jonathan norris

TRANSCRIPT

Private FundingTrends Presentation

Venture Healthcare – Industry Update

OIS 2015

November 2015

Jon Norris, Managing Director

Jon Norris - [email protected] 3

Manage West Coast Healthcare Relationshipsfor SVB across the SVB Platform, including

Fund of Funds (Investment as LP) Direct Equity (Co-Investments and Rights to Invest) Commercial Bank (Venture/Mezzanine Debt, Asset-based Debt,

New Fundings) Equity Financing Strategy for Early Stage and Venture-Backed

Companies Industry Thought Leadership

Jon Norris: Managing Director, SVB Capital

Jonathan NorrisManaging Director, HealthcareSilicon Valley Bank

Mobile [email protected]: @jonnysvb

Publications Trends in Healthcare Investments and Exits (2015) A Year of Dazzling Returns: 2014 Healthcare Investments

and Exits (2015) Trends in Healthcare Investments and Exits (2014) Strong Momentum in Healthcare (2013) First Mover Advantage (2012) Continued Rebound (2012) Trends in M&A (2011) Bringing Home the Bacon (2010)

Jon Norris - [email protected] 4

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015Total VC

Dollars ($B)$99 $38 $21 $19 $22 $23 $27 $31 $30 $20 $23 $28 $27 $30 $50 $47

Biopharma 4% 9% 15% 19% 19% 16% 17% 17% 15% 19% 17% 17% 16% 15% 12% 12%

Device 2% 5% 9% 8% 8% 10% 11% 12% 11% 13% 10% 10% 9% 7% 5% 4%

US Healthcare Investment/Total Venture Investment

Source: PricewaterhouseCoopers, and SVB proprietary data

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015

$ B

illio

ns

Total VC Dollars ($B) Biopharma Device

$99

5Jon Norris - [email protected] 5

Venture Investment into Device - Consistency since 2009

Year Device $ Invested Dollars as % of Total VC

2007 $3.7 Billion 12%

2008 $3.6 Billion 11%

2009 $2.6 Billion 13%

2010 $2.5 Billion 10%

2011 $2.9 Billion 10%

2012 $2.6 Billion 9%

2013 $2.1 Billion 7%

2014 $2.6 Billion 5%

Q3’15 $2.1 Billion (stable) 4%

Jon Norris - [email protected] 6

0%

100%

200%

300%

400%

500%

0

1

2

3

4

5

6

7

8

9

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$ B

illio

ns

Gap in Funding HC $ Fundraised HC $ Invested % Capital Flow Ratio

Source: PricewaterhouseCoopers, Thompson Reuters, and SVB proprietary data

US Healthcare: Venture Dollars Invested and Raised

Jon Norris - [email protected] 7

Most Active Venture Investors in New $ Deals 2013-2014

Biotech: Device:1. Orbimed Advisors 1. NEA2. AtlasVentures 2. BioStar Ventures3. Novo Ventures 3. Emergent Medical4. NEA 4. Orbimed Advisors5. Sofinnova Ventures 5. Novo Ventures6. MS Ventures 6. Lightstone et al7. Versant Ventures 7. L.S. Angels8. SR One 8. Longitude Capital 9. Novartis 9. Boston10.Polaris Partners 10. JJDC

Corporate Investors highlighted in red

Jon Norris - [email protected] 8

Top New Money Venture Investors in 1H 2015, Worldwide

Most Active Biotech VCInvestors

# of New Money Investments

MorningsideGroup 6

NEA 6

Fidelity Biosciences 5

Orbimed 5

Novo/Ally Bridge/Venrock 4 (tie)

Most Active Device VC Investors

# of New Money Investments

NEA 3

Ally Bridge Group 3

Venrock 2

AscensionVentures 2

Mountain Group Capital 2

Jon Norris - [email protected] 9

Q3 ‘15 Bio Financing Update

Q3 ‘15 Biotech Update: Top 10 VC Equity Rds.4 Deals >$100M rounds in Q3

No deal smaller than $75M 8/10 Deals w/ Cross Over participation;

8/10 in Q2 tooEarlier, Bigger Rounds:

3 Series A, 4 Series B, 3 Series C5 Oncology, 3 TGP, 2 Rare/Orphan4/10 OUS – 2UK, Swiss, Netherlands

Jon Norris - [email protected] 10

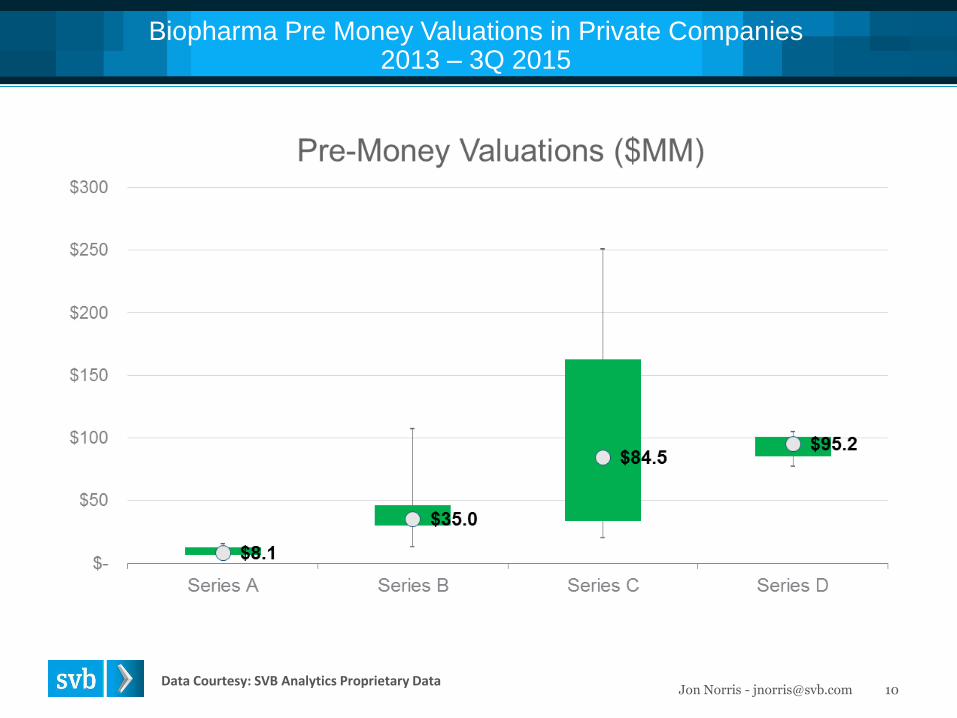

Biopharma Pre Money Valuations in Private Companies 2013 – 3Q 2015

Data Courtesy: SVB Analytics Proprietary Data

Jon Norris - [email protected] 11

Cross Over Activity Since 2013CB Insights/SVB Confidential Data

Cross Over Firm Ranking 2013/14 1H '15Q3'15 -

11/6/15

Trend

Line in

2nd Half

2015

Total Deals

Adage 5 2 2 - 9 Q3 Current top 5 Total since 2013

Casdin 3 5 3 - 11 Ra Capital 14 Ra Capital 38

Deerfield 13 5 4 22 Fidelity 12 Deerfield 22

Foresite 7 7 5 - 19 Rock Springs 12 Fidelity 21

Fidelity Inv 2 7 12 21 Cormorant 9 Foresite 19

Jennison 4 6 7 17

Perceptive 6 5 3 14

RA Capital 13 11 14 38

Redmile 9 2 5 16

Rock Springs 9 10 12 - 31

Wellington 5 7 2 14

Cormorant 0 5 9 14

Woodford 4 3 4 11

Jon Norris - [email protected] 12

Largest Biopharma Series B Venture Rounds and Step-up Trends(Q1 – Q2 2015)

If no Crossover participation,Median Series B step-up is

25%With Crossover participation, median Series B step-up is

78%with a wide range of 30% to 154%

RA Capital and Wellington were the most active investors in the

largest 2015 Series B rounds,

with 4 investments each

Source: CB Insights and SVB proprietary data

Jon Norris - [email protected] 13IPOs = VC backed IPOs raising > $25M

IPO Performance of Crossover Backed Companies vs. Peers(2013 – 1H 2015)

Median pre-money valuations

were 88% higher

than peer group

Median dollars raised at IPO

were 60% higher

than peer group

Median value, 9 months after IPO, was

15% higher than IPO price;

Average value was 45%* higher

than IPO price

Source: CB Insights and SVB proprietary data

*Calculation excludes one outlier (1,828%)

14Jon Norris - [email protected] 14

Q3 ‘15 Device Update

Q3 ‘15 Device Update:4 Deals > $100M rounds in Q3

Top deal in first half was only $57M.6/10 Deals w/ Cross Over participation, versus 3/10 in Q2.

New types of Xovers including Longwood, Third Point, Seneca and Woodford.

5/10 Deals included Corporate Venture, way up over previous years and up over Q2 (2/10)

Includes less known players like Sino, Santen, Intersect Partners, Healthcor, and Hoya.

Endavor Vision did three new deals in Q3 (Reshape, Gynesonics, and CeQur).

Swiss fund that raised $100M+ Medtech fund in late 2014Final Take away:

New $ moving in to the sector – be prepared for lots of China interest in 2016 (really, we mean it this time!)

15Jon Norris - [email protected] 15

Device Pre Money Valuations in Private Device Companies 2012 – 3Q2015

Jon Norris - [email protected] 16

0

10

20

30

40

50

60

70

80

90

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015

# o

f B

ig E

xits

Big Exit M&A VC-Backed IPOs

VC-Backed Healthcare IPOs and Big Exit M&A (2005- Q3 2015)M&A = Pvt. VC Backed M&A >$50M Upfront for Tools/Dx & Device & >$75M Upfront for Bio

IPO = VC Backed IPO raising >$25M

Source: Investment bank reports, VentureSource, PitchBook, press releases, and discussions with life science professionals

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015

Big Exit M&A

19 20 24 17 22 28 35 36 27 43 35

VC-Backed

IPOs32 29 21 2 3 12 7 11 37 83 48

Jon Norris - [email protected] 17

0

2

4

6

8

10

12

14

16

18

20

22

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 3Q2015

Tota

l Val

ue

($ B

illio

ns)

Big Exit Upfront Payments Big Exit Milestones to be Earned Pre-Money IPO Value*Potential distribution calculated as 75% of Upfront Payments, 25% of Milestones, and 75% of Pre-Money IPO Value

Potential Distributions* From VC-Backed IPOs and M&A(2005 – Q3 2015)

Source: Investment bank reports, VentureSource, press releases, CB Insights, and discussions with life science professionals

2015: Projected numbers outpace 2013and approach last year’s record returns

Frazier Life Sciences Retreat

Biopharma VC backed Exits by Quarter 2013- Q32015

Q1 Q2 Q3 Q4 Total

2013 IPO 3 10 11 8 32

M&A 3 3 4 4 14

2014 IPO 24 12 17 13 66

M&A 3 4 6 1 14

2015 IPO 11 13 9 33

M&A 7 4 6 17

• Q3: another 6 M&A to exceed 2014 full year numbers – now at 20 in Q4• 7 VC backed IPOs so far in Q4 – discounted IPO new norm?

Source: CB Insights, press releases, and SVB proprietary data 18

19Jon Norris - [email protected]

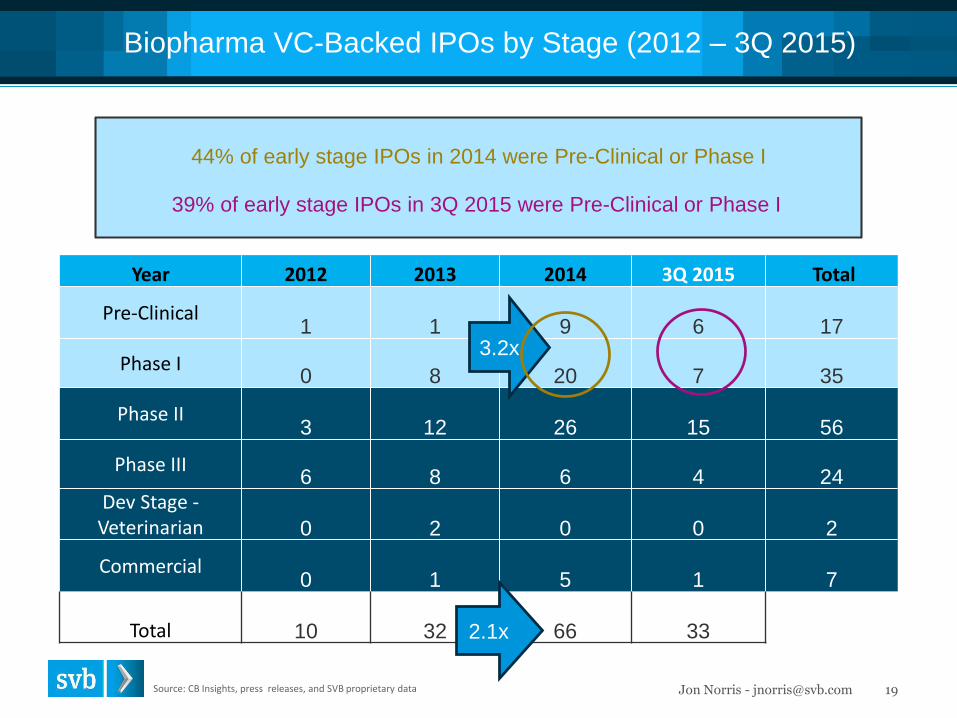

Biopharma VC-Backed IPOs by Stage (2012 – 3Q 2015)

Year 2012 2013 2014 3Q 2015 Total

Pre-Clinical1 1 9 6 17

Phase I0 8 20 7 35

Phase II3 12 26 15 56

Phase III6 8 6 4 24

Dev Stage -Veterinarian 0 2 0 0 2

Commercial0 1 5 1 7

Total 10 32 66 33

Source: CB Insights, press releases, and SVB proprietary data

2.1x

3.2x

44% of early stage IPOs in 2014 were Pre-Clinical or Phase I

39% of early stage IPOs in 3Q 2015 were Pre-Clinical or Phase I

Jon Norris - [email protected] 20

VC-Backed Biopharma IPOs: Median Pre-Money and Dollars Raised (2012 – 3Q 2015)

Source: CB Insights, press releases, and SVB proprietary data

2013 2014 3Q 2015

# of IPOs Raised Over $100MM 8 12 11

% of IPOs Raised over $100MM 25% 18% 33%

$61 $72

$62 $63 $67

$202

$174 $141

$139

$158

$0

$50

$100

$150

$200

$250

2012 2013 2014 1H 2015 3Q 2015

Med

ian

Val

ue (

$ M

illio

ns)

BioPharma IPO $ Raised BioPharma Pre-Money

21Jon Norris - [email protected]

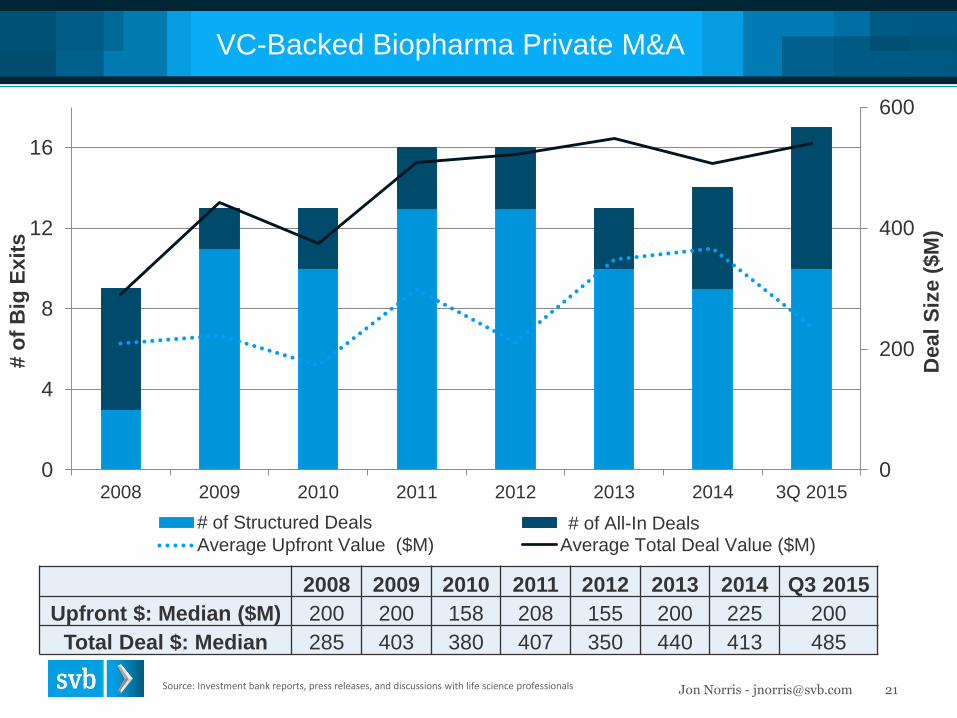

VC-Backed Biopharma Private M&A

Source: Investment bank reports, press releases, and discussions with life science professionals

0

200

400

600

0

4

8

12

16

2008 2009 2010 2011 2012 2013 2014 3Q 2015

Dea

l Siz

e ($

M)

# o

f B

ig E

xits

# of Structured Deals Total # of ExitsAverage Upfront Value ($M) Average Total Deal Value ($M)

# of All-In Deals

2008 2009 2010 2011 2012 2013 2014 Q3 2015Upfront $: Median ($M) 200 200 158 208 155 200 225 200

Total Deal $: Median 285 403 380 407 350 440 413 485

Jon Norris - [email protected] 22

0

2

4

6

8

10

12

14

16

18

2009 2010 2011 2012 2013 2014 3Q 2015

# o

f C

om

pan

ies

Pre-Clinical Phase I Phase II Phase III Commercial

VC-Backed Biopharma Private M&A by Stage since 2009

Source: Investment bank reports, press releases, CB Insights, and discussions with life science professionals

Jon Norris - [email protected] 23

VC Backed Device Exits by Quarter 2013 – Q32015

• Device IPOs: 4/7 IPOs in 1H’15 had <$11M Rev in Previous 12 months

• Q3: 9 M&A, with 5/9 companies Non-Approved; 3 CE Mark Only

Source: CB Insights, press releases, and SVB proprietary data

Q1 Q2 Q3 Q4 Total

2013 IPO 0 0 0 2 2

M&A 1 2 6 2 11

2014 IPO 1 5 1 3 10

M&A 2 9 5 2 18

2015 IPO 3 4 3 10

M&A 0 4 9 13

Jon Norris - [email protected] 24

VC-Backed Device M&A by Stage (2009 – 3Q2015)

Source: Press releases, CB Insights, and SVB proprietary data

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013 2014 3Q2015

# o

f B

ig E

xits

Non-Approved CE Mark U.S. Commercial

Represents number of IPOsRepresents Big Exit M&A

1 1

2

1

2

1 2 7

1 2 8

Jon Norris - [email protected] 25Source: Press releases, CB Insights, and SVB proprietary data

Recent Device M&A by Indication 2014- Q32015

0

1

2

3

4

5

6

7

8

9

10

# o

f C

om

pan

ies

Non-Approved CE Mark U.S. Commercial

Represents number of IPOsRepresents Big Exit M&A

1 1

1

1

1

2 3

2

1

1 1

Jon Norris - [email protected] 26

Trends in Venture Backed Device M&A >$50M

SVB Proprietary Data: Private Venture Backed Big ExitsAverage Multiple calculated at 85% of value divided by venture equity

2009-Q3’15Number of

ExitsStage:

Dev/CE/USAverage Years

to Exit

Vascular 18 1/6/11 7

Imaging 6 0/0/6 10

Cardiovascular 22 7/8/7 6.6

Surgical 16 1/2/13 7.7

Neuro 4 2/2/0 5

Orthopedics 7 0/0/7 7.3

Ophthalmology 6 1/2/3 6.7

Aesthetics 4 0/0/4 4.8

OVERALL AVERAGES 7.0

Jon Norris - [email protected] 27

Predictions in 2015 into 2016

The recent pullback in the global equity markets has impacted this sector, however we believe that the fundamentals of the healthcare venture market continue to be strong. We will be carefully watching how IPOs perform, and if investing patterns by crossover investors change.

• Strong Fundraising and Fast Pace of Investing in Biotech w/ record breaking numbers for HC investment into companies.

• Will there be Strong Participation of Cross-over Investors in Q4? I think there will, but in less deals - activity rate cannot continue. 80 investments by top X Overs in 2013-4, accelerating to 75 for1H’15, then 82 alone in Q3 to date.

• Where have the BioPharma Corporate VCs gone? Not as much Corporate VC activity as Cross Overs have taken up extra available capital in syndication rounds – will they come back when Cross Overs retreat?

• Biotech M&A has already outpaced 2014 and should remain strong in 2016 regardless of IPO activity; Device M&A numbers look good after great Q3.

• IPOs Market Stays Open but Not at 2014 Pace – VC- Backed BioPharma IPOs for 2015 Will Likely Be Between 45- 55

Thank you!!!