joe burgoyne director, options industry council options ... · stock and options transactions and...

TRANSCRIPT

1

Joe Burgoyne Director, Options Industry Council

www.OptionsEducation.org

Options Strategies for Big Stock Moves

2

Options involve risks and are not suitable for everyone. Individuals should not enter into options transactions until they have read and understood the risk disclosure document, Characteristics and Risks of Standardized Options, available by visiting OptionsEducation.org. To obtain a copy, contact your broker or The Options Industry Council at 125 S. Franklin St., Suite 1200, Chicago, IL 60606. In order to simplify the computations used in the examples in these materials, commissions, fees, margin, interest and taxes have not been included. These costs will impact the outcome of any stock and options transactions and must be considered prior to entering into any transactions. Investors should consult their tax advisor about any potential tax consequences. Any strategies discussed, including examples using actual securities and price data, are strictly for illustrative and educational purposes and should not be construed as an endorsement, recommendation, or solicitation to buy or sell securities. Past performance is not a guarantee of future results. Copyright © 2018. The Options Industry Council. All rights reserved.

Disclaimer

3

About OIC:

• FREE unbiased and professional options education

• OptionsEducation.org • Online courses, podcasts,

videos, & webinars • Investor Services desk at

4 U.S. Listed Options Exchanges

5 Annual Options Volume 1973-2017

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Cle

ared

Con

tract

s (B

illion

s)

OCC Annual Contract Volume by Contract Type

Equity Non-Equity

6 Presentation Outline

Delta Risks:

Vertical Spreads

Volatility Risks:

Strangle

Q&A

Considering Different Strategies

7

Joe Burgoyne Director, Options Industry Council

www.OptionsEducation.org

The Right Strategy is Key

8 Two Key Questions

Motivation? • Income • Risk Protection • Stock Acquisition

Outlook? • Bullish/Bearish/Neutral • Increase/Decrease in

Implied Volatility • Short/Long-term • Event Horizon

9

Joe Burgoyne Director, Options Industry Council

www.OptionsEducation.org

Vertical Spreads

10 A Spread Transaction

A spread involves two or more positions:

Buy or sell one option and buy or sell an option, stock or other product

• Usually the same underlying • Usually the same expiration dates

• Usually different strike prices

Different types of spreads: • Vertical Spreads • Horizontal (Time) Spreads • Diagonal Spreads

11 Vertical Spreads

Buy one option and sell another option

• Same underlying • Same expiration dates • Different strike prices

12 Two Types of Vertical Spreads

• Debit Spread (calls & puts) • You pay to initiate the position

• Credit Spread (calls & puts)

• You receive cash (or a credit) to initiate the position

• Defined risk in both spreads

13

Nov Calls

85 90

Jan Calls

80 90

Long Vertical Spreads • All calls or all puts • Same expiration • Different strikes

Nov 85/90 call spread

Jan 80/90 call spread

• Also known as bull call spread • Long leg has lower strike (more expensive) than short leg • Seeking price appreciation • Maximum value = difference in strikes • Maximum risk = debit paid for spread

Spread Basics Vertical

14 Bull Call Spread Example

XYZ @ $90 28 Days to Expiration

• Buy 1 28-day 90 Call $ 2.05 • Sell 1 28-day 95 Call $ 0.70 Net Debit $ 1.35

This is a Bull Call spread

Excludes transaction costs

15 Bull Call Spread Example

XYZ @ $90 28 Days to Expiration Buy the 90 – 95 bull call spread for $1.35

Excludes transaction costs

Breakeven:

Margin:

Maximum Risk:

Maximum Gain: $3.65

$1.35

$1.35*

$91.35

*MINIMUM margin requirement

16 Bull Call Spread Example

Buy a lower strike call and sell a higher strike call • Buy 1 90 Call $2.05 • Sell 1 95 Call $0.70 Net Debit $1.35

95 90 85 100

Max. Profit $3.65

Max. Loss $1.35

B/E: $91.35

Excludes transaction costs

17 Bear Put Spread Example

XYZ @ $88.50 28 Days to Expiration

• Buy 1 28-day 90 put $ 3.50 • Sell 1 28-day 85 put $ 1.80 Net Debit $ 1.70

This is a Bear Put spread

Excludes transaction costs

18 Bear Put Spread Example

XYZ @ $88.50 28 Days to Expiration Buy the 90 – 85 bear put spread for $1.70

Excludes transaction costs

Breakeven:

Margin:

Maximum Risk:

Maximum Gain: $3.30

$1.70

$1.70*

$88.30

*MINIMUM margin requirement.

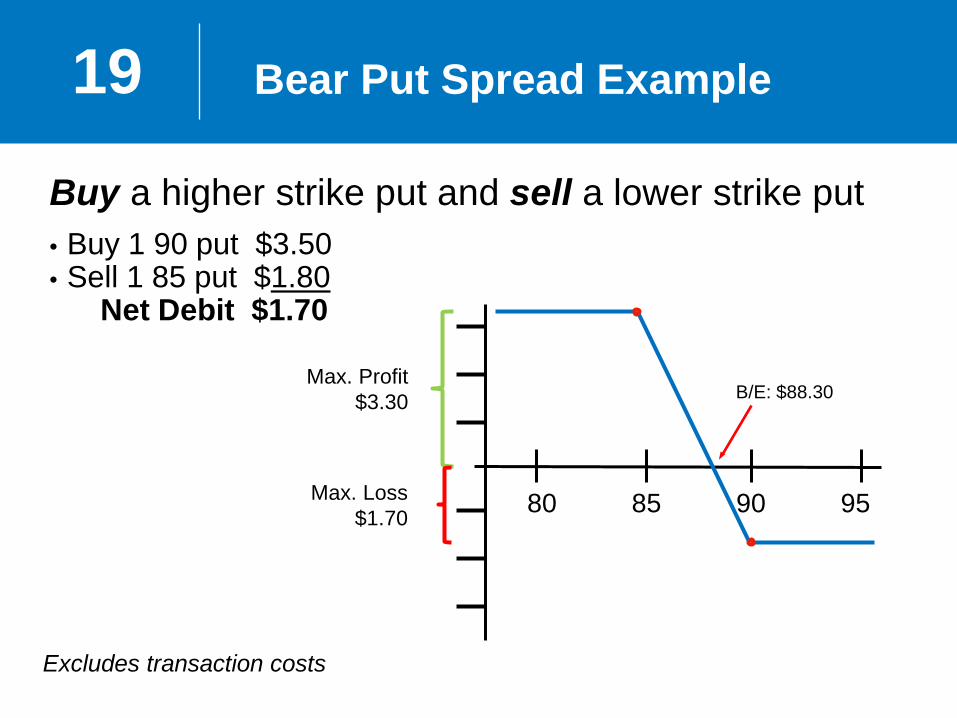

19 Bear Put Spread Example

Buy a higher strike put and sell a lower strike put • Buy 1 90 put $3.50 • Sell 1 85 put $1.80 Net Debit $1.70

90 85 80 95

Max. Profit $3.30

Max. Loss $1.70

B/E: $88.30

Excludes transaction costs

20 Call Credit Spread Example

XYZ @ $88.50 28 Days to Expiration

• Sell 1 28-day 90 Call $ 3.50 • Buy 1 28-day 95 Call $ 1.80 Net Credit $ 1.70

This is a bearish call spread

21 Call Credit Spread Example

XYZ @ $88.50 28 Days to Expiration Sell the 90 – 95 call credit spread at $1.70

What is this spread worth with XYZ at $88.50 in 21 days? In 7 days?

Excludes transaction costs

Breakeven:

Margin:

Maximum Risk:

Maximum Gain: $1.70

$3.30

$3.30

$91.70

22 Call Credit Spread Example

Sell a lower strike call and buy a higher strike call • Sell 1 90 Call $3.50 • Buy 1 95 Call $1.80 Net Credit $1.70

95 90 85 100

Max. Profit $1.70

Max. Loss $3.30

B/E: $91.70

23 What Happens at Expiration?

95 90 85 100

Stock is < or = $90?

Both options expire worthless Maximum profit of $1.70 achieved No stock position

Sell 1 90 Call $3.50 Buy 1 95 Call $1.80 Net Credit $1.70

24 What Happens at Expiration?

95 90 85 100

Stock is > or = $95?

Maximum loss = difference in strikes ($5) less premium received ($1.70) = $3.30 Short call is assigned, long call is exercised No stock position

Sell 1 90 Call $3.50 Buy 1 95 Call $1.80 Net Credit $1.70

25 What Happens at Expiration?

95 90 85 100

Stock is > $90 and < 95?

Short call is assigned = short stock Margin required Long call expires out of the money/worthless

Sell 1 90 Call $3.50 Buy 1 95 Call $1.80 Net Credit $1.70

26 Put Credit Spread Example

XYZ @ $88.50 28 Days to Expiration

• Sell 1 28-day 85 Put $ 2.05 • Buy 1 28-day 80 Put $ 0.70 Net Credit $ 1.35

This is a bullish put spread

27 Put Credit Spread Example

XYZ @ $88.50 28 Days to Expiration Sell the 85 – 80 put credit spread at $1.35

What is this spread worth with XYZ at $88.50 in 21 days? In 7 days?

Excludes transaction costs

Breakeven:

Margin:

Maximum Risk:

Maximum Gain: $1.35

$3.65

$3.65

$83.65

28 Put Credit Spread Example

Sell a higher strike put and buy a lower strike put • Sell 1 85 Put $2.05 • Buy 1 80 Put $0.70 Net Credit $1.35

85 80 75 90

Max. Profit $1.35

Max. Loss $3.65

B/E: $83.65

29 What Happens at Expiration?

85 80 75 90

Stock > or = $85?

Both options expire worthless Maximum profit of $1.35 achieved No stock position

Sell 1 85 Put $2.05 Buy 1 80 Put $0.70 Net Credit $1.35

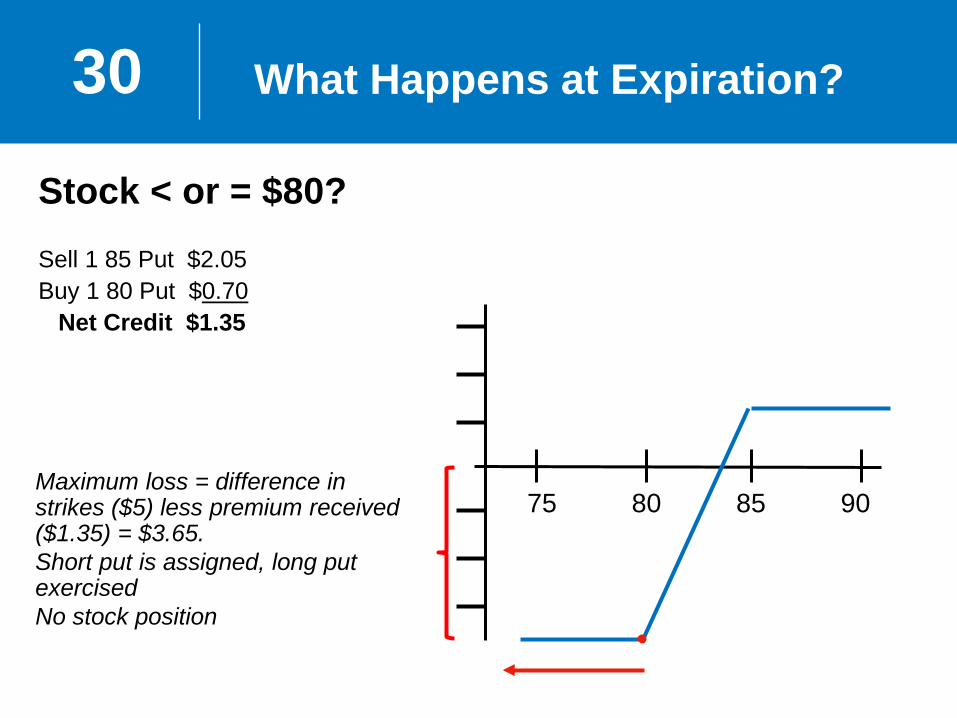

30 What Happens at Expiration?

85 80 75 90

Stock < or = $80?

Maximum loss = difference in strikes ($5) less premium received ($1.35) = $3.65. Short put is assigned, long put exercised No stock position

Sell 1 85 Put $2.05 Buy 1 80 Put $0.70 Net Credit $1.35

31 What Happens at Expiration?

85 80 75 90

Stock > $80 and < $85?

Stock price between strikes at expiration: Short put is assigned = long stock Long put expires out of the money/worthless

Sell 1 85 Put $2.05 Buy 1 80 Put $0.70 Net Credit $1.35

32 Long Straddle Example

• Buy 1 87.50 Call $2.15 • Buy 1 87.50 Put $1.85 Net Debit $4.00

90 85 80 95 Max. Loss

$4.00 B/E: $83.50 B/E: $91.50

Unlimited upside potential

Current share price of $87.50

Excludes transaction costs

33 Strategies: Strangles

Investor motivation:

• Same as the straddle, but with typically out-of-the money calls & puts, the investor has a wider opportunity to be “right” (long strangle) or “wrong” (short strangle)

• Typically lower risk (and lower reward) than the straddle

34 Strategies: Strangles

Long Strangle: • Buy call + buy put of different strike & same expiry

Short Strangle: • Sell call + sell put of different strike & same expiry

Buy 1 Dec 90 Call $ 2.15 + Buy 1 Dec 85 Put $ 1.85 Net Debit $ 4.00

Sell 1 Dec 90 Call $ 2.15 + Sell 1 Dec 85 Put $ 1.85 Net Credit $ 4.00

35 Long Strangle Example

XYZ @ $87.50 45 Days to Expiration

Excludes transaction costs

Breakeven: Margin: Maximum Risk:

Maximum Gain: Unlimited $2.50 (100% of investment) $2.50 $82.50 and $92.50

Buy 1 45-day 90.00 Call $ 1.20 Buy 1 45-day 85.00 Put $ 1.30 Net Debit $ 2.50

36 Long Strangle Example

90 85 80 95 Max. Loss

$2.50 B/E: $82.50 B/E: $92.50

Unlimited upside potential

Buy 1 45-day 90.00 Call $ 1.20 Buy 1 45-day 85.00 Put $ 1.30 Net Debit $2.50

Current share price of $87.50

Excludes transaction costs

37 Straddles versus Strangles

• Straddles: • Higher cost and lower leverage • Break-even points closer together

• Strangles: • Lower cost and higher leverage • Break-even points farther apart

• Both: time decay is painful and need big stock move

38 Things to Know:

• Historic Vol: Where the stock has been

• Implied Vol: Where the market thinks the stock is going based on the options price

• Long straddle/strangle: takes advantage of low IV and sharp stock price moves

39 The Options Education Program

• MyPath assessment--learn at your own pace online and customize your curriculum for your skill level.

Whether you’re an options novice or just deployed an iron condor, the Options Education Program has you covered.

• Download our podcasts and videos.

• Attend webinars and learn from the pros.

• Live options help from industry professionals at Investor Services.

• OptionsEducation.org

40

More Information www.OptionsEducation.org

Investor Services:

OIC YouTube Channel

Follow us on Twitter @Options_Edu!

For More Information