jordan ict sector profile - 2012

TRANSCRIPT

JORDAN ICT SECTOR PROFILEAnalysis, Achievements, AspirationsInformation &

Communications TechnologyAssociation - Jordan

This publication has been produced with the assistance of theEuropean Union & Jordan Enterprise. The contents of this publication

are the sole responsibility of int@j and can in no way be taken to reflect theviews of the European Union & Jordan Enterprise Development Corporation.

Jordan ICT Sector Profile, Published by The Information & Communications Technology Association - Jordan (int@j)Project funded by the European Union in cooperation with Jordan Enterprise Development Corporation.

�obgF(*���24&°*�¤A�i°b~|-(°*H�ibE¡���D*�f£��-�ibCx~7�f£��/��cB��E�f<¡c��D*� wG�4*v~8(*��- fJ2b~|gB°*��J4b~{�D*�xJ¡�gD�f£F24°*�f~z~6'¡�D*��E��Hb�gDb+�¤+H4H°*�2bp-°*��E��J¡�g+��D3H

The European Union is made up of 27 Member States who have decided to gradually link together their know-how, resources and destinies. Together, during a period of enlargement of 50 years, they have built a zone of stability, democracy and sustainable development whilst maintaining cultural diversity, tolerance and individual freedoms.

The European Union is committed to sharing its achievements and its values with countries and peoples beyond its borders.

The contents of this publication are the sole responsibility of the Jordan Information & Communications Technology Association (int@j) andcan in no way be taken to reflect the views of the European Union & Jordan Enterprise Development Corporation.

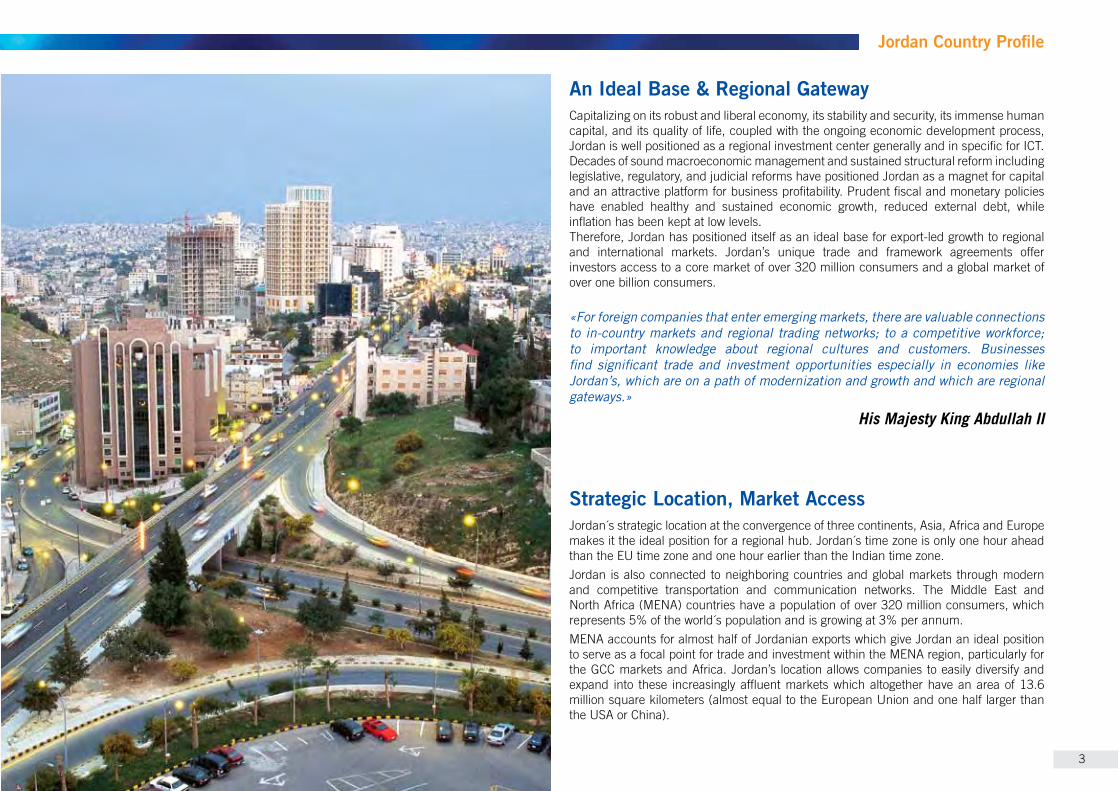

An Ideal Base & Regional GatewayCapitalizing on its robust and liberal economy, its stability and security, its immense human capital, and its quality of life, coupled with the ongoing economic development process, Jordan is well positioned as a regional investment center generally and in specific for ICT.Decades of sound macroeconomic management and sustained structural reform including legislative, regulatory, and judicial reforms have positioned Jordan as a magnet for capital and an attractive platform for business profitability. Prudent fiscal and monetary policies have enabled healthy and sustained economic growth, reduced external debt, while inflation has been kept at low levels.Therefore, Jordan has positioned itself as an ideal base for export-led growth to regional and international markets. Jordan’s unique trade and framework agreements offer investors access to a core market of over 320 million consumers and a global market of over one billion consumers.

«For foreign companies that enter emerging markets, there are valuable connections to in-country markets and regional trading networks; to a competitive workforce; to important knowledge about regional cultures and customers. Businesses find significant trade and investment opportunities especially in economies like Jordan’s, which are on a path of modernization and growth and which are regional gateways.»

His Majesty King Abdullah II

Strategic Location, Market AccessJordan´s strategic location at the convergence of three continents, Asia, Africa and Europe makes it the ideal position for a regional hub. Jordan´s time zone is only one hour ahead than the EU time zone and one hour earlier than the Indian time zone.Jordan is also connected to neighboring countries and global markets through modern and competitive transportation and communication networks. The Middle East and North Africa (MENA) countries have a population of over 320 million consumers, which represents 5% of the world´s population and is growing at 3% per annum. MENA accounts for almost half of Jordanian exports which give Jordan an ideal position to serve as a focal point for trade and investment within the MENA region, particularly for the GCC markets and Africa. Jordan’s location allows companies to easily diversify and expand into these increasingly affluent markets which altogether have an area of 13.6 million square kilometers (almost equal to the European Union and one half larger than the USA or China).

Jordan Country Profile

3

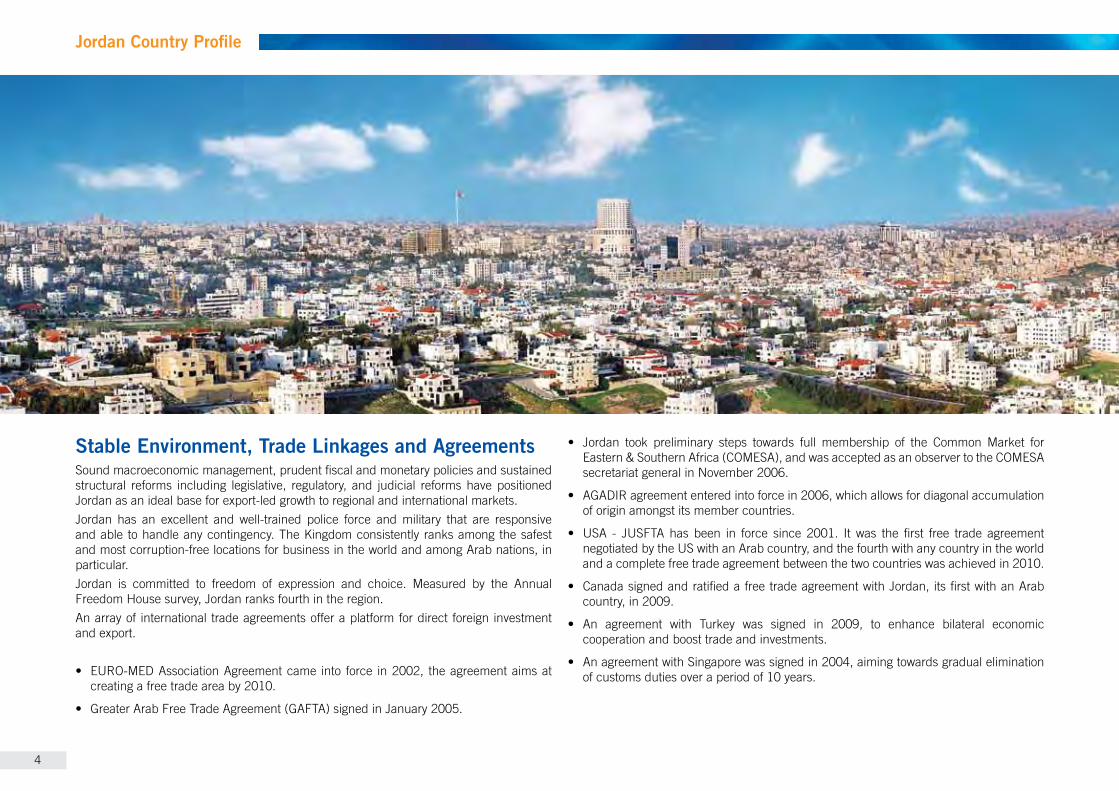

Stable Environment, Trade Linkages and AgreementsSound macroeconomic management, prudent fiscal and monetary policies and sustained structural reforms including legislative, regulatory, and judicial reforms have positioned Jordan as an ideal base for export-led growth to regional and international markets.Jordan has an excellent and well-trained police force and military that are responsive and able to handle any contingency. The Kingdom consistently ranks among the safest and most corruption-free locations for business in the world and among Arab nations, in particular.Jordan is committed to freedom of expression and choice. Measured by the Annual Freedom House survey, Jordan ranks fourth in the region.An array of international trade agreements offer a platform for direct foreign investment and export.

creating a free trade area by 2010.

secretariat general in November 2006.

of origin amongst its member countries.

negotiated by the US with an Arab country, and the fourth with any country in the world and a complete free trade agreement between the two countries was achieved in 2010.

country, in 2009.

cooperation and boost trade and investments.

of customs duties over a period of 10 years.

Jordan Country Profile

Cultural and Linguistic AffinityAlthough Jordan is ideally positioned to serve all the Arab nations including the Gulf countries, the Levant region, the North African countries, and even the Arabic-speaking population of the European Union and the USA, there is no doubt that Jordan´s closest geographical and cultural affinities will be found in the nearby states of the Gulf Cooperation Council (GCC).The members of the GCC are the Kingdom of Saudi Arabia; United Arab Emirates, Kuwait,

time zone and considerable cultural “kinship” with its affluent neighbors. Macroeconomic indicators are favorable for Jordanian workers. Educational enrollment per capita surpasses a number of regional competitors, and with services making up more than 86 percent of Jordan´s economic output, Jordanians are clearly oriented towards a services economy. Jordanians are recognized to be more technology savvy, with higher fixed and mobile line penetration as well as a higher Internet usage penetration per capita than most regional countries.

Location, Travel and Time ZoneThe Hashemite Kingdom of Jordan is located in Western Asia spanning the southern part of the Syrian Desert down to the Gulf of Aqaba. Jordan shares borders with Syria to the north, Iraq to the northeast, Saudi Arabia to the east and south, and the Palestinian territory of the West Bank and Israel to the west. The capital city is Amman. Jordan Time Zone is GMT +2 (+3 in summer time).

General InfrastructureJordan is endowed with excellent infrastructure to serve and move people, goods and ideas.

Three Airports: Queen Alia International Airport (Amman) which was recently expanded to serve 9 million passengers, King Hussein International Airport (Aqaba) and Amman Civil Airport at Marka for mostly domestic and some nearby international routes.

Seaport: for general cargo, containerized cargo and specialized cargo.

Railroad: There is a new railway master plan to improve and increase the existing 620 km long rail network.

Roads: Jordan has a well developed road network allowing quick access to all its territory.

Electric Energy:

towards increasing the use of renewable energy sources.

Jordan Country Profile

5

Sector Background & LandscapeThe Information and Communications Technology (ICT) field represents an opportunity for Jordan to increase its competitive advantage over other countries in the region; consequently Jordan has taken very serious steps in order to launch major initiatives aiming at developing the ICT sector.

In response to a challenge put forward by his Majesty King Abdullah II in 1999, the efforts were directed at devising a comprehensive framework for Jordan’s ICT sector, which

nurturing a vibrant, export-oriented, and internationally competitive ICT sector, followed by the National ICT Sector Strategy (2007-2011), and the soon to be launched National ICT Sectory Strategy (2012-2016). These strategies involved developing a regulatory framework, providing an enabling infrastructural environment, and offering sector advancement programs, human resource development, capital and finance.

Governments and non-governmental organizations worldwide have recognized the power

of ICT to improve business, reduce poverty, improve public services and create an industry in which developing countries can gain a competitive advantage. The ICT sector utilizes low capital costs, as principal inputs to ICT production are human resources. Therefore, Jordan is well positioned to build upon its strong foundation of people to cultivate growth in the ICT sector.

SWOT Analysis of Jordan ICT Sector

Strengths Weaknesses

�� Leadership support.��

to trade and foreign participation, taxation has become relatively liberal.

�� Jordan’s ICT sector enjoys a fully liberalized market.

�� High number of ICT graduates annually.�� High rate of entrepreneurship. �� Positive image.�� Location.

�� Product development.�� Building specialization. �� Legal and regulatory hurdles may affect

market efficiency.�� �mismatch between outputs of

academia and the industry requirments.��

standards.

Opportunities Threats

�� Major export markets are GCC and USA.

Million for 2010.�� Established international trade

agreements to develop business with other countries.

�� Products Development.�� Building specialization.

�������� Bureaucracy in Government

procurement.�� Brain drain, due to difficulty in attracting

and retaining ICT experts in Jordan.

Reference: int@j

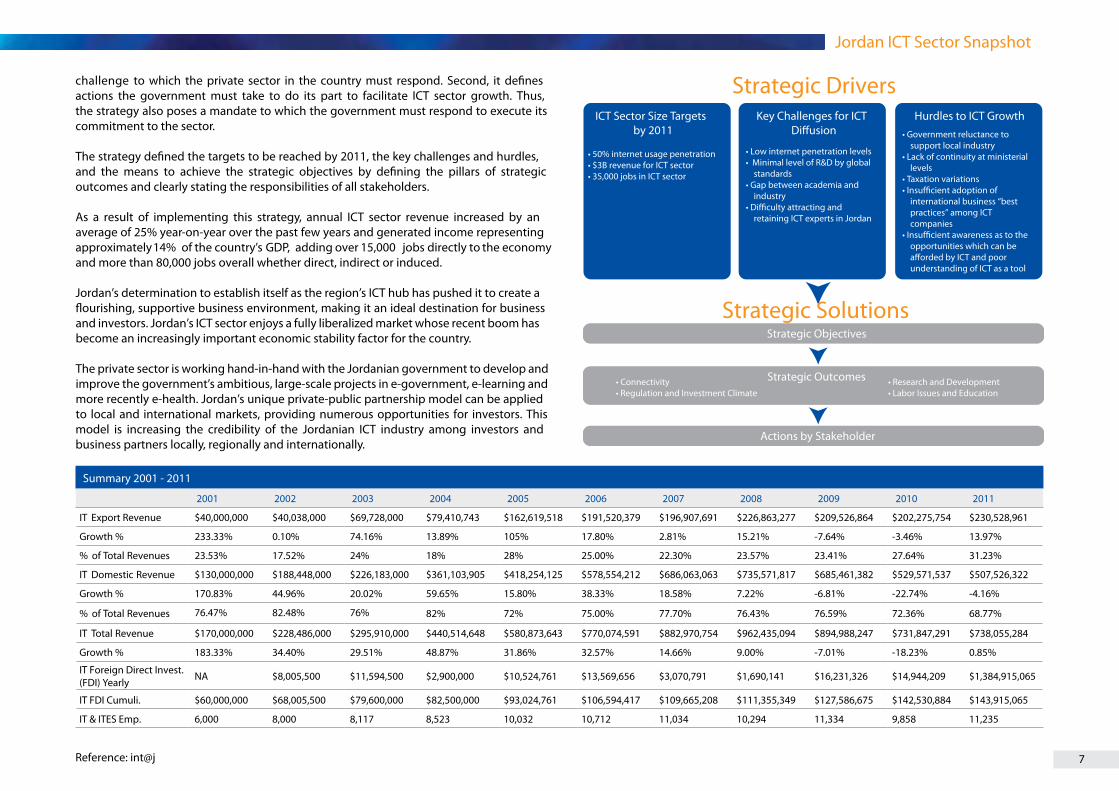

The National ICT Sector Strategy In 2007, the National ICT Strategy (2007-2011) was created as a continuation of the

at taking advantage of new markets, enhancing business maturity, investing in research and development, capitalizing on regional demand, cultivating foreign investment, and improving the ICT labor market.

The National ICT Strategy serves two basic goals. First, it identifies the ICT sub-sectors best-suited for growth given the environment in Jordan. Thus, the strategy poses a

Jordan ICT Sector Snapshot

6

challenge to which the private sector in the country must respond. Second, it defines actions the government must take to do its part to facilitate ICT sector growth. Thus, the strategy also poses a mandate to which the government must respond to execute its commitment to the sector.

The strategy defined the targets to be reached by 2011, the key challenges and hurdles, and the means to achieve the strategic objectives by defining the pillars of strategic outcomes and clearly stating the responsibilities of all stakeholders.

As a result of implementing this strategy, annual ICT sector revenue increased by an average of 25% year-on-year over the past few years and generated income representing approximately 14% of the country’s GDP, adding over 15,000 jobs directly to the economy and more than 80,000 jobs overall whether direct, indirect or induced.

Jordan’s determination to establish itself as the region’s ICT hub has pushed it to create a flourishing, supportive business environment, making it an ideal destination for business and investors. Jordan’s ICT sector enjoys a fully liberalized market whose recent boom has become an increasingly important economic stability factor for the country.

The private sector is working hand-in-hand with the Jordanian government to develop and improve the government’s ambitious, large-scale projects in e-government, e-learning and more recently e-health. Jordan’s unique private-public partnership model can be applied to local and international markets, providing numerous opportunities for investors. This model is increasing the credibility of the Jordanian ICT industry among investors and business partners locally, regionally and internationally.

Summary 2001 - 2011

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

IT Export Revenue $40,000,000 $40,038,000 $69,728,000 $79,410,743 $162,619,518 $191,520,379 $196,907,691 $226,863,277 $209,526,864 $202,275,754

Growth % 233.33% 0.10% 74.16% 13.89% 105% 17.80% 2.81% 15.21% -7.64% -3.46%

% of Total Revenues 23.53% 17.52% 24% 18% 28% 25.00% 22.30% 23.57% 23.41% 27.64%

IT Domestic Revenue $130,000,000 $188,448,000 $226,183,000 $361,103,905 $418,254,125 $578,554,212 $686,063,063 $735,571,817 $685,461,382 $529,571,537

Growth % 170.83% 44.96% 20.02% 59.65% 15.80% 38.33% 18.58% 7.22% -6.81% -22.74%

% of Total Revenues 76.47% 82.48% 76% 82% 72% 75.00% 77.70% 76.43% 76.59% 72.36%

IT Total Revenue $170,000,000 $228,486,000 $295,910,000 $440,514,648 $580,873,643 $770,074,591 $882,970,754 $962,435,094 $894,988,247 $731,847,291

Growth % 183.33% 34.40% 29.51% 48.87% 31.86% 32.57% 14.66% 9.00% -7.01% -18.23%

IT Foreign Direct Invest. (FDI) Yearly NA $8,005,500 $11,594,500 $2,900,000 $10,524,761 $13,569,656 $3,070,791 $1,690,141 $16,231,326 $14,944,209

IT FDI Cumuli. $60,000,000 $68,005,500 $79,600,000 $82,500,000 $93,024,761 $106,594,417 $109,665,208 $111,355,349 $127,586,675 $142,530,884

IT & ITES Emp. 6,000 8,000 8,117 8,523 10,032 10,712 11,034 10,294 11,334 9,858

Reference: int@j

Jordan ICT Sector Snapshot

Strategic DriversICT Sector Size Targets

by 2011

• 50% internet usage penetration• $3B revenue for ICT sector• 35,000 jobs in ICT sector

Key Challenges for ICT Di�usion

• Low internet penetration levels• Minimal level of R&D by global

standards• Gap between academia and

industry• Difficulty attracting and

retaining ICT experts in Jordan

Hurdles to ICT Growth• Government reluctance to

support local industry• Lack of continuity at ministerial

levels• Taxation variations• Insufficient adoption of

international business “best practices” among ICT companies

• Insufficient awareness as to the opportunities which can be a�orded by ICT and poor understanding of ICT as a tool

Strategic SolutionsStrategic Objectives

Strategic Outcomes • Connectivity• Regulation and Investment Climate

• Research and Development• Labor Issues and Education

Actions by Stakeholder

7

2011

$230,528,961

13.97%

31.23%

$507,526,322

-4.16%

68.77%

$738,055,284

0.85%

$1,384,915,065

$143,915,065

11,235

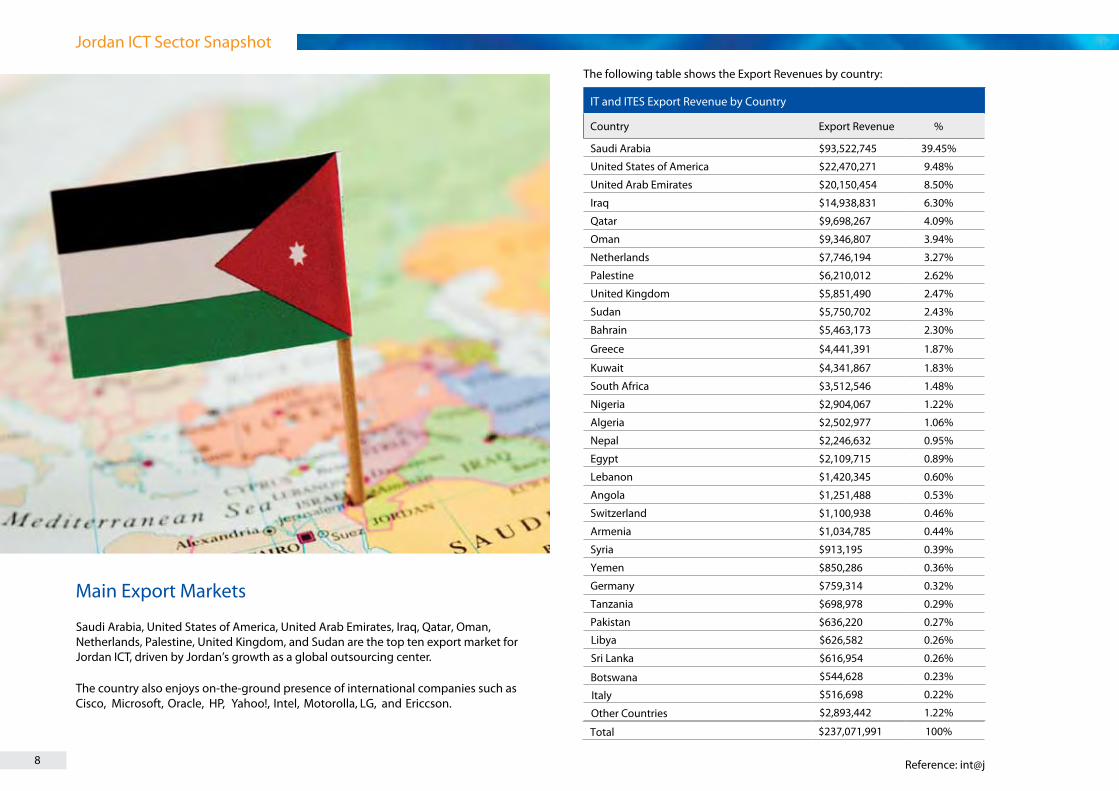

Main Export Markets

The country also enjoys on-the-ground presence of international companies such asCisco, Microsoft, Oracle, HP, Yahoo!, Intel, Motorolla, LG, and Ericcson.

The following table shows the Export Revenues by country:

IT and ITES Export Revenue by Country

Country Export Revenue %

Saudi Arabia $93,522,745 39.45%

United States of America $22,470,271 9.48%

United Arab Emirates $20,150,454 8.50%

Iraq $14,938,831 6.30%

Qatar $9,698,267 4.09%

Oman $9,346,807 3.94%

Netherlands $7,746,194 3.27%

Palestine $6,210,012 2.62%

United Kingdom $5,851,490 2.47%

Sudan $5,750,702 2.43%

Bahrain $5,463,173 2.30%

Greece $4,441,391 1.87%

Kuwait $4,341,867 1.83%

South Africa $3,512,546 1.48%

Nigeria $2,904,067 1.22%

Algeria $2,502,977 1.06%

Nepal $2,246,632 0.95%

Egypt $2,109,715 0.89%

Lebanon $1,420,345 0.60%

Angola $1,251,488 0.53%

Switzerland $1,100,938 0.46%

Armenia $1,034,785 0.44%

Syria $913,195 0.39%

Yemen $850,286 0.36%

Germany $759,314 0.32%

ainaznaT $698,978 0.29%

Pakistan $636,220 0.27%

Reference: int@j

Jordan ICT Sector Snapshot

8

Saudi Arabia, United States of America, United Arab Emirates, Iraq, Qatar, Oman, Netherlands, Palestine, United Kingdom, and Sudan are the top ten export market for Jordan ICT, driven by Jordan’s growth as a global outsourcing center.

Libya $626,582 0.26%

Sri Lanka $616,954 0.26%

$544,628 0.23%

$516,698 0.22%

$2,893,442 1.22%

Botswana

Italy

Other Countries

$237,071,991 100%Total

Policy & Regulatory Environment

(1) International Agreements

Jordan has a Free Trade Agreement with the United States, ratified in 2001. Duty free access to EU markets is enabled through the ratified Jordan-EU Partnership Agreement. Access is available to more than 10 Arab countries through the Arab Free Trade Agreement. Jordan also enjoys bilateral agreements and favorable protocols with over 20 countries, and is a member of the Multilateral Investment Guarantee Agency (MIGA).

(2) Sector Laws

A new Telecom Law is being developed by the Ministry of ICT and industry bodies, which lays the groundwork for the convergence concept of telecommunications, data and media. It also forms the basis for regulating the ICT sector in terms of data security and privacy issues.

(3) Support for ICT Education & Investments

Jordan possesses a very attractive business environment that combines smart and cost effective talent, world class infrastructure and supportive government policies. Jordan

• a knowledge hub has positioned it as a leading ICT and outsourcing destination in the region.

• beyond the traditional markets, Jordan offers a unique opportunity to tap the growing MENA market.

• allow companies the flexibility to invest freely and to employ the best talent.

• segment (15-25 years) providing a good source of manpower; supported by a modern education system that ensures graduates have the required language and technical skills to support ICT-enabled business operations. This has given rise to new niche specializations in online and mobile content and applications, outsourcing and games development.

• rate also means that appreciable hiring can take place with very little, if any, subsequent wage pressure or attrition risk.

(4) Modern and Progressive Society

Jordan is a regional tourist hub, with stable economic and political support for a progressive and multi-cultural society, making it an attractive destination for foreign nationals to work and reside.

Jordan ICT Sector Snapshot

9

Ministry of Information & Communication Technology (MoICT)www.MoICT.gov.jo

Established in April 2002, the Ministry of Information and Communications Technology (MoICT) is the governmental entity responsible for articulating policy in the areas of information technology, telecommunications, and post in the Hashemite Kingdom of Jordan. In addition to developing, incubating, and supporting ICT initiatives at a national level, the Ministry’s mandate includes stimulating local and foreign technology investments as well as promoting awareness and adoption of ICT by all segments of the population, in an all inclusive approach.

The Ministry, through a dynamic public-private partnership process, works to create, promote, and drive new ICT opportunities in Jordan, which will facilitate the positioning of the Kingdom as a regional player in technology adoption and development, a key step to creating a knowledge-based economy. The Ministry’s work plan reflects its objective of creating the enabling legal, commercial, and regulatory environment receptive for technology introduction as a catalyst towards the larger socio-economic development of Jordan.

e-Government is a national program dedicated to delivering services to people across society, irrespective of location, economic status, education or ICT ability. With its commitment to a customer-centric approach, e-Government transforms government and contributes to the Kingdom‘s economic and social development through the e-Government

Telecommunications Regulatory Commission (TRC)

In 1995, Jordan was the first country in the Arab region to enact a modern telecom law and to establish an independent telecommunications regulatory body tasked with the creation of the proper environment for investment in a competitive market, the Telecommunications

telecommunications, information technology and postal sectors. Jordan’s legal and regulatory framework for the telecommunications sector is continuously evolving to meet the changing dynamics in the technology, market and business models. Self regulation - while monitoring the diversity, reach, prices and quality of services - is the ultimate goal

times to reach this ultimate goal.

its mission and the country has seen the positive results of the coherence between the government policy and the regulatory framework.

National Information Technology Center (NITC)www.nitc.gov.jo

in providing better services to Jordanian citizens through the provision of relevant and effective electronic services.

The NITC was established with a vision for excellence, effectively contributing to the drawing and implementation of information technology strategies for the government of Jordan. This is to be achieved through the utilization of the latest technologies and tools needed to implement and manage ICT resources by means of maintaining a central governmental infrastructure for information technology and shared services; providing governmental entities with fit-for-purpose IT solutions and relevant consultations; launching innovative technological solutions in partnership with the private sector on the basis of mutual benefits; promoting a culture of excellence and innovation through the provision of a hospitable and incentive-based environment that encourages work ethics and provides equal opportunities and rewards outstanding players; and supporting local communities by facilitating access to technology and the Internet.

NITC represents the credible reference for assisting governmental entities to implement effective IT solutions that can enhance their productivity and improve their services offering.

Main ICT Stakeholders

10

Information & Communications Technology Association - Jordan (int@j) www.intaj.net

Information & Communications Technology Association - Jordan (int@j) was founded in the year 2000 as an industry-support association for Jordan’s ICT sector.

Building on the nation’s core asset of highly educated and skilled human resources, Jordan’s ICT sector is established as a leading regional ICT hub and an internationally recognized exporter of ICT products and services. int@j’s mission is to advance and promote the constituents it represents in both, the local and global markets.

The association realizes its mission through positively influencing policy and legislation, offering capacities building programs, carrying out local and regional marketing activities, and providing members with value-added services that help them grow and prosper.

extending its support to organizations that largely base their business model on technology and communications. This strategic expansion came as a natural outcome of the ICT sector’s success; following an initial period of developing core technologies, entrepreneurs seized valuable business opportunities that became gradually available, and launched enterprises that create additional jobs, generate exports, and attract investments.

companies, online and mobile content and applications developers, games publishers and developers and others are amongst the enterprises that have been integrated within int@j’s circle of constituents. int@j’s multi-tier membership packages are open to all organizations with a vested interest in the ICT and ITES sector.

The association’s members today are comprised of software developers, hardware providers, telecommunications and data services, call centers, help desks, system integrators, mobile and online content and applications companies, animation and games companies, and non-ICT & ITES support organizations such as banks, management consultants and law firms.

This diversified representation in companies and economic sectors attests to int@j’s critical role as a focal point where ICT/ITES enterprises can congregate with industries that largely depend on their products and services and vice-versa.

int@j Vision 2011-2013: Being the primary and exclusive private sector representative of ICT and ITES- enabled services companies in Jordan, thus duly representing the entire sector.

int@j Mission: To provide its members with a platform of products and services that support their continuous growth, expansion, and prosperity toward a mature sector that substantially contributes to the national economy and provides quality jobs for Jordanians.

Value Proposition: The true value of int@j as a business association lies in its ability to

its members with a real return for their membership investment.

Main ICT Stakeholders

11

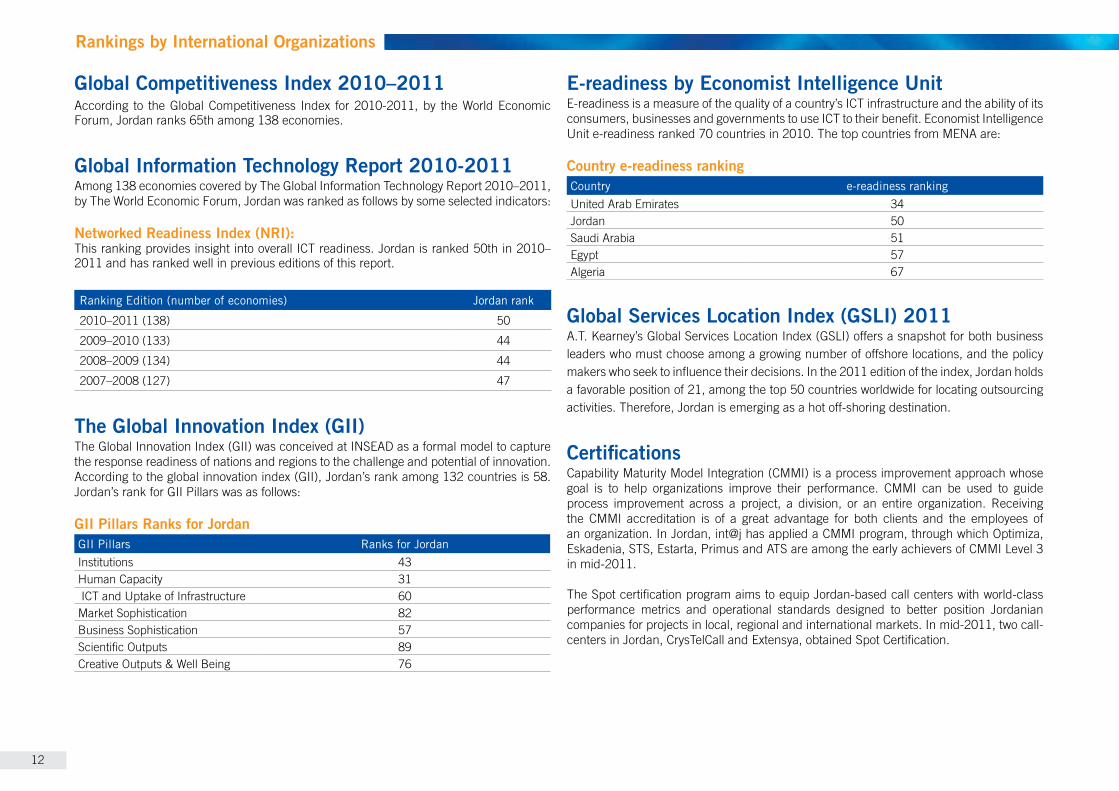

Global Competitiveness Index 2010–2011According to the Global Competitiveness Index for 2010-2011, by the World Economic Forum, Jordan ranks 65th among 138 economies.

Global Information Technology Report 2010-2011 Among

Networked Readiness Index (NRI):

2011 and has ranked well in previous editions of this report.

Ranking Edition (number of economies) Jordan rank

50

The Global Innovation Index (GII)The Global Innovation Index (GII) was conceived at INSEAD as a formal model to capture the response readiness of nations and regions to the challenge and potential of innovation.According to the global innovation index (GII), Jordan’s rank among 132 countries is 58.

GII Pillars Ranks for JordanGII Pillars Ranks for JordanInstitutions Human Capacity 31 ICT and Uptake of Infrastructure 60Market Sophistication 82Business Sophistication 57

8976

E-readiness by Economist Intelligence UnitE-readiness is a measure of the quality of a country’s ICT infrastructure and the ability of its consumers, businesses and governments to use ICT to their benefit. Economist Intelligence

Country e-readiness rankingCountry e-readiness rankingUnited Arab EmiratesJordan 50Saudi Arabia 51Egypt 57Algeria 67

Global Services Location Index (GSLI) 2011A.T. Kearney’s Global Services Location Index (GSLI) offers a snapshot for both business leaders who must choose among a growing number of offshore locations, and the policy makers who seek to influence their decisions. In the 2011 edition of the index, Jordan holds a favorable position of 21, among the top 50 countries worldwide for locating outsourcing activities. Therefore, Jordan is emerging as a hot off-shoring destination.

CertificationsCapability Maturity Model Integration (CMMI) is a process improvement approach whose goal is to help organizations improve their performance. CMMI can be used to guide

the CMMI accreditation is of a great advantage for both clients and the employees of

Eskadenia, STS, Estarta, Primus and ATS are among the early achievers of CMMI Level 3 in mid-2011.

The Spot certification program aims to equip Jordan-based call centers with world-class performance metrics and operational standards designed to better position Jordanian companies for projects in local, regional and international markets. In mid-2011, two call-centers in Jordan, CrysTelCall and Extensya, obtained Spot Certification.

Rankings by International Organizations

12

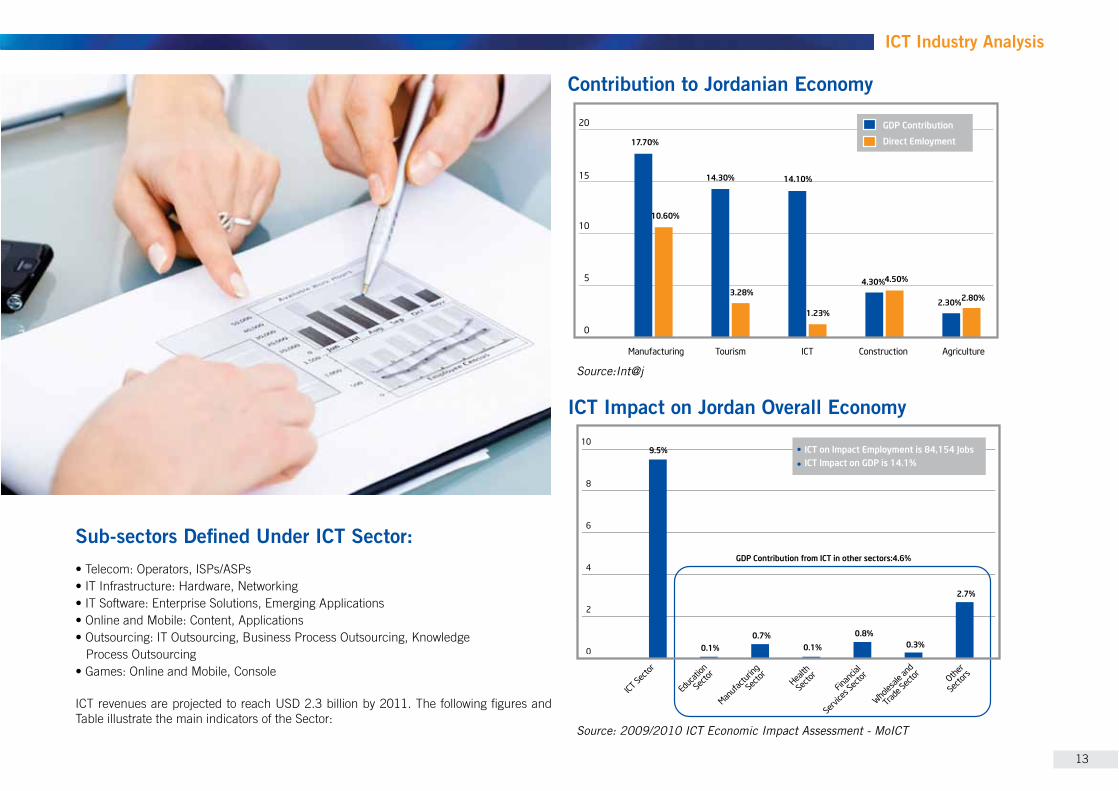

Sub-sectors Defined Under ICT Sector:

ICT revenues are projected to reach USD 2.3 billion by 2011. The following figures and

Contribution to Jordanian Economy

Manufacturing Tourism ICT Construction Agriculture

0

5

1010.60%

17.70%

14.30%

3.28%

14.10%

1.23%

4.30%4.50%

2.30%2.80%

15

20 GDP Contribution

Direct Emloyment

ICT Impact on Jordan Overall Economy

0

2

4

6

8

10

Educatio

n

Sector

Manufa

cturin

g

Sector

Health

Sector

Financia

l

Service

s Secto

r

Wholesale an

d

Trade Secto

rOth

er

Sectors

ICT Sector

9.5% ICT on Impact Employment is 84,154 JobsICT Impact on GDP is 14.1%

0.1% 0.1% 0.3%0.7% 0.8%

2.7%

GDP Contribution from ICT in other sectors:4.6%

ICT Industry Analysis

Source: 2009/2010 ICT Economic Impact Assessment - MoICT

Source:Int@j

13

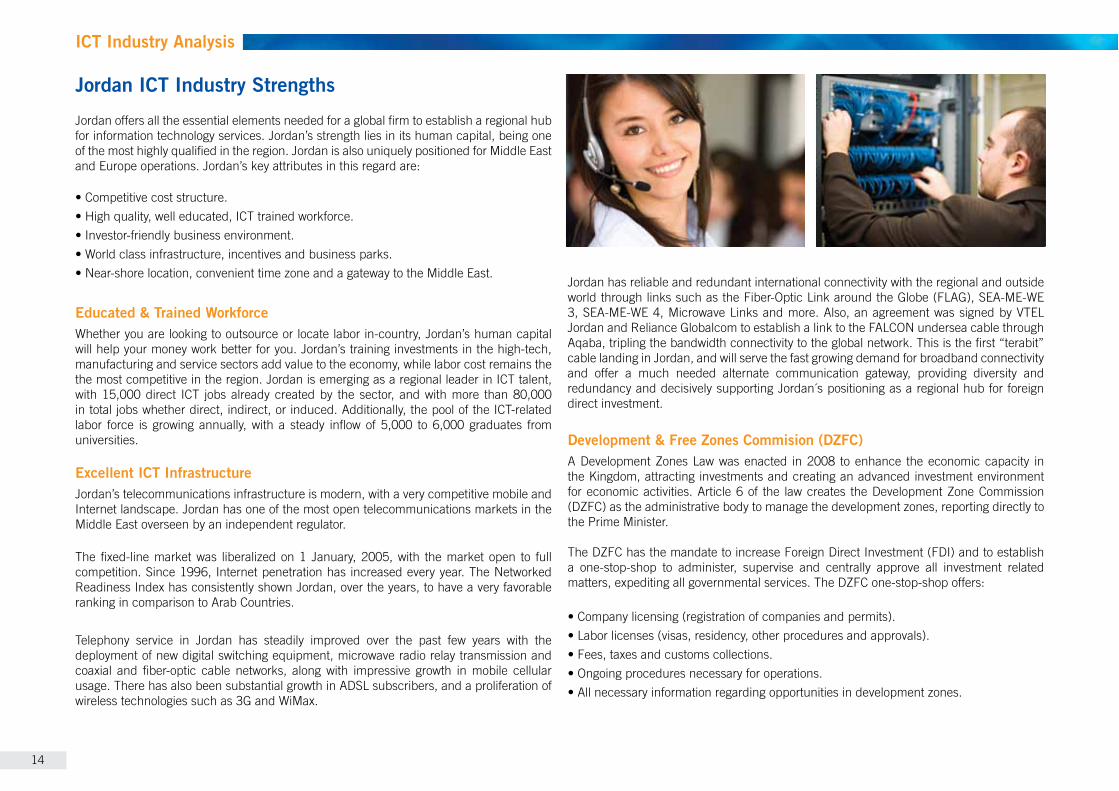

Jordan ICT Industry Strengths

Jordan offers all the essential elements needed for a global firm to establish a regional hub for information technology services. Jordan’s strength lies in its human capital, being one of the most highly qualified in the region. Jordan is also uniquely positioned for Middle East

Educated & Trained WorkforceWhether you are looking to outsource or locate labor in-country, Jordan’s human capital will help your money work better for you. Jordan’s training investments in the high-tech, manufacturing and service sectors add value to the economy, while labor cost remains the the most competitive in the region. Jordan is emerging as a regional leader in ICT talent, with 15,000 direct ICT jobs already created by the sector, and with more than 80,000 in total jobs whether direct, indirect, or induced. Additionally, the pool of the ICT-related labor force is growing annually, with a steady inflow of 5,000 to 6,000 graduates from universities.

Excellent ICT InfrastructureJordan’s telecommunications infrastructure is modern, with a very competitive mobile and Internet landscape. Jordan has one of the most open telecommunications markets in the Middle East overseen by an independent regulator.

The fixed-line market was liberalized on 1 January, 2005, with the market open to full competition. Since 1996, Internet penetration has increased every year. The Networked

ranking in comparison to Arab Countries.

Telephony service in Jordan has steadily improved over the past few years with the deployment of new digital switching equipment, microwave radio relay transmission and coaxial and fiber-optic cable networks, along with impressive growth in mobile cellular usage. There has also been substantial growth in ADSL subscribers, and a proliferation of wireless technologies such as 3G and WiMax.

Jordan has reliable and redundant international connectivity with the regional and outside

Aqaba, tripling the bandwidth connectivity to the global network. This is the first “terabit” cable landing in Jordan, and will serve the fast growing demand for broadband connectivity and offer a much needed alternate communication gateway, providing diversity and redundancy and decisively supporting Jordan´s positioning as a regional hub for foreign direct investment.

Development & Free Zones Commision (DZFC)A Development Zones Law was enacted in 2008 to enhance the economic capacity in the Kingdom, attracting investments and creating an advanced investment environment for economic activities. Article 6 of the law creates the Development Zone Commission (DZFC) as the administrative body to manage the development zones, reporting directly to the Prime Minister.

The DZFC has the mandate to increase Foreign Direct Investment (FDI) and to establish a one-stop-shop to administer, supervise and centrally approve all investment related

ICT Industry Analysis

Selected Development & Free Industrial ZonesThe Development Zones Strategy sets multiple and specialized zones targeted at specific industries. These zones offer aggressive financial incentives to complement existing

privately-owned free zone parks operating in Jordan, while there are three development zones in Jordan suitable for establishing ICT operations.

King Hussein Business Park Development Zone (KHBPD) King Hussein Business Park is destined to become a sustainable and enduring mixed-use city district that will provide future growth and development for Amman and Jordan. It offers international standard office environments with high quality residential developments, and a vast array of dining entertainment and leisure opportunities. Nine core clusters are

education, leisure & entertainment, safety security and compliance, and media and residential.

Irbid Development Area (IDA)The 3.2 square kilometer development area, located 20 km east of Irbid city and 80 km north of Amman, is ideally suited for ICT, Healthcare, Professional Services, Middle &

the IDA will host world-class community services, amenities and housing as an integral part of the development vision of the site.

King Hussein Bin Talal Development Area (KHBTDA)Strategically located in Mafraq, at the crossroads of major transportation highways linking Jordan, Syria, Iraq, and Saudi Arabia, this development zone comprises 21 km2 of land within its officially designated boundaries. KHBTDA represents an extraordinary opportunity for world class industrial, commercial and community development. It offers high quality infrastructure and services to support site industries and to promote environmentally sustainable economic development, on-site logistics facilities to take advantage of existing infrastructure, and quality of life-enhancing housing and auxiliary services.

Summary of Benefits to Foreign Investors

visas and family residence visas)

regulations)

other law applicable in Jordan

Under the Development Areas Law

Income Tax 5%Sales Tax 0%

economic activitiesImport Duties 0%

establishing, constructing and equipping an enterprise in the AreaSocial Services Tax 0%Dividends Tax 0%Exports 0% Exemption of all products and services produced within the Area

Overview of Investment Opportunities by ActivityJordan is a regional gateway to the Arab World, a region with a common language and culture. Accordingly, it is no surprise that two thirds of the country’s exports go to Gulf States. The Arab Middle East is a lucrative and virgin market and Jordan’s reputation is soaring as a center to serve this market. Today, Jordan also offers access to other regions through International and Bi-lateral Agreements.

ICT OutsourcingJordan enjoys a high level of ICT infrastructure and a large number of ICT graduates with strong industry focused skills. In fact, Jordan has long been a source of IT talent for major companies in the Middle East and is widely recognized as possessing the strongest ICT workforce in the region. Along with lower costs, a western style legal system, strong

development and testing to remote infrastructure management to providing technical assistance for sophisticated products.

ICT Industry Analysis

15

Intellectual PropertyJordan-based companies have built significant intellectual property (IP), specifically in software solutions and content creation. This has made local firms successful in penetrating the US, Europe and regional markets. Additionally, Jordan-based ICT entities have already outsourced work to major industry leaders globally.

Knowledge & Business Process OutsourcingKnowledge-based services require a qualified labor force with specific expertise, advanced knowledge, analytical interpretation, and technical skills. Jordan o�ers the required levels of manpower and human talent, coupled with the right telecom infrastructure. The investment climate, political and economic stability ensure that Jordan has emerged as a

Contact & Shared Service CentersJordan has a natural affinity to become a strong contact center outsourcing hub, with its strategic location as a gateway into the MENA region, and owing to a highly service oriented economy, a competitive cost structure, a young workforce and familiarity with both Western and regional cultures. With a relatively neutral English and Arabic accent, Jordan is fast emerging as the most viable contact center destination in the region. Several outsourcing providers operate out of Jordan, o�ering services to US, UK and the Middle East ranging from Customer Support, Pre-Sales and Loyalty management to Technical and Helpdesk support.

Opportunities by Selected SectorsTelecommunications: A Liberalized Telecom Sector (liberalized data, mobile and fixed line subsectors) that has resulted in an excellent infrastructure (WiMAX & 3G services already licensed) and more than 6 million mobile phone subscribers. The telecom sector

E-Learning: Jordan pioneered the adoption of ICT as a tool in education reform many years ago. The Jordan Education Initiative (JEI) has become a regional model, and this has resulted in local firms delivering world-class educational platforms and solutions. The model can be replicated.

E-Health: Already a regional center for health services, electronic health solutions

hospitals. It is now widely considered to be a model to build on and replicate in other countries.

Internet, Mobile & Gaming Content: Jordan is the leading Arabic content creation center in the region, and the growth potential is stunning with only 1% of content on the web currently in Arabic. The region’s top portals, and biggest success stories, emerged from Jordan. Today, Jordan is also recognized as the hotbed of Arabic game development. In mobile applications, local firms are already trailblazers with multiplatform applications.

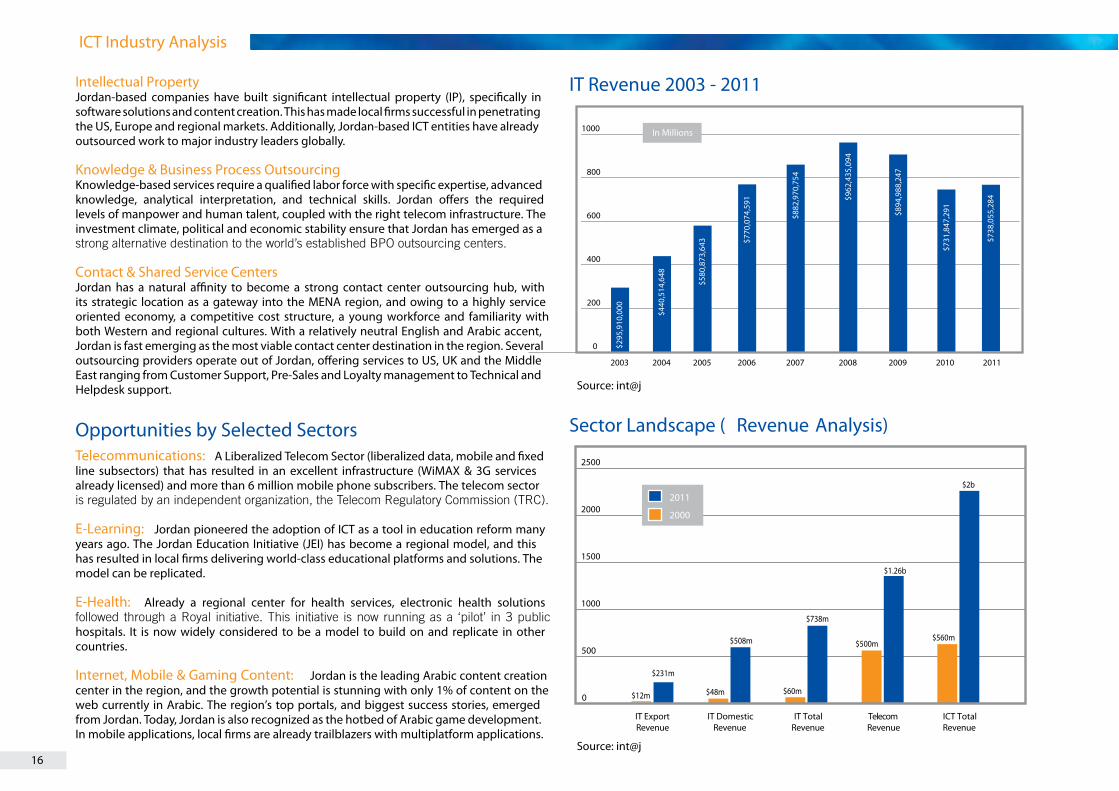

IT Revenue 2003 - 2011

0

200

400

600

800

1000

2003 2004 2005 2006 2007 2008 2009 2010

In Millions

$295

,910

,000

$440

,514

,648

$580

,873

,643 $7

70,0

74,5

91

$882

,970

,754

$894

,988

,247

$962

,435

,094

$731

,847

,291

Sector Landscape ( Revenue Analysis)

0

500

1000

1500

2000

2500

IT ExportRevenue

IT DomesticRevenue

IT TotalRevenue

TelecomRevenue

ICT TotalRevenue

2011

2000

$12m

$231m

$48m

$508m

$60m

$738m

$500m

$1.26b

$560m

$2b

ICT Industry Analysis

2011

$738

,055

,284

Source: int@j

Source: int@j16

USAID Jordan Economic Development ProgramInnovative ApproachesEconomic Development Program, implemented by Deloitte Consulting LLP, began in 2006 with the goals of enhancing Jordan’s competitiveness in global markets, deepening the public sector reform process, and increasing the number of jobs available for Jordanians in the economy. From its inception, the Program’s goals have been consistent with His Majesty King Abdullah II’s vision for Jordan’s emergence as a knowledge economy.

In doing so, it analyzed more than a dozen clusters to identify those that held the most potential for growing Jordan’s economy in the near term. Ultimately, this led to the

Entrepreneurship, Information and Communications Technology, Architecture and

potential. Extensive research and collaborative strategy development were conducted in each of these sectors, and specific actions initiated to achieve planned results. Much of the Program’s efforts have focused on the implementation of existing sector strategies (i.e. National Agenda and Jordan 2020 initiatives). Basing the Program’s activities on existing strategies in sectors that support the knowledge economy has led to significant and lasting results.

Supporting all of these activities are a series of enabling activities to improve the general business and investment environment through institutional strengthening and transformation, workforce development and gender integration, and increased public/

Daman Development Corporation (DDC) Daman Development Corporation (DDC) is a holding company that owns three entities responsible for the establishment, planning and development of three development areas in Jordan; Mafraq Development Corporation (MDC), Northern Development Corporation (NDC) and Business Park Company (BPC) . DDC is owned by Jordan’s Social Security Investment Unit (SSIU) and act as its investment arm in the development areas.

The new Development Areas Law formalizes MDC, NDC and BPC roles as the Master Developers of the three development areas, of which two are specialized in the ICT/ outsourcing sector and are mentioned below.

Jordan Enterprise Development Corporation (JEDCO)The Information and Communications Technology (ICT) sector is an area that is seen as an opportunity in which Jordan can increase its competitive advantage over other countries in the region, consequently Jordan have taken very serious steps in order to launch its major ICT initiatives aiming at developing the ICT sector. Jordan Enterprise Development Corporation was one of the public sector entities that assisted in lending hand for the

and international ICT related exhibitions such as GITEX and CEBIT.

provided funds for 20 companies and 2 associations at an amount of 1,580,901 Euros. The support was not limited to the financial one but included providing technical services to help ICT companies elevate their capabilities.

provides data gathering, processing and delivering high-quality, timely and cost-efficient information needed by SMEs clients to enhance their competitiveness and support their internationalization efforts, as well as the information needed by foreign companies interested in linking with Jordanian firms.

E-Commerce National Strategy.

Jordan Investment Board (JIB)Jordan Investment Board (JIB) was established in 1995 as the investment promotional agency of Jordan. JIB provides investors with an array of full-fledged services including comprehensive information related to investments in the kingdom, business opportunities and pre-feasibility studies for 150 project concepts in various sectors including agriculture, education, energy and utilities, health & pharmaceuticals, information and communication technology, mining and processing, tourism and others.

Additionally, JIB acts as a liaison between foreign investors and the Jordanian public and private sectors and grants financial exemptions from customs fees and sales tax on all

JIB provides prospects with full service assistance consisting of licensing and registration services. Through this service, investors can register and license their projects in Jordan

provided, in a continuous effort to enhance Jordan’s investment environment. JIB has five representative offices in the USA, UAE, Qatar, Kuwait, and China.

Jordan ICT Supporters

17

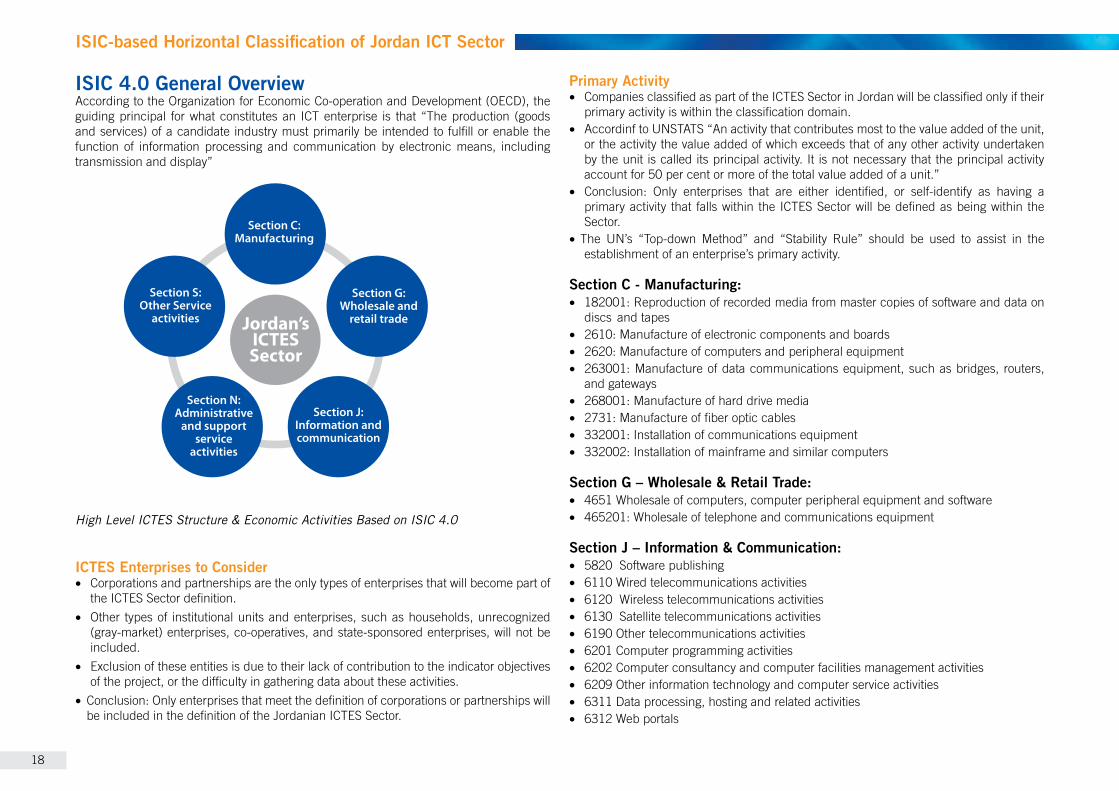

ISIC 4.0 General Overviewguiding principal for what constitutes an ICT enterprise is that “The production (goods and services) of a candidate industry must primarily be intended to fulfill or enable the function of information processing and communication by electronic means, including transmission and display”

High Level ICTES Structure & Economic Activities Based on ISIC 4.0

ICTES Enterprises to Consider• �Corporations and partnerships are the only types of enterprises that will become part of

the ICTES Sector definition.•

(gray-market) enterprises, co-operatives, and state-sponsored enterprises, will not be included.

• Exclusion of these entities is due to their lack of contribution to the indicator objectives of the project, or the difficulty in gathering data about these activities.

• be included in the definition of the Jordanian ICTES Sector.

Primary Activity• �Companies classified as part of the ICTES Sector in Jordan will be classified only if their

primary activity is within the classification domain.• Accordinf to UNSTATS “An activity that contributes most to the value added of the unit,

or the activity the value added of which exceeds that of any other activity undertaken by the unit is called its principal activity. It is not necessary that the principal activity account for 50 per cent or more of the total value added of a unit.”

• �primary activity that falls within the ICTES Sector will be defined as being within the Sector.

• establishment of an enterprise’s primary activity.

Section C - Manufacturing:• �

discs and tapes • �• �• �

and gateways• �• �• �• �

Section G – Wholesale & Retail Trade: • •

Section J – Information & Communication:• 5820 Software publishing• 6110 Wired telecommunications activities• 6120 Wireless telecommunications activities• 6130 Satellite telecommunications activities• • 6201 Computer programming activities• 6202 Computer consultancy and computer facilities management activities• • �6311 Data processing, hosting and related activities • 6312 Web portals

ISIC-based Horizontal Classification of Jordan ICT Sector

Section C:Manufacturing

Section S:Other Service

activities Jordan’sICTESSector

Section G:Wholesale and

retail trade

Section J:Information andcommunication

Section N:Administrative

and supportservice

activities

18

Section N – Administrative & Support Service Activities:•

Section S – Other Services Activities:• • •

modems)

The International Standard Industrial Classification of All Economic Activities (ISIC) consists of a coherent and consistent classification structure of economic activities based on a set of internationally agreed concepts, definitions, principles and classification rules. It provides a comprehensive framework within which economic data can be collected and reported in a format that is designed for purposes of economic analysis, decision-taking and policy-making. The classification structure represents a standard format to organize detailed information about the state of an economy according to economic principles and perceptions.

In practice, the classification is used for providing a continuing flow of information that is indispensable for the monitoring, analysis and evaluation of the performance of an economy over time. In addition to its primary application in statistics and subsequent economic analysis, where information needs to be provided for narrowly defined economic activities (also referred to as “industries”), ISIC is increasingly used also for administrative purposes, such as in tax collection, issuing of business licenses etc.

This fourth revision of ISIC enhances the relevance of the classification by better reflecting the current structure of the world economy, recognizing new industries that have emerged over the past 20 years and facilitating international comparison through increased comparability with existing regional classifications.

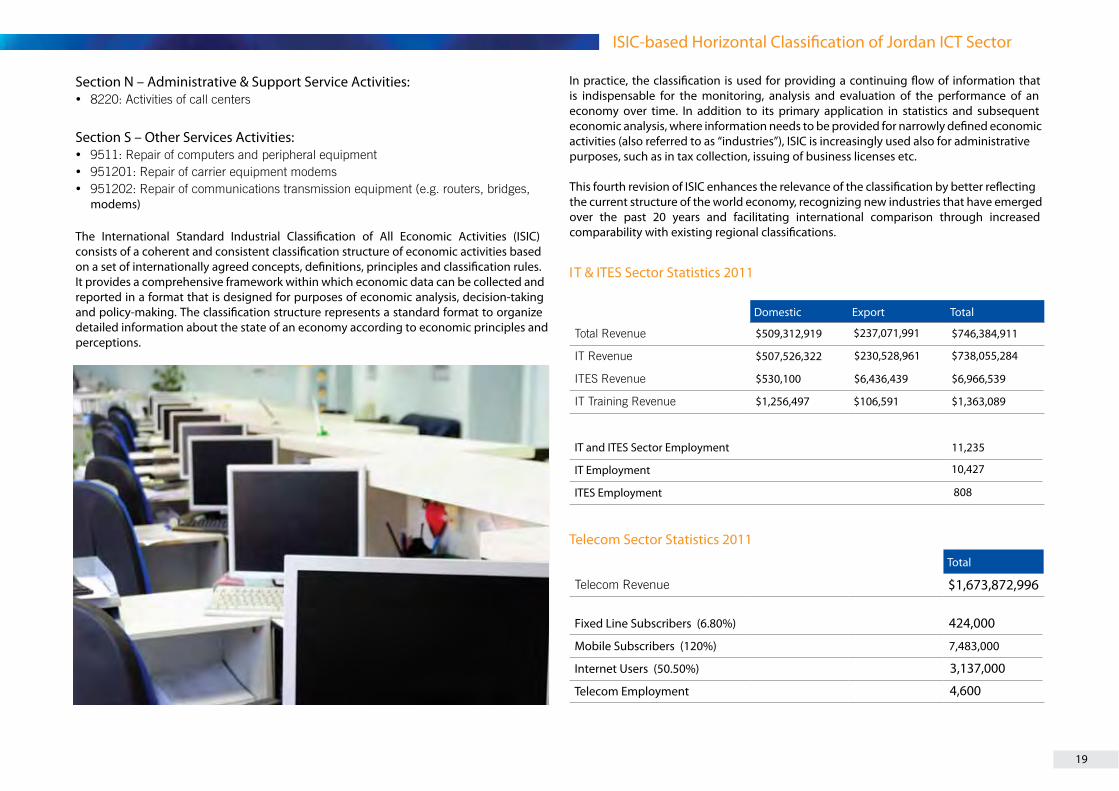

IT & ITES Sector Statistics 2011

Domestic Export Total

$509,312,919 $746,384,911

$507,526,322

$530,100 $6,966,539

$1,256,497 $106,591 $1,363,089

IT and ITES Sector Employment 11,235

IT Employment

ITES Employment

Telecom Sector Statistics 2011

Total

Fixed Line Subscribers (6.80%)

Mobile Subscribers (120%) 7,483,000

Internet Users (50.50%)

Telecom Employment

$1,673,872,996

424,000

3,137,000

4,600

$237,071,991

$230,528,961 $738,055,284

$6,436,439

10,427

808

ISIC-based Horizontal Classification of Jordan ICT Sector

19

Jordan’s ICT companies have served various economic sectors and verticals efficiently for decades, and have accumulated the knowledge and skills to effectively export complete ICT solutions and services to neighboring markets and beyond.Specific verticals which Jordan-based ICT companies serve with distinction and with

Hospitality (Travel and Tourism)Due to the importance of tourism as an economic sector in Jordan, software developers and system integrators have successfully catered to the varied and advanced requirements of this industry for several decades, and therefore gained the experience to serve emerging touristic locations in the Gulf and worldwide. Jordan is also emerging as a prominent call center location for tourism services in the Middle East.

TelecommunicationsBoasting the region’s most liberalized and competitive telecommunications sector, Jordan’s ICT vendors have benefited greatly from supplying and serving this industry, starting relatively early on for the region in the mid-nineties, and have therefore been pioneers in total ICT solutions in this field. Accordingly, many mobile operator networks implement technology solutions for all branches across the region, such as billing solutions.

Financial Sector (Insurance & Banking Systems)Probably the first sector where Jordan ICT companies implemented large-scale systems, banking and financial institutions have reaped the rewards of driving customized system integration experience in the country since the 1970s, which has peaked with Jordan’s software developers creating world-class and unique products and solutions now implemented worldwide, having already taken the lead in regional solutions such as the electronic check clearing system.

EducationJordan is among the most literate nations in the region, therefore Jordan’s academic institutions are well-served by technology solutions. Additionally, the country’s highly educated professionals have pioneered the field of e-learning with world-class software platforms and curricula which are utilized across the Middle East such as e-learning management solutions and content.

Healthmany neighboring countries, the considerable size of Jordan’s health sector has driven growth in ICT solutions to cater to this dynamic and evolving field. Solutions available today are best-in-class and are contributing to adding to Jordan’s reputation as also an emerging medical information and communication center such as e-services solutions.

Public Sector / GovernmentThe public sector remains one of the biggest IT customers in Jordan and continues to play a role in pushing local companies to provide advanced governmental, military and other solutions. The successful delivery and maintenance of mission critical, multi-platform and networked solutions to state entities has ensured that Jordan’s ICT companies are well positioned to take on similar projects in neighboring markets such as e-services solutions.

ManufacturingDriven by expansion in Jordan’s economy and government policies to create industrial zones and promote exports, manufacturing grew and flourished. Today, Jordan is home to major regional manufacturing groups whose ICT operations for all global branches are served from Jordan by locally-based ICT companies.

Transportation & LogisticsAs a regional cross-roads and trade center, Jordan was a natural ground for the evolution

of leading international logistics companies, based in Jordan, the sophistication and efficiency of these solutions have now been proven across the world.

Information & MediaThe proliferation of the media and entertainment industries in the Middle East, through local liberalization and the rise of pan-Arab media, has driven the need for both software and content. These relatively new industries have benefited from the accumulated ICT knowledge of many decades of serving more complex industries, and the renowned creativity of Jordanians in Arabic content creation and management.

Cross-Cutting SolutionsFueled by sector-specific ICT solutions, administrative systems across all sectors evolved as Jordan ICT companies sought to fully satisfy the needs of their biggest clients; and in doing so have created industry-leading Arabized solutions for office and industrial automation,

across the Middle East and North Africa.

Vertical Sectors Served by Jordan ICT Companies

20

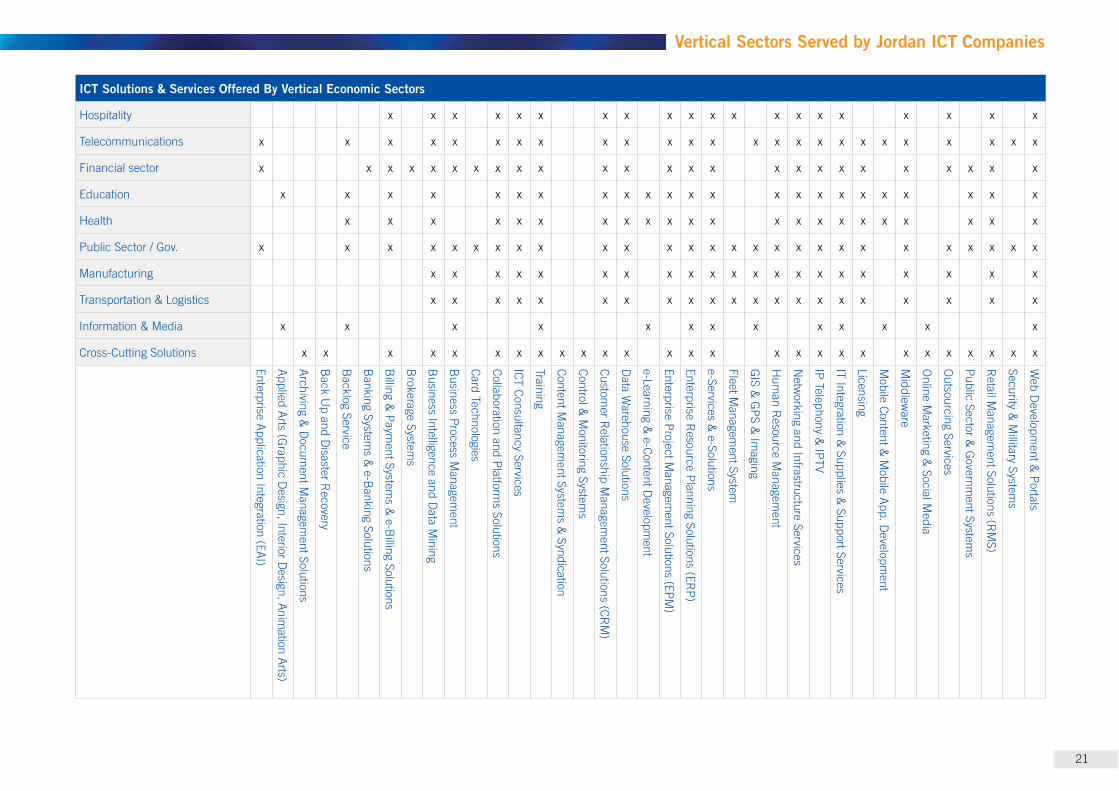

ICT Solutions & Services Offered By Vertical Economic Sectors

Hospitality x x x x x x x x x x x x x x x x x x x x

Telecommunications x x x x x x x x x x x x x x x x x x x x x x x x x

Financial sector x x x x x x x x x x x x x x x x x x x x x x x x x

Education x x x x x x x x x x x x x x x x x x x x x x x

Health x x x x x x x x x x x x x x x x x x x x x x

Public Sector / Gov. x x x x x x x x x x x x x x x x x x x x x x x x x x x

Manufacturing x x x x x x x x x x x x x x x x x x x x x

Transportation & Logistics x x x x x x x x x x x x x x x x x x x x x

Information & Media x x x x x x x x x x x x x

Cross-Cutting Solutions x x x x x x x x x x x x x x x x x x x x x x x x x x x

Enterprise Application Integration (EAI)

Applied Arts (Graphic D

esign, Interior Design, Anim

ation Arts)

Archiving & D

ocument M

anagement Solutions

Backlog Service

Banking System

s & e-B

anking Solutions

Billing &

Payment System

s & e-B

illing Solutions

Brokerage System

s

Business Intelligence and D

ata Mining

Business Process M

anagement

Card Technologies

Collaboration and Platforms Solutions

ICT Consultancy Services

Training

Content Managem

ent Systems &

Syndication

Control & M

onitoring Systems

Data W

arehouse Solutions

e-Learning & e-Content D

evelopment

Enterprise Project Managem

ent Solutions (EPM)

e-Services & e-Solutions

Fleet Managem

ent System

GIS &

GPS &

Imaging

Netw

orking and Infrastructure Services

IP Telephony & IPTV

IT Integration & Supplies &

Support Services

Licensing

Mobile Content &

Mobile App. D

evelopment

Middlew

are

Public Sector & G

overnment System

s

Security & M

illitary Systems

Web D

evelopment &

Portals

Vertical Sectors Served by Jordan ICT Companies

21

Global & Regional Companies Speak on Jordan ICT“Enlightened by His Majesty King Abdullah the II’s vision for the sector, paving the way for Jordan to become a regional hub in Information Technology and Communications,

started with 10 employees covering two domains; Technology Consulting and Sales. Within

This investment was encouraged by Jordan’s strategic geographic location, relatively low operation costs, political stability within the region, strong laws and regulations, and international and foreign companies enjoying all rights and privileges of domestic firms. We also strongly believe in capitalizing and investing in human resources in Jordan for many reasons; bilingual English-Arabic speakers, and excellent caliber and quality of work which

East and Africa are very pleased with the skills, knowledge and professionalism exhibited by the team in Jordan; there is no better proof than the expansion we have reached to date.”

Oracle “The IT sector in Jordan is witnessing significant growth. Therefore, as a provider of world class talent and skilled professionals, supported by a state-of-the-art telecom and IT infrastructure and logistics capabilities, Jordan is well positioned to become a regional hub for industry services and ‘back and from’ office operations. Cisco has a history of partnering with countries that are strong proponents of ICT as an enabler in driving social and economic benefit, have strong leadership from the top and a clear vision of what they want to achieve. Jordan has all of these attributes. It is for this reason that Cisco has already partnered with Jordan on a number of key initiatives including the Jordan Education Initiative, Madrasiti and the Cisco Networking Academy. Additionally, Jordan is an excellent choice for e-healthcare initiatives as it has a great reputation in the area of healthcare and a promising infrastructure with the National Broadband Network.Cisco has a long history of commitment to good corporate citizenship as we believe it is not just the right thing to do it is also good for business. In May 2011, we announced an investment of $10 million to seed a sustainable model of job-creation and economic development in Jordan. The five-year investment plan represents Cisco’s continued commitment toward building stronger and healthier global communities through strategic social investments. The commitment will include a multi-million dollar venture capital investment, targeted at high-potential small businesses. In the future, Cisco also intends to engage in a multi-stakeholder collaboration to encourage further inward investment into the Jordanian economy from local, regional and global organizations.”

Cisco

“Jordan is an important market for Microsoft and we strongly believe that Jordan’s ICT sector is an increasingly important economic stability factor for the Kingdom. Jordan is

talent and the creativity- therefore it continues to attract foreign investments, while fostering an ecosystem of innovation and entrepreneurship. Microsoft will continue on our path to invest, build partnerships and assist the Government in achieving the objectives it has outlined in its National ICT Strategy.”

Microsoft

“The vision and direction of His Majesty have been key drivers for growth in the economic power-house that has become the ICT sector. Productivity, competitiveness and market connectivity will continue to grow in this liberal market place that is being nurtured by the country’s strategic location, stability, growth-friendly regulations, a strong educational system, a quality talent pool, and focused capital expenditures. The sector’s most notable success has been its ability to embrace, nurture and develop a culture of innovation and entrepreneurship. This new culture gave rise to a large number of successful professionals, entrepreneurs, developers, product managers and young men and women who are the foundation of all the success that was witnessed in this vibrant sector.”

Umniah Telecom

“The development of the IT sector in Jordan has been very positive, under the reign of His Majesty King Abdullah, who has acted as a source of encouragement for many companies and start-ups to take the bull-by-the-horns and establish themselves as successful technology developers and e-solutions providers.Today the Kingdom has a stable and developing ICT labor force and is likely to continue increasing as more investments pour into the country from international venture capitalists groups. The IT market in Jordan is booming and dynamic. Many software companies have mushroomed in the country, providing top IT solutions to the countries of the region, making it a gateway to the Gulf States and North Africa, in which Jordanian companies already have a strong presence.”

SSS Process

Testimonials Supporting Jordan ICT

22

Information & Communications Technology Association - Jordan (int@j)

Tel + 962-6-581 2013

www.intaj.net

Fax + 962-6-581 2016