jnj pitch

TRANSCRIPT

JOHNSON & JOHNSON : JNJ March 5 , 2015

KELVIN LI BCOMM. 17

AGENDA

CONTENT SLIDE

INDUSTRY OUTLOOK 3

COMPANY OVERVIEW 4

INVESTMENT RATIONALE 5-7

CATALYSTS 8

RISKS 9

VALUATION 10-14

TARGET PRICE 15

INDUSTRY OVERVIEW

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview

• 6.5% annual growth rate will occur within the next 5 years. The past 5 year growth rate was 3.5%.

• 22% of revenues generated in Anastasia and Respiratory, another 22% in Irradiation Services

• JNJ having 7.1% market share of this specific sector

• US residents aged 65 and over will be the largest target market within the sector, growing at an annualized rate of 3.6%

• R&D spending and increasing technology bolster growth

SOURCE: IBIS WORLD 3

US MEDICAL DEVICES INDUSTRY OUTLOOK GLOBAL PHARMACEUTICAL OUTLOOK • Pharmaceutical manufacturers will exhibit growth over the next five

years, driven by the growing middle class enabling more individuals to afford pharmaceuticals.

• 3.7% forecasted annual growth rate

• larger players will likely pursue low-risk strategies, such as acquiring small companies that have developed commercial-ready technologies. ex. neurology and cardiology.

• the industry is primarily growing by cutting costs, developing strategies for more efficient R&D methods and completing mergers and acquisitions (M&As).

• 2012 and 2011 patent cliff have caused R&D expenditures to be constrained in 2014 due to increasing number of competitors.

COMPANY OVERVIEW BUSINESS OVERVIEW

DIVERSE PRODUCT PIPELINE

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview

• J&J is the world's comprehensive manufacturer of health care products, as well as a provider of related services, for the consumer, pharmaceutical, and medical devices market. together with its subsidiaries, researches and develops, manufactures, and sells various products in the health care field worldwide

MANAGEMENT TEAM

Alex Gorsky (CEO)

Sandra Peterson Group Worldwide

Chairman

Dominic Caruso (CFO)

Former worldwide chairman of medical

devices and diagnostic group

Oversees JNJ supply chain, Former CEO of Bayer

Medical Care

Former VP of Finance at Centecor

4

REVENUE BY GEOGRAPHIC SEGMENT

45%

26%

19%

10% USA

Europe

Asia- Pacific

Other

Strong domestic presence in the United States/ Brand Recognition

Market Cap: $283B Last Trading Price: $102.52 Beta: 0.57

INVESTMENT RATIONALE I

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 5

CONSISTENT CURRENT RATIO REDUCES RISK

2010 2011 2012 2013 2014 2015

Current Ratio 1.8x 2.1x 2.4x 1.9x 2.2x 2.4x

R² = 0.37136

0.0x 0.5x 1.0x 1.5x

2.0x 2.5x 3.0x

CURRENT RATIO PAST 5 YEARS

• JNJ’s current ratio remains consistent throughout the past 5 years. This highlights its ability to pay down debt if needed to be liquidated. Their ratios have held at a healthy mean of 2.1, demonstrating the company’s financial health. This number is not too high and also not too low.

• This gives JNJ minimal risk when considering further pharmaceutical projects.

2010 2011 2012 2013 2014 2015

Total Debt/Equity 28.7% 29.6% 35.4% 24.9% 24.5% 26.9%

R² = 0.21869

0.0%

10.0%

20.0%

30.0%

40.0%

DEBT/EQUITY % PAST 5 YEARS

DEBT LEVELS LOW: POSITIONED FOR GROWTH

• Financing through equity is important as banks prefer not to lend to high risk projects. Though JNJ’s size is large, its debt levels remain at a low level with minimal movement in the past 5 years. This demonstrates professional long term solvency and minimal risk moving forward.

SOURCE: CAPITAL IQ

INVESTMENT RATIONALE II

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 6

CONSISTENT R&D GROWTH SIGNALS INNOVATION MANY PHASE 3 STAGED DRUGS SIGNAL REVENUE INCREASE

SOURCE: CAPITAL IQ

2010 2011 2012 2013 2014 2015

R & D Exp. 6,986. 6,844. 7,548. 7,665. 8,183. 8,494.

R² = 0.93055

0

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0 R&D EXP.

• To produce pharmaceutical drugs and medical devices, R&D growth is vital. JNJ has consistently increased their R&D expenses historically. A five year growth rate of 20% has been achieved.

• Roughly 11% of revenue is spent on R&D expenditure, this ratio has also remained constant over the past 5 years. JNJ definitely has room to increase their R&D even more rapidly in the coming years

• There is roughly a 6% chance of a preclinical drug to reach phase 3 of the stage. With 39 preclinical drugs, one would expect only 2 phase 3 drugs to be reached. Currently 9 are present therefore demonstrating JNJ’s ability to have a high success rate with regards to FDA approval.

• There is a 64% chance of phase 3 drugs reaching the market, therefore we can expect roughly 6 new drugs to generate revenue in the coming few years.

INVESTMENT RATIONALE III

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 7

JNJ IS IN A POSITION FOR A LARGE ACQUISITION

SOURCE: CAPITAL IQ

• With the last large acquisition occurring on June 2012, JNJ is due to acquire another company. The past acquisition was a 21 billion dollars purchase of Synthes Inc.

• JNJ has consistently increased their free cash flow within the past 5 years, which can be used to subsidize an acquisition. Also with such a diverse product portfolio (493 to be exact), it isn’t surprising that JNJ is eager to add another company to it.

2010 2011 2012 2013 2014 2015

Levered Free Cash Flow 10,985.1 11,723.0 8,971.1 12,383.1 11,909.4 15,453.5

R² = 0.4434

0 2,000.0 4,000.0 6,000.0 8,000.0

10,000.0 12,000.0 14,000.0 16,000.0 18,000.0

LEVERED FREE CASH FLOW

CATALYSTS

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 8 SOURCE: SEEKING ALPHA

ABBVIE PURCHASING PHARMACYCLICS

• This 21 billion dollar deal allows synergies to occur within the two companies.

• Imbruvica is a drug sold by Pharmacyclics and is used to treat

Leukemia. Johnson and Johnson is a partner with Pharmacyclics with regards to this drug.

• Sales around 500 million with projected end of year sales of 1

billion dollars – 5 billion post acquisition statement.

• Though JNJ did not acquire Pharmacyclics as people claimed they would this past week, they still benefit from this deal.

• Cordis, owned by JNJ makes cardiology and endovascular devices • a divestiture would be in-line with management’s efforts to prioritize

its medical device business and focus on faster growth assets where J&J has strong competitive positioning

CARDINAL HEALTH BUYS CORDIS FROM JNJ

RISKS

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 9

COMPETITIVE PRESSURES RAPID TECHNOLOGICAL CHANGES

UNCERTAIN R&D OUTCOMES

• The development of new products increase the competitive environment for JNJ. Patents expiring for generic drugs allow competition to enter the market and produce the same product, forcing JNJ to compete on a basis of cost.

• Adverse or inconclusive results have the potential to delay the development of a product in testing. Uncertainty is always a common theme therefore any products in the pipeline are under risk of default. Profitability is always in danger even with JNJ’s high success rate.

• The medical device sector consistently requires technological updates. With a large segment of JNJ’s revenue coming from medical devices, there is a large amount of pressure to continuously update the company’s technology. Profits may weaken if new devices are not accepted in to the market as well as the research says it will.

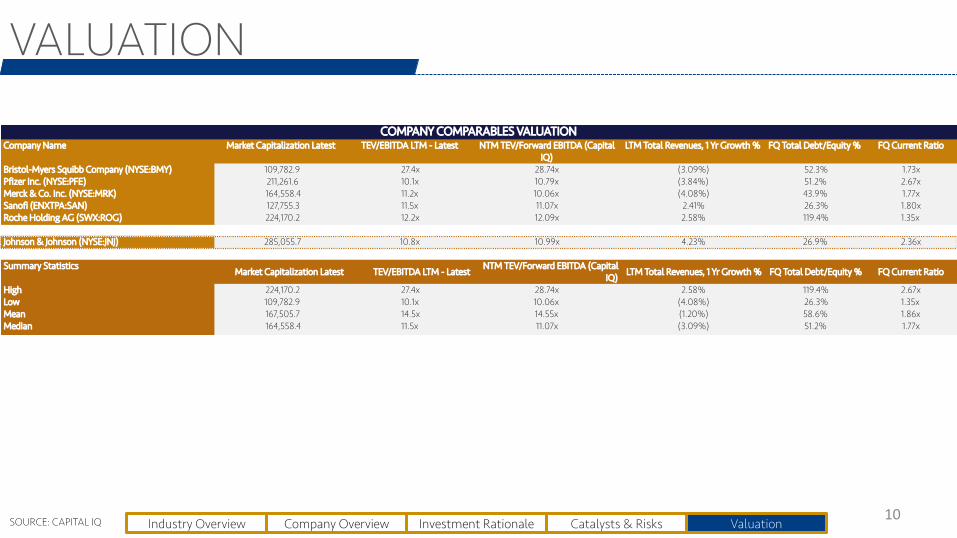

VALUATION

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 10 SOURCE: CAPITAL IQ

Company Name Market Capitalization Latest TEV/EBITDA LTM - Latest NTM TEV/Forward EBITDA (Capital IQ)

LTM Total Revenues, 1 Yr Growth % FQ Total Debt/Equity % FQ Current Ratio

Bristol-Myers Squibb Company (NYSE:BMY) 109,782.9 27.4x 28.74x (3.09%) 52.3% 1.73xPfizer Inc. (NYSE:PFE) 211,261.6 10.1x 10.79x (3.84%) 51.2% 2.67xMerck & Co. Inc. (NYSE:MRK) 164,558.4 11.2x 10.06x (4.08%) 43.9% 1.77xSanofi (ENXTPA:SAN) 127,755.3 11.5x 11.07x 2.41% 26.3% 1.80xRoche Holding AG (SWX:ROG) 224,170.2 12.2x 12.09x 2.58% 119.4% 1.35x

Johnson & Johnson (NYSE:JNJ) 285,055.7 10.8x 10.99x 4.23% 26.9% 2.36x

Summary StatisticsMarket Capitalization Latest TEV/EBITDA LTM - Latest

NTM TEV/Forward EBITDA (Capital IQ)

LTM Total Revenues, 1 Yr Growth % FQ Total Debt/Equity % FQ Current Ratio

High 224,170.2 27.4x 28.74x 2.58% 119.4% 2.67xLow 109,782.9 10.1x 10.06x (4.08%) 26.3% 1.35xMean 167,505.7 14.5x 14.55x (1.20%) 58.6% 1.86xMedian 164,558.4 11.5x 11.07x (3.09%) 51.2% 1.77x

COMPANY COMPARABLES VALUATION

VALUATION

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 11 SOURCE: CAPITAL IQ

DISCOUNTED CASH FLOW VALUATIONYEAR ENDING DEC 31

Revenue:Revenue Growth

COGSCOGS Growth

SG&ASG&A Growth

R&DR&D Growth

Amortization of Goodwill/IntangiblesEBIT Margin

EBITEBITDA

Less: Provision for TaxesUnlevered Net Income

Plus: D&A (excl. non-deductible GW amort.)Less: Capital ExpendituresLess: Increase in Net Working Capital

Unlevered Free Cash Flow

D&A % of SalesCapex % of SalesNWC Growth

COGSSG&AR&DTax Rate

DISCOUNTED CASH FLOW VALUATIONYEAR ENDING DEC 31 EBITDA Multiples Method

2012A 2013P 2014P 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 67,224.0 71,312.0 74,331.0 74,331.0 $76,375.1 $78,284.5 $80,045.9 $81,646.8 $83,075.6 $84,321.8 $85,375.8 $86,229.5 $86,876.3

3.4% 6.1% 4.2% 3.0% 2.8% 2.5% 2.3% 2.0% 1.8% 1.5% 1.3% 1.0% 0.8%

$21,313.0 $22,242.0 $22,746.0 $23,165.3 $23,802.3 $24,397.4 $24,946.3 $25,445.3 $25,890.5 $26,278.9 $26,607.4 $26,873.5 $27,075.05.1% 4.4% 2.3%

$20,869.0 $21,830.0 $21,954.0 $22,594.5 $23,215.8 $23,796.2 $24,331.6 $24,818.3 $25,252.6 $25,631.4 $25,951.8 $26,211.3 $26,407.9-0.4% 4.6% 0.6%

$7,665.0 $8,183.0 $8,494.0 $8,499.6 $8,733.3 $8,951.7 $9,153.1 $9,336.1 $9,499.5 $9,642.0 $9,762.5 $9,860.2 $9,934.11.5% 6.8% 3.8%

$1,146.0 $1,363.0 $1,398.0 $1,302.3 $1,380.5 $1,350.2 $1,341.4 $1,344.3 $1,357.4 $1,345.3 $1,347.7 $1,349.0 $1,350.125.8% 26.7% 28.4% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0% 27.0%

$17,377.0 $19,057.0 $21,137.0 $20,071.6 $20,623.6 $21,139.2 $21,614.8 $22,047.1 $22,432.9 $22,769.4 $23,054.1 $23,284.6 $23,459.2$19,897.0 $21,798.0 $23,634.0 $22,785.1 $23,411.7 $23,997.0 $24,536.9 $25,027.7 $25,465.7 $25,847.6 $26,170.7 $26,432.4 $26,630.7

(4,344.3) (4,764.3) (5,284.3) (5,017.9) (5,155.9) (5,284.8) (5,403.7) (5,511.8) (5,608.2) (5,692.4) (5,763.5) (5,821.1) (5,864.8)$21,721.3 $23,821.3 $26,421.3 $25,089.5 $25,779.5 $26,424.0 $27,018.5 $27,558.9 $28,041.2 $28,461.8 $28,817.6 $29,105.7 $29,324.0

2,520.0 2,741.0 2,497.0 2,713.5 2,788.1 2,857.8 2,922.1 2,980.6 3,032.7 3,078.2 3,116.7 3,147.8 3,171.5(2,934.0) (3,595.0) (3,714.0) (3,568.5) (3,666.6) (3,758.3) (3,842.8) (3,919.7) (3,988.3) (4,048.1) (4,098.7) (4,139.7) (4,170.7)

(461.0) 937.0 1,603.0 690.0 709.0 726.7 743.0 757.9 771.1 782.7 792.5 800.4 806.4$20,846.3 $23,904.3 $26,807.3 $14,888.7 $15,298.2 $15,680.6 $16,033.4 $16,354.1 $16,640.3 $16,889.9 $17,101.0 $17,272.0 $17,401.6

3.7% 3.8% 3.4% 3.7% 3.7% 3.7% 3.7% 3.7% 3.7% 3.7% 3.7% 3.7% 3.7%-4.4% -5.0% -5.0% -4.8% -4.8% -4.8% -4.8% -4.8% -4.8% -4.8% -4.8% -4.8% -4.8%-0.7% 1.3% 2.2% 0.9% 0.9% 0.9% 0.9% 0.9% 0.9% 0.9% 0.9% 0.9% 0.9%

32% 31% 31% 31.2% 31.2% 31.2% 31.2% 31.2% 31.2% 31.2% 31.2% 31.2% 31.2%31% 31% 30% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4%11% 11% 11% 11.4% 11.4% 11.4% 11.4% 11.4% 11.4% 11.4% 11.4% 11.4% 11.4%

25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0% 25.0%

VALUATION

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 12 SOURCE: CAPITAL IQ

EBITDA Multiples MethodWACC 5.6%

Multiples MethodExit Multiple 14.0 x2024E EBITDA $26,630.7Terminal Value $372,829.63

Total Enterprise Value $338,595.3Debt $15,122.0Cash 14523Minority Interest 0

Share PriceTotal Equity Value $337,996.3Shares Outstanding 2780.5

Fair Value Per Share $121.56Current Price $102.52Implied Upside 19%

Perpetuity Growth MethodWACC 5.6%

Enterprise ValuePerpetuity Growth Rate 1.0%2017E UFCF $17,401.6Terminal Value $384,110.95

Total Enterprise Value $345,152.5

Debt 15122Cash 14523Minority Interest 0Total Equity Value $344,553.5

Shares Outstanding 2780.5

Fair Value Per Share $123.92Current Price $102.52Implied Upside 21%

Rf 0.0212ErP 0.09Beta 0.57

Rs 6%

CAPM

Weighting Cost W * C

Equity 78.8% 6.0% 4.8%Debt Cost (1 - T) 21.2% 5.1% 0.8%Preferred Equity 0.0% 0.0% 0.0%WACC 5.6%

VALUATION

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 13 SOURCE: CAPITAL IQ

Multiples MethodEnterprise Value

Exit Multiple12.0 x 13.0 x 14.0 x 15.0 x 16.0 x

6.5% $286,766.54 $300,953.40 $315,140.26 $329,327.12 $343,513.997.0% $276,221.34 $289,759.04 $303,296.73 $316,834.42 $330,372.117.5% $266,163.56 $279,084.61 $292,005.66 $304,926.71 $317,847.75

8.0% $256,567.75 $268,902.91 $281,238.07 $293,573.24 $305,908.408.5% $247,409.93 $259,188.29 $270,966.66 $282,745.02 $294,523.39

Share PriceExit Multiple

12.0 x 13.0 x 14.0 x 15.0 x 16.0 x6.5% 102.92 108.02 113.12 118.23 123.337.0% 99.13 104.00 108.86 113.73 118.607.5% 95.51 100.16 104.80 109.45 114.10

8.0% 92.06 96.49 100.93 105.37 109.808.5% 88.76 93.00 97.24 101.47 105.71

Dis

coun

t Ra

te

(WA

CC)

Dis

coun

t Ra

te

(WA

CC)

Gordon Growth MethodEnterprise Value

Terminal Growth Rate0.5% 0.8% 1.0% 1.3% 1.5%

6.5% $271,801.31 $278,955.54 $286,760.16 $295,308.07 $304,710.787.0% $250,543.06 $256,367.86 $262,678.07 $269,536.99 $277,019.447.5% $232,330.36 $237,132.67 $242,304.40 $247,889.86 $253,940.78

8.0% $216,553.81 $220,556.17 $224,844.40 $229,450.29 $234,410.478.5% $202,756.39 $206,123.59 $209,715.27 $213,554.66 $217,668.29

Share PriceTerminal Growth Rate

0.5% 0.8% 1.0% 1.3% 1.5%6.5% $97.54 $100.11 $102.92 $105.99 $109.377.0% $89.89 $91.99 $94.26 $96.72 $99.417.5% $83.34 $85.07 $86.93 $88.94 $91.11

8.0% $77.67 $79.11 $80.65 $82.30 $84.098.5% $72.70 $73.92 $75.21 $76.59 $78.07

Dis

coun

t Ra

te

(WA

CC)

Dis

coun

t Ra

te

(WA

CC)

VALUATION

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 14 SOURCE: CAPITAL IQ

88.76

72.70

90.86

79.80

88.61

89.78

92.27

96.01

123.33

109.37

218.31

309.51

253.94

242.78

192.50

181.54

0.00 100.00 200.00 300.00 400.00 500.00 600.00 700.00

DCF Multiples Method (12x-16x)

DCF GGM (0.5%-1.5%)

DCF MODEL

P/E FY1

LTM P/E

FY1 EV/EBITDA

LTM EV/EBITDA

FY1 EV/Revenue

LTM EV/Revenue

Company Comparables

FOOTBALL FIELD VALUATION

$145.74

TARGET PRICE RETURNS

Valuation Catalysts & Risks Investment Rationale Company Overview Industry Overview 15 SOURCE: CAPITAL IQ

Price March 5, 2015: $102.52 Capital Gains 42%

Dividend Yield 2.73% Total Implied Return 44.73%

Target Price $145.74

THANK YOU

16