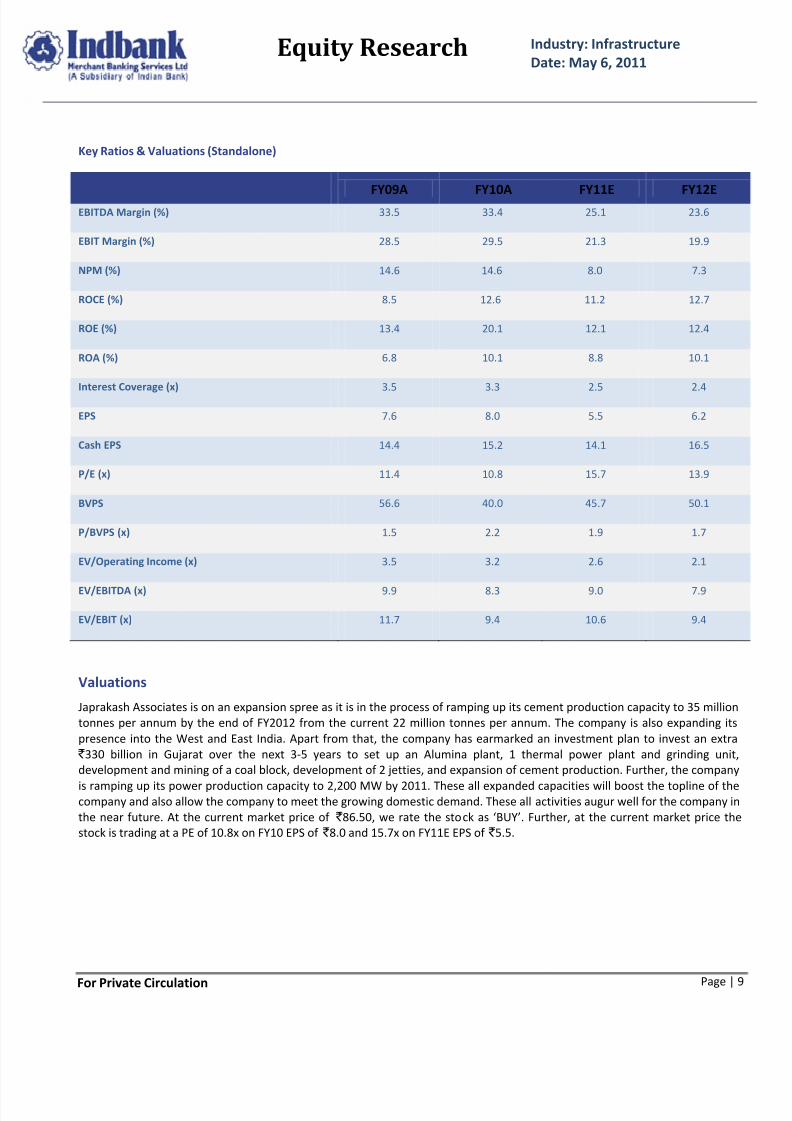

Key Ratios & Valuations (Standalone)

FY09A FY10A FY11E FY12EEBITDA Margin (%) 33.5 33.4 25.1 23.6

EBIT Margin (%) 28.5 29.5 21.3 19.9

NPM (%) 14.6 14.6 8.0 7.3

ROCE (%) 8.5 12.6 11.2 12.7

ROE (%) 13.4 20.1 12.1 12.4

ROA (%) 6.8 10.1 8.8 10.1

Interest Coverage (x) 3.5 3.3 2.5 2.4

EPS 7.6 8.0 5.5 6.2

Cash EPS 14.4 15.2 14.1 16.5

P/E (x) 11.4 10.8 15.7 13.9

BVPS 56.6 40.0 45.7 50.1

P/BVPS (x) 1.5 2.2 1.9 1.7

EV/Operating Income (x) 3.5 3.2 2.6 2.1

EV/EBITDA (x) 9.9 8.3 9.0 7.9

EV/EBIT (x) 11.7 9.4 10.6 9.4

Valuations

Japrakash Associates is on an expansion spree as it is in the process of ramping up its cement production capacity to 35 milliontonnes per annum by the end of FY2012 from the current 22 million tonnes per annum. The company is also expanding itspresence into the West and East India. Apart from that, the company has earmarked an investment plan to invest an extra

` 330 billion in Gujarat over the next 3-5 years to set up an Alumina plant, 1 thermal power plant and grinding unit,development and mining of a coal block, development of 2 jetties, and expansion of cement production. Further, the company

is ramping up its power production capacity to 2,200 MW by 2011. These all expanded capacities will boost the topline of thecompany and also allow the company to meet the growing domestic demand. These all activities augur well for the company inthe near future. At the current market price of ` 86.50, we rate the sto ck as ‘BUY’. Further, at the current market price thestock is trading at a PE of 10.8x on FY10 EPS of ` 8.0 and 15.7x on FY11E EPS of ` 5.5.

8/6/2019 Jaiprakash Associate Ltd

http://slidepdf.com/reader/full/jaiprakash-associate-ltd 10/10

Page | 10

Industry: InfrastructureDate: May 6, 2011

Equity Research

For Private Circulation

Indbank Merchant Banking Services Ltd.I Floor, Khiviraj Complex I,

No.480, Anna Salai, Nandanam, Chennai 600035Telephone No: 044 – 24313094 - 97

Fax No: 044 – 24313093www.indbankonline.com

Disclaimer

@ All Rights Reserved

This report and Information contained in this report is solely for information purpose and may not be used as an offer document or solicitationof offer to buy or sell or subscribe for securities or other financial instruments. The investment as mentioned and opinions expressed in thisreport may not be suitable for all investors. In rendering this information, we assumed and relied upon, without independent verification, theaccuracy and completeness of all information that was publicly available to us. The information has been obtained from the sources that webelieve to be reliable as to the accuracy or completeness. While every effort is made to ensure the accuracy and completeness of informationcontained, Indbank Limited and its affiliates take no guarantee and assume no liability for any errors or omissions of the information. Thisinformation is given in good faith and we make no representations or warranties, express or implied as to the accuracy or completeness of theinformation. No one can use the information as the basis for any claim, demand or cause of action.

Indbank and its affiliates shall not be liable for any direct or indirect losses or damage of any kind arising from the use thereof. Opinionexpressed is our current opinion as of the date appearing in this report only and are subject to change without any notice.

Recipients of this report must make their own investment decisions, based on their own investment objectives, financial positions and needs of the specific recipient. The recipient should independently evaluate the investment risks and should make such investigations as it deemsnecessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document and shouldconsult their advisors to determine the merits and risks of such investment.

The report and information contained herein is strictly confidential and meant solely for the selected recipient and is not meant for publicdistribution. This document should not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or tothe media or reproduced, duplicated or sold in any form.