jan. 24, - bloomberg.com · jan. 24, 2017 jan. 24, 2017 ... $19.6 bln (neg lt) sold ytd fixed: $4.6...

TRANSCRIPT

Tuesday

Jan. 24, 2017

Jan. 24, 2017

Bloomberg AAA Benchmark Yields

DESCRIPTION CURRENT PREVIOUS NET CHANGE

BVAL Muni Benchmark 1T 0.91 0.91 0

BVAL Muni Benchmark 2T 1.12 1.12 0

BVAL Muni Benchmark 3T 1.32 1.32 0

BVAL Muni Benchmark 4T 1.51 1.51 0

BVAL Muni Benchmark 5T 1.70 1.70 0

BVAL Muni Benchmark 6T 1.83 1.83 0

BVAL Muni Benchmark 7T 1.98 1.98 0

BVAL Muni Benchmark 8T 2.09 2.09 0

BVAL Muni Benchmark 9T 2.19 2.19 0

BVAL Muni Benchmark 10T 2.30 2.30 0

BVAL Muni Benchmark 20T 2.90 2.90 0

BVAL Muni Benchmark 30T 3.06 3.07 -0.01Source: GBY<GO>, GC I493 <GO>

Illinois Deal to End Deadlock Facing First Senate HurdleBy Eric EnglertIllinois lawmakers are facing the first test of a plan aimed at resolving a long-running stalemate over the budget as the state Senate today takes up a bi-partisan compromise that would raise income taxes, expand casino gambling and sell debt to cover a backlog of unpaid bills.

The measures result from a deal struck by Democratic Senate President John and the chamber’s Republican leader, that seeks to end Cullerton Christine Radogno,

the impasse that has left Illinois without a full-year spending plan in place since mid-2015. It includes some proposals that Republican Governor has sought, Bruce Rauner including a freeze on property taxes and changes to workers’ compensation laws.

"This bargain is uniquely crafted in that it fits both the urgency of the financial situation and the potential that anything less comprehensive would not generate the requisite votes," said the president of the Civic Federation, a non-profit that Laurence Msall,follows the state budget.

Illinois’s reliance on short-term spending plans has left it with the lowest credit rating of any U.S. state, stymied funding for colleges and cast fiscal uncertainty over local governments. The initial effort to resolve the impasse has been welcomed by bond investors, who pushed up the price of Illinois bonds this month and are demanding less additional yield to compensate for the risk of holding the securities.

Senate committees are set to meet today to review the 13-separate bills, with the full Senate potentially acting as soon as Wednesday. Among other steps, the bills would boost the individual income tax to 4.95 percent from 3.75 percent, raise the minimum wage, allow for the sale of as much as $7 billion of bonds to cover unpaid bills and take steps to cut Illinois’s pension costs.

It’s unclear how the measures, if adopted, would fare in the House, which would have to approve them. Rauner’s administration has also said that the legislation would still leave the state facing a $4.3 billion deficit in the current fiscal year, according to the Associated Press, while some lobbying groups have criticized the proposed tax increases. Full on the Terminal.story

STATE YIELD SPREAD TO AAA CHANGE

CA 2.51 21 -0.04

FL 2.40 10 -0.06

IL 4.54 223 -0.08

NY 2.33 3 -0.06

PA 2.97 67 -0.05

TX 2.51 21 -0.06

MUNICIPALITY AMOUNT

North Carolina Turnpike $142 million Rev

Los Angeles County MTA CA $456 million Rev

Yale University CT $125 million Rev

VIA Metro Transit TX $82 million Rev

Texas Tech $400 million RevSource: Bloomberg CDRA <GO>

AMOUNT OUTSTANDING

($MLNS)

MATURING NEXT 30

DAYS ($MLNS)

ANNOUNCED CALLS NEXT 30 DAYS ($MLNS)

3,585,221 12,630 11,273Source: MBM<GO>

Benchmark States 10-Year

30-Day Supply Fixed: $9.8 Bln (LT)30-Day Supply Fixed: $344 Mln (ST)Sold YTD Fixed: $19.6 Bln (Neg LT)Sold YTD Fixed: $4.6 Bln (Comp LT)Sold YTD Fixed: $1.1 Bln (ST)

Primary Fixed Rate

MSRB: $11.3 BlnPICK: $15.4 Bln

Secondary Market

SIFMA Muni Swap Rate: 0.66%Bloomberg Weekly AAA Rate: 0.662% Bloomberg Weekly AA Rate: 0.687% Daily Reset Inventory: $1.1 Bln Weekly Reset Inventory: $1.6 Bln

Variable Rate

In the Pipeline

Size of Market

Numbers in Context

Municipal Market 2 Jan. 24, 2017

Numbers in Context

Week Ahead Sales: Philadelphia, Nashville, L.A. MTA on TapBy Amanda AlbrightMajor U.S. metropolitan areas are coming to market this week, with Philadelphia scheduled to sell $248.8 million in bonds today to refund some of its $5.4 billion in outstanding debt. Nashville, which has attracted a steady stream of residents since 2000, will sell $457.3 million in a competitive sale, also planned for today. Given the credit concerns associated with large cities’ pensions, all eyes could be on the fiscal health of the two issuers’ retirement systems. With a funded ratio of 95 percent as of June 30, 2015, Nashville and Davidson County’s pension plan is in much better shape than Philadelphia’s, which was only 45 percent funded as of July 1, 2015.

Overall 30-day visible supply stands at about $9.8 billion, according to data

compiled by Bloomberg as of Jan. 23.

G.O. refundingBond type:: Tuesday, Jan. 24Tentative schedule

$248.8 millionPar Amount:: RBC Capital MarketsLead underwriter

: Moody’s A2, S&P A+, Fitch A-Rating: 2017 through 2041Maturities

: Philadelphia’s Municipal Key StatisticPension Plan was 45 percent funded as of July 1, 2015. The city’s unfunded actuarial liability totaled $5.9 billion as of the same period. Pension costs made up almost 13 percent of Philadelphia’s

Philadelphia

general fund budget in fiscal 2015, compared to 8 percent in fiscal 2006, according to bond documents.

: Sales tax revenueBond type: Electronic bids Tentative schedule

accepted till 8:30 A.M. PST on Wednesday, Jan. 25

: $455.7 millionPar amount: Competitive, UW TBDLead underwriter

: Moody’s Aa2, S&P AA+Rating: 2018 through 2042Maturities

: Total estimated ridership Key Statisticof the authority’s buses and rail systems has fallen about 10 percent since 2009 to about 415.9 million in 2016.

L.A. County Metropolitan Transportation Authority

Bond type: G.O. refunding: Tuesday, Jan. 24 - 11 a.m. ETSale date

: $457.3 millionPar AmountCompetitive, UW TBDLead underwriter:

: Moody’s Aa2, S&P AARating: 2018 through 2036Maturities

: The population of Key StatisticNashville has climbed 19 percent since 2000 to 678,889 people, according to 2015 estimates. In addition, there were 138 business expansions and relocations to the Nashville metropolitan area, adding 12,137 jobs in FY 2015-16, according to bond documents.

— With assistance from Danielle Moran,

Bloomberg Data

Nashville and Davidson County

Philadelphia G.O. Non-Call 2022, 2025

Municipal Market 4 Jan. 24, 2017

Q&A

2017 Macro Events Could Cause Flight to Municipals: BMO's Wimmel

The municipal market's performance will depend on Trump's policies, according to Wimmel, who oversees $3.9 billion in tax-exempt debt

Wimmel says he's more selective in the higher education sector due to cuts and demographic changes

Wimmel says hospital credits with lower exposure to Medicare and Medicaid reimbursement and a high market share are best positioned to withstand a repeal to the Affordable Care Act

Wimmel spoke with Amanda Albright on Jan. 13. Comments have been edited and condensed.

Robert Wimmel, head of municipal fixed income at BMO Global Asset Management

Q: Do you have a forecast for volume this year?A: We think it'll definitely be lower than the record issuance in 2016, perhaps down as much as 10 to 15 percent. Refundings will likely be lower this year. We saw a spike in advanced refunding deals last year, which will reduce refunding volume in 2017.

A positive for issuance this year is the high amount of bond measures with positive results on many of them. This shows a willingness for issuers to ask for more municipal financing. We're not placing much weight on President-elect Trump's plans for infrastructure spending this year because there are too many unknowns at this point. We don’t know if his intent will be to issue tax-exempt debt, which could obviously increase tax-exempt municipal issuance in 2017 or 2018. There are too many question marks over what form the $1 trillion in infrastructure spending will take.

Q: Where do you find value in the munimarket?

We have had a history of finding value A: in shorter maturities by smaller municipal issuers. Many of those deals are overlooked by the larger institutions. They can come relatively cheaper than to comparably rated, larger issues. The additional yield of those bonds helps performance over time. We like higher quality BB+ to A rated continuing care retirement community bonds. We also select out-of-favor credits, such as local school districts in Illinois.

Q: Why do you find value in Illinoisschool districts?

: They are experiencing some spread Awidening just due to the problems at the state level in Illinois. You can find good

value in very strong, AA rated local school districts, many in the Chicago suburban area, that come at a discount because of the name association with the state of Illinois. They're still solid credits.

Q: Are there any sectors you avoid? We don’t like to make a blanket A:

statement that we're not buying a certain sector in the municipal market. There's tens of thousands of active issuers. However, we are being more selective in the higher education sector.

The nation's demographic trends are working against that sector, with less high school graduates, particularly in the Northeast and Midwest. Secondly, strained state budgets are squeezing the funding to public higher education schools.

We look for institutions with good demand due to name recognition or some niche that they might have, like a good engineering or medical school. We're also looking for schools located in states with good demographics and finances, making the state less likely to cut higher education funding.

: Q How much of a concern are Trump'splans for tax reform?

: If you look at the correlation between Athe relative values of municipal bonds to Treasuries by looking at the yield ratio, there's not a good correlation to say that municipals will definitely be cheaper if President Trump lowers the highest effective tax bracket. There are periods of time where the highest marginal tax bracket was much lower than today but municipals were richer. What we believe is if he lowers tax rates and tax brackets in general, muni bonds do not necessarily have to under-perform. People will still want the tax-exemption. Going forward,

we're still the only tax exempt asset class out there.

Q: How do you evaluate the likelihood of the repeal of the Affordable Care

Act? Has this caused you to change your portfolio?A: It is definitely high potential. We think it is a good time to re-evaluate your hospital holdings. We're still actively buying hospital bonds. The reduction or elimination of subsidies is negative for hospitals as volumes will likely suffer and uncompensated care will likely increase. We looked at our lower quality hospital bonds, attempting to identify those that may be most affected by the repeal of ACA. Surprisingly, we only found a handful of hospitals that could see rating deterioration.

Q: What sorts of hospital credits do you see as most able to withstand a repeal of the Affordable Care Act? A: Look for the hospitals with lower exposure to Medicare and Medicaid reimbursement and look for the larger hospitals with a high market share and part of a regional system and multi-site system.

Q: How concerned are you about unfunded pension liabilities?

: Over the past two years, we've placed Amore weight on the pension funding for the stress that’s causing local issuers. I can't say at this time that it's my main concern in the municipal market. It's been a problem over the decade; it's been a problem that will take decades to work itself out. So far what we've seen is a willingness across the nation to address these pension problems on a local basis as well as on a statewide basis.

Continued on next page…

Municipal Market 5 Jan. 24, 2017

Continued from previous page...

Q&A…

Some credits are struggling more than others. In Chicago, it will take a while to get to a level of tax increases to support future pension plans. But progress is being made. I have perhaps too much faith, according to some of my colleagues, that it'll work out in the end. The wherewithal of the system, of politicians and their electors, is there to face that problem.

A: What else would you like to see Chicago do to address the

underfunding of its pension plans? I think they've done as much as the A:

public can take at this point in time. You can't lay too much on them to address the total pension un-funding in one or two years. It will take several years of different types of tax increases, as well as, perhaps, some give on the pension plans themselves to correct the problem long term. The mayor has done a very good job, so far, of beginning to show the willingness to address the problem.

Q: If not pensions, is there anything inthe market that keeps you up at night?

Now it would be the potential changes A: that the new administration might be bringing. As far as interest rates increasing over the coming year, I don’t think there's much of that to fear as many

investors do. There's too many potential macro and global policy problems that might crop up over the next year that could cause a flight to quality, particularly into Treasuries, and into the U.S. municipal bond market as well. We have Brexit out there — will we have a hard or soft landing? — you have problems in some of the European banks, particularly in Italy, you have elections in the not-so-distant future in several countries in Europe as well. You're going to see more concerns. The psychology of the market can turn on a dime, as you’ve seen in the past.

All of a sudden we're not talking about Trump's policies causing a significant increase in interest rates, we're seeing interest rates declining because of a flight

to quality. I think that could happen at any time this year.

Munis could benefit from any kind of global financial event. They would move in the same direction as Treasuries, albeit not as quickly.

Q: How many times do you predict the Federal Reserve will raise interest rates this year, given the potential for

these events you described? The best I can say is that I think that I A:

am giving very little credence to the number of hikes that the Fed has said they'd like to see in 2017. There are too many possible macro events that could occur for them to take interest rate hikes out of the market.

At a Glance

Residence: Chicago, IllinoisEducation: M.A. in Economics from the University of Illinois at Chicago and a B.A. in Anthropology cum laude from the University of CincinnatiCareer History: Started career at City of Chicago helping issue and manage debt. Spent several years as a municipal research analyst on the sell-side and then onto over 20 years in municipal asset management.Favorite Sports Team: Chicago BlackhawksHobbies: Hiking, biking and travelingIf I could have another career: Archaeologist

According To

Municipal Market 6 Jan. 24, 2017

According To

Hedge funds that hold Puerto Rico’s sales-tax backed bonds have offered $800 million of financing to alleviate the island’s cash crunch, according to a person familiar with the matter.

The offer comes as creditors are vying for position as Puerto Rico begins negotiations aimed at cutting its $70 billion debt.

A group holding Puerto Rico’s senior sales-tax debt, known as Cofina, that’s led by Tilden Park Capital Management LP, Merced Capital LP, Whitebox AdvisorsLLC and Goldentree Asset Management LP, proposed letting Puerto Rico access roughly $400 million in sales-tax revenue that has already been collected, according to the person. The creditors would then purchase about $400 million in long-term sales-tax bonds at market rates

Hedge Funds Said to Offer $800 Million Financing to Puerto Rico

as long as Puerto Rico doesn’t seek additional concessions from holders of Cofinas.

A spokesman for the federal fiscal board created to oversee the island’s finances didn’t immediately respond to an emailed request for comment. The Wall Street Journal reported the news earlier yesterday.

The governor’s representative to the board, Elias Sanchez, said that the government has received no formal offer but that the proposal was discussed in meetings.

— Rebecca Spalding

Connecticut’s agreement with labor unions to change some pension funding assumptions of the State Employees Retirement System has a “mildly positive”

Connecticut Deal With Unions on Pensions ‘Mildly Positive’: S&P

impact on the state’s credit, S&P Global Ratings said.

The agreement allows the state to avoid a potential spike in pension contributions in 10 years by extending the amortization period of unfunded pension liabilities, but doesn’t significantly increase contributions or change benefits. The deal reduces the assumed rate of return on pension to a “more reasonable,” 6.9 percent from 8 percent, S&P said.

The new return assumptions reduces the pension’s funded ratio to 35.5 percent, down from 41.5 percent. The stretched amortization schedule allows state to avoid higher contributions in fiscal 2017 and 2018, postponing budget pain.

S&P remains concerned that 32 percent of forecast 2018 general fund revenue goes to debt service, pensions and other post-employment benefits.

— Martin Z. Braun

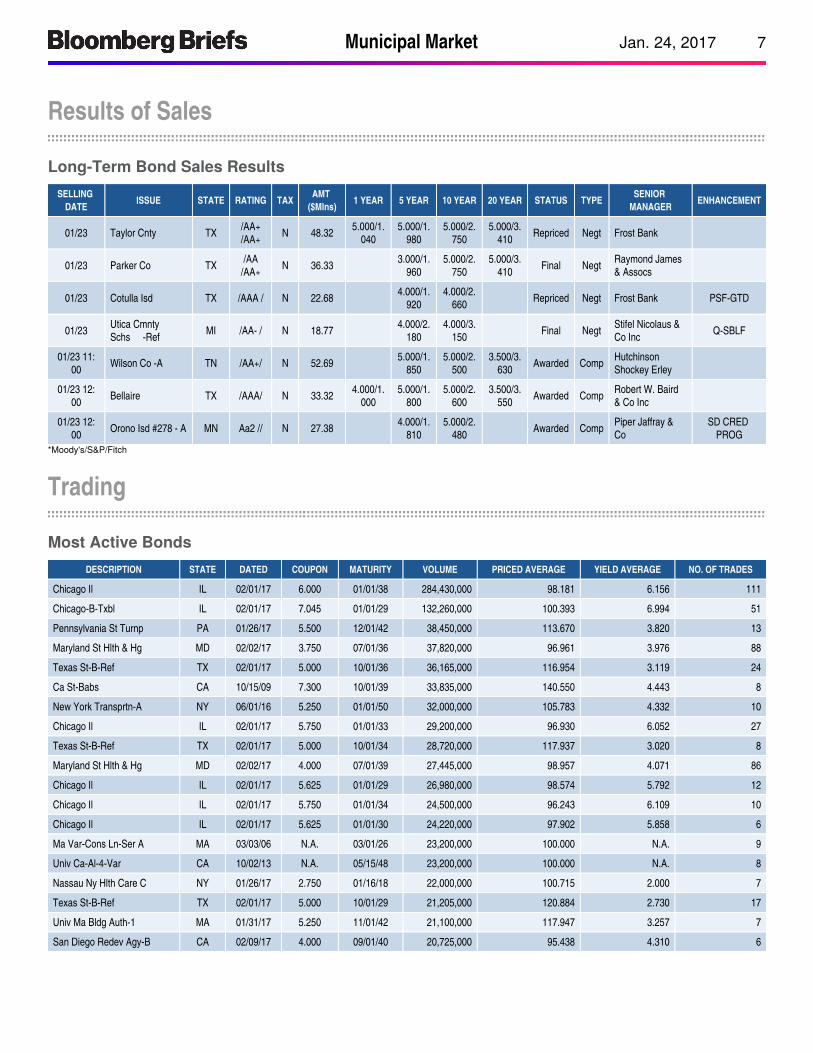

Results of Sales

Municipal Market 7 Jan. 24, 2017

Long-Term Bond Sales Results

SELLING DATE

ISSUE STATE RATING TAXAMT

($Mlns)1 YEAR 5 YEAR 10 YEAR 20 YEAR STATUS TYPE

SENIOR MANAGER

ENHANCEMENT

01/23 Taylor Cnty TX/AA+/AA+

N 48.325.000/1.

0405.000/1.

9805.000/2.

7505.000/3.

410Repriced Negt Frost Bank

01/23 Parker Co TX/AA

/AA+N 36.33

3.000/1.960

5.000/2.750

5.000/3.410

Final NegtRaymond James & Assocs

01/23 Cotulla Isd TX /AAA / N 22.684.000/1.

9204.000/2.

660Repriced Negt Frost Bank PSF-GTD

01/23Utica Cmnty Schs -Ref

MI /AA- / N 18.774.000/2.

1804.000/3.

150Final Negt

Stifel Nicolaus & Co Inc

Q-SBLF

01/23 11:00

Wilson Co -A TN /AA+/ N 52.695.000/1.

8505.000/2.

5003.500/3.

630Awarded Comp

Hutchinson Shockey Erley

01/23 12:00

Bellaire TX /AAA/ N 33.324.000/1.

0005.000/1.

8005.000/2.

6003.500/3.

550Awarded Comp

Robert W. Baird & Co Inc

01/23 12:00

Orono Isd #278 - A MN Aa2 // N 27.384.000/1.

8105.000/2.

480Awarded Comp

Piper Jaffray & Co

SD CRED PROG

*Moody's/S&P/Fitch

Most Active Bonds

DESCRIPTION STATE DATED COUPON MATURITY VOLUME PRICED AVERAGE YIELD AVERAGE NO. OF TRADES

Chicago Il IL 02/01/17 6.000 01/01/38 284,430,000 98.181 6.156 111

Chicago-B-Txbl IL 02/01/17 7.045 01/01/29 132,260,000 100.393 6.994 51

Pennsylvania St Turnp PA 01/26/17 5.500 12/01/42 38,450,000 113.670 3.820 13

Maryland St Hlth & Hg MD 02/02/17 3.750 07/01/36 37,820,000 96.961 3.976 88

Texas St-B-Ref TX 02/01/17 5.000 10/01/36 36,165,000 116.954 3.119 24

Ca St-Babs CA 10/15/09 7.300 10/01/39 33,835,000 140.550 4.443 8

New York Transprtn-A NY 06/01/16 5.250 01/01/50 32,000,000 105.783 4.332 10

Chicago Il IL 02/01/17 5.750 01/01/33 29,200,000 96.930 6.052 27

Texas St-B-Ref TX 02/01/17 5.000 10/01/34 28,720,000 117.937 3.020 8

Maryland St Hlth & Hg MD 02/02/17 4.000 07/01/39 27,445,000 98.957 4.071 86

Chicago Il IL 02/01/17 5.625 01/01/29 26,980,000 98.574 5.792 12

Chicago Il IL 02/01/17 5.750 01/01/34 24,500,000 96.243 6.109 10

Chicago Il IL 02/01/17 5.625 01/01/30 24,220,000 97.902 5.858 6

Ma Var-Cons Ln-Ser A MA 03/03/06 N.A. 03/01/26 23,200,000 100.000 N.A. 9

Univ Ca-Al-4-Var CA 10/02/13 N.A. 05/15/48 23,200,000 100.000 N.A. 8

Nassau Ny Hlth Care C NY 01/26/17 2.750 01/16/18 22,000,000 100.715 2.000 7

Texas St-B-Ref TX 02/01/17 5.000 10/01/29 21,205,000 120.884 2.730 17

Univ Ma Bldg Auth-1 MA 01/31/17 5.250 11/01/42 21,100,000 117.947 3.257 7

San Diego Redev Agy-B CA 02/09/17 4.000 09/01/40 20,725,000 95.438 4.310 6

Results of Sales

Trading

Tweet of the Day

Municipal Market 8 Jan. 24, 2017

Find Muni Data on the Bloomberg Terminal

DATA FREQUENCY ON THE TERMINAL

AAA Benchmark Valuation Daily GC i493 <GO>

Benchmark State Yields Daily MBM <GO>

VRDO Rates, Inventory Daily MBIX <GO>, ALLX BVRD <GO>

Upcoming Sales Daily CDRA <GO>

Volume, MSRB, PICK Daily SPLY <GO>, YTDM <GO>, MSRB <GO>, MBIX <GO>

Results of Sales Daily CDRA <GO>

Most Active Daily MSRB <GO>

Most Searched DES Every Wednesday SECF <GO>

Variable-Rate Calendar Every Thursday CDRV <GO>

Most Traded Borrowers Every Friday MFLO <GO>

Week-Ahead Calendar Every Monday CDRA <GO>

Supply and Demand Every Friday SPLY <GO>, BVMB <GO>

Muni Credit Risk Every Monday MRSK <GO>

Tweet of the Day

Misdrilled Holes May Have Compromised Span

Tom Kozlik@tomkozlik

Decades-old mistake may have caused bridge beam to fail #infrastructure #Bridge philly.com/philly/busines…Details

The PNC Bank managing director and municipal strategist tweets a link to a Philly.com story about what closed the Delaware River-Turnpike Bridge: "An apparent construction error six decades ago could have caused the fracture discovered Friday in a steel beam that forced the closure of the Delaware River Bridge, an engineering expert who viewed pictures of the cracked truss said on Sunday.''

— Joe Mysak

Bloomberg Brief:Municipal Market

Newsletter Managing Editor

Paul Smith

Municipal Market Editor

Joe Mysak

Municipal Market Reporter

Amanda Albright

Brief Editor

Siobhan Wagner

Contributing Analyst

Sowjana Sivaloganathan

Municipal Data Team

Marketing & Partnership Director

Courtney Martens

+1-212-617-2447

Advertising

Lucy Rosen

+1-212-617-6759

Reprints & Permissions

Lori Husted

+1-717-505-9701 x2204

Interested in learning more about the

Bloomberg terminal?

Request a free demo .here