joint venture analysis - entering into the chinese market

TRANSCRIPT

CARLTON & UNITED BREWERIES PTY LTD

PROJECT CHINA PROPOSAL 2015

IBUS 90002 ASIAN BUSINESS AND MANAGEMENT MELBOURNE BUSINESS SCHOOL SEMESTER ONE, 2015

ROBERT AU (329510) JAMES ANAGNOSTIDIS (319316) CHRISTIAN ANDERSEN (733691) LIEN NGUYEN (736333) DAVID NICHOLLS (390074)

Table of Contents

05 Executive Summary (From the Director)

06 About the Company

07 Financial Performance

10 Key Success Factors

12 Subregional Analysis

13 Entry Mode Analysis

16 Discussion

18 Proposed Strategy

21 Implementation Timeline

24 Reference

27 Appendices

FROM THE DIRECTORCarlton & United Breweries (CUB) is a subsidiary of SABMiller PLC, operating in Australia. Our portfolio comprises of iconic brands such as Carlton Draught, Foster’s and Crown Lager. We believe that timing is optimal for us to engage international expansion, setting our sights upon the Chinese market.

This report provides an analysis and evaluation of the proPitability of prospective opportunities for the international expansion of Carlton & United Breweries into China.

Factors deemed most responsible for the success of our expansion include creation of a strong brand identity through existing marketing channels, as well as continued growth in GDP per capita and increased disposable income, leading to increased consumer spending. Capitalising on existing distribution networks of a partner is vital in a market where distributors and suppliers have high bargaining power. Furthermore, three signiPicant decision factors were analysed in the proposed expansion into China: the differing levels of protectionist policies at the

local and regional government level; distribution of age groups, particularly those who consume alcohol regularly; and GDP per capita forecasts, using a proxy for determining levels of disposable income growth.

From our evaluation, we recommend the following: establish a strong relationship with a partner, forming a link-‐joint venture with Tsingtao, whose experience in the Chinese market, incorporates a Western Plair; compete in the premium beer market as in response to consumer preferences for foreign products; distribute and promote through our partner’s existing channels; enter swiftly during the upcoming 2016 Shanghai Grand Prix; and Pinally, to investigate the feasibility of foreign direct investment following the establishment of a strong brand identity.

Robert Au | Director, Business Analytics

ABOUT THE COMPANY

6 Project China Proposal

Carlton United Breweries (CUB) dates back to 1854 when our Plagship Australian beer, Victoria Bitter, was Pirst brewed in Melbourne, establishing the Pirst Carlton Brewery. Soon thereafter, and independently, the Foster’s brand was launched in 1888, with William and Ralph Foster brewing Foster’s Lager in Melbourne. It fast became one of Australia’s most iconic and internationally recognised brands. In 1903, the Carlton, Foster’s, Victoria, Shamrock, McCracken and Castlemaine breweries formed a cartel known as the Society of Melbourne Brewers; and merged in 1907 to create Carlton & United Breweries, an entity that transformed itself into Australia’s largest brewing business (Dun and Bradstreet, 2015; Anning, 2015). In 1983, Elders IXL purchased Carlton & United Breweries, renaming it Elders Brewing Group. The company underwent a name change to Foster’s Brewing Group Limited in 1990 to rePlect its most recognised product, before

settling on Foster’s Group Limited in 2001 (Dun and Bradstreet, 2015). In late 2011, SABMiller Beverage Investments Pty Ltd, a wholly-‐owned subsidiary of UK-‐based, SABMiller PLC, executed the buyout of Foster’s Group Limited. It was subsequently removed from the ASX, though trading continued as Carlton & United Breweries (Dun and Bradstreet, 2015). Today, we produce and market alcoholic beverages that services over 7,000 customers across on-‐premise and off-‐premise channels. Our national brewing, logistics and sales network delivers to over 20,000 customers including hotels , c lubs, l iquor stores, restaurants and bars. As a leading beer and cider company, our portfolio comprises of Australia’s most iconic brands, including Victoria Bitter, Carlton Draught, Foster’s and Crown Lager (Dun and Bradstreet, 2015).

2014 HIGHLIGHTS

- 4%Revenue 2014: US$26,311 million 2013: US$23,313 million

+ 1%EBITDA2014: US$6,453 million 2013: US$6,379 million

- 8%Net debt 2014: $US14,303 million 2013: $US15,600 million

- 21%Free cash Glow 2014: US$2,562 million 2013: US$15,600 million

203%Shareholder return Peer median: 105%

+ 3%Adjusted EPS: 2014: 242.0 US cents 2013: 237.2 US cents

+ 3%ProGit before tax 2014: $US4,823 million 2013: $US4,679 million

+ 1%Lager volumes 2014: 245 million hectolitres 2013: 242 million hectolitre

Figure 1: Financial performance highlights (Source: SABMiller, 2014)

Total 1,847 employees

Carlton Draught Victoria Bitter Crown Lager

Foster’s Cascade

Melbourne Bitter Miller Peroni

Pure Blonde Abbotsford

Great Northern Grolsch

Matilda Bay Pilsner Urquell

Strongbow Bulmers Mercury

Dirty Granny Kopparberg

CougarThe Black Douglas

Karloff Vodka Akropolis Oyzo

BEERCIDER SPIRITS

“SABMiller Beverage Investments Pty Ltd produces, distributes and markets alcoholic beverages through our CUB business. Our main focus is beer brewing and distribution, with CUB owning and distributing a number of leading brands from both Australia and around the

world.”Source: Dun and Bradstreet, 2015

Source: SABMiller, 2014

Source: IBISWorld, 2015

2014 REMARKS Our View of the Beer Market -‐ a Growth Opportunity On the local front, forecasted lager volumes were negatively impacted by persistent economic uncertainty and weak consumer sentiment, along with increased competitive intensity, experiencing only 1% growth. A continuing focus on price realisation and effective cost control resulted in EBITA growth (see Figure 1), which we aim to make more efPicient (SABMiller, 2014).

We believe that beer markets around the world can be developed further and are showing an increasing appetite for new beer styles and prices. Additionally, there is still signiPicant opportunities to increase beer consumption in the Asia-‐PaciPic, in particular in that of the Chinese market (see Appendix 1) (SABMiller, 2014).

Per capita, consumption in developing markets is substantially lower than in more mature markets (SABMiller, 2014). As these economies continue to grow, we expect to see a natural increase in momentum of the demand for beer (see Appendix 2). Brewers are continuing to produce a wider range of high quality brands and package formats. In conjunction with greater positioning and marketing strategies, the need to differentiate and diversify within the each category is paramount, as consumer trends are showing support of this evolution. Innovation and category expansion are two ways we can deliver more premium options; the fragmentation of consumer tastes and preferences seen over the past decade has become a dePining feature of the market for alcoholic beverages. This is both broadening the Pield of competition and re-‐igniting consumer interest (SABMiller, 2014). Traditional lagers still dominate the bulk of global industry volume and are continually being bolstered through inventive marketing and packaging strategies. However there is also a Plow of new product development, across different varieties; ranging from richer, more deeply Plavourful beers to sweeter or fruit-‐Plavoured ales, all appealing to more variety-‐seeking adult consumers in varying consumption contexts and with different palates (SABMiller, 2014). Across all beer markets, our interactions with national and local government regulators, supranational bodies and NGOs continue to support responsible consumption efforts. Brewers continue to work in the interests of consumer health and safety and to support the development of local communities and local enterprises up and down the value chain (SABMiller, 2014).

KEY SUCCESS FACTORS

The beer industry in China is a mature yet growing market with several key factors contributing to the success of market entry.

Increasing Brand Awareness

Upon market entry, it is imperative that we establish a foothold in consumers’ minds – by creating a perceived value-‐add in consumption. This is primarily dictated by the method of market entry. In a joint venture, leveraging existing marketing channels is critical for success; whereas being a late mover with direct investment, we would seek to incorporate the proven strategies of those before us whilst still aiming to differentiate (Wei, 2012).

The use of public events (national or international) can also be used to increase our brand awareness. This has been successful in the past with beer sponsorship at the 2008 Beijing Olympics, where all three beer sponsors, Budweiser, Tsingtao and Beijing-‐Yanjing, experiencing growth in market share, as well as Tsingtao’s sponsorship of the Shanghai Expo in 2010 which further grew the company’s market share (Madden, 2008; 2010). These campaign precedents will set the foundations for optimising our company’s strategy, where the focus lies upon understanding, and subsequently capturing, the world’s largest beer consumer market (IBISWorld, 2014).

“Competition is very intense in the distribution sector… products that cannot offer high-value adding services to clients would reduce profitability.” - Li & Fung Research Centre, 2012

Continued Growth in GDP Per Capita

The forecasted growth in GDP per capita (7.1% by 2014, according to the World Bank) will be a contributing factor to the success of the beer industry in China. As disposable income increases, so will consumer conPidence and subsequent consumption (NBSC, 2015). When viewed in conjunction with the increasing demands for consumer goods in the Chinese market, it presents a unique opportunity to capitalise on potentially attractive growth trend (NBSC, 2015).

11 Project China Proposal

Distribution Channels

Competition is extremely intensive in the distribution sector. Existing distributors have high bargaining power, and products that cannot offer value-‐adding services to clients, would have to reduce prices thereby reducing proPitability. Distributors often enjoy exclusive distribution rights which discourage potential market entrants , part icularly those of foreign investments (Li & Fung Research Centre, 2012). This discourages direct investment, though a market entry analysis can highlight approaches to mitigate this risk through strategic entrance methods that can ensure access to distribution networks.

SUBREGIONAL ANALYSISIn this section, we examine key decision factors based on regionality. With numerous regions, each rich and diverse in culture, it becomes necessary to consider what consumer trends have emerged in each respective market. This section therefore aims to provide the essential data and analysis required to determine which regions are most suitable for entry.

Level of Protectionist Policies -‐ Local Government

Each region within China is governed by a set of local policies.

The exac t na ture o f t hese h i gh ly protectionist policies are unknown, as these are not documented, and are more than often implemented in reaction to the entrance of a foreign investor into a region. However, there are certain instances, where policies are implemented to encourage companies to operate in the region, in order to stimulate local growth. These areas allow for ease of consolidation for a company’s operations, though this does not directly correlate to ease of access to local markets. Most of these areas are located along the coastline, with the majority located in Guangdong (Changhui, 2002).

Age Group (20 -‐ 30 years)

IBISWorld (2014) reports that the biggest consumers of beer in

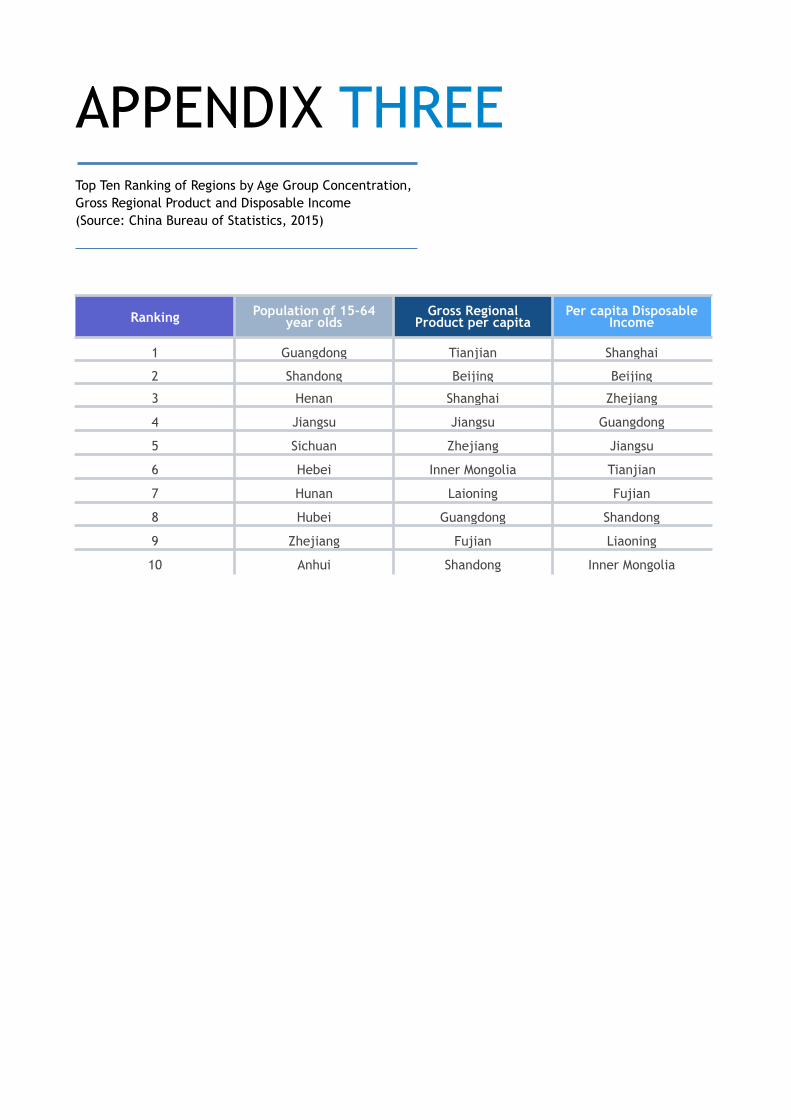

China are those in the 20-‐34 age bracket. The population distribution of ages 15-‐64 across the regions of China are ranked in Appendix 3; current statistics do not provide the exact data for our speciPic age demographic, but can be seen as an accurate representation of the trend of concentration of population by ranking. Regions with the highest concentrations of the target age group are located along the China’s coastlines, where urbanisation rates are also the highest (National Bureau of Statistics of China, 2015).

Per Capita Disposable Income Wealth distribution varies widely across the regions of China (see Appendix 3). The data indicates that coastal city citizens, on average, also have higher levels of

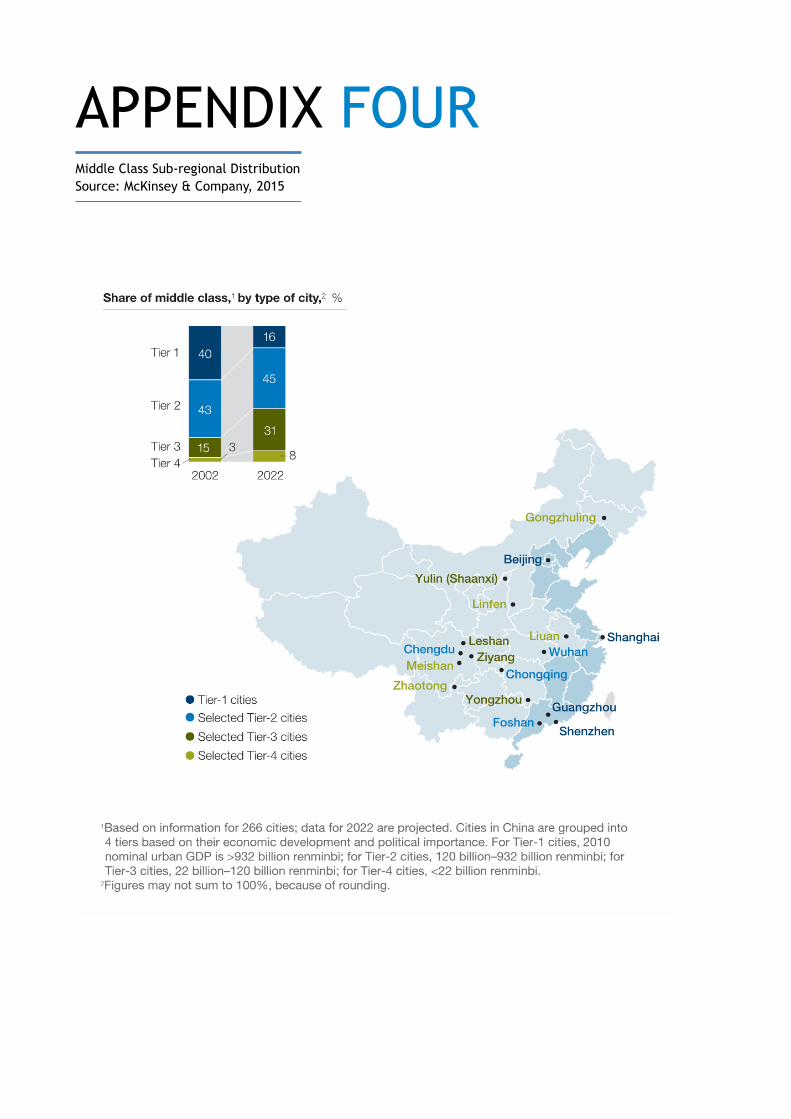

disposable income. These results align to the notion that coastal cities, such as Shanghai, Beijing, Guangzhou and Shenzhen, are known as the “metropolises” of China. However, McKinsey & Company (Barton et. al., 2013) forecasted regional growth trends across China and found that the middle class (those earning 60,000 to 229,000 CNY [AUD$9,000 to AUD$34,000] per year) demographic will spread from predominantly Tier-‐1 cities, characterised by economic development and political importance, to Tier-‐2 and Tier-‐3 cities, which comprise of relatively lower regional GDP (see Appendix 3).

Overall population in Tier-‐1 cities will not markedly decrease, though growth rates will be relatively higher in the lower-‐Tier cities. Trends show that despite the wealth disparity, there are forecasts this it will change in the coming future; and will be a strategic factor in determining company direction (Barton et. al., 2013).

Following analyses of the different regions according to the critical success factors, an overview of the benefits and disadvantages of the different entry modes are presented.

Foreign Direct Investment

Foreign direct investment (FDI) into China, via the opening of a new branch of CUB, will allow us to retain full decision-‐making power, develop our capacity further, maintain intellectual property over our products and operations, as well as providing our company access to all proPits. Although Xi Jingping has stated that he will “...protect the lawful rights and interests of foreign-‐invested companies...” and “...ensure their rights to equal participation in government procurement and independent innovation,” we bear all risks from our direct investment (BBC Business News, 2013). The consequences of this involves signiPicant monetary loss and damage to our brand, wasted time and resources involving the creation of new company tax and legal legislation, foreign exchange risk mitigation, and the forfeiture of any newly developed or purchase infrastructure. As mentioned, there are regions where it would be problematic to enter through FDI, and regions where the policies are more favourable (Carpenter and Dunung, 2015; Delios, Beamish & Lu 2012).

ENTRY MODE ANALYSIS

13 Project China Proposal

Joint Venture A joint venture into the Chinese market will allow us to reach areas of China that we may otherwise be unable to due to the protection by local governments (see Subregional Analysis, p. 12). Through a strategic alliance, we will be seen as a local entity within the Ch ine se marke t and gove rnmen t ; advantageous in to circumventing local policies. Additionally, a joint venture will minimise/remove a potential competitor for the duration of the partnership, assist our company in gaining market traction by using their existing client base as a starting point, as well as established channels of marketing and product distribution. As the two partners are contributing unique sets of resources, a Link-‐Joint venture would be negotiated, where both parties gain -‐ being intellectual property regarding recipes and manufacturing and market and distribution knowledge, respectively.

While these factors drastically reduce our investment risk (when compared to FDI), we must share intellectual property and technologies with a potential future competitor (in the case the JV ends) and may experience communication and integration problems when creating a joint venture between the two companies. Research shows that there are different survival rates linked with different levels of equity sharing and suggests that there is a benePit of handing over 50% of the equity to the local

partner (see Appendix 5). However, even with the equity decided upon, there is still the question of control. The Joint Venture can have dominant, shared or split control. Cultural differences between Western societies and China that may impact our integration strategy include: social and professional practices, gender inclusion, etiquette and language barriers (Carpenter and Dunung, 2011; Cheng and Bowskill, 2015; Delios, Beamish & Lu, 2012; MacLeod, 2015).

Exporting Exporting goods into China is a relatively low Pinancial risk option, It allows us to gauge an initial reaction to our products before embarking on a more penetrating venture. Although agencies exist that assist with marketing, placement and distribution, it does not provide us with much control. Exporting may also require us to modify the packaging or product itself to meet regulatory requirements or the needs of those acting our behalf through contractual agreements which requires research and additional costs. However, policies in China could pose a challenge due to their rigorous protection of local products. Exporting also runs the risk of brand damage as with limited knowledge in the region, our product may not meet these consumer expectations (Carpenter and Dunung, 2011; Delios, Beamish & Lu, 2012).

14 Project China Proposal

Acquisition

Similar to the joint ventures, the acquisition of a Chinese brewer poses many solutions to problems we would have with FDI. The acquirement over of a company will allow us to not only remove a competitor and realise a swift entry into China, but be provided with an established marketing and distribution network and knowledge of the market (with the retention of local employees). We realise the similarity in disadvantages to establishing a JV such as potentially experiencing problems with integration linked to cultural differences, overestimating the synergy achieved. In addition, there are premiums for the acquisition of a company and require the appropriate permits to successfully complete the transaction.

Currently, the Ministry of Commerce of the People retains powers of supervision and approval of foreign investments, but the Nat ional Development and Reform Commission (NDRC) also plays an important role in approving large investment projects, including foreign investment projects as the ex tens ive p roce s s may c l oud t he transparency of the transaction. This may incur high costs, and an acquisition may be in breach of certain laws within these regulatory statutes (Davies, 2013; Delios, Beamish & Lu, 2012).

15 Project China Proposal

DISCUSSION

Timing of Entry

As many joint ventures and FDIs have been attempted in the past decade, we therefore do not have the opportunity to capitalise upon neither majority market share nor Pirst mover advantages.

However, we a re ab le to observe inefPiciencies from other companies and tailor our operational strategies to mitigate against the same failures. Most notably, the high costs associated with research and development that a Pirst mover will experience, would have been previously established from prior competitors, and the opportunity cost can be reallocated towards the research and development of our new products and strategies, effectively strengthening our impact on the Chinese market (Delios, Beamish & Lu, 2012; Mat Isa et. al., 2012).

Culture Distance

Joint ventures and acquisitions are quite often difPicult to manage as a result of the cultural and ethical differences. However, these methods of market entry gives us support from our Chinese partners to assist with local government regulations as well as formalities and political risks.

As a wholly-‐owned enterprise introduced into the Chinese market, we will not experience cultural management and integration issues, though this does expose us to risks regarding lack of knowledge of the market and customary practices. This may lead to loss of sales, brand damage and potential failure of investment.

Advantages and disadvantages of each respective entry mode; measured against the key factors of success.

16 Project China Proposal

Market Barriers

Expansion into a foreign market will come with certain restrictions upon entry. Those speciPic to an international brewing company entering the Chinese market include:

-‐ Local Protectionism This makes acquisition and exporting quite difPicult as regional governments within China are aiming to protect local businesses and provide them a platform to grow, as opposed to allowing foreign competition. Joint ventures are more favorable as we are able to combine and create synergies with a local organisations, thereby bypassing protectionist legislation. Tax adjustments and alterations may cause pressure on prices (17% VAT and 3-‐5% excise), as regulation places increasing restrictions on the availability and marketing of beer anti-‐alcohol advocates erode industry reputation leading to stunted growth and proPitability, even though the awareness surrounding the effects of alcohol is still low in China (IBISWorld, 2014). A strategic alliance will allow for us to have access to the knowledge on how to manage these risks.

-‐ High Competition High competition within the distribution network means only companies who can create value for distributors and pay a premium for their services are able to transport their goods around the country; thereby increasing the price of distribution. The market is also seen as highly competitive as only companies under the protection of the government or those with great economies of scale survive, as they can produce at a lower costs, being able to cut their prices while retaining high levels of proPits (Li & Fung Research Centre, 2012). To minimise risk, joint ventures are preferable to capitalise on these intercontinental and government relationships and to expand operations creating less production costs.

-‐ Low Product Differentiation The Chinese beer market recognises low product differentiation (IBISWorld, 2014). As brewing is a difPicult process to vary from your competitors, it makes market entry challenging however it provides excellent opportunities for SABMiller if the ideas and implementation abilities for a new product line are available.

-‐ High Cost for PPE (Plant, Property and Equipment) Establishing new bricks and mortar through directly venturing into a country can be very expensive and increases the risk of investment (as well as price of failure), particularly with little experience in the area. Joint ventures allow for the sharing and use of previously established PPE and minimises risk upon initial entry.

-‐ Change in Consumer Preferences The beverage and alcohol industry may become more fragmented. Exporting is a less risky option, as we can focus on the product by offering beers that appeal to speciPic local tastes, before attempting a strategic alliance or sole venture into the country. A Joint venture will also allow for testing of the market with minimal risk.

17 Project China Proposal

PROPOSED STRATEGYOur recommendation to the board is that our company establish a strategic and long-‐term commitment to be facilitated by a third party, with established experience and knowledge of the Chinese market. This comprises of a focus on developing synergies and an equity joint venture where we will compete in the premium beer market, as per consumer preferences for foreign, upmarket and exotic products. This joint venture is seen as a more suitable option as the risk is spread between two parties, and depending upon the outcome of strategic negotiations, we recommend that CUB aim to retain control over the entity, due to the a higher success rate seen when at least 50% of the equity of the joint venture entity is owned by the local company (see Appendix 5).

Companies to consider are prominent Chinese brands such as Tsingtao, CR Snow, or a premium, boutique brand. There is a cost-‐benePit trade-‐off between a strategic alliance with smaller brands: our company are ab le to exer t more power in negotiations, whereas an alliance with one of China’s leading companies would allow our brand access to a wider range of available experience and resources.

18 Project China Proposal

Therefore, we suggest that the joint venture is made with Tsingtao. Founded by British and Germans, they have consolidated experience in working with Western brands and cultures, and their distribution networks extend to most of the world (Tsingtao, 2015). In the initial stages, our Chinese partner will initially manage the these established channels.

The choice of region to concentrate on would in the end be made in conjunction with the partnering company. It is shown that the populations with the highest rates of disposable income are located in coastal areas, along with the highest population of the target age group (see Appendix 4). However, in regards to target consumer age brackets, Sichuan ranks in the top 5, as well as being out the cluster of coastal options. We also noted that a cluster of Tier 2-‐4 cities are located in Sichuan, whose populations are steadily climbing. We suggest that distribution be set up here(with the possibility of setting up a production in the future), as intensity of competition would be milder due to minimal existing entries (see Appendix 4).

Additionally, as part of our fully-‐integrated expansion strategy, CUB will also aim to establish a presence in a more mature market, where initial production will be located in Ningbo, in the Zhejiang region. This region was a top contender in each factor of our demographic analyses (see Appendix 3). As Ningbo is a seaport city, transactions and operations between Australia and the Sino-‐Australian joint venture are smoother, with this hub acting as the economic center, thus offering preferential pol ic ies about foreign investments, such as reduced tax for projects with foreign investment exceeding U SD $ 3 0 m i l l i o n ( N F T Z b , 2 0 1 3 ) . Furthermore, Ningbo is only one of Pifteen Fre e Trade Z one s a u t ho r i z ed by government, a factor upon which, as a foreign entity, is something that we must take advantage of (NFTZa, 2013).

“Being founded by British and Germans, [Tsingtao] h a v e c o n s o l i d a t e d experience in working with We s t e r n b r a n d s a n d cultures.”

19 Project China Proposal

“With the Formula One being one of the most prestigious sporting events in the world, attracting 300 millions fans all over China and the globe,this sponsorship deal will be our alliance’s best opportunity to enter the market.”

Moreover, our Chinese partner will initially manage the distribution and promotion of the combined company through their established marketing networks. We will leverage our new partnership and sponsor the upcoming 2016 Chinese Grand Prix in Shanghai. With the Formula One attracting 300 millions fans all over China and the globe (Wu, 2015). Having recently ended their sponsorship agreement with UBS, the Chinese Grand Prix are now looking for new partnerships, and this sponsorship deal will be our alliance’s best opportunity to enter the market, investing mainly in advertising, promotions and athlete endorsements (Wu, 2015).

Finally, we recommend that a team is formed to further research the feasibility of our direct investment into the Chinese market in the long-‐term, once a robust and trustworthy brand identity has been established.

20 Project China Proposal

APRIL 2015CUB & Tsingtao enter agreement to establish a joint venture.

CUB & Tsingtao negotiate terms of arrangement.

OCT 2015

APRIL 2016

MAY 2016

APRIL 2018

SUMMER 2016-18

APRIL 2019

BEYOND 2019

Joint venture commences operations.

Production commences with Tsingtao resources.

Chinese Grand Prix sponsorship campaign.

Commencement of further expansion. Operations will have been established for two years, and joint venture will establish new plants in Ningbo/Sichuan to cater for growth.

Monitor/reassess expansion plan.

Commence takeover. As a foreign partner with local knowledge and experience, we will undertake the acquisition of the joint venture to become a wholly-owned subsidiary.

Step One (April 2015) Our strategic joint venture will be established with a third party, Tsingtao. Together, both parties provide unique skill sets and products to ensure successful integration and synergies imperative for growth; which would not be possible as separate entities.

Step Two (October 2015) Over the following six months, the boards from both the foreign and local parent companies will negotiate the speciPic terms of the agreement.

A transparent and thorough agreement that is consistent with guidelines set by Pinancial and government regulators must be developed, but must be done so in a way also conforms to both parties’ operational values, leaving both entities Pinancially and legally secure. Prior to commencing the joint venture operation, both parties are required to reach agreements on the following factors: -‐ Equity share; CUB ideally with a small controlling stake, as this would ease the later steps, while still allowing for a higher chance of success (see Appendix 5) -‐ The exact contributions of each entity; monetary, existing resources and technologies, human capital. Tsingtao will offer their current production, distribution resources and knowledge of the market to the joint venture, while our company would provide the brand, materials and production strategy (i.e. brewing methods and relevant expertise). -‐ Intentions of the joint venture; i.e. “What are the intended outcomes of this strategic alliance?” “How will the joint venture outcomes will be achieved efPiciently?” “What is on the investment horizon?” -‐ How development and progress with be monitored and measured. -‐ The establishment, distribution and protection of each party’s intellectual property. -‐ Conditions for termination of the agreement: How will joint intellectual property will be split and continue to be protected; how future proPits from combined projects will be split; how we can buy out the partner, and who will bear the responsibility for any future obligations. -‐ Management of speciPic business areas; deciding between dominant control, split or shared control of the joint venture.

Step Three (April 2016) Joint venture operations commence full-‐time.

Step Four (May 2016) In order to reduce our Pinancial risk associated with a foreign joint venture, production will initially utilise Tsingtao’s production facilities.

IMPLEMENTATION TIMELINE

Step Five (Summer 2016 -‐ 2018) The summer months present the optimal season to commence branding of our new luxury beer brand towards the Chinese market. Drawing upon Tsingtao’s marketing knowledge, as well as their experience in sponsoring worldwide events, such as the Beijing Olympics and Shanghai Expo, our new luxury brand will aid Western Plair towards an upmarket consumer group.

We will bid to sponsor 2016 Chinese Grand Prix, whom are currently searching for new partners since their partnership with UBS had been completed. With 300 million fans, this will be our promising opportunity to introduce the CUB brand.

Step Six (April 2018) After consolidating our venture, and gaining recognition in the Chinese market, we will consider further domestic expansion in order to cater to the growth of the population and demand. This involves setting up our own local production plants.

Depending upon an external cost-‐benePit analysis of further investment, Tsingtao may continue to produce our line of product. If expansion is necessary, we shall incorporate plants in Ningbo or Sichuan as per our previous analysis.

Step Seven (2016-‐2019) Through the venture’s formative years, it is crucial to follow our intended middle-‐class target demographic growth, and expand with it. At this stage, it is hard to precisely predict the outcome, we must follow our analyses and forecasts for different regions, and our operations focus on the continual reassessment of new marketing strategies that are required to be developed for differing regions and consumers.

Step Eight (2019 -‐ ) If the joint venture proves successful for our brand beyond the Pive-‐year horizon, we will begin to analyse the viability of a takeover. With what will be Pive-‐years of local knowledge and experience, we will be prepared for our eventual direct investment in the world’s largest beer consumption market, beginning with the newly-‐acquired venture that will become our wholly-‐owned subsidiary.

In conjunction with lagging local growth, we feel the time is right to expand Carlton & United Breweries into China: a mature market, that is continually seeking premium quality beer, presents an opportunity for proPit, that is still showing signs of growth. Strong brand awareness, along with continued growth in GDP and capitalisation of existing distribution channels, are key in determining success of the expansion. Through a joint venture, with Tsingtao, we believe CUB can overcome protectionist policies to take advantage of the rising disposable income of the growing middle class and burgeoning 20-‐34 age bracket in increasingly urbanised cities. Beyond the immediate horizon of international expansion through a strategic alliance, direct investment in wholly-‐owned subsidiary may be the next step in the direction towards integrated success for Carlton & United Breweries in the Asian market.

REFERENCEAll background images and stock photos courtesy of: www.gettyimages.com.au

Administrative Committee of Ningbo Free Trading Zone (NFTZ). [Webpage] (2013). About us. Retrieved at http://www.nftz.gov.cn/en/

Administrative Committee of Ningbo Free Trading Zone (NFTZ). [Webpage] (2013). Brief Introduction. Retrieved at http://www.nftz.gov.cn/en/newslist.aspx?NodeCode=10001000800010001

Anning, J. (2015). IBISWorld Industry Report C1212 Beer Manufacturing in Australia. Retrieved from IBISWorld database.

Asean-‐China Free Trade Area [Webpage]. (2009). Retreived at http://www.asean-‐cn.org/Item/585.aspx

Barton, D., Chen, Y. and Jin, A. (2013). Mapping China’s middle class: Generational change and the rising prosperity of inland cities will power consumption for years to come. McKinsey Quarterl, June 2013, Retrieved at http://www.mckinsey.com/insights/consumer_and_retail/mapping_chinas_middle_class

BBC Business News. (2013) Xi Jinping: 'China will protect foreign companies', BBS Business News, 8 april 2013, Retrieved at http://www.bbc.com/news/business-‐22061776 Carlton & United Breweries [Webpage]. (2015). Retrieved at http://cub.com.au/

Carpenter, Mason A. and Dunung, Sanjyot P. (2011). International Business: Opportunities and Challenges in a Flattening World, v. 1.0, Retrieved at http://catalog.Platworldknowledge.com/bookhub/3158?e=fwk-‐168388-‐chpr

Cheng, S. and Bowskill, E. (2015) Cultural tips for doing business in China, Retrieved at http://www.australianbusiness.com.au/international-‐trade/export-‐markets/china/cultural-‐tips-‐for-‐doing-‐business-‐in-‐china

Davies, K. (2013), “China Investment Policy: An Update”, OECD Working Papers on International Investment, 2013/01, OECD Publishing. http://dx.doi.org/10.1787/5k469l1hmvbt-‐en

Delios, A., Beamish, P. W. and Lu, J. W. (2012) International Business: An Asia PaciPic Perspective (2nd Edition). Pearson, FT Press

Dun and Bradstreet. (2015). Company 360 Carlton United Breweries [Company proPile]. Retrieved from Company 360 database

Dun and Bradstreet. (2013). SABMiller Beverage Investments Pty Ltd, proPile [Company proPile]. Retrieved from Company360 database.

Food and Agriculture Organization of the United Nations (FAO) (2009), agribusiness handbook: Barley, Malt, Beer. FAO, Rome, Italy. Retrieved at http://www.fao.org/Pileadmin/user_upload/tci/docs/AH3_BarleyMaltBeer.pdf

Fung, J. [Powerpoint] (2010). The China Malting Barley Market Current and future Trends, Supertime development Limited, Retrieved at http://www.ausgrainsconf.com/sites/default/Piles/Pile/presentations%202010/Fung.pdf

Haque,M. Shamsul. & Mudacumura, Gedeon M. (2004). Handbook of development policy studies. New York : Marcel Dekker

Li & Fung Research Centre (2012). Distribution in China: September 2012. Li & Fung Research Centre, Hong Kong. Retrieved at http://www.funggroup.com/eng/knowledge/research/china_dis_issue101.pdf

MacLeod, I (2015), Advantages & Disadvantage of a Joint Venture, Retrieved at http://www.rpemery.com.au/articles/advantages_and_disadvantages_jv.htm

Madden, N. [Webpage] (2008) One Olympics...But Three Beer Sponsors?. Nielsen Co, Ad Age. Retrieved at http://adage.com/china/article/special-‐report/one-‐olympicsbut-‐three-‐beer-‐sponsors/127464/

Madden, N. [Webpage] (2010) Tsingtao Taps Chinese Tourism With Expo Campaign. Nielsen Co, Ad Age. Retrieved at http://adage.com/china/article/spotlight/tsingtao-‐taps-‐chinese-‐tourism-‐with-‐expo-‐campaign/144182/

Mat Isa, C. M., Saman, H. M., Mohd Nasir, S. R. and Abd Rahman, N. H. (2012), Entry Mode and Entry Timing Decisions by Malaysian Construction Firms in International Market, National Postgraduate Seminar 2012, Retrieved at http://www.academia.edu/3160390/Entry_Mode_and_Entry_Timing_Decisions_by_Malaysian_Construction_Firms_in_International_Market

National Bureau of Statistics of China [Webpage]. (2015). Retreived at http://data.stats.gov.cn

OECD Working Papers on International Investment, 2013/01, OECD Publishing. Retrieved at http://dx.doi.org/10.1787/5k469l1hmvbt-‐en

SABMiller. (2014). SABMiller plc: Annual Report 2014 [Annual Report]. Retrieved from http://www.sabmiller.com/investors/reports

Tang, Y., Xiang, X., Wang, X., Cubells, J. F., Babor, T. F. & Hao, W. (2013) Alcohol and alcohol-‐related harm in China: policy changes needed. Bulletin of the World Health Organization 2013;91:270-‐276. doi: http://dx.doi.org/10.2471/BLT.12.107318

TsingTao [Webpage] (2015). The Rise of TsingTao: Historical Facts from TsingTao’s Past. Retrieved at https://www.tsingtaobeer.com/history

Wei, M. (2012). Budweiser Is Luxury in China Where Beer Costs 30 Cents. BloombergBusiness April 10, 2012. Retrieved at http://www.bloomberg.com/news/articles/2012-‐04-‐10/budweiser-‐is-‐luxury-‐in-‐china-‐where-‐beer-‐costs-‐30-‐cents

World Bank Group [Webpage] (2014). Economy Rankings. Retrieved at http://www.doingbusiness.org/rankings

Zhou, C., Delios, A. and Yang, J. Y. (2002) “Locational Determinants of Japanese Foreign Direct Investment in China,” Asia PaciPic Journal of Management, vol. 19, no. 1, pp. 63-‐86.

APPENDIX ONE Volume Growth Rates of Beer Consumption (Source: SABMiller, 2014)

APPENDIX TWO Premium Beer as Percentage of Total Beer Consumption Source: SABMiller, 2014

Top Ten Ranking of Regions by Age Group Concentration, Gross Regional Product and Disposable Income (Source: China Bureau of Statistics, 2015)

APPENDIX THREE

Ranking Population of 15-64 year olds

Gross Regional Product per capita

Per capita Disposable Income

1 Guangdong Tianjian Shanghai

2 Shandong Beijing Beijing

3 Henan Shanghai Zhejiang

4 Jiangsu Jiangsu Guangdong

5 Sichuan Zhejiang Jiangsu

6 Hebei Inner Mongolia Tianjian

7 Hunan Laioning Fujian

8 Hubei Guangdong Shandong

9 Zhejiang Fujian Liaoning

10 Anhui Shandong Inner Mongolia

Middle Class Sub-regional Distribution Source: McKinsey & Company, 2015

APPENDIX FOUR

APPENDIX FIVE Joint Venture Performance, Based on Equity Structure Source: Delios, Beamish, 2004

MELBOURNE BUSINESS SCHOOL APRIL 2015

DESIGNED BY ROBERT AU FOR JANE LU