jcp: how pennies make dollars - valuewalk - … how pennies make dollars ... accessories and...

TRANSCRIPT

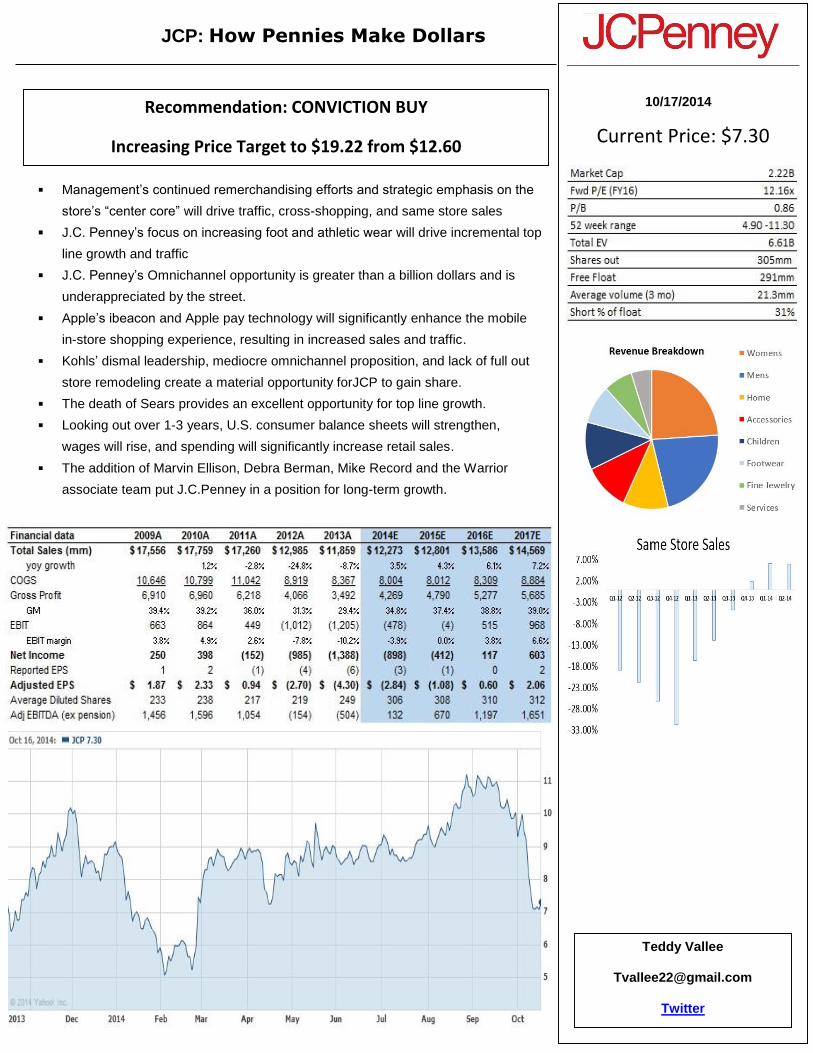

Current Price: $7.30

JCP: How Pennies Make Dollars

10/17/2014

Management’s continued remerchandising efforts and strategic emphasis on the

store’s “center core” will drive traffic, cross-shopping, and same store sales

J.C. Penney’s focus on increasing foot and athletic wear will drive incremental top

line growth and traffic

J.C. Penney’s Omnichannel opportunity is greater than a billion dollars and is

underappreciated by the street.

Apple’s ibeacon and Apple pay technology will significantly enhance the mobile

in-store shopping experience, resulting in increased sales and traffic.

Kohls’ dismal leadership, mediocre omnichannel proposition, and lack of full out

store remodeling create a material opportunity forJCP to gain share.

The death of Sears provides an excellent opportunity for top line growth.

Looking out over 1-3 years, U.S. consumer balance sheets will strengthen,

wages will rise, and spending will significantly increase retail sales.

The addition of Marvin Ellison, Debra Berman, Mike Record and the Warrior

associate team put J.C.Penney in a position for long-term growth.

Recommendation: CONVICTION BUY

Increasing Price Target to $19.22 from $12.60

Teddy Vallee

The recent sell-off in J.C. Penney provides an excellent entry point for a long-term investor. After trading up about two percent

during the analyst day presentation (10/8), the stock sold off significantly after the company lowered its Q3 guidance from mid-

single digits to low-single digits. Given America’s strengthening consumer, the appointment of a long-term CEO, a compelling

omnichannel strategy, and the mitigation of bankruptcy fears, I have significant conviction in J.C. Penney’s turnaround. The

company is worth $19.22 per share.

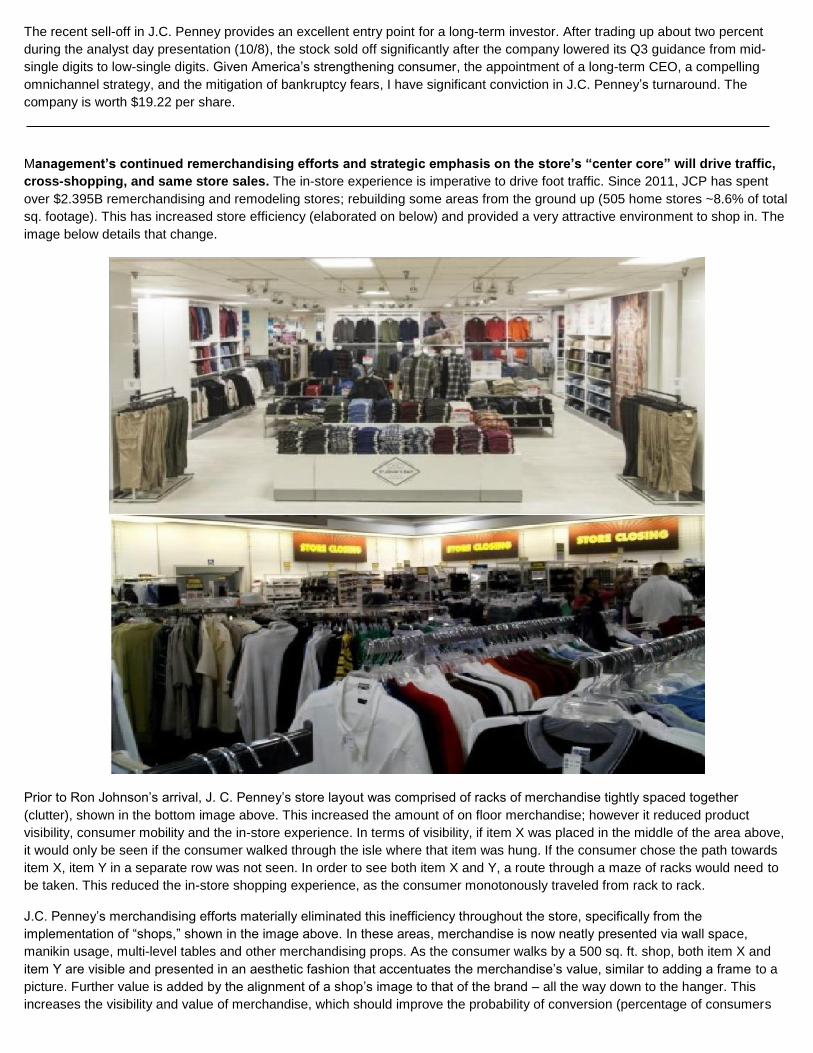

Management’s continued remerchandising efforts and strategic emphasis on the store’s “center core” will drive traffic,

cross-shopping, and same store sales. The in-store experience is imperative to drive foot traffic. Since 2011, JCP has spent

over $2.395B remerchandising and remodeling stores; rebuilding some areas from the ground up (505 home stores ~8.6% of total

sq. footage). This has increased store efficiency (elaborated on below) and provided a very attractive environment to shop in. The

image below details that change.

Prior to Ron Johnson’s arrival, J. C. Penney’s store layout was comprised of racks of merchandise tightly spaced together

(clutter), shown in the bottom image above. This increased the amount of on floor merchandise; however it reduced product

visibility, consumer mobility and the in-store experience. In terms of visibility, if item X was placed in the middle of the area above,

it would only be seen if the consumer walked through the isle where that item was hung. If the consumer chose the path towards

item X, item Y in a separate row was not seen. In order to see both item X and Y, a route through a maze of racks would need to

be taken. This reduced the in-store shopping experience, as the consumer monotonously traveled from rack to rack.

J.C. Penney’s merchandising efforts materially eliminated this inefficiency throughout the store, specifically from the

implementation of “shops,” shown in the image above. In these areas, merchandise is now neatly presented via wall space,

manikin usage, multi-level tables and other merchandising props. As the consumer walks by a 500 sq. ft. shop, both item X and

item Y are visible and presented in an aesthetic fashion that accentuates the merchandise’s value, similar to adding a frame to a

picture. Further value is added by the alignment of a shop’s image to that of the brand – all the way down to the hanger. This

increases the visibility and value of merchandise, which should improve the probability of conversion (percentage of consumers

that enter a store and make a purchase). It is also likely that transaction sizes and items per transaction increase as the consumer

is exposed to additional items previously hidden.

At the recent analyst day, the company highlighted the “center core” opportunity, which is comprised of beauty, footwear, jewelry,

handbags, accessories and intimate apparel attractions that drive customers to the heart of the store, facilitating cross shopping.

Center core is extremely important given its higher growth rate and operating margin relative to apparel. Management believes

that this is a $1B opportunity over the next three years, or $333mm per year in incremental revenue, and have acknowledged the

core area is currently deficient relative its competition. That said, piloted stores have seen major sales increases in each category,

with no additional space. The store improvements should be completed by the end of FY15. This will further increase the aesthetic

and likely the efficiency of the store, resulting in higher traffic, conversion rates, and same store sales. Below is a concept

sunglass shop and a piloted watch shop that will be located in the core area.

J.C. Penney’s focus on increasing foot and athletic wear will drive incremental top line growth and traffic. Footwear is a

major growth category for JCP. The company has acknowledge their current shoe selling environment is unexciting and cramped.

Going forward, women’s footwear selling space will be increased by 30% with a new clean full service environment for fashion

footwear. JCP noted that research has shown women consider shopping for shoes a form of entertainment. Men’s footwear was

also expanded, but metrics were not provided. The piloted studies exceeded management’s expectations, increasing “entire store

sales by several hundred basis points,” per Liz Sweney’s analyst day comments.

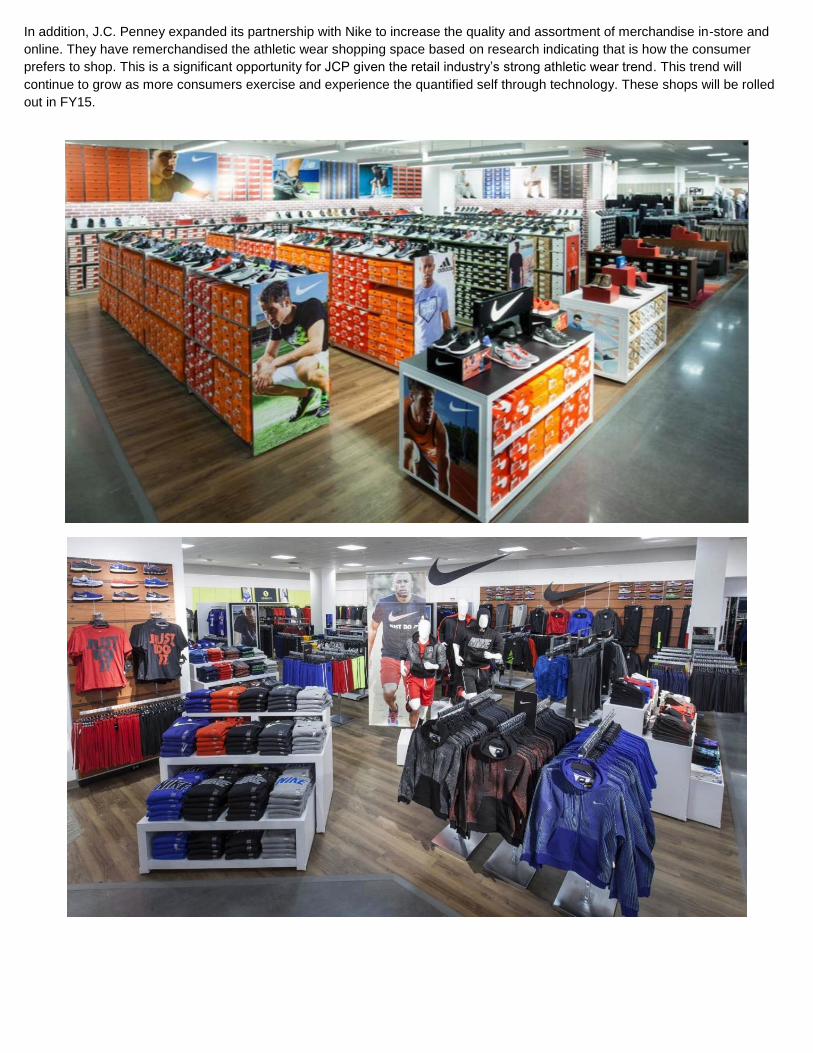

In addition, J.C. Penney expanded its partnership with Nike to increase the quality and assortment of merchandise in-store and

online. They have remerchandised the athletic wear shopping space based on research indicating that is how the consumer

prefers to shop. This is a significant opportunity for JCP given the retail industry’s strong athletic wear trend. This trend will

continue to grow as more consumers exercise and experience the quantified self through technology. These shops will be rolled

out in FY15.

J.C. Penney’s Omnichannel opportunity is greater than a billion dollars and is underappreciated by the street.

Omnichannel is a seamless relationship from marketing to browsing to check out between stores, online, and mobile devices.

Management outlined at the analyst day presentation that this is an $800mm opportunity through FY17, or $266mm on average in

incremental sales per year. I think $800mm is conservative based on the appointment of omnichannel veteran, Mike Rodgers,

from Saks Fifth Avenue. At the analyst day presentation Rodgers stated, “it's got to be fast, our website has got to be fast, our app

has got to be fast. We've got to get it to the customer quickly or get it back to the store for them to pick up, or pick up the same

day. Flexible, anywhere, anytime, anyplace on any device. For me, it's got to be personalized. We've got to deliver the right

content to the specific customer that it is interesting to them, not generalized.” Rodgers, more than any other executive at Penney,

understands what the industry will look like three to five years from now and is positioning the company today to be a leader

tomorrow.

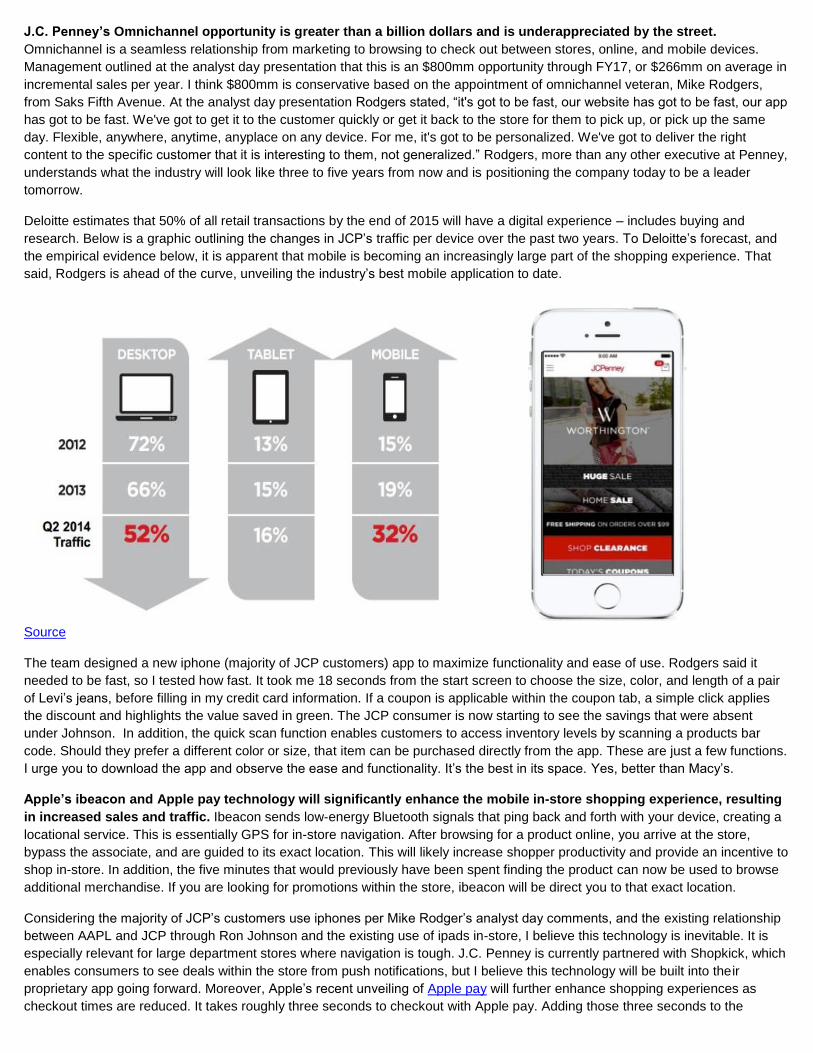

Deloitte estimates that 50% of all retail transactions by the end of 2015 will have a digital experience – includes buying and

research. Below is a graphic outlining the changes in JCP’s traffic per device over the past two years. To Deloitte’s forecast, and

the empirical evidence below, it is apparent that mobile is becoming an increasingly large part of the shopping experience. That

said, Rodgers is ahead of the curve, unveiling the industry’s best mobile application to date.

Source

The team designed a new iphone (majority of JCP customers) app to maximize functionality and ease of use. Rodgers said it

needed to be fast, so I tested how fast. It took me 18 seconds from the start screen to choose the size, color, and length of a pair

of Levi’s jeans, before filling in my credit card information. If a coupon is applicable within the coupon tab, a simple click applies

the discount and highlights the value saved in green. The JCP consumer is now starting to see the savings that were absent

under Johnson. In addition, the quick scan function enables customers to access inventory levels by scanning a products bar

code. Should they prefer a different color or size, that item can be purchased directly from the app. These are just a few functions.

I urge you to download the app and observe the ease and functionality. It’s the best in its space. Yes, better than Macy’s.

Apple’s ibeacon and Apple pay technology will significantly enhance the mobile in-store shopping experience, resulting

in increased sales and traffic. Ibeacon sends low-energy Bluetooth signals that ping back and forth with your device, creating a

locational service. This is essentially GPS for in-store navigation. After browsing for a product online, you arrive at the store,

bypass the associate, and are guided to its exact location. This will likely increase shopper productivity and provide an incentive to

shop in-store. In addition, the five minutes that would previously have been spent finding the product can now be used to browse

additional merchandise. If you are looking for promotions within the store, ibeacon will be direct you to that exact location.

Considering the majority of JCP’s customers use iphones per Mike Rodger’s analyst day comments, and the existing relationship

between AAPL and JCP through Ron Johnson and the existing use of ipads in-store, I believe this technology is inevitable. It is

especially relevant for large department stores where navigation is tough. J.C. Penney is currently partnered with Shopkick, which

enables consumers to see deals within the store from push notifications, but I believe this technology will be built into their

proprietary app going forward. Moreover, Apple’s recent unveiling of Apple pay will further enhance shopping experiences as

checkout times are reduced. It takes roughly three seconds to checkout with Apple pay. Adding those three seconds to the

previous 18 it took me to arrive at the checkout menu on the JCP app, yields a 21 second jean purchase. If that is not easy and

fast, I don’t know what is.

This is the future of retail and it is unfolding at J.C. Penney.

Kohls’ dismal leadership, mediocre omnichannel proposition, and lack of full out store remodeling create a material

opportunity forJCP to gain share. Kohls has traded flat over the past five years and for good reason. Its value proposition is

unclear, its stores are still filled with racks of clutter, and its CEO is outlining a “greatness agenda” that will put the company only

two steps behind J.C. Penney and Macy’s. The biggest piece of their new strategy is a loyalty program that will be launched next

month. Rather than exclusivity to Kohls’ card holders, the awards program will be open to all shoppers, regardless of their credit

quality or preferred payment method. This sounds like a direct hit to margins. Additionally, Kohls is increasing its national brand

mix (100-400 BPS lower margin) over its own private label. This will further reduce margins and is a potential warning sign on the

quality/style of its private label brands.

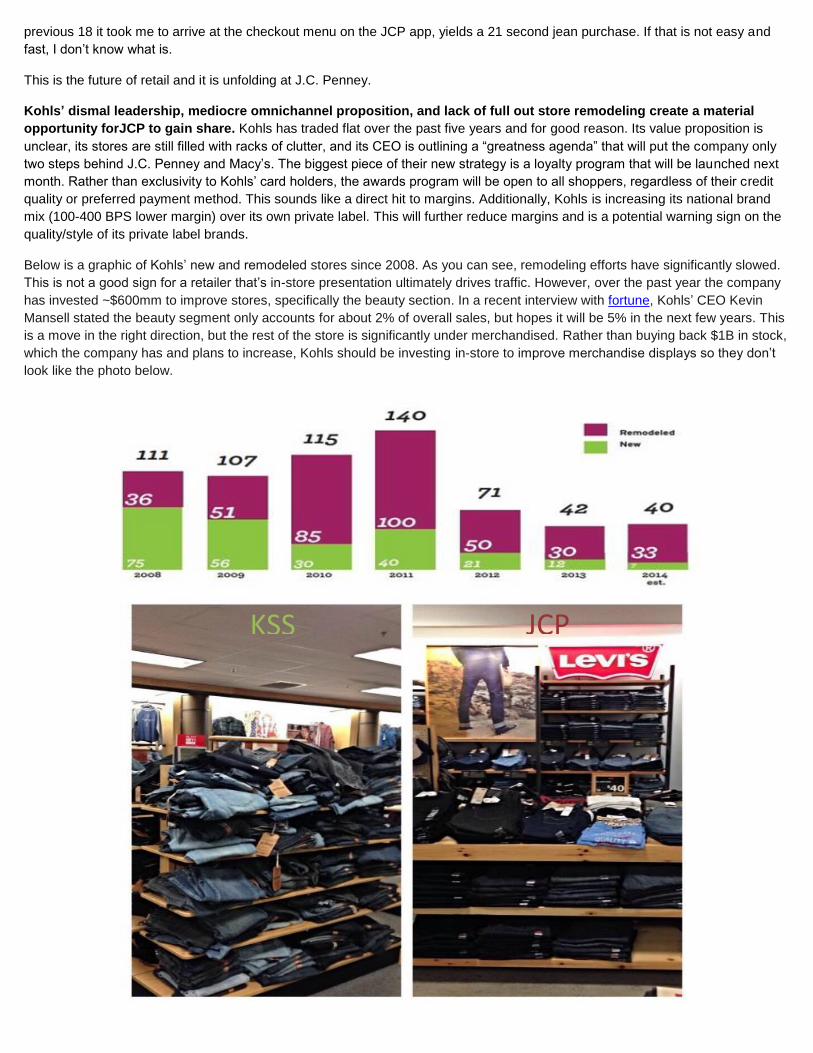

Below is a graphic of Kohls’ new and remodeled stores since 2008. As you can see, remodeling efforts have significantly slowed.

This is not a good sign for a retailer that’s in-store presentation ultimately drives traffic. However, over the past year the company

has invested ~$600mm to improve stores, specifically the beauty section. In a recent interview with fortune, Kohls’ CEO Kevin

Mansell stated the beauty segment only accounts for about 2% of overall sales, but hopes it will be 5% in the next few years. This

is a move in the right direction, but the rest of the store is significantly under merchandised. Rather than buying back $1B in stock,

which the company has and plans to increase, Kohls should be investing in-store to improve merchandise displays so they don’t

look like the photo below.

KSS JCP

Kohls has also failed to announce its intentions for same-day delivery, which may be a result of its distribution square footage

being 33% smaller than J.C. Penneys. Kohls also severely lags behind JCP and Macy’s mobile application, albeit the only one

with an ipad app. Kohls is farther behind than most of the street is willing to recognize, given that the majority of analysts have an

outperform rating. J.C. Penney outlined market share gains totaling $1B over the next three years and I see a sizable portion of

that $1B coming from Kohls.

The death of Sears provides an excellent opportunity for top line growth. Sears is in freefall. The company is losing over $1B

in operating cash flow per year and has roughly $840mm in cash and cash equivalents on the balance sheet as of August 2nd.

Suppliers are beginning to halt shipments after credit insurance providers sent out cancellation notices. Sears’ value is in its real

estate, which will only be recognized through liquidation. This is the most viable option, as shareholders are losing value daily.

That said, this provides a significant opportunity for J.C. Penney.

Sears had $9.495B in sales of apparel and soft home in 2013. Of their store base, 40% (786 / 1,980) are on-mall locations, in

which there is another anchor tenant. JCP has 50% of its stores on-mall versus Kohls’ 7%; the alternative being strip or

freestanding. Assuming that there is a 75% chance that JCP is the other anchor (given 50% of stores are on-mall vs. Kohls 7%),

27% of Sears U.S. sales are apparel and soft home (based on 2013 numbers - 9,495 / 35,544), 70% of sales transfer to the

competing anchor, and this applying to 40% of stores, yields $540mm opportunity. This is only on 40% of their store base, so

Sears itself could cover the full $1B market share opportunity that JCP has outlined. Capturing a conservative 10% of sales

equates to roughly the full share gain as well. I think this opportunity is much greater than what the market believes.

Looking out over 1-3 years, U.S. consumer balance sheets will strengthen, wages will rise, and spending will

significantly increase retail sales. Last month, Bank of America’s Senior Economist, Michelle Meyer, spoke to Bloomberg about

her recent study on wages since the great recession. She found that wages are sticky downwards, in other words, they maintain a

level that is higher than what should be realized during an economic downturn. The reasoning plays into the psychology of

employers with respect to employees; cutting wages reduces moral; however, cutting jobs allows costs to come down while

incentivizing the remaining few for making the cut. Thus, the reason why we are not seeing strengthening wages in the face of

robust job gains likely has to do with the current wage rate being at, or slightly below, its fair market value. That said, once this

level is met, the incremental gains will likely rise at a much higher clip than many anticipate, similar to a stock breaking through a

previous resistance level. I view this level to be on the horizon given the current stage of the U.S. recover. This will significantly

improve household balance sheets, providing an incentive to spend.

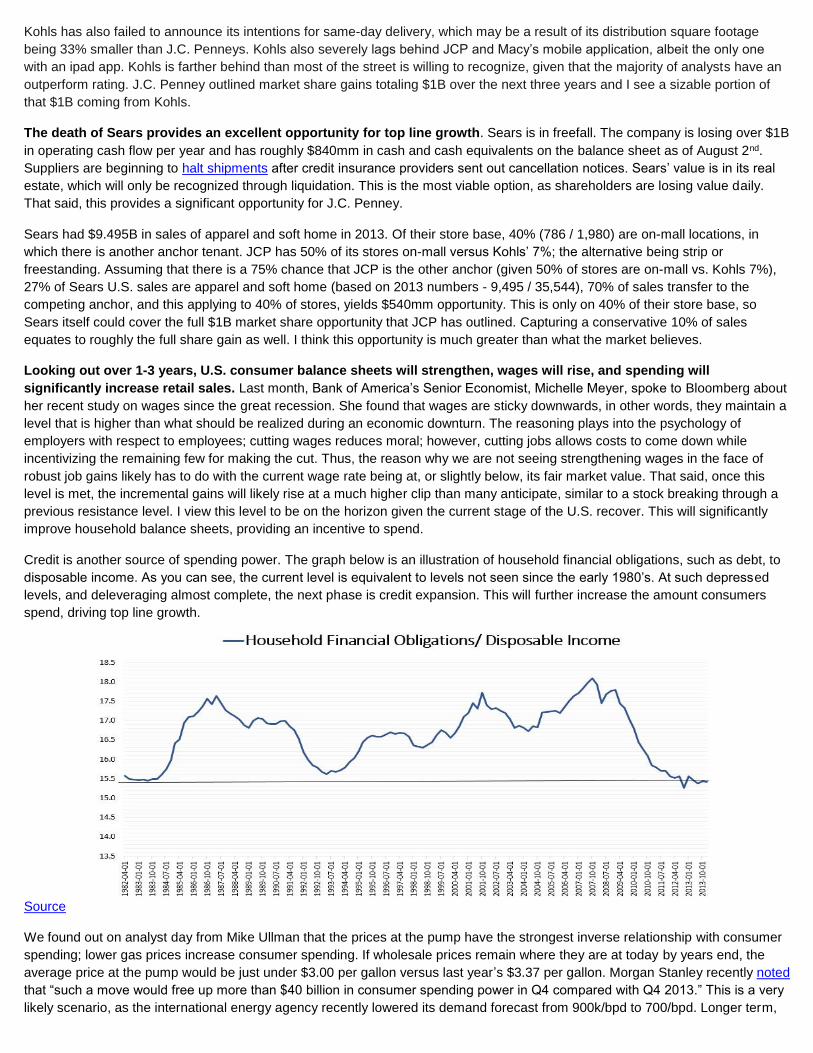

Credit is another source of spending power. The graph below is an illustration of household financial obligations, such as debt, to

disposable income. As you can see, the current level is equivalent to levels not seen since the early 1980’s. At such depressed

levels, and deleveraging almost complete, the next phase is credit expansion. This will further increase the amount consumers

spend, driving top line growth.

Source

We found out on analyst day from Mike Ullman that the prices at the pump have the strongest inverse relationship with consumer

spending; lower gas prices increase consumer spending. If wholesale prices remain where they are at today by years end, the

average price at the pump would be just under $3.00 per gallon versus last year’s $3.37 per gallon. Morgan Stanley recently noted

that “such a move would free up more than $40 billion in consumer spending power in Q4 compared with Q4 2013.” This is a very

likely scenario, as the international energy agency recently lowered its demand forecast from 900k/bpd to 700/bpd. Longer term,

oil prices will likely remain depressed as Saudi Arabia continues to increase supply to shake competition and gain share, as well

as the emergence of alternative energy sources, such as natural gas and solar reducing demand.

Increasing wages, reduced debt loads, and falling gas prices all provide the consumer with enough ammunition to significantly lift

retail sales over the next 1-3 years. Shorter term, it is likely Q3 spending numbers will not impress due to pent up demand being

unleashed in Q2. However, Q4 will likely see material gains, especially if the weather is relatively normal.

The addition of Marvin Ellison, Debra Berman, Mike Record and the Warrior associate team put J.C.Penney in a position

for long-term growth. This week, J.C.Penney appointed Marvin Ellison as the President and CEO designee after many months

of uncertainty. While many on the street are skeptical, I think this is a very intelligent move from the board. Ellison comes to a

company that has undergone a major transformation, beginning with Ron Johnson. Johnson laid out a framework and foundation

for department store retailing of the future similar to what Jobs did for Apple. Now, Marvin Ellison, the Tim Cook of JCP, can use

his supply chain retail experience to execute that vision and the omnichannel strategy, as it requires a significant amount of

logistics. Ullman has built a strong retail team around Ellison, which more than makes up for the softline/fashion prowess that

many think he lacks. Ellison’s back is up against the wall, but it’s a familiar feeling considering he was tasked with turning around

Home Depot after the housing crisis. With over 30 years of retail experience, I think he is the right man for the job.

As touched on above, Ed record is another key player to the JCP store.

Debra Berman (CMO) recently joined JCP from Kraft. She is another strong hire with significant experience in the industry. Under

her leadership over the past year, advertisements have been more engaging even though ad spending was lower than historical

levels. She has given the company an additional way to look at their consumer, addressing them through new sales and

promotions, ultimately increasing return on ad spend. The company noted that they will be returning marketing spend to historical

levels.

The Warrior program unveiled at the recent analyst day presentation will likely have a positive impact on in-store experiences. The

program essentially urges employees to foster a warrior’s win-at-all-costs mentality. It initially started with 16 leaders and turned

into 1,100 teams and 100,000 associates. Since starting the program, overall customer satisfaction has gone from 62, a point

higher than the industry average, to 71. This is a significant increase in one year.

Management’s FY17 guidance implies a conservative 36.5% gross margin, significantly below J.C. Penney’s historical

average of 37-39%. There is no question that the company will be able to print a GM between 37-39% in 2017 given its move into

higher margined categories (jewelry, footwear, handbags, sunglasses), cleaner inventory positions, and historical private label

brand sales mixes (400-500 BPS higher than national). In addition, the strength of the dollar relative to the Yuan decreases the

cost of inventory and increases GM. With the Federal Reserve tightening and a slow-down in China, the dollar should maintain

strength over the next 1-3 years. The industry is becoming more competitive, but a commonly misunderstood part of department

store retailing is pricing and markdowns. Below is graphic from J.C. Penney’s 1/25/12 rebrand event. Understanding that historical

margins were attained when greater than 72% of sales were marked down by 50% should mitigate concerns of competition driving

substantial markdowns, in turn adversely affecting margins.

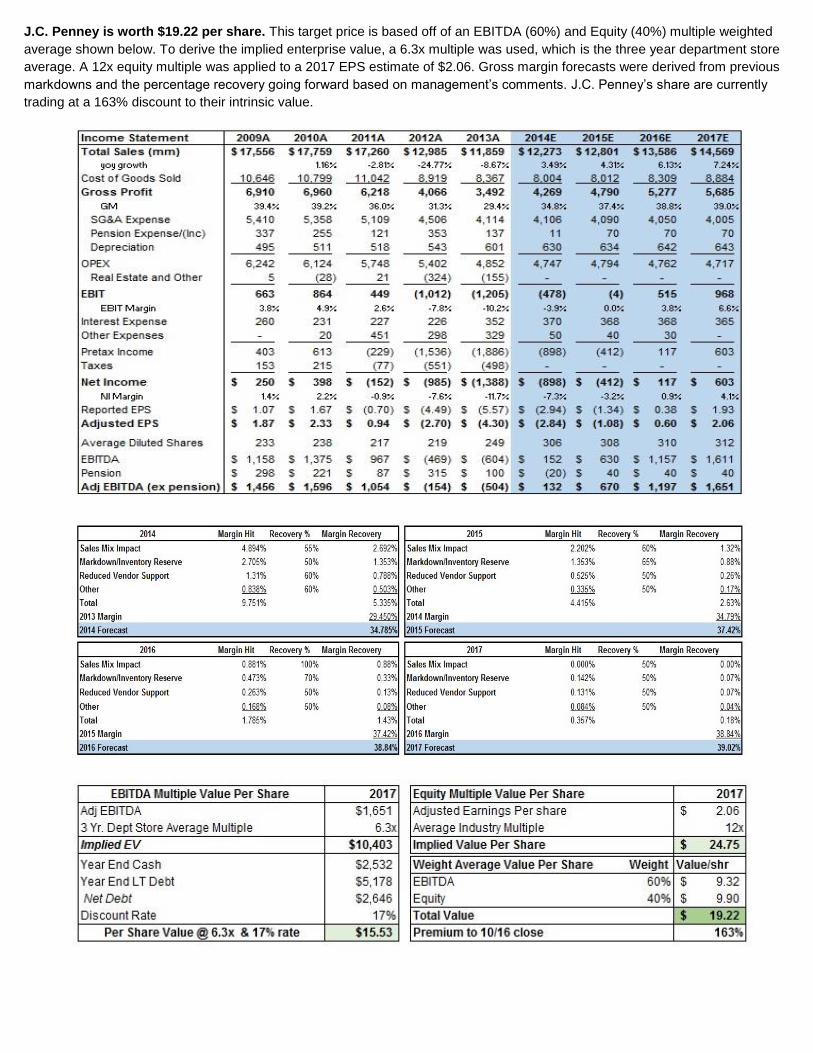

J.C. Penney is worth $19.22 per share. This target price is based off of an EBITDA (60%) and Equity (40%) multiple weighted

average shown below. To derive the implied enterprise value, a 6.3x multiple was used, which is the three year department store

average. A 12x equity multiple was applied to a 2017 EPS estimate of $2.06. Gross margin forecasts were derived from previous

markdowns and the percentage recovery going forward based on management’s comments. J.C. Penney’s share are currently

trading at a 163% discount to their intrinsic value.

Given the current share discount, I would begin to build a position in J.C. Penney. The shares are down roughly 35% from

their September high. Technically, the next level of support is around $6.50 and then sub $6. I personally do not believe they will

trade sub $6 now that bankruptcy is off the table. If JCP averages a 3% SSS gain through 2017 the shares are worth $7.07, or

roughly a 3% discount to where they are currently trading ($7.30). This puts a floor in from a valuation standpoint, as I have full

confidence in JCP comping 3% per year. However, continued market jitters and volatility could push shares down further. I would

be buying all the way down should the opportunity arise.